Attached files

| file | filename |

|---|---|

| EX-31.2 - Sino Clean Energy Inc | v216628_ex31-2.htm |

| EX-31.1 - Sino Clean Energy Inc | v216628_ex31-1.htm |

| EX-32.1 - Sino Clean Energy Inc | v216628_ex32-1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission file number: 000-51753

SINO CLEAN ENERGY INC.

(Exact name of Registrant as specified in its charter)

|

Nevada

|

75-2882833

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

Room 1605, Suite B, Zhengxin Building

No. 5 Gaoxin 1st Road, Gaoxin District

Xi’an, Shaanxi Province, PRC

|

N/A

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number: +86-29-82091099

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).* Yes o No o *The registrant has not yet been phased in to the Interactive Data requirements.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained herein, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

|

Smaller reporting company þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

As of June 30, 2010, the aggregate market value of the voting stock held by non-affiliates of the Registrant was approximately $70,394,843 based on a closing price of $6.20 per share of common stock as reported on the NASDAQ stock exchange on such date.

On March 31, 2011, we had 23,452,270 shares of common stock issued and outstanding.

TABLE OF CONTENTS

TO ANNUAL REPORT ON FORM 10-K

FOR YEAR ENDED DECEMBER 31, 2010

|

Page

|

||

|

PART I

|

1

|

|

|

ITEM 1.

|

BUSINESS

|

1

|

|

ITEM 1A.

|

RISK FACTORS

|

25

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

42

|

|

ITEM 2.

|

PROPERTIES

|

42

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

42

|

|

ITEM 4.

|

REMOVED AND RESERVED

|

22

|

|

PART II

|

42

|

|

|

ITEM 5.

|

MARKET FOR REGISTRANT'S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

|

42

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

45

|

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF OPERATION

|

45

|

|

ITEM 8.

|

FINANCIAL STATEMENTS

|

52

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURES

|

52

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

52

|

|

ITEM 9B.

|

OTHER INFORMATION

|

53

|

|

PART III

|

53

|

|

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

53

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

59

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

64

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

66

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

68

|

|

ITEM 15.

|

EXHIBITS

|

69

|

|

SIGNATURES

|

71

|

i

CAUTION REGARDING FORWARD-LOOKING INFORMATION

This report contains forward-looking statements. All forward-looking statements are inherently uncertain as they are based on current expectations and assumptions concerning future events or future performance of the Company. Readers are cautioned not to place undue reliance on these forward-looking statements, which are only predictions and speak only as of the date hereof. Forward-looking statements usually contain the words “estimate,” “anticipate,” “believe,” “expect,” or similar expressions, and are subject to numerous known and unknown risks and uncertainties. In evaluating such statements, prospective investors should carefully review various risks and uncertainties identified in this Report, including the matters set forth under the captions “Risk Factors” and in the Company’s other SEC filings. These risks and uncertainties could cause the Company’s actual results to differ materially from those indicated in the forward-looking statements.

Although forward-looking statements in this annual report on Form 10-K reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties, and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the heading “Risks Relating to Our Business” below, as well as those discussed elsewhere in this annual report on Form 10-K. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this annual report on Form 10-K. We file reports with the Securities and Exchange Commission (“SEC”). You can read and copy any materials we file with the SEC at the SEC’s Public Reference Room, 100 F. Street, NE, Washington, D.C. 20549 on official business days during the hours of 10 a.m. to 3 p.m. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including the Company.

We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this annual report on Form 10-K. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this annual report, which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

PART I

ITEM 1. BUSINESS

BUSINESS

Company Overview

We are a leading producer of clean coal heating and energy solutions for residential, commercial and industrial uses in China. We produce and distribute coal water slurry fuel ("CWSF"), which is a liquid fuel that consists of fine coal particles suspended in water, mixed with chemical additives, and is primarily used to fuel boilers and furnaces to generate steam and heat for both residential / commercial heating and industrial applications. CWSF is an economic and environmentally friendly alternative to oil and natural gas and provides many benefits over coal briquettes, including increased burn-off rates, improved thermal efficiency, and reduced emissions. We believe that the combination of China's heavy reliance on coal for heat and energy, its extensive coal reserves, and increased government attention to clean coal technologies, make CWSF an ideal alternative for cleaner heat and energy production in China.

China's economic growth over the last four decades has led to a rapid increase in energy demand. According to Frost & Sullivan, China accounted for 17.7% of global primary energy demand in 2008 and will overtake the United States as the world's largest consumer of energy in 2011. China is the largest producer and consumer of coal in the world, making it much more reliant on coal than other developed nations, as it is used extensively not only for power generation, but also for industrial applications and residential heating. Coal is the most widely used energy source in China for heating and electric power generation due to its abundance, broad geographic distribution, and mature power conversion infrastructure. According to the National Bureau of Statistics of China, coal is expected to be used for approximately 67% of total energy consumption in China in 2010 and represents more than 90% of estimated domestic fossil fuel reserves. Although significant progress has been made by Chinese central and provincial governments to utilize alternative sources of energy such as hydro, nuclear, solar and wind power, significant obstacles remain in establishing alternative energy to satisfy a significant portion of China's energy requirements primarily due to their relatively prohibitive capital costs, especially in light of the well established coal power conversion infrastructure that is already in place in China. According to Frost & Sullivan, overall CWSF demand in China is expected to grow at a compounded annual growth rate ("CAGR") of 24.7% from 2008 to 2014.

Our business was originally established in August 2002 to focus on the production and distribution of copolymer resin products. In 2004, we identified an attractive opportunity to enter the CWSF market due to the strong government push for clean coal technologies and the resulting market demand for more efficient and cleaner uses of coal. In April 2006, we decided to focus solely on the research, development, production, marketing and sale of CWSF and accordingly phased out our copolymer resin business in January 2007. We obtained our first sales contracts for CWSF in early 2007, completed the installation of our first 100,000 metric ton CWSF production line in June 2007, and commenced mass production and distribution of CWSF in July 2007. We have grown substantially in recent years by adding production capacity at existing and new locations, and are currently fully utilizing our in-place annual production capacity of 850,000 metric tons of CWSF.

We primarily use washed coal to produce CWSF, which we procure from local coal mines. We have established strong relationships with our suppliers and our ability to purchase large quantities of raw materials has allowed us to achieve favorable pricing and delivery terms. We sell our CWSF exclusively in China to residential complex development management companies, commercial businesses, industrial users, and government organizations that use CWSF predominantly for residential/commercial heating and industrial applications. Our customers adopt CWSF as a substitute for oil, natural gas and coal briquettes in their furnaces or boilers. We typically enter into three to five year framework agreements with our customers that provide guidance on CWSF sales volumes and prices. We have framework agreements in place with approximately 90% of our customers. Based on our experience, the CWSF consumption volume of any given boiler does not change materially from year to year. Once established, the customer base for CWSF is very stable, as consumption patterns are highly predictable, and the cost to switch CWSF boilers to other fuels is prohibitively expensive. Our strong reputation in the CWSF industry in China, together with our established track record for consistently delivering high quality products in large quantities, has enabled us to expand our customer base over time. As of December 31, 2010, we were servicing a total of 43 customers in Shaanxi and Liaoning Provinces.

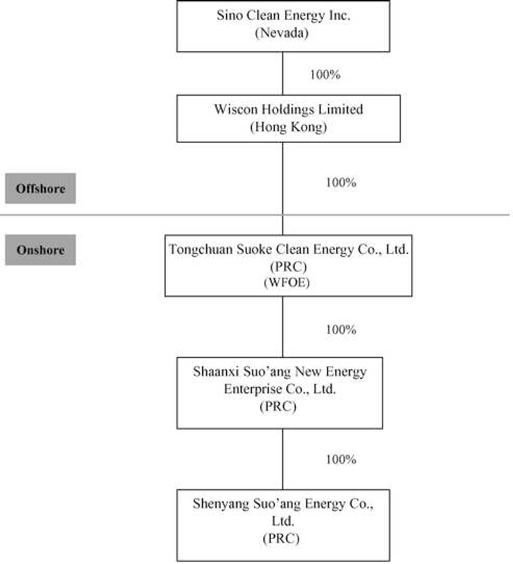

Corporate History and Structure

Our current corporate structure is the result of a number of complex corporate restructurings through which we acquired control of our CWSF business in the PRC. We entered into this series of corporate restructurings in part because certain rules and regulations in the PRC restrict the ability of non-PRC companies that are controlled by PRC residents to acquire PRC companies.

On October 20, 2006, we acquired control of Hangson Limited, a British Virgin Islands company ("Hangson") pursuant to a Share Exchange Agreement, dated October 18, 2006 (the "Exchange Agreement"). Hangson was a holding company that controlled Shaanxi Suo'ang Biological Science & Technology Co., Ltd., a PRC company ("Suo'ang BST") and Suo'ang BST's 80%-owned subsidiary at the time, Suo'ang New Energy, through a series of contractual arrangements. Sou'ang BST, through Suo'ang New Energy, commenced CWSF production in July 2007.

As part of a process to ultimately directly control 100% ownership of Suo'ang New Energy, we began to reorganize our corporate structure in June 2009. In June 2009, we acquired 100% of Wiscon, which established Suoke Clean Energy, the Company's wholly foreign owned enterprise, in Tongchuan, Shaanxi Province. We subsequently entered into a series of agreements transferring all of the rights and obligations of Hangson under the contractual arrangements with Suo'ang BST to Suoke Clean Energy.

2

On November 12, 2009, Suo'ang New Energy received a new business license from the Tongchuan Administration for Industry and Commerce, which reflected that the acquisition of 100% of the equity of Suo'ang New Energy by Suoke Clean Energy had been completed. As a result, our CWSF business is now conducted primarily through Suo'ang New Energy, which is a 100% wholly owned subsidiary of Suoke Clean Energy, under applicable PRC laws and we are now able to directly control Suo'ang New Energy through our 100% ownership of Suoke Clean Energy. On May 14, 2010, Suoke Clean Energy's acquisition of Suo'ang New Energy was recorded with the Tongchuan Bureau of Commerce.

On October 12, 2009, Suo'ang New Energy established a wholly-owned subsidiary, Shenyang Energy, to conduct business in Shenyang, Liaoning Province.

On December 31, 2009, Suoke Clean Energy terminated all of its contractual arrangements with Suo'ang BST. In connection with this termination, certain assets held by Suo'ang BST, such as office equipment, vehicles, bank deposits and accounts receivable, were transferred to Suoke Clean Energy. Employees of Suo'ang BST signed new employment contracts with Suoke Clean Energy and rights and obligations under certain remaining business operation agreements, and research and development contracts between Suo'ang BST and third parties, were assigned to Suo'ang New Energy. Hangson transferred all of its equity interests in Wiscon to us.

Although the equity transfers in the PRC described above were approved by local governmental agencies, they were not approved by the PRC Ministry of Commerce ("MOFCOM") or the China Securities and Regulatory Commission (the "CSRC"). For a discussion of the risks and uncertainties arising from these PRC rules and regulations, see "Risk Factors—The failure to comply with PRC regulations relating to mergers and acquisitions of domestic enterprises by offshore special purpose vehicles may subject us to severe fines or penalties, and create other regulatory uncertainties regarding our corporate structure." For a more detailed description of our corporate history and structure, see "Management's Discussion and Analysis of Financial Condition and Results of Operation—Corporate Organization and History."

3

The following chart shows our current corporate structure:

Company Strengths

Exclusive focus on CWSF, which has significant advantages over coal briquettes and other traditional fossil fuels

CWSF has several advantages over coal briquettes and other traditional fossil fuels, including:

• it is more energy efficient;

• it creates significantly less pollution;

• it is a cheaper source of energy;

• it is cleaner to transport and store; and

4

• it is safer to handle.

Compared to coal briquettes, CWSF has a higher burn-off rate (the percentage of combustible mass in a given unit of solid fuel mass) and thermal efficiency (the percentage of useful work in the output of total energy), which reduces carbon discharge and increases the utilization of the coal input. According to Frost & Sullivan, CWSF emits 80% less sulfur dioxide than coal briquettes and 49% less sulfur dioxide than oil. Depending on the geographic area, we believe CWSF may be approximately 50% cheaper than oil and approximately 30% cheaper than natural gas on a per-unit-of-energy basis. Compared to coal briquettes, CWSF is cleaner to transport and store, as it can be transmitted by tank trucks and through pipelines and can be stored for up to one year. CWSF is safer to handle than other traditional fossil fuels, as CWSF's relatively high burning point of over 800 degrees Celsius makes it more resistant to explosion.

The CWSF industry has strong government support and is growing rapidly

In China's 2010 Report on Central and Local Budgets, the Chinese government states that it has budgeted approximately US$12 billion for energy conservation and pollution reduction and to promote the development of low-carbon technologies. Since China began pursuing the development of CWSF technology in the 1980's, demand for CWSF has increased, logistics costs have been reduced, and suppliers have implemented better quality controls to ensure a more consistent product. According to Frost & Sullivan, in 2008, China's annual CWSF demand was 15.9 million metric tons, and CWSF was being used in 700 industrial furnaces and in hundreds of industrial kilns as a replacement for oil, natural gas and coal briquettes. According to Zhongjing Zongheng Economy Research, there are approximately 600,000 traditional fossil fuel burning industrial boilers and kilns currently installed in China, with approximately 100,000 requiring replacement or major repairs each year. We believe there is significant opportunity for the CWSF industry to fill the void left by older coal briquette burning boilers that are being phased out by legislation and obsolescence. According to Frost & Sullivan, overall CWSF demand is expected to grow at a CAGR of 24.7% from 2008 to 2014. Furthermore, we believe that a significant opportunity exists for third-party CWSF producers, which are expected to increase their market share from 13% in 2008 to 24% in 2011.

Dominant market position with a proven product and technology that is in full scale commercial production

Having commenced operations in 2006, we have established a first mover advantage as one of the first commercial CWSF producers in China and, to our knowledge, the only pure-play publicly listed CWSF producer in the world. We obtained our first sales contracts for CWSF in early 2007, completed the installation of our first CWSF production line in June 2007, and commenced mass production and distribution of CWSF in July 2007. We believe that there are currently 40 to 50 active CWSF suppliers in China, however, most are much smaller than us, with third party sales volumes of less than 100,000 metric tons. We are the largest third-party CWSF producer in China as measured by third party sales volume for 2010, and we currently have in-place CWSF production capacity of 850,000 metric tons. Third party CWSF producers do not include entities that produce CWSF in-house for their own consumption or parties that import CWSF for sale. We aim to increase our annual production capacity to 1,850,000 metric tons through the expansion of production capacity at existing facilities and the development of new facilities throughout China. For the year ended December 31, 2010, we had revenue and income from operations of approximately US$106 million and US$35 million, respectively.

Exclusive Agreements with Select Strategic Partners

We have agreements in place with strategic partners who we believe are highly complementary to our CWSF production business. We had a sales agency agreement with Qingdao Haizhong Enterprise Co., Ltd. ("Haizhong Boiler"), a CWSF boiler manufacturer with an estimated 78% share of the Chinese CWSF boiler market (according to Beijing Zhongjing Zhongheng Information and Consulting Center, Haizhong Boiler's market share was determined on December 30, 2009, whereby we acted as the exclusive distributor for Haizhong Boiler's CWSF boilers in Shaanxi Province. This agreement expired according to its terms in February 2011. Following the success of the sales agency agreement in Shaanxi Province, we entered into an exclusive nationwide strategic partnership agreement with Haizhong Boiler pursuant to which Haizhong Boiler focuses on selling CWSF boilers and in some markets operating heat supply plants, while we focus on supplying the requisite CWSF. We have an exclusive agreement with Shenyang Haizhong Heat Resource Co., Ltd, an unrelated third-party municipal heat supplier, to supply CWSF for residential and commercial heating in Shenyang. The current amount of CWSF required is approximately 300,000 metric tons and is estimated to increase to 850,000 metric tons by the end of 2012. We also have an agreement with Tongchuan City Investment and Development Co., Ltd. to develop a new heat supply company for the purpose of providing heating for the new district of Tongchuan. It is expected that 15 heat supply plants will need to be built and the requisite CWSF will be supplied by us. Suo'ang New Energy is expected to retain a 15% stake in the Tongchuan heat supply company.

5

Established relationships with customers and suppliers which provide visibility on long term cash flows

Since obtaining our first sales contracts for CWSF in January 2007, we have expanded our customer base to a point where we were serving a total of 43 customers as of December 31, 2010. We have developed a strong reputation in the CWSF industry in China, which, together with our established track record for consistently delivering high quality products in large quantities, has enabled us to maintain and expand our customer base. As the only CWSF producer in Shaanxi Province, we are greatly insulated from the risk of customer attrition to competing suppliers in that area. Since commencing commercial operations in 2007, we have achieved a 100% customer retention rate. Our customers include residential developers, commercial customers, industrial customers, and government organizations that use CWSF primarily for industrial uses and residential/commercial heating applications as a substitute for oil, natural gas or coal briquettes. We have entered into long term framework agreements with approximately 90% of our customers, which set out guidance on quantities and prices for CWSF, typically with a term of three to five years. We have established strong relationships with our suppliers, and our ability to purchase large quantities of raw materials has allowed us to achieve favorable pricing and delivery terms.

Experienced management team with a proven track record

We have a well seasoned and experienced senior management team with significant CWSF industry experience that we believe will enable us to execute on our expansion strategy. Our CEO, Mr. Baowen Ren, is a prominent figure in China's CWSF industry with over seven years' experience in CWSF research, development and sales. As a member of the China CWSF Research Center, the China Association of Environmental Protection Industry, and the China Association of Low-Carbon Economy, Mr. Ren is very familiar with China's clean energy policies, regulations, and directions, and the role that CWSF plays within China's clean coal technology plan. Since 2005, Mr. Ren has built the largest CWSF production base in northwest China. In 2008, Mr. Ren issued the paper "The Development of CWSF under the Movement of National Energy Conservation and Emission Reduction", which was adopted by the National CWSF Promotion Work Conference Paper Collection. Mr. Ren has received numerous accolades and acknowledgements for his achievements and success, including a designation as "Shaanxi Top 100 Entrepreneur". Mr. Peng Zhou, the chief operating officer of Shenyang Energy, brings strong operational expertise in CWSF industry. He is an expert in coal resources in west China, and has substantial knowledge of CWSF technologies and markets in China. He has managed operations in multiple industries for more than 10 years. His expertise and dedication to CWSF has significantly contributed to our strong growth. Our CFO, Ms. Wendy Fu brings more than twenty years of professional financial and accounting experience with public companies and accounting firms, including former roles as the CFO of China Shenghuo Pharmaceutical Holdings Inc. (AMEX: KUN), Vice President of Finance at Shengdatech, Inc. (Nasdaq: SDTH) and Assistant Finance Controller at Wal-Mart China.

Growth Strategy

Our objective is to be the leading supplier of CWSF in China. Key elements of our growth strategy include:

Pursue organic growth in existing markets

At the beginning of 2009, we had in-place CWSF production capacity of 350,000 metric tons, 100% of which was from our Tongchuan facility. In October 2009, we brought our 300,000 metric ton per annum Shenyang facility on-line, bringing aggregate annual in-place production capacity to 650,000 metric tons. Having added an additional 200,000 metric tons of capacity at our Tongchuan facility in January 2010, our run-rate production capacity increased to 850,000 metric tons per annum. For the year ended December 31, 2010, we sold approximately 982,167 metric tons of CWSF, representing substantially all of our production in that year. We believe that there is significant organic growth potential embedded within our current operations as we continue to bring new production capacity on-line in both of our existing markets. Our sales and marketing team consists of 12 in-house personnel which sell our CWSF to customers located mainly within a radius of 200 kilometers of our production facilities. We plan to further expand our customer base and market share by increasing our sales and service personnel.

6

Leverage strategic partnership with Haizhong Boller

In order to increase the adoption of CWSF technology, we have established collaborative market development programs with Haizhong Boiler, which is China’s largest CWSF boiler and furnace equipment manufacturer, which we believe will give us the ability to effectively market our CWSF products to prospective customers. We entered into an exclusive nationwide strategic partnership agreement with Haizhong Boiler pursuant to which Haizhong Boiler focuses on selling CWSF boilers, and in some markets operating heat supply plants, while we focus on supplying the requisite CWSF.

Capitalize on strong government support for CWSF

As China's economy continues to grow at a rapid pace, the demand for energy will continue to increase, placing further strain on China's energy infrastructure. Increasing urbanization rates and improved living standards are expected to increase the consumption of energy as the demand for residential heating continues to rise. Coal is the largest fuel source for heating and electric power generation in China, comprising approximately 67% of overall energy production. As China has low-cost, abundant and geographically distributed coal reserves and a mature coal-to-energy conversion infrastructure, it is expected that coal will continue to be one of the most important sources of energy for China in the foreseeable future and as a result, we believe that any solution to China's pollution problems must include clean coal technologies, such as CWSF. We believe that China's increased focus on the environment and its extensive coal reserves make CWSF an attractive alternative for cleaner energy production, which would drive demand for CWSF products over time. CWSF has been listed as a key scientific and technological project in each of China's Five-Year Plans since 1981, and in several other major sustainable development policy initiatives. Many provinces and cities across China have adopted specific and quantifiable targets, plans, policies and incentives to promote the usage of CWSF, including financial subsidies to CWSF consumers relating to boiler installations and incentives for attaining threshold levels of CWSF consumption. We have entered into an agreement with the Tongchuan municipal government to develop a network of 15 new residential heat supply plants over the next five to seven years that utilize our CWSF as a fuel source.

Grow through expansion and acquisitions in other regional markets

We plan to increase our CWSF production capacity through the construction of new facilities and the acquisition of existing CWSF production facilities in new geographic regions. Our geographic expansion plans will initially focus on Nanning, Guangxi Province and Guangdong Province. In addition, we plan to expand the production capacity at our current location in Shenyang, Liaoning Province. We expect that such growth initiatives will increase our aggregate annual CWSF production capacity to 1,850,000 metric tons.

Coal-Water Slurry Fuel

CWSF is a fuel that consists of fine coal particles suspended in water, mixed with chemical additives. By mass, CWSF is typically comprised of 70% fine dispersed coal particles, 29% water and 1% chemical additives. The presence of water in CWSF reduces harmful emissions into the atmosphere during the combustion process, as CWSF's water content can be turned into water vapor, which decreases the temperature within the boiler, thereby inhibiting the production of oxynitride. CWSF is burned in a liquid state within a boiler which is specifically designed for the combustion of CWSF. When burned, CWSF is pumped from a storage chamber into a duct which carries the fuel to an atomizer. The atomizer injects a fine spray into the combustion chamber in a manner similar to that used in oil boilers. This method of injection increases the burn-off rate and thermal efficiency of CWSF, making it much more efficient than traditional coal briquettes.

7

Coal particles in CWSF typically have a size of less than 200 to 300 microns and can be used in several different applications. Smaller-particle CWSF is more versatile in a broader range of potential applications, however, smaller CWSF is more difficult to manufacture. CWSF particles as small as 20 microns have been demonstrated to be viable substitutes for oil and natural gas in power plants. In the largest particle form, CWSF is a viable substitute for oils used to produce steam in boilers. At 80 microns or less, CWSF can be used as a co-fuel or substitute fuel in diesel engines. Currently, we are capable of producing CWSF with a particle size that is as fine as 20 to 30 microns. Although smaller particle CWSF has a broader range of applications, there is currently no significant price difference compared to larger particle CWSF.

CWSF can be stored for up to a year. By converting the coal into a liquid form, the delivery and dispensation of the fuel can be simplified. It is stored in tanks and can be transported by tank trucks and pipes similar to oil or natural gas, which is an advantage over coal briquettes. Furthermore, CWSF's water content increases its burning point which makes it safer to store and cleaner to transport than coal briquettes.

Benefits of CWSF

As CWSF's primary raw material is coal, it is a very competitive alternative to oil and natural gas on a per unit of energy basis, primarily because of the relatively low cost of coal in China. Depending on the geographic area, CWSF may be approximately 50% cheaper than oil and approximately 30% cheaper than natural gas on a per unit of energy basis. According to Frost & Sullivan, in 2009, the cost for oil in China was RMB 426 per billion calories and the price of natural gas was RMB 312 per billion calories, whereas the cost of CWSF was RMB 211 per billion calories. Due to China's ongoing support for research and development of CWSF and its abundant coal resources, CWSF is expected to maintain a price advantage over oil and natural gas.

Compared to coal briquettes, CWSF is significantly less harmful to the environment. CWSF has a higher burn-off rate and thermal efficiency than coal briquettes, thereby increasing the utilization of the input coal, which reduces sulfur dioxide, nitrogen oxide and soot. Sulfur dioxide is predominately captured by CWSF boilers and furnaces during the combustion process. Based on data from Frost & Sullivan, the use of CWSF reduces sulfur dioxide emissions by over 80% compared to burning coal briquettes and 49% compared to burning oil while generating the same amount of energy. As China's environmental regulations become more stringent, CWSF is expected to gradually replace coal briquettes in many industrial applications. The following charts illustrate the differences between coal briquettes, oil, natural gas and CWSF on an efficiency and emissions basis.

Fuel Performance Comparison

|

Coal Briquette

|

Oil

|

Natural Gas

|

CWSF

|

||||||||||||||

|

Operating assumptions

|

|||||||||||||||||

|

Energy per unit (kcal/t)

|

6.5 | M | 10.0 | M | 9,000/m | 3 | 4.5 | M | |||||||||

|

Burn-off rate

|

65 | % | 99 | % | 99 | % | 98 | % | |||||||||

|

Thermal efficiency

|

65 | % | 90 | % | 90 | % | 86 | % | |||||||||

|

Energy generated (kcal/t)

|

2,746,250 | 8,910,000 |

8,019 per m

|

3

|

3,792,600 | ||||||||||||

|

Economics

|

|||||||||||||||||

|

Market price of fuel (RMB/t)

|

680 | 3,800 |

2.5 (RMB/m

|

3)

|

800 | ||||||||||||

|

End user cost (RMB/Bcal)

|

248 | 426 | 312 | 211 | |||||||||||||

|

Emissions

|

|||||||||||||||||

|

SO2

|

Emissions (kg)

|

20.00 | 26.00 | 0.00 | 5.60 | ||||||||||||

|

Emission Index*

|

7.28 | 2.92 | 0.00 | 1.48 | |||||||||||||

|

NOx

|

Emissions (kg)

|

7.64 | 2.31 | 0.27 | n/a | ||||||||||||

|

Emission Index*

|

2.78 | 0.26 | 0.03 | n/a | |||||||||||||

|

Soot

|

Emissions (kg)

|

68.53 | — | — | 48.00 | ||||||||||||

|

Emission Index*

|

24.95 | — | — | 12.66 | |||||||||||||

*

"Emission Index" is "Emissions" / "Energy generated". Source Frost & Sullivan

8

CWSF is burned in boilers that are specially designed for its combustion. Although it is possible to retrofit oil burning boilers to be CWSF compliant, most adopters of CWSF elect to install new CWSF boilers due to their superior operating efficiency and lower on-going maintenance costs relative to retrofitted boilers. Based on previous experience, management believes that the cost to purchase and install a new CWSF boiler ranges from approximately $150,000 to $750,000, depending on output capacity, which is approximately 15% to 20% higher than the capital costs for purchasing and installing traditional coal briquette boilers. It is typically not economical to retrofit coal briquette or natural gas burning boilers.

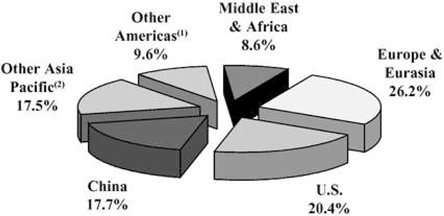

Energy and Coal

China's economic growth over the past four decades has led to a rapid increase in energy demand. According to Frost & Sullivan, China accounted for 17.7% of global energy consumption in 2008, and is expected to overtake the United States as the world's largest energy consumer in 2011.

Energy Consumption by Region (Global), 2008

Source: Frost & Sullivan, BP Statistical Review of World Energy (June 2009)

(1)

Other Americas include Canada, Mexico, Argentina, Brazil, Chile, Colombia, Peru, Venezuela, and so on.

(2)

Other Asia Pacific include Australia, Bangladesh, China Hong Kong, China Taiwan, India, Indonesia, Japan, Malaysia, New Zealand, and so on.

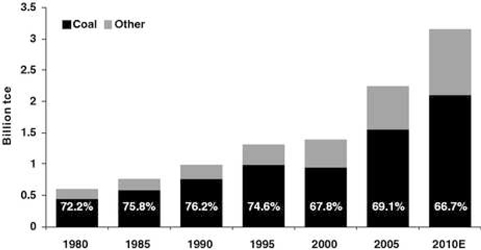

Globally, coal accounted for approximately 29% of total energy consumption in 2008. China is the largest producer and consumer of coal in the world, as it uses coal extensively not only for power generation, but also for industrial applications and residential heating. According to the BP Statistical Review of World Energy, China has become the world's largest emitter of carbon dioxide. Coal is the most widely used energy source in China for heating and electric power generation due to its abundance, broad geographic distribution, mature power conversion infrastructure, and low and stable delivery cost. In 2010, coal was expected to account for approximately 67% of overall energy consumption in China.

9

Energy Structure Forecasts (China), 1980 – 2010E

Source: Natural Bureau of Statistics of China, Frost & Sullivan

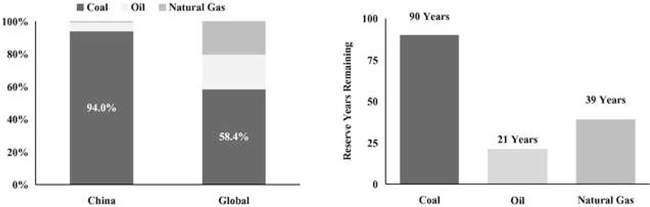

China has abundant deposits of coal. With proven coal reserves estimated at 114.5 billion metric tons, coal comprises 94.0% of China's proven fossil fuel reserves, while oil and natural gas represent only 5.4% and 0.6%, respectively. Assuming China's fossil fuel reserves continue to be extracted at current rates, China's coal reserves are likely to last another 90 years, whereas oil is expected to be depleted in only 21 years and natural gas in 39 years.

China's Proven Fossil Fuel Reserves, 2008

Source: Frost & Sullivan

10

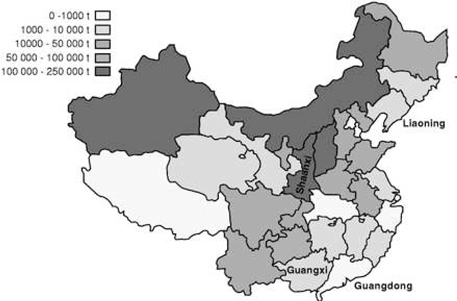

Map of China's Coal Resources

Source: Barlow and Jonker (2001)

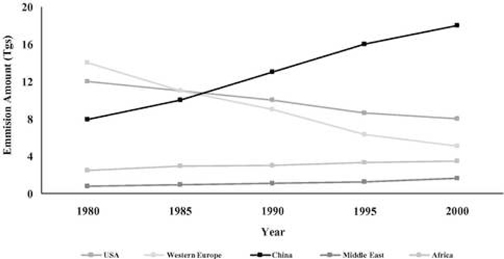

China's existing energy infrastructure is a major source of the country's pollution and may hinder the country's future economic growth as the increased reliance on coal continues to negatively impact the environment and public health. Pollutants created from the production, transportation and combustion of coal include sulphur dioxide, nitrogen oxide, soot, dust and ash. The World Bank estimates that around 400,000 people in China die each year from pollution-related illnesses. Sulfur dioxide has resulted in acid rain falling on more than 30% of China's total land, ruining croplands, threatening food chains and water systems, and leading to other negative environmental impacts. Climate change has already produced visible adverse effects on China's air quality, agriculture, livestock, forests, fresh water resources and coastal regions.

Total Sulfur Dioxide Emissions by Country (1980 – 2000)

Source: Frost & Sullivan

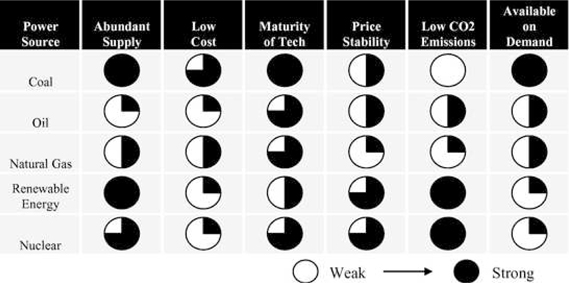

Alternative Energy and Clean Coal Technologies

Although alternative energies such as hydro, solar and wind power have begun to gain traction as increasingly important components of China's energy infrastructure, they are not expected to replace coal as China's core source of energy. Compared to coal, alternative energy sources generally have longer lead times, higher capital costs, and lower returns on investment relative to coal. Coal is expected to remain an attractive and important component of China's energy infrastructure due to its relative abundance, broad geographic distribution, mature power conversion infrastructure and low and stable delivery cost.

11

Comparative Assessment of Different Power Sources

Source: Frost & Sullivan

Developing and utilizing clean coal technology in order to overcome the lower energy efficiency and higher pollution properties of coal briquettes is essential to China's social and economic development. China has stressed the importance of the development of clean coal technology and established the Clean Coal Technology Plan ("CCTP") in 1997, with the objective of improving coal consumption efficiency and reducing environmental pollution. China's CCTP includes four major areas: (i) coal processing (which includes CWSF), (ii) high-efficiency clean combustion of coal, (iii) coal transformation, and (iv) pollution emission control and the disposal of waste materials. China budgeted approximately US$12 billion in 2010 for energy conservation and pollution reduction. The following table outlines the framework of China's CCTP, which includes 14 major technologies, including CWSF:

|

Coal Processing

|

High Efficiency Clean

Combustion and Power

Generation

|

Coal Transformation

|

Pollution Emission Control

and Waste Disposal

|

|||

|

• Coal Preparation

• Briquettes

• Coal Blending

• Coal Water Slurry Fuel

|

• Advanced Burners

• Fluid Bed Combustion (FBC)

• Integrated Gasification Combined Cycle (IGCC)

|

• Coal Gasification

• Coal Liquefaction

• Fuel Cells

|

• Flue Gas Cleaning (Desulfuration and Denitration)

• Development and Utilization of Coal-Bed Methane

• Comprehensive Utilization of Coal Gangue, Fly Ash and Coal Slurry

• Industrial Boilers and Furnace

|

Source: Frost & Sullivan

12

CWSF Market Development

CWSF originated in the Soviet Union in the 1950's, where experiments were conducted to develop new ways of utilizing coal sludges for power generation. The United States conducted further research into CWSF during the 1973 oil crisis, as it searched for alternatives to crude oil. China started pursuing the development of CWSF technology in the 1980s after CWSF had successfully been developed by the Bayi Coal Mine. After developing local CWSF production capabilities, China's central government set out to promote the increased use of CWSF, where it was used on a trial basis in key national projects and plants and was listed in several key national policy initiatives, including the "Current Catalogue of Key Industries, Products, and Technologies to be Encouraged" from 1991 to 1995. China's "9th Five Year Plan (1996 – 2000)" set out a research scope for CWSF and a demonstrative 220 t/h CWSF furnace was built to replace oil burning boilers in power plants. CWSF's prominence was enhanced in China's "10th Five Year Plan (2001 – 2005)", where the central government released a stand-alone report entitled "2010 Outline for Development of CWSF in China." Following the successful promotion of CWSF, the government has now moved on to encourage its wider application, and has been working with provincial and municipal governments to create local policies and incentives to encourage the use of CWSF. By 2008, China was leading the world in the technological development, production and consumption of CWSF. China's commitment to CWSF has allowed it to overcome issues such as cost (transportation and specialty CWSF furnaces), product quality and a customer base that initially inhibited commercial production.

Furthermore, demand has increased as a result of government subsidies that are being provided to encourage the installation of CWSF boilers and the usage of CWSF as a fuel, and suppliers have implemented better quality controls to ensure a more consistent product.

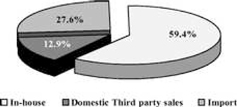

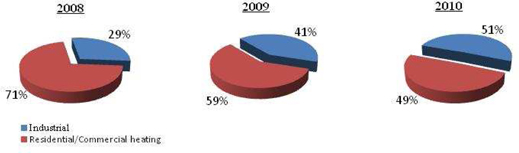

According to Frost & Sullivan, approximately 13% of CWSF demand was fulfilled by domestic third-party producers in 2008, which is expected to grow to approximately 24% by 2011. Third-party sales are provided by dedicated producers that supply energy producers with CWSF. Given that the in-house market is not externally focused, we expect that increased demand for CWSF will be met through thirty-party sales by dedicated producers such as us. The following charts indicate the breakdown of CWSF by source of supply in 2008 and 2011 respectively. In-house production consists primarily of state-owned coal manufacturers and/or electricity generators that produce CWSF for their own use.

|

CWSF Market: Breakdown by Source of Supply

(China), 2008

|

CWSF Market: Breakdown by Source of Supply

(China), 2011E

|

|

|

|

Source: Frost & Sullivan

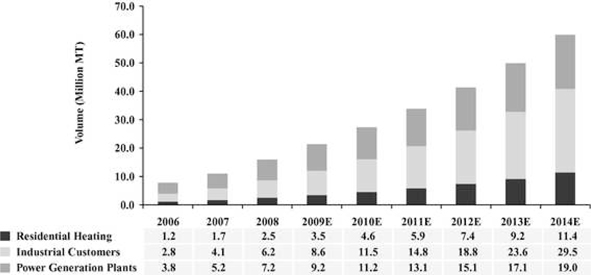

The market demand for CWSF in China in 2008 was 15.9 million metric tons. CWSF is used in 700 industrial furnaces and in hundreds of industrial kilns as a replacement for oil, natural gas and coal briquettes. According to Beijing Zhongjing Zongheng Information and Consulting Center, there are approximately 600,000 traditional fossil fuel burning industrial boilers and kilns currently installed in China, with approximately 100,000 requiring replacement or major repairs each year. According to Frost & Sullivan, overall CWSF demand is expected to grow at a CAGR of 24.7% from 2008 to 2014.

13

CWSF Market: Total Demand Breakdown (China), 2006 – 2014E

Source: Frost & Sullivan

Government policy mandates for the use of clean coal, and financial subsidies from central, provincial and municipal governments are expected to continue to drive demand for CWSF in the residential heating market, as well as for industrial applications in the metallurgy, ceramics and chemical industries. CWSF is an evolving technology, and future developments are expected to broaden the applications of CWSF, further expanding the size of the market. CWSF has been listed as a key scientific and technological project in each of China's Five-Year Plans since 1981, and in several other major sustainable development policy initiatives. Many provinces and cities across China have adopted specific and quantifiable targets, policies and regulations to promote the usage of CWSF, including financial subsidies to CWSF consumers relating to boiler installations and incentives for attaining threshold levels of CWSF consumption.

Local Chinese Government CWSF Policies and Incentives

|

Region

|

Policies and Plans

|

Incentives

|

||||||

|

Tongchuan, Shaanxi

|

•

|

Environmental-protection departments are required to strengthen comprehensive CWSF policies to save energy, reduce emissions and

|

•

|

2008 – 2012: Government allocated RMB 3.0 million each year as a subsidy for promoting CWSF boilers

|

||||

|

promote the application of CWSF and other new clean energies

|

•

|

Newly-built CWSF boilers: 10.0% of the total investment

|

||||||

|

•

|

Upgrading coal boilers to

|

|||||||

|

•

|

Convert all coal heating boilers to CWSF boilers or other clean energy sources by 2012

|

CWSF boilers: subsidizing 20.0% of the total investment

|

||||||

|

•

|

Starting in 2008, all new

|

• |

Upgrading oil boilers to CWSF boilers: RMB 100,000 subsidy

|

|||||

|

heating facilities must use CWSF or other clean energy sources

|

•

|

Centralized heat supply using CWSF: RMB 300,000 to RMB 500,000 subsidy

|

||||||

|

•

|

Develop 20 central heating stations using CWSF

|

depending on scale

|

||||||

14

|

Region

|

Policies and Plans

|

Incentives

|

||||||

|

Shenyang, Liaoning

|

•

|

Planned to build 56 CWSF

|

•

|

Favorable loan terms

|

||||

|

boilers from 2000 – 2003

|

•

|

Selected tax exemptions

|

||||||

|

Nanning, Guangxi

|

•

|

CWSF production of 1.5 million metric tons by 2010

|

•

|

2007 – 2010: Government allocated RMB 3.0 million each year as a subsidy for promoting

|

||||

|

•

|

Convert all coal-burning boilers

|

CWSF boilers

|

||||||

|

under 35mt/h to CWSF boilers or other clean energies by 2012

|

• |

Newly-built CWSF boilers: Subsidy of up to RMB 200,000 |

||||||

|

•

|

Centralized heat supply using CWSF: RMB 150,000 to RMB 500,000 subsidy depending on scale

|

|||||||

|

Dongguan, Guangdong

|

•

|

50 boiler users selected to use CWSF

|

•

|

Qualified users: one-time subsidy of 20% of the cost of equipment for upgrade, capped at RMB 1.0 million

|

||||

Source: Frost & Sullivan

Regional Market Size

We presently have CWSF production operations in the provinces of Shaanxi (at our Tongchuan facility) and Liaoning (at our Shenyang facility) and are planning to expand into the provinces of Guangxi and Guangdong. We believe the regional market size of our current and target markets to be as follows:

|

Province

|

Potential Addressable

Market Size

|

Sino Clean Energy's

In-place Capacity

|

# of Suppliers

|

|||||||||

|

(metric tons/annum)

|

(metric tons/annum)

|

(including Sino Clean Energy)

|

||||||||||

|

Shaanxi

|

5,000,000 | 550,000 | 1 | |||||||||

|

Liaoning

|

6,000,000 | 300,000 | 3 | |||||||||

|

Guangxi

|

9,000,000 | 0 | 3 | |||||||||

|

Guangdong

|

61,000,000 | 0 | 7 | |||||||||

Source: Beijing Zhongjing Zongheng Information and Consulting Center

Competition

We are the largest third-party CWSF producer in China, as measured by CWSF sales volume for the year 2010. The CWSF industry is still at an early stage in China and we have thus far experienced limited competition from domestic CWSF producers. We believe that there are currently no foreign competitors with a material presence in the CWSF industry in China. Currently there are approximately 40 to 50 active CWSF suppliers in China, although most have commercialized sales volumes of less than 100,000 metric tons. Competition is mainly based on establishing a large and stable local customer base in order to gain increased market share. CWSF producers in China compete on a localized level and often lack the capability to expand to a more regional or national scale. Establishing production capacity on a regional basis, typically within 200 kilometers of large customers, is of critical importance in the CWSF industry, as deliveries beyond this radius typically become uneconomical. The table below depicts the top five CWSF suppliers in China, as measured by third-party sales volume Q1 to Q2, 2010(i.e. excluding in-house production and consumption).

15

|

Rank

|

Supplier

|

Primary Geography

|

Domestic Third Party Sales

Volume Q1 to Q2 of 2010

(Thousand MT)

|

Market Share

|

|||||||

|

1

|

Sino Clean Energy

|

Xian, Shaanxi

|

440 | 15.9 | % | ||||||

|

2

|

Dongguan Power Fuel

|

Dongguan, Guangdong

|

383 | 13.8 | % | ||||||

|

3

|

Shandong Bayi

|

Zoazhuang, Shandong

|

220 | 7.9 | % | ||||||

|

4

|

Datong Huihai

|

Datong, Shanxi

|

125 | 4.5 | % | ||||||

|

5

|

Gansu Lvtianyuan

|

Lanzhou, Gansu

|

110 | 4.0 | % | ||||||

|

Others

|

1,491 | 53.9 | % | ||||||||

|

Total

|

2,769 | 100 | % | ||||||||

Source: Frost & Sullivan

Our Business Model

Based upon total third party sales revenue in China, we are a leading CWSF producer in China with current annual production capacity of 850,000 metric tons. We are aiming to increase our annual production capacity to approximately 1,900,000 metric tons through the expansion of our existing production facilities in Shenyang and the planned expansion into the provinces of Guangxi and Guangdong. We believe we were among the first companies in China to produce CWSF on a commercial scale, and our first-mover advantage, combined with our reputation for high quality products has allowed us to establish strong customer and supplier relationships. We believe we are well positioned to leverage our increasing scale in order to expand our customer base to meet China's growing demand for CWSF.

We launched our first CWSF plant in the city of Tongchuan, north of Xi'an, the provincial capital of Shaanxi Province in 2007. The Tongchuan plant presently has an annual production capacity of 550,000 metric tons and supplies our customers in Shaanxi Province. In October 2009, we commenced operations at our new CWSF production plant located in Shenyang, the capital of Liaoning Province in northeastern China. The Shenyang plant has an annual output capacity of 300,000 metric tons, increasing our total annual CWSF production capacity to 850,000 metric tons.

Our strong growth has been evidenced by our financial performance. Our revenue increased from $14.3 million in 2008 to $46 million in 2009 to $106 million in 2010, as a result of our success in expanding our production capacity and increasing our market penetration. During the same period, our income from operations increased from $4.4 million to $14.2 million to $34.7 million, respectively. We intend to grow our business by expanding production capacity at new and existing locations throughout China.

Raw Materials

CWSF is made from coal, water, and chemical additives. Input coal must have a grade of at least 4,500 kc/kg in order to qualify for the production of CWSF. Water does not need to be pre-processed prior to mixing with coal and depending on the source and its content, industrial waste water may be used directly in the production of CWSF. Chemical additives are used in absolving and stabilizing different qualities and sizes of coal with the water. By weight, CWSF is typically comprised of approximately 70% washed coal, 29% water and less than 1% chemical additives.

16

Sino Clean Energy – Cost of Good Sold Breakdown

for the year ended December 31, 2010

|

Input

|

% of COGS

|

|||

|

Washed coal

|

82.05 | % | ||

|

Chemical additives

|

6.27 | % | ||

|

Electricity

|

7.36 | % | ||

|

Depreciation

|

3.26 | % | ||

|

Wages

|

0.75 | % | ||

|

Water

|

0.24 | % | ||

|

Employee benefits

|

- | % | ||

|

Miscellaneous

|

0.07 | % | ||

|

Total

|

100.00 | % | ||

Coal is the primary raw material used to produce CWSF and accounted for approximately 82.05% of our cost of goods sold during the year ended December 31, 2010. We source coal from nearby coal mines for each of our production facilities. Coal is widely available in China and we maintain long-term relationships with our key suppliers, although alternative suppliers are available if necessary. Our suppliers provide us with washed coal at prevailing market prices, with volumes renegotiated each year. We determine raw material prices based on arm's-length negotiations with our suppliers shortly prior to delivery, with reference to market prices. Our reputation as a dependable counterparty enables us to obtain a stable and low-cost supply of raw material coal for our production facilities. Our long-standing supplier relationships provide us with a competitive advantage in China, and we intend to broaden these relationships to parallel our efforts to increase the scale of our production facilities, thereby maintaining a diverse supplier network while leveraging our purchasing power to obtain favorable pricing and delivery terms. Water and chemical additives are readily available and do not require supply contracts.

For 2008 and 2009 , our single largest supplier, Tongchuan Zhaojin Xinyuan Coal Mine, accounted for 85% and 87% of our total purchase of coal, respectively. In 2010, our two largest suppliers, Tiefa Coal Company and Tongchuan Mine Business, accounted for 35.9% and 31.6% of our purchase of coal, respectively. We typically pay for our coal supplies in advance, with a level of deposit that can range up to two months, as this helps to ensure that our coal requirements will be fulfilled.

The price of CWSF varies with the price of coal, and we typically have been able to increase our CWSF prices in response to increased coal prices. Our ability to adjust our selling prices has enabled us to maintain very stable gross margins, typically in the range of 30% to 40%.

Sino Clean Energy Historical Gross Margin

Source: Company reports

The demand for CWSF for residential heating tends to be seasonal in nature, with peak demand occurring between the months of October through March, as these are the peak heating periods in the markets which we currently serve. Demand for CWSF during peak periods is approximately 30% to 40% higher than during low periods. Demand for CWSF for industrial applications tends to be fairly stable throughout the year, as industrial applications are typically unrelated to heating. The price of CWSF tends to follow the price of coal, which does not necessarily follow seasonal fluctuations.

17

Processing

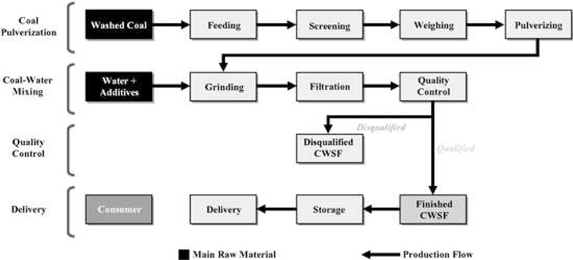

We use two methods to produce our CWSF: (i) the High Concentration Preparation with Mixed Grinding ("HCPMG," or grinding process) as illustrated below, and (ii) the Supersonic Fluid Dynamics Atomizer process ("SFDA," or atomizer process). HCPMG is the conventional CWSF production process and is comprised of four major steps: coal pulverization, water mixing, quality control and delivery. The SFDA process differs from the HCPMG process in that it uses a series of ultrasonic chambers to break coal briquettes down into smaller particle form, where it is then mixed with water to create CWSF, while the HCPMG process uses a mechanical pulverization process to mix coal briquettes and water in order to create a finely ground CWSF mixture. The SFDA process requires less electricity and is able to produce finer particle CWSF. The HCPMG production lines can produce coal particles as fine as 50 to 80 microns, while the SFDA production lines can rapidly break coal into particles as fine as 20 to 30 microns. Depending on the capacity and the type of production process, the cost to purchase and install a CWSF production line typically ranges from approximately US$10 to US$30 per metric ton, with higher capacity and more technologically advanced production lines being closer to the high end of this range. In order to reduce production costs, our plants are run primarily at nighttime when electricity costs have been approximately 1/3 of daytime rates.

High Concentration Preparation with Mixed Grinding process

Source: Frost & Sullivan

Inventory

Although coal is not subject to spoilage, we typically limit storage of coal in inventory to a maximum of two months. On average, we maintain a minimum coal reserve of approximately 5,000 metric tons in Tonghcuan and 3,000 metric tons in Shenyang. Shipments of approximately 3,600 metric tons and approximately 2,000 metric tons are typically delivered every 3 days to the Tongchuan and Shenyang locations, respectively. Production of CWSF is scheduled based substantially on customer orders, which allows us to minimize working capital requirements and to ensure that substantially no inventory is wasted or unusable. CWSF can be stored for up to one year (versus the national standard of one month), but we typically only hold the finished product in inventory for a maximum of two to three days. We currently have capacity to hold up to three days of finished product inventory on-site at each location. Storage and transportation of CWSF is very safe, as the presence of water in CWSF reduces its risk of explosion. As CWSF must be stored above freezing temperature, we use storage tanks that are specially designed to handle fluctuations in external temperatures. To date, we have shipped CWSF inventory using bulk liquid tanker trucks, however, transportation by train has been utilized by other CWSF producers in China. Transportation of CWSF by pipeline is currently under investigation by China's CWSF Research Center. Currently, third-party logistics providers transport approximately 70% of our finished products, with the balance shipped by our own fleet of trucks.

18

Quality Control

We apply rigorous quality control standards and safety procedures at each of our production facilities. Our manufacturing process is controlled and monitored by a centralized computer control system, which measures and dispenses the precise amount of water and chemical additives required for each production cycle to ensure that each batch of CWSF is consistent with all other batches that we produce. Our quality control technicians regularly test our CWSF production and measure it for condensate, viscosity, evaporation rate, energy content, particle size, sulfur content and ash content.

Although there is no mandatory national standard in China for CWSF quality, the General Administration of Quality Supervision, Inspection and Quarantine of China and the committee of the Standardization Administration of China implemented recommended standards for CWSF in 2002. Our own CWSF production standard exceeds the recommended national standard. We are in the process of obtaining ISO9001:2000 international quality management standard certification for our Tongchuan plant. We plan to obtain a similar certification for our Shenyang facility in the future.

Facilities

We have several production lines at each of our facilities, which are shown in the table below. To minimize technology risk, we have relied primarily on conventional HCPMG technology for CWSF production. In February 2009, we added a production line at our Tongchuan facility that employs SFDA technology, which consumes 10% less electricity than the conventional grinder method, and is able to produce smaller particle CWSF.

|

Production line

|

Method

|

Location

|

Start date

|

Capacity

(metric tons/yr)

|

||||||

|

In Place

|

||||||||||

|

Line 1

|

Grinder

|

Tongchuan

|

Jul-07

|

100,000 | ||||||

|

Line 2

|

Atomizer

|

Tongchuan

|

Feb-09

|

250,000 | ||||||

|

Line 3

|

Grinder

|

Shenyang

|

Oct-09

|

150,000 | ||||||

|

Line 4

|

Grinder

|

Shenyang

|

Oct-09

|

150,000 | ||||||

|

Line 5

|

Grinder

|

Tongchuan

|

Jan-10

|

200,000 | ||||||

|

Sub total

|

850,000 | |||||||||

|

Additional development

|

||||||||||

|

Line 6

|

Grinder

|

Guangdong

|

Jan-11

|

300,000 | ||||||

|

Line 7

|

Grinder

|

Guangdong

|

Aug-11

|

750,000 | ||||||

|

Grand total

|

1,900,000 | |||||||||

Our total CWSF production capacity as of December 31, 2010 is 850,000 metric tons. We intend to expand our CWSF production capacity by up to an additional 1,050,000 metric tons by expanding the production capacity at our Guangdong facility in 2011.

19

In January 2011, two new production lines at the Guangdong facility became operational, with a total capacity of 300,00 metric tons. We plan to add a new production line with capacity of 750,000 metric tons in August 2011. The facility is expected to have an annual production capacity of 1,050,000 metric tons and is expected to expand our total annual production capacity to 1,900,000 metric tons by the end of 2011. We are in the process of taking the necessary steps to obtain a land use right certificate, which is required for us to obtain the rights to use the land and the title to the buildings. We are also in the process of registering a business license of the facility.

The additional 750,000 metric tons of capacity in Guangdong is expected to require capital expenditures of approximately $13.6 million for the construction of production facilities. In addition, our expansion from 850,000 metric tons to 1,050,000 metric tons is expected to require additional net working capital of approximately $15 million in order to run the production lines at full capacity. We intend to complete the new production lines in August 2010, and reach total capacity of 1,900,000 metric tons in the fourth quarter of 2011.

We occupy both owned and leased properties for our operations. We own the land use right to a total of 43,956 square meters of land for our existing site in Tongchuan for a period of 50 years, expiring on December 8, 2057. The buildings and facilities at our Tongchuan location constructed by us are used for the purposes of production, research and development and employee housing. At our Shenyang facility, we have entered into a 10-year lease agreement for the land use right to a total of 7,400 square meters of land, which expires on August 1, 2019. Our principal executive and administrative offices are located in Xi'an, China in approximately 233 square meters of purchased office space.

Customers

Currently all of our customers are based in China and use our CWSF for either industrial purposes or for heating in residential and commercial buildings. As industrial users use the steam generated by CWSF boilers for power and heat in manufacturing processes, there is little seasonality in their consumption of CWSF. Currently, our industrial customers encompass a diverse range of industries such as wineries, paperboard manufacturing, food processing, and ceramic manufacturing. Residential and commercial heating customers experience peak heating demand for approximately 150 days between October and March, and their consumption of CWSF fluctuates accordingly. The following table sets forth the percentage of our revenues by our two principal groups of CWSF customers for the periods indicated:

Sino Clean Energy Customer Breakdown (2007 – 2010)

As of December 31, 2010, we had 43 customers, 38 of which were located within Shaanxi Province (which are being serviced by the Tongchuan facility), and five of which were located in Liaoning Province (which are being serviced by the Shenyang facility). In order minimize logistics costs, we typically sell our CWSF to customers within a 200 kilometer radius of our production facilities. We sell and distribute CWSF directly to our customers. In 2010, our ten largest customers represented 58.5% of total volume sold, while the single largest customer represented 33.5% of total volume sold. During 2010, our ten largest customers by tonnage sold were as follows:

20

2010 Top Ten Customers

|

Customer

|

Type

|

Sales Volume

(metric tons)

|

%

|

||||||

|

Shenyang Haizhong Heating

|

Residential Heating

|

329,341 | 33.5 | % | |||||

|

Shaanxi Dade Property

|

Residential Heating

|

40,629 | 4.1 | % | |||||

|

Shaanxi Tongchuan Yitong

|

Industrial Products

|

31,618 | 3.2 | % | |||||

|

Shaanxi Urban Development

|

Integrated Industrial

|

27,124 | 2.8 | % | |||||

|

Northwest Rubber

|

Industrial Products

|

27,106 | 2.8 | % | |||||

|

Qinqin Food

|

Integrated Industrial

|

25,476 | 2.6 | % | |||||

|

Xi’an Institute of Architecture

|

Integrated Industrial

|

23,717 | 2.4 | % | |||||

|

Shaanxi Baidu Industries

|

Industrial Products

|

23,329 | 2.4 | % | |||||

|

China Northern Airline

|

Industrial Products

|

23,114 | 2.4 | % | |||||

|

Shan’xi Yongxin Paper

|

Integrated Industrial

|

23,045 | 2.4 | % | |||||

|

Subtotal

|

574,499 | 58.5 | % | ||||||

|

Other

|

407,667 | 41.5 | % | ||||||

|

Total

|

982,166 | 100.0 | % | ||||||

We are the dominant CWSF producer in both of our present markets: Shannxi province and Liaoning province. We believe that we are able to differentiate ourselves from our competitors by building a track record and reputation for high quality products and service, by securing long-term customer contracts in each of the target markets, and by selectively expanding into new regional markets. We believe that our CWSF products' high quality gives us a competitive advantage in attracting new customers and retaining existing customers. The emerging growth of the CWSF industry in China, and the market opportunity require that CWSF suppliers have certain skills to work across the value chain. We believe that our management's vision and expertise enables us to forge the necessary partnerships with CWSF industry participants, including boiler vendors, local governments, coal suppliers, and CWSF consumers, allowing us to replicate our model in other geographic regions in order to expand more rapidly than our competitors.

Customer & Supply Contracts

Sales

Our sales contracts outline total sales volume, price, product specifications, delivery schedule, and method of delivery. We have entered into three to five year framework agreements with the majority of our customers whereby we provide CWSF at prevailing market prices, and volumes are renegotiated each year. We have framework agreements in place with approximately 90% of our customers. Typically, the CWSF consumption volume of any given boiler does not fluctuate significantly from year to year. Once established, the customer base for CWSF is very stable, as the consumption patterns are highly predictable and the costs to switch CWSF boilers to other fuels are prohibitively expensive. Current CWSF prices for sales contracts with customers in Tongchuan range from RMB 770 to RMB 810 per metric ton and CWSF prices for sales contracts with customers in Shenyang are RMB 960 per metric ton. CWSF transportation costs and the associated risks are covered by us at both the Tongchuan facility and the Shenyang facility. The prices paid by customers at the Shenyang facility are higher mostly because the coal materials cost is higher in Shenyang, as our customers are relatively farther away from the production facility. If the market price of CWSF differs by more than 10% of the original price quoted in the contract, either above or below, the sales price is re-negotiated. Pursuant to the annual sales agreements, customers generally pay for CWSF on a monthly basis, with payment collected in cash upon delivery. We occasionally provide our customers with extended credit terms of up to three months, for example to certain government residential heating agencies. We set payment methods depending on our business relationship, customers' credit records and prevailing market conditions.

21

Coal supply

We have entered into coal supply contracts with coal mines/coal washing facilities that are near our CWSF production facilities. We have agreements with three such suppliers in Tongchuan and another two in Shenyang. The supply contracts define supply volume, pricing, term, product specifications, and delivery schedule. We set the maximum amount of supply volume, which is guaranteed by the coal supplier. In Tongchuan, we have historically drawn most of our coal supplies from a single supplier and a small portion from another supplier. We are provided coal at prevailing market prices, and volumes are renegotiated each year. However, if the market price of coal exceeds the price initially quoted in the supply contract by 20%, then a new contract can be negotiated. Suppliers must deliver the coal to us within two months after we notify the supplier of our need for coal.

Guangdong facility

We are targeting large CWSF customers in Guangdong, as the province is one of the most economically developed in China, and has the largest consumer capacity for CWSF in China, according to Beijing Zhongjing Zongheng Information and Consulting Center. In August 2010, through our subsidiary, Suoke Clean Energy, we entered into an agreement with Dongguan Yongchang Paper Co. (“Dongguan Paper’), to purchase a land use right for approximately 5 acres of land and a production factory in Dongguan, Guandong Province for a total purchase price of approximately $5,550,000. We paid a deposit of $4,141,000 and the balance will be paid when legal title has been completed. Also, in connection with the acquisition of Dongguan Paper, we entered into an agreement pursuant to which we were transferred 100 % of the equity interest in Dongguan Clean Energy Water Coal Mixture Co. (“Dongguan Water Coal Mix Co.”) from its shareholders for nominal consideration (RMB2) because this transaction was part of the transaction with Dongguan Paper. We acquired Dongguan Water Coal Mix Co. solely because it has a business license to manufacture and sell CWSF in Guangdong. According to the agreement, we could receive the economic benefits and debt obligations after January 1, 2011. The completion of the governmental registration of the equity change and the transfer of the business license depends on Dongguan Water Coal Mix Co. passing its annual registered capital inspection, which is expected to be in May 2011.

In September 2010, we entered into an agreement to purchase two production lines to be operated within the new Guangdong facility for a total purchase price of approximately $5,372,000. The factory was completed and commenced production in January 2011. We are in the process of taking the necessary steps to obtain the land use right certificate, which is required for us to obtain the rights to use the land and the title to the buildings. We are still in the process of transferring the business license of the facility.

In early March of 2011, the City Government of Dongguan passed the Dongguan City Program for Removing and Upgrading Small- and Medium-Size Coal-Burning Boilers, clearly prescribing that small- and medium-size coal-burning boilers of up to and including 10 steam-tons (boiler power scale) must be removed. With the implementation of this policy, we believe that the demand for coal water slurry in Dongguan City will increase rapidly in the next year and a half.

Initially, we had planned to increase overall production capacity by expanding in Nanning and Shenyang, with the goal of adding additional capacity in Dongguan by August 2011. However, in an effort to take advantage of the opportunity presented by Dongguan City Program, we determined it was in our best interests to delay the progress in Nanning and Shenyang, and instead immediately increase production capacity in Dongguan in anticipation of the potential increase in demand. As a result, on March 10, 2011, through our new subsidiary, Dongguan Water Coal Mix Co., we entered into an agreement with Jiangsu Qiulin Heavy Industry Holdings. Co., Ltd. (“Jiangsu Qiulin”) to purchase a 750,000 metric ton production line for use in Guangdong. Based on the terms of the agreement, installation of this production line is expected to be complete by July 15, 2011. We expect this production line to be operational by August 2011. The total purchase price for this CWSF production line is approximately $10.4 million (RMB 69.5 million). With the addition of this new line, our Guangdong facility is expected to have an annual production capacity of 1,050,000 metric tons and is expected to expand our total annual production capacity to 1,900,000 metric tons by the end of 2011.

Nanning facility

The Nanning government is also aggressively promoting the usage of CWSF as an alternative fuel, and has publicly indicated its intention to establish local CWSF production capacity of 3 million metric tons. Presently, there are only two local CWSF producers in Nanning, each with a capacity of approximately 100,000 metric tons. We have entered into an agreement with Guangxi New Heat Energy Company ("GNHEC") pursuant to which we act as the exclusive CWSF provider in the Jin Kai Industrial Park of Nanning Economic and Technological Development Area.