Attached files

| file | filename |

|---|---|

| EX-24 - EX-24 - BALLANTYNE STRONG, INC. | a2204585zex-24.htm |

| EX-23 - EX-23 - BALLANTYNE STRONG, INC. | a2204585zex-23.htm |

| EX-32.1 - EX-32.1 - BALLANTYNE STRONG, INC. | a2204585zex-32_1.htm |

| EX-23.1 - X-23.1 - BALLANTYNE STRONG, INC. | a2204585zex-23_1.htm |

| EX-31.2 - EX-31.2 - BALLANTYNE STRONG, INC. | a2204585zex-31_2.htm |

| EX-31.1 - EX-31.1 - BALLANTYNE STRONG, INC. | a2204585zex-31_1.htm |

| EX-32.2 - EX-32.2 - BALLANTYNE STRONG, INC. | a2204585zex-32_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

Item 8. Financial Statements and Supplementary Data

DIGITAL LINK II, LLC TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2010 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File No. 1-13906 |

||

Ballantyne Strong, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

47-0587703 (I.R.S. Employer Identification No.) |

|

4350 McKinley Street, Omaha, Nebraska (Address of principal executive offices) |

68112 (Zip Code) |

Registrant's telephone number, including area code: (402) 453-4444

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of exchange on which registered | |

|---|---|---|

| Common Stock, $0.01 par value | NYSE Amex |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports filed pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definition of "accelerated filer", "large accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o No ý

The aggregate market value of the Company's voting common stock held by non-affiliates, based upon the closing price of the stock on the NYSE AMEX (formerly the American Stock Exchange) on June 30, 2010 was approximately $103.3 million. The Company does not have any non-voting common equity. As of March 8, 2011, 14,334,117 shares of common stock of Ballantyne Strong, Inc., were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company's Proxy Statement for its Annual Meeting of Stockholders to be held on May 4, 2011 are incorporated by reference in Part III, Items 10, 11, 12, 13 and 14.

Ballantyne Strong Inc. (the "Company") is filing this Amendment No. 1 to its Annual Report on Form 10-K for the fiscal year ended December 31, 2010 to reflect the inclusion under Part IV, Item 15 of this report, of separate financial statements of Digital Link II, LLC, a fifty percent or less owned entity of the Company, as required under SEC Rule 3-09 of Regulation S-X. Pursuant to Rule 3-09, Digital Link II, LLC was not a "significant subsidiary" at December 31, 2010. Therefore, the financial statements for Digital Link II, LLC's fiscal year ended March 25, 2011 are unaudited. However, audited financial statements for Digital Link II, LLC's prior two fiscal years are included as required.

This Amendment No. 1 did not impact the Company's revenue, net earnings, total assets, stockholders' equity or earnings per share.

Except as stated above, no other information included in the original Form 10-K is being amended. The remaining items contained within this Amendment No. 1 consist of all other items contained in the original Form 10-K, and are included for the convenience of the reader. This Amendment No. 1 continues to speak as of the date of the original Form 10-K and the Company has not updated the disclosures in this Amendment No. 1 to speak as of any later date. Accordingly, this Amendment No. 1 should be read in conjunction with Company filings made with the Securities and Exchange Commission subsequent to the filing of the original Form 10-K.

This Annual Report on Form 10-K contains not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements that are not historical are forward-looking and reflect expectations for future Company performance. In addition, forward-looking statements may be made in press releases, orally, at conferences, on the Company's worldwide web site, or otherwise, by or on behalf of the Company. For these statements, the Company claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve a number of risks and uncertainties, including but not limited to those discussed in the "Risk Factors" section contained in Item 1A. Given the risks and uncertainties, readers should not place undue reliance on any forward-looking statements and should recognize that the statements are predictions of future results which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described herein, as well as others not now anticipated. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in the forward-looking statements. Except as required by law, the Company assumes no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

(a) General Description of Business

General

We are a Delaware Corporation and maintain our corporate office and primary manufacturing facilities in Omaha, Nebraska. We were founded in 1932 and went public in 1995. Our shares are traded on the NYSE Amex under the symbol BTN. We primarily operate within two business segments, theatre and lighting. Approximately 97% of fiscal year 2010 sales were from theatre products and approximately 3% were from lighting products.

We are a manufacturer, distributor, integrator and service provider to the theatre exhibition industry on a worldwide basis. Through our Strong® trademark, we can fully outfit and automate a theatre projection booth for both film and digital projection. Our portfolio of cinema trademarks include: Apogee®, Century®, Optimax® and Strong Digital Systems®. Our lighting brands include: Gladiator®, Radiance®, Sky-Tracker®, Solutions™, Strong Britelight® and Technobeam®. We have sales and service offices in Hong Kong, Beijing and Shanghai, China. We also manufacture cinema screens in Joliette, Canada through our Strong/MDI Screens, Inc. subsidiary. We have a centralized Network Operating Center to track a full range of digital equipment from all makes of digital projection and audio systems, flat panels and the associated network systems. We also have an extended network of service technicians located throughout the country to install and service film, digital and other cinema and non-cinema products.

We also design, develop, manufacture and distribute lighting systems to the worldwide entertainment lighting industry through our Strong Entertainment lighting division.

3

Divestitures

During the second quarter of 2008, we sold our coater and marinade product line in exchange for $0.3 million in cash. The product line was sold to a former Chief Financial Officer of the Company.

(b) Operating Segments

We conduct our operations through two primary business segments: Theatre and Lighting. The presentation of segment information reflects the manner in which management assesses performance.

Theatre: This segment consists of the manufacture, distribution, installation and service of film and digital projection equipment and accessories for the movie exhibition industry.

Lighting: This segment consists of the design, manufacture and distribution of lighting systems to the worldwide entertainment lighting industry.

Refer to the Business Segment Information set forth in Note 23 of our consolidated financial statements for further information concerning the amounts of revenues, profits and total assets attributable to each segment for the last three fiscal years.

(c) Narrative Description of Business

The following information describes the principal products produced, services rendered, principal markets for, and methods of distribution of each business segment of the Company.

Theatre Segment

Overview

According to the National Association of Theatre Owners, there are approximately 107,000 screens worldwide that play major movie releases, with approximately 39,000 screens located in the United States. The industry is in the midst of a significant transformation from film to digital equipment. Theatre exhibition companies are retrofitting their existing complexes by removing the film equipment and replacing it with digital equipment providing an opportunity for us to deliver digital products and services as this conversion continues.

Products

Digital Equipment—Through distribution agreements with NEC and its subsidiaries, we distribute DLP Cinema projectors. NEC offers the NC3200S for large screen multiplexes, the NC2000C for medium- sized screens and the NC1200C for small theatres. All the projectors use the DLP cinema technology from Texas Instruments. The Starus NC3200S is designed for multiplexes with large screens up to 105 feet wide. The projector delivers 2K (2048 × 1080) resolution, 3D capabilities and high contrast images (>2200:1). The NC2000 projector is designed for medium sized screens up to 65 feet wide. The projector delivers 2K (2048 × 1080) resolution, 3D capabilities and high contrast images (>2200:1). The NC1200C projector is designed for screens up to 46 feet wide to employ DC 2K DMD technology at 2048 × 1080 pixel native resolution.

Prior to the release of the updated series of projectors in 2010, we sold NEC's first series of projectors including the Starus NC 2500S-A, NC 1600C-A and the NC 800C.

Through a formal distribution agreement with GDC Technology (USA), LLC the Company distributes GDC's line of digital cinema servers in North and South America; however, we also distribute servers of certain of GDC's competitors as well.

We also distribute accessories for digital cinema projectors including, but not limited to, replacement parts, lenses, lamps and automations, among other items.

4

The digital equipment we manufacture and distribute can fully outfit and automate a movie projection booth.

Motion Picture Projection Equipment—We are a manufacturer and distributor of commercial motion picture projection equipment worldwide. Our commercial motion picture projection equipment can fully outfit and automate a motion picture projection booth and consists of 35mm and 70mm motion picture projectors, xenon lamphouses and power supplies, a console system combining a lamphouse and power supply into a single cabinet, soundhead reproducers and related products such as sound systems. The commercial motion picture projection equipment is marketed under the industry-wide recognized trademarks of Strong® and Simplex®. We manufacture the majority of the motion picture projection systems in-house, except for the audio rack components, lamps and lenses. This equipment may be sold individually or as an integrated system with other components manufactured by us.

We also distribute film handling equipment consisting of a three-deck or five-deck platter and a make-up table, which allows the reels of a full-length motion picture to be spliced together, thereby eliminating the need for an operator to change reels during the showing of the motion picture. Our film transport systems are sold under the Strong® name.

Cinema Screens—We manufacture multiple standard and large format 2D and 3D screens for cinema and special venue applications through our manufacturing facility in Canada. In most instances, a screen can be used interchangeably with either a digital or film projector. There are certain digital 3D applications, such as the technology by RealD, that require special "silver" screens that we manufacture and were specially designed for digital or 35mm projection. We manufacture screens for the IMAX Corporation that are primarily used in large-format applications.

Xenon Lamps—We distribute xenon lamps for resale to the theatre (both digital and film) and lighting industries through a distributorship agreement with Phillips.

Replacement Parts—We have a significant installed base of 35,000 to 40,000 motion picture projection systems. Although these products have an average useful life in excess of 20 years, periodic replacement of components is required as a matter of routine maintenance, in most cases with parts manufactured by us. We also distribute parts to the growing digital cinema base of projectors.

Lenses—We sell digital and film projection lenses throughout the world.

Service & Maintenance—Through our wholly owned subsidiary, Strong Technical Services, Inc. (STS) we are a national provider of cinema services including film and digital projector maintenance, repair, installations, site surveys and other services. In response to increased demand for service we opened a state-of-the-art Network Operating Center in October 2010. This facility is capable of tracking a full range of digital equipment from all makes of digital projection and audio systems, flat panels and the associated network systems through our staff of hardware, network and engineering professionals. Our technicians are certified to install and service all digital, film and audio equipment, and related peripherals including the equipment of our competitors. We also offer service contracts to the theatre exhibition industry whereby for an agreed upon fee, a series of maintenance or repair services will be performed.

Markets

Our theatre business was founded in 1932. Our broad range of both standard and custom-made equipment along with other ancillary equipment can completely outfit and automate a digital or film movie projection booth.

We market and sell our products to end users and through a network of domestic and international dealers to major theatre exhibitors. During the past few years we have increasingly sold

5

directly to the end-users thereby bypassing this distribution network. We believe this trend will continue in the future and is changing how we market our products to the industry due in large part to the shift to digital cinema. Sales and marketing professionals principally develop business by maintaining regular personal customer contact including conducting site visits, while customer service and technical support functions are dispatched when needed. In addition, we market our products in trade publications such as Film Journal and Box Office and by participating in annual industry trade shows such as CinemaCon, ShowEast, CineAsia in Asia and Cinema Expo in Europe, among others. Our sales and marketing professionals have extensive experience with the Company's product lines and have long-term relationships with many current and potential customers.

Our current non-exclusive master reseller distribution agreements with NEC allow us to market digital projectors in North and South America, including the Caribbean. In addition, we have distribution rights in China, Hong Kong and certain other areas of Asia. We do not have any territorial restrictions for any of our other products and services.

Competition

Digital Equipment—The markets for our products in the theatre segment are highly competitive. Competition in the digital cinema equipment market includes two other licensed OEM's of the Texas Instruments' 2K DLP Cinema technology besides our partner, NEC; Christie Digital Systems and Barco. We also compete with SONY, which uses its own 4K digital cinema technology. During 2009, SONY made significant inroads into gaining market share when they announced agreements with Regal Cinemas, Inc. and AMC Entertainment, Inc. to deploy their 4K digital cinema projectors into these two large circuits. In response to this threat, Texas Instruments developed their own 4K resolution solution which will be ready during 2011. We believe that once the DLP 4K solution is ready for sale; the perceived difference in resolution will diminish. We compete in the digital marketplace primarily on the basis of fulfillment and delivery, price and after-sale technical support.

Screens—While there are numerous screen manufacturing companies in the world, the primary competitor in the cinema screen market is Harkness Screens.

Service—The competition in the cinema service industry is primarily driven by the two largest cinema service companies including ourselves and Christie Digital Cinema. There are several other smaller scale providers in the market.

Film Equipment—Major competitors for our products in the film cinema marketplace include Christie Digital Systems, Cinemeccanica SpA and Kinoton GmbH. The market for film products in the U.S. primarily comes from the sale of replacement parts and lenses due to the transition to digital cinema, which has significantly affected the sale of film projectors. We continue to sell film projectors to other parts of the world that are not as advanced regarding digital cinema. We compete overseas based on price, product name and customization capabilities.

We cannot assure that our equipment, whether it is film or digital equipment will not eventually become obsolete as technology advances. For a further discussion of potential new competition, see the "Business Strategy" section of this report under the caption "Expand Digital Opportunities".

The majority of our competitors for film and digital equipment have significantly greater resources than Ballantyne.

Lighting Segment

Overview

Under the trademark Strong®, we are a supplier of long-range followspots and other entertainment and architectural lighting products which are used for both permanent and touring applications.

6

Products

Followspots—We have been a developer, manufacturer and distributor of long-range followspots since 1950. Our followspots are primarily marketed under the Strong® trademark and recognized trademarked models such as Super Trouper® and Gladiator®. The Super Trouper® followspot has been the industry standard since 1958. Our long-range followspots are high-intensity general use illumination products designed for both permanent installations, such as indoor arenas, theatres, auditoriums, theme parks, amphitheatres and stadiums, and touring applications. Our manufactured followspot line consists of six basic models ranging in output from 850 watts to 4,500 watts. Lower wattage models, which have a range of 20 to 110 feet, are compact, portable and appropriate for small venues and truss mounting. The 4,500-watt model, which has a range of 300 to 600 feet, is a high-intensity xenon light followspot appropriate for large theatres, arenas and stadiums. Most of our followspots employ a variable focal length lens system which increases the intensity of the light beam as it is narrowed from flood to spot.

In response to a section of the marketplace demanding less expensive, smaller and more user-friendly products, we have introduced certain new spotlights over the last few years. We distribute an Italian manufactured followspot line called Canto. The Canto spotlight product line consists of seven basic models ranging in output from 250 watts to 2,000 watts.

Promotional and Other Lighting Products—We are a supplier of high intensity promotional searchlights and lighting systems for the motion picture production, television, live entertainment, theme park and architectural markets. Strong Britelight® specialty illumination products have been used in numerous feature films and have also been used at live performances such as Super Bowl half-time shows, the opening and closing ceremonies of the Winter Olympics and are currently illuminating such venues as the Luxor Hotel and Casino and the Stratosphere Hotel and Casino in Las Vegas, Nevada. Our Sky-Tracker® high intensity promotional searchlights come in single or multiple head configurations, primarily for use at outside venues requiring extremely bright lighting that can compete with other forms of outdoor illumination. These high intensity promotional searchlights have been used at Walt Disney World, Universal Studios, various Olympic Games and grand openings. We purchased a product line during 2007 called Technobeam® which projects logos, images and textures. This product is used in a variety of entertainment establishments.

In 2008 we expanded our effort to add new distribution lines to our lighting offerings. These new lines include a broad set of LED products marketed under the Litetude™ that are made for us in China and expanded offerings from our Italian supplier of Canto. In 2010 we signed an agreement to be the exclusive distributor of the DTS line of lighting products. DTS is another Italian manufacturer that supplies us with a wide-range of entertainment and architectural lighting products.

LED Products—During 2010, we introduced two new lines of LED lighting fixtures. The first product line will be marketed under the trademark name Solutions™. The line primarily is made up of two 650 watt fixtures. One, the Solutions 650, is a white LED fixture and the second, the 650C, is a color mixing RGB fixture. These lights are designed to fill a demand for efficient long-throw LED based lighting solutions for the entertainment lighting marketplace. We also intend to market these products to the architectural lighting markets. The second new product line is marketed under the trademark name Neeva™. Neeva is a unique product that fulfills the promise of a highly controllable LED light source that is positioned at a modest cost.

Markets

We sell our lighting products through a combination of a small direct sales force, dealer network and commissioned representatives to arenas, stadiums, theme parks, theatres, auditoriums and equipment rental companies. Our followspot products are marketed using the Strong® trademark and are used in over 100 major arenas throughout the world. Our high intensity promotional searchlights

7

are marketed under the Sky-Tracker® trademark. We expect to market our new LED products primarily through our existing sales channels.

Strategy

Our goal is to increase revenues using the remaining product lines within the segment and by increased emphasis on expanding our product offerings by developing and introducing new products such our new LED product offerings.

Competition

The markets for our lighting products are also highly competitive. We compete in the lighting industry primarily on the basis of quality, price, branding and product line variety. Many of our competitors have significantly greater resources than Ballantyne.

Business Strategy

Our strategy combines the following key elements:

Expand Digital Opportunities. We currently are a party to distribution agreements with NEC and their subsidiaries whereby we distribute their line of DLP Cinema projectors to certain areas of the world. We intend to gain market share in the digital cinema marketplace by leveraging our current industry leadership and relationships and gaining additional territories to distribute product under our distribution agreements with NEC.

We believe we can be a successful participant in the marketplace due to our agreements with NEC, our long term industry relationships, and the industry's familiarity with our Company and its large installed base worldwide. However, no assurance can be given that we will continue to be a part of the digital cinema marketplace. If we are unable to take advantage of future digital cinema opportunities or respond to the new competitive pressures, the result could have a material adverse effect on our business, financial condition, and operating results. In addition, the current relationships with NEC are through non-exclusive distributorship agreements, some of which can be terminated by either party upon 90 days notice. In addition, the gross margin we generate based on these distribution agreements is lower than the margin we experience on our film projectors. We have experienced an increase in price points and sales volume that has partially offset the lower margin; however, we cannot provide assurance that this trend will continue as the digital rollout continues to progress.

Expand Service Company. Our service subsidiary, Strong Technical Services, Inc. (STS) installed approximately 2,000 digital units in 2010, cementing our presence as the leader in digital installations. We have also entered into agreements to perform cabling and electrical installations for theatres throughout the country, establishing STS as a major force in digital rollouts for the entire industry. Capitalizing on our growth, capabilities and strategic partnerships, we have expanded our offerings to include cabling, wiring, digital menu boards, and digital signage. As a result of the above mentioned development and growth, we are in a position to increase our services contracts by 300 new digital locations including Barco, Sony, and Christie equipment. Building off the great reputation of the entire Ballantyne Strong, Inc. company we are able to work with industry leaders and we are currently working on major contracts to expand our services. It is our belief that with our capabilities in the field and corporate offices, we will expand our reach into the technology field of many organizations beyond the cinema world.

Network Operations Center. We completed the build-out of a Network Operations Center (NOC) in October 2010. Our business strategy associated with this development was to leverage our technical capabilities while meeting industry demands for remote digital systems monitoring. The NOC operates 24/7/365 utilizing Level I and Level II engineers to monitor our customers' equipment across secure

8

virtual private network ("VPN") links. High priority notifications automatically generate trouble tickets with the appropriate escalation procedures. Normal incident tracking procedures ensure the timely resolution of trouble tickets. When one of our NOC personnel observes an issue, the customer is proactively notified to explain the issue and begin the resolution process. Many issues are addressed by our NOC engineering team without having to dispatch a technician to the customer's location. By utilizing NOC personnel to solve customer issues whenever possible, we eliminate travel time and expenses normally incurred by sending a technician on site for repairs. Nearly any issue that doesn't involve parts replacements or physical contact with the hardware can be handled remotely using the available remote assistance technologies. We are anticipating growth in NOC revenues from monitoring digital cinema equipment, back room operations, and from industries outside cinema.

Transition from a Manufacturer to a Distributor. We believe that the digital transition taking place within the theatre industry will continue to substantially reduce the demand for the products we manufacture and that we will transition to more of a distribution and service business model. However, we believe that the Company will continue to manufacture film equipment parts for a period of time. We will also continue to manufacture cinema screens through our screen subsidiary and will also manufacture lighting products for our lighting segment. We continue to reduce costs at our Omaha manufacturing facility through a cost and inventory reduction program designed to bring costs and inventory in line with declining revenues and production.

Expand Screen Business. Our screen production facilities have been expanded to provide increased capacity to support the market demand for silver (3D) screens and jumbo screens, as well as serving the needs of the growing international markets. The plant has been refitted with state of the art radio frequency PVC welders and coating automation and application equipment, which has been specifically engineered to meet the high tolerance demands of our product lines while improving production efficiencies. The expanded production capabilities also provide an opportunity for our company to expedite screen deliveries through our "Fast-Track" service and capitalize on immediate demand orders. Strong/MDI is also developing new silver and gain coating formulations to enhance screen performance and expand our product offerings.

Growth Strategy. The management team is aggressively pursuing all growth opportunities as outlined in these respective areas. In addition, we are identifying and when appropriate will dynamically pursue acquisition targets that will complement our strategies.

Expand International Presence. We believe that international sales will continue to account for a significant portion of our digital sales. We also believe that film-related sales will continue for a longer period of time than for the U.S. as the full scale rollout of digital cinema is expected to lag behind. We continue to expand our distribution capabilities by allocating more resources in international countries. We are also working with NEC to expand our distribution territories for selling their digital projector line beyond North and South America, Hong Kong, China and certain other areas of Asia.

Expand Lighting Segment. Our goal is to increase revenues by aggressively marketing existing product lines, while adding complementary products through exclusive distribution agreements. In addition, our engineering group has partnered with product design firms to develop new technology lighting products such as the Solutions™ LED product line.

Subsidiaries

We have four wholly owned operational subsidiaries: Strong Westrex, Inc., Strong Technical Services, Inc., Strong/MDI Screen Systems, Inc. and the American West Beijing Trading Company, Ltd.

Strong Westrex, Inc. is the holding company for our sales and service office in Hong Kong and owns 100% of the American West Beijing Trading Company, Ltd.

9

Strong Technical Services, Inc. was formed in 2006 upon the purchase of National Cinema Service Corp. ("NCSC") to service the film and digital marketplace.

Strong/MDI Screen Systems, Inc. manufactures cinema screens and related accessories.

American West Beijing Trading Company, Ltd. is located in Beijing, China and is our sales and service office for China.

Backlog

At December 31, 2010 and 2009, we had backlogs of $24.0 million and $4.4 million, respectively. Such backlogs mainly consisted of orders received with a definite shipping date within twelve months; however, these orders are subject to cancellation. Our products are generally shipped within a few weeks following receipt of orders. The dollar amount of our order backlog is therefore not considered by management to be a leading indicator of our expected sales in any particular fiscal period.

Manufacturing

Our manufacturing operations are conducted in Omaha, Nebraska and Joliette, Canada. The Omaha facilities encompass design, fabrication, assembly and shipping of our various product lines excluding the majority of digital product lines. This central location reduces our transportation costs and delivery times of products throughout the United States. Our manufacturing strategy is to minimize costs through manufacturing efficiencies and reduce fixed costs pertaining to manufacturing film projection equipment. We believe that the digital transition taking place within the theatre industry has and will substantially reduce the demand for the products we manufacture and that we will transition to more of a distribution and service business model. However, we believe that the Company will continue to manufacture film equipment parts for a period of time. We will also continue to manufacture cinema screens through our screen subsidiary in Joliette, Canada and also manufacture lighting products for our lighting segment. We are implementing programs at our Omaha facility to reduce costs through a cost and inventory reduction program designed to bring costs and inventory in line with revenues.

The manufacturing operations in Joliette, Canada consist of a 75,000 square-foot facility for the manufacture of cinema screen systems. These facilities include expanded PVC welding operations with programmable automations, as well as two 90-foot high screen coating towers with state of the art precision coating application software and painting systems. This world class ISO certified operation has the capability of manufacturing multiple standard screens simultaneously to large format 2D and 3D screens for cinema and special venue applications.

Quality Control

We believe that our design standards, quality control procedures and the quality standards for the material and components used in our products have contributed significantly to the reputation of the products for high performance and reliability. Inspection of incoming material and components as well as the testing of all of the Company's products during various stages of assembly are key elements of this program.

Warranty Policy

We generally provide a warranty to end users for substantially all of our products, which normally covers a period of 12 months, but is extended under certain circumstances and for certain products. In most instances, our digital products are covered by the manufacturing firm's OEM warranty; however, there are certain customers where we grant warranties in excess of this warranty. Under our warranty policy, we will repair or replace defective products or components at our election. Costs of warranty

10

service and product replacements were approximately $0.8, $0.3 and $0.6 million for the years ended December 31, 2010, 2009 and 2008, respectively.

Patents and Trademarks

We own or otherwise have rights to numerous trademarks and trade names used in conjunction with the sale of our products. We currently own one patent. We believe our success will not be dependent upon patent or trademark protection, but rather upon our scientific and engineering capabilities and research and production techniques.

Employees

As of March 1, 2011, we had a total of 289 employees. Of these employees, 140 were considered manufacturing, 4 were executive, 71 were considered service related and 74 were considered sales and administrative. We are not a party to any collective bargaining agreement and believe that the relationship with our employees is strong.

Environmental Matters

We are subject to various federal, state and local laws and regulations pertaining to environmental protection and the discharge of material into the environment. During 2001, we were informed by a neighboring company of likely contaminated soil on certain parcels of land adjacent to Ballantyne's main manufacturing facility in Omaha, Nebraska. The Environmental Protection Agency ("EPA") and the Nebraska Department of Health and Human Services subsequently determined that certain parcels of Ballantyne property had various levels of contaminated soil relating to a former pesticide company which previously owned the property and that burned down in the 1960's. During October 2004, Ballantyne agreed to enter into an Administrative Order on Consent ("AOC") to resolve the matter. The AOC holds Ballantyne and two other parties jointly and severally responsible for the cleanup. In this regard, the three parties have also entered into a Site Allocation Agreement by which they will divide past, current and future costs of the EPA, the costs of remediation and cost of long term maintenance. In connection with the AOC, we have paid our share of the costs. At December 31, 2010, we have provided for management's estimate of any future payments relating to this matter which are not material to the consolidated financial statements.

Stockholder Rights Plan

The Company's Stockholders Rights Plan expired on June 9, 2010 in accordance with the terms of the Plan.

Executive Officers of the Company

Gary Cavey, age 61, has been our President, CEO and a member of the Board of Directors since November 2010. Mr. Cavey succeeded John Wilmers, age 66, who has retired as President, CEO and member of the Board of Directors. Mr. Wilmers will remain with Ballantyne over the next twelve months to assist in the transition and to help the business pursue opportunities in Asia.

Christopher Stark, age 50, assumed the responsibilities of VP-Operations in May of 2007 and is currently Senior Vice President and Chief Operating Officer.

Ray F. Boegner, age 61, has been Senior Vice President since 1997. Mr. Boegner joined us in 1985 and has acted in various sales roles.

Kevin S. Herrmann, age 45, assumed the responsibilities of CFO, Corporate Secretary and Treasurer in November 2006. Prior to the appointment, Mr. Herrmann had been our Corporate Controller since 1997.

11

Information available on Ballantyne Website

We make available free of charge on our website (www.ballantyne-strong.com) through a link to the Securities and Exchange Commission ("SEC") website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934, as amended, as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC. However, information posted on our website is not part of the Form 10-K. The Board of Directors has adopted the following governance documents which are also posted on our website:

- •

- Code of Ethics

- •

- Corporate Governance Principles, including procedures for bringing concerns or complaints to the attention of the Board,

any Committee or any individual Director.

- •

- Audit Committee Charter

- •

- Nominating and Corporate Governance Committee Charter

- •

- Compensation Committee Charter

These corporate governance documents are also available in print to any stockholder upon request by writing to:

| The Secretary Ballantyne Strong, Inc. 4350 McKinley Street Omaha, NE 68112 |

Financial Information About Geographic Areas

The information called for by this item is included in Note 23 of our consolidated financial statements in this report.

NYSE Amex Stock Exchange Certification

On June 30, 2010, our Chief Financial Officer certified to the NYSE Amex that he was not aware of any violation by the Company of the NYSE Amex Corporate governance listing standards as of that date. This certification is an annual certification required by the NYSE Amex.

12

You should carefully consider the following risk factors and other information contained in this Annual Report on Form 10-K before investing in shares of our common stock. Investing in our common stock involves a high degree of risk. If any of the following risk factors actually occurs, our business, financial condition and results of operations could be materially and adversely affected. In that event, the trading price of our common stock could decline and you may lose part or all of your investment. We undertake no obligation to revise or update any forward-looking statements contained herein to reflect subsequent events or circumstances or the occurrence of unanticipated events. Also refer to the note regarding Forward-Looking Statements in Item 7 of Part II of this Form 10-K.

NEC is the sole supplier of the digital projectors we distribute to the theatre industry.

Through distribution agreements with NEC, we distribute their DLP Cinema projectors to North and South America, the Caribbean, Hong Kong, China and certain other areas of Asia. These agreements are non-exclusive distributorship agreements, some of which could be terminated with 90 days advance notice. If we are unable to maintain our relationship with NEC, the results would have a material adverse impact on our business, financial condition and operating results until we could find an alternative source of digital equipment to distribute. Further, there can be no assurance that an alternative source of digital equipment could be found on favorable terms. We are also dependent on NEC to supply us digital products in a timely manner and if there were delays in receiving product, we could lose market share which would negatively affect our operations. In addition, the current relationship with NEC is a non-exclusive distributorship agreement and as such the gross margin is and will be lower than the margin we currently experience on our film projectors. We have experienced lower margins that have been partially offset by increased price points and sales volume; however, we cannot provide assurance that this trend will continue in the future.

Interruptions of, or higher prices of components from NEC and other vendors may affect our results of operations and financial performance.

We are dependent on our vendors and suppliers for certain products in addition to the digital products we purchase from NEC. We believe we have good vendor relationships and that we are generally able to obtain adequate pricing and other terms from vendors and suppliers. However, if we fail to maintain satisfactory relationships with our vendors and suppliers or if our vendors and suppliers experience significant financial problems, we could experience difficulty in obtaining needed goods and services. Some vendors could also decide to reduce inventories or increase prices to increase cash flow given current economic conditions. We utilize a single contract manufacturer for each of our intermittent movement components, lenses and xenon lamps on the film side and as already discussed, NEC is currently the sole supplier for the digital projectors we distribute to the theatre industries. The loss of any one or more of the contract manufacturers could have an adverse effect on our business unless alternative manufacturing arrangements are secured. We are not dependent upon any one contract manufacturer or supplier for the balance of our raw materials and components. The industry transition to digital cinema is currently underway and during this time, there could be pricing pressures placed upon us as we market the NEC line of digital equipment. While our partnership with NEC to-date has been to strategically price the NEC projectors to the market-place, there is no assurance that if future pricing pressures arise NEC will drop their prices to allow us to remain competitive. In addition, volatility in the price for certain raw materials and components such as steel and fuel could adversely affect our financial results.

13

Our gross margins are subject to fluctuation

We expect our gross margin as a percentage of revenues to decrease in the future primarily due to increased sales of digital projection equipment which carry lower margins compared to the film products we previously manufactured. However, the sales price on the digital projectors is higher than what we receive on film projectors which offsets gross margin dollars to a degree. Gross margins could also be impacted in the future by higher film manufacturing costs pertaining to lower demand for manufactured film products. We expect to purchase film inventory components in lower quantities resulting in some raw material price increases and to experience less manufacturing throughput in the Omaha plant to cover fixed overhead costs. As sales of film projectors continue to decline, our revenues become more reliant on these lower margin digital sales completed as a distributor. To-date, we have been able to offset this with cost reductions and growing our higher margin screen manufacturing business. However, if we are unable to further lower costs as our film manufacturing decreases or there is a significant drop in demand for our higher margin screen sales, our gross margins and profits will be adversely impacted.

If the current digital technology changes to a format not supported by the DLP cinema technology from Texas Instruments, we could lose our ability to participate fully in the digital cinema market place.

We cannot provide assurance that there will be a continued demand for the digital cinema products we distribute. There can be no assurance that other technologies developed, or being developed, by competing companies will not gain traction in the exhibition industry which could affect our ability to fully participate in the digital cinema market place.

If we were forced to participate in digital cinema in ways other than being a distributor and service provider, we may have to leverage the Company. There is no assurance that we would be able to access sufficient capital given the tightening of the global credit markets.

Our 44.4% ownership in our joint venture with RealD is subject to credit and concentration risk.

Digital Link II, LLC, ("Digital Link II") was formed between Ballantyne and RealD for the purposes of commercializing certain 3D technology and to fund the deployment of digital projection systems to third party exhibitors. As of December 31, 2010, Digital Link II has deployed $9.4 million of such projection equipment, net of accumulated depreciation of $1.7 million. Such equipment is subject to system use agreements with certain exhibitors whereby the exhibitors must purchase the equipment upon the occurrence of certain triggering events. However, if any of these exhibitors would file for bankruptcy protection or be unable to fulfill their commitments in other ways, Digital Link II would be forced to remove the equipment and attempt to resell such equipment. At this time, it is unclear what the financial impact would be to the joint venture, however, it would likely have a material adverse effect on Digital Link II and also our financial condition and results of operations.

In addition, Digital Link II has entered into notes payable arrangements to finance a portion of the deployments. Ballantyne and RealD have provided guarantees for such notes in the event that Digital Link II would be unable to fulfill the principal and interest obligations under such notes based on their respective ownership shares. As of December 31, 2010, we have outstanding guarantees of $1.2 million (excluding interest) for our 44.4% share.

The markets for our products are highly competitive.

The domestic and international markets for our product lines are highly competitive, evolving and subject to rapid technological and other changes. We expect the intensity of competition in each of these areas to increase in the future. Competitors for our digital equipment have significantly greater resources than we do. In addition, many of our competitors are manufacturing their own digital equipment, whereas, we employ a distribution business model through our distribution agreements with

14

NEC. As a result, we may suffer from pricing pressures that could adversely affect our ability to generate revenues. If we lose market share due to these issues, we may be unable to lower our cost structure quickly enough to offset the lost revenue. If we are unable to compete successfully, our business and results of operations will be seriously harmed. NEC, along with two other licensed OEM's of the Texas Instruments' DLP Cinema technology historically have held the majority of the market share for digital projection equipment. However, there are also other companies such as SONY using different digital technologies in the marketplace. During 2009, SONY made significant inroads into gaining market share when they announced agreements with Regal Cinemas, Inc. and AMC Entertainment, Inc. to display their 4K digital cinema projectors into these two large circuits. While we believe Texas Instruments is taking steps to respond to the SONY threat, there can be no assurances that they will be successful.

Our business is subject to the economic and political risks of selling products in foreign countries.

Sales outside the United States (mainly theatre sales) continue to be significant, accounting for 44% of consolidated sales in fiscal 2010. We are seeking to expand our share of foreign sales, which we expect will continue to account for a significant portion of our revenues. Foreign sales are subject to political and economic risks, including political instability, currency controls, fluctuating exchange rates with respect to sales not denominated in U.S. dollars, changes in import/export regulations, tariffs and freight rates. An increasing amount of our foreign sales are being denominated in foreign currencies. During 2010, such sales rose to $22.7 million compared to $18.5 million in 2009. To the extent that orders are denominated in foreign currencies, our reported sales and earnings are more subject to foreign exchange fluctuations. In addition, there can be no assurance that our remaining international customers will continue to accept orders denominated in U.S. dollars. In addition, for those sales which are denominated in U.S. sales, a weakening in the value of foreign currencies relative to the U.S. dollar could have a material adverse impact on us by increasing the effective price of our products in international markets. Certain areas of the world are also more cost conscious than the U.S. market and there are instances where our products are priced higher than local manufacturers. We are also exposed to foreign currency fluctuations between the Canadian and U.S. dollar due to our screen manufacturing facility in Canada where a majority of their sales are denominated in the U.S. dollar while their expenses are denominated in Canadian currency. We cannot assure that these factors will not adversely affect our foreign activities in the future.

The risk of non-compliance with U.S. and foreign laws and regulations applicable to our international operations could have a significant impact on our results of operations, financial condition or strategic objectives.

Our global operations subject us to regulation by U.S. federal and state laws and multiple foreign laws, regulations and policies, which could result in conflicting legal requirements. These laws and regulations are complex, change frequently, have tended to become more stringent over time and increase our cost of doing business. These laws and regulations include import and export control, environmental, health and safety regulations, data privacy requirements, international labor laws and work councils and anti-corruption and bribery laws such as the U.S. Foreign Corrupt Practices Act, the U.N. Convention Against Bribery and local laws prohibiting corrupt payments to government officials. We are subject to the risk that we, our employees, our affiliated entities, contractors, agents or their respective officers, directors, employees and agents may take action determined to be in violation of any of these laws, particularly as we expand our operations through organic growth and acquisitions. An actual or alleged violation could result in substantial fines, sanctions, civil or criminal penalties, and debarment from government contracts, curtailment of operations in certain jurisdictions, competitive or reputational harm, litigation or regulatory action and other consequences that might adversely affect our results of operations, financial condition or strategic objectives.

15

Current negative economic conditions could adversely affect our results.

The current issues in the global credit markets and weaker economies may continue to negatively impact the Theatre and Lighting markets we serve. This environment could serve to reduce demand for our products and adversely affect our operating results. These economic conditions may also impact the financial condition of one or more of our key suppliers, including NEC, which could affect our ability to secure product to meet our customers' demand.

Our financial results and growth depend largely on the health of the theatre exhibition industry.

In 2010, approximately 97% of our revenues resulted from sales to the theatre exhibition industry. From fiscal years 2000 to 2002, this industry experienced an unprecedented three-year decline. Several exhibition companies filed for federal bankruptcy protection. This resulted in our revenues declining from $83.4 million in fiscal 1999 to $33.8 million in fiscal 2002. While the health of the theatre exhibition industry has improved significantly, there are still risks in the industry which result in continued exposure to Ballantyne. In addition, growth in the number of new movie screens may be adversely affected by the economy or other factors such as the global credit situation as the industry is very capital intensive. A lack of movie screen growth would have a material adverse effect on our business, financial condition and results of operations.

The industry is in the midst of a significant transformation from film to digital equipment. Theatre exhibition companies are retrofitting their existing complexes by removing the film equipment and replacing it with digital equipment. This transformation requires significant investment and there can be no assurance that our customers will be able to obtain a sufficient amount of this capital to continue the transformation. Without access to this capital, our theatre customers would be unable to purchase our products which would have a material adverse effect on our business, financial condition and results of operations. In addition, while we expect the conversion to digital cinema to continue for a period of time, there is no assurance that once the first conversion cycle is over, there will be additional replacements of existing digital systems. If we are unable to expand our revenues streams with other products and services, our future growth could be significantly curtailed.

We are substantially dependent upon significant customers who could cease purchasing our products at any time.

Our top ten customers accounted for approximately 42% of 2010 consolidated net revenues. While we believe our relationships with such customers are stable, most arrangements are made by purchase order and are terminable at will by either party. A significant decrease or interruption in business from these significant customers could have a material adverse effect on our business, financial condition and results of operations.

The Company has recorded deferred tax assets that are subject to annual valuation testing.

At December 31, 2010, we have recorded net deferred tax assets of $1.9 million. In assessing the ability to realize the deferred tax assets, management considers whether it is more likely than not that some portion or all of the deferred tax assets will not be realized. If management would determine that some or all of these assets would not be realized, valuation reserves would be required which would have a material adverse affect on our results of operations.

Difficulty in recruiting and retaining qualified technicians could hamper our business model pertaining to our service business.

We have experienced an increased demand for service due to the start of the digital conversion as theatre operators in many instances have not had the necessary technical expertise to maintain the more technical nature of digital projectors and accessories. The competition for qualified technicians is

16

increasing and we cannot predict whether we will experience future technician shortages. If such a shortage were to occur, we could be unable to properly provide the necessary services to our customers and subsequently lose market share. In addition, if technician salary increases were necessary to attract and retain them, our results of operations would be negatively impacted to the extent we could not pass those additional costs to our customers. We also cannot provide assurance that we will be able to successfully operate the service business in a profitable manner as we have limited experience with the volume of work that will be necessary. Our efforts to take care of our customers' needs could lead to increased and unplanned operating and capital costs.

Growth through acquisition is a part of our business plan and we may not be able to successfully identify, finance or integrate acquisitions.

As discussed in further detail in the "Business Strategy" portion of Item 1, our strategy is to pursue acquisitions that would fit in our business plans. We expect to make acquisitions in the future. However, we cannot assure that we will be able to locate appropriate acquisition candidates, that any identified candidates will be acquired or that acquired operations will be effectively integrated or prove profitable. Additionally, our credit facility with Wells Fargo currently prohibits Ballantyne from making acquisitions over $7.5 million without the bank's consent.

If we fail to retain key members of management, our business may be materially harmed.

Our success depends, in substantial part, on the efforts and abilities of our current management team. Many of these individuals have acquired specialized knowledge and skills with respect to Ballantyne and its operations. If certain of these individuals were to leave unexpectedly, we could face difficulty in hiring qualified successors and could experience a loss in productivity while any successor obtains the necessary training and experience.

Our Board of Directors recently elected a new Chief Executive Officer, President and Director

On November 1, 2010, our Board elected Gary L. Cavey to the positions of Chief Executive Officer, President and Director. Mr. Cavey replaced John C. Wilmers who had served in those positions for 13 years and retired. Mr. Wilmers will remain with the Company to assist in transitioning Mr. Cavey into his new position as Mr. Cavey is new to the Company and our business. Mr. Wilmers will also focus on the Company's growing business opportunities in Asia. While the Board believes that Mr. Cavey is well qualified and will function well in the new positions, there is no guarantee that this will be the case. Mr. Cavey's failure to perform as expected may have a material adverse effect on our business, financial condition, results of operations and stock price.

Our stock price is vulnerable to significant fluctuations.

The trading price of our common stock has been highly volatile in the past and could be subject to significant fluctuations in response to variations in quarterly operating results, general conditions in the industries in which we operate and other factors. In addition, the stock market is subject to price and volume fluctuations affecting the market price for the stock of many companies generally, which fluctuations often are unrelated to operating performance.

Shares eligible for future sale could have a possible adverse effect on the market price.

Future sales of common stock in the public market, or the perception that such sales could occur, could adversely affect the market price of the common stock or our ability to raise additional capital through sales of our equity securities.

As of December 31, 2010, we had: i) 14,313,158 shares owned by stockholders and ii) 956,349 shares of common stock reserved for issuance under stock plans, of which 222,250 shares are issuable

17

pursuant to currently outstanding options, and 74,691 shares of common stock issued but unvested pursuant to our restricted stock plans. Of the shares outstanding, subject to outstanding options and reserved for issuance under the employee stock purchase plan, 14,238,467 shares are immediately eligible for resale in the public market without restriction.

We are unable to predict the effect that the sales of these shares may have on the prevailing market price of the common stock.

Item 1B. Unresolved Staff Comments

None.

Our headquarters, main manufacturing facility and Network Operating Center ("NOC") are located at 4350 McKinley Street, Omaha, Nebraska, where we own a building consisting of approximately 166,000 square feet on approximately 12.0 acres. The premises are used for offices, the manufacture, assembly and distribution of our products, and operating the NOC.

Our Strong/MDI Screen Systems, Inc. subsidiary purchased the existing 50,000 square-foot manufacturing plant in Joliette, Canada and constructed a 25,000 square-foot addition, nearly doubling the production capacity. The expanded facilities are used for offices, manufacturing, assembly and distribution of the cinema screens.

Our American West Beijing Trading Company Ltd. subsidiary leases sales and service offices in Beijing and Shanghai, China.

Strong Technical Services, Inc. leases a small administrative office in Fall River, Massachusetts.

We also lease a sales and service office in Hong Kong.

The Company is currently a defendant in an asbestos case entitled Manuel H. Chinea and Janet M. Chinea v. American Optical Company, Ballantyne Strong, Inc. a/k/a Ballantyne of Omaha, Inc. et al, filed August 17, 2010 in the Superior Court of the State of New York. The Company is one of twenty-five defendants. The Plaintiffs have agreed to dismiss the Company. The dismissal will be final assuming no defendant objects.

During December 2009, the Company settled an asbestos case entitled Larry C. Stehman and Leila Stehman v. Asbestos Corporation, Limited and Ballantyne Strong, Inc. individually and as successor in interest to Strong International, Strong Electric Corporation and Century Projector Corporation, et al, originally filed in the Superior Court of the State of California, County of San Francisco. The settlement, including legal fees, resulted in charges of approximately $0.4 million during 2009.

18

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is listed and traded on the NYSE Amex under the symbol "BTN". The following table sets forth the high and low per share sale price for the common stock as reported by the NYSE Amex.

| |

|

High | Low | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2010 | First Quarter | $ | 5.89 | $ | 3.10 | ||||

| Second Quarter | 9.00 | 5.45 | |||||||

| Third Quarter | 9.66 | 6.91 | |||||||

| Fourth Quarter | 9.74 | 6.48 | |||||||

2009 |

First Quarter |

$ |

2.42 |

$ |

0.88 |

||||

| Second Quarter | 3.27 | 1.80 | |||||||

| Third Quarter | 3.88 | 2.02 | |||||||

| Fourth Quarter | 3.98 | 3.08 | |||||||

2008 |

First Quarter |

$ |

5.97 |

$ |

4.02 |

||||

| Second Quarter | 5.20 | 3.85 | |||||||

| Third Quarter | 4.70 | 1.55 | |||||||

| Fourth Quarter | 2.23 | 0.99 | |||||||

Our common stock was held by approximately 167 stockholders of record as of March 8, 2011. Because many of our shares of common stock are held by brokers and other institutions on behalf of stockholders, we are unable to estimate the total number of stockholders. The last reported per share sale price for the common stock on March 8, 2011 was $7.12. We had 14,334,117 shares of common stock outstanding on March 8, 2011.

On November 12, 2008, our Board of Directors approved the repurchase of up to $1.0 million of our common stock. No shares were repurchased in 2009 or 2010. Approximately $0.9 million remains available for repurchase as of March 7, 2011. The Company may purchase shares from time to time depending on market, economic and other factors.

19

Equity Compensation Plan Information

The following table sets forth information regarding our Stock Option, Restricted Stock and Stock Purchase Plan Agreements as of December 31, 2010.

Plan Category

|

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted average exercise price of outstanding options, warrants and rights |

Number of securities remaining available for future issuance under equity compensation plans excluding securities reflected in column (a) |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(a) |

(b) |

(c) |

||||||||

Equity compensation plans approved by security holders |

172,250 | $ | 1.62 | 956,349 | (1) | ||||||

Equity compensation plans not approved by security holders |

— | — | — | ||||||||

Total |

172,250 | $ | 1.62 | 956,349 | (1) | ||||||

- (1)

- Includes 76,194 securities for the 2005 Stock Purchase Plan, 280,155 securities for our employee and director Restricted Stock Plans and 600,000 securities for our 2010 Long-Term Incentive Plan.

Dividend Policy

We intend to retain our earnings to assist in financing our business and do not anticipate paying cash dividends on our common stock in the foreseeable future. The declaration and payment of dividends by the Company are also subject to the discretion of the Board, and our credit facility contains certain prohibitions on the payment of cash dividends. Any determination by the Board as to the payment of dividends in the future will depend upon, among other things, business conditions, our financial condition and capital requirements, as well as any other factors deemed relevant by the Board. We have not paid cash dividends since we went public in 1995.

20

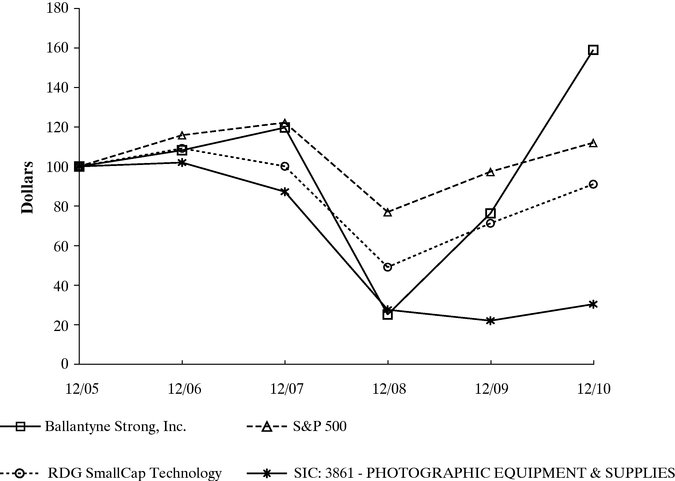

PERFORMANCE GRAPH

The following graph compares Ballantyne Strong's cumulative total stockholder return over the last five fiscal years with the Standard and Poor's 500 Index® ("S&P 500"), the Research Data Group, Inc. ("RDG") SmallCap Technology Index and a peer group consisting of the following issuers: American Tonerserve Corporation, Avid Technology, Inc., Chyron Corporation, Eastman Kodak Company, Ikonics Corporation, MDI, Inc., Swordfish Financial, Inc. and X-Rite, Inc. The Company has in good faith selected these peer issuers on the basis of their sharing the same SIC code (3861, Photographic Equipment & Supplies). The peer group total return was calculated using a weighted average market value. The graph assumes $100 was invested on December 31, 2005, and assumes reinvestment of all dividends.

Ballantyne Strong, Inc.

Comparison of Five-Year Cumulative Total Return

Copyright© 2011 Standard & Poor's, a division of The McGraw-Hill Companies Inc. All rights reserved. (www.researchdatagroup.com/S&P.htm)

| |

12/05 | 12/06 | 12/07 | 12/08 | 12/09 | 12/10 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Ballantyne Strong, Inc. |

100.00 | 108.18 | 119.63 | 25.15 | 76.28 | 158.90 | |||||||||||||

S&P 500 |

100.00 | 115.80 | 122.16 | 76.96 | 97.33 | 111.99 | |||||||||||||

RDG SmallCap Technology |

100.00 | 109.12 | 100.08 | 49.10 | 71.26 | 91.02 | |||||||||||||

SIC: 3861—PHOTOGRAPHIC EQUIPMENT & SUPPLIES |

100.00 | 101.96 | 87.21 | 27.58 | 22.04 | 30.39 | |||||||||||||

21

Item 6. Selected Financial Data (1)

| |

Years Ended December 31, | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||

Statement of operations data |

|||||||||||||||||

Net revenue |

$ | 136,335 | $ | 72,146 | $ | 54,815 | $ | 51,486 | 49,732 | ||||||||

Gross profit |

$ | 24,739 | $ | 14,732 | $ | 8,794 | $ | 9,456 | 10,826 | ||||||||

Net earnings (loss) |

$ | 8,433 | $ | 2,071 | $ | (3,034 | ) | $ | 228 | 1,568 | |||||||

Net earnings (loss) per share |

|||||||||||||||||

Basic |

$ | 0.60 | $ | 0.15 | $ | (0.22 | ) | $ | 0.02 | 0.12 | |||||||

Diluted |

$ | 0.59 | $ | 0.15 | $ | (0.22 | ) | $ | 0.02 | 0.11 | |||||||

Balance sheet data |

|||||||||||||||||

Working capital |

$ | 40,401 | $ | 35,805 | $ | 21,810 | $ | 32,390 | 34,974 | ||||||||

Total assets |

$ | 92,031 | $ | 60,210 | $ | 51,113 | $ | 54,140 | 49,908 | ||||||||

Total debt |

$ | — | $ | — | $ | — | $ | — | 15 | ||||||||

Stockholders' equity |

$ | 52,377 | $ | 42,518 | $ | 38,835 | $ | 43,042 | 42,389 | ||||||||

- (1)

- All amounts in thousands (000's) except per share data

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with the consolidated financial statements and notes thereto appearing elsewhere in this report. Management's discussion and analysis contains not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements that are not historical are forward- looking and reflect expectations for future Company performance. For these statements, the Company claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve a number of risks and uncertainties, including but not limited to those discussed in the "Risk Factors" section contained in Item 1A. Given the risks and uncertainties, readers should not place undue reliance on any forward-looking statement and should recognize that the statements are predictions of future results which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described herein, as well as others not now anticipated. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Except as required by law, the Company assumes no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

Overview

We are a manufacturer, distributor and service provider for the theatre exhibition industry on a worldwide basis. We also design, develop, manufacture and distribute lighting systems to the worldwide entertainment lighting industry through our Strong Entertainment lighting segment.

We have two primary reportable core operating segments: theatre and lighting. Approximately 97% of fiscal year 2010 sales were from theatre products and approximately 3% were lighting products. Additional information related to our reporting segments can be found in the notes to the consolidated financial statements.

22

Results of Operations:

The following table sets forth, for the periods indicated, the percentage of net revenues represented by certain items reflected in our consolidated statements of operations.

| |

Years Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||

Net revenue |

100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

Cost of revenues |

81.9 | 79.6 | 84.0 | 81.6 | 78.2 | |||||||||||

Gross profit |

18.1 | 20.4 | 16.0 | 18.4 | 21.8 | |||||||||||

Selling and administrative expenses(1) |

9.5 | 15.3 | 19.7 | 18.1 | 16.3 | |||||||||||

Income (loss) from operations |

8.8 | 5.1 | (7.4 | ) | (0.8 | ) | 3.0 | |||||||||

Net earnings (loss) |

6.2 | 2.9 | (5.5 | ) | 0.4 | 3.2 | ||||||||||

- (1)

- Amounts exclude goodwill impairment charges of $2.3, $0.6 and $1.3 million for the years ended December 31, 2008, 2007 and 2006, respectively.

Twelve Months Ended December 31, 2010 Compared to the Twelve Months Ended December 31, 2009 and December 31, 2008

Revenues

Net revenues during the twelve months ended December 31, 2010 rose to $136.3 million from $72.1 million in 2009.

| |

Twelve Months Ended December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | |||||||||

Theatre |

||||||||||||

Products |

$ | 125,043,983 | $ | 65,186,543 | $ | 47,158,724 | ||||||

Services |

7,881,593 | 3,810,626 | 3,186,650 | |||||||||

Total theatre revenues |

132,925,576 | 68,997,169 | 50,345,374 | |||||||||

Lighting |

3,409,041 | 3,121,840 | 4,260,868 | |||||||||

Other |

— | 26,748 | 208,319 | |||||||||

Total net revenues |

$ | 136,334,617 | $ | 72,145,757 | $ | 54,814,561 | ||||||

Theatre Segment

Sales of theatre products and services increased to $132.9 million in 2010 from $69.0 million in 2009 and $50.4 million in 2008.

Digital Product Sales

Sales of digital products rose to $87.0 million in 2010 from $27.9 million in 2009 as the industry change from analog to digital projection increased during 2010, primarily in the U.S. and China. The growth in business in the U.S. is primarily being driven by customers taking advantage of the opportunities that digital technology offers such as the ability to show 3D movies among other items. The growth in China is resulting not only from converting analog equipment to digital but also due to the construction of new theatre complexes in China. The majority of the increase in digital sales resulted from sales of digital projectors and certain accessories; however, sales of digital lamps also rose from $3.0 million in 2009 to $5.8 million in 2010 while sales of digital servers rose to $7.4 million from $1.2 million a year-ago. We also began to integrate projection equipment in our Omaha plant

23

where we consolidate and test digital equipment. Revenues generated from the product sold as part of this business was $5.0 million during 2010.

Sales of digital products rose to $27.9 million in 2009 from $12.6 million in 2008 as the industry change to digital projection equipment began to accelerate during 2009. The increased demand resulted from movie exhibitors wanting to show movies in 3D digital format as they believed that 3D movies result in higher box office receipts. The demand for digital equipment increased not only for the 3D benefits but also for such potential benefits as additional advertising and being able to project more alternative entertainment at the movie theatres. The majority of the increase in digital sales resulted from sales of digital projectors; however, sales of digital lamps also rose from $0.9 million in 2008 to $3.0 million in 2009.

Film Product Sales

Sales of film projection equipment declined to $10.9 million in 2010 from $12.0 million a year-ago due to the theatre exhibition industry's transition to digital based systems.

Sales of film projection equipment declined to $12.0 million in 2009 from $14.0 million in 2008 due to the theatre exhibition industry's transition to digital-based systems discussed above, coupled with a slowdown in new theatre construction in the United States and worldwide largely due to the economic and credit market conditions. Included in film equipment revenues were sales of used film equipment which amounted to $0.3 million in 2009 compared to $1.4 million in 2008. These used units were obtained from theatre chains which had converted their film auditoriums to digital and had no further use for the film projectors. The decrease in used equipment sales during 2009 resulted from the lack of quality used equipment in the market. While we anticipated a short-term opportunity to buy, refurbish and resell the suitably conditioned units as they became available, we have not seen a significant change in used equipment sales as a result of movie theatre complexes converting from film to digital equipment and only recorded immaterial sales related to these activities in 2010.