Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - EXELON GENERATION CO LLC | d8k.htm |

| EX-99.2 - PRESS RELEASE - EXELON GENERATION CO LLC | dex992.htm |

Deutsche Bank Alternative Energy, Utilities and

Power Conference

William A. Von Hoene, Jr., EVP Finance & Legal

May 12, 2011

Exhibit 99.1 |

Cautionary

Statements Regarding Forward-Looking Information

2

Except for the historical information contained herein, certain of the matters discussed in this

communication constitute “forward-looking statements” within the meaning of the

Securities Act of 1933 and the Securities Exchange Act of 1934, both as amended by the Private

Securities Litigation Reform Act of 1995. Words such as “may,” “will,” “anticipate,”

“estimate,” “expect,” “project,” “intend,” “plan,”

“believe,” “target,” “forecast,” and words and terms of similar substance

used in connection with any discussion of future plans, actions, or events identify

forward-looking statements. These forward-looking statements include, but are not

limited to, statements regarding benefits of the proposed merger, integration plans and

expected synergies, the expected timing of completion of the transaction, anticipated future financial

and operating performance and results, including estimates for growth. These statements are based on

the current expectations of management of Exelon Corporation (Exelon) and Constellation Energy

Group, Inc. (Constellation), as applicable. There are a number of risks and uncertainties that

could cause actual results to differ materially from the forward-looking statements

included in this communication. For example, (1) the companies may be unable to obtain

shareholder approvals required for the merger; (2) the companies may be unable to obtain regulatory

approvals required for the merger, or required regulatory approvals may delay the merger or

result in the imposition of conditions that could have a material adverse effect on the

combined company or cause the companies to abandon the merger; (3) conditions to the closing of

the merger may not be satisfied; (4) an unsolicited offer of another company to acquire assets or capital

stock of Exelon or Constellation could interfere with the merger; (5) problems may arise in

successfully integrating the businesses of the companies, which may result in the combined

company not operating as effectively and efficiently as expected; (6) the combined company may

be unable to achieve cost-cutting synergies or it may take longer than expected to achieve

those synergies; (7) the merger may involve unexpected costs, unexpected liabilities or unexpected delays, or

the effects of purchase accounting may be different from the companies’ expectations; (8) the

credit ratings of the combined company or its subsidiaries may be different from what the

companies expect; (9) the businesses of the companies may suffer as a result of uncertainty

surrounding the merger; |

Cautionary

Statements Regarding Forward-Looking Information

(Continued) 3

(10) the companies may not realize the values expected to be obtained for properties expected or

required to be divested; (11) the industry may be subject to future regulatory or legislative

actions that could adversely affect the companies; and (12) the companies may be adversely

affected by other economic, business, and/or competitive factors. Other unknown or unpredictable

factors could also have material adverse effects on future results, performance or achievements of the

combined company. Discussions of some of these other important factors and assumptions are contained

in Exelon’s and Constellation’s respective filings with the Securities and Exchange

Commission (SEC), and available at the SEC’s website at www.sec.gov, including: (1)

Exelon’s 2010 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7.

Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c)

ITEM 8. Financial Statements and Supplementary Data: Note 18; (2) Exelon’s Quarterly

Report on Form 10-Q for the quarterly period ended March 31, 2011 in (a) Part II, Other

Information, ITEM 1A. Risk Factors, (b) Part I, Financial Information, ITEM 2.

Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c)

Part I, Financial Information, ITEM 1. Financial Statements: Note 12; (3) Constellation’s

2010 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s

Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8.

Financial Statements and Supplementary Data: Note 12; and (4) Constellation’s Quarterly Report on

Form 10-Q for the quarterly period ended March 31, 2011 in (a) Part II, Other Information, ITEM

5.Other Information, (b) Part I, Financial Information, ITEM 2. Management’s Discussion

and Analysis of Financial Condition and Results of Operations and (c) Part I, Financial

Information, ITEM 1. Financial Statements: Notes to Consolidated Financial Statements,

Commitments and Contingencies. These risks, as well as other risks associated with the proposed merger,

will be more fully discussed in the joint proxy statement/prospectus that will be included in the

Registration Statement on Form S-4 that Exelon will file with the SEC in connection with

the proposed merger. In light of these risks, uncertainties, assumptions and factors, the

forward-looking events discussed in this communication may not occur. Readers are cautioned

not to place undue reliance on these forward-looking statements, which speak only as of the date of this

communication. Neither Exelon nor Constellation undertake any obligation to publicly release any

revision to its forward- looking statements to reflect events or circumstances after the

date of this communication. |

Additional

Information and Where to Find It 4

This communication does not constitute an offer to sell or the solicitation of an offer to buy any

securities, or a solicitation of any vote or approval, nor shall there be any sale of

securities in any jurisdiction in which such offer, solicitation or sale would be unlawful

prior to registration or qualification under the securities laws of any such jurisdiction. Exelon intends to

file with the SEC a registration statement on Form S-4 that will include a joint proxy

statement/prospectus and other relevant documents to be mailed by Exelon and Constellation to

their respective security holders in connection with the proposed merger of Exelon and

Constellation. WE URGE INVESTORS AND SECURITY HOLDERS TO READ THE JOINT PROXY

STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS WHEN THEY BECOME AVAILABLE, BECAUSE THEY

WILL CONTAIN IMPORTANT INFORMATION about Exelon, Constellation and the proposed merger.

Investors and security holders will be able to obtain these materials (when they are available) and

other documents filed with the SEC free of charge at the SEC's website, www.sec.gov. In

addition, a copy of the joint proxy statement/prospectus (when it becomes available) may be

obtained free of charge from Exelon Corporation, Investor Relations, 10 South Dearborn Street,

P.O. Box 805398, Chicago, Illinois 60680-5398, or from Constellation Energy Group, Inc.,

Investor Relations, 100 Constellation Way, Suite 600C, Baltimore, MD 21202. Investors and security

holders may also read and copy any reports, statements and other information filed by Exelon, or

Constellation, with the SEC, at the SEC public reference room at 100 F Street, N.E.,

Washington, D.C. 20549. Please call the SEC at 1-800- SEC-0330 or visit the

SEC’s website for further information on its public reference room.

Participants in the Merger Solicitation Exelon, Constellation, and their respective directors, executive officers and certain other members of

management and employees may be deemed to be participants in the solicitation of proxies in

respect of the proposed transaction. Information regarding Exelon’s directors and

executive officers is available in its proxy statement filed with the SEC by Exelon on March

24, 2011 in connection with its 2011 annual meeting of shareholders, and information regarding

Constellation’s directors and executive officers is available in its proxy statement filed with

the SEC by Constellation on April 15, 2011 in connection with its 2011 annual meeting of

shareholders. Other information regarding the participants in the proxy solicitation and a

description of their direct and indirect interests, by security holdings or otherwise, will be

contained in the joint proxy statement/prospectus and other relevant materials to be filed with the

SEC when they become available.

|

Transaction

Overview 100%

stock

–

0.930 shares of EXC for each share of CEG

Upfront transaction

premium

of

18.1%

(1)

$2.10 per share Exelon dividend maintained

Expect to close in early 1Q 2012

Exelon and Constellation shareholder approvals in 3Q 2011

Regulatory approvals including FERC, DOJ, MD, NY, TX

Executive Chairman: Mayo Shattuck

President and CEO: Chris Crane

Board of Directors: 16 total (12 from Exelon, 4 from Constellation)

Exelon Corporation

78% Exelon shareholders

22% Constellation shareholders

Corporate headquarters: Chicago, IL

Constellation headquarters: Baltimore, MD

No change to utilities’

headquarters

Significant employee presence maintained in IL, PA and MD

Company Name

Consideration

Pro Forma

Ownership

Headquarters

Governance

Approvals &

Timing

(1) Based on the 30-day average Exelon and Constellation closing stock

prices as of April 27, 2011. 5 |

Creating Value

Through a Strategic Merger Delivers financial benefits to both sets of

shareholders Increases scale and scope of the business across the value

chain Matches the industry’s premier clean merchant generating fleet

with the leading retail and wholesale customer platform

Diversifies the generation portfolio

Continued upside to power market recovery

Maintains a strong regulated earnings profile with large urban utilities

6

Combining Exelon’s generation fleet and Constellation’s customer-facing

businesses creates a strong platform for growth and delivers benefits to

investors and customers |

Exelon

Transaction Rationale Increases

geographic

diversity

of

generation,

load

and

customers

in

competitive

markets

Shared

Commitment to

Competitive

Markets

Enhances

Scalable Growth

Platform

Creates

Shareholder

Value

Expands a valuable channel to market our generation

Enhances margins in the competitive portfolio

Diversifies portfolio across the value chain

EPS break-even in 2012 and accretive by +5% in 2013

Maintains strong

credit profile and financial discipline

Maintains earnings upside to future environmental regulations and power market

recovery

Adds stability to earnings and cash flow

Adds mix of clean generation to the portfolio

Clean

Generation Fleet

This transaction meets all of our M&A criteria and can be executed

7 |

This

Combination Is Good for Maryland Maintains employee presence and platform for

growth in Maryland –

Exelon’s Power Team will be combined with Constellation’s wholesale and

retail business

under

the

Constellation

brand

and

will

be

headquartered

in Baltimore

–

Constellation and Exelon’s renewable energy business headquartered in

Baltimore –

BGE maintains independent operations headquartered in Baltimore

–

No involuntary merger-related job reductions at BGE for two years after

close Supports Maryland’s economic development and clean energy

infrastructure –

$10 million to spur development of electric vehicle infrastructure

–

$4 million to support EmPower Maryland Energy Efficiency Act

–

25 MWs of renewable energy development in Maryland

–

Charitable contributions maintained for at least 10 years

Provides direct benefits to BGE customers

–

$5 million

provided

for

Maryland’s

Electric

Universal

Service

Program

(EUSP)

–

Over $110 million to BGE residential customers from $100 one-time rate

credit 8

We

will

bring

direct

benefits

to

the

State

of

Maryland,

the

City

of

Baltimore

and

BGE

customers. Total investment in excess of $250 million.

|

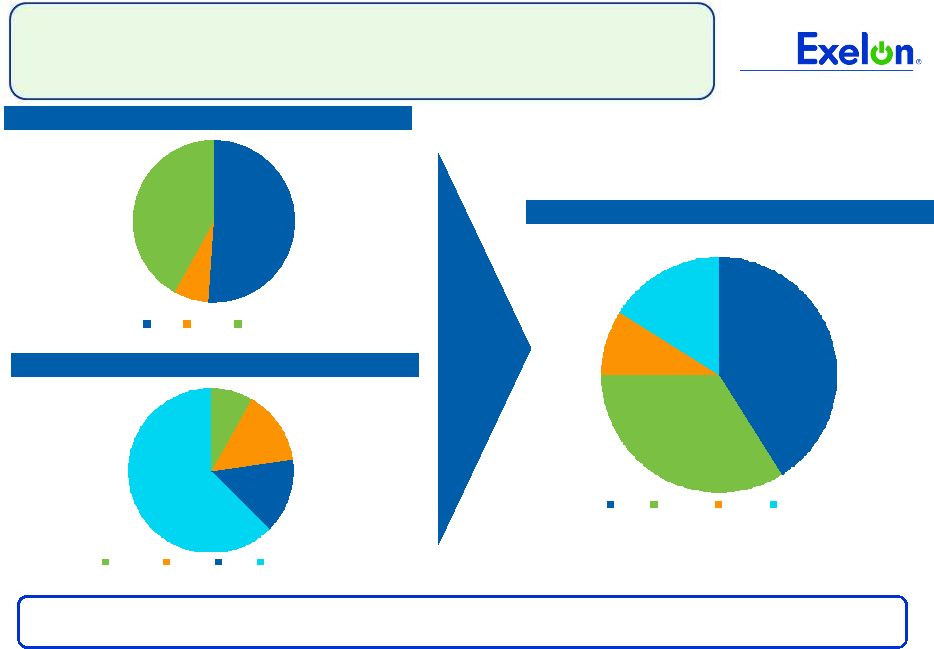

5.8

0.5

9.1

Exelon

Constellation

23.2

27.8

MISO (TWh)

South

(1)

(TWh)

ISO-NE & NY ISO

(2)

(TWh)

West (TWh)

Load

Generation

Exelon

Constellation

4.8

27.1

9.1

Exelon

Constellation

Exelon

Constellation

2.4

0.4

0.4

Exelon

Constellation

Load

Generation

Generation

Load

Load

Generation

Load

Generation

6.3

9.1

101.5

179.1

27.8

23.2

27.1

13.9

2.4

0.8

Portfolio Matches Generation with Load in

Key Competitive Markets

(1)

Represents load and generation in ERCOT, SERC and SPP.

(2)

Constellation load includes ~0.7TWh of load served in Ontario

Note: Data for Exelon and Constellation represents expected generation and load for

2011 as of 12/31/10. Exelon load includes ComEd Swap, load sold through

affiliates, fixed and indexed load sales and load sold through POLR auctions.

Constellation load includes load sold through affiliates, fixed and indexed load

sales and load sold through POLR auctions. The combination establishes

an industry-leading platform with regional diversification of the

generation fleet 9

147.3

31.8

42.8

58.7

PJM (TWh) |

Transaction

Economics Are Attractive for Both Companies

EPS break-even in 2012 and accretive by +5% in 2013

Free cash flow accretive beginning in 2012

Run-rate synergies of ~$260 million

–

Total costs to achieve of ~$500 million

–

Synergies primarily from corporate consolidation and power marketing platform

integration

Lower consolidated liquidity requirements, resulting in cost savings

Investment-grade ratings and credit metrics

10 |

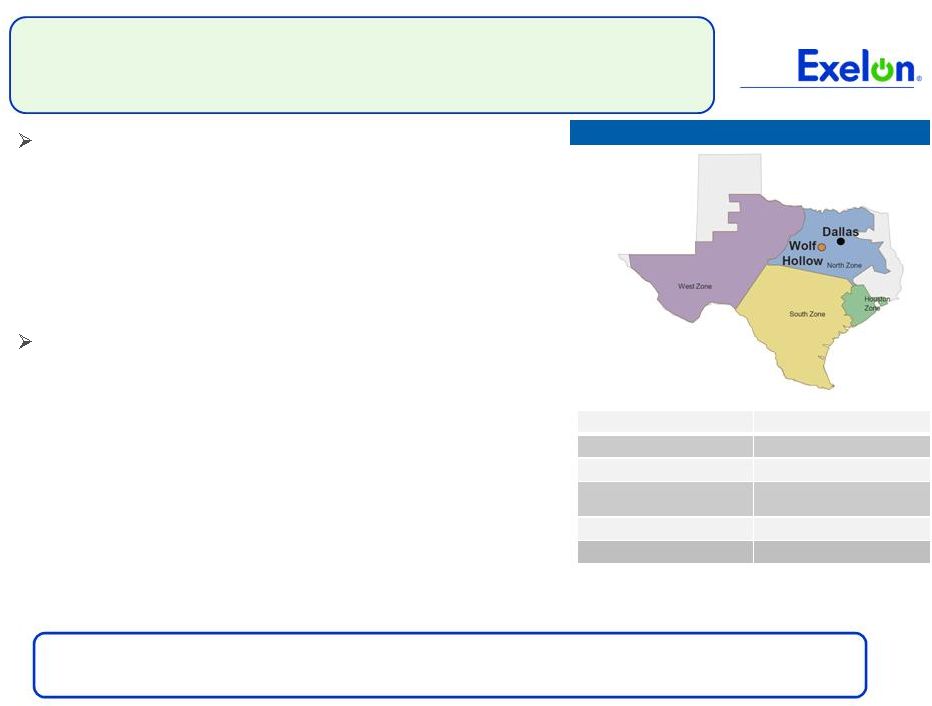

Wolf

Hollow Acquisition 11

Wolf Hollow Overview

Diversifies generation portfolio

•

Expands geographic and fuel characteristics

of fleet

•

Advances Exelon and Constellation merger

strategy of matching load with generation in

key competitive markets

Creates value for shareholders

•

Purchase price compares favorably to cost of

new build

•

Free cash flow accretive beginning in 2012;

earnings and credit neutral

•

Eliminates current above market purchase

power agreement (PPA) with Wolf Hollow

•

Enhances opportunity to benefit from future

market heat rate expansion in ERCOT

Transaction expected to close in Q3 2011

Location

Granbury, Texas

Commercial Operation Date

August 2003

Nominal Net Operating Capacity

720MW

Equipment Technology

2 Mitsubishi combined-cycle gas

turbines

Primary Fuel

Natural Gas

Secondary Fuel

None

ERCOT = Electric Reliability Council of Texas |

12

Appendix |

Coal

6%

Oil

8%

Gas

11%

Hydro

6%

Wind/Solar/Other

3%

Nuclear

67%

A Clean Generation Profile Creates Long-Term

Value in Competitive Markets

(1) Net of market mitigation assumed to be 2,648 MW.

(2)

Constellation generation includes Boston Generation acquisition (2,950 MW of natural

gas) and excludes Quail Run (~550 MW of natural gas). Constellation nuclear reflects 50.01%

interest in Constellation Energy Nuclear Group LLC.

Exelon Standalone

Total Generation: 25,619 MW

Constellation Standalone

(2)

Total Generation: 11,430 MW

Pro forma Company (Net of Mitigation)

(1)

Total Generation: 34,401 MW

Coal

24%

Nuclear

17%

Gas

52%

Wind/Solar/Other

2%

Hydro

3%

Oil

3%

Nuclear

55%

Coal

6%

Oil

7%

Gas

24%

Hydro

6%

Wind/Solar/

Other

2%

13

Combined company remains premier low-cost generator

|

16%

34%

41%

9%

RTO

EMAAC

MAAC

SWMAAC

8%

15%

15%

63%

EMAAC

MAAC

RTO

SWMAAC

42%

7%

51%

RTO

MAAC

EMAAC

Increased Regional Diversity in PJM:

Capacity Eligible for 2014/15 RPM Auction

(1)

Pro forma Company

4,390 MW

2,535 MW

9,230 MW

11,345 MW

Exelon Standalone

Constellation Standalone

8,700 MW

10,300 MW

1,500 MW

1,035 MW

4,390 MW

1,045 MW

530 MW

14

2014/15

RPM

auction

results

will

be

announced

on

May

13

,

2011

th

(1)

All generation values are approximate and not inclusive of wholesale transactions; all capacity values

are in installed capacity terms (summer ratings) located in the areas and adjusted for mid-year

PPA roll-offs.

|

15

Factors Influencing PJM RPM Capacity Auction

(Comparison of PY 14/15 and PY 13/14 Price Drivers)

Exelon

Price Impact

Cost of Environmental Upgrades

(1)

Higher Net CONE

(2)

Higher Net ACRs for Coal Units

(3)

Import Transmission Limits and Objectives

(muted impact on portfolio revenues due to regional diversification)

NJ CCGT Proposal / PJM Minimum Offer Price Rules

Peak Load

(4)

Demand Response Growth

2014/15 PJM Capacity Auction: Expected

Changes Since Planning Year 2013/14

Expect overall results to be similar to last year’s auction

N/A

(1) We expect generators to reflect cost of capital expenditures into their

cost based offers at the upcoming auction. (2) Cost of new entry

(CONE) increased by 7.6% (for RTO) and 5.3% to 6.5% (within Locational Deliverability Areas (LDAs)).

(3) Replacing 2007 net revenues with significantly lower 2010 revenues in the

Net ACR (avoidable cost rate) calculations for coal generators may increase offer caps for certain

coal generators

in

the

next

auction.

However,

some

coal

units

may

not

be

affected

due

to

high

net

revenues

compared

to

avoidable

costs.

(4) Peak load reduced by approx. 1% in RTO (excluding the impact from Duke

Ohio integration). Note:

RPM

=

Reliability

Pricing

Model;

CCGT

=

combined

cycle

gas

turbine |

16

16

16

ComEd Load Trends

Chicago

U.S.

Unemployment rate

(1)

8.5%

8.8%

2011 annualized growth in

gross domestic/metro product

(2)

2.5%

3.2% Note: C&I = Commercial &

Industrial Weather-Normalized Load Year-over-Year

Key Economic Indicators

Weather-Normalized Load

2010

1Q11 2011E

Average Customer Growth

0.2%

0.4%

0.5%

Average Use-Per-Customer

(1.4)%

(2.2)%

0.1%

Total Residential

(1.2)%

(1.8)% 0.5%

Small C&I

(0.6)%

0.6%

(0.3)%

Large C&I

2.6%

1.4%

(0.1)%

All Customer Classes

0.2%

(0.1)%

0.0%

(1)

Source: U.S. Dept. of Labor (March 2011) and Illinois

Department of Security (March 2011)

(2) Source: Global Insight February 2011

-6.0%

-3.0%

0.0%

3.0%

6.0%

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

-6.0%

-3.0%

0.0%

3.0%

6.0%

All Customer Classes

Large C&I

Residential

Gross Metro Product |

17

17

17

ComEd 2010 Rate Case Update

ComEd Reply Brief (2/23/11)

$343M increase requested

11.50% ROE / 47.28% equity ratio

Rate base $7,349M

2009 test year with pro forma plant additions through 6/30/11

ICC Staff Reply Brief Position (2/23/11)

$113M increase proposed

10.00% ROE / 47.11% equity ratio

Rate base $6,480M

Pro forma plant additions and depreciation reserve through 12/31/10

ALJ Proposed Order (4/1/11)

$152M increase proposed (after correcting ~$14M calculation error)

10.50% ROE / 47.28% equity ratio

Rate base $6,629M

Pro forma plant additions and depreciation reserve through 12/31/10 with very

limited exceptions (ICC Docket No. 10-0467)

Illinois Commerce Commission Final Order will be issued by May 31

|

Illinois Power Agency (IPA)

RFP Procurement

Note: Chart is for illustrative purposes only.

REC = Renewable Energy Credit; RFP = request for proposal

June 2011

June 2012

June 2013

June 2014

Financial Swap Agreement with ExGen

(ATC baseload energy only –

notional

quantity 3,000 MW)

Term

Fixed Price

1/1/11-12/31/11

$51.26/MWh

1/1/12-12/31/12

$52.37

1/1/13-5/31/13

$53.48

18

Financial Swap

2010 RFP

2011 RFP

2011 RFP

2011 RFP

2012 RFP

2012 RFP

2012 RFP

2013 RFP

2013 RFP

2014 RFP

ICC has approved Long Term REC Procurement held in November 2010

–

1.26 Million MWh of renewable resources annually beginning in June 2012 under 20

year contract –

8 winning suppliers with an average 2012-13 plan-year price of

$55.18/MWh Spring 2011 Procurement Plan

–

IPA Procurement Plan approved by the ICC

•

Standard Product bids due 5/16; ICC decision on 5/20

•

Annual REC bids due 5/18; ICC decision on 5/24

–

Provisions included:

•

Annual energy procurements over a three-year time frame

•

Target a 35%/35%/30% laddered procurement approach

•

No additional Energy Efficiency, Demand Response purchases

•

No additional long term contracts for renewables

•

No 10% overprocurement for summer peak energy

June 2015 |

19

PECO Load Trends

Philadelphia

U.S.

Unemployment rate

(1)

8.4%

8.8%

2010 annualized growth in

gross domestic/metro product

(2)

3.0%

3.2%

Note: C&I = Commercial & Industrial

Weather-Normalized Load Year-over-Year

Key Economic Indicators

Weather-Normalized Load

2010

1Q11 2011E

Average Customer Growth

0.3%

0.4%

0.4%

Average Use-Per-Customer

0.3%

0.2%

1.7%

Total Residential

0.5%

0.5% 2.1%

Small C&I

(1.9)%

(1.1)% 0.1%

Large C&I

0.8%

(2.7)% (1.6)%

All Customer Classes

0.1%

(1.1)% 0.1%

(1) Source: U.S Dept. of Labor data March 2011 -US

U.S Dept. of

Labor

prelim.

data

February

2011

-

Philadelphia

(2) Source: Global Insight February 2011

-6.0%

-3.0%

0.0%

3.0%

6.0%

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

-6.0%

-3.0%

0.0%

3.0%

6.0%

All Customer Classes

Large C&I

Residential

Gross Metro Product |

20

PECO Procurement Plan

(1)

See PECO Procurement website (http://www.pecoprocurement.com) for additional

details regarding PECO’s procurement plan and RFP results. (2)

For Large C&I customers who previously opted to participate in the 2011

fixed-priced full requirements product. (3)

Large C&I tranches which were not fully subscribed in the fall 2010

procurement Customer Class

Products

Residential

75% full requirements

20% block energy

5% energy only spot

Small Commercial

(peak demand <100 kW)

90% full requirements

10% full requirements spot

Medium Commercial

(peak demand >100 kW but

<= 500 kW)

85% full requirements

15% full requirements spot

Large Commercial &

Industrial

(peak

demand

>

500 kW)

Fixed-Priced Full

requirements

(2)

Hourly Full requirements

PECO

Procurement

Plan

(1)

Residential

80 MW of baseload (24x7) block energy product (for Jan-Dec 2012)

70 MW of Jun-Aug 2011 summer on-peak block energy product

40 MW of Dec 2011-Feb 2012 winter on-peak block energy product

Large

Commercial

and

Industrial

-

Hourly

36%

of

Hourly

Full

requirements

product

(Jun

2011-May

2012)

(3)

May

2,

2011

RFP

-

Fifth

in

a

series

of

nine procurements for the PUC-

approved Default Service Plan

Spring 2011 RFP was held on May 2, 2011, with results public 15 days thereafter

|

21

21

EPA Regulations Will Move Forward in 2011

2010

2011

2012

2013

2014

2015

2016

2017

2018

PJM RPM Auction

14/15

15/16

16/17

17/18

Hazardous Air

Pollutants

Criteria

Pollutants

Greenhouse

Gases

Coal

Combustion

By-Products

Cooling Water

Effluents

Develop Toxics Rule

Develop ICI

MACT

Pre Compliance Period

Compliance With Toxics Rule

Pre Compliance Period

Compliance With ICI MACT

Develop

Transport Rule

Compliance With Transport Rule

Interim CAIR

Develop O3

Transport

Rule (TR 2)

Estimated Compliance

Develop Criteria

NSPS revision

Compliance with Revised Criteria NSPS

Develop Revised

NAAQS

SIP provisions developed in response to revised NAAQS

(e.g., Ozone, PM2.5, SO2, NO2, NOx/SOx, CO)

Compliance with Federal GHG Reporting Rule

PSD/BACT and Title V Apply to GHG Emissions (PSD only for new and modified

sources) Develop GHG NSPS

Pre Compliance Period

Compliance With GHG NSPS

Develop Coal Combustion

By-Products Rule

Pre Compliance Period

Compliance With Federal CCB Regulations

Develop 316(b) Regulations

Pre Compliance Period

Phase In Of Compliance

Develop Effluent Regulations

Pre Compliance Period

Phase In Of

Compliance

Notes: RPM auctions take place annually in May.

For

definition

of

the

EPA

regulations

referred

to

on

this

slide,

please

see

the

EPA’s

Terms

of

Environment

(http://www.epa.gov/OCEPAterms/). |

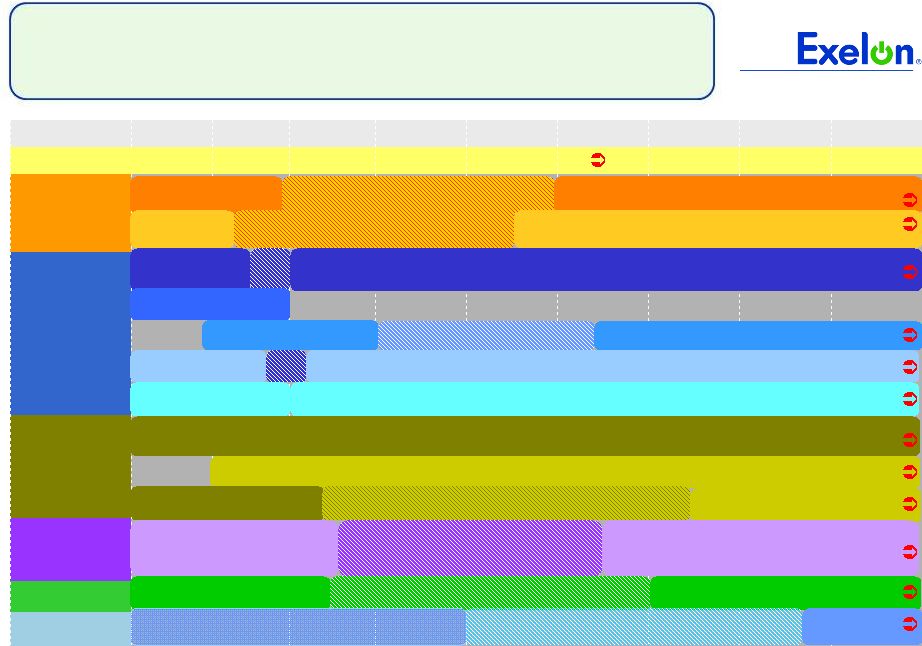

22

2011 Events of Interest

Q1

Q2

Q3

Q4

RPM Auction results

(5/13)

Illinois Power Agency

RFP (5/16)

ALJ Proposed Order

–

DST Rate Case

(4/1)

Procurement RFP

(bids accepted 5/2;

results by 5/17)

DST Rate Case Final

Order (by 5/31)

EPA Final Toxics

Rule (November)

Retirement of Cromby

1 & Eddystone 1 units

(5/31)

Proposed Toxics Rule

(3/16)

Procurement RFP

(bids due 9/19;

results by 10/19)

Retirement of

Cromby 2 unit

(12/31)

Proposed 316(b) EPA

Regulation (3/28)

For

definition

of

the

EPA

regulations

referred

to

on

this

slide, please see the EPA’s Terms of Environment

(http://www.epa.gov/OCEPAterms/). EPA Final Transport

Rule (June) |

23

Exelon Generation Hedging Disclosures

(as of March 31, 2011) |

24

24

Important Information

The following slides are intended to provide additional information regarding the hedging

program at Exelon Generation and to serve as an aid for the purposes of modeling Exelon

Generation’s gross margin (operating revenues less purchased power and fuel expense). The

information on the following slides is not intended to represent earnings guidance or a forecast

of future events. In fact, many of the factors that ultimately will determine Exelon

Generation’s actual gross margin are based upon highly variable market factors outside of

our control. The information on the following slides is as of March 31, 2011. We

update this information on a quarterly basis. Certain

information on the following slides is based upon an internal simulation model that incorporates

assumptions regarding future market conditions, including power and commodity prices, heat rates,

and demand conditions, in addition to operating performance and dispatch characteristics of our

generating fleet. Our simulation model and the assumptions therein are subject to

change. For example, actual market conditions and the dispatch profile of our generation

fleet in future periods will likely differ – and may differ significantly – from the

assumptions underlying the simulation results included in the slides. In addition, the

forward- looking information included in the following slides will likely change over time due

to continued refinement of our simulation model and changes in our views on future market

conditions. |

25

25

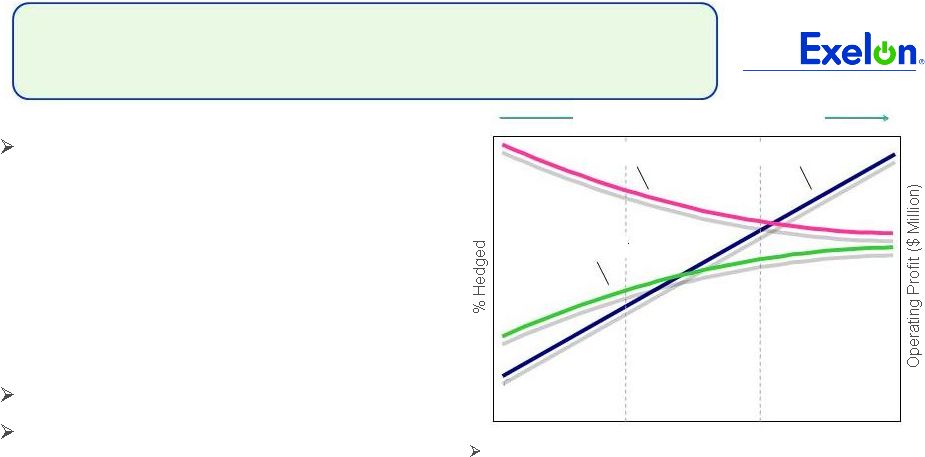

Portfolio Management Objective

Align Hedging Activities with Financial Commitments

Power Team utilizes several product types

and channels to market

•

Wholesale and retail sales

•

Block products

•

Load-following products

and load auctions

•

Put/call options

Exelon’s hedging program is designed to

protect the long-term value of our

generating fleet and maintain an

investment-grade balance sheet

•

Hedge enough commodity risk to meet future cash

requirements if prices drop

•

Consider: financing policy (credit rating objectives,

capital structure, liquidity); spending (capital and

O&M); shareholder value return policy

Consider market, credit, operational risk

Approach to managing volatility

•

Increase hedging as delivery approaches

•

Have enough supply to meet peak load

•

Purchase fossil fuels as power is sold

•

Choose hedging products based on generation

portfolio –

sell what we own

•

Heat rate options

•

Fuel products

•

Capacity

•

Renewable credits

% Hedged

High End of Profit

Low End of Profit

Open Generation

with LT Contracts

Portfolio

Optimization

Portfolio

Management

Portfolio Management Over Time |

26

26

Percentage of Expected

Generation Hedged

•

How many equivalent MW have been

hedged at forward market prices; all hedge

products used are converted to an

equivalent average MW volume

•

Takes ALL

hedges into account whether

they are power sales or financial products

Equivalent MWs Sold

Expected Generation

=

Our normal practice is to hedge commodity risk on a ratable basis

over the three years leading to the spot market

•

Carry operational length into spot market to manage forced outage and

load-following risks

•

By

using

the

appropriate

product

mix,

expected

generation

hedged

approaches the

mid-90s percentile as the delivery period approaches

•

Participation in larger procurement events, such as utility auctions, and some

flexibility in the timing of hedging may mean the hedge program is not

strictly ratable from quarter to quarter

Exelon Generation Hedging Program |

27

27

2011

2012

2013

Estimated

Open

Gross

Margin

($

millions)

(1)(2)

$5,250

$4,900

$5,500

Open gross margin assumes all expected generation is sold

at the Reference Prices listed below

Reference Prices

(1)

Henry Hub Natural Gas ($/MMBtu)

NI-Hub ATC Energy Price ($/MWh)

PJM-W ATC Energy Price ($/MWh)

ERCOT North ATC Spark Spread ($/MWh)

(3)

$4.47

$31.32

$44.23

$4.42

$5.06

$31.32

$46.19

$1.88

$5.41

$32.83

$48.10

$2.06

Exelon Generation Open Gross Margin and

Reference Prices

(1)

Based on March 31, 2011 market conditions.

(2)

Gross margin is defined as operating revenues less fuel expense and purchased power expense, excluding

the impact of decommissioning and other incidental revenues. Open gross margin is estimated

based upon an internal model that is developed by dispatching our expected generation to current market power and fossil

fuel prices. Open gross margin assumes there is no hedging in place other than fixed assumptions

for capacity cleared in the RPM auctions and uranium costs for nuclear power plants. Open

gross margin contains assumptions for other gross margin line items such as various ISO bill and ancillary revenues and costs and PPA

capacity revenues and payments. The estimation of open gross margin incorporates management

discretion and modeling assumptions that are subject to change.

(3)

ERCOT North ATC spark spread using Houston Ship Channel Gas, 7,200 heat rate, $2.50 variable

O&M. |

28

28

2011

2012

2013

Expected Generation

(GWh)

(1)

165,800

165,400

162,800

Midwest

99,000

97,800

96,100

Mid-Atlantic

56,300

57,200

56,400

South & West

10,500

10,400

10,300

Percentage of Expected Generation Hedged

(2)

93-96%

73-76%

38-41%

Midwest

93-96

75-78

35-38

Mid-Atlantic

94-97

72-75

42-45

South & West

76-79

59-62

40-43

Effective Realized Energy Price

($/MWh)

(3)

Midwest

$43.00

$41.00

$41.00

Mid-Atlantic

$56.50

$50.50

$50.50

South & West

$4.50

$0.00

($3.00)

Generation Profile

(1)

Expected

generation

represents

the

amount

of

energy

estimated

to

be

generated

or

purchased

through

owned

or

contracted

for

capacity.

Expected

generation

is

based

upon

a

simulated

dispatch

model

that

makes

assumptions

regarding

future

market

conditions,

which

are

calibrated

to

market

quotes

for

power,

fuel,

load

following

products,

and

options.

Expected

generation

assumes

12

refueling

outages

in

2011

and

10

refueling

outages

in

2012

and

2013

at

Exelon-operated

nuclear

plants

and

Salem.

Expected

generation

assumes

capacity

factors of 93.0%, 93.6% and 93.1% in 2011, 2012 and 2013 at Exelon-operated

nuclear plants. These estimates of expected generation in 2012 and 2013 do not represent guidance or a

forecast of future results as Exelon has not completed its planning or optimization

processes for those years. (2)

Percent of expected generation hedged is the amount of equivalent sales divided by

the expected generation. Includes all hedging products, such as wholesale and retail sales of power,

options, and swaps. Uses expected value on options. Reflects decision to

permanently retire Cromby Station and Eddystone Units 1&2 as of May 31, 2011.

(3)

Effective realized energy price is representative of an all-in hedged price, on

a per MWh basis, at which expected generation has been hedged. It is developed by considering the energy

revenues

and

costs

associated

with

our

hedges

and

by

considering

the

fossil

fuel

that

has

been

purchased

to

lock

in

margin.

It

excludes

uranium

costs

and

RPM

capacity

revenue,

but

includes

the

mark-to-market

value

of

capacity

contracted

at

prices

other

than

RPM

clearing

prices

including

our

load

obligations.

It

can

be

compared

with

the

reference

prices

used

to

calculate open gross margin in order to determine the mark-to-market value

of Exelon Generation's energy hedges. |

29

29

Gross Margin Sensitivities with Existing Hedges ($ millions)

(1)

Henry Hub Natural Gas

+ $1/MMBtu

-

$1/MMBtu

NI-Hub ATC Energy Price

+$5/MWH

-$5/MWH

PJM-W ATC Energy Price

+$5/MWH

-$5/MWH

Nuclear Capacity Factor

+1% / -1%

2011

$5

$(5)

$15

$(10)

$10

$(10)

+/-

$30

2012

$145

$(65)

$145

$(125)

$90

$(90)

+/-

$45

2013

$425

$(380)

$315

$(310)

$180

$(175)

+/-

$45

Exelon Generation Gross Margin Sensitivities

(with Existing Hedges)

(1)

Based on March 31, 2011 market conditions and hedged position. Gas price

sensitivities are based on an assumed gas-power relationship derived from an internal

model

that

is

updated

periodically.

Power prices sensitivities are derived by adjusting the power price assumption

while keeping all other prices inputs constant. Due to

correlation

of

the

various

assumptions,

the

hedged

gross

margin

impact

calculated

by

aggregating

individual

sensitivities

may

not

be

equal

to

the

hedged

gross

margin

impact calculated when correlations between the various assumptions are also

considered. |

30

30

95% case

5% case

$5,500

$7,100

$6,800

$6,200

Exelon Generation Gross Margin Upside / Risk

(with Existing Hedges)

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2011

2012

2013

$6,900

$4,900

(1)

Represents an approximate range of expected gross margin, taking into account hedges in place, between

the 5th and 95th percent confidence levels assuming all unhedged supply is sold into the spot

market. Approximate gross margin ranges are based upon an internal simulation model and are subject to change based upon market inputs, future

transactions and potential modeling changes. These ranges of approximate gross margin in 2012 and 2013

do not represent earnings guidance or a forecast of future results as Exelon has not completed

its planning or optimization processes for those years. The price distributions that generate this range are calibrated to market quotes for power, fuel,

load following products, and options as of March 31, 2011.

|

31

31

Midwest

Mid-Atlantic

South & West

Step 1

Start with fleetwide open gross margin

$5.25 billion

Step 2

Determine

the

mark-to-market

value

of

energy hedges

99,000GWh * 94% *

($43.00/MWh-$31.32MWh)

= $1.09 billion

56,300GWh * 95% *

($56.50/MWh-$44.23MWh)

= $0.66 billion

10,500GWh * 77% *

($4.50/MWh-$4.42/MWh)

= $0.00 billion

Step 3

Estimate

hedged

gross

margin

by

adding open gross margin to mark-to-

market value of energy hedges

Open gross

margin:

MTM value of energy

hedges:

Estimated hedged gross margin:

Illustrative Example

of Modeling Exelon Generation 2011 Gross Margin

(with Existing Hedges)

$5.25 billion

$1.09billion + $0.66billion + $0.00 billion

$7.00 billion |

32

35

40

45

50

55

60

65

70

75

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

32

32

20

25

30

35

40

45

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

50

55

60

65

70

75

80

85

90

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

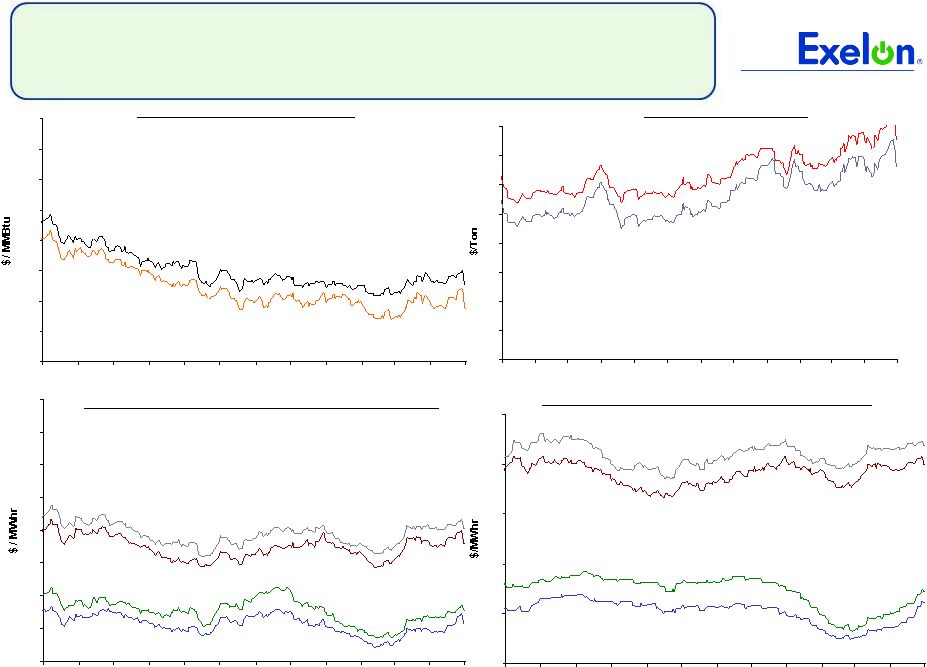

Market Price Snapshot

Forward NYMEX Natural Gas

PJM-West and Ni-Hub On-Peak Forward Prices

PJM-West and Ni-Hub Wrap Forward Prices

2012

$5.21

2013 $5.49

Rolling 12

months,

as

of

May

6th 2011.

Source:

OTC

quotes

and

electronic

trading

system.

Quotes

are

daily.

Forward NYMEX Coal

2012

$78.21

2013

$82.04

2012 Ni-Hub $40.60

2013 Ni-Hub

$42.66

2013 PJM-West $54.37

2012 PJM-West

$52.35

2012 Ni-Hub

$25.18

2013 Ni-Hub

$27.24

2013 PJM-West

$40.97

2012 PJM-West

$39.03 |

33

33

33

4.5

5.5

6.5

7.5

8.5

9.5

10.5

11.5

12.5

13.5

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

35

40

45

50

55

60

65

70

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

4/11

5/11

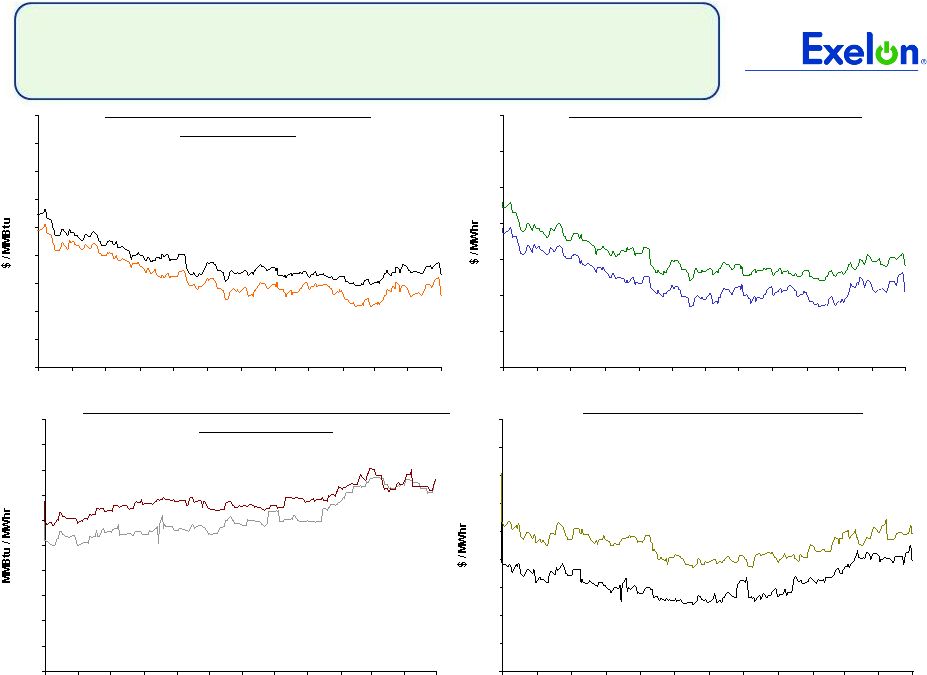

Market Price Snapshot

2013

9.36

2012

9.23

2012

$46.94

2013

$50.23

2012

$5.09

2013

$5.37

Houston Ship Channel Natural Gas

Forward Prices

ERCOT North On-Peak Forward Prices

ERCOT North On-Peak v. Houston Ship Channel

Implied Heat Rate

2012

$7.72

2013

$9.00

ERCOT North On Peak Spark Spread

Assumes a 7.2 Heat Rate, $1.50 O&M, and $.15 adder

Rolling 12

months,

as

of

May

6th

2011.

Source:

OTC

quotes

and

electronic

trading

system.

Quotes

are

daily. |