UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x |

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2011 | ||

| ||

o |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to | ||

Commission file number: 001-33894

MIDWAY GOLD CORP.

(Exact name of registrant as specified in its charter)

British Columbia |

| 98-0459178 |

(State of other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

Suite 280 - 8310 South Valley Highway |

|

|

Englewood, Colorado |

| 80112 |

(Address of principal executive offices) |

| (Zip Code) |

(720) 979-0900

(Registrant’s Telephone Number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. ![[midway10q05132011004.gif]](midway10q05132011004.gif) Yes

Yes ![[midway10q05132011006.gif]](midway10q05132011006.gif) No

No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ![[midway10q05132011008.gif]](midway10q05132011008.gif) Yes

Yes ![[midway10q05132011010.gif]](midway10q05132011010.gif) No

No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer” and “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer ![[midway10q05132011012.gif]](midway10q05132011012.gif) Accelerated filer

Accelerated filer ![[midway10q05132011014.gif]](midway10q05132011014.gif) Non-accelerated filer

Non-accelerated filer ![[midway10q05132011016.gif]](midway10q05132011016.gif) Smaller Reporting Company

Smaller Reporting Company ![[midway10q05132011018.gif]](midway10q05132011018.gif)

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ![[midway10q05132011020.gif]](midway10q05132011020.gif) Yes

Yes ![[midway10q05132011022.gif]](midway10q05132011022.gif) No

No

Number of Shares outstanding at May 10, 2011:, 102,521,121

| TABLE OF CONTENTS | ||

| PART I - FINANCIAL INFORMATION | 1 | |

| ITEM 1. | FINANCIAL STATEMENTS | 1 |

| ITEM 2. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

20 |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 35 |

| ITEM 4. | CONTROLS AND PROCEDURES | 35 |

| PART II - OTHER INFORMATION | 35 | |

| ITEM 1. | LEGAL PROCEEDINGS | 35 |

| ITEM 1A. | RISK FACTORS | 36 |

| ITEM 2. | UNREGISTERED SALE OF EQUITY SECURITIES AND USE OF PROCEEDS | 36 |

| ITEM 3. | DEFAULTS UPON SENIOR SECURITIES | 36 |

| ITEM 4. | [RESERVED] | 36 |

| ITEM 5. | OTHER INFORMATION | 36 |

| ITEM 6. | EXHIBITS | 36 |

| SIGNATURES | 38 | |

EXPLANATORY NOTE

All references to “$” in this report mean the Canadian dollar. All references to “US$” refer to the U.S. dollar, and unless otherwise indicated all currency amounts in this report are stated in Canadian dollars.

PART I - FINANCIAL INFORMATION

Item 1.

Financial Statements.

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED INTERIM BALANCE SHEETS

(Expressed in Canadian dollars)

| March 31, 2011 | December 31, 2010 |

| (unaudited) |

|

Assets |

|

|

|

|

|

Current assets: |

|

|

Cash and cash equivalents | $ 7,512,983 | $ 6,062,816 |

Amounts receivable (note 6(b)) | 54,649 | 91,710 |

Prepaid expenses and other current assets | 492,227 | 134,981 |

| 8,059,859 | 6,289,507 |

|

|

|

Investments (notes 3 and 4) | 130,353 | 80,687 |

Reclamation deposit (note 7) | 268,783 | 260,087 |

Equipment (note 5) | 367,642 | 197,224 |

Mineral properties (note 6) | 50,017,862 | 49,571,061 |

|

|

|

| $ 58,844,499 | $ 56,398,566 |

|

|

|

Liabilities and stockholders’ equity |

|

|

|

|

|

Current liabilities: |

|

|

Accounts payable and accrued liabilities (note 11) | $ 916,691 | $ 711,091 |

|

|

|

Warrant liability (notes 3 and 8) | - | 1,562,544 |

Future income tax liability | 6,430,628 | 6,951,570 |

|

|

|

Stockholders’ equity (note 8): |

|

|

Common stock authorized - unlimited, no par value |

|

|

Issued - 101,655,246 (2010 - 96,439,496) | 107,196,264 | 100,062,385 |

Additional paid in capital | 9,052,899 | 9,192,426 |

Accumulated other comprehensive income | 56,875 | 13,125 |

Deficit accumulated during exploration stage | (64,808,858) | (62,094,575) |

| 51,497,180 | 47,173,361 |

|

|

|

| $ 58,844,499 | $ 56,398,566 |

Nature and continuance of operations (note 1)

Contingency (note 9)

Commitments (note 10)

Subsequent events (note14)

The accompanying notes are an integral part of these consolidated interim financial statements.

1

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS

(Expressed in Canadian dollars) (unaudited)

| Three months ended March 31, 2011 | Three months ended March 31, 2010 |

Cumulative period from inception (May 14,1996) to March 31, 2011 |

|

|

|

|

Expenses |

|

|

|

Consulting (note 11) | $ 43,687 | $ 22,500 | $ 796,552 |

Depreciation | 20,492 | 25,688 | 709,078 |

Gain on sale of subsidiary | - | - | (2,806,312) |

Interest and bank charges | 5,004 | 1,624 | 896,757 |

Investor relations | 39,596 | 35,193 | 1,275,603 |

Legal, audit and accounting | 73,102 | 66,448 | 2,685,544 |

Management fees | (3,717) | (4,520) | 212,871 |

Mineral exploration expenditures (Schedule) | 1,385,222 | 148,476 | 48,866,160 |

Mineral property interests written-off | - | - | 4,391,734 |

Mineral property interests recovered | - | - | (60,120) |

Office and administration | 62,884 | 42,645 | 1,575,391 |

Salaries and benefits | 804,384 | 233,142 | 10,118,448 |

Transfer agent and filing fees | 60,861 | 34,851 | 660,173 |

Travel | 61,265 | 47,748 | 1,041,000 |

Operating loss | 2,552,780 | 653,795 | 70,362,879 |

|

|

|

|

Other income (expenses): |

|

|

|

Foreign exchange gain (loss) | 49,595 | 260,847 | 1,035,588 |

Loss on change in fair value of warrant liability | (592,026) | - | (1,235,700) |

Interest and investment income | 2,012 | 668 | 855,337 |

Gain (loss) on sale of equipment | - | - | (5,903) |

Gain (loss) on sale of investments (note 3) | - | - | 44,077 |

Investment write down (note 3) | - | - | (130,000) |

Unrealized gain (loss) on investments | 5,916 | - | (578,867) |

Other income | - | 60 | 87,281 |

| (534,503) | 261,575 | 71,813 |

|

|

|

|

Net loss before income tax | 3,087,283 | 392,220 | 70,291,066 |

Income tax recovery | 373,000 | - | 5,482,208 |

|

|

|

|

Net loss | $ 2,714,283 | $ 392,220 | $ 64,808,858 |

|

|

|

|

Basic and diluted loss per share | $ 0.03 | $ 0.01 |

|

|

|

|

|

Weighted average number of shares outstanding | 98,409,788 | 77,354,997 |

|

The accompanying notes are an integral part of these consolidated interim financial statements.

2

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

(Expressed in Canadian dollars) (unaudited)

| Three months ended March 31, 2011 | Three months ended March 31, 2010 |

|

Cash provided by (used in): |

|

|

|

Operating activities: |

|

|

|

Net loss | $ (2,714,283) | $ (392,220) | $ (64,808,858) |

Items not involving cash: |

|

|

|

Depreciation | 20,492 | 25,688 | 709,078 |

Stock-based compensation | 528,957 | 11,029 | 7,503,689 |

Unrealized foreign exchange loss (gain) | (147,942) | (271,449) | (1,476,952) |

Investment write down | - | - | 130,000 |

Unrealized (gain) loss on investment | (5,916) | - | 578,867 |

Non-cash interest expense | - | - | 234,765 |

Loss on change in liability of warrants | 592,026 | - | 1,235,700 |

Future income tax recovery | (373,000) | - | (5,482,208) |

Gain on sale of subsidiary | - | - | (2,806,312) |

Loss (gain) on sale of equipment | - | - | 5,903 |

Loss (gain) on sale of investments | - | - | (44,077) |

Mineral property interests written off | - | - | 4,391,734 |

Mineral property interest recovery | - | - | (60,120) |

Change in non-cash working capital items: |

|

|

|

Amounts receivable | 37,061 | 19,778 | (36,362) |

Prepaid expenses | (357,246) | (78,472) | (512,269) |

Accounts payable and accrued liabilities | 205,600 | 27,435 | 1,011,696 |

| (2,214,251) | (658,211) | (59,425,726) |

Investment activities: |

|

|

|

Proceeds on sale of subsidiary | - | - | 254,366 |

Proceeds on sale of equipment | - | - | 22,820 |

Proceeds on sale of mineral property | - | - | 233,459 |

Proceeds on sale of investments | - | - | 321,852 |

Mineral property acquisitions | (446,801) | (380,193) | (21,723,025) |

Deferred acquisition costs | - | - | (23,316) |

Purchase of equipment | (190,910) | (23,433) | (2,090,729) |

Reclamation deposit | (8,696) | 936 | (684,166) |

| (646,407) | (402,690) | (23,688,739) |

Financing activities: |

|

|

|

Advance from Red Emerald Ltd. | - | - | 12,010,075 |

Common stock issued, net of issue costs | 4,310,825 | 432,104 | 72,292,768 |

Promissory note | - | - | 2,000,000 |

Repayment of promissory note | - | - | (2,000,000) |

Convertible debenture | - | - | 6,324,605 |

| 4,310,825 | 432,104 | 90,627,448 |

Increase (decrease) in cash and cash equivalents | 1,450,167 | (628,797) | 7,512,983 |

Cash and cash equivalents, beginning of period | 6,062,816 | 1,740,322 | - |

Cash and cash equivalents, end of period | $ 7,512,983 | $ 1,111,525 | $ 7,512,983 |

Supplementary information (note 13)

The accompanying notes are an integral part of these consolidated interim financial statements.

3

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED STATEMENT OF COMPREHENSIVE LOSS

(Expressed in Canadian dollars) (unaudited)

| Three Months ended March 31, 2011 | Three Months ended March 31, 2010 |

Net loss for the period before other comprehensive loss | $ 2,714,283 | $ 392,220 |

Unrealized (gain) on investment | (43,750) | - |

Comprehensive loss | $ 2,670,533 | $ 392,220 |

The accompanying notes are an integral part of these consolidated interim financial statements.

4

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

(Expressed in Canadian dollars) (unaudited)

|

| Number of shares | Common stock | Additional paid-in capital | Accumulated other comprehensive loss | Accumulated deficit during the exploration stage | Total stockholders’ equity |

Balance, May 14, 1996 (date of inception) | - | $ - | $ - | $ - | $ - | $ - | |

Shares issued: |

|

|

|

|

|

| |

Private placements | 700,000 | 168,722 |

|

|

| 168,722 | |

Net loss | - | - | - | - | (114,800) | (114,800) | |

Balance, December 31, 1996 | 700,000 | 168,722 |

|

| (114,800) | 53,922 | |

Shares issued: |

|

|

|

|

|

| |

Initial public offering | 2,025,000 | 590,570 | - | - | - | 590,570 | |

Principal shares | 750,000 | 7,500 | - | - | - | 7,500 | |

Private placement | 1,000,000 | 1,932,554 | 321,239 | - | - | 2,253,793 | |

Exercise of share purchase warrants | 1,000,000 | 2,803,205 | - | - | - | 2,803,205 | |

Acquisition of mineral property interest | 1,000,000 | 2,065,500 | - | - | - | 2,065,500 | |

Finder’s fee | 150,000 | 309,825 | - | - | - | 309,825 | |

Net loss | - | - | - | - | (2,027,672) | (2,027,672) | |

Balance, December 31, 1997 | 6,625,000 | 7,877,876 | 321,239 | - | (2,142,472) | 6,056,643 | |

Shares issued: |

|

|

|

|

|

| |

Exercise of share purchase warrants | 100,000 | 332,124 | (32,124) | - | - | 300,000 | |

Acquisition of mineral property interest | 200,000 | 246,000 | - | - | - | 246,000 | |

Finder’s fee | 150,000 | 224,250 | - | - | - | 224,250 | |

Net loss | - | - | - | - | (1,943,674) | (1,943,674) | |

Balance, December 31, 1998 | 7,075,000 | 8,680,250 | 289,115 | - | (4,086,146) | 4,883,219 | |

Consolidation of shares on a two for one basis | (3,537,500) | - | - | - | - | - | |

Net loss | - | - | - | - | (2,378,063) | (2,378,063) | |

Balance, December 31, 1999 | 3,537,500 | 8,680,250 | 289,115 | - | (6,464,209) | 2,505,156 | |

Net loss | - | - | - | - | (4,718,044) | (4,718,044) | |

Balance, December 31, 2000 | 3,537,500 | 8,680,250 | 289,115 | - | (11,182,253) | (2,212,888) | |

Net earnings | - | - | - | - | 2,427,256 | 2,427,256 | |

Balance, December 31, 2001 | 3,537,500 | 8,680,250 | 289,115 | - | (8,754,997) | 214,368 | |

Shares issued: |

|

|

|

|

|

| |

Private placement | 4,824,500 | 2,133,786 | 246,839 | - | - | 2,380,625 | |

Exercise of share purchase warrants | 4,028,000 | 1,007,000 | - | - | - | 1,007,000 | |

Exercise of stock options | 32,000 | 12,800 | - | - | - | 12,800 | |

Financing shares issued | 31,250 | 35,000 | - | - | - | 35,000 | |

Acquisition of mineral property interest | 4,500,000 | 3,600,000 | - | - | - | 3,600,000 | |

Share issue costs | - | (544,260) | - | - | - | (544,260) | |

Stock based compensation | - | - | 27,000 | - | - | 27,000 | |

Net loss | - | - | - | - | (1,657,651) | (1,657,651) | |

Balance, December 31, 2002 | 16,953,250 | 14,924,576 | 562,954 | - | (10,412,648) | 5,074,882 | |

Shares issued: |

|

|

|

|

|

| |

Private placement | 700,000 | 638,838 | 201,162 | - | - | 840,000 | |

Exercise of share purchase warrants | 294,500 | 73,625 | - | - | - | 73,625 | |

Share issue costs | - | (19,932) | - | - | - | (19,932) | |

Stock based compensation | - | - | 531,000 | - | - | 531,000 | |

Net loss | - | - | - | - | (1,352,679) | (1,352,679) | |

Balance, December 31, 2003 | 17,947,750 | 15,617,107 | 1,295,116 |

| (11,765,327) | 5,146,896 | |

Shares issued: |

|

|

|

|

|

| |

Private placement | 2,234,400 | 2,122,269 | 175,407 | - | - | 2,297,676 | |

Exercise of share purchase warrants | 213,500 | 300,892 | (46,267) | - | - | 254,625 | |

Exercise of stock options | 250,000 | 157,000 | (27,000) | - | - | 130,000 | |

Share issue costs | - | (183,512) | - | - | - | (183,512) | |

Stock based compensation | - | - | 941,478 | - | - | 941,478 | |

Net loss | - | - | - | - | (2,994,702) | (2,994,702) | |

Balance, December 31, 2004 carried forward | 20,645,650 | 18,013,756 | 2,338,734 | - | (14,760,029) | 5,592,461 | |

The accompanying notes are an integral part of these consolidated interim financial statements.

5

MIDWAY GOLD CORP.

(An exploration stage company)

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY - CONTINUED

(Expressed in Canadian dollars) (unaudited)

The accompanying notes are an integral part of these consolidated interim financial statements.

6

MIDWAY GOLD CORP.

(An exploration stage company)

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES

(Expressed in Canadian dollars) (unaudited)

|

| Number of shares | Common stock | Additional paid-in capital | Accumulated other comprehensive loss | Accumulated deficit during the exploration stage | Total stockholders’ equity |

Balance, December 31, 2009, brought forward | 77,354,997 | $ 92,670,965 | $ 6,355,109 | $ - | $ (56,267,603) | $ 42,758,471 | |

Shares issued: |

|

|

|

|

|

| |

Private placement | 1,333,333 | 514,365 | 285,635 | - | - | 800,000 | |

Public offerings | 17,738,666 | 8,294,058 | 1,504,996 | - | - | 9,799,054 | |

Share issue costs | - | (1,431,027) | 212,109 | - | - | (1,218,918) | |

Exercise of share purchase warrants | 12,500 | 14,024 | (4,024) | - | - | 10,000 | |

Stock based compensation | - | - | 838,601 | - | - | 838,601 | |

Unrealized gain on investment | - | - | - | 13,125 | - | 13,125 | |

Net loss | - | - | - | - | (5,826,972) | (5,826,972) | |

Balance, December 31, 2010 | 96,439,496 | 100,062,385 | 9,192,426 | 13,125 | (62,094,575) | 47,173,361 | |

Shares issued: |

|

|

|

|

|

| |

Exercise of share purchase warrants | 5,215,750 | 7,202,486 | (668,484) | - | - | 6,534,002 | |

Share issue costs | - | (68,607) | - | - | - | (68,607) | |

Stock based compensation | - | - | 528,957 | - | - | 528,957 | |

Unrealized gain on investment | - | - | - | 43,750 | - | 43,750 | |

Net loss | - | - | - | - | (2,714,283) | (2,714,283) | |

Balance, March 31, 2011 | 101,655,246 | $107,196,264 | $ 9,052,899 | $ 56,875 | $ (64,808,858) | $ 51,497,180 | |

The accompanying notes are an integral part of these consolidated interim financial statements.

7

MIDWAY GOLD CORP.

(An exploration stage company)

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES

(Expressed in Canadian dollars) (unaudited)

| Three months ended March 31, 2011 | Three months ended March 31, 2010 |

|

Exploration costs incurred are summarized as follows: |

|

|

|

Midway project |

|

|

|

Assays and analysis | $ - | $ (12,412) | $ 316,043 |

Communication | - | - | 9,513 |

Drilling | (130) | 9,800 | 2,053,851 |

Engineering and consulting | 42,223 | 41,424 | 4,191,664 |

Environmental | - | 5,152 | 233,698 |

Field office and supplies | 1,851 | 4,213 | 237,859 |

Legal | 877 | - | 148,964 |

Property maintenance and taxes | (33) | 42 | 444,373 |

Reclamation costs | - | 24 | 30,949 |

Reproduction and drafting | - | - | 20,803 |

Salaries and labor | 19,846 | 28,176 | 638,743 |

Travel, transportation and accommodation | 21,200 | 6,268 | 425,141 |

| 85,834 | 82,687 | 8,751,601 |

Spring Valley project |

|

|

|

Assays and analysis | - | - | 3,329,900 |

Communication | - | - | 10,307 |

Drilling | - | - | 10,261,359 |

Engineering and consulting | 18,852 | 1,307 | 2,460,131 |

Environmental | - | - | 300,445 |

Equipment rental | - | - | 64,651 |

Field office and supplies | 27 | 144 | 549,018 |

Legal | - | - | 364,780 |

Operator fee | - | - | 108,339 |

Property maintenance and taxes | (144) | - | 487,921 |

Reclamation costs | - | - | 30,746 |

Reproduction and drafting | - | - | 29,724 |

Salaries and labor | 8,538 | 3,183 | 1,249,824 |

Travel, transportation and accommodation | 8,517 | - | 860,622 |

| 35,790 | 4,634 | 20,107,767 |

Pan project |

|

|

|

Assays and analysis | 36,022 | 23,791 | 706,527 |

Drilling | 276,013 | - | 2,708,000 |

Engineering and consulting | 459,616 | 9,674 | 1,563,741 |

Environmental | 21,583 | 4,036 | 184,317 |

Field office and supplies | 39,342 | 1,663 | 216,662 |

Legal | 9,284 | - | 144,799 |

Property maintenance and taxes | 79,839 | 82 | 532,636 |

Reclamation costs | - | - | 70,569 |

Reproduction and drafting | 3,429 | - | 9,167 |

Salaries and labor | 138,829 | 6,187 | 1,275,292 |

Travel, transportation and accommodation | 40,743 | 2,306 | 318,084 |

| 1,104,700 | 47,739 | 7,729,794 |

Sub-total balance carried forward | $ 1,226,324 | $ 135,060 | $ 36,589,162 |

The accompanying notes are an integral part of these consolidated interim financial statements.

8

MIDWAY GOLD CORP.

(An exploration stage company)

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES - CONTINUED

(Expressed in Canadian dollars) (unaudited)

| Three months ended March 31, 2011 | Three months ended March 31, 2010 | Cumulative period from inception (May 14,1996) to March 31, 2011 |

Sub-total balance brought forward | $ 1,226,324 | $ 135,060 | $ 36,589,162 |

Burnt Canyon project |

|

|

|

Assays and analysis | - | - | 21,921 |

Engineering and consulting | - | - | 24,736 |

Environmental | - | - | 462 |

Field office and supplies | - | - | 1,695 |

Legal | - | - | 2,828 |

Property maintenance and taxes | - | - | 50,224 |

Reproduction and drafting | - | - | 5,036 |

Salaries and labor | - | - | 2,923 |

Travel, transportation and accommodation | - | - | 4,142 |

| - | - | 113,967 |

Thunder Mountain project |

|

|

|

Assays and analysis | - | - | 14,568 |

Drilling | - | - | 77,956 |

Engineering and consulting | - | - | 706 |

Environmental | - | - | 1,717 |

Field office and supplies | - | - | 1,041 |

Property maintenance and taxes | - | - | 18,905 |

Reclamation costs | - | - | (578) |

Salaries and labor | 191 | - | 2,238 |

Travel, transportation and accommodation | - | - | 55 |

| 191 | - | 116,608 |

Gold Rock project |

|

|

|

Assays and analysis | - | - | 59,994 |

Drilling | - | - | 106,901 |

Engineering and consulting | 12,358 | 2,262 | 175,723 |

Environmental | - | 359 | 893 |

Field office and supplies | 123 | 447 | 24,876 |

Legal | - | - | 12,447 |

Property maintenance and taxes | 633 | 27 | 306,670 |

Reclamation costs | 8,990 | - | 10,594 |

Reproduction and drafting | 108 | - | 447 |

Salaries and labor | 11,541 | 199 | 49,860 |

Travel, transportation and accommodation | 1,075 | 197 | 33,953 |

| 34,828 | 3,491 | 782,358 |

Golden Eagle project |

|

|

|

Assays and analysis | - | - | 21,690 |

Drilling | - | - | 3,638 |

Engineering and consulting | 112,915 | 7,426 | 288,480 |

Field office and supplies | - | (84) | 2,185 |

Legal | - | - | 19,569 |

Property maintenance and taxes | - | - | 11,627 |

Salaries and labor | 4,463 | 319 | 4,844 |

Travel, transportation and accommodation | 1,398 | - | 16,176 |

| 118,776 | 7,661 | 368,209 |

Sub-total balance carried forward | $ 1,380,119 | $ 146,212 | $ 37,970,304 |

The accompanying notes are an integral part of these consolidated interim financial statements.

9

MIDWAY GOLD CORP.

(An exploration stage company)

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES - CONTINUED

(Expressed in Canadian dollars) (unaudited)

| Three months ended March 31, 2011 | Three months ended March 31, 2010 | Cumulative period from inception (May 14,1996) to March 31, 2011 |

Sub-total balance brought forward | $ 1,380,119 | $ 146,212 | $ 37,970,304 |

Abandoned properties |

|

|

|

Acquisition costs and option payments | - | - | 40,340 |

Assays and analysis | - | - | 53,791 |

Communications | - | - | 119,734 |

Drilling | - | - | 848,921 |

Engineering and consulting | - | - | 3,272,236 |

Equipment rental | - | - | 348,377 |

Field office and supplies | - | - | 306,551 |

Foreign exchange gain | - | - | (38,134) |

Freight | - | - | 234,956 |

Geological and geophysical | - | - | 63,481 |

Interest on convertible loans | - | - | 1,288,897 |

Legal and accounting | - | - | 462,534 |

Marketing | - | - | 91,917 |

Mining costs | - | - | 693,985 |

Processing and laboratory supplies | - | - | 941,335 |

Property maintenance and taxes | - | - | 447,610 |

Reclamation costs | - | - | 38,710 |

Recoveries | - | - | (40,000) |

Reproduction and drafting | - | - | 1,179 |

Security | - | - | 350,584 |

Salaries and labor | - | - | 19,203 |

Travel, transportation and accommodation | - | - | 429,499 |

Utilities and water | - | - | 59,425 |

| - | - | 10,035,131 |

Property investigations |

|

|

|

Assays and analysis | - | 1,714 | 174,119 |

Drilling | - | - | 169,129 |

Engineering and consulting | - | - | 210,391 |

Environmental | - | - | 22,761 |

Field office and supplies | (97) | 501 | 19,935 |

Legal | - | - | 10,952 |

Property maintenance and taxes | - | - | 123,230 |

Reclamation costs | - | - | 2,930 |

Reproduction and drafting | - | - | 4,942 |

Salaries and labor | 4,481 | - | 8,155 |

Travel, transportation and accommodation | 719 | 49 | 114,181 |

| 5,103 | 2,264 | 860,725 |

| $ 1,385,222 | $ 148,476 | $ 48,866,160 |

The accompanying notes are an integral part of these consolidated interim financial statements.

10

1.

Nature and continuance of operations

Midway Gold Corp. (the “Company” or “Midway”) was incorporated on May 14, 1996 under the laws of the Province of British Columbia and its principal business activities are the sourcing, exploration and development of mineral properties.

The Company has not generated revenues from operations. These consolidated financial statements are prepared on a going concern basis which assumes that the Company will be able to realize its assets and discharge its liabilities in the normal course of business in the foreseeable future. Management believes that the Company’s cash on hand at March 31, 2011 is sufficient to finance exploration activities and operations through the next twelve months. Additionally, as of April 21, 2011 (note 14), the Company is authorized by the Canadian Securities Exchanges and the Securities Exchange Commission to offer up to US$60,000,000 of the Company’s common shares. The Company’s ability to continue on a going concern basis beyond the next twelve months depends on its ability to successfully raise additional financing for the substantial capital expenditures required to achieve planned principal operations. While the Company has been successful in the past in obtaining financing, there is no assurance that it will be able to obtain adequate financing in the future or that such financing will be on terms acceptable to the Company.

These financial statements do not reflect adjustments that would be necessary if the going concern assumption were not appropriate.

2.

Significant accounting policies and change in accounting policy

These consolidated interim financial statements for the Company have been prepared in accordance with United States generally accepted accounting principles (“US GAAP”). They do not include all of the information and disclosures required by US GAAP for annual financial statements. In the opinion of management, all adjustments considered necessary for fair presentation have been included in these financial statements. The interim consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements including the notes thereto for the year ended December 31, 2010 which may be found on the Company’s profile on SEDAR and EDGAR.

The accounting policies followed by the Company are set out in note 2 to the audited consolidated financial statements for the year ended December 31, 2010 and have been consistently followed in the preparation of these consolidated interim financial statements, except as follows:

Recently adopted accounting policies

On April 16, 2010, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update ASU 2010-13 Compensation - Stock Compensation (Topic 718: Effect of Denominating the Exercise Price of a Share-Based Payment Award in the Currency of the Market in which the Underlying Equity Security Trades. This ASU is effective for interim and annual reporting periods for fiscal years beginning on or after December 15, 2010. This ASU added to or amends sections of Accounting Codification Standards (“ACS”) Topic 718. These amendments and additions impact the accounting treatment as follows:

a)

A share-based payment award with an exercise price denominated in the currency of a market in which a substantial portion of the entity’s equity securities trades shall not be considered to contain a condition that is not a market, performance, or service condition and, therefore shall not be classified as a liability if it otherwise qualifies for equity classification.

b)

If an award is indexed to a factor in addition the entity’s share price. If that factor is not a market, performance, or service condition (e.g., indexed to the market price of a commodity such as gold), the award shall be classified as a liability.

In accordance with ACS Topic 718, as amended, at March 31, 2011 the fair value of the Company’s share-based compensation is considered a component of equity. Adopting this ASU had no impact on the Company.

11

3.

Fair Value Measurements

Fair value measurement establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. These tiers include: Level 1, defined as observable inputs such as quoted prices in active markets; Level 2, defined as inputs other than quoted prices in active markets that are either directly or indirectly observable; and Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions.

The valuation of investments in marketable securities include available for sale securities. The Company’s Level 1 assets include common shares available for sale with no trading restrictions as determined using a market approach based upon unadjusted quoted prices for identical assets in an active market. Level 1 assets also include warrants that are considered derivatives and are marked to market each reporting period based upon unadjusted quoted prices for identical assets in active markets. The Company’s Level 2 assets include common shares with trading restrictions that will be removed within one year of the financial period reporting date as determined using a market approach and based upon quoted prices for identical assets in an active market adjusted by a discount to market comparable to the discount allowed by the TSX Venture Exchange for private placements. The Company’s Level 3 assets include warrants with trading restrictions that will be removed within one year of the financial reporting date as determined using the Black-Scholes valuation model and a discount to market comparable to the discount allowed by the TSX Venture Exchange for private placements.

The determination of fair value for financial reporting purposes is at March 31, 2011 utilizing the applicable framework is as follows:

Financial Instrument | Quoted prices in active markets for identical assets | Significant other observable inputs | Significant unobservable inputs | Total at March 31, 2011 |

| Level 1 | Level 2 | Level 3 |

|

Available-for-sale securities | $ 100,000 | $ - | $ -

| $ 100,000 |

Derivatives | - | 30,353 |

| 30,353 |

Total | $ 100,000 | $ 30,353 | $ - | $ 130,353 |

Financial instruments measured at fair value as at December 31, 2010 were as follows:

Financial Instrument | Quoted prices in active markets for identical assets | Significant other observable inputs | Significant unobservable inputs | Total 2010 |

| Level 1 | Level 2 | Level 3 |

|

Available-for-sale securities | $ - | $ 56,250 | $ - | $ 56,250 |

Derivatives | - | - | 24,437 | 24,437 |

Total | $ - | $ 56,250 | $ 24,437 | $ 80,687 |

Warrant liability | $ - |

$1,562,544 | $ - | $1,562,544 |

12

4.

Investments

As consideration of certain area of interest obligations of NV Gold Corporation (“NVX”) that apply to the Roberts Gold project, the Company was issued 250,000 common shares of NVX and 250,000 common share purchase warrants (the “NVX Warrants”) on October 26, 2010. The NVX Warrants entitle the Company to purchase one common share of NVX at an exercise price of $0.40 until October 26, 2012. If the volume weighted average price of the common shares of NVX exceed $0.60 for twenty consecutive trading days, NVX may notify the Company in writing that the NVX Warrants will expire 15 trading days from receipt of such notice unless exercised by the Company before such date. The common shares and the common shares issued pursuant to the exercise of any NVX Warrants were restricted from trading until February 27, 2011. Accordingly the NVX common shares were categorized as Level 2 and a discount of 25% was applied to the quoted market value on the date of receipt and on December 31, 2010. Subsequent to February 27, 2011, the date trading restrictions were removed, the NVX common shares were reclassified to Level 1 and the 25% discount was not applied to the March 31, 2011 fair value.

The NVX Warrants are considered derivatives. At December 31, 2010 they were categorized as Level 3 and were fair valued using the Black-Scholes valuation model and a discount of 25% applied to their fair value on the date of receipt and on December 31, 2010. The following assumptions were used on the date of receipt: expected life of 2 years; volatility of 100%; no dividend yield; and a risk free interest rate of 1.42%. The NVX Warrants will be revalued each reporting period with gains or losses recorded in the Statement of Operations. The following assumptions were used on December 31, 2010: expected life of 1.8 years; volatility of 100%; no dividend yield; and a risk free interest rate of 1.66%. With the trading restriction expiration on February 27, 2011 the warrants were reclassified from Level 3 to Level 2. The following Black-Scholes valuation assumptions were used on March 31, 2011: expected life of 1.56 years; volatility of 101%; no dividend yield; and a risk free interest rate of 1.72%.

| March 31, 2011 | ||||

| Number of shares or warrants | Cost | Accumulated unrealized gains (losses) | Fair Value | |

Available for sale - common shares | 250,000 | $ 43,125 | $ 56,875 | $ 100,000 | |

Warrants | 250,000 | 16,995 | 13,358 | 30,353 | |

Total investments |

| $ 60,120 | $ 70,233 | $ 130,353 | |

During the three month period ended March 31, 2011 the Company recorded an unrealized gain on the common shares of NVX of $43,750 in accumulated other comprehensive income and an unrealized gain on the NVX Warrants of $5,916 in the Statement of Operations for the difference in the fair value at March 31, 2011 as compared to December 31, 2010.

5.

Equipment

| March 31, 2011 |

| December 31, 2010 | ||||

| Cost | Accumulated depreciation | Net book value |

| Cost | Accumulated depreciation | Net book |

Computer equipment | $ 320,146 | $ 247,844 | $ 72,302 |

| $ 288,420 | $ 242,726 | $ 45,694 |

Leasehold improvements | 2,754 | 24 | 2,730 |

|

|

|

|

Office equipment | 102,141 | 33,400 | 68,741 |

| 79,049 | 30,859 | 48,190 |

Field equipment | 71,748 | 45,011 | 26,737 |

| 68,953 | 44,679 | 24,274 |

Trucks | 269,396 | 72,264 | 197,132 |

| 138,853 | 59,787 | 79,066 |

| $ 766,185 | $ 398,543 | $ 367,642 |

| $ 575,275 | $ 378,051 | $ 197,224 |

13

6.

Mineral properties

Details on the Company’s mineral properties are found in note 6 to the audited consolidated financial statements for the year ended December 31, 2010.

| December 31, 2010 | Additions | Written off | March 31, 2011 |

Midway | $ 7,036,314 | $ - | $ - | $ 7,036,314 |

Spring Valley | 5,664,517 | - | - | 5,664,517 |

Pan | 33,807,508 | 213,156 | - | 34,020,664 |

Gold Rock | 628,324 | 233,645 | - | 861,696 |

Burnt Canyon | 178,785 | - | - | 178,785 |

Golden Eagle | 2,255,613 | - | - | 2,255,613 |

| $ 49,571,061 | $ 446,801 | $ - | $ 50,017,862 |

(a)

Midway property, Nye County, Nevada

On July 1, 2009, and amended on October 14, 2009, the Company agreed with the Town of Tonopah (“Tonopah”) and Lumos & Associates (“Lumos”) to fund a study to identify the best alternatives which maximize the treatment and dewatering at a possible mine at the Midway Project for municipal use and/or re-injection, to minimize the need for redundant facilities and over costs to benefit the Company and Tonopah. Tonopah contracted with Lumos to prepare a Preliminary Engineering Report to identify the best alternatives to which the Company agreed to fund up to US$105,120 of which the full amount has been paid or accrued by December 31, 2010 (December 31, 2009, $79,120 (US$74,294)).

(b)

Spring Valley property, Nevada

At March 31, 2011 the Company had an amounts receivable of $21,638 (US$22,316) (December 31, 2010 $62,769 (US$63,110)) for recoverable salaries and expenses, from Barrick Gold Exploration Inc. pursuant to the Spring Valley exploration option and joint venture agreement, which was subsequently paid.

7.

Reclamation deposit

The Company is required to post bonds with the Bureau of Land Management (“BLM”) for reclamation of planned mineral exploration programs work associated with the Company’s mineral properties located in the United States. For the Company’s mineral properties that are being actively explored under funding arrangement agreements, the funding partners are responsible for bonding for the surface disturbance created by the exploration programs funded by each of them on those projects.

At March 31, 2011 the Company had posted a total of $268,783(US$277,210) reclamation deposits compared to $260,087 (US$261,499) at December 31, 2010.

8.

Share capital

(a)

The Company’s authorized to issue an unlimited number of common shares.

(b)

Share issuances

(i)

During 1996, the Company issued 420,000 common shares at $0.25 per share by way of a non-brokered private placement for proceeds of $98,722 net of issue costs. In addition the Company issued 280,000 flow-through common shares at $0.25 per share by way of a non-brokered private placement for proceeds of $70,000.

(ii)

During 1997, the Company completed an initial public offering of 2,000,000 common shares at $0.35 per share for proceeds of $590,570, net of issue costs. In connection with this offering, the Company’s agent received a selling commission of 10% or $0.035 per share and was issued 25,000 shares as a corporate finance fee.

14

(iii)

During 1997, the Company issued 1,000,000 units at $2.50 per unit by way of a private placement for proceeds of $2,253,793 net of issue costs. Each unit consisted of one common share and one non-transferable share purchase to purchase one additional common share at $3.00 per share until February 14, 1998. The proceeds of the financing of $2,500,000 were allocated $2,178,761 as to the common shares and $321,239 as to the warrants. During 1998 100,000 of the warrants were exercised and 900,000 expired. In connection with this private placement, the Company’s agent received a selling commission of 7.5% of the proceeds of the units sold or $0.1875 per unit and a corporate finance fee of $15,000.

(iv)

During 1997, the Company issued 750,000 common shares as performance shares for proceeds of $7,500 that were held in escrow in accordance with the rules of the regulatory authorities of British Columbia. The shares were released 25% in each of 1998, 1999, 2000 and 2001.

(v)

During 1997, pursuant to an equity participation agreement to acquire an interest in Gemstone Mining Inc. (“Gemstone”), a Utah Corporation that by agreement the creditors of Gemstone were issued 1,000,000 units of the Company on conversion of a debt of $2,065,500 (US$1,500,000). Each unit consisted of one common share and one non-transferable share purchase to purchase one additional common share at US$2.00 per share that was immediately exercised for proceeds of $2,803,205 (US$2,000,000). The first one-third tranche of a conditional finders’ fee was satisfied by the issue of 150,000 common shares in connection with the acquisition of Gemstone.

(vi)

During 1998, the Company issued 100,000 common shares pursuant to the exercise of share purchase warrants for proceeds of $300,000.

(vii)

During 1998, the Company issued 200,000 common shares in connection with the acquisition of Gemstone as well as the second tranche of finder’s fee in connection with that acquisition. The Company’s option to acquire Gemstone expired on January 31, 1998 and the remaining one-third tranche were not issued.

(viii)

During 1999, the Company consolidated its issued share capital on a two old for one new basis and changed its name from Neary Resources Corporation to Red Emerald Resource Corp.

(ix)

During 2002, the Company issued 3,500,000 units at $0.25 per unit for proceeds of $875,000 by way of a short form offering document under the policies of the TSX Venture Exchange. Each unit consists of one common share and one common share purchase warrant that entitled the holder to purchase one additional common share at $0.25 per share until October 19, 2002. The Company also issued 150,000 common shares as a finance fee in connection with this offering, and issued the agent 875,000 share purchase warrants exercisable at $0.25 per share until April 19, 2004. During 2002 the Company issued 1,134,500 special warrants at $1.25 per special warrant for proceeds of $1,418,125. Each Special Warrant automatically converted to a unit comprising one common share and one share purchase warrant that entitled the holder to purchase one additional common share at

$1.55 per share until November 6, 2003. The proceeds of the financing of $1,418,125 were allocated on a relative fair value basis as $1,171,286 to common shares and $246,839 as to the warrants. During 2003 all of the warrants expired unexercised. In connection with the offering the Company paid the agent a 10% commission totaling $113,450, issued the agent 40,000 common shares as a finance fee in connection with this offering, and issued the agent 170,175 share purchase warrant exercisable at $1.55 per share until July 5, 2003.

(x)

During 2002, the Company issued 4,028,000 common shares pursuant to the exercise of share purchase warrants for proceeds of $1,007,000.

(xi)

During 2002, the Company issued 32,000 common shares pursuant to the exercise of stock options for proceeds of $12,800.

(xii)

During 2002, the Company issued 31,250 common shares as additional consideration to a director who loaned the Company $780,000 bearing interest at 12% per annum. The loan and interest was repaid prior to December 31, 2002.

15

(xiii)

During 2002, the Company acquired Rex Exploration Corp. (“Rex”) in exchange for 4,500,000 common shares of the Company.

(xiv)

During 2003, the Company issued 700,000 units at $1.20 per unit for proceeds of $840,000 by way of a non-brokered private placement. Each unit consists of one common share and one share purchase warrant that entitled the holder to purchase one additional common share at $1.50 until May 25, 2004. The proceeds of the financing of $840,000 were allocated $638,838 as to common shares and $201,162 as to the warrants. During 2004 161,000 of the warrants were exercised and 539,000 expired. Share issue expenses were $19,932.

(xv)

During 2003, the Company issued 294,500 common shares pursuant to the exercise of share purchase warrants for proceeds of $73,625.

(xvi)

In January 2004, the Company issued 400,000 units at $2.00 per unit for proceeds of $800,000 by way of a private placement. Each unit consisted of one common share and one non-transferable share purchase warrant that entitled the holder to purchase one additional common share at $2.35 per share for a six month period. The proceeds of the financing of $800,000 were allocated on a relative fair value basis as $624,593 to common shares and $175,407 as to the warrants. All of the warrants expired unexercised in 2004. The Company issued 40,000 common shares as a finder’s fee for this private placement.

(xvii)

In August 2004, the Company issued 1,020,000 units at $0.75 per unit for proceeds of $765,000 by way of a private placement. Each unit consisted of one common share and one non-transferable share purchase warrant that entitled the holder to purchase one additional common share at $0.80 per share until August 25, 2005. All of the warrants were subsequently exercised. The Company issued 55,650 common shares as a finder’s fee for this private placement.

(xviii)

In December 2004, the Company issued 700,000 units at $0.85 per unit for proceeds of $595,000 by way of a private placement. Each unit consisted of one common share and one non-transferable share purchase warrant that entitled the holder to purchase one additional common share at $1.00 per share until December 20, 2005. All of the warrants were subsequently exercised. The Company issued 18,750 common shares as a finder’s fee for this private placement.

(xix)

In February 2005, the Company issued 2,500,000 units at $0.85 per unit for proceeds of $2,125,000 by way of a private placement. Each unit consisted of one common share and one non-transferable share purchase warrant that entitled the holder to purchase one additional common share at $1.00 per share until February 16, 2006. The proceeds of the financing of $2,125,000 were allocated on a relative fair value basis as $1,598,457 to common shares and $526,543 as to warrants. There were 23,000 warrants exercised in fiscal year 2005 and the balance exercised in fiscal year 2006. The Company issued 75,800 common shares for $64,430 and paid $69,700 in cash as a finder’s fee and incurred $26,709 in additional issue costs for this private placement.

(xx)

In July 2005, the Company issued 1,000,000 units at $1.15 per unit for proceeds of $1,150,000 by way of a private placement. Each unit consisted of one common share and one-half non-transferable share purchase warrant that entitled the holder to purchase one additional common share at $1.15 per share until July 27, 2006. The proceeds of the financing of $1,150,000 were allocated on a relative fair value basis as $995,193 to common shares and $154,807 as to warrants. All of the warrants were exercised in fiscal year 2006. The Company incurred $15,560 in issue costs.

(xxi)

In August 2005, the Company issued 500,000 units at $1.40 per unit for proceeds of $700,000 by way of a private placement. Each unit consisted of one common share and one-half nontransferable share purchase warrant that entitled the holder to purchase one additional common share at $1.45 per share until August 22, 2006. The proceeds of the financing of $700,000 were allocated on a relative fair value basis as $608,015 to common shares and $91,985 as to warrants. All of the warrants were exercised in fiscal year 2006. The Company incurred $8,261 in issue costs.

16

(xxii)

In January 2006, the Company issued 40,000 common shares at a value of $88,000 pursuant to a purchase and sale agreement to purchase mining claims for the Spring Valley project.

(xxiii)

In May 2006, the Company issued 3,725,000 units at $1.80 per unit for proceeds of $6,705,000 by way of a private placement. Each unit consisted of one common share and one-half nontransferable share purchase warrant. Each whole warrant entitled the holder to purchase one additional common share at $2.70 per share until May 16, 2007. The proceeds of the financing of $6,705,000 were allocated on a relative fair value basis as $5,998,846 to common shares and $706,154 as to warrants. The Company incurred $65,216 in issue costs. By May 16, 2007 1,725,000 of the warrants were exercised and 137,500 expired unexercised.

(xxiv)

In November 2006, the Company issued 2,000,000 units at $2.50 per unit for proceeds of $5,000,000 by way of a private placement. Each unit consisted of one common share and one-half nontransferable share purchase warrant. Each whole warrant entitles the holder to purchase one additional common share at $3.00 per share until November 10, 2007. The proceeds of the financing of $2,000,000 were allocated on a relative fair value basis as $1,761,509 to common shares and $238,491 as to warrants. The Company paid $88,750 in finders’ fees and incurred $94,546 in issue costs for this private placement. By November 10, 2007 908,782 of the warrants were exercised and 91,218 expired unexercised.

(xxv)

On April 16, 2007, the Company issued 7,764,109 common shares at a value of $25,000,431, 308,000 stock options at a value of $608,020 and 870,323 share purchase warrants at a value of $1,420,054 in connection with the acquisition of Pan-Nevada Gold Corporation. By December 31, 2007, 154,000 of the stock options had been exercised and 761,823 share purchase warrants had been exercised. By December 31, 2008 the remaining 108,500 share purchase warrants were exercised and 84,000 stock options had been exercised. On October 11, 2008 the final 70,000 stock options expired not exercised.

(xxvi)

On August 24, 2007, the Company issued 2,000,000 common shares at $2.70 per common share for proceeds of $5,400,000 by way of a private placement. The Company incurred $28,000 in share issue costs.

(xxvii)

On March 31, 2008, the Company issued 30,000 common shares at a value of $88,500 pursuant to a lease assignment of mining claims for the Gold Rock project. The Company incurred $1,489 in share issue costs.

(xxviii)

On June 12, 2008, the Company issued 1,421,500 common shares at $2.00 per common share for proceeds of $2,843,000 by way of a private placement. The Company incurred $75,371 in share issue costs.

(xxix)

On August 1, 2008 the Company issued 600,000 common shares at US$2.50 per common share for proceeds of $1,537,950 (US$1,500,000) by way of a private placement with Kinross Gold USA Inc. The Company incurred $39,450 in share issue costs.

(xxx)

On November 12, 2008 the Company issued 12,500,000 units at $0.22 per unit for proceeds of $2,750,000 by way of a private placement. Each unit consisted of one common share and one share purchase warrant. Each warrant entitles the holder to purchase one additional common share at $0.28 per share until May 12, 2009. The proceeds of the financing of $2,750,000 were allocated on a relative fair value basis as $1,793,491 to common shares and $956,509 as to warrants. The Company incurred $23,395 in issue costs for this private placement. In the year ended December 31, 2009 all of the 12,500,000 warrants were exercised for proceeds of $3,500,000.

(xxxi)

In addition to the 84,000 stock options reported exercised in paragraph xxv, during 2008, the Company issued a further 395,000 common shares pursuant to the exercise of stock options for proceeds of $613,250.

17

(xxxii)

During 2009, the Company issued 33,333 common shares pursuant to the exercise of stock options for proceeds of $21,651.

(xxxiii)

On April 9, 2010, the Company issued 1,333,000 units at $0.60 per unit for proceeds of $800,000 by way of a private placement. Each unit consisted of one common share and one share purchase warrant. Each warrant entitles the holder to purchase one additional common share until October 9, 2011 at an exercise price as follows: $0.70 if exercised on or before October 9, 2010; $0.80 if exercised after October 9, 2010 but on or before April 9, 2011; and $0.90 if exercised after April 9, 2011 but on or before October 9, 2011. The proceeds of the financing of $800,000 were allocated on a relative fair value basis as $514,365 to common shares and $285,635 as to warrants. The Company incurred $95,529 in issue costs for this private placement.

(xxxiv)

On June 16, 2010, the Company issued 11,078,666 units at $0.60 per unit for proceeds of $6,647,199 by way of a brokered offering in Canada and a non-brokered offering in the United States. Each unit consisted of one common share and one-half share purchase warrant. Each whole warrant entitles the holder to purchase one additional common share until June 16, 2012 at an exercise price of $0.80. The proceeds of the financing of $6,647,199 were allocated on a relative fair value basis as $5,142,202 to common shares and $1,504,997 as to warrants. The Company issued 658,840 agent’s warrants which entitle the holder to purchase one common share until June 16, 2010 at an exercise price of $0.80. These warrants have been recorded at the estimated fair value at the issue date of $212,109. The fair value of warrants was determined using a risk free interest rate of 1.82%, an expected volatility of 131%, an expected life of 2 years, and zero dividends for a fair value per warrant of $0.32. In addition, the Company paid finders’ fees in the amount of $395,304 and incurred other cash share issue costs of $307,553.

(xxxv)

In September 2010, the Company issued 12,500 common shares pursuant to the exercise of share purchase warrants for proceeds of $10,000.

(xxxvi)

In November 2010, the Company closed a public offering and the Company issued 6,660,000 units at US$0.60 per unit, each unit comprising one common share and one half of one non-transferable common share purchase warrant. Each whole warrant entitles the holder to purchase one common share of the Company at a price of US$0.90 per share until November 12, 2012, subject to acceleration provisions. The proceeds of the financing of $4,070,725 were allocated first to the fair value of the warrants at $918,870 with the residual amount of $3,151,855 to common shares.

At December 31, 2010 the fair value of warrants was $1,562,544.

The Company incurred $176,288 in issue costs and paid $244,244 to the agent as commission for this public offering. On February 9, 2011, the Company gave notice to the Warrant holders that it accelerated the expiry date of the warrants to March 14, 2011 and by that date 2,650,000 warrants were exercised and 680,000 warrants expired unexercised.

(xxxvii)

In the three month period ended March 31, 2011 the company issued 5,215,750 common shares pursuant to the exercise of share purchase warrants. Of the 5,215,750 shares issued, 2,650,000 shares were pursuant to the exercise of the warrants exercised which had an accelerated expiry date of March 14, 2011 and a fair value at December 31, 2010 of $1,562,544 as mentioned in xxxvi above. Proceeds received on the 5,215,750 common shares issued totalled $4,379,432.

(c)

Stock options

The Company has an incentive share option plan (the “Plan”) that allows it to grant incentive stock options to its officers, directors, employees and consultants. The Plan was amended on May 12, 2008 to add an appendix called the 2008 Stock Incentive Plan for United States Resident Employees (the “U.S. Plan”) to supplement and be a part of the Plan. The purpose of the U.S. Plan is to enable the Company to grant Incentive Stock Options, as that term is used in Section 422 of the Internal Revenue Code of 1986, as amended from time to time, and any regulations promulgated thereunder to qualifying employees who are citizens or residents of the United States of America. This does not change the aggregate number of options that can be granted pursuant to the Plan.

18

The purpose of the Plan permits the Company’s directors to grant incentive stock options for the purchase of shares of the Company to persons in consideration for services. Stock options must be non-transferable and the aggregate number of shares that may be reserved for issuance pursuant to stock options may not exceed 10% of the issued shares of the Company at the time of granting and may not exceed 5% to any individual (maximum of 2% to any consultant). The exercise price of stock options is determined by the board of directors of the Company at the time of grant and may not be less than the closing price of the Company’s shares on the trading day immediately preceding the date on which the option is granted and publicly announced, less an applicable discount, and may not otherwise be less than $0.10 per share. Options have a maximum term of ten years and terminate 90 days following the termination of the optionee’s employment, except in the case of death or disability, in which case they terminate one year after the event.

The continuity of stock options is as follows:

Expiry date | Exercise Price Per Share | Balance December 31, 2010 | Granted | Forfeited | Expired/ Cancelled | Balance March 31, 2011 |

|

|

|

|

|

|

|

March 9, 2011 | $2.00 | 75,000 | - | - | (75,000) | - |

May 4, 2011 | $2.00 | 30,000 | - | - | - | 30,000 |

June 15, 2011 | $2.25 | 235,000 | - | - | - | 235,000 |

August 30, 2011 | $2.63 | 40,000 | - | - | - | 40,000 |

November 30, 2011 | $2.70 | 140,000 | - | - | - | 140,000 |

January 23, 2012 | $3.00 | 25,000 | - | - | - | 25,000 |

July 31, 2012 | $2.71 | 500,000 | - | - | - | 500,000 |

October 30, 2012 | $3.36 | 50,000 | - | - | - | 50,000 |

December 6, 2012 | $3.32 | 15,000 | - | - | - | 15,000 |

April 13, 2014 | $2.04 | 400,000 | - | - | - | 400,000 |

July 16, 2013 | $2.00 | 100,000 | - | - | - | 100,000 |

January 7, 2014 | $0.56 | 1,295,000 | - | - | - | 1,295,000 |

September 9, 2014 | $0.86 | 1,000,000 | - | - | - | 1,000,000 |

May 17, 2015 | $0.71 | 500,000 | - | - | - | 500,000 |

June 16, 2015 | $0.58 | 1,705,000 | - | - | - | 1,705,000 |

October 22, 2015 | $0.61 | 350,000 | - | - | - | 350,000 |

January 13, 2016 | $0.95 | - | 815,000 | - | - | 815,000 |

|

| 6,460,000 | 815,000 | - | (75,000) | 7,200,000 |

Weighted average exercise price |

| $ 1.10 | $ 0.95 | - |

(75,000) |

$ 1.07 |

At March 31, 2011 all but 1,046,667 of the 7,200,000 stock options outstanding were exercisable. The intrinsic value of vested stock options outstanding at March 31, 2011 was $5,100,417. Intrinsic value for vested stock options is calculated on the difference between the exercise prices of the underlying options and the quoted price of $1.80 for our common stock as of March 31, 2011.

The Company recorded stock-based compensation expense, net of forfeitures, of $528,957 in the three months ended March 31, 2011 (March 31, 2010 - $11,029) for options vesting in that period of which $504,766 (March 31, 2010 - $(376)) was included in salaries and benefits in the statement of operations and $24,191 (March 31, 2010 - $11,405) was included in salaries and labor in the schedule of mineral exploration expenditures. There is a balance of $248,014 that will be recognized in fiscal 2011, fiscal 2012 and fiscal 2013 as the options vest.

19

d)

Share purchase warrants:

The continuity of share purchase warrants is as follows:

Expiry date | Exercise price per share | Balance December 31, 2010 | Issued | Exercised |

Expired | Balance March 31, 2011 | |

| US$ | Cdn$ |

|

|

|

|

|

October 9, 2011* |

| $0.80 | 1,333,333 | - | (960,000) | - | 373,333 |

June 16, 2012 |

| $0.80 | 6,185,673 | - | (1,605,750) | - | 4,579,923 |

November 12, 2012 | $0.90 |

| 3,330,000 | - | (2,650,000) | (680,000) | - |

|

|

| 10,849,006 | - | (5,215,750) | (680,000) | 4,953,256 |

|

|

| $ 0.83 | - | $ 0.86 | US$ 0.90 | $ 0.80 |

*

Each warrant entitles the holder to purchase one additional common share until October 9, 2011 at an exercise price as follows: $0.70 if exercised on or before October 9, 2010; $0.80 if exercised after October 9, 2010 but on or before April 9, 2011; and $0.90 if exercised after April 9, 2011 but on or before October 9, 2011.

9.

Contingency

On January 27, 2011 the Company was delivered a summons that it is being sued in the state of Nevada by Redcor

Drilling, Inc. (“Redcor”) for non-payment of the balance of a drilling invoice that is under dispute by the Company. Redcor is demanding the Company pay US$241,477.24 together with interest at the rate of 4% per annum from September 18, 2010. On March 10, 2011, the Company responded to the summons and intends to continue to protest payment of the amount demanded on the basis of non-performance of services. The Company has recorded the full amount as an accrued liability without accruing interest as the amount of the liability can be estimated and it is likely the Company may be required to pay some portion of the disputed amount.

Redcor placed a mechanic’s lien on a portion of the Pan project that the Company leases from Newark Valley Mining Corp. Subsequently, the Company posted a surety bond for the disputed amount, thereby releasing the mechanic’s lien.

10.

Commitments

The Company has obligations under operating leases for its corporate offices in Englewood, Colorado and office equipment until 2015 as follows. Future minimum lease payments for non-cancellable with initial lease terms in excess of one year are included.

Fiscal Year | Operating Leases |

2011 | $ 30,966 |

2012 | 49,552 |

2013 | 48,034 |

2014 | 4,555 |

Total | $ 133,107 |

11.

Related party transactions

The Company paid consulting fees of $25,875 (2010 - $22,500) to a company controlled by the Chief Financial Officer of the Company for accounting and corporate compliance services. That Chief Financial Officer resigned effective March 18, 2011, but, remained as Corporate Secretary at March 31, 2011.

Included in accounts payable and accrued liabilities at March 31, 2011 is $7,272 (December 31, 2010 - $12,944) payable to the company referred to in this note and other directors and officers.

These transactions are in the normal course of operations and are measured at the exchange amount, which is the amount of consideration established and agreed to by the related parties.

20

12.

Financial instruments

In all material respects, the carrying amounts for the Company’s cash and cash equivalents, amounts receivable, accounts payable and accrued liabilities approximate their fair values due to the short term nature of these instruments. Investments at March 31, 2011 and December 31, 2010 are recorded at fair values (note 4).

13.

Supplemental disclosure with respect to cash flows

The significant non-cash transactions for the three month period ended March 31, 2011 consisted of the transfer of $668,484 for the fair value of share purchase warrants exercised from paid in additional capital to share capital; the transfer of $2,154,570 for the fair value of share purchase warrants exercised or expired from warrant liability (note 8) to share capital.

The significant non-cash transactions for the three month period ended March 31, 2010 were nil.

14.

Subsequent events

Subsequent to March 31, 2011 the Company received confirmation that on April 21, 2011, the Canadian Securities Commissions accepted the Company’s Short Form Prospectus, which along with the Company’s S-3 Shelf Registration Statement under the Securities Act of 1933, as amended, declared effective by the SEC on February 14, 2011 (jointly the “2011 Prospectus”), allows the Company to offer and sell, from time to time over a twenty-five month period, up to US$60,000,000 of the Company’s common shares, without par value, with or without warrants to purchase common shares, or any combination thereof in one or more transactions under the 2011 Prospectus. The Company may also offer under this 2011 Prospectus any common shares issuable upon the exercise of warrants.

21

Item 2.

Management's Discussion and Analysis of Financial Condition and Results of Operations.

You should read the following discussion and analysis of our financial condition and results of operations together with our financial statements and related notes appearing elsewhere in this Quarterly Report filed on Form 10-Q. This discussion and analysis contains forward-looking statements that involve risks, uncertainties and assumptions. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of many factors, including, but not limited to, those set forth under the heading “Risk Factors and Uncertainties” in our Form 10-K filed with the SEC on March 17, 2011, and elsewhere in this report.

This discussion and analysis should be read in conjunction with the accompanying unaudited interim consolidated financial statements and related notes. The discussion and analysis of the financial condition and results of operations are based upon the unaudited interim consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires Midway to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of any contingent liabilities at the financial statement date and reported amounts of revenue and expenses during the reporting period. On an on-going basis Midway reviews its estimates and assumptions. The estimates were based on historical experience and other assumptions that Midway believes to be reasonable under the circumstances. Actual results are likely to differ from those estimates under different assumptions or conditions, but Midway does not believe such differences will materially affect our financial position or results of operations. Critical accounting policies, the policies Midway believes are most important to the presentation of its financial statements and require the most difficult, subjective and complex judgments, are outlined below in “Critical Accounting Policies,” and have not changed significantly.

Cautionary Note Regarding Forward-Looking Statements

In addition, certain statements made in this report may constitute “forward-looking statements”. These forward-looking statements involve known or unknown risks, uncertainties and other factors that may cause the actual results, performance, or achievements of Midway to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Except for historical information, the matters set forth herein, which are forward-looking statements, involve certain risks and uncertainties that could cause actual results to differ. Potential risks and uncertainties include, but are not limited to, unexpected changes in business and economic conditions; significant increases or decreases in gold prices; changes in interest and currency exchange rates; unanticipated grade changes; metallurgy, processing, access, availability of materials, equipment, supplies and water; determination of reserves; results of current and future exploration activities; results of pending and future feasibility studies; joint venture relationships; political or economic instability, either globally or in the countries in which we operate; local and community impacts and issues; timing of receipt of government approvals; accidents and labor disputes; environmental costs and risks; competitive factors, including competition for property acquisitions; and availability of external financing at reasonable rates or at all. Forward- looking statements can be identified by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continues” or the negative of these terms or other comparable terminology. Although Midway believes that the expectations reflected in the forward-looking statements are reasonable, it cannot guarantee future results, levels of activity, performance or achievements. Forward-looking statements are made based on management’s beliefs, estimates, and opinions on the date the statements are made, and Midway undertakes no obligation to update such forward-looking statements if these beliefs, estimates, and opinions should change, except as required by law.

Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates

The mineral estimates in this Form 10-Q have been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in United States Securities and Exchange Commission (“SEC”) Industry Guide 7 under the United States Securities Act of 1993, as amended. Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

22

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.

Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this Quarterly Report on Form 10-Q and the documents incorporated by reference herein contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Overview

Company Overview

Midway is an exploration stage company engaged in the acquisition, exploration, and, if warranted, development of gold and silver mineral properties in North America. Our mineral properties are located in Nevada and Washington. The Midway, Spring Valley, Pan, Gold Rock, and Golden Eagle gold properties are exploratory stage projects and have identified gold mineralization and the Thunder Mountain and Burnt Canyon projects are earlier stage gold and silver exploration projects.

Business Strategy and Development

The Company is currently working towards transitioning itself from an exploration company to a gold production company with plans to advance the Pan gold deposit located in White Pine County, Nevada through to production by as early as 2013.

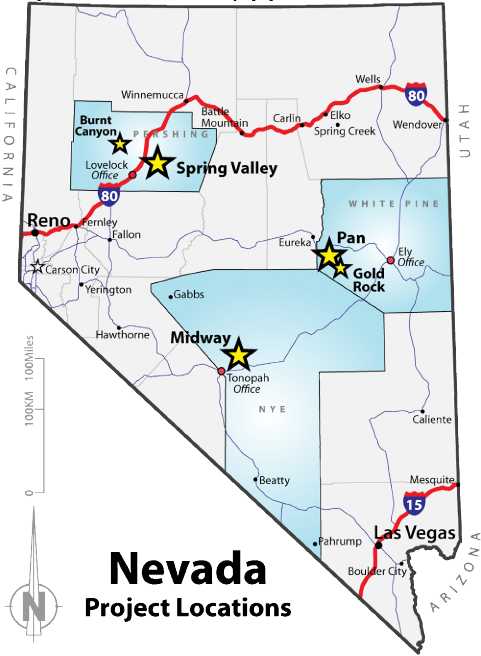

23

The map below shows the location of Midway’s properties located in Nevada, USA.

24

Highlights for the first quarter 2011 and up to May 10, 2011:

·

Spring Valley project - fourth quarter 2010 drilling results were received from Barrick and a new resource estimate was received

·

Pan project - a positive Prefeasibility Study was completed, an agreement for water rights was executed, and a reverse circulation drilling program commenced

·

Midway project - a cooperative agreement with the Town of Tonopah was signed, an initial underground mineable resource estimate was completed, and a core drilling program commenced

·

Gold Rock project - a technical report reviewing historic data was completed in advance of a planned 2011 work program

Activities on Midway’s properties in the first quarter ended March 31, 2011 and up to May 10, 2011 the date of this Quarterly Report filed on Form 10-Q, are described in further detail below.

Spring Valley Project, Pershing County, Nevada

Barrick conducted and funded exploration in 2010 on the Spring Valley project to meet its minimum expenditure requirement of US$5,000,000. Barrick has the exclusive right to earn a 60% interest in the Spring Valley project by spending US$30,000,000 on the property over five years. Barrick may increase its interest by 10% (70% total) by spending an additional US$8,000,000 in the year immediately after vesting at 60%. At the Company’s election, Barrick may also earn an additional 5% (75% total) by carrying the Company to a production decision and arranging financing for the Company’s share of mine construction expenses with the carrying and financing costs plus interest to be recouped by Barrick once production has been established.

Barrick forwarded results from fourth quarter 2010 drilling. The Company reported these results, including an extension of the mineralized strike length by about 1.8 km to the south-southwest of the previously known gold resource. A step out drill hole intersected strong, relatively shallow Spring Valley-type mineralization in similar structures and host rocks as seen in the existing gold resource. The drill hole is south of property acquired in December of 2010 and is believed to indicate very strong exploration potential for the new, untested parcels.

Barrick has informed Midway that it intends to conduct and fund the minimum required program of US$7,000,000 in 2011 for a cumulative amount of US$16,000,000 by December 31, 2011. Drilling in 2011 is expected to focus on expanding the resource and evaluating satellite targets, particularly within the recently acquired land south of the existing resource.

The Company engaged an independent engineer, Gustavson Associates, LLC of Lakewood, Colorado to review the drilling results and provide a new resource update that incorporated all Barrick drilling to date, resulting in the conversion of 2.16 million ounces of gold to the Measured and Indicated categories, consisting of 0.93 million ounces in the Measured category and 1.23 million ounces in the Indicated category at a cut-off grade of 0.14 grams per tonne (g/t). The new drilling also produced an additional Inferred resource of 1.97 million ounces of gold at the same cut-off grade. The Measured resource is contained within 59.0 million tonnes grading 0.49 g/t, the Indicated resource is contained within 85.8 million tonnes grading 0.45 g/t and the Inferred resource is contained within 103.9 million tonnes grading 0.59 g/t.

Measured and Indicated resources are estimated pursuant to Canadian industry standards. See “Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates” above. The Spring Valley project is without known reserves, as defined under SEC Guide 7, and the proposed program for the property is exploratory in nature.

Barrick is funding the majority of the ongoing costs of this project. In the three months ended March 31, 2011, the Company incurred $27,515 primarily to fund engineering and legal costs incurred on the portion of the Seymork land that falls outside of the Barrick agreement area of interest.

25

Pan Project, White Pine County, Nevada

The Pan property is located at the northern end of the Pancake mountain range in western White Pine County, Nevada, approximately 22 miles southeast of Eureka, Nevada, and 50 miles west of Ely, Nevada. The Pan deposit is a Carlin-style, disseminated gold deposit, located along the Battle Mountain-Eureka Trend.

Mine planning and engineering design were on-going through the first quarter. Initial results were reported as part of a positive Prefeasibility Study and additional work is underway for a Feasibility Study scheduled for completion in the first half of 2011. Environmental studies are continuing in support of permitting including a plan of operations and reclamation plan to be submitted to management agencies.