Attached files

| file | filename |

|---|---|

| 8-K - UIL HOLDINGS CORPORATION 8-K 11-4-2011 - UIL HOLDINGS CORP | form8k.htm |

46th Annual EEI Financial Conference

November 2011

Exhibit 99.1

Exhibit 99.1

2

2011 Fall EEI

2

Safe Harbor Provision

Certain statements contained herein, regarding matters that are not historical facts, are forward-looking statements (as defined in the

Private Securities Litigation Reform Act of 1995). These include statements regarding management’s intentions, plans, beliefs,

expectations or forecasts for the future. Such forward-looking statements are based on UIL Holdings’ expectations and involve risks and

uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements. Such risks and

uncertainties include, but are not limited to, general economic conditions, legislative and regulatory changes, changes in demand for

electricity, gas and other products and services, unanticipated weather conditions, changes in accounting principles, policies or

guidelines, and other economic, competitive, governmental, and technological factors affecting the operations, markets, products and

services of UIL Holdings’ subsidiaries, The United Illuminating Company, The Southern Connecticut Gas Company, Connecticut

Natural Gas Corporation and The Berkshire Gas Company. Such risks and uncertainties with respect to UIL Holdings’ recent

acquisition of The Southern Connecticut Gas Company, Connecticut Natural Gas Corporation and The Berkshire Gas Company

include, but are not limited to, the possibility that the expected benefits will not be realized, or will not be realized within the expected

time period. The foregoing and other factors are discussed and should be reviewed in UIL Holdings’ most recent Annual Report on

Form 10-K and other subsequent periodic filings with the Securities and Exchange Commission. Forward-looking statements included

herein speak only as of the date hereof and UIL Holdings undertakes no obligation to revise or update such statements to reflect events

or circumstances after the date hereof or to reflect the occurrence of unanticipated events or circumstances.

James P. Torgerson

President and Chief Executive Officer

3

2011 Fall EEI

Contents

q Overview

ú Corporate Structure

ú Investment Highlights

ú YTD 3Q ’11 Financial Results

ú Debt Maturities & Credit Ratings

ú ’11 Earnings Guidance

ú UIL Integration

q UIL Forecasts

ú Capital Expenditure

ú Average Rate Base

q Business Operations & Services

ú Gas distribution

ú Electric transmission

ú Electric distribution

ú Generation

ú Smart Systems

q Governmental and Regulatory Updates

q Conclusion

3

4

2011 Fall EEI

UIL - Corporate Structure

4

›

Service territory: 716 sq

miles

-

Greater Hartford

-

New Britain & Greenwich

›

~160,000 customers

›

319 employees

›

2,011 miles of mains with

~124,000 services

›

Allowed ROE of 9.41%

going forward

Service territory: 512 sq

miles from Westport, CT

to Old Saybrook, CT

›

~178,000 customers

›

290 employees

›

2,273 miles of mains with

~131,000 services

›

Allowed ROE of 9.36%

going forward

›

Service territory: 716 sq

miles

-

Greater Hartford

-

New Britain & Greenwich

›

~160,000 customers

›

319 employees

›

2,011 miles of mains with

~124,000 services

›

Connecticut Natural Gas

(CNG)

Service territory: 512 sq

miles from Westport, CT

to Old Saybrook, CT

›

~178,000 customers

›

290 employees

›

2,273 miles of mains with

~131,000 services

›

Southern Connecticut Gas

(SCG)

5

2011 Fall EEI

Investment Highlights

5

q Electric distribution & transmission and gas distribution utilities -

complementary earnings patterns

complementary earnings patterns

q Growth opportunities

q Disciplined capital investment program

q Commitment to investment grade credit profile

q Consistent history of dividend payments (5.1% yield as of 11/2/11)

Gas Operations

Electric Operations

ú Identified capital expenditure projects

with clear need

with clear need

ú Growth opportunities - converting

residentials and businesses to gas heat

residentials and businesses to gas heat

ú Winter peaking

ú Objective is to achieve allowed ROEs

ú Identified capital expenditure projects

with clear need

with clear need

ú Growth opportunities in transmission

ú Summer peaking

ú 50% owner in peaking generation

plants

plants

ú Opportunity to invest in regulated

renewables generation

renewables generation

ú Objective is to achieve allowed ROE

6

2011 Fall EEI

q $34M or 76% increase in net income compared to YTD 3Q ’10

ú Gas distribution net income of $29.7M YTD ’11, no comparable income in ‘10

ú Both GenConn peaking generation plants are now operating in the ISO-NE markets and YTD

contributed to UIL pre-tax income of $8.2M, compared to a pre-tax loss of $0.5M YTD 3Q ‘10

contributed to UIL pre-tax income of $8.2M, compared to a pre-tax loss of $0.5M YTD 3Q ‘10

ú YTD net income for electric transmission was $23.2M, an increase of $3.7M compared to YTD 3Q ’10,

primarily attributable to an increase in the allowance for funds used during construction due to

increased CWIP

primarily attributable to an increase in the allowance for funds used during construction due to

increased CWIP

q Average D & CTA ROE as of 9/30/11: 9.63%

q Preliminary average ROE as of 9/30/11: SCG 8.30-8.40%, CNG 8.90-9.00%

Net Income ($M)

6

YTD ’11 vs. YTD ‘10 Financial Results

by Business

by Business

7

2011 Fall EEI

** To be remarketed

Amounts may not add due to rounding

Based on current plans - expect no need for external equity at least through 2013

UI Pollution Control Revenue Bonds

UI Equity Bridge Loan repaid in July

UIL Debt retired in Feb

SCG, CNG & Berkshire

Near-Term Debt Maturities

($M)

$5

Berkshire note repaid in May

SCG notes refinanced

|

Issuer

|

S&P

|

Moody’s

|

|

UIL

Holdings |

BBB

(Stable) |

Baa3

(Stable) |

|

United

Illuminating |

BBB

(Stable) |

Baa2

(Stable) |

|

SCG

|

BBB

(Stable) |

Baa2

(Stable) |

|

CNG

|

BBB

(Stable) |

Baa1

(Stable) |

|

Berkshire

|

BBB

(Stable) |

Baa2

(Stable) |

Issuer

Credit Ratings

7

**

Debt Maturities & Credit Ratings

8

2011 Fall EEI

Current Assumptions

ú Electric distribution, CTA & other and Gas distribution ranges were narrowed reflecting year-to-date performance

ú GenConn expected to earn $0.12-$0.14 per share

ú UIL Corporate was reduced to reflect tax savings resulting from the deductibility of certain gas company acquisition costs

‘12 earnings expectations will be discussed on the

4Q ‘11 earnings call

4Q ‘11 earnings call

8

Increased ‘11 Earnings Expectations

as of 11/4/11

as of 11/4/11

9

2011 Fall EEI

Expected On-going Savings of $11.6M

9

$M

UIL Integration

q Integration progressing on schedule

q Successfully completed a major SAP system cutover from Iberdrola USA (IUSA) at the

beginning of August

beginning of August

q Substantially exited Transition Services Agreement as of the end of September ‘11

2011 Fall EEI

UIL Forecasts

11

2011 Fall EEI

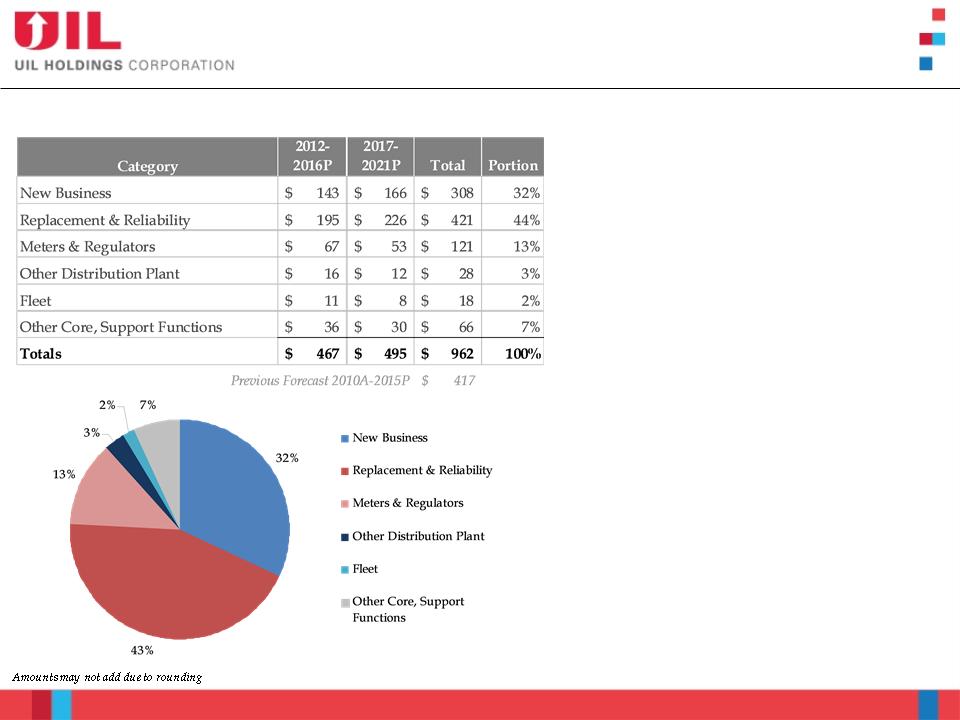

UIL 2012-2021 Capital Expenditure Forecast

11

* 2011 capex details can be found in the appendix

** Includes GenConn equity investment & 6-yr forecast (2010A-2015P) for Gas distribution

Does not include potential to construct, own and operate up to 10MW of Class I renewable generation

Amounts may not add due to rounding

Presentation format for 10-yr CapEx has

changed (and will be the format going

forward). Includes future 10 years (2012-

2021). Previous format included present

year and future 9 years.

changed (and will be the format going

forward). Includes future 10 years (2012-

2021). Previous format included present

year and future 9 years.

q Previous 2011 capex forecast, $383M*

q Identified projects with clear need

q Full 10-yr forecast for Gas distribution capex

ú Previous 6-yr forecast (2010A-2015P), $417

q Increased IT-related projects in UIL Corporate

12

2011 Fall EEI

GenConn Equity Investments:

Rate Base $M (Excluding GenConn Equity Investments):

$2,062

$2,235

$2,388

$2,535

$2,731

2%

43%

22%

33%

1%

41%

22%

36%

40%

22%

38%

40%

22%

38%

38%

24%

38%

Electric distribution

CTA

Gas distribution*

Electric transmission

Amounts may not add due to rounding

* Gas distribution rate base by company can be found in the appendix

12

CAGR 7.3%

Gas distribution

4.1%

4.1%

Electric transmission

9.2%

9.2%

Electric distribution

11.6%

11.6%

2012-2016 Average Rate Base Forecast

Gas distribution

14

2011 Fall EEI

American Community Survey’s selected housing characteristics estimates show a large percentage of

households in Connecticut do not use natural gas for heating

households in Connecticut do not use natural gas for heating

Litchfield

62%

13%

16%

4%

5%

Fairfield

47%

35%

15%

2%

1%

Connecticut

50%

31%

15%

2%

1%

New Haven

46%

35%

16%

2%

2%

Middlesex

63%

11%

18%

4%

3%

New London

63%

11%

19%

3%

4%

Windham

68%

9%

11%

8%

4%

Tolland

67%

9%

13%

5%

4%

Hartford

41%

42%

13%

1%

2%

Fuel oil, kerosene

Electricity

Utility gas

Bottled, tank or LP gas

Other¹

Source: U.S. Census Bureau; Average data for 2005-2009

1 Other includes coal or coke, wood, solar, no fuel used and other

# Occupied

housing units:

1,327,482

housing units:

1,327,482

73,704

339,516

52,993

42,653

104,468

65,476

322,752

325,920

(0)

(17)

(2)

(12)

(0)

(0)

(4)

(9)

The # in parentheses represents

the number of cities or towns in

that county that are served by a

UIL gas company.

UIL gas company.

Approximately 37% of businesses & households on UIL gas mains are not currently natural gas customers

14

Gas Distribution

Potential for Heating in CT

Potential for Heating in CT

15

2011 Fall EEI

(1) Residential and commercial

15

Gas Distribution

Heating Conversions

Heating Conversions

q Interest in conversions increasing as heating season begins

ú Direct mail marketing deployed in October to increase customers’ awareness of conversion

benefits

benefits

ú Financing options are being expanded to assist customers with up-front conversion costs

ú Natural gas supply prices are low and expected to remain low for the foreseeable future

q Approximately 6,800 customer(1) additions in 2010

ú Targeting 30,000-35,000 additional gas heating customers over the next 3 years

▪ ’11 - approximately 25% increase over ‘10 levels

▪ ’12 - approximately 50% increase over ’10 levels

q Through September, residential conversions are 13% ahead of ‘10 levels

ú YTD 9/30/11, there were 4,129 conversions, compared to 3,654 conversions for YTD

9/30/10

9/30/10

q New residential customers are anticipated to generate approximately $280-$315 of

distribution net operating income per customer

distribution net operating income per customer

16

2011 Fall EEI

q New main is required to serve the new construction

q New main will pass 79 homes that are mostly heated with oil

q 18 homes already signed up for conversion

q Opportunity - 61 homes that will be on the new main

16

Gas Distribution

Example of Neighborhood Expansion

Example of Neighborhood Expansion

17

2011 Fall EEI

17

Gas Distribution

CapEx Forecast

CapEx Forecast

Gas Distribution CapEx Forecast $M

q Previous 2011 capex forecast, $61M

q Revised UIL Gas distribution

forecast

forecast

ú Previous 5-yr forecast was provided

by IUSA

by IUSA

q Forecast addresses replacement of

cast iron & bare steel

cast iron & bare steel

ú Base spend of approx. $26M annually

ú Accelerated infrastructure spending

of approx. $121M over 10 years

of approx. $121M over 10 years

q New Business

ú Heating conversions

ú Main extensions

18

2011 Fall EEI

18

Gas Distribution

Examples of Projects

Examples of Projects

Replacement Services & Mains

ú Replacement of cast iron & bare steel

ú Enhances system performance

ú Program: on-going

~ $381M (2012-2021)

Electric transmission

20

2011 Fall EEI

20

Electric Transmission

CapEx Forecast

CapEx Forecast

q Previous 2011 capex forecast,

$69M

$69M

q CapEx is well-diversified in

scale and category

scale and category

ú Not highly dependent on a few

major projects or load growth

major projects or load growth

ú See next slide for examples

q Only includes high probability

projects …

projects …

ú Although UI is working on other

growth opportunities, they are not

included until highly likely

growth opportunities, they are not

included until highly likely

Transmission CapEx Forecast $M

21

2011 Fall EEI

21

Electric Transmission

Examples of Projects

Examples of Projects

Grand Avenue 115 kV Switching

Station Rebuild

Station Rebuild

Shelton 115/ 13.8 kV Substation

Union Avenue 115/ 26.4 kV

Substation

Substation

ú Addresses short circuit capability issues and

aged/obsolete infrastructure

aged/obsolete infrastructure

ú Under

construction

construction

ú Planned in-service

2012

2012

~ $60M*

ú Meets Greater Shelton area load growth

ú In Planning

ú Planned in-

service 2014

service 2014

~ $25M*

ú Under

construction

construction

ú Planned in-service

2012

2012

~ $15M*

ú Addresses infrastructure condition,

maintenance short circuit capability concerns

maintenance short circuit capability concerns

ú Phased

upgrades in

engineering and

construction

upgrades in

engineering and

construction

ú Planned in-

service 2011-

2013

service 2011-

2013

~ $22M*

East Shore 115 kV Substation Upgrades

* Dollars shown are rounded/approximate expected total project Transmission CapEx (generally including both spend to date and future expected spend); excluding AFUDC.

22

2011 Fall EEI

Electric Transmission

Growth Outside Service Territory

Growth Outside Service Territory

Region-wide RPS Satisfaction

22

New England East-West Solution (NEEWS)

ú 2020 gap is

significant

significant

ú Unlikely to be

satisfied by

current queue

satisfied by

current queue

ú Significant

transmission

will be needed

transmission

will be needed

ú Together with

NU, NStar,

NGrid, UI is

cooperatively

researching

economical

delivery

NU, NStar,

NGrid, UI is

cooperatively

researching

economical

delivery

UI Participation in CL&P Project:

ú UI’s portion of investment: greater of $60M* or 8.4%

of CL&P’s costs for the CT portions of:

of CL&P’s costs for the CT portions of:

▪ Greater Springfield Reliability, Interstate

Reliability, Central CT Reliability Projects

Reliability, Central CT Reliability Projects

ú UI deposits thru end Nov. ‘11: $9.6M

▪ Remaining investments expected to be made over a

period of 3 to 5 years

period of 3 to 5 years

ú On 8/29/11, FERC approved UI’s request for a 125

basis point ROE adder resulting in a total project

ROE of 12.89% once assets are in service

basis point ROE adder resulting in a total project

ROE of 12.89% once assets are in service

*Based on most recent information/estimate from NU

23

2011 Fall EEI

Electric Transmission

Developments

Developments

FERC Order 1000

q Issued by FERC on July 21, 2011. Includes

provisions related to:

provisions related to:

ú Incorporating public policy into transmission

planning

planning

ú Transmission cost allocation

ú Limitation on right of first refusal

ú Inter-regional transmission coordination

q Potentially enhances UIL’s ability to participate in

renewable transmission

renewable transmission

q Initial review indicates that New England is

already compliant with many of the

requirements …

already compliant with many of the

requirements …

ú But, stakeholders will need to reach consensus on

some, e.g. incorporation of public policy

some, e.g. incorporation of public policy

ú Initial stakeholder discussions have begun

23

Challenge to Regional Base

ROE

ROE

q “206” Complaint filed by multiple

state governmental parties on

September 30, 2011

state governmental parties on

September 30, 2011

ú Claims that New England TO’s base

ROE is too high …

ROE is too high …

q Multiple New England TOs

(including UI) filed a response on

October 20, 2011

(including UI) filed a response on

October 20, 2011

ú Demonstrates that ROE is at an

appropriate level

appropriate level

q FERC will decide, but date of

decision uncertain

decision uncertain

Electric distribution

25

2011 Fall EEI

25

Electric Distribution

CapEx Forecast

CapEx Forecast

Electric Distribution CapEx Forecast $M

q Previous 2011 capex forecast,

$172M

$172M

q CapEx is well-diversified in

scale and category

scale and category

ú Forecast is not highly

dependent on a few major

projects or load growth

dependent on a few major

projects or load growth

26

2011 Fall EEI

26

Electric Distribution

Examples of Projects

Central Facility - UI Office &

Operations Building

Operations Building

Splice Chamber Remediation

Network Infrastructure Replacement

Distribution Transformer

Replacement Program

Replacement Program

ú Consolidate all UI “Work Centers” onto a

single site referred to as the Central Facility

single site referred to as the Central Facility

ú Under

construction

construction

ú Planned in-service

2012

2012

~ $128M*

ú Rebuild deteriorated underground splicing

chambers

chambers

ú In progress

ú Annual program

over 10 years

over 10 years

~ $8M per year

ú In progress

ú Annual program

over 10 years

over 10 years

~ $5M per year

ú Infrastructure program to replace transformers due

to poor physical condition, inadequate capacity, that

could potentially contain levels of PCBs

to poor physical condition, inadequate capacity, that

could potentially contain levels of PCBs

ú In progress

ú Annual program

over 10 years

over 10 years

~ $7M per year

* Dollars shown are rounded/approximate expected total project Distribution CapEx (generally including both spend to date and future expected spend).

27

2011 Fall EEI

Electric Distribution

Recent Storm Update

Recent Storm Update

Tropical Storm Irene

q 59% of electrical circuits experienced outages

q More than 10,000 locations worked on by crews

q Nearly 50% of UI’s customers were without power at

the peak

the peak

ú 99.8% restored within 7 days

q Participated in post-Irene legislative hearings

q As of 9/30/11, the cost estimate was approximately

$20M, of which approximately $4M has been

capitalized

$20M, of which approximately $4M has been

capitalized

ú In accordance with PURA regulatory decision and past

storm guidance, a regulatory asset has been established

for storm-related O&M costs

storm guidance, a regulatory asset has been established

for storm-related O&M costs

ú Expect to seek recovery of these costs in a future rate

proceeding

proceeding

Autumnal Storm Alfred

q Approximately 16% of UI’s customers experienced

power outages

power outages

ú 99.9% of all customers had power within 3 days

27

Tropical Storm Irene

Impact across UI service territory

Peak of Tropical Storm Irene coincidental with

high tide - extensive flooding at two UI

substation properties

high tide - extensive flooding at two UI

substation properties

Generation

29

2011 Fall EEI

q Regulated COS approach

ú ROE, lifetime floor - 9.75%

ú 50/50 - debt/equity

ú Annual PURA rate case

q Both GenConn Devon & Middletown are now operating in the ISO-New England (ISO-NE)

markets

markets

ú UIL reported pre-tax income of $3.5M and $8.2M in the 3Q and first nine months of ’11, respectively

29

Generation

GenConn Energy - Peaking Generation

GenConn Energy - Peaking Generation

Project Highlights

|

Locations

|

Devon &

Middletown |

|

Technology

|

GE LM6000

|

|

Capacity

|

400 MW (188MW

each at Devon and Middletown) |

|

Off Taker

|

CL&P

|

50/50 Joint Venture between UI and NRG

Devon

Middletown

30

2011 Fall EEI

30

Generation

Regulated Renewables Development Opportunity

Regulated Renewables Development Opportunity

q CT Public Act 11-80 / Section 127 (effective July 1,

2011) authorizes UI to construct, own, operate and

rate base Class I renewable generation up to 10MW

2011) authorizes UI to construct, own, operate and

rate base Class I renewable generation up to 10MW

ú Solar Photovoltaics

ú Fuel Cells

ú Wind Turbines

q Expected investment up to $40-$50M over the next

two - three years

two - three years

q PURA filing expected by the first quarter 2012

q Entry into renewable generation

q Supports public policy objectives

q Aligns with sustainable business strategy

Smart Systems

32

2011 Fall EEI

32

Smart Systems

UI’s Mesh Network

UI’s Mesh Network

Modernization of UI’s Electric System

q Over 337,000 meters -

ú 80,000 two-way w/remote

disconnect capability

disconnect capability

ú Meters have

q Mesh Network

q Master Data is stored in Meter

Data Management - interface

with SAP

Data Management - interface

with SAP

q Outage Mgt System uses meter

intelligence for restoration and

communication

intelligence for restoration and

communication

q Over 33% of our customers

have Time-of-Day rates

have Time-of-Day rates

Governmental and Regulatory

Updates

Updates

34

2011 Fall EEI

q Annual revenue requirement filed with CT PURA on 7/29/11 (DN 11-07-

12)

12)

ú Requesting approximately $78M for the period commencing 1/1/12 -

12/31/12

12/31/12

ú Draft decision expected 12/7/11

ú Final decision expected 12/21/11

q Final decision by CT PURA approving CNG & SCG settlement of rate

case appeals was issued on 8/3/11 (DN 08-12-06RE02 & DN 08-12-07RE02)

case appeals was issued on 8/3/11 (DN 08-12-06RE02 & DN 08-12-07RE02)

ú Resolves all pending issues related to the rate case appeals

ú Removes the 10 basis point ROE penalty for monitoring

ú Authorized ROEs going forward: CNG - 9.41%, SCG - 9.36%

ú Terminates the SCG potential overearnings investigation

ú Companies are allowed to recover carrying charges on the interim rate

decrease amounts over-credited to customers during the stay of the rate case

decisions (since 2009)

decrease amounts over-credited to customers during the stay of the rate case

decisions (since 2009)

▪ Approximately $3.7M to be recovered and collected over the next two non-winter

periods, $2.2M booked to earnings in 3Q ‘11

periods, $2.2M booked to earnings in 3Q ‘11

q BGC - regulated by the Massachusetts Department of Public Utilities (DPU)

ú 10-yr rate plan expiring 1/31/12

34

Regulatory Update

35

2011 Fall EEI

q Electric Decoupling final decision (DN 08-07-04 RE03)

ú Issued on 8/31/11

ú Approved decoupling credit of $1.4M for ’10 rate year

ú Allows decoupling mechanism to continue until next general rate case proceeding

q Utility Company Storm Response Docket (DN 11-09-09)

ú Investigation of the service response and communications of utilities in CT

following Tropical Storm Irene

following Tropical Storm Irene

q Transmission ROE

ú Several New England governmental entities have filed a complaint with FERC

regarding the base return on equity for transmission investments

regarding the base return on equity for transmission investments

▪ Claim that the current approved base ROE on transmission investments of 11.14% is not

just and reasonable and are seeking a reduction of the base ROE to 9.20%

just and reasonable and are seeking a reduction of the base ROE to 9.20%

q Electric Distribution Rate Case

ú Evaluating timing of distribution rate case to reflect significant investments in

distribution infrastructure

distribution infrastructure

q Generic ROE Proceeding (DN 09-10-06)

ú PURA schedule has not been updated

35

Regulatory Update - continued

36

2011 Fall EEI

36

Governmental Update

q Implementation of Public Act 11-80

ú Department of Energy & Environmental Protection (DEEP) was created

ú Former DPUC has become the Public Utilities Regulatory Authority (PURA)

▪ Change from 5 DPUC commissioners to three PURA directors

§ Kevin DelGobbo (former DPUC chair), John Betkoski and Anna Ficeto

ú Allows each electric distribution company to develop and own up to 10 MW renewable

source generation

source generation

q Post-Storm Irene Investigations

ú Participated in two legislative hearings

ú Governor Malloy established a State Team Organized for the Review of Management of

Irene (S.T.O.R.M. Irene) assessment team

Irene (S.T.O.R.M. Irene) assessment team

q Low Income Home Energy Assistance Program (LIHEAP)

ú Anticipate significant reductions in funds available for home energy assistance

programs

programs

q Next Legislative Session February-May ‘12

Conclusion

38

2011 Fall EEI

Investment Highlights

38

q Electric distribution & transmission and gas distribution utilities -

complementary earnings patterns

complementary earnings patterns

q Growth opportunities

q Disciplined capital investment program

q Commitment to investment grade credit profile

q Consistent history of dividend payments (5.1% yield as of 11/2/11)

Gas Operations

Electric Operations

ú Identified capital expenditure projects

with clear need

with clear need

ú Growth opportunities - converting

residentials and businesses to gas heat

residentials and businesses to gas heat

ú Winter peaking

ú Objective is to achieve allowed ROEs

ú Identified capital expenditure projects

with clear need

with clear need

ú Growth opportunities in transmission

ú Summer peaking

ú 50% owner in peaking generation

plants

plants

ú Opportunity to invest in regulated

renewables generation

renewables generation

ú Objective is to achieve allowed ROE

Q & A

Appendices

41

2011 Fall EEI

41

3Q & YTD 2011 Financial Results - Details

q Electric distribution, CTA, GenConn & Other

ú 1% increase in net income YTD, 3Q was lower primarily due to mark to market & effective tax

rate adjustments, offset by GenConn earnings

rate adjustments, offset by GenConn earnings

▪ The mark to market & effective tax rate adjustments reduced net income by $2.3M & $3.4M for the

3Q & first nine months of ’11, respectively

3Q & first nine months of ’11, respectively

▪ GenConn contributed to UIL pre-tax income of $3.5M & $8.2M for the 3Q & first nine months of ’11,

respectively

respectively

ú Average D & CTA ROE as of 9/30/11: 9.63%

q Electric transmission

ú 19% increase in net income for the quarter & YTD

▪ Increase attributable to an increase in the allowance for funds used during construction due to

increased CWIP

increased CWIP

q Gas Distribution

ú YTD income of $29.7M , 3Q loss of $6.2M due to seasonality of earnings

ú YTD - colder than normal winter season in New England in ’11

ú Recovered approximately $2.2M pre-tax of carrying charges in the 3Q ’11 on interim rate

decrease amounts over-credited to customers during stay of rate case decisions

decrease amounts over-credited to customers during stay of rate case decisions

▪ Recovery of carrying charges will continue until the outstanding surcharge balance is exhausted

ú Preliminary average ROE as of 9/30/11: SCG 8.30-8.40%, CNG 8.90-9.00%

q Corporate

ú YTD after-tax costs of $9.4M, a decrease of $0.1M compared to ’10

ú After-tax costs of $2.3M in the 3Q, a decrease of $2M compared to 3Q ’10

ú The decrease for the quarter & YTD was primarily attributable to the absence in ’11 of after-tax

acquistion related costs that occurred in the 3Q ’10, partially offset by the interest expense related

to the October ‘10 issuance of $450M of public debt

ú Interest expense on the $450M of public debt was $3.2M & $9.5M for the 3Q and first nine

months of ’11, respectively

months of ’11, respectively

42

2011 Fall EEI

SCG

BGC

CNG

$882

$913

$957

$1,002

$1,036

8%

42%

50%

8%

42%

50%

8%

42%

50%

8%

41%

51%

8%

41%

51%

$M

Amounts may not add due to rounding

42

Gas Distribution

2012-2016 Average Rate Base Forecast by Company

2012-2016 Average Rate Base Forecast by Company

43

2011 Fall EEI

Previous 10-yr Capital Expenditure Forecast

43

*2010 Gas distribution CapEx reflects the full year amount; UIL ownership was for 6 weeks effective with the closing on the acquisition.

** Updated - February 23, 2011

*** Information as of November 2010, except for Gas distribution

Amounts may not add due to rounding

$M

44

2011 Fall EEI

44

Previous 5-yr Rate Base Forecast

45

2011 Fall EEI

CT RPS

45

Connecticut RPS Requirements

(Percentage of Retail Load)

Class 1 resources include energy derived from solar, wind, fuel cell, methane gas from landfills, ocean thermal, wave,

tidal, run-of-river hydropower (<5MW, began operation after July 1, 2003), sustainable biomass (NOx emission <0.075

lbs/MMBtu of heat input)

tidal, run-of-river hydropower (<5MW, began operation after July 1, 2003), sustainable biomass (NOx emission <0.075

lbs/MMBtu of heat input)

Class 2 resources include other biomass (NOx emission <0.2 lbs/MMBtu of heat input, began operation before July 1,

1998), small run-of-river hydroelectric (<5MW, began operation before July 1, 2003) and municipal solid waste trash-to-

energy facilities.

1998), small run-of-river hydroelectric (<5MW, began operation before July 1, 2003) and municipal solid waste trash-to-

energy facilities.

Class 3 include customer-sited combined heat and power (with operating efficiency >50% of facilities installed after

January 1, 2006), waste heat recovery systems (installed on or after April 1, 2007), electricity savings from conservation

and load management programs (began on or after January 1, 2006)

January 1, 2006), waste heat recovery systems (installed on or after April 1, 2007), electricity savings from conservation

and load management programs (began on or after January 1, 2006)