Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF

THE

SECURITIES EXCHANGE ACT OF 1934

August 30, 2011

Date of Report (Date of

earliest event reported)

XCELMOBILITY INC.

(Exact Name of Registrant as Specified in Charter)

| Nevada | 000-54333 | 98-0561888 |

| (State or Other Jurisdiction of Incorporation) | (Commission File Number) | (IRS Employer Identification No.) |

303 Twin Dolphins Drive, Suite 600

Redwood

City, CA 94065

(Address of Principal Executive Offices)

650-632-4210

(Registrant’s telephone number, including area code)

2377 Gold Meadow Way, Suite 100, Gold River, CA

95670

(Former Name or Former Address, if Changed Since Last Report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

[ ] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

[ ] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a -12)

[ ] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d -2(b))

[ ] Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e -4(c))

Cautionary Notice Regarding Forward-Looking Statements

This Current Report on Form 8-K (“Form 8-K”) and other reports filed by the Registrant from time to time with the Securities and Exchange Commission (collectively the “Filings”) contain or may contain forward-looking statements and information that are based upon beliefs of, and information currently available to, the Registrant’s management as well as estimates and assumptions made by the Registrant’s management. When used in the filings the words “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “plan” or the negative of these terms and similar expressions as they relate to the Registrant or the Registrant’s management identify forward-looking statements. Such statements reflect the current view of the Registrant with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this report entitled “Risk Factors”) relating to the Registrant’s industry, the Registrant’s operations and results of operations and any businesses that may be acquired by the Registrant. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although the Registrant believes that the expectations reflected in the forward-looking statements are reasonable, the Registrant cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the Registrant does not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with the Registrant’s financial statements and pro forma financial statements and the related notes filed with this Form 8-K.

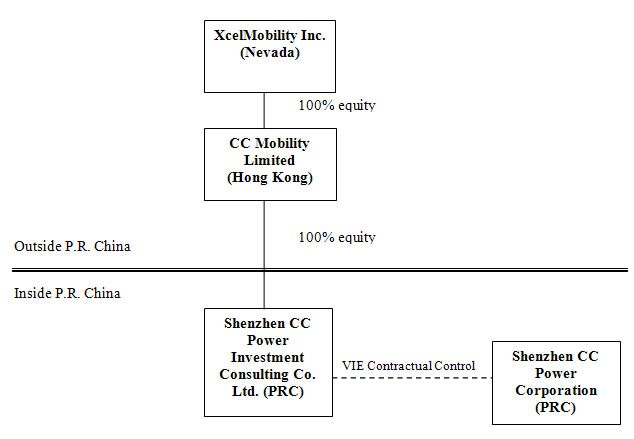

Unless otherwise indicated, in this Form 8-K, references to “we,” “our,” “us,” “XCLL,” the “Company” or the “Registrant” refer to XcelMobility Inc., a Nevada corporation and its wholly owned subsidiaries, CC Mobility Limited (“CC Mobility”), a company organized under the laws of the Hong Kong, Shenzhen CC Power Investment Consulting Co. Ltd. (“CC Investment”), a company organized under the laws of the People’s Republic of China, and a wholly-owned subsidiary of CC Mobility, and Shenzhen CC Power Corporation (“CC Power”), a company organized under the laws of the People’s Republic of China.

Section 2 - Financial Information

Item 2.01. Completion of Acquisition or Disposition of Assets.

On August 30, 2011 (the “Closing Date”), XcelMobility Inc., a Nevada corporation (the “Registrant,” “Company” or “Xcel”), closed a voluntary share exchange transaction with CC Mobility Limited, a company organized under the laws of Hong Kong (“CC Mobility”) and the shareholders of CC Mobility (“Selling Shareholders”) pursuant to a Share Exchange Agreement dated July 5, 2011 (the “Exchange Agreement”) by and among Xcel, CC Mobility, the Selling Shareholders and Shenzhen CC Power Corporation (“CC Power”), a company organized under the laws of the People’ Republic of China (“PRC”).

In accordance with the terms of Exchange Agreement, on the Closing Date, the Registrant issued 30,300,000 shares of its common stock to the Selling Shareholders in exchange for 100% of the issued and outstanding capital stock of CC Mobility (the “Exchange Transaction”). As a result of the Exchange Transaction, the Selling Shareholders acquired 50.50% of our issued and outstanding common stock, CC Mobility became our wholly-owned subsidiary, and the Registrant acquired the business and operations of CC Mobility and CC Power.

CC Power is primarily engaged in the research, development and commercialization of applications for mobile devices that access the Internet utilizing mobile phone networks. CC Power’s flagship product is the Mach 5 accelerator that enables subscribers to access and utilize the Internet significantly faster than without the product. CC Power also produces other products for mobile phones that leverage off the performance of the Mach 5 product as well as products that increase the speed of Virtual Private Networks.

2

Prior to the Exchange Transaction, we were a public reporting “shell company,” as defined in Rule 12b-2 of the Securities Exchange Act of 1934, as amended and the rules and regulations promulgated thereunder (“Exchange Act”). Accordingly, pursuant to the requirements of Item 2.01(a)(f) of Form 8-K, set forth below is the information that would be required if the Registrant were filing a general form for registration of securities on Form 10 under the Exchange Act, for the Registrant’s common stock, which is the only class of its securities subject to the reporting requirements of Section 13 or Section 15(d) of the Exchange Act upon consummation of the Exchange Transaction.

The following description of the terms and conditions of the Exchange Agreement and the transactions contemplated thereunder that are material to the Registrant does not purport to be complete and is qualified in its entirety by reference to the full text of the Exchange Agreement, a copy of which was filed as Exhibit 2.1 to our Current Report on Form 8-K on July 6, 2011 and is incorporated by reference into this Item 2.01.

Issuance of Common Stock. At the closing of the Exchange Transaction (“Closing”), the Registrant issued a total of 30,300,000 shares of its common stock to the Selling Shareholders in exchange for 100% of the issued and outstanding capital stock of CC Mobility. On August 11, 2011, Moses Carlo Supera Paez, one of our former directors and a shareholder, surrendered 17,700,000 shares of our common stock for cancellation. Further, on August 30, 2011, Mr. Paez surrendered an additional 7,350,000 shares of our common stock for cancellation and Mr. Jaime Brodeth, one of our former directors and a shareholder, surrendered 22,950,000 shares of our common stock for cancellation. As such, immediately prior to the Exchange Transaction and after giving effect to the foregoing cancellations, the Registrant had 29,700,000 shares of common stock issued and outstanding. Immediately after the Exchange Transaction, the Registrant had 60,000,000 shares of common stock issued and outstanding.

Change in Management. As a condition to closing the Exchange Agreement, effective on the Closing Date, Mr. Renyan Ge and Mr. Gregory D. Tse were appointed to the Registrant’s Board of Directors, Mr. Jaime Brodeth and Mr. Moses Carlo Supera Paez resigned from the Registrant’s Board of Directors and as officers of the Registrant, Mr. Ronald Edward Strauss was appointed as Executive Chairman of the Board of Directors, Mr. Renyan Ge was appointed as our Chief Executive Officer and Ms. Xili Wang was appointed as our Chief Financial Officer and Secretary.

The following persons consist of the Registrant’s new executive officers and directors subsequent to the closing of the Exchange Transaction:

| Name | Age | Position | |

| Mr. Ronald Edward Strauss | 52 | Executive Chairman of the Board of Directors | |

| Mr. Renyan Ge | 48 | Director, Chief Executive Officer | |

| Ms. Xili Wang | 42 | Chief Financial Officer, Secretary | |

| Mr. Gregory D. Tse | 51 | Director |

The Registrant previously filed and mailed the Information Statement required under Rule 14(f)-1 to its shareholders on or about August 10, 2011, and the ten-day period prior to the change in the majority of the Registrant’s directors as required under Rule 14(f)-1 expired on August 20, 2010. Additional information regarding the above-mentioned directors and/or executive officers is set forth below under the section titled “Management.”

3

From and after the Closing Date, our primary operations consist of the business and operations of CC Mobility and CC Power. In the Exchange Transaction, or reverse acquisition, the Registrant is the accounting acquiree and CC Mobility is the accounting acquirer. Accordingly, we are presenting the financial statements of CC Power and CC Mobility as set forth in Exhibit 99.1 and certain proforma financial information as set forth in Exhibit 99.2 of this report. Further, as noted above, we disclose information about the business, financial condition, and management of CC Mobility and CC Power in this Form 8-K.

DESCRIPTION OF BUSINESS

Except as otherwise indicated by context, references to “we,” “us” or “our” hereinafter in this Form 8-K are to the consolidated business of CC Mobility and CC Power, except that references to “our common stock,” “our shares of common stock” or “our capital stock” or similar terms shall refer to the common stock of the Registrant.

Overview

CC Mobility Limited (“CC Mobility”) was incorporated on May 3, 2011 under the laws of Hong Kong as a limited liability company.

Shenzhen CC Power Investment Consulting Co. Ltd. (“CC Investment”), a wholly-owned subsidiary of CC Mobility, was incorporated on July 27, 2011 under the laws of the People’s Republic of China (“PRC”) as a wholly foreign owned limited liability company.

Shenzhen CC Power Corporation (“CC Power”) is a Chinese enterprise incorporated on March 13, 2003 under the laws of the PRC. CC Power’s offices are located at: Room 706, Cyber Times Tower B, Tairan Road, Futian District, Shenzhen, PRC.

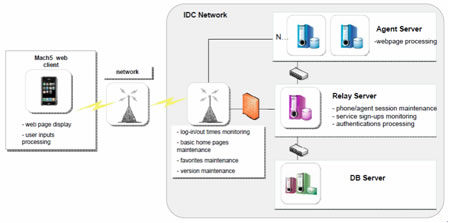

CC Power is primarily engaged in the research, development and commercialization of applications for mobile devices that access the Internet utilizing mobile phone networks. CC Power’s principal activity is the design, testing sale and support of software to support mobile Internet applications on cellular phones, smartphones, tablets and mobile computers in China. The principal product designed and built by CC Power is the Mach 5 Accelerator. This product has been independently tested by all 3 mobile phone carriers in China and we believe, accesses the Internet significantly faster than other mobile browsers. The speed of the Mach 5 browser enables CC Power to develop other mobile software that can leverage off the Mach 5 product’s speed of processing. In order to support CC Power products, CC Power has built a series of server locations throughout China. CC Power sells its products to corporations directly, to individual users via CC Power’s website and retail locations, through distribution agents and through all three mobile phone carriers in China.

As noted above, the primary purpose of CC Power is to develop software that allow users faster access to the Internet. CC Power’s primary focus is in the mobile Internet market, with a focus on providing software that significantly increases the speed that users of smartphones, tablets and laptops can access the Internet over cellular phone networks. CC Power also uses their technology to increase the speed at which users of Virtual Private Networks can access data from their networks.

CC Power is currently focusing the introduction of their products in Asia due to the size of the market and the tremendous use of the Asian market in accessing the Internet and social media through mobile devices. Through its Hong Kong subsidiary, CC Mobility, we are pursuing business opportunities in China, Japan and South Korea.

CC Power is currently deriving revenue from subscriptions to purchase its products and plans to increase its revenues by expanding its marketing efforts and to broaden its product offering to include software sales to cell phone manufacturers and provide application sales and enhanced products directly to consumers. CC Power currently has approximately 1,030,000 free and paying customers.

4

CC Power has been in the developmental stage since inception and has generated limited revenue. The technology underlying CC Power’s products is complex and as such, a significant amount of development time and expense has gone into the creation of the CC Power’s service infrastructure. To minimize startup costs, CC Power has used only a small number of fulltime employees, most of which are in the software development and testing areas. Sales and marketing efforts have concentrated on building strong relationships with the major carriers in China, Japan, and Korea. In addition, during the inception and development stages of CC Power, management was provided with limited compensation in connection with their service; rather, substantially all funds were put towards developing CC Power’s infrastructure. For more discussion on executive compensation of CC Power’s management, see “Executive Compensation” below.

CC Power’s business is subject to several significant risks, any of which could materially adversely affect its business, operating results, financial condition and the actual outcome of matters as to which it makes forward-looking statements. (See “Risk Factors”)

As discussed herein, CC Power and/or its shareholder have entered into various agreements with CC Investment to allow CC Investment’s effective control over CC Power. As noted above, the Registrant acquired 100% of the issued and outstanding capital stock of CC Mobility, which has a 100% equity interest in CC Investment, in exchange for the issuance of 30,300,000 shares of our common stock to the Selling Shareholders, which constitutes 50.50% of our issued and outstanding common stock. Through its ownership of CC Mobility, the Registrant acquired the business and operations of CC Mobility and CC Power.

Background

The Registrant was incorporated in the state of Nevada on December 27, 2007 under the name “Advanced Messaging Solutions, Inc.” The Registrant’s initial goal was to develop and market secure instant messaging software for desktop computer users, with products to be targeted towards instant messaging and file sharing using an encrypted transmission format. The Registrant has not generated any revenue from its business operations to date, and to date, the Registrant has been unable to raise additional funds to implement its operations.

Accordingly, as a result of the current difficult economic environment and the Registrant’s lack of funding to implement its business plan, in early 2011, the Registrant’s Board of Directors began to analyze strategic alternatives available to the Registrant to continue as a going concern. Such alternatives included raising additional debt or equity financing or consummating a merger or acquisition with a partner that may involve a change in its business plan. The Registrant identified CC Power as a potential strategic acquisition that the Board of Directors believed to be in the best interest of the Registrant and its shareholders. CC Power was attractive to the Registrant because it is in a growing telecommunications business, has a strong presence in the PRC and has plans to grow its business. CC Power believed the Registrant to be an attractive business combination partner, due in part, to the perceived benefits of being a publicly registered company, allowing for increased access to capital raising. Accordingly, the parties entered into a letter of intent with respect to the Exchange Transaction on March 8, 2011, executed the Exchange Agreement on July 5, 2011, and closed the Exchange Transaction on August 30, 2011.

5

Corporate Structure

As a result of the Exchange Transaction, the organizational structure of the Registrant is as follows:

6

CC Power is owned entirely by Xili Wang (the “CC Power Shareholder”), who is also our newly appointed Chief Financial Officer and Secretary. CC Power maintains all the licenses and approvals necessary to operate its business in the PRC.

PRC law places certain restrictions on roundtrip investments through the acquisition of a PRC entity by PRC residents. To comply with these restrictions, in conjunction with the Exchange Transaction, we (via our wholly-owned subsidiary, CC Investment), entered into and consummated certain contractual arrangements with CC Power and/or the CC Power Shareholder pursuant to which we provide CC Power with exclusive technology consulting and management services. Through these contractual arrangements, we have the ability to substantially influence CC Power’s daily operations and financial affairs, appoint its directors and senior executives, and approve all matters requiring board and/or shareholder approval. These contractual arrangements enable us to control CC Power and operate our business in the PRC through CC Power and we are considered the primary beneficiary of CC Power. Accordingly, our consolidated financial statements reflect the results of operations, assets and liabilities of CC Power.

On August 22, 2011, our subsidiary, CC Investment, entered into the following contractual arrangements with CC Power and/or the CC Power Shareholder, each of which is enforceable and valid in accordance with the laws of the PRC:

Entrusted Management Agreement. Pursuant to the Entrusted Management Agreement among CC Power, CC Investment, and the CC Power Shareholder, CC Investment agrees to provide, and CC Power agrees to accept, exclusive management services provided by CC Investment. Such management services include but are not limited to financial management, business management, marketing management, human resource management and internal control of CC Power. The Entrusted Management Agreement will remain in effect until the acquisition of all assets or equity of CC Power by CC Investment is complete (as more fully described in the Exclusive Purchase Option Agreement below).

Technical Services Agreement. Pursuant to the Technical Services Agreement among CC Power, CC Investment, and the CC Power Shareholder, CC Investment agrees to provide, and CC Power agrees to accept, exclusive technical services provided by CC Investment. Such technical services include but are not limited to software, computer system, data analysis, training and other technical services. CC Investment shall be entitled to charge CC Power service fees equivalent to CC Power’s total net income. The Technical Service Agreement will remain in effect until the acquisition of all assets or equity of CC Power by CC Investment is complete (as more fully described in the Exclusive Purchase Option Agreement below).

Exclusive Purchase Option Agreement. Under the Exclusive Purchase Option Agreement among CC Power, CC Investment, and the CC Power Shareholder, the CC Power Shareholder granted CC Investment an irrevocable and exclusive purchase option to acquire CC Power’s equity and/or assets at a nominal consideration. CC Investment may exercise the purchase option at any time.

Loan Agreement. Under the Loan Agreement between CC Investment and the CC Power Shareholder, CC Investment agreed to lend RMB 10,000,000 to the CC Power Shareholder, to be used solely for the operations of CC Power.

Equity Pledge Agreement. Under the Equity Pledge Agreement among CC Investment and the CC Power Shareholder, the CC Power Shareholder pledged all of its equity interests in CC Power, including the proceeds thereof, to guarantee all of CC Investment’s rights and benefits under the Entrusted Management Agreement, the Technical Service Agreement, the Exclusive Purchase Option Agreement and the Loan Agreement. Prior to termination of this Equity Pledge Agreement, the pledged equity interests cannot be transferred without CC Investment’s prior consent. The CC Power Shareholder covenants to CC Investment that among other things, it will only appoint/elect the candidates for the directors of CC Power nominated by CC Investment.

Subsidiaries

As a result of the Exchange Transaction, CC Investment and (via a contractual relationship) CC Power are wholly-owned subsidiaries of our subsidiary CC Mobility. CC Power does not have any subsidiaries.

7

Strategy

We, through CC Mobility and CC Power, are developing mobile applications directly for the mobile devices that utilize cellular networks to connect to the Internet and hardware/software products to increase the speed of Virtual Private Networks. While our strategy is to become global in scope, our focus at this time is the large mobile markets in Asia. We are currently developing unique strategies and products for each market we are currently engaged in and will eventually offer our products in North America and Europe. To that end, we have entered into an agreement with NetQin Mobile (Beijing) Technology Co., Ltd., (“NetQin”), a company organized under the laws of the PRC, to develop security software and products for mobile phones and mobile Internet platforms solely in the Japanese market that utilize and combine CC Power’s Mach 5 technology and March 5 brand and NetQin’s mobile security solutions, specifically antivirus and mobile manager platforms and services.

In all markets, the lead product is our Mach 5 Accelerator, which provides high speed web browsing for mobile devices. The Mach 5 product has the look and feel of a desktop browser but loads and processes material over the cellular Internet (e.g., websites, videos, pictures, etc.) significantly faster than conventional browsers that come with mobile devices. This enables us to develop and acquire other mobile software that will leverage off the speed and performance of the Mach 5 product line. In order to support CC Power’s products, we have built a series of server locations throughout China. Management believes it has the opportunity to grow significant revenues from operations in China and Japan if we successfully execute our business and financial objectives.

China Strategy

In China, CC Power is utilizing the license granted by the PRC to provide mobile Internet services to corporations and individuals. Since 2008, CC Power has been actively test marketing products throughout China. A large network of servers has been put in place to support all Mach 5 products. CC Power also has in place agreements with all three of China’s cellular carriers (China Mobile, China Telecom and China Unicom) in many of China’s provinces that allow CC Power to market to the carrier’s subscribers via mail, email, text messaging and other means to introduce CC Power products. These agreements are entered into in the ordinary course of CC Power’s business as each and every province in the PRC where CC Power operates requires a separate agreement with each of the three main cellular carriers. These three carriers currently have an estimated subscriber base of over 1 billion users, per the chart below. CC Power has established revenue sharing arrangements with each carrier in the ordinary course of business on a province by province basis.

| Cellular Carrier | Subscribers |

| China Mobile | 616 Million |

| China Unicom | 277 Million |

| China Telecom | 108 Million |

| Total | 1,001 Million |

In test marketing efforts from 2008 through 2011, CC power has attracted over 1 million subscribers. CC Power has found that the best method of marketing to the price sensitive Chinese market is to offer a base product for free and a superior product for a small fee (equivalent to approximately $0.50 per month). For cell phone OEMs that preinstall the Mach 5 software in the phone, CC Power will provide a free trial version of Mach 5 Premium (enhanced video) for a 3 month period, which will revert to the basic Mach 5 product if they do not purchase the Premium Mach 5 product.

In addition to marketing products through China’s three cellular carriers, CC Power is also working with cell phone manufacturers to embed the Mach 5 product in phones at the factory. CC Power is working with several large cellular phone companies on this strategy, including Hua Wei and ZTE, the two largest cellular phone manufacturers in China.

8

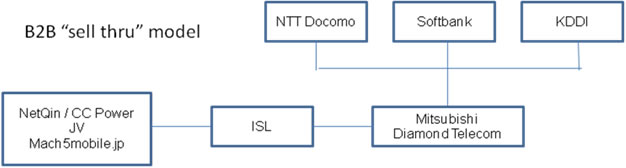

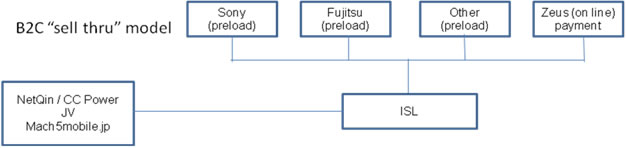

Japan Strategy

We are in the process of expanding into Japan through the utilization of a strategic partner. CC Power has a strategic, contractual relationship with International Strategic Leaders Inc. (ISL), a Tokyo-based company with relationships throughout Japan including with the largest cellular phone carriers, mobile device manufacturers and retailers.

In April 2011, we, through ISL, were introduced to Japan’s three largest cellular carriers to distribute the Mach 5 browser and our other products. Given the current estimated subscriber base of these carriers, noted in the chart below, this provides us with a significant foothold for expansion into the Japanese market:

| Cellular Carrier | Subscribers |

| NTT Docomo | 58 Million |

| KDDI | 33 Million |

| Softbank | 24 Million |

| Total | 115 Million |

The Japanese market represents a large and mature mobile device market that is quick to upgrade to the latest and most satisfying mobile device hardware and technology. Japanese carriers are also known to select the best of breed hardware and technology to offer their subscriber base. We have entered into an agreement where ISL will work with the three largest telecommunication carriers in Japan, NTT Docomo, KDDI and Softbank to aggressively market all Mach 5 branded products in Japan. We expect these agreements to start generating revenue before the end of 2011.

With ISL’s assistance, over the last few months, we have entered into preliminary contracts with NTT Docomo, KDDI, and Softbank, whereby they agreed to move forward with the Mach 5 mobile Web Browser and Mach 5 Security (a joint product development with Netqin). The products have been going through a number of due diligence and product testing cycles and have proven to be very robust.

To accomplish our objectives in the Japanese market, in addition to ISL, we have a strategic relationship with Mitsubishi Diamond Telecom (DT) through ISL. ISL is the exclusive distribution partner in the Japanese market, and DT will be the systems integrator to ensure the product suite gets installed successfully. They have been instrumental in moving the Japanese strategy forward, not only introducing us to the right people with the major carriers, but also with the key handset manufacturers located in Japan. ISL, as a value added service provider:

| a. |

will work with handset manufacturers to ensure that the Preload of both Xcel and Netqin products have properly been executed, and that devices are distributed in a timely fashion via standard channels. | |

| b. |

will assist Netqin and Xcel to review and perform quality control on their application services to ensure they are appropriately localized for the Japanese market. | |

| c. |

where ISL has relationships with local telecommunication operators or other distributors that have relationships with local telecommunication operators, ISL will work to set up billing and distribution relationships via these channels. These telecommunication operators and distributors include, but are not limited to KDDI, Softbank Mobile, NTT Docomo, E-Mobile, Mitsubishi Diamond Telecom and NEC. |

9

| d. |

ISL shall not engage with parties that have competitive solutions to Netqin or Xcel application services. | |

| e. |

shall provide local support for end users and payment providers for B2C billing channel and payment. This will include, but is not limited to, working with the local billing and payment providers to integrate necessary backend systems, creating the appropriate billing processes, and obtaining cash to be distributed among all parties. | |

| f. |

shall prepare a monthly report to Netqin and Xcel which outlines which users unsubscribe to the service. This report will include all necessary data for Netqin and Xcel to “turn off” functionality that cannot be used when unsubscribed. | |

| g. |

will help create and drive a local marketing campaign, which may or may not involve other parties. | |

| h. |

shall provide payment and payment reporting to Netqin and Xcel according to specified payment terms. |

South Korea Strategy

The South Korea market is very similar to the Japanese cellular market. In South Korea, we will follow the same sales and marketing strategy as used in Japan. We are actively looking for sales and marketing partner(s) in Korea. We hope to have a partnership agreement in place before the end of 2011.

Revenues and Customers

CC Power had revenues of $224,038 in 2009 and $273,948 in 2010. The Company currently has a customer base of approximately 1 million end users within China using our service free of charge with approximately 30,000 fee-paying enterprise customers. With our key products fully tested and approved by large cellular carriers in China and Japan, the Company believes that it will be able to grow its customer base and revenues in 2012.

10

Technology

We provide products for mobile Internet users which includes products for traditional cell phones, smartphones and PC access to the Internet through mobile phones.

CC Power’s marquis product is a web browser called Mach 5 for Mobile Phones. It is fully operational and currently being used by over 1 million Chinese mobile phone users. The Mach 5 Web enables users to take their full PC web browsing experience to their mobile devices. Featured websites and Rich Internet Applications (RIA) such as YouTube, Facebook, Google Apps, Google Maps, and many others with Flash, AJAX, JavaScript, ActiveX, Web 2.0 and more are easily accessed. YouTube videos and other compatible videos are Full-Screen supported.

With the latest and unique remote processing technologies, Mach 5 Web requires just minimal bandwidth and hardware resources to quickly access full websites and heavy web based applications.

Our products require a large powerful network to run our applications. Cell phone applications are provided and accelerated through server based compression software.

11

We have spent considerable time, effort and financial resources building a proven network throughout China.

12

Intellectual Property

CC Power has developed unique intellectual property for its service. The centerpiece of CC Power’s technology is compression algorithms that enable data to be passed from computers to phones. The compression software couples with high speed servers to accelerate data between a phone and the source of data. Management believes this technology is unique.

CC Power has significant intellectual property that we believe provides a competitive advantage over competitors and new entrants to the market:

| 1. |

Control of Source Code: CC Power protects its intellectual property by not allowing others to use its source code. | |

| 2. |

Trade Secret Agreements: All employees are bound by trade secret agreements. |

Copyrights

CC Power has copyrights to the following software applications in China, where it believes the majority of its customer base will be generated in the next few years.

| 1. |

Software Copyright Applications: CC Power has registered 3 software applications for copyright in China. | ||

| a. |

Mach 5 Internet acceleration software V.6.0, Register number: 2007SR09253, by National copyright administration of People’s Public of China. | ||

| b. |

Mach 5 Enterprise acceleration software V.3.3, Register number: 2009SR058767, by National copyright administration of People’s Public of China. | ||

| c. |

Mach 5 Web Browser software V.1.1.44.13, Register number: 2010SR001089, by National copyright administration of People’s Public of China. | ||

| 2. |

Licenses: CC Power also has obtained several licenses available only to Chinese companies from the PRC Ministry of Industry and technology and local Police Public Safety Departments (international website licenses). These licenses include the following: | ||

| • |

“Software Enterprise Recognition Certificate,” issued by Shenzhen Science Technology & Information Bureau on May 30, 2008, granted to Shenzhen CC Power Corporation. | |

|

| ||

| • |

“PRC Value-Added Telecommunication Service Operation License,” issued by the PRC Ministry of Industry and Information Technology on March 11, 2008, to expire on March 11, 2013, granted to Shenzhen CC Power Corporation. |

Awards

CC Power has also received the following awards and/or special recognitions:

|

• |

“Certificate of Honor,” issued by Beijing World of Telecommunication Magazine, Beijing Telecommunication Technology Magazine and Telecommunication Science Magazine in October 2007, granted to Shenzhen CC Power Corporation, indicating that the “MACH 5 Wireless Web Accelerator” Solution was awarded the Excellent Solution in the “Election of 2007 The 100 Most Successful Solutions in PRC Telecommunication Industry.” |

13

| • |

“Certificate of Honor,” issued by Beijing World of Telecommunication Magazine, Beijing Telecommunication Technology Magazine and Telecommunication Science Magazine in October 2009, granted to Shenzhen CC Power Corporation, indicating that the “MACH 5 Mobile Browser” Solution was awarded the Excellent Solution in the “Election of 2009 The 100 Most Successful Solutions in PRC Telecommunication Industry – Judges Choice Award.” | |

|

| ||

| • |

Recognition by Information Week Magazine, noting Shenzhen CC Power Corporation was included on its 2008 list of “The 100 Best PRC Commercial Technology Companies.” |

We will continue to evaluate the business benefits in pursuing patents and copyrights in the future. We currently protect all of our development work with confidentiality agreements with our engineers, employees and any outside contractors. However, third parties may, in an unauthorized manner, attempt to use, copy or otherwise obtain and market or distribute our intellectual property or technology or otherwise develop a product with the same functionality as our service. Policing unauthorized use of intellectual property rights is difficult, and nearly impossible on a worldwide basis. Therefore, we cannot be certain that the steps we have taken or will take in the future will prevent misappropriation of our technology or intellectual property, particularly in foreign countries where we do business or where our service is sold or used, where the laws may not protect proprietary rights as fully as do the laws of the United States or where the enforcement of such laws is not common or effective.

Products and Distribution

Products for Mobile Devices

We have a suite of products but our core retail product (named Mach 5 Wireless) is an application that significantly speeds up the Internet, email and text messaging processing of the phone in comparison to phones which do not use the product. In order to use Mach 5 Wireless, a user must either download the application over the Internet or mobile phone lines. Once installed the application utilizes CC Power-I’s server network located throughout China to relay, compress and encrypt web pages, emails and text messages. The Mach 5 Wireless product has enabled CC Power to develop a host of products that can take advantage of the increased speed of more complex products that would ordinarily take a significant amount of time to download.

The Mach 5 Wireless product provides us with a unique opportunity in China. Currently there are a limited number of Chinese applications available to the Chinese market, with few in the Chinese language. Part of our strategy is to develop an applications store (“App Store”), where Chinese applications, games and content can be downloaded and utilized by Mach 5 subscribers. We will work directly with proven application and game providers to modify applications to the Chinese language. Content will be provided from the existing Chinese media. Our App Store will resemble App Stores currently provided by Apple and Blackberry.

14

Xcel’s current suite of products includes:

- Mach 5 Wireless – Internet accelerator for mobile laptop/netbook users and soon, the iPad.

- Mach 5 Mobile – Internet accelerator and cell phone optimizer browser for mobile cell phone users

- Mach 5 Enterprise – Secure and reliable Internet accelerator specifically designed for each enterprises needs and uses.

- Mach 5 Mail – Device independent push mail delivery system. Works with the majority of smart and not so smart cell phones on the market today.

- Mach 5 Video – Mobile video accelerator. Offering the TV experience over mobile networks.

- Mach 5 LBS – Recently introduced mobile location based tracking service for smartphone users. Find lost phones, locate important people, market directly to location based cell phones. Today CC Power believes it is the first in China to offer this new technology for cell phone subscribers.

- Mach 5 Security – Through an exclusive partnership with NetQin, CC Power offers cell phone virus protection software to all its subscribers.

Virtual Private Network Product

A virtual private network (VPN) is a network that uses a public telecommunication infrastructure, such as the Internet, to provide remote offices or individual users with secure access to their organization’s network. A virtual private network can be contrasted with an expensive system of owned or leased lines that can only be used by one organization. The goal of a VPN is to provide the organization with the same capabilities, but at a much lower cost.

A VPN works by using the shared public infrastructure while maintaining privacy through security procedures and tunneling protocols such as the Layer Two Tunneling Protocol. In effect, the protocols, by encrypting data at the sending end and decrypting it at the receiving end, send the data through a “tunnel” that cannot be “entered” by data that is not properly encrypted. An additional level of security involves encrypting not only the data, but also the originating and receiving network addresses.

15

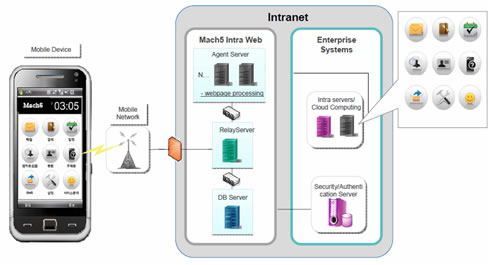

The XcelMobility Enterprise VPL - Mach 5 Intra Web

We have developed an enterprise solution for VPN which is branded the Mach 5 Intra Web. We believe we have an opportunity to seize a significant portion of the enterprise VPN market as the demand for mobile and cloud computing capabilities is increasing significantly as companies adopt mobile technology in their operations to enhance efficiency, increase productivity and strengthen customer relationships. Companies are facing the following challenges in implementing and managing mobile platforms:

- linking time critical work flow and information to existing internal operating systems that are not accessible from mobile devices;

- the cost of frequent client application upgrades and the maintenance of current mobile solutions; and

- reluctance to implement a mobile intranet platform adoption due to lack of IT resources.

We offer an enterprise solution for VPN owners that we believe provides the following benefits:

- flexibility for various businesses by being more cost efficient, easily implemented (plug and play), high level of security and is expandable;

- web based intranet applications through mobile devices with PC like experience;

- various sub systems to support PC line UX on Mobile environment;

- architecture offers easy integration and expandability;

16

- various enterprise work force applications using its server-based full browser technology increasing speed and accuracy;

- the flexibility to support various policies and environments (security, geographical regions, device platforms) set by users;

- easy expandability through Sub Systems;

- multimedia content support for videos, live broadcasts and social media; and

- proven solutions with low maintenance.

Products in Development

We plan to bring the following new mobile Internet applications to the Chinese market in the next twelve months:

Location Based Services: Many mobile devices today are GPS-enabled and can be tracked accurately around the world. Many new applications use this feature to provide accurate location-based services.

Mobile gaming: One of the largest and fastest growing areas of the mobile Internet is gaming. With the new devices with high resolution screens and power processors complex gaming has come to the mobile arena.

Mobile marketing: Location-based mobile marketing is a new and growing application for the mobile Internet.

Mobile Social Networking: One of the fastest growing applications of the mobile Internet is social networking.

Distribution

We provide mobile phone and Internet products through monthly subscriptions to large Chinese cell phone carriers and OEM partners. CC Power delivers its products through a powerful and sophisticated network of servers that are located throughout China

CC Power markets it products through 3 distribution channels:

| 1. |

As a product offered by all 3 of China’s cell phone carriers – China Mobile, China Telecom, and China Unicom | |

| 2. |

Through OEM partners that manufacture cell phones and accessories, and | |

| 3. |

Directly, through our website. |

Unlike applications that are currently developed for the iPhone and BlackBerry and marketed along with hundreds of thousands of other applications through iTunes or BlackBerry App World, our products avoid the clutter of the marketplace and are primarily marketed directly through all three Chinese cell phone carriers and OEM partners.

Marketing directly to the three carriers’ subscribers provides us a great advantage, as consumers either believe the Mach 5 brand is an extension of the carrier or the product is endorsed by the carrier. For example, recently Yao Ming, a former professional basketball player, has been featured in ads promoting Mach 5 products available through China Unicom.

17

Our product line is positioned to take advantage of the evolution of Chinese cell phones and carrier networks as devices to support PC access and social networking sites. While Facebook and You Tube are not yet available in China, the Chinese equivalents, Renren and Youku have experienced tremendous growth since there introduction. These China-based social networking sites are predominantly being accessed by smartphones which can utilize the fast Internet access and processing capabilities of Mach 5 Internet Accelerator and Mach 5 Video. With limited WiFi access in some areas, the Mach 5 Wireless product works like the Rogers Rocket Stick, using the cell phone network to provide Internet access. Both of these markets are in their infancy in China, with CC Power being well positioned with the 3 largest cell phone networks to provide products to service these sectors.

We have established a seamless position with the 3 largest cell phone networks. When a China Telecom, China Unicom or China Mobile customer subscribes to our product, the subscription becomes part of the monthly invoice, with the fee collected by the carrier and the revenue spilt with us. We are now working with the carriers to include their products as part of packages that provide on social networking, PC access, video and push email solutions. Products sold through OEM partners is also split with us.

Industry

Personal mobile communications and computing have advanced dramatically with the continuous build out of advanced mobile infrastructure and the introduction of increasingly sophisticated portable smart devices. Wireless technology and mobile Internet have allowed for increased interaction and collaboration among users beyond what can be achieved through the traditional Internet. This increased level of connectivity has created increasing demand for advanced mobile Internet services particularly in China, which has the largest mobile user population in the world. As of December 31, 2010, China had 859 million mobile subscribers, according to the Ministry of Industry and Information Technology, or the MIIT, representing a mobile penetration rate of 64.4% . With this large user population, consumer trends in the mobile industry in China often lead those in the rest of the world. The popularity of mobile services in China and globally has led to the development of a broad ecosystem of industry participants, including content providers, application developers, platform providers and device manufacturers, as users increasingly seek to enhance their mobile experience beyond voice communication.

Drivers of Demand for Mobile Internet Services

Early mobile services were primarily based on SMS technology and were largely focused on user entertainment. These included ring tones, games, screen wallpapers and other applications and such services have been widely popular, particularly in China. Advancements in 3G adoption and mobile technology have led to the development of a new generation of advanced services based on mobile Internet technology which address the need for more effective and efficient use of mobile devices. With the increasing adoption of smartphones, tablets and other 3G-enabled networked devices, mobile Internet services will become increasingly popular in users’ daily lives.

Adoption of 3G Networks

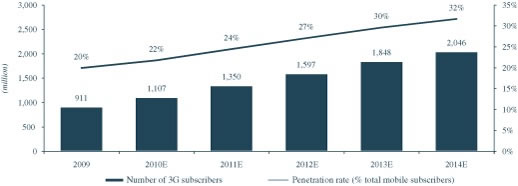

Advances in bandwidth provided by 3G mobile networks have created the necessary infrastructure for mass adoption of mobile Internet services. As mobile users increasingly adopting 3G networks worldwide the market opportunity for mobile services continues to expand. The number of 3G subscribers worldwide is projected to grow at a CAGR of 18% from 2009 to 2014 to reach over 2.0 billion users. In China, the number of mobile Internet users has already reached 303 million users as of December 2010, according to CNNIC.

18

Worldwide 3G Subscribers

| Source: Infonetics, October 2010 |

Popularity of Mobile Devices with Increased Functionality Based on Multiple Platforms

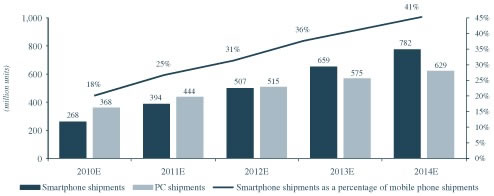

User adoption of 3G networks has generated increasing demand for advanced mobile devices with the necessary features to leverage mobile Internet services. As mobile devices evolve, they incorporate an ever-increasing range of functions at lower cost, which address a broadening array of users’ business and personal needs. Examples of such mobile devices include wireless-enabled personal computers, tablets and smartphones which provide a converging range of functionality. Smartphones, in particular, which offer advanced computing and networking capability in compact form factors, have gained increasing popularity. The worldwide shipments of smartphones are expected to exceed that of personal computers in 2013, according to Gartner.

19

Worldwide Smartphone Shipments

| Source: Gartner, September 2010 |

High-end smartphones, including Android models, Symbian models, the BlackBerry and the iPhone, are expected to develop and share similarities with tablet PCs in computing performance and mobility over time. The trend of convergence in computing and mobility is just beginning and is creating further user demand for innovative mobile Internet services. China, with its large mobile user base, is likely to become a leading mobile market for the adoption of smartphones and mobile Internet services in the future.

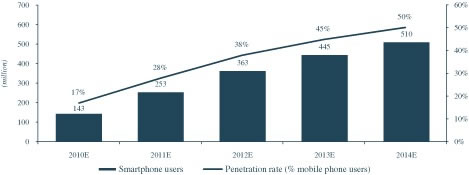

Smartphone Penetration in China

| Source: Frost & Sullivan, January 2011 |

Various ecosystems encompassing hardware manufacturers, application developers, application stores, operating system providers and wireless carriers have developed based on different mobile technology platforms. As a result, the mobile device market, and the smartphone market in particular, is and will continue to be highly fragmented with different platforms dominating different regions. Given the rapid growth in smartphone usage and the fragmentation among operating systems, there is a distinct demand for third party mobile Internet services which are compatible across technology platforms. Such services enhance user experiences and provide capabilities unavailable from device manufacturers.

20

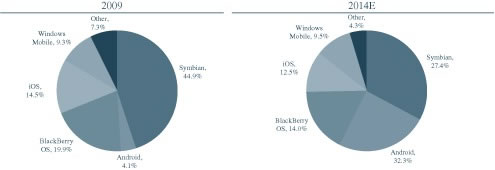

Worldwide Smartphone Shipments Breakdown by Operating System

| Source: IDC, December 2010 |

The Mobile Internet Services Industry

With the introduction of 3G networks, wireless carriers have actively promoted cooperation among mobile industry participants to develop mobile Internet services. A number of significant industry advancements have helped to define the mobile Internet computing paradigm. Users are increasingly accessing mobile Internet services through specially designed mobile applications installed on devices which provide users with convenient access to specific services. Given the form factors of mobile devices, mobile applications provide user-friendly interfaces through which users can interact with mobile Internet services. In addition, many mobile applications incorporate a cloud platform as a means to expand the capability of mobile Internet services beyond the computing power available from individual mobile devices.

Mobile Applications

In order to fully leverage the increasing computing power of smartphones and other mobile devices, developers have created a large universe of mobile applications to fulfill growing user requirements. The emergence of mobile application stores, such as those run by Apple, Research in Motion, Nokia, Google and GetJar, also provide direct channels for developers to distribute mobile applications.

21

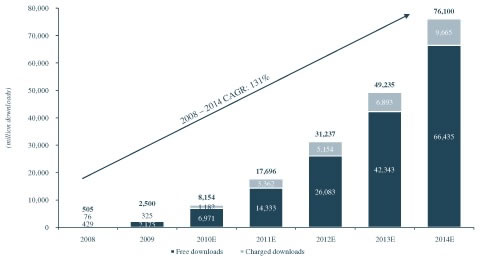

Global Mobile Application Downloads from Application Stores

| Source: Gartner, December 2010 |

Popular mobile applications include the following:

| (i) |

Connectivity applications, such as email, instant messenger, GPS navigation, remote access. |

| (ii) |

Business applications, such as mobile banking, stock monitoring and trading, document processing and calendar planning. |

| (iii) |

Life-style applications, such as ecommerce, bill payment, health monitoring, digital reading, and social-networking. |

| (iv) |

Entertainment applications, such as news, games, multimedia player, photo and video editor. |

As users start to enjoy the rich experience of mobile computing made possible by the enhanced computing power of mobile Internet enabled devices, additional user requirements have emerged. In particular, the mass adoption of applications makes mobile devices increasingly susceptible to security threats. Users of mobile applications are reliant on external downloads of data and networked communications to support their applications. This interconnectivity increases the likelihood that security threats can invade a mobile device. In addition, the proliferation of applications on mobile devices has led users to process and store more personal data on mobile devices and has created the need for third-party mobile services for users to manage their personal data more efficiently and to optimize the performance of mobile devices. As mobile computing becomes more advanced, mobile Internet services that can help users to maximize the capabilities and performance of their mobile devices will become increasingly vital.

22

Cloud Platform

A cloud platform describes an architecture that allows on-demand delivery of data and services over the Internet. The cloud allows mobile users to leverage resources beyond limitations of a single mobile device. For example, mobile Internet users can use a cloud platform to store data permanently for continuous access by different devices. This is particularly useful if a device is lost and existing data needs to be restored on a new device. Similarly, as direct peer-to-peer networking among mobile users is not feasible, a cloud platform provides a common computing resource through which mobile users can access and exchange data. This ubiquitous access is possible because cloud computing is designed to be device agnostic and to allow ease of access for different mobile technologies. Users can access mobile Internet services on a cloud platform without concern for the infrastructure that supports the applications and without downloading client end software. Services offered by a cloud platform can also be upgraded by mobile payment service providers without causing any disruption to the user. The functionality and convenience provided by cloud computing enhances the capabilities of mobile devices and will support further demand for innovative cloud services.

Mobile ecosystem participants also benefit from the cloud by utilizing cloud platforms to develop advanced mobile applications. For example, wireless carriers can leverage cloud platforms to seamlessly integrate third-party applications into their own mobile service offerings. Cloud platforms allow application developers to easily share distributed computing resources and deliver more powerful services to mobile users.

Competition

There are three main competitors in China for high speed data services and products. We believe that the testing of the Mach 5 browser by all three of China’s cellular carriers and testing by Japan’s three largest cellular carriers, who chose Mach 5 over several other competitors, independently verifies that our products are superior to our competition.

Bytemobile Inc. – www.bytemobile.com

Bytemobile’s technology allows wireless network operators to offer mobile

data, Web, and multimedia applications from cell phones and laptops. Its various

software applications manage network traffic, analyze traffic, optimize data,

and adapt to different platforms. More than 100 carriers, including most of the

world’s largest cell phone companies such as China Mobile, AT&T, and

Vodaphone, rely on Bytemobile’s software. The company serves customers in more

than 50 countries from offices in Asia, Europe, and the US. It was founded in

2000.

I-accele Corporation – www.i-accele.com

I-accele

Corporation, which was established in Japan in 2002, is a global provider of

software solutions that accelerate and optimize data services over wireless and

wire line networks. I-accele range of products for Wireless operators, ISPs, and

Enterprises, allows corporate customers and individual end-users of all networks

to benefit from accelerated and rich data services, without changing the

applications or devices they use, and without compromising their security needs.

Several carriers and vendors in Japan, China and Malaysia have selected I-accele

products to optimize their data applications, and I-accele is currently

extending its product distribution in the Asia market.

UC Web – www.ucweb.com

UC focuses on

serving faster, more stable and flexible Internet experience to users. In April

2004, UC launched its core product UC Browser, which now runs on almost any

mobile platform - Android, iOS, BlackBerry OS, Symbian, WinCE, bada, Java, MTK,

Brew etc. More than 3000 phone models in 200 brands can perfectly support UC

Browser. With UC Browser, mobile users can easily get online service, such as

web news, web games, e-commerce, and so forth. By March 2011, UC Browser have

served more than 150 countries and areas, and got more than 700 million

downloads. Per month, 200 million users visits 60 billion pages through UC

Browser, which ranked 1st in the world.

Seasonality

Our business is not subject to seasonality.

23

Government Regulation

Overview

The PRC government has imposed extensive and stringent measures to regulate the telecommunications and software development industries. The State Council of the PRC, or the State Council, the Ministry of Industry and Information Technology, or the MIIT (formerly the Ministry of Information Industry, or the MII), and other relevant authorities in the PRC have issued various regulations with respect to the telecommunications and software development industries. This section summarizes the principal PRC laws and regulations relevant to our business and operations.

Business license

Any company that conducts business in the PRC must have a business license that covers a particular type of work. Our business license covers our present business to design, develop, and produce mobile Internet software. Prior to expanding our business beyond that of our business license, we are required to apply and receive approval from the PRC government.

Employment laws

We are subject to laws and regulations governing our relationship with our employees, including: wage and hour requirements, working and safety conditions, citizenship requirements, work permits and travel restrictions. These include local labor laws and regulations, which may require substantial resources for compliance. China’s National Labor Law, which became effective on January 1, 1995, and China’s National Labor Contract Law, which became effective on January 1, 2008, permit workers in both state and private enterprises in China to bargain collectively. The National Labor Law and the National Labor Contract Law provide for collective contracts to be developed through collaboration between the labor union (or worker representatives in the absence of a union) and management that specify such matters as working conditions, wage scales, and hours of work. The laws also permit workers and employers in all types of enterprises to sign individual contracts, which are to be drawn up in accordance with the collective contract.

Regulation on the Telecommunications Industry

Types of Telecommunications Services

On September 25, 2000, the State Council issued the Regulations on Telecommunications of the PRC, or the Regulations on Telecommunications, which became effective on September 25, 2000 and which regulates the telecommunications industry and other related activities and services within the PRC. The MIIT regulates the telecommunications industry on a national level while the provincial-level communications administrative bureaus, or the CABs, supervise and regulate the telecommunications industry in their respective administrative regions. The Regulations on Telecommunications classifies telecommunications services into two main categories: (1) core telecommunications services and (2) value-added telecommunications services, and further divides each main category into several sub-categories. According to the Catalog for Classification of Telecommunications Businesses, which became effective on April 1, 2003, our business operates under the provision of information services through mobile networks and the Internet, thus fitting into the category of value-added telecommunications services.

24

Value-added Telecommunications Services

Providers of value-added telecommunications services in the PRC are subject to examination and approval from, and require licenses issued by, the MIIT or the relevant CABs. Pursuant to the Regulation on Telecommunications, to provide value-added telecommunications services in more than two provinces, autonomous regions or centrally administered municipalities, the value-added telecommunication service provider shall obtain the Transregional Value-added Telecommunication Business Operation License from the MIIT; to provide value-added telecommunications services within one province, autonomous region or centrally administered municipality, the value-added telecommunication service provider shall obtain the Value-Added Telecommunication Business Operation License from relevant CABs. On March 1, 2009, the MIIT issued the Administrative Measures for Licensing of Telecommunications Business Operations which set forth the basic requirements for a license to provide value-added telecommunications services in the PRC. Such requirements mainly include the following:

-

the applicant is a duly incorporated company;

-

the applicant has necessary funds and professional staff suitable for its business activities;

-

the applicant has the reputation or capability of providing customers with long-term services;

-

to operate value-added telecommunications services business across multiple provinces, autonomous regions or centrally administered municipalities, the applicant shall have a minimum registered capital of RMB10,000,000; to operate value-added telecommunications services business within a single province, autonomous region or centrally administered municipality, the applicant shall have a minimum registered capital of RMB1,000,000;

-

the applicant has necessary premises, facilities and technical scheme; and

-

the applicant and its major capital contributors and business managers have no record of violating rules on telecommunication supervision and administration during the past three years.

We have obtained the China Value-Added Telecommunications Business License permitted by the MII (B2-20080062) and the China Value-Added Telecommunications Business License permitted by the Guangdong Provincial Communications Authority (B2-20050598). These are the only value-added telecommunications business licenses that we currently require to operate our business in the PRC.

Short Message Services

On April 15, 2004, the MII issued the Notice on Certain Issues Regarding Regulating Short Message Services which specifies that only those telecommunications services providers that hold specific short message service licenses may provide such services in the PRC. The notice also requires short message services providers to censor the contents of short messages, to automatically collect information such as the time that short messages are sent and received and the telephone numbers or codes of the sending and receiving terminals and to keep such records for five months within the time each short message is delivered.

Telecommunications Networks Code Number Resources

On January 29, 2003, the MII issued the Administrative Measures on Telecommunications Networks Code Number Resources to administer the code number resources including mobile communications network code number. According to the administrative measures, the entity shall apply to the MII for a code number to be used in the inter-provincial operations and shall apply to the relevant CAB for a separate code number for

25

intra-provincial operations. The administrative measures specify the qualifications for a code number, required application materials and application procedures.

Specifications for Telecommunications Services

On March 13, 2005, the MII issued the Specifications for Telecommunications Services specifying the telecommunications service qualities to which all telecommunications service providers in the PRC should conform. It also requires all telecommunications services providers to establish a sound service quality management system and make periodical reports to the relevant telecommunications authorities.

Foreign Investments in Value-added Telecommunications Services Industry

Foreign direct investment in telecommunications services industry in China is regulated under Regulations on the Administration of Foreign-Invested Telecommunications Enterprises, or the FITE Regulations. The FITE Regulations were issued by the State Council on December 11, 2001 and amended by the State Council on September 10, 2008. According to the FITE Regulations, foreign investors’ ultimate equity interests in any entity providing value-added telecommunications services in the PRC may not exceed 50%. A foreign investor must demonstrate a good track record and prior experience in providing value-added telecommunications services outside the PRC prior to acquiring any equity interest in any value-added telecommunications services business in the PRC.

On July 13 2006, the MII issued the Notice Regarding Strengthening the Administration of Foreign Investment in Operating Value-Added Telecommunications Businesses, or the MII Notice, which prohibits value-added telecommunications services operation license holders, including Trans-regional Value-added Telecommunications Services Operation License and Telecommunications Value-added Services Operation License holders, from leasing, transferring or selling their licenses to any foreign investors in any manner, or providing any resources, premises or facilities to any foreign investors for illegal operation of telecommunications services business in the PRC. The MII Notice also requires that, (1) value-added telecommunications services operation license holders or their shareholders must directly own the domain names and trademarks used by such license holders in their daily operations; (2) each license holder must have necessary facilities for its approved business operations and maintain such facilities in the regions specified by its license; and (3) all value-added telecommunications service providers are required to maintain network and Internet security in accordance with the standards set forth in relevant PRC regulations. If a license holder fails to comply with the requirements in the MII Notice and fails to remedy such non-compliance within a designated period, the MIIT or relevant CABs may take administrative actions against such license holder, including revocation of their valued-added telecommunications services operation licenses. We provide our services through our controlled affiliated entity that owns Value-added Telecommunications Services Operation Licenses. We believe our controlled affiliated entity is in compliance with the MII Notice.

Regulations Concerning the Software Development Industry

Software Products

On March 1, 2009, the MIIT issued the Administrative Measures for Software Products, or the Measures for Software Products, to regulate the development, production, sale, and import and export of software products, including computer software, software embedded in information systems and equipments, and computer software provided in conjunction with other information or technology services. Any entity or individual shall not develop, produce, sell and import or export any software product which infringes upon the intellectual property rights of third parties, contains computer viruses, endangers computer system security, is not in compliance with the software standard specification of the PRC, or contains contents prohibited under PRC laws and regulations. To that end, for any software products, the Measures for Software Products require registration and filing with the provincial level software registration institutions authorized to accept and review software products registration applications. Once accepted for review, the software product registration application shall be filed with and publicly announced by the MIIT, and if no objection is received within a seven-working-day publication period, a software registration number and a software product registration certificate will be granted. A software registration certificate is valid for five years and may be renewed upon expiration. We have obtained a Software Company Certification, as issued by the Technology and Information Bureau of Shenzhen City (R2007-0033).

26

Software Enterprises

A PRC enterprise that develops one or more software products and meets the Certifying Standards and Administrative Measures for Software Enterprises (Proposed), promulgated by the MII, Ministry of Education, Ministry of Science and Technology and the State Administration of Taxation, or the SAT on October 16, 2000, can be certified as a “software enterprise.” The certification standards for software enterprises include the following:

-

the applicant shall be an enterprise established in PRC which engages in the business of computer software development and production, system integration, application service, etc., and whose operating revenue is primarily derived from the above referenced business activities;

-

the enterprise develops one or more software products or possesses one or more intellectual property rights of software products, or provides technical services such as computer information system integration that has passed qualification and grade certification;

-

the proportion of technical staff in the work of software development and technical service shall be no less than 50% of the total staff in the enterprise;

-

the applicant shall possess relevant technical equipments and premises necessary for developing software and providing relevant services;

-

the applicant shall possess methods and ability to safeguard the qualify of the software products and the technical services;

-

the development fund for software technique and products shall be above 8% of the enterprise’s annual software income; and

-

the annual sale income of software shall be more than 35% of the total annual income of the enterprise, with the income of self-developed software more than 50% of the software sales income;

-

the enterprise has clearly-established ownership, standardized management and complies with disciplines and laws.

Enterprises that qualified as “software enterprises” are entitled to certain preferential treatments in the PRC. According to the Circular on Relevant Policies for Encouraging the Development of the Software and Integrate Circuit Industries (Circular No. 25) (2002) by the Ministry of Finance and the General Administration of Customs State Administration of Taxation, or the SAT, newly-established software manufacturing enterprises (i.e. those established after July 1, 2000) may be exempt from income tax in the first two years of profitability and enjoy 50% income taxes reduction for the next three years, such policy is known as the “Two Free, Three Half” preferential policy. On February 22, 2008, the Ministry of Finance and SAT promulgated the Notice on Several Preferential Policies in Respect of Enterprise Income Tax, or the Notice 2008 No. 1, which reiterated that a software production enterprise newly established within China may, upon certification, enjoy the Two Free, Three Half preferential treatment. On April 24, 2009, the Ministry of Finance and SAT promulgated the Notice on Several Issues Relevant to the Implementation of the Preferential Policies on Enterprise Income Tax, which states that, the software production enterprises and the integrated circuit production enterprises established prior to the end of 2007 may, upon certification, enjoy the preferential policies on the enterprise income tax reductions and exemptions within specified periods as provided in the Notice 2008 No. 1. An enterprise which became profitable in or before 2007 and started enjoying the enterprise income tax reductions and exemptions within specified periods may continue to enjoy the relevant preferential treatment from 2008 until the expiration of the specified periods.

27

Foreign Investments in Software Development Industry

According to the Catalogue of Industries for Guiding Foreign Investment amended in 2007, foreign investment is encouraged in the software development and production sector. As such, there are no restrictions on foreign investment in the software development industry in the PRC aside from business licenses and other permits that every software development entity in the PRC must obtain.

Regulations on Internet Domain Name and Content

Internet Domain Name

Internet domain names in the PRC are regulated by the Administrative Measures on the PRC Internet Domain Name, which were promulgated by the MII and which came into effect on December 20, 2004, and the Implementation Rules of Registration of Domain Name, which were promulgated by PRC’s domain name registrar, China Internet Network Information Center, or CNNIC and which came into effect on December 1, 2002, and were amended by CNNIC on June 5, 2009. Domain name service organizations accept applications for network domain names; successful applicants become holders of the registered domain names after registration. A holder needs to pay operation fees on time to keep the registered domain names, otherwise the domain name registrar may revoke the domain names. In case there is any changes to the registration information of a domain name, the holder shall file the changes with the domain name registrar within 30 days after such changes. The CNNIC is responsible for the administration of .cn domain names and domain names in Chinese language. Disputes in respect of domain names are regulated by the Measures on Resolution of Disputes regarding Domain Names which were issued by CNNIC and revised on February 14, 2006, and shall be settled by organizations approved by the CNNIC. We have obtained an Internet Registration Certification from the Shenzhen Municipal Public Security Bureau, No. 3303101901203.

Content of Internet Information

Provision of Internet information services in the PRC is regulated by the Administrative Measures on Internet Information Services adopted by the State Council on September 20, 2000. According to these measures, provision of Internet information services regarding news, publication, education, medical and health care, pharmacy and medical appliances are subject to examination, approval and regulation by relevant authorities responsible for regulating these sectors. Internet content providers are not allowed to provide services beyond the scope of an applicable license or registration. The measures also provide a list of prohibited content on the Internet. Internet information service providers are required to monitor and censor the information on their websites, and when prohibited content is found, they shall terminate the transmission immediately, keep the relevant record and report immediately to relevant authorities.

According to these measures, commercial Internet information service providers must obtain a License for Internet Content Providers, or ICP license, in order to engage in such business. Moreover, provision of ICP services in multiple provinces, autonomous regions and centrally administered municipalities may require a trans-regional ICP license. We have obtained an ICP license (ICP No. 07047476).

28

On November 6, 2000, the MII issued the Regulations for the Administration of Internet Electronic Notice Services to regulate the provision of information via Internet in the form of, among others, electronic bulletin boards, electronic whiteboards, electronic forums, Internet chat-rooms and message boards. The Internet electronic bulletin service providers are required to record the content and time of information released, the website or domain name in the electronic bulletin system, keep such records for at least 60 days, and to provide such information to the relevant authorities upon request.

Regulations on Technology Export

The Technology Import and Export Administrative Regulations of the PRC promulgated by the State Council on December 10, 2001 and the Regulations of Protection of Computer Software which came into effect on January 1, 2002, requires approval of imports and exports of restricted technology, and registration of contracts to import or export unrestricted technology. Software is part of the technology governed by this regime. To implement this requirement, the Administrative Measures for Registration of Technology Import and Export Contracts, or the Registration Measures, was promulgated by the Ministry of Commerce, or the MOFCOM and become effective on March 1, 2009; the Administrative Measures on Prohibited and Restricted Technology Exports, or the Technology Export Measures was jointly promulgated by the MOFCOM and the Ministry for Science and Technology and become effective on May 20, 2009, and the Administrative Measures on Prohibited and Restricted Technology Imports, or the Technology Import Measures was promulgated by the MOFCOM and become effective on March 1, 2009. Pursuant to these regulations, the technology within the prohibited list for import and/or export shall not be imported and/or exported, and a permit for import and/or export shall be obtained by the importer and/or exporter if the technology to be imported and/or exported are listed within the restricted list for import and/or export. For any import or export technology, the relevant department of commerce is responsible for the registration of contracts for such technology import or export.

Regulations on Intellectual Property Rights

The PRC’s intellectual property protection regime is consistent with those of other modern industrialized countries. The PRC has domestic laws for the protection of rights in copyrights, patents, trademarks and trade secrets.

The PRC is also signatory to most of the world’s major intellectual property conventions, including:

| • |

Convention establishing the World Intellectual Property Organization (WIPO Convention) (June 3, 1980); |

| • |

Paris Convention for the Protection of Industrial Property (March 19, 1985); |

| • |

Patent Cooperation Treaty (January 1, 1994); and |

| • |

The Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPs) (December 11, 2001). |

Trademarks