Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PRUDENTIAL FINANCIAL INC | d250297d8k.htm |

PRUDENTIAL FINANCIAL,

INC.

NOVEMBER

3,

2011

Exhibit 99.1 |

2

Forward-Looking Statements

Certain of the statements included in this presentation constitute

forward-looking statements within the meaning of the U. S. Private Securities

Litigation

Reform

Act

of

1995.

Words

such

as

“expects,”

“believes,”

“anticipates,”

“includes,”

“plans,”

“assumes,”

“estimates,”

“projects,”

“intends,”

“should,”

“will,”

“shall,”

or variations of such words are generally part of forward-looking

statements. Forward-looking statements are made based on

management’s current expectations and beliefs concerning future developments and their potential effects upon Prudential Financial, Inc. and its

subsidiaries.

There

can

be

no

assurance

that

future

developments

affecting

Prudential

Financial,

Inc.

and

its

subsidiaries

will

be

those

anticipated

by

management.

These

forward-looking

statements

are

not

a

guarantee

of

future

performance

and

involve

risks

and

uncertainties,

and

there

are

certain important factors that could cause actual results to differ, possibly

materially, from expectations or estimates reflected in such forward-

looking statements, including, among others: (1)

general economic, market and political conditions, including the

performance and fluctuations of

fixed income, equity, real estate and other financial markets; (2) the availability

and cost of additional debt or equity capital or external financing for our

operations; (3) interest rate fluctuations or prolonged periods of low

interest rates; (4) the degree to which we choose not to hedge risks, or the

potential ineffectiveness or insufficiency of hedging or risk management strategies

we do implement, with regard to variable annuity or other product

guarantees;

(5)

any

inability

to

access

our

credit

facilities;

(6)

reestimates

of

our

reserves

for

future

policy

benefits

and

claims;

(7)

differences

between actual experience regarding mortality, morbidity, persistency, surrender

experience, interest rates or market returns and the assumptions we

use

in

pricing

our

products,

establishing

liabilities

and

reserves

or

for

other

purposes;

(8)

changes

in

our

assumptions

related

to

deferred

policy

acquisition

costs,

value

of

business

acquired

or

goodwill;

(9)

changes

in

assumptions

for

retirement

expense;

(10)

changes

in

our

financial

strength

or credit ratings; (11) statutory reserve requirements associated with term and

universal life insurance policies under Regulation XXX and Guideline

AXXX;

(12)

investment

losses,

defaults

and

counterparty

non-performance;

(13)

competition

in

our

product

lines

and

for

personnel;

(14)

difficulties

in

marketing

and

distributing

products

through

current

or

future

distribution

channels;

(15)

changes

in

tax

law;

(16)

economic,

political,

currency

and

other

risks

relating

to

our

international

operations;

(17)

fluctuations

in

foreign

currency

exchange

rates

and

foreign

securities

markets;

(18)

regulatory or legislative changes, including the recently enacted Dodd-Frank

Wall Street Reform and Consumer Protection Act; (19) inability to

protect

our

intellectual

property

rights

or

claims

of

infringement

of

the

intellectual

property

rights

of

others;

(20)

adverse

determinations

in

litigation

or

regulatory matters and our exposure to contingent liabilities, including in

connection with our divestiture or winding down of businesses; (21)

domestic or international military actions, natural or man-made disasters

including terrorist activities or pandemic disease, or other events

resulting

in

catastrophic

loss

of

life;

(22)

ineffectiveness

of

risk

management

policies

and

procedures

in

identifying,

monitoring

and

managing

risks;

(23)

effects of acquisitions, divestitures and restructurings, including possible

difficulties in integrating and realizing the projected results of

acquisitions,

including

risks

associated

with

the

acquisition

of

certain

insurance

operations

in

Japan;

(24)

interruption

in

telecommunication,

information

technology

or

other

operational

systems

or

failure

to

maintain

the

security,

confidentiality

or

privacy

of

sensitive

data

on

such

systems;

(25)

changes

in

statutory

or

U.S.

GAAP

accounting

principles,

practices

or

policies;

(26)

Prudential

Financial,

Inc.’s

primary

reliance,

as

a

holding

company, on dividends or distributions from its subsidiaries to meet debt payment

obligations and the ability of the subsidiaries to pay such dividends

or

distributions

in

light

of

our

ratings

objectives

and/or

applicable

regulatory

restrictions;

and

(27)

risks

due

to

the

lack

of

legal

separation

between our Financial Services Businesses and our Closed Block Business. Prudential

Financial, Inc. does not intend, and is under no obligation, to update any

particular forward-looking statement included in this presentation. See

“Risk Factors” included in Prudential Financial, Inc.’s

Annual Report on Form 10-K and Quarterly Reports on Form 10-Q for discussion of

certain risks relating to our businesses and investment in our securities.

_______________________________________________________________________________

Prudential Financial, Inc. of the United States is not affiliated with Prudential

PLC which is headquartered in the United Kingdom. |

Non–GAAP Measures

This

presentation

includes

references

to

“adjusted

operating

income.”

Adjusted

operating

income

is

a

non-GAAP

measure

of

performance

of

our

Financial

Services

Businesses

(“FSB”).

Adjusted

operating

income

excludes

“Realized

investment

gains

(losses),

net,”

as

adjusted,

and

related

charges

and

adjustments.

A

significant

element

of

realized

investment

gains

and

losses are impairments and credit-related and interest rate-related gains

and losses. Impairments and losses from sales of credit-impaired securities, the timing of which depends largely

on market credit cycles, can vary considerably across periods. The timing of other

sales that would result in gains or losses, such as interest rate-related gains or losses, is largely

subject

to

our

discretion

and

influenced

by

market

opportunities

as

well

as

our

tax

and

capital

profile.

Realized investment gains (losses) within certain of our businesses for which such

gains (losses) are a principal source of earnings, and those associated with terminating hedges of

foreign currency earnings and current period yield adjustments are included in

adjusted operating income. Adjusted operating income excludes realized investment gains and losses from

products

that

contain

embedded

derivatives,

and

from

associated

derivative

portfolios

that

are

part

of

a

hedging

program

related

to

the

risk

of

those

products.

Adjusted

operating

income

also excludes gains and losses from changes in value of certain assets and

liabilities relating to foreign currency exchange movements that have been economically hedged or

considered part of our capital funding strategies for our international

subsidiaries, as well as gains and losses on certain investments that are classified as other trading account assets.

Adjusted operating income also excludes investment gains and losses on trading

account assets supporting insurance liabilities and changes in experience-rated contractholder liabilities

due to asset value changes, because these recorded changes in asset and liability

values are expected to ultimately accrue to contractholders. Trends in the underlying profitability of

our

businesses

can

be

more

clearly

identified

without

the

fluctuating

effects

of

these

transactions.

In

addition,

adjusted

operating

income

excludes

the

results

of

divested

businesses,

which are not relevant to our ongoing operations. Discontinued operations, which is

presented as a separate component of net income under GAAP, is also excluded from adjusted

operating income.

We

believe

that

the

presentation

of

adjusted

operating

income

as

we

measure

it

for

management

purposes

enhances

understanding

of

the

results

of

operations

of

the

Financial

Services

Businesses by highlighting the results from ongoing operations and the underlying

profitability of our businesses. However, adjusted operating income is not a substitute for income

determined in accordance with GAAP, and the adjustments made to derive adjusted

operating income are important to an understanding of our overall results of operations.

Return on equity (“ROE”) based on adjusted operating income is determined

by dividing adjusted operating income after-tax (giving effect to the direct equity adjustment for earnings per

share calculation) by average attributed equity for the Financial Services

Businesses excluding accumulated other comprehensive income related to unrealized gains and losses on

investments and accumulated other comprehensive income related to pension and

postretirement benefits. Beginning on January 1, 2012, ROE will be determined using average

attributed equity for the Financial Services Businesses excluding all of

accumulated other comprehensive income, which is indicated on slide 11 by the reference to “DAC/CTA policy

change.”

Our guidance for Common Stock earnings per share and our expectations of ROE are

based on after-tax adjusted operating income. Because we do not predict future realized

investment gains / losses or recorded changes in asset and liability values that

are expected to ultimately accrue to contractholders, we cannot provide a measure of our Common Stock

earnings

per

share

or

ROE

expectations

based

on

income

from

continuing

operations

of

the

Financial

Services

Businesses,

which

is

the

GAAP

measure

most

comparable

to

adjusted

operating income.

For

additional

information

about

adjusted

operating

income

and

the

comparable

GAAP

measure,

including

reconciliation

between

the

two,

please

refer

to

our

Forms

10-K

and

10-Q

located

on

the

Investor

Relations

website

at

www.investor.prudential.com.

Additional

historical

information

relating

to

the

Company’s

financial

performance

is

also

located

on

the

Investor

Relations website.

The

information

referred

to

above

and

on

the

prior

page,

as

well

as

the

risks

of

our

businesses

described

in

our

Forms

10-K

and

10-Q,

should

be

considered

by

readers

when

reviewing

forward-looking statements contained in this presentation.

3 |

PRUDENTIAL FINANCIAL,

INC.

NOVEMBER

3,

2011 |

PRUDENTIAL FINANCIAL, INC.

FINANCIAL OUTLOOK

|

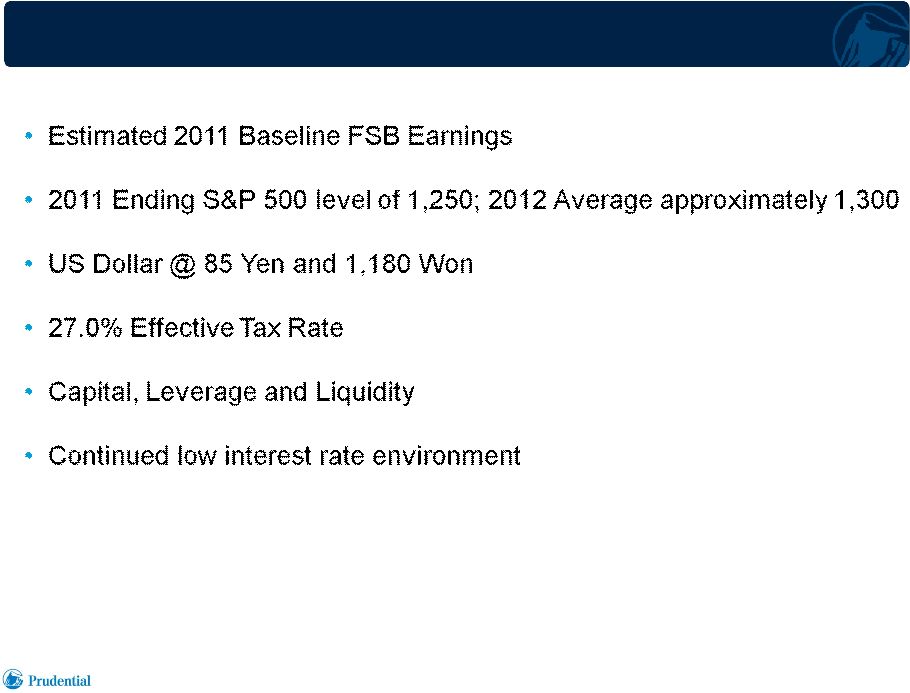

Assumptions for 2012 Outlook

(1)

1)

Financial Services Businesses [FSB].

6 |

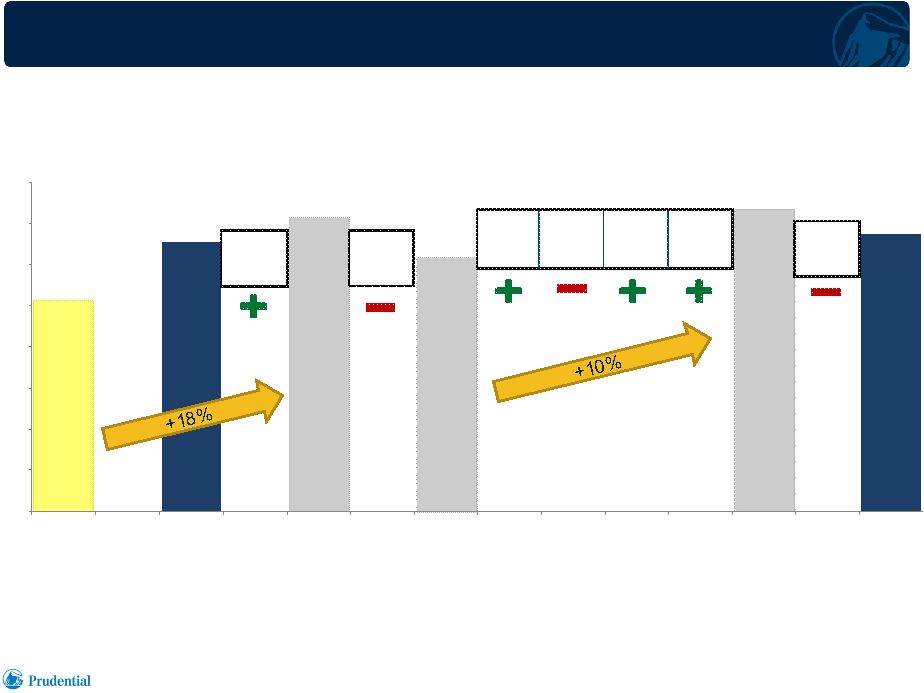

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

Financial Services Businesses

2012 FSB Earnings Guidance

1) Includes 10 months of Star & Edison earnings.

2011

Projected

[Reported]

(1)

2012

(Excl.

Star/Edison

Integration

Costs)

2012

Guidance

2010

Baseline

(Excl. DAC

Change)

$6.50 -

$6.90

$6.05 -

$6.15

$6.50 -

$6.60

$6.25 -

$6.35

$6.20 -

$6.60

2011

Baseline

Estimate

(Incl. DAC

Change)

(1)

$5.50-

$5.60

2011

Baseline

Estimate

(Excl. DAC

Change)

(1)

Unusual/

Non-

Recurring

Items

DAC

Accounting

Change

Capital

Deployment

Organic

Business

Growth

Corporate

& Other

Star/Edison

Earnings

(Excl.

Integration

Costs)

Star/Edison

Integration

Costs

7 |

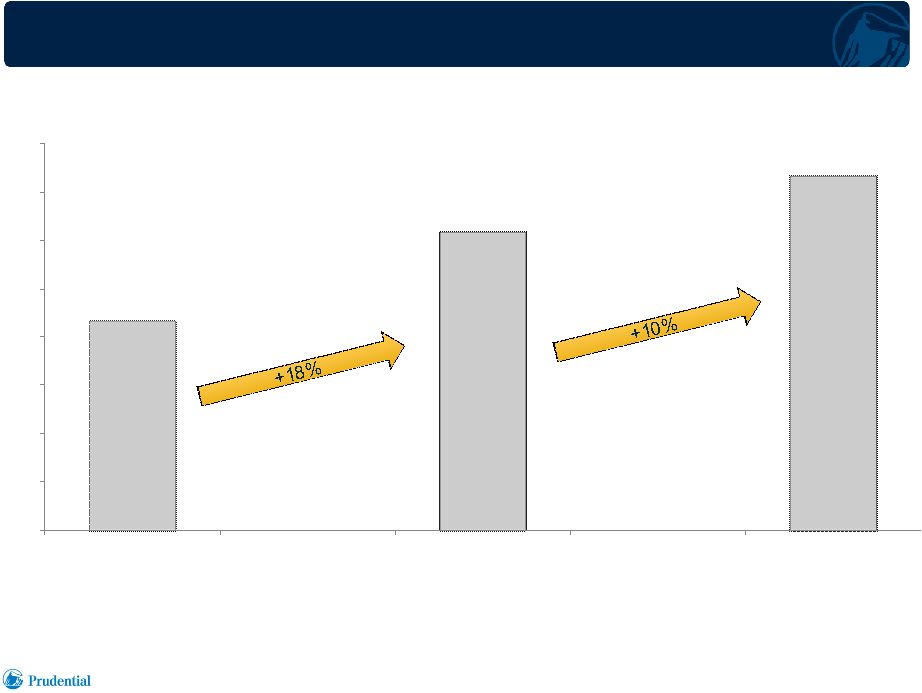

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

Financial Services Businesses

2012 FSB Earnings Guidance

2011

Baseline

Estimate

(Incl. DAC

Change)

$6.45 -

$6.55

$6.05 -

$6.15

2010

Baseline

(Incl. DAC

Change)

2012

Baseline

Guidance

(Incl. DAC

Change)

$6.50 -

$6.90

$5.10-

$5.20

8 |

2011

Capital and Liquidity Financial Services Businesses (“FSB”)

1)

Required

Capital

represents

the

amount

of

GAAP

capital

necessary

to

support

business

risk

based

on

AA

rating

targets

at

the

operating

entities.

2)

Excludes accumulated other comprehensive income related to unrealized gains and

losses on investments and pension and postretirement benefits. 3)

Based on targeted Risk Based Capital (“RBC”) ratio of 400% for Prudential

Insurance. 4)

For the purposes of calculating this ratio, PFI’s outstanding hybrid

securities are considered 25% equity and 75% debt. 5)

Net cash includes cash, cash equivalents, and short-term investments, reduced

by commercial paper borrowings and cash held in an intra-company liquidity account at PFI.

6)

Prudential

Insurance

RBC

as

of

the

fiscal

year

end,

December

31,

2010.

The

inclusion

of

RBC

measures

is

intended

solely

for

the

information

of

investors

and

is

not

intended

for

the

purpose of ranking any insurance company or for use in connection with any

marketing, advertising or promotional activities. 7)

Calculated under new solvency margin rules as of fiscal year end March 31,

2011 and March 31, 2012. Gibraltar March 31, 2012 forecast is pro forma for the merger with Star/Edison.

($ in Billions)

12/31/2010 Pro-Forma for

Acquisition of Star/Edison

and Divestiture of Global

Commodities

12/31/2011

Required Capital

(1)

$35.0 –

$35.5

$37.0 -

$37.5

Attributed Equity

(2)

$29.2

$31.2

Capital Debt and Hybrids Outstanding

$10.3

$10.3

Total Capital Outstanding

$39.5

$41.5

Total

Available

On

Balance

Sheet

Capital

(3)

$4.0 –

$4.5

$4.0 -

$4.5

Estimated “Readily Deployable”

Capital

$2.2 –

$2.7

$2.2 -

$2.7

Capital Debt to Capital Ratio

(4)

25%

24%

Prudential Financial, Inc. Net Cash

(5)

~$3.0

~$3.2

Regulatory Capital Ratios

Prudential Insurance RBC

(6)

533%

>500%

POJ Solvency Margin Ratio

(7)

703%

>700%

Gibraltar Solvency Margin Ratio

(7)

657%

>650%

9 |

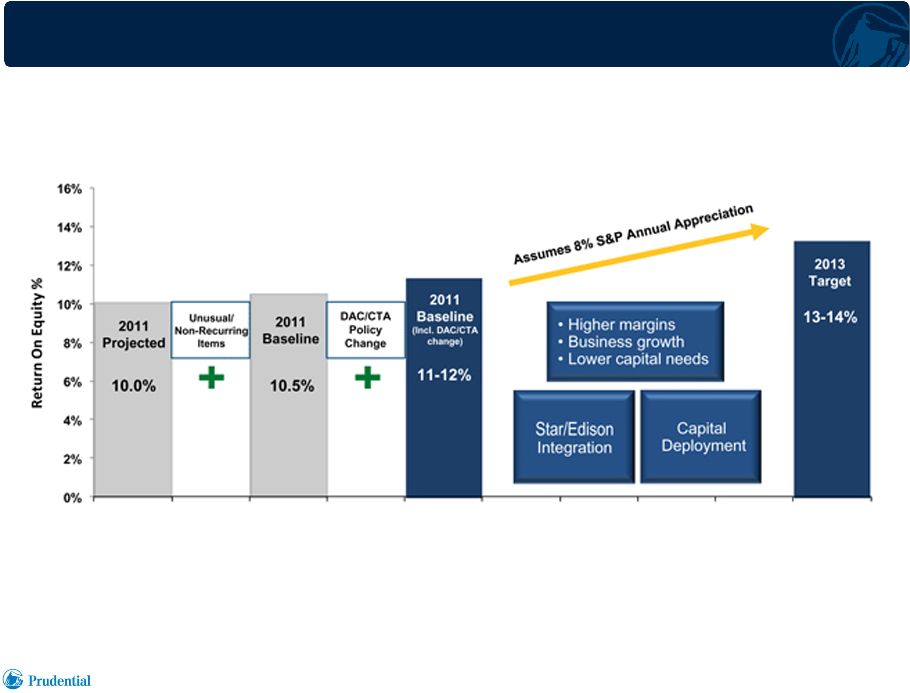

Considerations for Long Term ROE

(1)

1)

Financial Services Businesses.

•

Capital Deployment

–

Funding Organic Growth, Acquisitions and/or Share Repurchases

•

Organic Business Growth

•

8% S&P Growth

•

US Dollar @ 78 Yen and 1,110 Won

•

Successful Integration of Star Edison

•

AOCI Treatment Consistent with Peers

•

Debt to Capital @ 25%

10 |

Business Plan for ROE Growth: 2011 –

2013

(1)

1) Financial Services Businesses.

11 |

QUESTIONS AND ANSWERS PRUDENTIAL FINANCIAL,

INC.

NOVEMBER

3,

2011 |