Attached files

| file | filename |

|---|---|

| 8-K - MEADOWBROOK INSURANCE GROUP INC 8-K 8-9-2011 - MEADOWBROOK INSURANCE GROUP INC | form8k.htm |

| EX-99.1 - EXHIBIT 99.1 - MEADOWBROOK INSURANCE GROUP INC | ex99_1.htm |

Exhibit 99.2

Investor Supplement

Second Quarter Update - 2011

2

Forward-Looking Statements

Certain statements made by Meadowbrook Insurance Group, Inc. in this

presentation may constitute forward-looking statements including, but not limited

to, those statements that include the words "believes," "expects," "anticipates,"

"estimates," or similar expressions. Please refer to the Company's most recent

10-K, 10-Q, and other Securities and Exchange Commission filings for more

information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the

following: the frequency and severity of claims; uncertainties inherent in reserve

estimates; catastrophic events; a change in the demand for, pricing of,

availability or collectability of reinsurance; increased rate pressure on premiums;

obtainment of certain rate increases in current market conditions; investment

rate of return; changes in and adherence to insurance regulation; actions taken

by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions.

Meadowbrook is not under any obligation to (and expressly disclaims any such

obligation to) update or alter its forward-looking statements whether as a result

of new information, future events or otherwise.

presentation may constitute forward-looking statements including, but not limited

to, those statements that include the words "believes," "expects," "anticipates,"

"estimates," or similar expressions. Please refer to the Company's most recent

10-K, 10-Q, and other Securities and Exchange Commission filings for more

information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the

following: the frequency and severity of claims; uncertainties inherent in reserve

estimates; catastrophic events; a change in the demand for, pricing of,

availability or collectability of reinsurance; increased rate pressure on premiums;

obtainment of certain rate increases in current market conditions; investment

rate of return; changes in and adherence to insurance regulation; actions taken

by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions.

Meadowbrook is not under any obligation to (and expressly disclaims any such

obligation to) update or alter its forward-looking statements whether as a result

of new information, future events or otherwise.

3

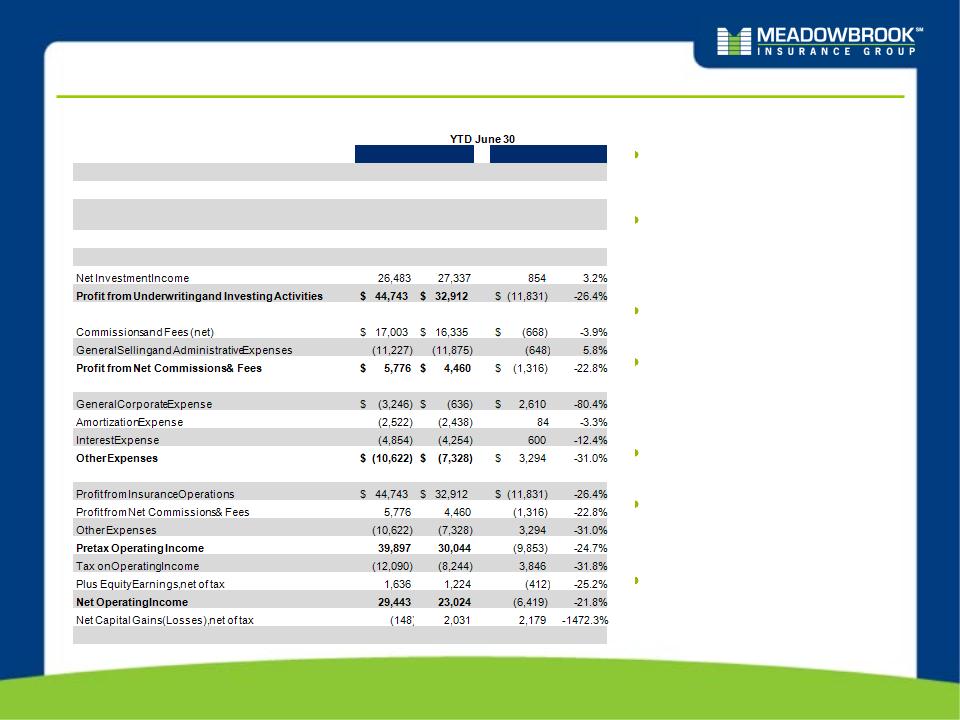

Six Months Ended 2011 vs. 2010 Comparison

Underwriting and Investing

Activities

Activities

Top line earned premium growth

driven primarily by growth within our

existing programs and new business

from recent years.

driven primarily by growth within our

existing programs and new business

from recent years.

Excluding prior year development,

profit from underwriting activities has

increased meaningfully year over

year.

profit from underwriting activities has

increased meaningfully year over

year.

Net Commissions & Fees

Decline in fee and commission

revenue is driven by conversion of

USSU to our paper.

revenue is driven by conversion of

USSU to our paper.

The increase in GS&A relates

primarily to investments in sales

initiatives to stimulate revenue growth

in net commissions and fees.

primarily to investments in sales

initiatives to stimulate revenue growth

in net commissions and fees.

Other Expenses

General Corporate expenses are

down as a result of a reduction in the

variable compensation accrual.

down as a result of a reduction in the

variable compensation accrual.

Interest expense is down due to a

decrease in the average outstanding

debt (term loan).

decrease in the average outstanding

debt (term loan).

Taxes

Taxes are lower because tax exempt

interest accounts for a larger portion

of pre-tax income in 2011. The 2011

YTD effective tax rate on operating

income (adjusted for unusual storm

losses) is 27.7%.

interest accounts for a larger portion

of pre-tax income in 2011. The 2011

YTD effective tax rate on operating

income (adjusted for unusual storm

losses) is 27.7%.

|

|

2010

|

2011

|

|

$ Change

|

% Change

|

|

Net Earned Premium

|

$ 314,201

|

$ 352,128

|

|

$ 37,927

|

12.1%

|

|

Net Losses & Loss Adjustment Expenses-AY

|

(203,161)

|

(229,032)

|

|

(25,871)

|

12.7%

|

|

Favorable Development on Prior Accident Year Reserves

|

16,469

|

2,367

|

|

(14,102)

|

-85.6%

|

|

Policy Acquisition and Other Underwriting Expenses

|

(109,249)

|

(119,888)

|

|

(10,639)

|

9.7%

|

|

Profit from Underwriting Activities

|

$ 18,260

|

$ 5,575

|

|

$ (12,685)

|

-69.5%

|

|

|

|||||

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

|

|||||

|

Net Income

|

$ 29,295

|

$ 25,055

|

|

$ (4,240)

|

-14.5%

|

4

Six Months Ended 2011 vs. 2010 Combined Ratio Analysis

Loss and LAE Ratio

The 2011 Loss and LAE ratio includes 0.6 points of

favorable development compared to 5.3 points of

favorable development in 2010.

favorable development compared to 5.3 points of

favorable development in 2010.

The 2011 Loss and LAE ratio includes 1.6 points of

unusual storm losses compared to 0.6 points in

2010.

unusual storm losses compared to 0.6 points in

2010.

Expense Ratio

The 2011 expense ratio decreased 0.8 points in

comparison to the same 2010 period. The

decrease reflects a reduction in the variable

compensation accrual.

comparison to the same 2010 period. The

decrease reflects a reduction in the variable

compensation accrual.

*Unusual Storm Losses

The 6/30 YTD unusual storm losses (net of tax) for

2010 and 2011 are $1.3M and $3.6M respectively.

2010 and 2011 are $1.3M and $3.6M respectively.

The 6/30 QTD unusual storm losses (net of tax) for

2010 and 2011 are $1.3M and $4.1M respectively.

2010 and 2011 are $1.3M and $4.1M respectively.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2011 Return on Average Equity ROAE Contribution Estimates Ex Unusual Storm Losses With Unusual Storm Losses Combined Ratio 96.5% 97.4% Underwriting Margin 3.5% 2.6% x Underwriting Leverage (NEP / Equity) 1.28 1.28 ROAE from Underwriting 4.4% 3.4% NII / Avg. Cash and Inv. Assets 4.0% 4.0% x Investment Leverage (Avg Cash & Inv. Assets / Equity) 2.4 2.4 ROAE from Investments 9.6% 9.6% ROAE from Commission and Fee 1.5% 1.5% Amortization of intangible assets contribution to ROAE -0.8% -0.8% Holding Company contribution to ROAE -1.7% -1.7% Pretax ROAE 13.0% 12.0% Impact of taxes -3.5% -3.2% Equity earnings 0.3% 0.3% Realized Gains and Losses 0.3% 0.3% After Tax ROAE 10.1% 9.4% ROAE Excluding Unrealized Gains 10.8% 10.0%

ROAE Components 2011 Projected ROAE Including and Excluding Unusual Storm Losses

6

ROAE & Combined Ratio Illustration

We strive to deliver predictable earnings across the market cycle with a return on average

equity target of 10% - 17%.

equity target of 10% - 17%.

2010 - ROAE of 11.4%, Combined Ratio of 95.0% and Investment Yield of 4.2%

2011 - Projected ROAE of 9.4%, Combined Ratio of 97.4% and Investment Yield of 4.2%

2010A

7

Investment Portfolio Appendix

We Maintain a High Quality, Low Risk Investment Portfolio

We maintain a conservative investment portfolio

Portfolio Allocation and Quality

Low equity risk exposure

– 98% fixed income and

cash

cash

– 2% equity

High credit quality

– 99% of bonds are

investment grade

investment grade

– Average S&P rating of

AA / Moody’s of Aa3

AA / Moody’s of Aa3

Interest Rate Risk Protection

– Hold to Maturity

– High Credit Quality =

Low Historical

Impairments

Low Historical

Impairments

– Access to additional

capital if needed

capital if needed

NOTE: Data above as of June 30, 2011

|

$’s in (000’s)

|

%

Allocation 6/30/2011 |

Fair Value

|

Gross

Unrealized Gain Position |

Avg.

Moody's |

Avg.

S&P |

|

Fixed Income

|

|

|

|

|

|

|

US Government and Agencies

|

2%

|

$ 24,696

|

$ 1,373

|

Aaa

|

AAA

|

|

Corporate

|

34%

|

$ 456,077

|

$ 23,993

|

A2

|

A

|

|

Mortgage and Asset Backed

|

18%

|

$ 243,220

|

$ 13,725

|

Aaa

|

AAA

|

|

Municipal

|

43%

|

$ 571,583

|

$ 29,643

|

Aa2

|

AA+

|

|

Preferred Stock Debt

|

0%

|

$ 2,416

|

$ 492

|

Ba2

|

BB

|

|

Total Fixed Income

|

98%

|

$1,297,993

|

$ 69,226

|

|

|

|

Equities

|

|

|

|

|

|

|

Preferred Stock

|

1%

|

$ 13,881

|

$ 2,509

|

|

|

|

Mutual Funds

|

1%

|

$ 15,783

|

$ 1,020

|

|

|

|

Total Equities

|

2%

|

$ 29,664

|

$ 3,529

|

|

|

9

Municipal Bonds - June 30, 2011 Profile

Summary Profile

$571.6M market value; 43% of the

investment portfolio

investment portfolio

June 30, 2011 net unrealized gain was

$29.6M

$29.6M

Tax exempt unrealized gain $28.0M

Taxable unrealized gain $ 1.6M

Average tax equivalent yield: 5.48%

Quality Indicators & Geographic

Distribution

Distribution

Municipals vs. Entire Portfolio

|

State

|

% of Municipal Allocation

|

|

Texas

|

7.6%

|

|

New York

|

6.5%

|

|

Washington

|

6.2%

|

|

Colorado

|

3.8%

|

|

Virginia

|

3.8%

|

|

Nevada

|

3.5%

|

|

Oregon

|

3.3%

|

|

Minnesota

|

3.2%

|

|

Indiana

|

3.2%

|

|

Missouri

|

3.1%

|

|

All other

|

55.8%

|

10

Structured Securities - June 30, 2011 Profile

Summary Profile

$243.2M market value; 18% of the managed

portfolio

portfolio

June 30, 2011 unrealized gain was $13.7M

RMBS unrealized gain $11.3M

CMBS unrealized loss $ 1.3M

ABS unrealized loss $ 1.1M

Average investment yield: 5.04%

Quality Indicators

Structured vs. Entire Portfolio

Structured Profile

11

Corporate Fixed Income- June 30, 2011 Profile

Summary Profile

$456.1M market value; 34% of the investment

portfolio

portfolio

June 30, 2011 unrealized gain was $24.0M.

Average investment yield: 4.41%

Quality Indicators

Corporate vs. Entire Portfolio

Corporate Profile

|

|

Corporates

|

|

Average Quality

|

A

|

|

Investment Grade

|

98%

|

|

|

|

|

A-/A3 or Better

|

78%

|

|

AII BBB and Baa

|

20%

|

|

Not Rated

|

0%

|

|

Non Investment Grade

|

2%

|

|

Banking

|

15.1%

|

|

Healthcare/Pharmaceutical

|

13.9%

|

|

Energy

|

10.0%

|

|

Electric

|

9.6%

|

|

Technology

|

7.0%

|

|

Capital Goods

|

6.5%

|

|

Food, Beverage

|

5.1%

|

|

Chemicals

|

4.5%

|

|

Natural Gas

|

3.7%

|

|

Telecommunications

|

3.4%

|

|

All Other Sectors

|

21.2%

|

12

Government and Agency - June 30, 2011 Profile

Summary Profile

$24.7 million market value; approximately 2% of

the managed portfolio

the managed portfolio

100% rated AAA

June 30, 2011 unrealized gain was $1.4 million

Average investment yield: 3.24%

Government & Agency vs. Entire

Portfolio

Portfolio

Government vs. Agency

13

Equities - June 30, 2011 Profile

Summary Profile

$29.7million market value; 2% of the managed

portfolio

portfolio

June 30, 2011 unrealized gain was $3.5M

Preferred stock unrealized gain $2.5M

Bond mutual fund unrealized gain

$1.0M

$1.0M

Average tax equivalent yield: 8.61%

Equities vs. Entire Portfolio

Equity Mix