Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FNB CORP/PA/ | d231668d8k.htm |

Second Quarter 2011

Investor Presentation

Dated: September 13, 2011

Exhibit 99.1

F.N.B. Corporation |

Forward-Looking Statements

This presentation and the reports F.N.B. Corporation files with the Securities and

Exchange Commission often

contain

“forward-looking

statements”

relating

to

present

or

future

trends

or

factors

affecting

the

banking industry and, specifically, the financial operations, markets and products

of F.N.B. Corporation. These forward-looking statements involve certain

risks and uncertainties. There are a number of important factors that could

cause F.N.B. Corporation’s future results to differ materially from historical performance or

projected performance. These factors include, but are not limited to: (1) a

significant increase in competitive pressures among financial institutions;

(2) changes in the interest rate environment that may reduce interest

margins; (3) changes in prepayment speeds, loan sale volumes, charge-offs and

loan loss provisions; (4) general economic conditions; (5) various monetary

and fiscal policies and regulations of the U.S. government that may

adversely affect the businesses in which F.N.B. Corporation is engaged; (6)

technological issues which may adversely affect F.N.B. Corporation’s financial

operations or customers; (7) changes

in

the

securities

markets;

(8)

risk

factors

mentioned

in

the

reports

and

registration

statements

F.N.B. Corporation files with the Securities and Exchange Commission; (9) housing

prices; (10) job market; (11) consumer confidence and spending habits; (12)

estimates of fair value of certain F.N.B. Corporation assets and liabilities

or (13) the effects of current, pending and future legislation, regulation and regulatory

actions. F.N.B. Corporation undertakes no obligation to revise these

forward-looking statements or to reflect events or circumstances after

the date of this presentation. 2 |

Forward-Looking Statements

3

ADDITIONAL

INFORMATION

ABOUT

THE

MERGER

F.N.B. Corporation and Parkvale Financial Corporation will file a proxy

statement/prospectus and other relevant documents with the SEC in connection

with the merger. SHAREHOLDERS OF PARKVALE FINANCIAL CORPORATION ARE ADVISED

TO READ THE PROXY STATEMENT/PROSPECTUS WHEN IT BECOMES AVAILABLE AND ANY

OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR

SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT

INFORMATION. The proxy statement/prospectus and other relevant materials

(when they become available), and any other documents F.N.B. Corporation has

filed with the SEC, may be obtained free of charge at the SEC's website at

www.sec.gov.

In

addition,

investors

and

security

holders

may

obtain

free

copies

of

the

documents

F.N.B.

Corporation has filed with the SEC by contacting James Orie, Chief Legal Officer,

F.N.B. Corporation, One F.N.B. Boulevard, Hermitage, PA 16148, telephone:

(724) 983-3317 or Parkvale Financial Corporation by contacting Gilbert

A. Riazzi, Chief Financial Officer, 4220 William Penn Highway, Monroeville, PA 15146,

telephone: (412) 373-4804.

Parkvale Financial Corporation and its directors, executive officers and other

members of its management and employees may be deemed to be participants in

the solicitation of proxies from its shareholders in connection

with

the

proposed

merger.

Information

concerning

such

participants'

ownership

of

Parkvale

Financial

Corporation

common

stock

will

be

set

forth

in

the

proxy

statement/prospectus

relating

to

the

merger

when it becomes available. This communication does not constitute an offer of any

securities for sale. |

Non-GAAP Financial Information

4

To supplement its consolidated financial statements presented in accordance with Generally Accepted

Accounting Principles (GAAP), the Corporation provides additional measures of operating

results, net income and earnings per share (EPS) adjusted to exclude certain costs, expenses,

and gains and losses. The Corporation believes that these non-GAAP financial measures

are appropriate to enhance the understanding of its past performance as well as prospects for

its future performance. In the event of such a disclosure or release, the Securities and

Exchange Commission’s Regulation G requires: (i) the presentation of the most directly

comparable financial measure calculated and presented in accordance with GAAP and (ii) a

reconciliation of the differences between the non-GAAP financial measure presented and the most

directly comparable financial measure calculated and presented in accordance with GAAP. The

required presentations and reconciliations are contained herein and can be found at our

website, www.fnbcorporation.com, under “Shareholder and Investor Relations” by

clicking on “Non-GAAP Reconciliation.”

The Appendix to this presentation contains non-GAAP financial measures used by the Corporation to

provid information useful to investors in understanding the Corporation's operating performance

and trends, and facilitate comparisons with the performance of the Corporation's peers.

While the Corporation believes that these non-GAAP financial measures are useful in

evaluating the Corporation, the information should be considered supplemental in nature and not

as a substitute for or superior to the relevant financial information prepared in accordance

with GAAP. The non-GAAP financial measures used by the Corporation may differ from

the non-GAAP financial measures other financial institutions use to measure their results of operations.

This information should be reviewed in conjunction with the Corporation’s financial results

disclosed on July 25, 2011 and in its periodic filings with the Securities and Exchange

Commission. |

F.N.B.

Corporation Headquarters: Hermitage,

PA

Bank Charter: 1864

Assets: $9.9B (4th largest bank in PA)

Market Capitalization: $1.1B at August 31, 2011

Current Locations

234 Banking: 223 (PA), 11 (OH)

65 Consumer Finance: 22 (PA), 19 (TN), 17 (OH), 7 (KY)

Business Lines

Banking

Wealth Management

Insurance

Consumer Finance

Merchant Banking

5 |

Experienced Management Team

Name

Position

Years of

Banking

Experience

Steve Gurgovits

Chief Executive Officer

50

Vince Delie

President

CEO, First National Bank of PA

24

Brian Lilly

Chief Operating Officer

Vice Chairman

30

Vince Calabrese

Chief Financial Officer

23

Gary Guerrieri

Chief Credit Officer

24

6 |

Board

Leadership Thirteen Independent Directors

Seven Former Financial Services Executives

Three Involved as Financial Services Investors

7 |

Manage

our business for profitability and growth Operate in markets we know and

understand Maintain a low-risk profile

Drive growth through relationship banking

Fund loan growth through deposits

Target neutral asset / liability position to manage interest rate risk

Build fee income sources

Maintain rigid expense controls

Operating Strategy

8 |

Market

Characteristics Stable Markets

Modest Growth

#2 Ranking State College

(1)

#3 Ranking Pittsburgh

(1)

Regional Management

Local Advisory Boards

Marcellus Shale Exposure

FNB

Region

Market

Size

Deposits

FNB

Deposit

Ranking

FNB

Branches

Pittsburgh

$76.4B

3

rd

114

Northwest

$25.5B

3

rd

54

Capital

$45.8B

10

th

42

Central

Mountain

$11.8B

1

st

71

Source: SNL, company data; based on June 30, 2010 deposit data,

excludes custodian bank, pro-forma ownership as of September 1,

2011.

(1)

MSA

9 |

Banking Locations

Current First National Bank Locations

As of September 1, 2011

10 |

Organic Growth Opportunity

Source: SNL Financial

Deposit data as of June 30, 2010; excludes custodian bank, pro-forma

ownership as of September 1, 2011. Attractive market rank of #3 for counties

of operation 11

Rank

Institution

Branch

Count

Total Deposits in

Market ($000)

Total Market

Share (%)

1

PNC Financial Services Group Inc.

347

45,417,165

29.71

2

Royal Bank of Scotland Group Plc

228

10,374,299

6.79

3

F.N.B. Corp.

281

8,639,847

5.65

4

M&T Bank Corp.

137

6,196,246

4.05

5

Huntington Bancshares Inc.

127

5,769,478

3.77

6

Wells Fargo & Co.

64

4,942,063

3.23

7

First Commonwealth Financial Corp.

101

4,164,090

2.72

8

Banco Santander SA

75

3,755,597

2.46

9

First Niagara Financial Group Inc.

70

3,562,975

2.33

10

Susquehanna Bancshares Inc.

85

3,387,912

2.22

Total (1-165)

2,863

152,854,759

100.00

Counties of Operation |

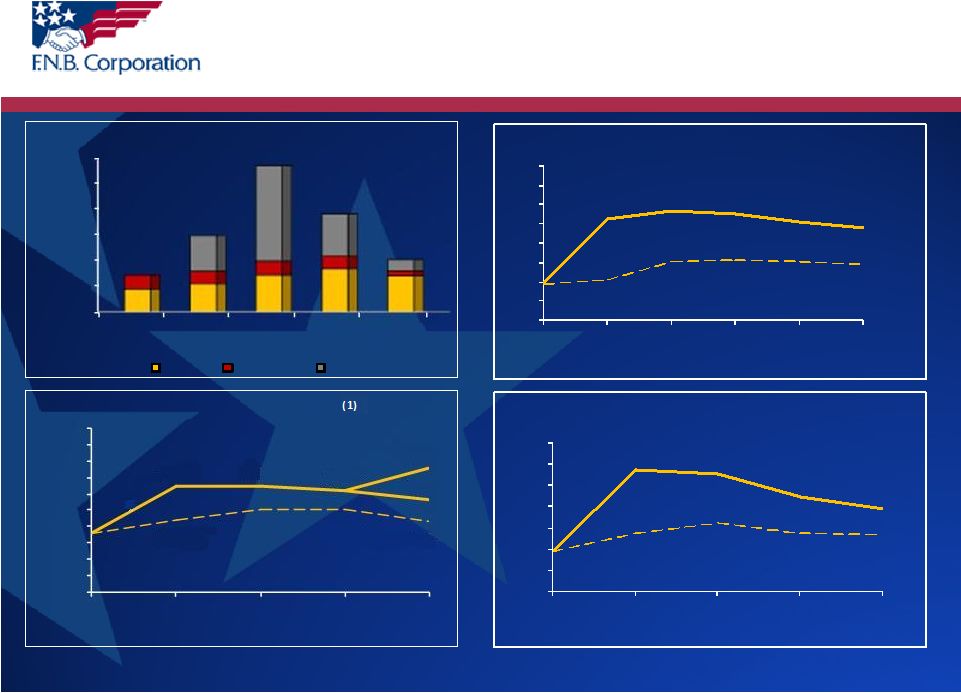

Winning Market Share

Total Organic Loan Growth

(1)

Eighth Consecutive Quarter of Organic Growth

(1) Based on average balances; percentage organic growth annualized and as

compared to the prior quarter. 12 |

Winning Market Share

Second

Quarter

2011

Ninth consecutive linked-

quarter organic growth for

Pennsylvania commercial

loans

(2)

Pennsylvania commercial loan

organic

growth

of

8.7%

(1)

(2)

Commercial line utilization

rates remain historically low

Commercial Organic Loan Growth

(1)

(1)

Based on average balances; percentage organic growth annualized and as compared to

the prior quarter. (2)

Pennsylvania commercial portfolio organic loan growth, excludes Florida.

13

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2Q11

1Q11

4Q10

3Q10

2Q10

8.7%

10.7%

2.5%

0.6%

4.7%

7.4%

8.3%

0.1%

-1.1%

3.6%

Pennsylvania Commercial Growth

Total Commercial Growth |

Winning Market Share

Transaction Deposit and Customer Repurchase Agreements

Organic Growth

(1)

(1) Based on average balances; percentage organic growth annualized and as

compared to the prior quarter; transaction deposits includes DDA, Savings,

NOW and MMDA. 14 |

Loan

Composition Based on average balances for each period presented.

15

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

$6.0

$6.5

$7.0

2007

2008

2009

2010

2Q11

Other

Commercial Leases

Regency

Indirect

Residential Mortgage

Consumer Home Equity

Commercial |

Funding

Based on average balances for each period presented.

Loans to deposits and

customer repurchase

agreements ratio of 84%

Deposits and Customer

Repurchase Agreements –

$8.0 Billion at June 30, 2011

16

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

2007

2008

2009

2010

2Q11

Transaction Deposits and Customer Repos

Time Deposits

Total Borrowings

Trust Preferred

Customer

Repos

9%

Time Deposits

28%

DDA

16%

Savings, NOW,

MMDA

47% |

Proven Merger Integrator |

Proven

Merger Integrator Proven significant

acquisition

and

integration

experience

-

since

2002,

completed eight

bank acquisitions ($6.1 billion in assets), four insurance acquisitions and one

consumer finance

acquisition.

Pending

-

acquisition

of

Parkvale

Financial

($1.8

billion

in

assets)

announced June 15, 2011.

Significant

acquisition

opportunities

exist

in

Pennsylvania

-

currently

over 50

Pennsylvania

headquartered

institutions

with

assets

between

$300

million

and

$3

billion

(1)

.

Pre-2002 Presence

Acquisition Related Expansion

(1)

Source:

SNL:

Includes

all

banks

and

thrifts

headquartered

in

PA,

excludes

mutuals

and

MHCs.

18 |

Well

Diversified Business F.N.B.

F.N.B.

Corporation

Corporation

Banking

Banking

Wealth

Wealth

Management

Management

Merchant

Merchant

Banking

Banking

Consumer

Consumer

Finance

Finance

Insurance

Insurance |

Regency

Finance Company Over 80 years of consumer lending experience

65 Offices –

9 opened since October, 2010

High-Performing Affiliate

•

2Q2011

YTD

ROTCE

31.80%

(1)

•

2Q2011 YTD ROA 2.74%

•

2Q2011 ROE 28.31%

Consumer Finance

(1)

Return on average tangible common equity (ROTCE) is calculated by dividing net

income less amortization of intangibles by average common equity less

average intangibles. Pennsylvania

Ohio

Ohio

Kentucky

20

Tennessee |

Regency

Finance

Company

Loan

Portfolio

$163

Million

87% of Real Estate Loans are First Mortgages

12%

32%

56%

As of June 30, 2011

Consumer Finance

21 |

Insurance

Property, Casualty, Life and

Employee Benefits

Risk Management, Risk Transfer

and Cost Containment Services

Seven offices, located in Central

and Western PA

80% Commercial; 20% Personal

•

78% Property and Casualty

•

22% Life and Benefits

Annual premiums of $97 Million

Wealth Management and Insurance

Wealth

Management

Trust, Fiduciary and Institutional

Investment Services

•

Over 70 Years Managing Wealth

•

$2.4 Billion Under Administration

at June 30, 2011

Individual Investment Services

•

Brokerage, Mutual Funds and

Annuities

•

Life and Long-Term Care

Insurance Planning

22 |

Merchant Banking

Junior capital provider offering flexible financing solutions

•Mezzanine debt, subordinated notes, equity capital

•Growth or expansion capital, buyouts and ownership

transition financing

•No early stage or real estate financing

•Typical investment between $1 million and $7 million

Total outstandings of $22 million as of June 30, 2011

Successfully harvested two relationships in 2010 contributing

$2.3 million to fee revenue

Founded in 2005

23 |

Parkvale Financial Corporation

Transaction Highlights

Announce Date: June 15, 2011 |

Strengthens FNB’s

Leading Pittsburgh

Position

Solidifies FNB’s leading status in the Pittsburgh market

–

Pittsburgh MSA market rank moves significantly from #7 to #3

Significantly enhances distribution capabilities and scale

One of few meaningful opportunities left in the market

Low Execution Risk

In-market transaction

Leverages experienced Pittsburgh-market management team

FNB is a proven merger integrator –

completed eight bank

acquisitions since 2002 ($6.1 billion in assets)

Financially

Attractive

Effective deployment of capital

–

EPS accretion of 6%

–

IRR

20%

Significant operating efficiencies –

35% cost savings

Neutral to tangible book value per share, after recent capital raise

–

Accretive to March 31, 2011 tangible book value per share

(pre-capital raise)

Parkvale Financial

Compelling Strategic Rationale

25 |

Leadership Position

Pittsburgh MSA

Strong # 3 pro forma market share

position (FNB currently #7)

(1)

#1 community bank in the market

Leverages existing strengths to build on

momentum in market

FNB/Parkvale branch overlap –

19

branches, or 40%, within 1 mile

26

Source: SNL Financial.

(1) Excludes custodian banks.

Pennsylvania

Parkvale Financial (47 branches)

F.N.B. (234 branches)

Beaver

Butler

Westmoreland

Armstrong

Fayette

Washington

Allegheny

•

Parkvale Financial (40 branches)

•

F.N.B. (61 branches)

Pittsburgh

Pittsburgh MSA

•

• |

Total

Foreclosures, First Quarter – 2011

Attractive Pittsburgh Market

Source: PittsburghTODAY.org derived from Bureau of Labor Statistics, RealtyTrac and

FHFA. 27

Source: SBA firms and employment by MSA 2008, Census.gov.

0

500

1,000

1,500

2,000

500+ Employees Middle Market and

Corporate

Pittsburgh MSA

Pennsylvania MSA

Average

National MSA Average

Pittsburgh Commercial Market –

Continued Opportunity

Pittsburgh MSA Economic Indicators

Third Best %

Job Growth

% Change in Jobs, July 2010 –

July 2011

Total Nonfarm

#1 Housing

Appreciation

1 Year Appreciation Rates

4th Quarter 2010

Second Lowest First

Quarter 2011 Total

Foreclosures

10,000

20,000

30,000

40,000

50,000

<20 Employees Small Businesses

<500 Employees Businesses |

Transaction Overview

Consideration:

$22.48

(1)

per Parkvale Financial share

Fixed 2.178x exchange ratio

100% stock

Deal Value:

Approximately

$130

million

(1)

Detailed Due

Diligence:

Completed

Required Approvals:

Customary regulatory and Parkvale shareholders

Expected Closing:

Early January 2012

TARP Repayment:

Parkvale intends to redeem its $32 million of TARP prior to closing,

subject to Treasury approval.

Board Seats:

Robert J. McCarthy, Jr. will join the Board of Directors of F.N.B.

Corporation, and one Parkvale board member, as mutually agreed, will

become a director of First National Bank of Pennsylvania.

(1)

Based

on

FNB

stock

price

as

of

announcement

date,

Wednesday,

June

15,

2011,

$10.32.

28 |

Pennsylvania Marcellus Shale |

Pennsylvania Marcellus Shale

PA Marcellus Shale Formation

(3)

Sources: (1) “The Pennsylvania Marcellus Natural Gas Industry: Status,

Economic Impacts and Future Potential”, July 20, 2011, Penn

State; (2) “Banking on the Marcellus”, June 7, 2010, Sterne Agee Industry Report; (3) MarcellusCoalition.org

Fully developed -

Marcellus Shale has potential to

be the second largest natural gas field in the

world.

(1)

Estimated/projected Pennsylvania jobs

(1):

•

2020, cumulative, respectively

FNB screened as second best positioned in

Pennsylvania based on overlap of market share,

drilling permits issued and wells being dug.

(2)

PA Marcellus Drilling Permits

F.N.B. Banking Locations

30

60,000, 157,000 and 256,000 - 2009, 2011 and

|

Surveyors

Real Estate

Rocks and

Quarries

Utilities

Oil and Gas

(Direct Effect)

Drilling, Extraction,

Support Activities

Indirect Impact

(Supply Chain Effect)

Heavy

Equipment

Commodity

Traders

Other Gas

Distribution

Iron and

Steel

Construction

Pipelines

Machinery

Manufacturers

Gas

Processors

Rig Parts

Cement

Induced Impact

(Consumption Effect)

Food and

drink

Utilities

Travel

Higher

Education

Housing

Entertainment

Attorneys

Marcellus Shale Effect

31 |

2011

2015

2020

Economic Value:

$12.8 Billion

$17.2 Billion

$20.2 Billion

State/Local Taxes:

$1.2 Billion

$1.7 Billion

$2.0 Billion

Total Jobs:

156,695

215,979

256,420

Pennsylvania Marcellus Shale

The Future: Economic Opportunity

2011 Status, Economic Impacts and Future Potential

Source: “The Pennsylvania Marcellus Shale Natural Gas Industry:

Status, Economic Impacts and Future Potential “, July 20, 2011, Penn

State 32 |

LOAN

COMPOSITION &

CREDIT QUALITY |

Diversified Loan Portfolio

$6.7 Billion Outstanding as of June 30, 2011

Shared National Credits

•

3.6%

of

total

loan

portfolio

•

In-market customers and

prospects

Avoided subprime and Alt-A

mortgages

Construction and land

development total only 3.4%

and 0.7%, respectively, of

FNB’s total loan

portfolio 34 |

Commercial Real Estate Portfolio

$1.2 Billion in CRE Non-Owner Occupied

as of June 30, 2011 (excluding Florida)

Diverse Portfolio

Solid Credit Quality Results

•

2.20% Total delinquency

•

1.84% Non-performing

loans + OREO/Total loans

+ OREO

35 |

Credit

Quality (1)

2.02% when including credit mark in both reserve for loan losses and total

loans, refer to non-GAAP reconciliation in Appendix

2.62%

2.84%

2.74%

2.54%

2.42%

0.94%

1.06%

1.51%

1.56%

1.51%

1.44%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2007

2008

2009

2010

1Q11

2Q11

Dashed Line Excludes Florida

NPL's and OREO % of Total Loans and OREO

3.38%

3.28%

2.76%

2.46%

1.47%

1.87%

2.14%

1.87%

1.84%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2007

2008

2009

2010

2Q11

Dashed Line Excludes Florida

Total Past Due & Non-Accrual Loans

% of Total Loans

36

1.22%

1.80%

1.79%

1.74%

1.63%

1.38%

1.51%

1.50%

1.37%

2.02%

0.5%

0.7%

0.9%

1.1%

1.3%

1.5%

1.7%

1.9%

2.1%

2.3%

2.5%

2007

2008

2009

2010

2Q11

Dashed Line Excludes Florida

Reserves % of Total Loans

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

2007

2008

2009

2010

2Q11

YTD

NCO's % of Total Average Loans

Bank

Regency

Florida |

Florida Focus:

Land-Related Exposure

Florida Land-Related Exposure

•

Loans of $53 million represent under

1% of total loan portfolio

•

OREO of $21 million

•

Year-over-year exposure reduction of

$24 million, or 25%

Total Florida Portfolio

•

Loans of $180 million represent only

2.7% of total loan portfolio

•

Year-over-year exposure reduction of

$39 million, or 16%

Florida

Land-Related Exposure

Composition

(1)

Exposure refers to period-end loans plus OREO

37

$74 Million in Florida Land-Related Exposure as of June 30, 2011

(1) |

FINANCIALS |

Investment

Ratings By

Investment -

%

Amount

(1)

(in $ millions)

Agency

–

MBS

AAA

$999

Agency -

Senior Notes

AAA

$338

CMO

–

Agency

AAA

$250

Municipals

AAA

–

2%

AA

–

93%

A

–

5%

$198

CMO

–

Private

Label

AAA

–

30%

AA

–

9%

A

-

4%

BBB

–

20%

CCC

–

36%

$28

Short-Term

AAA

$17

Trust

Preferred

(2)

BBB

–

26%

BB

–

22%

B

–

12%

C

–

40%

$17

Bank Stocks

Non-Rated

$2

Total

$1,849

% of Total $1.8 Billion Portfolio

Earning Assets -

Investments

(1) Amounts shown reflect GAAP

(2) Original cost of $48 million; adjusted cost of $30

million; fair value of $16 million

Investment Portfolio Ratings as of June 30, 2011

39 |

Solid

Financial Results

EPS of $0.18 per diluted share

Seventh consecutive quarter of revenue growth

Eighth consecutive quarter of total loan growth

Continued strong transaction deposits and customer repo growth

Continued good credit quality results

Parkvale Financial

Announcement

Effective deployment of capital

–

EPS accretion of 6%

–

IRR

20%

Solidifies FNB’s leading status in the Pittsburgh market

Completed

Common Stock

Offering

$63 million net proceeds

Attractive price of $10.70

Completed in conjunction with FNB inclusion in the S&P 600

Second Quarter Highlights

40 |

Second

Quarter Results (1)

Calculated by dividing net income less amortization of intangibles by average

common equity less average intangibles. (2)

Calculated by dividing net income less amortization of intangibles by average

assets less average intangibles. (3)

Annualized linked-quarter organic growth data, based on average balances.

41

* 1Q11 amounts adjusted for one-time merger costs, refer to non-GAAP

reconciliation included in Appendix 2Q11

1Q11

2Q10

Profitability

Earnings per Common Share*

0.18

$

0.16

$

0.16

$

Return on Tangible Equity

(1)

*

16.77%

15.97%

15.65%

Return on Tangible Assets

(2)

*

1.02%

0.94%

0.92%

Operating

Loan Growth

(3)

5.1%

5.5%

3.3%

Total Deposit and

Customer Repurchase Agreements Growth

(3)

6.3%

1.0%

9.2%

Transaction Deposits and

Customer Repurchase Agreements Growth

(3)

10.7%

4.3%

13.7%

Net Interest Margin

3.78%

3.81%

3.81%

Efficiency Ratio

60.54%

63.72%

60.45% |

Stable

Net Interest Margin Source: SNL Financial

Regional peers include: CBCR, CBCYB, CBSH, CBU, CHFC, CRBC, CSE,

FCF, FFBC, FINN, FMBI, FMER, FRME,

FULT, MBFI, NBTB, NPBC, ONB, PRK, PVTB, SBNY, SRCE, STBA, SUSQ, TAYC, TCB,

UBSI, UMBF, VLY, WSBC, and WTFC

42 |

Fee

Income Excludes securities gains.

43

-$20

-$10

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

2007

2008

2009

2010

2Q10

YTD

2Q11

YTD

Gain-Sale of Residential Mtg Loans

Bank-Owned Life Insurance

Securities Commissions and Fees

Other

Trust Fees

Insurance Commissions and Fees

Service Charges

OTTI Charges

2Q11 YTD Fee Income as Percentage of Operating Revenue -- 27% |

Well

Capitalized Capital ratios at June 30, 2011 reflect the offering completed

May 18, 2011 of 6.0 million shares of common stock with net proceeds of $63

million. 44

4%

6%

8%

10%

12%

14%

Total Risk-Based

Tier One

Leverage

Tangible Common

Equity

December 31, 2010

March 31, 2011

June 30, 2011

Regulatory “Well Capitalized”

Threshold |

INVESTMENT THESIS |

Long-Term Investment Thesis

Targeted EPS Growth

5-6%

Expected Dividend Yield

(Payout Ratio 60-70%)

4-6%

= Total Shareholder Return

9-12%

46 |

(1)

Based on August 31, 2011 closing prices (F.N.B.=$8.97)

(2)

Represents total common equity less intangibles

Relative Valuation Multiples

47

F.N.B.

Corporation

Regional

Banks

National

Banks

Price

(1)

/Earnings Ratio

FY11 Consensus EPS (F.N.B.=$0.69)

13.00x

14.03x

13.81x

FY12 Consensus EPS (F.N.B.=$0.85)

10.55x

11.37x

11.40x

Price

(1)

-to-Tangible Common Book Value

(2)

1.90x

1.28x

1.26x

Dividend Yield

(1)

5.35%

2.01%

1.96%

Peer Median |

Summary

Leading market share among community banks in

Central and Western PA

Executing organic growth strategy and capitalizing

on opportunities presented in markets of operation

Experienced management team with proven ability

to integrate acquisitions

Diversified revenue stream

48 |

APPENDIX

Loan Risk Profile

Established Board of Directors

GAAP to Non-GAAP Reconciliations

Second Quarter 2011 Earnings Release (July 25, 2011) |

Loan

Risk Profile Appendix

Balance

(1)

% of

Loans

YTD Net

Charge-

Offs/Loans

(2)

Total Past

Due / Loans

NPL/Loans

CRE Owner Occupied

1,294,489

19%

0.18%

3.03%

2.13%

CRE Non-Owner Occupied

1,189,744

18%

0.38%

2.20%

1.48%

Commercial & Industrial

1,111,311

17%

0.37%

0.99%

0.78%

Home Equity & Other Consumer

1,486,879

22%

0.31%

0.90%

0.79%

Residential Mortgage

623,926

9%

0.02%

2.56%

1.39%

Indirect Consumer

519,550

8%

0.42%

1.00%

0.17%

Florida

180,232

3%

1.44%

24.92%

24.91%

Regency Finance

163,150

2%

3.76%

3.62%

3.95%

Other

133,314

2%

0.88%

1.65%

0.56%

Total

6,702,595

100.0%

0.42%

2.46%

1.90%

(1) Period end balances, in $ millions

(2) Annualized

Loan Risk Profile as of June 30, 2011 |

Director

Name

Age

Since

Biography

Stephen J. Gurgovits

68

1981

President and Chief Executive Officer

William B. Campbell

73

1975

Chairman of the Board

Henry M. Ekker

72

1994

Partner with Ekker, Kuster, McConnell & Epstein, LLP

Philip E. Gingerich

74

2008

Director of Omega from 1994 to 2008; Retired Real Estate

Appraiser and Consultant

Robert B. Goldstein

71

2003

Principal of CapGen Financial Advisors LLC since 2007;

Former Chairman of Bay View Capital

Dawne S. Hickton

53

2006

Vice Chairman and CEO of RTI International Metals, Inc. since

2007

David J. Malone

57

2005

President and CEO of Gateway Financial since 2004

D. Stephen Martz

69

2008

Former Director, President and COO of Omega

Harry F. Radcliffe

60

2002

Investment Manager

Arthur J. Rooney II

58

2006

President, Pittsburgh Steelers Sports, Inc.; of Counsel with

Buchanan, Ingersoll & Rooney LLP

John W. Rose

62

2003

Principal of CapGen Financial Advisors LLC since 2007;

President of McAllen Capital Partners, Inc. since 1991

Stanton R. Sheetz

56

2008

CEO and Director of Sheetz, Inc.; Director of Omega from 1994

to 2008; Director of Quaker Steak and Lube Restaurant, Inc

William J. Strimbu

50

1995

President of Nick Strimbu, Inc. since 1994

Earl K. Wahl, Jr.

70

2002

Owner, J.E.D. Corporation

Appendix

Established Board of Directors |

GAAP

to Non-GAAP Reconciliation Appendix

2011

2010

Second

First

Second

Quarter

Quarter

Quarter

Return on average tangible equity (1):

Net income (annualized)

$89,695

$69,653

$71,886

Amortization of intangibles, net of tax (annualized)

4,707

4,734

4,376

94,402

74,387

76,262

Average total shareholders' equity

1,166,305

1,129,622

1,052,569

Less: Average intangibles

(603,552)

(595,436)

(565,294)

562,753

534,186

487,275

Return on average tangible equity (1)

16.77%

13.93%

15.65%

Return on average tangible assets (2):

Net income (annualized)

$89,695

$69,653

$71,886

Amortization of intangibles, net of tax (annualized)

4,707

4,734

4,376

94,402

74,387

76,262

Average total assets

9,866,025

9,695,015

8,874,430

Less: Average intangibles

(603,552)

(595,436)

(565,294)

9,262,473

9,099,579

8,309,136

Return on average tangible assets (2)

1.02%

0.82%

0.92% |

GAAP

to Non-GAAP Reconciliation Appendix

2011

2010

Second

First

Second

Quarter

Quarter

Quarter

Tangible book value per share:

Total shareholders' equity

$1,203,150

$1,128,414

$1,058,004

Less: intangibles

(601,958)

(601,475)

(564,495)

601,192

526,939

493,509

Ending shares outstanding

127,024,899

120,871,383

114,532,890

Tangible book value per share

$4.73

$4.36

$4.31

Tangible equity / tangible assets (period end):

Total shareholders' equity

$1,203,150

$1,128,414

$1,058,004

Less: intangibles

(601,958)

(601,475)

(564,495)

601,192

526,939

493,509

Total assets

9,857,163

9,755,281

8,833,060

Less: intangibles

(601,958)

(601,475)

(564,495)

9,255,205

9,153,806

8,268,565

Tangible equity / tangible assets (period end)

6.50%

5.76%

5.97% |

GAAP

to Non-GAAP Reconciliation Appendix

2011

Second

First

Quarter

Quarter

Allowance for loan losses + credit marks / total

loans + credit marks:

Allowance for loan losses

$109,224

$107,612

Credit marks

26,622

26,919

135,846

134,531

Total loans

6,702,595

6,559,952

Credit marks

26,622

26,919

6,729,217

6,586,871

Allowance for loan losses + credit marks / total

loans + credit marks

2.02%

2.04%

(1) Return on average tangible equity is calculated by dividing net income less

amortization of intangibles by average equity less average

intangibles. (2) Return on average tangible assets is calculated by dividing

net income less amortization of intangibles by average assets less average

intangibles. |

GAAP

to Non-GAAP Reconciliation Appendix

2011

2011

First

First

Quarter

Quarter

Adjusted

net

income:

Adjusted

return

on

average

tangible

equity

(1):

Net income

$17,175

Adjusted net income (annualized)

$80,582

Merger-related costs, net of tax

2,695

Amortization of intangibles, net of tax (annualized)

4,734

Less: Pension credit, net of tax

0

85,317

Adjusted net income

$19,870

Average total shareholders' equity

1,129,622

Adjusted

diluted

earnings

per

share:

Less: Average intangibles

(595,436)

Diluted earnings per share

$0.14

534,186

Effect of merger-related costs, net of tax

0.02

Adjusted return on average tangible equity (1)

15.97%

Less: Effect of pension credit, net of tax

0.00

Adjusted diluted earnings per share

$0.16

Adjusted

return

on

average

tangible

assets

(2):

Adjusted net income (annualized)

$80,582

Amortization of intangibles, net of tax (annualized)

4,734

85,317

Average total assets

9,695,015

Less: Average intangibles

(595,436)

9,099,579

Adjusted return on average tangible assets (2)

0.94%

(1) Return on average tangible equity is calculated by dividing net income less

amortization of intangibles by average equity less average intangibles. (2)

Return on average tangible assets is calculated by dividing net income less amortization of intangibles by average assets less average intangibles. |