Attached files

Table of Contents

As filed with the Securities and Exchange Commission on October 21, 2011

Registration Statement No. 333-175579

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NORWEGIAN CRUISE LINE HOLDINGS LTD.

(Exact name of registrant as specified in its charter)

| Bermuda | 4400 | 98-0691007 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

7665 Corporate Center Drive

Miami, Florida 33126

(305) 436-4000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Daniel S. Farkas

Senior Vice President and General Counsel

Norwegian Cruise Line Holdings Ltd.

7665 Corporate Center Drive

Miami, Florida 33126

Telephone: (305) 436-4000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Gregory A. Ezring, Esq. Tracey A. Zaccone, Esq. Paul, Weiss, Rifkind, Wharton & Garrison LLP 1285 Avenue of the Americas New York, New York 10019 Telephone: (212) 373-3000 Facsimile: (212) 757-3990 |

William B. Kuesel, Esq. O’Melveny & Myers LLP 7 Times Square New York, New York 10036 Telephone: (212) 326-2000 Facsimile: (212) 326-2061 |

Jonathan A. Schaffzin Luis R. Penalver Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005 Telephone: (212) 701-3000 Facsimile: (212) 269-5420 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ | |

|

Non-accelerated filer (Do not check if a smaller reporting company) x |

Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Offering Price(1)(2) |

Amount of Fee(3) | ||

| Ordinary shares, par value $.001 per share |

$250,000,000 | $29,025 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purposes of calculating the amount of the registration fee pursuant to Rule 457(o). |

| (2) | Including ordinary shares which may be purchased by the underwriters. |

| (3) | The registration fee was paid in full in connection with the initial filing of this Form S-1 on July 15, 2011. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

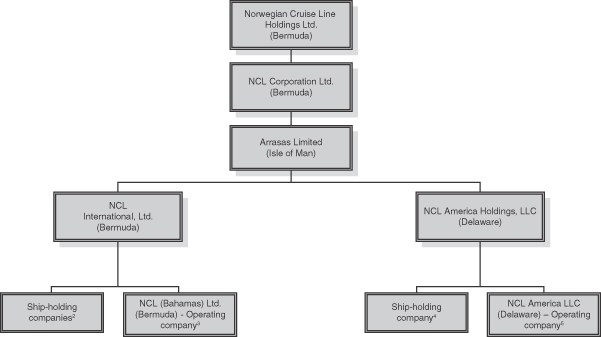

EXPLANATORY NOTE

This Registration Statement on Form S-1 is being filed by Norwegian Cruise Line Holdings Ltd. (the “Issuer”). Following completion of a corporate reorganization to be commenced in connection with consummation of the offering of ordinary shares covered by this Registration Statement, the Issuer will become the direct parent company of NCL Corporation Ltd.

NCL Corporation Ltd. has previously filed a Registration Statement on Form S-1 (File No. 333-170141) that relates to a comparable offering to the offering contemplated by this Registration Statement. In connection with the filing of this Registration Statement, NCL Corporation Ltd. is withdrawing its Registration Statement.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 21, 2011

PRELIMINARY PROSPECTUS

Ordinary Shares

NORWEGIAN CRUISE LINE HOLDINGS LTD.

This is the initial public offering of our ordinary shares, par value $.001 per share, which we refer to as our ordinary shares. We are a newly formed holding company which, upon the consummation of this offering, will own 100% of the ordinary shares of NCL Corporation Ltd. and will be the issuer of the ordinary shares being offered hereby. We are selling an aggregate of ordinary shares in this offering.

Prior to the offering, there has been no public market for our ordinary shares. We expect the initial public offering price to be between $ and $ per ordinary share. We expect to apply for listing of our ordinary shares on the NASDAQ Global Select Market under the symbol “NCLH”.

We have granted the underwriters an option for a period of 30 days to purchase from us an aggregate of up to additional ordinary shares.

Investing in our ordinary shares involves a high degree of risk. See “Risk Factors” beginning on page 18 to read about certain factors you should consider before buying our ordinary shares.

| Per Share | Total | |||

| Initial public offering price |

||||

| Underwriting discounts and commissions |

||||

| Proceeds to new holding company before expenses |

The underwriters expect to deliver the ordinary shares on or about , 2011.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Ordinary shares may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 1998, which regulates the sale of securities in Bermuda. Further, the Bermuda Monetary Authority (the “BMA”) must approve all issues and transfers of shares of a Bermuda exempted company under the Exchange Control Act of 1972 and regulations thereunder (together, the “ECA”). The BMA has given a general permission which will permit the issue of the ordinary shares and the free transferability of such shares under the ECA so long as voting securities of the Company are admitted to trading on the NASDAQ Global Select Market or any other appointed stock exchange. In addition, we will deliver to and file a copy of this prospectus with the Registrar of Companies in Bermuda in accordance with Bermuda law. The BMA and the Registrar of Companies do not accept any responsibility for the financial soundness of any proposal or for the correctness of any of the statements made or opinions expressed herein.

| UBS Investment Bank | Barclays Capital |

Goldman, Sachs & Co.

The date of this prospectus is , 2011.

Table of Contents

Table of Contents

| Page | ||||

| ii | ||||

| v | ||||

| 1 | ||||

| 18 | ||||

| 32 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 39 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

41 | |||

| 54 | ||||

| 79 | ||||

| 86 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

106 | |||

| 110 | ||||

| 116 | ||||

| 125 | ||||

| 137 | ||||

| 138 | ||||

| 141 | ||||

| 142 | ||||

| 149 | ||||

| 149 | ||||

| 149 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus. We and the underwriters have not authorized anyone to provide you with information that is different from or additional to, that contained in this prospectus. This prospectus may only be used where it is legal to sell our ordinary shares. The information in this prospectus may only be accurate on the date of this prospectus.

i

Table of Contents

Unless otherwise indicated by the context, references in this prospectus to (i) the “Company,” “we,” “our,” “us” and “NCL” refer, prior to the consummation of this offering, to NCL Corporation Ltd. and its subsidiaries and, upon and after the consummation of this offering, to the Issuer (as defined below) and its subsidiaries, (ii) “Norwegian Cruise Line” or “Norwegian” refers to the Norwegian Cruise Line brand and “NCL America” or “NCLA” refers to our U.S.-flagged operations, (iii) “Apollo” refers to Apollo Global Management, LLC and the “Apollo Funds” refers to one or more of NCL Investment Limited, NCL Investment II Ltd., AIF VI NCL (AIV), L.P., AIF VI Euro Holdings, L.P., AAA-Guarantor Co-Invest VI, L.P., Apollo Overseas Partners (Delaware) VI, L.P., Apollo Overseas Partners (Delaware 892) VI, L.P., Apollo Overseas Partners VI, L.P. and Apollo Overseas Partners (Germany) VI, L.P., (iv) “TPG Capital” refers to TPG Capital, L.P. and the “TPG Viking Funds” refers to one or more of TPG Viking I, L.P., TPG Viking II, L.P., TPG Viking, L.P., TPG Viking AIV I, L.P., TPG Viking AIV II, L.P., and TPG Viking AIV III, L.P. and/or certain other affiliated investment funds, each an affiliate of TPG Capital, (v) “Genting HK” refers to Genting Hong Kong Limited and/or its affiliates (formerly Star Cruises Limited and/or its affiliates), and (vi) “Affiliate(s)” refers to Genting HK, the Apollo Funds and/or the TPG Viking Funds. References to the “U.S.” are to the United States of America, “dollars” or “$” are to U.S. dollars and “euros” or “€” are to the official currency of the Eurozone.

Unless otherwise indicated in this prospectus, the following terms have the meanings set forth below (all principal amounts refer to the original principal amount incurred or issued, as applicable):

| • | $334.1 million Norwegian Jewel loan. $334.1 million secured loan agreement, dated as of April 20, 2004, as amended and restated on April 2, 2009 and as further amended, by and among Norwegian Jewel Limited, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | $750.0 million senior secured revolving credit facility. $750.0 million credit agreement, dated October 28, 2009, by and among NCL Corporation Ltd., as borrower, various lenders and Nordea Bank Norge ASA, and related guarantee by Norwegian Dawn Limited, Norwegian Sun Limited, Norwegian Spirit, Ltd. and Norwegian Star Limited. |

| • | $450.0 million senior secured notes. $450.0 million aggregate amount of 11.75% senior secured notes due 2016 issued by NCL Corporation Ltd. on November 12, 2009, and guaranteed by Norwegian Dawn Limited, Norwegian Sun Limited, Norwegian Spirit, Ltd. and Norwegian Star Limited. |

| • | $250.0 million senior notes. $250.0 million aggregate amount of 9.50% senior notes due 2018 issued by NCL Corporation Ltd. on November 9, 2010. |

| • | Adjusted EBITDA. EBITDA subject to certain adjustments as set forth in note 6 to the “Prospectus Summary—Summary Consolidated Financial Data” included elsewhere in this prospectus. |

| • | Adjusted EBITDA Margin. Adjusted EBITDA as a percentage of total revenue. |

| • | Berths. Double occupancy capacity per cabin even though many cabins can accommodate three or more passengers. |

| • | Capacity Days. Berths multiplied by the number of cruise days for the period. |

| • | Charter. The hire of a ship for a specified period of time. The contract for a charter is called a charter party. A ship is “chartered-in” by an end user and “chartered-out” by the provider of the ship. |

| • | CLIA. Cruise Lines International Association, a non-profit marketing and training organization formed in 1975 to promote cruising. |

| • | Constant Currency. A calculation whereby foreign currency-denominated revenue and expenses in a period are converted at the U.S. dollar exchange rate of a comparable period in order to eliminate the effects of the foreign exchange fluctuations. |

| • | Dry-dock. A process whereby a ship is positioned in a large basin where all the fresh/sea water is pumped out in order to carry out cleaning and repairs of those parts of a ship which are below the water line. |

ii

Table of Contents

| • | €40.0 million Pride of America commercial loan. €40.0 million secured loan agreement, dated as of April 4, 2003, as amended and restated on April 2, 2009 and as further amended, by and among Pride of America Ship Holding, LLC, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | €258.0 million Pride of America loan. €258.0 million secured loan agreement, dated as of April 4, 2003, as amended and restated on April 2, 2009 and as further amended, by and among Pride of America Ship Holding, LLC, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | €308.1 million Pride of Hawai’i loan. €308.1 million Pride of Hawai’i Loan, dated as of April 20, 2004, as amended and restated on April 2, 2009 and as further amended, by and among Pride of Hawaii, LLC, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | €624.0 million Norwegian Pearl and Norwegian Gem revolving credit facility. €624.0 million revolving loan facility agreement, dated October 7, 2005, as amended and restated on April 2, 2009 and as further amended, by and among NCL Corporation Ltd., as borrower, and a syndicate of international banks, and related guarantees by Norwegian Pearl, Ltd. and Norwegian Gem, Ltd. |

| • | €662.9 million Norwegian Epic loan. €662.9 million syndicated loan facility, dated September 22, 2006, as amended and restated on April 2, 2009 and as further amended, by and among Norwegian Epic, Ltd. (f/k/a F3 Two, Ltd.), as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | Existing senior secured credit facilities. Our Newbuild credit facilities, our $750.0 million senior secured revolving credit facility, €624.0 million Norwegian Pearl and Norwegian Gem revolving credit facility, €308.1 million Pride of Hawai’i loan, $334.1 million Norwegian Jewel loan, €258.0 million Pride of America loan, €40.0 million Pride of America commercial loan, and our €662.9 million Norwegian Epic loan. |

| • | GAAP. Generally Accepted Accounting Principles in the U.S. |

| • | Gross Cruise Cost. The sum of total cruise operating expense and marketing, general and administrative expense. |

| • | Gross Tons. A unit of enclosed passenger space on a cruise ship, such that one gross ton = 100 cubic feet or 2.831 cubic meters. |

| • | Gross Yield. Total revenue per Capacity Day. |

| • | IMO. International Maritime Organization, a United Nations agency that sets international standards for shipping. |

| • | Issuer. Norwegian Cruise Line Holdings Ltd., a newly formed holding company which, upon the consummation of this offering, will own 100% of the ordinary shares of NCL Corporation Ltd. and will be the issuer of the ordinary shares being offered hereby. For additional detail regarding the Issuer, we refer you to “Prospectus Summary—Corporate Reorganization.” |

| • | Major North American Cruise Brands. Norwegian Cruise Line, Carnival Cruise Lines, Royal Caribbean International, Holland America, Princess Cruises and Celebrity Cruises. |

| • | MARPOL. The International Convention for the Prevention of Pollution from Ships, an international environmental regulation. |

| • | Net Cruise Cost. Gross Cruise Cost less commissions, transportation and other expense and onboard and other expense. |

| • | Net Revenue. Total revenue less commissions, transportation and other expense and onboard and other expense. |

iii

Table of Contents

| • | Net Yield. Net Revenue per Capacity Day. |

| • | Newbuild credit facilities. Our export credit facilities and term loan facilities entered into in connection with our agreement to purchase the two new ships we have agreed to build with Meyer Werft GmbH (the “New Ships”) as described in “Description of Certain Indebtedness—Newbuild Export Credit Facilities” and “Description of Certain Indebtedness—Newbuild Term Loan Facilities.” |

| • | Norwegian Shipboard Retirement Plan or Shipboard Retirement Plan. An unfunded defined benefit pension plan for certain crew members which computes benefits based on years of service, subject to certain requirements. |

| • | Occupancy Percentage. The ratio of Passenger Cruise Days to Capacity Days. A percentage in excess of 100% indicates that three or more passengers occupied some cabins. |

| • | Passenger Cruise Days. The number of passengers carried for the period, multiplied by the number of days in their respective cruises. |

| • | Reimbursement and Distribution Agreement or RDA. The Reimbursement and Distribution Agreement, dated August 17, 2007, by and among NCL Investment Limited, Genting HK and NCL Corporation Ltd., as amended, supplemented or modified from time to time. |

| • | SEC. U.S. Securities and Exchange Commission. |

| • | Single-day cruises. Cruises which do not enter a foreign port and vary in length from one night to several nights. |

| • | SOLAS. The International Convention for the Safety of Life at Sea, an international safety regulation. |

| • | Terminal. A building in a port through which ship passengers arrive and depart. |

iv

Table of Contents

MARKET AND INDUSTRY DATA AND FORECASTS

This prospectus includes market share and industry data and forecasts that we obtained from industry publications, third-party surveys and internal company surveys. Industry publications, including those from CLIA, and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. All CLIA information, obtained from the CLIA website “cruising.org”, relates to CLIA member lines, which represent 26 of the major North American cruise lines including NCL Corporation Ltd., which together represented 97% of the North American cruise capacity as of June 30, 2011. All other references to third party information are publicly available at nominal or no cost. We use the most currently available industry and market data to support statements as to our market position.

Although we believe that the industry publications and third-party sources are reliable, we have not independently verified any of the data from industry publications or third-party sources. Similarly, while we believe our internal estimates with respect to our industry are reliable, our estimates have not been verified by any independent sources. While we are not aware of any misstatements regarding any industry data presented herein, our estimates, in particular as they relate to market share and our general expectations, involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

v

Table of Contents

The following summary includes highlights of the more detailed information and consolidated financial statements included elsewhere in this prospectus. This summary sets forth the material terms of the offering but does not contain all of the information that you should consider before investing in our ordinary shares. For a more complete understanding of us, our business and the offering, we urge you to read this prospectus carefully, including the sections entitled “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements” and “Additional Information” and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment.

Our Company

We are a leading global cruise line operator, offering cruise experiences for travelers with a wide variety of itineraries in North America (including Alaska and Hawaii), the Mediterranean, the Baltic, Central America, Bermuda and the Caribbean. We strive to offer an innovative and differentiated cruise vacation with the goal of providing our customers the highest levels of overall satisfaction on their cruise experience. In turn, we aim to generate the highest customer loyalty and greatest numbers of repeat customers. We created a distinctive style of cruising called “Freestyle Cruising” onboard all of our ships, which we believe provides our passengers with the freedom and flexibility associated with a resort style atmosphere and experience as well as more dining options than a traditional cruise. We established the very first private island developed by a cruise line in the Bahamas with a diverse offering of activities for passengers. We are also the only cruise line operator to offer an entirely inter-island itinerary in Hawaii. By providing such a distinctive experience and appealing combination of value and service, we straddle both the contemporary and premium segments. As a result, we have been recognized for our achievements as the recipient of multiple honorary awards mainly consisting of reviews tabulated from the readers of travel periodicals such as Travel Weekly, Condé Nast Traveler, and Travel & Leisure. Our newest ship, Norwegian Epic, was awarded “Gold” in the Contemporary Ship Category as “Best Cruise Ship Overall” by Travel Weekly for the 2010 Magellan Award.

We offer a wide variety of cruises ranging from one day to three weeks. During 2010, we docked at over 125 ports worldwide, with itineraries originating from 17 ports of which 10 are in North America. In line with our strategy of innovation, many of these North American ports are part of our “Homeland Cruising” program in which we have homeports which are close to major population centers, such as New York, Boston and South Florida. This reduces the need for vacationers to fly to distant ports to embark on a cruise and helps reduce our customers’ overall vacation cost. We offer a wide selection of exotic itineraries outside of the traditional cruising markets of the Caribbean and Mexico; these include cruises in Europe, including the Mediterranean and the Baltic, Bermuda, Alaska and the industry’s only entirely inter-island itinerary in Hawaii, with our U.S.-flagged ship, Pride of America. This itinerary is unparalleled in the cruise industry, as all other competing cruise lines are registered outside the U.S. and are required to dock at a distant foreign port when providing their customers with a Hawaiian-based cruise itinerary.

Our new management team has driven the Company to achieve substantial improvements in operating results and growth in revenue and cash flow generation in a challenging market environment. Since joining the Company in late 2007, our President and Chief Executive Officer, Kevin M. Sheehan, has led a successful turnaround of the Company, including overseeing major initiatives such as improving onboard service and amenities across the fleet, expanding the line’s European presence and repositioning two of the line’s Hawaii-based ships, which had a significant impact on the profitability of the business. In addition, we appointed Wendy A. Beck as our new Executive Vice President and Chief Financial Officer and augmented our senior management team with five new Senior Vice Presidents in the areas of Sales, Marketing, Hotel Operations and Finance.

1

Table of Contents

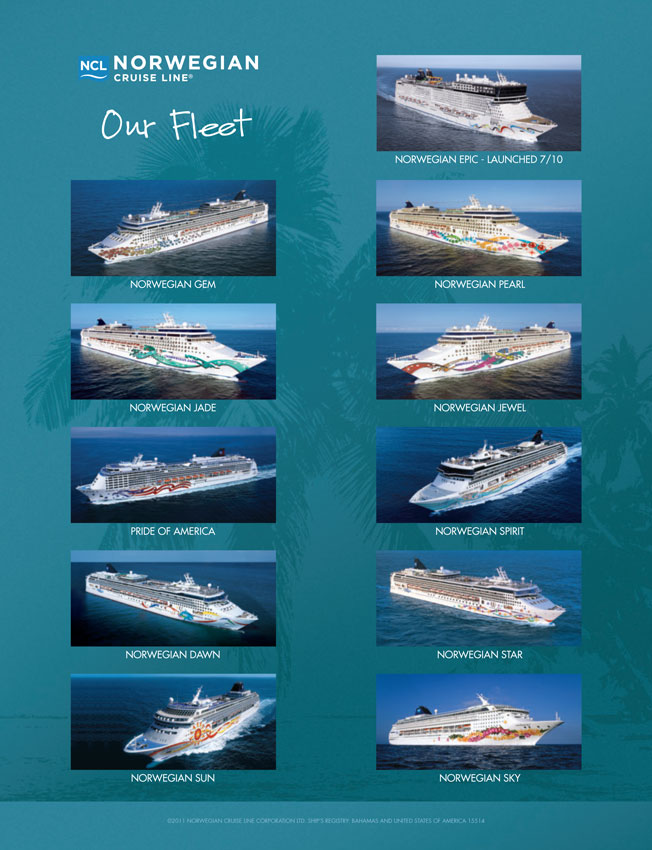

Our fleet of eleven modern ships has been purpose-built to deliver “Freestyle Cruising,” which we believe provides us with a competitive advantage given our consistent “Freestyle Cruising” product offering. By focusing on “Freestyle Cruising,” we have been able to achieve higher onboard spend levels, greater customer loyalty and the ability to attract a more diverse clientele. At the end of June 2010, we took delivery of our largest cruise ship, Norwegian Epic (4,100 Berths), which represents the next evolution of “Freestyle Cruising,” offering 21 dining options and what we believe to be the widest array of entertainment options at sea. As of June 30, 2011, we have the youngest fleet of cruise ships in the industry among the Major North American Cruise Brands, with a weighted-average age of 6.6 years.

As a result of our positive operating performance over the last three years, the successful launch of Norwegian Epic, the growing demand we see for our distinctive cruise offering, and the rational supply outlook for the industry, we believe that it is an optimal time for the Company to add two new ships to our fleet, in order to continue to grow the Norwegian brand and drive shareholder value. In September 2010, we reached an agreement with Meyer Werft GmbH of Germany to build two new cruise ships for delivery in the second quarter of 2013 and 2014, respectively. Building on the success of Norwegian Epic, we have designed these two new next-generation “Freestyle Cruising” ships to include some of the most popular elements of our recently delivered ships together with new and differentiated features. We have entered into financing arrangements for approximately 90% of the contract price of the two ships. Each ship will approximate 143,500 Gross Tons and 4,000 Berths with an aggregate contract price of the two ships of approximately €1.2 billion, or $1.7 billion based on the euro/U.S. dollar exchange rate as of June 30, 2011. This is approximately €155,000 per Berth, or $225,000 per Berth based on the euro/U.S. dollar exchange rate as of June 30, 2011.

For the twelve months ended June 30, 2011, we generated total revenue of $2,181.8 million, Net Revenue of $1,611.5 million, net income of $72.2 million and Adjusted EBITDA of $454.9 million and an Adjusted EBITDA margin of 20.8%. For the six months ended June 30, 2011, we generated total revenue of $1,064.1 million, Net Revenue of $786.0 million, net income of $18.6 million, Adjusted EBITDA of $205.4 million and an Adjusted EBITDA margin of 19.3%. For the six months ended June 30, 2010, we generated total revenue of $894.4 million, Net Revenue of $653.8 million, net loss of $31.1 million, Adjusted EBITDA of $155.3 million and an Adjusted EBITDA margin of 17.4%. This represents an increase of 190 basis points in period over period Adjusted EBITDA margin as a result of improved ticket pricing and onboard spending coupled with various business improvement, product enhancement and cost reduction initiatives. We refer you to note 6 to our “Summary Consolidated Financial Data” included elsewhere in this prospectus for a reconciliation of Adjusted EBITDA to net income (loss).

Our Industry

We believe that the cruise industry demonstrates the following positive fundamentals:

Strong Growth with Low Penetration and Significant Upside

Cruising is a vacation alternative with broad appeal, as it offers a wide range of products and services to suit the preferences of vacationing customers of all ages, backgrounds and interests. Since 1980, cruising has been one of the fastest growing segments of the North American vacation market. According to CLIA, in 2010 approximately 15 million passengers took cruises of two consecutive nights or more on CLIA member lines versus 7.2 million passengers in 2000, representing a compound annual growth rate of approximately 8%. Based on CLIA’s research, we believe that cruising is under-penetrated and represents approximately 10% of the North American vacation market. As measured in Berths or room count, the cruise industry is relatively nascent as compared to the wide variety of much more established vacation travel destinations across North America.

According to the Orlando/Orange County Convention & Visitors Bureau and the Las Vegas Convention and Visitors Authority, there are approximately 264,000 rooms in just Orlando and Las Vegas combined. By

2

Table of Contents

comparison, the estimated Major North American Cruise Brands’ capacity in terms of Berths is approximately 224,000. In addition, according to industry research, only 24% of the U.S. population has ever taken a cruise and we believe this percentage should increase. The European vacation market, the fastest growing market globally, remains under-penetrated by the cruise industry, with approximately 1% of Europeans having taken a cruise in a given year, compared with 3% of the population in the U.S. and Canada.

We believe that improving leisure travel trends along with a relatively low supply outlook in the near term from the Major North American Cruise Brands lead to an attractive business environment for our Company to operate in.

Attractive Demographic Trends to Drive Cruising Growth

The cruise market is comprised of a broad spectrum of customers and appeals to virtually all demographic categories. Based on CLIA’s 2011 study, the target North American cruise market, defined as households with income of $40,000 or more headed by a person who is at least 25 years old, is estimated to be 132.9 million people. Also according to the study, the average cruise customer is 50 years old with a household income of $109,000, with 69% of all cruise customers falling between the ages of 40 to 74. We believe this represents a very attractive segment of the population as the Brookings Institution recently reported that over the past decade the 55 to 64 age group was the fastest growing age group in the U.S. It is our belief that “Freestyle Cruising” will help us attract customers not only in the lucrative older population segment of North America, but also with younger generations, as well as Europeans, who we believe are more likely to enjoy greater levels of freedom during their cruise through the “Freestyle Cruising” product offering than was traditionally offered within the cruise industry.

Significant Value Proposition and High Level of Guest Satisfaction

We believe that the cost of a cruise vacation, relative to a comparable land-based resort or hotel vacation in Orlando or Las Vegas, offers an exceptional value proposition. When one considers that a typical cruise, for one all-inclusive price, offers its guests transportation to a variety of destinations, hotel-style accommodations, a generous diversity of food choices and a selection of daily entertainment options, this is compelling support for the cruise value proposition relative to other leisure alternatives. Cruises have become even more affordable for a greater number of North American customers over the past few years through the introduction of “Homeland Cruising”, which eliminates the cost of airfare commonly associated with a vacation.

According to CLIA’s 2011 study, approximately 70% of persons who have taken a cruise rate cruising as a high-value vacation alternative. In this same survey, CLIA reported that approximately 80% of cruise passengers agree that a cruise vacation is a good way to sample various destinations which they may visit again on a land-based vacation.

High Barriers to Entry

The cruise industry is characterized by high barriers to entry, including the existence of several established and recognizable brands, the large expense of building a new, sophisticated cruise ship, the long lead time necessary to construct new ships and limited newbuild shipyard capacity. Based on new ships announced over the past several years, the cost to build a cruise ship can range from approximately $500 million to $1.4 billion or approximately $200,000 to $425,000 per Berth, depending on the ship’s size and quality of product offering. The construction time of a newbuild ship is typically between 27 months to 36 months and requires significant upfront cash payments to fund construction costs before a dollar of revenue is generated. In addition, the shipbuilding industry is experiencing tightened capacity as the size of ships increases and the industry consolidates, with virtually all new capacity added in the last 20 years having been built by one of three major European shipbuilders.

3

Table of Contents

Segments and Brands

The different cruise lines that make up the global cruise vacation industry have historically been segmented by product offering and service quality into contemporary, premium and luxury brands. The contemporary segment generally includes cruises on larger ships that last seven days or less, provides a casual ambiance and is less expensive on average than the premium or luxury segments. The premium segment is generally characterized by cruises that last from seven to 14 nights with a higher quality product offering than the contemporary segment, appealing to a more affluent demographic. The luxury segment generally offers the highest level of service and quality, with longer cruises on the smallest ships. In classifying our competitors within the Major North American Cruise Brands, the contemporary segment has historically included Carnival Cruise Lines and Royal Caribbean International. The premium segment has historically included Celebrity Cruises, Holland America and Princess Cruises. By providing a diverse set of itineraries and a “Freestyle Cruising” experience, we believe that we straddle both the contemporary and premium segments as well as offer a unique combination of value and leisure services to cruise customers. Based on fleet counts as of December 31, 2010, the Major North American Cruise Brands together represent approximately 90% of the North American cruise market as measured by total Berths.

Our Competitive Strengths

We believe that the following business strengths will enable us to execute our strategy:

Leading Cruise Operator with High-Quality Product Offering

We believe that our modern fleet provides us with operational and strategic advantages as our entire fleet has been purpose-built for “Freestyle Cruising” with a wider range of passenger amenities relative to many of our competitors.

We believe that in recent years the distinction has been blurred between segments of the market historically known as “premium” and “contemporary,” with the Major North American Cruise Brands each offering a wide range of onboard experiences across their respective fleets. With the completion of our fleet renewal initiative, we believe that based on a number of different metrics that directly impact a passenger’s onboard experience, we compare favorably against the other Major North American Cruise Brands, with product attributes more in line with the premium segment.

| • | Youngest Fleet. With a weighted-average age of 6.6 years (as of June 30, 2011) and no ships built before 1998, we have the youngest fleet among the Major North American Cruise Brands, which we believe allows us to offer a high-quality passenger experience with a significant level of consistency across our entire fleet. As a result of our younger fleet, we have a substantially higher percentage of outside balcony cabins across our fleet than the other contemporary brands, which helps drive higher Net Yields. |

| • | Rich Cabin Mix. As of June 30, 2011, 48% of our cabins had private balconies representing a higher mix of outside balcony cabins than the other contemporary brands. In addition, five of our ships offer a complex of private courtyard villas of up to approximately 570 square feet each. Customers staying in these villas are provided with personal butler service and exclusive access to a private courtyard area with private pools, sundeck, hot tubs, and fitness center. Six of our ships also offer luxury garden villas of up to 6,694 square feet, making them the largest accommodations at sea. |

| • | High-Quality Service. We believe we offer a very high level of onboard service, as demonstrated by our guest-to-crew ratio of 2.2 to 1, which is among the best of all the Major North American Cruise Brands. |

4

Table of Contents

| • | Diverse Selection of Premium Itineraries. For the year ended December 31, 2010, approximately 54% of our itineraries, by Capacity Days, were in more exotic, under-penetrated and less traditional locations, including Alaska, Hawaii, Bermuda and Europe, compared to the other contemporary brands which are focused primarily on itineraries in the Caribbean and Mexico. This mix of destinations is more consistent with the brands in the premium segment, and these itineraries typically attract higher Net Yields than Caribbean and Mexico sailings. |

We believe that this high-quality product offering positions us well in comparison to the other Major North American Cruise Brands and provides an opportunity for continued Net Yield growth.

“Freestyle Cruising”

The most important differentiator for our brand is the “Freestyle Cruising” concept onboard all eleven of our ships. The essence of “Freestyle Cruising” is to provide a cruise experience that offers more freedom and flexibility than any other traditional cruise alternative. While many cruise lines have historically required guests to dine at assigned group tables and at specified times, “Freestyle Cruising” offers the flexibility and choice to our passengers who prefer to dine when they want, with whomever they want and without having to dress formally. Additionally, we have increased the number of activities and dining facilities available onboard, allowing passengers to tailor their onboard experience to their own schedules, desires and tastes. The key elements of “Freestyle Cruising” include:

| • | flexible dining policy; no fixed dining times or pre-assigned seating in our dining rooms; |

| • | up to 21 dining options; in addition to multiple main dining rooms, a casual action station buffet and quick service outdoor grill, our ships offer a wide variety of specialty restaurants, with most offering a classic steakhouse, fine French, Japanese teppanyaki, sushi, Italian, Mexican and Asian fusion restaurants, which we believe is the widest selection of full-service dining options among the fleets of the Major North American Cruise Brands; |

| • | resort-casual dress code acceptable throughout the ship at all times; |

| • | increased service staff for a more personalized vacation experience; |

| • | replacement of cash tipping with an automated service charge system; |

| • | diverse “lifestyle” activities, including cultural and educational onboard programs along with an increased adventure emphasis for shore excursions; and |

| • | passenger-friendly disembarkation policies. |

All of our ships have been custom designed and purpose-built for “Freestyle Cruising,” which we believe differentiates us significantly from our major competitors. We further believe that “Freestyle Cruising” attracts a passenger base that prefers the less structured, resort-style experience of our cruises. Building on the success of “Freestyle Cruising,” we implemented across our fleet “Freestyle 2.0” featuring significant enhancements to our onboard product offering. These enhancements include a major investment in the total dining experience; upgrading the stateroom experience across the ship; new wide-ranging onboard activities for all ages; and additional recognition, services and amenities for premium-priced balcony, suite and villa passengers. With Norwegian Epic we have enhanced “Freestyle Cruising” by offering what we believe to be unmatched flexibility in entertainment, offering guests a wide variety of activities and performances to choose from at any time of day or night.

5

Table of Contents

Established Brand Recognition

The Norwegian Cruise Line brand is well established in the cruise industry with a long track record of delivering a world class cruise product offering to its customers. We achieve high-quality feedback scores from our customers in the areas of overall service, physical ship attributes, onboard products and services, food and beverage offerings and overall entertainment and land-based excursion quality. Based on recent guest experience and loyalty reports, the quality of our guests’ experience generates high levels of customer loyalty, as demonstrated by the fact that approximately 30% of our customers are repeat customers and approximately 70% say they would recommend Norwegian Cruise Line to their friends and family. Brand recognition is also strong with over 93% of cruisers reporting familiarity with Norwegian. Additionally, our brand is known for freedom, flexibility and choice, all highly valued benefits within the cruise industry demographic.

Strong Cash Flow

Nearly all of our capital expenditures, other than those related to our newbuild projects (which are substantially financed) and the current renovation of our private island, relate to the maintenance of our young and modern fleet and shoreside operations, which includes investments in our IT infrastructure and business intelligence systems. Our newbuild projects include very attractive financing which will fund approximately 90% of the required pre-delivery and delivery date construction payments; as such, we expect the cost of our newbuild projects to have a minimal impact on our cash flow in the near term.

We are able to generate significant levels of cash flow due to our ability to pre-sell tickets and receive customer deposits with long lead times ahead of sailing. Our debt financing is relatively low cost, with a weighted-average interest rate cost of 6.05% as of June 30, 2011. In addition, we believe that the favorable U.S. federal income tax regime applicable to international shipping income will enhance our cash flow from operations that can be utilized to significantly de-lever our balance sheet over time.

Highly Experienced Management Team

Our senior management team is comprised of experienced executives with an average of 14.8 years in the cruise, travel, leisure and hospitality-related industries. Since the Apollo Funds’ and the TPG Viking Funds’ investment in January 2008, 28 of the top 37 members of our senior management team (including 12 of the top 14) have been newly recruited or promoted to their current position under the leadership of our President and Chief Executive Officer, Kevin M. Sheehan. Their combined experience in related hospitality industries coupled with their financial expertise is a significant contributor to improving the operating and financial performance of our Company.

Strong and Experienced Shareholders

Our shareholders or their affiliates have extensive experience investing in the cruise, leisure and travel-related industries. Affiliates of the Apollo Funds have invested significant equity and resources to the cruise and leisure industry with its investment in Prestige Cruise Holdings, Inc. which operates through two distinct upscale cruise brands, Oceania Cruises and Regent Seven Seas Cruises. In addition, affiliates of both Apollo and TPG Capital own Caesars Entertainment Corporation (“Caesars Entertainment”), with whom we have created a marketing alliance. Affiliates of TPG Capital are also significant investors in Sabre Holdings, a leading GDS (global distribution system) and parent of Travelocity.com. Genting HK, headquartered in Hong Kong, operates a leading Asian cruise line with destinations in Malaysia, Singapore, Hong Kong, Taiwan and Japan.

6

Table of Contents

Our Business Strategies

We seek to attract vacationers by offering new products and services and creating differentiated itineraries in new markets through new and existing modern ships with the aim of delivering a better, value-added, vacation experience to our customers relative to other broad-based or land-based leisure alternatives.

Attractive Product Offerings

We have a long history of product development within the cruise industry as one of the most established consumer brands. We became the first cruise operator to buy a private island in the Bahamas to offer a private beach experience to our passengers; and we were the first to introduce a 2,000-Berth megaship into the Caribbean market in 1980. More recently, we pioneered new concepts in cruising over the last decade with the development of “Homeland Cruising” and the launch of “Freestyle Cruising.”

We continue to enhance our product offerings with the delivery of Norwegian Epic in June 2010, which offers 21 dining options, a diverse range of accommodations and what we believe is the widest array of entertainment at sea. In addition to several differentiated full-service complimentary dining rooms, Norwegian Epic also features specialty restaurants including a classic steakhouse, sushi, Japanese teppanyaki, Brazilian churrascaria, Asian noodle bar, traditional Chinese, fine French and Italian restaurants. Guest accommodations on Norwegian Epic include the groundbreaking Studios, 128 cabins designed for solo travelers centered around the Studio Lounge, a private two-story lounge for studio guests. On its top decks, Norwegian Epic offers a “ship within a ship” in the largest suite complex at sea; the exclusive Villas compound includes two decks with 52 villas and penthouses, a private pool with multiple hot tubs and sundecks, a private fitness center and steam rooms, fine dining in the Epic Club restaurant, casual outdoor dining at the Courtyard Grill, and 24-hour concierge service, all exclusively for villa and penthouse guests. Entertainment onboard Norwegian Epic includes a wide variety of branded entertainment for guests to choose from, including exclusive engagements with Blue Man Group, Cirque Dreams & Dinner, Legends in Concert, Nickelodeon and the improvisational comedy troupe, The Second City.

Building on the success of Norwegian Epic, we are drawing on our legacy of new product development to create two new next-generation “Freestyle Cruising” ships, scheduled for delivery in the second quarter of 2013 and 2014, respectively. These 4,000 Berth ships will include many of the most popular elements of Norwegian Epic and the rest of our fleet together with new groundbreaking features, while keeping the consistent innovative spirit of “Freestyle Cruising” in the core of the design.

In 2009, we initiated a $25 million renovation to our private island, Great Stirrup Cay, which includes a new dining and bar facility to enhance the guest experience, as well as offering new activities such as wave runners, an aqua park and a stingray encounter experience. The enhancements are scheduled to be completed in phases through the end of 2011 and are expected to provide us with additional revenue generating opportunities on the island.

Maximize Net Yields

We are focused on growing our revenue through various initiatives aimed at increasing our ticket prices and occupancy as well as onboard spending to drive higher overall Net Yields. To maximize passenger ticket revenue, our revenue management strategy is focused on optimizing pricing and generating demand throughout the booking curve. We base-load our capacity by booking passengers as early before sailing as possible.

Base-loading is a strategy by which we focus on selling inventory further from the cruise departure date by targeting sales and marketing tactics, such as full ship Charters and corporate meetings which generate business with longer booking windows. Our base-loading strategy also includes strategic relationships with travel agencies and international tour operators, who commit to purchasing a certain level of inventory with long lead times.

7

Table of Contents

Through base-loading, we believe we will increase our Net Yields by filling our ships earlier, rather than discounting close to sailing dates in order to achieve our targeted Load Factors. Our specific initiatives to achieve this include:

| • | Casino Player Strategy. As part of this strategy, we have non-exclusive arrangements with approximately 90 casino partners worldwide including Caesars Entertainment, which is owned by affiliates of both Apollo and TPG Capital, whereby loyal gaming customers are offered cruise reward certificates redeemable for cruises on our ships. Through property sponsored events and joint marketing programs, we have the opportunity to market cruises to Caesars Entertainment’s customers. These arrangements with our casino partners have the dual benefit of filling open inventory and reaching customers expected to generate above average onboard revenue through the casino and other onboard spending. |

| • | Strategic Relationships. Our base-loading strategy also includes strategic relationships with travel agencies and international tour operators, who commit to purchasing a certain level of inventory with long lead times. |

| • | Charter, Meeting & Incentive (“CM&I”) Sales. We are increasing our focus on driving additional business through the CM&I channel, which typically books very far in advance and can represent a significant portion of the ship, or even an entire sailing, in one transaction. |

| • | PROS Yield Management System. In late 2009, we implemented the PROS yield management system which allows us to better analyze and maximize our overall pricing decisions. |

We continue to focus on various initiatives to drive increased onboard revenue across a variety of areas. From the year ended December 31, 2007 to the twelve months ended June 30, 2011, our net onboard and other revenue yield increased by approximately 25% from $42.86 to $53.49 primarily due to strong performance in casino, beverage sales, specialty dining and shore excursions. Our strategy for further driving increased onboard revenue includes, among other things, generating additional casino revenue through our arrangements with our casino partners, including Caesars Entertainment and Genting HK. These arrangements incorporate marketing resources to deliver cross-company advertising and marketing campaigns to promote our brand. We also focus on optimizing the utilization of our specialty restaurants that carry a cover charge, pre-booking and pre-selling additional onboard activities and encouraging our staff to offer our passengers additional revenue generating products and services. In addition, the delivery of Norwegian Epic has created additional onboard revenue opportunities through ticket sales and merchandising, based on our unique and premium entertainment offerings.

Brand Expansion Through Disciplined Newbuild Program

In September 2010, we reached an agreement with Meyer Werft GmbH of Papenburg, Germany to build two new cruise ships with financing commitments in place from a syndicate of banks for export credit financing. The new ships are scheduled for delivery in the second quarter of 2013 and 2014, respectively. Building on the success of Norwegian Epic, we have designed these two new next-generation “Freestyle Cruising” ships to include some of the most popular elements of our most recently delivered ships together with new and differentiated features, consistent with Norwegian Cruise Line’s legacy of new product development in the cruise industry. We believe that these ships will allow us to continue to expand the reach of our brand while driving shareholder value. Our financing arrangements provide for financing for approximately 90% of the contract price of the two ships. Each ship will approximate 143,500 Gross Tons and 4,000 Berths with an aggregate contract price of approximately €1.2 billion, or $1.7 billion based on the euro/U.S. dollar exchange rate as of June 30, 2011. This is approximately €155,000 per Berth, or $225,000 per Berth based on the euro/U.S. dollar exchange rate as of June 30, 2011, which we believe compares favorably against other recent newbuild ship orders in the industry.

8

Table of Contents

Improve Operating Efficiency and Lower Costs

We are continually focused on driving financial improvement through a variety of cost savings initiatives. These initiatives are focused on reducing costs while at the same time improving the overall product we deliver to our customers. Since the beginning of 2008, we have significantly reduced our operating cost base through various programs including contract renegotiations, overhead rationalization, and fuel consumption reduction initiatives. We also typically hedge a majority of our near term fuel consumption in order to provide greater visibility of our fuel expense; as of June 30, 2011, we had hedged approximately 61% of our remaining 2011 projected fuel consumption. We have also reduced our maintenance expense as a result of our fleet renewal program, as younger, more modern ships are typically less costly to maintain than older ships. Beginning in early 2008, we reduced our capacity in the Hawaii market, re-flagging and relocating two of three ships, which significantly reduced crew payroll expenses aboard those ships creating substantial margin expansion. In addition, we expect the economies of scale from our two newbuild ships to drive further operating efficiencies over the long term.

Expand and Strengthen Our Product Distribution Channels

As part of our growth strategy, we are continually looking for ways to deepen and expand our customer sales channels. We restructured our sales and marketing organization, which included the hiring of two Senior Vice Presidents and five Vice Presidents, to provide better focus on distribution through four primary channels: retail/travel agent, direct, international, and CM&I.

| • | Retail/Travel Agent. We have implemented close to 100 individual projects specifically designed to improve our efficiency with the travel agency channels and our guests, ranging from more timely commission payments to aggressive call center quality monitoring. We also restructured our travel agent sales force, allowing us to more effectively support the larger accounts, which represent approximately 50% of our customers, with specific expertise and also gain access to a significantly larger number of travel partners through an outbound call center based in our Miami headquarters. We believe that our travel agent partners have witnessed a material improvement in our business practices and overall communication since the arrival of our new management team. |

| • | Direct. We continue to grow our direct business through investments in our brand and our website as well as increasing our direct sales force. Passengers booking directly with us tend to book earlier and in premium category inventory which provides higher Net Yields. |

| • | International. We have an international sales presence, with over 145 people in Europe and representatives covering Latin America, Australia and Asia. We are primarily focused on increasing our business in the European market, which has grown significantly in recent years but remains under-penetrated. In Europe, we now offer local itineraries year-round and our “Freestyle Cruising” has been well received. We are in the process of expanding our direct sales force in Europe which will allow us to develop our direct distribution in Europe in a manner similar to our U.S. operation. In support of this European strategy, we deployed our newest and most sophisticated ship, Norwegian Epic, in Europe for an extended summer season which began in May 2011. We are forging a closer distribution partnership with Genting HK, to develop product distribution across the Asia Pacific region. |

| • | CM&I. Our CM&I business focuses on full ship Charters as well as corporate meeting and incentive travel. These sales often have very long lead times and generate a higher level of Net Yield than sales through our other channels. |

Across every distribution channel we are undertaking a major effort to grow demand with a targeted sales and marketing program for our premium stateroom categories, including our balcony and other premium stateroom categories, with a particular emphasis on our suites and villa complexes, which have increased as a percentage of our total inventory as a result of our fleet renewal.

9

Table of Contents

Our Fleet

Our ships are purpose-built ships that enable us to provide our customers with the ultimate “Freestyle Cruising” experience. Our ships have state-of-the-art passenger amenities, including up to 21 dining options together with hundreds of private balcony cabins on each ship. As of June 30, 2011, 48% of our cabins have private balconies representing a higher mix of outside cabins than the other contemporary brands. Private balcony cabins are very popular with passengers and offer the opportunity for increased revenue by allowing us to charge a premium. Five of our ships offer a complex of private courtyard villas, each with up to approximately 570 square feet, which provide personal butler service and exclusive access to a private courtyard area with private pools, sundeck, hot tubs, and fitness center. In addition, six of our ships have luxury garden villas with up to 6,694 square feet, making them the largest accommodations at sea. These luxury garden villas offer three separate bedroom areas, spacious living and dining room areas, as well as 24-hour, on-call butler and concierge service.

Continuing our tradition of new product development and the extension of the Norwegian Cruise Line brand, we took delivery of Norwegian Epic in June 2010. Norwegian Epic offers our passengers itineraries to the western and eastern Caribbean as well as Europe. The ship offers our customers a large aqua park, sports complex, two three-lane bowling alleys and our two-story Wii™ Wall. In addition, the ship features a spa facility and fitness center with more than 31,000 square feet. There are 21 dining options on Norwegian Epic offering one of the widest choices of dining experiences among the fleets of the Major North American Cruise Brands. Exclusive entertainment is offered aboard Norwegian Epic with the addition of brand new entertainment choices including Blue Man Group, Cirque Dreams & Dinner, Legends in Concert and Nickelodeon at Sea. We offer world-class entertainment in our jazz and blues club and our comedy club features the improvisational comedy troupe, The Second City. Norwegian Epic has been very well received by the market with the strongest bookings we have ever seen for a new ship, both in terms of price and volume. This positive reception has also benefited the rest of our fleet, which experienced significant bookings due to the uplift that Norwegian Epic has created for our brand overall. We believe the premium cabin mix of Norwegian Epic will drive further increases in Net Yield.

As further described in “—Our Business Strategies—Brand Expansion Through Disciplined Newbuild Program,” building on the successful launch of Norwegian Epic, we recently announced two new ships with approximately 4,000 Berths each, scheduled for delivery in the second quarter of 2013 and 2014, respectively.

Our Shareholders

Apollo

Apollo is a leading global alternative asset manager with offices in New York, Los Angeles, London, Frankfurt, Luxembourg, Singapore, Hong Kong and Mumbai. As of December 31, 2010, Apollo had assets under management of $67.6 billion invested in its private equity, capital markets and real estate businesses. Apollo owns a controlling interest in Prestige Cruises International, Inc. which operates through two distinct upscale cruise brands, Oceania Cruises and Regent Seven Seas Cruises. Apollo also has current investments in other travel and leisure companies, including Caesars Entertainment and AMC Entertainment and has in the past invested in Vail Resorts and Wyndham International and other hotel properties.

TPG Capital

TPG Capital is a leading private investment firm with $48 billion of assets under management as of June 30, 2011. TPG Capital has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, joint ventures and restructurings. TPG Capital seeks to invest in world-class franchises across a range of industries. Current investments include Caesars Entertainment,

10

Table of Contents

Neiman Marcus, Sabre, Energy Future Holdings (formerly TXU) and Univision. Past investments include Alltel, Burger King, Continental Airlines, Fairmont Raffles, Hotwire, Seagate and Texas Genco.

Genting HK

Genting HK was founded in 1993 and operates a leading cruise line in the Asia-Pacific region. Its headquarters are located in Hong Kong and it is represented in more than 20 locations worldwide, with offices and representatives in Asia, Australia, Europe, United Arab Emirates and the U.S. Genting HK currently has a fleet of seven ships, which offer various cruise itineraries in the Asia Pacific region.

Corporate Reorganization

In connection with the consummation of this offering, the Issuer will become the 100% owner and parent company of NCL Corporation Ltd. (the “Corporate Reorganization”). The Corporate Reorganization will be effected solely for the purpose of reorganizing our corporate structure as described herein. The Issuer will not, prior to the completion of the Corporate Reorganization, conduct any activities other than those incidental to its formation and to preparations for the Corporate Reorganization and this offering. The Issuer has only nominal assets and no liabilities prior to the consummation of the Corporate Reorganization and this offering. Upon closing, its only assets will be 100% of the ordinary shares of NCL Corporation Ltd. and cash proceeds of this offering not otherwise used or contributed to NCL Corporation Ltd. Also, as part of the Corporate Reorganization, (i) NCL Corporation Ltd.’s outstanding ordinary shares will be exchanged for our ordinary shares and (ii) we will issue an economically equivalent number of our ordinary shares, at an exchange formula based on the initial public offering price in this offering, in exchange for NCL Corporation Ltd.’s outstanding profits interests granted under the Profits Sharing Agreement, including the Ordinary Profits Units described below in “Compensation Discussion & Analysis.” Our executive officers and directors will be the same as the executive officers and directors of NCL Corporation Ltd. in effect immediately prior to the Corporate Reorganization, except that certain of our shareholders have a contractual right under the Shareholders’ Agreement to appoint two additional members, in the aggregate, to our board of directors (our “Board of Directors”) and we anticipate that they will do so prior to the consummation of this offering, thereby increasing the size of our Board of Directors to nine members. See “Certain Relationships and Related Party Transactions—The Shareholders’ Agreement.” Upon consummation of the Corporate Reorganization, our memorandum of association and bye-laws, and the rights, privileges and interests of our shareholders that will be in effect as of the consummation of this offering, will be as described in “Description of Share Capital.” See also “Management,” “Security Ownership of Certain Beneficial Owners and Management,” and “Certain Relationships and Related Party Transactions—The Shareholders’ Agreement.”

Additional Information

We are incorporated under the laws of Bermuda. Our registered offices are located at Cumberland House, 9th Floor, 1 Victoria Street, Hamilton HM 11, Bermuda. Our principal executive offices are located at 7665 Corporate Center Drive, Miami, Florida 33126. Our telephone number is (305) 436-4000. Our website is www.ncl.com. The information that appears on our website is not part of, and is not incorporated by reference into, this prospectus.

11

Table of Contents

The Offering

| Issuer |

Norwegian Cruise Line Holdings Ltd. which, upon the consummation of this offering, will own 100% of the ordinary shares of NCL Corporation Ltd. |

| Ordinary shares offered by us |

| Ordinary shares to be outstanding after this offering |

(assuming no exercise of the underwriters’ option to purchase additional ordinary shares) based upon an assumed initial public offering price of $ per ordinary share, which is the midpoint of the estimated price range set forth on the cover of this prospectus. In connection with the Corporate Reorganization and prior to the consummation of this offering, we will issue an economically equivalent number of our ordinary shares, based on the initial public offering price in this offering, in exchange for all outstanding NCL Corporation Ltd. profits interests granted under the Profits Sharing Agreement, including the Ordinary Profits Units (each as described in “Compensation Discussion & Analysis”). |

| There will be ordinary shares available for future awards under our new long-term incentive plan as of the consummation of this offering. |

| A $1.00 increase or decrease in the assumed offering price of $ per ordinary share, which is the midpoint of the initial public offering price range set forth on the cover of this prospectus, would increase or decrease the number of ordinary shares to be outstanding after this offering by approximately shares as a result of an increase or decrease in the ordinary shares we will issue in exchange for the profits interests, assuming the number of ordinary shares offered by us, as set forth above and on the cover page of the prospectus, remains the same. |

| Underwriters’ option to purchase additional shares |

We have granted the underwriters an option for a period of 30 days to purchase from us an aggregate of up to additional ordinary shares. |

| Use of proceeds |

We estimate that we will receive net proceeds from the sale of our ordinary shares in this offering, after deducting the underwriting discount and other estimated expenses, of approximately $ million, assuming the ordinary shares are offered at $ per ordinary share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus. We intend to use the net proceeds that we receive to redeem or prepay outstanding debt and to pay expenses associated with this offering. A $1.00 increase or decrease in the assumed offering price of $ |

12

Table of Contents

| per ordinary share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, would increase or decrease the net proceeds we receive from this offering by approximately $ million, assuming the number of ordinary shares offered by us, as set forth above and on the cover of this prospectus, remains the same and after deducting the underwriting discounts and other estimated expenses. |

| Listing |

We expect to apply for listing of our ordinary shares on the NASDAQ Global Select Market under the symbol “NCLH”. |

| Dividend policy |

We do not intend to pay dividends following this offering. Our debt agreements, among other things, restrict our ability to pay cash dividends to our shareholders. In addition, any determination to pay dividends in the future will be at the discretion of our Board of Directors and will depend upon our results of operations, financial condition, business opportunities, contractual restrictions, restrictions imposed by applicable law and other factors that our Board of Directors deems relevant. See “Dividend Policy.” |

| Voting rights |

Each of our ordinary shares will entitle its holder to one vote on all matters to be voted on by shareholders generally. Our public shareholders will have approximately % of the voting power of the Issuer (or approximately % if the underwriters exercise in full their option to purchase additional ordinary shares) and Genting HK, the Apollo Funds and the TPG Viking Funds, who will be contractually bound by the terms of the Shareholders’ Agreement (as defined elsewhere in this prospectus) with respect to the exercise of their voting rights in certain matters, will have approximately % of the voting power of the Issuer (or approximately % if the underwriters exercise in full their option to purchase additional ordinary shares). See “Description of Share Capital—Ordinary Shares—Transfer Restrictions.” |

| Risk factors |

You should carefully read and consider the information set forth under “Risk Factors” beginning on page 18 of this prospectus and all other information set forth in this prospectus before investing in our ordinary shares. |

| Tax considerations |

See “Material U.S. Federal Income Tax Considerations,” “Material Bermuda Tax Considerations” and “Business—Taxation of the Company” for more information regarding tax considerations. |

13

Table of Contents

Summary Consolidated Financial Data

The summary consolidated financial and operating data presented in the tables below should be read in conjunction with “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus. In the table below, the consolidated balance sheets as of December 31, 2010, 2009 and 2008 and the related consolidated statements of operations and of cash flows for each of the three years in the period ended December 31, 2010 have been derived from our financial statements included elsewhere in this prospectus, with the exception of the consolidated balance sheet as of December 31, 2008 and pro forma earnings (loss) per share as adjusted which are not included. In addition, the consolidated balance sheets as of June 30, 2011 and June 30, 2010 and the related consolidated statements of operations and of cash flows for each of the six month periods ended June 30, 2011 and 2010 and the notes thereto have been derived from our unaudited financial statements also appearing herein, with the exception of the consolidated balance sheet as of June 30, 2010 and pro forma earnings (loss) per share as adjusted which are not included. The data as of and for the six months ended, in the opinion of management, contain all normal recurring adjustments, necessary for a fair statement of the results for the unaudited interim periods. Our financial data (unaudited) is also presented for the twelve months ended June 30, 2011. Historical results are not necessarily indicative of results that may be expected for any future period.

| Twelve Months Ended June 30, |

Six Months Ended June 30, |

Year Ended December 31, | ||||||||||||||||||||||

| (in thousands, except per share data) | 2011 | 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||||||

| Revenue |

||||||||||||||||||||||||

| Passenger ticket |

$ | 1,510,134 | $ | 725,343 | $ | 607,715 | $ | 1,392,506 | $ | 1,275,844 | $ | 1,501,646 | ||||||||||||

| Onboard and other |

671,673 | 338,753 | 286,702 | 619,622 | 579,360 | 604,755 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenue |

2,181,807 | 1,064,096 | 894,417 | 2,012,128 | 1,855,204 | 2,106,401 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Cruise operating expense |

||||||||||||||||||||||||

| Commissions, transportation and other |

404,143 | 194,990 | 170,502 | 379,655 | 377,036 | 410,061 | ||||||||||||||||||

| Onboard and other |

166,144 | 83,087 | 70,080 | 153,137 | 158,330 | 182,817 | ||||||||||||||||||

| Payroll and related |

283,316 | 144,569 | 126,643 | 265,390 | 252,426 | 309,083 | ||||||||||||||||||

| Fuel |

230,913 | 120,610 | 96,907 | 207,210 | 162,683 | 258,262 | ||||||||||||||||||

| Food |

124,901 | 62,522 | 51,685 | 114,064 | 118,899 | 126,736 | ||||||||||||||||||

| Other |

249,469 | 121,368 | 99,741 | 227,842 | 220,080 | 291,522 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total cruise operating expense |

1,458,886 | 727,146 | 615,558 | 1,347,298 | 1,289,454 | 1,578,481 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other operating expense |

||||||||||||||||||||||||

| Marketing, general and administrative |

271,582 | 133,169 | 125,985 | 264,398 | 241,676 | 299,827 | ||||||||||||||||||

| Depreciation and amortization |

186,205 | 92,767 | 76,753 | 170,191 | 152,700 | 162,565 | ||||||||||||||||||

| Impairment loss(1) |

— | — | — | — | — | 128,775 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total other operating expense |

457,787 | 225,936 | 202,738 | 434,589 | 394,376 | 591,167 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

265,134 | 111,014 | 76,121 | 230,241 | 171,374 | (63,247 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Non-operating income (expense) |

||||||||||||||||||||||||

| Interest income |

59 | 24 | 65 | 100 | 836 | 2,796 | ||||||||||||||||||

| Interest expense, net of capitalized interest |

(195,461 | ) | (94,575 | ) | (72,886 | ) | (173,772 | ) | (115,350 | ) | (152,364 | ) | ||||||||||||

| Other income (expense)(2) |

2,508 | 2,088 | (34,372 | ) | (33,952 | ) | 10,373 | 1,012 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total non-operating income (expense) |

(192,894 | ) | (92,463 | ) | (107,193 | ) | (207,624 | ) | (104,141 | ) | (148,556 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) as reported |

$ | 72,240 | $ | 18,551 | $ | (31,072 | ) | $ | 22,617 | $ | 67,233 | $ | (211,803 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Pro forma net income (loss) as adjusted(a) |

$ | $ | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

14

Table of Contents

| Twelve Months Ended June 30, |

Six Months Ended June 30, |

Year Ended December 31, | ||||||||||||||||||||||

| (in thousands, except per share data) | 2011 | 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||||

| Earnings (loss) per share as reported |

||||||||||||||||||||||||

| Basic |

$ | $ | $ | $ | 1.07 | $ | 3.24 | $ | (10.59 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Diluted |

$ | $ | $ | $ | 1.06 | $ | 3.23 | $ | (10.59 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Pro forma earnings per share as adjusted(b)(c) |

||||||||||||||||||||||||

| Basic |

$ | $ | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Diluted |

$ | $ | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| (a) | Pro forma net income (loss) as adjusted reflects an interest expense adjustment of $ . This was derived by applying the applicable interest rates to the change in certain of our outstanding debt associated with the use of proceeds from this offering. See “Use of Proceeds.” |

The interest expense adjustment per facility is as follows:

| $450.0 million senior secured notes |

$ | |||

|

|

|

|||

| $250.0 million senior secured notes |

$ | |||

|

|

|

|||

| $750.0 million senior secured revolving credit facility |

$ | |||

|

|

|

There was no tax effect on the interest expense adjustment based on our current tax structure.