Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SIGMA ALDRICH CORP | d246500d8k.htm |

| EX-99.1 - PRESS RELEASE - SIGMA ALDRICH CORP | d246500dex991.htm |

Sigma-Aldrich Corporation

Q3 2011 Earnings Review & 2011 Outlook

•

Enabling Science to Improve the Quality of Life

Exhibit 99.2 |

2

2

Cautionary Statements

Our presentation today will include forward looking statements relating to the

Company’s future performance, goals, strategic actions and initiatives

and similar intentions and beliefs, including expectations, outlook, goals, beliefs, intentions and the like regarding future sales,

earnings, free cash flow, share repurchases, acquisitions and other matters. These

statements are based on assumptions regarding Company operations, investments

and acquisitions and conditions in the markets the Company serves. We believe that these

assumptions

are

reasonable

and

well-founded.

The

forward-looking

statements

in

this

presentation

are

subject

to

risks

and

uncertainties

including, among others, certain economic, political and technological factors.

Actual results could differ materially from those stated or implied during

this review or contained in other Company communications due to, but not limited to, such factors as (1) global economic

conditions, (2) changes in pricing and the competitive environment and the global

demand for our products, (3) fluctuations in foreign currency

exchange

rates,

(4)

changes

in

research

funding

and

the

success

of

research

and

development

activities,

(5)

failure

of

planned

sales initiatives in our Research and SAFC businesses, (6) dependence on

uninterrupted manufacturing operations, (7) failure to achieve planned cost

reductions in global supply chain initiatives and restructuring actions, (8) changes in the regulatory environment in which the

Company operates, (9) changes in worldwide tax rates or tax benefits from domestic

and international operations, including the matters described

in

Note

10–Income

Taxes–

to

the

Consolidated

Financial

Statements

in

the

Company’s

Form

10-K

report

for

the

year

ended

December 31, 2010, (10) exposure to litigation, including product liability

claims, (11) the ability to maintain adequate quality standards, (12)

reliance

on

third

party

package

delivery

services,

(13)

an

unanticipated

increase

in

interest

rates,

(14)

other

changes

in

the

business

environment in which the Company operates, (15) the outcome of the outstanding

matters described in Note 11-Contingent Liabilities and Commitments to

the Consolidated Financial Statements-in the Company’s Form 10-K report for the year ended December 31, 2010, and

(16) acquisitions or divestitures of businesses. A further discussion of risk

factors can be found in Item 1A of Part 1 of the Company’s Form

10-K report for the year ended December 31, 2010. The Company does not undertake any obligation to publicly update the matters

covered in this presentation.

With over 60% of sales denominated in currencies other than the U.S. dollar,

management uses currency adjusted sales growth when analyzing

Company

performance,

and

believes

it

is

useful

as

well

to

investors,

to

judge

the

Company’s

performance.

Organic

sales

growth

data

presented

in

this

review

excludes

currency

and

acquisitions

impacts.

The

Company

calculates

the

impact

of

changes

in

foreign

currency rates by multiplying current period activity by the difference between

current period exchange rates and prior period exchange rates, the result is

the defined impact of “changes in foreign currency exchange rates”. While we are able to report currency impacts after

the

fact,

we

are

unable

to

estimate

changes

that

may

occur

later

in

2011

to

applicable

exchange

rates.

Any

significant

changes

in

currency

exchange

rates

would

likely

have

a

significant

impact

on

our

reported

growth

rates

due

to

the

volume

of

our

sales

denominated

in

foreign

currencies.

Management also uses adjusted net income and EPS and adjusted operating income and

operating income margins and free cash flow, non-GAAP

measures,

to

judge

its

performance

and

ability

to

pursue

opportunities

that

enhance

shareholder

value.

Due

to

the

uncertain

timing

of

future

restructuring

and

other

special

charges,

we

are

unable

to

include

these

charges

in

the

2011

diluted

adjusted

EPS

forecast

or provide a reconciliation to the corresponding GAAP measures. Management believes

this non-GAAP information is useful to investors as well. Management

believes this non-GAAP information is useful to investors as well. Reconciliations of GAAP to non-GAAP information

are included in the Company’s October 25, 2011 earnings release posted on its

website, www.sigma-aldrich.com, and in the Appendix –

Reconciliation of GAAP to Non-GAAP Financial Measures beginning on Slide

15. |

3

Third Quarter 2011 Financial Results

($ in millions, except per share amounts)

3

YEAR-OVER-YEAR

Net

Income

and

Diluted

EPS

Up

25%

As

Reported

Q3 2011

Excluding

Restructuring

As

Reported

Excluding

Restructuring

and Impairment

Net Income

$ 117

$ 118

26%

15%

Diluted EPS

$0.95

$0.96

25%

16%

Free Cash Flow

$ 90

26%

Q3 2011

As

Reported

Excluding

Currency and

Acquisition

Impacts

Sales

$ 626

11%

4%

YEAR-OVER-YEAR

(1)

(1)

See page 20 for reconciliation of Net Cash Provided by Operating Activities to Free Cash Flow

|

4

First Nine Months

2011 Financial Results

($ in millions, except per share amounts)

4

YEAR-OVER-YEAR

Year-to-Date Sales and Earnings On-Track

Excluding

Restructuring

As

Reported

Excluding

Restructuring

and Impairment

Net Income

$ 349

$ 354

20%

16%

Diluted EPS

$ 2.84

$ 2.88

20%

16%

Free Cash Flow

$ 300

10%

Nine

Months

2011

As

Reported

Excluding

Currency and

Acquisition

Impacts

Sales

$1,895

12%

6%

YEAR-OVER-YEAR

Nine

Months

2011

(1)

See page 20 for reconciliation of Net Cash Provided by Operating Activities to

Free Cash Flow (1) |

5

5

2011 Sales Growth

RESEARCH

71%

29%

SAFC

Sales Mix (YTD)

Double Digit Reported Sales Growth in 2011

Research

SAFC

Total

Company

Organic*

*Adjusted for Currency & Acquisitions

Reported

Q3 2011 / Q3 2010

Organic*

Reported

Nine Months 2011/

Nine Months 2010

13%

4%

12%

4%

8%

2%

14%

9%

11%

12%

6%

4% |

6

25.4%

100 basis points

40 basis points

6

Margin Analysis

Adjusted Operating Margins Show Improvement Year-Over-Year

PERCENTAGE OF SALES

25.6%

0.4

0.4

YTD

25.7%

0.4

0.4

Reported Operating Margin -

2011

Q3

26.1%

Restructuring Costs

Adjusted Operating Margin -

2011

Acquisitions

26.4%

26.5%

Adjusted Operating Margin -

2010

Improvement |

7

7

Free Cash Flow

(in millions)

2011

$349

79

(85)

30

373

(73)

$300

Net Income

Free Cash Flow

Net Cash Provided by Operating Activities

Less Capital Expenditures

Other

Changes in Performance Working Capital*

Depreciation & Amortization

2010

$290

69

(24)

62

397

(65)

$332

*Accounts Receivable + Inventory –

Accounts Payable

NINE MONTHS ENDED SEPTEMBER 30

Working Capital Increase to Support Sales Growth |

8

Strategic Priorities for Growth

•

Research Business Growth

•

Innovation and product leadership in faster growing segments

•

Leverage broad offering, customer service and distribution

•

New

products

in

proteomics,

epigenomics

and

molecular

biology

•

SAFC Growth

•

Cell culture media for biological drugs and suite of capabilities for biological

manufacturing customers

•

Chemicals for electronic applications (LEDs, semiconductors, solar panels,

other) Driving Growth Along Several Fronts |

9

Strategic Priorities for Growth

•

Geographic Growth

•

Focus on faster growing emerging markets in Asia Pacific and Latin America

•

E-

Commerce

•

Enhanced search experience

•

Expand local language capability

•

M&A

•

Robust pipeline

Driving Growth through Channel and Footprint Expansion

|

10

10

Q3 Sales Performance

Innovation

Reported

Organic

(1)

•

Analytical, Biology, Materials Science

Sales Growth

(2)

10-22%

3-10%

SAFC Sales

•

Build on momentum in key product segments

8%

2%

Geographic Growth

•

North America

6%

3%

•

Europe

11%

2%

•

Asia Pacific/Latin America

22%

9%

•

Focus Markets –

India, China, Brazil

46%

25%

eCommerce Sales

% of Research Sales

•

Research Sales via eCommerce

channels

50%

Initiatives Collectively on Track

(1)

Adjusted for currency and acquisitions. See pages 18 & 19 for

reconciliation of reported growth to organic growth. (2)

Varies for individual product lines |

11

11

Third Quarter 2011 Highlights

•

ZFN technology applications growing with increased market penetration

•

Introduced ZFN modified Chinese Hamster Ovary cell lines for bioproduction

•

Established collaboration to develop novel energy and electronics materials

including rare earth materials and quasicrystals

•

Wuxi, China facility is on pace to open near year end 2011

•

Completed expansion of Bangalore, India facility to provide expanded

distribution and packaging

•

Increased capacity for liquid media

•

Taiwan SAFC Hitech facility construction expected to be completed in Q1 2012

Continued Focus on Long-term Growth Opportunities |

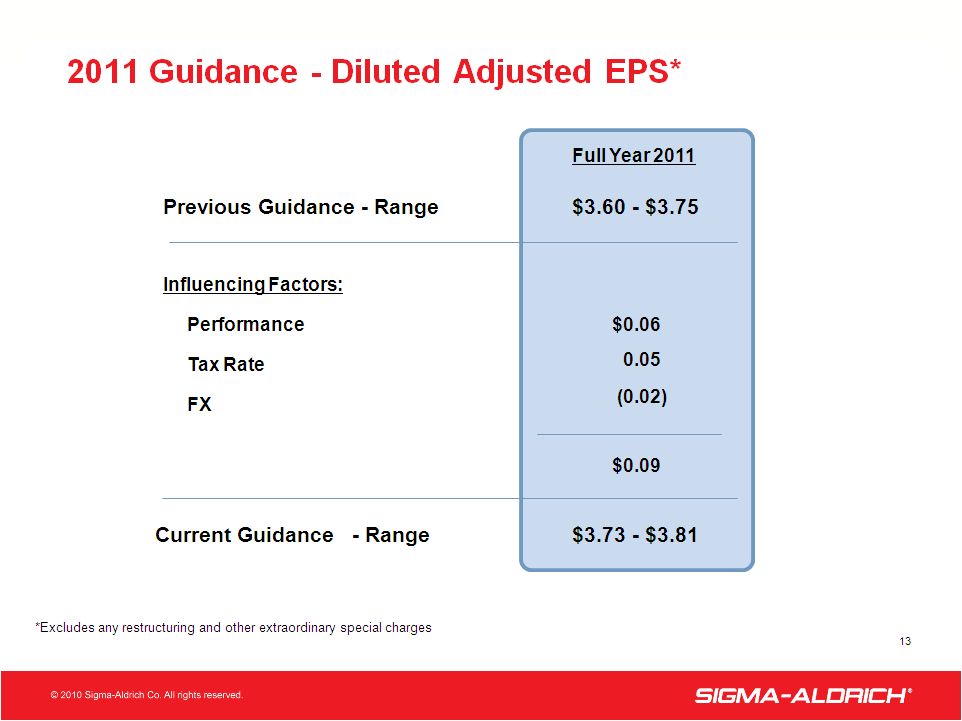

12

12

2011 Guidance

Organic Revenue Growth

Free Cash Flow

Mid-single digits

~$400M

*Excludes any restructuring and other extraordinary special charges

Diluted Adjusted EPS*

Q1

Q2

Q3

Q4

Full Year

$0.98

28%

Tax Rate

$0.93

28%

$0.96

$0.85 -

$0.93

$3.73 -

$3.81

27%

28% -

29%

30% -

31% |

2011

Guidance - Diluted Adjusted EPS* |

14

QUESTIONS?

Sigma-Aldrich Corporation

Q3 2011 Earnings Review |

15

Appendix

Reconciliation of GAAP to Non-GAAP

Financial Measures |

16

Reconciliation of Reported Net Income and Diluted Earnings

Per Share to Adjusted Net Income and Adjusted Diluted

Earnings Per Share (Unaudited)

2011

2010

2011

2010

Reported net income

117

$

93

$

0.95

$

0.76

$

Restructuring costs

1

3

0.01

0.02

Impairment costs

-

7

-

0.05

Adjusted net income

118

$

103

$

0.96

$

0.83

$

2011

2010

2011

2010

Reported net income

349

$

290

$

2.84

$

2.36

$

Restructuring costs

5

9

0.04

0.07

Impairment costs

-

7

-

0.05

Adjusted net income

354

$

306

$

2.88

$

2.48

$

(in millions)

Per Share

Nine Months Ended

Nine Months Ended

Net Income

Diluted Earnings

Net Income

Diluted Earnings

(in millions)

Per Share

September 30,

September 30,

September 30,

September 30,

Three Months Ended

Three Months Ended |

17

Reconciliation of Reported Operating Income Margin to

Adjusted Operating Income Margin (Unaudited)

2011

2010

2011

2010

Reported operating income margin

25.6%

23.4%

25.7%

24.9%

Restructuring costs

0.4%

0.7%

0.4%

0.8%

Impairment Costs

-

1.3%

-

0.4%

Operating income margin excluding restructuring

26.0%

25.4%

26.1%

26.1%

and impairment costs

Acquisitions

0.4%

0.4%

Adjusted operating income margin

26.4%

25.4%

26.5%

26.1%

Three Months Ended

Nine Months Ended

September 30,

September 30, |

18

Reconciliation of Reported Sales Growth to Adjusted (Organic)

Sales Growth (Unaudited)

Three Months Ended September 30, 2011

Reported

FX Impact

Acquisitions

Organic

•

Analytical, Biology, Materials Science Sales

Growth 10-22%* 6-7%* 0-12%* 3-10%*

Geographic Growth

•

North

America

6%

–% 3%

3%

•

Europe

11%

9% –%

2%

•

Asia Pacific/Latin

America

22%

8% 5%

9%

•

Focus

Markets

–

India, China,

Brazil

46%

5%

16% 25% *Varies for individual

product areas |

19

Reconciliation of Reported Sales Growth to Adjusted (Organic)

Sales Growth (Unaudited)

Currency

Acquisition

Adjusted

Reported

Benefit

Benefit

(Organic)

Research Essentials

15%

6%

3%

6%

Research

Specialties 12%

6%

4%

2%

Research

Biotech 12%

6%

-

6%

Research

Chemicals 13%

6%

3%

4%

SAFC

8%

4%

2%

2%

Total Customer

Sales 11%

5%

2%

4%

Currency

Acquisition

Adjusted

Reported

Benefit

Benefit

(Organic)

Research Essentials

13%

5%

2%

6%

Research

Specialties 11%

5%

3%

3%

Research

Biotech 10%

5%

-

5%

Research

Chemicals 12%

5%

3%

4%

SAFC

14%

4%

1%

9%

Total Customer

Sales 12%

5%

1%

6%

Ended September 30, 2011

Nine Months

Three Months

Ended September 30, 2011 |

20

Reconciliation of Net Cash Provided by Operating Activities to

Free Cash Flow (Unaudited)

In millions

2011

2010

Net cash provided by operating activities

119

$

150

$

Less: Capital expenditures

(29)

(28)

Free cash flow

90

$

122

$

2011

2010

Net cash provided by operating activities

373

$

397

$

Less: Capital expenditures

(73)

(65)

Free cash flow

300

$

332

$

Three Months Ended

September 30,

September 30,

Nine Months Ended |