Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - PHOENIX COMPANIES INC/DE | pnx_8k.htm |

Exhibit 99.1

1

As of March 31, 2011

The Phoenix Companies, Inc.

Investment Portfolio Supplement

Investment Portfolio Supplement

2

Important disclosures

This presentation may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. We intend these

forward-looking statements to be covered by the safe harbor provisions of the federal securities laws relating to forward-looking statements. These forward-

looking statements include statements relating to trends in, or representing management’s beliefs about, our future transactions, strategies, operations and

financial results, and often contain words such as “will,” “anticipate,” “believe,” “plan,” “estimate,” “expect,” “intend,” “may,” “should” and other similar words or

expressions. Forward-looking statements are made based upon management’s current expectations and beliefs concerning trends and future developments

and their potential effects on us. They are not guarantees of future performance. Our actual business, financial condition or results of operations may differ

materially from those suggested by forward-looking statements as a result of risks and uncertainties, which include, among others: (i) unfavorable general

economic developments including, but not limited to, specific related factors such as the performance of the debt and equity markets and changes in interest

rates; (ii) the potential adverse affect of interest rate fluctuations on our business and results of operations; (iii) the effect of adverse capital and credit market

conditions on our ability to meet our liquidity needs, our access to capital and our cost of capital; (iv) the effect of guaranteed benefits within our products; (v)

potential exposure to unidentified or unanticipated risk that could adversely affect our businesses or result in losses; (vi) the consequences related to variations

in the amount of our statutory capital due to factors beyond our control; (vii) the possibility that we not be successful in our efforts to implement a new business

plan; (viii) the impact on our results of operations and financial condition of any required increase in our reserves for future policyholder benefits and claims if

such reserves prove to be inadequate; (ix) changes in our investment valuations based on changes in our valuation methodologies, estimations and

assumptions; (x) further downgrades in our debt or financial strength ratings; (xi) the possibility that mortality rates, persistency rates, funding levels or other

factors may differ significantly from our assumptions used in pricing products; (xii) the availability, pricing and terms of reinsurance coverage generally and the

inability or unwillingness of our reinsurers to meet their obligations to us specifically; (xiii) our ability to attract and retain key personnel in a competitive

environment; (xiv) our dependence on third parties to maintain critical business and administrative functions; (xv) the strong competition we face in our

business from banks, insurance companies and other financial services firms; (xvi) our reliance, as a holding company, on dividends and other payments from

our subsidiaries to meet our financial obligations and pay future dividends, particularly since our insurance subsidiaries' ability to pay dividends is subject to

regulatory restrictions; (xvii) the potential need to fund deficiencies in our closed block; (xviii) tax developments that may affect us directly, or indirectly through

the cost of, the demand for or profitability of our products or services; (xix) the possibility that the actions and initiatives of the U.S. Government, including

those that we elect to participate in, may not improve adverse economic and market conditions generally or our business, financial condition and results of

operations specifically; (xx) legislative or regulatory developments; (xxi) regulatory or legal actions; (xxii) potential future material losses from our discontinued

reinsurance business; (xxiii) changes in accounting standards; (xxiv) the potential effect of a material weakness in our internal control over financial reporting

on the accuracy of our reported financial results; and (xxv) other risks and uncertainties described herein or in any of our filings with the SEC.

forward-looking statements to be covered by the safe harbor provisions of the federal securities laws relating to forward-looking statements. These forward-

looking statements include statements relating to trends in, or representing management’s beliefs about, our future transactions, strategies, operations and

financial results, and often contain words such as “will,” “anticipate,” “believe,” “plan,” “estimate,” “expect,” “intend,” “may,” “should” and other similar words or

expressions. Forward-looking statements are made based upon management’s current expectations and beliefs concerning trends and future developments

and their potential effects on us. They are not guarantees of future performance. Our actual business, financial condition or results of operations may differ

materially from those suggested by forward-looking statements as a result of risks and uncertainties, which include, among others: (i) unfavorable general

economic developments including, but not limited to, specific related factors such as the performance of the debt and equity markets and changes in interest

rates; (ii) the potential adverse affect of interest rate fluctuations on our business and results of operations; (iii) the effect of adverse capital and credit market

conditions on our ability to meet our liquidity needs, our access to capital and our cost of capital; (iv) the effect of guaranteed benefits within our products; (v)

potential exposure to unidentified or unanticipated risk that could adversely affect our businesses or result in losses; (vi) the consequences related to variations

in the amount of our statutory capital due to factors beyond our control; (vii) the possibility that we not be successful in our efforts to implement a new business

plan; (viii) the impact on our results of operations and financial condition of any required increase in our reserves for future policyholder benefits and claims if

such reserves prove to be inadequate; (ix) changes in our investment valuations based on changes in our valuation methodologies, estimations and

assumptions; (x) further downgrades in our debt or financial strength ratings; (xi) the possibility that mortality rates, persistency rates, funding levels or other

factors may differ significantly from our assumptions used in pricing products; (xii) the availability, pricing and terms of reinsurance coverage generally and the

inability or unwillingness of our reinsurers to meet their obligations to us specifically; (xiii) our ability to attract and retain key personnel in a competitive

environment; (xiv) our dependence on third parties to maintain critical business and administrative functions; (xv) the strong competition we face in our

business from banks, insurance companies and other financial services firms; (xvi) our reliance, as a holding company, on dividends and other payments from

our subsidiaries to meet our financial obligations and pay future dividends, particularly since our insurance subsidiaries' ability to pay dividends is subject to

regulatory restrictions; (xvii) the potential need to fund deficiencies in our closed block; (xviii) tax developments that may affect us directly, or indirectly through

the cost of, the demand for or profitability of our products or services; (xix) the possibility that the actions and initiatives of the U.S. Government, including

those that we elect to participate in, may not improve adverse economic and market conditions generally or our business, financial condition and results of

operations specifically; (xx) legislative or regulatory developments; (xxi) regulatory or legal actions; (xxii) potential future material losses from our discontinued

reinsurance business; (xxiii) changes in accounting standards; (xxiv) the potential effect of a material weakness in our internal control over financial reporting

on the accuracy of our reported financial results; and (xxv) other risks and uncertainties described herein or in any of our filings with the SEC.

This information is provided as of March 31, 2011. Certain other factors which may impact our business, financial condition or results of operations or which

may cause actual results to differ from such forward-looking statements are discussed or included in our periodic reports filed with the SEC and are available

on our Web site, www.phoenixwm.com in the Investor Relations section. You are urged to carefully consider all such factors. We do not undertake or plan to

update or revise forward-looking statements to reflect actual results, changes in plans, assumptions, estimates or projections, or other circumstances occurring

after the date of this presentation, even if such results, changes or circumstances make it clear that any forward-looking information will not be realized. If we

make any future public statements or disclosures which modify or impact any of the forward-looking statements contained in or accompanying this

presentation, such statements or disclosures will be deemed to modify or supersede such statements in this presentation.

may cause actual results to differ from such forward-looking statements are discussed or included in our periodic reports filed with the SEC and are available

on our Web site, www.phoenixwm.com in the Investor Relations section. You are urged to carefully consider all such factors. We do not undertake or plan to

update or revise forward-looking statements to reflect actual results, changes in plans, assumptions, estimates or projections, or other circumstances occurring

after the date of this presentation, even if such results, changes or circumstances make it clear that any forward-looking information will not be realized. If we

make any future public statements or disclosures which modify or impact any of the forward-looking statements contained in or accompanying this

presentation, such statements or disclosures will be deemed to modify or supersede such statements in this presentation.

3

Table of contents

Page(s)

Summary 4

Total Invested Assets 5

Historical Portfolio Ratings 6

Bond Portfolio Detail 7 - 8

Alternative Asset Detail 9

Structured Securities Portfolio 10

Realized Credit Impairment Losses 11

Unrealized Gains/Losses 12

Commercial Mortgage-Backed Securities (CMBS) 13 - 14

Residential Mortgage-Backed Securities (RMBS) 15 - 18

Collateralized Debt Obligations (CDO) Holdings 19

Appendix: 20 - 23

Phoenix Life Insurance Company (PLIC) Closed Block

4

Summary

> General account investment portfolio is well diversified and liquid; managed by a team with a

successful track record of investing over a variety of market cycles, following a disciplined monitoring

process

successful track record of investing over a variety of market cycles, following a disciplined monitoring

process

> Approximately 92% of bond investments are investment grade. Emphasis is on liquidity with 72% of

bonds invested in public securities

bonds invested in public securities

> Strict limits on individual financial exposures that mitigate loss potential to any one particular entity; as

a result, there is limited exposure to the financial institutions that have been in the news

a result, there is limited exposure to the financial institutions that have been in the news

> Net unrealized gains of $314 million versus $266 million at year-end 2010

> Residential mortgage-backed securities (RMBS) exposure is high quality and diversified. Exposure is

concentrated in agency and non agency prime-rated securities

concentrated in agency and non agency prime-rated securities

> Commercial mortgage exposure is in highly rated commercial mortgage-backed securities with

minimal direct loan or real estate holdings

minimal direct loan or real estate holdings

> No credit default swap (CDS) exposure

As of March 31, 2011

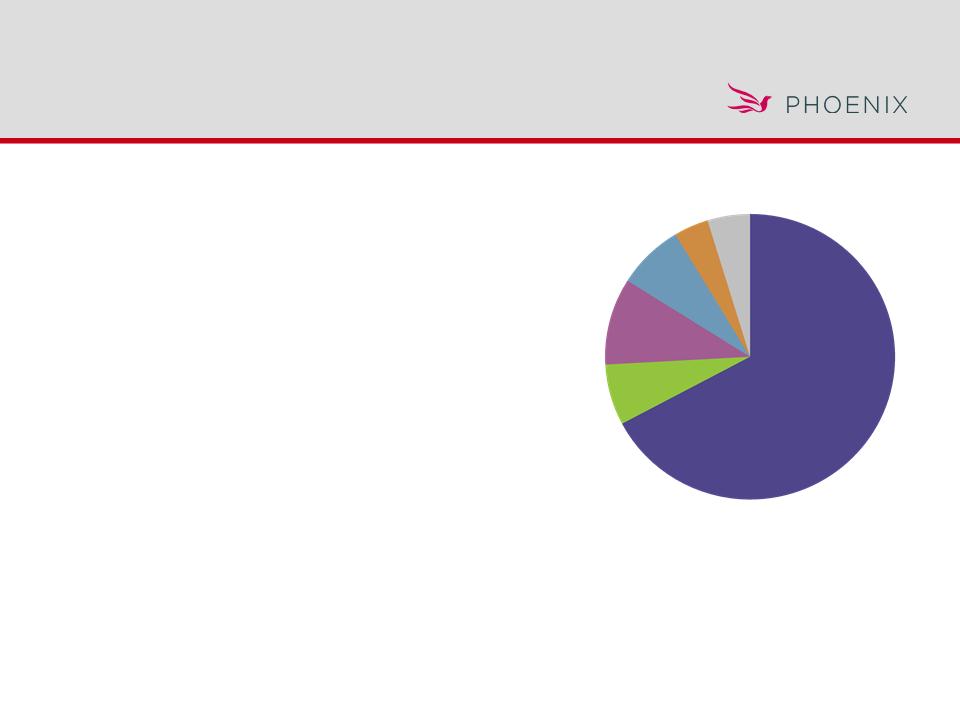

5

Portfolio comprised

primarily of fixed income securities

primarily of fixed income securities

Bonds $11,160

77%

Policy Loans $2,374

16%

Cash & Cash Equivalents $107 1%

Private Equity $226 2%

Stock $52 0%

Other Invested Assets $404 3%

Mezzanine Funds $178 1%

Total Invested Assets: $14.5 Billion

$ in millions

Market value as of March 31, 2011

6

Portfolio quality improved

Percentages based on GAAP Value

As of March 31, 2011

|

|

1Q10

|

2Q10

|

3Q10

|

4Q10

|

1Q11

|

|

Investment Grade Bonds

|

89.9%

|

90.9%

|

91.0%

|

91.3%

|

91.8%

|

|

Below Investment Grade (BIG) Bonds

|

10.1

|

9.1

|

9.0

|

8.7

|

8.2

|

|

Percentage of BIG in NAIC 3

|

53.8

|

55.1

|

59.0

|

49.5

|

51.1

|

|

Percentage of BIG in NAIC 4-6

|

46.2

|

44.9

|

41.0

|

50.5

|

48.9

|

|

Corporate

|

|

|

|

|

|

|

Investment Grade

|

90.3

|

91.0

|

91.1

|

91.2

|

91.9

|

|

Below Investment Grade

|

9.7

|

9.0

|

8.9

|

8.8

|

8.1

|

|

Structured

|

|

|

|

|

|

|

Investment Grade

|

89.6

|

90.7

|

91.0

|

91.3

|

91.5

|

|

Below Investment Grade

|

10.4

|

9.3

|

9.0

|

8.7

|

8.5

|

7

RMBS

6%

CMBS 4%

$ in millions

Market value as of March 31, 2011

1 Includes $231.9 million of Home Equity Asset Backed Securities also included in the RMBS exhibits

2 Includes $36.5 million of CMBS CDO’s also included in the CMBS exhibits

Bond portfolio diversified by sector

U.S. Corporates

56%

Foreign Corporates

7%

ABS 4%

Emerging Markets

3%

Below Investment Grade (BIG) Bonds

by Sector

|

As of March 31, 2011

|

Market Value |

% of Total |

|

Industrials

|

$2,463.6

|

22.1

|

|

Residential MBS1

|

2,112.2

|

18.9

|

|

Foreign Corporates

|

1,598.3

|

14.3

|

|

Financials

|

1,500.6

|

13.5

|

|

Commercial MBS

|

1,174.1

|

10.5

|

|

U.S. Treasuries / Agencies

|

719.4

|

6.4

|

|

Asset Backed Securities

|

519.7

|

4.7

|

|

Utilities

|

504.7

|

4.5

|

|

CBO/CDO/CLO2

|

253.8

|

2.3

|

|

Municipals

|

213.0

|

1.9

|

|

Emerging Markets

|

100.1

|

0.9

|

|

Total

|

$11,159.5

|

|

Bonds by Rating

NAIC 1

59.0%

NAIC 2

32.8%

NAIC 3 & Lower

(BIG)

(BIG)

8.2%

CDO/CLO

20%

8

Top 10 fixed income holdings

|

Issuer |

Market

Value

|

% of

Fixed Income

|

Issuer

Rating

|

|

Bank of America Corp

|

$59.4

|

0.5%

|

A2/A

|

|

Wells Fargo

|

47.6

|

0.4

|

Aa2/AA

|

|

General Electric

|

41.6

|

0.4

|

Aa2/AA+

|

|

Citigroup

|

39.2

|

0.4

|

A3/A

|

|

AT&T Corporation

|

36.4

|

0.3

|

A2/A-

|

|

Walgreens

|

34.6

|

0.3

|

A2/A

|

|

Riverside Health System

|

34.5

|

0.3

|

A2/A

|

|

Berkshire Hathaway Inc.

|

34.4

|

0.3

|

Aa2/AA+

|

|

Reed Elsevier Inc.

|

31.5

|

0.3

|

Baa1/BBB+

|

|

Enterprise Products

|

30.4

|

0.3

|

Baa3/BBB-

|

$ in millions

As of March 31, 2011

9

Alternative asset balances

|

|

12/31/2010 |

3/31/2011 |

|

Private Equity

|

$220.0

|

$225.7

|

|

Mezzanine Funds

|

187.5

|

177.8

|

|

Infrastructure Funds

|

33.5

|

34.4

|

|

Hedge Fund of Funds

|

30.3

|

31.3

|

|

Other

|

38.3

|

37.8

|

|

Leveraged Lease

|

28.1

|

28.3

|

|

Mortgage & Real Estate Funds

|

14.8

|

19.0

|

|

Direct Equity

|

15.2

|

15.5

|

|

|

$567.7

|

$569.8

|

$ in millions

As of March 31, 2011

10

High quality

structured securities portfolio

structured securities portfolio

> Structured portfolio is 91.5% investment grade

> RMBS (46.3%) and CMBS (28.9%) dominate the structured portfolio

AAA

67.3%

B or less - 4.8%

BBB - 7.7%

AA - 7.0%

A - 9.5%

BB - 3.7%

$ in millions

Market value as of March 31, 2011, Quality rating breakdown based on NAIC ratings

1 Includes $36.5 million of CMBS CDOs

|

As of March 31, 2011

|

Market Value |

% of Total

|

|

Residential MBS

|

$ 1,880.3

|

46.3

|

|

Commercial MBS

|

1,174.1

|

28.9

|

|

Other ABS

|

264.4

|

6.5

|

|

CBO/CDO/CLO1

|

253.8

|

6.3

|

|

Home Equity

|

231.9

|

5.7

|

|

Auto Loans

|

163.4

|

4.0

|

|

Aircraft Equipment Trust

|

56.1

|

1.4

|

|

Manufactured Housing

|

35.8

|

0.9

|

|

Total

|

$4,059.8

|

|

11

Moderation in credit impairments

GAAP Credit Impairments

|

|

1Q10

|

2Q10

|

3Q10

|

4Q10

|

1Q11

|

|

Prime RMBS

|

$0.7

|

$1.9

|

-

|

$1.6

|

-

|

|

Alt-A RMBS

|

4.6

|

2.4

|

0.5

|

2.5

|

1.0

|

|

Subprime RMBS

|

0.1

|

-

|

-

|

1.5

|

0.3

|

|

CLO/CDO

|

5.5

|

3.4

|

3.6

|

3.5

|

-

|

|

CMBS

|

1.4

|

0.7

|

2.9

|

1.7

|

-

|

|

Corporate

|

1.9

|

1.7

|

1.1

|

-

|

4.4

|

|

Other ABS/MBS

|

-

|

2.1

|

3.7

|

-

|

-

|

|

Total Debt

|

$14.2

|

$12.2

|

$11.8

|

$10.8

|

$5.7

|

|

Schedule BA

|

-

|

-

|

-

|

-

|

-

|

|

Equity

|

0.3

|

0.2

|

0.1

|

-

|

-

|

|

Total Credit Impairments

|

$14.5

|

$12.4

|

$11.9

|

$10.8

|

$5.7

|

$ in millions

As of March 31, 2011

12

Portfolio in a gain position

$ in millions

1 Market value of $1,174.1 million includes $36.5 million of CMBS CDO’s

2 All Other - Corporates, RMBS Agency, Other ABS, Foreign, US Government

|

|

12/31/2010

Unrealized

|

3/31/2011

Unrealized

|

3/31/2011

Invested Assets |

|

RMBS Prime

|

$(21.2)

|

$(10.8)

|

$535.7

|

|

Subprime/Alt-A

|

(58.5)

|

$(51.0)

|

499.4

|

|

CDO/CLO1

|

(47.9)

|

(36.1)

|

253.8

|

|

CMBS

|

24.5

|

31.7

|

1,174.1

|

|

Financial

|

(25.2)

|

(0.2)

|

1,500.5

|

|

All Other High Yield

|

0.9

|

4.9

|

434.4

|

|

All Other2

|

393.5

|

375.4

|

6,761.6

|

|

Total

|

$266.1

|

$313.9

|

$11,159.5

|

13

Highly rated, seasoned

CMBS portfolio

CMBS portfolio

> $1.2 billion in market value

> $140.3 million or 11.6% Government

guaranteed

guaranteed

> 77.3% AAA and 3.2% BB and below

> 71.1% 2005 and prior origination

> Only 3% in CMBS CDO’s

Market value as of March 31, 2011

Percentages based on market value

$ in millions

14

Well constructed CMBS portfolio

Phoenix CMBS Portfolio

> High levels of credit enhancement

> Excellent credit characteristics vs.

market

market

> Avoided 2006 and 2007 aggressive

underwriting

underwriting

|

|

Market1

|

Phoenix

|

|

Weighted average credit

enhancement |

27%

|

29%

|

|

Weighted average credit

enhancement (U.S. Treasury defeasance adjusted) |

28%

|

33%

|

|

Interest Only (I/O) loans

|

67%

|

34%

|

|

Weighted average coupon

|

5.74%

|

6.28%

|

|

Weighted average loan age

|

65 months

|

85 months

|

|

60+ Delinquency Rate

|

8.3%

|

5.6%

|

As of March 31, 2011

1Sources: Barclays CMBS Index, Trepp, Bloomberg

15

High quality, diversified RMBS portfolio

$ in millions

Market value as of March 31, 2011

|

Rating |

Book Value |

Market Value |

% General Account |

AAA |

AA |

A |

BBB |

BB &

Below |

|

Agency

|

$1,047.0

|

$1,077.1

|

7.4%

|

100.0% |

-

|

-

|

-

|

-

|

|

Prime

|

546.5

|

535.7

|

3.7%

|

57.7%

|

11.9%

|

3.6%

|

1.4%

|

25.4%

|

|

Alt-A

|

346.2

|

314.8

|

2.2%

|

43.8%

|

17.8%

|

6.2%

|

4.1%

|

28.1%

|

|

Subprime

|

204.2

|

184.6

|

1.3%

|

55.8%

|

17.9%

|

-

|

7.4%

|

18.9%

|

|

Total

|

$2,143.9

|

$2,112.2

|

14.6%

|

77.0%

|

7.2%

|

1.9%

|

1.6%

|

12.3%

|

16

High quality, seasoned

non-agency prime RMBS holdings

non-agency prime RMBS holdings

> $535.7 million market value

> 70% AAA and AA rated

> 82% 2005 and prior origination

> 93.8% fixed rate vs. 47% for the market

> Phoenix 60+ day delinquent 7.5% vs.

13.4% for the prime RMBS market

13.4% for the prime RMBS market

$ in millions

As of March 31, 2011

Source: JPM MBS Research

17

Well constructed

non-agency prime RMBS portfolio

non-agency prime RMBS portfolio

As of March 31, 2011

Source: JP Morgan MBS Research - March 2011, Bloomberg

Market Phoenix

Weighted average credit enhancement 4.0% 10.3%

Weighted average 60+ day delinquent loan 13.4% 7.5%

Phoenix prime portfolio loss coverage: using 40% loss severity 0.75x 3.4x

18

Seasoned

non-agency Alt-A RMBS holdings

non-agency Alt-A RMBS holdings

> $314.8 million market value

> 62% AAA or AA rated

> 82% 2005 and prior originations

> 100% fixed rate collateral vs. 34% for market

> Phoenix 60+ day delinquent 15.2% vs.

28.4% for Alt-A market

28.4% for Alt-A market

$ in millions

Market value as of March 31, 2011

Source: JPM MBS Research

19

Diversified CDO holdings

$ in millions

No affiliated CDO holdings as of March 31, 2011

Percentages based on market value

|

Collateral |

Book

Value |

Market

Value |

% General

Account |

AAA |

AA |

A |

BBB |

BB &

Below |

|

Bank Loans

|

$231.1

|

$213.3

|

1.5%

|

3.2%

|

4.9%

|

14.5%

|

23.6%

|

53.8%

|

|

Inv Grade Debt

|

4.5

|

4.0

|

-

|

-

|

12.4%

|

-

|

87.6%

|

-

|

|

CMBS

|

54.3

|

36.5

|

0.3%

|

9.8%

|

56.4%

|

5.9%

|

20.0%

|

7.9%

|

|

Total

|

$289.9

|

$253.8

|

1.8%

|

4.1%

|

12.4%

|

13.0%

|

24.1%

|

46.4%

|

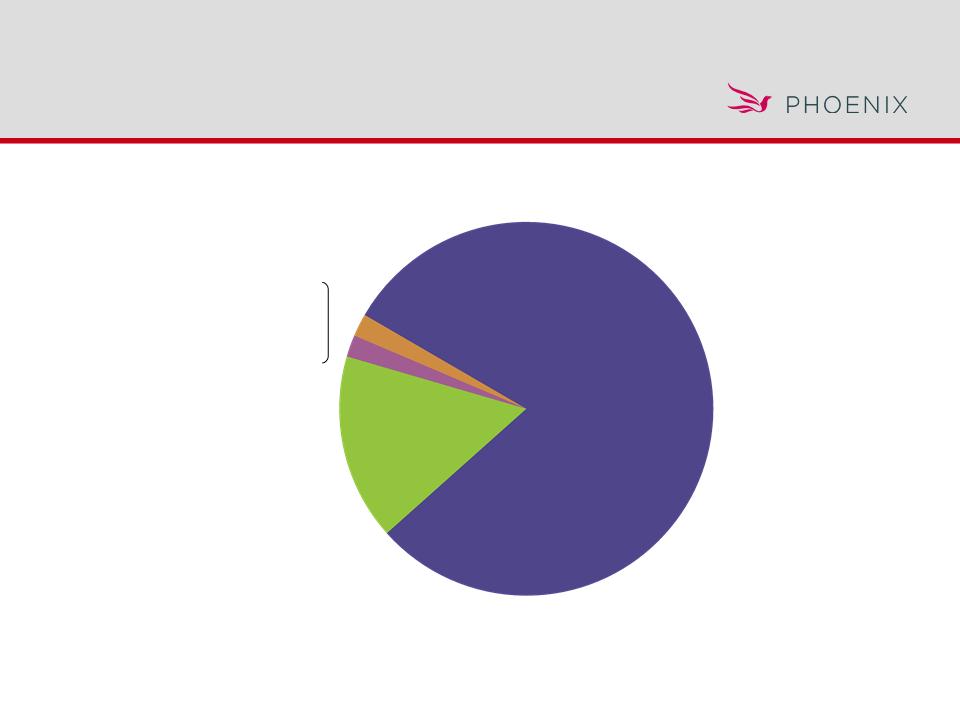

Appendix

21

PLIC Closed Block investments

primarily fixed income

primarily fixed income

Bonds $6,385

79%

Policy Loans $1,315

16%

Cash & Cash Equivalents $11 0%

Private Equity $215 3%

Stock $22 0%

Mezzanine Funds $80 1%

Other Invested Assets $58 1%

Invested Assets: $8.1 Billion

$ in millions

Market value as of March 31, 2011

22

PLIC Closed Block

portfolio high quality

portfolio high quality

Percentages based on GAAP Value

As of March 31, 2011

|

|

1Q10

|

2Q10

|

3Q10

|

4Q10

|

1Q11

|

|

Investment Grade Bonds

|

92.0%

|

92.5%

|

92.6%

|

92.9%

|

93.1%

|

|

Below Investment Grade (BIG) Bonds

|

8.0

|

7.5

|

7.4

|

7.1

|

6.9

|

|

Percentage of BIG in NAIC 3

|

62.1

|

62.6

|

67.3

|

59.4

|

59.8

|

|

Percentage of BIG in NAIC 4-6

|

37.9

|

37.4

|

32.7

|

40.6

|

40.2

|

|

Public Bonds

|

68.2

|

67.5

|

66.5

|

67.0

|

67.3

|

|

Private Bonds

|

31.8

|

32.5

|

33.5

|

33.0

|

32.7

|

23

PLIC Closed Block

portfolio diversified

portfolio diversified

U.S. Corporates

60%

Foreign Corporates

8%

ABS - 3%

Emerging Markets -5%

$ in millions

Market value as of March 31, 2011

1 Includes $35.7 million of Home Equity Asset Backed Securities

2 Includes $21.4 million of CMBS CDO’s

Below Investment Grade (BIG) Bonds

by Sector

|

Bond Portfolio

Phoenix Closed Block

|

|

|

|

As of March 31, 2011

|

|

|

|

Industrials

|

$1,631.6

|

25.6%

|

|

Foreign Corporates

|

989.9

|

15.5

|

|

Residential MBS1

|

978.5

|

15.3

|

|

Financials

|

912.9

|

14.3

|

|

Commercial MBS

|

678.5

|

10.6

|

|

U.S. Treasuries / Agencies

|

432.6

|

6.8

|

|

Utilities

|

325.7

|

5.1

|

|

Asset Backed Securities

|

130.9

|

2.1

|

|

Municipals

|

130.5

|

2.0

|

|

CBO/CDO/CLO’s2

|

98.0

|

1.5

|

|

Emerging Markets

|

75.5

|

1.2

|

|

Total

|

$6,384.6

|

|

Bonds by Rating

NAIC 1

58.1%

NAIC 2

35.0%

NAIC 3 & Lower

6.9%

RMBS - 7%

CLO/CDO

14%

CMBS - 3%