Attached files

| file | filename |

|---|---|

| EX-2.1 - EXHIBIT 2.1 - Q Therapeutics, Inc. | v237419_ex2-1.htm |

| EX-16.1 - EXHIBIT 16.1 - Q Therapeutics, Inc. | v237419_ex16-1.htm |

| EX-99.2 - EXHIBIT 99.2 - Q Therapeutics, Inc. | v237419_ex99-2.htm |

| EX-10.1 - EXHIBIT 10.1 - Q Therapeutics, Inc. | v237419_ex10-1.htm |

| EX-99.1 - EXHIBIT 99.1 - Q Therapeutics, Inc. | v237419_ex99-1.htm |

| EX-10.3 - EXHIBIT 10.3 - Q Therapeutics, Inc. | v237419_ex10-3.htm |

| EX-99.3 - EXHIBIT 99.3 - Q Therapeutics, Inc. | v237419_ex99-3.htm |

| EX-10.2 - EXHIBIT 10.2 - Q Therapeutics, Inc. | v237419_ex10-2.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of

The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 13, 2011

GRACE 2, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

000-52062

|

20-3708500

|

||

|

(State or other jurisdiction of incorporation)

|

(Commission File Number)

|

(IRS Employer Identification No.)

|

||

|

615 Arapeen Drive, Suite 102

Salt Lake City, UT

|

84108

|

|||

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code:

Phone: 801-582-5400; Fax: 801-582-5401

N/A

(Former name or former address, if changed since last report.)

With a copy to:

Joseph M. Patricola, Esq.

The Sourlis Law Firm

The Courts of Red Bank

130 Maple Avenue, Suite 9B2

Red Bank, New Jersey 07701

Direct Dial: (732) 618-2843

T: (732) 530-9007

F: (732) 530-9008

JoePatricola@SourlisLaw.com

www.SourlisLaw.com

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

|

¨

|

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

|

|

¨

|

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

|

|

¨

|

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

|

|

¨

|

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Current Report on Form 8-K contains forward-looking statements that involve risks and uncertainties, principally in the sections entitled “Description of Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” All statements other than statements of historical fact contained in this Current Report on Form 8-K, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should,” or “will” or the negative of these terms or other comparable terminology. Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks outlined under “Risk Factors” or elsewhere in this Current Report on Form 8-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements.

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations, and financial needs. These forward-looking statements are subject to certain risks and uncertainties that could cause our actual results to differ materially from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Current Report on Form 8-K, and in particular, the risks discussed below and under the heading “Risk Factors” and those discussed in other documents we file with the Securities and Exchange Commission that are incorporated into this Current Report on Form 8-K by reference. The following discussion should be read in conjunction with our consolidated financial statements and notes thereto included in this Report. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this Current Report on Form 8-K may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this Current Report on Form 8-K. Before you invest in our common stock, you should be aware that the occurrence of the events described in the section entitled “Risk Factors” and elsewhere in this Current Report on Form 8-K could negatively affect our business, operating results, financial condition and stock price. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this Current Report on Form 8-K to conform our statements to actual results or changed expectations.

2

ITEM 1.01. ENTRY INTO A MATERIAL DEFINITIVE AGREEMENT.

General

Grace 2, Inc. (hereinafter “Grace 2”, “Grace” or “the Company”), a corporation formed in the State of Delaware on October 27, 2005, which upon completion of the Company’s name change shall be known as Q Holdings, Inc. (throughout this Current Report on Form 8-K Grace 2 sometimes referred to as “Q Holdings” depending on context) is a holding company which, through its wholly owned subsidiary, Q Therapeutics, Inc., a corporation formed in the State of Delaware on March 28, 2002 (hereinafter “Q Therapeutics” or “Q”), is a biotechnology company headquartered in Salt Lake City, Utah. We believe that our company has taken a novel path to developing treatments for debilitating and sometimes fatal diseases of the central nervous system (“CNS”), utilizing and patenting ‘stem or progenitor cell’ therapeutics and their cellular progeny for the treatment of such devastating illnesses.

Merger Agreement

On October 13, 2011, Grace 2 entered into an Agreement and Plan of Merger (the “Agreement”) with Q Acquisition, Inc., a Delaware corporation and wholly owned subsidiary of the Company (“Merger Sub”), and Q Therapeutics. Pursuant to the Agreement, Merger Sub merged with and into Q Therapeutics with Q Therapeutics being the surviving corporation (the “Merger”). Upon the consummation of the Merger, the Company acquired 100% of Q Therapeutics. The Agreement is attached hereto as Exhibit 2.1 to this Current Report on Form 8-K.

As a result of the Merger:

|

|

·

|

Douglas Dyer, the sole director and officer of Grace 2, resigned.

|

|

|

·

|

Q Therapeutics shareholders received, on a pro rata basis, an aggregate of 22,671,923 shares of Grace 2 Common Stock (including shares underlying warrants and options), which immediately upon the consummation of the Merger, represented an 89.7% interest in the Company , thereby rendering Q Therapeutics shareholders the majority owners of the Company;

|

|

|

·

|

Grace 2 filed a Schedule 14C with the US Securities and Exchange Commission notifying the market of its immediate plans to change the Company’s corporate name to Q Holdings, Inc. by way of Amendment to the Company’s Certificate of Incorporation with the State of Delaware (Grace 2 thereafter referred to as “Q Holdings”);

|

|

|

·

|

Q Therapeutics’ existing senior management assumed the same positions with Q Holdings; and

|

|

|

·

|

Q Therapeutics became the wholly owned subsidiary of the Company with the Company conducting all of its operations through Q Therapeutics.

|

Securities Purchase Agreement

Immediately after the Merger, we entered into a securities purchase agreement (the “Purchase Agreement”) with certain accredited investors (the “Investors”) for the issuance and sale in a private placement of investment units (the “Units”), with each Unit consisting of (a) one share of the Company’s common stock, par value $0.0001 per share (the “Common Stock”), (b) a seven-year detachable warrant (“Warrant A”) to purchase one share of Common Stock with an exercise price of $1.00 per share, and (c) a seven-year detachable warrant (“Warrant B” and together with Warrant A, the “Warrants”) to purchase one share of Common Stock with an exercise price of $2.00 per share, for aggregate gross proceeds of $3,803,047 (the “Private Placement”). In the aggregate, we issued to the Investors a total of 3,803,047 shares of Common Stock and a seven-year Warrant A to purchase up to 3,803,047 shares of common stock and a seven-year Warrant B to purchase up to 3,803,047 shares of common stock.

3

Registration Rights Agreement

In connection with the Private Placement, we also entered into a registration rights agreement (the “Registration Rights Agreement”) with the Investors, pursuant to which the Company agreed to file a registration statement on Form S-1 (or any other applicable form exclusively for this offering) (the “Registration Statement”) with the Securities and Exchange Commission (the “SEC”) to register for resale (i) 100% of the shares of our common stock within the Units; and (ii) 100% of the shares of our common stock underlying the Warrants (collectively, the “Registrable Shares”), within 60 calendar days following the closing of the Private Placement, and use the Company’s best efforts to have the registration statement declared effective within 180 calendar days after closing of the Private Placement. If a Registration Statement covering the registration of the Registrable Shares is not filed with the SEC by the Required Filing Date or is not declared effective by the Required Effective Date, the Company shall pay to each Investor as liquidated damages, a cash payment equal to 3% of the aggregate amount invested by such Investor in the Private Placement for every 30-day period until the Registration Statement has been filed or declared effective, or a portion thereof. Such liquidated damages shall not exceed 18% per annum.

Series A Warrants

Each Series A Warrant:

|

(a)

|

entitles the holder or its registered assigns to purchase one share of common stock;

|

|

(b)

|

is exercisable any time after the Closing Date and expires on the date that is seven years following the original issuance date of the Warrants;

|

|

(c)

|

is exercisable, in whole or in part, at an exercise price of $1.00 per share (the “Exercise Price”);

|

|

(d)

|

is exercisable only for cash; and

|

|

(e)

|

is callable by us at a redemption price of $0.001 per warrant share by providing the holder ten day written notice (the “Redemption Period”); provided, however, that no redemption may occur unless (i) the Company’s Common Stock has had a per share closing sales price of at least $1.50 for ten consecutive trading days and (ii) at the date of the redemption notice and during the entire Redemption Period there is an effective registration statement covering the resale of the Warrant Stock.

|

Series B Warrants

Each Series B Warrant:

|

(a)

|

entitles the holder or its registered assigns to purchase one share of common stock;

|

4

|

(b)

|

is exercisable any time after the Closing Date and expires on the date that is seven years following the original issuance date of the Warrants;

|

|

(c)

|

is exercisable, in whole or in part, at an exercise price of $2.00 per share (the “Exercise Price”);

|

|

(d)

|

is exercisable only for cash; and

|

|

(e)

|

is callable by us at a redemption price of $0.001 per warrant share by providing the holder ten day written notice (the “Redemption Period”); provided, however, that no redemption may occur unless (i) the Company’s Common Stock has had a per share closing sales price of at least $3.00 for ten consecutive trading days and (ii) at the date of the redemption notice and during the entire Redemption Period there is an effective registration statement covering the resale of the Warrant Stock.

|

ITEM 2.01. COMPLETION OF ACQUISITION OR DISPOSITION OF ASSETS.

See “ITEM 1.01. ENTRY INTO A MATERIAL DEFINITIVE AGREEMENT.” above and incorporated by reference herein.

Description of Business

Company Overview

Q Holdings, Inc., through our wholly owned subsidiary Q Therapeutics, Inc. is a Salt Lake City, Utah based biopharmaceutical company that is developing human cell-based therapies intended to treat degenerative diseases of the brain and spinal cord, the primary components of the central nervous system (“CNS”). Q Therapeutics, Inc. was incorporated in the state of Delaware in March 2002.

The technology upon which these therapies are based was developed by Q Therapeutics’ co-founder Mahendra Rao, M.D., Ph.D., a global leader in glial stem cell biology, during Dr. Rao’s tenure as a Professor at the University of Utah and as Head of the Stem Cell Section at the National Institutes of Health. Q Therapeutics is managed by an experienced team of biotechnology executives with demonstrated start-up success and advised by leaders in the neurology and stem cell therapeutics fields.

Every year, hundreds of thousands of people suffer with debilitating neurodegenerative diseases such as Amyotrophic Lateral Sclerosis (ALS, or Lou Gehrig’s disease), Multiple Sclerosis, Transverse Myelitis and Spinal Cord Injuries. Traditional drugs tend to fail as long-term treatments of the damages to the CNS caused by these diseases due to the complex nature of these diseases and the nerve damage they inflict. Q Therapeutics is developing a new and nontraditional approach to improve the health of people suffering from neurodegenerative diseases: a human cell based product called Q-Cells®.

Q-Cells® are healthy human glial cells. The job of glial cells in the body is to support and protect neurons, which are the signal transmission lines of the nervous system, by forming an insulating “myelin sheath” around them and providing the necessary growth factors needed to maintain a healthy nervous system. Many neurodegenerative diseases arise when glial cells are damaged or destroyed, causing neurons to malfunction and eventually die. Q-Cells® technology aims to treat neurodegenerative diseases by supplementing the damaged or missing glia in the body with new, healthy cells that can help maintain and/or restore neuron function to a more robust state.

5

The diseases targeted by Q Therapeutics’ products are not well treated with current drug therapies. At best, patients suffering from these diseases can, in some cases, only hope to slow their inexorable progression and the associated disabilities. A handful of companies are exploring the possibility of harnessing the power of stem cells to treat these conditions, though no clear leader has emerged. In addition to utilizing its proprietary cellular products as therapeutic products, Q Therapeutics may evaluate novel ways to utilize these cells to screen for new drugs (small molecule compounds) that could also provide treatments for neurological diseases.

The Company believes that a worldwide market measured in the tens of billions of dollars exists for those companies whose cell-based treatments become commercial products. Q Therapeutics’ patent protected technology represents an opportunity to build on the recent advancements in the stem cell field and bring to market a therapeutic approach that will change the way medicine is practiced in treating many disabling and fatal conditions of the CNS.

Q Therapeutics is raising capital to complete preparations necessary to move into and initiate human clinical trials, initially treating patients that suffer from the always-fatal Amyotrophic Lateral Sclerosis (ALS, or Lou Gehrig’s Disease). Future trials are anticipated in other neurodegenerative diseases, such as Multiple Sclerosis and spinal cord injury.

Q Therapeutics’ Semi-Virtual Business Model

As described below, Q Therapeutics uses a semi-virtual business model to develop its products. Q believes this type of business model to be capital efficient while allowing it to augment its own expertise and capabilities with those of its development partners at the time that outside resources are needed. Q’s semi-virtual business model includes utilizing third parties for certain functions and outsourced services. For example, Q utilizes outside collaborators and contractors to:

|

|

·

|

Leverage its research and development resources by forming collaborations with outside scientists specialized in our areas of interest

|

|

|

·

|

Contract GLP and GMP manufacturing to facilities specialized in such production

|

|

|

·

|

Utilize experienced regulatory consultants to work with FDA

|

|

|

·

|

Contract safety/toxicology studies to qualified GLP labs

|

|

|

·

|

Conduct the clinical trials with physicians and institutions with relevant experience

|

|

|

·

|

Enter into pharmaceutical company collaborations to maximize product sales

|

Q Therapeutics – Taking a Cell-Based Therapeutic Approach to Treatment of Degenerative Conditions of the Central Nervous System

Q Therapeutics was founded in 2002 to further the development and commercialization of the pioneering work of Mahendra Rao, M.D., Ph.D., conducted at the University of Utah (Utah) and National Institutes of Health (NIH). Dr. Rao, a global leader in the development of stem cells as therapeutics, was one of the first to identify and seek patent coverage on stem cells and their progeny cells found in the CNS. After licensing Dr. Rao’s technology from Utah / NIH and raising capital, Q commenced operations in the spring of 2004 to develop cell based therapeutic products that can be sold as “off-the-shelf” pharmaceuticals. That work continues to advance Dr. Rao’s initial findings toward a commercial product.

6

Objectives of Company

Q Therapeutics aims to change the way medicine is practiced in the treatment of many debilitating and often fatal diseases of the brain and spinal cord. Q intends to bring its initial product, Q-Cells® to the market to treat Lou Gehrig’s disease, and eventually other indications, potentially including Multiple Sclerosis, spinal cord injury, Parkinson’s and Alzheimer’s diseases.

Initially, Q is targeting orphan diseases, where the Food and Drug Administration (FDA) allows applying for fast track approvals and market exclusivity, and for which smaller, less expensive clinical trials are often warranted. This approach can result in accelerated commercialization efforts while maintaining a financing approach focused on capital efficiency.

Q’s Approach to the Problem

Q Therapeutics believes it has taken a novel path to developing treatments for debilitating and sometimes fatal diseases of the CNS for which there are currently no long-term effective treatments. Traditional drugs have seen little success as long-term treatments for many neurodegenerative diseases, primarily due to the complex nature of those diseases and the difficulty of replacing damaged nerve cells, or neurons.

The majority of cells in the brain and spinal cord are glial cells that serve to support the health of the neurons. Without healthy and properly functioning glial cells, neurons cannot function properly and will eventually die. In many neurodegenerative diseases, damage to glial cells causes or accelerates loss of function and death of neurons. Q’s approach takes advantage of the normal support and repair mechanisms present in the healthy nervous system whereby supplementation of damaged glial cells with healthy glial cells in patients suffering from neurodegenerative diseases is intended to enable the return to healthy neuron function, thereby ameliorating the negative effects of the disease.

Q’s Initial Proprietary Product - Q-Cells®

Q is developing a new pharmaceutical product (Q-Cells®) intended to provide support to neurons in the patient’s CNS and ameliorate the deleterious effects of diseased cells. This product is comprised of healthy human glial cells that perform therapeutic tasks via multiple mechanisms:

(1) Serving as ‘mini-factories’ to produce the requisite growth factors and other nutrients as well as to remove toxic compounds, all needed for a healthy CNS; and

(2) Forming the insulating layer known as myelin around the axons of neurons, enabling their normal function for signal transmission.

Q-Cells® accomplish these complementary functions in a process that is unique to stem and progenitor cells. After Q-Cells® are injected into the CNS, they differentiate into the two mature glial cell subtypes found in the brain and spinal cord:

(1) Oligodendrocytes which provide the needed myelin insulation for proper signal transmission by the conducting neurons,

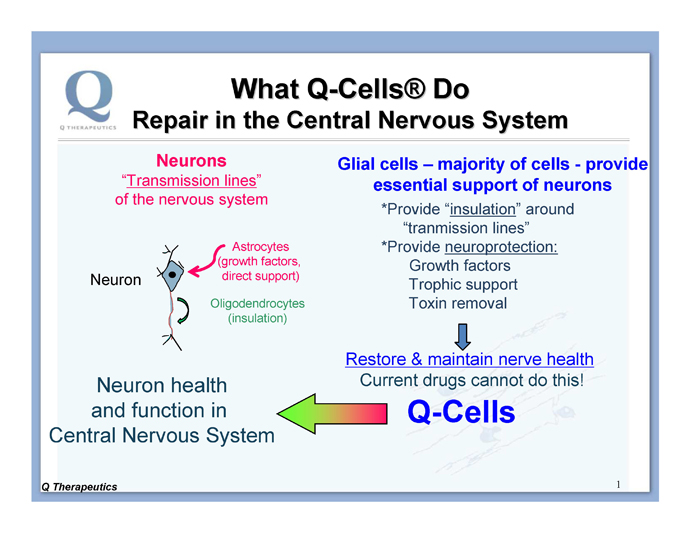

(2) Astrocytes, which provide support to neurons through production of growth factors and other trophic support mechanisms (Figure 1).

Q-Cells® technology aims to restore health and function to neurons prior to their death by using the natural support mechanisms in the CNS, rather than by replacing the neurons. No current drug can achieve this outcome.

7

Figure 1. The majority of the cells in the brain and spinal cord are glia cells that provide support function for the neurons. Q-Cells® provide support for neurons, which Q believes is a more straightforward task than replacing neurons.

The Science behind Q-Cells®

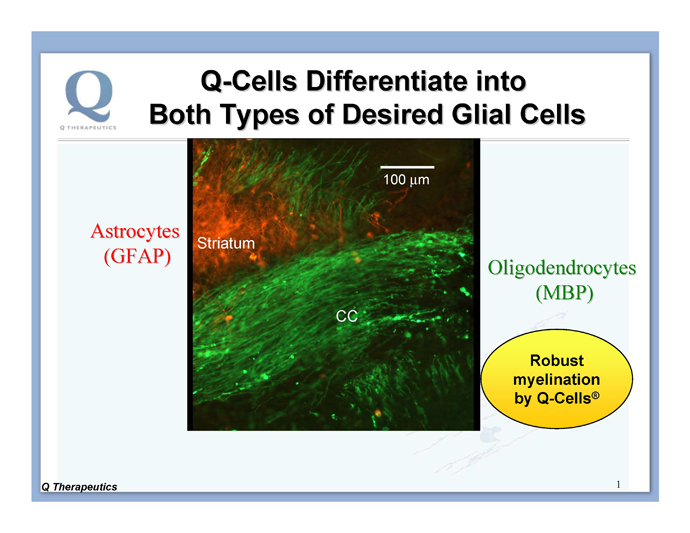

During normal development, glia are formed by a progenitor cell called the glial-restricted precursor (“GRP”). Human GRPs, together with their progeny, have been trademarked as Q-Cells®. Q-Cells® naturally do three things in the CNS: replicate, migrate and differentiate into mature glial cells. The resulting differentiated cells (astrocytes and oligodendrocytes, shown in Figure 2) then can perform the support functions of these glial cells in vivo as described above. The Company is taking advantage of Q-Cells®’ natural abilities to follow the local molecular cues present in the brain or spinal cord, and intends to transplant Q-Cells® to treat certain diseases where glia are defective.

Figure 2. Q-Cells® differentiate into both types of glial cells: oligodendrocytes (green stain for myelin basic protein [MBP]) and astrocytes (red stain for human glial fibrillary acidic protein [GFAP]) in the shiverer mouse brain. Q-Cells® were implanted into the brains of newborn shiverer mice.

In demyelinating diseases such as Multiple Sclerosis, inflammatory attack damages the oligodendrocytes, resulting in demyelination, i.e., loss of the insulating myelin sheath; this is the primary pathology that causes loss of proper neuronal function and can lead to neuron death. Q-Cells® can follow endogenous cues to replace the missing myelin (which is part of the living oligodendrocyte cells produced by Q-Cells®) on the damaged neurons, which Q believes can provide restorative therapy for demyelinating diseases. Other drugs have not been able to achieve this.

In many other neurodegenerative diseases, the diseased astrocytes are dysfunctional or harmful, hastening neuronal death. Supplementing diseased astrocytes with healthy astrocytes that are produced by Q-Cells® may reduce or prevent neuronal death. Healthy astrocytes are an important part of normal homeostasis in the CNS.

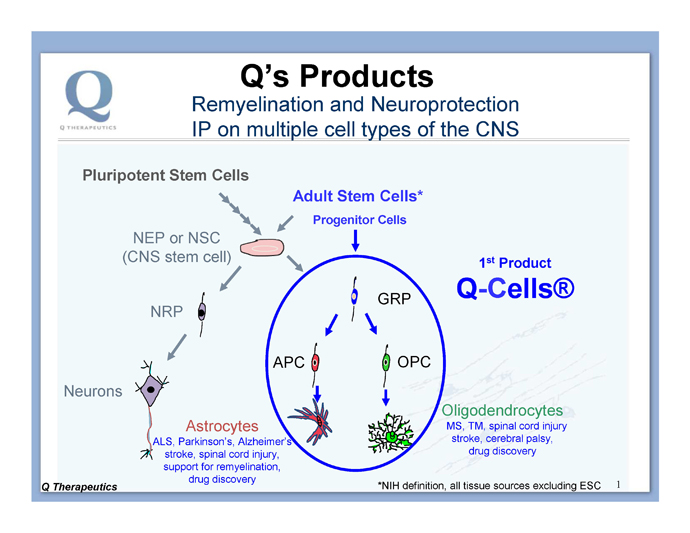

Q-Cells® (whether isolated directly from somatic tissue or derived from CNS stem cells or pluripotent cells) are late-stage lineage-restricted progenitor cells and have a restricted differentiation path: they become astrocytes and oligodendrocytes. In contrast, transplantation of the earlier-stage CNS stem cells (NSCs or NEPs, see Figure 3) can produce neurons in vivo in addition to glial cells. The Company believes that this less-restricted differentiation potential of the stem cells (in contrast to the more differentiated lineage-restricted glial progenitor cells) of the CNS has the potential to produce neurons inappropriately, which may form aberrant synaptic connections leading to neurological complications. Q has confirmed that terminal differentiation of Q-Cells® in animal models is naturally restricted to the two desired cell types: astrocytes and oligodendrocytes.

8

Benefits and features of Q-Cells®

Advantages of Q-Cells® include:

|

|

(1)

|

Q-Cells® provide important growth factors and other trophic functions that support neuronal health, providing treatment options for diseases directly involving neuronal degeneration such as ALS and Parkinson’s disease.

|

|

|

(2)

|

Q-Cells® provide myelin repair functions for diseases involving demyelination such as Multiple Sclerosis, Transverse Myelitis, Cerebral Palsy, and Spinal Cord Injury.

|

|

|

(3)

|

When placed in the CNS, Q-Cells® predictably replicate, migrate, and terminally differentiate into physiologically relevant glial cells: oligodendrocytes and astrocytes.

|

|

|

(4)

|

Q-Cells® don’t give rise to appreciable numbers of neurons, reducing potential for unwanted effects due to aberrant neuronal connections.

|

|

|

(5)

|

The isolation process is readily scalable to GMP.

|

|

|

(6)

|

Tissue-sourced Q-Cells® spend little time in culture prior to freezing of the cells to produce the product for shipment to treatment sites, providing advantages in production.

|

For all these reasons, Q believes that Q-Cells® are a desirable product for CNS cell therapeutics.

Many normal CNS cells remain viable in the CNS through a person’s life; our clinical trials are intended to ascertain whether transplanted Q-Cells® function for significant periods of time, or if periodic (e.g., annual) treatments will be appropriate. This replacement therapy will build on the model of successful bone marrow transplants, where stem cells in donor bone marrow replace diseased blood cells. However, unlike bone marrow transplants, Q-Cells® will be banked in vials containing the cells and shipped frozen to hospitals and clinics. Thus, Q plans to sell products following the model of a traditional specialty pharmaceutical company in that Q-Cells® will be prepared and inventoried in advance, and will not be generated uniquely for each patient.

Although the CNS has a degree of immune privilege, Q plans to initially use marketed immunosuppressants for a transient period, to mitigate potential for immune rejection associated with transplants.

Q-Cells® Can Be Obtained from a Variety of Sources

Q-Cells® can be obtained from several sources (Figure 3): (i) from somatic tissue (termed adult stem cells, isolated from fetal or adult tissue), (ii) differentiated from CNS stem cells [neuroepithelial stem cells (NEP) or neural stem cells (NSC)] which can be isolated from somatic tissue or derived from pluripotent cells), or (iii) differentiated from pluripotent cells (e.g., embryonic stem cells (ESC) or other pluripotent cells such as induced pluripotent stem cells (iPSC)). The Company has intellectual property (IP) covering multiple sources, giving it a strong IP position. Because of this broad IP position, Q has the ability to follow a development path that enables cost and time-efficient development of its cellular therapeutics. For these reasons, Q has chosen to develop its initial Q-Cells® product by isolating the cells directly from somatic (fetal cadaver) tissue, followed by expansion in the production facility, as this provides cells that are at the desired cell type without the need for additional in vitro differentiation.

Figure 3. Stem and progenitor cells of the brain and spinal cord. Stem cells can be derived from pluripotent stem cells (e.g., ESCs or iPSCs) or isolated from somatic tissue sources (called Adult Stem Cells). The Company’s strategy is to start with the more straightforward path: isolate and use unmodified cells that are already, naturally, at the desired cell type. Q believes that the restricted fate of Q-Cells® lowers the chance of unwanted side effects, such as inappropriate production of neurons. NRP = neuronal restricted precursor, GRP = glial restricted precursor, APC = astrocyte precursor cell, OPC = oligodendrocyte precursor cell.

9

Manufacturing

The Company has developed manufacturing protocols to isolate Q-Cells® directly from somatic (fetal cadaver) tissue, without the need for additional differentiation in vitro. Q has developed proprietary methods to expand the cells at this stage to enable treatment of larger numbers of patients from each preparation. Q’s strategy is to start with the most straightforward path: isolate and characterize unmodified cells that are already, naturally, at the desired stage of differentiation, to achieve proof of activity in clinical trials. Q believes that this strategy enables development of Q-Cells® and other cellular therapeutics in the most cost and time-effective manner.

The Company will use a centralized laboratory (contract GMP cell production manufacturer) for cell isolation and expansion and to provide the necessary quality control. The clinical transplant sites will receive frozen cells, which they will subsequently thaw, wash and inject into the target site of the patient. Use of allogeneic cells (i.e., cells derived from a tissue not obtained from the patient), rather than autologous cells (cells derived from the patient’s own tissues) both enables use of what Q believes will be the most effective healthy cells as well as permits cell therapy to be an off-the-shelf treatment, promoting more widespread use. The manufacturing of the Q-Cells® is done via a proprietary process developed by Q. This process can be shared with Q’s contract manufacturer of choice, or with several manufacturers to mitigate the risk of loss of any one manufacturing subcontractor.

The Company is currently working with the GLP/GMP Cell Therapy Facility (CTF) operated by the University of Utah. Q may seek other manufacturers as its development programs progress, certainly once Q-Cells® have been approved for commercial sale.

Q Therapeutics’ Intellectual Property

Q Therapeutics has exclusive worldwide rights to its Q-Cells® product, either through an agreement with the University of Utah Research Foundation (“UURF”) or through owned, internally developed intellectual property. The Q patent portfolio encompasses five families of neural lineage progenitor or stem cell technologies. Currently, Q has rights to 14 (11 US) issued patents to which it has a license agreement with the University of Utah and the National Institutes of Health. This license provides for royalties on the Company’s and sublicensees’ sales and contains due diligence obligations and related provisions; a portion of the consideration to the University of Utah was equity in Q. In addition, Q has rights to 5 U.S., 2 Canadian, 1 Japanese, 1 South Korean, 1 PCT and 1 EPO pending patent applications in the field of neural lineage progenitor and stem cells.

Q also holds a U.S. Trademark to its first product name, Q-Cells® (serial number: 78869175; registration number: 3,385,490), and U.S. and international Trademarks/Service marks to: Q Therapeutics® (U.S. serial number: 78-415,125; U.S. registration number: 3,280,432; international registration number: 867,474).

Q’s issued/granted patents and patent applications that are licensed or owned by Q as of September 30, 2011, include the following:

Common Neural Progenitor for the CNS and PNS

Mahendra S. Rao, Tahmina Mujtaba

ISSUED U.S. Patent 6,830,927

Generalization, Characterization, and Isolation of Neuroepithelial Stem Cells and Lineage Intermediate Precursor

10

Mahendra S. Rao, Margot Mayer-Proschel, Tahmina Mujtaba

PCT/US98/ 09630, Filed 5/7/98, published PCT application

Isolation of Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel

ISSUED U.S. Patent 6,734,015

Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel and Anjali J. Kalyani

ISSUED U.S. Patent 6,787,353

Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel, Anjali J. Kalyani

PCT/US98/ 13875, filed, 7/3/98, published PCT application

Lineage Restricted Glial Precursors from the Central Nervous System

Mahendra S. Rao, Mark Noble, Margot Mayer-Proschel

ISSUED U.S. Patent 6,235,527

Lineage Restricted Glial Precursors from the Central Nervous System

Mahendra S. Rao, Mark Noble, Margot Mayer-Proschel

PCT/US98/ 24456, filed, 11/17/98, published PCT application

Generation, Characterization, and Isolation of Neuroepithelial Stem Cells and Lineage Restricted Intermediate Precursor

Mahendra S. Rao, Margot Mayer-Proschel, Tahmina Mujtaba

2,289,021, filed 5/7/98, published Canadian patent application

Generation, Characterization, and Isolation of Neuroepithelial Stem Cells and Lineage Restricted Intermediate Precursor

Mahendra S. Rao, Margot Mayer-Proschel, Tahmina Mujtaba

GRANTED Israeli Patent, 132584

[Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel, Anjali J. Kalyani

2,294,737, filed 7/3/98, published Canadian patent application

Note: the above Canadian patent application is abandoned with the right to revive until July 2012.]

Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel, Anjali J. Kalyani

GRANTED Israeli Patent, 133799

Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel, Anjali J. Kalyani

ISSUED Japanese Patent 4,371,179

Lineage-Restricted Precursor Cells Isolated From Mouse Neural Tube and Mouse Embryonic Stem Cells

Tahmina Mujtaba and Mahendra S. Rao

PCT/US00/ 12446, filed 5/5/00, published PCT application

11

Lineage Restricted Glial Precursors from the Central Nervous System

Mahendra S. Rao, Mark Noble and Margot Mayer-Proschel

ISSUED U.S. Patent 6,900,054

Method of Isolating Human Neuroepithelial Precursor Cells from Human Fetal Tissue

Margot Mayer-Proschel, Mahendra S. Rao, Patrick A. Tresco and Darin J. Messina

ISSUED U.S. Patent 6,852,532

Isolation of Mammalian CNS Glial Restricted Precursor Cells

Mahendra S. Rao and Margot Mayer-Proschel

ISSUED U.S. Patent 7,037,720

Isolation of Mammalian CNS Glial-Restricted Precursor Cells

Mahendra S. Rao and Margot Mayer-Proschel

ISSUED U.S. Patent 7,595,194

Generation, Characterization and Isolation of Neuroepithelial Stem Cells and Lineage Restricted Intermediate Precursor

Mahendra S. Rao and Margot Mayer-Proschel

12/568,419, filed 9/28/09, published U.S. patent application

Methods Using Lineage Restricted Glial Precursors from the Central Nervous System

Mahendra S. Rao, Mark Noble and Margot Mayer-Proschel

ISSUED U.S. Patent 7,214,372

Lineage Restricted Glial Precursors

Mahendra S. Rao and Tahmina Mujtaba

ISSUED U.S. Patent 7,795,021

Lineage Restricted Glial Precursors

Mahendra S. Rao and Tahmina Mujtaba

12/209,559, filed 9/12/08, published U.S. patent application

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba and YuanYuan Wu

PCT/US2003 /002356, filed 1/23/03, published PCT application

Lineage-Restricted Neuronal Precursors

Mahendra S. Rao, Margot Mayer-Proschel and Anjali J. Kalyani

12/233,857, filed 9/19/08, published U.S. patent application

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba, YuanYuan Wu and Ying Liu

2,473,749, filed 1/23/03, published Canadian patent application

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba, YuanYuan Wu and Ying Liu

03732101.5, filed 1/23/03, published European patent application

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba, YuanYuan Wu and Ying Liu

2008-139534, filed 1/23/03, published Japanese patent application

12

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba, YuanYuan Wu and Ying Liu

2004-7011381, filed 1/23/03, published South Korean patent application

Pure Populations of Astrocyte Restricted Precursor Cells

Mahendra S. Rao, Tahmina Mujtaba, YuanYuan Wu and Ying Liu

12/433,060, filed 4/30/09, published U.S. patent application

Method of Isolating Human Neuroepithelial Precursor Cells from Human Fetal Tissue

Margot Mayer-Proschel, Mahendra S. Rao, Patrick A. Tresco and Darin J. Messina

ISSUED U.S. Patent 7,517,521

Method of Isolating Human Neuroepithelial Precursor Cells from Human Fetal Tissue

Margot Mayer-Proschel, Mahendra S. Rao, Patrick A. Tresco and Darin J. Messina

12/395,677, filed 3/1/09, published U.S. patent application

Methods and Compositions for Expanding, Identifying, Characterizing and Enhancing Potency of Mammalian-Derived Glial Restricted Progenitor Cells. Robert Sandrock, James Campanelli and Deborah A. Eppstein, PCT/US2010/055956, filed November 2010, published PCT application

In addition, Q has entered into out-license agreements with Life Technologies (LIFE), Molecular Transfer, Inc, (MTI), and xCell Science LLC, (xCell), under which the licensees may develop, manufacture and sell certain cell products covered by Q’s IP for research and drug discovery use only, for which Q (or its subsidiary NeuroQ) is anticipated to receive royalty payments, and in the case of xCell, Q may provide certain payments for research activities.

CNS Therapeutic Market Overview

The global CNS therapeutics market was valued at almost $100 billion in 2007. (Datamonitor Healthcare CNS Market Overview, 2008). This market is comprised of three main segments:

(1) Neurology (e.g. Parkinson’s and Alzheimer’s Diseases, Multiple Sclerosis, Spinal Cord Injury, ALS)

(2) Psychiatry (e.g. Depression, ADHD, Schizophrenia)

(3) Pain (e.g. Migraine).

While the psychiatry market represents nearly half of all dollars spent on CNS drug therapies, the neurology segment of the market is the fastest growing. Market growth overall is fueled by the increasing aging of the population as well as the increasing reported incidence of CNS disorders due to better diagnostic techniques.

The United States represents approximately half of this global market and is realizing the fastest growth rates. This is the result of three factors: Higher prices charged for the drugs themselves compared to other markets; the larger volume of patients seeking treatment; and the higher rates of pharmacotherapy compared to other countries.

13

The Unmet Need in the CNS Therapeutic Market

The CNS therapeutic market is based primarily on traditional drug therapies (small molecules and biologics). While this growing market is large and represents nearly 25% of all dollars spent on prescription pharmaceuticals worldwide, there remains a high unmet need in the treatment of many neurological diseases where current therapies are inadequate or yet to be developed. Two examples are Multiple Sclerosis (MS) and Lou Gehrig’s disease (Amyotrophic Lateral Sclerosis, or ALS).

The annual worldwide pharmacotherapy market for Multiple Sclerosis is approximately $10 billion. The vast majority of all approved MS therapies seek to slow disease progression by “knocking down” the autoimmune component of the disease, which causes the damage and destruction of the myelin sheath that surrounds the neurons. However there is no approved product that repairs this damage once it has occurred. Thus, while current therapies may slow or even halt the progression of the disease, once the damage is done, there is currently no means of repairing that damage. This represents a substantial unmet need in the MS disease space.

Similarly, there is only one approved drug for the treatment of ALS/Lou Gehrig’s disease. This drug, Rilutek ®, prolongs the life expectancy of ALS patients by approximately 60-90 days. ALS is always fatal, and there are no approved drugs that substantially slow or halt the progression of the disease, much less reverse its devastating effects. This too represents an unmet need in the CNS therapeutic market. ALS strikes approximately as many people (5,000-6,000) a year in the U.S. as does MS, but due to the rapid disease progression leading to death in 2-5 years after diagnosis, the estimated prevalence in the U.S. is only 30,000 patients, thus ALS is classified as an orphan disease.

Given these and many other shortcomings in the approved pharmacopeia for injuries and diseases of the CNS, there is an opportunity to substantially expand the CNS therapeutic market with new technologies that address the unmet needs. Stem cell-based therapy holds the promise of significantly expanding the CNS market and satisfying the unmet needs that exist.

The Potential of Stem Cell-Based Therapy

Stem cell based therapy is seen by many as the next great advance in the treatment of disease and injury. It holds the promise of better therapy for disorders which are currently not well treated and new therapies to meet currently unmet needs. Should this promise hold true, the currently available therapies could be displaced and the pharmacotherapuetic market substantially expanded as new stem and progenitor cell therapies are approved for human use.

The immense promise of stem cell biology has prompted the formation of several companies seeking to exploit the therapeutic potential of stem cells. Approaches to creating stem cell therapies fall into two broad categories:

|

|

(1)

|

Isolating and purifying new populations of stem or progenitor cells from various tissues, expanding them as necessary and transplanting the cells into various target organs. One challenge with this approach is ensuring that the exact desired population can be reproducibly purified and expanded. This affects safety and efficacy as well as the ease of scaled-up manufacturing.

|

|

|

(2)

|

Stimulating existing stem cells to “wake up,” expand and differentiate inside the body at an accelerated rate. Challenges associated with this approach include manipulating complex interactions among multiple growth factors and endogenous signals to generate the desired outcomes, as well as complications due to malfunctioning or mutant endogenous cells in certain diseases.

|

14

Q believes that the fastest route to a safe and effective product is through the first route – therapy with well characterized, unmodified cells that perform their tasks as nature intended, functioning as ‘mini-factories’ and playing roles appropriate to the specific disease state.

Several types of cells are under evaluation for use in cell therapy, including embryonic stem cells, human cord blood and placental stem cells, and fetal or adult tissue from various organ sites. Purified cell populations can be injected intravenously or transplanted directly into target organs such as brain, heart, pancreas, blood and bone. For most neurodegenerative diseases, Q believes that CNS cells, not hematopoietic or mesenchymal lineage cells, are needed.

Market Opportunity for Q Therapeutics

Q Therapeutics aims to change the way medicine is practiced in the treatment of many debilitating and often fatal diseases of the brain and spinal cord by bringing to market a patented cell-based therapeutic that addresses substantial unmet needs in the CNS therapeutic market today. The Company believes that its initial Q-Cells® product could meet a variety of these needs across a number of CNS diseases. By demonstrating that Q-Cells® are safe and effective first in smaller orphan indications and later in larger target markets, the Company believes it can both augment and/or displace current therapeutic approaches as well as expand the therapeutic market in currently untreatable CNS conditions. Should this prove true, Q-Cells® would address a multi-billion dollar market opportunity in treatment of neurodegenerative diseases for which there are no effective treatments.

Q intends to bring Q-Cells® to the market first to treat ALS (Lou Gehrig’s disease) to demonstrate the safety and efficacy of its cell based therapeutic. Thereafter, Q-Cells® will be brought to other indications potentially including Multiple Sclerosis, Spinal Cord Injury, Parkinson’s and Alzheimer’s diseases. Q estimates that the annual market opportunity for its initial orphan disease targets exceeds $1 billion worldwide. Application of its Q-Cells® product to other larger market diseases such as MS would substantially expand the market available to Q.

Orphan Disease Strategy for Initial Commercialization

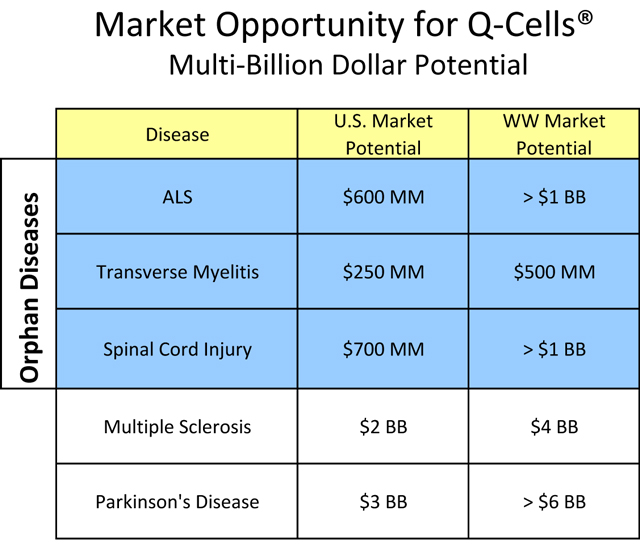

Q’s first commercial targets are orphan diseases with billion-dollar market potential (Figure 4). The Orphan Drug Act of 1983 (in this paragraph, the “Act”) defined an “orphan drug” as a therapy intended to treat rare “orphan” diseases, those affecting fewer than 200,000 Americans. The benefits provided by the Act may include more rapid regulatory timelines, tax benefits, and seven-year market exclusivity for the first product approved for an indication. Despite the smaller numbers of affected patients, orphan diseases often have highly motivated patient advocacy groups that are eager to assist companies with patient recruitment and therapeutic development. Moreover, substantial annual per-patient treatment prices effectively offset the relatively small patient populations. Due to the focused nature of marketing permitted by targeting orphan indications, Q might be able to capture a significant portion of the U.S. market for certain orphan diseases without need for a major marketing partner, provided that it has adequate financial resources. This ability to target patients suffering from orphan diseases also provides an incentive to potential Q development partners with interest in funding development costs and providing developmental expertise in exchange for marketing rights.

Figure 4. Multi-billion dollar market potential for Q-Cells®. The initial orphan diseases may allow Q or its partner to market the product with a focused specialty sales force. Market opportunity size was calculated using a lifetime treatment cost projection of $200,000, assuming 50%, 30% and 35% patient population penetration for the orphan diseases of ALS, Transverse Myelitis and Spinal Cord Injury, respectively, and 2% and 10% patient penetration for Multiple Sclerosis and Parkinson’s disease, respectively. Further market opportunities exist for additional neurodegenerative disease targets.

15

Q Market Development Strategy – Orphan Indications First, Larger Markets Follow

|

|

A.

|

Initial target indications

|

Q-Cells® offer multiple repair mechanisms from one product due to Q-Cells®’ ability to differentiate into both oligodendrocytes and astrocytes (discussed earlier in this Description of Business section). We have broadly characterized the disease targets into three general but overlapping groups: diseases primarily of myelination deficiencies, diseases where neuronal loss is the dominant mechanism, and diseases where both of the above fall into play. Evaluation of Q-Cells® in these various neurodegenerative diseases provides multiple shots on goal.

|

|

1.

|

Amyotrophic Lateral Sclerosis (ALS), or Lou Gehrig’s Disease

|

ALS is diagnosed in 5,000-6,000 new individuals per year in the U.S., comparable in annual incidence to Multiple Sclerosis. Patient death generally occurs 2-5 years after diagnosis, resulting in an estimated prevalence of 30,000 (ALS Association). ALS is a neurodegenerative disease causing progressive deterioration and loss of motor neurons, affecting both upper and lower motor neurons. The loss of nerve stimulus to specific muscles results in atrophy and progressive weakness that leads to paralysis. Death usually results from respiratory failure.

There is no curative treatment for ALS. The only drug approved for treatment for the disease—riluzole (Rilutek®) - is believed to reduce (but not reverse) damage to motor neurons by decreasing the release of glutamate, and prolongs survival by only 60-90 days.

Studies in mouse models of ALS suggest that abnormalities in astrocytes and microglia, in addition to motor neurons, play a role in disease onset as well as progression. Astrocytes play a prominent role in CNS homeostasis. In both ALS patients and animal models, astrocyte abnormalities and physiological dysfunction can be seen many months before motor neuron degeneration and precede clinical disease [literature references include Clement et al, Science 302, 113-117 (2003); Rothstein et al Neuron 18, 327-338 (1997); Lepore et al, Nature Neuroscience 11, 1294-1301 (2008); Yamanaka et al, Nature Neuroscience 11, 251-253 (2008); Wang et al, Human Molecular Genetics 20, 286-293 (2011)]. Further in support of the role of diseased astrocytes in causing motor neuron degeneration in ALS, the Maragakis lab recently demonstrated that transplanting rat astrocyte precursors carrying the SOD mutation (this mutation gives rise to ALS in patients carrying such mutation) into healthy rats results in degeneration of motor neurons in the previously healthy rats [Proc Natl Acad Sci on line edition Oct 2011 10.1073 (2011)]

This altered physiology of CNS astrocytes contributes to disease progression by resulting in further susceptibility to motor neuron loss. Supplementing these diseased astrocytes with healthy ones (such as occurs via transplantation of GRP cells) is a reasonable hypothesis for a promising therapeutic approach for slowing and/or halting the ALS disease course.

Maragakis and colleagues have demonstrated the validity of this hypothesis, showing therapeutic benefits following transplantation of rat GRPs into the SODG93A rat model (Lepore et al, Nature Neuroscience 11, 1294-1301 (2008)). Administration of rat GRPs (the rat cells homologous to human Q-Cells®) into the cervical spinal cord after onset of disease resulted in enhanced survival and motor function.

16

The results demonstrating that Q-Cells® exhibit characteristics of cell survival, migration and differentiation into mature glial phenotypes in animal models, in conjunction with safety data, the scientific literature and the above mentioned benefits obtained with rat GRPs implanted into the SODG93A rat, provide the rationale for testing Q-Cells® in clinical trials involving motor neuron degeneration in ALS patients. Implantation of Q-Cells®, which produce non-diseased astrocytes, may ultimately provide normal astrocytic function overcoming the dysfunction of the patient’s diseased astrocytes, thereby restoring homeostatic control and reducing or preventing further death of motor neurons.

|

|

2.

|

Demyelinating Diseases: Multiple Sclerosis and Transverse Myelitis

|

Q is also evaluating Q-Cells® in animal studies for Multiple Sclerosis (MS), a chronic autoimmune-triggered demyelinating neurodegenerative disease, and Transverse Myelitis (TM), a related but acute, localized inflammatory disease of the spinal cord. Multiple clinical and pathological studies suggest that there are many common features of the inflammation and neural injury between TM and MS, with a shared primary pathology of demyelination due to immune attack destroying the oligodendrocytes. TM may offer some technical advantages over MS for initial proof of concept clinical trials, as the inflammatory-induced lesion occurs in only one location in the spinal cord (often thoracic) and does not recur: i.e., TM is mono-focal and mono-phasic. Due to the similarity of the lesion pathology in TM and MS, demonstration of efficacy of remyelination in the orphan disease TM may be an indicator for efficacy in the more prevalent disease of MS. The rationale for using Q-Cells® in these indications is based on data obtained using both animal and human GRPs in models of disease. Demonstration of remyelination in lesions in TM and MS patients may also be relevant for developing treatments of other diseases in which demyelination is a significant factor such as cerebral palsy, white-matter stroke and certain traumatic spinal cord injuries.

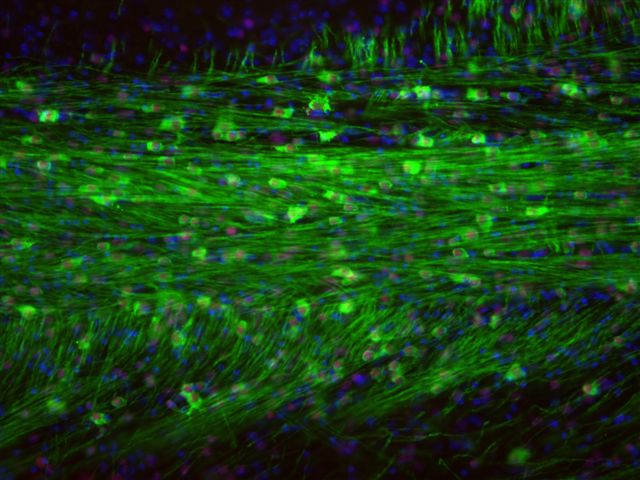

Shiverer is an established myelin-deficiency model in which the entire CNS is defective in normal myelination. Q and its collaborators at Johns Hopkins have demonstrated that Q-Cells® engrafted into shiverer (a) effectively compete with host (defective) oligodendrocytes, (b) myelinate host axons resulting in normal myelin and (c) demonstrate benefits in a focal inflammatory spinal cord lesion model (Figure 5, Q data; Walczak et al, GLIA 59, 499-501 (2011)). Others have shown that human GRPs transplanted into shiverer/rag2 mice extended survival of a portion of the mice (Windrem et al, Cell Stem Cell 2, 553-565 (2008)). They also documented that the implanted human cells interacted effectively with the host proteins and did not leave the CNS. The efficacy of a localized treatment that does not produce toxicities in other organs is a significant finding. This is supported further by an extensive body of literature demonstrating remyelination by rodent glial precursors and related cells in multiple animal models [including publications from Blakemore (1999), Ben Hur (2006), Cummings (2005), Duncan (2004, 2005), Goldman (2008), Keirstead (2004, 2005), Whittemore (2010), Rao (1997-2010), Sandrock (2010), and Walczak (2011).] This myelination has occurred in both the presence and the absence of an ongoing inflammatory process.

Figure 5. Myelination by implanted Q-Cells® that produced oligodendrocytes.

Shiverer is a mouse with a mutation that produces defective myelin basic protein (MBP) and hence defective myelin. Q-Cells® implanted in shiverer/rag2 brain mature into oligodendrocytes that produced normal MBP (green). All MBP seen here is produced by Q-Cells® that matured into oligodendrocytes (human cell-specific red nuclei stain).

17

|

|

3.

|

Traumatic Spinal Cord Injury

|

Spinal Cord Injury (“SCI”) due to trauma results in 10,000-12,000 people paralyzed each year in the U.S., and it is estimated that over 250,000 people are living with spinal cord injury in the U.S. This has tremendous costs both in terms of patient care, lost productivity as well as quality of life. It has been projected that the U.S. could save up to $400 billion in future healthcare costs if there were effective therapies to treat and prevent spinal cord injuries (Christopher and Dana Reeve Foundation, Centers for Disease Control, University of Alabama National Spinal Cord Injury Statistical Center). Q has collaborated with Itzhak Fischer, PhD, at Drexel University to test Q-Cells® in animal models of traumatic spinal cord injury. Recently published studies by Q and its collaborators at Drexel document the safety and statistically-significant, reproducible, disease modifying activity of Q-Cells transplanted into the injury site in an athymic rat model of thoracic contusion SCI (Jin et al., J Neurotrauma; 28(4):579-94; 2011).

|

4.

|

Parkinson’s Disease

|

Parkinson’s Disease (“PD”) affects more than one million patients in the U.S., and the numbers are expected to increase with the aging of the population. Symptoms of PD are caused by the gradual loss of neurons in a relatively small part of the brain, the substantia nigra. These neurons normally secrete dopamine, and lack of dopamine leads to symptoms such as shaking, rigidity, difficulty and slowness in movement, and postural instability. Although patients initially respond to treatment with L-dopa or dopaminergic agonists, over time this response decreases. Several early trials have found that administration of single growth factors failed to provide meaningful clinical benefits in PD patients.

Studies in animal Parkinson’s disease models have suggested non-cell autonomous killing of neurons, with diseased astrocytes playing a critical initiating role. Astrocytes in culture exert a protective effect on neuronal cells in a setting where both cell-types are co-cultured. Studies in a primate model of Parkinson’s disease showed functional benefits after implantation of neural cells. Upon autopsy, a large number of progeny astrocytes were found juxtaposed with the host nigrostriatal circuitry suggesting that the “homeostatic adjustments” to the microenvironment results in preservation of the remaining host nigrostriatal pathway (Redmond et al, Proceedings of National Academy of Sciences USA 104, 12175–12180 (2007)). As Q-Cells® produce healthy astrocytes, this provides potential for protective effects including those via production of multiple growth factors and other trophic support, rather than relying on a single factor. Q anticipates that it will pursue studies of Q-Cells® in Parkinson’s disease models upon availability of appropriate additional funding.

C. Other Disease Targets

Q-Cells® provide a platform technology that may be useful to treat not only demyelinating diseases, but other neurodegenerative diseases that can benefit from the neuronal support provided by growth factors and other trophic support by Q-Cells®. The patient populations and markets for Q’s follow-on therapeutic targets may be substantial, in addition to the opportunity in ALS, MS, TM, Spinal Cord Injury and Parkinson’s Disease discussed above:

|

|

·

|

Alzheimer’s Disease (“AD”) is a progressive, neurodegenerative disease characterized by abnormal clumps (amyloid plaques) and tangled bundles of fibers (neurofibrillary tangles) in the brain. Symptoms include memory loss, language deterioration and confusion and eventually lead to loss of cognition and personality. It is estimated that about 5.3 million people in the U.S. suffer from AD, with annual healthcare costs in excess of $170 billion. The number of patients is projected to reach 13.5 million by 2050 (Alzheimer’s Association, 2010).

|

18

Transplantation of neural cells that produce glial cells (both astrocytes and oligodendrocytes) as well as transplantation of astrocyte precursors, provided benefits in Alzheimer’s Disease mouse models, rescuing neurons and improving memory (Hampton et al, Journal of Neuroscience 30(3), 9973-9983 (2010); Blurton-Jones et al, PNAS 106(32), 13594-13599 (2009)). Since Q-Cells® mature into glial cells after transplantation, Q believes there may be an opportunity for ultimate use of Q-Cells® potentially to both slow decline and/or restore function for Alzheimer’s disease patients. Q is evaluating initiating a collaboration to further investigate the efficacy of Q-Cells® in animal models once additional financing has been obtained.

|

|

·

|

Traumatic Brain Injury (“TBI”) has been reported to occur in 1.4 million Americans each year, leaving 50,000 dead and more than 80,000/year with lifelong disabilities, and costing over $60 billion in 2000. The U.S. Centers for Disease Control estimates that at least 5.3 million Americans are living with the need for help in daily activities due to TBI. TBI is a leading injury for active military personnel in war zones. Other than acute phase treatments to prevent further injury (e.g., surgery, relief of pressure build-up), treatment of headaches, seizures and physical rehabilitation, there is no treatment for and nothing to reverse TBI. The multiple support functions of Q-Cells® may be beneficial in achieving recovery from TBI.

|

|

|

·

|

Cerebral Palsy (“CP”) has a U.S. patient population of about 750,000. An initial target may be for spastic diplegia, with involves injury to the cerebral cortex and represents approximately 70% of CP. As Q-Cells® can provide myelinating oligodendrocytes, they may provide benefits to CP patients.

|

|

|

·

|

Stroke afflicts almost 800,000 people and is the third leading cause of death in the U.S, with total annual costs over $40 billion. Market projections are significant even if only a small portion of these patients were treated. Q-Cells® may be beneficial in treating stroke both for restoring myelination, as well as the support provided by astrocytes to restoring neuron function.

|

|

|

·

|

Leukodystrophies and CNS storage diseases: These are several inherited pediatric diseases for which the molecular cause is known to involve a single gene defect. There are no treatment options for most of these diseases, often resulting in death at a young age. Although a few companies including Genzyme and Biomarin have developed enzyme replacement therapies to successfully treat systemic manifestations of a few of these diseases, the systemically-administered enzyme pharmaceuticals do not cross the blood-brain barrier to treat CNS targets. Such CNS diseases may provide future opportunity to Q as there are many storage disorders with severe CNS manifestations that involve destruction of oligodendrocytes with concomitant demyelination. Q-Cells®, as they are transplanted directly into the CNS, may be able to provide both the missing enzyme in the CNS as well as replace the destroyed oligodendrocytes and thus provide remyelination.

|

|

|

·

|

Peripheral Neuropathies have no effective treatments. In addition to causing severe pain, they are a leading cause of amputations in the developed world. Eight million diabetes patients have neuropathy in the U.S. alone. Q has patents on cells that support the peripheral nervous system.

|

Q-Cells® - Benefits of Localized Therapy

The ability of animal results to predict human results, and accordingly the drug development risk profile, depends on many factors including:

(1) The pharmacokinetic and metabolic profiles of a drug in animals vs. humans, which can greatly influence both efficacy and safety

19

(2) How the drug affects the target diseased and disease-causing tissues

(3) What the drug does to non-target cells.

Many drug candidates fail in development because they affect not only their intended target but have toxic off-target effects in other organ systems as well. For example, a drug intended to treat headache pain may fail to become a commercial product due to unacceptable toxic systemic effects in other organs, e.g., heart or kidneys. Q-Cells® are a localized treatment in the CNS. Studies conducted by Windrem et.al. (Cell Stem Cell 2, 553-565(2008)) indicate that human GRPs stop at the boundary where the central nervous system meets the peripheral nervous system. Q anticipates that this localized nature of the planned Q-Cell® therapy may reduce risk from systemic toxicity, which Q believes may reduce the risk of drug failure in early clinical trials due to systemic toxicities. Animal safety studies to be conducted are intended to evaluate safety both locally in the spinal cord and brain as well as systemically before initiating clinical trials.

In addition to the initial disease target of ALS, Q’s IP portfolio can be applied to additional follow-on indications as discussed above under Q Market Development Strategy. Q’s IP portfolio can also be applied to novel assays for drug screening, to identify new products for drug therapy with a focus on diseases of the central nervous system.

Competition

Q believes that Q-Cells® are different from other cell therapy products both in their novel mechanism of action / capabilities as well as the ease of production. The competitive landscape involves companies working on a range of alternative treatments for diseases of the CNS including traditional drug products, protein therapeutics, gene therapy and different types of cell therapy. Q believes that the cell therapy approach has many advantages over single drug therapeutics for many neurodegenerative diseases. Thus, the closest direct competition is other cell therapy companies working on the same disease targets.

Direct competition

A limited number of companies are working on the therapeutic neurological application of stem cells, including the public companies Geron (NASDAQ: GERN), StemCells Inc. (NASDAQ: STEM), ReNeuron (LSE: RENE.L), and Neuralstem (AMEX: CUR), and the private company California Stem Cells, Inc. Geron is conducting Phase 1 clinical trials in the U.S. with embryonic stem cell-derived oligodendrocyte precursor cells to treat traumatic spinal cord injury. Their approach involves isolating and expanding human embryonic stem cells, then differentiating them in culture to produce oligodendrocyte precursor cells. StemCells Inc. uses human fetal-derived neural stem cells and has completed an initial Phase 1 clinical trial in early infantile Batten disease, a rare congenital lysosomal storage disorder; this company also has filed an IND for Pelizaeus-Merzbacher disease, which is a very rare pediatric leukodystrophy. StemCells Inc. also recently initiated Phase 1 clinical trials in Switzerland in patients with traumatic spinal cord injury, and is conducting preclinical studies for retinal disorders. ReNeuron uses human fetal-derived neural stem cells that it has conditionally immortalized with a c-mycER gene, and it has commenced clinical trials in stroke patients in the United Kingdom. Neuralstem is conducting Phase 1 clinical trials in patients with ALS using a neural stem cell product. California Stem Cells is exploring use of embryonic stem cell-derived motor neurons in animal models of spinal muscular atrophy and ALS.

20

Why Q Therapeutics’ approach may prove superior

A noteworthy distinction between Q and other CNS cell therapy companies involves the specific properties of Q-Cells®. These cells produce mature glial cells (astrocytes and oligodendrocytes) that can both achieve myelination of neuronal axons as well as otherwise promote neuron health, while minimizing unwanted and potentially deleterious neuron formation. Q-Cells® are a more mature cell type - at a more advanced stage of differentiation - than are the cells used by StemCells Inc., ReNeuron, and Neuralstem, who all use the less-differentiated CNS stem cells that produce neurons as well as glial cells (see Figure 3). Unlike ReNeuron, Q does not use genetically immortalized cells, which Q believes could raise safety issues, e.g., concerns about deleterious effects such as tumor formation.

Truly pluripotent stem cells could also be a starting source. This approach requires the identification of proper signaling factors and establishing the sequence of use to correctly and safely induce differentiation into the desired CNS cell type and to ensure sufficient elimination of the undifferentiated ESCs which can form tumors, prior to transplantation. In contrast to Geron, Q-Cells® are not derived from undifferentiated (pluripotent) embryonic stem cells. Rather, Q-Cells® are isolated already at the desired final cell type, and require no in vitro differentiation protocols such as those used by Geron with its ESC-derived oligodendrocyte progenitor cells. Q believes that the progenitor cell therapies it is developing, generated from pre-formed cells that naturally occur, offer safety and efficacy benefits.

Other Potential Competitors

Another approach is the use of cells or virus-based vectors implanted in the brain as delivery vehicles for gene therapy, with the goal of achieving local production of desired proteins and growth factors. NsGene is studying the use of encapsulated, genetically-modified cells to secrete biological growth factors in the treatment of Alzheimer’s and Parkinson’s diseases. Ceregene is conducting clinical trials with virus-based vectors for gene therapy for Parkinson’s and Alzheimer’s diseases, with other disease targets in earlier research. Q’s approach differs significantly in that it does not rely on a single growth factor for success, and in that it does not use genetically-modified cells or viruses; rather, unmodified Q-Cells® produce the range of growth factors and trophic support that is typical of healthy glial cells.

Other companies working in the CNS space have focused on stimulating endogenous differentiation of nascent adult stem cells with administration of molecules to trigger their expansion and differentiation in vivo (e.g., NeuroNova, Braincells). Still other pharmaceutical and biotechnology companies (including, among others Genzyme, Biogen-Idec, Acorda, Merck-Serono, GlaxoSmithKline, Roche, and Sanofi-Aventis) have programs to identify therapeutics to treat neurodegenerative diseases such as MS, Parkinson’s disease and Alzheimer’s disease. Some of these programs might yield effective therapeutics that could compete with Q’s products, and which might prove less costly and easier to administer.

Description of Property.

Q Therapeutics utilizes leased office and laboratory space located at 615 Arapeen Drive, Suite 102, Salt Lake City, UT 84108, and owns the equipment it uses therein which is summarized in the Financial Statements. The cost of the lease is $12,192 per month for the year ending December 31, 2011.

Legal Proceedings.

None.

Submission of Matters to a Vote of Security Holders.

On October 12, 2011, the sole director of Grace 2, all of the directors of Q Acquisition, Inc., a majority of the shareholders of Q Acquisition, Inc., over two-thirds of the holders of Q Therapeutics Series A and Series B preferred stock, a majority of the common shareholders of Q Therapeutics and all of the directors of Q Therapeutics voted in favor of the transactions contemplated by the Merger Agreement.

21

Market for Common Equity and Related Stockholder Matters and Small Business Issuer Purchases of Equity Securities.

Market Information

Our common stock is not currently trading on any stock exchange and it is not quoted on any quotation system or traded in any other manner in the public markets. We are not aware of any market activity in our stock since inception through the date of this filing.

The Company, through a registered broker-dealer, plans to submit a Form 211 Application to FINRA, in an effort to have the Company’s Common Stock quoted on the OTC Bulletin Board. We cannot guarantee that we will obtain a listing. There is currently no trading activity in our securities, and there can be no assurance that a regular trading market for our common stock will ever be developed.

Holders

As of the date of this filing, there are 148 record holders of 24,557,632 shares of our common stock.

Dividends

We do not intend to pay cash dividends on our common stock and preferred stock for the foreseeable future, but currently intend to retain any future earnings to fund the development and growth of our business. The payment of dividends if any, on the common stock and the preferred stock will rest solely within the discretion of the Board of Directors and will depend, among other things, upon our earnings, capital requirements, financial condition, and other relevant factors. We have not paid or declared any dividends upon our common stock or preferred stock since inception.

Recent Sales of Unregistered Securities

In connection with the Merger Agreement, on October 13, 2011, we issued an aggregate of 22,671,923 shares of Common Stock (including shares underlying warrants and options), or 89.7% of the outstanding shares prior to the offering, to Q Therapeutics, Inc. Shareholders in exchange for 100% of the outstanding shares of Q Therapeutics, Inc., which merger resulted in Q Therapeutics, Inc. becoming our wholly owned subsidiary. These securities qualified for exemption under Section 4(2) of the Securities Act since the issuing of securities by us did not involve a public offering. The offering was not a “public offering” as defined in Section 4(2) due to the insubstantial number of persons involved in the deal, size of the offering, manner of the offering and number of securities offered. We did not undertake an offering in which we sold a high number of securities to a high number of investors. In addition, these shareholders had the necessary investment intent as required by Section 4(2) since they agreed to and received share certificates bearing a legend stating that such securities are restricted pursuant to Rule 144 of the Securities Act. This restriction ensures that these securities would not be immediately redistributed into the market and therefore not be part of a “public offering.” Based on an analysis of the above factors, we have met the requirements to qualify for exemption under Section 4(2) of the Securities Act for this transaction.

22

On August 30, 2011, Q Therapeutics, Inc. received $450,000 in bridge financing from investors, (including $90,000 in credit towards the advancement of consulting fees and out-of-pocket expenses) evidenced by secured convertible promissory notes (“Notes”) and a unit, consisting of an aggregate of (a) one, Seven-Year Common Stock Purchase Warrant to purchase one share of the Company’s common stock exercisable at $1.00 per share of the Company’s common stock, (b) one Seven-Year Common Stock Purchase Warrant to purchase one share of the Company’s common stock exercisable at $2.00 per share of the Company’s common stock and (c) one Seven-Year Common Stock Purchase Warrant to purchase one share of the Company’s common stock with an exercise price equal to the lesser of (a) the price per share of the Company’s Shares issued in a financing or (b) the Fair Market Value (“FMV”) of the Company’s Shares. An automatic conversion feature is in place for each Note, whereby upon the attainment of the Company’s Private Placement Offering’s minimum raise amount of $3,000,000, each Note’s outstanding principal and interest balance will automatically be converted into common stock of Q Therapeutics, Inc. at the same purchase price and upon the same terms as investors in the Company’s Private Placement Offering. These securities qualified for exemption under Section 4(2) of the Securities Act since the issuance securities by us did not involve a public offering. The offering was not a “public offering” as defined in Section 4(2) due to the insubstantial number of persons involved in the deal, size of the offering, manner of the offering and number of securities offered. Q Therapeutics, Inc. did not undertake an offering in which we sold a high number of securities to a high number of investors. In addition, these shareholders had the necessary investment intent as required by Section 4(2) since they agreed to and received share certificates bearing a legend stating that such securities are restricted pursuant to Rule 144 of the Securities Act. This restriction ensures that these securities would not be immediately redistributed into the market and therefore not be part of a “public offering.” Based on an analysis of the above factors, Q Therapeutics, Inc. has met the requirements to qualify for exemption under Section 4(2) of the Securities Act for this transaction.

As more fully described in Item 1.01 above, on October 13, 2011, immediately following the Merger, pursuant to the Purchase Agreement, we consummated the Private Placement for the issuance and sale of Units, consisting of an aggregate of (a) one share of Common Stock, (b) one Seven-Year Common Stock Purchase Warrant to purchase one share of the Company’s common stock exercisable at $1.00 per share, and (c) one Seven-Year Common Stock Purchase Warrant to purchase one share of the Company’s common stock exercisable at $2.00 per share, for aggregate gross proceeds of $3,803,047. Such securities were not registered under the Securities Act. The issuance of these securities was exempt from registration under Regulation D, Regulation S and Section 4(2) of the Securities Act. We made this determination based on the representations of Investors, which included, in pertinent part, that such shareholders were either (a) “accredited investors” within the meaning of Rule 501 of Regulation D promulgated under the Securities Act, or (b) not a “U.S. person” as that term is defined in Rule 902(k) of Regulation S under the Act, and that such shareholders were acquiring our common stock, for investment purposes for their own respective accounts and not as nominees or agents, and not with a view to the resale or distribution thereof, and that the shareholders understood that the shares of our common stock may not be sold or otherwise disposed of without registration under the Securities Act or an applicable exemption therefrom.