Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - CROSSROADS LIQUIDATING TRUST | a50058708ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - CROSSROADS LIQUIDATING TRUST | a50058708ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - CROSSROADS LIQUIDATING TRUST | a50058708ex32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - CROSSROADS LIQUIDATING TRUST | a50058708ex32-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

FOR THE QUARTER ENDED SEPTEMBER 30, 2011.

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

COMMISSION FILE NUMBER: 0-53504

KEATING CAPITAL, INC.

(Exact name of registrant as specified in its charter)

|

Maryland

|

26-2582882

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

5251 DTC Parkway, Suite 1100

Greenwood Village, CO 80111

(Address of principal executive office)

(720) 889-0139

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o |

Accelerated filer ¨

|

|

| Non-accelerated filer x |

Smaller reporting company ¨

|

|

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

The number of shares of the issuer’s Common Stock, $0.001 par value, outstanding as of November 8, 2011 was 9,283,604.

TABLE OF CONTENTS

| 1 | |||||

| 1 | |||||

| 2 | |||||

| 3 | |||||

| 4 | |||||

| 5 | |||||

| 7 | |||||

| 8 | |||||

| 9 | |||||

| 24 | |||||

| 53 | |||||

| 53 | |||||

|

|

|||||

| 54 | |||||

| 54 | |||||

| 55 | |||||

| 55 | |||||

| 55 | |||||

| 56 | |||||

| 57 | |||||

|

|

58 | ||||

i

|

Financial Statements

|

Statement of Assets and Liabilities

(Unaudited)

| September 30, | December 31, | |||||||

| 2011 | 2010 | |||||||

|

Assets

|

||||||||

|

Investments in portfolio company securities at fair value:

|

||||||||

|

Non-control/non-affiliate investments:

|

||||||||

|

Private portfolio companies

|

||||||||

|

(Cost: $21,356,850 and $3,600,491, respectively)

|

$ | 21,115,681 | $ | 4,177,607 | ||||

|

Publicly-traded portfolio companies

|

||||||||

|

(Cost: $1,999,991 and $0, respectively)

|

2,078,000 | - | ||||||

|

Affiliate investments:

|

||||||||

|

Private portfolio companies

|

||||||||

|

(Cost: $8,000,080 and $0, respectively)

|

8,726,000 | - | ||||||

|

Total, investments in portfolio company securities at fair value

|

31,919,681 | 4,177,607 | ||||||

|

Short-term investments at fair value

|

||||||||

|

(Cost: $0 and $13,500,000, respectively)

|

- | 13,500,000 | ||||||

|

Cash and cash equivalents

|

45,082,822 | 4,753,299 | ||||||

|

Prepaid expenses and other assets

|

100,363 | 92,125 | ||||||

|

Deferred offering costs

|

- | 333,682 | ||||||

|

Total Assets

|

77,102,866 | 22,856,713 | ||||||

|

Liabilities

|

||||||||

|

Base management fees payable to Investment Adviser

|

129,512 | 90,631 | ||||||

|

Accrued incentive fees payable to Investment Adviser

|

112,552 | 115,423 | ||||||

|

Administrative expenses payable to Investment Adviser

|

32,792 | 41,348 | ||||||

|

Reimbursable expenses payable to Investment Adviser

|

- | 3,068 | ||||||

|

Accounts payable

|

49,356 | 80,275 | ||||||

|

Accrued expenses and other liabilities

|

28,304 | 69,568 | ||||||

|

Total Liabilities

|

352,516 | 400,313 | ||||||

|

Net Assets

|

$ | 76,750,350 | $ | 22,456,400 | ||||

|

Components of Net Assets:

|

||||||||

|

Common stock, $0.001 par value; 200,000,000 shares authorized;

|

||||||||

|

9,283,604 and 2,860,299 shares issued and outstanding as of

|

||||||||

|

September 30, 2011 and December 31, 2010, respectively

|

$ | 9,284 | $ | 2,860 | ||||

|

Additional paid-in capital

|

82,693,321 | 25,378,355 | ||||||

|

Accumulated undistributed net investment loss

|

(6,068,178 | ) | (3,501,931 | ) | ||||

|

Accumulated distributions in excess of net realized gains on investments

|

(446,837 | ) | - | |||||

|

Net unrealized appreciation on investments

|

562,760 | 577,116 | ||||||

|

Net Assets

|

$ | 76,750,350 | $ | 22,456,400 | ||||

|

Common Shares Outstanding

|

9,283,604 | 2,860,299 | ||||||

|

Net Asset Value Per Outstanding Common Share

|

$ | 8.27 | $ | 7.85 | ||||

The accompanying notes are an integral part of these financial statements.

1

|

Three Months Ended

|

Nine Months Ended

|

|||||||||||||||

|

September 30,

|

September 30,

|

September 30,

|

September 30,

|

|||||||||||||

|

2011

|

2010

|

2011

|

2010

|

|||||||||||||

|

Investment Income

|

||||||||||||||||

|

Interest and dividend income:

|

||||||||||||||||

|

Certificate of deposit and money market investments

|

$ | 6,382 | $ | 12,428 | $ | 49,660 | $ | 26,047 | ||||||||

|

Other income

|

- | - | - | 10,000 | ||||||||||||

|

Total Investment Income

|

6,382 | 12,428 | 49,660 | 36,047 | ||||||||||||

|

Operating Expenses

|

||||||||||||||||

|

Base management fees

|

389,007 | 59,709 | 764,375 | 128,245 | ||||||||||||

|

Incentive fees (decrease)

|

(155,391 | ) | - | (2,871 | ) | - | ||||||||||

|

Administrative expenses allocated from Investment Adviser

|

96,757 | 112,921 | 330,263 | 284,761 | ||||||||||||

|

Legal and professional fees

|

89,337 | 45,063 | 357,135 | 244,580 | ||||||||||||

|

Directors' fees

|

31,289 | 25,250 | 90,289 | 82,750 | ||||||||||||

|

Stock transfer agent fees

|

40,555 | 48,362 | 163,215 | 142,642 | ||||||||||||

|

Printing and fulfillment expenses

|

23,444 | 26,757 | 152,583 | 48,938 | ||||||||||||

|

Postage and delivery expenses

|

7,201 | 19,310 | 136,696 | 43,627 | ||||||||||||

|

Stock issuance expenses

|

1,625 | 8,747 | 114,388 | 115,940 | ||||||||||||

|

General and administrative expenses

|

65,772 | 80,495 | 509,834 | 172,141 | ||||||||||||

|

Total Operating Expenses

|

589,596 | 426,614 | 2,615,907 | 1,263,624 | ||||||||||||

|

Net Investment Loss

|

(583,214 | ) | (414,186 | ) | (2,566,247 | ) | (1,227,577 | ) | ||||||||

|

Net Change in Unrealized Appreciation (Depreciation) on Investments

|

||||||||||||||||

|

Non-control/non-affiliate investments

|

(1,502,874 | ) | 27,364 | (740,276 | ) | 577,364 | ||||||||||

|

Affiliate investments

|

725,920 | - | 725,920 | - | ||||||||||||

|

Net Change in Unrealized Appreciation (Depreciation) On Investments

|

(776,954 | ) | 27,364 | (14,356 | ) | 577,364 | ||||||||||

|

Net Decrease in Net Assets Resulting From Operations

|

$ | (1,360,168 | ) | $ | (386,822 | ) | $ | (2,580,603 | ) | $ | (650,213 | ) | ||||

|

Net Decrease in Net Assets Resulting from Operations

|

||||||||||||||||

|

Per Common Share

|

$ | (0.15 | ) | $ | (0.26 | ) | $ | (0.42 | ) | $ | (0.59 | ) | ||||

|

Weighted Average Number of Common Shares Outstanding:

|

||||||||||||||||

|

Basic and Diluted

|

9,103,658 | 1,493,101 | 6,125,439 | 1,097,041 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

2

Statements of Changes in Net Assets

(Unaudited)

|

Nine Months Ended

|

||||||||

|

September 30,

|

September 30,

|

|||||||

|

2011

|

2010

|

|||||||

|

Changes in Net Assets from Operations

|

||||||||

|

Net investment loss

|

$ | (2,566,247 | ) | $ | (1,227,577 | ) | ||

|

Net change in unrealized appreciation (depreciation) on investments

|

(14,356 | ) | 577,364 | |||||

|

Net Decrease in Net Assets Resulting from Operations

|

(2,580,603 | ) | (650,213 | ) | ||||

|

Changes in Net Assets from Stockholder Distributions

|

||||||||

|

Distributions in excess of net realized gains on investments

|

(446,837 | ) | - | |||||

|

Net Decrease in Net Assets Resulting from Stockholder Distributions

|

(446,837 | ) | - | |||||

|

Changes in Net Assets from Capital Stock Transactions

|

||||||||

|

Issuance of common stock in continuous public offering (1)

|

63,990,347 | 11,884,658 | ||||||

|

Offering costs from issuance of common stock

|

(6,180,594 | ) | (1,147,023 | ) | ||||

|

Amortization of deferred offering costs

|

(488,363 | ) | (327,014 | ) | ||||

|

Net Increase in Net Assets Resulting From Capital Stock Transactions

|

57,321,390 | 10,410,621 | ||||||

|

Net Increase in Net Assets

|

54,293,950 | 9,760,408 | ||||||

|

Net assets at beginning of period

|

22,456,400 | 3,719,496 | ||||||

|

Net Assets at End of Period (2)

|

$ | 76,750,350 | $ | 13,479,904 | ||||

|

(1)

|

All shares were sold at a price of either $9.30 or $10.00, depending on whether or not sales commissions were waived by the dealer manager.

|

|

(2)

|

Net Assets at September 30, 2011 and 2010 include no accumulated undistributed net investment income and no accumulated undistributed net realized gains.

|

The accompanying notes are an integral part of these financial statements.

3

|

Nine Months Ended

|

||||||||

|

September 30,

|

September 30,

|

|||||||

|

2011

|

2010

|

|||||||

|

Cash Flows From Operating Activities

|

||||||||

|

Net decrease in net assets resulting from operations

|

$ | (2,580,603 | ) | $ | (650,213 | ) | ||

|

Adjustments to reconcile net decrease in net assets resulting from operations

|

||||||||

|

to net cash used in operating activities:

|

||||||||

|

Net change in unrealized depreciation (appreciation) on investments

|

14,356 | (577,364 | ) | |||||

|

Changes in operating assets and liabilities:

|

||||||||

|

(Increase) in prepaid expenses and other assets

|

(8,238 | ) | (52,339 | ) | ||||

|

Increase in base management fees payable to Investment Adviser

|

38,881 | 30,241 | ||||||

|

(Decrease) in accrued incentive fees payable to Investment Adviser

|

(2,871 | ) | - | |||||

|

(Decrease) increase in administrative expenses payable to Investment Adviser

|

(8,556 | ) | 45,785 | |||||

|

(Decrease) in reimbursable expenses payable to Investment Adviser

|

(3,068 | ) | (18,063 | ) | ||||

|

(Decrease) increase in accounts payable

|

(30,919 | ) | 16,964 | |||||

|

(Decrease) increase in accrued expenses and other liabilities

|

(41,264 | ) | 3,240 | |||||

|

Net cash used in operating activities

|

(2,622,282 | ) | (1,201,749 | ) | ||||

|

Cash Flows From Investing Activities

|

||||||||

|

Investments in portfolio companies

|

(27,756,430 | ) | (2,500,491 | ) | ||||

|

Purchases of short-term investments

|

(89,000,000 | ) | (52,500,000 | ) | ||||

|

Proceeds from maturities of short-term investments

|

102,500,000 | 47,500,000 | ||||||

|

Net cash provided by (used in) investing activities

|

(14,256,430 | ) | (7,500,491 | ) | ||||

|

Cash Flows From Financing Activities

|

||||||||

|

Gross proceeds from issuance of common stock

|

63,990,347 | 11,884,658 | ||||||

|

Offering costs from issuance of common stock

|

(6,180,594 | ) | (1,147,023 | ) | ||||

|

Additions to deferred stock offering costs

|

(154,681 | ) | (210,875 | ) | ||||

|

Stockholder distributions

|

(446,837 | ) | - | |||||

|

Net cash provided by financing activities

|

57,208,235 | 10,526,760 | ||||||

|

Net increase in cash and cash equivalents

|

40,329,523 | 1,824,520 | ||||||

|

Cash and cash equivalents, beginning of period

|

4,753,299 | 367,918 | ||||||

|

Cash and cash equivalents, end of period

|

$ | 45,082,822 | $ | 2,192,438 | ||||

|

Supplemental Disclosure of Non-Cash Financing Activities

|

||||||||

|

Amortization of deferred offering costs

|

$ | 488,363 | $ | 327,014 | ||||

The accompanying notes are an integral part of these financial statements.

4

|

% of

|

||||||||||||||||||||

|

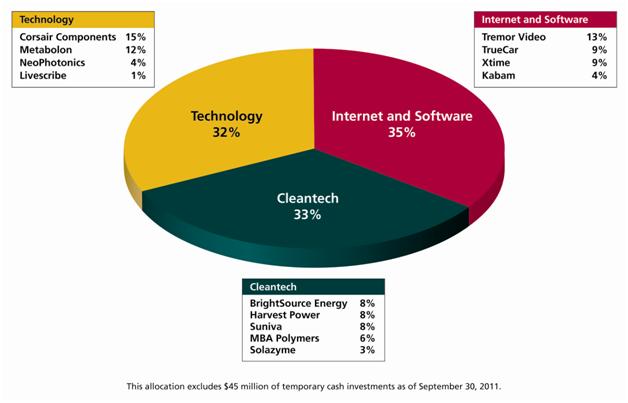

Portfolio Company

|

Industry / Description

|

Type of Investment

|

Shares

|

Cost

|

Fair Value

|

Net Assets

|

||||||||||||||

|

Non-Control/Non-Affiliate Investments (1)

|

||||||||||||||||||||

|

Private Portfolio Companies:

|

||||||||||||||||||||

|

Livescribe, Inc.

|

Technology - Consumer Electronics

|

Series C Convertible Preferred Stock (3)(4)

|

1,000,000 | 471,295 | 257,000 | 0.33 | % | |||||||||||||

|

Series C Convertible Preferred Stock Warrants (7)

|

125,000 | 29,205 | 6,229 | 0.01 | % | |||||||||||||||

|

Series C-1 Convertible Preferred Stock (3)(4)

|

54,906 | 25,925 | 14,001 | 0.02 | % | |||||||||||||||

|

Series C-1 Convertible Preferred Stock Warrants (8)

|

6,863 | 1,556 | 426 | 0.00 | % | |||||||||||||||

|

MBA Polymers, Inc.

|

Cleantech - Plastics Recycling

|

Series G Convertible Preferred Stock (3)(4)

|

2,000,000 | 2,000,000 | 2,000,000 | 2.61 | % | |||||||||||||

|

BrightSource Energy, Inc.

|

Cleantech - Solar Thermal Energy

|

Series E Convertible Preferred Stock (3)(4)

|

288,531 | 2,500,006 | 2,500,006 | 3.26 | % | |||||||||||||

|

Harvest Power, Inc.

|

Cleantech - Waste Management

|

Series B Convertible Preferred Stock (3)(5)

|

580,496 | 2,499,999 | 2,499,999 | 3.26 | % | |||||||||||||

|

Suniva, Inc.

|

Cleantech - Solar Photovoltaic Cells

|

Series D Convertible Preferred Stock (3)(4)

|

197,942 | 2,500,007 | 2,500,007 | 3.26 | % | |||||||||||||

|

Xtime, Inc.

|

Internet & Software - Software as a Service

|

Series F Convertible Preferred Stock (3)(4)

|

1,573,234 | 3,000,000 | 3,000,000 | 3.91 | % | |||||||||||||

|

Common Stock Warrants (9)

|

22,581 | - | 9,156 | 0.01 | % | |||||||||||||||

|

Kabam, Inc.

|

Internet & Software - Online Multiplayer Games

|

Series D Convertible Preferred Stock (3)(4)

|

1,046,017 | 1,328,860 | 1,328,860 | 1.73 | % | |||||||||||||

|

Tremor Video, Inc.

|

Internet & Software - Online Video Advertising

|

Series F Convertible Preferred Stock (3)(4)

|

642,994 | 4,000,001 | 4,000,001 | 5.20 | % | |||||||||||||

|

TrueCar, Inc.

|

Internet & Software - Consumer Website

|

Common Stock (6)

|

566,037 | 2,999,996 | 2,999,996 | 3.91 | % | |||||||||||||

|

Subtotal - Non-Control/Non-Affiliate Investments, Private Portfolio Companies

|

$ | 21,356,850 | $ | 21,115,681 | 27.51 | % | ||||||||||||||

|

Publicly-Traded Portfolio Companies:

|

||||||||||||||||||||

|

NeoPhotonics Corporation

|

Technology - Communications Equipment

|

Common Stock (11)

|

160,000 | 1,000,000 | 1,101,000 | 1.43 | % | |||||||||||||

|

Solazyme, Inc.

|

Cleantech - Renewable Oils and Bioproducts

|

Common Stock (12)

|

112,927 | 999,991 | 977,000 | 1.27 | % | |||||||||||||

|

Subtotal - Non-Control/Non-Affiliate Investments, Publicly-Traded Portfolio Companies

|

$ | 1,999,991 | $ | 2,078,000 | 2.70 | % | ||||||||||||||

|

Affiliate Investments (1)

|

||||||||||||||||||||

|

Private Portfolio Companies:

|

||||||||||||||||||||

|

Metabolon, Inc.

|

Technology - Molecular Diagnostics and Services

|

Series D Convertible Preferred Stock (3)(4)

|

2,229,021 | 4,000,000 | 4,000,000 | 5.21 | % | |||||||||||||

|

Corsair Components, Inc.

|

Technology - PC Gaming Hardware

|

Common Stock (6)

|

3,200,000 | 3,411,080 | 4,096,000 | 5.34 | % | |||||||||||||

|

Common Stock Warrants (10)

|

800,000 | 589,000 | 630,000 | 0.82 | % | |||||||||||||||

|

Subtotal - Affiliate Investments, Private Portfolio Companies

|

$ | 8,000,080 | $ | 8,726,000 | 11.37 | % | ||||||||||||||

|

Total - Investments in Portfolio Company Securities (2)

|

$ | 31,356,921 | $ | 31,919,681 | 41.59 | % | ||||||||||||||

The accompanying notes are an integral part of these financial statements.

5

Schedule of Investments

September 30, 2011

(Unaudited)

|

% of

|

|||||

|

Reconciliation to Net Assets

|

Amount

|

Net Assets

|

|||

|

Investments in portfolio company securities at fair value

|

$ |

31,919,681

|

41.59%

|

||

|

Cash and cash equivalents

|

45,082,822

|

58.74%

|

|||

|

Prepaid expenses and other assets

|

100,363

|

0.13%

|

|||

|

Less: Total Liabilities

|

(352,516)

|

-0.46%

|

|||

|

Net Assets

|

$ |

76,750,350

|

100.00%

|

||

|

(1)

|

Control investments are defined by the Investment Company Act of 1940, as amended (the "1940 Act"), as investments in which more than 25% of the voting securities are owned or where the ability to nominate greater

|

|

than 50% of the board representation is maintained. Affiliate investments are defined by the 1940 Act as investments in which between 5% and 25% of the voting securities are owned.

|

|

|

Non-Control/Non-Affiliate investments are defined by the 1940 Act as investments that are neither Control Investments nor Affiliate Investments.

|

|

|

(2)

|

The aggregate cost basis for federal income tax purposes of investments in portfolio company securities is $31,356,921. The gross unrealized appreciation based on the tax cost basis of these securities is $836,076.

|

|

The gross unrealized depreciation based on the tax cost basis of these securities is $273,316. The net unrealized appreciation based on the tax cost basis of these securities is $562,760.

|

|

|

(3)

|

The shares of common and preferred stock represented by these investments are subject to legal restrictions on transfer pursuant to the Securities Act of 1933, as amended (the "Securities Act") and may only be sold

|

|

pursuant to a registration statement under the Securities Act or an available exemption from registration thereunder. These shares are also subject to a contractual lockup for a period of six months following completion of an

|

|

|

initial public offering.

|

|

|

(4)

|

The shares of preferred stock represented by these investments carry a non-cumulative, preferred dividend payable when and if declared by the portfolio company's board of directors.

|

|

Since no dividends have been declared or paid with respect to these investments, these investments are considered to be non-income producing.

|

|

|

(5)

|

The shares of preferred stock represented by this investment carry a cumulative preferred dividend, which is payable only when declared by the portfolio company's board of directors or upon a qualifying liquidation event.

|

|

Since no dividends have been declared or paid with respect to this investment, this investment is considered to be non-income producing.

|

|

|

(6)

|

The shares of common stock represented by these investments are considered to be non-income producing.

|

|

(7)

|

The warrants grant the holder the right to purchase shares of Series C convertible preferred stock at an exercise price of $0.50 per share, have a contractual life of five years, and expire on June 30, 2015.

|

|

(8)

|

The warrants grant the holder the right to purchase shares of Series C-1 convertible preferred stock at an exercise price of $0.50 per share, have a contractual life of five years, and expire on July 8, 2016.

|

|

(9)

|

The warrants grant the holder the right to purchase shares of common stock at an exercise price of $0.01 per share, have a contractual life of seven years, and expire on August 24, 2018. In the event the issuer completes a qualifying IPO, the number of warrants will be reduced by 50%.

|

|

(10)

|

The warrants grant the holder the right to purchase up to 800,000 shares of common stock from certain selling stockholders at an exercise price of $0.01 per share. The warrants expire on the earlier of: (i) the consummation of an

an initial public offering ("IPO") by Corsair Components, Inc. ("Corsair") at an offering price of at least $2.50 per share of common stock, (ii) upon a sale of Corsair which results in holders of Corsair common stock receiving

net sales proceeds of at least $2.50 per share, or (iii) July 6, 2016. The warrants are exercisable only upon: (i) Corsair completing an IPO of its common stock at an offering price of less than $2.50 per share, (ii) a sale of Corsair which results in holders of Corsair common stock receiving net sales proceeds of less than $2.50 per share, and (iii) if Corsair does not complete an IPO or sale prior to July 6, 2016, the warrants will be deemed to have been automatically exercised on such date. If the warrants become exercisable as a result of an IPO or sale of Corsair, the number of warrants will be proportionately decreased from 800,000 to the extent that the IPO price or net sales proceeds, as the case may be, exceeds $2.00 per share but is less than $2.50 per share, and the number of warrants will be reduced to zero if the IPO price or net sale proceeds, as the case may be, equals or exceeds $2.50 per share.

|

|

(11)

|

On February 2, 2011, NeoPhotonics completed an initial public offering of its common stock at a price of $11.00 per share. Immediately prior to the initial public offering, the Company’s Series X convertible preferred stock

|

|

converted into 160,000 shares of NeoPhotonics common stock, which common shares were subject to a 180 day lockup provision that expired in August 2011.

|

|

|

(12)

|

On May 27, 2011, Solazyme completed an initial public offering of its common stock at a price of $18.00 per share. Immediately prior to the initial public offering, the Company’s Series D convertible preferred stock

|

|

converted into 112,927 shares of Solazyme common stock, which common shares are subject to a 180 day lockup provision expiring in November 2011.

|

The accompanying notes are an integral part of these financial statements.

6

|

% of

|

||||||||||||||||||||

|

Portfolio Company

|

Industry / Description

|

Type of Investment

|

Shares

|

Cost

|

Fair Value

|

Net Assets

|

||||||||||||||

|

Non-Control/Non-Affiliate Investments (1)

|

||||||||||||||||||||

|

Private Portfolio Companies:

|

||||||||||||||||||||

|

NeoPhotonics Corporation

|

Technology - Communications Equipment

|

Series X Convertible Preferred Stock (3)(4)(7)

|

10,000 | $ | 1,000,000 | $ | 1,550,000 | 6.90 | % | |||||||||||

|

Livescribe, Inc.

|

Technology - Consumer Electronics

|

Series C Convertible Preferred Stock (3)(4)

|

1,000,000 | 471,295 | 500,000 | 2.23 | % | |||||||||||||

| Series C Convertible Preferred Stock Warrants (5) | 125,000 | 29,205 | 27,616 | 0.12 | % | |||||||||||||||

|

Solazyme, Inc.

|

Cleantech - Renewable Oils and Bioproducts

|

Series D Convertible Preferred Stock (3)(4)

|

112,927 | 999,991 | 999,991 | 4.45 | % | |||||||||||||

|

MBA Polymers, Inc.

|

Cleantech - Plastics Recycling

|

Series G Convertible Preferred Stock (3)(4)

|

1,100,000 | 1,100,000 | 1,100,000 | 4.90 | % | |||||||||||||

|

Total - Investments in Portfolio Company Securities (2)

|

$ | 3,600,491 | $ | 4,177,607 | 18.60 | % | ||||||||||||||

|

Short-Term Investments

|

||||||||||||||||||||

|

Certificates of Deposit Maturing on January 6, 2011 (6)

|

||||||||||||||||||||

|

Annual Percentage Yield of 0.45%

|

$ | 13,500,000 | $ | 13,500,000 | 60.12 | % | ||||||||||||||

|

Total - Short-Term Investments

|

$ | 13,500,000 | $ | 13,500,000 | 60.12 | % | ||||||||||||||

|

Total - Investments in Portfolio Company Securities and Short-Term Investments

|

$ | 17,100,491 | $ | 17,677,607 | 78.72 | % | ||||||||||||||

|

% of

|

||||||||||||||||||||

|

Reconciliation to Net Assets

|

Amount

|

Net Assets

|

||||||||||||||||||

|

Investments in portfolio company securities and short-term investments

|

$ | 17,677,607 | 78.72 | % | ||||||||||||||||

|

Cash and cash equivalents

|

4,753,299 | 21.17 | % | |||||||||||||||||

|

Prepaid expenses and other assets

|

92,125 | 0.41 | % | |||||||||||||||||

|

Deferred offering costs

|

333,682 | 1.48 | % | |||||||||||||||||

|

Less: Total Liabilities

|

(400,313 | ) | -1.78 | % | ||||||||||||||||

|

Net Assets

|

$ | 22,456,400 | 100.00 | % | ||||||||||||||||

|

(1)

|

Control investments are defined by the Investment Company Act of 1940, as amended (the "1940 Act"), as investments in which more than 25% of the voting securities are owned or where the ability to nominate greater

|

|

than 50% of the board representation is maintained. Affiliate investments are defined by the 1940 Act as investments in which between 5% and 25% of the voting securities are owned.

|

|

|

Non-Control/Non-Affiliate investments are defined by the 1940 Act as investments that are neither Control Investments nor Affiliate Investments.

|

|

|

(2)

|

The aggregate cost basis for federal income tax purposes of Non-Control/Non-Affiliate investments is $3,600,491. The gross unrealized appreciation based on the tax cost basis of these securities is $578,705.

|

|

The gross unrealized depreciation based on the tax cost basis of these securities is $1,589.

|

|

|

(3)

|

The shares of preferred stock represented by these investments are subject to legal restrictions on transfer pursuant to the Securities Act and may only be sold pursuant to a registration statement

|

|

under the Securities Act or an available exemption from registration thereunder. These shares are also subject to a contractual lockup for a period of 180 days following completion of an initial public offering.

|

|

|

(4)

|

The shares of preferred stock represented by these investments carry a non-cumulative, preferred dividend payable when and if declared by the portfolio company's board of directors.

|

|

Since no dividends have been declared or paid with respect to these investments, these investments are considered to be non-income producing.

|

|

|

(5)

|

The warrants grant the holder the right to purchase shares of Series C convertible preferred stock at an exercise price of $0.50 per share, have a contractual life of five years, and expire on June 30, 2015.

|

|

(6)

|

Fair value reflects amortized cost as of December 31, 2010.

|

|

(7)

|

On February 2, 2011, NeoPhotonics completed an initial public offering of its common stock at a price of $11.00 per share. Immediately prior to the initial public offering, the Company’s Series X convertible preferred

|

|

stock converted into 160,000 shares of NeoPhotonics common stock, which common shares were subject to a 180 day lockup provision that expired in August 2011.

|

The accompanying notes are an integral part of these financial statements.

7

|

Nine Months Ended

|

||||||||

|

September 30,

|

September 30,

|

|||||||

|

2011

|

2010

|

|||||||

|

Per Common Share Data

|

||||||||

|

Net asset value, beginning of period (1)

|

$ | 7.85 | $ | 6.53 | ||||

|

Net investment loss (2)

|

(0.42 | ) | (1.12 | ) | ||||

|

Net change in unrealized appreciation on investments (2)

|

- | 0.53 | ||||||

|

Net (decrease) increase in net assets resulting from operations

|

(0.42 | ) | (0.59 | ) | ||||

|

Stockholder distributions:

|

||||||||

|

Distributions in excess of net realized gains on investments (2)

|

(0.07 | ) | - | |||||

|

Net decrease in net assets resulting for stockholder distributions

|

(0.07 | ) | - | |||||

|

Capital stock transactions:

|

||||||||

|

Issuance of common stock in continuous public offering (3)

|

2.00 | 3.06 | ||||||

|

Offering costs from issuance of common stock (2)

|

(1.01 | ) | (1.05 | ) | ||||

|

Amortization of deferred offering costs (2)

|

(0.08 | ) | (0.30 | ) | ||||

|

Net increase in net assets from capital stock transactions

|

0.91 | 1.71 | ||||||

|

Net asset value, end of period (1)

|

$ | 8.27 | $ | 7.65 | ||||

|

Common shares outstanding, beginning of period

|

2,860,299 | 569,900 | ||||||

|

Common shares outstanding, end of period

|

9,283,604 | 1,762,971 | ||||||

|

Weighted average common shares outstanding during period

|

6,125,439 | 1,097,041 | ||||||

|

Total return based on change in net asset value and stockholder distributions (4)

|

17.15 | % | ||||||

|

Supplemental Data and Ratios

|

||||||||

|

Net assets, beginning of period

|

$ | 22,456,400 | $ | 3,719,496 | ||||

|

Net assets, end of period

|

$ | 76,750,350 | $ | 13,479,904 | ||||

|

Average net assets during period

|

$ | 49,603,375 | $ | 8,599,700 | ||||

|

Annualized ratio of operating expenses to average net assets

|

7.03 | % | 19.59 | % | ||||

|

Annualized ratio of net investment loss to average net assets

|

-6.90 | % | -19.03 | % | ||||

|

Portfolio turnover (5)

|

- | - | ||||||

|

(1)

|

Based on total shares outstanding at the beginning and end of the corresponding period.

|

|

(2)

|

Based on weighted average shares outstanding during the period.

|

|

(3)

|

Represents the average increase in net asset value attributable to each share issued during the nine months ended September 30, 2011 and 2010.

|

|

(4)

|

Total return for the nine months ended September 30, 2011 and 2010 was calculated as the change in net asset value per share for each period, plus stockholder distributions per weighted average share paid during each period, divided by the net asset value per share at the beginning of the period. For the nine months ended September 30, 2011 and 2010, total return has not been annualized.

|

|

(5)

|

For the nine months ended September 30, 2011 and 2010, the only investment activity subject to the calculation of portfolio turnover was an aggregate of $27,756,430 and $2,500,491, respectively, in portfolio company investments. Since there were no sales of portfolio company investments during these periods, there was no portfolio turnover.

|

The accompanying notes are an integral part of these financial statements.

8

Notes to Financial Statements

(Unaudited)

1. Organization

Keating Capital, Inc. (“Keating Capital” or the “Company”) was incorporated on May 9, 2008 under the laws of the State of Maryland and is an externally managed, non-diversified, closed-end management investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940, as amended (the “1940 Act”), as of November 20, 2008. During 2010, the Company satisfied the requirements to qualify as a regulated investment company (“RIC”) and has elected to be treated as a RIC under Subchapter M of the Internal Revenue Code (the “Code”) effective for the 2010 tax year (see Federal and State Income Taxes under Note 2).

The Company specializes in making pre-initial public offering (“IPO”) investments in innovative, high growth private companies that are committed to and capable of becoming public. The Company generally acquires equity securities, including convertible preferred securities that are convertible into common stock, common stock, and warrants exercisable into common or preferred stock. The Company may in some cases invest in debentures that are convertible into common stock. The Company’s investments are made principally through direct investments in prospective portfolio companies. However, the Company may also purchase equity securities in secondary transactions from selling stockholders in later stage, private, pre-IPO companies, who are typically either current or former management or early stage investors in these companies.

Keating Investments, LLC (“Keating Investments” or the “Investment Adviser”) serves as the Company’s external investment adviser and also provides the Company with administrative services necessary for it to operate. In this capacity, Keating Investments is primarily responsible for the selection, evaluation, structure, valuation and administration of the Company’s investment portfolio, subject to the supervision of the Company’s Board of Directors. Keating Investments is a registered investment adviser under the Investment Advisers Act of 1940, as amended.

2. Significant Accounting Policies

Basis of Presentation

The interim financial statements of the Company are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and pursuant to the requirements for reporting on Form 10-Q and Regulation S-X. In the opinion of management, all adjustments, all of which were of a normal recurring nature, considered necessary for the fair presentation of financial statements for the interim period have been included. The results of operations for the current period are not necessarily indicative of results that ultimately may be achieved for any other interim period or for the year ending December 31, 2011. The interim unaudited financial statements and notes hereto should be read in conjunction with the audited financial statements and notes thereto contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010.

Consolidation

Under the 1940 Act rules and the regulations pursuant to Article 6 of Regulation S-X, the Company is precluded from consolidating any entity other than another investment company or an operating company that provides substantially all of its services and benefits to the Company. The Company’s financial statements include only the accounts of Keating Capital as the Company has no subsidiaries.

Reclassifications

For the three and nine months ended September 30, 2011, the Company separately classified Stock Transfer Agent Fees, Printing and Fulfillment Expenses, and Postage and Delivery Expenses as individual line items in its Statement of Operations. Stock Transfer Agent Fees were previously included as a component of Legal and Professional Fees, and Printing and Fulfillment Expenses and Postage and Delivery Expenses were previously included as components of General and Administrative Expenses in the Statement of Operations. For comparative purposes, these line items have also been separately classified in the Company’s Statement of Operations for the three and nine months ended September 30, 2010.

Use of Estimates

The preparation of financial statements in conformity with Generally Accepted Accounting Principles in the United States of America (“GAAP”) requires the Company’s management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reported period. Actual results could differ from these estimates and the differences could be material. The Company considers its significant estimates to include the fair value of investments in portfolio company securities (see Note 3).

9

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

Valuation of Investments

Investments are stated at value as defined under the 1940 Act, in accordance with the applicable regulations of the Securities and Exchange Commission (the “SEC”) and in accordance with Accounting Standards Codification Topic 820, “Fair Value Measurement and Disclosures,” (“ASC 820”). Value, as defined in Section 2(a)(41) of the 1940 Act, is: (i) the market price for those securities for which a market quotation is readily available, and (ii) the fair value as determined in good faith by, or under the direction of, the Board of Directors for all other assets (see Note 3).

At September 30, 2011, the Company’s financial statements included portfolio company investments valued at $31,919,681, with a cost of $31,356,921. The fair value of the Company’s portfolio company investments was determined in good faith by the Company’s Board of Directors and in accordance with ASC 820. Upon sale of the Company’s portfolio company investments, the value that is ultimately realized could be different from what is currently reflected in the Company’s financial statements, and this difference could be material.

Portfolio Company Investment Classification

The Company classifies its portfolio company investments in accordance with the requirements of the 1940 Act. Under the 1940 Act, “Control Investments” are defined as investments in which the Company owns more than 25% of the voting securities or has rights to maintain greater than 50% of the board representation. Under the 1940 Act, “Affiliate Investments” are defined as investments in which the Company owns between 5% and 25% of the voting securities. Under the 1940 Act, “Non-Control/Non-Affiliate Investments” are defined as investments that are neither Control Investments nor Affiliate Investments.

Cash and Cash Equivalents

Cash and cash equivalents are comprised of demand deposits and investments in money market funds with original maturities of 90 days or less.

Deferred Offering Costs

Deferred offering costs were comprised of expenses directly related to the continuous public offering of the Company’s common stock, which concluded on June 30, 2011. These expenses were initially deferred and subsequently amortized and charged against the gross proceeds of the continuous public offering, as a reduction to additional paid-in capital, on a straight-line basis beginning with the closing of the first common stock issuance on January 11, 2010 and continuing through the conclusion of the offering period on June 30, 2011. Offering expenses incurred subsequent to January 11, 2010 associated with maintaining the registration of the continuous public offering (e.g., legal, accounting, printing and blue sky) were expensed as incurred, while other offering-related expenses were capitalized and subsequently charged against the gross proceeds of the continuous public offering on a straight-line basis through June 30, 2011 (see Note 6).

Concentration of Credit Risk

The Company may place its cash and cash equivalents with various financial institutions and, at times, cash held in depository accounts at such institutions may exceed the Federal Deposit Insurance Corporation insured limit.

Securities Transactions

Securities transactions are accounted for on the date the transaction for the purchase or sale of the securities is entered into by the Company (i.e., trade date). Securities transactions outside conventional channels, such as private transactions, are recorded as of the date the Company obtains the right to demand the securities purchased or to collect the proceeds from a sale, and incurs an obligation to pay for securities purchased or to deliver securities sold, respectively.

Interest and Dividend Income

Interest income from certificates of deposit and other short-term investments is recorded on an accrual basis to the extent such amounts are expected to be collected, and accrued interest income is evaluated periodically for collectability.

The Company’s preferred equity investments may pay fixed or adjustable rate non-cumulative dividends and will generally have a “preference” over common equity in the payment of non-cumulative dividends and the liquidation of a portfolio company's assets. In order to be payable, non-cumulative distributions on such preferred equity must be declared by the portfolio company's board of directors. Non-cumulative dividend income from preferred equity investments in portfolio companies is recorded when such dividends are declared or at the point an obligation exists for a portfolio company to make a distribution.

10

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

In limited instances, the Company’s preferred equity investments may include cumulative dividend provisions, where such cumulative dividends, whether or not declared, accrue at a specified rate from the original investment date, have a “preference” over other classes of preferred equity and common equity with respect to payment, and are payable only when declared by a portfolio company’s board of directors or upon a qualifying liquidation event. Cumulative dividends are recorded when such dividends are declared by the portfolio company’s board of directors, or when a specified event occurs triggering an obligation to pay such dividends. When recorded, cumulative dividends are added to the balance of the preferred equity investment and are recorded as dividend income in the statement of operations.

During the three and nine months ended September 30, 2011 and 2010, there were no non-cumulative or cumulative dividends recorded.

Other Income

Other income is comprised of fees, if any, for due diligence, structuring, transaction services, consulting services and management services rendered to portfolio companies and prospective portfolio companies. For services that are separately identifiable from the Company’s investment, income is recognized as earned, which is generally when the investment or other applicable transaction closes, or when the services are rendered if payment is not subject to the closing of an investment transaction.

During the nine months ended September 30, 2010, the Company recorded $10,000 in other income representing a non-refundable due diligence fee received from a prospective portfolio company in December of 2009, which was initially recorded as deferred income and was subsequently recognized as income when the proposed investment transaction failed to close in February 2010.

Realized Gain or Loss and Unrealized Appreciation or Depreciation of Portfolio Investments

Realized gain or loss is recognized when an investment is disposed of and is computed as the difference between the Company's cost basis in the investment at the disposition date and the net proceeds received from such disposition. Realized gains and losses on investment transactions are determined by specific identification. Unrealized appreciation or depreciation is computed as the difference between the fair value of the investment and the cost basis of such investment.

Federal and State Income Taxes

During 2010, the Company satisfied the requirements to qualify as a RIC under Subchapter M of the Code and has elected to be treated as a RIC for U.S. federal income tax purposes effective for the 2010 tax year. To maintain RIC tax treatment, the Company must meet specified source-of-income and asset diversification requirements and distribute annually at least 90% of its investment company taxable income (which is generally the Company’s net ordinary income plus the excess, if any, of realized net short-term capital gains over realized net long-term capital losses).

As a RIC, the Company generally will not have to pay corporate-level federal income taxes on any investment company taxable income or any realized net capital gains (which is generally realized net long-term capital gains in excess of realized net short-term capital losses) that the Company distributes to its stockholders. In the event the Company retains any of its realized net capital gains, including amounts retained to pay incentive fees to the Investment Adviser or to pay annual operating expenses, the Company will likely designate the retained amount as a deemed distribution to stockholders and will be required to pay corporate-level tax on the retained amount.

The Company would also be subject to certain excise taxes imposed on RICs if it fails to distribute during each calendar year an amount at least equal to the sum of: (i) 98% of its ordinary income for the calendar year, (ii) 98.2% of its capital gains in excess of capital losses for the one-year period ending on October 31 of the calendar year, and (iii) any ordinary income and net capital gains for preceding years that were not distributed during such years. The Company will not be subject to this excise tax on amounts on which the Company is required to pay corporate income tax (such as retained realized net capital gains).

The Company has made no provision for income taxes as of September 30, 2011 since it expects to continue to qualify as a RIC for its 2011 taxable year and did not generate any investment company taxable income or realized net capital gains during the three or nine months ended September 30, 2011.

11

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

| The Company evaluates tax positions taken or expected to be taken in the course of preparing its tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions deemed to meet a “more-likely-than-not” threshold would be recorded as a tax benefit or expense in the applicable period. Although the Company files federal and state tax returns, its major tax jurisdiction is federal. The 2008, 2009 and 2010 federal tax years for the Company remain subject to examination by the Internal Revenue Service. | |

|

As of September 30, 2011 and December 31, 2010, the Company had not recorded a liability for any unrecognized tax positions. Management’s evaluation of uncertain tax positions may be subject to review and adjustment at a later date based upon factors including, but not limited to, an on-going analysis of tax laws, regulations and interpretations thereof. The Company’s policy is to include interest and penalties related to income taxes, if applicable, in general and administrative expenses. There were no such expenses for the three and nine months ending September 30, 2011 and 2010.

|

|

|

The aggregate cost of portfolio company securities for federal income tax purposes and portfolio company securities with unrealized appreciation and depreciation based on tax cost basis, were as follows as of September 30, 2011 and December 31, 2010:

|

|

September 30,

|

December 31,

|

||||||||

|

2011

|

2010

|

||||||||

|

Aggregate cost of portfolio company securities

|

|||||||||

|

for federal income tax purposes

|

$ | 31,356,921 | $ | 3,600,491 | |||||

|

Gross unrealized appreciation of portfolio company securities

|

836,076 | 578,705 | |||||||

|

Gross unrealized depreciation of portfolio company securities

|

(273,316 | ) | (1,589 | ) | |||||

|

Net unrealized appreciation of portfolio company securities

|

$ | 562,760 | $ | 577,116 | |||||

|

Dividends and Distributions

|

|

|

Dividends and distributions to common stockholders are recorded when declared.

|

|

|

Net realized capital gains, if any, after reduction for any incentive fees payable to the Investment Adviser, annual operating expenses and any other retained amounts, are expected to be distributed at least annually. In the event the Company retains some or all of its realized net capital gains, including amounts retained to pay incentive fees to the Investment Adviser or annual operating expenses, the Company will likely designate the retained amount as a deemed distribution to stockholders. In such case, among other consequences, the Company will pay corporate-level tax on the retained amount, each U.S. stockholder will be required to include its share of the deemed distribution in income as if it had been actually distributed to the U.S. stockholder, and the U.S. stockholder will be entitled to claim a credit or refund equal to its allocable share of the corporate-level tax the Company pays on the retained realized net capital gain.

|

|

|

On February 11, 2011, the Company’s Board of Directors declared a special cash distribution of $446,837, or $0.13 per share outstanding on the record date. The distribution was paid on February 17, 2011 to the Company’s stockholders of record as of February 15, 2011 (see Note 7).

|

|

|

Per Share Information

|

|

|

Net changes in net assets resulting from operations per common share, or basic earnings per share, are calculated using the weighted average number of common shares outstanding for the period presented. Diluted earnings per share are not presented as there are no potentially dilutive securities outstanding.

|

|

|

Recently Issued Accounting Pronouncements

|

|

|

From time to time, new accounting pronouncements are issued by the Financial Accounting Standards Board (“FASB”) or other standards setting bodies that are adopted by the Company as of the specified effective date. Unless otherwise discussed, the Company believes that the impact of recently issued standards that are not yet effective will not have a material impact on its financial statements upon adoption.

|

12

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

In May 2011, the FASB issued Accounting Standards Update No. 2011-04 - Fair Value Measurement: Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRS, or ASU 2011-04. ASU 2011-04 clarifies the application of existing fair value measurement and disclosure requirements, changes the application of some requirements for measuring fair value and requires additional disclosure for fair value measurements. In addition, the disclosure requirements are expanded to include for fair value measurements categorized in Level 3 of the fair value hierarchy: (i) a quantitative disclosure of the unobservable inputs and assumptions used in the measurement; (ii) a description of the valuation processes in place; and (iii) a narrative description of the sensitivity of the fair value to changes in unobservable inputs and interrelationships between those inputs. ASU 2011-04 is effective for interim and annual periods beginning after December 15, 2011, for public entities. The Company is evaluating the impact that the adoption of this update may have on its financial position, results of operations and related disclosures.

3. Valuation of Investments

The 1940 Act requires periodic valuation of each investment in the Company’s portfolio to determine the Company’s net asset value. Under the 1940 Act, unrestricted securities with readily available market quotations are to be valued at the current market value; all other assets must be valued at fair value as determined in good faith by or under the direction of the Board of Directors.

Investments for which market quotations are readily available are recorded in the Company’s financial statements at such market quotations. However, investments for which market quotations are readily available, but which are subject to lockup provisions restricting the resale of such investments for a specified period of time, are valued at a discount to the most recently available closing market prices.

With respect to investments for which market quotations are not readily available, the Company’s Board of Directors undertakes a multi-step valuation process each quarter, as described below:

|

|

·

|

The Company’s quarterly valuation process begins with each portfolio company investment being initially valued by Keating Investments’ senior investment professionals responsible for the portfolio investment;

|

|

|

·

|

Third-party valuation firms engaged by the Company’s Board of Directors review these preliminary valuations at such times as determined by the Company’s Board of Directors, provided, however, that a review will be conducted by a third-party valuation firm for each new portfolio company investment made during a calendar quarter, at such time as the valuation for a specific portfolio company investment is increased, and at least once every twelve months;

|

|

|

·

|

The Company’s Valuation Committee reviews the preliminary valuations, and the Company’s Investment Adviser and the third-party valuation firms respond and supplement the preliminary valuation to reflect any comments provided by the Valuation Committee; and

|

|

|

·

|

The Company’s Board of Directors discusses the valuations and determines, in good faith, the fair value of each investment in the Company’s portfolio for which market quotations are not readily available based on the input of the Company’s Investment Adviser, the third-party valuation firms, and the Company’s Valuation Committee.

|

Investment Categories and Approaches to Determining Fair Value

ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (exit price). In accordance with ASC 820, the Company uses a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value as follows:

|

|

·

|

Level 1: Observable inputs such as unadjusted quoted prices in active markets;

|

|

|

·

|

Level 2: Includes inputs such as quoted prices for similar securities in active markets and quoted prices for identical securities where there is little or no activity in the market; and

|

13

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

|

|

·

|

Level 3: Unobservable inputs for which little or no market data exists, therefore requiring an entity to develop its own assumptions.

|

The Company applies the framework for determining fair value as described above to the valuation of investments in each of the following categories:

Short-Term Investments

Short-term investments, which were comprised of investments in certificates of deposit with original maturities of 90 days or less at December 31, 2010, are valued at amortized cost, which approximates fair value. The amortized cost method involves recording a security at its cost (i.e., principal amount plus any premium and less any discount) on the date of purchase and thereafter amortizing/accreting that difference between the principal amount due at maturity and cost assuming a constant yield to maturity as determined at the time of purchase.

As of September 30, 2011, the Company no longer held any instruments classified as short-term investments, as its cash balances were invested in a money market fund and classified as a component of cash and cash equivalents. The money market fund in which the Company has invested its cash balances invests primarily in U.S. Treasury securities, U.S. Government agency securities, and repurchase agreements fully-collateralized by such securities. During the nine months ended September 30, 2011, prior to the investment of cash balances in this money market fund, the Company’s cash balances were invested in certificates of deposit and classified as short-term investments. During the nine months ended September 30, 2011, cumulative purchases of certificates of deposit totaled $89,000,000 and cumulative maturities totaled $102,500,000. During the nine months ended September 30, 2010 the Company’s short-term investments were comprised exclusively of investments in certificates of deposit with four week maturities, with cumulative purchases totaling $52,500,000 and cumulative maturities totaling $47,500,000.

Equity Investments

Equity investments for which market quotations are readily available are generally valued at the most recently available closing market prices. However, equity investments for which market quotations are readily available, but which are subject to lockup provisions restricting the resale of such investments for a specified period of time, are valued at a discount to the most recently available closing market prices.

The fair values of the Company’s equity investments for which market quotations are not readily available (including investments in convertible preferred stock) are determined based on various factors. To determine the fair value of a portfolio company, the Company analyzes the portfolio company’s historical and projected financial results, industry valuation benchmarks and public market comparables, and other factors. The Company also considers other events, including private mergers and acquisitions, the transaction in which we acquired our securities, public offering or subsequent equity sales. In addition, the Company considers the trends of the portfolio company’s basic financial metrics from the time of our original investment until the measurement date, with material improvement of these metrics indicating a possible increase in fair value, while material deterioration of these metrics may indicate a possible reduction in fair value. The fair values of the Company’s portfolio companies’ securities are generally discounted for lack of marketability or when the securities are illiquid, such as when there are restrictions on resale or the lack of an established trading market.

The fair value of common and preferred stock warrants is generally determined by using the Black-Scholes option pricing model or, in cases of certain “structured” warrants where the Company’s ability to exercise may be contingent or be subject to certain performance metrics, an option pricing model based on large numbers of simulations that take into account these special terms.

14

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

|

Fair Value of Investments

|

|

|

The following table categorizes the Company’s cash equivalents, short-term investments, and portfolio company investments measured at fair value based upon the lowest level of significant input used in the valuation as of September 30, 2011 and December 31, 2010:

|

|

Quoted Prices In

|

||||||||||||||||

|

Active Markets

|

Significant Other

|

Significant

|

||||||||||||||

|

For Identical Assets

|

Observable Inputs

|

Unobservable Inputs

|

Total

|

|||||||||||||

|

Description

|

(Level 1)

|

(Level 2)

|

(Level 3)

|

Fair Value

|

||||||||||||

|

As of September 30, 2011

|

||||||||||||||||

|

Private Portfolio Company Securities:

|

||||||||||||||||

|

Preferred Stock

|

$ | - | $ | - | $ | 22,099,874 | $ | 22,099,874 | ||||||||

|

Preferred Stock Warrants

|

- | - | 6,655 | 6,655 | ||||||||||||

|

Common Stock

|

- | - | 7,095,996 | 7,095,996 | ||||||||||||

|

Common Stock Warrants

|

- | - | 639,156 | 639,156 | ||||||||||||

|

Publicly-Traded Portfolio Company Securities:

|

||||||||||||||||

|

Common Stock (1)

|

1,101,000 | - | 977,000 | 2,078,000 | ||||||||||||

|

Cash Equivalents:

|

||||||||||||||||

|

Money Market Funds

|

45,069,165 | - | - | 45,069,165 | ||||||||||||

|

Total

|

$ | 46,170,165 | $ | - | $ | 30,818,681 | $ | 76,988,846 | ||||||||

|

As of December 31, 2010

|

||||||||||||||||

|

Private Portfolio Company Securities:

|

||||||||||||||||

|

Preferred Stock

|

$ | - | $ | - | $ | 4,149,991 | $ | 4,149,991 | ||||||||

|

Preferred Stock Warrants

|

- | - | 27,616 | 27,616 | ||||||||||||

|

Short-Term Investments:

|

||||||||||||||||

|

Certificates of Deposit (2)

|

||||||||||||||||

|

(Maturing on January 6, 2011)

|

- | 13,500,000 | - | 13,500,000 | ||||||||||||

|

Total

|

$ | - | $ | 13,500,000 | $ | 4,177,607 | $ | 17,677,607 | ||||||||

|

(1)

|

Though a quoted price in an active market exist for the Company's common stock investment in Solazyme, Inc. with a fair value of $977,000 at September 30, 2011, this investment is subject to a lockup provision which has not expired as of September 30, 2011 and, as a result, this investment has been valued at a discount to the quoted market price and catorgized as Level 3 in the fair value hierarchy. |

|

(2)

|

Fair value reflects amortized cost as of December 31, 2010.

|

|

The following table provides a reconciliation of the changes in fair value for the Company’s portfolio company investments measured at fair value using significant unobservable inputs (Level 3) for the three months ended September 30, 2011:

|

|

Level 3

|

Level 3

|

Level 3

|

Level 3

|

|||||||||||||||||

|

Portfolio Company

|

Portfolio Company

|

Portfolio Company

|

Portfolio Company |

|

||||||||||||||||

|

Investments

|

Investments

|

Investments

|

Investments

|

|||||||||||||||||

|

Three months ended September 30, 2011:

|

(Preferred Stock)

|

(Preferred Warrants)

|

(Common Stock)

|

(Common Warrants)

|

Total

|

|||||||||||||||

|

Fair Value at June 30, 2011

|

$ | 12,985,012 | $ | 24,205 | $ | 3,331,000 | $ | - | $ | 16,340,217 | ||||||||||

|

New investments in Level 3 portfolio company securities at cost

|

9,354,786 | 1,556 | 6,411,076 | 589,000 | 16,356,418 | |||||||||||||||

|

Gross transfers out of Level 3 to Level 1

|

- | - | (996,000 | ) | - | (996,000 | ) | |||||||||||||

|

Total unrealized appreciation (depreciation) on Level 3 portfolio company securities included in change in net assets

|

(239,924 | ) | (19,106 | ) | (673,080 | ) | 50,156 | (881,954 | ) | |||||||||||

|

Fair Value at September 30, 2011

|

$ | 22,099,874 | $ | 6,655 | $ | 8,072,996 | $ | 639,156 | $ | 30,818,681 | ||||||||||

|

Total unrealized appreciation (depreciation) on Level 3 portfolio company securities included in change in net assets that were still held by the Company at September 30, 2011.

|

$ | (239,924 | ) | $ | (19,106 | ) | $ | (673,080 | ) | $ | 50,156 | $ | (881,954 | ) | ||||||

15

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

|

As of June 30, 2011, the Company’s common stock investment in NeoPhotonics Corporation (“NeoPhotonics”) had a fair value of $996,000 as determined in good faith by the Company’s Board of Directors and was included as a component of Level 3 Portfolio Company Investments (Common Stock). Though a quoted price in an active market existed for the Company’s common stock investment in NeoPhotonics as of June 30, 2011, such investment was subject to a 180 day lockup provision expiring in August 2011 and, as a result, was valued at a 10% discount to the quoted market price of $6.92 per share as of June 30, 2011 and categorized within Level 3 of the fair value hierarchy. Upon expiration of the 180 day lockup provision in August 2011, the Company’s common stock investment in NeoPhotonics was transferred out of Level 3 and into Level 1 within the fair value hierarchy, with the fair value of the Company’s common stock investment in NeoPhotonics of $1,101,000 based on the quoted market price of $6.88 per share as of September 30, 2011, resulting in an increase in unrealized appreciation of $105,000 during the three months ended September 30, 2011.

|

|

|

The following table provides a reconciliation of the changes in fair value for the Company’s portfolio company investments measured at fair value using significant unobservable inputs (Level 3) for the nine months ended September 30, 2011:

|

|

Level 3

|

Level 3

|

Level 3

|

Level 3

|

|||||||||||||||||

|

Portfolio Company

|

Portfolio Company

|

Portfolio Company

|

Portfolio Company

|

|||||||||||||||||

|

Investments

|

Investments

|

Investments

|

Investments

|

|||||||||||||||||

|

Nine months ended September 30, 2011:

|

(Preferred Stock)

|

(Preferred Warrants)

|

(Common Stock)

|

(Common Warrants)

|

Total

|

|||||||||||||||

|

Fair Value at December 31, 2010

|

$ | 4,149,991 | $ | 27,616 | $ | - | $ | - | $ | 4,177,607 | ||||||||||

|

New investments in Level 3 portfolio company securities at cost

|

20,754,798 | 1,556 | 6,411,076 | 589,000 | 27,756,430 | |||||||||||||||

|

Transfers from preferred stock to common stock within Level 3

|

(999,991 | ) | - | 999,991 | - | - | ||||||||||||||

|

Gross transfers out of Level 3 to Level 1

|

(1,550,000 | ) | - | - | (1,550,000 | ) | ||||||||||||||

|

Total unrealized appreciation (depreciation) on Level 3 portfolio company securities included in change in net assets

|

(254,924 | ) | (22,517 | ) | 661,929 | 50,156 | 434,644 | |||||||||||||

|

Fair Value at September 30, 2011

|

$ | 22,099,874 | $ | 6,655 | $ | 8,072,996 | $ | 639,156 | $ | 30,818,681 | ||||||||||

|

Total unrealized appreciation (depreciation) on Level 3 portfolio company securities included in change in net assets that were still held by the Company at September 30, 2011.

|

$ | (254,924 | ) | $ | (22,517 | ) | $ | 661,929 | $ | 50,156 | $ | 434,644 | ||||||||

|

As of December 31, 2010, the Company’s Series X convertible preferred stock investment in NeoPhotonics Corporation (“NeoPhotonics”) had a fair value of $1,550,000 as determined in good faith by the Company’s Board of Directors and was included as a component of Level 3 Portfolio Company Investments (Preferred Stock) as NeoPhotonics was a private company for which market quotations for its shares were not available as of December 31, 2010. As a result of NeoPhotonics’ initial public offering on February 2, 2011 (where the Company’s preferred stock was converted into common stock) and upon expiration of the 180 day lockup provision associated with such shares of common stock in August 2011, the Company’s common stock investment in NeoPhotonics was transferred out of Level 3 and into Level 1 within the fair value hierarchy, with the fair value of the Company’s common stock investment in NeoPhotonics of $1,101,000 based on the quoted market price of $6.88 per share as of September 30, 2011, resulting in an increase in unrealized (depreciation) of $(449,000) during the nine months ended September 30, 2011.

|

|

|

As of December 31, 2010, the Company’s Series D convertible preferred stock investment in Solazyme, Inc. (“Solazyme”) had a fair value of $999,991 as determined in good faith by the Company’s Board of Directors and was included as a component of Level 3 Portfolio Company Investments (Preferred Stock) as Solazyme was a private company for which market quotations for its shares were not available as of December 31, 2010. As a result of Solazyme’s initial public offering on May 27, 2011 and the conversion of the Company’s preferred stock into common stock, such investment was reclassified from preferred stock to common stock within Level 3 of the fair value hierarchy during the nine months ended September 30, 2011. Though a quoted price in an active market exists for the Company’s common stock investment in Solazyme as of September 30, 2011, such investment is subject to a 180 day lockup provision expiring in November 2011 and, as a result, has been valued at price of $8.65 per share, a 10% discount to the quoted market price of $9.61 per share as of September 30, 2011, and categorized within Level 3 of the fair value hierarchy.

|

16

Keating Capital, Inc.

Notes to Financial Statements

(Unaudited)

4. Investment Portfolio

During the three months ended September 30, 2011, the Company made investments totaling $16,356,418 in six private companies, consisting of preferred stock, common stock, and warrants to acquire preferred stock and common stock.

During the nine months ended September 30, 2011, the Company made investments totaling $27,756,430 in 11 private companies, consisting of preferred stock, common stock, and warrants to acquire preferred stock and common stock.

Portfolio Company Investment Activity – Quarter Ended March 31, 2011

MBA Polymers, Inc. On February 22, 2011, the Company made a $900,000 follow-on investment in Series G convertible preferred stock of MBA Polymers, Inc. (“MBA Polymers”). This follow-on investment was in addition to the $1.1 million investment in the Series G convertible preferred stock of MBA Polymers made by the Company in October 2010.

BrightSource Energy, Inc. On March 1, 2011, the Company completed a $2,500,006 investment in the Series E convertible preferred stock of BrightSource Energy, Inc. (“BrightSource”). BrightSource is a private company headquartered in Oakland, California and is a developer of utility scale solar thermal plants which generate solar energy for utility and industrial companies using its proprietary solar thermal tower technology. On April 22, 2011, BrightSource filed a registration statement on Form S-1 to go public through a $250 million initial public offering of its common stock. BrightSource filed amendment No. 4 to its registration statement on October 12, 2011. In the event of a qualifying initial public offering, the Series E convertible preferred stock would be automatically converted into shares of BrightSource’s common stock. The common stock issued upon conversion would be subject to a 180 day lockup period following the completion of the initial public offering.

Harvest Power, Inc. On March 9, 2011, the Company made a $2,499,999 investment in the Series B convertible preferred stock of Harvest Power, Inc. (“Harvest Power”). Harvest Power is a private company headquartered in Waltham, Massachusetts that acquires, owns and operates organic waste facilities that convert organic waste, such as food scraps and yard debris, into compost, mulch and renewable energy.

Suniva, Inc. On March 31, 2011, the Company made a $2,500,007 investment in the Series D convertible preferred stock of Suniva, Inc. (“Suniva”). Suniva is a private company headquartered in Norcross, Georgia and is a manufacturer of high-efficiency solar photovoltaic cells and modules focused on delivering high-power solar energy products.

Portfolio Company Investment Activity – Quarter Ended June 30, 2011