Attached files

| file | filename |

|---|---|

| EX-32.1 - China Industrial Waste Management Inc. | v218509_ex32-1.htm |

| EX-31.2 - China Industrial Waste Management Inc. | v218509_ex31-2.htm |

| EX-32.2 - China Industrial Waste Management Inc. | v218509_ex32-2.htm |

| EX-21.1 - China Industrial Waste Management Inc. | v218509_ex21-1.htm |

| EX-31.1 - China Industrial Waste Management Inc. | v218509_ex31-1.htm |

| EX-10.8 - China Industrial Waste Management Inc. | v218509_ex10-8.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2010

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________________ to __________________

Commission File Number 002-95836-NY

CHINA INDUSTRIAL WASTE MANAGEMENT, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

13-3250816

|

|

|

(State or other jurisdiction of incorporation or organization)

|

||

|

No. 1 Huaihe West Road, E-T-D-Zone, Dalian, China

|

116600

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code 011-86-411-82595139

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section to file reports pursuant to Section 13 or 15(d) of the Act.

Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company:

|

Large accelerated filer

|

¨

|

Accelerated filer

|

¨

|

|

Non-accelerated filer

(Do not check if smaller reporting company)

|

¨

|

Smaller reporting company

|

þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked prices of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter: $7,174,100 as of June 30, 2010 based on the closing price $1.40 of the Company’s common stock on such date.

The number of issued and outstanding shares of the registrant’s common stock as of April 11, 2011 was 15,336,535.

DOCUMENTS INCORPORATED BY REFERENCE

None.

FORWARD-LOOKING STATEMENTS AND ASSOCIATED RISK

This report includes "forward-looking statements." You can identify these statements by the fact that they do not relate strictly to historical or current facts. These statements contain such words as "may," "project," "might," "expect," "believe," "anticipate," "intend," "could," "would," "estimate," "continue," or "pursue," or the negative or other variations thereof or comparable terminology. In particular, they include statements relating to, among other things, future actions, new projects, strategies, future performance, the outcomes of contingencies and our future financial results. These forward-looking statements are based on current expectations and projections about future events.

Investors are cautioned that forward-looking statements are not guarantees of future performance or results and involve risks and uncertainties that cannot be predicted or quantified and, consequently, our actual performance may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, but are not limited to, the following factors, as well as other factors described from time to time in our reports filed with the Securities and Exchange Commission (including the sections entitled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained therein): the timing and magnitude of technological advances; the prospects for future acquisitions; the effects of political, economic and social uncertainties regarding the governmental, economic and political circumstances in the People’s Republic of China, the possibility that a current customer could be acquired or otherwise be affected by a future event that would diminish their waste management requirements; the competition in the waste management industry and the impact of such competition on pricing, revenues and margins; uncertainties surrounding budget reductions or changes in funding priorities of existing government programs and the cost of attracting and retaining highly skilled personnel; our projected sales, profitability, and cash flows; our growth strategies; anticipated trends in our industries; our future financing plans; and our anticipated needs for working capital.

Forward-looking statements speak only as of the date on which they are made, and, except to the extent required by federal securities laws, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act“) expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. If we are ever considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

CONVENTIONS AND GENERAL MATTERS

The official currency of the People’s Republic of China is the Chinese “Yuan” or “Renminbi” (“Yuan,” “Renminbi” or “RMB”). For the convenience of the reader, amounts expressed in this report as RMB have been translated into United States dollars (“US$” or “$”) at the rate quoted by the Federal Reserve System. The Renminbi is not freely convertible into foreign currencies and the quotation of exchange rates does not imply convertibility of Renminbi into U.S. Dollars or other currencies. All foreign exchange transactions take place either through the Bank of China or other banks authorized to buy and sell foreign currencies at the exchange rates quoted by the People'’s Bank of China, or PBOC. No representation is made that the Renminbi or U.S. Dollar amounts referred to herein could have been or could be converted into U.S. Dollars or Renminbi, as the case may be, at the PBOC exchange rate or at all.

The "Company," "we," "us," "our" and similar words refer to China Industrial Waste Management, Inc, and its direct and indirect, wholly-owned and partially-owned subsidiaries.

2

Form 10-K ANNUAL REPORT FISCAL YEAR ENDED DECEMBER 31, 2010

TABLE OF CONTENTS

|

Page

No.

|

||

|

Forward Looking Statements and Associated Risk

|

2 | |

|

Conventions and General Matters

|

2 | |

|

Part I

|

||

|

Item 1.

|

Business.

|

4 |

|

Item 1A.

|

Risk Factors.

|

18 |

|

Item 1B.

|

Unresolved Staff Comments.

|

27 |

|

Item 2.

|

Properties.

|

27 |

|

Item 3.

|

Legal Proceedings.

|

28 |

|

Item 4.

|

(Removed and Reserved.)

|

28 |

|

Part II

|

||

|

Item 5.

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

28 |

|

Item 6.

|

Selected Financial Information.

|

29 |

|

Item 7.

|

Management's Discussion and Analysis of Financial Condition and Results of Operations.

|

30 |

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk.

|

36 |

|

Item 8.

|

Financial Statements and Supplementary Data

|

37 |

|

Item 9.

|

Changes In and Disagreements With Accountants on Accounting and Financial Disclosure.

|

37 |

|

Item 9A.

|

Controls and Procedures.

|

37 |

|

Item 9B.

|

Other Information.

|

38 |

|

Part III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance.

|

39 |

|

Item 11.

|

Executive Compensation.

|

42 |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

|

46 |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence.

|

47 |

|

Item 14.

|

Principal Accounting Fees and Services.

|

48 |

|

Part IV

|

||

|

Item 15.

|

Exhibits, Financial Statement Schedules.

|

49 |

|

SIGNATURES

|

50 | |

|

EXHIBIT INDEX

|

||

|

FINANCIAL STATEMENTS

|

||

3

PART I

|

ITEM 1.

|

BUSINESS.

|

Overview

We are a leading provider of comprehensive environmental services and solutions in northeastern China. We currently have two primary areas of business. In our Industrial Solid Waste Treatment and Recycling business, we collect, store, treat, dispose and recycle industrial solid waste. In our Sludge and Sewage Treatment business, we are licensed to treat municipal sewage generated from a designated portion of Dalian, China, as well as treat the sludge resulting from the processing of sewage routed to us from 14 sewage treatment facilities located in Dalian and surrounding areas. In addition, we recently began to offer sludge processing equipment supply and engineering services, which are not yet a significant contributor to our revenues, but represent an important part of our growth strategy. We believe we are the largest and most technologically advanced provider of environmental services in our principal geographic market of Liaoning Province.

We are headquartered in Dalian, a city with a population of over 7 million located at the tip of the Liaodong Peninsula that serves as a large trading, industrial and financial center in northeastern China. As of December 31, 2010, we provided services to 808 customers located in Dalian, including Chinese and foreign companies, and the Dalian municipal government. In addition, under our Build-Operate-Transfer (BOT) contracts with the Dalian municipal government, we operate one of eight sewage treatment facilities currently operating in Dalian and the only sludge treatment facility in Dalian, which was the first BOT project to implement centralized municipal sludge treatment in China.

We generate revenues from two business areas, (i) service fees charged for industrial solid waste, sewage and sludge treatment services and (ii) sales of recycled materials, including cupric sulfate, as well as metals and methane derived from sludge treatment. During the fiscal years ended December 31, 2010 and 2009, our revenues were approximately $21.2 million and $10.6 million, respectively, and our net income was $4.6 million and $2.0 million, respectively. All of our sales for these periods were in the People’s Republic of China, or PRC.

We provide environmental pollution remediation services to the Dalian municipal government upon request when environmental damage occurs in the Dalian region, such as the pollution caused by the oil spill in 2010. On July 16, 2010, an explosion in the port area of Dalian resulted in 1,500 tons of crude oil spilling into Dalian harbor and covering an area of 11 square kilometers, producing the largest recorded oil spill in China. Immediately following the accident, the Dalian government requested the Company to assist the government in its clean up operations. We provided advisory support as well as disposal of oil-saturated sand and oil absorption felts in our waste treatment and recycling plants to prevent secondary contamination.

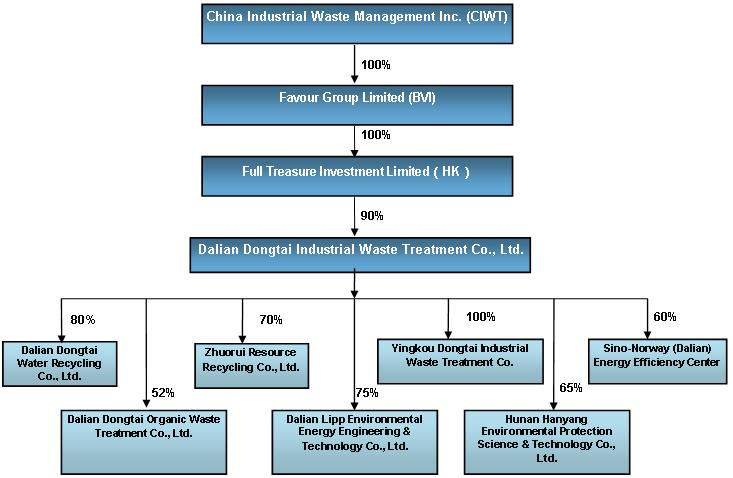

Corporate Structure

Through a series of equity investments and joint ventures, we have established seven operating subsidiaries in the PRC through which we conduct our business. Each subsidiary focuses on a particular business or geographic area to enable us to take advantage of opportunities in the growing environmental services market. We entered our present line of business as a result of a reverse merger transaction in November 2005 in which Dalian Dongtai Industrial Waste Treatment Co., Ltd. (“Dalian Dongtai”), a PRC company engaged in solid waste treatment and disposal since 1991, became an indirect subsidiary of our company. See “Organizational History”.

4

The following chart depicts our current organizational structure:

Our principal executive offices are located at Room 1709 Rainbow Building, No. 23 Renmin Road, Zhongshan District, Dalian City, China 116001. Our telephone number is (011) 86-411-82595139 and our website address is www.chinaciwt.com.

Products and Services

As of December 31, 2010, we conducted our business in two primary areas of operations, two of which, (i) industrial solid waste treatment and recycling and (ii) municipal sludge and sewage treatment, currently generate substantially all of our revenues. We recently began to offer additional services in environmental equipment and engineering, an area that we expect to grow as the overall demand for sludge treatment and ancillary services expands.

For the years ended December 31, 2010 and 2009, our industrial solid waste and recycling business generated the majority of our revenues, however our growth strategy includes significant investment in and expansion of our sludge treatment business and our sludge processing equipment supply and engineering services business which should result in greater contributions to our revenues and net income over the next three to five years.

Industrial Solid Waste Treatment and Recycling

Our solid waste treatment and recycling services is our largest and serves as our most profitable area of operations. We began providing solid waste treatment and recycling services in 1991 and serve as the only provider of comprehensive industrial solid waste treatment solutions in Liaoning Province. During the fiscal years ended December 31, 2010 and 2009, we earned approximately $17 million and $9.5 million, respectively, in revenues from our solid waste treatment and recycling services, representing approximately 80% and 90% of our total revenues for such periods. We earn revenue from service fees received from solid waste treatment and disposal and the sales of recycled products, such as cupric sulfate and other materials produced from the recycling process. We have a very diverse customer base of over 800 customers, including companies engaged in the electronic, chemical, petrochemical, mechanical treatment, pharmacy, shipbuilding and automobile industries.

Our industrial solid waste operations consist of three components: industrial solid waste collection and disposal, sales of recycled materials and waste catalyst treatment and comprehensive reuse.

5

Industrial Solid Waste Collection and Disposal

We collect industrial solid waste from customers and charge service fees for disposal based on the weight of the collected waste. These services include waste collection and transportation, final disposal via incineration and/or landfill, physical and/or chemical treatment, material processing, packaging, analysis and storage. We operate a fleet of 19 vehicles, including 16 collection trucks equipped with navigational and electronic waste monitoring systems, which are equipped to collect and transport industrial solid waste, including hazardous waste such as organic solvents, oil, catalysts and emulsions, to our facilities for treatment, disposal or recycling.

We are the only company in Liaoning Province that provides “one-stop” comprehensive waste treatment services to customers. We are licensed to dispose of almost all hazardous industrial solid wastes defined by national standards except for certain groups containing waste such as nuclear waste and polychlorinated biphenyl.

Although our typical waste management contract with a customer is for a term of one year and renewable on an annual basis, the contracts are essentially for the long term since we are likely the only company qualified to handle a customer’s particular waste disposal requirements. We charge customers a monthly service fee for solid waste disposal based on a combination of factors, including collection frequency, type of collection equipment required, type and volume or weight of the waste collected, distance to our disposal facility, labor costs, cost of disposal and general market factors. As part of our service, we provide steel containers to most of our customers to store their solid waste between pick-up dates. Our storage containers vary in size and type according to the needs of our customers and the restrictions of their communities. Many containers are designed to be lifted mechanically and either emptied into a truck’s compaction hopper or directly into a disposal site. By using these containers, we can service most of our industrial solid waste customers with trucks operated by only one or two employees.

In 2010, we collected and treated approximately 117,627 tons of industrial solid waste and received approximately $11.7 million in service fees. In addition, we generated approximately $5.7 million from sales of recycled materials produced from the waste we treated.

Our facilities contain several workshops equipped with proprietary and non-proprietary systems enabling us to be a full service provider of comprehensive industrial solid waste treatment, disposal and recycling solutions. Systems include, among others, an “Electric Garbage Dismantling System” for the dismantling and recycling of used photocopier ink cartridges and electric components of certain household appliances, an “Organic Solvent Distillation Recycling System” designed to handle organic solvents including triclene, acetone, ethyl acetate and isopropyl alcohol and a “Waste Etchant Liquor Treatment System” to process etchant (an acid or corrosive chemical) containing waste copper to generate cupric sulfate through neutralization, acidification and metathesis.

With respect to disposal solutions for solid waste, we operate the only hazardous waste landfill located on Haiqing Island of Dalian, with designed capacity of 20,000 tons, and an industrial solid waste landfill in Qianguan Village, with designed capacity of 20,000 tons, that can process non-hazardous industrial wastes. In addition, to reduce environmental pollution and properly dispose of industrial waste, including hazardous chemicals, we also operate an automated incineration system to dispose of wastes, including organic solvents, waste oil and combustible solid industrial garbage.

Our operating philosophy is to minimize waste and maximize recycling. As a result, our management believes that all of our workshops and waste disposal systems and methods, including incinerator and landfill, are integral factors enabling us to provide “one-stop” waste management solutions to our customers. The diagram below sets forth the various stages of processing we employ for solid waste in order to achieve maximum efficiency in accordance with our operating philosophy.

6

As part of our vertically integrated operations, we also offer advisory services to our customers on pollution/waste reduction and on-site services, where our employees work full-time inside a customer’s facilities to provide full-service waste management solutions. The breadth of our service offerings and the experience we have with waste management practices allows us to provide valuable guidance to customers in identifying recycling opportunities, minimizing waste, and determining the most efficient means available for waste collection and disposal.

On August 1, 2010, we were designated as an authorized service provider for the dismantling, processing and recycling of discarded domestic appliances in Dalian, and one of only four licensed provider of these services in Liaoning Province under the Discarded Domestic Appliance Recycling Program (the “Recycling Program”) sponsored by the PRC Ministries of Commerce, Treasury, and Environmental Protection. By participating in this program, the Company expects to generate approximately $2 million in revenues over the program's 17-month duration. The revenue generated from recycling electronic waste under this program consists of two components: (i) fees received from the central government for processing the electronic waste and (ii) revenues generated from sales of recycled materials. The Recycling Program began in August 2010 in Dalian and runs through the end of December 2011.

To meet the growing demand for industrial solid waste disposal and treatment, we are constructing a new solid waste treatment facility in Dalian, which has been designated by the PRC National Development and Reform Commission, or NDRC, as one of 55 authorized hazardous waste treatment centers in China, and will be one of two such centers in Liaoning Province. The objective of the NDRC is for every province in China to have one or two such solid waste treatment facilities. Our new facility, which we call our Dagushan Expansion Project, is 90% complete and is expected to commence operations in the third quarter of 2011, at which time our solid waste treatment capacity is anticipated to increase to 114,000 tons annually, which is twice that of our existing capacity. The total investment for the Dagushan Expansion Project is estimated to be approximately $16 million, of which up to 30% (approximately $4.8 million) is being subsidized by the PRC central government. Once the Dagushan Expansion Project becomes operational, management believes that the Company will be well positioned to fully capitalize on the rapid industrial and environmental development in Liaoning Province.

Sales of Recycled Materials

After waste collection and treatment, we further process recovered etchant and convert it into cupric sulfate, a copper compound, in a form that can be utilized by companies engaged in chemical engineering, agriculture and mining. In 2010, we sold 991.6 tons of cupric sulfate primarily to mining and trading companies. In addition, we generate valuable material contained in industrial waste such as waste metal and waste plastic through our recyclable materials processing operation. The table below indicates the volume and types of recycled materials other than cupric sulfate that we sold during 2010 and 2009.

7

|

Category

|

Volume (in Tons)

|

||||||||

|

|

2010

|

2009

|

|||||||

|

1

|

Plastic

|

878 | 187 | ||||||

|

2

|

Waste oil

|

2,785 | 1,367 | ||||||

|

3

|

Waste iron

|

108 | 1,703 | ||||||

|

4

|

Waste slag

|

4,709 | 1,146 | ||||||

|

5

|

Waste circuit board

|

67 | 130 | ||||||

|

6

|

Valuable Metals

|

5,615 | 425 | ||||||

|

7

|

Waste paper

|

962 | 77 | ||||||

|

8

|

Waste Drum (small)

|

191 | 327 | ||||||

|

9

|

Waste Drum (big)

|

263 | 288 | ||||||

|

10

|

Other

|

3,047 | 379 | ||||||

|

Total

|

18,625 | 6,029 | |||||||

Waste Catalyst Treatment and Comprehensive Reuse

We have operations focused on the separation and purification of waste catalysts generated during the oil refinery process, treatment of industrial wastes and utilization of waste catalysts or similar materials to produce ammonium metavanadate, molybdic acid and nickel slag for sale by the Company. Catalysts are used in the petroleum refining and petrochemical industry for, among other things, production of gasoline, jet fuels, petrochemicals and plastics. During the oil refining process, catalysts will become contaminated with impurities in the crude oil feed and become a waste product.

West Pacific Petrochemical and Dalian Petrochemical, two of the Company’s customers and among China’s largest oil refining companies with a 10 million and 20 million ton annual capacity, respectively, collectively produce approximately 3,000 tons of waste catalysts per year, which we purchase. In addition, as other refining plants in northeast China modernize their facilities to address high-sulfur oil content, we estimate the annual volume of waste catalyst should reach 8,000 to 10,000 tons in northeastern China.

Municipal Sludge and Sewage Treatment

Our sludge and sewage treatment business is one of our fastest growing areas of operations. We earn revenues from municipal sludge and sewage treatment in the form of service fees paid by the Dalian government on a monthly or quarterly basis based on the volume of wastewater or sludge treated by our facilities. During each of the fiscal years ended December 31, 2009 and 2010, we earned approximately $1 million in revenues from the Dalian government for our sewage treatment services, representing approximately 9.7% and 4.4% of our total revenues for such periods. For the year ended December 31, 2010, we earned approximately $3.5 million in revenues from our sludge treatment business which commenced operations in January, 2010, which represented approximately 16% of our total revenues for 2010. Revenues generated from service fees (sludge processing) and sales of methane were approximately $2.23 million and $1.25 million, respectively, in 2010.

We operate our sludge treatment and sewage treatment facilities pursuant to BOT contracts executed with the Dalian municipal government. In a typical BOT project, we bid on the project and the municipal government selects a winner based on the best combination of price and construction and operating model for the project. The winning bidder finances the construction of the BOT project and, in exchange, is granted the right to operate the facility and charge service fees for a fixed term of 20 to 25 years commencing from the date set forth in the BOT contract.

Our BOT sewage contract permits us to process domestic wastewater generated from designated portions of Dalian until June 2028. Phase 1 of our sewage treatment plant operates at its current maximum treatment capacity of 30,000 tons per day. Construction of Phase 2 of the plant is anticipated to start in 2013 and upon completion is expected to increase the treatment capacity to a total of 100,000 tons per day. Our facilities utilize advanced treatment equipment to treat sewage and we focus our research and development efforts on processing wastewater into useable water for industrial applications.

8

In accordance with our BOT sludge contract, we are permitted to treat and dispose of sludge generated from sewage treatment plants, including our own plant, located in Dalian. The 20-year exclusivity term of the BOT sludge contract will begin once our sludge treatment facility achieves operating capacity of 70%. Our sludge treatment facility is the first BOT project to implement centralized municipal sludge treatment in China, and is currently operating at approximately 67% capacity or 400 tons per day. In addition, we earn revenues from sales of methane, a by-product of the anaerobic fermentation method of processing sludge, which provides us with the flexibility to offer substantially lower cost of sludge treatment per ton as compared to alternative sludge treatment processes currently available in China. In addition, our facility was voted the "Best Sewage Sludge Process Application of China" during the 2nd Water Specialist Conference held in Shanghai on August 31, 2010.

Sludge is a liquid/solid composed of by-products collected at different stages of the wastewater treatment process and usually contains compounds of agricultural value, including organic matter, nitrogen, phosphorus and potassium, and to a lesser extent, calcium, sulphur and magnesium, as well as pollutants that usually consist of heavy metals, organic pollutants and pathogens. As a result, rather than treat sludge through traditional methods of incineration or landfill, we process sludge by anaerobic fermentation, which reduces pollution and generates methane. In addition to sludge treatment fees, we generate revenues from sales of methane to the Dalian Gas Company.

In 2011, we expect to finalize an agreement with the Dalian municipal government granting us an exclusive license to process food waste generated in Dalian, including expired food items from stores and restaurants, at our sludge treatment facility. We expect the treatment of food waste under this agreement will require our sludge treatment facility to operate at maximum capacity by increasing our processing volume by approximately 200 tons per day. The amount of methane that will be produced from processing sludge and food waste is expected to be approximately 2.5 times the amount of methane produced from sludge treatment alone. At prevailing market prices, this translates into approximately $21,000 per day of methane as compared to approximately $5,700 per day of methane without food processing.

Sludge Processing Equipment Supply and Engineering

We are also engaged in the design, manufacture, installation and post-sale technical support for our Lipp tanks, which are fermentation tanks used for sludge treatment in China. We conduct this business through Dalian Lipp Environmental Energy Engineering & Technology Co., Ltd. (“Dalian Lipp”) our 75% owned subsidiary and joint venture with Lipp Gmbh. Lipp tanks are proprietary to Lipp Gmbh, which holds a patent registered in Germany on the design of Lipp tanks.

We have not yet generated any revenues from this business, but plan to sell Lipp tanks at a sales price of approximately $670,000 per tank. To take advantage of the growing sludge treatment market, we intend to design, build and sell our Lipp tanks and ancillary equipment, and provide product related consulting services. We believe that the Lipp tanks we build will offer competitive advantages such as superior quality, onsite assembly, short construction period, lower cost and maintenance expense. We plan to begin sales of Lipp tanks in 2011, primarily to companies that operate BOT sludge projects in China.

Ancillary Services

To enhance our comprehensive service offerings, we have also invested in businesses and partnerships that are designed to offer services and solutions that complement our current operations. These investments include our partnership with Dalian Huineng Science and Technology Co., Ltd. and the Dalian Enterprise Confederation in Sino-Norway Dalian Energy Efficiency Center Co., Ltd., or Sino-Norway EEC, a joint venture incorporated in November 2009. Sino-Norway EEC was formed to engage in the business of energy efficiency audit and consultation, and is sponsored under the Energy Efficiency Planning Program initiated by the Chinese and Norwegian governments. We expect this joint venture to generate business as the demand for advisory services increases.

9

Facilities

The following table summarizes the various facilities we use in our business operations and their processing capacity before and after the construction of our Dagushan Expansion Project.

|

|

|

|

|

|

|

Capacity*

|

||

|

Nature of Service

|

|

Type of Facility

|

|

Description

|

|

Existing

|

|

Post-

Expansion

|

|

|

|

Incinerator

|

|

Incineration Treatment

|

|

3,300 t/a

|

|

9,000 t/a

|

|

Solid Waste Treatment and Disposal

|

|

Landfill

|

|

Disposal of Waste by Landfill

|

|

13,000 t

|

|

40,000 t

|

|

|

Effulent Treatment System

|

|

Handling of Various Industrial Effluent

|

|

18,000 t/a

|

|

25,000 t/a

|

|

|

|

|

Etchant Utilization System

|

|

Generation of Cupric sulfate from Etchant

|

|

2,000 t/a

|

|

—

|

|

Resource Recovery

|

|

Waste Solvent Recovery System

|

|

Production of Industrial-Class Organic Solvent Products with Waste Solvent

|

|

1,000 t/a

|

|

3,000 t/a

|

|

|

|

Valuable Metal Recovery System

|

|

Yielding of Valuable Alloy or Metal Oxide Products

|

|

5,000 t/a

|

|

10,000t/a

|

|

|

|

|

|

|

|

|

|

|

|

Collection and Sales of Recycled Material

|

|

Waste Sorting and Filtrating System

|

|

—

|

|

10,000 t/a

|

|

—

|

|

|

|

|

|

|

|

|

|

|

|

Sewage Treatment

|

|

Sewage Treatment Plant Operation (BOT)

|

|

Municipal Sewage Treatment Plant Operation and Management

|

|

30,000 t/d

|

|

100,000 t/d

|

|

Sludge Treatment

|

|

Municipal Sludge Treatment Plant Operation (BOT Project)

|

|

Municipal Sludge Plant Operation and Management

|

|

400 t/d

|

|

600 t/d

|

* Key: t = tons; t/d = tons per day; t/a = tons annually.

Customers

Our current customer base generally consists of the Dalian municipal government and Chinese and foreign manufacturers with industrial operations in the Dalian area that require collective handling and disposal of their waste products or by-products. The Dalian Gas Company is our sole customer for methane and customers purchasing our recycled materials are primarily commodity traders and metallurgical companies.

10

For the year ended December 31, 2010, our top 10 customers accounted for approximately 30% of our total revenues, and except for the Dalian municipal government which paid us $3.2 million in service fees in 2010, representing approximately 15% of our total revenues, no other single customer accounted for more than 10% of our revenues within our two primary areas of operation, industrial solid waste, sewage and sludge treatment and recycled materials. Our largest customers contributing the most revenue to our business include Canon Office Machine (Dalian), Toshiba (Dalian), STX Shipbuilding (Dalian), Yisheng Dahua Petrochemicals Co., Ltd., PetroChina Fushun Petrochemical, Dalian Pacific Electronic Co., Ltd., Dalian Pacific Multi-layer PCB Co., Ltd and Bosch (Dalian). The top 20 largest customers of the Company account for 4% of all customers and 59% of total treatment fees, whereas the remaining 96% of our customers contribute 41% of our revenues generated from waste treatment fees.

Industrial Solid Waste Treatment and Recycling. During the year ended December 31, 2010, we performed solid waste disposal services for more than 800 Chinese and foreign companies in Dalian. We typically enter into one-year renewable service agreements with our customers. For the year ended December 31, 2010 and 2009, our 10 largest solid waste disposal customers accounted for approximately 30 % and 23%, respectively, of our total revenues for such periods. The three largest solid waste treatment customers during 2010 were Dalian PetroChemical Co., Ltd., STX (Dalian) Co., Ltd. and PetroChina Liaoyang Petrochemical Company, Ltd., contributing 7%, 6% and 5%, respectively, to our total revenues from industrial solid waste for 2010.

In 2010, our main customers for recycled materials were manufacturers and trading companies, such as Xintai Alloy Co., Ltd and Jinbo Material Co., Ltd. During the fiscal years ended December 31, 2010 and 2009, we earned approximately $5.7 million and $3.6 million, respectively, in revenues from sales of recycled materials, representing approximately 26% and 34.3 % of our total revenues for such periods.

Municipal Sludge and Sewage Treatment. The Dalian municipal government is our sole customer for our sewage treatment business, and major customer for sludge treatment business. We have a BOT sewage treatment contract to process a portion of wastewater from Dalian until 2028. For our wastewater services, we receive quarterly service fees from the Dalian municipal government based on the volume of sewage that we process. Our fees for sewage treatment were approximately $1 million and $1 million in 2010 and 2009, respectively, representing 4.4% and 9.6% of our total revenues during such periods.

We operate the only sludge treatment facility in Liaoning Province, which became operational in 2010, pursuant to a 20 year BOT sludge contract. This facility generated approximately $2.23 million in service fees in 2010, which represented 10% of our total revenues in 2010. The methane we generated from sludge treatment is sold to the Dalian Gas Company. Our sales of methane in 2010 were approximately $1.25 million, representing 6% of our total revenues in 2010.

Competition

The environmental services industry in China is highly fragmented as it is in the early stage of development. The source of competition varies by locality and by type of service rendered, with competition coming from national and regional waste services companies, and numerous privately-owned firms of varying sizes and capabilities. Each of these competitors is able to provide one or more of the environmental services offered by us.

We believe our potential competitors are the large companies with comparable service offerings to ours, including Shenzhen Dongjiang Environmental Co., Ltd., Tianjin Hejia Veolia Environmental Service Co., Ltd., Hangzhou Dadi Environmental Protection Co., Ltd., and the Shanghai Solid Waste Disposal Center. These companies provide solid waste recycling services, recovery and treatment of waste materials, production and sale of recycled products, operation of environmental protection facilities through BOT projects and/or manufacture of environmental protection equipment. However, none of these companies currently operate in the Dalian area. We believe that our full service offerings in the industrial solid waste treatment and recycling, municipal sludge and sewage treatment and environmental equipment and engineering markets are very competitive with those of these larger competitors.

Within our principal market of Dalian and the surrounding areas of Liaoning Province, we believe we are the leader in our various areas of operation. We believe our longstanding relationship with the Dalian municipal government and 808 customers, about half of which are foreign multinational corporations, provides us with a distinct competitive advantage in this geographic market. Our main competitors in Liaoning Province are Liaoning Zhen Xing Ltd. and Liaoning Muchang Solid Waste Disposal Co., Ltd., companies focused primarily on solid waste disposal in Shenyang and the surrounding area. Within Dalian, our principal competitor is Dalian Pingan Environmental Protection, a smaller-capacity, private enterprise involved with the disposal of certain categories of hazardous waste.

11

The principal points of competition for all market participants are price, quality, reliability and scope of services, customer service and technical proficiency. Operating costs, disposal costs and collection fees vary throughout the geographic areas in which we operate. The fees we charge for waste treatment and sales of methane or recycled materials are either determined by the applicable BOT contract or determined through negotiations based on volume and weight, type of waste collected, treatment and transportation requirements, and risk of handling or disposal. We believe our comprehensive range of service offerings, technical expertise, established reputation/leadership and competitive pricing, provides us with a significant advantage over our competitors.

Our potential competitors must address certain barriers and issues in connection with entering the environmental services market in China, including (i) substantial capital investment in facilities and equipment; (ii) retention of qualified management; (iii) development of a loyal customer base and effectively servicing their waste treatment needs; and (iv) the procurement of government licenses and permits, especially for hazardous waste treatment.

Competitive Advantages

We believe that we possess significant competitive advantages over our competitors, including:

|

|

·

|

Strong Industry Reputation. With an operating history of over 20 years, we have established ourselves as the leading comprehensive waste management company in Liaoning Province and we enjoy a strong reputation for the quality of our services. Because of our expertise, Dalian government officials consult us on environmental protection regulatory matters. Furthermore, our Dagushan Expansion Project has been included as an authorized treatment center in the national centralized hazardous waste disposal facility plan established by the PRC National Development and Reform Commission. Our sewage and sludge treatment facility was voted the "Best Sewage Sludge Process Application of China" during the 2nd Water Specialist Conference held in Shanghai on August 31, 2010. We believe our strong reputation will make us a preferred service provider for future BOT projects and other environmental service agreements.

|

|

|

·

|

Broad and Growing Customer Base. In addition to serving the Dalian municipal government, we have a diverse customer base of 808 companies, including multinational companies such as Canon, Pfizer, Toshiba and Panasonic. Management anticipates that as additional large multinational enterprises establish operations in Liaoning Province, we will be their first choice to provide environmental services as we possess the advanced technologies to meet their specific waste management requirements.

|

|

|

·

|

Exclusivity and First Mover Advantage in Sludge Treatment. Our sludge treatment plant in Dalian is the only sludge treatment plant in Liaoning Province and is operated pursuant to an exclusive 20 year BOT project. We intend to use our award winning sludge treatment facility as a model to expand into other municipal sludge treatment BOT projects and to promote the installation of our Lipp sludge treatment tanks in other cities.

|

|

|

·

|

Comprehensive Service Capabilities. We provide a comprehensive range of services including solid waste treatment, waste collection and transportation, sludge and sewage treatment, environmental protection services, storage to landfill and on-site management. Our service capabilities enable us to customize a package of services to meet the needs of the clients that we service. We operate the only hazardous landfill in Dalian and operate our own fleet of vehicles to transport hazardous materials.

|

|

|

·

|

Strong research and development team. We believe we have an exceptionally strong research and development team with highly skilled and experienced personnel that collaborates with top universities and research institutions in China, as well as international companies to develop the most advanced and efficient technologies in the industry.

|

|

|

·

|

Experienced Management. Our senior management has extensive experience in environmental protection. Mr. Jinqing Dong, our Chief Executive Officer, founded Dalian Dongtai in 1991, and has over 20 years of experience in the waste treatment industry.

|

Sales and Marketing

Companies operating in Dalian and surrounding areas must comply with stringent regulations regarding waste disposal imposed by the Dalian municipal government. As the largest and most comprehensive service provider of industrial solid waste treatment solutions in Liaoning Province, we are generally the most viable alternative for companies to help them dispose of waste materials. As a result, we have not had to focus significant resources on sales and marketing efforts. As we expand our services to other geographic markets, we anticipate that we will need to conduct substantial sales and marketing activities to gain customers and increase market share.

12

Growth Strategy

Our goal is to become the premier provider of a comprehensive environmental services and solutions in China. The main components of our growth strategy are to:

|

|

·

|

Increase Research and Development to Develop and Commercialize New Technologies. We intend to increase our research and development efforts in order to capitalize on synergies and market opportunities. Through our significant research and development capabilities and collaborative partnerships, we can develop advanced technologies to expand the range of treatment services offered to our customers as well as open additional opportunities for our business.

|

|

|

·

|

Focus Core Business on Industrial Solid Waste Treatment. To maintain our focus on our core business of industrial solid waste treatment in order to take advantage of the treatment demand created by growing industrialization in Liaoning and Hunan Provinces. We are constructing our Dagushan Expansion Project to increase our hazardous waste processing capacity in Dalian to 114,000 tons per year, and focusing on the development of our hazardous waste treatment center in Changsha, Hunan, and our industrial waste disposal and recycling facilities in the Coastal Industrial Base of Yingkou, Liaoning. By handling higher waste volume, we can increase utilization of our facilities and enhance our overall profitability.

|

|

|

·

|

Expand Sludge Treatment Services to Selected Markets. To expand our sludge treatment services into other geographic markets in China, including Guangdong Province, through joint ventures, BOT projects, consulting and technology licensing. By promoting our nationally recognized sludge treatment process, we will be able to capture market share and revenues from the growing market for industrial and municipal sludge treatment.

|

|

|

·

|

Expand Geographic Coverage of Existing Service Portfolio. To penetrate other geographic markets in China through equity investments, joint ventures or BOT projects in the areas of industrial solid waste and sludge treatment. As the largest and most technologically advanced provider of waste treatment services in Dalian, we expect to expand our business into other major areas of Liaoning province where we currently do not have a presence, including the capital city of Shenyang.

|

|

|

·

|

Develop Ancillary Revenue Streams. To invest and develop our other revenue generating sources including engineering and consulting services, the sale of methane, recycled materials and Lipp tanks. We expect a growing demand for such ancillary services and products as business volume across our main lines of operations increases.

|

Research and Development

We generally spend approximately 5% of our annual revenues on research and development activities as we consider research and development to be a critical factor to maintaining our competitive edge over our competitors. For each of the two years ended December 31, 2010 and 2009 we expended approximately $358,973 and $513,631, respectively, on research and development activities.

Our current research and development projects include:

|

|

·

|

Development of an advanced hydration process to dispose of oily sludge generated from oil refineries.

|

|

|

·

|

Development of an efficient process to treat degradable wastes, such as kitchen waste, which can increase the volume of methane generated from the treatment process, and, in turn, sales of methane.

|

Intellectual Property

We have invested significantly in the development of proprietary technology and also to establish and maintain an extensive knowledge of leading technologies and incorporate these technologies into the services we offer and provide to our customers. We rely on a combination of patent and trade secret protection and other unpatented proprietary information to protect our intellectual property rights and to maintain and enhance our competitiveness.

As of December 31, 2010, we hold eight patents registered in China covering waste disposal systems and techniques and sludge treatment applications. In addition, we have three pending patent applications related to waste disposal and methane generation.

13

|

Status

|

Description

|

Patent Number

|

Expiry Date

|

|||

|

Granted

|

The Disposal of Powdered Ink Waste from Copy Machines

|

ZL 01 1 27963.X

|

7/20/21

|

|||

|

Granted

|

Consecutive Destructive Distillation Stove

|

ZL 200420069745.5

|

7/9/14

|

|||

|

Granted

|

Plasma Fusion Pyrolysis Device

|

ZL 200420069742.1

|

7/9/14

|

|||

|

Granted

|

The Disposal of Waste Catalyst

|

ZL 200410021093.2

|

1/20/24

|

|||

|

Granted

|

Method and Equipment For High-Efficiency Solid-Liquid Separation Under High Pressure

|

ZL 200610046723.0

|

5/26/26

|

|||

|

Granted

|

Equipment for High-Efficiency Solid-Liquid Separation Under High Pressure

|

ZL 200620091047.4

|

05/25/16

|

|||

|

Granted

|

Sludge Separation Method under High Pressure

|

ZL 200810010197.1

|

01/21/28

|

|||

|

Granted

|

Disposal System of Dehydrant Sludge

|

ZL 201020192022.X

|

05/11/20

|

|||

|

In Application

|

New Type of Solid Recycling Fuel and Its Manufacturing Method

|

—

|

—

|

|||

|

In Application

|

Hazard-free disposal of cathode tube

|

—

|

—

|

|||

|

In

Application

|

Purified System of Bio-gas

|

—

|

—

|

Under the PRC Patent Law, a patent is valid for a term of 20 years in the case of an invention and a term of 10 years in case of utility models and designs. Our registered patents are utility patents. Any use of a patent without consent or a proper license from the patent owner constitutes an infringement of patent rights. We cannot provide assurances that any patent applications filed by us will be approved in the future. We believe that we hold adequate rights to all intellectual property used in our business and that we do not infringe upon any intellectual property rights held by other parties.

We rely on unpatented technologies to protect the proprietary nature of our product and processing techniques. To that end, we require that our management team and key employees enter into confidentiality agreements that require the employees to assign the rights to any inventions developed by them during the course of their employment with us. The confidentiality agreements include noncompetition and nonsolicitation provisions that remain effective during the course of employment and for periods following termination of employment, which vary depending on position and location of the employee.

14

Industry Overview

Solid Waste Industry

The solid waste treatment industry in China currently is highly fragmented and in a very early-stage of development. The current market is primarily dominated by regional small-medium sized enterprises (SMEs), which account for approximately 90% of all environmental protection enterprises in the PRC. However, the technology and equipment utilized by SMEs are usually not very sophisticated. Only a few of those companies are involved in the industrial solid waste treatment business and there are currently no national players in that space.

The volume of solid waste generated by industrial companies is highly correlated with resource utilization rate, industrial production scale and consumption, and is expected to grow by over 10% per year according to the National Bureau of Statistics of China. In addition, according to estimates from the PRC Ministry of Environmental Protection, the production of industrial waste was approximately 1.34 billion tons in 2010, excluding approximately 13 million tons of hazardous industrial waste.

Solid Waste Market in Liaoning Province

Liaoning Province, where our primary operations are currently located, is in the midst of increased industrialization. Liaoning Province has a heavy industrial base with a broad group of companies engaged in the petrochemical, steel and iron, equipment engineering, shipbuilding, automobile making and pharmacy industries. The strong economic performance in Liaoning should facilitate rapid growth of our industrial solid waste business.

Major sources of industrial waste in the Dalian area include industrial enterprises, scientific research institutions and university laboratories. According to our internal research data, the total amount of solid waste the Company collected and disposed of in Dalian and surrounding areas grew from approximately 11,000 tons in 2001 to approximately 117,627 tons in 2010. Through our extensive solid waste treatment services, we believe we are well positioned to take a larger share of the growing solid waste treatment market in our principal market of Liaoning.

Wastewater Treatment Industry

China has very limited water resources with approximately 2,200 cubic meters per capita, which is only 25% of the world average according to a report by the United Nations. Water supply and demand has become an increasingly vital issue in China, especially the surging demand for clean water required for general and industrial usage. China has a very high rate of industrial water consumption, especially compared to that of developed nations, which offers many opportunities for water conservation and re-usage programs. China has experienced rapid economic growth and industrial expansion since the late 1970’s without too much regard for protecting its environment. Consequently, wastewater treatment and pollution control have recently become priority issues for the PRC government. In 2009, China discharged approximately 59 billion tons of wastewater, up 3.5% from 2008, and is expected to continue to grow to 79 billion tons by 2015, according to the PRC Ministry of Environmental Protection.

According to the PRC Ministry of Housing and Urban-Rural Development’s report dated June 11, 2010, as of March 2010 there were a total of 2,157 municipal wastewater treatment plants with a total daily treatment capacity reaching 109 million cubic meters. There were also 1,949 wastewater projects under construction, which were expected to add another 55 million cubic meters of treatment capacity. In the first quarter of 2010, the utilization rate of wastewater treatment plants in 36 major cities and counties in China was 82.2%, about 6% higher than the national average rate, with total processed volume of 2.93 billion cubic meters of wastewater, which reduced chemical oxygen demand discharge by 915,800 metric tons. By mandate from the State Council of China, 15 million cubic meters of additional wastewater treatment capacity was added by the end of 2010.

The escalating urbanization and industrialization trends in China today could further aggravate the problem. Despite new regulations and some improvement seen in recent years, clean water supply and sewage treatment remain crucial issues for the PRC central government. Water treatment is still a major problem for many cities in China and the success achieved in the past few years can easily be set back by continued rapid industrialization and urbanization. China’s wastewater treatment rate is still significantly below the rates commonly achieved in developed countries, while the treatment rate for municipal wastewater in China remains very low at 57.4%.

Sludge Treatment Industry

With China’s growing focus on wastewater treatment, there is a rising demand for sludge treatment as well, since sludge is the main terminal residue of wastewater treatment. In the next 10 years, there are expected to be thousands of wastewater treatment facilities located throughout China, which would increase the need for sludge treatment facilities. After processing, sludge can be used as raw material for fertilizer or new energy. Historically, however, most of the resulting sludge was not treated and thus caused secondary pollution. Wastewater and sludge treatment is a consistent process since without the utilization of sludge treatment, environmental benefits from wastewater treatment are greatly reduced. According to research by China Water Net, an online research organization focused on environmental protection, in 2009 a total of 20.05 million metric tons of sludge were discharged in the environment and is currently forecasted to grow to 23 million metric tons in 2010 and by approximately 15% annually thereafter. This creates an addressable market of approximately $28.8 billion in China, with municipal wastewater being the principal growth driver for the next few years as the total investment on sludge treatment facilities as of December 2010 is only 40% of that invested in existing wastewater treatment facilities.

15

Currently, the prevailing sludge treatment technologies are dehydrating and land filling. However, these methods are becoming outdated and more costly to implement. Another technology that was recently introduced in China from Europe is anaerobic fermentation, which is a series of processes in which microorganisms break down biodegradable material in the absence of oxygen. This offers a number of advantages, including reducing secondary pollution and producing a methane gas suitable for energy production. The Company utilizes anaerobic fermentation to dispose of municipal sludge and sells the resulting methane to the Dalian Gas Company.

Normally, net weight of dehydrated sludge accounts for approximately 0.6% of wastewater that is being processed. Currently, the China national standard “GB 24188-2009: Quality of sludge from municipal wastewater treatment plant” requires moisture content to be less than 80%, in addition to specific limitations on heavy metal content. In developed countries, however, the moisture content rate is generally substantially lower than 80%. Once the sludge has been treated, it can be recycled or disposed of using any of three methods: recycling to agriculture (land spreading), incineration or land filling.

Since the cost of sludge treatment is relatively high, historically there has not been much development in the sludge treatment market in China. However, following the recent regulation enforcement and the pressure of environmental protection, we expect this market to be a priority in the PRC’s upcoming 12th five-year plan.

According to the China Environmental Science Academy, sludge generated from sewage treatment plants throughout China will generate approximately 35 million tons of sludge per year by 2015. Only a few larger cities like Beijing, Shanghai and Guangzhou currently have sludge treatment facilities. As a result, we expect that there will be a surge in treatment demand for sludge and other degradable wastes within the next 10 years. Liaoning Province, for example, currently has 42 sewage treatment plants processing 4 million tons of wastewater every day, which are expected to generate 1 million tons of sludge per year in the aggregate (approximately 2,800 tons per day). However, there is currently only one sludge treatment plant in Liaoning Province, which is operated by the Company and has a daily capacity of 600 tons. In addition, Dalian Lipp, which targets degradable organic waste treatment market, is well positioned to capture additional opportunities in the sewage sludge treatment market, as well as the treatment of organic waste like kitchen waste and animal waste.

Since landfill and composting are not eco-friendly and have relatively high costs, we view these technologies as outdated. As a result, we believe anaerobic fermentation is becoming the most attractive and beneficial method for processing sludge.

Sludge Equipment and Engineering Services Industry

Sludge is an end product of the wastewater treatment process. Due to the increased construction of wastewater treatment plants in China triggered by the economic stimulus plan in 2009, the increase of sewage sludge will pose a rising threat to environmental conservation in China. To address the concern, the PRC Ministry of Environmental Protection has placed an increased emphasis on sludge treatment throughout China. The PRC central government has determined to increase the urban sewage treatment rate to 60% by 2010, when it is expected that the sewage treatment plants in China will collectively generate approximately 30 million tons of sludge per year, which should undoubtedly create a significant market for sewage sludge treatment in China. Through Dalian Lipp, we plan to market Lipp tanks and ancillary services to the growing sludge treatment market, including markets for degradable organic waste, such as kitchen waste and animal waste.

Government Regulation

We are subject to China’s national Environmental Protection Law, which was enacted on December 26, 1989, as well as a number of other national and local laws and regulations governing landfills, and air, water, and noise pollution and establishing pollutant discharge standards for wastewater.

Furthermore, on July 1, 2004, the PRC central government adopted the Measures for the Administration of Permit for Operation of Dangerous Wastes (the “Measures”). The Measures are intended to strengthen supervision and administration of activities relating to the collection, storage and disposal of dangerous wastes, and preventing dangerous wastes from polluting the environment.

Both the PRC Ministry of Environment Protection and local bureaus of environmental protection license and regulate companies engaged in waste disposal and treatment in China. The requirements for licensing have become more stringent, with applicants having to demonstrate a sufficient operating history and a number of professional technicians, as well as to comply with national and local environmental standards. The licensing process is also very time consuming and requires lengthy lead times.

16

Permits and Certifications

Companies operating in the solid waste processing industry in China are subject to stringent licensing and certification requirements on the national and provincial levels, including a mandatory three years industry experience for company management, transportation capabilities that comply with legal and environmental requirements and technical processes and technologies that are compliant with regulations on handling hazardous wastes. Our principal operating subsidiary, Dalian Dongtai, has been awarded an Environmental Protection Facility Operation License by the PRC Ministry of Environmental Protection. In addition, pursuant to the Measures, Dalian Dongtai has received a Permit for the Operation of Dangerous Wastes by the Liaoning provincial Bureau of Environmental Protection. Pursuant to such licenses, we are authorized for a term of three years to collect and process industrial waste in Dalian and the surrounding areas of Liaoning Province. Licenses can be renewed upon application to the PRC Ministry of Environmental Protection containing qualifying information on financial statements, operating history, verifications of technically trained staff, and research and development capabilities.

As of December 31, 2010, the Company believes that it is in material compliance with all applicable licensing and certification requirements relating to its business operations. However, there is no assurance that the central or provincial governments will not adopt new regulations or licensing requirements that will make it more difficult for the Company to operate in the environmental protection industry.

Employees

As of December 31, 2010, we had a total of 570 full-time employees. None of our employees are under collective bargaining agreements. We believe that we maintain a satisfactory working relationship with our employees and we have not experienced any significant labor disputes or any difficulty in retaining our employees or recruiting staff for our operations.

As part of our commitment to employee safety and quality customer service, we have an extensive training program and a certified staff to handle hazardous materials. We adhere to a risk management policy designed to reduce the likelihood of accidents and potential liabilities to us and to our customers. In addition, our property insurance provides limited coverage against pollution liability caused by our daily operations.

Organizational History

We were originally incorporated as a Delaware corporation in 1987 under the name of Egan Systems, Inc. In 1987, we acquired ENVYR Corporation as a wholly owned subsidiary and established our headquarters in Raleigh, North Carolina. From 1987 to 2003, we were primarily engaged in the business of developing, selling and supporting computer software products, particularly products related to the COBOL computer language.

In 2003, we acquired mining claims from Goldtech Mining Corporation, a Washington corporation, and in connection with the acquisitions, we changed our name to Goldtech Mining Corporation and re-domiciled to the State of Nevada.

We operated in two lines of business, mining properties and computer software until September 2004 when we sold our computer business. In September 2005, we ceased mining operations.

In 2005, we acquired a 90% indirect ownership interest (through a wholly owned Delaware subsidiary known as Dontech Waste Services Inc., which was originally known as Dalian Acquisition Corp.) in Dalian Dongtai, a waste services business in the PRC, in a reverse merger transaction. Dalian Dongtai was formed on January 9, 1991 as a limited liability company under the laws of the PRC.

As a result of the reverse merger, Dalian Dongtai became a joint venture with foreign investment under the laws of the PRC. The formation of the joint venture was approved by the Dalian Industry and Commerce Bureau, and the term of the joint venture is 12 years.

In March 2009, Dontech Waste Services Inc. was merged with and into the Company and Dalian Dongtai became an indirect 90%-owned subsidiary of China Industrial Waste Management, Inc.

17

|

ITEM 1A.

|

RISK FACTORS

|

Our business and operations are subject to a variety of risks and uncertainties and, consequently, actual results may differ materially from those projected by forward-looking statements. Factors that could cause actual results to differ from those projected, include, but are not limited to, those described below. There may be additional risks of which we are not presently aware or that we currently believe are immaterial which could have an adverse impact on our business. We make no commitment to revise or update any forward-looking statements in order to reflect events or circumstances that may change. You should carefully consider the risks described below and the other information contained in this Annual Report on Form 10-K before deciding to invest in our common stock.

Risks Related to our Business

Our failure to effectively compete in the industrial solid waste market may have a material adverse effect on our growth prospects and our ability to generate revenue.

We compete primarily on the basis of our ability to secure contracts with industrial companies, and local government entities in Dalian, China and surrounding areas for solid waste processing and disposal or for the purchase by us of waste material which we recycle. We enter into one-year contracts with our solid waste customers that are renewable on an annual basis. There can be no assurance that we will be able to execute such contracts with customers in new areas as we attempt to expand or that our competitors will negotiate more favorable arrangements with our current customers. We expect that we will be required to continue to invest in building waste treatment and disposal infrastructure.

Our competitors include both domestic companies and international companies operating in the waste treatment and disposal industry in China. Some of these competitors have significantly greater financial and marketing resources and name recognition than we have. As the Chinese government continues to allocate funds to be spent in our industry, more domestic and international competitors may enter the market. We believe that the Chinese market for our services is subject to intense regional competition, with a relatively limited number of large competitors. While we effectively compete in our primary market of Dalian and surrounding areas of Liaoning Province, our competitors occupy a substantial competitive position in other geographic markets into which we plan to expand. If the Chinese government continues to emphasize spending on environmental protection and continues to allocate funds to our industry, the number of our competitors throughout China will likely increase, so we cannot assure you that we will be able to compete successfully against any new or existing competitors, or against any new technologies our competitors may implement. All of these competitive factors could have a material adverse effect on our revenues, profitability and growth prospects.

We rely on our governmental permits and certifications to operate our business, the loss of any of which would have a material adverse impact on our business.

Only those companies that have been granted operating licenses issued by the PRC central and local governments are permitted to engage in the industrial waste treatment and disposal business in China. Our Dagushan expansion project has been listed as one of the 55 authorized centers in the Hazardous Waste and Medical Waste Treatment Facility Construction Program approved by National Development and Reform Commission. The central and local governments of the PRC impose strict requirements on companies regarding the technology which must be employed and the qualifications and training of management employees which must be maintained. While we possess the necessary permits and certifications to operate our business, the central government or Liaoning provincial government could determine at any time that we are not in compliance with certain technological or management requirements and revoke or suspend our permits to engage in the industrial waste business. If this were to occur, we cannot assure you that we can renew or obtain the necessary permits and certifications in a timely manner, or at all. As a result, the termination or suspension of our licenses to operate would have a material adverse impact on our revenue and business.

If we fail to introduce new products or services or our existing products and services do not meet the requirements of our customers, we may not gain or may lose market share.

Our continued growth is dependent upon our ability to generate increased revenue from our existing customers, obtain new customers and raise capital from outside sources. We believe that in order to continue to capture additional market share and generate additional revenue, we will have to raise more capital to fund the construction and installation of additional facilities and to obtain additional equipment to collect, process and dispose of industrial waste and recycle waste for our existing and future customers. We anticipate that the total funding requirement that we will require to finance the construction and installation of additional facilities, including our Dagushan Expansion Project, and to obtain additional equipment for us to accommodate a sharp increase in demand for waste management services and comply with more stringent regulatory criteria in environmental management, as well as to strengthen our presence outside of Dalian, China, through investment and/or acquisition, is approximately RMB28 million (approximately $4.3 million). We anticipate that such funding will be provided through a variety of sources including bank loans, equity financing and net cash flow generated from operations.

18

We expect to seek participation in additional BOT sludge treatment projects or form joint ventures for such projects, although no such projects have been identified by us at this time. In the future we may be unable to obtain the necessary financing for our capital requirements on a timely basis and on acceptable terms, which may prevent or delay the expansion of our service offerings. Our failure to provide new products or services may prevent us from retaining customers or gaining new customers, which may adversely affect our financial position, competitive position, growth and profitability. Our ability to obtain acceptable financing at any time may depend on a number of factors, including, our financial condition and results of operations; the condition of the PRC economy and the industrial waste treatment industry in PRC, and conditions in relevant financial markets in the United States, PRC and elsewhere in the world.

The rapid expansion of our business could strain our resources and adversely affect our ability to effectively control and manage our growth.

If our business and markets grow and develop, it will be necessary for us to finance and manage expansion in an efficient fashion. We may face challenges in managing our industrial waste treatment and disposal business over an expanded geographical area as well as managing expanded service offerings, including, among other things, sludge treatment services. In addition, we may encounter difficulties in integrating acquired businesses with our own. Such eventualities will increase demands on our existing management, workforce and facilities. Failure to satisfy such increased demands could interrupt or adversely affect our operations and cause administrative inefficiencies.

If we are unable to successfully complete and integrate our service offerings in new geographic areas in a timely manner, our growth strategy could be adversely impacted.

An important element of our growth strategy is expected to be the expansion of our existing service portfolio, including industrial solid waste, sewage and sludge treatment services, to other geographic markets outside of Dalian, China. However, integrating businesses involves a number of specific risks, including the possibility that management may be distracted from regular business concerns by the need to integrate operations, unforeseen difficulties in integrating operations and systems, problems relating to assimilating and retaining the employees of acquired businesses, accounting issues that arise in connection with acquisitions, challenges in retaining customers, and potential adverse short-term effects on operating results. In addition, we may incur debt to finance future operational locations, and we may issue securities in connection with future operational locations that may dilute the holdings of our current or future stockholders. If we are unable to successfully complete and integrate new operational locations in a timely manner, our business, growth strategy and financial results could be materially and adversely impacted.

Our waste treatment operations can be hazardous and may subject us to civil liabilities as a result of hazards posed by such operations.