Attached files

| file | filename |

|---|---|

| EX-10.30 - EXHIBIT 10.30 - CANTALOUPE, INC. | ex10-30.htm |

| EX-32 - EXHIBIT 32 - CANTALOUPE, INC. | ex32.htm |

| EX-31.2 - EXHIBIT 31.2 - CANTALOUPE, INC. | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - CANTALOUPE, INC. | ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - CANTALOUPE, INC. | ex23-1.htm |

| EX-10.29 - EXHIBIT 10.29 - CANTALOUPE, INC. | ex10-29.htm |

| EX-10.31 - EXHIBIT 10.31 - CANTALOUPE, INC. | ex10-31.htm |

| EX-10.32 - EXHIBIT 10.32 - CANTALOUPE, INC. | ex10-32.htm |

| EX-10.23 - EXHIBIT 10.23 - CANTALOUPE, INC. | ex10-23.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended June 30, 2011

|

|

OR

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934

|

|

For the transition period from ____________________ to _____________________

|

Commission file number 000-50054

|

USA Technologies, Inc.

|

|

|

|

(Exact name of registrant as specified in its charter)

|

||

|

Pennsylvania

|

|

23-2679963

|

|

|||

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|||||

|

100 Deerfield Lane, Suite 140, Malvern, Pennsylvania

|

|

19355

|

|

|||

|

(Address of principal executive offices)

|

(Zip Code)

|

|||||

|

(610) 989-0340

|

|

|||||

|

(Registrant’s telephone number, including area code)

|

||||||

|

Securities registered pursuant to Section 12(b) of the Act:

|

||||||

|

Title of Each Class

|

|

Name Of Each Exchange On Which Registered

|

|

|||

|

Common Stock, no par value

Series A Convertible Preferred Stock

Warrants to Purchase Common Stock

|

The NASDAQ Stock Market LLC

|

|||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer o Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes o No x

The aggregate market value of the voting common equity securities held by non-affiliates of the Registrant was $26,186,473 as of the last business day of the most recently completed second fiscal quarter, December 31, 2010, based upon the closing price of the Registrant’s Common Stock on that date.

As of August 31, 2011, there were 32,285,690 outstanding shares of Common Stock, no par value.

USA TECHNOLOGIES, INC.

TABLE OF CONTENTS

|

PAGE

|

||||||

|

4

|

||||||

|

20

|

||||||

|

28

|

||||||

|

28

|

||||||

|

29

|

||||||

|

31

|

||||||

|

32

|

||||||

|

40

|

||||||

|

41

|

||||||

|

42

|

||||||

|

42

|

||||||

|

42

|

||||||

|

43

|

||||||

|

46

|

||||||

|

60

|

||||||

|

62

|

||||||

|

63

|

||||||

|

64

|

||||||

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding, among other things, the anticipated financial and operating results of the Company. For this purpose, forward-looking statements are any statements contained herein that are not statements of historical fact and include, but are not limited to, those preceded by or that include the words, “estimate,” “could,” “should,” “would,” “likely,” “may,” “will,” “plan,” “intend,” “believes,” “expects,” “anticipates,”

“projected,” or similar expressions. Those statements are subject to known and unknown risks, uncertainties and other factors that could cause the actual results to differ materially from those contemplated by the statements. The forward looking information is based on various factors and was derived using numerous assumptions. Important factors that could cause the Company’s actual results to differ materially from those projected, include, for example:

|

|

●

|

general economic, market or business conditions;

|

|

|

●

|

the ability of the Company to generate sufficient sales to generate operating profits, or to sell products at a profit;

|

|

|

●

|

the ability of the Company to raise funds in the future through sales of securities;

|

|

|

●

|

the ability of the Company to obtain commercial acceptance of its products and services;

|

|

|

●

|

the ability of the Company to compete with its competitors to obtain market share;

|

|

|

●

|

whether the Company’s customers purchase or rent ePort devices or our other products in the future at levels currently anticipated by our Company, including our Jump Start Program;

|

|

|

●

|

whether the Company’s customers continue to operate or commence operating ePorts received under the Jump Start Program or otherwise at levels currently anticipated by the Company;

|

|

|

●

|

whether the Company’s customers continue to utilize the Company’s transaction processing and related services, as our customer agreements are generally cancelable by the customer on thirty to sixty days’ notices;

|

|

|

●

|

whether the recent significant increase in the interchange fees to be charged by Visa and MasterCard for small ticket debit card transactions would adversely affect our business, including our revenues, gross profits, and anticipated future connections to our network;

|

|

|

●

|

whether the Company would be able to pass along to its customers the recent significant increase in interchange fees charged by Visa and MasterCard for small ticket debit card transactions without those customers cancelling their contracts with us;

|

|

|

●

|

the ability of the Company to obtain sufficient funds through operations or otherwise to repay its debt obligations, or to fund development and marketing of its products;

|

|

|

●

|

the ability of the Company to satisfy its trade obligations included in accounts payable and accrued liabilities;

|

|

|

●

|

the ability of the Company to predict or estimate its future quarterly or annual revenues and expenses given the developing and unpredictable market for its products and the lack of established revenues;

|

|

|

●

|

the ability of the Company to retain key customers from whom a significant portion of its revenues is derived;

|

|

|

●

|

the ability of a key customer to reduce or delay purchasing products from the Company; and

|

|

|

●

|

as a result of the slowdown in the economy and/or the tightening of the capital and credit markets, our customers may modify, delay or cancel plans to purchase our products or services, and suppliers may increase their prices, reduce their output or change their terms of sale.

|

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. Actual results or business conditions may differ materially from those projected or suggested in forward-looking statements as a result of various factors including, but not limited to, those described above and in the “Risk Factors” section of this Form 10-K. We cannot assure you that we have identified all the factors that create uncertainties. Moreover, new risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all risks on our business or the

extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. Readers should not place undue reliance on forward-looking statements.

Any forward-looking statement made by us in this Form 10-K speaks only as of the date of this Form 10-K. Unless required by law, we undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Form 10-K or to reflect the occurrence of unanticipated events.

3

USA TECHNOLOGIES, INC.

OVERVIEW

We are a provider of technology-enabled solutions that facilitate electronic payment transactions and value-added services within the unattended Point of Sale (“POS”) market and a leading provider in the small ticket, beverage and food vending industry. Since our founding in 1992, we have designed and marketed systems and solutions that facilitate electronic payment options, as well as the ability to remotely monitor, control and report on the results of distributed assets such as vending machines, kiosks, personal computers, photocopiers, and laundry equipment. Historically, these distributed assets have relied on cash for payment in the form of coins or bills, whereas, our systems

allow them to accept cashless payments such as through the use of a credit card. We derive revenues from the sale, lease and rental of our POS terminals, from license and/or service fees and transaction fees on installed POS terminals. As of June 30, 2011, the Company had approximately 119,000 devices connected to its network. The Company counts its ePort connections upon shipment of an active terminal to a customer under contract, at which time activation on its network is performed by the Company, and the terminal is capable of conducting business via the Company's network and related services. An ePort connection does not necessarily mean that the unit is actually installed

by the customer on a vending machine, or that the unit has begun processing transactions, or that the Company has begun receiving monthly service fees in connection with the unit. At the time of shipment of the ePort, the customer becomes obligated to pay the one-time activation fee, and is obligated to pay monthly service fees in accordance with the terms of the customer's contract with the Company. During the year ended June 30, 2011, the Company processed approximately 72 million cashless transactions totaling approximately $120 million, representing a 95% increase in transaction volume and a 76% increase in dollars processed from the 37 million cashless transactions

totaling over $68 million in the previous fiscal year ended June 30, 2010. Pursuant to its agreements with customers, the Company earns transaction processing fees equal to a percentage of the dollar volume processed by the Company, which are included as licensing and transaction processing revenues in its Consolidated Statements of Operations. The Company’s transaction processing volume is not indicative of the gross profit from license and transaction fees which is based upon the monthly service fees and transaction processing fees paid to us by our customers.

Our solutions consist predominately of POS electronic payment devices, proprietary operating systems, certified payment software and reporting and communication capabilities. Our solutions are able to process traditional magnetic stripe credit and debit cards, contactless credit and debit cards, as well as near-field communication (“NFC”) equipped mobile phones where consumers could make payments with their cell phones. Our proprietary POS solutions enable electronic micro-payments at unattended POS locations.

Our customers primarily consist of beverage and food vending machine owners and operators; commercial laundry operators servicing colleges, universities and multi-family housing; brand marketers wishing to provide their products or services via kiosks or vending machines; equipment manufacturers that would like to incorporate our networked devices (e.g., remote monitoring, reporting and control as well as cashless payments) into their products; and business center operators, which include hotels and audio visual companies. The functionality of our solutions includes the flexibility to execute a variety of payment applications on a single system, transaction security, connectivity options, compliance with

certification standards, and centralized, accurate, real-time sales and inventory data to manage distributed assets.

The Company also manufactures and sells energy management products which reduce the electrical power consumption of equipment, such as refrigerated vending machines and glass front coolers, thus reducing the electrical energy costs associated with operating this equipment. We derive equipment revenues from our energy management products through the sale of the product.

We have a nineteen year history in our industry, a recognized brand name, value proposition for our customers, and reputation of innovation in our product and services. We believe that the foregoing positions us to capitalize on industry trends.

THE INDUSTRY

We operate in the small ticket electronic payments industry and more specifically the unattended POS market. Our solutions facilitate electronic payments in industries that have traditionally relied on cash transactions. In addition, our solutions provide electronic monitoring and online reporting for distributed assets. We believe the following industry trends will drive growth in demand for electronic payment systems in general and more specifically within the markets we serve:

|

|

■

|

the shift toward electronic payment transactions and away from cash and checks;

|

|

|

■

|

the increase in both consumer and merchant/operator demand for electronic transaction functionality; and

|

|

|

■

|

improving POS technology and NFC equipped mobile phone payment technology.

|

4

Shift toward electronic payment transactions and away from cash and checks

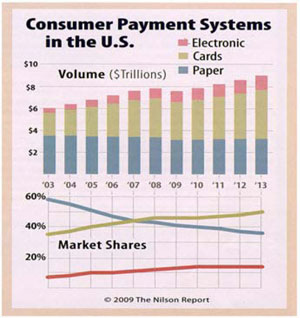

There has been a shift away from paper-based methods of payment, including cash and checks, towards electronic-based methods of payment. While consumers continue to use checks and cash to pay for goods and services, there is a migration towards the use of card-based payment to purchase items. According to The Nilson Report, a news and research publication on consumer payment systems, electronic payment transaction volume surpassed paper-based transaction volume for the first time in 2006, continuing the trend of migration of consumer transactions from paper-based to electronic payments. According to the December 2009 Nilson Report, the four card-based systems—credit, debit, prepaid, and electronic

benefits transfer—generated $3.59 trillion in the United States in 2009. The number of payment transactions using credit cards, debit cards, prepaid cards, and EBT cards totaled 66.74 billion in 2008—up 6.7% from 2007. By 2013, card-based purchases are projected to reach nearly $4.5 trillion, with over 89 billion transactions projected for this same period.

Increase in Consumer and Merchant/Operator Demand for Electronic Payments

Increase in Consumer Demand. The unattended, vending and kiosk POS market has historically been dominated by cash purchases. However, oftentimes, cash purchases at unattended POS locations represent a cumbersome transaction for the consumer because they do not have the correct monetary value (paper or coin), or the consumer does not have the ability to convert their bills into coins. We believe electronic payment system providers such as USA Technologies that can meet consumers’ demand within the unattended market will be able to offer retailers, card associations, card issuers and payment processors and business owners an expanding value

proposition at the POS.

Increase in Merchant/Operator Demand. Increasingly, merchants and operators of unattended payment locations (e.g., vending machines, car wash, tabletop games, etc.) are utilizing electronic payment alternatives. Several of the Company’s customers have been able to drive increased revenue of their distributed assets through this expanded market opportunity. Furthermore, owners have demonstrated the ability to increase the price of their goods with little to no decline in transaction volume. In addition, electronic payment systems provide merchants and operators real-time sales and inventory data utilized for back-office reporting and

forecasting, helping them to manage their business.

Increase in Demand for Networked Assets. M2M technology includes capturing value from wireless modules and electronic devices to improve business productivity and customer service. The term M2M describes any kind of 2-way communication system between geographically distributed devices through a centrally managed software application without human intervention. According to M2M Magazine (“Is it Touching Our Everyday Lives?”, M2M, November 18, 2008), there are over 50 billion machines capable of being networked.

Networked assets provide improved internal business processes such as energy management systems capable of collecting diagnostic information and communicating with the operator’s host information system to optimize energy consumption. Networked assets also have the ability to remotely monitor merchandise to maximize sales and track inventory in real-time. In addition, networked assets provide valuable information regarding consumers’ purchasing patterns and payment preferences allowing operators to more effectively reach and satisfy consumers. Networked assets allow information to be centralized and reported in electronic format enabling the data to be more accurately and thoroughly

analyzed and digitally presented and available online. According to the M2M Magazine article cited above, the networked asset industry is in its nascency, and electronic solution providers that can provide interconnectivity between distributed assets offer consumers, retailers, machine operators and manufacturers an expanded value proposition by optimizing the capabilities of a distributed asset.

5

POS Technology and NFC Equipped Mobile Phone Payment Improvements

Advances in Computing. History has shown that advances in microprocessing technology, storage capacity and software are enabling increasing complexity and functionality of electronic payment systems at unattended POS locations. Such advances are expanding the range of services and functionality offered by electronic payment systems, including credit and debit, prepaid cards, gift cards and loyalty card programs, electronic bill payment and electronic check truncation. In addition, advances in technology, computing and telecommunications over the past decade have reduced the cost of production and operations of more sophisticated electronic payment

systems, thereby reducing the barrier of adoption for merchants and operators.

Card Innovation at the POS. Recent industry developments such as the emergence of NFC or contactless equipped mobile phone payment have resulted in the POS becoming an important area of differentiation for card associations, card issuers and payment processors. As the market for issuing credit cards has become more saturated in the U.S., card associations and card issuers are differentiating their brands by expanding their offerings. Payment processors are also differentiating themselves by expanding their offerings as front-end authorization and back-end clearing and settlement have become more commoditized. Card associations, card issuers

and payment processors are differentiating their offerings, in part, by offering value-added applications and incorporating innovative technologies including contactless / NFC equipped mobile phone payment technology.

Payment Terminal Innovations at the POS. NFC and mobile payments are projected to continue on an upward trajectory, with 65% of total tablets and smartphones equipped with NFC payment capabilities and as many as 800 million consumers with NFC-enabled handsets by 2014 (Goldman Sachs Equity Research Report, June 9, 2011). This same report cites that Google believes that there are approximately 300,000 existing POS terminals worldwide that are compatible with the Google Wallet, with about 120,000 of those in the US. With approximately 50,000 NFC and mobile payments ready ePorts shipped to our customers, we believe that the continued increase in consumer

preferences towards contactless payments may represent a significant growth opportunity for the Company.

SPECIFIC MARKETS WE SERVE

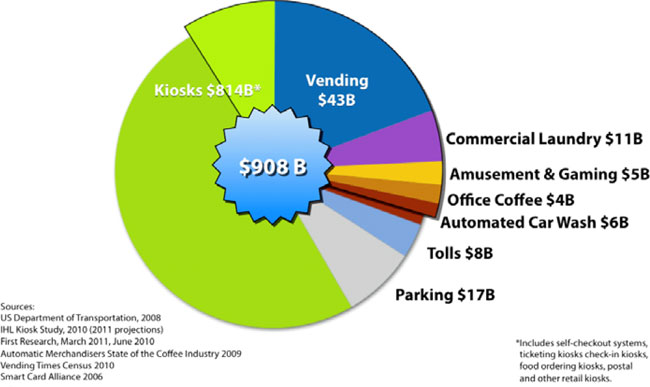

Our current customers are primarily in the self-serve, small ticket retail markets including beverage and food vending and kiosk, commercial laundry, car wash, amusement and gaming, and office coffee. While these industry sectors represent only a small fraction of our total market potential, as depicted below, these are the areas where we have gained the most traction. In addition to being our primary markets, these sectors serve as a proof-of-concept for other unattended POS industry applications.

6

Vending. According to Vending Times’ 2010 Census of the Industry, annual U.S. sales in the vending industry sector were estimated to be approximately $43 billion. The market segment can be addressed by our end-to-end solution consisting primarily of vended products retailing for $1.00 or greater. According to this census, the vending industry experienced a 6% decline in 2010 versus 2009, due in large part to the downturn in the economy and the decrease in serviceable locations such as manufacturing plants, but the contraction of growth prompted operators to look for additional ways to make up revenue. According to Automatic Merchandiser State of

the Industry Report 2011, operators increased their investment in technology to improve business efficiencies and increase margins. Among these technology investments, 3.5% of operators surveyed indicated that they had invested in cashless payments system while 1.7% indicated they had installed a remote monitoring system. With the continued shift to electronic payments and the advancement in mobile and POS technology, we believe the traditional beverage and food vending industry will continue to look to cashless payments systems to increase sales and margins and help growth.

Kiosk. According to IHL Consulting Group Market Study dated July 1, 2010, approximately $678 billion was transacted through self‐service kiosks in 2009, which represents an increase of 9.7% from the previous year. Furthermore, IHL projects that spending at self-service kiosks will grow approximately 10% during 2010 and that demand for self-service kiosks should push sales at these terminals to over $1 trillion by 2014. Kiosks are becoming increasingly popular as self-service “specialty” shops within larger retail environments. Value-added services, such as photo

enlargement and custom imaging are a prominent example, located within many major retailers. As merchants continue to seek new ways to reach their customers outside of retail locations and mobile and electronic payment technology make this expansion more plausible, we believe electronic payment system providers who can service the payment needs of kiosk-driven transactions will be able to offer retailers, card associations, card issuers and payment processors an expanding value proposition at the POS.

In 2008/2009, Single Cup/Office Coffee Service (“OCS”) sales posted a five percentage point decline from the prior 12-month period, marking the first setback since 2003/2004. OCS revenues totaled $3.73 billion in 2009/2010, according to the 2010 Automatic Merchandiser State of the Coffee Service Industry Report, September 2010. According to this same publication, the 4-year gain from 2003/2004 to 2007/2008 was the longest consistent growth trend in the industry’s history, driven by higher pricing and investment in better quality products and equipment, and the decline in sales was a direct result of declining worksite populations and employer cost cutting. According to the National Coffee

Association’s 2008 National Coffee Drinking Trends survey, 2007 was the first year that daily coffee consumption among adults surpassed soft drink consumption. The 2011 study listed 40% of the 18-24 year olds who responded as drinking coffee daily, up from 31% in 2010 with a total of 58% of the population surveyed saying they drank coffee in the past day, up from 56% in 2010 but down 60% in 2009. In October 2008, entered into a three year contract with Starbucks pursuant to which Starbucks will offer coffee in unattended kiosk locations using the ePort G-8 cashless payment system. As of the date hereof, there are a couple of hundred ePort devices being deployed in unattended kiosks pursuant to this agreement.

Commercial Laundry. According to a 2010 Report on Dry Cleaning and Laundry Services published by Anything Research, the current size of the laundry services market is $22.4 billion, and although the industry experienced a revenue decline of 5% in 2009 compared to 2008, long term forecasts for the industry project positive growth. The Dry Cleaning and Laundry Facilities Industry Profile published by First Research dated July 11, 2011, states that the laundry services industry includes about 30,000 companies with combined annual revenue of approximately $10 billion. Major companies include Coinmach Service, DRYCLEAN USA, Mac-Gray, and Martin Franchises. The

industry includes about 20,000 companies that provide retail laundry and dry cleaning services, and 10,000 that provide services through coin-operated laundromats. The coin-laundry segment is fragmented: the 50 largest firms generate about 40% of revenue. This segment of the business is made up of both coin-operated laundries and coin-operated machines located in multi-family housing developments such as apartments, condominiums and universities. The Coin Laundry Association’s website, www.coinlaundry.org, points out that “...coin laundries thrive in periods of both growth and recession. During periods of recession, when home ownership decreases, the self-service laundry market expands as more people are unable to afford to repair, replace or purchase new washers and dryers, or as they move to apartment housing with inadequate or nonexistent laundry facilities.” The

self-service laundry market consists of an estimated primary customer base of approximately 96 million people living in rental housing, as of the 2010 U.S. Census. A secondary customer base consists of the over 2 million resident college and university students in the US (U.S. Census Bureau, 2004). We reach our target market primarily via the seven largest laundry operators in the US.

Business Centers. According to the American Hotel & Lodging Association, the hotel and lodging industry was a nearly $134 billion industry with approximately 47,000 hotels in the United States and 300,000 worldwide in 2008. With the increased globalization of our economies and the increased need for travel for both personal and business reasons, there remains a demand for unattended business center availability in hotels, with ever-greater percentages of travelers needing and expecting use of computers, printers, fax machines, copiers, and other business services.

OUR COMPETITIVE STRENGTHS

We believe that we benefit from a number of advantages gained through our nineteen year history in our industry. They include:

Trusted Brand Name. The USA Technologies brand has a strong national reputation for quality, reliability and innovation. We believe that card associations, payment processors and merchants/operators trust our system solutions to handle financial transactions in a secure operating environment. Our trusted brand name is best exemplified through several one-way exclusive relationships, each averaging three years in duration, which we have solidified with several leading organizations within the unattended POS industry, including Merit/AMI Entertainment and Air-Serv.

7

Large Installed Base. We have a large installed base of unattended POS electronic payment systems. As of June 30, 2011, we had approximately 119,000 connections to our network. Our technology provides POS payment solutions as well as real-time POS and diagnostic data to our customers. Our customers maintain both the payment solution as well as the real-time data with one provider rather than through multiple providers. Our installed base supports our sales and marketing infrastructure by enhancing our ability to establish or expand our market position. Finally, our

installed base provides several opportunities for referrals for new business, either from the merchant or operator of the deployed asset or through one of our several strategic relationships.

Attractive Value Proposition for Our Customers. We believe that our solutions provide our customers an attractive value proposition. Our solutions make possible increased purchases by consumers who in the past were limited to the physical cash value on hand while making a purchase at an unattended terminal. Rather than search for coins or dollar bills to feed a vending machine, customers have the option of paying by card. We believe our solutions make possible increased convenience and a broader universe of potential customers – those with cash or electronic forms of payment. Furthermore, the cost of our solution continues to decrease

making it more economically attractive for our customers to install our devices in their machines. Our historical data demonstrates that approximately 26% of all of the transactions on traditional beverage and food vending machines utilizing our ePort® terminals consist of credit/debit card transactions.

Large and Increasing Scale. During the year ended June 30, 2011, we generated total licensing and processing fees of $16.4 million, successfully processed approximately 72 million transactions accounting for more than $120 million in purchases and, as of June 30, 2011 had approximately 119,000 connections to our network. We believe that our scale and footprint enable us to market and distribute our products more effectively and in more markets than most of our competitors, and to provide our customers with innovative, comprehensive and reliable system solutions.

Leading Research and Development. Our research and development initiatives focus on adding features and functionality to our system solutions through the development and utilization of our processing and reporting network and new technology. Since we began operations in 1992, we have been granted 81 patents and currently have 12 patent applications pending. We have developed innovative and reliable unattended POS electronic payment devices and solutions over the past several years. For example, our most recent cashless vending solution, the ePort EDGE™, was made available for sale to our customers during the fourth quarter of the 2009

fiscal year. Our ePortG-8 is an integrated one-piece design, combining the card-reader and processor while enabling magnetic swipe card transactions and NFC equipped mobile phone payment, and is 65% smaller than our previous G-7 model.

NFC Ready. USA Technologies’ ePort G series and ePort Connect service would accept and process NFC and/or mobile payments at the point of sale. The Company partnered with Visa, MasterCard and others for a significant rollout of these devices, resulting in approximately 50,000 NFC and mobile-ready ePort devices shipped to our customers. The Company continues to connect its current G-series model, the ePort G8 to its network, putting it in a position to benefit from any growth in consumer adoption of these payment methods.

One-Stop Shop, End-to-End Solution. We believe that our ability to bundle the services included in our cashless payment solution, as well as the ability to tailor them to individual customer needs, makes it easy and efficient for our customers to adopt and deploy our technology, and results in a service unmatched in the small ticket self-service retail vending market today. Other cashless payment solutions available in the market today require the operator to set up their own accounts for cashless processing, manage multiple service providers (i.e. hardware terminal manufacturer, wireless network provider and credit card processor), as well as to implement

their own cashless systems. Our solution provides all of the following, under one cohesive service umbrella;

|

|

●

|

A broad product line of devices or software, consisting of the ePort G8 which can accept multiple forms of cashless payment, from swipe and contactless and the 2010 National Automatic Merchandising Association (“NAMA”) -Innovation-Award-winning ePort EDGE.

|

|

|

●

|

Unique payment programs such as our JumpStart and leasing programs, which help operators acquire the ePort hardware without an up-front capital investment.

|

|

|

●

|

Our comprehensive end-to-end ePort Connect cashless payment service which includes merchant account set-up, wireless activation, merchant services, over-the-air updates, and 24x7 customer service and support.

|

|

|

●

|

Business deployment planning services to help operators successfully deploy cashless payment systems. This program is based on extensive market data, which helps guide operators to the locations where cashless vending machines would be most successful.

|

8

OUR GROWTH OPPORTUNITY

Our objective is to enhance our position as a leading provider of technology that enables electronic payment transactions and value-added services at small-ticket, self-service, retail locations such as traditional beverage and food vending, kiosks and commercial laundry. The key elements of our strategy are to:

Leverage Existing Customers/Partners. We have a solid base of key customers across multiple markets (vending, kiosk, etc.) that have deployed our solutions. We have worked to build these relationships, drive future deployments, and develop customized network interfaces. Our customers have seen the benefits of our products and services first-hand and represent the largest opportunity to scale our solution. These customers are a key component of our plan to drive sales.

Expand Distribution in Core Markets. We have worked to develop a strong market presence in the vending and energy markets. Increasing sales and distribution to our largest customers is important to the long-term success of the Company, but we are intently focused on building a broader base of customers within these core markets to drive long term revenue and value. Our efforts in this regard have led to the addition of approximately 900 new customers during the fiscal year 2011.

Further Penetrate Attractive Adjacent Markets. We plan to continue to increase the functionality of our system solutions to address the specific needs of various markets. We currently focus on specific segments of unattended POS markets, including traditional beverage and food vending, kiosk, commercial laundry and business center industry sectors. We believe we have the ability to penetrate a much larger addressable market by selling or licensing our technologies to equipment makers of everyday devices such as toll booths, tire inflation and vacuum equipment, car washes and countless other devices. Using wired and/or wireless networks and centralized,

server-based software applications, managers can remotely monitor, control, and optimize a network of devices regardless of where they are located. Networked devices enable cashless transactions, sales analysis, remote monitoring, and optimized machine maintenance.

New Product Innovation. We are a leading innovator of technology that enables electronic payment transactions and value-added services at the unattended POS locations. We will continue enhancing our solutions in order to satisfy our customers and the end-consumers relying on our products at the POS locations. Our product innovation team enhances the design, size, and speed of data transmission, as well as security and compatibility with other electronic payment solution providers’ technologies. We believe our continued product innovation will lead to further adoption in the unattended POS payments market. For example, our newer

ePort G-8™ solution is 65% smaller than our previous model, and the current retail cost of the ePort EDGE™ is $199 per device.

Leverage Intellectual Property. We have been granted 81 patents which assert various claims, including claims relating to unattended payment processing, networking and energy management devices. In addition, we own numerous trademarks, copyrights, design rights and trade secrets. We will continue to leverage this intellectual property to add value for customers, attain an increased share of the market, address competition and attempt to generate licensing revenues.

Capitalize on High Growth Opportunities in International Markets. We are currently focused on the U.S. and Canadian market for our ePort devices and related network but may seek to establish a presence in emerging, high growth electronic payment markets in Europe, Asia and Latin America. In order to do so, we would have to invest in additional sales and marketing and research and development resources targeted towards these regions. Our energy management devices have been shipped to customers located in the U.S., Canada, Mexico, United Kingdom, Germany, France, Japan, Australia, and the Philippines.

Capitalize on the growing NFC and mobile payments trends. NFC and mobile payments are projected to continue on an upward trajectory, with 65% of total tablets and smartphones equipped with NFC payment capabilities and as many as 800 million consumers with NFC-enabled handsets by 2014 (Goldman Sachs Equity Research Report, June 9, 2011). This same report cites that Google believes that there are approximately 300,000 existing POS terminals worldwide that are compatible with the Google Wallet, with about 120,000 of those in the U.S. With approximately 50,000 NFC and mobile payments ready ePorts shipped to our customers, the Company believes that the continued

increase in consumer preferences towards contactless payments represents a significant growth opportunity for the Company.

OUR PRODUCTS

Our products are available in several distinctive modular configurations, offering our customers flexibility to install a POS solution that best fits their needs and customer demands.

Intelligent Vending™ and Kiosk. As of June 30, 2011, we have approximately 110,000 ePort® and other cashless devices that are connected to our ePort Connect® solution for the vending and kiosks industries. Our ePort Connect® solution for the vending and kiosk industries enables cashless payments at unattended POS machines. ePort Connect® is an

end-to-end suite of cashless payment and telemetry services for the self service retail industries.

The Company counts its ePort connections upon shipment of an active terminal to a customer under contract, at which time activation on its network is performed by the Company, and the terminal is capable of conducting business via the Company’s network and related services. An ePort connection does not necessarily mean that the unit is actually installed by the customer on a vending machine, or that the unit has begun processing transactions, or that the Company has begun receiving monthly service fees in connection with the unit. At the time of shipment of the ePort, the customer becomes obligated to pay the one-time activation fee, and is

obligated to pay monthly service fees in accordance with the terms of the customer's contract with the Company.

9

Intelligent Vending™. Our latest improvement to Intelligent Vending™ is our ePort® G-8, which provides the same benefits as the G-7, plus important new features at a lower price. The G-8 solution is 65% smaller than the G-7 and combines traditional magnetic strip and NFC equipped mobile phone payment capabilities. In addition, our ePort Edge™ product became available for sale to customers during the fourth quarter of the 2009 fiscal year. The ePort Edge™ is a one-piece design and is intended for those in the vending industry who want a magnetic swipe-only cashless system at a current retail price of $199 per

device.

Kiosk. We provide an ePort® solution that utilizes our ePort® or software client, USALive®, and our comprehensive technology support and customer service to offer an electronic payment option and web-based remote monitoring and management for all kiosk types. Our ePort® solution enables kiosks to sell an increased variety of items and at a higher price point as compared to cash-only kiosks as consumers are

typically limited to the amount of available cash-on-hand. Kiosks permit a host of new services to become available at the point-of-demand, such as Sony’s self-service and Picture Station kiosks, where consumers can produce prints from their own digital media. In addition, our ePort® solution powers the POS solutions for unattended kiosk providers such as Merit Megatouch, Fantasy Photobooth and AIR-serv. In October 2008 Starbucks chose our ePort® mobile solution to deliver their product to customers through coffee kiosks.

eSuds™. eSuds™ is our solution developed for the commercial laundry industry. eSuds™ offers an e-mail alert system to notify users regarding machine availability, cycle completion, and other events and supports a variety of value-added services such as custom advertising or subscription-based payments.

Our eSuds™ system enables laundry operators to provide customers cashless transactions via the use of their credit cards, debit cards and other payment mediums such as student IDs. In addition, our eSuds™ service reduces operational costs through utilization of our remote monitoring technology, thereby maximizing the scheduling of service visits and increasing machine up-time. The system increases customer satisfaction through improved maintenance, higher machine availability, specialized services (i.e., e-mail alerts to indicate that laundry cycle is finished) and the convenience of non-cash transactions.

Installations of our eSuds™ product have been completed at 56 college and universities and are serviced on approximately 7,600 washer and dryer machines. For example, installations of our eSuds™ product have been completed at Carnegie Mellon University, Rutgers University, Case Western Reserve, Johns Hopkins University, Temple University and others. We are working with resellers and distributors, such as Caldwell & Gregory, to install eSuds™ at other colleges and universities. The Company also has a presence in the multi-family-housing laundry market through its relationship with CoinMach, a firm which has indicated that it operates approximately 850,000 laundry machines in North

America.

As of June 30, 2011, we had 830 eSuds™ room controllers servicing approximately 7,600 washer and dryer machines. We count an eSuds as a connection upon actual installation of our device on a washer or dryer or room controller.

Business Express®. We originally developed Business Express® to provide self-service business center solutions to the Hotel and Motel industry. With the introduction of the ePort® SDK and ePort® Transact® our target market has expanded to include printer and copier dealers and manufacturers. The Business Express® solution includes the ePort® SDK for computer-based transactions such as a Public PC®, and the ePort® Transact®, which enables printers and copiers to accept credit and debit cards for payment. These products are coupled with our customer

service support and ePort Connect® back-end system for payment processing and other value-added services.

ePort® Transact®, which became available in March 2010, is the latest version of our original payment technology system developed for self-service business center devices such as printers and copy machines. It is a cashless-transaction-enabling terminal that permits customers to use office equipment with a swipe of their credit or debit card. The ePort® Transact® can be sold as a stand-alone device to hotel, motel and other locations with business center needs, or to printer and copier dealers and manufacturers to be sold to their customers with the cashless option already installed.

As of June 30, 2011, we have several hundred Business Express® units installed nationwide with several of the major hotel chains.

Energy Management Products. Our Company offers energy conservation products (“Energy Misers” ®) that reduce the electrical power consumption of various types of existing equipment, such as vending machines, glass front coolers and other “always-on” appliances by allowing the equipment to selectively operate in a power saving mode when the full power mode is not necessary. Each of the Company’s Energy Miser® products utilizes occupancy sensing technology to determine when the surrounding area is vacant

or occupied. The Energy Miser® then utilizes occupancy data, room and product temperatures, and an energy saving algorithm to selectively control certain high-energy components (e.g. compressor and fan) to realize electrical power savings over the long-term use of the equipment. Customers of our VendingMiser® product benefit from reduced energy consumption costs, depending on regional energy costs, machine type, and utilization of the machine. Our Energy Misers® also reduce the overall stress loads on the equipment, helping to reduce associated maintenance costs.

10

The Energy Miser® family of energy-control devices includes:

VendingMiser® - installs in a cold drink vending machine and reduces the electrical power consumption of the vending machine.

CoolerMiser™ - reduces the electrical energy used by sliding glass or pull open glass-front coolers that contain non-perishable goods.

VM2IQ® and CM2IQ® - the second generation of the VendingMiser® and CoolerMiser™ devices that is installed directly inside the machine and has the capability to control the cooling system and the advertising lights separately.

SnackMiser® - reduces the amount of electricity used by non-refrigerated snack vending machines.

PlugMiser™ - reduces the amount of electricity used by all types of plug loads including those found in personal or modular offices (printers, personal heaters, and radios), video arcade games, and more.

We do not consider our energy management products as connections to our network.

OUR SERVICES

Through ePort Connect®, we offer end-to-end services to support our ePort devices and ePort SDK.

The ePort Connect® service includes card payment and processing services and M2M operational data such as:

Card Processing Services. Through our existing relationships with card processors and card associations, we provide merchant account and terminal ID set up, pre-negotiated discounted fees on small ticket purchases and direct electronic funds transfers EFTs to our customer’s bank account for all settled card transactions as well as ensure compliance with current processing regulations.

Wireless Connectivity. We manage the wireless SIM account activation, distribution, and the relationship with wireless providers for our customers.

Customer/Consumer Services. We support our installed base by providing 24-hour help desk support, repairs, and replacement of impaired system solutions. In addition, as the merchant of record on all transactions, all inbound billing inquiries are handled through a 24-hour help desk, thereby eliminating the need for merchants and operators to be bothered with customer billing inquiries and potential chargebacks.

Online Sales Reporting and Remote Management. Effective remote management is essential to cost effective deployment, maintenance and management of unattended POS locations. Via the USALive online reporting system, we provide reporting of credit and cash transactions, user configuration, reporting by machine and region, by date range and transaction type, data reports for operations and finance, graphical reporting for sales and to customers, and condition monitoring for equipment service as well as activation of new devices and location redeployments.

Over-the-Air Update Capabilities. Automatic over-the-air updates to software, settings, and security protocol from our network to our ePort card reader keep our customers’ hardware up-to-date and enable customers to benefit from any advancement made after their hardware or software purchase.

We enter into a processing and licensing agreement, or ePort Connect Services Agreement, with our customers pursuant to which we act as the exclusive provider of cashless financial services for the customer’s distributed asset, and the customer agrees to pay us an activation fee, monthly service fees, and transaction processing fees. Our agreements are generally cancelable by the customer upon thirty to sixty days notice to us.

OUR TECHNOLOGY-BASED SOLUTION

We believe that our ability to bundle our products and services, as well as the ability to tailor them to individual customer needs, makes it easy and efficient for our customers to adopt and deploy our technology, and results in a service unmatched in the vending market today. This one-stop-shop solution includes the ePort Connect® end-to-end payment and processing services and our cashless payment device or software for distributed assets such as vending machines, kiosks, laundry equipment, car wash, amusement and gaming, office coffee and other small-ticket, self-service industries.

The Client. The Company offers its customers several different devices or software to connect their distributed assets. These range from software to hardware devices consisting of control boards, magnetic strip card readers, and NFC readers. The devices or software can be embedded inside the host equipment, such as ePort SDK software residing in the central processing unit of a Kiosk or table-top game; it can be integrated as part of the host equipment, such as our ePort® G8 or EDGE hardware that can be attached to the door of a vending machine, at a payment hub in a self service car wash; or it

can be a peripheral, stand-alone terminal, such as our eTransAct® terminal for Copier Express.

ePort® is the Company’s core device, which is currently being utilized in vending and commercial laundry applications. Our ePort® product facilitates cashless payments by capturing the payment media and transmitting the information to our network for authorization with the payment system (e.g. credit card processors). Additional capabilities of our ePort® consist of control/access management by authorized users, collection of audit information (e.g. product or service sold, date and time of sale and sales amount), diagnostic

information of the host equipment, and transmission of this data back to our network for web-based reporting.

ePort TransAct® is the latest version of the Company’s original cashless, transaction-enabling device developed for self-service business center equipment such as PCs, fax machines and copiers. Similar to the ePort®, the ePort TransAct® capabilities include control/access management, collection of sales data (e.g. date and time of sale, sales amount and product or service purchased), and transmission back to our network for reporting to customers.

11

The Connectivity Mediums. Our solutions are interconnected for the transfer of our customers’ data through our USALive® network, providing multiple connectivity options such as phone line, ethernet or wireless. Increasing wireless connectivity options, coverage and reliability have allowed us to service a greater number of customer locations. Additionally, we make it easy for our customers to deploy wireless solutions by acting as a single point of contact. We have contracted with Verizon Wireless and AT&T in the United States and Rogers Wireless in Canada in order to supply our

customers with wireless network coverage.

The Network. Our USALive® network is responsible for transmitting payment information from our terminals for processing as well as transmitting sales and diagnostic data for storage and reporting to our customers. Also, the network, through server-based software applications, provides remote management information and enables control of the networked device’s functionality. Through our network we have the ability to upload software and update devices remotely enabling us to manage the devices (e.g., change protocol functionality, software upgrades, and change terminal display

messages).

USALive® is the enabler of turnkey cashless payment processing for our customers. The network is certified with several cashless payment systems, such as credit card processors and property management systems, facilitating the authorization and settlement of credit cards, debit cards, hotel room keys and student identification cards. The network also has the capability to act as its own payment processing system for other cashless payment media, such as on-line stored value or employee payroll deduction. The network authorizes transactions, occurring at the host equipment, with the appropriate payment system and sends approval or decline

responses back to the networked device to allow or terminate the transaction for the purchase of the product or service. The network consolidates successfully approved transactions from multiple devices, batches, and then transmits these batched transactions to the payment system for settlement.

Data Security. Visa has listed the Company as a PCI DSS Compliant Service Provider in the North American region as a result of validation conducted by a third party as of January 1, 2011. The USAT listing on Visa’s list of compliant companies can be found online at http://usa.visa.com/download/merchants/cisp-list-of-pcidss-compliant-service-providers.pdf.

SALES AND MARKETING

The Company’s sales strategy includes both direct sales and channel development, depending on the particular dynamics of each of our markets. Our marketing strategy is diversified and includes media relations, direct mail, conferences and client referrals. As of August 31, 2011, the Company was marketing and selling its products through its full time staff consisting of eleven people.

Direct Sales

We sell directly to the major operators in each of our target markets. Each of our target markets is dominated by a handful of large companies, and these companies comprise our primary customer base. In the small ticket beverage and food vending sector, approximately ten large operators dominate the sector; in the commercial laundry sector, seven operators currently control the majority of the market. We also work directly with hoteliers for our eTransAct® and Business Express® products.

Within the small ticket beverage and food vending industry, our customers include soft drink bottlers and independent vending operators throughout the United States and Canada. On the soft drink bottler side, we are attempting to secure additional distribution agreements and servicing our existing customer’s requirements for cashless locations and the related network services.

Indirect Sales/ Distribution

We have entered into agreements with resellers and distributors in connection with our energy management products. We also have agreements with select resellers in the car wash, amusement and gaming and vending markets in an effort of broaden our reach and subsidize direct sales efforts in these markets.

Marketing

Our marketing strategy consists of building our brand by creating a company and product presence at industry conferences and events in order to raise visibility within our industry, create opportunity to conduct product demonstrations, and consult with potential customers one-on-one; sponsoring educational workshops with trade associations such as National Automated Merchandiser Association (“NAMA”), to educate the industry on the importance and benefits of our solution and establish our position as the industry leader; develop several case studies to illustrate the value of our products; the use of direct mail campaigns; and advertising in vertically-oriented trade publications such as Vending Times,

Automatic Merchandiser and Energy User News.

12

IMPORTANT RELATIONSHIPS

AT&T Mobility

In November 2009, we signed an amendment to our existing agreement to use AT&T’s digital wireless wide area network for transport of data, including credit card transactions and inventory management data. The initial term of the amendment is three years, expiring November 2012. At the end of the initial term, the agreement automatically renews for successive one year terms unless terminated by either party. AT&T is a provider of advanced wireless voice and data services for consumers and businesses, operating the largest digital wireless network in North America and the fastest nationwide wireless data network in the United States. We offer AT&T’s wireless services in connection with our

ePort® devices which are utilized in the traditional small ticket beverage and food vending market in the United States.

Verizon Wireless

In April 2011, we signed an agreement to use Verizon’s digital wireless wide area network for transport of data, including credit card transactions and inventory management data. The initial term of the agreement is three years, expiring April 2014. At the end of the initial term, the agreement automatically renews for successive one month periods unless terminated by either party upon thirty day’s notice. Verizon Wireless operates the nation’s fastest, most advanced 4G network and largest, most reliable 3G network. The company serves 104 million total wireless connections, including more than 88 million retail customers. We offer Verizon’s wireless services in connection with our

ePort® devices which are utilized in the traditional small ticket beverage and food vending market in the United States.

On September 21, 2011, the Company and Verizon entered into a Joint Marketing Addendum (the “Verizon Agreement”) which amended the three year agreement described above. Pursuant to the Verizon Agreement, the Company and Verizon would work together to help identify business opportunities for the Company’s products and services. Verizon may introduce the Company to existing or potential Verizon customers that Verizon believes are potential purchasers of the Company’s products or services, and may attend sales calls with the Company made to these customers. The Company and Verizon would collaborate on marketing and communications materials that would be used by each of them to educate and

inform customers regarding their joint marketing work. Verizon has the right to list the Company’s products and services in its Data Solutions Guide for use by its sales and marketing employees and in its external website. The Company has agreed to pay to Verizon a one-time referral fee for each customer introduced to the Company by Verizon that would become a customer of the Company. The Verizon Agreement is terminable by either party upon 45 days notice after six months.

Crane Payment Solutions

In December 2010, Crane Payment Solutions (“Crane”), a business unit within the Merchandising Systems Segment of Crane Co. and the Company entered into a three-year Strategic Partnership Agreement to deliver a combined cashless vending solution to Crane customers in North America. Under the agreement, USA Technologies will become the lead provider and supplier of all card processing, wireless communications and data services for Crane’s customers in conjunction with the new Currenza® cashless bill validator card reader. In addition to the card processing capabilities of the Company, the Company will provide certain hardware solutions and grant Crane a license for designated USAT patents as a

part of the relationship.

VISA

On April 1, 2009 we entered into a Contactless Terminal Support Agreement with VISA U.S.A. INC. (“VISA”), pursuant to which VISA would pay us the amount of $200 for each ePort® that we deployed prior to December 31, 2009. The agreement covered up to a maximum of 4,000 ePorts®. These ePorts® would accept credit and debit cards utilizing VISA’s contactless technology as well as VISA’s magnetic stripe payment cards. In June 2009, the agreement was amended to provide funding for up to an additional 2,500

ePorts® which may be installed on vending machines owned by The Compass Group. VISA would pay us an aggregate of $800,000 if all 4,000 ePorts® were timely deployed. Our customer (i.e., the location owner) would enter into a three-year exclusive processing agreement with us in connection with the vending machine utilizing the ePort®. The Company deployed a total of 2,961 units, or $592,200, under this agreement during the period of July 1, 2009 through December 31, 2009.

On August 16, 2010, we entered into an Acceptance and Promotional Agreement with VISA. Pursuant to the agreement, VISA agreed, among other things, to pay to the Company up to $250,000 per year, for total payments of up to $750,000. The payments to the Company are to be used by the Company over the three year term of the agreement to support and promote the installation and deployment of at least 50,000 additional ePort®, or other payment terminals, in vending machines. If the Company does not install at least 50,000 ePorts®, or other payment terminals, over the term of the three year agreement, the Company would be required to refund a pro-rata portion of the funds. Through June 30, 2011, we have

installed and made operational approximately 33,000 units under this agreement.

Compass/Foodbuy

On June 30, 2009, we entered into a Master Purchase Agreement (“MPA”) with Foodbuy, LLC (“Foodbuy”), the procurement company for Compass Group USA, Inc. (“Compass”) and other customers. As per its website, Compass is a $9.9 billion organization with locations throughout the US, Mexico, and Canada, is the leader in vending, foodservice management and support services, is the largest national vending operating company, operating 200 branches, has 18,000 locations, and is one of the leading owners and operators of vending machines in the United States. Compass is a division of UK-based Compass Group PLC.

The MPA provides, among other things, that for a period of thirty-six months, Foodbuy on behalf of Compass shall utilize USAT as the sole credit or debit card vending system hardware and related software and connect services provider for not less than seventy-five percent of the vending machines of Compass utilizing cashless payments solutions. The MPA also provides that for a period of thirty-six months, USAT shall be a preferred supplier and provider to Foodbuy and its customers, including Compass, of USAT’s products and services. The MPA provides for initial pricing for the ePort hardware and monthly service and DEX telemetry fees at USAT’s standard pricing. Foodbuy’s customers have the right

under the MPA to acquire USAT’s G-8 or Edge ePort devices through USAT’s Quick Start Program. The MPA also provides for the ability of the customer to obtain DEX telemetry services from USAT in connection with vending machines utilizing the ePort devices.

13

On July 1, 2009, USAT and Compass, in conjunction with the MPA described above, entered into a Quick Start Master Lease Agreement pursuant to which Compass could purchase USAT’s G-8 or Edge ePort devices utilizing USAT’s Quick Start Program. The Quick Start Program enables Compass to acquire USAT’s ePort through a 36 month non-cancellable lease. Under the Quick Start Program, Compass will pay USAT a monthly amount, per terminal, that includes the lease of the ePort hardware and activation fee. The total monthly payment due under the Quick Start Program would be deducted by USAT directly out of the gross revenues generated from the Compass vending machines. Compass would be able to utilize the

Quick Start Program to acquire ePorts during the three year term of the Master Purchase Agreement referred to above.

On July 1, 2009, USAT and Compass, in conjunction with the MPA described above, also entered into a new three year ePort Connect Services Agreement pursuant to which USAT will provide Compass with all card processing, data, network, communications and financial services, and DEX telemetry data services required in connection with all Compass vending machines utilizing ePorts.

Merit/AMI Entertainment

In October of 2008, we entered into an exclusive three-year agreement for the supply of ePort® devices and ePort Connect® cashless services with Merit Entertainment (“Merit”). Merit is the provider of Megatouch countertop entertainment systems and selected the ePort® software and ePort Connect® Services to help give Megatouch players the ability to pay with their debit or credit cards. Under this agreement every newly manufactured Megatouch system will

include our ePort Connect® software. Merit has indicated to us that it currently has an installed base of over 250,000 touch screen games.

JUMP START PROGRAM

In December 2009, the Company commenced a program for its customers referred to as the Jump Start Program (“Jump Start”). Pursuant to the Jump Start Program, the Company would continue to own the ePort device utilized by its customer. At the time of the shipment of the ePort device, the customer is obligated to pay to the Company the standard one-time activation fee, is obligated to pay monthly service fees in accordance with the terms of the customer's contract with the Company, and the Company receives transaction processing fees generated from the device. The Jump Start Program also includes the ePort Connect® services package for wireless connectivity, card processing, consumer

services, online reporting, and over-the-air machine alerts.

Because Jump Start is designed to help vending operators and bottlers acquire the ePort cashless terminal at no upfront cost, paying only a low monthly service fee, and avoiding the need to make a major upfront capital investment, the Company anticipates that the Jump Start Program will accelerate adoption in the marketplace of its ePort technology as well as increase its license and transaction fee revenues.

When the program was commenced, the Company anticipated that the Jump Start Program would consist of at least 15,000 ePort Edge devices. In May 2010, the Company expanded the program to include the ePort G8 terminal. In July 2010, the Company expanded the program to an aggregate of 35,000 ePort terminals and the program terminated in December 2010. During the Spring of 2011, the Company reintroduced the Jump Start Program and anticipates approximately 40,000 Jump Start units to be connected during the 2012 fiscal year.

MANUFACTURING

The Company utilizes independent third party companies for the manufacturing of its products. The Company purchases other components of its business center (computers, printers, fax and copy machines) through various manufacturers and resellers. Our manufacturing process mainly consists of quality assurance of materials and testing of finished goods received from our contract manufacturers. We have not entered into a long-term contract with our contract manufacturers, nor have we agreed to commit to purchase certain quantities of materials or finished goods beyond those submitted under routine purchase orders, typically covering short-term forecasts.

COMPETITION

The cashless vending, remote business service and energy conservation industries are competitive markets. While the Company offers unique products and services within smaller niche markets of these industries, a number of competitors in the broader market may offer products and services within our niche market in the future. In the cashless vending market, we are not aware of any direct competitor that provides a complete end-to-end solution, offering a cashless/remote monitoring device and turnkey service, which includes card processing services. We are aware of four competitors that offer a cashless hardware device, MEI, Coin Acceptors Inc. (Coinco), Cantaloupe Systems, Inc. and InOne Technology,

LLC. We are aware of four competitors that offer a remote monitoring device, MEI, Cantaloupe Systems, Inc, InOne Technology, LLC, and Crane Streamware. We are aware of one direct competitor that offers a wireless service for cashless processing, Apriva. In addition, there are numerous credit card processors that offer card processing services to traditional retail establishments that could decide to offer similar services to the industries that we serve.

14

In May 2010, NAMA, an association serving the vending, coffee service and foodservice management industries, announced a cashless vending program for their members. As described by NAMA on their website, the goal of the program is to enable NAMA members to offer their customers the convenience of cashless payments at a reasonable cost across small and large average transaction pricing in a variety of industry segments. They further describe the NAMA Cashless Solution program as a networked end-to-end solution that is hardware neutral, works with qualified communication suppliers and card associations for payment reconciliation and account management. In addition, NAMA states they are working to provide members

with a broad range of preferential financial services. This program includes one or more of the competitors to the Company referred to in the preceding paragraph.

In the cashless laundry market, we are aware of one direct competitor, Mac-Gray Corporation. In the automated business center market, we are aware of three direct competitors. In the energy management market, we are aware of one direct competitor for our Energy Miser products in the United States of America; and, we are aware of one competitor for energy management products in Europe. The businesses which have developed unattended, credit card activated control systems currently in use in non-vending machine applications (e.g., gasoline dispensing, public telephones, prepaid telephone cards and ticket dispensing machines), might be capable of

developing products or utilizing their existing products in direct competition with our ePort® control systems targeted to the vending industry. The Company is also aware of several businesses that make available use of the Internet and use of personal computers to hotel guests in their hotel rooms. Such services might compete with the Company’s Business Express, and the locations may not order the Business Express, or if ordered, the hotel guest may not use it. Finally, the production of highly efficient vending machines and glass front coolers or alternative energy conservation products may reduce or replace the need for our energy management products.

The Company’s key competitive factors include our unique products, our integrated services, product performance and price. In addition, it includes our ability to deliver these as a one-stop-shop, which we believe makes our technology easier to adopt and deploy for the operator. Our competitors are well established, have substantially greater resources than the Company and have established reputations for success in the development, sale and service of high quality products. Any increase in competition in the future may result in reduced sales and/or lower percentages of gross revenues being retained by the Company, or otherwise may reduce potential profits or result in a loss of some or all of its

customer base.

CUSTOMER CONCENTRATIONS

Financial instruments that subject the Company to a concentration of credit risk consist principally of cash and cash equivalents and accounts and finance receivables. The Company maintains cash and cash equivalents with various financial institutions. Approximately 22% and 52% of the Company’s accounts and finance receivables at June 30, 2011 and 2010, respectively, were concentrated with one and two (28% with one and 24% with another) customer(s), respectively. Approximately 48%, 52%, and 44% of the Company’s license and transaction processing revenues for the years ended June 30, 2011, 2010, and 2009, respectively, were concentrated with two (25% with one and 23% with another), two (35% with one and

17% with another), and one customer(s), respectively. There was no concentration of equipment sales revenue for the year ended June 30, 2011. For each of the years ended June 30, 2010 and 2009 approximately 11% of the Company’s equipment sales revenue was concentrated with one customer. The Company’s customers are principally located in the United States.

TRADEMARKS, PROPRIETARY INFORMATION AND PATENTS

The Company received federal registration approval of the following trademarks: Blue Light Sequence®, CM2iQ®, EnergyMiser®, ePort®, ePort Connect®, ePort Edge®, Intelligent Vending®, PC Express®, Public PC®, SnackMiser®, The Office That Never Sleeps®, TransAct®, USA Technologies & Design®, USALive®, VendingMiser®, and VM2iQ®. The Company has three trademarks pending registration, Pay Dot™, Creating Value Through Innovation™ and eSuds™.

Much of the technology developed or to be developed by the Company is subject to trade secret protection. To reduce the risk of loss of trade secret protection through disclosure, the Company has entered into confidentiality agreements with its key employees. There can be no assurance that the Company will be successful in maintaining such trade secret protection, that they will be recognized as trade secrets by a court of law, or that others will not capitalize on certain aspects of the Company’s technology.

Through June 30, 2011, 73 United States patents and 8 foreign patents have been issued to the Company, and 5 United States and 7 foreign patent applications are pending.

The list of issued patents that remain in force is as follows:

|

|

●

|

U.S. Patent No. 6,856,820 entitled “An in-vehicle device for wirelessly connecting a vehicle to the internet and for transacting e-commerce and e-business”;

|

|

|

●

|

U.S. Patent No. 5,844,808 entitled “Apparatus and methods for monitoring and communicating with a plurality of networked vending machines”;

|

15

|

|

●

|

U.S. Patent No. 7,690,495 entitled “Card reader assembly”;

|

|

|

●

|

U.S. Patent No. 7,076,329 entitled “Cashless vending transaction management by a Vend Assist mode of operation”;

|

|

|

●

|

U.S. Patent No. 7,464,867 entitled “Cashless vending transaction management by a Vend Assist mode of operation”;

|

|

|

●

|

U.S. Patent No. 7,131,575 C1 entitled “Cashless vending transaction management by a Vend Assist mode of operation”;

|

|

|

●

|

U.S. Patent No. 7,693,602 entitled “Cashless vending transaction management by a vend assist mode of operation”;

|

|

|

●

|

U.S. Patent No. 6,615,186 entitled “Communicating interactive digital content between vehicles and internet based data processing resources for the purpose of transacting e-commerce or conducting e-business”;

|

|

|

●

|

U.S. Patent No. 7,003,289 entitled “Communication interface device for managing wireless data transmission between a vehicle and the internet”;

|

|

|

●

|

Canadian Patent No. 2,207,603 entitled “Credit and debit card operated vending machine”;

|

|

|

●

|

U.S. Patent No. 5,637,845 entitled “Credit Card and Bank Issued Debit Card Operated System and Method for Controlling a Prepaid Card Encoding/Dispensing Machine”;

|

|

|

●

|

U.S. Patent No. 6,119,934 entitled “Credit Card and Bank Issued Debit Card Operated System and Method for Controlling a Prepaid Card Encoding/Dispensing Machine”;

|

|

|

●

|