Attached files

| file | filename |

|---|---|

| EX-31.2 - ASSEMBLY BIOSCIENCES, INC. | v216864_ex31-2.htm |

| EX-32.2 - ASSEMBLY BIOSCIENCES, INC. | v216864_ex32-2.htm |

| EX-32.1 - ASSEMBLY BIOSCIENCES, INC. | v216864_ex32-1.htm |

| EX-31.1 - ASSEMBLY BIOSCIENCES, INC. | v216864_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Transition Period from to

Commission File Number 001-35005

VENTRUS BIOSCIENCES, INC.

(Exact name of registrant specified in its charter)

|

Delaware

|

2834

|

20-8729264

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification No.)

|

99 Hudson Street, 5th Floor

New York, New York 10013

(Address of Principal Executive Offices)

(212) 554-4506

(Telephone Number, Including Area Code)

Securities Registered Pursuant to Section 12(b) of the Exchange Act:

|

Title of Each Class

|

Name of Exchange on which Registered

|

|

|

Common Stock, $0.001 Par Value

|

Nasdaq Capital Market

|

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

Non-accelerated filer ¨

|

Smaller reporting company x

|

||

|

|

|

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant, as of December 31, 2010, was approximately $37,348,210. Such aggregate market value was computed by reference to the closing price of the common stock as reported on the Nasdaq Capital Market on December 31, 2010. For purposes of making this calculation only, the registrant has defined affiliates as including only directors and executive officers and shareholders holding greater than 10% of the voting stock of the registrant as of December 31, 2010. The registrant used December 31, 2010 as the measurement date because it completed its initial public offering on December 22, 2010 and prior to that time no market existed for its voting stock.

As of April 8, 2011 there were 7,189,706 shares of the registrant’s common stock, $0.001 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The Company’s definitive Proxy Statement for its 2011 Annual Meeting of Stockholders (certain parts, as indicated in Part III).

VENTRUS BIOSCIENCES, INC.

TABLE OF CONTENTS

|

Page

|

||

|

PART I

|

1

|

|

|

Item 1.

|

Business

|

1

|

|

Item 2.

|

Properties

|

54

|

|

Item 3.

|

Legal Proceedings

|

54

|

|

Item 4.

|

[Removed and Reserved]

|

54

|

|

PART II

|

54

|

|

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

54

|

|

Item 6.

|

Selected Financial Data

|

54

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operation

|

55

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

63

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

63

|

|

Item 9A.

|

Controls and Procedures

|

64

|

|

Item 9B.

|

Other Information

|

64

|

|

PART III

|

65

|

|

|

Item 10.

|

Directors and Executive Officers of the Registrant

|

65

|

|

Item 11.

|

Executive Compensation

|

65

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

65

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

66

|

|

Item 14.

|

Principal Accounting Fees and Services

|

66

|

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

66

|

PART I

Item 1. Business

Overview

We are a development stage specialty pharmaceutical company focused on the development of late-stage prescription drugs for gastrointestinal disorders for which there are no approved prescription drugs in the U.S., specifically hemorrhoids, anal fissures and fecal incontinence. We are not aware of any prescription treatments for these conditions that have been approved by the U.S. Food and Drug Administration, or FDA, yet there are approximately 12.5 million Americans suffering from hemorrhoids, 7 million from fecal incontinence and over 4 million from anal fissures. Our lead product, Inferanserin (VEN 309) is a new chemical entity, or NCE, for the topical treatment of hemorrhoids. In multiple clinical studies in 359 patients, VEN 309 demonstrated good tolerability and no severe adverse events, and statistically significant improvements in bleeding, itchiness and pain. We have filed a special protocol assessment, or SPA, with the FDA to allow us to begin the first of two Phase III clinical trials for VEN 309.

Our additional product candidate portfolio consists of two in-licensed late-stage drugs intended to treat anal fissures (VEN 307) and fecal incontinence (VEN 308). These candidates are two molecules that were previously approved and marketed for other indications and that have been formulated into our proprietary topical treatments for these new gastrointestinal indications. In August 2007, we had a pre-investigational new drug, or IND, meeting with the FDA concerning VEN 307 (diltiazem cream for the treatment of pain from anal fissures) where it was established that next clinical studies needed for approval were two pivotal Phase III trials, preceded (if conducted in the U.S.) by three short-term dermal toxicology studies. In June 2007, we had a pre-IND meeting with the FDA concerning VEN 308 (phenylephrine gel for the treatment of fecal incontinence associated with ileal pouch anal anastomosis) where it was established that the next clinical study in the program should be a Phase II(b) study where multiple doses will be assessed and that existing toxicology data are sufficient to support this study. We have not had further meetings with the FDA on either VEN 307 or VEN 308 since the meetings in 2007. The development of the three products, VEN 307, VEN 308 and VEN 309, was delayed subsequent to the FDA meetings due to a lack of financial resources prior to the completion of our initial public offering in December 2010. We intend to use the proceeds from that offering to advance VEN 309 and VEN 307 through the next stage of development.

Major pharmaceutical progress has been made in the gastrointestinal therapeutic areas of gastroesophageal reflux, peptic ulcer disease and inflammatory bowel disease. However, many major gastrointestinal disorders still lack medical treatments. We are pursuing treatments for three of the ten most prevalent gastrointestinal disorders in the U.S. We estimate that the patient population of these three disorders exceeds 23 million adults in the U.S., based on the data we cite for each indication in this report.

Our Products and Development Strategy

Our three late-stage product candidates are:

Iferanserin ointment (VEN 309) for the topical treatment of hemorrhoids. Hemorrhoids, which are characterized by the inflammation and swelling of veins around the anus or lower rectum, can cause bleeding, itching, pain and difficulty defecating. Iferanserin (VEN 309), a NCE formulated as an ointment for intra-anal application, has highly selective, antagonistic activity against peripheral 5-HT 2 A receptors involved in clotting and the contraction of arteries and veins, two events believed to be associated with hemorrhoid formation. By limiting 5-HT2 A receptor activity, VEN 309 improves the flow of blood out of the dilated veins that comprise the hemorrhoid, thereby reducing bleeding, itchiness and pain. As reported by the National Institute of Diabetes and Digestive Kidney Diseases, hemorrhoids affect approximately 12.5 million adults in the U.S. Despite such a high prevalence, we are not aware of any FDA-approved prescription drugs for the treatment of hemorrhoids in the U.S. While there are commonly used prescription drugs in the U.S. for hemorrhoids in the U.S., such as Anusol, none have been approved by the FDA because they entered the market prior to 1962 and have not been designated by the FDA as safe and effective. Various combination products (such as the Preparation H line of products) are available in the U.S. over-the-counter, or OTC, under the FDA’s OTC monograph rule. The great majority of these treatments provide only temporary relief from the symptoms of hemorrhoids and do not address the cause of hemorrhoids. These treatments’ mechanism of action is either general, such as steroids, or acting as a protective coating on the hemorrhoid, in the case of most of the Preparation H products, or unknown, in the case of herbal remedies, and we are not aware of any reports published in medical journals on the efficacy or safety of any product currently marketed in the U.S. for the treatment of hemorrhoids. We believe VEN 309 to be more effective than the currently available conventional hemorrhoid topical therapies and more attractive than surgical procedures, which are the only other currently validated treatment options.

1

We have licensed Iferanserin ointment (VEN 309) from Sam Amer & Co., Inc., or Amer, who had developed VEN 309 through Phase II studies and up to readiness for Phase III studies in the U.S. and Europe. Our license includes rights to all existing intellectual property and any further improvements on VEN 309 owned by Amer for the topical treatment of anorectal disorders.

Diltiazem cream (VEN 307), a topical treatment for the relief of pain associated with anal fissures. Anal fissures are small tears or cuts in the skin that lines the anus. They can be extremely painful, cause bleeding and often require surgery, which itself can have unsatisfactory outcomes. At present, we are not aware of any FDA-approved drugs for the treatment of anal fissures. Diltiazem cream, however, is currently used as the preferred treatment by many gastroenterologists across the U.S. in a version that must be specially mixed for each patient in the pharmacy. Topical nitroglycerine has also been used in this way but has a higher rate of side effects than topical diltiazem, notably headaches. Custom-mixed diltiazem, however, is not an FDA-approved use nor is the cost reimbursed by Medicare or health insurance plans. When applied topically for the treatment of anal fissures, diltiazem, which has been used for decades for hypertension and angina, dilates the blood vessels supplying the region, reduces anal sphincter tone, and thereby substantially decreases pain. In the majority of multiple clinical trials conducted against placebo or topical nitroglycerine conducted between 1999 and 2002 by various researchers, diltiazem cream significantly reduced the pain associated with anal fissures. Our product VEN 307 is a proprietary formulation of diltiazem that when applied topically is only minimally absorbed, at one-tenth the amount of the lowest dose used for cardiovascular treatment. We believe this low absorption improves VEN 307’s safety profile and lowers the risk of side effects. We expect to capture immediate market share if VEN 307 is approved due to its known efficacy among gastroenterologists, its ease of prescription as a pre-formulated FDA-approved product with no need for custom mixing necessary at the pharmacy, and the ability for patients to be reimbursed through their health plan or Medicare. We have licensed the exclusive North American rights to VEN 307 for the topical treatment of anal fissures from S.L.A. Pharma who has completed early-stage clinical trials, toxicology studies and manufacturing for VEN 307 up to the end of Phase II.

Phenylephrine gel (VEN 308) for the treatment of fecal incontinence associated with ileal pouch anal anastomosis, an FDA orphan indication. Ileal pouch anal anastomosis, or IPAA, is a surgical procedure used as part of a colectomy, which is a treatment for patients with ulcerative colitis. Fecal incontinence resulting from dysfunctional sphincter tone is a common consequence of this procedure. According to a U.S. community based epidemiology study (Nelson et al., JAMA, 1995), 2.2% of U.S. adults suffer from fecal incontinence, which we estimate to be approximately 7 million people, based on 2009 Census Bureau adult population estimates. Currently, there are few options available to treat this problem, consisting of bulk laxatives, fiber diets, Imodium, which is a treatment for diarrhea, and invasive surgical procedures. In addition, Oceana Therapeutics is developing Solesta™, an injectable inert bulking agent product approved in the European Union for the treatment of fecal incontinence in adult patients who have failed conservative therapy. Solesta is injected submucosally around the anal sphincter and consequently has to be administered in an outpatient setting by qualified physicians. Oceana Therapeutics is currently pursuing approval of Solesta by the FDA. Also, Norgine plans to conduct a Phase I trial with NRL001, a suppository formulation of an alpha adrenergic stimulating agent for the treatment of fecal incontinence, which is anticipated to start in Europe in early 2011. We are not aware of any FDA-approved drugs for fecal incontinence. In multiple clinical trials with patients suffering from IPAA-associated fecal incontinence, topical phenylephrine significantly (and in some patients, dramatically) improved patient bowel control. In clinical trials with other forms of incontinence, improvements were also observed following application of topical phenylephrine, depending on the cause of the incontinence.

2

Our product VEN 308 is a gel formulation of phenylephrine. Applied topically, VEN 308 increases anal sphincter tone, thereby improving fecal incontinence in patients where sphincter tone is the major cause of their symptoms, such as post-IPAA surgery. We believe VEN 308 has significant advantages over the limited treatment options currently available for fecal incontinence associated with IPAA including, but not limited to, increased efficacy and/or reduced invasiveness. We have licensed the exclusive North American rights to VEN 308 from S.L.A. Pharma who developed the specific formulation of phenylephrine for the topical use in fecal incontinence and developed the manufacturing method. S.L.A. Pharma’s previous partner, Solvay, conducted important pharmacokinetic studies. We do not expect to continue developing VEN 308 in the short term.

Our Development Efforts

We do not own and did not develop any of our product candidates. We have licensed our three product candidates from third parties. All clinical trials to date have been conducted either by the licensor, the licensor’s previous partners or by independent investigators, as have the preclinical studies and product formulation activities. Since the time we licensed these products, we have focused our efforts on establishing and clarifying the regulatory pathway for late phase clinical trials and regulatory approval, and on establishing the contract manufacturing capacity and methods necessary to allow late phase clinical trials to proceed, all of which will be conducted by contracted third parties under our direction. These development efforts have not required many employees and we have historically operated with only a handful of employees with the scientific expertise necessary to progress our product candidates down the development path outlined above. This has helped us contain our operating costs. Subsequent to the completion of our initial public offering in late December 2010, we hired five employees and contracted with three individuals or entities to complete our staffing needs for our planned initial Phase III trial of VEN 309. However, we remain dependent on the availability and competency of these third parties for the continued development of our product candidates.

Our Management

Although incorporated in 2005, we began active operations in the spring of 2007 upon the licensing of VEN 307 and VEN 308 by Paramount BioSciences from S.L.A. Pharma. Shortly thereafter, we hired Thomas Rowland as our chief executive officer (who was then and remains one of our directors), Dr. Terrance Coyne as our chief medical officer, and Dr. John Dietrich as our vice president of clinical operations, as well as other employees. Due to our lack of capital, Drs. Coyne and Dietrich resigned in February 2009. Mr. Rowland resigned as our chief executive officer in February 2009, but he continued to act as our president from the date of his resignation in February 2009 until May 2010. Simultaneously with the resignation of Dr. Dietrich, we entered into a consulting agreement with him whereby he provides consultation on manufacturing, preclinical and clinical aspects of our drug programs on an as-needed basis. These arrangements with Mr. Rowland and Dr. Dietrich allowed us to continue minimal operations following their resignations until June 2010. Between February 2009 and June 2010, our only business activities consisted of maintaining our licenses with S.L.A. Pharma and Amer and financing and business development activities. Upon the successful completion of our convertible promissory note offering in May 2010, our Board of Directors determined to proceed with our initial public offering to raise capital to finance the partial development of VEN 309 and VEN 307. To conserve our resources, and recognizing that permanent employment would be dependent on our raising capital in our initial public offering, in June 2010, we entered into consulting agreements with Dr. Russell Ellison, our Chief Executive Officer and Chief Medical Officer, and David Barrett, our Chief Financial Officer. Between June 2010 and December 2010, our only business activities consisted of maintaining our licenses with S.L.A. Pharma and Amer and activities connected with our initial public offering. Effective on the completion of our initial public offering, we entered into employment agreements with Dr. Ellison and Mr. Barrett. From late December 2010 through February 2011, we completed the staffing for our planned development of VEN 309, including the extension of the consulting agreement with Dr. Dietrich through February 2012. We also added a clinician, two clinical project managers, a head of manufacturing, and an executive assistant, on a contract or permanent employment basis.

3

IFERANSERIN OINTMENT (VEN 309)

Background on hemorrhoids

Incidence and prevalence

Hemorrhoids are a common anal disorder, characterized by bleeding, itching, pain, swelling, tenderness and difficulty defecating. Based on information from an article entitled The Prevalence of Hemorrhoids and Chronic Constipation by J. Johanson and A. Sonnenberg published in Gastroenterology (1990; 98: 380-386), the point prevalence of symptomatic hemorrhoids in the U.S. adult population is approximately 5.7%, representing approximately 12.5 million cases based on 2009 population data published by the U.S. Census Bureau. The prevalence of hemorrhoids peaks in adults aged 45 to 65 years.

Patho-physiology of hemorrhoids

Hemorrhoids are symptomatic abnormalities of normal vascular structures in the anal canal that are manifested by dilation of the local arteries and veins due to constriction and partial obstruction of the exiting colonic veins. Although the exact mechanism for hemorrhoid formation is not clear, the progressive occlusion of venous exit vessels (e.g., as seen in straining during defecation, heavy lifting and pregnancy) is thought to produce stretching of the vessels in the hemorrhoidal plexus combined with vascular stasis. This stasis causes exposure of the blood to collagen, which in turn causes platelet clumping with the release of the platelet’s artery and vein constricting contents, including serotonin, which via stimulation of the 5HT2 receptor causes localized constriction of the exit arteries and veins, where most of the vascular smooth muscles are, and, in combination with other factors, causes a cascade effect producing clot formation. These events result in additional stasis of the blood, perpetuating and further worsening the situation. As hemorrhoids worsen, the trapped blood forms piles (protruding skin folds filled with static and thrombosed blood), initially above the pectinate line (internal hemorrhoids) and then below the pectinate line (external hemorrhoids). The classification of internal hemorrhoid grades by Banov is accepted by most specialists. This system consists of four grades and symptoms: first degree (grade I): hemorrhoids bleed but do not protrude; second degree (grade II): hemorrhoids protrude but reduce on their own; third degree (grade III): hemorrhoids protrude and require manual re-insertion; and fourth degree (grade IV): hemorrhoids protrude and cannot be manually re-inserted.

The cardinal symptom and most common manifestation of internal hemorrhoids is bleeding. Bleeding is often the only sign in grade I hemorrhoids, but it can also be accompanied by other symptoms as the hemorrhoids further enlarge, such as discomfort, itching, prolapse, and fecal soilage.

Current treatments

Despite the high prevalence of hemorrhoids, we are not aware of any FDA-approved prescription drugs for the treatment of hemorrhoids in the U.S. While there are commonly used prescription drugs for hemorrhoids in the U.S., such as Anusol, none have been approved by the FDA because they entered the market prior to 1962 and have not been designated by the FDA as safe and effective. Various combination products (such as the Preparation H line of products) are available in the U.S. under the FDA’s OTC monograph rule. The great majority of these treatments provide only temporary relief from the symptoms of hemorrhoids and do not address the cause of hemorrhoids. These treatments’ mechanism of action is either general, such as steroids, or acting as a protective coating on the hemorrhoid, in the case of most of the Preparation H products, or unknown, in the case of herbal remedies, and we are not aware of any reports published in medical journals on the efficacy or safety of any product currently marketed in the U.S. for the treatment of hemorrhoids. By contrast, our product, iferanserin ointment (VEN 309), has highly selective, antagonistic activity against peripheral 5-HT2 A receptors (5HT2 A >5HT2C>>5HT2B) involved in clotting and the contraction of arteries and veins, two events believed to be associated with hemorrhoid formation. By limiting 5-HT2 A receptor activity, VEN 309 improves the flow of blood out of the dilated veins that comprise the hemorrhoid, thereby reducing bleeding, itchiness and pain. We believe that the potential for side effects is likely to be limited because iferanserin is topically applied and iferanserin does not enter the brain to affect 5HT2 CNS receptors, at the exposures seen with topical application. In multiple clinical trials, iferanserin ointment significantly reduced bleeding, pain and itchiness compared to placebo with minimal adverse effects. As a result, we believe VEN 309 to be more effective and/or less invasive than the currently available conventional hemorrhoid topical therapies and more attractive than surgical procedures, which are the only other currently validated treatment options. Patients with persistent symptoms, especially bleeding, usually require an invasive procedure. The most common is rubber band ligation, which involves banding the internal hemorrhoid for four to seven days. Other procedures are the injection of a sclerosing agent, electrocoagulation, light therapy and hemorrhoidectomy. Most physicians treating hemorrhoids start with conservative therapy consisting of diet modification, fiber, sitz baths and stool softeners. In addition to this conservative therapy, physicians might prescribe topical steroids. The only other alternatives are invasive procedures and/or surgery. Because of the lack of effective prescription products, most hemorrhoid patients will use over-the-counter preparations or the prescription drugs available, which are similar to the over-the-counter treatment, but formulated with a higher dose of topical steroid. According to IMS Health (2006), 4.0 million prescriptions are written per year in the U.S. for unapproved hemorrhoid prescription products and 22 million units per year are sold in the U.S. for the unapproved OTC hemorrhoid products. If VEN 309 receives FDA approval in the U.S., we expect our competition for patient use and physician prescribing will be these drugs which have not been approved by the FDA and lack any medical study dated supporting their efficacy and safety. In Europe it appears that, from our discussions with experts and staff from other companies, many products exist, differently from country to country, and are mostly herbal extracts and mixtures in topical and systemic forms which are either prescribed or available over-the-counter. We do not have market data concerning these products in Europe, other than product acceptance market research, nor is their precise regulatory status clear to us.

4

INFERANSERIN OINTMENT (VEN 309) DEVELOPMENT

Background on Iferanserin

The early proof of concept for the utilization of a 5-HT2 A antagonist for the treatment of hemorrhoid was developed by Sam Amer PhD, a former director of research and development at Bristol Myer. Dr. Amer explored the potential application of serotonin drugs, which would not enter the brain at therapeutic concentrations, for use in various venous conditions. After successful pre-clinical and clinical experiments, Dr. Amer filed a method of use patent covering this molecule in 1992. Dr. Amer subsequently separated the S-isomer from this racemic mixture and filed new composition of matter patents for the S-isomer in 1998. Also in 1998, the early stage product was licensed to Tsumura, a Japanese company. Tsumura conducted over 350 pre-clinical and six clinical studies, but was not able to continue development due to financial difficulty and returned the product to Dr. Amer. Upon the return, Dr. Amer’s company, Sam Amer & Co., Inc., or Amer, conducted a double-blind, placebo controlled, multi-center confirmatory non-pivotal phase III study in Europe. After the successful completion of that study in 2003, Novartis Pharmaceuticals licensed iferanserin from Amer to be part of its gastroenterology portfolio strategy. Novartis improved the iferanserin manufacturing processes and completed important toxicology and metabolite studies. In 2005, Novartis’ lead gastroenterology product, Zelnorm™ was experiencing increased FDA scrutiny on the safety of that product, which would ultimately lead to its eventual withdrawal from the market. We believe that with the impending loss of their lead gastroenterology product, Novartis decided to dissolve the gastrointestinal franchise. In 2005, Novartis returned iferanserin to Amer. According to Amer, no safety or clinical issues were ever communicated as reasons for the return.

On February 5, 2008, in conjunction with Amer, we held an End of Phase II meeting with the FDA, to confirm the U.S. regulatory status and pathway to a new drug application, or NDA, for iferanserin ointment where it was agreed that the product may enter late-stage Phase III development. In March 2008, we licensed exclusive worldwide rights to develop and market iferanserin ointment for the treatment of anorectal disorders from Amer.

Mechanism of action on iferanserin

Iferanserin has selective antagonistic activity against 5-HT2 receptors, especially against those involved in contraction of vascular smooth muscle and platelet aggregation (clotting), the 5HT2A receptors. It is a particularly potent high-affinity antagonist of 5HT2A, has less affinity for and is a moderate antagonist of 5HT2C and has considerably less affinity for 5HT2B receptors. In a specific validated model, iferanserin did not demonstrate any agonism activity at 5HT2B receptors, but did demonstrate moderate antagonistic activity. Unlike other 5HT2 receptor antagonists, iferanserin’s 5HT2 receptor antagonism, clinically, is entirely peripheral, meaning it occurs outside the central nervous system because iferanserin does not cross the bloodbrain barrier except in extremely high exposures far above those seen with topical application. Studies conducted in 1997 and 1998 by Amer in rats addressed the potential effects of iferanserin on impaired rectal mucosal blood flow and increased peripheral vascular resistance after administration of serotonin or thrombin. At doses of 3 mg/kg and above administered intrarectally, iferanserin improved rectal mucosal blood flow and normalized the peripheral vascular resistance. Iferanserin had minimal effects on arterial blood pressure.

5

Preclinical safety

Iferanserin has been extensively tested in multiple preclinical models. The iferanserin exposure from dosing in humans topically using 0.5% applied twice daily (the dose to be used in our planned studies) ranges from 1/17th to 1/88th of the exposure that produces toxicity and from 1/45th to 1/85th of the exposure that produces cardiovascular effects in animal toxicology studies and 1/60th − 1/100th of the exposure that produces these effects in vitro. In addition, iferanserin exhibits low systemic exposure, with less than 10% bioavailability, based on a pre-clinical rat study.

Clinical trials and patent status

A total of seven clinical trials with iferanserin have been completed by Amer (excluding Japan) and Tsumura in Japan between 1993 and 2003. One Phase I study and one Phase II study were completed using the racemic mixture of iferanserin. After the successful Phase II proof-of-principle study, the licensor, Amer, separated the R- and S-isomers (the two active components of most small molecule pharmaceuticals), determined that the primary activity was focused in the S-isomer and filed a patent claiming this isomer. The patent issued in the U.S. and other countries and expires in 2015. In the U.S., the patent was filed with Dr. Amer as the inventor and in all foreign countries with Amer as the assignee. After the development of the S-isomer in the mid 1990s and the patent filing in 1998, the remaining studies — two Phase I studies, two Phase II studies, and one Phase III study — were all conducted with the S-isomer product. This development progression (racemic to S-isomer) is a common pharmaceutical practice, enabling companies to use the purest form of the molecule in late-stage clinical trials.

Our license agreement with Amer includes the rights to all intellectual property owned by or assigned to Amer as well as to any new improvements owned by or assigned to Amer. Different concentrations of a drug are separately patentable. Because of unexpected differences between concentrations of the product that were observed in the clinical program (i.e. that 0.5% concentration is superior to a 0.25% and a higher 1.0% concentration in the comprehensive reduction in hemorrhoid symptoms), which data have not been previously published, we filed in August 2010 a patent claiming our specific concentration range (among other claims) which, we believe, if issued, would be considered new art and provide patent protection for 20 additional years. Dr. Amer is the inventor in this U.S. application and the assignee in the patent application. However the original S-isomer patent could be challenged by a third party and invalidated, and the concentration patent may never issue and even if issued could be challenged by a third party, in which case we would have five years of U.S. market exclusivity under the Hatch-Waxman Act.

An investigator IND for iferanserin was filed with the FDA in November 1991 and transferred to Amer as the sponsor in January 1994 and remains open.

Trial Results

Overall safety

In the seven clinical studies of iferanserin conducted by Amer and Tsumura in 359 individuals, of whom 220 were exposed to iferanserin, the adverse effects, at least possibly related to the iferanserin administration, were mostly gastrointestinal (diarrhea, lower abdominal discomfort, residual stools, and anal irritation). These events were considered mild by the investigators and required no medical treatment. There were no serious adverse events judged by the investigator as related to iferanserin and no mortality in these studies. There was one report of exacerbation of atopic dermatitis requiring observation in hospital with an uncertain relationship to iferanserin.

6

Clinical Pharmacology in Normal Volunteers (Phase I)

Two clinical pharmacology studies were conducted in Japan by Tsumura in 1998 and 1999 in 18 healthy volunteers exposed to a single dose and in six healthy volunteers exposed to six days of dosing with the 1% preparation. Three mild adverse events where the drug could not be ruled out were observed in three patients in the single dose group and four mild adverse events were observed in three patients in the multi-dose group. There is no accumulation of the drug on twice daily dosing and the half life at one and six days is 1.6 hours. Peak concentrations are similar at one and six days and well below the lowest exposure where toxicity was observed in toxicology experiments in animals.

One patient was identified as having a very compromised activity of an enzyme, CYP2D6, and the maximum concentration of the drug in this patient was three times the maximum observed in the other patients and the total exposure (AUC) was 17 times that observed in the other patients. However, these exposures to the drug were still well below the lowest exposures where toxicity was observed in animal toxicology experiments, and this patient did not experience any adverse events.

As is typical of several modern drugs for depression such as Fluoxetine and older drugs such as tri-cyclic anti-depression agents and other drugs extensively prescribed, iferanserin is an inhibitor of the enzyme CYP2D6 and is at least partially dependant on this enzyme for its metabolism. Therefore kinetic interactions with other drugs that are potent inhibitors of CYP2D6 and or are highly dependent on CYP2D6 for their metabolism are possible. There are several of these drugs and most are psychiatric medications, and one is tamoxifen. We will exclude patients from the clinical trials who are taking such drugs, and will be conducting extensive drug-drug interaction studies as part of our clinical pharmacology program to clarify which drugs could be affected by or could affect iferanserin. We intend to conduct these studies contingent on having sufficient resources after the completion of the first planned Phase III trial.

Proof-of-concept study (U.S.)

A double-blind, placebo-controlled study of 26 patients conducted by Amer that was completed in August 1992 and published in August 1994 was the first clinical trial to test the activity of the racemic mixture of iferanserin. Topical 1% iferanserin ointment was applied three times daily for five days to calculate the effect on bleeding and other symptoms in patients with grade I to III external hemorrhoids. Treatment produced statistically significant improvements in ease of defecation, throbbing, fullness, bleeding and tenderness. Itchiness and pain were also reduced following treatment. These positive treatment effects started immediately after treatment and were maintained throughout the study.

Early Phase II dose-ranging study (Japan)

Topical iferanserin ointment, in twice-a-day doses of 0.25%, 0.5%, and 1.0%, was provided to 72 patients for 14 days to treat symptomatic internal and mixed internal/external hemorrhoids. A total of 68 patients were evaluable for analysis: 23 patients in the 0.25% dose group, 24 patients in the 0.5% dose group, and 21 patients in the 1.0% dose group.

There was a significant change in ease of defecation between dose groups by day 7 but no other differences in improvements of symptoms among the three dose groups. Anal discomfort and pain persistence improved with increasing dose on a visual analog scale, or VAS, of pain. For the symptom of bleeding, a significant difference between dose levels (P = 0.016) and a paired comparison statistical analysis showed that the 0.5% dose was more effective than either the 0.25% dose or the 1.0% dose. By day 14, hemorrhoid swelling was reduced in the 0.5% dose group (41%) and the 1.0% dose group (43%). A review of patient diaries revealed that all symptoms started improvement on day 1, with improvement peaking at day 7 and being maintained to day 14. Comparison of all doses showed, unexpectedly, that the 0.5% dose provided the most consistent improvements.

7

There were 45 adverse events, but only five (11%) were judged as related to iferanserin ointment. These iferanserin-related adverse events were mostly mild diarrhea or lower abdominal discomfort, which required no medical treatment. Laboratory tests were generally normal, with the exception of one case of mild elevation of total bilirubin one month after trial completion, which required no therapy. Further evaluation of metabolites revealed no relationship to adverse events. The unexpected and novel finding that 0.5% concentration is superior to both a lower (0.2%) and higher (1%) concentration supports our patent claiming a specific concentration range that we filed in August 2010, which, if issued will expire in 2030.

Late Phase II study (Japan)

A double-blind, placebo-controlled trial was conducted by Tsumura Company with three different concentrations of iferanserin ointment (0.25%, 0.5% and 1%) administered twice daily for four weeks for treatment of 104 patients with grade I to III internal hemorrhoids. The study was completed in July 2002 and published in February 2003. Inclusion criteria required a minimal degree of either bleeding or prolapse. The primary endpoint was physician-rated size reduction of the hemorrhoids; secondary endpoints included subjective symptoms as assessed by patient diaries and VAS. By day 28, compared with placebo, the concentrations of 0.5% and 1% of iferanserin showed the most consistent improvements across groups for secondary symptoms, such as bleeding, pain severity and duration, and ease of defecation.

PhaseIIB/III study (E.U.)

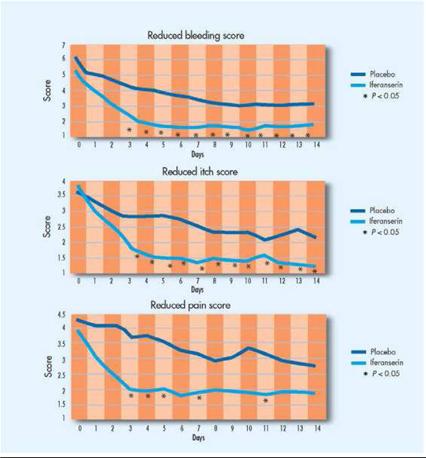

Based on the results of the two Tsumura Phase II trials, a double-blind, randomized, placebo-controlled study was conducted by Amer to compare 0.5% iferanserin ointment with placebo when administered twice daily for 14 days for treatment of 121 patients with symptomatic grade I to III internal hemorrhoids. The disease specific inclusion criterion was diagnosis of grade I − III hemorrhoids with bleeding episodes of at least every other day during the last two weeks before enrollment in the study. Exclusion criteria included patients with protruding or irreducible hemorrhoids (grade IV), and patients with anal fistulas, periproctitis or hemorrhagic diathesis. Daily patient diaries for bleeding, itching and pain/discomfort were recorded for 14 days, and patient assessments were recorded at days 7 and 14 based on a 10-point scale. A physician evaluation for prolapse and size occurred at baseline and day 14. Fifty-six patients, each in the active and placebo treatment groups, were evaluable for the primary endpoint, which was bleeding. Not all patients had each of the other symptoms, but sufficient numbers were available for statistical analyses to be performed for bleeding, pain, itching and dyschezia, which is extensive straining with stools.

Compared with placebo, iferanserin ointment significantly reduced bleeding (P < 0.05) by day 3, a reduction maintained to day 14 (Figure 1). Total cessation of bleeding occurred in 89% of the iferanserin-treated patients versus 68% of the placebo-treated patients. Compared with placebo, iferanserin ointment also significantly reduced itching (P < 0.05) by day 3. Total elimination of itching by day 14 was achieved in 90% of the iferanserin-treated patients versus 62% of the placebo-treated patients. Finally, compared with placebo, iferanserin ointment significantly reduced pain (P < 0.05) by day 3, effecting a total elimination of pain in 78% of patients versus 46% of patients in the placebo group. There were also no clinically significant adverse findings for either iferanserin or placebo.

8

Figure 1. In a Phase III double-blind, randomized, placebo-controlled study of 121 patients with grades I to III internal hemorrhoids, iferanserin ointment significantly improved bleeding, itching, and pain.

After the end of Phase II meeting with the FDA and as part of the SPA review process, we commissioned a post hoc analysis of the study for the end point that the FDA agreed would be the primary efficacy endpoint for the pivotal trials. This endpoint is defined as time to cessation of bleeding that lasts for three days or more for which iferanserin 0.5% twice daily will be compared with placebo. In this analysis, the median time to cessation of bleeding in this 14 day study was 10.5 days in the placebo group and 4.5 days in the treatment group which was statistically significant (P < 0.01) (Figure 2).

9

Figure 2. In a Phase III double-blind, randomized, placebo-controlled study of 121 patients with grades I to III internal hemorrhoids, the median time to complete cessation of bleeding was 4.5 days for iferanserin ointment versus 10.5 days for placebo (p 0.01).

In this Phase III double-blind, randomized, placebo-controlled study of 121 patients with grades I to III internal hemorrhoids, iferanserin provided rapid and sustained improvements of the main symptoms of this disorder: bleeding, itching and pain. Maximal improvements of symptoms occurred by day 7 and were maintained to day 14 at the end of the trial.

Iferanserin ointment (VEN 309) development plan

At the end-of Phase II meeting held in February 2008, the FDA advised us that, as is common for chronic or repeated use drugs, it would require for submission of the NDA:

|

|

·

|

a total safety database of 1,500 patients exposed to iferanserin, a proportion of which need to be followed for repeat use for six months and 12 months (standard International Conference on Harmonization recommendation);

|

|

|

·

|

included in this safety database, two placebo controlled studies would be required with the primary endpoint being time to cessation of bleeding for a minimum of three days;

|

|

|

·

|

also included in the safety database a clinical pharmacology program consisting of a thorough QT study (standard for most drugs), drug-drug interaction studies, and pharmacology in special populations will be required; and

|

|

|

·

|

as is usual for chronic or repeated use drugs, carcinogenicity studies in two species exposed for 104 weeks, preceded by dose ranging studies and 6 months toxicology in rats and 9 months in dogs.

|

As the carcinogenicity study (including the prior dose ranging study) will take up to 40 months to complete, we intend to conduct the Phase III studies sequentially as this will not delay the program, will conserve funds and allow adjustments (for example, increased sample size) to the second Phase III study to optimize its potential. We anticipate that we will initiate the first patient randomized into the first Phase III trial on or about the end of the second quarter of 2011, and that data will be available in the first quarter of 2012. We also intend to initiate the dose ranging part of the carcinogenicity studies in 2011, and to initiate the carcinogenicity studies themselves in the second half of 2011. We originally filed in June 2008 an SPA with the FDA to ensure their explicit agreement with our Phase III protocol for VEN 309. Due to lack of funds we could not follow up or complete the process but were able to resume with another filing in March 2010 and received comments in May 2010. We filed another submission in July 2010 which could not be processed because the FDA required us to reformulate the questions set forth in the filing. In August and September 2010, we had a series of emails and telephone calls with the FDA in which we believed that agreement has been reached on the precise definition of the endpoints and how to assess recurrence of hemorrhoids in the study and on October 28, 2010 we filed another submission reflecting these discussions.

10

In that SPA, we originally proposed for the pivotal trial design:

|

|

·

|

400 patients randomized, double blind, to either placebo ointment or iferanserin 0.5%, both applied twice daily (to be conducted in 60 community sites in the U.S. and Canada);

|

|

|

·

|

14 days treatment with follow up at 28 days;

|

|

|

·

|

Rolling over all patients to active treatment after 28 days double blind follow up visit, to be followed for 12 months, with retreatment for recurrence monitored;

|

|

|

·

|

Inclusion criteria to include patients with symptomatic Grade I to III internal hemorrhoids, bleeding from hemorrhoids every day for the two days immediately preceding the day that they are randomized and study medication applied, with pain or itching accompanying the bleeding for the two days;

|

|

|

·

|

Exclusion criteria to exclude patients with grade IV hemorrhoids; thrombosed internal or external hemorrhoids; laxatives, anticoagulants, over-the-counter anti-hemorrhoidal agents, topical steroids, suppositories of any kind, non-steroidal anti-inflammatory drugs (NSAIDs), Cox-2 inhibitors, and other drugs and conditions including potent inhibitors of CYP2D6 such as fluoxitene; and

|

|

|

·

|

The primary endpoint will be time to cessation of bleeding for a minimum of 3 days and secondary endpoints will be cessation of pain and cessation of itching for three days.

|

In March 2011, we had a formal meeting with the FDA to discuss the feedback received on the SPA that we submitted to the FDA in October 2010, in order to resolve remaining issues that would allow an agreement of the protocol between us and the FDA. The primary focus of the meeting was the FDA’s recommendations for changes to the definitions of the primary and key secondary efficacy endpoints of the protocol submitted in the SPA. We viewed the suggestions as improvements to the endpoints as well as enhancing their clinical meaningfulness and readily agreed to the changes. We submitted a new SPA on March 16, 2011, that includes a revised protocol, including the newly defined endpoints, and expect a response within 45 days, which is the customary FDA review period.

For the double-blind part of the study, where patients are treated twice daily for two weeks and then followed up on Day 28, the improved, FDA-recommended definitions for the endpoints, which remain subject to FDA agreement with the protocol for the SPA, are:

|

|

·

|

Primary: Proportion of patients with cessation of bleeding by the end of Day 7 that persists for the remainder of the treatment period (through Day 14) (replaced cessation of bleeding for a minimum of 3 days); and

|

|

|

·

|

Key Secondary: Proportion of patients with cessation of pain and/or itching by the end of Day 7 that persists for the remainder of the treatment period (through Day 14) (replaced cessation of pain and cessation of itching for three days).

|

We have modeled the potential performance of these new endpoints for the Phase III study using data from a prior double-blind Phase IIb study conducted in Germany which randomized 121 patients to iferanserin or placebo ointment. In the German study, using the statistical methodology proposed for the analyses of the primary endpoint in our planned Phase III study, the difference between the proportion of patients responding to treatment under the new endpoint definition for cessation of bleeding in the iferanserin arm (57% responders) and the placebo arm (20% responders) was considerable with a p <.0001 (Figure 3).This is an improvement over the prior endpoints, which were time-to-bleeding cessation (defined as three consecutive days of no bleeding) as the primary, and proportion of patients who had three days cessation of pain and/or itching as the secondary, due to a more rigorous definition of the endpoint in terms of the duration of effect required for a response. In fact, the difference in proportion of responders between treatment arms in this analysis of the proposed revised primary endpoint is almost twice that seen in an analysis of the previously defined primary endpoint, mostly due to the much lower response in the placebo group as would be expected with a more rigorous definition. Similarly, analyses of the key secondary endpoints of pain and/or itching also showed considerable differences between iferanserin and placebo.

11

We believe the new endpoint definitions confirm the projected power of > 90% for the primary endpoint and > 90% for the key secondary endpoints for the proposed Phase III study design of 400 patients randomized 1:1 to iferanserin or placebo ointment. Since the study size and power appear to be re-affirmed by this change, and since all of our clinical study sites will be using central Institutional Review Boards (IRBs) with rapid review times, and contracting with sites is already underway, we believe that our estimated timelines for study start (mid-summer 2011), completion of enrollment (year-end 2012), and availability of data (first quarter 2012), remain unaffected by the proposed new endpoints.

Figure 3. Analysis of new endpoints in the Phase IIB study: In a Phase III double-blind, randomized, placebo-controlled study of 121 patients with grades I to III internal hemorrhoids, 57% of iferanserin treated patients had cessation of bleeding by day 7 that continued through day 14 versus 20% of placebo treated patients (p < 0.0001).

After the results of the Phase III study are available, and if we raise additional capital, we intend to continue the carcinogenicity study, conduct the 6 and 9 month chronic toxicology studies and launch either an identical Phase III trial and a safety study, or a larger Phase III trial to provide adequate numbers of patients exposed, and to complete the clinical pharmacology program which, will include extensive drug-drug interaction studies to clarify the CYP2D6 interactions and a ‘‘thorough QT study’’ to test the arrythmogenic potential, which studies are routinely required by the FDA. We will also explore at that time the feasibility of lifecycle options for follow-on products such as combinations with steroids and other agents or different formulations such as suppositories, which could be developed for launch after approval of the original VEN 309 product.

We expect that the earliest we will be able to file a NDA with the FDA will be mid 2014, and the earliest the product could be approved in the U.S. would be in 2015. However, the Phase III trial may not meet the primary endpoint, or unexpected safety problems could arise, or even if the study is successful we may not be able to obtain more capital for other reasons, in which case we may not be able to complete the development of the product and we may not be able to effect the payments due to Amer on a timely basis, which could result in the loss of our rights to the product.

Commercial summary for iferanserin (VEN 309)

Market research regarding hemorrhoids

Market research conducted in 2001 by Amer with both patients and physicians shows a significant dissatisfaction with current treatment options and the need for a product that relieves multiple hemorrhoidal symptoms. In a survey conducted with 57 hemorrhoid patients, average satisfaction with current prescription treatment was rated at 6.0 on a 10-point scale. The most desired treatment effects of a new hemorrhoidal medication that patients described would be ‘‘fast onset,’’ and ‘‘bleeding cessation.’’ The most frequent hemorrhoidal symptoms these patients reported experiencing were itching (79%), bleeding (77%) and pain (68%).

12

A research study conducted by Amer of 40 physicians (30 primary-care physicians, five proctologists, and five colon and rectal surgeons) evaluated their satisfaction with current treatment for hemorrhoidal treatment on a 10-point scale. The level of satisfaction with current treatment for reducing bleeding was 6.4; for relieving itch, 7.1; and for reducing pain, 6.8. The physicians indicated that the most desirable treatment effects of new hemorrhoidal medication would be ‘‘fast onset (2 to 3 days)’’ and ‘‘multi-symptom relief.’’ Another research study of 98 physicians showed that most physicians would replace their current first line therapy with iferanserin ointment, if it is approved.

DILTIAZEM CREAM (VEN 307)

Background on anal fissure

Incidence and prevalence

Anal fissure, which is a crack in the skin of the anal canal that results from reduced blood supply to the area and/or from increased sphincter tone, is a common anal disorder characterized by severe anal pain and bleeding with or after bowel movements. Because there are no approved pharmacological treatments for anal fissure, many cases progress to surgery because of the severe pain. There are no formal epidemiology studies for anal fissure, but its prevalence has been estimated indirectly. When 1,500 unselected neurological inpatients were screened in studies between 1990 and 1998 conducted in the U.S. by Dr. Wolfgang Jost, the prevalence of anal fissure was estimated at 1.6% in males and 2.2% in females. By extrapolation to the 2009 U.S. population of 227 million adults, we estimate that the general prevalence rate is 1.9%, with approximately 4.3 million current cases.

Physiology of anal fissure

Although hypertonia, or an increase in tightness of muscle tone, of the internal anal sphincter, or IAS, is associated with anal fissure, its contribution to the cause of anal fissure remains unclear. Hypertonia of the IAS does, however, contribute to chronic anal fissure. Anatomical, angiographic, and blood-flow studies have shown that the vascular supply of the anal epithelium, or tissue lining the anus, is very poor in the posterior midline, the anal area most commonly affected by fissures. Thus, it is possible that decreased anodermal blood supply to this area contributes to the pain and ischemia, or decrease in the blood supply, of traumatized anal epithelium, perpetuating ulceration and preventing healing. Whether the primary event for anal fissure is hypertonia of the IAS or decreased blood supply, hypertonia itself reduces vascular perfusion in the anal area. This reduction of vascular perfusion has been compared with that associated with ischemic pain in the lower limbs.

Current treatments

Presently, there are no FDA-approved drugs of which we are aware for the treatment of anal fissure in the U.S. The clinical goal in treating anal fissures is to reduce the pain associated with the fissure long enough for it to heal naturally and prevent the patient from having to resort to surgery. Currently, most physicians start treatment with diet modification, fiber, sitz baths and stool softeners. If these conservative treatments fail, physicians proceed to pharmacologic therapy, prescribing topical steroids or by directing special pharmacies to create compound topical formulations by mixing raw diltiazem, and in some cases nitroglycerin, into a cream for topical use by fissure patients. If these pharmacologic treatments fail to manage the pain, physicians consider, and often perform, surgery. In some instances, physicians initially prescribe pharmacologic therapy in addition to conservative treatments; in other instances because of the severe pain, they initially perform surgery.

13

The purpose of surgery is to reduce hypertonia of the IAS by either manual dilatation or lateral sphincterotomy. Both procedures are highly successful in relieving the pain and promoting healing of fissures. Although a relatively simple and effective surgical procedure, lateral sphincterotomy is also associated with short-term mild-to-moderate fecal incontinence. This is not an insignificant adverse effect and can become permanent or at least chronic in a fairly high percentage of patients. Studies have shown 6-8% of patients had incontinence to flatus or minor fecal soiling at a time greater than five years after surgery. In another study, at a mean follow-up time of 66.6 months (range 30-84 months), 10% of patients who had a lateral internal sphincterotomy were incontinent.

Over the last decades, a drug developer attempted to gain FDA approval for the topical treatment of anal fissures with nitroglycerin, an agent that reduces IAS and anal fissure pain. Early attempts to develop nitroglycerin utilizing a healing endpoint failed as it was discovered most fissures will heal naturally if the patient can endure the pain for the first several weeks of the disorder. However, it was discovered during development that lowering IAS hypertonia did have a significant benefit in reducing the pain associated with anal fissures. The subsequent pivotal studies with pain as a primary endpoint demonstrated a 33% reduction in pain scores in patients with baseline pain score >48 (1-100 mm on the visual analog scale, or VAS). However because the developer did not use minimum pain scores as an inclusion criteria, the overall effect was diluted to 22%. In addition, 64% of subjects reported headaches, which is a known systemic side effect of nitroglycerin. The FDA denied its approval, concluding that the risk benefit ratio for nitroglycerin as topical treatment for anal fissure pain was not favorable due to the modest overall effect and high incidence of systemic side effects. We have planned a clinical program that focuses on pain as the primary endpoint and includes only patients who have adequate pain scores on entry into the studies, which we believe will avoid the modest effects seen in the earlier study. In addition, based on results of previously published trials (such as Kocher et al. 2002; see Table 1 below), we believe that the side effects of diltiazem cream are likely to be less than those observed with topical nitroglycerin, which primarily were headaches.

DILTIAZEM CREAM (VEN 307) DEVELOPMENT

Background on diltiazem

Diltiazem was first approved in 1982 in oral form for the treatment of angina and high blood pressure. It has been prescribed in the U.S. for millions of patients in oral dosages typically from 240 mg to 360 mg per day. In contrast, daily doses of VEN 307 for treatment of anal fissures will range from 15 to 45 mg. Because of the extensive patient exposure to diltiazem as a cardiovascular agent and the wide safety margin as a low dose topical therapy, we intend to develop the topical formulation as a Section 505(b)(2) NDA, as agreed with the FDA at our pre- IND meeting in August 2007. A special NDA procedure, known as a ‘‘section 505(b)(2) application’’ or a ‘‘paper NDA,’’ allows an applicant to seek approval on the basis of a combination of a prior approval of a similar product or published literature, and some new clinical studies conducted or sponsored by the applicant. Section 505(b)(2) applications are often used for changes in a drug that require clinical investigations and thus cannot be handled through the generic drug process, such as a new indication or change in dosage.

Compounded diltiazem (prepared by the pharmacist, for each patient, using a general cream base and diltiazem from oral formulations) is currently listed in the U.S. and E.U. anal fissure treatment guidelines as a preferred agent prior to attempting surgery. According to advice we have received from members of our scientific advisory board, who are experts in gastroenterology and gastrointestinal surgery, compounded diltiazem is utilized by many colorectal and gastroenterology specialists each year for the treatment of anal fissures and, according to these experts, has also reduced the number of surgeries required. As a result, awareness and utilization of diltiazem as an effective treatment for anal fissures is high among physicians that treat this disorder. However, compounded diltiazem for anal fissure is not an FDA-approved use nor is it an FDA-approved product, and as such, the cost is not reimbursed by Medicare or health insurance plans. Data on unit and dollar volumes of compounded preparations are not routinely collected and not available to us. We expect to capture immediate market share if VEN 307 is approved due to its known efficacy and the current use of the compounded version. We expect that VEN 307 will be highly competitive with the compounded version because of the ease of prescription (already formulated, and approved by the FDA), with no need for custom mixing at the pharmacy, and because VEN 307 will be eligible for reimbursement under Medicare and other health plans, which the compounded version is not. For these reasons, we believe that the use of the compounded form of diltiazem will greatly decrease if VEN 307 is approved. The use of diltiazem for the treatment of anal fissures was first discovered at St. Mark gastroenterology teaching hospital in London. Professors Kamm and Robins filed the original method of use patent application in 1996. In 1997, diltiazem patent application and rights were assigned to S.L.A. Pharma, who filed the current patent application in 1998 (the original 1996 patent had lapsed). In 2001, North American rights were licensed to Solvay Pharmaceuticals, SA. During the time that Solvay held the rights, it improved the manufacturing processes and formulation and conducted important pharmacokinetic studies. In 2004, the new CEO of Solvay Pharmaceuticals refocused the R&D strategy on CNS and cardio-metabolic programs, discontinuing gastroenterology and women’s health projects. Consequently, in 2005, the license rights to diltiazem cream were returned to S.L.A. Pharma. From 2005 to the March 2007 licensing by Paramount BioSciences, S.L.A. Pharma focused on regulatory and manufacturing priorities, preparing diltiazem for further development.

14

In August 2007, we acquired North American rights to diltiazem from Paramount BioSciences, which previously acquired rights from S.L.A. Pharma in the United Kingdom for developing and marketing a proprietary diltiazem cream for relief of pain associated with anal fissures. We incurred a liability to Paramount BioSciences in the amount of $1,087,876, which represented the fees Paramount BioSciences had paid through August 2007 for both VEN 307 and VEN 308. Paramount BioSciences had acquired the S.L.A. rights in March 2007 and began working with Ventrus immediately to advance the development of these assets while an asset transfer agreement was finalized. S.L.A. Pharma is developing diltiazem cream for the European market and S.L.A. Pharma began a Phase III clinical trial in the E.U. in November 2010. We are financially supporting the E.U. trial and are obligated to make the following payments to S.L.A. Pharma for VEN 307 development milestones.

|

Amount Due

|

Date Due

|

Fee Description

|

||

|

$41,500

|

Monthly beginning October 1, 2010, and continuing until S.L.A. Pharma is no longer managing the development program for VEN 307.

|

Project management fees for VEN 307.

|

||

|

$600,000

|

December 31, 2010

|

Development costs for VEN 307.

|

||

|

$800,000

|

Upon the completion of enrollment into the Phase III clinical trial that S.L.A. Pharma is conducting in Europe, anticipated at the end of 2011.

|

Development costs for VEN 307.

|

||

|

Up to $400,000

|

If contingencies are met, payable monthly as invoiced by S.L.A. Pharma.

|

Development expenses for VEN 307. Contingent upon (i) receipt of a final study report from the S.L.A. Pharma Phase III VEN 307 trial in Europe (anticipated in the third quarter of 2012), and (ii) if we have raised net proceeds of at least $20.0 million from sales of securities and/or licensing of rights to our products by that time.

|

In August 2007, we concluded a pre-IND meeting with the FDA in anticipation of our IND submission for permission to initiate Phase III trials in the U.S. This meeting also afforded us an opportunity to gain agreement on the key design issues of the studies (including the one which S.L.A. Pharma is implementing) and additional information required for an approval of an NDA. We anticipate the availability of data from the S.L.A Phase III study in the second quarter of 2012 and, if the E.U. trial is successful, we plan to initiate the U.S. pivotal program by the second half of 2012, contingent on the availability of additional capital. We expect to collaborate closely with S.L.A. Pharma in order to leverage clinical data for different regulatory agencies and to rationalize manufacturing capacity.

Mechanism of action

The mechanism of action for topical diltiazem cream was demonstrated in human pharmacodynamic studies that showed an anal maximal resting pressure, or MRP, reduction of 28% that was sustained for 3−5 hours. This MRP reduction is believed to decrease the pain associated with anal fissures by normalizing internal anal sphincter pressure, which improves vascular blood supply and reduces ischemic pain.

15

Preclinical safety

Studies have been conducted in rabbits and guinea pigs to assess the topical safety of diltiazem cream. Clinicians treated rabbits in and around the anus with 2% diltiazem or placebo cream twice daily for 90 days to evaluate the chronic safety of the product. Although exterior anal tissue showed an increase in erythema, or redness of the skin, and edema, or accumulation of fluid beneath the skin, the clinicians concluded that these effects were due to the application procedure, to a possible reaction to latex gloves or to both. There were no histological findings. In this study, topical 2% diltiazem cream had no other adverse effects. Clinicians used guinea pigs to assess the potential for 2% diltiazem cream to elicit contact sensitization, or skin reaction to the application. This study did not demonstrate any sensitization potential of the diltiazem cream in guinea pigs.

Investigator-initiated clinical studies (studies sponsored by individual clinicians)

The investigator studies conducted with diltiazem cream applied topically in the perianal area in normal subjects and in patients with anal fissures are summarized in Table 1. These studies were conducted by independent investigators and not by us or any partner of ours. The year the study was published is given in the column headed ‘‘Study.’’

Table 1. Summary of Investigator-initiated clinical studies.

|

Study

|

Condition,

treatment, dosage

|

Study design,

endpoints

|

Efficacy

|

Adverse events

|

||||

|

Carapeti, E.A., et al, Gut, 45:719 – 722, 1999

|

10 normal subjects; placebo (PBO) or diltiazem (DTZ) gel (0.1%, 0.5%, 1%, 2%, 5%, and 10%)

|

DTZ or PBO gel applied once to anal margin; maximum resting anal pressure (MRP) and anodermal blood flow measured starting 1 hour after treatment

|

DTZ decreased MRP at concentrations of 1% and higher, maximum decrease of 28% at 2% gel, no further effect of 5% or 10%; effect at 2% lasted 3 – 5 hours; no change in blood flow

|

No local or systemic adverse events (AEs) reported

|

||||

|

Carapeti, E.A., et al, Dis Colon rectum, 43:1359 – 1362, 2000

|

15 patients with chronic anal fissures (CAF); 2% DTZ gel, three times-per-day (TID) for 8 weeks

|

DTZ gel applied to anal margin; MRP, anodermal blood flow and healing rate monitored every 2 weeks, daily diary cards for worst pain (scale of 0 – 10) of the day

|

Fissures healed in 67% of subjects; significant decrease in MRP and pain (decreased from 5.5 pretreatment to 1 post-treatment); no effect on blood flow

|

No AEs

|

||||

|

Bhardwaj, R., et al, Annual Meeting of British Association of Colon proctologists, Brighton, United Kingdom, 2000

|

44 patients with CAF, 2% DTZ gel, TID for 8 weeks

|

27 patients assessed at 2 months, 15 patients evaluated at 4 months (included 9 who had healed at 2 months and remained healed); assessed for healing, pain, rectal bleeding, MRP

|

Fissures healed in 56% of subjects at 2 months, 73% at 4 months; pain abolished in 88%, bleeding in 92%; MRP decreased by 24% at 2 months

|

1 patient had minor incontinence to flatus

|

||||

|

Jonas, M., et al, Dis Colon rectum, 44:1074 – 1078, 2001

|

50 patients with CAF, 24 treated with oral DTZ (60 mg), 26 with topical DTZ (2% gel), twice per day (BID) for 8 weeks

|

DTZ gel applied 1cm inside anus and to anal margin; pain, bleeding, perianal irritation (all 3 measured on a scale of 1 – 100 mm), MRP, healing monitored every 2 weeks

|

Fissures healed in 38% of subjects (oral) vs. 65% (topical) (9 in each group had previously failed on glyceryl trinitrate (GTN); 7 of these healed on topical vs. 1 on oral DTZ); both oral and topical DTZ decreased MRP; pain, bleeding and irritation reduced by both formulations (pain went from 70 to 7 after 8 weeks on oral, from 68 to 3 on topical)

|

No AEs in topical group; AEs reported in 8 patients on oral DTZ (headaches, nausea and/or vomiting, rash, decreased sense of taste and smell)

|

||||

|

Knight, J,S., et al, Br J Surg, 88:553 – 556, 2001

|

71 patients with CAF, 2% DTZ gel, BID, additional 8-12 weeks for subjects who did not heal on original regimen

|

DTZ applied perianally; healing monitored;

|

75% healed after 2-3 months, a total of 89% healed after a median duration of 9 weeks (range of 2-16 weeks); after a median of 32 weeks follow-up (range 14 – 67 weeks) 66% symptom-free, 17% had mild symptoms, and 7% had reoccurrence

|

4 patients reported perianal dermatitis, 1 reported headache

|

16

|

Study

|

Condition,

treatment, dosage

|

Study design,

endpoints

|

Efficacy

|

Adverse events

|

||||

|

Griffin, N., et al, Colorectal Dir, 4:430 – 435, 2002

|

47 patients with CAF who failed topical GTN, 2% DTZ cream, BID for 8 weeks

|

Treatment administered in anal verge; daily diary for pain, bleeding and itching (scale of 0 – 100); healing monitored

|

Fissures healed in 48% of subjects; pain and bleeding decreased after 8 weeks, no effect on itching; 2 patients relapsed after median duration of follow-up 45 weeks (range 23 – 54)

|

1 patient developed a local perianal rash; up to 25% reported increased perianal itch

|

||||

|

DasGupta, R., et al, Colorectal Dir, 4:20 – 22, 2002

|

23 patients with CAF, 2% DTZ gel, TID for up to 12 weeks

|

DTZ applied to lower half of anal canal, healing monitored

|

Fissures healed in 48% of subjects, in a median of 8 weeks (range 1 – 12 weeks); of 8 who had previously failed GTN, 6 (75%) healed; no recurrences at 3 months

|

No AEs

|

||||

|

Kocher, H.M., et al, Br J Surg, 89:413 – 417, 2002

|

60 patients with CAF, 0.2% GTN ointment (29 patients) or 2% DTZ cream (31 patients), BID for 6 – 8 weeks

|

DTZ or GTN applied to anal verge, monitored every 3 weeks for healing; pain recorded on VAS (0 – 100) scale

|

At 8 weeks fissures healed or improved in 12 and 13 patients, respectively, after GTN (86%) vs. 8 (healed) and 16 (improved) after DTZ (77%); both decreased pain to approximately same extent; at 12 weeks 2 GTN patients had recurred vs. none in the DTZ group

|

21/29 GTN subjects (72%) reported AEs vs. 13/31 (42%) in DTZ group; 17 /29 in GTN group had headaches, vs. 8/31 of DTZ patients

|

||||

|

Bielecki, K., et al, Colorectal Dir, 5:256 – 257, 2003

|

43 patients with CAF, 0.5% GTN ointment (21 patients) or 2% DTZ ointment (22 patients), BID for 8 weeks

|

Patients monitored 3 times during treatment

|

Fissures healed in 86% of GTN, 86% of subjects with DTZ, 3 failures in each group

|

Mainly headache in 7 GTN patients (33%), no AEs reported in DTZ patients

|

||||

|

Shrivastava, U.K., et al, Surg Today, 37:482 – 485, 2007

|

90 patients with CAF; 2% DTZ ointment (30 patients), 0.2% GTN ointment (30 patients), BID; no treatment (30 patients)

|

Treatments applied BID to anus, patients monitored for healing and pain (VAS) twice 2 per week then every 2 weeks

|

Fissures healed in 80%, 73% and 33% for DTZ, GTN and control subjects, respectively; mean time for healing 6.6 weeks, 7.0 weeks and 7.6 weeks for DTZ, GTN and controls, respectively; pain decreased by 75% for DTZ, 59% for GTN and 29% for controls at 6 weeks; recurrence rate 12.5%, 32% and 50% for DTZ, GTN and controls, respectively

|

No AEs in DTZ patients, 67% of GTN patients had headaches

|

DTZ = diltiazem; GTN = glyceryltrinitrate (nitroglycerin)

Clinical trials of diltiazem cream sponsored by S.L.A. Pharma

In 2004 and 2005, S.L.A. Pharma assessed the pharmacokinetic profile of topical diltiazem cream over a four-day period in subjects with anal fissure. Clinical dosing was completed in November 2005 and published in January 2007. Clinicians treated patients with eight doses of either 2%, 4%, or 8% diltiazem cream. Clinicians administered a single dose perianally on day 1, followed by doses three times a day on days 2 and 3, followed by another single dose on day 4. The clinicians collected blood over 24 hours on days 1 and 4. Maximum blood levels and area under the curve increased with the dose, and there appeared to be accumulation of diltiazem in blood on day 4 after multiple dosing. The time to maximum blood levels was five to seven hours, and the plasma half-life was less than 12 hours. However, the maximum amount of diltiazem that was absorbed was much less (at least five-fold less) than observed after oral dosing. Side effects, such as anal irritation, headache, and nausea, were mild.

Blood pressure was measured at the following times after the single dose on days 1 and 4: predose, 15, 30 and 45 minutes and 1, 1.5, 2, 4 and 8 hours after dosing. The relatively small maximum mean decreases (mmHg) in blood pressure in patients receiving 2%, 4% and 8% cream (3-4 patients per group) by day 4 ranged from 4 to 8mmHg systolic blood pressure, or SBP, and 4 to 6 mmHg diastolic blood pressure, or DBP. The changes were, in general, transient and asymptomatic and blood pressure had returned to at or near baseline by the next reading. There was no clear dose-related effect among the 2%, 4% and 8% creams with respect to decreases in blood pressure. In clinical trials with oral diltiazem for hypertension, the patients receiving placebo had mean decreases of blood pressure from 2 to 4 mmHg.

17