Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - JONES LANG LASALLE INC | d8k.htm |

Investor Presentation

May 2011

..40,000 employees….185 offices….60 countries….1 global platform..

Exhibit 99.1 |

Forward looking statements

2

Statements in this presentation regarding, among other things, future financial results

and performance, achievements, plans and objectives and dividend payments may be

considered forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks,

uncertainties and other factors which may cause actual results, performance,

achievements, plans and objectives of Jones Lang LaSalle to be materially

different from those expressed or implied by such forward-looking statements.

Factors that could cause actual results to differ materially include those discussed

under “Business,” “Risk Factors,” “Management’s

Discussion and Analysis of Financial Condition and Results of Operations,” “Quantitative and

Qualitative Disclosures about Market Risk,” “Cautionary Note Regarding

Forward-Looking Statements” and elsewhere in Jones Lang LaSalle’s

Annual Report on Form 10-K for the year ended December 31, 2010 and in other reports filed

with the Securities and Exchange Commission. There can be no assurance that future

dividends will be declared since the actual declaration of future dividends, and

the establishment of record and payment dates, remains subject to final

determination by the Company’s Board of Directors. Statements speak only as of

the date of this presentation. Jones Lang LaSalle expressly disclaims any

obligation or undertaking to update or revise any forward-looking statements

contained herein to reflect any change in Jones Lang LaSalle’s expectations or

results, or any change in events.

© Jones Lang LaSalle IP, Inc. 2011. All rights reserved. No part of this publication

may be reproduced by any means, whether graphically, electronically, mechanically

or otherwise howsoever, including without limitation photocopying and recording on

magnetic tape, or included in any information store and/or retrieval system without prior written

permission of Jones Lang LaSalle IP, Inc.

|

Table of Contents

I.

Company Description

II.

Financial Overview

III.

Market Environment

IV.

Global Growth Strategy

V.

2011 Priorities

3 |

Company Description |

Jones

Lang Wootton founded in London 1783

1968

1997

1999

LaSalle Partners founded, operating primarily in the Americas

LaSalle Partners initial public offering

LaSalle Partners and Jones Lang Wootton merge to create Jones Lang LaSalle

Integrated global platform (NYSE ticker

“JLL”) Jones Lang

LaSalle Company history

Present

2008

The Staubach Company and Jones Lang LaSalle combine operations

Largest merger in JLL history transforms U.S. local markets position

•

Integrated global services platform

•

Industry-leading research

•

Superior client relationship management

•

Consistent service delivery

•

Innovative solutions to maximize value

•

Strong brand

•

Investment grade balance sheet

5

Leasing

Capital

Markets

& Hotels

Property

& Facility

Mgmt.

Project &

Development

Services

Advisory

&

Consulting

Investment

Management

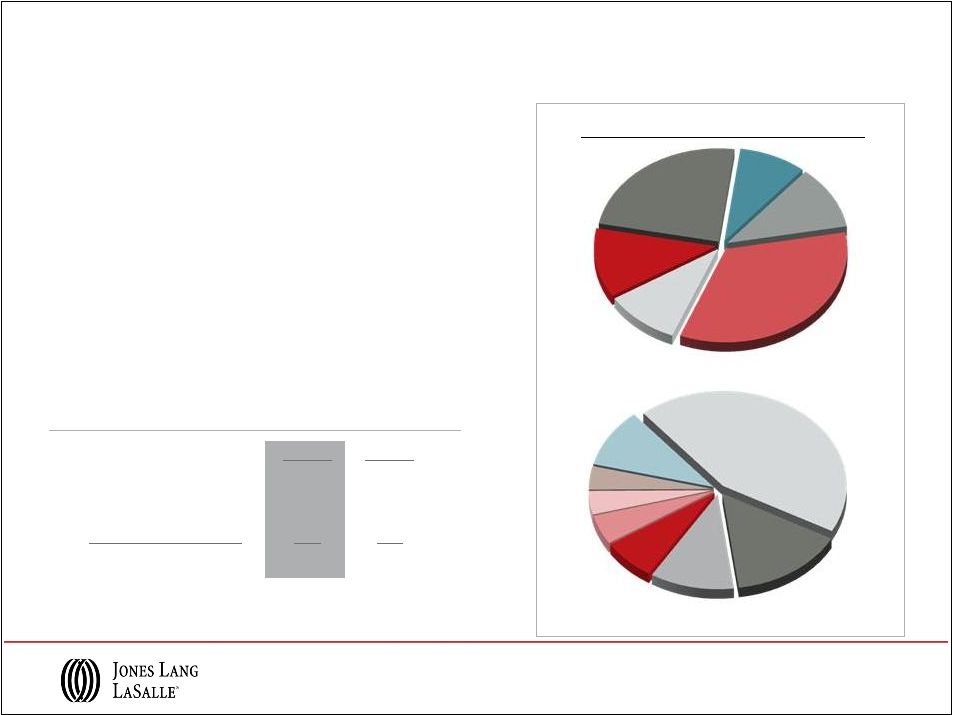

$2.9B

2010

Revenue |

FY

2010 FY 2009

Americas

43%

42%

EMEA

25%

26%

Asia Pacific

23%

22%

LaSalle Investment Mgmt.

9%

10%

Consolidated

100%

100%

Jones Lang LaSalle

(1)

Excludes equity losses

2010 Revenue = $2.9 billion

…

And Global Market Reach

Diversified Service Lines…

•

Consolidator

in

a

consolidating

industry

-

more

than

30 mergers and acquisitions since 2005

•

Corporate Solutions driving growth and providing

annuity revenue as outsourcing trend continues

•

LaSalle

Investment

Management

-

a

premier

global

investment manager winning new mandates

•

Cash generating business model with investment

grade balance sheet

`

Revenue by Segment

(1)

Medium-term outlook continues to benefit from cyclical recovery

6

United

States 44%

United

Kingdom

11%

Continental

Europe

15%

Greater China

5%

Developing &

Other Countries

10%

Japan 4%

India 4%

Australia

7%

Property &

Facility

Management

24%

Project &

Development

Services

12%

LaSalle

Inv.

Mgmt.

9%

Advisory

Consulting &

Other 11%

Leasing

34%

Capital

Markets

10% |

More than

30 acquisitions since 2005 Market Share and Service Line

Expansion •

Middle Market Corporate Solutions

•

Leasing

•

Capital Markets

•

Property Management

•

Project & Development Services

•

Retail

•

Industrial

•

Energy & Sustainability Services

•

Infrastructure

•

Hospital / Healthcare

Market share growth

Product and services expansion

7

EMEA

Americas

Asia

Pacific

RL Davis

Leechiu

Creer

NSC

Sallmanns

Shore Industrial

Meghraj

Rogers Chapman

Littman Partnership

RSP Group

Area Zero

Hargreaves Goswell

Troostwijk Makelaars

KHK Group

Camilli & Veiel

GVA

Upstream

Tetris

Creevy LLH Ltd.

Brune

Alkas

Kemper’s

Churston Heard

Staubach

Spaulding & Slye

Zietsman

Klatskin

CRA

Standard Group

ECD

HIA

TCF

Strengthening

our platform

and

connecting

our people

Asset Realty Managers

GGP

PCA

RECF |

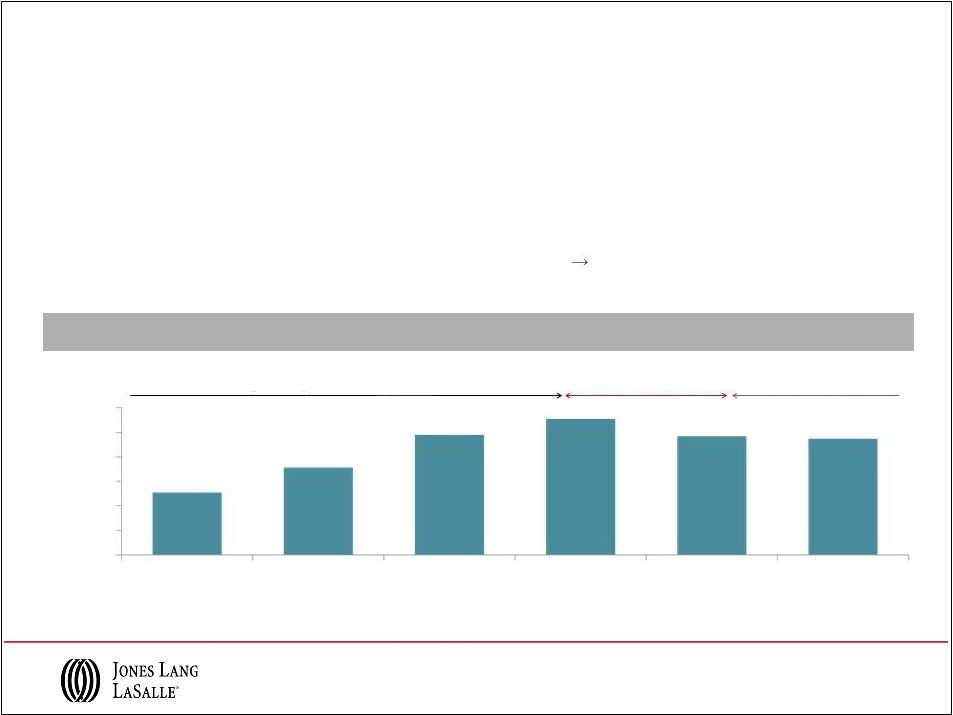

$40.6

B $49.7 B

$46.2 B

AUM

($ millions)

$39.9 B

2005 to 2010 Advisory Fees: 13% Compound Annual Growth Rate

LaSalle Investment Management

A decade of accomplishments

$41.3 B

$29.8 B

Global Financial Crisis

Stabilized Advisory Fees

Building Advisory Fees in Healthy Markets

8

•

Global

platform:

More

than

300

institutional

clients

worldwide

-

investor

base

greater

than

90%

institutional

•

Investment

Expertise:

Core,

value

add,

opportunistic

private

investing

across

major

property

types

•

Consistent

client

service

delivery

system

-

worldwide

•

Fully integrated global management team, compensation linked to growth in high-margin

advisory revenue •

Results:

Ability

to

weather

global

property

cycles,

annuity

revenue

growth

financial

stability,

achieved

scalable

operations

2005

2006

2007

2008

2009

2010

$0

$50

$100

$150

$200

$250

$300

$127.8

$178.1

$245.1

$277.9

$242.2

$237.5 |

Jones Lang LaSalle

More than 40,000 employees driving growth across service lines

LEED-accredited professionals

585

Property and corporate facilities

under management (s.f.)

1.8B

Investment assets

under management

$41B

Tenant representation

transactions (s.f.)

8,400 transactions

159M

Agency leasing transactions (s.f.)

19,400 transactions

323M

Annual energy savings for

clients

$125M

Global JLL Hotels Activity

$4.1B

Property & Facility

Management 24%

Project &

Development

Services 12%

LaSalle Inv.

Mgmt. 9%

Advisory

Consulting &

Other 11%

Leasing 34%

Capital

Markets 10%

Global JLL Capital Markets

Activity

$33B

9

Return to Table of Contents |

Financial Overview |

•

Record revenue of $2.9 billion , up 18% over 2009

•

Global Leasing revenue reaches $1 billion; up

28% over 2009

•

Property & Facility Management currently 24% of

global revenue

•

LaSalle Investment Management raised $5 billion

in net capital commitments; AUM = $41 billion

•

Adjusted operating income margin of 9.1% vs.

6.6% in 2009

Demonstrating competitive strength

Consolidated Earnings Scorecard

2010 Highlights

FY 2010

FY 2009

Revenue

$2.9B

$2.5B

% change

18%

(8%)

Net Income

$154M

($4M)

Adjusted Net Income

(1)

$166M

$70M

Earnings Per Share

$3.48

($0.11)

Adjusted Earnings Per Share

(1)

$3.77

$1.75

Adjusted EBITDA

$336M

$238M

Adjusted EBITDA margin

11.5%

9.6%

Market Capitalization

$3.6B

$2.5B

(1)

Adjusted

for

restructuring

and

non-cash

co-investment

charges

11 |

FY 2010 Revenue Performance

Note: Equity losses of $58.9M and $11.4M in 2009 and 2010, respectively, are included

in segment results, however, are excluded from Consolidated totals.

($ in millions)

Americas

EMEA

Asia Pacific

Consolidated

18%

LaSalle

$1,031.6

$1,261.5

12 |

Asia

Pacific Americas

EMEA

Leasing

Capital Markets &

Hotels

Property & Facility

Management

Project &

Development Services

Advisory, Consulting

& Other

Total RES

Operating Revenue

$637.9

$84.1

$269.4

$158.9

$110.9

$1,261.2

28%

120%

19%

1%

1%

22%

$202.6

$141.2

$142.9

$115.0

$127.2

$728.9

17%

32%

5%

6%

4%

13%

$159.4

$80.4

$303.7

$63.5

$71.4

$678.4

42%

38%

14%

44%

17%

25%

$999.9

$305.7

$716.0

$337.4

$309.5

$2,668.5

28%

50%

14%

8%

5%

20%

Total RES

Revenue

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). 2010 Real Estate

Services Revenue ($ in millions)

13 |

Q1

2011: 26% (1)

$593

$781

$753

$557

$317

$203

($ in millions)

Q1 2011: 23%

(1)

Full Year Comparison

(1)

Compared to Q1 2010

Full Year Comparison

($ in millions)

Leasing

Capital Markets

$1,000

$306

Local and Regional Real Estate Services

Leasing and Capital Markets capturing incremental revenue

Asia Pacific

EMEA

Americas

14 |

Asia

Pacific Americas

EMEA

Leasing

Capital Markets &

Hotels

Property & Facility

Management

Project &

Development Services

Advisory, Consulting

& Other

Total RES

Operating Revenue

$143.1

$19.8

$66.7

$37.2

$20.7

$287.5

35%

108%

15%

18%

9%

26%

$37.2

$28.7

$35.9

$38.4

$28.0

$168.2

4%

10%

4%

48%

8%

11%

$29.8

$17.5

$83.9

$18.1

$16.2

$165.5

17%

5%

24%

69%

7%

22%

$210.1

$66.0

$186.5

$93.7

$64.9

$621.2

23%

26%

16%

37%

21%

Total RES

Revenue

2%

Q1 2011 Real Estate Services Revenue

($ in millions)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). 15 |

Solid Cash Flows and Balance Sheet

($ in millions)

Positioned to drive growth and investment

2010 Free Cash Flow

(1)

(1)

Free

cash

flow

calculated

as

EBITDA

plus

non-cash

charges

and

change

in

working

capital

Investment grade balance

sheet

Effective tax management

(24% effective tax rate)

Disciplined CapEx spending

Opportunity to grow and

invest in the business

16

$440 |

Solid Cash Flows and Balance Sheet Position

•

Healthy position after Q1 2011

incentive compensation payments

•

Net debt repayment of $184 million

over the last twelve months

•

Cash interest expense of $1.8 million,

down 51% from Q1 2010 expense of

$3.7 million

•

Investment grade ratings:

Standard & Poor’s:

BBB-

(Outlook: Stable)

Moody’s Investor Services:

Baa2

(Outlook:

Stable)

Cash Flows

Q1 2011

Q1 2010

Cash from Earnings

$42

$46

Working Capital

(239)

(192)

Cash used in Operations

($197)

($146)

Primary Uses

Capital Expenses

(1)

(17)

(5)

Acquisitions & Deferred Payment Obligations

(25)

(27)

Co-Investment

(2)

(10)

Dividends

-

-

Net Cash Outflows

($44)

($42)

Net Share Activity & Other Financing

(4)

(5)

Net Bank Debt (Borrowings) / Repayments

($245)

($193)

Balance Sheet

Q1 2011

Q1 2010

Cash

$101

$60

Short Term Borrowings

42

47

Credit Facility

278

335

Net Bank Debt

$219

$322

Deferred Business Obligations

293

374

Total Net Debt

$512

$696

($ in millions)

(1)

Capital Expenditures for Q1 2011 and Q1 2010 net of tenant improvement allowances

received were $16 million and $4 million, respectively Q1 2011

Highlights 17

Return to Table of Contents |

Market Environment |

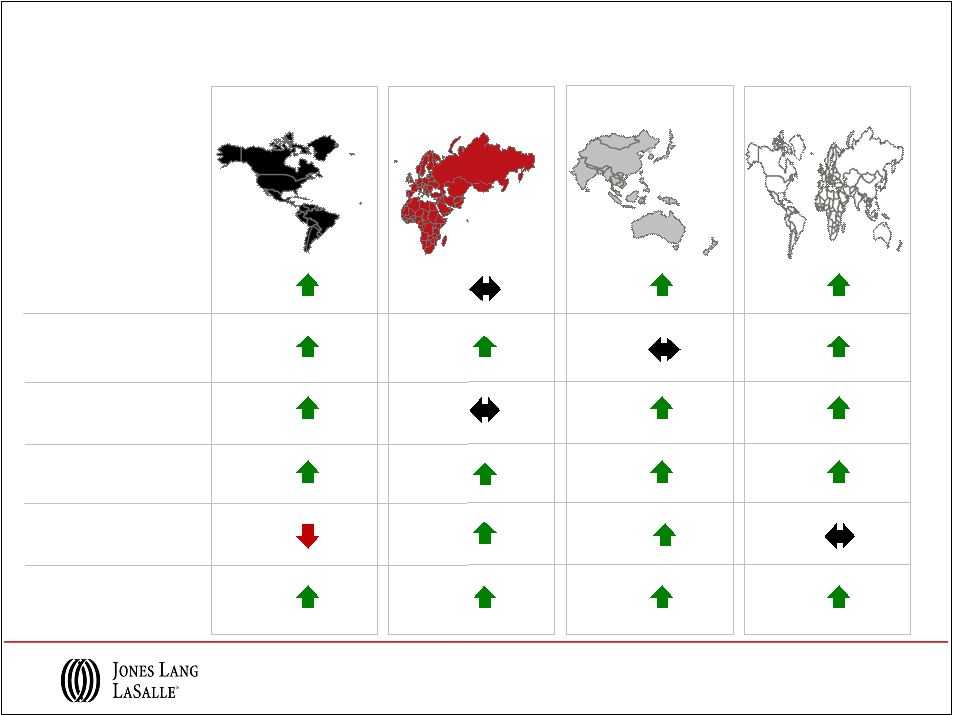

Increasingly synchronized recovery

Capital Markets Leading Real Estate Fundamentals

Americas

EMEA

Asia Pacific

As of Q1 2011

Capital Values

Leasing Fundamentals

The Jones

Lang

LaSalle

Property

Clocks

SM

19

San Francisco,

Singapore

New York,

San Francisco

Singapore

New York,

Shanghai

Moscow, Stockholm

Beijing,

Hong Kong,

Washington DC

Chicago

Amsterdam,

Dallas

Sao Paulo,

London

Detroit

Seoul

Milan

Berlin, Paris

Brussels

Mumbai, Tokyo

Stockholm

Dallas,

Milan

Detroit

Seoul, Tokyo

Brussels,

Mumbai

Capital Value

growth slowing

Capital Value

falling

Capital Value

growth

accelerating

Capital Value

bottoming out

Rental growth

slowing

Rental growth

falling

Rental

growth

accelerating

Rents

bottoming

out

Sydney,

Toronto

Shanghai

Beijing

Toronto,

Moscow

Amsterdam,

Hong Kong,

Washington DC,

Sao Paulo

Chicago

London

Berlin, Paris, Sydney |

%

change Based

on

rents

for

Grade

A

space

in

CBD

or

equivalent.

In

local

currency.

Source:

Jones

Lang

LaSalle,

April

2011

Global

Market

Perspective

Americas

Europe

Asia Pacific

Q1 2010 –

Q1 2011 rental change

Prime Offices

20 |

Global Markets Perspective

Prime offices –

projected value change in 2011

*New York –

Midtown, London –

West End. Nominal rates in local currency.

Source: Jones Lang LaSalle, April

2011

Global

Market

Perspective

Capital Values

Rental Values

+ 10-20%

+ 5-10%

+ 0-5%

-

0-5%

-

5-10%

+ 20%

-

10-20%

Click here

to see the JLL 2011 Real Estate Outlook, including our Top 10 trends for 2011

21

Return to Table of Contents

Shanghai, Singapore, Washington DC

San Francisco, London*, New York*,

Toronto, Sao Paulo

Paris, Mumbai

Sydney

Frankfurt, Amsterdam

Chicago, Los Angeles

Madrid

Paris, Chicago

Los Angeles, Mumbai

Sydney, Frankfurt,

Amsterdam, Mexico City

Madrid

Hong Kong, Moscow

Dubai

Dubai

Hong Kong, Moscow

San Francisco, Washington DC

Brussels, Tokyo

Mexico City

Brussels, Tokyo

Shanghai, Singapore

New York*, Toronto

Sao Paulo, London* |

Global Growth Strategy |

Jones Lang LaSalle

Global strategy for renewed growth

G5

G1

G2

G4

G3

Build our leading local and regional market positions

Grow our leading positions in Corporate Solutions

Capture

the

leading

share

of

global

capital

flows

for

investment

sales

Strengthen LaSalle Investment Management’s leadership position

Connections: Differentiate by connecting across the firm, and with clients

23 |

Merger

Impact: Tenant Representation Market Leadership •

Reinforced JLL’s position as the high quality brand for occupier clients

•

Significantly improved our market position; 990 brokers in the field today; up more

than 200% over 2007 •

Attained a market leading tenant representation position in 27 markets (vs. 6 markets

in 2007) •

Built

Industrial

market

presence;

220

professional

brokers

in

40

markets;

#3

or

better

in

top

8

markets

Local and Regional Services

G1

Staubach merger transforms U.S. local markets position

2007

Americas Leasing revenue growth of 29% in 2010

Southern

California

(excluding San

Diego)

Philadelphia

Boston

Atlanta

Northern

New Jersey

Chicago

Raleigh/Durham

DC Metro

San Francisco

Silicon Valley

Charlotte

Dallas / Ft.

Worth

New York

2010

Silicon Valley

San Francisco

Seattle

Sacramento

West Palm Beach

Orlando

Tampa

Westchester

Richmond

Baltimore

Market Leader –

#1-2-3

Offices

As of Year End ‘10; Market share based on SF of completed deals of 10,000+ SF

Source: JLL Research & CoStar

24

Raleigh/Durham

Denver

Atlanta

Houston

Los Angeles

Orange County

Phoenix

Charlotte

San Diego

Suburban

Maryland

Dallas / Ft.

Worth

Philadelphia

Boston CBD

New York

Northern

New Jersey

Chicago CBD

Northern VA

Chicago Suburbs

Boston

Suburbs/

Cambridge

Ft Lauderdale

Miami |

Local and Regional Services

European retail acquisitions providing scale in key markets

•

Managing 81 million sq ft of retail assets

•

Leasing 75 million sq ft of space in 200 shopping centers

•

Valuation of 450 shopping centres of 97 million sq ft

•

More than 1,000 dedicated retail staff across Europe

•

EMEA’s only dedicated regional retail capital markets

team, with more than 80 professionals working in more

than 12 markets

Over €1.3bn

in Multi Portfolio

acquisition

Over €513m

in 2 acquisitions

3.6m sq ft

11 Shopping Centres

Over €2.5 bn

disposal advice

EMEA Retail revenue = approximately 20% of Total EMEA revenue in

2010

Select EMEA Retail highlights:

Approx.

€2.5 bn

valued quarterly

25

Fully integrated approach

maximizing client value |

Leading

position with unique expertise across services & geographies

•

Accelerate new client wins and innovate for existing clients to broaden

relationship -

60 new wins, 33 expansions and 32 renewals in 2010

-

More than 700 million sq ft under management as of December 31, 2010; 18% compound

annual growth rate over the past 5 years

•

Target new industry segments for continued market share growth

-

Replicate Financial/Pharma/IT success

Global Corporate Solutions

Integrated

Facility

Management

Transaction

Management

Project

Management

Lease

Administration

Mobile

Engineering

Energy &

Sustainable

Services

Strategic

Consulting

Corporate

Finance /

CMG

Client

Relationship

Management

G2

Corporate

Retail

Services

2010 Highlights

•

Property & Facility Management revenue up

14% vs. 2009

•

Project & Development Services revenue up 8%

vs. 2009; corporates starting to re-open capital

expenditure budgets

26 |

Asia

Pacific gaining share with local and multinational corporates

Global Corporate Solutions

Alcatel-Lucent

Philips

Sanyo

Wipro

Infosys

Sony

Telestra

AFP

Centrelink

Fonterra

Citi

Merck

27 |

2010 Highlights

Capture Global Capital Flows for Investment Sales

Positioned to leverage leading share as markets recover

G3

Source: Jones Lang LaSalle

•

Volumes continuing cyclical recovery

•

Demand high for core products;

supply remains constrained

•

Global Hotels business gaining

momentum; captured $4.1B of $24.3B

total deal volume in 2010

2011 volumes expected to increase a further 35-40%

Direct Commercial Real Estate Investment, 2005-2011

For more information on Jones Lang

LaSalle

Hotels,

visit

www.joneslanglasallehotels.com.

28

Leasing

Receivership

Services

Development &

Construction

Management

Property & Asset

Management

Loan

Restructuring &

Debt Advisory

Research on

Local Martkets

Planning &

Developing

Strategic

Review

Investment

Sales

Leasing

Receivership

Services

Development &

Construction

Management

Property & Asset

Management

Loan

Restructuring &

Debt Advisory

Research on

Local Martkets

Planning &

Developing

Strategic

Review

Leasing

Receivership

Services

Development &

Construction

Management

Property & Asset

Management

Loan

Restructuring &

Debt Advisory

Research on

Local Martkets

Planning &

Developing

Strategic

Review

Leasing

Receivership

Services

Development &

Construction

Management

Property & Asset

Management

Loan

Restructuring &

Debt Advisory

Research on

Local Martkets

Planning &

Developing

Strategic

Review

Investment

Sales

Connecting

clients to

innovative

solutions

Connecting

clients to

innovative

solutions

+60%

+30%

+15-20% |

•

$5 billion of net new capital raised in 2010, 2

nd

best year in

LaSalle history

•

Strong capital raising continues, $1.5 billion of net new capital

commitments in Q1 2011

•

Momentum continues with new separate account mandates

New Business Activity

Product

Assets Under

Management

($ in billions)

Average

Performance

Private Equity

U.K.

$11.0

Above benchmark

Continental Europe

$4.3

Return: +1x equity

North America

$10.2

Above benchmark

Asia Pacific

$8.0

Return: +1x equity

Public Securities

$9.5

Above benchmark

Total Q1 2011 AUM

$43.0 B

AUM by Fund type

($ in billions)

A premier global investment manager

LaSalle Investment Management

G4

Note: AUM data reported on a one-quarter lag

29 |

Connecting

JLL to add

value for

clients

JLL

Brand

Market

Knowledge &

Experience

Thought

Leadership &

Research

Colleagues

Sharing

Relationships

Extensive

Capabilities

& Products

Client First

www.joneslanglasalle.com

G5

Technology

JLL OneView

Connecting Across the Firm and With Clients

Technology enabling value added connections

30 |

Energy and Sustainability Services

Energy conservation and cost savings a growing priority

“I chose Ray Quartararo and Jones

Lang LaSalle because of our

successful history together taking on

and figuring out difficult projects and

the company’s deep sustainability

expertise and track record.”

--Anthony E. Malkin, Building Owner,

Empire State Building Company

•

Nearly 600 LEED Accredited Professionals

•

116 LEED projects globally, including

•

1

st

LEED Platinum high-rise; One Bryant Park, New York

•

1

LEED building registered in India; Sohrabji Godrej Green

•

1

LEED-EB O&M multi-tenant building in the U.S.; 550 W.

Washington, Chicago

•

Documented over $125M in energy savings for clients

•

Reduced 563,000 tons of greenhouse gas emissions

•

Equivalent to the emissions of nearly 70 million gallons of

gasoline consumed

Making an Impact

G5

31

Return to Table of Contents

st

st |

2011 Priorities |

2011 Priorities

Enhance margin and strengthen income quality

Margin Performance

•

Leverage strengthening local markets

positions •

Continue growing scale in Corporate

Solutions •

Maintain LaSalle Investment Management’s stable advisory

fee margins; enhance with transaction and incentive fees

•

Grow operating margin to medium term target of 12%

Historic Adjusted Operating Income Margin

Historic Adjusted EBITDA Margin

Note: Adjusted Operating Income excludes restructuring charges, adjusted EBITDA

excludes restructuring charges and non-cash co-investment

charges. 2007 results have been adjusted to exclude significant advisory fees from one large corporate portfolio.

33 |

Opportunity Target

Secure market leadership –

Goal to be #1, #2 or

#3 in targeted local and regional market services

Provide specialized technical services to

Corporate Solutions outsourcing clients

Capture recovering cross-border capital flows and

strengthen Hotels market

Maximize opportunities created by financial

regulatory legislation and financial crisis fallout

Differentiate by connecting across the firm, and

with clients

Strategy

G1

G2

G3

G4

G5

34

2011 Priorities and Consolidation Opportunities

Capture opportunities reappearing in the marketplace

Financial Objective

•

Major growth to

shareholders

•

Accretive within

12-18 months

•

Maintain

investment grade

strength

|

Market

Trends Early stages of cyclical recovery

Leverage leading global market positions for improved

transactional revenue

Jones Lang LaSalle Opportunity

Outsourcing trend continuing and

broadening across sectors

Continue Corporate Solutions leadership; capture emerging

sectors (e.g. Healthcare, Government and Infrastructure)

Strongest real estate asset managers

attracting capital

LaSalle raised $5 billion of net new capital in 2010; strong

reputation and good momentum entering 2011

Industry consolidation resuming

Pursue growth within G5 strategy and financial objectives

Jones Lang LaSalle

Leading brand well positioned for growth

35

Return to Table of Contents |

Appendix |

FY

2010 FY 2009

GAAP net income (loss)

$ 153.5

$ (4.1)

Shares (in 000's)

44,084

38,543

GAAP earnings (loss) per share

$ 3.48

$ (0.11)

GAAP net income (loss)

$ 153.5

$ (4.1)

Restructuring, net of tax

4.9

35.6

Non-cash co-investment charges, net of tax

7.9

38.5

Adjusted net income

$ 166.3

$ 70.0

Shares (in 000's)

44,084

40,106

Adjusted earnings per share

$ 3.77

$ 1.75

($ in millions)

Reconciliation of GAAP Net Income (Loss) to

Adjusted Net Income

Note: Basic shares outstanding are used in the calculation of GAAP EPS for the twelve

months ending December 31, 2009, as the use of dilutive shares outstanding would

cause that EPS calculation to be anti-dilutive. Return to Consolidated

Earnings Scorecard 37

Return to Table of Contents |

($ in

millions) Reconciliation of GAAP Operating Income to Adjusted

Operating Income and Net Income (Loss) to EBITDA

and Adjusted EBITDA

FY 2010

FY 2009

GAAP Operating Income

$ 260.7

$ 116.4

Restructuring charges

6.4

47.4

Adjusted Operating Income

$ 267.1

$ 163.8

Net income (loss)

$ 153.5

$ (4.1)

Interest expense, net of interest income

45.8

55.0

Provision (benefit) for income taxes

49.0

5.7

Depreciation and amortization

71.6

83.3

EBITDA

$ 319.9

$ 139.9

Non-cash co-investment charges

10.4

51.3

Restructuring

6.4

47.4

Adjusted EBITDA

$ 336.7

$ 238.6

Return to Consolidated Earnings Scorecard

38

Return to Table of Contents |

FY

2010 FY 2009

Net Income (Loss)

$154

($4)

Interest Expense, net of interest income

46

55

Provision (benefit) for income taxes

49

6

Depreciation and amortization

72

83

EBITDA

$321

$140

Change in working capital

68

7

Deferred Compensation Amortization and

non-cash co-investment charges

51

97

Free Cash Flow

$440

$244

($ in millions)

Reconciliation of GAAP Net Income (Loss) to

EBITDA and Free Cash Flows

Return to Free Cash Flow Chart

39

Return to Table of Contents |