Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-34574

TRANSATLANTIC PETROLEUM LTD.

(Exact name of registrant as specified in its charter)

| Bermuda | None | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| Akmerkez B Blok Kat 5-6 Nisbetiye Caddesi 34330 Etiler, Istanbul, Turkey |

None | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: +90 212 317 25 00

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common shares, par value $0.01 | NYSE Amex |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | þ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of common shares, par value $0.01, held by nonaffiliates of the registrant, based on the last sale price of the common shares on June 30, 2010 (the last business day of the registrant’s most recently completed second fiscal quarter), was approximately $482.5 million. For purposes of this computation, all officers, directors and 10% beneficial owners of the registrant are deemed to be affiliates. Such determination should not be deemed an admission that such officers, directors or 10% beneficial owners are, in fact, affiliates of the registrant.

As of April 15, 2011, there were 346,234,355 common shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Annual Report on Form 10-K, to the extent not set forth herein, is incorporated by reference to the registrant’s definitive proxy statement relating to the 2011 Annual Meeting of Shareholders which will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Annual Report on Form 10-K relates.

Table of Contents

TRANSATLANTIC PETROLEUM LTD.

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

i

Table of Contents

Forward-Looking Statements

Certain statements in this Annual Report on Form 10-K constitute “forward-looking statements” within the meaning of applicable U.S. and Canadian securities legislation. Additionally, forward-looking statements may be made orally or in press releases, conferences, reports, on our website or otherwise, in the future, by us or on our behalf. Such statements are generally identifiable by the terminology used such as “plans,” “expects,” “estimates,” “budgets,” “intends,” anticipates,” “believes,” “projects,” “indicates,” “targets,” “objective,” “could,” “should,” “may” or other similar words.

By their very nature, forward-looking statements require us to make assumptions that may not materialize or that may not be accurate. Forward-looking statements are subject to known and unknown risks and uncertainties and other factors that may cause actual results, levels of activity and achievements to differ materially from those expressed or implied by such statements. Such factors include, among others: fluctuations in and volatility of the market prices for natural gas, natural gas liquids and oil products; the ability to produce and transport natural gas, natural gas liquids and oil; the results of exploration and development drilling and related activities; global economic conditions, particularly in the countries and provinces in which we carry on business, especially economic slowdowns; actions by governmental authorities including increases in taxes, changes in environmental and other regulations, and renegotiations of contracts; political uncertainty, including actions by insurgent groups or other conflict; the negotiation and closing of material contracts; future capital requirements and availability of financing; estimates and economic assumptions used in connection with our acquisitions; risks associated with drilling and operating wells; actions of third party co-owners of interests in properties in which we also own an interest; our ability to effectively integrate companies and properties that we acquire; and the other factors discussed in other documents that we file with or furnish to the U.S. Securities and Exchange Commission (the “SEC”) and Canadian securities regulatory authorities. The impact of any one factor on a particular forward-looking statement is not determinable with certainty as such factors are interdependent upon other factors; our course of action would depend upon our assessment of the future considering all information then available. In that regard, any statements as to future natural gas or oil production levels; capital expenditures; the allocation of capital expenditures to exploration and development activities; sources of funding for our capital program; drilling of new wells; demand for natural gas and oil products; expenditures and allowances relating to environmental matters; dates by which certain areas will be developed or will come on-stream; expected finding and development costs; future production rates; ultimate recoverability of reserves; dates by which transactions are expected to close; future cash flows; uses of cash flows; collectibility of receivables; availability of trade credit; expected operating costs; changes in any of the foregoing and other statements using forward-looking terminology are forward-looking statements, and there can be no assurance that the expectations conveyed by such forward-looking statements will, in fact, be realized.

Although we believe that the expectations conveyed by the forward-looking statements are reasonable based on information available to us on the date such forward-looking statements were made, no assurances can be given as to future results, levels of activity, achievements or financial condition.

Readers should not place undue reliance on any forward-looking statement and should recognize that the statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described above, as well as others not now anticipated. The foregoing statements are not exclusive and further information concerning us, including factors that potentially could materially affect our financial results, may emerge from time to time. We do not intend to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

ii

Table of Contents

Glossary of selected oil and natural gas terms

The following are abbreviations and definitions of terms commonly used in the oil and natural gas industry and this Annual Report on Form 10-K.

2D seismic. Geophysical data that depict the subsurface strata in two dimensions.

3D seismic. Geophysical data that depict the subsurface strata in three dimensions. 3D seismic typically provides a more detailed and accurate interpretation of the subsurface strata than 2D, or two-dimensional, seismic.

Appraisal wells. Wells drilled to convert an area or sub-region from the resource to the reserves category.

Bbl. One stock tank barrel, or 42 U.S. gallons liquid volume, used in reference to oil or other liquid hydrocarbons.

Bcf. One billion cubic feet of natural gas.

Boe. Barrels of oil equivalent. Boe is not included in the DeGolyer and MacNaughton report and is derived by the Company by converting natural gas to oil in the ratio of six Mcf of natural gas to one Bbl of oil. The conversion factor is the current convention used by many oil and gas companies. Boe may be misleading, particularly if used in isolation. A Boe conversion ratio of six Mcf to one Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Commercial well; commercially productive well. An oil and natural gas well which produces oil and natural gas in sufficient quantities such that proceeds from the sale of such production exceed production expenses and taxes.

Completion. The installation of permanent equipment for the production of oil or natural gas, or, in the case of a dry hole, the reporting of abandonment to the appropriate agency.

Developed acreage. The number of acres which are allocated or assignable to producing wells or wells capable of production.

Development well. A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

Dry hole; dry well. A well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas well.

Exploitation. The continuing development of a known producing formation in a previously discovered field. To maximize the ultimate recovery of oil or natural gas from the field by development wells, secondary recovery equipment or other suitable processes and technology.

Exploratory well. A well drilled to find a new field or to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir. Generally, an exploratory well is any well that is not a development well.

Farm-in or farm-out. An assignment of an interest in a drilling location and related acreage conditional upon the drilling of a well on that location, the completion of other work commitments related to that acreage, or some combination thereof.

Formation. A succession of sedimentary beds that were deposited under the same general geologic conditions.

Fracture stimulation. A stimulation treatment involving the fracturing of a reservoir and then injecting water, sand and chemicals, such as proppants, into the fractures under pressure to stimulate hydrocarbon production in low-permeability reservoirs.

Gross acres or gross wells. The total acres or wells, as the case may be, in which a working interest is owned.

Initial production rate. Generally, the maximum 24 hour production volume from a well.

Mbbl. One thousand stock tank barrels.

Mboe. One thousand barrels of oil equivalent.

Mcf. One thousand cubic feet of natural gas.

iii

Table of Contents

Mmbbl. One million stock tank barrels.

Mmboe. One million barrels of oil equivalent.

Mmcf. One million cubic feet of natural gas.

Net acres or net wells. The sum of the fractional working interests owned in gross acres or gross wells.

Overriding royalty interest. An interest in an oil or natural gas property entitling the owner to a share of oil and natural gas production free of costs of production.

Play. A term applied to a portion of the exploration and production cycle following the identification by geologists and geophysicists of areas with potential oil and gas reserves.

Present value of estimated future net revenues or PV-10. The present value of estimated future net revenues is an estimate of future net revenues from a property at the date indicated, without giving effect to derivative financial instrument activities, after deducting production and ad valorem taxes, future capital costs, abandonment costs and operating expenses, but before deducting future federal income taxes. The future net revenues have been discounted at an annual rate of 10% to determine their “present value.” The present value is shown to indicate the effect of time on the value of the net revenue stream and should not be construed as being the fair market value of the properties. Estimates have been made using constant oil and natural gas prices and operating and capital costs at the date indicated, at its acquisition date, or as otherwise indicated. We believe that the present value of estimated future net revenues before income taxes, while not a financial measure in accordance with U.S. generally accepted accounting principles, is an important financial measure used by investors and independent oil and natural gas producers for evaluating the relative significance of oil and natural gas properties and acquisitions because the tax characteristics of comparable companies can differ materially.

Productive well. A productive well is a well that is not a dry well.

Proved developed reserves. Developed oil and gas reserves are reserves of any category that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate.

Proved reserves. Those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible, from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations, prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

The area of the reservoir considered as proved includes: (i) the area identified by drilling and limited by fluid contacts, if any, and (ii) adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible oil or gas on the basis of available geoscience and engineering data.

In the absence of data on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons (LKH) as seen in a well penetration unless geoscience, engineering, or performance data and reliable technology establishes a lower contact with reasonable certainty. Where direct observation from well penetrations has defined a highest known oil (HKO) elevation and the potential exists for an associated gas cap, proved oil reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering, or performance data and reliable technology establish the higher contact with reasonable certainty.

Reserves which can be produced economically through application of improved recovery techniques (including, but not limited to, fluid injection) are included in the proved classification when: (i) successful testing by a pilot project in an area of the reservoir with properties no more favorable than in the reservoir as a whole, the operation of an installed program in the reservoir or an analogous reservoir, or other evidence using reliable technology establishes the reasonable certainty of the engineering analysis on which the project or program was based; and (ii) the project has been approved for development by all necessary parties and entities, including governmental entities.

iv

Table of Contents

Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. The price shall be the average price during the 12-month period prior to the ending date of the period covered by the report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

Proved undeveloped reserves. Reserves of any category that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion.

Reserves on undrilled acreage shall be limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances. Undrilled locations can be classified as having undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years, unless the specific circumstances justify a longer time.

Under no circumstances shall estimates for undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir or by other evidence using reliable technology establishing reasonable certainty.

Recompletion. An operation within an existing well bore to make the well produce oil or gas from a different, separately producible zone other than the zone from which the well had been producing.

Reasonable certainty. If deterministic methods are used, reasonable certainty means a high degree of confidence that the quantities will be recovered. If probabilistic methods are used, there should be at least a 90% probability that the quantities actually recovered will equal or exceed the estimate. A high degree of confidence exists if the quantity is much more likely to be achieved than not, and, as changes due to increased availability of geoscience (geological, geophysical, and geochemical), engineering, and economic data are made to estimated ultimate recovery (EUR) with time, reasonably certain EUR is much more likely to increase or remain constant than to decrease.

Reservoir. A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

Royalty interest. An interest in an oil or natural gas property entitling the owner to a share of oil and natural gas production free of costs of production.

Shale. Fine-grained sedimentary rock composed mostly of consolidated clay or mud. Shale is the most frequently occurring sedimentary rock.

Standardized Measure of discounted future net cash flows or the Standardized Measure. Under the Standardized Measure, future cash flows for the years ended December 31, 2010 and 2009 are estimated by applying the simple average spot prices for the trailing twelve month period using the first day of each month beginning on January 1 and ending on December 1 of each respective year, adjusted for fixed and determinable escalations, to the estimated future production of year-end proved reserves. Future cash inflows are reduced by estimated future production and development costs based on period-end and future plugging and abandonment costs to determine pre-tax cash inflows. Future income taxes are computed by applying the statutory tax rate to the excess of pre-tax cash inflows over our tax basis in the associated properties. Future net cash inflows after income taxes are discounted using a 10% annual discount rate to arrive at the Standardized Measure.

Undeveloped acreage. License or lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

Working interest. The operating interest that gives the owner the right to drill, produce and conduct activities on the property and a share of production.

v

Table of Contents

| Item 1. | Business. |

In this Annual Report on Form 10-K, references to “we,” “us,” “our,” or “the Company” refer to TransAtlantic Petroleum Ltd. and its subsidiaries on a consolidated basis. Unless stated otherwise, all sums of money stated in this Form 10-K are expressed in U.S. Dollars.

Development of Our Business

We are a vertically integrated, international oil and gas company engaged in the acquisition, exploration, development and production of crude oil and natural gas. We hold interests in developed and undeveloped oil and gas properties in Turkey, Morocco, Bulgaria and Romania. We own our own drilling rigs and oilfield service equipment, which we use to develop our properties in Turkey and Morocco. In addition, our drilling services business provides oilfield services and drilling services to third parties in Turkey and Iraq. As of April 1, 2011, approximately 44.2% of our outstanding common shares are beneficially owned by N. Malone Mitchell, 3rd, the chairman of our board of directors.

Strategic Transformation

In 2008, we changed our operating strategy from a prospect generator to a vertically integrated project developer. To execute this strategy, we entered into the following transactions:

| • | in December 2008, we acquired Longe Energy Limited (“Longe”) from Longfellow Energy, LP (“Longfellow”) in consideration for the issuance of 39,583,333 common shares and 10,000,000 common share purchase warrants to Longfellow. At the time of the acquisition, Longe’s assets included drilling rigs and equipment as well as interests in the Tselfat and Guercif exploration permits in Morocco. Immediately after the Longe acquisition, we purchased an additional $8.3 million in drilling and service equipment, tubulars and supplies from Viking Drilling, LLC (“Viking Drilling”). Mr. Mitchell, his wife and his children indirectly own 100% of Longfellow. Dalea Partners, LP (“Dalea”) owns 85% of Viking Drilling. Mr. Mitchell and his wife own 100% of Dalea. In addition, Mr. Mitchell is a partner of Dalea and a manager of Dalea Management, LLC, the general partner of Dalea. |

| • | in March 2009, we acquired Incremental Petroleum Limited, now called Incremental Petroleum Pty Ltd (“Incremental”), for total consideration of $54.9 million. The acquisition of Incremental expanded our rig fleet and increased our workforce of field staff, engineers and geologists in Turkey. At the time of the acquisition, Incremental’s Turkish properties included the producing Selmo oil field, a 55% interest in the Edirne gas field and additional exploration acreage. |

| • | in July 2009, we acquired Energy Operations Turkey, LLC, now called Talon Exploration, Ltd. (“Talon”), for total cash consideration of $7.7 million. At the time of the acquisition, Talon’s assets included a 50% interest in the producing Arpatepe oil field and additional exploration acreage, inventory and seismic data. |

| • | in August 2010, we acquired Amity Oil International Pty Ltd (“Amity”) and Petrogas Petrol Gaz ve Petrokimya Ürünleri Inşaat Sanayi ve Ticaret A.Ş. (“Petrogas”) for total cash consideration of $96.5 million. At the time of the acquisition, Amity’s and Petrogas’ Turkish properties included a producing gas field, completed gas wells awaiting connection to a pipeline and additional exploration acreage and equipment. |

| • | in February 2011, we acquired Direct Petroleum Morocco, Inc. (“Direct Morocco”), Anschutz Morocco Corporation (“Anschutz”) and Direct Petroleum Bulgaria EOOD (“Direct Bulgaria”) for cash consideration of $2.0 million and the issuance of 8,924,478 common shares, for total consideration of $30.0 million. At the time of the acquisition, Direct Morocco and Anschutz owned a 50% working interest in the Ouezzane-Tissa and Asilah exploration permits in Morocco and Direct Bulgaria owned 100% of the working interests in the A-Lovech and Aglen exploration permits in Bulgaria. |

1

Table of Contents

Drilling Services Business

Beginning with the acquisition of Longe in 2008, we have established a significant and comprehensive drilling services business. As of December 31, 2010, we owned six drilling rigs and four workover and completion rigs in Turkey, and we owned two drilling rigs in Morocco. In addition, we managed one drilling rig in Turkey for Viking Drilling and one drilling rig in Iraq for Maritas A.Ş. (“Maritas”) pursuant to management services agreements. We believe that ownership of our own drilling rigs and service equipment will enable us to lower drilling and operating costs over the long term and control the timing of the development of our properties, thereby providing a competitive advantage.

In 2010, we expanded our drilling services activities, particularly in Turkey, to include products and services used to drill and evaluate oil and natural gas wells. Through our wholly-owned subsidiary, Viking International Limited (“Viking International”), we provide the following oilfield services: wireline, pressure pumping (including fracture stimulation, acid stimulation and cementing), construction (including location building, road building and pipeline construction), rental tools and underbalanced drilling, pulling units, drilling fluids, inventory, yards and trucking, and mudlogging.

Through Viking International, we are able to provide a full range of services and materials to our exploration and production business, reducing costs over the long term and the need to rely on third party service providers. In addition, when our drilling rigs and equipment are not operating on our properties, we can use them to provide drilling and oilfield services to third parties in Turkey and northern Iraq. Viking International is aggressively pursuing third party work to generate additional returns on our capital investment. Viking International is not currently active in Bulgaria or Romania. During 2010, Viking International generated revenues of approximately $7.3 million from providing oilfield services to third parties in Turkey and the Kurdistan region of northern Iraq.

Through our wholly-owned subsidiary, Viking Geophysical Services, Ltd. (“Viking Geophysical”), we operate two seismic data acquisition crews with equipment capable of acquiring 2D, 3D and microseismic data. In 2010, our seismic crews acquired 774 kilometers of 2D seismic data, of which 262 kilometers were acquired for third parties, and 791 square kilometers of 3D seismic data, of which 365 square kilometers were acquired for third parties. During 2010, Viking Geophysical generated revenues of approximately $8.4 million from providing seismic services to third parties in Turkey.

Application of Modern Drilling and Completion Techniques in Turkey

Historically, the oil and gas exploration and production industry in Turkey has not used modern drilling and completion techniques. One of our strategies is to apply these modern techniques to our properties in Turkey. To implement this strategy, we began to drill wells using polycrystalline diamond compact bits and downhole motors and to utilize underbalanced drilling equipment. These technologies increase the speed at which wells can be drilled and in many cases reduce the cost of drilling wells. In addition, we have employed modern acid stimulation techniques and modern fracture stimulation techniques. Generally, acid stimulation removes damage near the wellbore caused by the invasion of drilling fluids and can make certain reservoirs, such as the carbonate reservoirs in the Selmo oil field, more productive. Fracture stimulation involves fracturing the reservoir and pumping proppants into the fractures to increase the flow of oil or natural gas from the wellbore. In North America, many reservoirs are routinely fracture stimulated and would not produce oil or natural gas on a commercial basis without fracture stimulation. In the fourth quarter of 2010, we began the first fracture stimulations of natural gas wells in the Thrace Basin in northwestern Turkey. We plan to continue our fracture stimulation program in the Thrace Basin and are considering the use of fracture stimulation for our wells in Bulgaria and Romania. We anticipate that employing fracture stimulation techniques will result in the commercial development of natural gas reserves that would have not been commercial otherwise.

Recent Developments

During 2010 and the first quarter of 2011, we completed the following material acquisitions, financings and operations:

Commencement of Edirne Gas Sales. On April 8, 2010, we commenced natural gas sales from our Edirne gas field in northwestern Turkey. AKSA Dogolgaz Toptan Satis A.Ş. (“AKSA”), a natural gas distributor in Turkey, purchases all of our natural gas production from the Edirne field at a price equal to a 15% discount to the Industrial Interruptible Tariff benchmark set by BOTAŞ Petroleum Pipeline Corporation (“BOTAŞ”), the state-owned crude oil and natural gas pipelines and trading company in Turkey.

2

Table of Contents

TPAO Memorandum of Understanding. On April 9, 2010, we entered into a memorandum of understanding with Turkiye Petrolleri Anonim Ortakligi (“TPAO”), a Turkish government-owned oil and gas company, to explore for unconventional resources in Turkey. In the initial phase of the agreement, we will participate in two licenses, one in the Thrace Basin and one in southeastern Turkey, and will re-enter a total of four wells and drill a total of four wells. These wells will target tight sand and shale formations that do not produce under normal conditions.

Successful Completion of Bakuk-101 Well. During April and May 2010, with our partner and operator, Tiway Turkey, Ltd. (“Tiway”), we drilled a successful natural gas well, the Bakuk-101, with potential production of up to 10.0 Mmcf of natural gas per day. The Bakuk-101 well is located on License 4069, which is located in southeastern Turkey near the Syrian border. In November 2010, we re-entered the Bakuk-2 well, which failed to establish an oil leg in the reservoir. We have completed construction of a 23 kilometer, 6-inch pipeline from the Bakuk-101 well to an existing pipeline to the south and expect to begin limited natural gas sales in the second quarter of 2011. We are now evaluating options for further appraisal of the reservoir. As a result of drilling the Bakuk-101 well, we earned a 50% working interest in the Bakuk licenses.

Dalea Credit Agreement. On June 28, 2010, our wholly-owned subsidiary, TransAtlantic Worldwide, Ltd. (“TransAtlantic Worldwide”) entered into a credit agreement with Dalea for the purpose of funding the acquisition of all of the shares of Amity and Petrogas and for general corporate purposes. The amounts due under the credit agreement accrue interest at a rate of three-month LIBOR plus 2.50% per annum. The Company borrowed an aggregate of $73.0 million under the credit agreement and used the proceeds to finance a portion of the purchase price of the shares of Amity and Petrogas.

Short-Term Secured Credit Agreement. On August 25, 2010, TransAtlantic Worldwide, entered into a $30.0 million short-term secured credit agreement with Standard Bank, Plc (“Standard Bank”). We borrowed $30.0 million under the short-term secured credit agreement and used the proceeds to finance a portion of the purchase price for the shares of Amity and Petrogas. See “Liquidity and Capital Resources—Short-Term Secured Credit Agreement.”

Completion of Amity and Petrogas Acquisition. On August 25, 2010, TransAtlantic Worldwide acquired all of the shares of Amity and Petrogas for total cash consideration of $96.5 million. Through the acquisition of Amity and Petrogas, we acquired interests ranging from 50% to 100% of eighteen exploration licenses and one production lease, consisting of approximately 1.3 million gross acres (1.0 million net acres) in the Thrace Basin and 730,000 gross and net acres in central Turkey, and equipment. With the completion of the acquisition, we added approximately 7.0 Mmcf of natural gas production per day in the Thrace Basin and approximately 10.0 Mmcf of natural gas production per day in completed gas wells in the Thrace Basin awaiting connection to a pipeline. We funded $66.5 million of the purchase price from borrowings under our credit agreement with Dalea and $30.0 million of the purchase price from borrowings under our short-term secured credit agreement with Standard Bank.

Sale of Common Shares. From September 30, 2010 through October 8, 2010, we closed a public offering of an aggregate of 30,357,143 common shares at a purchase price of $2.80 per share, raising gross proceeds of $85.0 million. Of the 30,357,143 common shares sold, we offered and sold 1,788,643 common shares to Dalea. The net proceeds from the offering, after deducting the placement agency fee and estimated offering expenses, were approximately $80.6 million. We used $19.0 million of the net proceeds to pay off the principal amount and accrued interest under the loan and security agreement between Viking International and Dalea, and we used the remainder of the net proceeds for general corporate purposes.

Pinnacle Turkey and TBNG Option Agreement. On November 8, 2010, TransAtlantic Worldwide entered into an option agreement with Mustapha Mehmet Corporation (“MMC”) regarding the purchase of all of the shares of Thrace Basin Natural Gas (Turkiye) Corporation (“TBNG”) and Pinnacle Turkey, Inc. (“Pinnacle”). Pursuant to the option agreement, TransAtlantic Worldwide paid MMC an option fee of $10.0 million and had until February 11, 2011 to exercise the option to acquire all of the shares of TBNG and Pinnacle. On February 10, 2011, TransAtlantic Worldwide exercised its option under the option agreement.

On a combined basis, TBNG and Pinnacle currently produce approximately 25.0 Mmcf of natural gas per day and hold interests in a total of approximately 600,000 net onshore acres in Turkey. TBNG and Pinnacle sell their natural gas production through a wholly-owned pipeline distribution system.

Upon the closing of the transactions contemplated by the option agreement, TransAtlantic Worldwide or its affiliates or assigns would acquire all of the shares of TBNG and Pinnacle in consideration for (i) $100.0 million in cash, (ii) the issuance of 18.5 million of our common shares pursuant to a private placement, and (iii) the transfer of certain overriding royalty interests (ranging from 1% to 2.5% of the working interests owned by TBNG and Pinnacle on specified exploration licenses) to an affiliate of MMC. At closing, the $10.0 million option fee will be credited towards the cash purchase price. According to the terms of the option agreement, TransAtlantic Worldwide has the ability to transfer its rights to acquire all of the shares of TBNG and/or Pinnacle to an affiliate or a newly formed entity that is formed for the purpose of acquiring the shares. The closing of the TBNG and Pinnacle acquisition is subject to regulatory approval, stock exchange approval and customary closing conditions, and there is no assurance the transaction will close.

3

Table of Contents

TransAtlantic Worldwide intends to seek a total of $100.0 million from third party investors to fund the cash portion of the purchase price. At the time of closing, Pinnacle would own a 65% working interest in five onshore exploration licenses in the Thrace Basin and a 25% working interest in three shelf and five offshore licenses in the Sea of Marmara. Pinnacle would also own a 37.5% working interest in five exploration licenses in the Gaziantep area in southeastern Turkey. At the time of closing, TBNG would own the other 35% working interest in the five onshore licenses, 100% of the working interest in four production leases in the Thrace Basin, a 25% working interest in three shelf and five offshore licenses in the Sea of Marmara, drilling rigs and equipment. TBNG would remain the operator of the TBNG and Pinnacle licenses and production leases.

Valeura Energy Letter Agreement. On February 9, 2011, we entered into a letter agreement with Valeura Energy Inc. (“VEI”), whereby VEI offered to acquire 61.54% of the shares of Pinnacle and certain interests from Pinnacle and TBNG in certain exploration licenses and production leases on properties in the Thrace Basin and Gaziantep areas of Turkey, together with associated assets. VEI’s acquisition of these assets would have an effective date of October 1, 2010. Under the letter agreement, VEI would provide approximately $61.5 million in funding to acquire 61.54% of the shares of Pinnacle and certain assets.

Under the letter agreement, the parties agreed to negotiate in good faith the terms of certain definitive agreements, including agreements to transfer 61.54% of the shares of Pinnacle and certain assets, and to use reasonable commercial efforts to finalize the definitive agreements no later than April 25, 2011. If any of the conditions precedent of the letter agreement are not satisfied before closing or if closing has not occurred by July 11, 2011, any party is entitled to terminate its obligations under the letter agreement. If VEI’s acquisition of the interests in Pinnacle does not proceed as a result of a material breach by TransAtlantic Worldwide, us or VEI of the letter agreement, a material breach by TransAtlantic Worldwide of the TBNG option agreement or a material breach by TransAtlantic Worldwide or VEI of certain other agreements entered into in contemplation of the acquisition of TBNG and Pinnacle, the breaching party shall be liable to the non-breaching party for all direct damages, costs and expenses suffered by the non-breaching party as a direct result thereof, up to a maximum of $9.2 million.

Direct Petroleum Acquisition. On February 18, 2011, TransAtlantic Worldwide acquired Direct Morocco and Anschutz, and our wholly-owned subsidiary, TransAtlantic Petroleum Cyprus Limited (“TransAtlantic Cyprus”), acquired Direct Bulgaria. In addition, TransAtlantic Worldwide purchased from the seller, Direct Petroleum Exploration, Inc. (“Direct”), all of Direct’s right, title and interest in the amounts due to Direct by each of Direct Morocco, Anschutz and Direct Bulgaria. As consideration for the acquisition, TransAtlantic Worldwide paid $2.0 million in cash to Direct, and we issued 8,924,478 of our common shares to Direct in a private placement, for total consideration of $30.0 million. In addition, if certain post-closing milestones are achieved, we will issue additional consideration to Direct equal to: (i) $6.0 million worth of our common shares if the GRB-1 well in Morocco is a commercial success; (ii) $10.0 million worth of our common shares if the Deventci-R2 well in Bulgaria is a commercial success; and (iii) $10.0 million worth of our common shares if Direct Bulgaria receives a production concession for a specified area in Turkey.

In connection with the acquisition, we entered into a registration rights agreement whereby Direct is entitled to certain piggyback registration rights for the common shares issued to Direct, including any common shares issued to Direct as part of the additional consideration, for a period of six months following the date of issuance to Direct. The piggyback registration rights permit Direct to elect to have the common shares included in a registration statement filed by us, subject to the limitations and conditions set forth in the registration rights agreement.

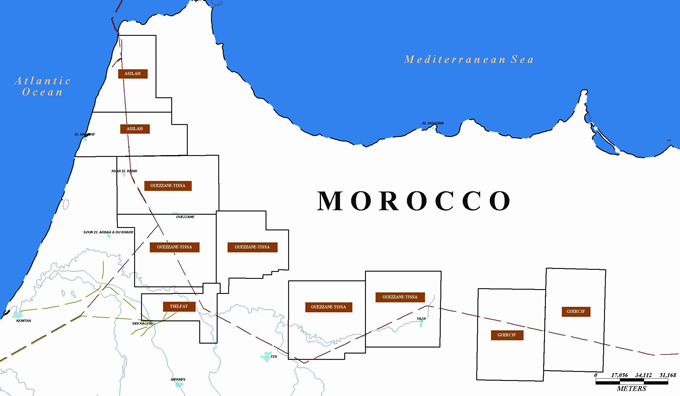

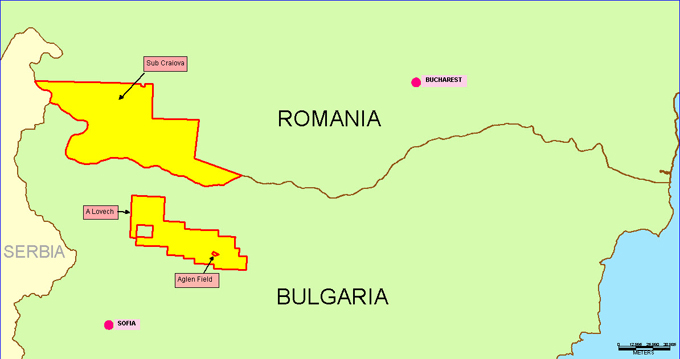

At the time of closing, Direct Morocco and Anschutz owned a 50% working interest in the Ouezzane-Tissa and Asilah exploration permits, which cover an aggregate of approximately 2,356,000 acres (9,533 square kilometers) in northern Morocco. As a result of the acquisition, we own 100% of those exploration permits. Direct Bulgaria owns 100% of the working interests in the A-Lovech exploration permit and the Aglen exploration permit, subject to a 3% and a 1% overriding royalty interest, respectively, which cover an aggregate of approximately 600,000 acres (2,288 square kilometers) in northwestern Bulgaria. The A-Lovech permit contains the Deventci-R1 well, which discovered a reservoir in the Jurassic Orzirovo formation at a depth of approximately 4,200 meters. The well is currently producing approximately 250 Mcf of natural gas per day, on a limited test basis. We plan to appraise this discovery by drilling a second well, the Deventci-R2 well, on the A-Lovech exploration permit in 2011.

The A-Lovech exploration permit is also estimated to contain over 300,000 acres prospective for Etropole shale (at a depth of approximately 3,800 meters), which was recently certified as a geologic discovery by the Bulgarian government. We anticipate coring the Etropole shale interval, which will enhance the technical understanding of the potential of this shale play. The third established prospective area is a deep gas field on the Aglen exploration permit that produced approximately 9.0 Bcf of natural gas before being abandoned in the late 1990s.

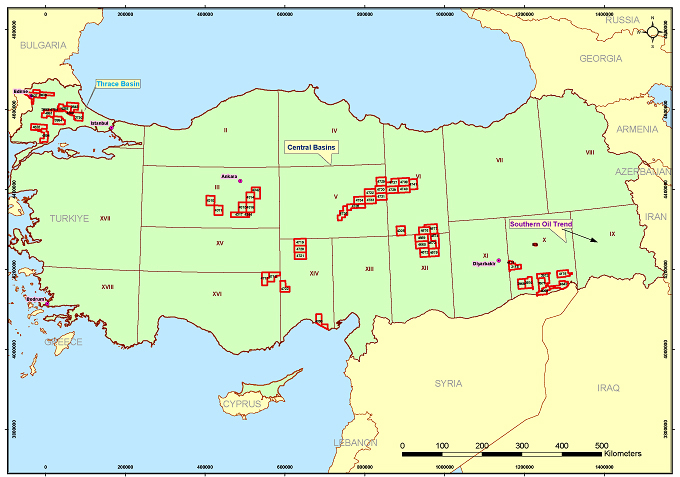

Exploration, Development and Production

Turkey Exploration and Production. We began 2010 with interests in 25 onshore exploration licenses and one onshore production lease in Turkey. As of April 1, 2011, we held interests in 56 onshore exploration licenses and three onshore production leases covering a total of 6.4 million gross acres (6.0 million net acres) in Turkey.

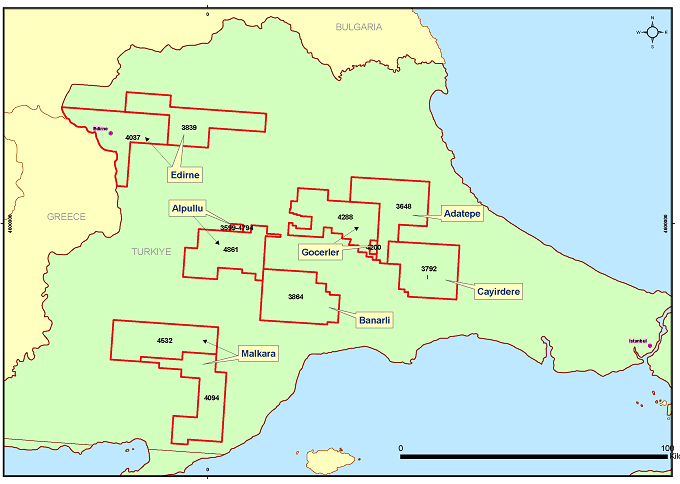

Thrace Basin. Through the Amity and Petrogas acquisition in August 2010, we acquired a 100% working interest in the Alpullu production lease in the Thrace Basin in northwestern Turkey, a 50% working interest in the Gocerler production lease in the Thrace Basin and additional exploration licenses in the Thrace Basin and in southern Turkey. Zorlu Dogal Gaz Ithalat Ihracat ve Toptan Ticaret A.S. (“Zorlu”), a privately owned natural gas distributor in Turkey, purchases substantially all of our natural gas production from the Alpullu field at a price equal to a 15% discount to the Industrial Interruptible Tariff benchmark set by BOTAŞ. At the time of closing, natural gas production from the acquired properties was approximately 7.0 Mmcf per day net to our interest. In addition, there were wells capable of producing an additional 10.0 Mmcf of natural gas per day net to our interest upon connection to a pipeline. We are constructing a 20 kilometer, 10-inch pipeline to carry natural gas from the Alpullu gas field in the Thrace Basin to an existing pipeline. We expect to place all wells in production in the second quarter of 2011.

4

Table of Contents

In April 2010, we commenced natural gas sales from our Edirne gas field, which we acquired through the Incremental acquisition in 2009. AKSA purchases all of our natural gas production from the Edirne field at a price equal to a 15% discount to the Industrial Interruptible Tariff benchmark set by BOTAŞ.

For 2010, our net production of natural gas in the Thrace Basin, after royalties, was 1,707 Mmcf. For the fourth quarter of 2010, our net production of natural gas in the Thrace Basin, after royalties, was 887 Mmcf, or approximately 9,642 Mcf per day. We currently have 37 producing wells in the Thrace Basin, and we plan to drill between 30 and 40 new wells on our Thrace Basin licenses in 2011.

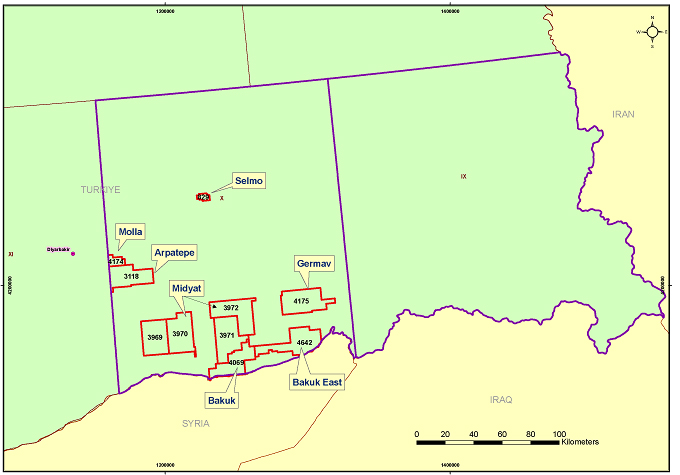

Southeastern Turkey. Through the Incremental acquisition in 2009, we acquired a 100% working interest in the Selmo production lease in southeastern Turkey. For 2010, our net production of crude oil in the Selmo field, after royalties, was approximately 631,000 Bbls of crude oil at an average rate of approximately 1,700 Bbls per day. Substantially all of our crude oil production is currently concentrated in the Selmo field. TPAO, a Turkish government-owned oil and gas company, and Türkiye Petrol Rafinerileri A.Ş. (“TUPRAS”), a privately-owned oil refinery in Turkey, purchase all of our crude oil production from the Selmo field. We currently have 39 producing wells in the Selmo field, and we plan to drill and complete at least 24 wells at Selmo in 2011. Production of oil from Selmo for the month of March 2011 averaged 2,833 Bbls per day, before royalties.

Through the Talon acquisition in July 2009, we acquired a 50% working interest in the producing Arpatepe exploration license. For 2010, our net production of crude oil in the Arpatepe field, after royalties, was approximately 58,700 Bbls at an average rate of approximately 160 Bbls per day. We currently have three producing wells in the Arpatepe field, and we plan to drill up to five additional wells at Arpatepe in 2011.

In May 2010, we acquired a 50% working interest in the Bakuk licenses in southeastern Turkey by drilling the Bakuk-101 well. The Bakuk-101 well was successful, with potential production of up to 10.0 Mmcf of natural gas per day. In November 2010, we re-entered the Bakuk-2 well, which failed to establish an oil leg in the reservoir. We have completed construction of a 23 kilometer, 6-inch pipeline from the Bakuk-101 well to an existing pipeline to the south and expect to begin limited natural gas sales in the second quarter of 2011.

Turkey Development. We also have substantial exploration acreage in Turkey. In April 2010, we entered into a memorandum of understanding with TPAO to explore for unconventional resources in Turkey. In the initial phase of the agreement, we will participate in two licenses, one in the Thrace Basin and one in southeastern Turkey, and will re-enter a total of four wells and drill a total of four wells. These wells will target tight sand and shale formations that do not produce under normal conditions.

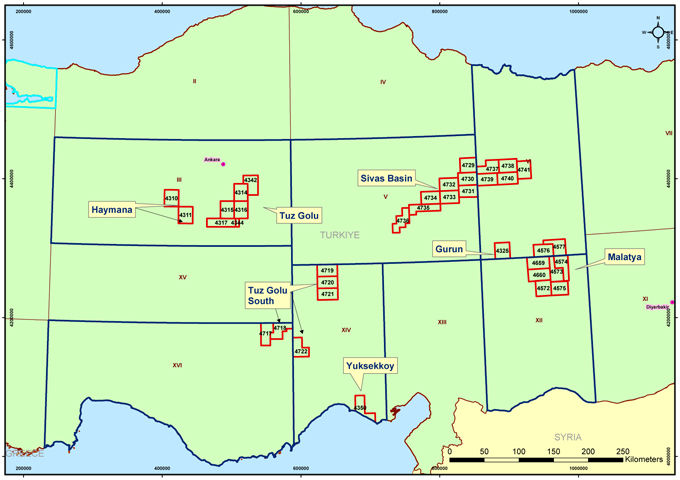

In March 2010, we entered into a farm-in agreement with TBNG to acquire a 50% interest in five Gaziantep licenses in south-central Turkey. To earn that interest, we will pay 62.5% of total drilling and seismic costs until 12.5% of total drilling and seismic costs paid equals $750,000. Thereafter, we will pay 50% of drilling and seismic costs incurred. We expect to terminate this farm-in agreement upon our acquisition of TBNG, which is expected to occur in the second quarter of 2011.

Through the Incremental acquisition in 2009, we acquired the six Tuz Golu and two Haymana exploration licenses in central Turkey and the four Midyat licenses in southeastern Turkey. We have also expanded our portfolio of properties in Turkey by applying for licenses directly with the Turkish General Directorate for Petroleum Affairs (“GDPA”). In 2009, we were awarded eight Malatya licenses. In 2010, we were awarded the Alpullu exploration license, the Bakuk East license, six Tuz Golu South licenses and thirteen Sivas Basin licenses. Each of these licenses was awarded to us based on an approved work program.

Morocco Exploration and Development. As of April 1, 2011, we owned interests in eight onshore exploration permits in northern Morocco. We are the operator and 100% working interest owner in the Tselfat exploration permit (subject to a 25% participation interest by the national oil company of Morocco, Office of National des Hydrocarbures et des Mines (“ONHYM”) once production is achieved), which was awarded to us in May 2006. As part of our recent extension of the license period, in January 2011 we relinquished 45% of our Tselfat exploration permit acreage. The Tselfat exploration permit covers three existing fields; Haricha, Brou Draa and Tselfat. In 2009, we drilled the HR-33 bis well in the Haricha field to help assess whether there is the opportunity for redevelopment of the previously produced but abandoned Haricha field. We have put the HR-33 bis well on an extended production test to determine its commerciality. We commenced crude oil production in January 2011. The crude oil produced during the test is trucked approximately 200 kilometers to a refinery operated by Société Anonyme Marocaine de I’Industrie de Raffinage (“SAMIR”) in Mohammedia, Morocco. If testing confirms the commerciality of the HR-33 bis well, we plan to delineate the oil field and apply for an exploitation concession. In 2010, we drilled the BTK-1 well and the GUW-1 well, which have both been plugged and abandoned after failing to

5

Table of Contents

discover hydrocarbons in commercial quantities. We plan to drill three exploration wells to a depth of at least 1,500 meters on the Tselfat exploration permit in 2011.

We are the operator and 100% working interest owner in the two Asilah exploration permits (subject to a 25% participation interest by ONHYM once production is achieved). In December 2010, we commenced drilling the GRB-1 well, which reached total depth in March 2011. The GRB-1 well targeted tertiary-aged reservoirs, and in 2011, we plan to test numerous intervals that had gas shows while drilling.

We are the operator and 100% working interest owner in five Ouezzane-Tissa exploration permits. In 2010, we drilled at our cost three wells on the Ouezzane-Tissa exploration permits. The first well, the OZW-1 well, encountered an extremely high pressure water zone near 9,000 feet which we could not drill through and was plugged and abandoned. We drilled the second well, the HKE-1 well, which did not reach target depth and was plugged and abandoned. The third well, the HKE-1 bis well, did not discover hydrocarbons in commercial quantities, and is being plugged and abandoned. We plan to relinquish the Ouezzane-Tissa exploration permits in 2011, and upon ONHYM’s acceptance of our final report, we expect to have $3.0 million in work commitment bank guarantees returned to us.

We were awarded two Guercif exploration permits in January 2008. We are the operator and 80% working owner of the Guercif permits. As part of our Guercif work program, we re-entered, logged and tested the MSD-1 well, which we completed as a dry hole in the fourth quarter of 2008. The logs and test failed to establish the presence of hydrocarbons. In December 2010, we abandoned our interests in the Guercif exploration permits. As part of our agreement with ONHYM for the abandonment of the Guercif exploration permits, we transferred an obligation to drill one well from the Guercif exploration permits to the Tselfat exploration permit. Upon ONHYM’s acceptance of our final report, we expect to have $2.0 million in work commitment bank guarantees returned to us.

Bulgaria Exploration and Development. As of April 1, 2011, we owned interests in two onshore exploration permits in Bulgaria. We have a 100% working interest in the A-Lovech and Aglen exploration permits, subject to 3% and 1% overriding royalty interests, respectively, in northwestern Bulgaria. The A-Lovech permit contains the Deventci-R1 well, which discovered a reservoir in the Jurassic Orzirovo formation at a depth of approximately 4,200 meters. The well is currently producing approximately 250 Mcf of natural gas per day on a limited test basis, which is sold to a compressed natural gas facility adjacent to the Deventci-R1 well. We plan to appraise this discovery by drilling a second well, the Deventci-R2 well, on the A-Lovech permit in 2011. We have submitted an application for a production concession covering approximately 160,000 acres of the A-Lovech permit.

The A-Lovech permit is also estimated to contain over 300,000 acres prospective for Etropole shale (at a depth of approximately 3,800 meters), which was recently certified as a geologic discovery by the Bulgarian government. We anticipate coring the Etropole shale interval, which will enhance the technical understanding of the potential of this shale play.

Romania Exploration and Development. As of April 1, 2011, we owned an interest in an onshore production license in Romania. In June 2009, we entered into an agreement with Sterling Resources Ltd. (“Sterling”) to farm-in to Sterling’s Sud Craiova Block E III-7 in western Romania. In exchange for a 50% working interest, we agreed to drill three exploration wells on the Sud Craiova license, each to a depth of approximately 3,280 feet (1,000 meters). We drilled three wells at our cost on the Sud Craiova license in 2009 and 2010, all of which have been plugged and abandoned for failing to discover hydrocarbons in commercial quantities. We are currently reprocessing seismic data previously shot over the Sud Craiova license and plan to drill an exploration well to test the Silurian-aged shale formations at a depth of approximately 4,200 meters. Sterling is the operator of the Sud Craiova license.

In February 2006, we were awarded the Izvoru, Vanatori and Marsa production licenses. We drilled a total of five wells on these licenses in 2009 and 2010, all of which were plugged and abandoned after failing to discover hydrocarbons in commercial quantities. In December 2010, we relinquished our interests in each of these three licenses.

Drilling Services Business

At December 31, 2010, we owned six drilling rigs and four workover and completion rigs in Turkey, and we owned two drilling rigs in Morocco. In addition, we managed one drilling rig in Turkey for Viking Drilling and one drilling rig in Iraq for Maritas pursuant to management services agreements. We believe that ownership of our own drilling rigs and service equipment will enable us to lower drilling and operating costs over the long term and control the timing of the development of our properties, thereby providing a competitive advantage.

In 2010, we expanded our drilling services activities, particularly in Turkey, to include products and services used to drill and evaluate oil and natural gas wells. Through Viking International, we provide the following oilfield services: wireline,

6

Table of Contents

pressure pumping (including fracture stimulation, acid stimulation and cementing), construction (including location building, road building and pipeline construction), rental tools and underbalanced drilling, pulling units, drilling fluids, inventory, yards and trucking, and mudlogging.

Through Viking International, we are able to provide a full range of services to our exploration and production business, reducing costs and the need to rely on third party service providers. In addition, when our drilling rigs and equipment are not operating on our properties, we can use them to provide drilling and oilfield services to third parties. Viking International is aggressively pursuing third party work to generate additional returns on our capital investment. Viking International is not currently active in Bulgaria or Romania. During 2010, Viking International generated revenues of approximately $7.3 million from providing oilfield services to third parties in Turkey and the Kurdistan region of northern Iraq.

Through Viking Geophysical, we operate two seismic data acquisition crews with equipment capable of acquiring 2D, 3D and microseismic data. In 2010, our seismic crews acquired 774 kilometers of 2D seismic data, of which 262 kilometers were acquired for third parties, and 791 square kilometers of 3D seismic data, of which 365 square kilometers were acquired for third parties. During 2010, Viking Geophysical generated revenues of approximately $8.4 million from providing seismic services to third parties in Turkey.

Planned 2011 Operations

We continue to actively explore and develop our existing oil and gas properties in Turkey, Morocco and Bulgaria and evaluate the opportunities for further activities in Romania. Our success will depend in part on discovering additional hydrocarbons in commercial quantities and then bringing these discoveries into production. In 2011, we are focused on accomplishing the following objectives:

| • | Increasing Production. Our goal is to achieve a production rate of 10,000 Boe per day in Turkey by the end of 2011. We plan to increase our crude oil and natural gas production in Turkey through continuous drilling in Selmo and the Thrace Basin, the completion of pipelines to bring shut-in gas to market, the application of modern well stimulation techniques such as gelled acidizing and fracture stimulation, and the introduction of directional drilling. |

| • | Securing Partners to Reduce Exploration Risk. We are actively seeking partners for our exploration acreage in Turkey, Morocco, Bulgaria and Romania. Through farm-outs, we expect to reduce our exploration risk and accelerate the exploration and development activities on the farmed-out properties. We have begun consolidating and analyzing well data and seismic data for our properties in Bulgaria and our exploration acreage in Turkey. It is our intention to remain as operator in the properties that we farm out. |

| • | Integrating Acquisitions. We expect to complete the acquisition of TBNG and Pinnacle in the second quarter of 2011, which will bring additional acreage, production, personnel and equipment into our Turkey operations. We will continue to integrate the recent acquisitions of Amity, Petrogas and Direct Bulgaria. |

Capital expenditures for 2011 are expected to range between $125.0 million and $150.0 million. Approximately 50% of these anticipated expenditures will occur in the Thrace Basin in Turkey, devoted to developing conventional and unconventional natural gas production, building infrastructure and acquiring seismic data. Approximately 35% of these anticipated expenditures will occur in southeastern Turkey, devoted to developing crude oil production at Selmo and Arpatepe and drilling exploratory wells on various licenses. The balance of the estimated budget is divided between exploration activities in Morocco and Romania. We are seeking a joint venture partner to fund our anticipated capital expenditures in Bulgaria in 2011. If cash on hand, borrowings from our senior secured credit facility and cash flow from operations are not sufficient to fund our capital expenditures, then we will either curtail our discretionary capital expenditures or seek other funding sources. We currently plan to execute the following drilling and exploration activities in 2011:

Turkey. We plan to drill approximately 90-100 wells during 2011, including wells to be drilled on acreage held by TBNG, which we expect to acquire in the second quarter of 2011. If we do not complete the acquisition of TBNG, the number of wells we expect to drill in 2011 may change. We also plan to construct the infrastructure necessary to produce and sell oil and natural gas from the productive wells we drill.

Morocco. On our Tselfat exploration permit, we are currently producing oil from the HR-33 bis well on an extended production test to determine if the well is commercially viable. If testing confirms the HR-33 bis well as a commercial well, we plan to delineate the oil field, apply for an exploitation concession and drill at least one additional well in the Haricha field. We also plan to drill the TKN-1 well to test another 3D seismic prospect that is similar to the Haricha field. If the TKN-1 well is a commercial well, we would likely drill an additional appraisal well. We plan to drill three exploration wells to a depth of at least 1,500 meters on the Tselfat exploration permit in 2011. On our Asilah exploration permit, we are planning to test the recently to completed the GRB-1 well, which had substantial gas shows during drilling. If that well is completed as a commercial well, we would likely drill additional appraisal wells and develop plans to commercialize those wells.

7

Table of Contents

Bulgaria. We plan to drill the Deventci-R2 well on the A-Lovech exploration permit to appraise the Deventci-R1 well gas discovery. While drilling the appraisal well on the A-Lovech permit, we plan to test the productivity of the Etropole shale interval. We may also drill an additional appraisal well on the Aglen exploration permit. If the appraisal well on the Aglen permit is successful, we anticipate planning the construction of a pipeline to connect the Deventci wells to a natural gas pipeline to the south. We are seeking to enter into a joint venture where the joint venture partner would carry us in the capital expenditures incurred in Bulgaria in 2011.

Romania. We plan to drill an exploration well to test the Silurian-aged shale formations present on the Sud Craiova license. We may also drill an exploration well to test the Coyote oil prospect on the southeastern portion of the Sud Craiova license.

Drilling Services Business. We plan to continue to increase drilling services revenues by providing drilling services and seismic acquisition services to third parties in Turkey and northern Iraq.

Principal Capital Expenditures and Divestitures

The following table sets forth our principal capital expenditures during 2010 (in thousands of dollars):

| Expenditure Type |

Year Ended December 31, 2010 |

|||

| Oil and gas properties |

$ | 53,766 | ||

| Drilling services and other equipment |

58,817 | |||

| Subtotal |

112,583 | |||

| Acquisition of Amity and Petrogas, net of cash received |

96,248 | |||

| Total capital expenditures |

$ | 208,831 | ||

There were no capital divestitures during 2010.

Principal Markets

In accordance with the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 280, Segment Reporting (“ASC 280”), we have two reportable operating segments, exploration and production of oil and natural gas (“E&P”) and drilling services, and three reportable geographic segments: Romania, Turkey and Morocco. For financial information about our operating segments and geographic areas, refer to “Note 14—Segment information” to our consolidated financial statements.

Customers

During 2010, substantially all of our crude oil production was concentrated in the Selmo field in Turkey. TPAO, a Turkish government-owned oil and gas company, and TUPRAS, a privately-owned oil refinery in Turkey, purchase all of our crude oil production from the Selmo field. During 2010, we sold $48.0 million of crude oil to TPAO and TUPRAS, representing 56.1% of our total revenues. We sell our crude oil to TPAO and TUPRAS pursuant to two separate agreements.

Our wholly-owned subsidiary, TransAtlantic Exploration Mediterranean International Pty. Ltd. (“TEMI”), entered into a domestic crude oil purchase and sale agreement with TUPRAS, effective as of January 26, 2009. Under the purchase and sale agreement, TUPRAS purchases crude oil produced by TEMI and delivered to TEMI’s BOTAŞ/Batman tanks and to the BOTAŞ/Dörtyol plant. The price of the crude oil delivered pursuant to the purchase and sale agreement is determined under the Petroleum Market Law No. 5015 under the laws of the Republic of Turkey. The purchase and sale agreement had an initial one year term, which automatically renews thereafter for successive one-year terms unless earlier terminated in writing by either party.

TEMI also entered into a domestic crude oil swap agreement with TPAO, effective as of January 1, 2010. Under the swap agreement, TPAO purchases crude oil produced by TEMI from the Selmo oil field. The swap agreement requires TEMI to deliver oil in-kind for the royalties due to the Republic of Turkey. In addition, the swap agreement required TEMI to pay 3% of the insurance amount paid by TPAO to cover transportation of crude oil. Pricing of the crude oil delivered pursuant to the swap agreement is determined by a pricing formula provided under Petroleum Market Law No. 5015 under the laws of

8

Table of Contents

the Republic of Turkey. The swap agreement had an initial one year term, which automatically renews thereafter for successive one-year terms unless earlier terminated in writing by either party.

During 2010, substantially all of our natural gas production was concentrated in the Edirne and Alpullu gas fields in the Thrace Basin in northwestern Turkey. AKSA, a natural gas distributor in Turkey, purchases all of our natural gas production from the Edirne field at a price equal to a 15% discount to the Industrial Interruptible Tariff benchmark set by BOTAŞ. Zorlu, a privately owned natural gas distributor in Turkey, purchases substantially all of our natural gas production from the Alpullu field that we operate at a price equal to a 15% discount to the Industrial Interruptible Tariff benchmark set by BOTAŞ.

Competition

Exploration, Development and Production. We operate in the highly competitive areas of oil and gas exploration, development, production and acquisition with a substantial number of other companies, including U.S.-based and international companies doing business in each of the countries in which we operate. We face intense competition from independent, technology-driven companies as well as from both major and other independent oil and gas companies in each of the following areas:

| • | seeking oil and gas exploration licenses and production licenses and leases; |

| • | acquiring desirable producing properties or new leases for future exploration; |

| • | marketing natural gas and oil production; |

| • | integrating new technologies; and |

| • | acquiring the equipment and expertise necessary to develop and operate properties. |

Many of our competitors have substantially greater financial, managerial, technological and other resources than we do. These companies are able to pay more for exploratory prospects and productive oil and gas properties than we can. To the extent competitors are able to pay more for properties than we are paying, we will be at a competitive disadvantage. Further, many of our competitors enjoy technological advantages over us and may be able to implement new technologies more rapidly than we can. Our ability to explore for natural gas and oil prospects and to acquire additional properties in the future will depend upon our ability to successfully conduct operations, implement advanced technologies, evaluate and select suitable properties and consummate transactions in this highly competitive environment.

Drilling Services Business. We operate in the competitive area of drilling services in Turkey, with a number of other U.S.-based, international and government owned companies. We face competition from large international companies, including Schlumberger N.V. and Halliburton Company, in providing modern stimulation and completion techniques in Turkey. We also face competition for providing conventional drilling services in Turkey from U.S.-based, international and government owned companies, including TPAO, Aladdin Middle East, Ltd. (“Aladdin”) and Perenco. We face intense competition from other drilling services providers in the areas of technological innovation, the quality of services provided and in price differentiation.

Many of our competitors in drilling services have substantially greater financial, managerial, technological and other resources than we do. These companies are able to pay more for technological innovations and may be able to implement new technologies more rapidly than we can. In addition, these companies may be able to offer a larger variety of services at lower prices. Our ability to provide drilling services in the future will depend upon our ability to successfully implement advanced technologies, provide quality services and offer competitive prices in this competitive environment.

Governmental Regulations

Government Regulation. Our current or future operations, including exploration and development activities on our properties, require permits from various governmental authorities, and such operations are and will be governed by laws and regulations governing exploration, development, production, exports, taxes, labor laws and standards, occupational health, waste disposal, toxic substances, land use, environmental protection and other matters. Compliance with these requirements

9

Table of Contents

may prove to be difficult and expensive. Due to our international operations, we are subject to the following issues and uncertainties that can affect our operations adversely:

| • | the risk of expropriation, nationalization, war, revolution, political instability, border disputes, renegotiation or modification of existing contracts, and import, export and transportation regulations and tariffs; |

| • | the risk of not being able to procure residency and work permits for our expatriate personnel; |

| • | taxation policies, including royalty and tax increases and retroactive tax claims; |

| • | exchange controls, currency fluctuations and other uncertainties arising out of foreign government sovereignty over international operations; |

| • | laws and policies of the United States affecting foreign trade, taxation and investment; |

| • | the possibility of being subjected to the exclusive jurisdiction of foreign courts in connection with legal disputes and the possible inability to subject foreign persons to the jurisdiction of courts in the United States; and |

| • | the possibility of restrictions on repatriation of earnings or capital from foreign countries. |

Permits and Licenses. In order to carry out exploration and development of oil and gas interests or to place these into commercial production, we may require certain licenses and permits from various governmental authorities. There can be no guarantee that we will be able to obtain all necessary licenses and permits that may be required. In addition, such licenses and permits are subject to change and there can be no assurances that any application to renew any existing licenses or permits will be approved. We also store, transport and use explosive materials in certain of our drilling service operations, which are also subject to special controls and regulatory regimes in certain countries in which we conduct our services.

Repatriation of Earnings. Currently, there are no restrictions on the repatriation of earnings or capital to foreign entities from Turkey, Morocco, Bulgaria or Romania. However, there can be no assurance that any such restrictions on repatriation of earnings or capital from the aforementioned countries or any other country where we may invest will not be imposed in the future. We may be liable for payment of taxes upon repatriation of certain earnings from the aforementioned countries.

Environmental. The oil and natural gas industry is subject to extensive and varying environmental regulations in each of the jurisdictions in which we operate. Environmental regulations establish standards respecting health, safety and environmental matters and place restrictions and prohibitions on emissions of various substances produced concurrently with oil and natural gas. In most instances, the regulatory requirements relate to the handling and disposal of drilling and production waste products and waste created by water and air pollution control procedures. These regulations can have an impact on the selection of drilling locations and facilities, potentially resulting in increased capital expenditures. In addition, environmental legislation may require those wells and production facilities to be abandoned and sites reclaimed to the satisfaction of local authorities. Such regulation has increased the cost of planning, designing, drilling, operating and in some instances, abandoning wells. We are committed to complying with environmental and operation legislation wherever we operate.

Such laws and regulations not only expose us to liability for our own negligence, but may also expose us to liability for the conduct of others or for our actions that were in compliance with all applicable laws at the time those actions were taken. We may incur significant costs as a result of environmental accidents, such as oil spills, natural gas leaks, ruptures, or discharges of hazardous materials into the environment, including clean-up costs and fines or penalties. Additionally, we may incur significant costs in order to comply with environmental laws and regulations and may be forced to pay fines or penalties if we do not comply.

Employees

As of April 1, 2011, we employed approximately 826 people and, through a service agreement with Longfellow, Viking Drilling, MedOil Supply, LLC and Riata Management, LLC (“Riata”), contracted for the services of approximately 67 additional people. As of April 1, 2011, approximately 55 of our employees at one of our Turkish subsidiaries are represented by collective bargaining agreements with the Turkish Employers Association of Chemical, Oil and Plastic

10

Table of Contents

Industries (KIPLAS) and the Petroleum, Chemical and Rubber Workers Union of Turkey (PETROL-IS). The collective bargaining agreements expire January 31, 2012. We consider our union and employee relations to be satisfactory.

Formation

We were incorporated under the laws of British Columbia, Canada on October 1, 1985 under the name Profco Resources Ltd. and continued to the jurisdiction of Alberta, Canada under the Business Corporations Act (Alberta) on June 10, 1997. Effective December 2, 1998, we changed our name to TransAtlantic Petroleum Corp. Effective October 1, 2009, we continued to the jurisdiction of Bermuda under the Bermuda Companies Act 1981 under the name TransAtlantic Petroleum Ltd.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are made available free of charge on our website at www.transatlanticpetroleum.com as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC.

11

Table of Contents

| Item 1A. | Risk Factors. |

Risks Related to Our Business

We will require significant capital to continue our exploration and development activities beyond May 25, 2011.

We may not have sufficient funds to continue our operations beyond May 25, 2011, the maturity date of our short-term secured credit agreement with Standard Bank. If we are unable to finance our operations on acceptable terms or at all, our business, financial condition and results of operations may be materially and adversely affected.

Future cash flows and the availability of debt or equity financing will be subject to a number of variables, such as:

| • | the success of our prospects in Turkey, Morocco, Bulgaria and Romania; |

| • | success in finding and commercially producing reserves; and |

| • | prices of natural gas and oil. |

Debt financing could lead to:

| • | a substantial portion of operating cash flow being dedicated to the payment of principal and interest; |

| • | our company being more vulnerable to competitive pressures and economic downturns; and |

| • | restrictions on our operations. |

If sufficient capital resources are not available, we might be forced to cease operations entirely, curtail developmental and exploratory drilling and other activities or be forced to sell some assets on an untimely or unfavorable basis, which would have a material adverse effect on our business, financial condition and results of operations.

We have a history of losses and may never be profitable.

We have incurred substantial losses in prior years. During 2010, our comprehensive loss was approximately $78.9 million and we used $43.5 million of cash in operating activities. We may suffer significant additional losses in the future and may never be profitable. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. We expect to incur losses unless and until such time as one or more of our properties generates sufficient revenue to fund our continuing operations.

The future performance of our business will depend upon our ability to identify, acquire and develop additional oil and gas reserves that are economically recoverable. Success will depend upon the ability to acquire working and revenue interests in properties upon which oil and gas reserves are ultimately discovered in commercial quantities, and the ability to develop prospects that contain additional proven oil and gas reserves to the point of production. Without successful acquisition and exploration activities, we will not be able to develop additional oil and gas reserves or generate additional revenues. There are no assurances that additional oil and gas reserves will be identified or acquired on acceptable terms, or that oil and gas reserves will be discovered in sufficient quantities to enable us to recover our exploration and development costs or sustain our business.