Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - JOHNSON CONTROLS INC | d248422d8k.htm |

| EX-99.1 - PRESS RELEASE ISSUED BY JOHNSON CONTROLS, INC., DATED OCTOBER 27, 2011 - JOHNSON CONTROLS INC | d248422dex991.htm |

October 27, 2011

Quarterly update

FY 2011 fourth quarter

Exhibit 99.2 |

Agenda

Introduction

Glen Ponczak, Vice President, Global Investor Relations

Overview

Steve Roell, Chairman and Chief Executive Officer

Business results and financial review

Bruce McDonald, Executive Vice President and Chief Financial Officer

Q&A

FORWARD-LOOKING STATEMENT

Johnson Controls, Inc. has made forward-looking statements in this document

pertaining to its financial results for fiscal 2012 and beyond that are

based on preliminary data and are subject to risks and uncertainties. All

statements, other than statements of historical fact, are statements that

are,

or

could

be,

deemed

"forward-looking"

statements

and

include

terms

such

as

"outlook,"

"expectations,"

"estimates"

or

"forecasts."

For

those

statements, the Company cautions that numerous important factors, such as

automotive vehicle production levels, mix and schedules, energy and

commodity

prices,

the

strength

of

the

U.S.

or

other

economies,

currency

exchange

rates,

cancellation

of

or

changes

to

commercial

contracts,

changes in the levels or timing of investments in commercial buildings as well as

other factors discussed in Item 1A of Part I of the Company's most recent

Form 10-k filing (filed November 23, 2010) could affect the Company's actual results and could cause its actual consolidated results to

differ materially from those expressed in any forward-looking statement made

by, or on behalf of, the Company. 2 |

3

Record FY 2011 results despite a mixed

macro environment

-

(+) Benefitted from global automotive recovery

-

(-) Weak Building Efficiency markets

-

(-) Negative impact of Japan earthquake /

tsunami

Outperformed our underlying markets

Increased clarity of AGM growth opportunity

Record level of investments to support growth

2011 full year results

Record sales and earnings

–

$1.4 billion in acquisitions

–

$1.3 billion in capital expenditures

–

FY 2011: Double-digit top and bottom line

improvements, market share gains in all three

businesses |

2011

full year results Record sales and earnings

Sales: $40.8 billion

vs. $34.3 billion in 2010 (+19%)

Segment income*: $2.4 billion

vs. $1.9 billion in 2010

Net income*: $1.7 billion

vs. $1.4 billion in 2010

EPS*: $2.40 per diluted share

vs. $1.99 in 2010 (+21%)

4

*Excluding non-recurring items |

Entering 2012

Good momentum

Benefits of strategic M&A and capital growth

investments

Strong backlogs

–

$2.3 billion in newly booked business leading to

Automotive

backlog

of

$4.2

billion

(2012

–

14)

–

Building Efficiency up 8% at end of 2011

Geographic and capacity expansions

in emerging markets

Underlying strength of battery aftermarket

Operational / quality improvements

Johnson Controls

5 |

2011

fourth quarter Record sales and earnings

Sales: $10.8 billion

vs. $9.0 billion in 2010 (+19%)

Segment income*: $725 million

vs. $586 million in Q4 2010

Net income*: $514 million

vs. $409 million in Q4 2010

EPS*: $0.75 per diluted share

vs. $0.60 in Q4 2010 (+25%)

6

*Excluding non-recurring items in 2011 and 2010 quarters

Q4 results are consistent with the

October 12, 2011 earnings pre-announcement |

2011

fourth quarter Automotive Experience

2011

2010

Net sales

$5.1B

$4.1B

24%

Europe up 45%

–

Up 26%, excluding acquisitions

North America up 7%

Asia up 15%; strength in Korea; Japan slightly lower

China sales (mostly non-consolidated): up 20% to $1.1 billion Segment income*

$234M

$129M

81%

Higher volume

Europe: $79 million turnaround vs. Q4 2010

–

Margin of 2.9% vs. loss in prior year

–

“Containment

costs”

trending

lower

Higher JV profitability in Asia

7

2012-2014: $4.2B backlog

2012 $1.0 billion

2013 $1.5 billion

2014 $1.7 billion

71% consolidated; 29%

non-consolidated

53% Europe, 34% Asia,

13% North America

*Excluding non-recurring items

Fiscal Q4 production

North America up 6%

Europe up 5%

China up 8% |

2011

fourth quarter Building Efficiency

2011

2010

Net sales

$4.1B

$3.6B

14%

Higher revenues in all segments

–

Global Workplace Solutions up 24%

–

North America up 7%

–

Asia up 17%

–

Middle East up 51%

–

Europe up 9%

Segment income*

$278M

$275M

1%

Double

digit

increases

in

Asia

(up

27%),

North

America

systems

(up

13%),

Middle

East

(“Other”

segment,

up

34%)

Lower segment income

–

North America Services: Solutions contract reserves,

acquisition-related costs, investments in infrastructure

–

Global Workplace Solutions: costs associated with new

contracts

NOTE: 9.3% segment income margin excluding GWS

8

Commercial backlog

and orders

(at September 30, 2011)

Record $5.1B, up 8%

Backlog up in all

geographic markets,

strongest in Asia

Orders level with 2010

–

Asia up 18%

–

Europe up 10%

–

N. America flat

Timing of energy

solutions orders

–

Middle East down

*Excluding restructuring and non-recurring items

Global chiller

shipments up 19% |

2011

fourth quarter Power Solutions

2011

2010

Net sales

$1.6B

$1.3B

19%

Sales up 12%, excluding lead

Aftermarket unit volume up 4%

OE unit volume up 2%

Benefitting from favorable product mix

Segment income*

$213M

$182M

17%

Improving product mix

Increased vertical integration

Production interruption in China

9

*Excluding non-recurring items

Q4 average lead prices

2011:

$2,558

/

ton

-

up

26%

2010:

$2,030

/

ton |

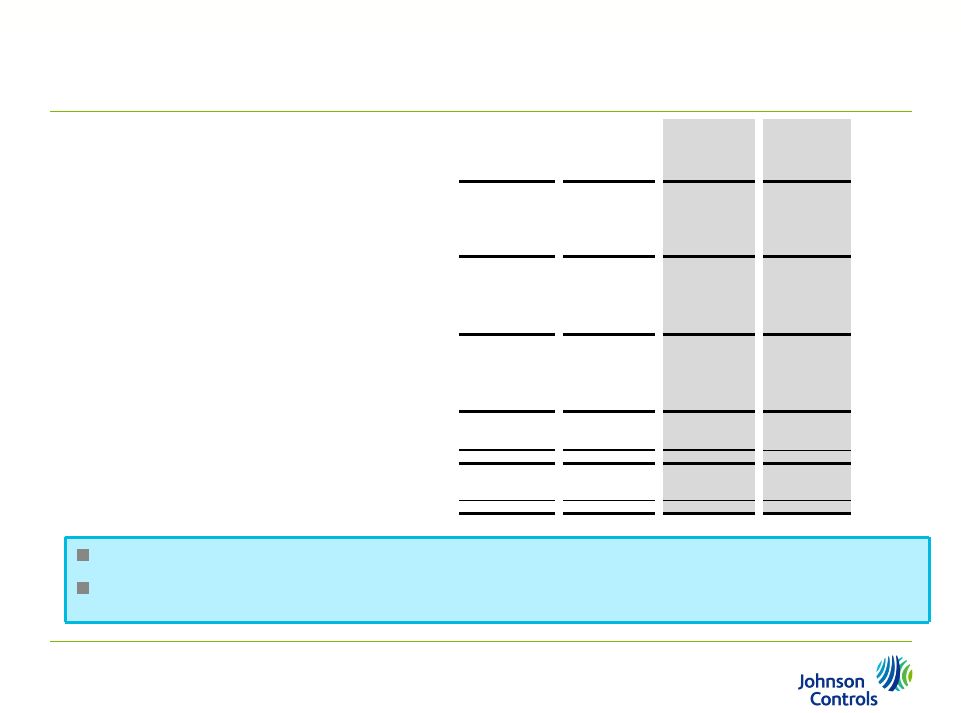

Fourth quarter 2011

Financial highlights

10

(in millions)

2011*

(excluding items)

2010*

(excluding items)

%

change

2011

(reported)

2010

(reported)

Sales

$10,788

$9,040

19%

$10,788

$9,040

Gross profit

% of sales

1,732

16.1%

1,502

16.6%

15%

1,732

16.1%

1,491

16.5%

SG&A expenses

1,085

975

11%

1,128

985

Equity income

78

59

32%

115

98

Segment income

$725

$586

24%

$719

$604

6.7%

6.5%

6.7%

6.7%

FX

–

Euro

to

U.S.

dollar

average

exchange

rate

at

$1.41

in

Q4

2011

vs.

$1.29

in

2010

Sales

–

Excluding

FX,

sales

up

15%

Gross

profit

–

Higher

volumes

offset

by

product

mix

SG&A

–

Investments

in

innovation

and

growth

opportunities;

70

bps

improvement

vs.

prior

year

as a percentage of sales

* 2011 excludes net one-time income on joint ventures of $37 million and

restructuring charges of $43 million; 2010 excludes an one-time

gain on a Korean JV acquisition of $37 million and an impairment charge of $19 million in

Automotive Experience. |

Fourth quarter 2011

Financial highlights

Income tax provision –

Underlying 2011 tax rate of 19% vs. 18% in 2010

Non-controlling interests –

Improved profitability in consolidated Automotive JVs

11

(in millions, except earnings per share)

2011*

(excluding

items)

2010*

(excluding

items)

2011

(reported)

2010

(reported)

Segment income

$725

$586

$719

$604

Financing charges -

net

50

53

50

53

Income before taxes

675

533

669

551

Income tax provision

126

96

96

74

Net income

549

437

573

477

Income attributable to non-controlling interests

35

28

35

28

Net income attributable to JCI

$514

$409

$538

$449

Diluted earnings per share

$0.75

$0.60

$0.78

$0.66

* 2011

excludes

net

one-time

income

on

joint

ventures

of

$37

million,

restructuring

charges

of

$43

million

and

non-

recurring tax benefits of $30 million. 2010 excludes an one-time gain on

a Korean JV acquisition of $37 million, an impairment charge of $19 million

in Automotive Experience and non-recurring tax benefits of $22 million. |

2011

fourth quarter Balance sheet

12

Cash provided by operations of $587 million

Discretionary pension and post-retirement

funding

–

Approximately $175 million in Q4 ($440m in FY11)

Improved Q4 working capital performance

–

Adjusted for discretionary pension / retirement

funding, source of $45 million versus a use of

$200 million in Q4 2010

Increased capital spending to $425 million,

$174 million higher than Q4 2010

Strong balance sheet

Net debt / total capitalization:

31% at year-end |

2012

outlook 13

Forecast: Fiscal year 2012

Revenues:

$44.2

billion,

up

8%

EPS:

$2.85

-

$3.00,

up

19

–

25%

Q1 2012

$0.60 -

$0.62 / share

9 -

13% improvement Y-O-Y

Near-term outlook

No change to the

October 12, 2011 guidance

Automotive volumes remain stable Operational and quality improvements Integration of

acquisitions

Execution of backlogs

China battery production interruptions |