Attached files

| file | filename |

|---|---|

| 8-K - HINES REIT Q1 2011 PRESENTATION - HINES REAL ESTATE INVESTMENT TRUST INC | hreitq12011presentation.htm |

Exhibit 99.1

Hines Real Estate Investments, Inc., Member FINRA/SIPC, is the Dealer Manager. 6/11

Hines Real Estate Investment Trust, Inc. (Hines REIT) is closed to new investors.

Hines REIT Update

As of March 31, 2011

Jeffrey C. Hines and Gerald D. Hines

Hines History

Gerald D. Hines founded Hines Interests Limited

Partnership (Hines)1 upon a single premise: buildings

of superior quality and architectural merit backed by

responsive, professional management attract better

tenants; command higher rents; and retain their value

longer despite the ups and downs of real estate cycles.

He also imbued the organization with a constant quest

for excellence and an adherence to the highest tenets

of ethical behavior. This foundation, coupled with the

firm’s sound financial policies, has fueled Hines’

growth from a one-person endeavor to a fully

integrated, international real estate firm of

approximately 3,200 employees.

Partnership (Hines)1 upon a single premise: buildings

of superior quality and architectural merit backed by

responsive, professional management attract better

tenants; command higher rents; and retain their value

longer despite the ups and downs of real estate cycles.

He also imbued the organization with a constant quest

for excellence and an adherence to the highest tenets

of ethical behavior. This foundation, coupled with the

firm’s sound financial policies, has fueled Hines’

growth from a one-person endeavor to a fully

integrated, international real estate firm of

approximately 3,200 employees.

2

1Hines REIT Investors do not receive an interest in Hines or its affiliates. The performance and experience of Hines may not be

indicative of future results for Hines REIT.

indicative of future results for Hines REIT.

Ownership & Structure of Hines1

3

1All data as of December 31, 2010

LEADERSHIP

Name

Tenure w/Hines

(yrs)

Gerald D. Hines

54

Jeffrey C. Hines

29

C. Hastings Johnson

33

Charles M. Baughn

26

James C. Buie, Jr.

30

Mark A. Cover

27

Christopher D. Hughes

24

E. Staman Ogilvie

37

Thomas D. Owens

38

C. Kevin Shannahan

28

Michael J. G. Topham

35

Jerrold P. Lea

30

|

TENURE OF HINES

EXECUTIVES

|

||

|

TITLE

|

NO. OF

EMPLOYEES |

AVG.

TENURE (YEARS) |

|

EVP

|

10

|

31

|

|

SVP

|

43

|

22

|

|

VP

|

125

|

16

|

Hines Worldwide Operations

§ Approximately 3,200

employees worldwide

employees worldwide

§ Operations in 66 U.S. cities

and 17 countries worldwide

and 17 countries worldwide

§ Local market knowledge

and expertise

and expertise

4

4

Superior Property Management

5

TENANT SATISFACTION

TENANT RETENTION

HIGHER OCCUPANCY

PROPERTY

OUTPERFORMANCE

OUTPERFORMANCE

|

TENURED HINES PROPERTY MANAGEMENT AND LEASING PERSONNEL

|

|

|

|

AVERAGE HINES

U.S. TENURE (YRS)1

|

|

Property Managers

|

9+

|

|

Assistant Property Managers

|

4+

|

|

Chief Engineers and Engineering Managers

|

12+

|

|

Assistant Chief Engineers

|

7+

|

|

Building Engineers / Maintenance Technicians / Apprentice Engineers

|

5+

|

|

Marketing / Leasing Managers

|

6+

|

1Average Hines U.S. Tenures as of 12/31/2010.

Broker-Dealer Use Only. This material may not be quoted, reproduced nor shown to members of the public, nor used as sales

material for public use. Hines Real Estate Investments, Inc., Member FINRA, SIPC

material for public use. Hines Real Estate Investments, Inc., Member FINRA, SIPC

Hines REIT Portfolio*

* As of March 31, 2011

6

Corporate Headquarters

Williams Tower

Houston, Texas

Houston, Texas

One North Wacker

Chicago, Illinois

Atrium on Bay

Toronto, Ontario

Toronto, Ontario

Hines REIT Portfolio Summary

(as of March 31, 2011)

(as of March 31, 2011)

§ Holds a diversified portfolio of commercial real estate assets including:

– Primarily institutional-quality office properties

– Grocery-Anchored Retail

– Mixed-Use office

– Industrial

§ Invests through direct acquisitions and joint ventures

§ As of 3/31/11 owns directly or indirectly 59 properties:

– Over 29 million square feet

– Portfolio 89% leased, 4% above the national average

– Both domestic and international holdings:

§ 57 domestic assets totaling approximately 27.5 million square feet

§ 2 international assets totaling in excess of 1.7 million square feet

– Total real estate assets of $3.7 billion acquired

– Minimal near term rollover with an average annual lease roll of 8.81% through 2015

– Current leverage 58%

– Current refinancing exposure is approximately $286 million in 2011 and 2012 and represents

approximately 18.5% of the fund’s total debt.

approximately 18.5% of the fund’s total debt.

§ Proceeds raised in excess of $2.5 billion

§ Approximately 58,000 shareholders

§ Total shareholder distributions since inception: $511.5 million

§ Delivered annualized distributions at a rate of 5.0% - 6.35% (based on $10.08 share price) since inception

in November 2004 through June 30, 2011*

in November 2004 through June 30, 2011*

*On May 24, 2011, as required by FINRA Regulatory Notice 09-09, the board of directors of Hines REIT established an estimated

per-share value of Hines REIT’s common stock of $7.78 per share. Based upon that estimated valuation, the annualized

distribution rate is 6.5%

per-share value of Hines REIT’s common stock of $7.78 per share. Based upon that estimated valuation, the annualized

distribution rate is 6.5%

7

Hines REIT Portfolio

(as of March 31, 2011)

(as of March 31, 2011)

8

San Diego

Houston

Chicago

San Francisco

Seattle

Atlanta

Los Angeles

Richmond

Sacramento

Charlotte

Dallas

Miami

East Bay

Toronto

Minneapolis

Phoenix

Kansas City

Denver

Orlando

San Antonio

Memphis

New York

Washington, D.C.

Raleigh

Rio de Janeiro

Chase Tower

Dallas, TX

1,252,019 Square Feet

Acquired 11/07

88% leased

Minneapolis Office/Flex

Portfolio

Portfolio

Minneapolis, MN

767,859 Square Feet

Acquired 9/07

86% leased

Williams Tower

Houston, TX

1,479,764 Square Feet

Acquired 05/08

87% leased

2555 Grand Blvd

Kansas City, MO

595,607 Square Feet

Acquired 2/08

100% leased

4050/4055 Corporate

Drive

Drive

Dallas, TX

643,429 Square Feet

Acquired 05/08

100% leased

Citymark

Dallas, TX

219,117 Square Feet

Acquired 8/05

84% leased

321 North Clark

Chicago, IL

888,837 Square Feet

Acquired 4/06

75% leased

Three Huntington

Quadrangle

Quadrangle

Long Island, NY

407,912 Square Feet

Acquired 7/07

52% leased

Airport Corporate

Center

Miami, FL

1,018,428 Square Feet

Acquired 1/06

83% leased

Hines REIT Portfolio

(as of March 31, 2011)

(as of March 31, 2011)

9

San Diego

Houston

Chicago

San Francisco

Seattle

Atlanta

Los Angeles

Richmond

Sacramento

Charlotte

Dallas

Miami

East Bay

Toronto

Minneapolis

Phoenix

Kansas City

Denver

Orlando

San Antonio

Memphis

New York

Washington, D.C.

Raleigh

Rio de Janeiro

Denver Industrial

Denver, CO

484,737 Square Feet

Acquired 12/08

84% leased

5th & Bell

Seattle, WA

197,135 Square Feet

Acquired 6/07

91% leased

Seattle Design Center

Redmond, WA

390,684 Square Feet

Acquired 6/07

74% leased

Daytona-Hart Portfolio

Redmond, WA

711,974 Square Feet

Acquired 12/06, 1/07

100% leased (Daytona)

85% leased (Laguna)

1900/2000 Alameda

San Mateo, CA

254,145 Square Feet

Acquired 6/05

91% leased

1515 S Street

Sacramento, CA

349,740 Square Feet

Acquired 11/05

99% leased

3400 Data Drive

Sacramento, CA

149,703 Square Feet

Acquired 11/06

100% leased

2100 Powell

Emeryville, CA

344,433 Square Feet

Acquired 12/06

100% leased

One Wilshire

Los Angeles, CA

661,553 Square Feet

Acquired 8/07

95% leased

Hines REIT Portfolio

(as of March 31, 2011)

(as of March 31, 2011)

10

Distribution Park Rio

Rio de Janeiro, Brazil

693,115 Square Feet

Acquired 07/07

100% leased

50%1

San Diego

Houston

Chicago

San Francisco

Seattle

Atlanta

Los Angeles

Richmond

Sacramento

Charlotte

Dallas

Miami

East Bay

Toronto

Minneapolis

Phoenix

Kansas City

Denver

Orlando

San Antonio

Memphis

New York

Washington, D.C.

Raleigh

Rio de Janeiro

Weingarten Retail

Portfolio

Portfolio

Various locations

1,497,298 Square Feet

Acquired 11/08 - 3/09

93% leased

70%1

Raytheon/DirecTV

El Segundo, CA

550,579 Square Feet

Acquired 3/08

100% leased

1Italicized percentage numbers represent Hines REIT’s effective ownership in each property listed.

2Atrium on Bay was sold on June 1, 2011 for $344.8 million CAD ($353 million based on the exchange rate in effect on the date of sale)

Atrium on Bay2

Toronto, Ontario

1,077,496 Square Feet

Acquired 02/07

98% leased

Hines US Core Office Fund Portfolio

(as of March 31, 2011)1

(as of March 31, 2011)1

11

San Francisco

Houston

Chicago

Seattle

Atlanta

San Diego

Los Angeles

New York

Richmond

Charlotte

Phoenix

Sacramento

Washington D.C.

499 Park Ave

New York, NY

291,515 Square Feet

Acquired 8/03

94% leased

11%2

425 Lexington Ave

New York, NY

700,034 Square Feet

Acquired 8/03

100% leased

11%2

Riverfront Plaza

Richmond, VA

951,616 Square Feet

Acquired 11/06

97% leased

22%2

Charlotte Plaza

Charlotte, NC

625,026 Square Feet

Acquired 6/07

89% leased

22%2

Carillon

Charlotte, NC

472,222 Square Feet

Acquired 7/07

85% leased

22%2

1200 19th Street

Washington D.C.

337,486 Square Feet

Acquired 8/03

83% leased

11%2

1As of March 31, 2011, Hines REIT owned a 26.8% interest in the Hines US Core Office Fund.

2Italicized percentage numbers represent Hines REIT’s effective ownership in each property listed.

Hines US Core Office Fund Portfolio

(as of March 31, 2011)1

(as of March 31, 2011)1

12

One Shell Plaza

Houston, TX

1,230,395 Square Feet

Acquired 5/04

99% leased

11%2

Two Shell Plaza

Houston, TX

565,573 Square Feet

Acquired 5/04

97% leased

11%2

One Atlantic Center

Atlanta, GA

1,100,312 Square Feet

Acquired 7/06

90% leased

22%2

Three First National

Chicago, IL

1,423,515 Square Feet

Acquired 3/05

92% leased

18%2

One North Wacker

Chicago, IL

1,373,754 Square Feet

Acquired 3/08

94% leased

22%2

Renaissance

Square

Square

Phoenix, AZ

965,508 Square Feet

Acquired 12/07

83% leased

22%2

333 West Wacker

Chicago, IL

855,056 Square Feet

Acquired 4/06

75% leased

18%2

101 Second Street

San Francisco, CA

388,370 Square Feet

Acquired 9/04

83% leased

22%2

The KPMG Building

San Francisco, CA

379,328 Square Feet

Acquired 9/04

88% leased

22%2

Golden Eagle Plaza

San Diego, CA

449,180 Square Feet

Acquired 8/05

95% leased

22%2

Warner Center

Los Angeles, CA

808,274 Square Feet

Acquired 10/06

89% leased

18%2

720 Olive Way

Seattle, WA

300,710 Square Feet

Acquired 1/06

84% leased

18%2

Douglas Boulevard

Sacramento, CA

884,320 Square Feet

Acquired 05/07

62% leased

18%2

Wells Fargo Center

Sacramento, CA

502,365 Square Feet

Acquired 05/07

96% leased

18%2

1As of March 31, 2011, Hines REIT owned a 26.8% interest in the Hines US Core Office Fund.

2Italicized percentage numbers represent Hines REIT’s effective ownership in each property listed.

Hines REIT Portfolio Summary

Geographical Diversification

Geographical Diversification

13

REGIONAL MIX1

% OF TOTAL PORTFOLIO—BASED ON ESTIMATED AGGREGATE VALUE

1Weighted by Hines REIT’s effective ownership as of 3/31/11

CITY MIX1

% OF TOTAL PORTFOLIO—BASED ON ESTIMATED AGGREGATE VALUE

San Francisco

Houston

Chicago

Seattle

Atlanta

San Diego

Los Angeles

Washington, DC

New York

Dallas

Sacramento

Miami

Richmond

East Bay

Toronto

Charlotte

Minneapolis

Phoenix

Kansas City

San Antonio

Orlando

Memphis

Denver

ASSET CLASS MIX1

% OF TOTAL PORTFOLIO—BASED ON ESTIMATED AGGREGATE VALUE

Hines REIT Lease Rollover and Tenant Industry

14

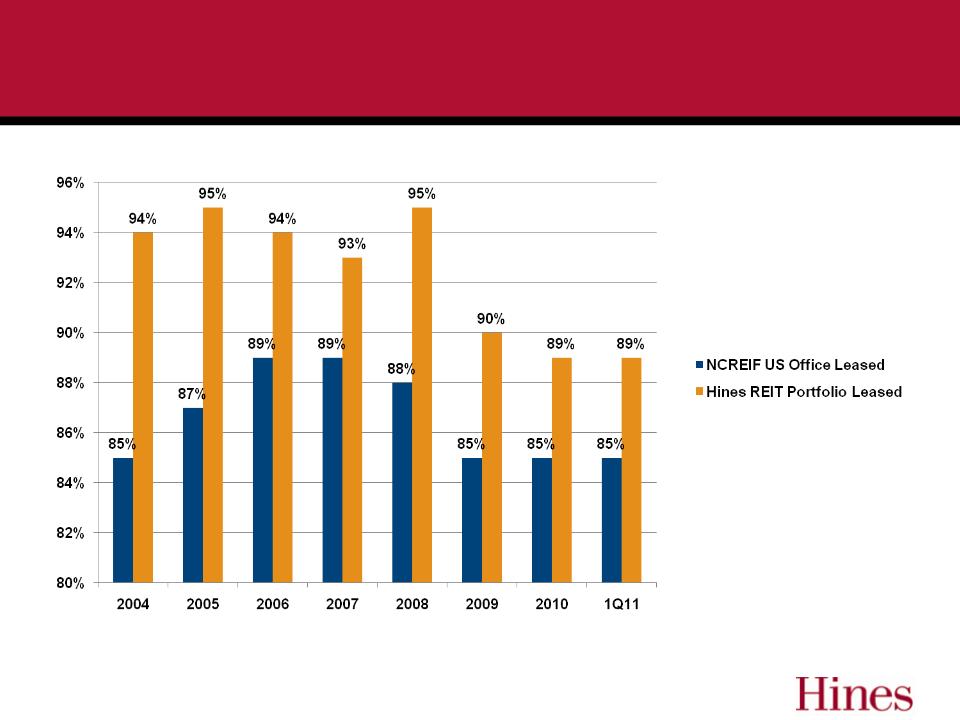

ROLLOVER1 (Portfolio occupancy was 89%)

% OF TOTAL LEASABLE SQUARE FEET IN PORTFOLIO

TENANT CREDIT QUALITY1

% OF TOTAL PORTFOLIO—BASED ON SQUARE FOOTAGE

TENANT INDUSTRY MIX1

% OF TOTAL PORTFOLIO—BASED ON SQUARE FOOTAGE

1Weighted by Hines REIT’s effective ownership as of 3/31/11

2Other represents all of the tenant industry mix categories that have less than 1% of the total portfolio

2

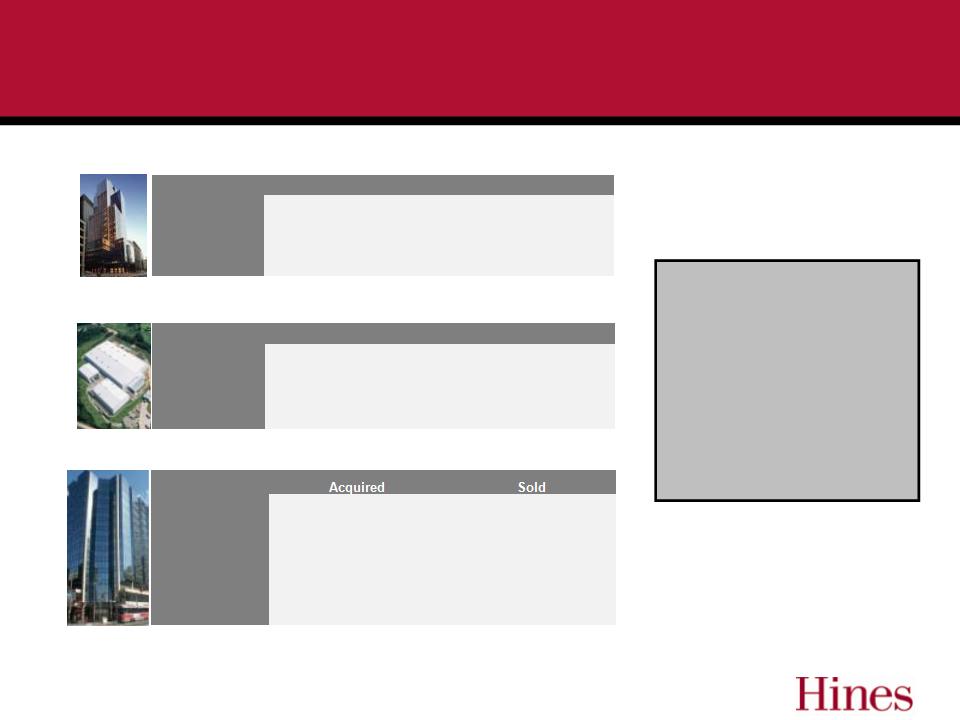

Hines REIT Strategic Dispositions

(1) Hines REIT owned an 11.67% effective ownership interest in this property prior to its sale. The REIT’s economic gain is

based

based

on its effective ownership interest prior to the sale.

15

|

|

Acquired

|

Sold

|

|

Date

|

Dec-08

|

Jan-2010 & April-2010

|

|

Price

|

$115M

|

$141M

|

|

Exchange Rate

|

2.35BRL/$USD

|

1.81BRL & 1.76BRL/$USD

|

|

Gain

|

REIT Economic gain of $11.8M

|

|

|

|

Acquired

|

Sold

|

|

Date

|

Feb-04

|

May-10

|

|

Price

|

$91.6M

|

$193M

|

|

Lease %

|

76%

|

94%

|

|

Gain

|

Economic gain of $79M (REIT economic gain of $9.6M)

(1) |

|

Since the closing of Hines REIT in

December 2009, the firm has

evaluated opportunities for

targeted asset sales.

December 2009, the firm has

evaluated opportunities for

targeted asset sales.

The proceeds from these sales

continue to support the overall

objectives of deleveraging the

portfolio, managing liquidity,

funding capital expenditures and

leasing costs, and maximizing

shareholder distributions.

continue to support the overall

objectives of deleveraging the

portfolio, managing liquidity,

funding capital expenditures and

leasing costs, and maximizing

shareholder distributions.

Araucaria, Elouveira and Vinhedo

600 Lexington(1)

Atrium on Bay

|

|

Acquired

|

Sold

|

|

Date

|

Feb-07

|

June-11

|

|

Price

|

$250M CAD

$215M USD

|

$344.8M CAD

$353M USD

|

|

Exchange Rate

|

$CAD/$0.861USD

|

$CAD/$1.023USD

|

|

Lease %

|

86%

|

98%

|

|

Gain

|

Net sales proceeds of $128.7M (USD)

|

|

Hines REIT - Tracking Occupancy

Source: NCREIF

16

Finding Success in Challenging Markets

Q1 2011

Q1 2011

§ Houston, TX - Williams Tower

– Williams Companies, an integrated natural gas company, renewed 265,000 Square

Feet (SF) for 10 years

Feet (SF) for 10 years

§ Atlanta, GA - One Atlantic Center

– National law firm Alston + Bird renewed 365,000 SF for 17 years

§ Sacramento, CA - Wells Fargo Center

– Wells Fargo Bank (subsidiary of NYSE: WFC), a nationwide, diversified, community-

based financial services company with $1.2 trillion in assets, executed a 45,000 SF

lease extension for five years

based financial services company with $1.2 trillion in assets, executed a 45,000 SF

lease extension for five years

§ Richmond, VA - Riverfront Plaza

– Morgan Stanley Smith Barney, a premier global wealth management firm, executed

a 23,000 SF lease for 11 years

a 23,000 SF lease for 11 years

17

Finding Success in Challenging Markets

Q1 2011

Q1 2011

§ Los Angeles, CA - Warner Center

– HealthNetInc. (NYSE: HNT), a managed care organization, executed a 334,000 SF

lease renewal for 10 years

lease renewal for 10 years

§ Roseville, CA - Douglas Boulevard

– Intel-GE Care Innovations, a firm that creates technology-based solutions that give

people confidence to live independently, executed a 19,000 SF lease

people confidence to live independently, executed a 19,000 SF lease

§ Los Angeles, CA - One Wilshire

– Executed three leases for a total of 13,000 SF

18

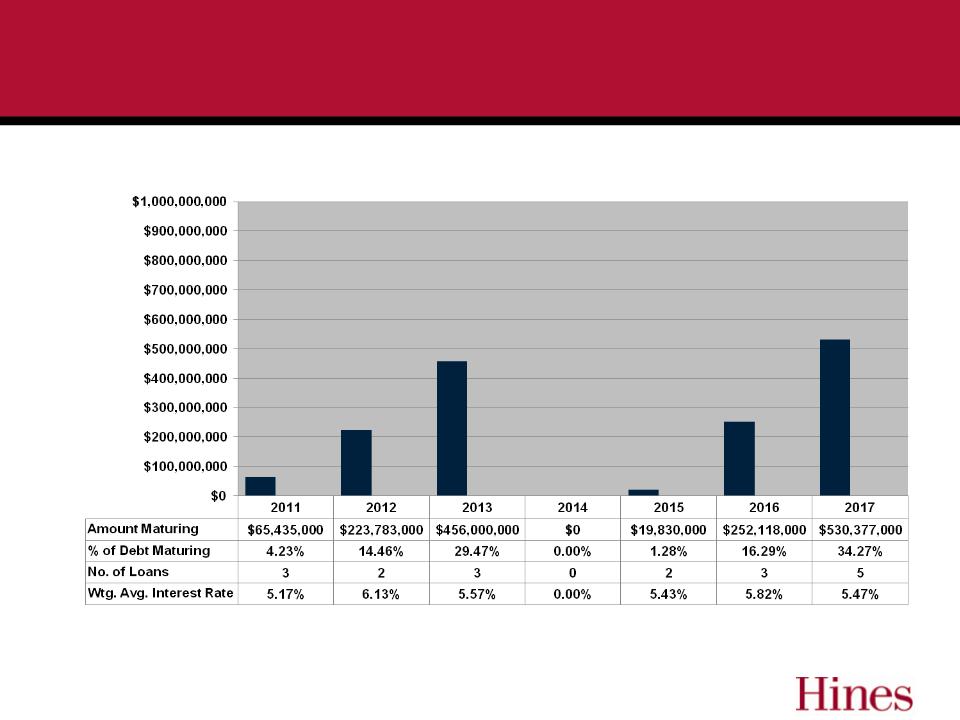

Hines REIT Debt Maturity Chart

($ in millions as of March 31, 2011)

($ in millions as of March 31, 2011)

19

Portfolio Weighted Average Interest Rate 5.64%

Hines REIT is contractually obligated to make principal payments on its outstanding notes payable for the period of April 1, 2011 through December

31, 2011, for each of the years ending December 31, 2012 through December 31, 2015 and for the period thereafter (in thousands): $$66,945,

$224,638, $457,480, $3,820, $22,833 and $771,827.

31, 2011, for each of the years ending December 31, 2012 through December 31, 2015 and for the period thereafter (in thousands): $$66,945,

$224,638, $457,480, $3,820, $22,833 and $771,827.

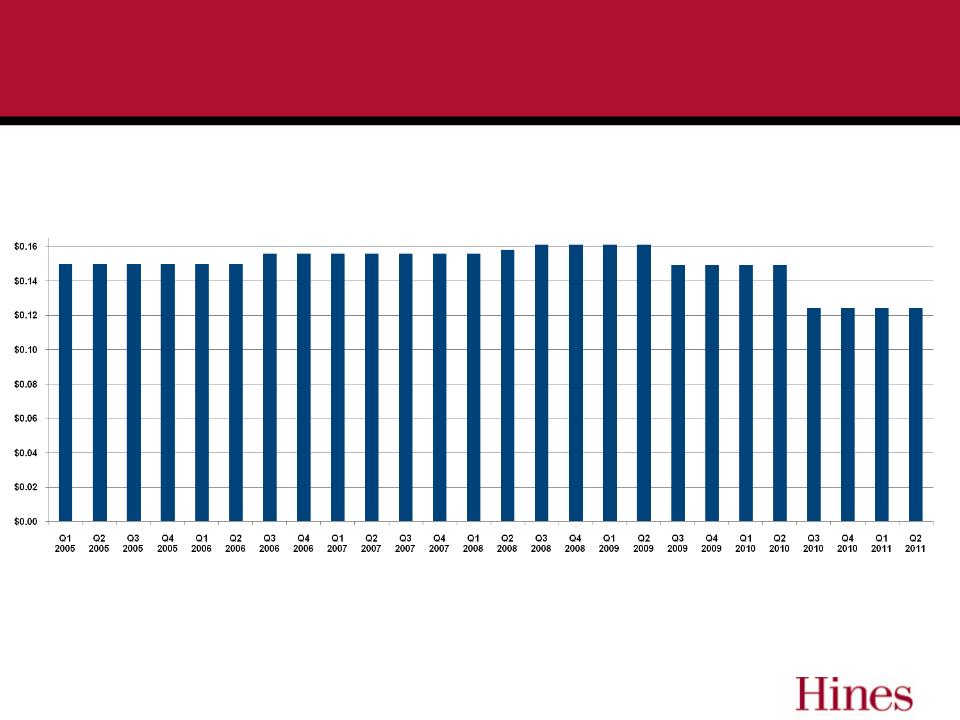

Distribution History -

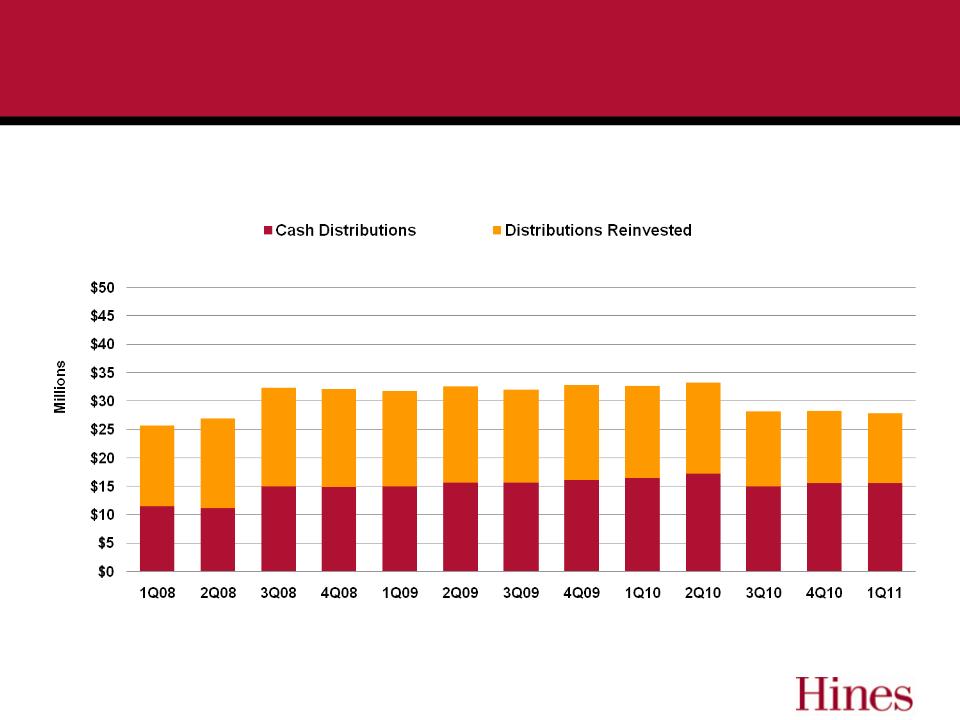

Cents Per Share Paid Quarterly

Cents Per Share Paid Quarterly

20

Relatively Stable Distribution

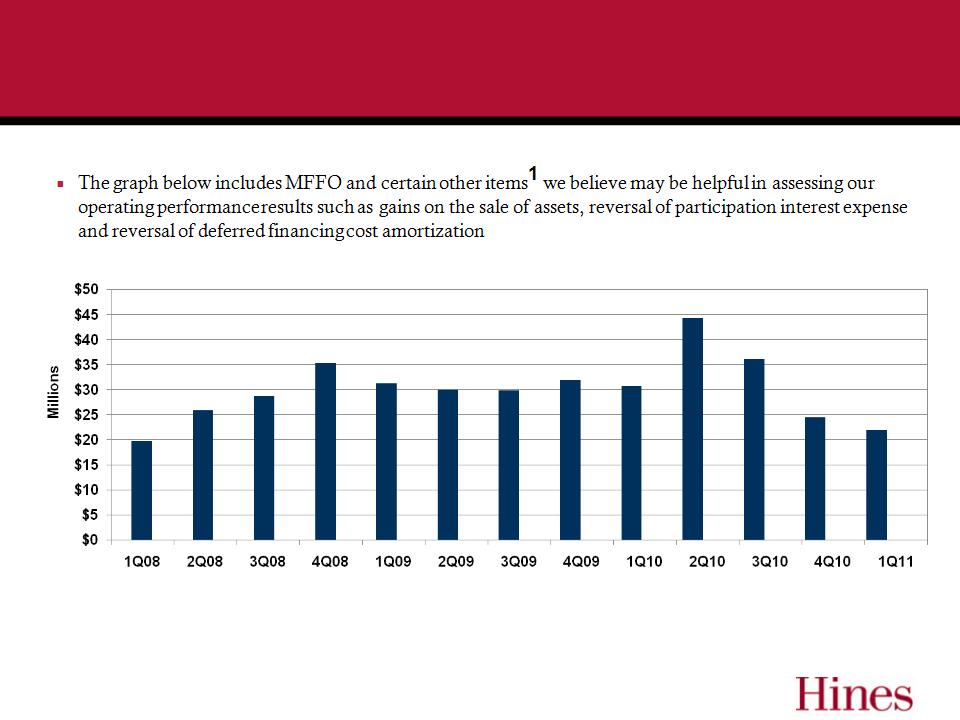

Modified Funds From Operations

§ Modified Funds From Operations (“MFFO”) is a non-

GAAP supplemental earnings-based performance

measure used to evaluate REIT operating performance.

GAAP supplemental earnings-based performance

measure used to evaluate REIT operating performance.

§ MFFO was derived by making certain adjustments to

Funds From Operations, which was originally defined by

NAREIT in 1991 and last modified in 2002.

Funds From Operations, which was originally defined by

NAREIT in 1991 and last modified in 2002.

§ Currently the IPA and certain issuers are working through

an agreed upon definition of MFFO with the SEC and

other regulators.

an agreed upon definition of MFFO with the SEC and

other regulators.

21

Evaluating Operating Performance

22

§ MFFO is used by Senior Management and the Board of Directors to evaluate operating performance

1Includes IPA-defined MFFO and gains on asset sales, as well as adjustments to reverse participation interest expense and deferred financing cost

amortization. Deferred financing costs are amortized into interest expense over the terms of the related obligations. Hines REIT records a liability in its balance

sheet related to the interests (Participation Interest) owned by Hines’ subsidiaries. This liability is based on its estimated settlement value, which is measured at

fair value based on the Company's redemption price in place as of each balance sheet date. Periodic increases in the Participation Interest, as well as

adjustments required to record this liability at fair value, are included in asset management and acquisition fees in the Company's statements of operations.

amortization. Deferred financing costs are amortized into interest expense over the terms of the related obligations. Hines REIT records a liability in its balance

sheet related to the interests (Participation Interest) owned by Hines’ subsidiaries. This liability is based on its estimated settlement value, which is measured at

fair value based on the Company's redemption price in place as of each balance sheet date. Periodic increases in the Participation Interest, as well as

adjustments required to record this liability at fair value, are included in asset management and acquisition fees in the Company's statements of operations.

Appendix 1: Evaluating Operating Performance

Funds from Operations and Modified Funds from Operations

§ Funds from Operations (“FFO”) is a non-GAAP financial performance measure defined by the National Association of Real Estate Investment Trusts

(“NAREIT”) widely recognized by investors and analysts as one measure of operating performance of a real estate company. FFO excludes items such as real

estate depreciation and amortization and gains and losses on the sale of real estate assets. Depreciation and amortization, as applied in accordance with

GAAP, implicitly assumes that the value of real estate assets diminishes predictably over time. Since real estate values have historically risen or fallen with

market conditions, it is management’s view, and we believe the view of many industry investors and analysts, that the presentation of operating results for real

estate companies by using the historical cost accounting alone is insufficient. In addition, FFO excludes gains and losses from the sale of real estate, which we

believe provides management and investors with a helpful additional measure of the historical performance of our real estate portfolio, as it allows for

comparisons, year to year, that reflect the impact on operations from trends in items such as occupancy rates, rental rates, operating costs, general and

administrative expenses and interest costs.

(“NAREIT”) widely recognized by investors and analysts as one measure of operating performance of a real estate company. FFO excludes items such as real

estate depreciation and amortization and gains and losses on the sale of real estate assets. Depreciation and amortization, as applied in accordance with

GAAP, implicitly assumes that the value of real estate assets diminishes predictably over time. Since real estate values have historically risen or fallen with

market conditions, it is management’s view, and we believe the view of many industry investors and analysts, that the presentation of operating results for real

estate companies by using the historical cost accounting alone is insufficient. In addition, FFO excludes gains and losses from the sale of real estate, which we

believe provides management and investors with a helpful additional measure of the historical performance of our real estate portfolio, as it allows for

comparisons, year to year, that reflect the impact on operations from trends in items such as occupancy rates, rental rates, operating costs, general and

administrative expenses and interest costs.

§ In addition to FFO, management uses modified funds from operations (“MFFO”) as defined by the Investment Program Association (“IPA”) as a non-GAAP

supplemental financial performance measure, to evaluate our operating performance. MFFO includes funds generated by the operations of our real estate

investments and funds used in our corporate-level operations. MFFO is based on FFO, but includes certain additional adjustments which we believe are

appropriate due to changes in the accounting and reporting rules under GAAP that have been put into effect since the establishment of NAREIT’s definition of

FFO. These changes have prompted a significant increase in the magnitude of non-cash and non-operating items included in FFO, as defined. Such items

include amortization of out-of-market lease intangible assets and liabilities and certain tenant incentives, the effects of straight-line rent revenue recognition, fair

value adjustments to derivative instruments that we have not designated as hedging instruments for accounting purposes, non-cash impairment charges and

certain other items as described in the footnotes below. We believe that MFFO more closely reflects the overall impact on the performance of our real estate

investments of occupancy rates, rental rates, property operating costs, as well as corporate-level general and administrative expenses and interest costs,

which is not immediately apparent from net income (loss).

supplemental financial performance measure, to evaluate our operating performance. MFFO includes funds generated by the operations of our real estate

investments and funds used in our corporate-level operations. MFFO is based on FFO, but includes certain additional adjustments which we believe are

appropriate due to changes in the accounting and reporting rules under GAAP that have been put into effect since the establishment of NAREIT’s definition of

FFO. These changes have prompted a significant increase in the magnitude of non-cash and non-operating items included in FFO, as defined. Such items

include amortization of out-of-market lease intangible assets and liabilities and certain tenant incentives, the effects of straight-line rent revenue recognition, fair

value adjustments to derivative instruments that we have not designated as hedging instruments for accounting purposes, non-cash impairment charges and

certain other items as described in the footnotes below. We believe that MFFO more closely reflects the overall impact on the performance of our real estate

investments of occupancy rates, rental rates, property operating costs, as well as corporate-level general and administrative expenses and interest costs,

which is not immediately apparent from net income (loss).

§ As such, we believe FFO and MFFO, in addition to net income (loss) and cash flows from operating activities as defined by GAAP, are meaningful

supplemental performance measures and are useful to investors in understanding how our management evaluates our ongoing operating performance.

However, FFO and MFFO should not be considered as alternatives to net income (loss) or to cash flows from operating activities and are not intended to be

used as liquidity measures indicative of cash flow available to fund our cash needs. Additionally, please see the limitations listed below associated with the use

of MFFO as compared to net income (loss):

supplemental performance measures and are useful to investors in understanding how our management evaluates our ongoing operating performance.

However, FFO and MFFO should not be considered as alternatives to net income (loss) or to cash flows from operating activities and are not intended to be

used as liquidity measures indicative of cash flow available to fund our cash needs. Additionally, please see the limitations listed below associated with the use

of MFFO as compared to net income (loss):

– MFFO excludes gains (losses) related to changes in estimated values of our interest rate swaps. Although we expect to hold these instruments to

maturity, if we were to settle these instruments currently, it would have an impact on our operations.

maturity, if we were to settle these instruments currently, it would have an impact on our operations.

– MFFO excludes impairment charges related to long-lived assets that have been written down to current market valuations. Although these losses are

included in the calculation of net income (loss), we have excluded them from MFFO because we believe doing so more appropriately presents the

operating performance of our real estate investments on a comparative basis.

included in the calculation of net income (loss), we have excluded them from MFFO because we believe doing so more appropriately presents the

operating performance of our real estate investments on a comparative basis.

– MFFO excludes acquisition fees payable to our Advisor. Although these amounts reduce net income, we fund such costs with proceeds from our public

offerings and acquisition-related indebtedness and do not consider these fees in the evaluation of our operating performance and determining MFFO.

offerings and acquisition-related indebtedness and do not consider these fees in the evaluation of our operating performance and determining MFFO.

23

Appendix 1: Evaluating Operating Performance

24

|

1)

|

Represents the depreciation and amortization of various real estate assets. Historical cost accounting for real estate assets in accordance with GAAP implicitly

assumes that the value of real estate assets diminishes predictably over time. Since real estate values have historically risen or fallen with market conditions, we believe that such depreciation and amortization may be of limited relevance in evaluating current operating performance and, as such, these items are excluded from our determination of FFO. This amount includes $1.1 million, $1.1 million, $1.9 million and approximately $67,000 of depreciation and amortization related to discontinued operations for the three months ended March 31, 2011 and the years ended December 31, 2010, 2009 and 2008, respectively. |

|

2)

|

Represents the gain on disposition of certain real estate investments. Although this gain is included in the calculation of net income (loss), we have excluded it from

FFO because we believe doing so more appropriately presents the operating performance of our real estate investments on a comparative basis. |

|

3)

|

Includes adjustments to equity in earnings (losses) of unconsolidated entities, net, similar to those described in Notes 1, 2 and 7 for our unconsolidated entities, which

are necessary to convert our share of income (loss) from unconsolidated entities to FFO and MFFO. |

|

|

2011-Q1

|

2010-Q4

|

2010-Q3

|

2010-Q2

|

2010-Q1

|

2009-Q4

|

2009-Q3

|

2009-Q2

|

2009-Q1

|

2008-Q4

|

2008-Q3

|

2008-Q2

|

2008-Q1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (Loss)

|

$(9,282,000) |

$14,276,000 |

$(28,302,000) |

$(8,419,000) |

$(12,938,000) |

$5,120,000 |

$(25,789,000) |

$23,549,000 |

$3,805,000 |

$(104,212,818) |

$(23,780,066) |

$8,836,804 |

$(43,186,923) |

|

Add (deduct) NAREIT defined

adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization(1)

|

25,680,000 |

27,157,263 |

28,379,702 |

27,371,787 |

28,875,107 |

31,423,724 |

31,859,012 |

31,009,829 |

31,778,589 |

32,312,877 |

32,888,148 |

32,215,784 |

25,381,478 |

|

Gain on sale of real estate(2)

|

- |

(25,098) |

- |

(18,310,535) |

(4,226,561) |

- |

- |

- |

(612,000) |

|

|

|

|

|

Adjustments to equity in earnings

(losses) of unconsolidated subsidiaries(3) |

8,863,000 |

9,027,651 |

9,306,047 |

(2,714,681) |

10,585,753 |

9,464,294 |

9,526,393 |

9,846,055 |

10,432,052 |

14,307,417 |

9,702,314 |

10,090,246 |

9,400,774 |

|

Income (loss) to minority interests (4)

|

(1,003,000) |

(1,926,908) |

(372,449) |

72,218 |

(747,212) |

(1,460,735) |

(484,670) |

(1,941,983) |

(1,316,404) |

1,519,282 |

(483,589) |

(1,294,098) |

204,838 |

|

NAREIT Defined FFO

|

24,258,000 |

48,508,908 |

9,011,299 |

(2,000,211) |

21,549,088 |

44,547,282 |

15,111,735 |

62,462,901 |

44,087,237 |

(56,073,242) |

18,326,807 |

49,848,737 |

(8,199,833) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Add (deduct) our MFFO adjustments

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Gain) loss on derivative

instruments (5) |

(5,196,000) |

(27,144,111) |

15,441,318 |

24,373,854 |

5,853,592 |

(14,207,567) |

11,700,747 |

(35,894,682) |

(10,895,939) |

74,685,772 |

10,529,600 |

(26,780,236) |

27,444,828 |

|

Impairment on land parcel(6)

|

- |

- |

810,536 |

- |

- |

- |

3,412,163 |

- |

- |

- |

- |

- |

- |

|

Other non-cash components of

revenues and expenses(7) |

(2,173,000) |

(3,752,457) |

(4,647,523) |

(1,708,545) |

(3,172,038) |

(4,183,574) |

(4,905,616) |

(3,980,490) |

(5,395,288) |

(1,993,712) |

(3,647,595) |

(4,549,551) |

(4,939,235) |

|

Acquisition fees(8)

|

- |

- |

- |

- |

- |

- |

- |

1 |

1,159,901 |

8,123,377 |

- |

1,571,500 |

1,446,500 |

|

Adjustments to equity in earnings

(losses) of unconsolidated subsidiaries(3) |

87,000 |

510,142 |

141,937 |

135,871 |

401,010 |

378,327 |

382,385 |

456,725 |

489,747 |

1,626,108 |

141,836 |

28,020 |

(27,138) |

|

Income (loss) to minority interests(4)

|

289,000 |

1,160,107 |

(398,864) |

(797,763) |

(102,989) |

560,123 |

(328,692) |

1,188,682 |

418,952 |

(2,177,781) |

(180,351) |

752,360 |

(583,750) |

|

MFFO

|

$17,265,000 |

$19,282,590 |

$20,358,702 |

$20,003,206 |

$24,528,663 |

$27,094,592 |

$25,372,722 |

$24,233,136 |

$29,864,610 |

$24,190,522 |

$25,170,297 |

$20,870,829

|

$15,141,372 |

Appendix 1: Evaluating Operating Performance

25

|

4)

|

Includes income attributable to noncontrolling interests and all adjustments to eliminate the noncontrolling interests’ share of the adjustments to convert our net

income (loss) to FFO and MFFO. |

|

5)

|

Represents components of net income (loss) related to the estimated changes in the values of our interest rate swap derivatives. We have excluded these changes in

value from our evaluation of our operating performance and MFFO because we expect to hold the underlying instruments to their maturity and accordingly the interim gains or losses will remain unrealized. |

|

6)

|

Represents impairment charges recorded in the third quarters of 2010 and 2009 in accordance with GAAP. Although such charges are included in the calculation of net

income (loss), we have excluded them from MFFO because we believe doing so more appropriately presents the operating performance of our real estate investments on a comparative basis. |

|

7)

|

Includes the following components of revenues and expenses that we do not consider in evaluating our operating performance and determining MFFO for the three

months ended March 31, 2011 and the years ended December 31, 2010, 2009 and 2008 (in thousands): |

|

a)

|

Represents the adjustments to rental revenue as required by GAAP to recognize minimum lease payments on a straight-line basis over the

respective lease terms. We have excluded these adjustments from our evaluation of the operating performance of the Company and in determining MFFO because we believe that the rent that is billable during the current period is a more relevant measure of the Company’s operating performance for such period. |

|

b)

|

Represents the amortization of lease incentives and out-of-market leases. As stated in Note 1 on the previous slide, historical cost accounting

for real estate assets in accordance with GAAP implicitly assumes that the value of real estate assets diminishes predictably over time. Since

real estate values have historically risen or fallen with market conditions, we believe that such amortization may be of limited relevance in evaluating current operating performance and, as such, these items are excluded from our determination of MFFO. |

|

|

2011-Q1

|

2010-Q4

|

2010-Q3

|

2010-Q2

|

2010-Q1

|

2009-Q4

|

2009-Q3

|

2009-Q2

|

2009-Q1

|

2008-Q4

|

2008-Q3

|

2008-Q2

|

2008-Q1

|

|

Other components of revenues and

expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Straight Line Rent Adjustments

|

$(2,350,000)

|

(2,662,719)

|

(2,933,835)

|

(723,687)

|

(1,977,490)

|

(1,552,355)

|

(2,633,424)

|

(1,831,787)

|

(3,417,929)

|

(3,566,572)

|

(4,243,951)

|

(4,652,920)

|

(3,925,028)

|

|

Amortization of Lease Incentives

|

2,815,000

|

2,442,658

|

2,237,208

|

1,957,599

|

1,787,982

|

1,468,973

|

1,301,896

|

1,264,734

|

1,270,470

|

1,471,652

|

1,076,880

|

896,599

|

773,271

|

|

Out-of-market Lease Amortization

|

(2,849,000)

|

(3,695,643)

|

(4,164,311)

|

(3,155,884)

|

(3,196,281)

|

(3,706,270)

|

(3,788,830)

|

(3,627,862)

|

(3,625,008)

|

(437,983)

|

(765,096)

|

(1,078,418)

|

(2,054,596)

|

|

Amortization of Deferred Financing Costs

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

|

Other Non-cash Components

|

211,000

|

163,247

|

213,415

|

213,427

|

213,750

|

(393,921)

|

214,741

|

214,425

|

377,180

|

539,191

|

284,572

|

285,188

|

267,118

|

|

Other components of revenues and

expenses |

$(2,173,000)

|

(3,752,457)

|

(4,647,523)

|

(1,708,545)

|

(3,172,038)

|

(4,183,574)

|

(4,905,616)

|

(3,980,490)

|

(5,395,288)

|

(1,993,712)

|

(3,647,595)

|

(4,549,551)

|

(4,939,235)

|

Appendix 1: Evaluating Operating Performance

26

|

|

|

|

8) Represents acquisition expenses and acquisition fees paid to our Advisor that are expensed in our consolidated statements of operations. We fund

such costs with proceeds from our offering and acquisition-related indebtedness, and therefore do not consider these expenses in evaluating our

operating performance and determining MFFO.

such costs with proceeds from our offering and acquisition-related indebtedness, and therefore do not consider these expenses in evaluating our

operating performance and determining MFFO.

Set forth below is additional information relating to certain items excluded from the analysis above which may be helpful in assessing our operating

results:

results:

• Pursuant to the terms of the Grocery Anchored Portfolio joint venture agreement, for the three months ended March 31, 2011, we received

distributions of approximately $670,000 and for the years ended December 31, 2010, 2009 and 2008, we received distributions of

approximately $1.1 million, $1.7 million and $161,000 in excess of our pro-rata share of the joint venture’s MFFO, respectively.

distributions of approximately $670,000 and for the years ended December 31, 2010, 2009 and 2008, we received distributions of

approximately $1.1 million, $1.7 million and $161,000 in excess of our pro-rata share of the joint venture’s MFFO, respectively.

• On January 22, 2010, we sold Distribution Park Araucaria, an industrial property located in Curitiba, Brazil, which we acquired in December

2008 for $33.0 million. Net proceeds from the sale after deducting transaction costs, fees and taxes were $34.6 million.

2008 for $33.0 million. Net proceeds from the sale after deducting transaction costs, fees and taxes were $34.6 million.

• On April 22, 2010, we sold Distributions Park Elouveira and Vinhedo, two industrial properties located in Sao Paulo, Brazil, which we

acquired in December 2008 for $83.1 million. Net proceeds from the sale after deducting transaction costs, fees and taxes were $93.3 million.

acquired in December 2008 for $83.1 million. Net proceeds from the sale after deducting transaction costs, fees and taxes were $93.3 million.

• On May 22, 2010, the Core Fund sold 600 Lexington, an office property located in New York, New York, which it acquired in February 2004.

The Core Fund’s total cost basis in 600 Lexington was approximately $103.8 million and the net proceeds from the sale after deducting

transaction costs, taxes and fees were approximately $185.9 million. Our effective ownership in this asset on the date of sale was 11.67%.

The Core Fund’s total cost basis in 600 Lexington was approximately $103.8 million and the net proceeds from the sale after deducting

transaction costs, taxes and fees were approximately $185.9 million. Our effective ownership in this asset on the date of sale was 11.67%.

• On September 14, 2010, we sold a land parcel located in Houston, Texas, which we acquired in connection with our purchase of Williams

Tower. The sales price of the land parcel was $12.8 million. Proceeds received after closing costs and fees were $11.8 million. We recorded

impairment charges of approximately $811,000 and $3.4 million for the years ended December 31, 2010 and 2009, respectively, which is

included in other losses in the accompanying condensed consolidated statements of operations but have been excluded from MFFO. See

Note 6.

Tower. The sales price of the land parcel was $12.8 million. Proceeds received after closing costs and fees were $11.8 million. We recorded

impairment charges of approximately $811,000 and $3.4 million for the years ended December 31, 2010 and 2009, respectively, which is

included in other losses in the accompanying condensed consolidated statements of operations but have been excluded from MFFO. See

Note 6.

• We received $4.0 million in net proceeds from our sale of the Williams Tower waterwall and park in December 2008.

• We received $1.2 million in net proceeds from our sale of land owned in connection with the Laguna Buildings in December 2009.

• Amortization of deferred financing costs was $709,000, $2.8 million, $2.8 million and $1.7 million for the three months ended March 31, 2011

and for the years ended December 31, 2010, 2009 and 2008, respectively, and was deducted in determining MFFO.

and for the years ended December 31, 2010, 2009 and 2008, respectively, and was deducted in determining MFFO.

• A portion of our acquisition and asset management fees are paid in equity through the Participation Interest. For the three months ended

March 31, 2011, this amount was $3.9 million. For the years ended December 31, 2010, 2009 and 2008, these amounts were $15.5 million,

$12.4 million and $18.6 million, respectively.

March 31, 2011, this amount was $3.9 million. For the years ended December 31, 2010, 2009 and 2008, these amounts were $15.5 million,

$12.4 million and $18.6 million, respectively.

• We received master lease payments of $1.2 million and $7.0 million for the years ended December 31, 2009 and 2008, respectively. These

leases were entered into in conjunction with certain asset acquisitions.

leases were entered into in conjunction with certain asset acquisitions.

• We incurred organizational and offering expenses of $3.7 million as of December 31, 2008. These expenses are paid to our Advisor and

expensed in our consolidated statement of operations.

expensed in our consolidated statement of operations.

Distribution History - Quarterly in Dollars

27

We funded our cash distributions with cash flows from operating activities, distributions received from our unconsolidated investments,

proceeds from the sales of our real estate investments and cash generated during prior periods, which had cash flows from operating activities

and distributions received from our unconsolidated investments in excess of distributions.

proceeds from the sales of our real estate investments and cash generated during prior periods, which had cash flows from operating activities

and distributions received from our unconsolidated investments in excess of distributions.

Hines REIT Repricing Discussion

§ FINRA Regulatory Notice 09-09 requires publishing estimated share value 18

months after closing of the offering (June 30, 2011 for Hines REIT). The new

share value was $7.78 based upon this most recent estimated share

valuation .

months after closing of the offering (June 30, 2011 for Hines REIT). The new

share value was $7.78 based upon this most recent estimated share

valuation .

§ The estimated share value was determined based primarily on:

– Valuations of substantially all of our real estate investments by

independent third parties;

independent third parties;

– Internal valuations of our real estate investments by the Company’s

management using methodologies that are commonly used in the

commercial real estate industry (including discounted cash flow analyses

and reviews of current, historical and projected capitalization rates for

properties comparable to those owned by the Company);

management using methodologies that are commonly used in the

commercial real estate industry (including discounted cash flow analyses

and reviews of current, historical and projected capitalization rates for

properties comparable to those owned by the Company);

– Valuations of our notes payable by an independent third party; and

– The estimated values of other assets and liabilities determined by

management as of March 31, 2011.

management as of March 31, 2011.

28

Hines REIT Exit Strategy

§ Overall goal is to maximize returns to investors

§ Exit strategy may include the targeted sale of

individual or groups of assets

individual or groups of assets

§ May also consider a sale, merger or listing on a

national exchange

national exchange

§ Will continue to identify opportunities for strategic

asset sales

asset sales

29

Current Priorities & Focus

§ Our Near-Term Priorities Consist of:

– Leasing of Existing Assets in Our Portfolio

– Strategic Asset Sales

– Managing Liquidity & Maximizing Distributions to Shareholders

§ Our Long-Term Priorities Consist of:

– Evaluating Potential Exit Strategies

– Managing Our Debt Maturities

§ These Priorities are Designed to Assist Us in Meeting Our

Primary Objective of Maximizing Shareholder Returns

over the Long Term

Primary Objective of Maximizing Shareholder Returns

over the Long Term

30

“Hines began as a one-man operation in 1957

with the sole focus of delivering better quality

services and products to tenants and investors.

More than half a century later, with 3,200

professionals working on four continents, our

philosophy has not wavered and our

commitment to excellence in the built

environment is stronger than ever.”

with the sole focus of delivering better quality

services and products to tenants and investors.

More than half a century later, with 3,200

professionals working on four continents, our

philosophy has not wavered and our

commitment to excellence in the built

environment is stronger than ever.”

31

Gerald D. Hines

Thank You