Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CAPSTEAD MORTGAGE CORP | d8k.htm |

| EX-99.2 - FIRST QUARTER 2011 INVESTOR FACT SHEET - CAPSTEAD MORTGAGE CORP | dex992.htm |

CAPSTEAD

Information as of March 31, 2011

Investor Presentation

Exhibit 99.1 |

Safe

Harbor Statement - Private Securities Litigation Reform Act of 1995

Cautionary Statement Concerning Forward-looking Statements

This

document

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

include,

without

limitation,

any

statement

that

may

predict,

forecast,

indicate

or

imply

future

results,

performance

or

achievements,

and

may

contain

the

words

“believe,”

“anticipate,”

“expect,”

“estimate,”

“intend,”

“project,”

“will

be,”

“will

likely

continue,”

“will

likely

result,”

or

words

or

phrases

of

similar

meaning.

Forward-looking

statements

are

based

largely

on

the

expectations

of

management

and

are

subject

to

a

number

of

risks

and

uncertainties

including,

but

not

limited

to,

the

following:

In

addition

to

the

above

considerations,

actual

results

and

liquidity

are

affected

by

other

risks

and

uncertainties

which

could

cause

actual

results

to

be

significantly

different

from

those

expressed

or

implied

by

any

forward-looking

statements

included

herein.

It

is

not

possible

to

identify

all

of

the

risks,

uncertainties

and

other

factors

that

may

affect

future

results.

In

light

of

these

risks

and

uncertainties,

the

forward-looking

events

and

circumstances

discussed

herein

may

not

occur

and

actual

results

could

differ

materially

from

those

anticipated

or

implied

in

the

forward-looking

statements.

Forward-looking

statements

speak

only

as

of

the

date

the

statement

is

made

and

the

Company

undertakes

no

obligation

to

update

or

revise

any

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise.

Accordingly,

readers

of

this

document

are

cautioned

not

to

place

undue

reliance

on

any

forward-looking

statements included herein.

–

changes in general economic conditions;

–

fluctuations in interest rates and levels of mortgage

prepayments;

–

the effectiveness of risk management strategies;

–

the impact of differing levels of leverage employed;

–

liquidity of secondary markets and credit markets;

–

the availability of financing at reasonable levels and terms to

support investing on a leveraged basis;

–

the availability of new investment capital;

–

the

availability

of

suitable

qualifying

investments

from

both

an investment return and regulatory perspective;

–

changes

in

legislation

or

regulation

affecting

Fannie

Mae

and Freddie Mac (the “GSEs”) and similar federal

government agencies and related guarantees;

–

deterioration

in

credit

quality

and

ratings

of

existing

or

future

issuances of GSE or Ginnie Mae Securities; and

–

increases in costs and other general competitive factors.

2 |

Company Summary

Proven Strategy

Experienced

Management Team

Company Overview

•

We were founded in 1985 and are the oldest publicly-traded agency mortgage

REIT.

•

At

March

31,

2011,

we

had

a

total

investment

portfolio

of

$10.43

billion,

supported

by long-term investment capital of $1.19 billion levered 7.91 times.*

•

Our three-year compound annual growth rate of 15.5% exceeds that of most of

our peers.**

•

We invest in residential adjustable-rate mortgage (ARM) securities issued and

guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae.

•

Our

prudently

leveraged

portfolio

provides

financial

flexibility

to

manage

changing

market conditions.

•

Our focus on ARM securities differentiates Capstead from our peers and is

recognized as the most defensively-positioned Agency mortgage REIT.

•

We are self-managed with low operating costs and a conservative incentive

compensation structure.

•

We have over 80 years of combined mortgage finance industry experience,

including nearly 75 years at Capstead.

3

* Long-term

investment

capital

includes

stockholders’

equity

and

unsecured

borrowings,

net

of

investments

in

related

unconsolidated

affiliates.

** Compound annual growth rate is based on cumulative total returns

assuming an investment in Capstead was made December 31, 2007 and dividends were reinvested. |

Market

Snapshot (dollars in thousands, except per share amounts)

Perpetual Preferred

Trust

Total Long-Term

Common

Series A

Series B

Preferred

Investment Capital

NYSE Stock Ticker

CMO

CMOPRA

CMOPRB

Shares outstanding

(b) 77,358

187

15,819

Cost of preferred capital

11.44%

11.28%

8.49%

10.28%

Price as of May 5, 2011

$13.21

$21.57

$14.46

Book Value per common share

(b)

$12.15

Price as a multiple of March 31, 2011

book value

108.7%

Recorded value

(b)

$

915,165

$2,618

$176,703

$99,978

$1,194,464

Market capitalization as of May 5, 2011

(a)

$1,021,899

$4,034

$228,743

$99,978

$1,354,654

(a)

As of March 31, 2011.

(b)

Includes common shares issued subsequent to quarter-end. Through May 5, 2011 we raised an

additional $30 million in new common equity capital through the issuance of 2.3 million

shares under our at-the-market continuous offering

program. 4 |

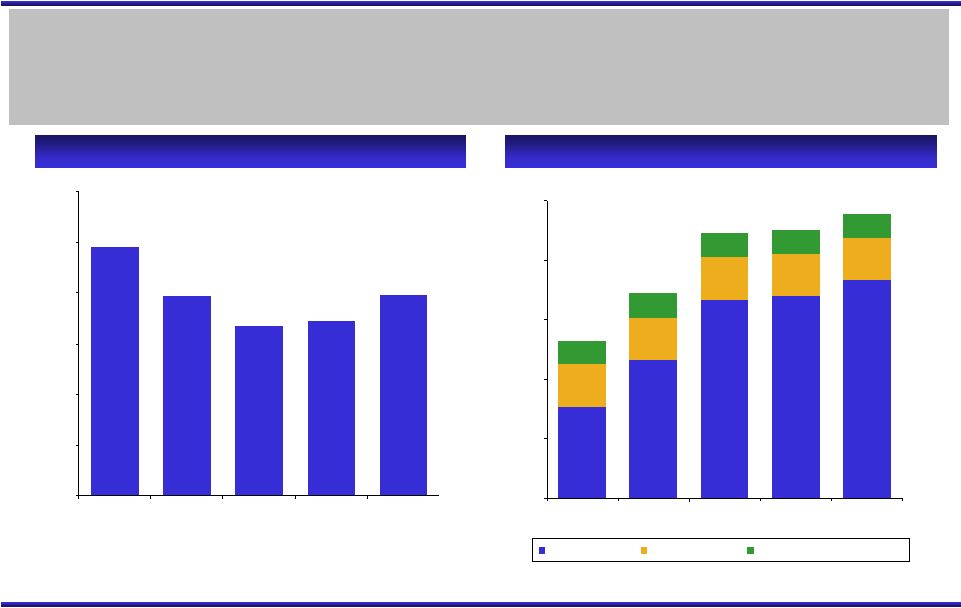

37%

63%

21%

79%

Proven Investment & Financing Strategy

5

As of March 31, 2011

As of March 31, 2011

Low

risk

agency-guaranteed

residential

ARM

securities

financed

primarily

with

30-90

day

“repo”

borrowings,

augmented with two-year interest rate swap agreements for hedging

purposes. Residential ARM Securities Portfolio

Repurchase Arrangements & Similar Borrowings

Total: $9.45 billion

* Based on fair market value as of the indicated balance sheet

date. Total:

$10.43

billion*

Most of our securities are backed by well-seasoned

mortgage loans with coupon interest rates that reset

at least annually or begin doing so after an initial

fixed-rate period of five years or less.

We have long-term relationships with numerous

lending counterparties, including 24 active

counterparties at March 31, 2011.

At March 31, 2011 we held $3.5 billion notional

amount of currently-paying

two-year

interest rate

swaps requiring fixed rate payments averaging

1.03% with average maturities of 13 months. An

additional $600 million notional amount of two-year

swaps were held at quarter-end that require fixed

rate payments averaging 0.99% beginning in May

2011.

The duration of our investment portfolio and related

‘repo’

borrowings was approximately 10 months and

6¾

months, respectively, at March 31, 2011. This

resulted in a net duration gap of approximately 3¼

months. Duration is a measure of market price

sensitivity to interest rate movements.

Longer-to-Reset

ARMs

$2.22 Billion

Current-Reset

ARMs

$8.21 Billion

Borrowings Hedged with

Currently-Paying

Interest Rate Swaps

$3.50

Billion

Unhedged

Borrowings

$5.95

Billion |

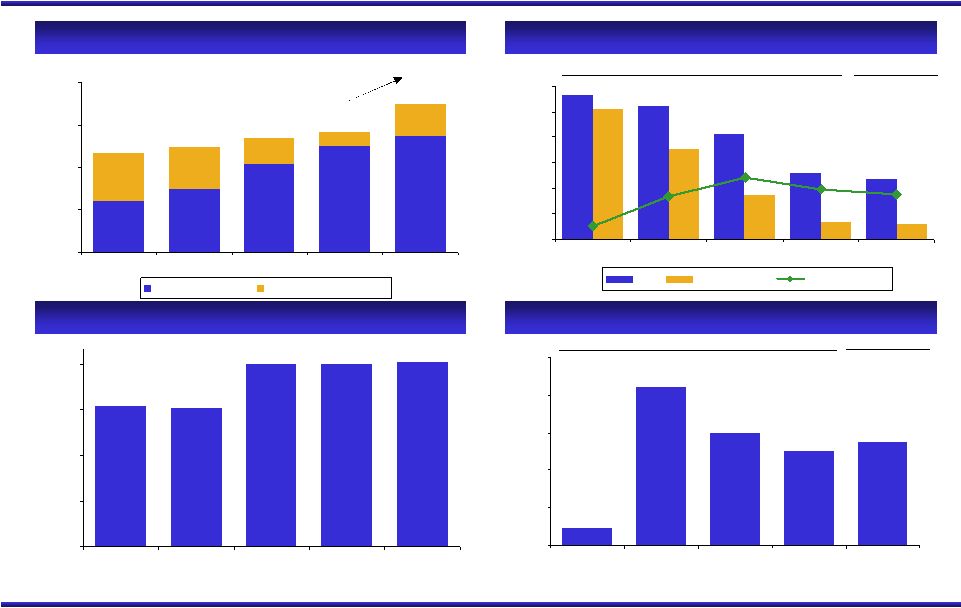

Portfolio Leverage & Long-Term Investment Capital

6

**

Borrowings under repurchase arrangements divided by long-term investment

capital. During the first quarter of 2011 we increased our portfolio leverage

one full multiple which completed the re-leveraging of our investment

capital. In our view, borrowing at current levels represents an appropriate and prudent use of leverage for an agency-guaranteed

ARM securities portfolio in today’s market conditions.

With the re-leveraging of our investment capital during the first quarter, we

began issuing new common equity capital using our at-the-market

continuous offering program. Net proceeds totaled $60 million during the first

quarter and $30 million subsequent to quarter-end through May 5,

2011. ($ in millions)

Portfolio Leverage*

Long-Term Investment Capital

$661

$860

$1,114

$1,127

$1,194

58%

67%

75%

75%

77%

27%

21%

16%

16%

15%

8%

9%

9%

12%

15%

$

$250

$500

$750

$1,000

$1,250

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

Common Stock

Preferred Stock

Trust Prefered Securities, net

9.84x

7.85x

6.67x

6.91x

7.91x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

$100

$179

$915

Common Stock

Preferred Stock

Trust Preferred Securities, net |

5.64%

5.22%

4.13%

2.60%

2.36%

0.66%

0.59%

1.73%

5.12%

3.53%

1.77%

1.94%

2.40%

1.69%

0.52%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

Yield

Borrowing Rate

Financing Spread

$7.04

$8.07

$8.52

$10.43

51%

60%

77%

88%

79%

49%

40%

23%

12%

21%

$7.44

$0.00

$3.00

$6.00

$9.00

$12.00

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

Current-Reset ARMs

Longer-to-Reset ARMs

Historical Financial Overview

7

* See page 15 for discussion of use of financing spread on mortgage assets, a

non-GAAP financial measure. ** Defined as annualized net income

available to common stockholders divided by average common equity capital.

($ in billions)

Residential ARM Securities Portfolio

Financing Spread on Mortgage Assets*

Book Value Per Common Share

Annualized Return on Average Common Equity**

$9.25

$9.14

$11.99

$12.02

$12.15

$0.00

$3.00

$6.00

$9.00

$12.00

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

2.3%

21.0%

14.9%

12.7%

13.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

12/31/07

12/31/08

12/31/09

12/31/10

3/31/11

Yield

Borrowing Rate

Financing Spread

Current-Reset ARMs

Longer-to-Reset ARMs

Year ended

Quarter ended

Quarter ended

22%

Year ended

|

Financing Spreads

0.0%

2.0%

4.0%

6.0%

8.0%

12/00

12/01

12/02

12/03

12/04

12/05

12/06

12/07

12/08

12/09

12/10

Financing spreads have largely recovered from the adverse effects of GSE buyouts of

a backlog

of

seriously

delinquent

loans

in

2010.

Portfolio

yields

fluctuate

with

levels

of

mortgage

prepayments,

portfolio

acquisitions

at

current

market

rates,

and

changes

in

coupon

interest

rates

on

ARM

loans

underlying

the

portfolio

as

they

periodically

reset

to

rates

more

reflective

of

the current interest rate environment.

Our

repo

borrowing

rates

remain

at

favorable

levels

with

average

repo

borrowing

rates

of

0.28% at March 31, 2011 (0.57% including related interest rate swaps).

* See page 15 for discussion of use of financing spread on

mortgage assets, a non-GAAP financial measure. **

Source: Bloomberg.

8

Yields on Mortgage Assets vs. Borrowing Rates

Fed Funds vs. 1-Month LIBOR**

Financing Spread on Mortgage Assets*

Yield

Borrowing Rate

Fed Funds Rate

1-Month LIBOR

0.0%

2.0%

4.0%

6.0%

8.0%

12/00

3/02

6/03

9/04

12/05

3/07

6/08

9/09

12/10

Avg. Spread on mortgage assets:

1.77%* |

First

Quarter 2011 Highlights Our earnings increased $1.7 million to $34.7 million

or $0.41 per diluted common share. Our total financing spreads decreased 9

basis points to average 1.62%, reflecting continued lower ARM loan coupon

interest rate resets, as well as marginally higher mortgage prepayments partially

offset by further declines in related borrowing rates.

Our book value increased $0.13 to $12.15 per common share.

We raised $60 million in new common equity capital using our at-the-market,

continuous offering program contributing $0.06 to the increase in book value

per common share. Our investment portfolio increased 22% or $1.91 billion to

$10.43 billion and our portfolio leverage increased to 7.9 times our

long-term investment capital. Comments from our May 4, 2011 earnings

press release: “With this quarter’s portfolio growth, we have

completed re-leveraging our investment capital, which should benefit

financial results in future quarters. In our view, borrowing at current levels

represents an appropriate and prudent use of leverage for an agency-guaranteed

mortgage securities portfolio in today’s market conditions,

particularly for a portfolio consisting almost entirely of short-

duration ARM securities. Provided capital can continue to be deployed at

attractive levels and financing

conditions

remain

favorable,

we

anticipate

maintaining

our

portfolio

leverage

near

current

levels in future quarters. We may continue augmenting our existing capital

base through our continuous offering program or by other means if conditions

warrant, focusing on transactions that are accretive to our existing common

stockholders. “We

remain

confident

in

and

focused

on

our

investment

strategy

of

managing

a

conservatively

leveraged portfolio of agency-guaranteed residential ARM securities that can

produce attractive risk- adjusted returns over the long term while

reducing, but not eliminating, sensitivity to changes in interest

rates.” 9 |

*

*

*

*

*

CAPSTEAD

Appendix

CAPSTEAD

10 |

Comparative Balance Sheet

(dollars in thousands, except per share amounts)

11

March 31,

December 31,

December 31,

December 31,

December 31,

2011

2010

2009

2008

2007

(unaudited)

Assets

Mortgage securities and similar investments

10,428,003

$

8,515,691

$

8,091,103

$

7,499,530

$

7,108,719

$

Cash collateral receivable from interest rate swap counterparties

27,650

35,289

30,485

53,676

1,800

Interest rate swap agreements at fair value

11,851

9,597

1,758

-

-

Cash and cash equivalents

162,936

359,590

409,623

96,839

6,653

Receivables and other assets

84,670

76,078

92,817

76,200

88,637

Investments in unconsolidated affiliates

3,117

3,117

3,117

3,117

3,117

10,718,227

$

8,999,362

$

8,628,903

$

7,729,362

$

7,208,926

$

Liabilities

Repurchase arrangements and similar borrowings

9,449,490

$

7,792,743

$

7,435,256

$

6,751,500

$

6,500,362

$

Cash collateral payable to interest rate swap counterparties

9,950

9,024

-

-

-

Interest rate swap agreements at fair value

13,212

16,337

9,218

46,679

2,384

Unsecured borrowings

103,095

103,095

103,095

103,095

103,095

Common stock dividend payable

30,798

27,401

37,432

22,728

9,786

Accounts payable and accrued expenses

17,196

23,337

29,961

44,910

32,382

9,623,741

7,971,937

7,614,962

6,968,912

6,648,009

Stockholders' Equity

Perpetual preferred stock

179,321

179,323

179,333

179,460

179,533

Common stock

734,822

674,202

661,724

618,369

344,423

Accumulated other comprehensive income (loss)

180,343

173,900

172,884

(37,379)

36,961

1,094,486

1,027,425

1,013,941

760,450

560,917

10,718,227

$

8,999,362

$

8,628,903

$

7,729,362

$

7,208,926

$

Book value per common share

liquidation preferences for the Series A and B preferred stock)

12.15

$12.02

$11.99

$9.14

$9.25

Long-term investment capital

unsecured borrowings, net of investments in related

unconsolidated affiliates)

$1,194,464

$1,127,403

$1,113,919

$860,428

$660,895

Portfolio leverage

divided by long-term investment capital)

7.91:1

6.91:1

6.67:1

7.85:1

9.84:1

(calculated assuming

(stockholders' equity and

(borrowings under repurchase arrangements |

Comparative Income Statement

(dollars in thousands, except per share amounts) (unaudited)

12

* Represents total runoff (scheduled payments and

prepayments). The constant prepayment rate, or CPR, represents only prepayments and will typically be 150 to 250

basis points lower than total runoff during any given period.

** See page 15 for discussion of use of financing spread on mortgage

assets, a non-GAAP financial measure. March

December

September

June

March

2011

2010

2010

2010

2010

Interest income:

Mortgage securities and similar investments

53,141

$

50,902

$

40,614

$

47,634

$

60,150

$

Other

113

140

111

135

92

53,254

51,042

40,725

47,769

60,242

Interest expense:

Repurchase arrangements and similar borrowings

(12,322)

(11,892)

(11,096)

(11,146)

(13,368)

Unsecured borrowings

(2,187)

(2,187)

(2,186)

(2,187)

(2,187)

Other

(4)

(2)

-

-

-

(14,513)

(14,081)

(13,282)

(13,333)

(15,555)

38,741

36,961

27,443

34,436

44,687

Other revenue (expense):

Miscellaneous other revenue (expense)

(218)

(174)

(427)

(98)

(205)

Incentive compensation expense

(1,233)

(1,327)

(983)

(1,330)

(1,415)

General and administrative expense

(2,663)

(2,498)

(2,424)

(3,314)

(2,695)

(4,114)

(3,999)

(3,834)

(4,742)

(4,315)

Income before equity in earnings of unconsolidated affiliates

34,627

32,962

23,609

29,694

40,372

Equity in earnings of unconsolidated affiliates

65

65

64

65

65

Net income

34,692

$

33,027

$

23,673

$

29,759

$

40,437

$

Net income per diluted common share

$0.41

$0.40

$0.27

$0.35

$0.51

Average balance of mortgage assets

8,993,926

$

8,110,095

$

7,313,810

$

7,460,379

$

7,779,081

$

Investment premium amortization

12,832

11,098

17,689

15,342

13,466

Portfolio runoff *

Average financing spread on mortgage assets**

Quarter Ended

1.77

19.9%

1.89

19.4%

2.35

31.8%

1.56

35.6%

1.91

37.9% |

Yield

/ Cost Analysis (dollars in thousands, unaudited)

13

Basis

Yield/Cost

Runoff

Basis

Yield/Cost

Runoff

Agency-guaranteed securities:

Fannie Mae/Freddie Mac:

Fixed-rate

$ 4,890

6.68%

8.9%

$ 5,106

6.60%

18.3%

ARMs

8,293,715

2.34

20.5

7,600,085

2.49

19.4

Ginnie Mae ARMs

681,375

2.59

11.8

486,215

2.57

12.7

8,979,980

2.36

19.9

8,091,406

2.50

19.0

Unsecuritized residential mortgage loans:

Fixed-rate

3,433

5.89

6.7

3,491

7.03

6.4

ARMs

7,036

3.36

21.2

7,353

3.79

7.6

10,469

4.19

17.2

10,844

4.83

7.2

Commercial loans

-

-

-

4,339

8.75

100.0

3,477

7.65

3.3

3,506

8.07

3.5

8,993,926

2.36

19.9

8,110,095

2.51

19.4

Other interest-earning assets

235,864

0.19

273,016

0.20

9,229,790

2.31

8,383,111

2.44

30-day to 90-day interest rates, as adjusted

for hedging results

8,304,926

0.59

7,465,108

0.62

Structured financings

3,477

7.65

3,506

8.07

8,308,403

0.59

7,468,614

0.62

Other interest-paying liabilites

10,344

0.16

4,323

0.19

Unsecured borrowings

103,095

8.49

103,095

8.49

8,421,842

0.69

7,576,032

0.73

Capital employed/Total financing spread

$ 807,948

1.62

$ 807,079

1.71

Financing spread on mortgage assets*

1.77

1.89

Secured borrowings based on:

Collateral for structured financings

First Quarter 2011 Average

Fourth Quarter 2010 Average

*

See

page

15

for

discussion

of

use

of

financing

spread

on

mortgage

assets,

a

non-GAAP

financial

measure. |

Fully

Indexed

Average

Months

Principal

Cost

Basis Fair Market

Net

Net

Net

to

Balance

Premiums

($)

%

Value

WAC

WAC*

Margins

Roll

Current-reset ARMs:

Fannie Mae Agency Securities

$

5,576,226

$119,468

$

5,695,694

102.14

$

5,811,784

2.75%

2.28%

1.71%

4.8

Freddie Mac Agency Securities

1,819,842

45,424

1,865,266

102.50

1,907,731

3.47

2.43

1.89

7.0

Ginnie Mae Agency Securities

460,880

5,812

466,692

101.26

475,241

2.62

1.78

1.52

5.6

Residential Mortgage Loans

6,688

23

6,711

100.34

6,611

3.46

2.40

2.05

5.0

7,863,636

170,727

8,034,363

102.17

8,201,367

2.91

2.29

1.74

5.3

Longer-to-reset ARMs:

Fannie Mae Agency Securities

985,459

30,974

1,016,433

103.14

1,022,387

3.70

2.54

1.76

43.7

Freddie Mac Agency Securities

642,284

24,468

666,752

103.81

674,4432

4.82

2.56

1.78

31.9

Ginnie Mae Agency Securities

499,728

17,628

517,356

103.53

517,978

3.65

1.78

1.51

46.9

2,127,471

73,070

2,200,541

103.43

2,214,807

4.02

2.37

1.71

40.9

$

9,991,107

$243,797

$10,234,904

102.44

$10,416,174

3.15

2.30

1.73

12.9

Residential ARM Portfolio Statistics

As of March 31, 2011 (dollars in thousands, unaudited)

14

•

Fully

indexed

net

weighted

average

coupon,

or

WAC,

represents

the

coupon

upon

one

or

more

resets

using

interest

rates

indices

as

of

March

31,

2011

and

the

applicable

net

margin. NOTE: Excludes $11 million of fixed-rate investments.

|

Financing Spread on

Mortgage Assets,

Total Financing Spread,

a

Non-GAAP

a

GAAP Measure

Financial Measure

(a)

Interest

Income

(Expense)

Yield/Cost

Difference

Interest

Income

(Expense)

Yield/Cost

Corresponding

Fourth Quarter

2010

Yield/Cost

Interest income:

Mortgage assets

$

53,141

2.36%

$

–

$

53,141

2.36%

2.51%

Other interest-earning assets

(b)

113

0.19

(113)

–

–

–

53,254

2.31

(113)

53,141

2.36

2.51

Interest expense:

Secured borrowings (borrowings under

repurchase arrangements)

(12,322)

0.59

–

(12,322)

0.59

0.62

Unsecured borrowings

(c)

(2,187)

8.49

2,187

–

–

–

Other interest-paying liabilities

(d)

(4)

0.16

4

–

–

–

(14,513)

0.69

2,191

(12,322)

0.59

0.62

Net interest margin/financing spread

$

38,741

1.62

$

2,078

$

40,819

1.77

1.89

Use of Financing Spread on Mortgage Assets,

a Non-GAAP Financial Measure

First Quarter 2011 (dollars in thousands, unaudited)

15

(a)

Net

interest

margin

on

mortgage

assets

and

Financing

spread

on

mortgage

assets

are

non-GAAP

financial

measures

(based

solely

on

interest

income

and

yields

on

the

Company’s

portfolio

of

mortgage

securities,

net

of

borrowings

under

repurchase

agreements).

These

measures

are

similar

to

the

all-inclusive

GAAP

measures,

Total

net

interest

margin

and

Total

financing

spread

(based

on

all

interest-earning

assets

and

all

interest-bearing

liabilities).

(b)

Other

interest-earning

assets

consist

of

overnight

investments

and

cash

collateral

receivable

from

interest

rate

swap

counterparties.

(c)

Unsecured

borrowings

consist

of

junior

subordinated

notes

with

original

terms

of

30

years

issued

in

2005

and

2006

by

Capstead

to

statutory

trusts

formed

to

issue

$3.1

million

of

the

trusts’

common

securities

to

Capstead

and

to

privately

place

$100.0

million

of

preferred

securities

to

unrelated

third

party

investors.

Capstead

reflects

its

investment

in

the

trusts

as

unconsolidated

affiliates

and

considers

the

unsecured

borrowings,

net

of

these

affiliates,

a

component

of

its

long-term

investment

capital.

(d)

Other

interest-paying

liabilities

consist

of

cash

collateral

payable

to

interest

rate

swap

counterparties. |

Experienced Management Team

16

Over 80 years of combined mortgage finance industry experience, including nearly 75

years at Capstead Andrew F. Jacobs –

President and Chief Executive Officer, Director

–

Has served as president and chief executive officer since 2003 and has held various

executive positions at Capstead since 1988 –

Certified Public Accountant (“CPA”), member of the Board of Governors of

the National Association of Real Estate Investment Trusts

(“NAREIT”), chairman of NAREIT’s Council of Mortgage REITs, member

of the executive committee of the Chancellors Council of the University of

Texas System, the Executive Council of the Real Estate Finance and Investment Center at the University of Texas

at Austin, the American Institute of Certified Public Accountants

(“AICPA”), and the Financial Executive International (“FEI”)

Phillip A. Reinsch

–

Executive Vice President and Chief Financial Officer, Secretary

–

Has

held

various

financial

accounting

and

reporting

positions

at

Capstead

since

1993

–

Formerly employed by Ernst & Young LLP as an audit senior manager focusing on

mortgage banking and asset securitization –

CPA, Member AICPA, FEI

Robert A. Spears

–

Executive Vice President, Director of Residential Mortgage Investments

–

Has served in asset and liability management positions at Capstead since 1994

–

Formerly Vice President of secondary marketing with NationsBanc Mortgage

Corporation Michael W. Brown –

Senior Vice President, Asset and Liability Management, Treasurer

–

Has served in asset and liability management positions at Capstead since 1994

–

MBA, Southern Methodist University, Dallas, Texas |