Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - W&T OFFSHORE INC | d8k.htm |

CLSA

Energy Forum New York

May 11, 2011

Exhibit 99.1 |

1

1

Current Snapshot

(1) Data as of 12/31/10, except for number of producing fields.

(2) Includes 6,628 gross and 4,644 net acres onshore.

(3) Excludes recently announced Permian acquisition and the pending fourth Shell

property. Key Financials ($ in MMs)

1Q11

2010

2009

Reserve Data

2010

2009

Revenue

$211

$706

$611

Proved Reserves (Bcfe)

485

371

Adjusted EBITDA

$133

$450

$341

Proved Developed %

81

%

76

%

CAPEX

$40

$416

$276

Oil and Liquids %

47

%

55

%

Field Statistics

(1)

Current Production

(3)

# of Producing Fields w/WI

68

Average Daily Production (MMcfe)

273+/-

Approx. Acreage (Gross/Net)

(2)

853,603 / 553,485

Oil and Liquids %

43

%

% Held-by-Production

82

%

Operated Production % (net)

78

%

2011 Guidance

$ MM

~$/Mcfe

~$/Boe

Production (Bcfe)

87.0 -

101.1

Lease Operating Expense

$190 -

$220

$2.18

$13.08

Gathering, Transportation & Taxes

$25 -

$28

$0.29

$1.74

General & Administrative

$69 -

$80

$0.79

$4.74 |

2

2

Key Investment Considerations

1)

R/P increases from 5.2 to 6.5 years and W&T’s

% of oil / liquids

increases from 47% to 58% with recently announced onshore

acquisition

2)

Adding Permian Basin to the portfolio with recent acquisition

–

Oily, longer-lived proved reserves

–

Provides “predictable growth”

opportunities, and complements our shelf and

deepwater assets with high cash flow and upside potential

3)

Large acreage position in the Gulf of Mexico primarily held by

production –

27 years of operating safely in the GOM

4)

Balanced mix of oil to gas reserves and production with growing oil

production

5)

Strong cash flow & good liquidity

6)

Active drilling program with 36 (27 onshore, 9 offshore) wells

planned on capital program of $310 million |

3

3

Company Diversification in Progress

•

Since April 2010, we have diversified our existing portfolio by

acquiring producing assets at attractive prices in the deepwater

GOM and the Permian basin

(1) Pro forma for recently announced Permian basin acquisition.

Permian Basin

(1)

•

Proved Reserves: 164 Bcfe

/

27 MMBoe

•

Acreage: 30,900 Net

•

~6% of Production

GOM Deepwater

•

Proved Reserves:

144 Bcfe

/

24 MMBoe

•

Acreage: 137,792 Gross /

93,670 Net

•

~31% of Production

(1)

GOM Shelf

•

Proved Reserves: 341 Bcfe

/

57 MMBoe

•

Acreage: 709,183 Gross /

455,171 Net

•

~62% of Production

(1)

Gulf Coast |

4

4

Company Strategy –

Focus on Growth

•

Complete pending GOM Shelf acquisition with Shell Offshore

•

Effectively incorporate recently announced acquisition of

West Texas property into existing operations

•

Exploit

recently

acquired

Shell

properties

-

Tahoe

and

S.E.

Tahoe properties

•

Continue evaluations of other potential acquisitions. Divest

“non-core”

properties as appropriate

•

Pursue active and balanced drilling program to increase

reserves and production

•

Expand/acquire acreage positions in onshore prospect areas

|

Onshore |

6

6

Permian Basin Acquisition Provides Base

for Transformation

•

Signed purchase and sale agreement to acquire approximately

21,900 gross acres (21,500 net acres) from private sellers for

approximately $377 million

•

Strong volumes from proved developed production

–

Current gross daily production of about 2,800 BOE

–

Production grew ~47% from 1,900 BOE at Jan. 1, 2011

–

Currently 70 producing wells

•

Proved and probable reserves

–

27 MMBOE of proved reserves

–

26 MMBOE of additional probable reserves

•

Conservative estimates of reserves

–

Assumed

an

average

EUR

of

~100

MBOE

net

per

well

for

PUDs

and

40

acres

spacing in our analyses

•

High ratio of oil and liquid (91%) to gas production and reserves

–

R/P increases from 5.2 to 6.5 years and W&T’s % of oil / liquids

increases from 47% to 58%. |

7

7

Permian Basin Acquisition Provides

Long-term Growth

•

Low risk operations with a multi-year extensive drilling inventory

–

450

to

500

drilling

locations

indentified

for

future

exploration

and

development

–

Currently operating on 40 acre spacing but certain nearby operators are using

20 acre spacing

–

3 drilling and 2 workover rigs working

•

Plan for three drilling rigs working throughout remainder of 2011

–

Primarily targeting the “Wolfberry”

trend, but deeper targets have been tested

and are producing

–

2011

Capital

Expenditures

of

$35

Million

-

$40

million

–

Expect to drill 7 exploratory & 15-20 developmental wells in 2011

|

8

8

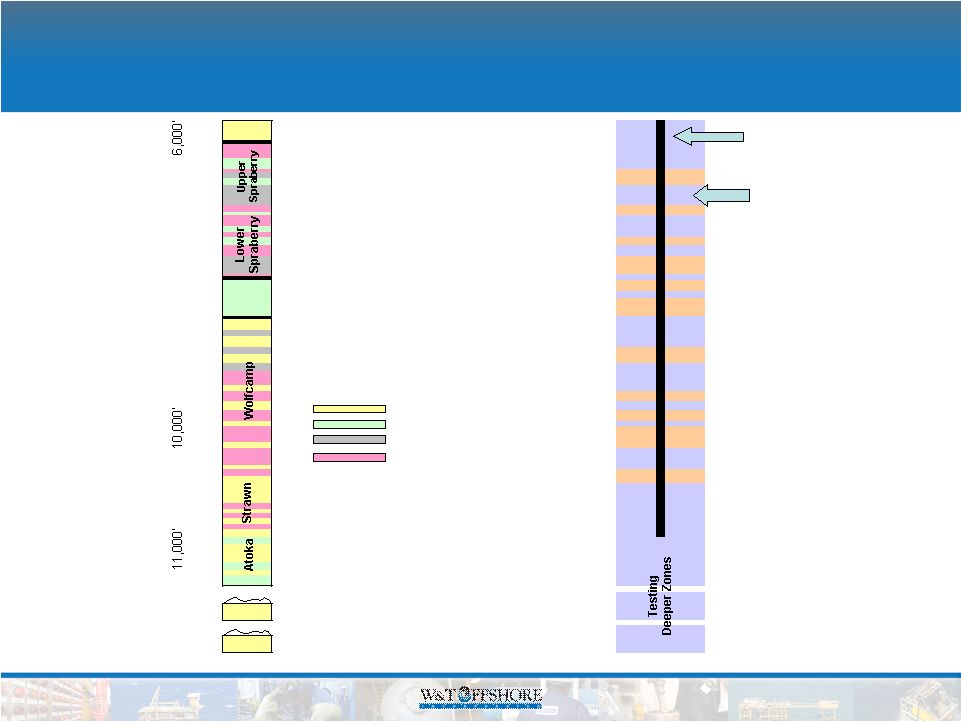

Newly Acquired Assets in West Texas

: Martin, Dawson, Andrews & Gaines Counties |

Wolfberry West Texas Completions *

Limestone Pay

Organic Rich Shale Play

Average Cased Depth

of Wellbore

Fractured Stimulation

Stages

Clear-

fork

Dean

Non-organic Shale Non-pay

Sandstone Play

12,500’

13,250’

Devonian

Silurian

* Not drawn to scale. |

10

10

Onshore 2011 Drilling Program

South Texas

WI: 50%

2 Wells

East Texas

WI: 25%

1 well

Exploration

Development

West Texas

WI: 25% to 100%

7 -

8 Wells

West Texas

WI: 100%

15 –

20 Wells

•

In addition to the recently announced

Permian acquisition, we have also

acquired 9,400 net exploratory acres in

the Permian basin |

Gulf

of Mexico |

12

Gulf of Mexico Attributes

•

Great history of production and reserves

–

Highly prolific with multiple pay zones

–

Reserves at deeper but virtually untapped zones, significant

upside potential

–

Established infrastructure on shelf

–

Substantial percentage of oil reserves

–

Reserve to production profile is consistent

•

Attractive reservoir characteristics

–

High porosity rock provides quick return on investment

–

Cash flow velocity significantly higher than most other basins

–

Balanced growth opportunities (high impact or low risk)

|

13

Our Historical Gulf of Mexico Focus

•

Operating successfully in the Gulf of Mexico for 27 yrs

–

10 year exploration drilling success rate of 77%

–

10 year development drilling success rate of 91%

–

Established infrastructure allows for accelerated cash flow

–

Excellent safety track record and culture for operating excellence

•

Large acreage position

–

WTI

holds

interest

in

about

67

fields

-

spread

across

the

GOM

–

Significant reserve upside potential in deeper zones

–

Extensive seismic, production and log data

–

Quality prospect inventory

•

Costs historically adjust quickly to commodity prices due to

shorter contract terms

•

Historically active M&A and joint venture market that has the

potential to be even more active in 2011 |

14

14

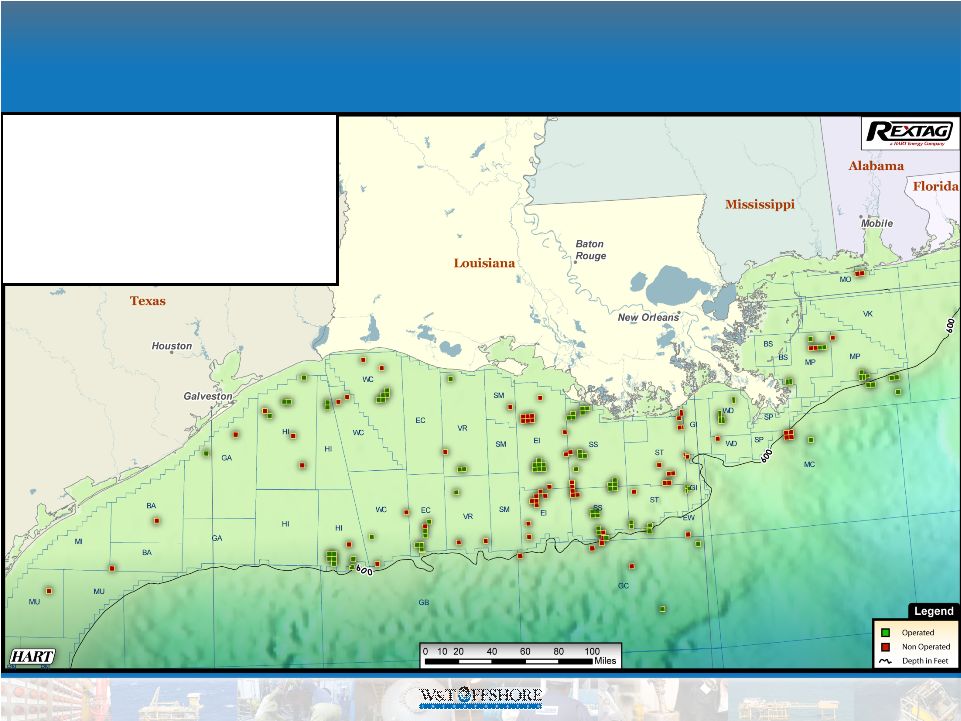

Gulf of Mexico Proved Reserve with

Geographic Diversification

•

67 fields

•

78% operated

•

548,841 net acres

•

82% held by production

•

Producing 272 MMcfe per day

•

43% oil & liquids / 57% gas |

15

Recent Deepwater Acquisitions

15

Shell

Total

Number of Deepwater

Properties Acquired

3

2

Close date

11/3/2010

5/3/2010

Purchase Price ($MM)

(1)

$138

$150

Proved Res. (MMBoe)

(1)

13.9

11.6

Purchase Price per Unit

(1)

$1.66/Mcfe; $9.93/Boe

$2.15/Mcfe; $12.90/Boe

% Liquids

(2)(3)

10%

64%

Block locations

VK 783 & 784, GC 244

MC 243, VK 822 & 823

~ Current net daily prod.

(3)

8.2 Mboe

4.7 Mboe

(1) As of effective date.

(2) Determined using the ratio of six Mcf of natural gas to one barrel of crude oil or NGL.

(3) Average daily production for March 2011.

Sellers |

16

16

Investment Highlights of Conventional

Shelf Property

•

Letter of intent to acquire a fourth field from Shell Offshore, Inc.

which is located in water depth of 20 to 30 feet

•

W&T will be operator and have a large ownership position

–

64.3% working interest

•

Strong volumes from proved developed production

–

Net daily production of 21.6 MMcfe

in March

•

Associated gas treatment plant to be acquired |

17

17

Main Pass 108 Field -

Back Online

•

Pipeline was down since June 2010 and affected production

at MP 98, MP 108, MP 163 and MP 180 fields

•

Production is back online as of March 31, 2011 via a new

pipeline route

–

Netbacks should increase with the new route

•

High-yield condensate field with net production of

46

MMcfe

per

day,

or

38

MMcf

and

1,400

barrels

per

day

–

We expect the rate to increase another eight to 10 MMcfe

per day when the Main Pass 108 E-3 well comes online

|

18

18

Concentrated Operations in Recently

Acquired GOM Fields and Focus Areas |

19

19

Offshore 2011 Drilling Program

Viosca

Knoll

Mississippi Canyon

Atwater Valley

Green Canyon

Garden Banks

East Breaks

Mustang

Island

Matagorda

Island

Brazos

Galveston

High

Island

E.

Cameron

Vermilion

Eugene

Island

Ship

Shoal

South

Timbalier

Ewing

Bank

West

Delta

Grand

Isle

Main

Pass

S. and E.

Main

Pass

W.

Cameron

Exploration

Development

MP 180 A-2

WI: 100%

Shelf

(Drilled and

successful)

SS 349 B

WI: 100%

Shelf

MP 108 #8 & Tex W5

WI: 75%

Shelf

West Cameron 73 #2

WI: 30%

Deep Shelf

Deepwater

Prospect

WI: 20%

MP 108 D-3 ST

WI: 100%

Shelf

(Drilling)

SS 349 E

WI: 100%

Shelf

ST 316 A-2 ST

WI: 40%

Shelf |

20

Regulatory Developments --

Deepwater

•

Ten drilling permits approved since such work was halted

after last year’s spill (as of 5/8/11)

•

Well

control

options

–

Operators

to

show

how

they

would

respond to subsea well control issue.

–

Helix Well Containment Group (HWCG)

–

Marine Well Containment Company (MWCC)

–

Total Deepwater Solution (TDWS)

•

W&T has executed a contract with HWCG

•

The first 3 approved deepwater drilling permit were

members of the HWCG |

Other

Operational and Financial Information |

22

22

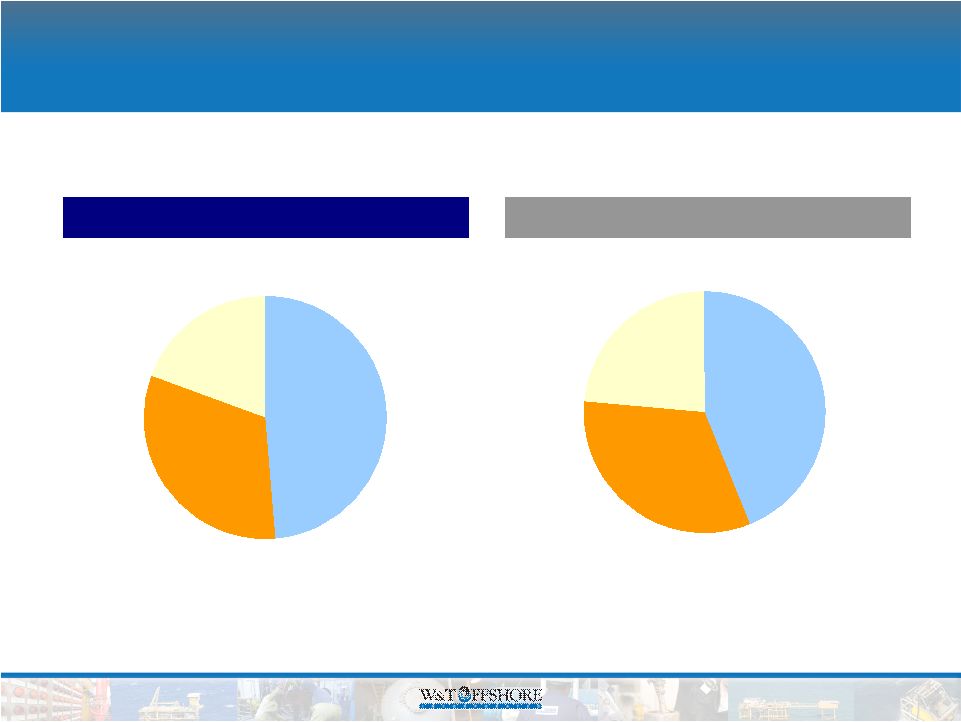

Proved Reserves by Year

PDP

43%

PDNP

33%

PUD

24%

PDP

49%

PDNP

32%

PUD

19%

2010

2009

2010 proved reserves increased 31% over 2009

485

Bcfe

371

Bcfe |

23

23

Production Profile

51.6

44.7

43.2

42.3

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2009

2010

2011E

Oil & NGLs

(Bcfe)

Natural Gas (Bcf)

94.8

Full-Year

Guidance

87.0 –

101.1

87.0

1Q

22.7

51.6

44.7

43.2

42.3

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2009

2010

2011E

Oil & NGLs

(Bcfe)

Natural Gas (Bcf)

94.8

Full-Year

Guidance

87.0 –

101.1

87.0

1Q

22.7 |

24

24

Drilling Within Cash Flow

Adjusted EBITDA vs. Capital Expenditures

($ in millions)

Capital

expenditures

funded

largely

through

internally

generated

cash

flow

$884

$820

$341

$450

$687+

$416

$276

$775

$359

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2007

2008

2009

2010

2011E

Adj. EBITDA

CAPEX, Excl. Acquisitions

Acquisition CAPEX

$884

$820

$341

$450

$687+

$416

$276

$775

$359

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2007

2008

2009

2010

2011E

Adj. EBITDA

CAPEX, Excl. Acquisitions

Acquisition CAPEX |

25

25

W&T’s

Strong Liquidity

•

Cash balance at April 26, 2011 ~ $140 million

•

New four-year revolver with $525 million borrowing

base

•

Borrowing base increases to $575 million when the

fourth Shell property closes; the newly acquired

Permian Basin assets have yet to be considered

•

Net cash provided by operating activities $464.8

million for 2010*

* includes $99.8 million tax reimbursement |

26

26

Key Investment Considerations

1)

R/P increases from 5.2 to 6.5 years and W&T’s

% of oil / liquids

increases from 47% to 58% with recently announced onshore

acquisition

2)

Adding Permian Basin to the portfolio with recent acquisition

–

Oily, longer-lived proved reserves

–

Provides “predictable growth”

opportunities, and complements our shelf and

deepwater assets with high cash flow and upside potential

3)

Large acreage position in the Gulf of Mexico primarily held by

production –

27 years of operating safely in the GOM

4)

Balanced mix of oil to gas reserves and production with growing oil

production

5)

Strong cash flow & good liquidity

6)

Active drilling program with 36 (27 onshore, 9 offshore) wells

planned on capital program of $310 million |

27

Reconciliation of Net Income to EBITDA

We

define

EBITDA

as

net

income

(loss)

plus

income

tax

expense

(benefit),

net

interest

expense

(which

includes

interest

income),

depreciation,

depletion,

amortization

and

accretion

and

impairment

of

oil

and

natural

gas

properties.

Adjusted

EBITDA

excludes

the

loss

on

extinguishment

of

debt,

the

unrealized

gain

or

loss

related

to

our

derivative

contracts

and

other

items

as

described

above.

Although

not

prescribed

under

GAAP,

we

believe

the

presentation

of

EBITDA

and

Adjusted

EBITDA

provide

useful

information

regarding

our

ability

to

service

debt

and

fund

capital

expenditures

and

they

help

our

investors

understand

our

operating

performance

and

make

it

easier

to

compare

our

results

with

those

of

other

companies

that

have

different

financing,

capital

and

tax

structures.

EBITDA

and

Adjusted

EBITDA

should

not

be

considered

in

isolation

from

or

as

a

substitute

for

net

income,

as

an

indication

of

operating

performance

or

cash

flow

from

operating

activities

or

as

a

measure

of

liquidity.

EBITDA

and

Adjusted

EBITDA,

as

we

calculate

them,

may

not

be

comparable

to

EBITDA

and

Adjusted

EBITDA

measures

reported

by

other

companies.

In

addition,

EBITDA

and

Adjusted

EBITDA

do

not

represent

funds

available

for

discretionary

use.

The following table presents a reconciliation of our consolidated net income to

consolidated EBITDA to Adjusted EBITDA: |

28

Forward-Looking Statement Disclosure

This

presentation,

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995,

Section

27A

of

the

Securities

Act

and

Section

21E

of

the

Exchange

Act.

Forward-looking

statements

give

our

current

expectations

or

forecasts

of

future

events.

They

include

statements

regarding

our

future

operating

and

financial

performance.

Although

we

believe

the

expectations

and

forecasts

reflected

in

these

and

other

forward-looking

statements

are

reasonable,

we

can

give

no

assurance

they

will

prove

to

have

been

correct.

They

can

be

affected

by

inaccurate

assumptions

or

by

known

or

unknown

risks

and

uncertainties.

You

should

understand

that

the

following

important

factors,

could

affect

our

future

results

and

could

cause

those

results

or

other

outcomes

to

differ

materially

from

those

expressed

or

implied

in

the

forward-looking

statements

relating

to:

(1)

amount,

nature

and

timing

of

capital

expenditures;

(2)

drilling

of

wells

and

other

planned

exploitation

activities;

(3)

timing

and

amount

of

future

production

of

oil

and

natural

gas;

(4)

increases

in

production

growth

and

proved

reserves;

(5)

operating

costs

such

as

lease

operating

expenses,

administrative

costs

and

other

expenses;

(6)

our

future

operating

or

financial

results;

(7)

cash

flow

and

anticipated

liquidity;

(8)

our

business

strategy,

including

expansion

into

the

deep

shelf

and

the

deepwater

of

the

Gulf

of

Mexico,

and

the

availability

of

acquisition

opportunities;

(9)

hedging

strategy;

(10)

exploration

and

exploitation

activities

and

property

acquisitions;

(11)

marketing

of

oil

and

natural

gas;

(12)

governmental

and

environmental

regulation

of

the

oil

and

gas

industry;

(13)

environmental

liabilities

relating

to

potential

pollution

arising

from

our

operations;

(14)

our

level

of

indebtedness;

(15)

timing

and

amount

of

future

dividends;

(16)

industry

competition,

conditions,

performance

and

consolidation;

(17)

natural

events

such

as

severe

weather,

hurricanes,

floods,

fire

and

earthquakes;

and

(18)

availability

of

drilling

rigs

and

other

oil

field

equipment

and

services.

We

caution

you

not

to

place

undue

reliance

on

these

forward-looking

statements,

which

speak

only

as

of

the

date

of

this

presentation

or

as

of

the

date

of

the

report

or

document

in

which

they

are

contained,

and

we

undertake

no

obligation

to

update

such

information.

The

filings

with

the

SEC

are

hereby

incorporated

herein

by

reference

and

qualifies

the

presentation

in

its

entirety.

Cautionary

Note

to

U.S.

Investors

The

United

States

Securities

and

Exchange

Commission

permits

oil

and

gas

companies,

in

their

filings

with

the

SEC,

to

disclose

only

proved

reserves

that

a

company

has

demonstrated

by

actual

production

or

conclusive

formation

tests

to

be

economically

and

legally

producible

under

existing

economic

and

operating

conditions.

U.S.

Investors

are

urged

to

consider

closely

the

disclosure

in

our

Form

10-K

for

the

year

ended

December

31,

2010,

available

from

us

at

Nine

Greenway

Plaza,

Suite

300,

Houston,

Texas

77046.

You

can

obtain

these

forms

from

the

SEC

by

calling

1-800-SEC-0330. |