Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 0-16148

MULTI-COLOR CORPORATION

| Incorporated in the State of Ohio |

IRS Employer Identification Number 31-1125853 |

4053 Clough Woods Dr.

Batavia, OH 45103

(Address of principal executive offices)

(513) 381-1480

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, no par value

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ¨.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $133,237,000 based upon the closing price of $15.40 per share of Common Stock on the NASDAQ Global Select Market as of September 30, 2010, the last business day of the registrant’s most recently completed second fiscal quarter.

As of May 31, 2011, 13,367,927 shares of no par value Common Stock were issued and 13,298,712 shares of no par value Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement to be filed pursuant to Regulation 14A of the Exchange Act for its 2011 Annual Meeting of Shareholders to be held on August 10, 2011 are incorporated by reference into Parts II and III of Form 10-K.

Table of Contents

FORWARD-LOOKING STATEMENTS

The Company believes certain statements contained in this report that are not historical facts constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, and are intended to be covered by the safe harbors created by that Act. Reliance should not be placed on forward-looking statements because they involve known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements to differ materially from those expressed or implied. Any forward-looking statement speaks only as of the date made. The Company undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date on which they are made.

Statements concerning expected financial performance, on-going business strategies, and possible future actions which the Company intends to pursue in order to achieve strategic objectives constitute forward-looking information. Implementation of these strategies and the achievement of such financial performance are each subject to numerous conditions, uncertainties and risk factors. Factors which could cause actual performance by the Company to differ materially from these forward-looking statements include, without limitation, factors discussed in conjunction with a forward-looking statement; changes in general economic and business conditions; the ability to consummate and successfully integrate acquisitions; the ability to manage foreign operations; currency exchange rate fluctuations; the success and financial condition of the Company’s significant customers; competition; acceptance of new product offerings; changes in business strategy or plans; quality of management; the Company’s ability to maintain an effective system of internal control; availability, terms and development of capital and credit; cost and price changes; raw material cost pressures; availability of raw materials; ability to pass raw material cost increases to its customers; business abilities and judgment of personnel; changes in, or the failure to comply with, government regulations, legal proceedings and developments; risk associated with significant leverage; increases in general interest rate levels affecting the Company’s interest costs; ability to manage global political uncertainty; and terrorism and political unrest. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

2

Table of Contents

| ITEM 1. | BUSINESS |

(In thousands, except for statistical and per share data)

OVERVIEW

Multi-Color Corporation (Multi-Color, MCC, We, Us, Our or the Company), headquartered in Cincinnati, Ohio, is a leader in global label solutions supporting a number of the world’s most prominent brands including leading producers of home and personal care, wine & spirit, food and beverage and specialty consumer products. MCC serves international brand owners in North, Central and South America, Europe, Australia, New Zealand, South Africa and China with a comprehensive range of the latest label technologies in Pressure Sensitive, Glue-Applied (Cut and Stack), In-Mold, Shrink Sleeve and Heat Transfer. MCC is a public company trading on the NASDAQ Global Select Market (company symbol: LABL).

The Company was incorporated in 1985, succeeding the predecessor business. Our corporate offices are located at 4053 Clough Woods Drive, Batavia, Ohio 45103 and our telephone number is (513) 381-1480.

Our common stock, no par value, is listed on the NASDAQ Global Select Market under the symbol “LABL”. See “Item 5 – Market for the Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities.” We maintain a website (www.mcclabel.com) which includes additional information about the Company. The website includes corporate governance information for our shareholders and our Code of Ethics can be found under the corporate governance section. Shareholders can also obtain on and through our website, free of charge, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after the Company electronically files such materials with or furnishes such materials to the Securities and Exchange Commission (SEC).

PRODUCTS AND SERVICES

The Company provides a wide range of products for the packaging needs of our customers and is one of the world’s largest producers of high quality pressure sensitive, in-mold and heat transfer labels, and a major manufacturer of glue-applied and shrink sleeve labels. The Company also provides a full complement of print methods including flexographic, lithographic, rotogravure and digital, plus in-house pre-press services.

Pressure Sensitive Labels:

Pressure sensitive labels adhere to a surface with pressure. The label typically consists of four elements – a substrate, which may include paper, foil or plastic; an adhesive, which may be permanent or removable; a release coating; and a backing material to protect the adhesive against premature contact with other surfaces. The release coating and protective backing are removed prior to application to the container, exposing the adhesive, and the label is pressed or rolled into place. Innovative features of this product include promotional neckbands, peel-away coupons, resealable labels, see-through window graphics, and holographic foil enhancements to cold and hot foil stamping.

The pressure sensitive market is the largest category of the overall label market and represents a significant growth opportunity. Our strategy is to be a premier global supplier of pressure sensitive labels that demand high impact graphics or are otherwise technically challenging.

In-Mold Labels:

The in-mold label (IML) process applies a label to a plastic container as the container is being formed in the mold cavity. The finished IML product is a finely detailed label that performs consistently well for plastic container manufacturers and adds marketing value and product security for consumer product companies.

Each component of the IML production process requires a special expertise for success. The components include the substrate (the base material for the label), inks, overcoats, varnishes and adhesives. We are unique in the industry in that we manufacture IMLs on rotogravure, flexographic and lithographic printing presses. There are several critical characteristics of a successful IML: the material needs a proper coefficient of friction so that the finished label is easily and consistently picked up and applied to the blow-molded container, the substrate must be able to hold the label’s inks, including metallics and fluorescents, overlay varnishes and adhesives and the material must be able to lay smoothly, without wrinkle or bulge, when applied to a very hot, just molded plastic container that will quickly shrink, along with the label, as its temperature falls. We continually search for alternate substrates to be used in the IML process in order to improve label performance and capabilities as well as to reduce substrate costs. Technical innovations in this area include the use of peel-away IML coupons, scented and holographic labels.

Glue-Applied Labels (Cut and Stack):

Glue-applied labels are adhered to containers using an adhesive applied during the labeling process. Available in roll-fed and sheeted formats, the labels are an attractive and cost-effective choice for high volume applications. Our facilities in Norway, Michigan, Watertown, Wisconsin, Napa, California, Griffith and Barossa Valley, Australia and Tuscany, Italy supply either offset or rotogravure glue-applied labels printed on paper and film.

3

Table of Contents

Our innovations within glue-applied labels include peel-away promotional labels, thermochromics, holographics and metalized films. We also offer promotional products such as scratch-off coupons, static-clings and tags.

Heat Transfer Labels (HTL):

HTL are reverse printed and transferred from a special release liner onto the container using heat and pressure. The labels are a composition of inks and lacquers tailored to the customer’s specific needs. These labels are printed and then shipped to blow molders and/or contract decorators who transfer the labels to the containers. Once applied, the labels are permanently adhered to the container. The graphics capabilities include fine vignettes, metallic and thermochromatic inks, as well as the patented “frost”, giving an acid-etch appearance.

Therimage™ is our pioneer heat transfer label technology developed primarily for applications involving plastic containers serving consumer markets in personal care, home improvement products, food and beverage, and health and beauty. The addition of the Clear ADvantage™ brand provides premium graphics on both glass and plastic containers enabling this decorating technology to achieve the highly sought after “no label” look for the health and beauty aid, beverage, personal care, household chemical and promotional markets. Most recently, we have added the new “ink only” and flameless HTL technology to our capabilities in this area. Flameless technology enables us to provide a solution to customers who want to remove open flames from their operations, which are normally required to pre-treat and post-treat containers for Therimage™ and Clear ADvantage™ products. Flameless technology has applications in all the aforementioned markets.

Shrink Sleeve Labels:

Shrink sleeve labels are produced in colorful, cutting edge styles and materials. The labels are manufactured as sleeves, slid over glass or plastic bottles and then heated to conform precisely to the contours of the container. The 360-degree label and tamper resistant feature of the label are marketing advantages that many of our customers seek when choosing this label type.

The shrink sleeve market is a growing decorating technology as consumer product companies look for ways to differentiate their products. Several markets, such as the beverage market within the consumer goods industry, have adopted this decorating technology. Demand for this label solution in the food and personal care markets continues to grow and should broaden the sales opportunities for shrink sleeve labels.

Graphic Services:

We provide graphics and pre-press services for our customers at all of our manufacturing locations. These services include the conversion of customer digital files and artwork into proofs, production of print layouts and printing plates, and product mock ups and samples for market research.

As a result of these capabilities, we are able to go from concept to printed label, thus increasing our customers’ speed to market and further enhancing our value proposition.

RESEARCH AND DEVELOPMENT

Our product leadership group focuses on research and development, product commercialization and technical service support. The group includes chemical, packaging and field engineers who are responsible for developing and commercializing innovative label and application solutions. Technical service personnel also assist customers and manufacturers in improving container and label performance. The services provided by this group differentiate us from many of our competitors and drive our selection for the most challenging projects.

Our research and development expenditures totaled approximately $2,628 in 2011, $2,658 in 2010, and $3,426 in 2009.

SALES AND MARKETING

We provide a complete line of label solutions and a variety of technical and graphic services. Our vision is to be the premier global resource of decorating solutions. We sell to a broad range of consumer product, food, beverage and wine & spirit companies located in North, Central and South America, Europe, Australia, New Zealand, South Africa and China. Our sales strategy is a consultative selling approach. Our sales organization reviews the requirements of the container and offers a number of alternative decorating methods. Our customers view us as an expert source of materials, methods and technologies with the ability to offer the most cost effective solution.

We have continued to make progress in expanding our customer base and portfolio of products, services and manufacturing locations in order to address issues related to customer concentration. During 2011, 2010 and 2009, sales to major customers (those exceeding 10% of the Company’s net revenues in one or more of the periods presented) approximated 22%, 28% and 32%, respectively, of the Company’s consolidated net revenues. Approximately 16%, 18% and 19% of sales in 2011, 2010 and 2009, respectively, were to the Procter & Gamble Company; approximately 6%, 10% and 13% of sales in 2011, 2010 and 2009, respectively, were to the Miller Brewing Company. Since 2008, sales concentration with our major customers has been significantly reduced since we have added new customers and products with our acquisition of Collotype, which has manufacturing operations in Australia, South Africa and California and our acquisitions of Guidotti CentroStampa (CentroStampa) and Monroe Etiquette, which have manufacturing operations in Italy and France.

4

Table of Contents

MANUFACTURING

As of March 31, 2011, we had 14 manufacturing facilities across the U.S., Australia, South Africa, Europe and Asia. Due to the acquisitions of La Cromografica in April 2011, and the label operations in Santiago, Chile and Mendoza, Argentina in May 2011, we currently have 17 manufacturing facilities across the U.S., Australia, South Africa, Europe, Asia and South America. Our wide range of capabilities and versatility facilitates our ability to respond quickly and effectively to changing customer needs. Our current printing equipment consists of gravure, offset, flexographic, letterpress and digital presses and label finishing operations. As part of a manufacturing expansion in North America, plants in Troy and Batavia, Ohio were consolidated into a new and larger facility in Batavia, Ohio. The pre-existing Batavia facility was sold in June 2008 and the Troy facility was sold in July 2009. In July 2009, we closed our Framingham manufacturing facility and the business was transitioned into our Batavia, Ohio and Scottsburg, Indiana facilities. In February, 2010, the Company entered into a supply agreement to fulfill gravure cylinder requirements. As a part of the agreement, the Company sold certain assets associated with the manufacturing of gravure cylinders. The Erlanger facility is currently held for sale. The Norway, Michigan, Watertown and Green Bay, Wisconsin, Adelaide, South Australia and Tuscany, Italy plants are ISO 9001 certified.

At March 31, 2011, our backlog was approximately $14,704 ($13,615 at March 31, 2010). The backlog at March 31, 2011 represents one to two weeks of production volume at current staffing levels and is expected to be completed in the next fiscal year.

EMPLOYEES

As of March 31, 2011, we had approximately 1,353 permanent employees and 77 temporary employees, of which 73 are represented by the Graphics Communications Conference of the International Brotherhood of Teamsters Local 77P. The related labor contracts with this union expire in June 2011 and July 2013. We consider our labor relations to be good and have not experienced any work stoppages during the previous decade. Our human resource and compensation systems have been developed to align our objectives with the goals of our shareholders.

RAW MATERIALS

Common to the printing industry, we purchase proprietary products from a number of raw material suppliers. To prevent potential disruptions to our manufacturing facilities, we have developed relationships with more than one supply source for each of our critical raw materials. Our raw material suppliers are major corporations with successful historical performance. Although we intend to prevent any long-term business interruption due to our inability to obtain raw materials, there could be short-term manufacturing disruptions during the customer qualification period for any new raw material source.

ACQUISITIONS

We are continually in pursuit of selective acquisitions that will contribute to our growth. We believe that acquisitions are a method of increasing our presence in existing markets, expanding into new markets, gaining new customers and product offerings and improving operating efficiencies through economies of scale. Through acquisitions, we intend to broaden our revenue stream by expanding our lines of innovative label solutions, offering a variety of technical and graphic services and fulfilling the specific needs and requirements of our customers. The printing and packaging industry is highly fragmented and offers many opportunities for acquisitions.

On July 1, 2010, we acquired Guidotti CentroStampa, a leading European wine & spirit and olive oil label specialist based in Tuscany, Italy. The acquisition expanded MCC’s global presence in the wine & spirit label market and provided an entry into the olive oil label market.

On October 1, 2010, we acquired Monroe Etiquette, a French wine label specialist based in Montagny, France. The acquisition reinforced MCC’s commitment to expanding its global presence in the wine label market.

During the third quarter of fiscal 2011, we announced plans to invest in establishing operations in China. Our operations, which are located in the major southern city of Guangzhou, became fully operational in the first quarter of fiscal 2012.

On April 1, 2011, we acquired La Cromografica, an Italian wine label specialist located in Florence, Italy. La Cromografica specializes in high quality wine labels for Italian premium wines.

On May 2, 2011, we acquired 70% ownership in two label operations, one in Santiago, Chile and the other in Mendoza, Argentina. These label operations will focus on providing premium labels to the expanding Latin American wine & spirit markets.

See Note 17 to our consolidated financial statements for geographic information relating to our net revenues and long-lived assets. See Note 3 to our consolidated financial statements for further information regarding the CentroStampa and Monroe Etiquette acquisitions. See Note 24 to our consolidated financial statements for further information regarding the acquisitions of La Cromografica and the label operations in Chile and Argentina.

COMPETITION

We have a large number of competitors in the pressure sensitive and glue-applied label markets and several competitors in each of the IML, shrink sleeve and HTL markets. Some of these competitors in the pressure sensitive and glue-applied label markets have greater financial and other resources than us. The competitors in IML, shrink sleeve and HTL markets are either private companies or subsidiaries of public companies and we cannot assess the financial resources of these organizations. We could be adversely affected should a competitor develop labels similar or technologically superior to our labels. We believe competition is principally dependent upon product performance, service, pricing, technical support and innovation.

5

Table of Contents

PATENTS AND LICENSES

We own a number of patents and patent applications in the U.S., Australia, South Africa and the European Union that relate to the products and services we offer to our customers. Although these patents are important to us, we are not dependent upon any one patent. We believe that these patents, collectively, along with our ability to be a single source provider of many packaging needs, provide us with a competitive advantage over our competition. The expiration or unenforceability of any one of our patents would not have a material adverse effect on us.

REGULATION

Our operations are subject to regulation by federal, state and foreign (Australia, South Africa, Italy, France, China and South America) environmental protection agencies. To ensure ongoing compliance with these requirements, we have implemented an internal compliance program. Additionally, we continue to make capital investments to maintain compliance with these environmental regulations and to improve our existing equipment. However, there can be no assurances that these regulations will not require expenditures beyond those that are currently anticipated.

In the U.S., the Food and Drug Administration regulates the raw materials used in labels for various products. These regulations apply to the consumer product companies for which we produce labels. We use materials specified by the consumer product companies in producing labels.

| ITEM 1A. | RISK FACTORS |

We rely on several large customers and the loss of one of these customers would have a material adverse impact on our operating results and cash flows.

For the fiscal year ended March 31, 2011, two customers accounted for approximately 22% of our consolidated sales and our top twenty-five customers accounted for 61% of our consolidated sales. While we maintain sales contracts with certain of our largest customers, such contracts do not guarantee sales levels and these contracts require renewal on a regular basis in the ordinary course of business. We cannot guarantee that these contracts will be successfully renewed in the future. The loss or substantial reduction in business of any of our major customers could have a material adverse impact on our operating results and cash flows.

Competition in our business could limit our ability to retain current customers and attract new customers.

We have a large number of competitors in the markets in which we operate. Some of our competitors have greater financial and other resources than us. We could face competitive pressure through (a) new products developed by our competitors that are of superior quality, fit our customers’ needs better or have lower prices; (b) patents obtained or developed by competitors; (c) consolidation of our competitors; (d) pricing pressures; and (e) loss of proprietary supplies of certain materials. The inability to successfully overcome competition in our business could have a material adverse impact on our operating results and cash flows.

Raw material cost increases or shortages could adversely affect our results of operations and cash flows.

As a manufacturer, our sales and profitability are dependent upon the availability and cost of raw materials, which are subject to price fluctuations, and the ability to control or pass on fluctuating costs of raw materials. Inflationary and other increases in the costs of raw materials and energy have occurred in the past and are continuing to recur. Our future performance depends in part on our ability to improve operating efficiencies and pass raw material cost increases to our customers.

We have risks related to continued uncertain global economic and credit conditions.

The Company’s operating cash flows provide funding for debt repayment and various discretionary items such as capital expenditures and dividends. Uncertainty in global economic conditions has negatively impacted the overall economy which has adversely impacted demand for our products and our ability to manage commercial relationships with our customers, suppliers and creditors.

Slower growth or a decline in key markets could adversely affect our profitability.

Our business could be negatively impacted by continued slower growth or a decline in key end use markets or applications for our products and services which could adversely affect our operating results and cash flows.

Changes in the regulatory or administrative environment could adversely affect our financial condition and results of operations.

Laws and regulations at both the state, federal and international levels frequently change and the cost of compliance cannot be precisely estimated. Any changes in regulations, the imposition of additional regulations, or the enactment of any new governmental legislation that impacts employment/labor, trade, health care, tax, environmental or other business issues could have an adverse impact on our financial condition and results of operations.

We are subject to risks associated with our international operations.

We have operations in the United States, Australia, South Africa, Europe and China and we intend to continue expansion of our international operations. As a result, our business is exposed to risks inherent in foreign operations. These risks, which can vary substantially by market, include the difficulties associated with managing an organization with operations in multiple countries,

6

Table of Contents

compliance with differing laws and regulations (including tax laws, regulations and rates), enforcing agreements and collecting receivables through foreign legal systems, restrictive actions by foreign governments, changes in economic conditions in each market, foreign customers who may have longer payment cycles than customers in the United States, political and social conditions (including wars, terrorist acts and political instability) and acts of nature, such as typhoons, tsunamis, or earthquakes. Approximately 37% of our net revenues were derived from our foreign operations (based on the country from which the product was shipped) during fiscal 2011.

We also face the challenges and uncertainties associated with operating in developing markets such as China, which may subject us to a relatively high risk of political instability and economic volatility, all of which are enhanced, in many cases, by uncertainties as to how local law is applied and enforced, including in areas most relevant to commercial transactions and foreign investment.

Currency exchange rate fluctuations could have an adverse effect on our revenue and financial results.

Our revenues and earnings and the value of our foreign net assets are affected by fluctuations in foreign currency exchange rates, which may favorably or adversely affect reported earnings and net assets. Currency exchange rates fluctuate in response to, among other things, changes in local, regional or global economic conditions, the imposition of currency exchange restrictions and unexpected changes in regulatory or taxation environments.

Our ability to develop and market new products is critical for maintaining growth.

Our success depends upon the timely introduction of new products as well as improvements to current products. Research and development relies on innovation and requires anticipation of market trends. Our future results and ability to maintain or improve our competitive position will depend on our ability to successfully identify, develop and sell new or improved products.

We rely primarily on printing presses.

The long-term shutdown of our presses or malfunctions experienced with our presses could negatively impact our ability to fulfill customers’ orders and on-time delivery needs and adversely impact our operating results and cash flows.

Our ability to stay current with our information technology systems could have a material adverse impact on our business.

We are increasingly dependent on the information technology systems we have put into place and any significant breakdown, viruses or destruction could negatively impact our business. We upgrade and install new systems, which if installed or programmed incorrectly, could cause significant disruptions. If a disruption occurs, we could incur losses and costs for interruption of our operations.

If the quality of our products and services does not meet our customer expectations, we may experience decreased sales and earnings.

Occasionally, we ship products with quality issues resulting from defective material, manufacturing, packaging or design. Issues discovered after shipment may cause additional shipping costs, possible discounts or refunds, and potential loss of future sales. Issues discovered before shipping may cause delays in shipping, delays in the manufacturing process and potential cancelled orders. These quality issues could adversely affect our profitability as well as negatively impact our reputation.

Our business growth strategy is partially executed through acquisitions and we may not be successful with acquisitions.

Although we have completed many acquisitions, there can be no assurance that we will find quality businesses at acceptable prices to acquire in the future. With each acquisition that we may complete, we will encounter risks and uncertainties associated with the transaction. We may be unable to retain certain customers and employees and the integration of product lines, procedures, systems and goals may not be successful. Any expected cost synergies from an acquisition may be difficult to obtain. The failure in our ability to successfully integrate an acquisition may negatively impact our operating results and cash flows. Future acquisitions could cause us to incur additional debt, contingent liabilities and increased interest expense, as well as experience dilution in earnings per share.

Our leverage and restrictions contained in our debt agreements could have significant consequences.

As of March 31, 2011, our consolidated indebtedness, including current maturities of long-term indebtedness, was $127,331, which could have important consequences including the following:

| • | Increasing our vulnerability to general economic and industry conditions; |

| • | Requiring a substantial portion of cash flows from operating activities to be dedicated to the payment of principal and interest on our indebtedness and, as a result, reducing our ability to use our cash flows to fund our operations and capital expenditures, pay dividends, capitalize on future business opportunities and expand our business; |

| • | Exposing us to the risk of increased interest expense as certain of our borrowings are at variable rates of interest; |

| • | Limiting our ability to obtain additional financing for working capital, capital expenditures, additional acquisitions and other business purposes; and |

| • | Limiting our flexibility to adjust to changing market conditions and react to competitive pressures. |

7

Table of Contents

We may be able to incur additional indebtedness in the future, subject to the restrictions contained in our debt agreements. If new indebtedness is added to our current debt levels, the related risks that we now face could intensify.

Our debt agreements contain covenants that limit our flexibility in operating our business.

The agreements governing our indebtedness contain various covenants that may adversely affect our ability to operate our business. Among other things, these covenants limit our ability to:

| • | Incur additional indebtedness; |

| • | Make certain investments or loans; |

| • | Transfer or sell certain assets; |

| • | Create or permit liens on assets; and |

| • | Consolidate, merge, sell or otherwise dispose of all or substantially all of our assets. |

The agreements governing our indebtedness also require us to maintain (i) a minimum consolidated net worth, (ii) a maximum consolidated leverage ratio of 3.75 to 1.00, stepping down to 3.25 to 1.00 from September 30, 2011 to March 31, 2012 and stepping down again to 3.00 to 1.00 at June 30, 2012 for each fiscal quarter thereafter; and (iii) a minimum consolidated interest charge coverage ratio of 4.00 to 1.00. A breach of any of these covenants could result in a default under our debt agreements, which could prompt the lenders to declare all amounts outstanding under the debt agreements to be immediately due and payable and terminate commitments to extend further credit. If we were unable to repay these amounts, the lenders could proceed against the collateral that secures the indebtedness.

We need to comply with various environmental, health and safety laws.

We are subject to environmental, health and safety laws and regulations. We routinely incur costs in complying with these regulations and, if we fail to comply, could incur significant penalties. In addition, failure to comply with environmental requirements could require us to shut down or reduce production or create liability exposure. New environmental laws or regulations may be adopted that could constrain our operations or increase our environmental compliance costs.

We must be able to continue to effectively manage our growth.

We have experienced significant and steady growth over the last several years. Our growth, in particular the acquisitions of Monroe Etiquette in October 2010, CentroStampa in July 2010 and Collotype in February 2008, places significant demands on our resources and personnel and we must continue to motivate and guide our growing and evolving workforce. The failure to effectively manage our growth could have a material adverse impact on our operating results and cash flows.

We have a significant amount of goodwill and other intangible assets on our balance sheet; an impairment of our goodwill or other intangible assets may adversely affect our operating results.

As of March 31, 2011, we had $196,573 of goodwill and intangible assets on our balance sheet, the value of which depends on a number of factors, including earnings growth, market capitalization and the overall success of our business. Accounting standards require us to test goodwill annually for impairment, and more frequently when events or circumstances indicate impairment may exist. There can be no assurance that future reviews of our goodwill and other intangible assets will not result in impairment charges. Although it does not affect cash flow, an impairment charge does have the effect of decreasing our earnings, assets and shareholders’ equity.

| ITEM 1B. | UNRESOLVED SECURITIES AND EXCHANGE COMMISSION STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

As of March 31, 2011, the Company owned 5 manufacturing facilities in the U.S and leased 9 manufacturing facilities in the U.S., Australia, South Africa, France, Italy and China.

8

Table of Contents

See below for listing of facilities at March 31, 2011:

| Location |

Approximate Square Feet |

Owned/ Leased |

||||||

| Batavia, Ohio |

247,830 | Owned | ||||||

| Green Bay, Wisconsin |

39,600 | Owned | ||||||

| Norway, Michigan |

133,000 | Owned | ||||||

| Watertown, Wisconsin |

63,300 | Owned | ||||||

| Napa, California |

52,000 | Leased | ||||||

| Scottsburg, Indiana |

120,500 | Owned | ||||||

| Tuscany, Italy |

119,479 | Leased | ||||||

| Montagny, France |

20,000 | Leased | ||||||

| Guangzhou, China |

43,056 | Leased | ||||||

| Adelaide, Australia |

65,246 | Leased | ||||||

| Queensland, Australia |

38,642 | Leased | ||||||

| Barossa, Australia |

25,306 | Leased | ||||||

| Griffith, Australia |

21,775 | Leased | ||||||

| Paarl, South Africa |

25,726 | Leased | ||||||

All of the Company’s properties are in good condition, well maintained and adequate for our intended uses.

| ITEM 3. | LEGAL PROCEEDINGS |

On April 5, 2011, the Company and four MCC employees who were formerly employed by the John Henry Company, as defendants, entered into a Confidential Settlement Agreement and Mutual General Release with the John Henry Company and Multi Packaging Solutions, as plaintiffs. The settlement relates to the complaint for damages and injunctive relief filed by plaintiffs in the Superior Court for Napa County, California on February 26, 2010. The complaint included allegations of improper taking and use of certain confidential and proprietary information by the employee defendants, which were denied by MCC and the employee defendants.

Pursuant to the Agreement and upon MCC’s payment of $2,800 to the John Henry Company, in April 2011, plaintiffs filed a request for dismissal of the complaint, the mutual release of all claims and potential claims arising out of the complaint became effective and the related injunction was deemed dissolved.

The Company is also subject to various legal claims and contingencies that arise out of the normal course of business, including claims related to commercial transactions, product liability, health and safety, taxes, environmental, employee-related matters and other matters. Litigation is subject to numerous uncertainties and the outcome of individual claims and contingencies is not predictable. It is possible that some legal matters for which reserves have not been established could result in an unfavorable outcome for the Company and any such unfavorable outcome could have a material adverse effect on our financial condition, results of operations and cash flows.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

[Removed and Reserved]

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON STOCK, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our shares trade in the NASDAQ Global Select Market under the symbol LABL. The following table sets forth the high and low closing sales prices of our common stock (“Common Stock”) as reported in the NASDAQ Stock Market during fiscal years 2011 and 2010. Our stock is thinly traded and accordingly, the prices below may not be indicative of prices at which a large number of shares can be traded or reflective of prices that would prevail in a more active market.

| Quarter Ending: |

High | Low | Dividend Per Share | |||||||||

| March 31, 2011 |

$ | 20.30 | $ | 16.62 | $ | 0.05 | ||||||

| December 31, 2010 |

$ | 20.42 | $ | 15.48 | $ | 0.05 | ||||||

| September 30, 2010 |

$ | 15.45 | $ | 10.26 | $ | 0.05 | ||||||

| June 30, 2010 |

$ | 13.53 | $ | 9.83 | $ | 0.05 | ||||||

| March 31, 2010 |

$ | 13.60 | $ | 11.03 | $ | 0.05 | ||||||

| December 31, 2009 |

$ | 14.73 | $ | 10.92 | $ | 0.05 | ||||||

| September 30, 2009 |

$ | 17.55 | $ | 12.08 | $ | 0.05 | ||||||

| June 30, 2009 |

$ | 14.44 | $ | 10.76 | $ | 0.05 | ||||||

As of May 31, 2011, there were approximately 330 shareholders of record of the Common Stock.

Beginning in and since the fourth quarter of the fiscal year ended March 31, 2005, we have paid a quarterly dividend of $0.05 per common share.

9

Table of Contents

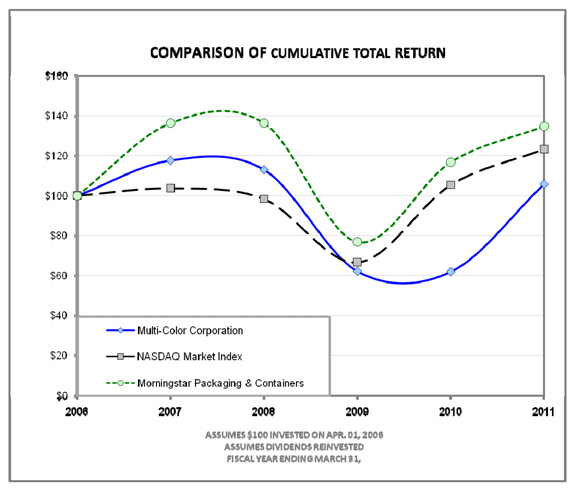

FIVE YEAR PERFORMANCE GRAPH

The following performance graph compares Multi-Color’s cumulative annual total shareholder return from April 1, 2006 through March 31, 2011, to that of the NASDAQ Market Index, a broad market index and the Morningstar Packaging & Containers Index (“Morningstar index”), an index of approximately 40 printing and packaging industry peer companies. The graph assumes that the value of the investment in the common stock and each index was $100 on April 1, 2006, and that all dividends were reinvested. Stock price performances shown in the graph are not indicative of future price performances. This data was furnished by Morningstar, Inc.

| Company/Market/Peer Group |

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||||

| Multi-Color Corporation |

$ | 100.00 | $ | 117.72 | $ | 113.09 | $ | 62.28 | $ | 62.02 | $ | 105.92 | ||||||||||||

| NASDAQ Market Index |

$ | 100.00 | $ | 103.72 | $ | 98.30 | $ | 66.56 | $ | 105.37 | $ | 123.35 | ||||||||||||

| Morningstar Packaging & Containers |

$ | 100.00 | $ | 136.45 | $ | 136.45 | $ | 76.81 | $ | 116.90 | $ | 134.88 | ||||||||||||

10

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA |

(In thousands, except per share data)

| Year Ended March 31, | ||||||||||||||||||||

| 2011(1) | 2010(2)(7) | 2009(3)(7) | 2008(4)(7) | 2007(5)(7) | ||||||||||||||||

| Net revenues |

$ | 338,284 | $ | 276,821 | $ | 289,763 | $ | 210,307 | $ | 192,551 | ||||||||||

| Gross profit |

67,978 | 48,601 | 52,806 | 38,926 | 37,149 | |||||||||||||||

| Operating income |

32,260 | 22,911 | 22,865 | 17,499 | 13,846 | |||||||||||||||

| Income from continuing operations |

18,411 | 14,268 | 11,435 | 16,007 | 8,612 | |||||||||||||||

| Income (loss) from discontinued operations |

— | — | (137 | ) | 6,977 | 2,414 | ||||||||||||||

| Net income |

18,411 | 14,268 | 11,298 | 22,984 | 11,026 | |||||||||||||||

| Basic earnings per share: |

||||||||||||||||||||

| Income from continuing operations (6) |

$ | 1.42 | $ | 1.17 | $ | 0.94 | $ | 1.57 | $ | 0.87 | ||||||||||

| Income (loss) from discontinued operations (6) |

— | — | (0.01 | ) | 0.68 | 0.24 | ||||||||||||||

| Basic earnings per common share (6) |

$ | 1.42 | $ | 1.17 | $ | 0.93 | $ | 2.25 | $ | 1.11 | ||||||||||

| Diluted earnings per common share: |

||||||||||||||||||||

| Income from continuing operations (6) |

$ | 1.40 | $ | 1.16 | $ | 0.93 | $ | 1.52 | $ | 0.84 | ||||||||||

| Income (loss) from discontinued operations (6) |

— | — | (0.01 | ) | 0.66 | 0.24 | ||||||||||||||

| Diluted earnings per common share (6) |

$ | 1.40 | $ | 1.16 | $ | 0.92 | $ | 2.18 | $ | 1.08 | ||||||||||

| Weighted average shares outstanding – basic (6) |

13,005 | 12,209 | 12,156 | 10,212 | 9,904 | |||||||||||||||

| Weighted average shares outstanding – diluted (6) |

13,139 | 12,332 | 12,355 | 10,520 | 10,221 | |||||||||||||||

| Dividends declared per common share (6) |

$ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.16 | $ | 0.12 | ||||||||||

| Dividends paid |

2,612 | 2,469 | 2,449 | 1,688 | 1,323 | |||||||||||||||

| Working capital |

30,357 | 19,934 | 13,531 | 18,517 | 15,832 | |||||||||||||||

| Total assets |

411,829 | 285,342 | 258,208 | 314,080 | 107,081 | |||||||||||||||

| Short-term debt |

12,304 | 10,001 | 10,002 | 10,003 | 5,150 | |||||||||||||||

| Long-term debt |

115,027 | 75,642 | 92,317 | 121,748 | — | |||||||||||||||

| Stockholders’ equity |

$ | 191,826 | $ | 146,628 | $ | 103,032 | $ | 119,938 | $ | 64,423 | ||||||||||

| 1) | Fiscal 2011 results include a charge of $2,800 related to the settlement of a legal dispute with the John Henry Company. Results also include a pre-tax reduction of $258 to the initial charge recorded in fiscal 2010, in connection with the relocation of the Company’s corporate headquarters from Sharonville, Ohio to its Batavia, Ohio facility, to incorporate the impact of the additional sublease income on the sublease of the remaining unoccupied space. |

| 2) | Fiscal 2010 results include a pre-tax gain of $3,451 ($2,141 after-tax) related to the sale of certain assets associated with the manufacture of gravure cylinders and a charge of $1,219 ($959 after-tax) for remaining lease obligations and other costs related to the relocation of the Company’s corporate headquarters from Sharonville, Ohio to its Batavia, Ohio facility. |

| 3) | Fiscal 2009 results include a pre-tax charge of $2,553 ($1,634 after-tax) for expenses related to the closure of the Framingham manufacturing facility. |

| 4) | Fiscal 2008 results include a pre-tax gain of $7,659 ($5,001 after-tax) on foreign currency forward contracts (included in income from continuing operations) and a pre-tax gain of $11,278 ($6,922 after-tax) from the sale of Quick Pak (included in income (loss) from discontinued operations). |

| 5) | Fiscal 2007 results include $3,048 in pre-tax charges for expenses related to two potential acquisitions that were terminated during the third quarter 2007. |

| 6) | All share amounts have been adjusted to reflect the 3-for-2 stock split effective September 17, 2007. |

| 7) | Certain prior year amounts have been reclassified to conform to the current year presentation. |

Refer to Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of the impact of acquisitions completed during recent fiscal years that would impact the comparability of the selected financial data noted above. During fiscal 2011, we acquired Monroe Etiquette and CentroStampa which have manufacturing plants in France and Italy, respectively. On February 29, 2008, we acquired Collotype which included seven label manufacturing plants in Australia, South Africa and the United States.

11

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

(In thousands, except per share data)

The following discussion and analysis should be read in conjunction with Multi-Color’s consolidated financial statements and notes thereto appearing elsewhere herein.

RESULTS OF OPERATIONS

The following table shows for the periods indicated, certain components of Multi-Color’s consolidated statements of income as a percentage of net revenues.

| Percentage of Net Revenues | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| Net revenues |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cost of revenues |

79.9 | % | 82.4 | % | 81.8 | % | ||||||

| Gross profit |

20.1 | % | 17.6 | % | 18.2 | % | ||||||

| Selling, general & administrative expenses |

9.9 | % | 10.0 | % | 9.5 | % | ||||||

| Gain on sale of certain cylinder assets |

— | (1.2 | )% | — | ||||||||

| Loss on legal settlement |

0.8 | % | — | — | ||||||||

| Facility closure expense/(income), net |

(0.1 | )% | 0.5 | % | 0.9 | % | ||||||

| Operating income |

9.5 | % | 8.3 | % | 7.8 | % | ||||||

| Interest expense |

2.1 | % | 1.7 | % | 2.4 | % | ||||||

| Other (income) expense, net |

(0.1 | )% | (0.1 | )% | (0.1 | )% | ||||||

| Income from continuing operations before income tax |

7.5 | % | 6.7 | % | 5.5 | % | ||||||

| Income tax expense |

2.1 | % | 1.5 | % | 1.7 | % | ||||||

| Income from continuing operations |

5.4 | % | 5.2 | % | 3.8 | % | ||||||

| Income from discontinued operations, net of tax |

— | — | — | |||||||||

| Net income |

5.4 | % | 5.2 | % | 3.8 | % | ||||||

EXECUTIVE SUMMARY

We provide a complete line of innovative decorative label solutions and offer a variety of technical and graphic services to our customers based on their specific needs and requirements. Our customers include a wide range of consumer product companies and we supply labels for many of the world’s best known brands and products, including laundry detergent, fabric care, food, beverages and wine & spirit.

During fiscal 2011, the Company had net revenues of $338,284 compared to $276,821 in the prior year. The majority of the increase in revenues was due to the acquisitions of CentroStampa and Monroe Etiquette which contributed $44,323 or 16% of the revenue increases. The remaining increase was due to a 4% increase in sales volume and a 3% favorable foreign exchange impact, partially offset by a 1% unfavorable pricing impact.

Gross profit increased $19,377 or 40% compared to the prior year. The acquisitions of CentroStampa and Monroe Etiquette contributed 21% to the gross profit increase. The remaining increase was due to higher sales volumes, foreign exchange and improved operating efficiencies. Gross margins increased to 20% from 18% of sales revenues compared to the prior year.

Operating income increased $9,349 or 41% compared to the prior year. The CentroStampa and Monroe Etiquette acquisitions contributed 28% to the operating income increase. The remaining increase in operating income was due primarily to higher sales volumes, improved operating efficiencies, other cost decreases and the impact of foreign exchange.

The label markets we serve continue to experience a competitive environment and price pressures. We continually search for ways to reduce our costs through improved production and labor efficiencies, reduced substrate waste, new substrate options and lower substrate pricing.

We have continued to make progress in expanding our customer base and portfolio of products, services and manufacturing locations in order to address issues related to customer concentration. During 2011, 2010 and 2009, sales to major customers (those exceeding 10% of the Company’s net revenues in one or more of the periods presented) approximated 22%, 28% and 32%, respectively, of the Company’s consolidated net revenues. Approximately 16%, 18% and 19% of sales in 2011, 2010 and 2009, respectively, were to the Procter & Gamble Company; approximately 6%, 10% and 13% of sales in 2011, 2010 and 2009, respectively, were to the Miller Brewing Company. Sales concentration with our major customers has been significantly reduced since we have added new customers and products with our acquisitions of Monroe Etiquette, CentroStampa and Collotype which have manufacturing operations in France, Italy, Australia, South Africa and California.

On October 1, 2010, MCC acquired 100% of the shares of Monroe Etiquette for Euro 8,000, less net debt assumed (the Purchase Price). The seller received approximately 89% of the proceeds in the form of cash on October 1, 2010. The remaining 11% of the Purchase Price will be paid in cash, but is deferred for five years after the closing date. The seller has agreed to indemnify MCC with respect to the acquisition, including certain losses arising out of a breach of their warranties or covenants under the Agreement.

On June 28, 2010, the Company entered into a stock purchase agreement to acquire CentroStampa. On July 1, 2010, pursuant to the stock purchase agreement, the Company acquired 100% of the shares of CentroStampa for Euro 50,454 less net debt assumed. The

12

Table of Contents

selling shareholders received approximately 80% of the proceeds in the form of cash and 20% in the form of 934,567 shares of MCC common stock. This stock represented approximately 8% of MCC’s shares outstanding immediately prior to consummation of the acquisition.

On June 28, 2010, the Company entered into an amendment (the First Amendment) to the Company’s Credit Agreement dated as of February 29, 2008 (Credit Agreement) with the lenders thereunder, effective simultaneously with the closing of the acquisition.

The First Amendment amended the Credit Agreement to (i) permit the acquisition of CentroStampa by the Company; (ii) increase the Aggregate U.S. Revolving Commitment (as defined in the First Amendment) by $20,000 thereby increasing the total borrowing capacity from $180,000 to $200,000, with the potential to increase total borrowing capacity by $50,000; (iii) allow up to $40,000 of U.S. revolving loans to be advanced in alternative currencies; (iv) extend the maturity date of the Credit Facilities (as defined in the Credit Agreement) to April 1, 2014; (v) increase the maximum leverage ratio to 3.75 to 1.00 with scheduled step-downs; and (vi) implement a change in interest rate margins over the applicable Eurocurrency or Australian BBSY rate ranging from 1.75% to 3.25% based on the leverage ratio. The Company incurred $1,682 of debt issuance costs related to the debt modification which are being deferred and amortized over the life of the amended Credit Facility.

On February 12, 2010, the Company entered into a supply agreement to fulfill gravure cylinder requirements. As a part of the agreement, the Company sold certain assets associated with the manufacturing of gravure cylinders for $4,250 in cash. The Company recorded an after-tax gain of $2,141 on the sale in its fourth quarter fiscal 2010 financial results. The Erlanger facility is currently held for sale.

During fiscal 2010, the Company relocated its corporate headquarters from Sharonville, Ohio to its Batavia, Ohio facility in order to consolidate certain employees into existing owned office space. The lease for the Sharonville, Ohio location expires in April 2017. In connection with the relocation, the Company recorded a charge of $1,219 for remaining lease obligations and other costs related to its Sharonville facility. During the third quarter of fiscal 2011, the Company entered into a contract to sublease the remaining unoccupied space and recorded an adjustment of $258 to the initial charge to incorporate the impact of the additional sublease income.

In January 2009, the Company announced plans to consolidate its heat transfer label (HTL) manufacturing business located in Framingham, Massachusetts into its other existing facilities. The transition began immediately with final plant closure occurring in the second quarter of fiscal 2010. In connection with the closure of the Framingham facility, the Company recorded a total pre-tax charge of $2,553 during the fourth quarter period ending March 31, 2009, consisting of $1,407 in cash charges for employee severance and other termination benefits related to 62 associates and $1,146 in non-cash charges related to asset impairments.

On February 29, 2008, we acquired Collotype International Holdings Pty. Ltd. (Collotype) which is headquartered in Adelaide, South Australia. Collotype is the world’s leading and highly awarded pressure sensitive wine & spirit label manufacturer and a growing provider of labels in the fast-moving consumer goods marketplace in Australia. Collotype has manufacturing operations in Australia, South Africa and the United States.

Our vision is to be a premier global resource of decorating solutions. We currently serve customers located throughout North, Central and South America, Australia, South Africa, New Zealand, Italy, France and China. We continue to monitor and analyze new trends in the packaging and consumer products industries to ensure that we are providing appropriate services and products to our customers. Certain factors that influence our business include consumer spending, new product introductions, new packaging technologies and demographics.

Our key objectives for fiscal year 2012 include winning new customers, growing with existing customers, providing greater support to our blue chip customer base, improving our low cost manufacturing market position and continuing to develop our global operations foot print through selective acquisitions.

As part of our initiative to develop our global operations, on April 1, 2011, we acquired La Cromografica, an Italian wine label specialist located in Florence, Italy. La Cromografica specializes in high quality wine labels for Italian premium wines. On May 2, 2011, we also acquired 70% ownership in two label operations, one in Santiago, Chile and the other in Mendoza, Argentina. These label operations will focus on providing premium labels to the expanding Latin American wine & spirit markets.

COMPARISON OF FISCAL YEARS ENDED MARCH 31, 2011 AND MARCH 31, 2010

| 2011 | 2010 | $ Change |

% Change |

|||||||||||||

| Net Revenues | $ | 338,284 | $ | 276,821 | $ | 61,463 | 22 | % | ||||||||

Net revenues increased 22% to $338,284 from $276,821. The majority of the increase in revenues was due the acquisitions of CentroStampa and Monroe Etiquette which contributed $44,323 or 16% of the revenue increases. The remaining increase was due to a 4% increase in sales volume and a 3% favorable foreign exchange impact, partially offset by a 1% unfavorable pricing impact.

13

Table of Contents

| 2011 | 2010 | $ Change |

% Change |

|||||||||||||

| Cost of Revenues | $ | 270,306 | $ | 228,220 | $ | 42,086 | 18 | % | ||||||||

| % of Net Revenues |

79.9 | % | 82.4 | % | ||||||||||||

| Gross Profit | $ | 67,978 | $ | 48,601 | $ | 19,377 | 40 | % | ||||||||

| % of Net Revenues |

20.1 | % | 17.6 | % | ||||||||||||

Cost of revenues increased 18% or $42,086 due to the acquisitions of CentroStampa and Monroe Etiquette, which contributed 15% to the cost of revenue increase, higher sales volumes and foreign exchange.

Gross profit increased $19,377 or 40% compared to the prior year. The acquisitions of CentroStampa and Monroe Etiquette contributed 21% to the gross profit increase. The remaining increase was due to higher sales volumes, foreign exchange and improved operating efficiencies. Gross margins increased to 20% from 18% of sales revenues compared to the prior year.

Selling, General & Administrative (SG&A) and Other Operating Items

| 2011 | 2010 | $ Change |

% Change |

|||||||||||||

| Selling, General & Administrative (SG&A) Expense |

$ | 33,176 | $ | 27,662 | $ | 5,514 | 20 | % | ||||||||

| % of Net Revenues |

9.9 | % | 10.0 | % | ||||||||||||

| Gain on Sale of Certain Cylinder Assets |

$ | — | $ | (3,451 | ) | $ | 3,451 | 100 | % | |||||||

| % of Net Revenues |

— | % | (1.2 | %) | ||||||||||||

| Loss on Legal Settlement |

2,800 | $ | — | $ | 2,800 | 100 | % | |||||||||

| % of Net Revenues |

0.8 | % | — | % | ||||||||||||

| Facility Closure Expense |

$ | (258 | ) | $ | 1,479 | $ | (1,737 | ) | (117 | %) | ||||||

| % of Net Revenues |

(0.1 | %) | 0.5 | % | ||||||||||||

SG&A expenses increased 20% compared to the prior year due to $3,936 of SG&A from the acquisitions of CentroStampa and Monroe Etiquette during the year, $1,334 in acquisition and start-up expenses and $1,069 in legal fees partially offset by headcount reductions and other cost decreases.

In the fourth quarter of fiscal 2010, the Company sold certain assets associated with the manufacturing of gravure cylinders for $4,250 in cash and recorded a pre-tax gain of $3,451 during the fourth quarter of fiscal 2010.

In the fourth quarter of fiscal 2011, the Company recorded a charge of $2,800 related to the settlement of a legal dispute with the John Henry Company.

In fiscal 2010, the Company recorded facility closure expenses of $1,219 in connection with the relocation of its corporate headquarters and during the third quarter of fiscal 2011, recorded a pre-tax reduction to the initial charge of $258 to incorporate the impact of the additional sublease income on the sublease of the remaining unoccupied space. In fiscal 2010, the Company also incurred employee retention charges of $260 in connection with the closure of the Framingham facility.

Interest and Other (Income) Expense

| 2011 | 2010 | $ Change |

% Change |

|||||||||||||

| Interest Expense |

$ | 7,021 | $ | 4,753 | $ | 2,268 | 48 | % | ||||||||

| Other (Income) Expense, net |

$ | (210 | ) | $ | (326 | ) | $ | 116 | 36 | % | ||||||

Interest expense increased to $7,021 compared to $4,753 in the prior year due primarily to the increase in debt borrowings to finance the acquisitions of CentroStampa and Monroe Etiquette. Also contributing to the increase was the impact of higher interest rates and higher interest expense related to the present value adjustments of various lease and other liabilities.

Other income decreased $116 due primarily to higher realized losses on foreign exchange in fiscal 2011.

| 2011 | 2010 | $ Change |

% Change |

|||||||||||||

| Income Tax Expense | $ | 7,038 | $ | 4,216 | $ | 2,822 | 67 | % | ||||||||

The Company’s effective tax rate was 28% in fiscal 2011 compared to 23% in the prior year due primarily to an increase in income in higher tax jurisdictions, partially offset by the release of reserves for uncertain tax positions whose statute of limitations expired during fiscal 2011 and the finalization of the new tax structure related to the European operations. The Company recognized a tax benefit related to a foreign exchange loss on intercompany loans and other items resulting in a $1,069 benefit to income tax expense in the fourth quarter of fiscal 2010. The Company expects its annual effective tax rate to be approximately 27% in fiscal year 2012.

14

Table of Contents

COMPARISON OF FISCAL YEARS ENDED MARCH 31, 2010 AND MARCH 31, 2009

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Net Revenues | $ | 276,821 | $ | 289,763 | $ | (12,942 | ) | (4 | %) | |||||||

Net revenues decreased 4% to $276,821 from $289,763. The decrease in revenues was due to a 6% decline in sales volume and pricing partially offset by a 2% favorable foreign exchange impact. The sales decline attributable to volume and pricing was comprised of a $14,215 or 5% decrease in sales volume and mix and $3,952 or 1% of lower pricing. The 5% sales volume decline is primarily related to lower sales volumes to our top two customers.

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Cost of Revenues | $ | 228,220 | $ | 236,957 | $ | (8,737 | ) | (4 | %) | |||||||

| % of Net Revenues |

82.4 | % | 81.8 | % | ||||||||||||

| Gross Profit | $ | 48,601 | $ | 52,806 | $ | (4,205 | ) | (8 | %) | |||||||

| % of Net Revenues |

17.6 | % | 18.2 | % | ||||||||||||

Cost of revenues decreased 4% or $8,737 to $228,220 due to lower North American sales volumes in fiscal year 2010. Gross profit decreased 8% or $4,205 in 2010 compared to 2009 due to a decrease in revenues as a result of lower sales volume to our top two customers and lower pricing. Gross profit margins remained steady at approximately 18% of sales revenues compared to the prior year.

Selling, General & Administrative (SG&A), Gain on Sale of Certain Cylinder Assets and Facility Closure Expense

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Selling, General & Administrative (SG&A) Expense |

$ | 27,662 | $ | 27,388 | $ | 274 | 1 | % | ||||||||

| % of Net Revenues |

10.0 | % | 9.5 | % | ||||||||||||

| Gain on Sale of Certain Cylinder Assets |

$ | (3,451 | ) | $ | — | $ | (3,451 | ) | (100 | %) | ||||||

| % of Net Revenues |

(1.2 | %) | — | % | ||||||||||||

| Facility Closure Expense |

$ | 1,479 | $ | 2,553 | $ | (1,074 | ) | (42 | %) | |||||||

| % of Net Revenues |

0.5 | % | 0.9 | % | ||||||||||||

SG&A expenses increased $274 compared to the prior year due to $1,034 in severance charges and $940 in non-cash fixed asset impairments partially offset by the impact of cost reduction actions implemented in the prior year.

On February 12, 2010, the Company entered into a supply agreement to fulfill gravure cylinder requirements. As a part of the agreement, the Company sold certain assets associated with the manufacturing of gravure cylinders for $4,250 in cash. The Company recorded a pre-tax gain of $3,451 in the fiscal fourth quarter.

In connection with the closure of the Framingham facility, the Company incurred employee retention charges of $260 in fiscal year 2010 and in fiscal year 2009, a charge of $2,553 consisting of $1,407 in cash charges for employee severance and other termination benefits and plant shut down costs and $1,146 in non-cash asset impairments.

In connection with the relocation of the Company’s corporate headquarters from Sharonville, Ohio to Batavia, Ohio, the Company recorded a charge of $1,219 in facility closure expense in fiscal year 2010.

Interest and Other (Income) Expense

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Interest Expense |

$ | 4,753 | $ | 6,841 | $ | (2,088 | ) | (31 | %) | |||||||

| Other (Income) Expense, net |

$ | (326 | ) | $ | (378 | ) | $ | 52 | 14 | % | ||||||

Interest expense decreased $2,088 due to a $17,303 or 16% net repayment of bank debt and lower interest rates. The decrease in other income was due primarily to lower scrap sales in fiscal year 2010.

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Income Tax Expense | $ | 4,216 | $ | 4,967 | $ | (751 | ) | (15 | %) | |||||||

The Company’s effective tax rate was 23% in 2010 compared to 30% in 2009 due to income in lower tax jurisdictions and a recognized tax benefit related to a foreign exchange loss on intercompany loans and other items resulting in a $1,069 benefit to income tax expense in the fourth quarter of fiscal 2010.

15

Table of Contents

| 2010 | 2009 | $ Change |

% Change |

|||||||||||||

| Income (Loss) from Discontinued Operations, Net of Tax | $ | — | $ | (137 | ) | $ | 137 | 100 | % | |||||||

The sale of Quick Pak was completed during fiscal year 2008 and additional income tax expense related to the sale was recorded in fiscal year 2009. There was no discontinued operations activity during fiscal year 2010.

Critical Accounting Policies and Estimates

The preparation of consolidated financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenue and expenses. We continually evaluate our estimates, including, but not limited to, those related to revenue recognition, bad debts, inventories and any related reserves, income taxes, fixed assets, goodwill and intangible assets. We base our estimates on historical experience and on various other assumptions believed to be reasonable under the facts and circumstances. Actual results may differ from these estimates under different assumptions or conditions.

We believe the following critical accounting policies impact the more significant judgments and estimates used in the preparation of our consolidated financial statements. Additionally, our senior management has reviewed the critical accounting policies and estimates with the Board of Directors’ Audit and Finance Committee. For a more detailed discussion of the application of these and other accounting policies, refer to Note 2 of the Consolidated Financial Statements.

Revenue Recognition

The Company recognizes revenue on sales of products when the customer receives title to the goods, which is generally upon shipment or delivery depending on sales terms. Revenues are generally denominated in the currency of the country from which the product is shipped and are net of applicable returns and discounts.

Inventories

Inventories are valued at the lower of cost or market value and are maintained using the FIFO (first-in, first-out) or specific identification method. Excess and obsolete cost reductions are generally established based on inventory age.

Accounts Receivable

Our customers are primarily major consumer product, food, and wine & spirit companies and container manufacturers. Accounts receivable consist of amounts due from customers in connection with our normal business activities and are carried at sales value less allowance for doubtful accounts. The allowance for doubtful accounts is established to reflect the expected losses of accounts receivable based on past collection history, age and specific individual risks identified. Losses may also depend to some degree on current and future economic conditions. Although these conditions are unknown to us and may result in additional credit losses, we do not anticipate significant adverse credit circumstances in fiscal 2012. If we are unable to collect all or part of the outstanding receivable balance, there could be a material impact on the Company’s operating results and cash flows.

Goodwill and Other Acquired Intangible Assets

Goodwill is not amortized and the Company tests goodwill annually, as of the last day of February of each fiscal year, for impairment by comparing the fair value of the reporting unit goodwill to its carrying amount. Impairment is also tested when events or changes in circumstances indicate that the assets’ carrying values may be greater than the fair values. Intangible assets with definite useful lives are amortized using the straight-line method, which estimates the economic benefit, over periods of up to twenty years. Intangible assets are also tested for impairment when events or changes in circumstances indicate that the assets’ carrying values may be greater than the fair values.

The Company’s $158,553 of goodwill at March 31, 2011 relates primarily to the acquisitions of Collotype in 2008 and CentroStampa and Monroe Etiquette in fiscal 2011. The Company completed its annual goodwill impairment test in the fourth quarter of fiscal 2011. The first step of the impairment review compares the fair value of the Company to the carrying value. The fair value was calculated as of February 28, 2011 by calculating the Multi-Color market capitalization and adding a 15% control premium and comparing it to the Company’s shareholders’ equity balance. The result of the first step did not indicate potential impairment as the estimated fair value of its reporting unit exceeded the carrying value by $96,495. As a result, the second step of the impairment test was not required. Reasonably possible fluctuations in the stock price and market capitalization did not indicate impairment.

Impairment of Long-Lived Assets

We review long-lived assets for impairment whenever events or changes in circumstances indicate that assets might be impaired and the related carrying amounts may not be recoverable. The determination of whether impairment exists involves various estimates and assumptions, including the determination of the undiscounted cash flows estimated to be generated by the assets involved in the review. The cash flow estimates are based upon our historical experience, adjusted to reflect estimated future market and operating conditions. Measurement of an impairment loss requires a determination of fair value. We base our estimates of fair values on quoted market prices when available, independent appraisals as appropriate and industry trends or other market knowledge. Changes in the market condition and/or losses of a production line could have a material impact on the consolidated statements of income. The Company did not record any material impairment charges to long-lived assets during fiscal 2011.

16

Table of Contents

Income Taxes

Income taxes are recorded based on the current year amounts payable or refundable, as well as the consequences of events that give rise to deferred tax assets and liabilities. Deferred tax assets and liabilities result from temporary differences between the tax basis and reported book basis of assets and liabilities and result in taxable or deductible amounts in future years. Our accounting for deferred taxes involves certain estimates and assumptions that we believe are appropriate. Future changes in regulatory tax laws and/or different positions held by taxing authorities may affect the amounts recorded for income taxes.

The benefits of tax positions are not recorded unless it is more likely than not the tax position would be sustained upon challenge by the appropriate tax authorities. Tax benefits that are more likely than not to be sustained are measured at the largest amount of benefit that is cumulatively greater than a 50% likelihood of being realized.

Derivative Financial Instruments

The Company accounts for derivative financial instruments by recognizing derivative instruments as either assets or liabilities in the balance sheet at fair value and recognizing the resulting gains or losses as adjustments to earnings or accumulated other comprehensive income. The Company does not hold or issue derivative financial instruments for trading or speculative purposes.

The Company manages interest costs using a mixture of fixed rate and variable rate debt. Additionally, the Company enters into interest rate swaps whereby it agrees to exchange with a counterparty, at specified intervals, the difference between fixed and variable interest amounts calculated by reference to an agreed upon notional principal amount.

The Company’s interest rate swaps have been designated as effective cash flow hedges at inception and on an ongoing quarterly basis and therefore, any changes in fair value are recorded in other comprehensive income. If a hedge or portion thereof is determined to be ineffective, any changes in fair value would be recorded in the consolidated income statement. See Note 10.

The Company manages foreign currency exchange rate risk by entering into forward currency contracts. The forward contracts have been designated as effective fair value hedges at inception and on an ongoing quarterly basis and therefore, any changes in fair value are recorded in earnings. See Note 10.

Fair Value Disclosure

The carrying value of financial instruments approximates fair value.

The Company defines fair value as the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date. To increase consistency and comparability in fair value measurements, the Company uses a fair value estimating three-level hierarchy that prioritizes the use of observable inputs. The three levels are:

Level 1 – Quoted market prices in active markets for identical assets and liabilities

Level 2 – Observable inputs other than quoted market prices in active markets for identical assets and liabilities

Level 3 – Unobservable inputs

The determination of where an asset or liability falls in the hierarchy requires significant judgment.

The Company has two interest rate swaps, a $40,000 non-amortizing swap and a $40,000 amortizing swap, to convert variable interest rates on a portion of outstanding debt to fixed interest rates. The Company adjusts the carrying value of these derivatives to their estimated fair values and records the adjustment in other comprehensive income.

The Company has a forward currency hedge to fix the U.S. dollar value of a press purchased in Euros and delivered to the Batavia, Ohio plant. The forward contract is designated as a fair value hedge. The Company adjusts the carrying value of this derivative to its estimated fair value and records the adjustment in earnings.

Fair value measurements of nonfinancial assets and nonfinancial liabilities are primarily used in goodwill and other intangible asset impairment analyses and in the valuation of assets held for sale. The Company tests goodwill annually, as of the last day of February of each fiscal year, for impairment by comparing the fair value of the reporting unit goodwill to its carrying amount. Impairment is also tested when events or changes in circumstances indicate that the assets’ carrying values may be greater than the fair values.

Liquidity and Capital Resources