Attached files

| file | filename |

|---|---|

| EX-10.1 - EXHIBIT 10.1 - PROSPER MARKETPLACE, INC | exhibit10d13d31d2011.htm |

| EX-10.2 - EXHIBIT 10.2 - PROSPER MARKETPLACE, INC | exhibit10d23d31d2011.htm |

| EX-32.1 - EXHIBIT 32.1 - PROSPER MARKETPLACE, INC | exhibit32d13d31d2011.htm |

| EX-31.1 - EXHIBIT 31.1 - PROSPER MARKETPLACE, INC | exhibit31d13d31d2011.htm |

| EX-31.2 - EXHIBIT 31.2 - PROSPER MARKETPLACE, INC | exhibit31d23d31d2011.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q/A

Amendment No. 1

(Mark One)

|

þ

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended March 31, 2011

or

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission File Number: 333-147019

PROSPER MARKETPLACE, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

6199

|

73-1733867

|

||

|

(State or other jurisdiction of

|

(Primary Standard Industrial

|

(I.R.S. Employer

|

||

|

incorporation or organization)

|

Classification Code Number

|

Identification Number)

|

111 Sutter Street, 22nd Floor

San Francisco, CA 94104

(415) 593-5400

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o(Do not check if a smaller reporting company)

|

Smaller reporting company þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

As of April 28, 2011, there were 4,588,832 shares of the registrant’s common stock outstanding.

TABLE OF CONTENTS

|

Page No.

|

|

|

i

|

|

|

1

|

|

|

2

|

|

|

3

|

|

|

4

|

|

|

5

|

|

|

23

|

|

|

42

|

|

|

42

|

|

|

43

|

|

|

43

|

|

|

50

|

|

|

50

|

|

| Item 4. Removed and Reserved | 50 |

|

50

|

|

|

50

|

|

|

52

|

|

|

53

|

|

EXPLANATORY PARAGRAPH

On May 11, 2011, Prosper Marketplace, Inc. (“we”, “us”, “our” or the “Company”) inadvertently filed a draft version of our Quarterly Report on Form 10-Q for the quarter ended March 31, 2011 (the “Draft 10-Q”). We are filing this amended quarterly report on Form 10-Q (the "Form 10-Q/A") to replace the Draft 10-Q. Investors should not rely on any information included in the Draft 10-Q, which is superseded in its entirety by this Form 10-Q/A.

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes forward-looking statements within the meaning of Section 27A of the Securities Exchange Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can generally be identified by the use of words such as “may,” “believe,” “will,” “expect,” “project,” “estimate,” “intend,” “anticipate,” “plan,” “continue” or similar expressions. In particular, information appearing under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” includes forward-looking statements. Forward-looking statements inherently involve many risks and uncertainties that could cause actual results to differ materially from those projected in these statements.

Where, in any forward-looking statement, we express an expectation or belief as to future results or events, such expectation or belief is based on the current plans and expectations of our management and expressed in good faith and believed to have a reasonable basis, but there can be no assurance that the expectation or belief will result or be achieved or accomplished. More information on factors that could cause actual results or events to differ materially from those anticipated is included from time to time in our reports filed with the Securities and Exchange Commission (the “SEC”), including our Annual Report on Form 10-K for the year ended December 31, 2010, particularly under the caption “Risk Factors.”

All forward-looking statements speak only as of the date of this Quarterly Report on Form 10-Q and are expressly qualified in their entirety by the cautionary statements included in this Quarterly Report on Form 10-Q or our Annual Report on Form 10-K for the year ended December 31, 2010, particularly under the caption “Risk Factors.” We undertake no obligation to update or revise forward-looking statements that may be made to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events, other than as required by law.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and current reports and other information with the SEC. You can inspect, read and copy these reports and other information at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You can obtain information regarding the operation of the SEC’s Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at www.sec.gov that makes available reports, proxy statements and other information regarding issuers that file electronically.

PART I. Financial Information

Item 1. Financial Statements

|

Prosper Marketplace, Inc.

|

||||||||

|

Balance Sheets

|

||||||||

|

March 31,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

(Unaudited)

|

(Note 2)

|

|||||||

|

ASSETS

|

||||||||

|

Cash and cash equivalents

|

$ | 3,226,438 | $ | 4,284,228 | ||||

|

Restricted cash

|

2,977,743 | 2,566,631 | ||||||

|

Servicing rights

|

967 | 2,986 | ||||||

|

Receivables

|

22,205 | 6,306 | ||||||

|

Borrower Loans Receivable at fair value

|

30,359,534 | 23,689,950 | ||||||

|

Property and equipment, net

|

739,291 | 765,210 | ||||||

|

Prepaid and other assets

|

129,964 | 174,805 | ||||||

|

Intangible assets, net

|

20,123 | 50,306 | ||||||

|

Total assets

|

$ | 37,476,265 | $ | 31,540,422 | ||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

Accounts payable

|

$ | 669,138 | $ | 554,347 | ||||

|

Accrued liabilities

|

1,518,447 | 1,219,239 | ||||||

|

Borrower Payment Dependent Notes at fair value

|

30,026,687 | 23,478,046 | ||||||

|

Repurchase obligation

|

13,001 | 71,001 | ||||||

|

Notes payable

|

294,297 | 288,594 | ||||||

|

Total liabilities

|

32,521,570 | 25,611,227 | ||||||

|

Commitments and contingencies (see Note 12)

|

||||||||

|

Stockholders' Equity

|

||||||||

|

Convertible preferred stock – Series A ($0.001 par value; 4,023,999 shares authorized, issued and outstanding as of March 31, 2011 and December 31, 2010)

|

4,024 | 4,024 | ||||||

|

Convertible preferred stock – Series B ($0.001 par value; 3,310,382 shares authorized, issued and outstanding as of March 31, 2011 and December 31, 2010)

|

3,310 | 3,310 | ||||||

|

Convertible preferred stock – Series C ($0.001 par value; 2,063,558 shares authorized, issued and outstanding as of March 31, 2011 and December 31, 2010)

|

2,064 | 2,064 | ||||||

|

Convertible preferred stock – Series D ($0.001 par value; 20,543,819 shares authorized; 20,340,705 issued and outstanding as of March 31, 2011 and December 31, 2010)

|

20,341 | 20,341 | ||||||

|

Convertible preferred stock – Series D-1 ($0.001 par value; 3,110,188 shares authorized, issued and outstanding as of March 31, 2011 and December 31, 2010)

|

3,110 | 3,110 | ||||||

|

Common stock ($0.001 par value; 43,860,321 shares authorized; 4,498,667 shares and 4,478,667 shares issued and outstanding as of March 31, 2011 and December 31, 2010, respectively)

|

4,485 | 4,480 | ||||||

|

Additional paid-in capital

|

56,745,700 | 56,659,849 | ||||||

|

Accumulated deficit

|

(51,828,339 | ) | (50,767,983 | ) | ||||

|

Total stockholders' equity

|

4,954,695 | 5,929,195 | ||||||

|

Total liabilities and stockholders' equity

|

$ | 37,476,265 | $ | 31,540,422 | ||||

|

The accompanying notes are an integral part of these financial statements.

|

||||||||

|

Prosper Marketplace, Inc.

|

||||||||

|

Statements of Operations

|

||||||||

|

(Unaudited)

|

||||||||

|

Three Months Ended March 31,

|

||||||||

|

2011

|

2010

|

|||||||

|

Revenues

|

||||||||

|

Origination fees

|

$ | 393,302 | $ | 148,605 | ||||

|

Loan servicing fees

|

12,019 | 65,085 | ||||||

|

Interest income on Borrower Loans and Payment Dependent Notes, net

|

80,274 | 25,874 | ||||||

|

Rebates and promotions

|

(166,404 | ) | (1,668 | ) | ||||

| 319,191 | 237,896 | |||||||

|

Cost of revenues

|

||||||||

|

Cost of services

|

(302,823 | ) | (182,391 | ) | ||||

|

Reversal of (Provision for) loan and Note repurchases

|

60,669 | (8,033 | ) | |||||

|

Net revenues

|

77,037 | 47,472 | ||||||

|

Operating expenses

|

||||||||

|

Compensation and benefits

|

1,558,209 | 1,174,825 | ||||||

|

Marketing and advertising

|

517,995 | 287,048 | ||||||

|

Depreciation and amortization

|

123,264 | 129,731 | ||||||

|

General and administrative

|

||||||||

|

Professional services

|

596,960 | 724,209 | ||||||

|

Facilities and maintenance

|

150,198 | 163,856 | ||||||

|

Other

|

227,694 | 315,327 | ||||||

|

Total expenses

|

3,174,320 | 2,794,996 | ||||||

|

Loss before other income

|

(3,097,283 | ) | (2,747,524 | ) | ||||

|

Other income

|

||||||||

|

Interest income

|

1,034 | 469 | ||||||

|

Change in fair value on Borrower Loans and Payment Dependent Notes, net

|

284,692 | 90,709 | ||||||

|

Insurance recoveries

|

1,728,273 | - | ||||||

|

Other income

|

22,929 | 13,626 | ||||||

|

Total other income, net

|

2,036,928 | 104,804 | ||||||

|

Loss before income taxes

|

(1,060,355 | ) | (2,642,720 | ) | ||||

|

Provision for income taxes

|

- | - | ||||||

|

Net loss

|

$ | (1,060,355 | ) | $ | (2,642,720 | ) | ||

|

Net loss per share – basic and diluted

|

$ | (0.24 | ) | $ | (0.59 | ) | ||

|

Weighted average shares - basic and diluted net loss per share

|

4,497,556 | 4,460,667 | ||||||

|

The accompanying notes are an integral part of these financial statements.

|

||||||||

|

Prosper Marketplace, Inc.

|

||||||||||||||||||||||||||||

|

Statements of Stockholders' Equity (Deficit)

|

||||||||||||||||||||||||||||

|

Preferred Stock

|

Common Stock

|

Additional Paid-In

|

Accumulated

|

|||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Total

|

||||||||||||||||||||||

|

Balance as of January 1, 2010 (Audited)

|

9,397,939 | $ | 9,398 | 4,460,667 | $ | 4,462 | $ | 41,406,457 | $ | (40,625,261 | ) | $ | 795,056 | |||||||||||||||

|

Exercise of stock options

|

- | |||||||||||||||||||||||||||

|

Issuance of common stock warrants

|

96,625 | 96,625 | ||||||||||||||||||||||||||

|

Compensation expense

|

59,222 | 59,222 | ||||||||||||||||||||||||||

|

Net loss

|

(2,642,720 | ) | (2,642,720 | ) | ||||||||||||||||||||||||

|

Balance as of March 31, 2010 (Unaudited)

|

9,397,939 | $ | 9,398 | 4,460,667 | $ | 4,462 | $ | 41,562,304 | $ | (43,267,981 | ) | $ | (1,691,817 | ) | ||||||||||||||

|

Balance as of January 1, 2011 (Audited)

|

32,848,832 | $ | 32,849 | 4,478,667 | $ | 4,480 | $ | 56,659,849 | $ | (50,767,983 | ) | $ | 5,929,195 | |||||||||||||||

|

Exercise of stock options

|

20,000 | 5 | 4,995 | 5,000 | ||||||||||||||||||||||||

|

Issuance of common stock warrants

|

8,958 | 8,958 | ||||||||||||||||||||||||||

|

Compensation expense

|

71,898 | 71,898 | ||||||||||||||||||||||||||

|

Net loss

|

(1,060,355 | ) | (1,060,355 | ) | ||||||||||||||||||||||||

|

Balance as of March 31, 2011 (Unaudited)

|

32,848,832 | $ | 32,849 | 4,498,667 | $ | 4,485 | $ | 56,745,700 | $ | (51,828,338 | ) | $ | 4,954,696 | |||||||||||||||

|

The accompanying notes are an integral part of these financial statements.

|

||||||||||||||||||||||||||||

|

Prosper Marketplace, Inc.

|

|||||||

|

Statements of Cash Flows

|

|||||||

|

(Unaudited)

|

|||||||

|

Three Months Ended March 31,

|

|||||||

|

2011

|

2010

|

||||||

|

Cash flows from operating activities:

|

|||||||

|

Net loss

|

$ | (1,060,355 | ) | $ | (2,642,720 | ) | |

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

|||||||

|

Depreciation and amortization

|

123,264 | 129,731 | |||||

|

Change in fair value of Borrower Loans

|

295,451 | 634,691 | |||||

|

Change in fair value of Borrower Payment Dependent Notes

|

(580,143 | ) | (725,400 | ) | |||

|

Stock-based compensation expense

|

71,898 | 59,222 | |||||

|

Promotional and marketing expenses paid with warrants

|

8,958 | – | |||||

|

Provision for (Reversal of) loan and Note repurchases

|

(60,669 | ) | 8,033 | ||||

|

Change in fair value of servicing rights

|

2,019 | 7,114 | |||||

|

Amortization of discount on long-term debt

|

5,703 | 74,649 | |||||

|

Changes in operating assets and liabilities:

|

|||||||

|

Restricted cash

|

(411,112 | ) | 114,675 | ||||

|

Receivables

|

(15,899 | ) | 5,946 | ||||

|

Prepaid and other assets

|

44,841 | 42,330 | |||||

|

Accounts payable and accrued liabilities

|

413,999 | 241,187 | |||||

|

Loan and Note repurchases

|

2,669 | 1,967 | |||||

|

Net cash used in operating activities

|

(1,159,376 | ) | (2,048,575 | ) | |||

|

Cash flows from investing activities:

|

|||||||

|

Origination of Borrower Loans held at fair value

|

(11,471,874 | ) | (5,933,690 | ) | |||

|

Repayment of Borrower Loans held at fair value

|

4,506,839 | 1,337,679 | |||||

|

Purchases of property and equipment

|

(67,163 | ) | (144,162 | ) | |||

|

Net cash used in investing activities

|

(7,032,198 | ) | (4,740,173 | ) | |||

|

Cash flows from financing activities:

|

|||||||

|

Proceeds from issuance of Notes held at fair value

|

11,471,874 | 5,933,690 | |||||

|

Payment of Notes held at fair value

|

(4,343,090 | ) | (1,311,571 | ) | |||

|

Proceeds from the issuance of notes payable

|

– | 2,300,000 | |||||

|

Proceeds from issuance of common stock

|

5,000 | – | |||||

|

Net cash provided by financing activities

|

7,133,784 | 6,922,119 | |||||

|

Net increase (decrease) in cash and cash equivalents

|

(1,057,790 | ) | 133,371 | ||||

|

Cash and cash equivalents at beginning of the period

|

4,284,228 | 616,089 | |||||

|

Cash and cash equivalents at end of the period

|

$ | 3,226,438 | $ | 749,460 | |||

|

The accompanying notes are an integral part of these financial statements.

|

|||||||

PROSPER MARKETPLACE, INC.

Notes to Consolidated Financial Statements

(Unaudited)

1. Operations and Business

Prosper Marketplace, Inc. (“Prosper,” the “Company,” “we,” “us,” “our”) was incorporated in the state of Delaware on March 22, 2005. Prosper is an online marketplace for peer-to-peer lending. Prosper’s website provides an online marketplace for loans where people list and bid on loans with interest rates of return determined by Prosper. Lender members access our platform and “bid” the amount they are willing to commit to the purchase of a Note that is dependent for payment on the corresponding borrower loan, at interest rates set by Prosper. Loan terms are subject to minimum and maximum loan amounts determined by the borrower’s credit bureau score and Prosper score, at interest rates set by Prosper. Prosper facilitates the lending and borrowing activities and acts as an agent to the lender by maintaining its online marketplace. Prosper also handles all ongoing loan administration tasks, including loan servicing and collections on behalf of the lenders. Prosper generates revenue by collecting one-time fees from borrowers on funded loans and from loan servicing fees paid by lender members.

All loans requested and obtained by Prosper borrower members through our platform are unsecured obligations of individual borrower members with a fixed interest rate and a loan term set at one, three or five years as of March 31, 2011. All borrowers are funded by WebBank, an FDIC-insured, Utah-chartered industrial bank. After funding a loan, WebBank assigns the loan to Prosper, without recourse to WebBank, in exchange for the principal amount of the borrower loan. WebBank does not have any obligation to purchasers of the Notes.

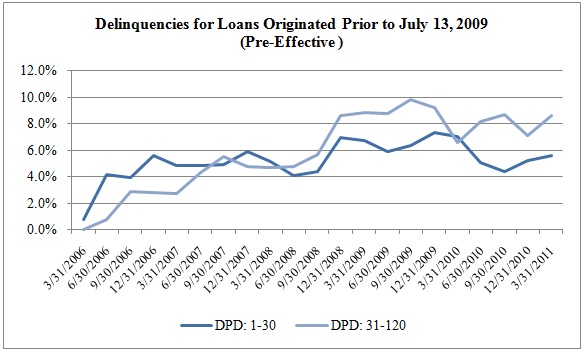

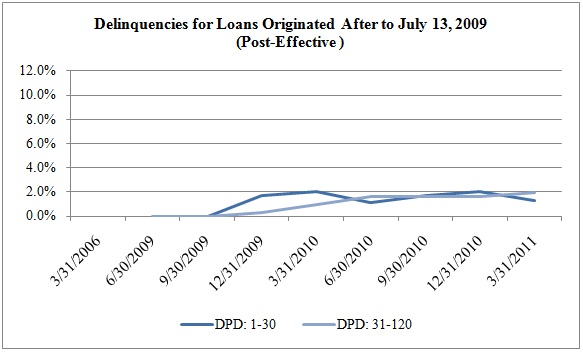

On July 13, 2009, we implemented a new operating structure and began issuing Borrower Payment Dependent Notes (“Notes”). The post registration operating structure resulted in Prosper purchasing loans from WebBank, and holding the loans until maturity. Prosper issues new securities, the Notes, to the winning lenders. Prosper’s obligation to repay the Notes is conditioned upon the repayment of the associated borrower loan owned by Prosper. As a result of these changes, borrower loans and the Notes originated on or after July 13, 2009 are carried on Prosper’s balance sheet as assets and liabilities, respectively. Prosper has elected to carry the borrower loans and the Notes on its balance sheet at fair value.

As reflected in the accompanying financial statements, Prosper has incurred net losses and negative cash flows from operations since inception, and has an accumulated deficit of approximately $51.8 million as of March 31, 2011. For the three months ended March 31, 2011, the Company incurred a net loss of $1.1 million and the Company had negative cash flows from operations of $1.2 million. The Company does not believe that its cash resources are sufficient to sustain its operations through 2011 without obtaining additional financing. Since its inception, Prosper has financed its operations primarily through equity financing from various sources. The Company is dependent upon raising additional capital or debt financing to fund its current operating plan. Failure to obtain sufficient debt and equity financings and, ultimately, to achieve profitable operations and positive cash flows from operations could adversely affect Prosper’s ability to achieve its business objectives and continue as a going concern. Although, the Company does not currently have any agreements in place with respect to any such additional financing or strategic opportunity, management believes it will secure additional financing in the near future sufficient to meet its ongoing operations and strategic plan through 2011.

2. Summary of Significant Accounting Policies

Basis of Presentation

The Company’s unaudited interim financial statements have been prepared in accordance with U.S. generally accepted accounting principles (US GAAP) and disclosure requirements for interim financial information and the requirements of Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by US GAAP for complete financial statements. The unaudited interim financial statements should be read in conjunction with the audited financial statements and notes included in our Annual Report on Form 10-K for the year ended December 31, 2010. The balance sheet at December 31, 2010 has been derived from the audited financial statements at that date. Management believes these unaudited interim financial statements reflect all adjustments, including those of a normal recurring nature, which are necessary for a fair presentation of the results for the interim periods presented. The results of operations for the interim periods are not necessarily indicative of the results that may be expected for the full year or any other interim period.

Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make certain estimates, judgments and assumptions that affect the reported amounts of assets and liabilities and the related disclosures at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. These estimates, judgments and assumptions include but are not limited to the following: valuation of borrower loans receivable and associated member payment dependent notes, valuation of servicing rights, valuation allowance on deferred tax assets, valuation and amortization periods of intangible assets, repurchase obligation, stock-based compensation expense, and contingent liabilities. Prosper bases its estimates on historical experience and on various other assumptions that Prosper believes to be reasonable under the circumstances. Actual results could differ from those estimates.

Certain Risks and Concentrations

In the normal course of its business, Prosper encounters two significant types of risk: credit and regulatory. Financial instruments that potentially subject Prosper to significant concentrations of credit risk consist primarily of cash, cash equivalents and restricted cash. The Company places cash, cash equivalents and restricted cash with high-quality financial institutions. Prosper is exposed to credit risk in the event of default by these institutions to the extent the amount recorded on the balance sheet exceeds FDIC insured amounts. Prosper performs periodic evaluations of the relative credit standing of these financial institutions and has not sustained any credit losses from instruments held at these financial institutions.

As previously described, beginning on July 13, 2009, loans originated by Prosper are carried on our balance sheet. The loans are funded by the Notes and repayment of the Notes is wholly dependent on the repayment of the loan associated with a Note. As a result, Prosper does not bear the risk associated with the repayment of principal on loans carried on its balance sheet. A decrease in the value of the loans carried on Prosper’s balance sheet associated with increased credit risk is directly offset by a reduction in the value of the Notes Prosper issued in association with the loan. However, Prosper charges a servicing fee that is deducted from loan payments. To the extent that loan payments are not made, Prosper’s servicing income will be reduced.

Prosper is subject to various regulatory requirements. The failure to appropriately identify and address these regulatory requirements could result in certain discretionary actions by regulators that could have a material effect on Prosper’s financial position and results of operations (See Note 12 — Commitments and Contingencies — Securities Law Compliance).

Cash and Cash Equivalents

Prosper invests its excess cash primarily in money market funds and in highly liquid debt instruments of U.S. municipalities, and the U.S. government and its agencies. All highly liquid investments with stated maturities of three months or less from date of purchase are classified as cash equivalents. Cash equivalents are recorded at cost, which approximates fair value. Such deposits periodically exceed amounts insured by the FDIC.

Restricted Cash

Restricted cash consists primarily of an irrevocable letter of credit held by a financial institution in connection with the Company’s office lease and cash deposits required to support the Company’s Automated Clearing House activities and secured corporate credit cards.

Servicing Rights

Prosper accounts for its servicing rights for loans originated prior to October 16, 2008 under the fair value measurement method of reporting in accordance with Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 860-50, Servicing Assets and Liabilities. Under the fair value method, Prosper measures its servicing rights at fair value at each reporting date and reports changes in fair value in earnings in the period in which the changes occur.

Prosper estimates the fair value of the servicing rights using a discounted cash flow model to project future expected cash flows based upon a set of valuation assumptions. Prosper believes market participants would use for similar rights. The primary assumptions Prosper uses to value its servicing rights include prepayment speeds, default rates, cost to service, profit margin, and discount rate. Prosper reviews these assumptions quarterly to ensure that they remain consistent with market conditions. Inaccurate assumptions in valuing servicing rights could affect Prosper’s results of operations.

Borrower Loans and Borrower Payment Dependent Notes

As of July 13, 2009, the Company implemented its new operating structure and began issuing Notes and purchasing loans from WebBank, and holding the loans until maturity. Prosper’s obligation to repay the Notes is conditioned upon the repayment of the associated borrower loan owned by Prosper. As a result of these changes, borrower loans and the Notes are carried on our balance sheet as assets and liabilities, respectively. In conjunction with our new operating structure, we adopted the provisions of ASC Topic 825, Financial Instruments. ASC Topic 825 permits companies to choose to measure certain financial instruments and certain other items at fair value on an instrument-by-instrument basis with unrealized gains and losses on items for which the fair value option has been elected reported in earnings. The fair value election, with respect to an item, may not be revoked once an election is made. In applying the provisions of ASC Topic 825, we recorded assets and liabilities measured using the fair value option in a way that separates these reported fair values from the carrying values of similar assets and liabilities measured with a different measurement attribute. We do not record a specific allowance account related to the borrower loans and Notes in which we have elected the fair value option, but rather estimate the fair value of the borrower loans and Notes using discounted cash flow methodologies adjusted for Prosper’s historical loss and recovery rates. We have reported the aggregate fair value of the borrower loans and Notes as separate line items in the assets and liabilities sections of the balance sheet using the methods described in ASC Topic 820, Fair Value Measurements and Disclosures– See Fair Value Measurement. We did not apply the provisions of ASC Topic 825 to loans issued prior to July 13, 2009.

Property and Equipment

Property and equipment consists of computer equipment, office furniture and equipment, and software purchased or developed for internal use. Property and equipment are stated at cost, less accumulated depreciation and amortization. Depreciation and amortization are computed using the straight-line method based on the estimated useful lives of the assets, which range from three to seven years. Prosper capitalizes expenditures for replacements and betterments and expenses amounts for maintenance and repairs as they are incurred. Depreciation and amortization commences once the asset is placed in service.

Internal Use Software and Website Development

Prosper accounts for internal use software costs, including website development costs, in accordance with ASC Topic 350-40, Internal Use Software and ASC Topic 350-50, Website Development Costs. In accordance with ASC Topic 350-40 and 350-50, the costs to develop software for Prosper’s website and other internal uses are capitalized when management has authorized and committed project funding, preliminary development efforts are successfully completed, and it is probable that the project will be completed and the software will be used as intended. Capitalized software development costs primarily include software licenses acquired, fees paid to outside consultants, and salaries for employees directly involved in the development efforts.

Costs incurred prior to meeting these criteria, together with costs incurred for training and maintenance, are expensed. Costs incurred for upgrades and enhancements that are considered to be probable to result in additional functionality are capitalized. Capitalized costs are included in Property and Equipment and amortized to expense using the straight-line method over their expected lives. The Company evaluates its software assets for impairment whenever events or changes in circumstances indicate that the carrying amount of such assets may not be recoverable. Recoverability of software assets to be held and used is measured by a comparison of the carrying amount of the asset to the future net undiscounted cash flows expected to be generated by the asset. If such software assets are considered to be impaired, the impairment to be recognized is the excess of the carrying amount over the fair value of the software asset.

Intangible Assets

Prosper records the purchase of intangible assets not purchased in a business combination in accordance with ASC Topic 350. Prosper has an intangible asset resulting from the purchase of the “Prosper.com” domain name. The intangible asset is amortized on a straight-line basis over five years.

Impairment of Long-Lived Assets Including Acquired Intangible Assets

In accordance with ASC Topic 360, Property Plant and Equipment, Prosper reviews property and equipment and intangible assets for impairment whenever events or changes in circumstances indicate that the carrying values of those assets may not be recoverable. Recoverability of assets to be held and used is measured by comparing the carrying value of the asset to future net undiscounted cash flows that the assets are expected to generate. If an asset is considered to be impaired, the impairment to be recognized equals the amount by which the asset’s carrying value exceeds its fair value. Fair value is estimated using discounted net cash flows.

Repurchase Obligation

Prosper is obligated to indemnify lenders and repurchase certain Notes sold to lenders in the event of Prosper’s violation of applicable federal, state, or local lending laws, or verifiable identify theft. The amount of the loan repurchase obligation is estimated based on historical experience. Prosper accrues a provision for the repurchase obligation when the loans are funded. Repurchased loans and Notes associated with federal, state, or local lending laws, or verifiable identity thefts are written off at the time of repurchase.

Revenue Recognition

Prosper recognizes revenue in accordance with ASC Topic 605, Revenue Recognition. Under ASC Topic 605, Prosper recognizes revenue when persuasive evidence of an arrangement exists, delivery has occurred or services have been rendered, the price of the services is fixed and determinable and collectability is reasonably assured.

Origination Fees

Origination fees are a percentage of the amount borrowed varying by Prosper Rating and are recognized when the loan is funded to the borrower. Effective July 26, 2010, borrowers with a Prosper Rating of AA are charged an origination fee of 0.5% of the aggregate principal balance of the loan with no minimum fee, borrowers with a Prosper Rating of A through B are charged an origination fee of 3% of the aggregate principal balance of the loan or $75 whichever is greater and borrowers with a Prosper Rating of C through HR are charged an origination fee of 4.5% of the aggregate principal balance of the loan or $75, whichever is greater. As of December 20, 2010, we eliminated the $75 minimum fee. Prior to July 26, 2010, borrowers with a Prosper Rating of AA were charged an origination fee of 0.5% of the aggregate principal balance of the loan with no minimum fee, borrowers with a Prosper Rating of A through HR were charged an origination fee of 3% of the aggregate principal balance of the loan or $50 whichever was greater.

Loan servicing fees

Loan servicing revenue includes monthly loan servicing fees and non-sufficient funds (NSF) fees on loans originated prior to October 16, 2008. Loan servicing fees are accrued daily based on the current outstanding loan principal balance of the borrower loan but are not recognized until payment is received due to the uncertainty of collection of borrower loan payments. Servicing fees for a loan vary based on the credit grade of the borrower. Prosper charges a NSF fee to borrowers on the first failed payment of each billing period. NSF fees are charged to the borrower and collected and recognized immediately.

Interest income (expense) on Borrower Loans receivable and Payment Dependent Notes

We recognize interest income on our borrower loan receivable using the accrual method based on the stated interest rate to the extent that we believe it to be collectable. We record interest expense on the corresponding Payment Dependent Note based on the contractual interest rate. Gross interest income earned and gross interest expense incurred was $1,458,204 and $1,377,930, and $459,491 and $433,617, for the three months ended March 31, 2011 and 2010, respectively.

Advertising and Promotional Expenses

Under the provisions of ASC Topic 720, Other Expenses, the costs of advertising are expensed as incurred. Advertising costs were approximately $518,000 and $287,000 for the three months ended March 31, 2011 and 2010, respectively.

Stock-Based Compensation

The Company accounts for its stock-based compensation for employees using fair-value-based accounting in accordance with ASC Topic 718, Stock Compensation. ASC Topic 718 requires companies to estimate the fair value of stock-based awards on the date of grant using an option-pricing model. The stock-based compensation related to awards that is expected to vest is amortized using the straight line method over the vesting term of the stock-based award, which is generally four years. Expected forfeitures of unvested options are estimated at the time of grant and reduce the recognized stock-based compensation expense. The forfeitures were estimated based on historical experience. The Company estimated its annual forfeiture rate to be 23.4% and 23.5% for the three months ended March 31, 2011 and 2010, respectively.

Prosper has granted options to purchase shares of common stock to nonemployees in exchange for services performed. Prosper accounts for stock options and restricted stock issued to nonemployees in accordance with the provisions of ASC Topic 505-50, Equity-Based Payments to Non-Employees, which requires that equity awards be recorded at their fair value. Under ASC Topic 718 and 505-50, Prosper uses the Black-Scholes model to estimate the value of options granted to nonemployees at each vesting date to determine the appropriate charge to stock-based compensation. The volatility of common stock was based on comparative company volatility.

The fair value of stock option awards for the three months ended March 31, 2011 and 2010 was estimated at the date of grant using the Black-Scholes model with the following average assumptions:

|

Three Months Ended

|

|||

|

March 31,

|

|||

|

2011

|

2010

|

||

|

Volatility of common stock

|

65.84%

|

**

|

|

|

Risk-free interest rate

|

1.70%

|

**

|

|

|

Expected life*

|

4.5 years

|

**

|

|

|

Dividend yield

|

0%

|

**

|

|

|

Weighted-average fair value of grants

|

$0.20

|

**

|

|

|

*For nonemployee stock option awards, the expected life is the contractual term of the award, which is generally ten years.

**No stock option awards were granted during the quarter ended March 31, 2010.

|

The Black-Scholes model requires the input of highly subjective assumptions, including the expected stock price volatility. Because Prosper’s equity awards have characteristics significantly different from those of traded options, the changes in the subjective input assumptions can materially affect the fair value estimate.

Total stock-based compensation expense for employee and non-employee stock-option awards reflected in the statements of operations for the three months ended March 31, 2011 and 2010 was $71,898 and $59,222, respectively. As of March 31, 2011, the unamortized stock-based compensation expense related to unvested stock-based awards was approximately $314,764 which will be recognized over the remaining vesting period of approximately 2.7 years.

Net Loss Per Share

Prosper computes net loss per share in accordance with ASC Topic 260 Earnings Per Share. Under ASC Topic 260, basic net loss per share is computed by dividing net loss per share available to common stockholders by the weighted average number of common shares outstanding for the period and excludes the effects of any potentially dilutive securities. Diluted earnings per share, if presented, would include the dilution that would occur upon the exercise or conversion of all potentially dilutive securities into common stock using the “treasury stock” and/or “if converted” methods as applicable. At March 31, 2011, there were outstanding convertible preferred stock, warrants and options convertible into 32,848,832, 572,703 and 6,716,503 common shares, respectively, which may dilute future earnings per share. Due to the Company reporting a net loss for the three months ended March 31, 2011 and 2010, there is no calculation of fully-diluted earnings per share as all common stock equivalents are anti-dilutive.

Income Taxes

Prosper uses the liability method to account for income taxes. Under this method, deferred income tax assets and liabilities are based on the differences between the financial statements and tax bases of assets and liabilities that will result in taxable or deductible amounts in the future based on enacted tax laws and rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established when necessary to reduce deferred tax assets to the amount expected to be realized. Under ASC Topic 740, Income Taxes. our policy to include interest and penalties related to gross unrecognized tax benefits within our provision for income taxes did not change.

Fair Value Measurement

Prosper adopted ASC Topic 820 on January 1, 2008. ASC Topic 820 provides a framework for measuring the fair value of assets and liabilities. ASC Topic 820 also provides guidance regarding a fair value hierarchy, which prioritizes information used to measure fair value and the effect of fair value measurements on earnings and provides for enhanced disclosures determined by the level within the hierarchy of information used in the valuation. ASC Topic 820 applies whenever other standards require (or permit) assets or liabilities to be measured at fair value but does not expand the use of fair value in any new circumstances.

ASC Topic 820 defines fair value in terms of the price that would be received upon the sale of an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The price used to measure the fair value is not adjusted for transaction costs while the cost basis of certain financial instruments may include initial transaction costs. Under ASC Topic 820, the fair value measurement also assumes that the transaction to sell an asset occurs in the principal market for the asset or, in the absence of a principal market, the most advantageous market for the asset. The principal market is the market in which the reporting entity would sell or transfer the asset with the greatest volume and level of activity for the asset. In determining the principal market for an asset or liability under ASC Topic 820, it is assumed that the reporting entity has access to the market as of the measurement date. If no market for the asset exists or if the reporting entity does not have access to the principal market, the reporting entity should use a hypothetical market.

Under ASC Topic 820, assets and liabilities carried at fair value in the balance sheets are

classified among three levels based on the observability of the inputs used to determine fair value:

|

Level 1 — The valuation is based on quoted prices in active markets for identical instruments.

|

|

|

Level 2 — The valuation is based on observable inputs such as quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based valuation techniques for which all significant assumptions are observable in the market.

|

|

Level 3 — The valuation is based on unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the instrument. Level 3 valuations are typically performed using pricing models, discounted cash flow methodologies, or similar techniques, which incorporate management’s own estimates of assumptions that market participants would use in pricing the instrument or valuations that require significant management judgment or estimation.

|

Prosper determines the fair values of its financial instruments based on the fair value hierarchy established in that standard, which requires an entity to maximize the use of quoted prices and observable inputs and to minimize the use of unobservable inputs when measuring fair value. Various valuation techniques are utilized, depending on the nature of the financial instrument, including the use of market prices for identical or similar instruments, or discounted cash flow models. When possible, active and observable market data for identical or similar financial instruments are utilized. Alternatively, fair value is determined using assumptions that management believes a market participant would use in pricing the asset or liability.

The Company’s financial instruments consist principally of cash and cash equivalents, restricted cash, receivables, borrower loans, servicing rights, accounts payable and accrued liabilities, Borrower Payment Dependent Notes and long-term debt. The estimated fair values of cash and cash equivalents, restricted cash, accounts payable and accrued liabilities approximate their carrying values because of their short term nature.

The following tables present the assets and liabilities measured at fair value on a recurring basis as of March 31, 2011 and December 31, 2010:

|

December 31, 2010

|

Level 1 Inputs

|

Level 2 Inputs

|

Level 3 Inputs

|

Fair Value

|

|||||||||

|

Assets

|

|||||||||||||

|

Servicing rights

|

—

|

—

|

$

|

2,986

|

$

|

2,986

|

|||||||

|

Borrower Loans receivable

|

—

|

—

|

23,689,950

|

23,689,950

|

|||||||||

|

Liabilities

|

|||||||||||||

|

Borrower Payment Dependent Notes

|

—

|

—

|

$

|

23,478,046

|

$

|

23,478,046

|

|||||||

|

March 31, 2011

|

Level 1 Inputs

|

Level 2 Inputs

|

Level 3 Inputs

|

Fair Value

|

|||||||||

|

Assets

|

|||||||||||||

|

Servicing rights

|

—

|

—

|

$

|

967

|

$

|

967

|

|||||||

|

Borrower Loans receivable

|

—

|

—

|

30,359,534

|

30,359,534

|

|||||||||

|

Liabilities

|

|||||||||||||

|

Borrower Payment Dependent Notes

|

—

|

—

|

$

|

30,026,687

|

$

|

30,026,687

|

|||||||

As observable market prices are not available for the borrower loans and Notes we hold, or for similar assets and liabilities, we believe the borrower loans and Notes should be considered Level 3 financial instruments under ASC Topic 820. In a hypothetical transaction as of the measurement date, the Company believes that differences in the principal marketplace in which the loans are originated and the principal marketplace in which the Company might offer those loans may result in differences between the originated amount of the loans and their fair value as of the transaction date. For borrower loans, the fair value is estimated using discounted cash flow methodologies based upon valuation assumptions including prepayment speeds, roll rates, recovery rates and discount rates based on the perceived credit risk within each credit grade.

Our obligation to pay principal and interest on any Note is equal to the loan payments, if any, we receive on the corresponding borrower loan, net of our 1.0% servicing fee. As such, the fair value of the Note is approximately equal to the fair value of the borrower loans, adjusted for the 1.0% servicing fee. Any unrealized gains or losses on the borrower loans and Notes for which the fair value option has been elected is recorded as a separate line item in the statement of operations. The effective interest rate associated with the Notes will be less than the interest rate earned on the borrower loans due to the 1.0% servicing fee. See Note 4 for a rollforward and further discussion of the significant assumptions used to value borrower loans and Notes.

Servicing rights related to loans originated prior to October 16, 2008 do not trade in an active open market with readily observable prices. Although sales of servicing assets do occur, the nature and character of the assets underlying those transactions are not similar to those held by the Company and, therefore, the precise terms and conditions typically seen in the marketplace would likely not be available to the Company. Accordingly, management determines the fair value of its servicing rights using a discounted cash flow model to project future expected cash flows based upon a set of valuation assumptions Prosper believes market participants would use for similar rights. The primary assumptions Prosper uses for valuing its servicing asset include prepayment speeds, default rates, cost to service, profit margin, and discount rate.

Prosper reviews these assumptions to ensure that they remain consistent with the market conditions. Inaccurate assumptions in valuing the servicing rights could affect Prosper’s results of operations. Due to the nature of the valuation inputs, servicing assets are classified as Level 3. The change in the fair-value of servicing rights is included in cost of services in the statement of operations. See Note 3 for a further discussion of the significant assumptions used to value servicing rights.

The changes in Level 3 assets measured at fair value on a recurring basis are as follows:

|

Fair Value Measurements Using Significant Unobservable Inputs (Level 3)

|

||||||||||||

|

Servicing Rights

|

Borrower Loans

|

Borrower Payment Dependent Notes

|

Total

|

|||||||||

|

Balance at January 1, 2010

|

$

|

24,319

|

|

$ |

7,020,363

|

$ |

(6,903,173)

|

$

|

141,509

|

|||

|

Originations

|

5,933,690

|

(5,933,690)

|

—

|

|||||||||

|

Principal repayments

|

(1,337,679)

|

1,311,571

|

(26,108)

|

|||||||||

|

Change in fair value on borrower loans and Payment Dependent Notes

|

(634,691)

|

725,400

|

90,709

|

|||||||||

|

Change in fair value of servicing rights

|

(7,114)

|

—

|

—

|

(7,114)

|

||||||||

|

Balance at March 31, 2010

|

$

|

17,205

|

$

|

10,981,683

|

$

|

(10,799,892)

|

$

|

198,996

|

||||

|

Balance at January 1, 2011

|

$

|

2,986

|

$

|

23,689,950

|

$

|

(23,478,046)

|

$

|

214,890

|

||||

|

Originations

|

11,471,874

|

(11,471,874)

|

—

|

|||||||||

|

Principal repayments

|

(4,506,839)

|

4,343,090

|

(163,749)

|

|||||||||

| Change in fair value on borrower loans and Payment Dependent Notes | (295,451) | 580,143 | 284,692 | |||||||||

|

Change in fair value of servicing rights

|

(2,019)

|

—

|

—

|

(2,019)

|

||||||||

|

Balance at March 31, 2011

|

$ | 967 | $ | 30,359,534 | $ | (30,026,687) | $ | 333,814 | ||||

New Accounting Pronouncements

In January 2010, FASB issued ASU No. 2010-06, “Fair Value Measurements and Disclosures,” that requires reporting entities to make new disclosures about recurring or nonrecurring fair-value measurements including significant transfers into and out of Level 1 and Level 2 fair-value measurements and information on purchases, sales, issuances, and settlements on a gross basis in the reconciliation of Level 3 fair-value measurements. The FASB also clarified existing fair-value measurement disclosure guidance about the level of disaggregation, inputs, and valuation techniques. The new and revised disclosures are required to be implemented in fiscal years beginning after December 15, 2009. The adoption of this standard did not have a material impact on our financial statements.

3. Servicing Rights

Prosper calculates the fair value of the servicing asset based on the following assumptions:

|

March 31,

|

|||

|

2011

|

2010

|

||

|

Unpaid principal loan balance under service

|

$2,200,000

|

$20,100,000

|

|

|

Servicing fees

|

0.0% - 1.0%

|

0.0% - 1.0%

|

|

|

Projected prepayment speed

|

2.32%

|

1.20%

|

|

|

Discount rate

|

25%

|

25%

|

|

No servicing rights were purchased or sold during the three months ended March 31, 2011.

4. Borrower Loans and Borrower Payment Notes Held at Fair Value

Prosper estimates the fair value of the borrower loans and Notes using discounted cash flow methodologies based upon a set of valuation assumptions. The main assumptions Prosper used to value the borrower loans and Notes include prepayment rates derived from historical prepayment rates for each credit score, default rates derived from historical performance, recovery rates and discount rates applied to each credit tranche based on the perceived credit risk of each credit grade. Our obligation to pay principal and interest on any Note is equal to the loan payments, if any, we receive on the corresponding borrower loan, net of our 1.0% servicing fee. As such, the fair value of the Note is approximately equal to the fair value of the borrower loans, adjusted for the 1.0% servicing fee. The effective interest rate associated with the Notes will be less than the interest rate earned on the borrower loans due to the 1.0% servicing fee.

For borrower loans originated and Notes issued after July 13, 2009, we used the following average assumptions to determine the fair value as of March 31, 2011:

|

Monthly prepayment rate speed

|

0.49%

|

|

Recovery rate

|

5.32%

|

|

Discount rate *

|

19.07%

|

|

Weighted average default rate

|

9.30%

|

|

* This is the average discount rate among all of Prosper’s credit grades

|

|

The following table presents additional information about borrower loans and Notes measured at fair value on a recurring basis for the three months ended March 31, 2011:

|

Borrower Loans

|

Notes

|

|||||||

|

Fair value at January 1, 2011

|

$

|

23,689,950

|

$

|

23,478,046

|

||||

|

Originations

|

11,471,874

|

11,471,874

|

||||||

|

Principal repayments

|

(4,175,417)

|

(4,011,668)

|

||||||

|

Borrower Loans and Notes charged-off during the period

|

(331,422)

|

(331,422)

|

||||||

|

Realized and unrealized losses included in earnings

|

(295,451)

|

—

|

||||||

|

Realized and unrealized gains included in earnings

|

—

|

(580,143)

|

||||||

|

Fair value at March 31, 2011

|

$

|

30,359,534

|

$

|

30,026,687

|

||||

Due to the recent origination of the borrower loans and Notes, the change in fair value attributable to instrument-specific credit risk is immaterial. The Company had no originations of borrower loans or issuances of Notes prior to July 13, 2009. Of the loans originated from July 13, 2009 to March 31, 2011, the Company had 333 loans which were 90 days or more delinquent for an aggregate principal amount of $1,213,774 and a fair value of $55,971 as of March 31, 2011.

5. Notes Payable

As of March 31, 2011 and December 31, 2010, notes payable consist of the following:

|

March 31, 2011

|

December 31, 2010

|

|||||||

|

Non-interest bearing promissory note

|

$ | 300,000 | $ | 300,000 | ||||

|

Unamortized discount on the non-interest bearing note

|

(5,703 | ) | (11,046 | ) | ||||

|

Total promissory notes payable

|

$ | 294,297 | $ | 288,594 | ||||

Non-interest bearing promissory note

In 2006, we entered into a non-interest bearing promissory note in the amount of $380,000 for the purchase of the “Prosper.com” domain name. The note was discounted by $109,583 for a net payable of $270,417. The promissory note includes both principal and interest and is payable in annual installments of $20,000 due on the first, second, third, and fourth anniversary of the note and $300,000 due on the fifth anniversary of the note. Interest on the note was imputed at an 8% annual rate and is amortized to interest expense over the five year life of the loan. The carrying value at March 31, 2011 and 2010 is $294,297 and $292,051, respectively. The fair value is calculated based on discounted cash flows and is estimated to be $289,025 and $268,266 at March 31, 2011 and 2010, respectively. We recorded amortized interest expense of $5,703 and $5,514 for the three months ended March 31, 2011 and 2010, respectively.

6. Accrued Liabilities

As of March 31, 2011 and December 31, 2010, accrued liabilities consist of the following:

|

March 31,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

Legal accruals and fees

|

$ | 525,775 | $ | 373,572 | ||||

|

Audit, tax and accounting

|

334,951 | 411,256 | ||||||

|

Payroll and benefits

|

199,316 | 161,732 | ||||||

|

Loan servicing costs

|

120,216 | 115,364 | ||||||

|

Other

|

338,189 | 157,315 | ||||||

| $ | 1,518,447 | $ | 1,219,239 | |||||

7. Repurchase Obligation

Changes in the repurchase obligation are summarized below:

|

Balance at January 1, 2011

|

$

|

71,001

|

||

|

Reversal of provision for Loans and Notes repurchases

|

(55,331)

|

|||

|

Repurchased Loans and Notes recoveries during the period

|

(2,669)

|

|||

|

Balance at March 31, 2011

|

$

|

13,001

|

As mentioned in Note 2, the Company computes net loss per share in accordance with ASC Topic 260. Under ASC Topic 260, basic net loss per share is computed by dividing net loss per share available to common stockholders by the weighted average number of common shares outstanding for the period and excludes the effects of any potentially dilutive securities. Diluted earnings per share, if presented, would include the dilution that would occur upon the exercise or conversion of all potentially dilutive securities into common stock using the “treasury stock” and/or “if converted” methods as applicable.

Basic and diluted loss per share was calculated as follows:

|

Three Months Ended March 30,

|

||||||||

|

2011

|

2010

|

|||||||

|

Numerator:

|

||||||||

|

Net loss

|

$

|

(1,060,355)

|

$

|

(2,642,720)

|

||||

|

Denominator:

|

||||||||

|

Weighted average shares used in computing basic and diluted net loss per share

|

4,497,556

|

4,460,667

|

||||||

|

Basic and diluted net loss per share

|

$

|

(0.24)

|

$

|

(0.59)

|

||||

|

March 31,

|

||||

|

2011

|

2010

|

|||

|

Excluded Securities:

|

||||

|

Convertible preferred stock issued and outstanding

|

32,848,832

|

9,397,939

|

||

|

Stock options issued and outstanding

|

6,716,503

|

1,757,440

|

||

| Warrant issued and outstanding | 572,703 | - | ||

|

Total common stock equivalents excluded from diluted net loss per common share computation

|

40,138,038

|

11,155,379

|

||

Preferred Stock

Under Prosper’s certificate of incorporation, preferred stock is issuable in series, and the Board of Directors is authorized to determine the rights, preferences, and terms of each series.

In April 2005, Prosper issued and sold 4,023,999 shares of Series A convertible preferred stock (Series A) in a private placement for $7,464,450, net of issuance costs of $80,550. In February 2006, Prosper issued and sold 3,310,382 shares of Series B convertible preferred stock (Series B) in a private placement for $12,412,302, net of issuance costs of $87,700. In June 2007, Prosper issued and sold 2,063,558 shares of Series C convertible preferred stock (Series C) in a private placement for $19,919,009, net of issuance costs of $80,996. In April 2010, Prosper issued and sold 20,340,705 shares of Series D (Series D) and 3,110,188 shares of Series D-1 (Series D-1) convertible preferred stock in a private placement for $14,595,709, which is net of issuance costs of $125,903.

Dividends

The holders of the Series A, Series B, Series C and Series D preferred stock are entitled to receive dividends at an annual rate of 8% per share for the preferred stock times the Liquidation Preference for such shares of preferred stock payable in preference and priority to any declaration or payment of any distribution on common stock or Series D-1 preferred stock. The Series D-1 preferred stock are not entitled to receive dividends in preference and priority to or on a pari passu basis with the other preferred stock. In addition, the Series D-1 preferred stock are not entitled to receive dividends in preference and priority to any distribution of common stock. Such dividends shall be payable only when, as, and if declared by the Board of Directors. To date, no dividends have been declared, and there are no dividends in arrears at March 31, 2011. The right to receive dividends on shares of Series D shall be cumulative from and after the date of issuance of the Series D preferred stock. The right to receive dividends of Series A, Series B and Series C are not cumulative. No right to such dividends shall accrue to holders of Preferred Stock by reason of the fact that dividends on said shares are not declared or paid in any calendar year.

Conversion

Each share of preferred stock shall automatically be converted into fully-paid, non-assessable shares of common stock at the conversion rate for such share (i) immediately prior to the closing of a firm commitment underwritten initial public offering with aggregate proceeds to Prosper of at least $25,000,000 (after deducting underwriters commissions and expenses), pursuant to an effective registration statement filed under the Securities Act of 1933, as amended (the “Securities Act”), covering the offer and sale of Prosper’s common Stock, or (ii) upon the receipt of a written request for such conversion from the holders of more than sixty percent (60%) of the voting power of all then outstanding shares of preferred stock, or, if later, the effective date for conversion specified in such requests, provided that shares of Series D shall not be automatically converted pursuant to this clause (ii) unless the holders of eighty-two percent (82%) of the outstanding shares of Series D approve such conversion. In addition, in the event shares of Series C Preferred Stock are converted in connection with a Liquidation Event and as a result there are fewer than 1,000,000 shares of Series C Preferred Stock outstanding, each share of Series D-1 Preferred Stock shall automatically be converted into fully-paid, non-assessable shares of Common Stock at the then effective Conversion Rate for such shares.

Liquidation Rights

In the event of any liquidation, dissolution, or winding up of Prosper, whether voluntary or involuntary, Series D preferred stock shall be entitled to receive, prior and in preference to any distribution of the proceeds to the holders of Series A, Series B, Series C, Series D-1 or Common Stock by reason of their ownership of such stock, an amount per share for each share of Series D Preferred Stock held by them equal to the sum of $0.7385 (as adjusted for any stock dividends, combinations, or splits), plus all declared but unpaid dividends (if any) on each share of preferred stock. If upon such Liquidation Event, the assets of the Company legally available for distribution to the holders of the Series D Preferred Stock are insufficient to pay the preferential amount, then the entire assets of the Corporation legally available for distribution shall be distributed with equal priority and pro rata among the holders of the Series D Preferred Stock.

After the payment or setting aside for payment to the holders of Series D Preferred Stock of the preferential amount, then the entire assets and funds of Prosper legally available for distribution will be distributed ratably among the holders of the Series A, Series B and Series C and Series D-1 in proportion to the preferential amount each such holder is otherwise entitled to receive ($0.938 for each share of Series A, $1.888 for each share of Series B, $4.846 for each share of Series C, and $1.00 for each share of Series D-1).

Voting

Each holder of shares of the preferred stock shall be entitled to the number of votes equal to the number of shares of common stock into which such shares of preferred stock could be converted and shall have voting rights and powers equal to the voting rights and powers of the common stock (except as otherwise expressly provided herein or as required by law), voting together with the common stock as a single class, and shall be entitled to notice of any stockholders’ meeting in accordance with the Bylaws of Prosper. The holders of the preferred stock shall vote as one class with the holder of the common stock except with respect to certain matters that require separate votes.

Common Stock

Prosper is authorized to issue up to 43,860,321 shares of common stock, $0.001 par value, of which 4,498,667 and 4,478,667 shares were issued and outstanding as of March 31, 2011, and December 31, 2010, respectively. Each holder of common stock shall be entitled to one vote for each share of common stock held.

Common Stock Issued upon Exercise of Stock Options

For the three months ended March 31, 2011, the Company issued 20,000 shares upon the exercise of options for cash proceeds of $5,000.

10. Stock Option Plan and Other Stock Compensation

In 2005, Prosper’s Board of Directors, which at such time was comprised of the Company’s sole stockholders, approved the adoption of the 2005 Stock Option Plan (the “Plan”). Under the Plan, options to purchase up to 1,879,468 shares of common stock were reserved for grants to employees, directors, and consultants by the Board of Directors to promote the success of Prosper’s business. On January 31, 2008, the Board of Directors increased the total number of options under the Plan by 500,000 for a total of 2,379,468 options available for grant. On October 6, 2009, the Board of Directors increased the total number of options under the Plan by an additional 500,000 for a total of 2,879,468 options available for grant. On April 15, 2010, the Board of Directors increased the total number of options under the Plan by an additional 6,109,321 for a total of 8,988,789 options available to grant.

Incentive stock options are granted to employees at an exercise price not less than 100% of the fair value of Prosper’s common stock on the date of grant. Nonstatutory stock options are granted to consultants and directors at an exercise price not less than 85% of the fair value of Prosper’s common stock on the date of grant. If options are granted to stockholders who hold 10% or more of Prosper’s common stock on the option grant date, then the exercise price shall not be less than 110% of the fair value of Prosper’s common stock on the date of grant. The fair value is based on a good faith estimate by the Board of Directors at the time of each grant. As there is no active trading market for these options, such estimates may ultimately differ from valuations completed by an independent party. The options generally vest over four years, which is the same as the performance period. In no event are options exercisable more than ten years after the date of grant.

Option activity under the Option Plan is summarized as follows for the periods below:

|

Options Issued and Outstanding

|

Weighted-Average Exercise Price

|

|||||||

|

Balance as of January 1, 2010

|

1,897,126 | $ | 0.96 | |||||

|

Options granted (weighted average fair value of $0.00)

|

- | $ | 0.00 | |||||

|

Options exercised

|

- | $ | 0.00 | |||||

|

Options canceled

|

(139,686 | ) | $ | 1.05 | ||||

|

Balance as of March 31, 2010

|

1,757,440 | $ | 0.95 | |||||

|

Balance as of January 1, 2011

|

5,766,859 | $ | 0.30 | |||||

|

Options granted (weighted average fair value of $0.20)

|

1,112,978 | $ | 0.20 | |||||

|

Options exercised

|

(20,000 | ) | $ | 0.25 | ||||

|

Options canceled

|

(143,334 | ) | $ | 0.39 | ||||

|

Balance as of March 31, 2011

|

6,716,503 | $ | 0.28 | |||||

|

Options outstanding and exercisable at March 31, 2011

|

764,827 | $ | 0.73 | |||||

Other Information Regarding Stock Options

Additional information regarding common stock options outstanding as of March 31, 2011 is as follows:

|

Options Outstanding

|

Options Exercisable

|

|||||||||||||||||||||||||||

|

Range of Exercise Prices

|

Number Outstanding

|

Weighted Avg. Remaining Life

|

Weighted Avg. Exercise Price

|

Intrinsic Value

|

Number Exercisable

|

Weighted Avg. Exercise Price

|

Intrinsic Value

|

|||||||||||||||||||||

|

$0.20 - $0.20

|

5,842,917 | 9.36 | $ | 0.20 | $ | – | 127,290 | $ | 0.20 | $ | – | |||||||||||||||||

|

$0.25 - $0.25

|

34,158 | 4.43 | 0.25 | – | 34,158 | 0.25 | – | |||||||||||||||||||||

|

$0.50 - $0.50

|

304,117 | 5.62 | 0.50 | – | 303,595 | 0.50 | – | |||||||||||||||||||||

|

$0.56 - $0.56

|

365,000 | 8.34 | 0.56 | – | 154,685 | 0.56 | – | |||||||||||||||||||||

|

$1.94 - $1.94

|

125,311 | 7.76 | 1.94 | – | 110,829 | 1.94 | – | |||||||||||||||||||||

|

$2.17 - $2.17

|

45,000 | 6.94 | 2.17 | – | 34,270 | 2.17 | – | |||||||||||||||||||||

| 6,716,503 | 9.06 | $ | 0.28 | $ | – | 764,827 | $ | 0.73 | $ | – | ||||||||||||||||||

The intrinsic value is calculated as the difference between the value of Prosper's common stock at March 31, 2011, which was $0.20 per share, and the exercise price of the options.

No compensation expense is recognized for unvested shares that are forfeited upon termination of service, and the stock-based compensation expense for the three months ended March 31, 2011 and 2010 reflect the expenses that Prosper expects to recognize after the consideration of estimated forfeitures.

11. Income Taxes

As part of the process of preparing the Company’s financial statements, the Company is required to estimate its income taxes in each of the jurisdictions in which it operates. This process involves determining the Company’s income tax expense (benefit) together with calculating the deferred income tax expense (benefit) related to temporary differences resulting from differing treatment of items, such as deferred revenue or deductibility of certain intangible assets, for tax and accounting purposes. These differences result in deferred tax assets and liabilities, which are included within the accompanying balance sheet. The Company must then assess the likelihood that the deferred tax assets will be recovered through the generation of future taxable income.

Due to the book and tax net losses incurred during the three months ended March 31, 2011 and 2010, Prosper has not incurred any income tax expense during those periods. In addition, Prosper has maintained a full valuation allowance against its net deferred tax assets because the realization of those deferred tax assets is dependent upon future earnings, and the amount and timing of those earnings, if any is uncertain.

12. Commitments and Contingencies

Future minimum lease payments and other commitments

Prosper leases its corporate office and co-location facility under noncancelable operating leases that expire in July 2011 and August 2011, respectively. Prosper’s corporate office lease has the option to renew for an additional three years. On February 25, 2011, we exercised our option to extend our corporate office lease term by two years so that the lease will expire on July 31, 2013. Future minimum rental payments under these leases as of March 31, 2011 are as follows:

|

Remaining nine months ended December 31, 2011

|

$

|

278,371

|

||

|

Years ended December 31:

|

||||

|

2012

|

293,184

|

|||

|

2013

|

171,024

|

|||

|

Total future operating lease obligations

|

$

|

742,579

|

Rental expense under premises-operating lease arrangements was approximately $102,400 for both the three months ended March 31, 2011, and March 31, 2010, respectively.

On April 14, 2008, the Company entered into an agreement with a WebBank, Utah-chartered industrial bank whereby all loans originated through the Prosper marketplace resulting from listings posted on or after April 15, 2008 are made by WebBank under its bank charter. The arrangement allows for loans to be offered to borrowers at uniform nationwide terms. The Company is required to pay WebBank the greater of a monthly minimum fee or a fee calculated based on a certain percentage of monthly loan origination volume.

On March 3, 2009, the Company entered into an agreement with a third party broker-dealer in which the third party agreed to operate and maintain Prosper’s Note Trader Platform on which lender members may offer their Notes for sale to other lender members. The Company, if any, is required to pay the third party broker-dealer an agreed upon monthly fee which equals the difference between the minimum monthly fee and the transaction fees collected by the third party provider during that month.

Securities Law Compliance

From inception through October 16, 2008, the Company sold approximately $178.1 million of loans to unaffiliated lender members, and $1.0 million of loans to affiliated lender members through the Prosper platform whereby the Company assigned promissory notes directly to lender members. The Company did not register the offer and sale of the promissory notes offered and sold through the Prosper platform under the Securities Act of 1933 or under the registration or qualification provisions of the state securities laws. The Company’s management believes that the question of whether or not the operation of the Prosper platform involved an offer or sale of a “security” involved a complicated factual and legal analysis and was uncertain. If the sales of promissory notes offered through the Company’s platform were viewed as a securities offering, the Company would have failed to comply with the registration and qualification requirements of federal and state laws and lender members who hold these promissory notes may be entitled to rescission of unpaid principal, plus statutory interest. Generally, the federal statute of limitations for noncompliance with the requirement to register securities under the Securities Act of 1933 is one year from the violation.