Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - VALASSIS COMMUNICATIONS INC | d8k.htm |

Investor Presentation

August 2011

Exhibit 99.1

1 |

2

Safe Harbor

Cautionary

Statements

Regarding

Forward-looking

Statements

This

document

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995. Such forward-looking statements involve known and unknown risks and

uncertainties and other factors which may cause our actual results,

performance or achievements to be materially different from any future results, performance or

achievements expressed or implied by such forward-looking statements. Such

factors include, among others, the following: price

competition

from

our

existing

competitors;

new

competitors

in

any

of

our

businesses;

a

shift

in

client

preference

for

different promotional materials, strategies or coupon delivery methods, including,

without limitation, as a result of declines in newspaper

circulation;

an

unforeseen

increase

in

paper

or

postal

costs;

changes

which

affect

the

businesses

of

our

clients

and

lead

to

reduced

sales

promotion

spending,

including,

without

limitation,

a

decrease

of

marketing

budgets

which

are

generally discretionary in nature and easier to reduce in the short-term than

other expenses; our substantial indebtedness, and ability to refinance such

indebtedness, if necessary, and our ability to incur additional indebtedness, may affect our

financial health; the financial condition, including bankruptcies, of our clients,

suppliers, senior secured credit facility lenders or

other

counterparties;

certain

covenants

in

our

debt

documents

could

adversely

restrict

our

financial

and

operating

flexibility; fluctuations in the amount, timing, pages, weight and kinds of

advertising pieces from period to period, due to a change in our

clients’ promotional needs, inventories and other factors; our failure

to attract and retain qualified personnel may affect our business and

results of operations; a rise in interest rates could increase our borrowing costs; we may be

required to recognize additional impairment charges against goodwill and intangible

assets in the future; possible governmental regulation or litigation

affecting aspects of our business; clients experiencing financial difficulties, or otherwise

being

unable

to

meet

their

obligations

as

they

become

due,

could

affect

our

results

of

operations

and

financial

condition;

uncertainty in the application and interpretation of applicable state sales tax

laws may expose us to additional sales tax liability; and general economic

conditions, whether nationally, internationally, or in the market areas in which we conduct our

business, including the adverse impact of the ongoing economic downturn on the

marketing expenditures and activities of our

clients

and

prospective

clients

as

well

as

our

vendors,

with

whom

we

rely

on

to

provide

us

with

quality

materials

at

the

right prices and in a timely manner. These and other risks and uncertainties

related to our business are described in greater detail in our filings with

the United States Securities and Exchange Commission, including our reports on Forms 10-K and

10-Q and the foregoing information should be read in conjunction with these

filings. We disclaim any intention or obligation to update or revise

any forward-looking statements, whether as a result of new information, future events or otherwise. |

Delivering

value

how,

when

and

where

consumers want it

Shared Mail

•

70 million households

•

31 billion inserts distributed

Digital

•

13,000+ websites in the RedPlum Digital Network

•

75 million opt-in email list

In-Store

•

Nearly 3,000 stores in the network

at the end of first quarter 2011

Newspaper

•

15,000+ newspapers

•

6 billion inserts distributed

•

90 billion FSI pages

(including Shared Mail distribution)

Information for the year ended 12/31/10

except where noted otherwise

3 |

4

RedPlum Shared Mail

Free-standing inserts (FSI) -

Co-op newspaper inserts

Coupon and promotion clearing

Digital portfolio

In-store media

Canadian media operations

Sweepstakes/security consulting

Direct mail sampling/advertising

Loyalty marketing software

Newspaper inserts

On-page newspaper advertising (ROP)

Newspaper polybag sampling/advertising

Door hanger sampling/advertising (Direct-to-Door)

Shared mail wrap

Shared mail inserts

Saturation mail

List services

Neighborhood Targeted

RedPlum Free-standing Inserts

International, Digital

Media & Services

$479.9

M +7.9%*

$367.6M +1.7%*

$178.8M +12.5%*

$1,307.2

M +2.2%*

2010 Segment

Revenue/Profit

$156.8M +42.3%*

2010 Total

$2,333.5M +4.0%*

$225.0M*** +23.0%*

$20.6M -43.3%*

$24.9M +116.5%*

$22.7M

-9.2%* *Compared to 2009

segment revenue and profit, respectively **Compared to 2Q10 segment revenue

and profit, respectively ***Total segment profit is a non-GAAP financial

measure. Important information regarding operating results and

reconciliations

of

non-GAAP

financial

measures

to

the

most

comparable

GAAP

measures

may

be

found

under

“Reconciliation of Non-GAAP Financial Measures”

on slides 18-22.

$88.8

M -23.6%**

$89.2M -5.7%** $50.0M +16.8%**

$337.2

M +3.3%**

2Q11 Segment

Revenue/Profit

(unaudited)

$47.7M

+17.5%**

2Q11 Total

$565.2M

-2.5%** $63.2M*** +4.6%** $0.8M

-84.9%** $8.3M

-27.2%** $6.4M

+106.5%** |

5

Diversification -

2010

Revenue by Product

Revenue by Client

Other

1.9%

Direct Marketers, 1.9%

Financial, 2.2%

Discount Stores, 3.2%

Satellite

5.0%

Telecom

7.5%

Consumer Services

8.8%

Restaurants

12.2%

Specialty Retail

16.4%

Grocery & Drug

19.7%

Consumer

Packaged Goods

21.2%

Shared Mail

56.0%

Neighborhood

Targeted

20.6%

Free-standing

Insert

15.7%

IDMS

7.7% |

Shared

Mail Performance – Newspaper Coverage Correlation

Sources:

Valassis Internal Tracking for Shared Mail pieces per package data for calendar

year 2010. Newspaper Penetration: Audited and Paid newspapers (major and

local) with over 100k circulation in the Top 75 Designated Marketing Areas (DMA’s) for 2010 where shared mail is distributed.

There is no newspaper coverage greater than 40% in the Top 75 DMA's.

Low Newspaper Coverage = Larger Shared Mail Packages

7.0

8.0

9.0

10.0

11.0

12.0

< 15%

15-20%

21-25%

26-30%

31-35%

36-40%

Newspaper Penetration

Combined SM Pieces Per Package is 10.7 in

DMA’s with 25% or less newspaper coverage

Combined SM Pieces Per Package is 8.5

in DMA’s with > 26% newspaper coverage |

7

Source: BIGresearch Simultaneous Media Survey, June 2010

Power of Value-Oriented Products

Purchase Category

Electronics

Apparel

Home

Improvement

Grocery

Eating

Out

Word of Mouth

43%

34%

33%

39%

50%

Circulars/ Inserts

24%

26%

21%

40%

27%

TV Broadcast

28%

23%

22%

26%

26%

Internet

25%

19%

12%

13%

15%

Email

24%

26%

11%

15%

20%

Coupons

21%

31%

18%

71%

53% |

8

What Sets Valassis Apart? Our Targeting & Portfolio

Hypothetical Retail Example

Newspaper Only

Buy

Valassis

Optimized

Recommendation

# of Stores

45

45

Newspaper

370,583

188,747

Shared Mail

0

180,449

Total Distribution

370,583

369,196

% of Stores Covered

43.5%

66.4%

% of Targeted HH’s Covered

40.3%

91.1%

Sales Dollars Covered

$7.1M

$10.8M |

9

Long-term Growth Strategy

Drive sustainable revenue and profit growth

•

Shared Mail

–

Benefits from declining newspaper circulations

–

3 billion more Shared Mail inserts delivered in 2010 vs. 2009

–

Strong operating leverage

•

FSI

–

Marketers’

response to consumers’

demand for value drives unit

growth;

89.6%

of

all

coupon

delivery

(1)

–

Marketers distributed a record-breaking

332

billion

coupons

in

2010

(2)

•

In-Store

–

Better concept for retailers and consumers

–

Unique business model for retailers

–

Retailer network is growing

(1)

Source:

NCH

Coupon

Fact

Report

–

Mid-year

2011

(NCH

Marketing

Services,

Inc.

is

a

Valassis

company)

(2)

Source:

NCH

Coupon

Fact

Report

–

Year-end

2010 |

10

Long-term Growth Strategy (continued)

•

Digital

–

Ongoing investment

–

Expanding digital portfolio

–

Opportunity for integration of offline and online media

•

Cash Flow Utilization

–

Improve EPS

Share repurchase

–

Invest in the business

New client development

New product development

Acquisitions

Secure print

Email

Display ads

Coupon to Card/ID

Mobile offer to ID

Drive sustainable revenue and profit growth |

11

2011 Guidance

Full-year

2011

Guidance

(as

of

7/28/11)

(1)

Diluted earnings per share

Diluted

cash

earnings

per

share

(2)

Adjusted EBITDA

(2)

Capital expenditures

$2.76

$3.71

Approximately $355 million

Approximately $30 million

(1)

All data are as of July 28, 2011. This guidance by management was based on

the economic environment as of such date. Actual results may differ materially. No

reference (oral or written) to such data should be construed as an update,

revision, confirmation or clarification of same. (2)

Diluted cash earnings per share and Adjusted EBITDA are non-GAAP financial

measures. Important information regarding operating results and reconciliations of non-

GAAP

financial

measures

to

the

most

comparable

GAAP

measures

may

be

found

under

“Reconciliation

of

Non-GAAP

Financial

Measures”

on

slides

18-22. |

12

($ in millions)

(1)

On 12/17/09, we entered into an interest rate swap agreement effective 12/31/10

fixing an amortizing notional amount (initially $300 million) of the variable rate debt under

our senior secured credit facility at an effective interest rate, based on the

current spread of 1.75%, of 3.755% per annum through 6/30/12. For additional details, refer to our

10-Q

filed

with

the

SEC

on

8/9/11

and

slide

23

for

the

amortization

schedule.

(2)

On 7/6/11, we entered into a forward-starting interest rate swap agreement

which, effective 6/30/12 (the expiration date of our existing interest rate swap agreement), will fix

an

amortizing

notional

amount

(initially

$186.25

million)

of

the

variable

rate

debt

under

our

senior

secured

credit

facility

at

an

effective

interest

rate,

based

on

the

current

spread

of

1.75%,

of

3.62%

per

annum

through

6/30/15.

For

additional

details,

refer

to

our

8-K

filed

with

the

SEC

on

7/6/11

and

slide

23

for

the

amortization

schedule.

(3)

Based on three-month LIBOR as of 6/27/11 of 0.250% plus spread.

(4)

$100 million less $50 million previously drawn and less approximately $11.0 million

in letters of credit is current available credit. Capital Structure

As of

6/30/11

Interest

Rate

Due

Cash and

equivalents

$119.0

Senior Secured Debt:

Senior

Secured

Credit

Facility

–

fixed

portion

220.0

3.755%

6/27/2016

current swap expires 6/30/12

(1)(2)

Senior

Secured

Credit

Facility

–

floating

portion

80.0

2.000%

(3)

6/27/2016

LIBOR +175

Senior

Secured

Credit

Facility

–

Revolver

-

$100mm

(4)

50.0

2.000%

(3)

6/27/2016

LIBOR +175

Senior Secured Convertible Notes

0.1

--

5/22/2033

interest no longer payable

Total Secured Debt

$350.1

Senior Unsecured Notes

260.0

6.625%

2/1/2021

fixed rate

Total Debt

$610.1

Total Net Debt

$491.1

Current Market Capitalization

1,174.4

50.167M fully diluted shares

Total Capitalization

$1,665.5

8/9/11 closing price of $23.41

Comments |

13

Debt Refinancing and Interest Rate Hedging

•

Refinanced our existing senior secured credit facility with a new

senior secured credit facility in June 2011.

–

Includes a $300 million Term Loan A and a $100 million revolving

line of

credit, of which $50 million was drawn at closing (exclusive of any

outstanding letters of credit).

–

Expected to save $2.4 million in cash interest expense in the second

half of 2011.

–

Provides increased flexibility in how we can deploy cash flow.

•

Entered into a new swap agreement in July 2011 (effective June 30,

2012, upon the expiration of our existing interest rate swap

agreement).

–

Fixed the underlying interest rate for a portion of our variable

rate debt

under our new senior secured credit facility at 1.8695%.

–

After giving effect to the swap agreement, our effective interest rate for

the notional amount of the swap, based on the current spread of 1.75%,

will be 3.62% per annum through June 30, 2015.

–

The initial notional amount is $186,250,000 and amortizes quarterly

through the expiration date. For the amortization schedule see slide

23. |

14

Second Quarter 2011 Financial Highlights

•

2Q11

Adjusted

Net

Earnings

(1)

were

$33.7

million,

an

increase

of

30.6%

from

$25.8

million

for

the

prior

year

quarter.

•

2Q11

Adjusted

Diluted

Earnings

Per

Share

(1)

was

$0.67,

an

increase of 36.7% from $0.49 for the prior year quarter.

•

Total cash was $119.0 million at June 30, 2011, a decrease of

$111.2 million from March 31, 2011, due primarily to a net debt

repayment of $112.2 million and share repurchases of $60.3 million;

offset, in part, by cash generated from operations of $73.1 million in

the quarter.

•

Stock Repurchase Update: During the quarter, we repurchased

$60.3 million, or 2.1 million shares, of our common stock at an

average price of $28.14 per share, including commissions, under

our stock repurchase program. During the first half of the year, we

have repurchased $105.9 million, or 3.8 million shares, of our

common stock.

(2)

(1)

Adjusted net earnings and adjusted diluted earnings per share are non-GAAP

financial measures. Important information regarding operating

results

and

reconciliations

of

non-GAAP

financial

measures

to

the

most

comparable

GAAP

measures

may

be

found

under

“Reconciliation

of

Non-GAAP

Financial

Measures”

on

slides

18-22.

(2)

Our ability to make stock repurchases may be limited by the documents governing our

indebtedness. |

15

•

Consumer demand for value-oriented media and clients’

desire for measurable results

•

Value proposition

–

long-term newspaper coverage declines = shift to shared mail

(improved margins)

–

one-of-a-kind shared mail distribution

–

shared mail and newspaper blended solution (plus integration

of online media)

–

digital and in-store contribution

•

Low-cost capital structure

•

Cash flow yield

•

Experienced, results-oriented management team

Summary |

16

Questions |

17

Appendix |

18

Reconciliation of Non-GAAP Financial Measures

Non-GAAP Financial Measures

*We define adjusted EBITDA as net earnings before interest expense, net, other

non-cash expenses (income), net, income taxes, gain or loss on

extinguishment of debt, depreciation, amortization, stock-based compensation

expense, and News America litigation settlement proceeds, net of related

payments.

We

define

diluted

cash

EPS

as

net

earnings

per

common

share,

diluted,

plus

the

per-share

effect

of

depreciation,

amortization,

stock-based

compensation expense and loss on extinguishment of debt, net of tax, less the

per-share effect of capital expenditures and News America litigation

settlement proceeds, net of tax and related payments. We define adjusted net

earnings and adjusted diluted EPS as net earnings and diluted EPS

excluding

the

effect

of

News

America

litigation

settlement

proceeds,

net

of

tax

and

related

payments,

and

loss

on

extinguishment

of

debt,

net

of

tax.

We

define total segment profit as earnings from operations excluding a gain from News

America litigation settlement proceeds, net of related payments. Adjusted

EBITDA, adjusted net earnings, adjusted diluted EPS, diluted cash EPS and total segment profit are non-GAAP financial measures commonly

used

by

financial

analysts,

investors,

rating

agencies

and

other

interested

parties

in

evaluating

companies,

including

marketing

services

companies.

Accordingly, management believes that these non-GAAP measures may be useful in

assessing our operating performance and our ability to meet our debt service

requirements. In addition, these non-GAAP measures are used by management to measure and analyze our operating performance and,

along

with

other

data,

as

our

internal

measure

for

setting

annual

operating

budgets,

assessing

financial

performance

of

business

segments

and

as

a

performance criteria for incentive compensation. Management also believes

that diluted cash EPS is useful to investors because it provides a measure

of our profitability on a more comparable basis to historical periods and provides

a more meaningful basis for forecasting future performance, by

replacing

non-cash

amortization

and

depreciation

expenses,

which

are

currently

running

significantly

higher

than

our

annual

capital

needs,

with

actual

and forecasted capital expenditures. Additionally, because of

management’s focus on generating shareholder value, of which profitability is a primary

driver,

management

believes

these

non-GAAP

measures,

as

defined

above,

provide

an

important

measure

of

our

results

of

operations.

However,

these

non-GAAP

financial

measures

have

limitations

as

analytical

tools

and

should

not

be

considered

in

isolation

from,

or

as

alternatives

to,

operating income, cash flow, EPS or other income or cash flow data prepared in

accordance with GAAP. Some of these limitations are: adjusted EBITDA does not

reflect our cash expenditures for capital equipment or other contractual commitments;

although

depreciation

and

amortization

are

non-cash

charges,

the

assets

being

depreciated

or

amortized

may

have

to

be

replaced

in

the

future,

and

adjusted EBITDA does not reflect cash capital expenditure requirements for such

replacements; adjusted

EBITDA

and

diluted

cash

EPS

do

not

reflect

changes

in,

or

cash

requirements

for,

our

working

capital

needs;

adjusted EBITDA does not reflect the significant interest expense or the cash

requirements necessary to service interest or principal payments on our

indebtedness;

adjusted

EBITDA

does

not

reflect

income

tax

expense

or

the

cash

necessary

to

pay

income

taxes;

adjusted EBITDA, adjusted net earnings, adjusted diluted EPS, diluted cash EPS and

total segment profit do not reflect the impact of earnings or charges

resulting from matters we consider not to be indicative of our ongoing operations; and

other

companies,

including

companies

in

our

industry,

may

calculate

these

measures

differently

and

as

the

number

of

differences

in

the

way

two

different companies calculate these measures increases, the degree of their

usefulness as comparative measures correspondingly decreases. Because of

these limitations, adjusted EBITDA, adjusted net earnings, adjusted diluted EPS, diluted cash EPS and total segment profit should not be

considered as measures of discretionary cash available to us to invest in the

growth of our business or reduce indebtedness. We compensate for these

limitations by relying primarily on our GAAP results and using these non-GAAP financial measures only supplementally. Further important

information

regarding

reconciliations

of

these

non-GAAP

financial

measures

to

their

respective

most

comparable

GAAP

measures

can

be

found

on

slides 19-22. |

19

Reconciliation of Full-year 2011 Adjusted EBITDA Guidance to

Full-year

2011

Net

Earnings

Guidance

(1)

:

Full-year 2011

Guidance

($ in millions)

Net Earnings

$138.3

plus: Interest expense, net

Income taxes

Depreciation and amortization

Loss on extinguishment of debt

less: Other non-cash income

EBITDA

plus: Stock-based compensation expense

36.7

89.0

62.5

16.3

(3.4)

$339.4

15.6

Adjusted EBITDA

$355.0

(1)

Due to the forward-looking nature of adjusted EBITDA, information necessary to

reconcile adjusted EBITDA to cash flows from operating activities is not

available without unreasonable effort. We believe that the information necessary to reconcile these

measures is not reasonably estimable or predictable.

|

20

Reconciliation of Full-year 2011 Diluted Cash EPS Guidance to

Full-year 2011 Diluted EPS Guidance:

Full-year

2011

Guidance

Net Earnings (in millions)

$138.3

Diluted EPS

plus effect of:

Loss on extinguishment of debt and related charges, net

of tax

Depreciation

Amortization

Stock-based compensation expense

less effect of:

Capital expenditures

$2.60

(1)

0.22

0.93

0.24

0.29

(0.57)

Diluted Cash EPS

$3.71

Shares Outstanding (in thousands)

53,100

(2)

(1)

Includes the effect of $8.2 million in costs, net of tax, related to the

extinguishment of our 8¼% Senior Notes due 2015 during the first quarter of

2011, and $3.4 million in costs, net of tax, related to the refinancing of our

senior secured credit facility. (2)

Shares outstanding for 2011 is based on the estimated 53.1 million fully diluted

shares in our original full-year 2011 financial guidance reported on

Dec. 15, 2010 and does not include the effect of any share repurchases, option exercises or changes in dilution caused by movement in the

stock price. Actual weighted average shares outstanding, diluted, for the

quarter ended June 30, 2011 was 50.2 million. |

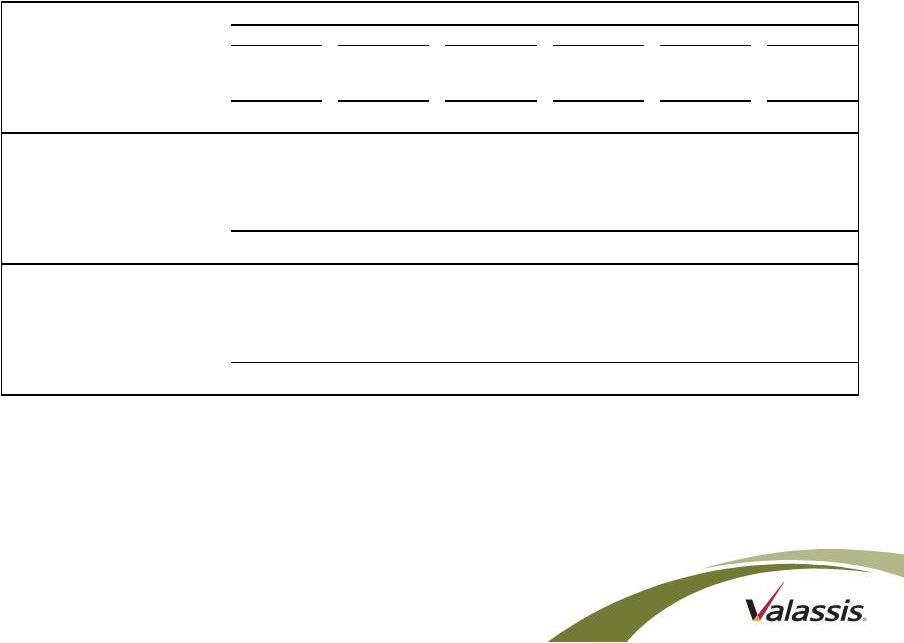

21

Reconciliation of Adjusted EBITDA to Net Earnings and Cash

Flows from Operating Activities

($ in millions)

Three Months Ended

Six Months Ended

6/30/2011

6/30/2011

Net Earnings - GAAP

30.3

$

51.7

$

plus:

Income taxes

19.8

33.1

Interest expense, net

11.6

21.2

Loss on extinguishment of debt

2.9

16.3

Depreciation and amortization

15.4

31.1

less:

Other non-cash income, net

(1.4)

(2.3)

EBITDA

78.6

$

151.1

$

Stock-based compensation expense

2.5

4.4

Adjusted EBITDA

81.1

$

155.5

$

Income taxes

(19.8)

(33.1)

Interest expense, net

(11.6)

(21.2)

Changes in operating assets and liabilities

23.4

(10.2)

Cash Flows from Operating Activities

73.1

$

91.0

$

|

22

Reconciliation of Adjusted Net Earnings and Adjusted Diluted

EPS to Net Earnings and Diluted EPS:

Three Months Ended

June 30, 2011

June 30, 2010

(in millions)

Net Earnings

Diluted EPS

Net Earnings

Diluted EPS

As reported

$30.3

$0.60

$11.1

$0.21

Loss on extinguishment of debt

and related charges, net of tax

(1)

3.4

0.07

14.7

0.28

As adjusted

$33.7

$0.67

$25.8

$0.49

(1)

Net earnings for three months ended June 30, 2011 include $3.4 million, net of tax,

in costs related to the refinancing of our senior secured credit facility and net earnings for three

months

ended

June

30,

2010

include

$14.7

million,

net

of

tax,

in

costs

related

to

the

repurchase

of

$297.8

million

of

our

8¼%

senior

notes

due

2015.

Reconciliation of Segment Profit to Earnings from Operations

Year Ended

Three Months Ended

December 31, 2010

Total segment profit

$225.0

Unallocated amounts:

Gain from litigation settlement

490.1

Earnings from operations

$715.1

$63.2

June 30, 2011

(in millions)

$63.2

--- |

23

Senior Secured Credit Facility Principal Balance and

Interest

Rate

Swaps

Schedule

(1)

(1)

The total principal balances reflected in the table represent the average balance

per quarter shown. However, pursuant to the terms of the credit agreement, the principal

amount of the term loan A amortizes on the last day of each quarter in the amount

of $3.75 million for each of the quarters shown above. The amounts included in this

schedule assume that no further amounts will be drawn or repaid on the revolving

line of credit. (2)

The fixed amounts are the quarterly notional amounts of (i) our $300 million

December 2009 interest rate swap that amortizes by $40 million per quarter through June 2012,

and (ii) our $186.25 million July 2011 forward-starting interest rate swap that

amortizes quarterly by $2,812,000 from 6/30/12 through 9/30/13 and terminates on 6/30/15. For

additional details on the amortization schedule after 9/30/13, refer to our 8-K

filed with the SEC on 7/6/11. (3)

The

floating

amount

represents

the

difference

between

the

outstanding

principal

amounts

of

the

term

loan

A

and

revolving

line

of

credit

less

the

notional

amount

of

the

applicable interest rate swap, each as of the date indicated.

(4)

The rate applied to the fixed amounts indicated above is based on the interest rate

swap agreement in effect as of the date indicated. See footnote (2) and slide 12 for

additional information.

(5)

The actual spread will be based upon the applicable margin in effect at the

time. As of 6/30/11, the applicable margin was 1.75%. (6)

For

the

definition

of

Adjusted

LIBOR,

see

the

definition

for

“Adjusted

LIBO

Rate”

included

in

our

credit

agreement

filed

as

an

exhibit

to

the

8-K

filed

with

the

SEC

on

7/1/11.

(000's)

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Fixed

amount

(2)

220,000

$

180,000

$

140,000

$

100,000

$

186,250

$

183,438

$

Floating

amount

(3)

130,000

166,250

202,500

238,750

148,750

147,813

Total

350,000

$

346,250

$

342,500

$

338,750

$

335,000

$

331,250

$

Applicable fixed rate

(4)

Swap rate

2.0050%

2.0050%

2.0050%

2.0050%

1.8695%

1.8695%

+

Spread

(5)

1.5% to 2.0%

Effective fixed rate

Applicable floating rate

Adjusted

LIBOR

(6)

+

Spread

(5)

1.5% to 2.0%

Effective floating rate

Senior

Secured

Credit

Facility

Principal

Balance

During

Quarter

Ended

(1) |