Attached files

| file | filename |

|---|---|

| 8-K - LIVE FILING - NORTHRIM BANCORP INC | htm_42457.htm |

EXHIBIT 99.1

|

||

Contact:

|

Joe Schierhorn, Chief Financial Officer (907) 261-3308 |

|

NEWS RELEASE

Northrim BanCorp Second Quarter 2011 Profits Increase 49% to $3.2 Million, or $0.49 per

Share

ANCHORAGE, AK—July 26, 2011—Northrim BanCorp, Inc. (NASDAQ: NRIM) today reported that net income increased 49% to $3.2 million, or $0.49 per diluted share, in the second quarter of 2011, compared to $2.1 million, or $0.33 per diluted share in the second quarter a year ago. In the first quarter this year, Northrim earned $2.5 million, or $0.37 per diluted share. For the first six months of 2011, net income grew 40% to $5.6 million, or $0.86 per diluted share, compared to $4.0 million, or $0.62 per diluted share, in the like period a year ago.

Financial Highlights (at or for the quarter ended June 30, 2011, compared to March 31, 2011, and June 30, 2010)

| • | Nonperforming assets declined to $16.9 million, or 1.61% of total assets at June 30, 2011, compared to $22.2 million, or 2.02% of total assets at March 31, 2011, and $28.4 million, or 2.82% of total assets a year ago, due in part to the sale of a $3.8 million condominium complex that was classified as other real estate owned and that generated a gain on sale of $449,000. |

| • | The allowance for loan losses totaled 2.46% of gross loans at June 30, 2011, compared to 2.31% in the preceding quarter and 2.30% a year ago. The allowance for loan losses to nonperforming loans also increased to 132.6% at June 30, 2011, from 128.4% in the preceding quarter and 93.6% a year ago. |

| • | Other operating income, which includes revenues from service charges, electronic banking and financial services affiliates, contributed 22% to second quarter 2011 total revenues. |

| • | Northrim remains well-capitalized with Tier 1 Capital to Risk Adjusted Assets at 15.59%, up from 14.97% in the first quarter of 2011 and 14.77% in the second quarter of 2010. Tangible common equity to tangible assets was 10.90% at quarter end, up from 10.13% in the first quarter of 2011 and 10.53% in the second quarter of 2010. |

| • | The net interest margin (NIM) was 4.65% down slightly from 4.72% for the first quarter of 2011 and 5.06% a year ago. |

| • | Tangible book value grew 7% to $17.63 per share and book value per share grew 6% to $18.96 per share from a year ago. |

| • | Northrim continues to pay a quarterly cash dividend which provides a yield of approximately 2.50% at current market share prices. |

“With strong capital, improving asset quality and continued profitability, we have invested in our infrastructure to position Northrim for the future,” said Marc Langland, Chairman, President and CEO of Northrim BanCorp, Inc. “Our initiatives include investments in our technology and upgrading of our equipment, networking, and data management facilities. Our improved IT capabilities will improve internal and external communications speed, improve efficiencies, and enhance security and reliability for all our systems.”

Alaska Economic Update

With continuing strong prices for commodities, particularly oil, minerals and fisheries, Alaska’s

economy continues to outperform the rest of the nation. Alaska provides one–tenth of the nation’s

domestic oil supply. In a presentation to the Arctic Imperative Summit in June, Dan Sullivan,

Alaska’s Commissioner of Natural Resources (DNR), shared information about Alaska’s resources. If

Alaska were a country, according to DNR research, the state would be a leader in a number of

important resources:

| • | Coal: 2nd in the world, with 17% of the world’s resources |

| • | Copper: 3rd in the world, with 6% |

| • | Lead: 6th in the world, with 2% |

| • | Gold: 7th in the world, with 3% |

| • | Zinc: 8th in the world, with 3% |

| • | Silver: 8th in the world, with 2% |

Alaska’s housing market continues to be one of the healthiest in the nation. The first quarter 2011 Mortgage Bankers’ Association National Delinquency Survey shows that Alaska has the lowest level of residential foreclosures started this year and the lowest level of total foreclosure inventory in the country. For the last two years, the percentage of foreclosures started in Alaska in a given quarter was about 0.5% of the total number of mortgages outstanding, which is about half the national average. The total inventory of foreclosures in process is only 0.8% in Alaska, while the entire country has a much larger lingering foreclosure inventory at 3.4% due to higher rates during the recession and longer resolution times.

“The strength of the Alaska economy has translated into strong state budget surpluses over the past few years. Recently, the State of Alaska passed a $2.8 billion capital budget, primarily for infrastructure projects. The strong stimulus from this spending package should continue to support local businesses and residents,” said Mark Edwards, Northrim’s Vice President Commercial Loan Officer and Economist.

Northrim Bank sponsors the Alaskanomics blog to provide news, analysis and commentary on Alaska’s economy. With contributions from economists, business leaders, policy makers and everyday Alaskans, Alaskanomics aims to engage readers in an ongoing conversation about our economy, now and in the future. Join the conversation at Alaskanomics.com or for more information on the Alaska economy, visit www.northrim.com and click on the “About Alaska” tab.

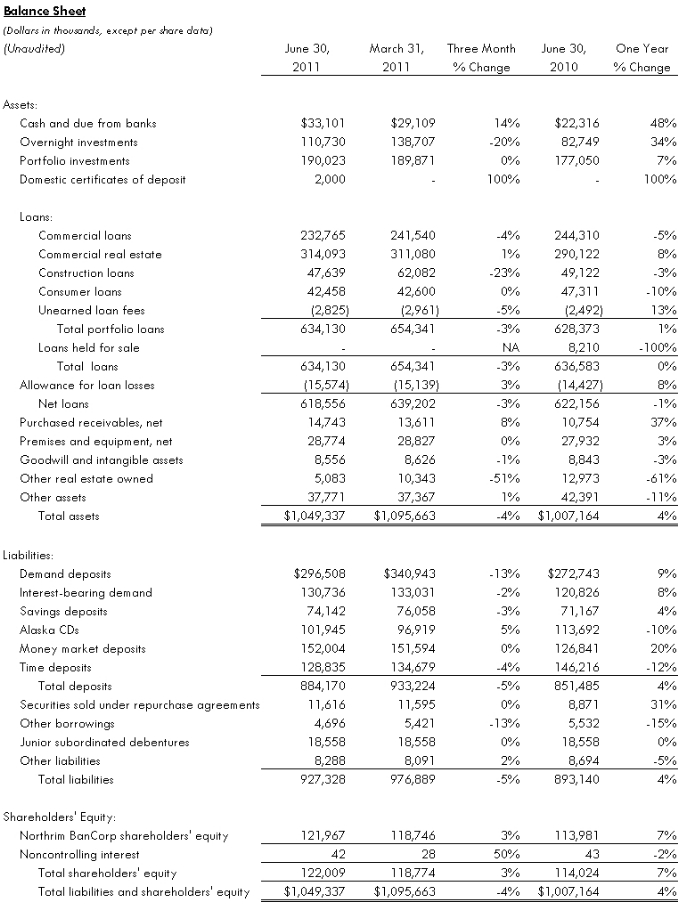

Asset Quality and Balance Sheet Review

Northrim’s assets totaled $1.05 billion at June 30, 2011 compared to $1.10 billion at March 31, 2011, and $1.01 billion a year ago.

The loan portfolio was $634.1 million at the end of the second quarter of 2011 down from $654.3 million at March 31, 2011, with declines in commercial loans and construction loans partially offset by increases in commercial real estate loans. At June 30, 2011, commercial loans accounted for 37% of the loan portfolio and commercial real estate loans accounted for 49% of the loan portfolio, as compared to 39% and 46%, respectively, a year ago. Construction and land development loans accounted for 8% of the loan portfolio at the end of June 2011 and 2010, respectively, and were down 23% to $47.6 million at June 30, 2011 from $62.1 million at March 31, 2011, reflecting the conversion of two commercial real estate construction loans into term commercial real estate loans during the quarter.

Nonperforming assets (NPAs), declined by $11.5 million to $16.9 million at June 30, 2011 from $28.4 million a year ago and by $5.3 million from $22.2 million at the end of March 2011. The nonperforming assets to total assets ratio stood at 1.61% at the end of June 2011, down from 2.02% three months earlier and 2.82% a year ago.

“We closed the sale of a $3.8 million condominium complex in Anchorage, generating a $449,000 gain, which contributed to cutting our portfolio of real estate owned in half in the second quarter,” said Joe Beedle, President of Northrim Bank. “In addition to sales we have completed in the last few years, we believe this sale further confirms the strength of the local real estate market.”

Loans measured for impairment decreased to $12.7 million at June 30, 2011, compared to $14.1 million at March 31, 2011, and $25.1 million in the second quarter a year ago. Net charge-offs in the second quarter of 2011, totaled $115,000, compared to net recoveries of $184,000, in the prior quarter. Net recoveries in the first six months of 2011 totaled $69,000 compared to net charge-offs of $1.4 million in the first half a year ago.

“We have eight restructured loans, which are included in NPAs and totaled $1.9 million at the end of the second quarter of this year,” Beedle noted. “These borrowers are current on payments and have pledged collateral to support the loans; however, the borrowers were granted concessions on the terms of their loans due to their financial difficulty. As a result of the modifications to these loans, they are now classified as restructured loans and included in nonperforming assets.”

The coverage ratio of the allowance for loan loss to nonperforming loans increased slightly to 132.6% at the end of June 2011, compared to 128.4% at March 31, 2011, and to 93.6% a year ago. The allowance for loan losses was $15.6 million, or 2.46% of total loans at quarter end , compared to $15.1 million, or 2.31% of total loans at March 31, 2011, and $14.4 million, or 2.30% of total loans a year ago.

Investment securities totaled $190.0 million at the end of the second quarter of 2011, up 7% from $177.1 million a year ago. At June 30, 2011, the investment portfolio was comprised of 62% U.S. Agency securities (primarily Federal Home Loan Bank and Federal Farm Credit Bank debt), 10% Alaskan municipality, utility, or state agency securities, 16% corporate bonds, 11% U.S. Treasury Notes, and 1% stock in the Federal Home Loan Bank of Seattle. The average estimated duration of the investment portfolio is less than two years.

“Our deposit base includes a number of transaction oriented businesses, which may cause deposit balances to fluctuate from day to day,” said Joe Schierhorn, Chief Financial Officer. At the end of June 2011, total deposits were $884.2 million, compared to $933.2 million at March 31, 2011, and $851.5 million a year ago. Year-to-date 2011, average deposit balances grew 6% to $875.8 million from $829.5 million in the first six months of 2010.

Noninterest-bearing demand deposits at June 30, 2011, increased 9% from a year ago and account for 34% of total deposits. Interest-bearing demand deposits at the end of June 2011 grew 8% year-over-year. Money market balances at the end of the second quarter of 2011 were up 20% from year ago levels and savings account balances were up 4% from a year ago. The Alaska CD (a flexible certificate of deposit program) was down 10% at the end of the second quarter, while time deposit balances fell 12% compared to the second quarter a year ago. At the end of the second quarter of 2011, noninterest-bearing demand deposits accounted for 34% of total deposits, interest-bearing demand accounts were 15%, savings deposits were 8%, money market balances accounted for 17%, the Alaska CD accounted for 11% and time certificates were 15% of total deposits. “We do not have any brokered deposits in our deposit base, which contributes to our stability,” Schierhorn noted.

Shareholders’ equity increased 7% to $122 million, or $18.96 per share, at June 30, 2011, compared to $114 million, or $17.85 per share, a year ago. Tangible book value per share was $17.63 at the end of June, compared to $16.46 a year ago. Northrim remains well-capitalized with Tier 1 Capital to Risk Adjusted Assets of 15.59% at June 30, 2011.

Review of Operations

“Contributions from our affiliates continue to be a strong point for our franchise,” said Chris Knudson, Chief Operating Officer. “Affiliate income is a steady contributor to profits by adding more than $1.4 million to second quarter 2011 and $2.5 million to first half 2011 revenues. These steady producers have continued to generate growth and help offset some of the margin pressure that has impacted top-line revenues this year.”

Second quarter 2011 net interest income, before the provision for loan losses, was down 5% year-over-year to $10.6 million from $11.1 million in the second quarter of 2010. Year to date 2011, net interest income before the provision for loan losses was down 5% to $21.3 million from $22.4 million in the first half a year ago.

Northrim’s net interest margin (net interest income as a percentage of average earning assets on a tax equivalent basis) was 4.65% in the second quarter of 2011, compared to 4.72% in the prior quarter and 5.06% in the second quarter a year ago. For the first six months of 2011, the net interest margin was down 52 basis points to 4.68% from 5.20% in the first six months of 2010. “We have traditionally generated net interest margins well above peer averages, but we are continuing to see yields on earning assets decline while cost of funding, particularly deposits, have bottomed out,” said Beedle.

Reflecting the continuing improvement in credit quality, the loan loss provision in the second quarter of 2011 totaled $550,000, in line with $549,000 recorded in the preceding quarter and down from the $1.4 million in the second quarter a year ago. For the first six months of 2011, the loan loss provision totaled $1.1 million down from $2.8 million a year ago.

Total other operating income increased 11% to $3.1 million in the second quarter of 2011, compared to $2.8 million for the first quarter ended March 31, 2011 due to growth in affiliate income. In the second quarter a year ago, Northrim’s other operating income totaled $3.2 million. Total other operating income for the first half of 2011 was stable at $5.8 million, with lower service charges on deposit accounts and fewer gains from sale of securities offset by growth in affiliate revenues.

Service charges on deposit accounts for the second quarter of 2011 were down 22% from the second quarter a year ago. Year to date 2011 service charges on deposit accounts also fell 24% from a year ago. “The new regulatory environment has impacted fees assessed for overdraft services for all financial institutions,” said Knudson. “Offsetting the effect of these new regulations are contributions from electronic banking fees which increased 4% in the second quarter of 2011 as compared to the preceding quarter and 7% from a year ago. For the first six months of 2011, electronic banking income grew 10% over the same period of 2010, reflecting increased consumer demand for the convenience of debit card transactions in particular.”

Purchased receivables income contributed $565,000 to second quarter 2011 revenues and $1.2 million to first half 2011 revenues. “Receivable financing is an attractive alternative to conventional loans for businesses to gain working capital, and we are finding strong demand in the Pacific Northwest for these services,” said Beedle.

Income from Northrim Benefits Group, Northrim’s employee benefit plan affiliate, contributed $593,000 to second quarter and $1.1 million to first half 2011 revenues. “Small and medium sized businesses greatly value the consultative approach we provide in identifying and evaluating health benefit plans for their employees. This service provides another point of differentiation for Northrim in the Alaska business market,” noted Knudson. “Our two wealth management affiliates in which we have an ownership interest, Elliott Cove Capital and Pacific Wealth Advisors, also add value to the overall customer relationships.”

Operating expenses were down in both the second quarter and first half of 2011 compared to earlier periods, reflecting, the gain on sale of other real estate owned (OREO), overall lower OREO costs and lower FDIC insurance assessments as well as lower salary and personnel expenses and no impairment on purchased receivables. Second quarter 2011 other operating expenses were $8.6 million compared to $9.3 million in the first quarter of 2011 and $9.8 million in the second quarter a year ago. For the first six months of the year, other operating expenses were $17.9 million compared to $19.7 million in the year ago period.

About Northrim BanCorp

Northrim BanCorp, Inc. is the parent company of Northrim Bank, a commercial bank that provides personal and business banking services through locations in Anchorage, Eagle River, Wasilla, and Fairbanks, Alaska, and a factoring/asset based lending division in Washington. The Bank differentiates itself with a “Customer First Service” philosophy. Affiliated companies include Elliott Cove Capital Management, LLC; Residential Mortgage, LLC; Northrim Benefits Group, LLC; and Pacific Wealth Advisors, LLC. In June 2010, Northrim Bancorp was added to the Russell 2000 Index, a subset of the Russell 3000 Index. Both indices are widely used by professional money managers as benchmarks for investment strategies.

www.northrim.com

Sources include the April 2011 Alaska Economic Update by Mark Edwards available at http://www.northrim.com/home/fiFiles/static/documents/econ—overview.pdf; the US Energy Information Administration at http://www.eia.gov/dnav/pet/pet—crd—crpdn—adc—mbblpd—a.htm, the Alaska’s Commissioner of Natural Resources, Dan Sullivan, and 2011 Mortgage Bankers’ Association National Delinquency Survey. For more information on this data, visit http://www.alaskanomics.com/.

This release may contain “forward-looking statements” that are subject to risks and uncertainties. Readers should not place undue reliance on forward-looking statements, which reflect management’s views only as of the date hereof. All statements, other than statements of historical fact, regarding our financial position, business strategy and management’s plans and objectives for future operations are forward-looking statements. When used in this report, the words “anticipate,” “believe,” “estimate,” “expect,” and “intend” and words or phrases of similar meaning, as they relate to Northrim or management, are intended to help identify forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Although we believe that management’s expectations as reflected in forward-looking statements are reasonable, we cannot assure readers that those expectations will prove to be correct. Forward-looking statements are subject to various risks and uncertainties that may cause our actual results to differ materially and adversely from our expectations as indicated in the forward-looking statements. These risks and uncertainties include our ability to maintain or expand our market share or net interest margins, and to implement our marketing and growth strategies. Further, actual results may be affected by our ability to compete on price and other factors with other financial institutions; customer acceptance of new products and services; the regulatory environment in which we operate; and general trends in the local, regional and national banking industry and economy as those factors relate to our cost of funds and return on assets. In addition, there are risks inherent in the banking industry relating to collectibility of loans and changes in interest rates. Many of these risks, as well as other risks that may have a material adverse impact on our operations and business, are identified in our other filings with the SEC. However, you should be aware that these factors are not an exhaustive list, and you should not assume these are the only factors that may cause our actual results to differ from our expectations.

1 Tangible book value is shareholder’s equity, less intangible assets, divided by common stock outstanding.

| 2 | Tangible common equity to tangible assets is a non-GAAP ratio that represents total equity less goodwill and intangible assets divided by total assets less goodwill and intangible assets. This ratio has received more attention over the past several years from stock analysts and regulators. The GAAP measure of common equity to assets would be total equity to total assets. Total equity to total assets was 11.63% at June 30, 2011 as compared to 10.84% at March 31, 2011 and 11.32% at June 30, 2010. |

3 Tax-equivalent net interest margin is a non-GAAP performance measurement in which interest income on non-taxable investments and loans is presented on a tax-equivalent basis using a combined federal and state statutory rate of 41.11% in both 2011 and 2010.

| 4 | The efficiency ratio is a non-GAAP ratio that is calculated by dividing other operating expense, exclusive of intangible asset amortization, by the sum of net interest income and other operating income. |