Attached files

| file | filename |

|---|---|

| EX-32 - SECTION 1350 CERTIFICATION - WisdomTree Investments, Inc. | d234483dex32.htm |

| EX-31.2 - CERTIFICATION OF CHIEF FINANCIAL OFFICER PURSUANT TO RULES 13A-14 - WisdomTree Investments, Inc. | d234483dex312.htm |

| EXCEL - IDEA: XBRL DOCUMENT - WisdomTree Investments, Inc. | Financial_Report.xls |

| EX-31.1 - CERTIFICATION OF CHIEF EXECUTIVE OFFICER PURSUANT TO RULES 13A-14 - WisdomTree Investments, Inc. | d234483dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-10932

WisdomTree Investments, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 13-3487784 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 380 Madison Avenue, 21st Floor New York, New York |

10017 | |

| (Address of principal executive officers) | (Zip Code) | |

212-801-2080

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act’) during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of November 4, 2011 there were 115,961,628 shares of the registrant’s Common Stock, $.01 par value per share, outstanding (voting shares).

Table of Contents

WISDOMTREE INVESTMENTS, INC.

Form 10-Q

For the Quarterly Period Ended September 30, 2011

2

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q, or this Report, contains forward-looking statements that are based on our management’s belief and assumptions and on information currently available to our management. Although we believe that the expectations reflected in these forward-looking statements are reasonable, these statements relate to future events or our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology. These statements are only predictions. You should not place undue reliance on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which are, in some cases, beyond our control and which could materially affect results. Factors that may cause actual results to differ materially from current expectations include, among otherthings, those listed in the section entitled “Risk Factors” and elsewhere in this Report. If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee of future performance. You should read this Report and the documents that we reference in this Report and have filed with the Securities and Exchange Commission as exhibits to the registration statement, of which this Report is a part, completely and with the understanding that our actual future results may be materially different from any future results expressed or implied by these forward-looking statements, please see Item 1A. “Risk Factors” in this Report.

In particular, forward-looking statements in this Report include statements about:

| • | anticipated trends, conditions and investor sentiment in the global markets; |

| • | anticipated levels of inflows into and outflows out of our exchange traded funds; |

| • | our ability to deliver favorable rates of return to investors; |

| • | our ability to develop new products and services; |

| • | our ability to maintain current vendors or find new vendors to provide services to us at favorable costs; |

| • | competition in our business; and |

| • | the effect of laws and regulations that apply to our business. |

The forward-looking statements in this Report represent our views as of the date of this Report. We anticipate that subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so except to the extent required by applicable law. Therefore, these forward-looking statements do not represent our views as of any date other than the date of this Report.

3

Table of Contents

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Balance Sheets

(In Thousands, Except Per Share Amounts)

| September 30, 2011 |

December 31, 2010 |

|||||||

| (Unaudited) | ||||||||

| Assets |

||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 21,052 | $ | 14,233 | ||||

| Investments |

— | 1,295 | ||||||

| Accounts receivable |

5,737 | 4,825 | ||||||

| Other current assets |

1,184 | 642 | ||||||

|

|

|

|

|

|||||

| Total current assets |

27,973 | 20,995 | ||||||

| Fixed assets, net |

640 | 756 | ||||||

| Investments |

9,233 | 7,300 | ||||||

| Other noncurrent assets |

59 | 91 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 37,905 | $ | 29,142 | ||||

|

|

|

|

|

|||||

| Liabilities and stockholders’ equity |

||||||||

| Liabilities |

||||||||

| Current liabilities: |

||||||||

| Fund management and administration payable |

$ | 8,866 | $ | 5,714 | ||||

| Compensation and benefits payable |

2,987 | 3,638 | ||||||

| Accounts payable and other liabilities |

2,810 | 2,263 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

14,663 | 11,615 | ||||||

| Other noncurrent liabilities |

186 | 292 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

14,849 | 11,907 | ||||||

|

|

|

|

|

|||||

| Stockholders’ equity |

||||||||

| Preferred stock, par value $0.01; 2,000 shares authorized: |

— | — | ||||||

| Common stock, par value $0.01; 250,000 shares authorized: issued: 115,963 and 115,291 outstanding: 114,520 and 113,132 |

1,159 | 1,152 | ||||||

| Additional paid-in capital |

161,847 | 158,236 | ||||||

| Accumulated deficit |

(139,950 | ) | (142,153 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

23,056 | 17,235 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 37,905 | $ | 29,142 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these consolidated financial statements

4

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Statements of Operations

(In Thousands, Except Per Share Amounts)

(Unaudited)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Revenues |

||||||||||||||||

| ETF advisory fees |

$ | 17,554 | $ | 9,860 | $ | 48,341 | $ | 27,456 | ||||||||

| Other income |

182 | 270 | 644 | 743 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

17,736 | 10,130 | 48,985 | 28,199 | ||||||||||||

| Expenses |

||||||||||||||||

| Compensation and benefits |

5,085 | 4,405 | 14,912 | 14,260 | ||||||||||||

| Fund management and administration |

5,093 | 3,569 | 14,991 | 10,272 | ||||||||||||

| Marketing and advertising |

911 | 745 | 3,240 | 2,331 | ||||||||||||

| Sales and business development |

954 | 766 | 2,612 | 1,972 | ||||||||||||

| Professional and consulting fees |

1,473 | 795 | 3,922 | 2,526 | ||||||||||||

| Occupancy, communication and equipment |

288 | 273 | 846 | 829 | ||||||||||||

| Depreciation and amortization |

68 | 80 | 200 | 235 | ||||||||||||

| Third party sharing arrangements |

1,794 | 609 | 4,434 | 1,485 | ||||||||||||

| Other |

711 | 405 | 1,625 | 1,258 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

16,377 | 11,647 | 46,782 | 35,168 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income/(loss) before provision for income taxes |

1,359 | (1,517 | ) | 2,203 | (6,969 | ) | ||||||||||

| Provision for income taxes |

625 | — | 1,013 | — | ||||||||||||

| Tax benefit |

(625 | ) | — | (1,013 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income/(loss) |

$ | 1,359 | $ | (1,517 | ) | $ | 2,203 | $ | (6,969 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income/(loss) per share—basic |

$ | 0.01 | $ | (0.01 | ) | $ | 0.02 | $ | (0.06 | ) | ||||||

| Net income/(loss) per share—diluted |

$ | 0.01 | $ | (0.01 | ) | $ | 0.02 | $ | (0.06 | ) | ||||||

| Weighted average common shares—basic |

114,238 | 112,424 | 113,886 | 111,675 | ||||||||||||

| Weighted average common shares—diluted |

136,075 | 112,424 | 135,615 | 111,675 | ||||||||||||

The accompanying notes are an integral part of these consolidated financial statements

5

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

| Nine Months Ended September 30, |

||||||||

| 2011 | 2010 | |||||||

| Cash flows from operating activities |

||||||||

| Net income/(loss) |

$ | 2,203 | $ | (6,969 | ) | |||

| Adjustments to reconcile net income/(loss) to net cash provided by/(used in) operating activities: |

||||||||

| Depreciation, amortization and other |

200 | 235 | ||||||

| Stock-based compensation |

5,427 | 6,529 | ||||||

| Deferred rent |

(115 | ) | (70 | ) | ||||

| Accretion to interest income |

79 | (6 | ) | |||||

| (Increase)/decrease in operating assets and liabilities: |

||||||||

| Accounts receivable |

(912 | ) | (842 | ) | ||||

| Other assets |

(510 | ) | 88 | |||||

| Fund management and administration payable |

3,152 | 760 | ||||||

| Compensation and benefits payable |

(651 | ) | (406 | ) | ||||

| Accounts payable and other liabilities |

556 | 12 | ||||||

|

|

|

|

|

|||||

| Net cash provided by/(used in) operating activities |

9,429 | (669 | ) | |||||

|

|

|

|

|

|||||

| Cash flows from investing activities |

||||||||

| Purchase of fixed assets |

(84 | ) | (87 | ) | ||||

| Purchase of investments |

(5,833 | ) | (6,114 | ) | ||||

| Proceeds from the redemption of investments |

5,116 | 7,183 | ||||||

|

|

|

|

|

|||||

| Net cash (used in)/provided by investing activities |

(801 | ) | 982 | |||||

|

|

|

|

|

|||||

| Cash flows from financing activities |

||||||||

| Shares repurchased |

(2,130 | ) | — | |||||

| Proceeds from exercise of stock options |

321 | 1 | ||||||

|

|

|

|

|

|||||

| Net cash (used in)/provided by financing activities |

(1,809 | ) | 1 | |||||

|

|

|

|

|

|||||

| Net increase in cash and cash equivalents |

6,819 | 314 | ||||||

| Cash and cash equivalents—beginning of period |

14,233 | 11,476 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents—end of period |

$ | 21,052 | $ | 11,790 | ||||

|

|

|

|

|

|||||

| Supplemental disclosure of cash flow information |

||||||||

| Cash paid for income taxes |

$ | 12 | $ | 11 | ||||

|

|

|

|

|

|||||

| Non-cash investing and financing activities: |

||||||||

| Cashless exercise of stock options |

$ | 391 | $ | 60 | ||||

|

|

|

|

|

|||||

The accompanying notes are an integral part of these consolidated financial statements

6

Table of Contents

WisdomTree Investments, Inc. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(In Thousands, Except Share and Per Share Amounts)

(unaudited)

1. Organization and Description of Business

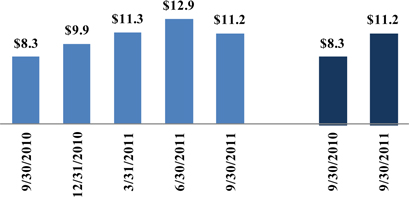

WisdomTree Investments, Inc. (“WisdomTree” or the “Company”) is a New York-based exchange-traded fund sponsor and asset manager. The Company is the eighth largest sponsor of ETFs in the United States based on assets under management (“AUM”). In June 2006, the Company launched 20 ETFs and, as of September 30, 2011, had 47 ETFs with AUM of $11.2 billion. Through its operating subsidiary, the Company provides investment advisory and other management services to the WisdomTree Trust (“WTT”) and WisdomTree ETFs. The Company also licenses its indexes to third parties and promotes the use of WisdomTree ETFs in 401(k) plans. The Company has the following subsidiaries:

| • | WisdomTree Asset Management, Inc. (“WTAM”)—a wholly owned subsidiary formed in February 2005, is an investment advisor registered with the Securities and Exchange Commission (“SEC”). WTAM provides investment advisory and other management services to WTT and the WisdomTree ETFs. In exchange for providing these services, the Company receives advisory fee revenues based on a percentage of the ETFs average daily net assets under management. |

| • | WisdomTree Retirement Services, Inc. (“WTRS”)—a wholly owned subsidiary formed in August 2007, markets with selected third parties the use of WisdomTree ETFs in 401(k) plans as well as offering a platform that offers ETFs to the 401(k) marketplace. |

The WisdomTree ETFs are issued by WTT. WTT, a non-consolidated third-party, is a Delaware statutory trust registered with the SEC as an open-end management investment company. WTT offers ETFs across international and domestic equities, currency, fixed income and alternatives asset classes. The Company has licensed the use of its own fundamentally-weighted indexes on an exclusive basis to WTT for the WisdomTree ETFs. The Board of WTT, or the Trustees, is separate from the Board of the Company. The Trustees are primarily responsible for overseeing the management and affairs of the WisdomTree ETFs and the Trust for the benefit of the WisdomTree ETF shareholders and has contracted with the Company to provide for general management and administration services of WTT and the WisdomTree ETFs. The Company, in turn, has contracted with third parties to provide the majority of these administration services. In addition, certain officers of the Company provide general management services for WTT.

2. Significant Accounting Policies

Basis of Presentation

These consolidated financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“GAAP”), and in the opinion of management reflect all adjustments, consisting of only normal recurring adjustments, necessary for a fair statement of financial condition, results of operations and cash flows for the periods presented. The consolidated financial statements include the accounts of the Company’s wholly owned subsidiaries WTAM and WTRS. All intercompany accounts and transactions have been eliminated in consolidation. Certain accounts in the prior periods’ consolidated financial statements have been reclassified to conform to the current period’s consolidated financial statements presentation. These reclassifications had no effect on the previously reported net losses. These consolidated financial statements should be read in conjunction with the audited consolidated financial statements and footnotes for the year ended December 31, 2010.

Use of Estimates

The preparation of the Company’s consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the balance sheet dates and the reported amounts of revenues and expenses for the periods presented. Actual results could differ from those estimates.

Revenue Recognition

The Company earns investment advisory fees for ETFs and separately managed accounts as well as licensing fees from third parties. ETF advisory fees are based on a percentage of the ETFs average daily net assets and recognized over the period the related service is provided. Fees for separately managed accounts and licensing are based on a percentage of the average monthly net assets and recognized over the period the related service is provided.

7

Table of Contents

Depreciation and Amortization

Depreciation is provided for using the straight-line method over the estimated useful lives of the related assets as follows:

| Equipment |

3 years | |||

| Furniture and fixtures |

7 years |

Leasehold improvements are amortized over the term of their respective leases or service lives of the improvements, whichever is shorter. Fixed assets are stated at cost less accumulated depreciation and amortization.

Marketing and Advertising

Advertising costs, including media advertising are expensed when incurred.

Cash and Cash Equivalents

The Company considers all highly liquid investments with an original maturity of 90 days or less at the time of purchase to be classified as cash equivalents. Cash and cash equivalents are held with one large financial institution.

Accounts Receivable and Allowance for Doubtful Accounts

Accounts receivable are customers’ obligations due under normal trade terms. An allowance for doubtful accounts is not provided because, in the opinion of management, all accounts receivable recorded are deemed collectible.

Impairment of Long-Lived Assets

On a periodic basis, the Company performs a review for the impairment of long-lived assets when events or changes in circumstances indicate that the estimated undiscounted future cash flows expected to be generated by the assets are less than their carrying amounts or when other events occur which may indicate that the carrying amount of an asset may not be recoverable.

Earnings/(Loss) per Share

Basic earnings or loss per share is computed by dividing net income or loss available to common stockholders by the weighted-average number of common shares outstanding for the period. Diluted earnings per share reflects the potential reduction in earnings per share that could occur if options or other contracts to issue common stock were exercised or converted into common stock. Options and restricted shares to purchase shares of common stock were included in the three and nine months ended September 30, 2011 but not included in the computation of diluted loss per share for the three and nine months ended September 30, 2010 as the Company incurred losses during those periods.

Investments

The Company accounts for all of its investments as held-to-maturity, which are recorded at amortized cost, which approximates fair value. For held-to-maturity investments, the Company has the intent and ability to hold investments to maturity and it is not more likely than not that the Company will be required to sell the investments before recovery of their amortized cost bases, which may be maturity.

On a periodic basis, the Company reviews its portfolio of investments for impairment. If a decline in fair value is deemed to be other-than-temporary, the security is written down to its fair value through earnings.

Subsequent Events

The Company has evaluated subsequent events after the date of the consolidated financial statements to consider whether or not the impact of such events needed to be reflected or disclosed in the consolidated financial statements. Such evaluation was performed through the issuance of these interim consolidated financial statements.

Stock-Based Awards

Accounting for share-based compensation requires the measurement and recognition of compensation expense for all equity awards based on estimated fair values. The Company accounts for stock-based compensation for its employees based on the cost of employee services received in exchange for a stock-based award. Stock-based compensation is measured based on the grant-date fair value of the award and are amortized over the relevant service period.

8

Table of Contents

Stock-based awards granted to non-employees for goods or services are valued at the fair value of the equity instruments issued or the fair value of consideration received, whichever is a more reliable measure of the fair value of the transaction, and recognized when performance obligations are complete.

Income Taxes

The Company accounts for income taxes using the liability method, which requires the determination of deferred tax assets and liabilities based on the differences between the financial and tax basis of assets and liabilities using the enacted tax rates in effect for the year in which differences are expected to reverse. Deferred tax assets are adjusted by a valuation allowance if, based on the weight of available evidence, it is more-likely-than-not that some portion or all of the deferred tax assets will not be realized.

In order to recognize and measure any unrecognized tax benefits, management evaluates and determines whether any of its tax positions are more-likely-than-not to be sustained upon examination, including resolution of any related appeals or litigation processes, based on the technical merits of the position. Once it is determined that a position meets this recognition threshold, the position is measured to determine the amount of benefit to be recognized in the consolidated financial statements. Management does not believe that the Company has any material uncertain tax positions. The Company records interest and penalties, if any, related to income taxes within the provision for income taxes in the consolidated statements of operations.

The Company had tax years December 31, 1996 through December 31, 2010 open for examination by federal and state agencies as of September 30, 2011.

Related-Party Transactions

The Company’s revenues are derived primarily from investment advisory agreements with WTT and WisdomTree ETFs. Under these agreements, the Company has granted WTT an exclusive license to its own indexes for operation of the WisdomTree ETFs. The Trustees are primarily responsible for overseeing the management and affairs of the WisdomTree ETFs and the Trust for the benefit of the WisdomTree ETF stockholders and has contracted with the Company to provide for general management and administration of WTT and the WisdomTree ETFs. The Company is also responsible for expenses of WTT, including the cost of transfer agency, custody, fund administration and accounting, legal, audit, and other non-distribution services. In exchange, the Company receives fees based on a percentage of the ETF average daily net assets. The advisory agreements may be terminated by WTT upon notice. Certain officers of the Company also provide general management oversight of WTT; however, these officers have no material decision making responsibilities and primarily implement the decisions of the Trustees. At September 30, 2011 and December 31, 2010, the balance of accounts receivable from WTT was approximately $5,574 and $4,612, respectively. Revenue from ETF advisory services provided to WTT for the three months ended September 30, 2011 and 2010 was approximately $17,554 and $9,860, respectively and for the nine months ended September 30, 2011 and 2010 was approximately $48,341 and $27,456, respectively.

Third Party Sharing Arrangements

Included in third party sharing arrangements expense are payments (reimbursements) from/(to) the Company with respect to (i) a collaborative arrangement and (ii) marketing agreements with third parties:

Collaborative Arrangement—In 2008, the Company entered into a mutual participation agreement with Mellon Capital Management Corporation (“Mellon Capital”) and The Dreyfus Corporation (“Dreyfus”) in which the parties agreed to collaborate in developing currency and fixed income ETFs under WTT. Under the agreement, the Company is responsible for operating the ETFs and providing sales, marketing and research support at its own cost. Mellon Capital and Dreyfus are responsible for providing sub-advisory, fund administration and accounting services for these collaborative ETFs at its own cost. Any revenues less third party costs, such as marketing, legal, accounting or fund management, related to these collaborative products are shared equally, including any losses (“net profit/(loss)”). The Company is responsible for arranging any third party costs related to this collaborative arrangement. This agreement expires in March 2013. The Company has determined it is the principal participant for transactions under this collaborative arrangement and as such, records these transactions on a gross basis reflecting all of the revenues and third party expenses on its consolidated financial statements in accordance with the nature of the revenue or expense. Any net profit/(loss) payments are reflected in Third Party Sharing Arrangements expense on the consolidated financial statements.

9

Table of Contents

Revenues and expenses under this collaborative arrangement included in the Company’s consolidated financial statement are as follows:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| ETF advisory fees revenue |

$ | 3,882 | $ | 1,658 | $ | 9,653 | $ | 4,608 | ||||||||

| Expenses: |

||||||||||||||||

| Fund management and administration |

381 | 331 | 1,073 | 775 | ||||||||||||

| Marketing and advertising |

41 | 18 | 389 | 679 | ||||||||||||

| Sales and business development |

69 | 95 | 115 | 186 | ||||||||||||

| Other |

— | 1 | — | 3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total third party expenses |

491 | 445 | 1,577 | 1,643 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net profit |

3,391 | 1,213 | 8,076 | 2,965 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 50% sharing |

$ | 1,696 | $ | 606 | $ | 4,038 | $ | 1,482 | ||||||||

Marketing agreements—In 2010, the Company entered into agreements with two external marketing firms to serve as the external marketing agents for the WisdomTree ETFs in the U.S. independent broker-dealer channel and in Latin America. Under these agreements, the Company will pay a percentage of their advisory fee revenue, subject to caps, to the marketing agents based on incremental growth in assets under management in the respective sales channel. The Company incurred marketing fees for the three and nine months ended September 30, 2011 of $98 and $396, respectively and $3 for the three and nine months ended September 30, 2010.

Segment, Geographic and Customer Information

The Company operates as one business segment, as an ETF sponsor and asset manager providing investment advisory services. Revenues are derived in the U.S. and all of the Company’s assets are located in the U.S.

Recently Issued Accounting Pronouncements

In January 2010, ASU No. 2010-6, Improving Disclosures About Fair Value Measurement, adds required disclosures about items transferring into and out of Levels 1 and 2 in the fair value hierarchy; adding separate disclosures about purchase, sales, issuances, and settlements relative to Level 3 measurements; and clarifying, among other things, the existing fair value disclosures about the level of disaggregation. ASU No. 2010-6 is effective for interim and annual reporting periods beginning after December 15, 2009, except for the requirement to provide Level 3 purchases, sales, issuances, and settlements on a gross basis, which is effective for fiscal years beginning after December 15, 2010. This standard impacts disclosure requirements only and did not have a material impact on our consolidated financial statements.

In May 2011, FASB issued ASU No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and International Financial Reporting Standards (“IFRS”).” ASU No. 2011-04 includes common requirements for measurement of and disclosure about fair value between U.S. GAAP and IFRS. ASU No. 2011-04 will require reporting entities to disclose the following information for fair value measurements categorized within Level 3 of the fair value hierarchy: quantitative information about the unobservable inputs used in the fair value measurement, the valuation processes used by the reporting entity and a narrative description of the sensitivity of the fair value measurement to changes in unobservable inputs and the interrelationships between those unobservable inputs. In addition, ASU No. 2011-04 will require reporting entities to make disclosures about amounts and reasons for all transfers in and out of Level 1 and Level 2 fair value measurements. The new and revised disclosures are effective for interim and annual reporting periods beginning after December 15, 2011. At this time, management is evaluating the implications of ASU No. 2011-04 and its impact on the Company’s consolidated financial statements.

3. Investments and Fair Value Measurements

The following table is a summary of the Company’s investments:

| September 30, 2011 | December 31, 2010 | |||||||

| Held-to-Maturity | Held-to-Maturity | |||||||

| Federal agency debt instruments |

$ | 9,233 | $ | 8,595 | ||||

|

|

|

|

|

|||||

| Total |

$ | 9,233 | $ | 8,595 | ||||

|

|

|

|

|

|||||

10

Table of Contents

The following table summarizes unrealized gains, losses, and fair value on investments:

| September 30, 2011 | December 31, 2010 | |||||||

| Held-to-Maturity | Held-to-Maturity | |||||||

| Cost/amortized cost |

$ | 9,233 | $ | 8,595 | ||||

| Gross unrealized gains |

50 | 47 | ||||||

| Gross unrealized losses |

(41 | ) | (151 | ) | ||||

|

|

|

|

|

|||||

| Fair value |

$ | 9,242 | $ | 8,491 | ||||

|

|

|

|

|

|||||

The Company’s table sets forth the maturity profile of investments:

| September 30, 2011 | December 31, 2010 | |||||||

| Held-to-Maturity | Held-to-Maturity | |||||||

| Due within one year |

$ | — | $ | 1,295 | ||||

| Due one year through five years |

— | 249 | ||||||

| Due five years through ten years |

1,150 | 796 | ||||||

| Due over ten years |

8,083 | 6,255 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 9,233 | $ | 8,595 | ||||

|

|

|

|

|

|||||

Fair Value Measurement

Under the accounting for fair value measurements and disclosures, fair value is defined as the price that would be received to sell an asset or paid to transfer a liability, or the exit price, in an orderly transaction between market participants at the measurement date. The accounting guidance establishes a hierarchy of valuation techniques based on whether the inputs to those valuation techniques are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s market assumptions.

These three types of inputs create the following fair value hierarchy:

Level 1—Quoted prices for identical instruments in active markets.

Level 2—Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable.

Level 3—Instruments whose significant value drivers are unobservable.

This hierarchy requires the use of observable market data when available. The Company’s held-to-maturity securities are categorized as Level 1. The amortized cost of the held-to-maturity securities approximates fair value. The Company does not intend to sell its investments held-to maturity before the recovery of their amortized cost bases which may be at maturity.

Some of our financial instruments are not measured at fair value on a recurring basis but are recorded at amounts that approximate fair value due to their liquid or short-term nature. Such financial assets and financial liabilities include: cash and cash equivalents, accounts receivable, certain other current assets, accounts payable and other liabilities, fund management and administration payable, and compensation and benefits payable.

4. Commitments and Contingencies

Contractual Obligations

The Company has entered into obligations under operating leases with initial non-cancelable terms in excess of one year for office space, telephone, and data services. Expenses recorded under these agreements for the three months ended September 30, 2011 and 2010 were approximately $267 and $248 respectively. Expenses for the nine months ended September 30, 2011 and 2010 were approximately $781 and $761 respectively.

11

Table of Contents

Future minimum lease payments with respect to non-cancelable operating leases at September 30, 2011 are approximately as follows:

| Remainder of 2011 |

$ | 352 | ||

| 2012 |

1,372 | |||

| 2013 |

1,298 | |||

| 2014 |

74 | |||

| 2015 and thereafter |

— | |||

|

|

|

|||

| Total |

$ | 3,096 | ||

|

|

|

Letter of Credit

The Company collateralizes its leased office space through a standby letter credit in the amount of $700 held as an investment in debt securities, which is included in investments on the consolidated balance sheets at September 30, 2011 and December 31, 2010.

Contingencies

The Company is subject to various routine regulatory reviews and inspections by the SEC as well as legal proceedings arising in the ordinary course of business. The Company is not currently party to any litigation or other legal proceedings that management believes are reasonably likely to have a material adverse effect on the Company’s operating results, financial condition or cash flows.

5. Stock-Based Awards

Stock Options and Restricted Stock

The Company grants stock options to employees, certain directors and non-employee consultants and special advisors for services. Options are issued generally for terms of ten years and vest between two to four years. Options are issued with an exercise price equal to the fair value of the Company on the date of grant. The Company estimated the fair value for options using the Black-Scholes Option Pricing Model.

The Company grants restricted stock to employees and certain directors. All restricted stock awards require future service as a condition of delivery of the underlying shares of common stock along with certain other requirements outlined in the award agreements. Restricted stock awards generally vest over one to four years.

From time-to-time, the Company also grants restricted and common stock to nonemployee consultants, special advisors and vendors for services. In general, theses awards vest over the contractual period of the consulting arrangement. The fair value of these awards is measured at the grant dated fair value and re-measured at each reporting period. Fair value is determined as the closing price of the Company’s common stock on the date of grant.

A summary of options and restricted stock activity is as follows:

| Options | Weighted Average Exercise Price of Options |

Restricted Stock Awards |

||||||||||

| Balance at January 1, 2011 |

21,443,617 | $ | 0.60 | 2,158,509 | ||||||||

| Granted |

755,000 | $ | 5.68 | 561,526 | ||||||||

| Exercised/vested |

(535,842 | ) | $ | 1.12 | (1,251,896 | ) | ||||||

| Forfeitures or expirations |

(109,066 | ) | $ | 2.32 | (25,405 | ) | ||||||

|

|

|

|

|

|||||||||

| Balance at September 30, 2011 |

21,553,709 | $ | 0.76 | 1,442,734 | ||||||||

|

|

|

|

|

|

|

|||||||

A summary of stock-based compensation expense is as follows:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Employees and directors |

$ | 995 | $ | 1,492 | $ | 3,374 | $ | 5,319 | ||||||||

| Non-employees |

808 | 476 | 2,053 | 1,210 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 1,803 | $ | 1,968 | $ | 5,427 | $ | 6,529 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

12

Table of Contents

6. Earnings and Dividend Per Share

The following is a reconciliation of the basic and diluted earnings per share computation:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2011 | 2010 | 2011 | 2010 | |||||||||||||

| Net income/(loss) |

$ | 1,359 | $ | (1,517 | ) | $ | 2,203 | $ | (6,969 | ) | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Shares of common stock and common stock equivalents: |

||||||||||||||||

| Weighted averages shares used in basic computation (in thousands) |

114,238 | 112,424 | 113,886 | 111,675 | ||||||||||||

| Dilutive effect of stock options and unvested restricted stock (in thousands) |

21,837 | — | 21,729 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted averages shares used in dilutive computation (in thousands) |

136,075 | 112,424 | 135,615 | 111,675 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic earnings per share |

$ | 0.01 | $ | (0.01 | ) | $ | 0.02 | $ | (0.06 | ) | ||||||

| Dilutive earnings per share |

$ | 0.01 | $ | (0.01 | ) | $ | 0.02 | $ | (0.06 | ) | ||||||

Diluted earnings per share reflects the potential reduction in earnings per share that could occur if options or other contracts to issue common stock were exercised or converted into common stock. Options and restricted shares to purchase shares of common stock were included in the three and nine months ended September 30, 2011 but not included in the computation of diluted loss per share for the three and nine months ended September 30, 2010 as the Company incurred losses during those periods. The number of outstanding options and unvested restricted stock excluded for the three and nine months ended September 30, 2010 were 21,765 and 2,582, respectively.

7. Income Taxes

At September 30, 2011 and December 31, 2010, the Company had net operating losses carry forward of $97,022 and $101,856, respectively, which it carries as a deferred tax asset which had been completely offset by a valuation allowance. For the three and nine months ended September 30, 2011, the Company has utilized $625 and $1,013, respectively, of its net operating loss by applying a 45.96% rate.

8. Shares Repurchased

During the nine months ended September 30, 2011, the Company repurchased 383,201 shares of its Company stock for an aggregate price of $2,130. The shares repurchased related to the vesting of restricted common stock granted to employees.

9. Subsequent Event

On October 17, 2011 the Company filed a registration statement on Form S-1 with the Securities and Exchange Commission for a proposed public offering of shares of its common stock by the Company and certain of its stockholders. The number of shares to be offered by the stockholders has not yet been determined but the Company intends to issue up to one million new shares. BofA Merrill Lynch and Morgan Stanley & Co. LLC are acting as joint book-running managers for the offering.

13

Table of Contents

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read together with our consolidated financial statements and the related notes and the other financial information included elsewhere in this Report. In addition to historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to these differences include those discussed below. For a more complete description of the risks noted above and other risks that could cause our actual results to materially differ from our current expectations, please see Item 1A. “Risk Factors” of this Report. We assume no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law.

Executive Summary

We are the eighth largest sponsor of ETFs in the United States based on assets under management, or AUM, with an AUM of approximately $11.2 billion as of September 30, 2011. An ETF is an investment fund that holds securities such as stocks or bonds and trades at approximately the same price as the net asset value of its underlying assets. ETFs offer exposure to a wide variety of investment themes, including domestic, international and global equities, fixed income securities, currencies or commodities, as well as securities in specific industries and countries. We launched 20 ETFs in June 2006 and as of September 30, 2011, we offer a comprehensive family of 47 ETFs, which includes 34 international and domestic equity ETFs, nine currency ETFs, two recently launched international fixed income ETFs and two recently launched alternative strategy ETFs.

Through our operating subsidiary, we provide investment advisory and other management services to the WisdomTree ETFs. In exchange for providing these services, we receive advisory fee revenues based on a percentage of the ETFs average daily net assets under management.

Our expenses are predominantly related to selling, operating and marketing our ETFs. We have contracted with third parties to provide certain operational services for the ETFs. We have contracted with BNY Mellon to act as sub-advisor and provide portfolio management services, fund administration, custody, accounting and other related services for the WisdomTree ETFs.

Through our dedicated salesforce, we distribute our ETFs through all major channels within the asset management industry, including brokerage firms, registered investment advisors, institutional investors, private wealth managers and discount brokers. We do not target our ETFs for sale directly to the retail segment but rather to the financial advisor who acts as the intermediary between the end-client and us.

Our revenues are highly correlated to the level and relative mix of our AUM, as well as the fee rate associated with our ETFs. A significant portion of our AUM is invested in securities issued outside of the United States. Therefore, our AUM and our revenues are affected by movements in global capital market levels and the strengthening or weakening of the U.S. dollar against other currencies. Another factor impacting our revenues is the fees associated with our ETFs. Our overall average fee rate is affected by the mix of flows into our ETFs. With a significant portion of our AUM invested in securities issued outside of the U.S., favorable market sentiment to emerging markets, currencies and international fixed income is likely to have a positive effect on our overall revenue. Likewise, unfavorable market sentiments in these areas may cause a decrease in our revenues. In addition, we currently compete within the ETF market against several large ETF sponsors, many smaller sponsors, as well as new entrants to the marketplace, and will compete against large asset management companies who have recently launched or announced intentions to launch ETF products. However, it is our belief that our ability to gather inflows into our ETFs, coupled with general stock market trends, will have the greatest impact on our business.

14

Table of Contents

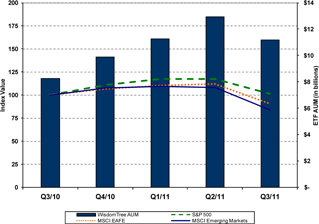

Market Environment

We have been and continue to operate in an extremely challenging and highly competitive business environment. The following chart reflects our ETF assets under management and major market equity indexes since the third quarter of last year:

Equity markets worldwide were in a general upward trend since the bottom of the financial crises of 2008 and 2009 and this positive momentum continued into the first half of 2011. We, in turn, also experienced robust growth and expansion of our AUM, net inflows and market share of industry inflows. However, despite the recovery, concerns remained regarding high unemployment and the rate of economic recovery in the United States, the stability of European economies and their banks, and rising inflation in the emerging market countries. These concerns came to the forefront recently as the U.S. equity markets together with other equity markets worldwide experienced significant volatility. This recent volatility was led by the U.S. debt ceiling debates in Congress and the subsequent downgrade of U.S. government debt by Standard and Poor’s coupled with significant concerns over stability of European banks and the possibility of Greece defaulting on its debt. Our AUM reached a high of $13.5 billion on July 26, 2011; however, has declined to $11.2 billion as of September 30, 2011, primarily as a result of negative market movement.

Our Results

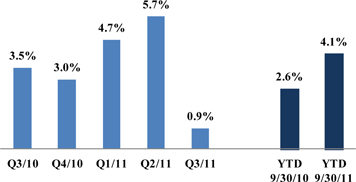

The following charts reflect our net ETF inflows, market share of ETF industry inflows and ETF AUM on a quarterly basis since the third quarter of last year and as of and for the nine months ended September 30, 2010 and 2011:

Market Share of Industry Inflows

15

Table of Contents

Net Inflows

(in millions)

AUM

(in billions)

For the nine months ended September 30, 2011, our revenues were $49.0 million, compared to $28.2 million for the first nine months of 2010, and our expenses increased to $46.8 million from $35.2 million for the nine months ended September 30, 2010. We recorded net income of $2.2 million in the nine months ended September 30, 2011, compared to a net loss of $7.0 million in the comparable period in 2010.

Key Operating Statistics

The following table presents key operating statistics that serve as indicators for the performance of our business:

| As of and for the Three Months Ended | As of and for the Nine Months Ended |

|||||||||||||||||||

| September 30, 2011 |

June 30, 2011 |

September 30, 2010 |

September 30, 2011 |

September 30, 2010 |

||||||||||||||||

| Total ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 12,934 | $ | 11,284 | $ | 6,240 | $ | 9,891 | $ | 5,979 | ||||||||||

| Inflows/(outflows) |

179 | 1,699 | 1,161 | 3,142 | 1,864 | |||||||||||||||

| Market appreciation/(depreciation) |

(1,929 | ) | (49 | ) | 859 | (1,849 | ) | 417 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 11,184 | $ | 12,934 | $ | 8,260 | $ | 11,184 | $ | 8,260 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 12,762 | $ | 12,062 | $ | 7,055 | $ | 11,706 | $ | 6,709 | ||||||||||

16

Table of Contents

| ETF Industry and Market Share (in billions) |

||||||||||||||||||||

| ETF industry net inflows |

$ | 21 | $ | 30 | $ | 33 | $ | 77 | $ | 73 | ||||||||||

| WisdomTree market share of industry inflows |

0.8 | % | 5.7 | % | 3.5 | % | 4.1 | % | 2.6 | % | ||||||||||

| International Developed Equity ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 2,619 | $ | 2,613 | $ | 1,674 | $ | 2,062 | $ | 1,953 | ||||||||||

| Inflows/(outflows) |

50 | 33 | (20 | ) | 564 | (32 | ) | |||||||||||||

| Market appreciation/(depreciation) |

(370 | ) | (27 | ) | 246 | (327 | ) | (21 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 2,299 | $ | 2,619 | $ | 1,900 | $ | 2,299 | $ | 1,900 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 2,488 | $ | 2,596 | $ | 1,794 | $ | 2,434 | $ | 1,957 | ||||||||||

| Emerging Markets Equity ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 3,988 | $ | 3,759 | $ | 1,728 | $ | 3,780 | $ | 1,431 | ||||||||||

| Inflows/(outflows) |

102 | 344 | 707 | 506 | 1,043 | |||||||||||||||

| Market appreciation/(depreciation) |

(860 | ) | (115 | ) | 361 | (1,056 | ) | 322 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 3,230 | $ | 3,988 | $ | 2,796 | $ | 3,230 | $ | 2,796 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 3,719 | $ | 3,863 | $ | 2,153 | $ | 3,733 | $ | 1,741 | ||||||||||

| International Sector Equity ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 248 | $ | 252 | $ | 190 | $ | 249 | $ | 358 | ||||||||||

| Inflows/(outflows) |

7 | 1 | 20 | 1 | (105 | ) | ||||||||||||||

| Market appreciation/(depreciation) |

(53 | ) | (5 | ) | 37 | (48 | ) | (6 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 202 | $ | 248 | $ | 247 | $ | 202 | $ | 247 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 234 | $ | 258 | $ | 218 | $ | 246 | $ | 259 | ||||||||||

| US Equity ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 2,612 | $ | 2,218 | $ | 1,406 | $ | 2,057 | $ | 1,330 | ||||||||||

| Inflows/(outflows) |

241 | 374 | 211 | 668 | 368 | |||||||||||||||

| Market appreciation/(depreciation) |

(330 | ) | 20 | 162 | (202 | ) | 81 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 2,523 | $ | 2,612 | $ | 1,779 | $ | 2,523 | $ | 1,779 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 2,528 | $ | 2,364 | $ | 1,540 | $ | 2,352 | $ | 1,484 | ||||||||||

| Currency ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 1,896 | $ | 1,467 | $ | 1,242 | $ | 1,179 | $ | 907 | ||||||||||

| Inflows/(outflows) |

(566 | ) | 382 | (19 | ) | 87 | 328 | |||||||||||||

| Market appreciation/(depreciation) |

(136 | ) | 47 | 43 | (72 | ) | 31 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 1,194 | $ | 1,896 | $ | 1,266 | $ | 1,194 | $ | 1,266 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 1,786 | $ | 1,677 | $ | 1,224 | $ | 1,599 | $ | 1,226 |

17

Table of Contents

| International Fixed Income ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 1,379 | $ | 902 | — | $ | 564 | — | ||||||||||||

| Inflows/(outflows) |

280 | 442 | 262 | 1,057 | 262 | |||||||||||||||

| Market appreciation/(depreciation) |

(166 | ) | 35 | 10 | (128 | ) | 10 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 1,493 | $ | 1,379 | $ | 272 | $ | 1,493 | $ | 272 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 1,780 | $ | 1,195 | $ | 126 | $ | 1,218 | $ | 42 | ||||||||||

| Alternative Strategy ETFs (in millions) |

||||||||||||||||||||

| Beginning of period assets |

$ | 192 | $ | 73 | — | — | — | |||||||||||||

| Inflows/(outflows) |

65 | 123 | — | $ | 259 | — | ||||||||||||||

| Market appreciation/(depreciation) |

(14 | ) | (4 | ) | — | (16 | ) | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| End of period assets |

$ | 243 | $ | 192 | — | $ | 243 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average assets during the period |

$ | 227 | $ | 109 | — | $ | 124 | — | ||||||||||||

| Average ETF assets during the period |

||||||||||||||||||||

| Emerging markets equity ETFs |

29 | % | 32 | % | 31 | % | 32 | % | 26 | % | ||||||||||

| International developed equity ETFs |

20 | % | 21 | % | 25 | % | 21 | % | 29 | % | ||||||||||

| US equity ETFs |

20 | % | 20 | % | 22 | % | 20 | % | 22 | % | ||||||||||

| Currency ETFs |

14 | % | 14 | % | 17 | % | 14 | % | 18 | % | ||||||||||

| International fixed income ETFs |

14 | % | 10 | % | 2 | % | 10 | % | 1 | % | ||||||||||

| International sector equity ETFs |

2 | % | 2 | % | 3 | % | 2 | % | 4 | % | ||||||||||

| Alternative strategy ETFs |

1 | % | 1 | % | 0 | % | 1 | % | 0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average ETF advisory fee during the period |

0.55 | % | 0.55 | % | 0.56 | % | 0.55 | % | 0.55 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Number of ETFs - end of the period |

||||||||||||||||||||

| International developed equity ETFs |

14 | 14 | 14 | 14 | 14 | |||||||||||||||

| US equity ETFs |

12 | 12 | 12 | 12 | 12 | |||||||||||||||

| Currency ETFs |

9 | 9 | 9 | 9 | 9 | |||||||||||||||

| Emerging markets equity ETFs |

4 | 4 | 4 | 4 | 4 | |||||||||||||||

| International sector equity ETFs |

4 | 4 | 4 | 4 | 4 | |||||||||||||||

| International fixed income ETFs |

2 | 2 | 1 | 2 | 1 | |||||||||||||||

| Alternative strategy ETFs |

2 | 1 | — | 2 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

47 | 46 | 44 | 47 | 44 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Headcount |

64 | 61 | 56 | 64 | 56 |

18

Table of Contents

Three Months Ended September 30, 2011 compared to September 30, 2010

Overview

| As of and

For the Three Months Ended September 30, |

Percent | |||||||||||||||

| 2011 | 2010 | Change | Change | |||||||||||||

| Assets Under Management (in millions) |

||||||||||||||||

| Beginning of period assets |

$ | 12,934 | $ | 6,240 | ||||||||||||

| Net inflows |

179 | 1,161 | ($982 | ) | (84.6 | %) | ||||||||||

| Market appreciation/(depreciation) |

(1,929 | ) | 859 | |||||||||||||

|

|

|

|

|

|||||||||||||

| End of period assets |

$ | 11,184 | $ | 8,260 | $ | 2,924 | 35.4 | % | ||||||||

|

|

|

|

|

|||||||||||||

| Financial Results (in thousands) |

||||||||||||||||

| Total revenues |

$ | 17,736 | $ | 10,130 | $ | 7,606 | 75.1 | % | ||||||||

| Total expenses |

16,377 | 11,647 | 4,730 | 40.6 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net income/(loss) |

$ | 1,359 | ($1,517 | ) | $ | 2,876 | nm | |||||||||

|

|

|

|

|

|

|

|||||||||||

Our AUM was $11.2 billion at September 30, 2011, a decrease of $1.8 billion or 13.5% from $12.9 billion at June 30, 2011, primarily due to a $1.9 billion decline in the market value of securities held by our ETFs. Our AUM at September 30, 2010 reflected an increase of $2.0 billion or 32.4% from $6.2 billion at June 30, 2010, primarily due to $1.2 billion of net inflows into our ETFs. We reported net income of $1.4 million in the three months ended September 30, 2011 compared to a loss of $1.5 million in the comparable period in 2010.

Revenues

| Three Months Ended Sept. 30, |

Change | Percent Change |

||||||||||||||

| 2011 | 2010 | |||||||||||||||

| Average assets under management (in millions) |

$ | 12,762 | $ | 7,055 | $ | 5,707 | 80.9 | % | ||||||||

| Average ETF advisory fee |

0.55 | % | 0.56 | % | (0.01 | ) | (1.8 | %) | ||||||||

| ETF advisory fees (in thousands) |

$ | 17,554 | $ | 9,860 | $ | 7,694 | 78.0 | % | ||||||||

| Other income (in thousands) |

182 | 270 | (88 | ) | (32.6 | %) | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total revenues (in thousands) |

$ | 17,736 | $ | 10,130 | $ | 7,606 | 75.1 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

Our total revenues for the three months ended September 30, 2011 increased 75.1% to a record $17.7 million as compared to $10.1 million in the third quarter of 2010, primarily due to higher average assets under management from strong net ETF inflows.

ETF advisory fees

ETF advisory fees revenue increased 78.0% from $9.9 million in the three months ended September 30, 2010 to a record $17.6 million in the comparable period in 2011. This increase was primarily due to higher average asset balances. Average ETF assets under management were $12.8 billion in the third quarter of 2011, as compared to $7.1 billion in the third quarter of 2010. Our average assets under management during the three months ended September 30, 2011 did not decline in absolute terms as our end of period assets under management. We experienced strong net inflows through most of the third quarter; however, due to the volatility in the market place, we experienced a large outflow from certain of our emerging market currency and international fixed income ETFs during the last week of the quarter. As a result, our net inflows and AUM declined. As this outflow happened at the end of the

19

Table of Contents

period, it did not have a material effect on our average assets or our revenues for the three months ended September 30, 2011; however, this decline will likely have a negative effect on our average assets and revenues for the fourth quarter. Also affecting our average assets was a decline of $1.9 billion in the market value of securities held by our ETFs due to the market volaility. Our average ETF advisory fees decreased from 0.56% in the three months ended September 30, 2010 to 0.55% in the comparable period in 2011 due to a change in the mix of average assets of our ETFs.

Other income

Other income decreased 32.6% from $0.3 million in the three months ended September 30, 2010 to $0.2 million in the comparable period in 2011. This decline was primarily due to lower separate account revenues. Following the first quarter of 2011, we no longer managed separate accounts.

Expenses

| (in thousands) |

Three Months Ended Sept. 30, |

Percent Change |

||||||||||||||

| 2011 | 2010 | Change | ||||||||||||||

| Compensation and benefits |

$ | 5,085 | $ | 4,405 | $ | 680 | 15.4 | % | ||||||||

| Fund management and administration |

5,093 | 3,569 | 1,524 | 42.7 | % | |||||||||||

| Marketing and advertising |

911 | 745 | 166 | 22.3 | % | |||||||||||

| Sales and business development |

954 | 766 | 188 | 24.5 | % | |||||||||||

| Professional and consulting fees |

1,473 | 795 | 678 | 85.3 | % | |||||||||||

| Occupancy, communications and equipment |

288 | 273 | 15 | 5.5 | % | |||||||||||

| Depreciation and amortization |

68 | 80 | (12 | ) | (15.0 | %) | ||||||||||

| Third-party sharing arrangements |

1,794 | 609 | 1,185 | nm | ||||||||||||

| Other |

711 | 405 | 306 | 75.6 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

$ | 16,377 | $ | 11,647 | $ | 4,730 | 40.6 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| As a Percent of Revenues: |

Three Months Ended Sept. 30, |

|||||||

| 2011 | 2010 | |||||||

| Compensation and benefits |

28.7 | % | 43.5 | % | ||||

| Fund management and administration |

28.7 | % | 35.2 | % | ||||

| Marketing and advertising |

5.1 | % | 7.4 | % | ||||

| Sales and business development |

5.4 | % | 7.6 | % | ||||

| Professional and consulting fees |

8.3 | % | 7.8 | % | ||||

| Occupancy, communications and equipment |

1.6 | % | 2.7 | % | ||||

| Depreciation and amortization |

0.4 | % | 0.8 | % | ||||

| Third-party sharing arrangements |

10.1 | % | 6.0 | % | ||||

| Other |

4.0 | % | 4.0 | % | ||||

|

|

|

|

|

|||||

| Total expenses |

92.3 | % | 115.0 | % | ||||

|

|

|

|

|

|||||

In the three months ended September 30, 2011, our total expenses increased 40.6% to $16.4 million from $11.6 million in the third quarter of 2010, primarily due to an increase in fund management and administration expense resulting from higher average assets under management, higher compensation and benefits expense, higher third-party sharing arrangements due to higher asset balances in our currency and fixed income ETFs, and higher marketing and advertising and sales and business development expenses to support our growth.

Compensation and benefits

Compensation and benefits expense increased 15.4% from $4.4 million in the three months ended September 30, 2010 to $5.1 million in the comparable period in 2011 primarily due to higher accrued incentive compensation due to our strong year to date results, as well as costs associated with higher headcount. Our headcount increased from 56 at the end of September 2010 to 64 at the end of September 2011. Stock-based compensation expense decreased $0.5 million as equity awards granted to employees in prior years with higher fair values become fully vested and replaced with a lower number of awards at lower fair values.

20

Table of Contents

Fund management and administration

Fund management and administration expense increased 42.7% from $3.6 million in the three months ended September 30, 2010 to $5.1 million in the comparable period in 2011. Higher average assets under management led to an increase of $1.2 million in portfolio management, fund administration and accounting, index licensing, and distribution fees. Printing fees for our regulatory reports increased $0.2 million due to an increase in the number of shareholders of our ETFs. We had 47 ETFs at September 30, 2011 compared to 44 at the September 30, 2010.

Marketing and advertising

Marketing and advertising expense increased 22.3% from $0.7 million in the three months ended September 30, 2010 to $0.9 million in the comparable period in 2011 primarily due to higher levels of television, print and online advertising to support our growth. We expect to continue our marketing efforts into the fourth quarter.

Sales and business development

Sales and business development expense increased 24.5% from $0.8 million in the three months ended September 30, 2010 to $1.0 million in the comparable period in 2011 primarily due to increased new product development related activities.

Professional and consulting fees

Professional and consulting fees increased 85.3% from $0.8 million in the three months ended September 30, 2010 to $1.5 million in the comparable period in 2011 primarily due to a $0.3 million increase in variable stock based compensation expense from $0.5 million to $0.8 million as a result of the higher price of our common stock. Legal and accounting fees associated with the preparation of our SEC registration statement on Form 10 in connection with the listing of our common stock onto the NASDAQ Global Market were $0.2 million in the three months ended September 30, 2011.

Occupancy, communications and equipment

Occupancy, communications and equipment expense remained relatively unchanged at $0.3 million in the three months ended September 30, 2010 and the comparable period in 2011.

Depreciation and amortization

Depreciation and amortization expense remained relatively unchanged in the three months ended September 30, 2010 from the comparable period in 2011.

Third-party sharing arrangements

Third-party sharing arrangements increased $1.2 million from $0.6 million in the three months ended September 30, 2010 to $1.8 million in the comparable period in 2011. This increase was primarily due to a $1.1 million increase in net profits in our currency and fixed income ETFs, which are subject to a profit sharing agreement with Mellon Capital and Dreyfus. Under the agreement, we share revenues and third party costs equally. This expense increased due to the higher average asset balances in these ETFs. In addition, fees paid to third parties for marketing our ETFs in the independent broker-dealer channel and Latin America increased by $0.1 million.

Other

Other expenses increased 75.6% to $0.7 million in the three months ended September 30, 2011 primarily due to higher administration related expenses.

21

Table of Contents

Nine Months Ended September 30, 2011 compared to September 30, 2010

Overview

| As of and for the Nine Months Ended Sept. 30, |

Change | Percent Change |

||||||||||||||

| 2011 | 2010 | |||||||||||||||

| Assets Under Management (in millions) |

||||||||||||||||

| Beginning of period assets |

$ | 9,891 | $ | 5,979 | ||||||||||||

| Net inflows |

3,142 | 1,864 | $ | 1,278 | 68.6 | % | ||||||||||

| Market appreciation/(depreciation) |

(1,849 | ) | 417 | |||||||||||||

|

|

|

|

|

|||||||||||||

| End of period assets |

$ | 11,184 | $ | 8,260 | $ | 2,924 | 35.4 | % | ||||||||

|

|

|

|

|

|||||||||||||

| Financial Results (in thousands) |

||||||||||||||||

| Total revenues |

$ | 48,985 | $ | 28,199 | $ | 20,786 | 73.7 | % | ||||||||

| Total expenses |

46,782 | 35,168 | 11,614 | 33.0 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Net income/(loss) |

$ | 2,203 | ($6,969 | ) | $ | 9,172 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

Our AUM in the nine months of 2011 increased 13.1% primarily due to strong net inflows into our ETFs partly offset by negative market movement. We reported net income of $2.2 million in the nine months ended September 30, 2011 compared to a loss of $7.0 million in the comparable period in 2010.

Revenues

| Nine Months Ended June 30, |

Change | Percent Change |

||||||||||||||

| 2011 | 2010 | |||||||||||||||

| Average assets under management (in millions) |

$ | 11,706 | $ | 6,709 | $ | 4,997 | 74.5 | % | ||||||||

| Average ETF advisory fee |

0.55 | % | 0.55 | % | — | — | ||||||||||

| ETF advisory fees (in thousands) |

$ | 48,341 | $ | 27,456 | $ | 20,885 | 76.1 | % | ||||||||

| Other income (in thousands) |

644 | 743 | (99 | ) | (13.3 | %) | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total revenues (in thousands) |

$ | 48,985 | $ | 28,199 | $ | 20,786 | 73.7 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

Our total revenues for the nine months ended September 30, 2011 increased 73.7% to a $49.0 million as compared to $28.2 million in the comparable period in 2010, primarily due to higher average assets under management from strong net ETF inflows.

ETF advisory fees

ETF advisory fees revenue increased 76.1% from $27.5 million in the nine months ended September 30, 2010 to a record $48.3 million in the comparable period in 2011. This increase was primarily due to higher average asset balances due to strong net inflows. The average fee earned remained unchanged at 0.55% during the nine months ended September 30, 2011 and September 30, 2010.

Other income

Other income decreased 13.3% from $0.7 million in the nine months ended September 30, 2010 to $0.6 million in the comparable period in 2011. This decline was primarily due to lower separate account revenues. Following the first quarter of 2011, we no longer managed separate accounts.

22

Table of Contents

Expenses

| (in thousands) |

Nine Months Ended Sept. 30, |

Change | Percent Change |

|||||||||||||

| 2011 | 2010 | |||||||||||||||

| Compensation and benefits |

$ | 14,912 | $ | 14,260 | $ | 652 | 4.6 | % | ||||||||

| Fund management and administration |

14,991 | 10,272 | 4,719 | 45.9 | % | |||||||||||

| Marketing and advertising |

3,240 | 2,331 | 909 | 39.0 | % | |||||||||||

| Sales and business development |

2,612 | 1,972 | 640 | 32.5 | % | |||||||||||

| Professional and consulting fees |

3,922 | 2,526 | 1,396 | 55.3 | % | |||||||||||

| Occupancy, communications and equipment |

846 | 829 | 17 | 2.1 | % | |||||||||||

| Depreciation and amortization |

200 | 235 | (35 | ) | (14.9 | %) | ||||||||||

| Third-party sharing arrangements |

4,434 | 1,485 | 2,949 | 198.6 | % | |||||||||||

| Other |

1,625 | 1,258 | 367 | 29.2 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

$ | 46,782 | $ | 35,168 | $ | 11,614 | 33.0 | % | ||||||||

|

|

|

|

|

|

|

|||||||||||

| As a Percent of Revenues: |

Nine Months Ended Sept. 30, |

|||||||

| 2011 | 2010 | |||||||

| Compensation and benefits |

30.4 | % | 50.6 | % | ||||

| Fund management and administration |

30.6 | % | 36.4 | % | ||||

| Marketing and advertising |

6.6 | % | 8.3 | % | ||||

| Sales and business development |

5.3 | % | 7.0 | % | ||||

| Professional and consulting fees |

8.0 | % | 9.0 | % | ||||

| Occupancy, communications and equipment |

1.7 | % | 2.9 | % | ||||

| Depreciation and amortization |

0.4 | % | 0.8 | % | ||||

| Third-party sharing arrangements |

9.1 | % | 5.3 | % | ||||

| Other |

3.3 | % | 4.5 | % | ||||

|

|

|

|

|

|||||

| Total expenses |

95.5 | % | 124.7 | % | ||||

|

|

|

|

|

|||||

For the nine months ended September 30, 2011, our total expenses increased $11.6 million or 33.0% to $46.8 million as compared to $35.2 million in the comparable period in 2010. This increase was primarily due to higher fund management and administration expenses due to higher average asset balances, higher third-party sharing arrangements due to higher asset balances in our currency and fixed income ETFs, and higher marketing and advertising and sales and business development expenses to support our growth.

Compensation and benefits

Compensation and benefits expense increased 4.6% from $14.3 million in the nine months ended September 30, 2010 to $14.9 million in the comparable period in 2011 primarily due to higher accrued incentive compensation due to our strong year to date results, as well as costs associated with higher headcount. Our headcount increased from 56 at the end of September 2010 to 64 at the end of September 2011. Partly offsetting this increase was a decrease of $2.0 million in stock-based compensation as equity awards granted to employees in prior years with higher fair values become fully vested and replaced with a lower number of awards at lower fair values.

Fund management and administration

Fund management and administration expense increased 45.9% from $10.3 million in the nine months ended September 30, 2010 to $15.0 million in the comparable period in 2011. Higher average assets under management led to an increase of $3.3 million in portfolio management, fund administration and accounting, index licensing, and distribution fees. Included in the nine months ended September 30, 2011 is a one-time charge of $0.7 million related to reimbursing the WisdomTree India ETF for excess fees we collected as a result of overestimating the operating expense recapture fees for the India ETF’s fiscal year ended March 31, 2011. Lastly, printing related fees increased $0.3 million due to an increase in the number of shareholders owning our ETFs. We had 47 ETFs at the end of September 2011 compared to 44 at the end of September 2010.

23

Table of Contents

Marketing and advertising