Attached files

| file | filename |

|---|---|

| EX-10.1 - EX-10.1 - IMPAC MORTGAGE HOLDINGS INC | a11-9507_1ex10d1.htm |

| EX-31.2 - EX-31.2 - IMPAC MORTGAGE HOLDINGS INC | a11-9507_1ex31d2.htm |

| EX-32.1 - EX-32.1 - IMPAC MORTGAGE HOLDINGS INC | a11-9507_1ex32d1.htm |

| EX-31.1 - EX-31.1 - IMPAC MORTGAGE HOLDINGS INC | a11-9507_1ex31d1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2011

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to .

Commission File Number: 1-14100

IMPAC MORTGAGE HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

|

Maryland |

|

33-0675505 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

19500 Jamboree Road, Irvine, California 92612

(Address of principal executive offices)

(949) 475-3600

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

|

Accelerated filer ¨ |

|

|

|

|

|

Non-accelerated filer o |

|

Smaller reporting company x |

|

(Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2) Yes o No x

There were 7,789,946 shares of common stock outstanding as of May 13, 2011.

IMPAC MORTGAGE HOLDINGS, INC.

FORM 10-Q QUARTERLY REPORT

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS

IMPAC MORTGAGE HOLDINGS, INC. AND SUBSIDIARIES

(dollars in thousands, except share data)

|

|

|

March 31, |

|

December 31, |

| ||

|

|

|

2011 |

|

2010 |

| ||

|

|

|

(Unaudited) |

|

|

| ||

|

ASSETS |

|

|

|

|

| ||

|

Cash and cash equivalents |

|

$ |

7,750 |

|

$ |

11,507 |

|

|

Restricted cash |

|

2,507 |

|

1,495 |

| ||

|

Trust assets |

|

|

|

|

| ||

|

Investment securities available-for-sale |

|

415 |

|

645 |

| ||

|

Securitized mortgage collateral |

|

6,053,766 |

|

6,011,675 |

| ||

|

Derivative assets |

|

37 |

|

40 |

| ||

|

Real estate owned |

|

74,709 |

|

92,708 |

| ||

|

Total trust assets |

|

6,128,927 |

|

6,105,068 |

| ||

|

|

|

|

|

|

| ||

|

Mortgage loans held-for-sale |

|

31,888 |

|

4,283 |

| ||

|

Finance receivables |

|

3,911 |

|

— |

| ||

|

Assets of discontinued operations |

|

296 |

|

373 |

| ||

|

Other assets |

|

30,515 |

|

31,213 |

| ||

|

Total assets |

|

$ |

6,205,794 |

|

$ |

6,153,939 |

|

|

|

|

|

|

|

| ||

|

LIABILITIES |

|

|

|

|

| ||

|

Trust liabilities |

|

|

|

|

| ||

|

Securitized mortgage borrowings |

|

$ |

6,056,577 |

|

$ |

6,012,745 |

|

|

Derivative liabilities |

|

46,243 |

|

65,916 |

| ||

|

Total trust liabilities |

|

6,102,820 |

|

6,078,661 |

| ||

|

|

|

|

|

|

| ||

|

Warehouse borrowings |

|

34,266 |

|

4,057 |

| ||

|

Long-term debt |

|

12,030 |

|

11,728 |

| ||

|

Notes payable |

|

4,763 |

|

6,874 |

| ||

|

Liabilities of discontinued operations |

|

12,004 |

|

13,053 |

| ||

|

Other liabilities |

|

13,155 |

|

11,869 |

| ||

|

Total liabilities |

|

6,179,038 |

|

6,126,242 |

| ||

|

|

|

|

|

|

| ||

|

Commitments and contingencies |

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

STOCKHOLDERS’ EQUITY |

|

|

|

|

| ||

|

Series A junior participating preferred stock, $0.01 par value; 2,500,000 shares authorized; none issued or outstanding |

|

— |

|

— |

| ||

|

Series B 9.375% redeemable preferred stock, $0.01 par value; liquidation value $16,904; 2,000,000 shares authorized, 665,592 noncumulative shares issued and outstanding as of March 31, 2011 and December 31, 2010, respectively |

|

7 |

|

7 |

| ||

|

Series C 9.125% redeemable preferred stock, $0.01 par value; liquidation value $35,389; 5,500,000 shares authorized; 1,405,086 noncumulative shares issued and outstanding as of March 31, 2011 and December 31, 2010, respectively |

|

14 |

|

14 |

| ||

|

Common stock, $0.01 par value; 200,000,000 shares authorized; 7,788,546 and 7,787,546 shares issued and outstanding as of March 31, 2011 and December 31, 2010, respectively |

|

78 |

|

78 |

| ||

|

Additional paid-in capital |

|

1,076,451 |

|

1,076,375 |

| ||

|

Net accumulated deficit: |

|

|

|

|

| ||

|

Cumulative dividends declared |

|

(822,520 |

) |

(822,520 |

) | ||

|

Retained deficit |

|

(228,545 |

) |

(227,558 |

) | ||

|

Net accumulated deficit |

|

(1,051,065 |

) |

(1,050,078 |

) | ||

|

Total Impac Mortgage Holdings, Inc. stockholders’ equity |

|

25,485 |

|

26,396 |

| ||

|

Noncontrolling interests |

|

1,271 |

|

1,301 |

| ||

|

Total equity |

|

26,756 |

|

27,697 |

| ||

|

Total liabilities and stockholders’ equity |

|

$ |

6,205,794 |

|

$ |

6,153,939 |

|

See accompanying notes to consolidated financial statements.

IMPAC MORTGAGE HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(Unaudited)

|

|

|

For the Three Months |

| ||||

|

|

|

Ended March 31, |

| ||||

|

|

|

2011 |

|

2010 |

| ||

|

|

|

|

|

|

| ||

|

INTEREST INCOME |

|

$ |

218,082 |

|

$ |

279,876 |

|

|

INTEREST EXPENSE |

|

216,547 |

|

279,106 |

| ||

|

Net interest income |

|

1,535 |

|

770 |

| ||

|

|

|

|

|

|

| ||

|

NON-INTEREST INCOME: |

|

|

|

|

| ||

|

Change in fair value of net trust assets, excluding REO |

|

4,896 |

|

7,372 |

| ||

|

Losses from REO |

|

(4,249 |

) |

(1,108 |

) | ||

|

Non-interest income - net trust assets |

|

647 |

|

6,264 |

| ||

|

|

|

|

|

|

| ||

|

Change in fair value of long-term debt |

|

238 |

|

(291 |

) | ||

|

Mortgage and real estate services fees |

|

11,690 |

|

10,950 |

| ||

|

Other |

|

295 |

|

80 |

| ||

|

Total non-interest income |

|

12,870 |

|

17,003 |

| ||

|

|

|

|

|

|

| ||

|

NON-INTEREST EXPENSE: |

|

|

|

|

| ||

|

General and administrative |

|

4,579 |

|

4,778 |

| ||

|

Personnel expense |

|

10,766 |

|

9,681 |

| ||

|

Total non-interest expense |

|

15,345 |

|

14,459 |

| ||

|

(Loss) earnings from continuing operations before income taxes |

|

(940 |

) |

3,314 |

| ||

|

Income tax expense from continuing operations |

|

12 |

|

85 |

| ||

|

(Loss) earnings from continuing operations |

|

(952 |

) |

3,229 |

| ||

|

(Loss) earnings from discontinued operations, net of tax |

|

(350 |

) |

2,386 |

| ||

|

Net (loss) earnings |

|

(1,302 |

) |

5,615 |

| ||

|

Net loss attributable to noncontrolling interests |

|

315 |

|

303 |

| ||

|

Net (loss) earnings attributable to IMH |

|

$ |

(987 |

) |

$ |

5,918 |

|

|

|

|

|

|

|

| ||

|

(Loss) earnings per common share - basic: |

|

|

|

|

| ||

|

(Loss) earnings from continuing operations attributable to IMH |

|

$ |

(0.08 |

) |

$ |

0.46 |

|

|

(Loss) earnings from discontinued operations |

|

(0.04 |

) |

0.31 |

| ||

|

Net (loss) earnings per share available to common stockholders |

|

$ |

(0.12 |

) |

$ |

0.77 |

|

|

|

|

|

|

|

| ||

|

(Loss) earnings per common share - diluted: |

|

|

|

|

| ||

|

(Loss) earnings from continuing operations attributable to IMH |

|

$ |

(0.08 |

) |

$ |

0.42 |

|

|

(Loss) earnings from discontinued operations |

|

(0.04 |

) |

0.29 |

| ||

|

Net (loss) earnings per share available to common stockholders |

|

$ |

(0.12 |

) |

$ |

0.71 |

|

See accompanying notes to consolidated financial statements

IMPAC MORTGAGE HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(Unaudited)

|

|

|

For the Three Months |

| ||||

|

|

|

Ended March 31, |

| ||||

|

|

|

2011 |

|

2010 |

| ||

|

CASH FLOWS FROM OPERATING ACTIVITIES: |

|

|

|

|

| ||

|

Net (loss) earnings |

|

$ |

(1,302 |

) |

$ |

5,615 |

|

|

|

|

|

|

|

| ||

|

Losses from real estate owned |

|

4,249 |

|

1,108 |

| ||

|

Change in fair value of mortgage servicing rights |

|

99 |

|

— |

| ||

|

Gain on sale of loans |

|

(646 |

) |

— |

| ||

|

Origination of mortgage loans held-for-sale |

|

(53,444 |

) |

— |

| ||

|

Sale and principal reduction on mortgage loans held-for-sale |

|

26,768 |

|

— |

| ||

|

Change in fair value of net trust assets, excluding REO |

|

(21,950 |

) |

(43,300 |

) | ||

|

Change in fair value of long-term debt |

|

(238 |

) |

291 |

| ||

|

Accretion of interest income and expense |

|

87,158 |

|

125,906 |

| ||

|

Change in REO impairment reserve |

|

(10,305 |

) |

(5,951 |

) | ||

|

Stock-based compensation |

|

76 |

|

350 |

| ||

|

Net change in restricted cash |

|

(1,012 |

) |

— |

| ||

|

Net cash used in operating activities of discontinued operations |

|

(1,076 |

) |

(1,204 |

) | ||

|

Net change in other assets and liabilities |

|

(1,907 |

) |

(5,107 |

) | ||

|

Net cash provided by operating activities |

|

26,470 |

|

77,708 |

| ||

|

|

|

|

|

|

| ||

|

CASH FLOWS FROM INVESTING ACTIVITIES: |

|

|

|

|

| ||

|

Net change in securitized mortgage collateral |

|

178,988 |

|

185,917 |

| ||

|

Net change in mortgages held-for-investment |

|

3 |

|

6 |

| ||

|

Maturity of short-term investments |

|

— |

|

5,000 |

| ||

|

Purchase of premises and equipment |

|

(351 |

) |

(436 |

) | ||

|

Net principal change on investment securities available-for-sale |

|

56 |

|

70 |

| ||

|

Proceeds from the sale of real estate owned |

|

49,736 |

|

63,563 |

| ||

|

Net cash provided by investing activities of discontinued operations |

|

— |

|

864 |

| ||

|

Net cash provided by investing activities |

|

228,432 |

|

254,984 |

| ||

|

|

|

|

|

|

| ||

|

CASH FLOWS FROM FINANCING ACTIVITIES: |

|

|

|

|

| ||

|

Repayment of warehouse borrowings |

|

(32,169 |

) |

— |

| ||

|

Borrowings under warehouse agreement |

|

62,378 |

|

— |

| ||

|

Repayment of securitized mortgage borrowings |

|

(287,146 |

) |

(329,986 |

) | ||

|

Principal payments on notes payable |

|

(1,826 |

) |

(4,224 |

) | ||

|

Net cash used in financing activities |

|

(258,763 |

) |

(334,210 |

) | ||

|

|

|

|

|

|

| ||

|

Net change in cash and cash equivalents |

|

(3,861 |

) |

(1,518 |

) | ||

|

Cash and cash equivalents at beginning of period |

|

11,620 |

|

25,850 |

| ||

|

Cash and cash equivalents at end of period - Continuing Operations |

|

7,750 |

|

23,023 |

| ||

|

Cash and cash equivalents at end of period - Discontinued Operations |

|

9 |

|

1,309 |

| ||

|

Total cash and cash equivalents at end of period |

|

$ |

7,759 |

|

$ |

24,332 |

|

|

|

|

|

|

|

| ||

|

NON-CASH TRANSACTIONS (Continuing and Discontinued Operations): |

|

|

|

|

| ||

|

Transfer of securitized mortgage collateral to real estate owned |

|

$ |

25,735 |

|

$ |

41,894 |

|

|

Net effect of consolidation of net trust assets from adoption of accounting principle |

|

— |

|

119,631 |

| ||

|

Net effect of consolidation of net trust liabilities from adoption of accounting principle |

|

— |

|

(119,631 |

) | ||

See accompanying notes to consolidated financial statements.

IMPAC MORTGAGE HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(dollars in thousands, except share and per share data or as otherwise indicated)

Note 1.—Summary of Business, Market Conditions, Status of Operations, Liquidity, and Financial Statement Presentation

Business Summary

Impac Mortgage Holdings, Inc. (the Company or IMH) is a Maryland corporation incorporated in August 1995 and has the following subsidiaries: Integrated Real Estate Service Corporation (IRES), IMH Assets Corp. (IMH Assets), Impac Warehouse Lending Group, Inc. (IWLG) and Impac Funding Corporation (IFC).

The Company’s continuing operations include the long-term mortgage portfolio (residual interests in securitizations determined as total trust assets minus total trust liabilities in the consolidated balance sheets) and the mortgage and real estate fee-based business activities conducted by IRES. The discontinued operations include the former non-conforming mortgage and retail operations conducted by IFC and subsidiaries, and warehouse lending operations conducted by IWLG.

The information contained throughout this document is presented on a continuing operations basis, unless otherwise stated.

Market Update, Status of Operations and Liquidity

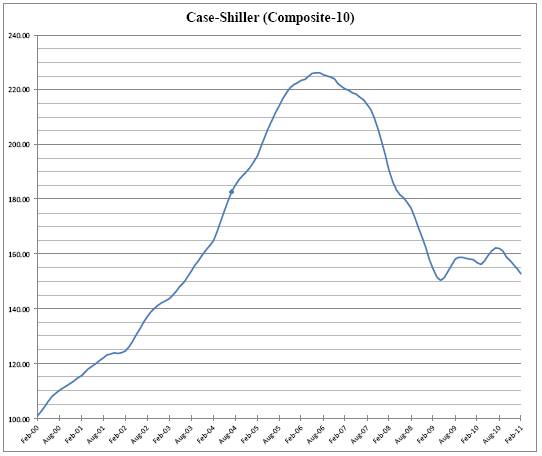

Beginning in the third quarter of 2010 and continuing through the first quarter of 2011, we continue to see home price declines in many markets as the homebuyer tax credit expired and housing prices remained under pressure due to elevated foreclosure levels. In addition, foreclosure delays as a result of reviews into foreclosure practices of some prominent loan servicers in the fourth quarter of 2010, among other market conditions may result in continued downward pressure on home prices for the foreseeable future.

Mortgage lending and credit market conditions remained soft through the first quarter of 2011 due primarily to an increase in mortgage rates and weak economy. Existing uncertainties surrounding the housing market, economy and regulatory environment will continue to present challenges for the Company. The ongoing economic stress or further deterioration of general economic conditions could prolong or increase borrower defaults leading to deteriorating performance of our long-term mortgage portfolio.

In March 2011, the Company expanded its mortgage lending operations by moving into the Pacific Northwest and Gulf Coast Regions, opening regional production offices in Lake Oswego, Oregon, and Baton Rouge, Louisiana. In addition to the Company’s mortgage lending operations in Irvine, California, this expansion gives the Company origination capabilities throughout the entire West Coast and Gulf Coast regions with additional regional operation centers and retail and wholesale locations. As part of this expansion, the Company invested approximately $2.0 million in its mortgage lending operations infrastructure, consisting principally of additional personnel and occupancy costs (included in total non-interest expense in the consolidated statement of operations). Also during the quarter ended March 31, 2011, the Company obtained an additional warehouse borrowing facility of $20.0 million bringing total warehouse borrowing capacity to $73.5 million at March 31, 2011. Through both retail and wholesale channels, the Company funded $53.4 million in mortgage loans during the quarter ended March 31, 2011 of primarily government sponsored and conventional loans eligible for sale to Ginnie Mae, Fannie Mae and Freddie Mac, respectively.

The ability to meet the Company’s long-term liquidity requirements is subject to several factors, such as generating fees from the mortgage and real estate business activities and realizing cash flows from the long-term mortgage portfolio. The Company’s future financial performance and success are dependent in large part upon the ability to grow the mortgage and real estate business activities, including providing services to third parties and expanding the mortgage lending operations. The Company believes that current cash balances, cash flows from mortgage and real estate services fees generated from the long-term mortgage portfolio, and residual interest cash flows from the long-term mortgage portfolio are adequate for the current operating needs. However, the mortgage and real estate services market is volatile, highly competitive and subject to increased regulation. The Company’s ability to successfully compete in the mortgage and real estate services industry may be challenging as its business activities have been established in the last few years and many competitors have recently entered or have established businesses delivering similar services. Additionally, the mortgage lending environment is extremely competitive and highly regulated. The future success of the mortgage lending operations will depend on a number of factors, including the ability to procure adequate financing to fund loan production, maintaining associated financial covenants of lenders, how well the Company competes, housing market conditions, economic recovery and financial regulatory reform. If the Company is unsuccessful, the Company may be unable to satisfy the future operating costs and liabilities, including repayment of the note payable and long-term debt. To be successful in expanding the business and providing adequate returns to the shareholders, the Company may seek financing in the form of debt or equity capital.

Financial Statement Presentation

The accompanying unaudited consolidated financial statements of IMH and its subsidiaries (as defined above) have been prepared in accordance with Accounting Principles Generally Accepted in the United States of America (GAAP) for interim financial information and with the instructions to Form 10-Q and Rule 8-03 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments, consisting of normal recurring adjustments considered necessary for a fair presentation, have been included. Operating results for the three months ended March 31, 2011 are not necessarily indicative of the results that may be expected for the year ending December 31, 2011. These interim period condensed consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements, which are included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010, filed with the United States Securities and Exchange Commission (SEC).

All significant inter-company balances and transactions have been eliminated in consolidation. In addition, certain amounts in the prior periods’ consolidated financial statements have been reclassified to conform to the current year presentation.

Management has made a number of estimates and assumptions relating to the reporting of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period to prepare these consolidated financial statements in conformity with GAAP. The items affected by such estimates and assumptions include the valuation of trust assets and trust liabilities, the estimated obligation of repurchase liabilities related to sold loans, the valuation of long-term debt and mortgage loans held-for-sale. Actual results could differ from those estimates and assumptions.

Recently Adopted Accounting Pronouncements

In January 2010, the FASB issued Accounting Standards Update (ASU) No. 2010-6 “Improving Disclosures About Fair Value Measurements” (ASU 2010-6). The ASU amends Codification Topic 820 “Fair Value Measurements and Disclosures” to add new disclosure requirements for transfers into and out of Levels 1 and 2 fair value measurements, as well as separate disclosures about purchases, sales, issuances, and settlements relating to Level 3 fair value measurements. ASU 2010-6 also clarifies existing fair value disclosures regarding the level of disaggregation and inputs and valuation techniques used to measure fair value. ASU 2010-6 is effective for the first reporting period (including interim periods) beginning after December 15, 2009, except for the requirement to provide the Level 3 activity of purchases, sales, issuances, and settlements on a gross basis, which will be effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years. ASU 2010-6 only adds new disclosure requirements and as a result, its adoption did not have an impact on the Company’s consolidated financial statements.

Income Taxes and Deferred Charge

The Company recorded income tax expense of $12 thousand and $85 thousand for the three months ended March 31, 2011 and 2010, respectively. The income tax expense for 2011 and 2010 is the result of state income taxes primarily from states where the Company does not have net operating loss carryforwards.

As of December 31, 2010, the Company had estimated federal and California net operating loss carryforwards of approximately $490.6 million and $492.1 million, respectively, of which $271.7 million (federal) relate to discontinued operations. During the year ended December 31, 2010, estimated net operating loss carryforwards were reduced as a result of the Company generating taxable income from cancellation of debt for approximately $426.2 million of securitized mortgage borrowings. Federal and state net operating loss (NOL) carryforwards begin to expire in 2020 and 2017, respectively. California net operating loss carryforwards have been suspended by the state until 2012, thus the expiration begins in 2017. The Company recorded a full valuation allowance against the deferred tax assets as it believes that as of March 31, 2011 it is more likely than not that the deferred tax assets will not be recoverable.

During the fourth quarter of 2009, the Company received a federal income tax refund in the amount of $8.9 million as a result of an election to carryback NOLs five years pursuant to 2009 federal legislation, The Worker, Homeownership, and Business Assistance Act of 2009. The Company files income tax returns in the U.S. federal and various state jurisdictions. The Company is subject to routine income tax audits in the various jurisdictions. A subsidiary of the Company is currently under examination by the Internal Revenue Service for tax year 2008. Management believes that there are no unresolved issues or claims likely to be material to our financial position. As of March 31, 2011, the Company has no material uncertain tax positions.

The deferred charge represents the deferral of income tax expense on inter-company profits that resulted from the sale of mortgages from taxable subsidiaries to IMH in prior years. The deferred charge is included in other assets in the accompanying consolidated balance sheets and is amortized as a component of income tax expense in the accompanying consolidated statement of operations over the estimated life of the mortgages retained in the securitized mortgage collateral. There was no amortization of deferred charge during the three months ended March 31, 2011.

Legal Proceedings

On May 6, 2011 a case entitled Massachusetts Mutual Life Insurance Company v Impac Funding Corporation, et al was filed in the United States District Court for the District of Massachusetts as Case No. 3:11-cv-30127. The complaint names Impac Funding Corporation and Impac secured Assets Corporation along with two of their officers as defendants. The action alleges violations of the Massachusetts Uniform Securities Act and the plaintiff seeks rescission or damages for their purchase of bonds from two securitization trusts issued by the Defendants. The plaintiff alleges that the loans deposited into the trusts did not meet the representations made in the offering documents when they purchased their bonds.

On or about April 20, 2011, an action was filed in the Superior Court of the Commonwealth of Massachusetts as case No. B.L.S. 11-1533 entitled Federal Home Loan bank of Boston v. Ally financial Inc., et al. Named as defendants in that action are IMH Assets Corp, Impac Funding Corporation, Impac Mortgage Holdings, Inc. and Impac Secured Assets Corp. The complaint alleges misrepresentations in connection with the materials used to market mortgage backed securities that the plaintiff purchased. The complaint seeks damages and attorney’s fees in an amount to be established at time of trial.

On or about May10, 2011 a purported class action complaint was filed in the United States District court, Central district of California as Case No. SACV11-00717 entitled Norma B. Power Trust, individually and on Behalf of All Others Similarly Situated v Impac Mortgage Holdings, Inc., et al. The action alleges that the Defendants filed unauthorized false, invalid amendments to the Company’s corporate charter with regards to the holders of series B Preferred Stock and Series C Preferred Stock. The action seeks recovery under Section 10(b) of the Exchange Act and Rule 10b-5, Section 13(a) of the Exchange Act, Rules 12b-20, 13a-1 and 13a-11. It also seeks recovery under Rule 14(e) and Section 20(a) of the Exchange Act. The Plaintiff seeks compensatory damages, costs, expenses, attorney’s fees and rescission.

We are party to other litigation and claims which are normal in the course of our operations. While the results of such other litigation and claims cannot be predicted with certainty, we believe the final outcome of such matters will not have a material adverse effect on our financial condition or results of operations.

The Company believes that it has meritorious defenses to the above claims and intends to defend these claims vigorously and as such the Company believes the final outcome of such matters will not have a material adverse effect on its financial condition or results of operations. Nevertheless, litigation is uncertain and the Company may not prevail in the lawsuits and can express no opinion as to their ultimate resolution. An adverse judgment in any of these matters could have a material adverse effect on the Company’s financial position and results of operations.

Please refer to IMH’s report on Form 10-K for the year ended December 31, 2010 for a description of litigation and claims.

Note 2.—Fair Value of Financial Instruments

The use of fair value to measure the Company’s financial instruments is fundamental to its consolidated financial statements and is a critical accounting estimate because a substantial portion of its assets and liabilities are recorded at estimated fair value.

For securitized mortgage collateral and securitized mortgage borrowings, the underlying Alt-A residential and commercial loans and mortgage-backed securities market have experienced significant declines in market activity, along with a lack of orderly transactions. The Company’s methodology to estimate fair value of these assets and liabilities include the use of internal pricing techniques such as the net present value of future expected cash flows (with observable market participant assumptions, where available) discounted at a rate of return based on the Company’s estimates of market participant requirements. The significant assumptions utilized in these internal pricing techniques, which are based on the characteristics of the underlying collateral, include estimated credit losses, estimated prepayment speeds and appropriate discount rates. The following table presents the estimated fair value of financial instruments included in the consolidated financial statements as of the dates indicated:

|

|

|

March 31, 2011 |

|

December 31, 2010 |

| ||||||||

|

|

|

Carrying |

|

Estimated |

|

Carrying |

|

Estimated |

| ||||

|

Assets |

|

|

|

|

|

|

|

|

| ||||

|

Cash and cash equivalents |

|

$ |

7,750 |

|

$ |

7,750 |

|

$ |

11,507 |

|

$ |

11,507 |

|

|

Restricted cash |

|

2,507 |

|

2,507 |

|

1,495 |

|

1,495 |

| ||||

|

Investment securities available-for-sale |

|

415 |

|

415 |

|

645 |

|

645 |

| ||||

|

Securitized mortgage collateral |

|

6,053,766 |

|

6,053,766 |

|

6,011,675 |

|

6,011,675 |

| ||||

|

Derivative assets |

|

37 |

|

37 |

|

40 |

|

40 |

| ||||

|

Mortgage servicing rights |

|

1,340 |

|

1,340 |

|

1,439 |

|

1,439 |

| ||||

|

Mortgage loans held-for-sale |

|

31,888 |

|

31,888 |

|

4,283 |

|

4,283 |

| ||||

|

Call option |

|

483 |

|

483 |

|

706 |

|

706 |

| ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Liabilities |

|

|

|

|

|

|

|

|

| ||||

|

Securitized mortgage borrowings |

|

6,056,577 |

|

6,056,577 |

|

6,012,745 |

|

6,012,745 |

| ||||

|

Derivative liabilities |

|

46,243 |

|

46,243 |

|

65,916 |

|

65,916 |

| ||||

|

Long-term debt |

|

12,030 |

|

12,030 |

|

11,728 |

|

11,728 |

| ||||

|

Warehouse borrowings |

|

34,266 |

|

34,266 |

|

4,057 |

|

4,057 |

| ||||

|

Notes payable |

|

4,763 |

|

4,716 |

|

6,874 |

|

6,818 |

| ||||

|

Put option |

|

61 |

|

61 |

|

61 |

|

61 |

| ||||

The fair value amounts above have been estimated by management using available market information and appropriate valuation methodologies. Considerable judgment is required to interpret market data to develop the estimates of fair value in both inactive and orderly markets. Accordingly, the estimates presented are not necessarily indicative of the amounts that could be realized in a current market exchange. The use of different market assumptions and/or estimation methodologies may have a material effect on the estimated fair value amounts.

The carrying amount of cash and cash equivalents and restricted cash approximates fair value.

Refer to Recurring Fair Value Measurements below for a description of the valuation methods used to determine the fair value of investment securities available for sale, securitized mortgage collateral and borrowings, derivative assets and liabilities, long-term debt, mortgage servicing rights, loans held-for-sale, and call and put options.

Warehouse borrowings fair value approximates carrying amounts due to the short-term nature of the liabilities and do not present unanticipated interest rate or credit concerns.

Note payable is recorded at amortized cost. Notes payable includes notes with maturities ranging from less than a year to three years. For notes with maturities of less than a year, the estimated fair value approximates carrying value due to the short-term nature of the liabilities. Notes with maturities greater than a year, the estimated fair value is determined using a discounted cash flow model using market rates. The estimated fair value is less than the carrying value as certain notes are non-interest bearing.

Fair Value Hierarchy

The application of fair value measurements may be on a recurring or nonrecurring basis depending on the accounting principles applicable to the specific asset or liability or whether management has elected to carry the item at its estimated fair value.

FASB ASC 820-10-35 specifies a hierarchy of valuation techniques based on whether the inputs to those techniques are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s market assumptions. These two types of inputs create the following fair value hierarchy:

· Level 1—Quoted prices (unadjusted) in active markets for identical instruments or liabilities that an entity has the ability to assess at measurement date.

· Level 2—Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; inputs other than quoted prices that are observable for an asset or liability, including interest rates and yield curves observable at commonly quoted intervals, prepayment speeds, loss severities, credit risks and default rates; and market-corroborated inputs.

· Level 3—Valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable.

This hierarchy requires the Company to use observable market data, when available, and to minimize the use of unobservable inputs when estimating fair value.

As a result of the lack of observable market data resulting from inactive markets, the Company has classified its investment securities available-for-sale, securitized mortgage collateral and borrowings, net derivative liabilities, long-term debt, mortgage servicing rights, and call and put options as Level 3 fair value measurements. Level 3 assets and liabilities were 99% and 100%, respectively, of total assets and total liabilities measured at estimated fair value at March 31, 2011 and December 31, 2010.

Recurring Fair Value Measurements

We assess our financial instruments on a quarterly basis to determine the appropriate classification within the fair value hierarchy, as defined by ASC Topic 810. Transfers between fair value classifications occur when there are changes in pricing observability levels. Transfers of financial instruments among the levels occur at the beginning of the reporting period. There were no material transfers between our Level 1 and Level 2 classified instruments during the three months ended March 31, 2011.

The following tables present the Company’s assets and liabilities that are measured at estimated fair value on a recurring basis, including financial instruments for which the Company has elected the fair value option at March 31, 2011 and December 31, 2010, based on the fair value hierarchy:

|

|

|

Recurring Fair Value Measurements |

| ||||||||||||||||

|

|

|

March 31, 2011 |

|

December 31, 2010 |

| ||||||||||||||

|

|

|

Level 1 |

|

Level 2 |

|

Level 3 |

|

Level 1 |

|

Level 2 |

|

Level 3 |

| ||||||

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Investment securities available-for-sale |

|

$ |

— |

|

$ |

— |

|

$ |

415 |

|

$ |

— |

|

$ |

— |

|

$ |

645 |

|

|

Mortgage loans held-for-sale |

|

— |

|

31,888 |

|

— |

|

— |

|

4,283 |

|

— |

| ||||||

|

Mortgage servicing rights (1) |

|

— |

|

— |

|

1,340 |

|

— |

|

— |

|

1,439 |

| ||||||

|

Call option (1) |

|

— |

|

— |

|

483 |

|

— |

|

— |

|

706 |

| ||||||

|

Securitized mortgage collateral |

|

— |

|

— |

|

6,053,766 |

|

— |

|

— |

|

6,011,675 |

| ||||||

|

Total assets at fair value |

|

$ |

— |

|

$ |

31,888 |

|

$ |

6,056,004 |

|

$ |

— |

|

$ |

4,283 |

|

$ |

6,014,465 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

Securitized mortgage borrowings |

|

$ |

— |

|

$ |

— |

|

$ |

6,056,577 |

|

$ |

— |

|

$ |

— |

|

$ |

6,012,745 |

|

|

Derivative liabilities, net (2) |

|

— |

|

— |

|

46,205 |

|

— |

|

— |

|

65,876 |

| ||||||

|

Long-term debt |

|

— |

|

— |

|

12,030 |

|

— |

|

— |

|

11,728 |

| ||||||

|

Put option (3) |

|

— |

|

— |

|

61 |

|

— |

|

— |

|

61 |

| ||||||

|

Total liabilities at fair value |

|

$ |

— |

|

$ |

— |

|

$ |

6,114,873 |

|

$ |

— |

|

$ |

— |

|

$ |

6,090,410 |

|

(1) Included in other assets in the accompanying balance sheets.

(2) At March 31, 2011, derivative liabilities, net included $37 thousand in derivative assets and $46.2 million in derivative liabilities, included within trust assets and trust liabilities, respectively. At December 31, 2010, derivative liabilities, net included $40 thousand in derivative assets and $65.9 million in derivative liabilities, included within trust assets and trust liabilities, respectively.

(3) Included in other liabilities in the accompanying balance sheets.

The following tables present a reconciliation for all assets and liabilities measured at estimated fair value on a recurring basis using significant unobservable inputs (Level 3) for the three months ended March 31, 2011 and 2010:

|

|

|

Level 3 Recurring Fair Value Measurements |

| ||||||||||||||||||||||

|

|

|

For the three months ended March 31, 2011 |

| ||||||||||||||||||||||

|

|

|

Investment |

|

Securitized |

|

Securitized |

|

Derivative |

|

Mortgage |

|

Call option |

|

Put Option |

|

Long-term |

| ||||||||

|

Fair value, December 31, 2010 |

|

$ |

645 |

|

$ |

6,011,675 |

|

$ |

(6,012,745 |

) |

$ |

(65,876 |

) |

$ |

1,439 |

|

$ |

706 |

|

$ |

(61 |

) |

$ |

(11,728 |

) |

|

Total gains (losses) included in earnings: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

Interest income (1) |

|

28 |

|

107,369 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| ||||||||

|

Interest expense (1) |

|

— |

|

— |

|

(194,015 |

) |

— |

|

— |

|

— |

|

— |

|

(540 |

) | ||||||||

|

Change in fair value |

|

(202 |

) |

139,446 |

|

(137,278 |

) |

2,930 |

|

(99 |

) |

(223 |

) |

— |

|

238 |

| ||||||||

|

Total gains (losses) included in earnings |

|

(174 |

) |

246,815 |

|

(331,293 |

) |

2,930 |

|

(99 |

) |

(223 |

) |

— |

|

(302 |

) | ||||||||

|

Transfers in and/or out of Level 3 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| ||||||||

|

Purchases, issuances and settlements |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

Purchases |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| ||||||||

|

Issuances |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| ||||||||

|

Settlements |

|

(56 |

) |

(204,724 |

) |

287,461 |

|

16,741 |

|

— |

|

— |

|

— |

|

— |

| ||||||||

|

Fair value, March 31, 2011 |

|

$ |

415 |

|

$ |

6,053,766 |

|

$ |

(6,056,577 |

) |

$ |

(46,205 |

) |

$ |

1,340 |

|

$ |

483 |

|

$ |

(61 |

) |

$ |

(12,030 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

Unrealized gains (losses) still held (2) |

|

$ |

202 |

|

$ |

(4,342,090 |

) |

$ |

6,222,257 |

|

$ |

(46,475 |

) |

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

58,733 |

|

(1) Amounts primarily represent accretion to recognize interest income and interest expense using effective yields based on estimated fair values for trust assets and trust liabilities. The total net interest income, including cash received and paid, was $1.5 million for the three months ended March 31, 2011, as reflected in the accompanying consolidated statement of operations.

(2) Represents the amount of unrealized gains (losses) relating to assets and liabilities classified as Level 3 that are still held and reflected in the fair values at March 31, 2011.

|

|

|

Level 3 Recurring Fair Value Measurements |

| |||||||||||||

|

|

|

For the three months ended March 31, 2010 |

| |||||||||||||

|

|

|

Investment |

|

Securitized |

|

Securitized |

|

Derivative |

|

Long-term |

| |||||

|

Fair value, December 31, 2009 |

|

$ |

813 |

|

$ |

5,666,122 |

|

$ |

(5,659,865 |

) |

$ |

(126,457 |

) |

$ |

(9,773 |

) |

|

Total gains (losses) included in earnings: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Interest income (1) |

|

47 |

|

130,229 |

|

— |

|

— |

|

— |

| |||||

|

Interest expense (1) |

|

— |

|

— |

|

(255,513 |

) |

— |

|

(668 |

) | |||||

|

Change in fair value |

|

178 |

|

681,408 |

|

(656,199 |

) |

(18,015 |

) |

(291 |

) | |||||

|

Total gains (losses) included in earnings |

|

225 |

|

811,637 |

|

(911,712 |

) |

(18,015 |

) |

(959 |

) | |||||

|

Adoption of ASU 2009-17 (2) |

|

(298 |

) |

116,907 |

|

(110,618 |

) |

(9,013 |

) |

— |

| |||||

|

Transfers in and/or out of Level 3 |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||

|

Purchases, issuances and settlements |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Purchases |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||

|

Issuances |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||

|

Settlements |

|

(70 |

) |

(227,811 |

) |

330,305 |

|

35,609 |

|

— |

| |||||

|

Fair value, March 31, 2010 |

|

$ |

670 |

|

$ |

6,366,855 |

|

$ |

(6,351,890 |

) |

$ |

(117,876 |

) |

$ |

(10,732 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Unrealized (losses) gains still held (3) |

|

$ |

368 |

|

$ |

(5,491,407 |

) |

$ |

7,093,620 |

|

$ |

(119,405 |

) |

$ |

60,031 |

|

(1) Amounts primarily represent accretion to recognize interest income and interest expense using effective yields based on estimated fair values for trust assets and trust liabilities. The total net interest income, including cash received and paid, was $770 thousand for the three months ended March 31, 2010, as reflected in the accompanying consolidated statement of operations.

(2) Amounts represent the consolidation and deconsolidation of trust assets and liabilities as a result of the adoption of ASU 2009-17 on January 1, 2010. See Note 1. — Summary of Market Conditions and Liquidity, Business and Financial Statement Presentation including Significant Accounting Policies in our Annual Report on Form 10K for the year ended December 31, 2010 for the impact of the adoption of ASU 2009-17 on our consolidated financial statements.

(3) Represents the amount of unrealized gains (losses) relating to assets and liabilities classified as Level 3 that are still held at March 31, 2010.

The following tables present the changes in recurring fair value measurements included in net earnings (loss) for the three months ended March 31, 2011 and 2010:

|

|

|

Recurring Fair Value Measurements |

| ||||||||||||||||

|

|

|

Changes in Fair Value Included in Net Earnings |

| ||||||||||||||||

|

|

|

For the three months ended March 31, 2011 |

| ||||||||||||||||

|

|

|

|

|

|

|

Change in Fair Value of |

|

Other non-interest |

|

|

| ||||||||

|

|

|

Interest Income (1) |

|

Interest Expense (1) |

|

Net Trust Assets |

|

Long-term Debt |

|

income |

|

Total |

| ||||||

|

Investment securities available-for-sale |

|

$ |

28 |

|

$ |

— |

|

$ |

(202 |

) |

$ |

— |

|

$ |

— |

|

$ |

(174 |

) |

|

Securitized mortgage collateral |

|

107,369 |

|

— |

|

139,446 |

|

— |

|

— |

|

246,815 |

| ||||||

|

Securitized mortgage borrowings |

|

— |

|

(194,015 |

) |

(137,278 |

) |

— |

|

— |

|

(331,293 |

) | ||||||

|

Mortgage servicing rights |

|

— |

|

— |

|

— |

|

— |

|

(99 |

) |

(99 |

) | ||||||

|

Call option |

|

— |

|

— |

|

— |

|

— |

|

(223 |

) |

(223 |

) | ||||||

|

Put option |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| ||||||

|

Derivative instruments, net |

|

— |

|

— |

|

2,930 |

(2) |

— |

|

— |

|

2,930 |

| ||||||

|

Long-term debt |

|

— |

|

(540 |

) |

— |

|

238 |

|

— |

|

(302 |

) | ||||||

|

Total |

|

$ |

107,397 |

|

$ |

(194,555 |

) |

$ |

4,896 |

(3) |

$ |

238 |

|

$ |

(322 |

) |

$ |

(82,346 |

) |

(1) Amounts primarily represent accretion to recognize interest income and interest expense using effective yields based on estimated fair values for trust assets and trust liabilities.

(2) Included in this amount is $20.0 million in changes in the fair value of derivative instruments, offset by $17.1 million in cash payments from the securitization trusts for the three months ended March 31, 2011.

(3) For the three months ended March 31, 2011, change in the fair value of trust assets, excluding REO was $4.9 million. Excluded from the $22.0 million change in fair value of net trust assets, excluding REO, in the accompanying consolidated statement of cash flows is $17.1 million in cash payments from the securitization trusts related to the Company’s net derivative liabilities.

|

|

|

Recurring Fair Value Measurements |

| |||||||||||||

|

|

|

Changes in Fair Value Included in Net Loss |

| |||||||||||||

|

|

|

For the three months ended March 31, 2010 |

| |||||||||||||

|

|

|

|

|

|

|

Change in Fair Value of |

|

|

| |||||||

|

|

|

Interest Income (1) |

|

Interest Expense (1) |

|

Net Trust Assets |

|

Long-term Debt |

|

Total |

| |||||

|

Investment securities available-for-sale |

|

$ |

47 |

|

$ |

— |

|

$ |

178 |

|

$ |

— |

|

$ |

225 |

|

|

Securitized mortgage collateral |

|

130,229 |

|

— |

|

681,408 |

|

— |

|

811,637 |

| |||||

|

Securitized mortgage borrowings |

|

— |

|

(255,513 |

) |

(656,199 |

) |

— |

|

(911,712 |

) | |||||

|

Derivative instruments, net |

|

— |

|

— |

|

(18,015 |

)(2) |

— |

|

(18,015 |

) | |||||

|

Long-term debt |

|

— |

|

(668 |

) |

— |

|

(291 |

) |

(959 |

) | |||||

|

Total |

|

$ |

130,276 |

|

$ |

(256,181 |

) |

$ |

7,372 |

(3) |

$ |

(291 |

) |

$ |

(118,824 |

) |

(1) Amounts primarily represent accretion to recognize interest income and interest expense using effective yields based on estimated fair values for trust assets and trust liabilities.

(2) Included in this amount is $17.9 million in changes in the fair value of derivative instruments, offset by $35.9 million in cash payments from the securitization trusts for the three months ended March 31, 2010.

(3) For the three months ended March 31, 2010, change in the fair value of net trust assets, excluding REO was $7.4 million. Excluded from the $43.3 million change in fair value of net trust assets, excluding REO, in the accompanying consolidated statement of cash flows is $35.9 million in cash payments from the securitization trusts related to the Company’s net derivative liabilities.

The following is a description of the measurement techniques for items recorded at estimated fair value on a recurring basis.

Investment securities available-for-sale—The Company elected to carry all of its investment securities available-for-sale at fair value. The investment securities consist primarily of non-investment grade mortgage-backed securities. The fair value of the investment securities is measured based upon the Company’s expectation of inputs that other market participants would use. Such assumptions include judgments about the underlying collateral, prepayment speeds, future credit losses, forward interest rates and certain other factors. Given the market disruption and lack of observable market data as of March 31, 2011 and December 31, 2010, the estimated fair value of the investment securities available-for-sale was measured using significant internal expectations of market participants’ assumptions.

Mortgage servicing rights—The Company elected to carry all of its mortgage servicing rights arising from its newly acquired mortgage lending operation at fair value. The fair value of mortgage servicing rights is based upon an internal discounted cash flow model. The valuation model incorporates assumptions that market participants would use in estimating the fair value of servicing. These assumptions include estimates of prepayment speeds, discount rate, cost to service, escrow account earnings, contractual servicing fee income, prepayment and late fees, among other considerations. Mortgage servicing rights are considered a Level 3 measurement at March 31, 2011.

Mortgage loans held-for-sale—The Company elected to carry its mortgage loans held-for-sale originated from its recently formed residential mortgage lending platform at fair value. Fair value is based on quoted market prices, where available, prices for other traded mortgage loans with similar characteristics, and purchase commitments and bid information received from market participants. Given the meaningful level of secondary market activity for conforming mortgage loans, active pricing is available for similar assets and accordingly, the Company classifies its mortgage loans held-for-sale as a Level 2 measurement at March 31, 2011.

Call option—As part of the acquisition of AmeriHome Mortgage Corporation (AmeriHome) as more fully discussed in Note 18.—Business Combinations of our Annual Report on Form 10-K for the year ended December 31, 2010, the purchase agreement included a call option to purchase an additional 39% of AmeriHome. The estimated fair value is based on a multinomial model incorporating various assumptions including expected future book value of AmeriHome, the probability of the option being exercised, volatility, expected term and certain other factors. The call option is considered a Level 3 measurement at March 31, 2011.

Put option—As part of the acquisition of AmeriHome, a put option which allows the noncontrolling interest holder to sell his remaining 49% of AmeriHome to the Company in the event the Company does not exercise the call option discussed above. The estimated fair value is based on a multinomial model incorporating various assumptions including expected future book value of AmeriHome, the probability of the option being exercised, volatility, expected term and certain other factors. The put option is considered a Level 3 measurement at March 31, 2011.

Securitized mortgage collateral—The Company elected to carry all of its securitized mortgage collateral at fair value. These assets consist primarily of non-conforming mortgage loans securitized between 2002 and 2007. Fair value measurements are based on the Company’s internal models used to compute the net present value of future expected cash flows with observable market participant assumptions where available. The Company’s assumptions include its expectations of inputs that other market participants would use in pricing these assets. These assumptions include judgments about the underlying collateral, prepayment speeds, estimated future credit losses, forward interest rates, investor yield requirements and certain other factors. As of March 31, 2011, securitized mortgage collateral had an unpaid principal balance of $10.4 billion, compared to an estimated fair value of $6.1 billion. The aggregate unpaid principal balance exceeds the fair value by $4.3 billion at March 31, 2011. As of March 31, 2011, the unpaid principal balance of loans 90 days or more past due was $1.8 billion compared to an estimated fair value of $0.5 billion. The aggregate unpaid principal balances of loans 90 days or more past due exceed the fair value by $1.3 billion at March 31, 2011.

Securitized mortgage borrowings—The Company elected to carry all of its securitized mortgage borrowings at fair value. These borrowings consist of individual tranches of bonds issued by securitization trusts and are primarily backed by non-conforming mortgage loans. Fair value measurements include the Company’s judgments about the underlying collateral and assumptions such as prepayment speeds, estimated future credit losses, forward interest rates, investor yield requirements and certain other factors. As of March 31, 2011, securitized mortgage borrowings had an outstanding principal balance of $10.6 billion compared to an estimated fair value of $6.1 billion. The aggregate outstanding principal balance exceeds the fair value by $4.5 billion at March 31, 2011.

Long-term debt—The Company elected to carry all of its long-term debt (consisting of trust preferred securities and junior subordinated notes) at fair value. These securities are measured based upon an analysis prepared by management, which considered the Company’s own credit risk, including settlements with trust preferred debt holders and discounted cash flow analysis. As of March 31, 2011, long-term debt had an unpaid principal balance of $70.5 million compared to an estimated fair value of $12.0 million. The aggregate unpaid principal balance exceeds the fair value by $58.5 million at March 31, 2011.

Derivative assets and liabilities—For non-exchange traded contracts, fair value is based on the amounts that would be required to settle the positions with the related counterparties as of the valuation date. Valuations of derivative assets and liabilities are based on observable market inputs, if available. To the extent observable market inputs are not available, fair values measurements include the Company’s judgments about future cash flows, forward interest rates and certain other factors, including counterparty risk. Additionally, these values also take into account the Company’s own credit standing, to the extent applicable; thus, the valuation of the derivative instrument includes the estimated value of the net credit differential between the counterparties to the derivative contract.

Nonrecurring Fair Value Measurements

The Company is required to measure certain assets and liabilities at estimated fair value from time to time. These fair value measurements typically result from the application of specific accounting pronouncements under GAAP. The fair value measurements are considered nonrecurring fair value measurements under FASB ASC 820-10.

The following tables present financial and non-financial assets and liabilities measured using nonrecurring fair value measurements at March 31, 2011 and 2010, respectively:

|

|

|

Nonrecurring Fair Value Measurements |

|

Total Gains (Losses) |

| ||||||||

|

|

|

March 31, 2011 |

|

For the Three Months Ended |

| ||||||||

|

|

|

Level 1 |

|

Level 2 |

|

Level 3 |

|

March 31, 2011 (5) |

| ||||

|

REO (1) |

|

$ |

— |

|

$ |

62,656 |

|

$ |

— |

|

$ |

(4,247 |

) |

|

Lease liability (2) |

|

— |

|

— |

|

(2,246 |

) |

(217 |

) | ||||

|

Deferred charge (3) |

|

— |

|

— |

|

13,144 |

|

— |

| ||||

|

Intangible assets (4) |

|

— |

|

— |

|

1,479 |

|

— |

| ||||

(1) Amounts are included in continuing operations. For the three months ended March 31, 2011, the $4.3 million loss related to additional impairment write-downs during the period is within continuing operations.

(2) Amounts are included in discontinued operations. For the three months ended March 31, 2011, the Company recorded $217 thousand in losses resulting from changes in lease liabilities as a result of changes in our expected minimum future lease payments.

(3) Amounts are included in continuing operations. For the three months ended March 31, 2011, the Company recorded zero in income tax expense resulting from impairment write-downs based on changes in estimated cash flows and lives of the related mortgages retained in the securitized mortgage collateral.

(4) Amount is included in other assets in the accompanying consolidated balance sheets.

(5) Total gains (losses) reflect gains and losses from all nonrecurring measurements during the period.

|

|

|

Non-recurring Fair Value Measurements |

|

Total Gains |

| ||||||||

|

|

|

March 31, 2010 |

|

For the Three Months Ended |

| ||||||||

|

|

|

Level 1 |

|

Level 2 |

|

Level 3 |

|

March 31, 2010 (6) |

| ||||

|

Mortgage loans held-for-sale (1) |

|

$ |

— |

|

$ |

— |

|

$ |

3,049 |

|

$ |

254 |

|

|

REO (2) |

|

— |

|

95,794 |

|

— |

|

1,028 |

| ||||

|

Lease liability (3) |

|

— |

|

— |

|

(3,178 |

) |

479 |

| ||||

|

Deferred charge (4) |

|

— |

|

— |

|

13,144 |

|

— |

| ||||

|

Intangible asset (5) |

|

— |

|

— |

|

1,000 |

|

— |

| ||||

(1) Relates to Alt-A loans held-for-sale included in assets of discontinued operations.

(2) Includes $95.6 million and $175 thousand in REO within continuing and discontinued operations, respectively, at March 31, 2010 which had additional impairment write-downs subsequent to the date of foreclosure. For the three months ended March 31, 2010, the $1.0 million gain during the period included $672 thousand and $355 thousand within continuing and discontinued operations, respectively.

(3) Amounts are included in discontinued operations. For the three months ended March 31, 2010, the Company recorded $485 thousand in gains resulting from changes in lease liabilities as a result of changes in our expected minimum future lease payments, respectively.

(4) Amounts are included in continuing operations. For the three months ended March 31, 2010, the Company recorded zero in income tax expense resulting from impairment write-downs based on changes in estimated cash flows and lives of the related mortgages retained in the securitized mortgage collateral.

(5) Amount is included in other assets in the accompanying consolidated balance sheets.

(6) Total gains (losses) reflect gains and losses from all nonrecurring measurements during the period.

Mortgage loans held-for-sale—Mortgage loans held-for-sale (included in assets of discontinued operations) for which the fair value option was not elected are carried at the lower of cost or market (LOCOM). When available, such measurements are based upon what secondary markets offer for portfolios with similar characteristics, and are considered Level 2 measurements. If market pricing is not available, such measurements are significantly impacted by the Company’s expectations of other market participants’ assumptions, and are considered Level 3 measurements. The Company utilizes internal pricing processes to estimate the fair value of these loans, which is based on recent loan sales and estimates of the fair value of the underlying collateral. Loans held-for-sale from the discontinued non-conforming lending division is considered Level 3 fair value measurements at March 31, 2010.

Real estate owned—REO consists of residential real estate acquired in satisfaction of loans. Upon foreclosure, REO is adjusted to the estimated fair value of the residential real estate less estimated selling and holding costs, offset by expected contractual mortgage insurance proceeds to be received, if any. Subsequently, REO is recorded at the lower of carrying value or estimated fair value less costs to sell. Fair values of REO are generally based on observable market inputs, and considered Level 2 measurements at March 31, 2011.

Lease liability—In connection with the discontinuation of our non-conforming mortgage, retail mortgage, warehouse lending and commercial operations, a significant amount of office space that was previously occupied is no longer being used by the Company. The Company has subleased a significant amount of this office space. The Company has recorded a liability, included within discontinued operations, representing the present value of the minimum lease payments over the remaining life of the lease, offset by the expected proceeds from sublet revenue related to this office space. This liability is based on present value techniques that incorporate the Company’s judgments about estimated sublet revenue and discount rates. Therefore, this liability is considered a Level 3 measurement at March 31, 2011.

Deferred charge—Deferred charge represents the deferral of income tax expense on inter-company profits that resulted from the sale of mortgages from taxable subsidiaries to IMH in prior years. The deferred charge is amortized as a component of income tax expense over the estimated life of the mortgages retained in the securitized mortgage collateral. The Company evaluates the deferred charge for impairment quarterly using internal estimates of estimated cash flows and lives of the related mortgages retained in the securitized mortgage collateral. If the deferred charge is determined to be impaired, it is amortized as a component of income tax expense. Deferred charge is considered a Level 3 measurement at March 31, 2011.

Intangible assets—Intangible assets deemed to have an indefinite life are tested annually for impairment, or more frequently if events or changes in circumstances indicate that the asset might be impaired. Impairment losses are recognized if carrying amount of an intangible asset exceeds its estimated fair value. Intangible asset, which is included in other assets of continuing operations, is considered a Level 3 measurement at March 31, 2011.

Note 3.—Stock Options

There were no options granted during the three months ended March 31, 2011 or 2010, respectively.

The following table summarizes activity, pricing and other information for the Company’s stock options for the three months ended March 31, 2011:

|

|

|

|

|

Weighted- |

| |

|

|

|

|

|

Average |

| |

|

|

|

Number of |

|

Exercise |

| |

|

|

|

Shares |

|

Price ($) |

| |

|

Options outstanding at January 1, 2011 |

|

1,476,704 |

|

$ |

6.28 |

|

|

Options granted |

|

— |

|

— |

| |

|

Options exercised |

|

(1,000 |

) |

0.53 |

| |

|

Options forfeited / cancelled |

|

(58,632 |

) |

37.71 |

| |

|

Options outstanding at March 31, 2011 |

|

1,417,072 |

|

$ |

4.98 |

|

|

Options exercisable at March 31, 2011 |

|

1,025,534 |

|

$ |

5.83 |

|

As of March 31, 2011, there was approximately $820 thousand of total unrecognized compensation cost related to stock option compensation arrangements granted under the plan, net of estimated forfeitures. That cost is expected to be recognized over the remaining weighted average period of 2.64 years.

The following table summarizes activity, pricing and other information for the Company’s restricted stock units (RSU’s) for the three months ended March 31, 2011:

|

|

|

|

|

Weighted- |

| |

|

|

|

|

|

Average |

| |

|

|

|

Number of |

|

Grant Date |

| |

|

|

|

Shares |

|

Fair Value |

| |

|

RSU’s outstanding at January 1, 2011 |

|

24,000 |

|

$ |

2.73 |

|

|

RSU’s granted |

|

— |

|

— |

| |

|

RSU’s exercised |

|

— |

|

— |

| |

|

RSU’s forfeited / cancelled |

|

— |

|

— |

| |

|

RSU’s outstanding at March 31, 2011 |

|

24,000 |

|

$ |

2.73 |

|

As of March 31, 2011, there was approximately $58 thousand of total unrecognized compensation cost related to the RSU compensation arrangements granted under the plan. That cost is expected to be recognized over a weighted average period of 2.68 years.

Note 4.—Reconciliation of Earnings Per Share

The following table presents the computation of basic and diluted earnings (loss) per common share, including the dilutive effect of stock options and cumulative redeemable preferred stock outstanding for the periods indicated:

|

|

|

For the Three Months |

| ||||

|

|

|

Ended March 31, |

| ||||

|

|

|

2011 |

|

2010 |

| ||

|

Numerator for basic earnings (loss) per share: |

|

|

|

|

| ||

|

(Loss) earnings from continuing operations |

|

$ |

(952 |

) |

$ |

3,229 |

|

|

Net loss attributable to noncontrolling interest |

|

315 |

|

303 |

| ||

|

(Loss) earnings from continuing operations attributable to IMH |

|

(637 |

) |

3,532 |

| ||

|

(Loss) earnings from discontinued operations |

|

(350 |

) |

2,386 |

| ||

|

(Loss) earnings per share available to common stockholders |

|

$ |

(987 |

) |

$ |

5,918 |

|

|

|

|

|

|

|

| ||

|

Denominator for basic earnings (loss) per share (1): |

|

|

|

|

| ||

|

Basic weighted average common shares outstanding during the year |

|

7,788 |

|

7,698 |

| ||

|

|

|

|

|

|

| ||

|

Denominator for diluted earnings per share (1): |

|

|

|

|

| ||

|

Basic weighted average common shares outstanding during the year |

|

7,788 |

|

7,698 |

| ||

|

Net effect of dilutive stock options |

|

— |

|

620 |