Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K/A

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission File Number 000-53765

SILVER FALCON MINING, INC.

(Exact name of registrant as specified in its charter)

Delaware | 26-1266967 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

7322 Manatee Avenue West Bradenton, Florida 34209

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (941) 761-7819

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $0.0001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Ac. Yes [ ] No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No [ ]

1

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No [ ]

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K/A or any amendment to this Form 10-K/A. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] | Accelerated filer [ ] | |

Non-accelerated filer [ ](Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ]No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $34,595,689 based upon a market price of $0.16 per share.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: 304,665,315 Class A Shares and 3,884,321 Class B Shares as of March 9, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K/A (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980). None.

EXPLANTORY NOTE: The Registrant is filing this amended to edit a date typo on the first page of this filing.

2

PART I

ITEM 1. BUSINESS.

Overview

We were formed in the State of Delaware on October 15, 2007. On October 15, 2007, we completed a holding company reorganization with Dicut Holdings, Inc. (“Dicut”) pursuant to Section 251(g) of the Delaware General Corporation Law. Dicut previously operated in the information technology business, but ceased operations in 2005.

On September 14, 2007, GoldLand Holdings, Co. (“GoldLand”) acquired an interest in 174.82 acres of land on War Eagle Mountain in Idaho, consisting of a 100% interest in 103 acres, and a 29.166% interest in 71.82 acres.

On October 11, 2007, we entered into a lease agreement with GoldLand, under which we leased GoldLand’s owned and leased acreage on War Eagle Mountain, Idaho. The lease expires on April 1, 2025, although we have the right to extend the lease for an additional five years upon payment of a lease extension fee of $1,000,000. Under the lease, we are responsible for all mining activities on the land, and we are obligated to make annual lease payments of $1,000,000 per year payable monthly, plus a nonaccountable expense allowance of $10,000 per month for any month in which ore is mined from the property, and a royalty of 15% from any proceeds we receive from a smelter of ore produced from land. Pierre Quilliam, our chairman and chief executive officer, was also the chairman and chief executive officer of GoldLand at the time the lease was entered into.

On September 21, 2008, we acquired from Mineral Extraction, Inc. all mineral, mining and access rights to two mining claims on War Eagle Mountain, covering 18.877 total acres, and filed lode claims for four mill site locations and the Sinker Tunnel location. In December 2009, we acquired a mill site at the foot of War Eagle Mountain, and constructed a mill on the site.

We began actual operations in May 2010. Initially, our operations will consist of processing tailings left on the mine site from prior mining operations, which estimate are about 500,000 tons. Later, after we complete a confirmation program to prove up and locate reserves on our property, and make further capital improvements to the mine site, we plan to begin mining and processing raw ore.

In 2010, the roads to the Sinker Tunnel Complex were upgraded to allow 25-ton trucks access to the site, and an area 300x400 feet was prepared to act as a staging area at the 5,200 foot level. The Sinker Tunnel was aerated in its entire length and the entrance to the Sinker Tunnel was permanently extended and secured to avoid land or snow slides to block access to the Sinker Tunnel. Permanent drainage pipes are being laid in the Sinker Tunnel as it was determined that the Sinker Tunnel is the main drain for the War Eagle complex. Mining and shoring or rock bolting of some weak points in the top wall is underway. Permitting for exploration of the Sinker Tunnel is underway with training for underground personnel and safety measures being installed per the latest mining rules and regulations.

History of Mining on War Eagle Mountain

3

War Eagle Mountain is one of three peaks in Southwest Idaho that form a contiguous fault trend, and which have all produced minerals from the same veins: Delamar Mountain, Florida Mountain, and War Eagle Mountain.

In the summer of 1862, the Oro Fino Vein on top of War Eagle Mountain was discovered. During 1863 a number of lode claims were located and mining in earnest began. By the end of 1875 a total of ten shafts had been sunk in the Oro Fino Vein ranging in depth from 300 feet to 1,250 feet. The Oro Fino Shaft at the North end is 300 feet deep and the Mahogany Shaft at the South end is 1,100 feet deep. The Golden Chariot and Ida Elmore shafts are 1,250 feet and 1,000 feet respectively.

By 1866, all the major mines in the area had been discovered and were being developed. The major mines were the Oro Fino, Cumberland, Poorman, Ida Elmore, Golden Chariot, Minnesota, Mahogany and the Morning Star in Silver City. There were 12 mills in the area with a total of 132 stamps to pulverize the ore, separate the metal from the rock and pour the raw metal into rectangular bricks of bullion dore. This bullion was then shipped out of the area, sometimes as far away as Europe, for refining into pure gold and silver. By the end of 1875, approximately 750,000 ounces of gold equivalent were reportedly extracted from the shafts on War Eagle Mountain.

In August 1875, a financial panic that had started in New York in 1873, culminated with the San Francisco bank crash, and then the closure of the San Francisco Stock Exchange. A nationwide depression occurred, which resulted in source of working capital for the mines drying up. The miners continued to work without pay until October 1875, when they left the mountain for employment elsewhere. During the winter of 1875-1876, because the mines were not being used, the shafts filled with water. This condition has existed for the past 134 years, which has resulted in the preservation of these historical vein systems without being disturbed by intruders or miners.

From 1875 through 1899, mining men who had managed and worked in the underground mines and milling operations tried to promote a project that would allow them to recover the remaining submerged gold and silver reserves they knew existed. Finally, in November 1899, American Smelting and Refining Company (ASARCO) funded the Sinker Tunnel Project. The project objective was to drive a 10 x 10 tunnel from Sinker Creek on the North-East side of War Eagle Mountain, at an elevation of 5200 feet, approximately 2,000 feet below the bottom of the Golden Chariot Shaft. This tunnel was named the Sinker Tunnel, and its intended use was to drain water out of War Eagle Mountain and to haul ore mined from the veins to the surface for milling. The cost of the project was about $250,000 (or the equivalent of $25,000,000 today).

It was anticipated that the Sinker Tunnel would intersect the Oro Fino Vein at about 7,000 feet from the tunnel portal. The Oro Fino Vein was actually intersected at 6,890 feet in May 1902. After the Sinker Tunnel was extended north about 80 feet, a raise was started upwards toward the bottom of the Golden Chariot Shaft. When this raise reached 620 feet in height it was only 150 feet below the bottom of the Golden Chariot Shaft, which contained about 1,100 feet of water. At this point the amount of water permeating down into the raise was increasing every day, which caused the miners to become anxious about their safety, and raised concerns as to how ASARCO would punch the final hole into the bottom of the Golden Chariot shaft. The miners raised concerns with the Idaho Inspector of Mines about the working conditions, which resulted in the Idaho Inspector of Mines stopping any further work in the area until safety measures were implemented. At that time, ASARCO elected to close the project down, and return later if conditions changed, which never happened.

4

During 1932 and 1933, some additional exploration tunnels were driven to the north and to the south from the raise. In 1941, salvagers opened the Sinker Tunnel and removed all the steel rail and pipe scrap for the war effort. Shortly thereafter, a landslide completely buried the entrance to the tunnel under 50 feet or more of earth and rock, and the Sinker Tunnel complex was forgotten.

In 1993, Mineral Extraction, Inc., the current owner at the time, rediscovered the location of the tunnel and over several years attempted to refurbish the Sinker Tunnel complex, with the exception of the raise, nearest the bottom of the Golden Chariot shaft. The entrance was excavated, and a semi permanent structure was built to protect the site. In 2010, the roads to the Sinker Tunnel Complex were upgraded to allow 25-ton trucks access to the site, and an area 300x400 feet was prepared to act as a staging area at the 5,200 foot level. The tunnel was aerated in its entire length and the entrance to the tunnel was permanently extended to avoid land or snow slides to block access to the tunnel. Permanent drainage pipes are being laid in the tunnel as it was determined that the Tunnel is the main drain for the War Eagle complex. Mining and shoring or rock bolting of some weak points in the top wall is underway. Permitting for exploration of the tunnel is underway with training for underground personnel and safety measures being installed as per the latest mining rules and regulations. The company is also a member, in good standing, of the Idaho mining rescue system.

The mines on War Eagle Mountain were very productive in the first few years because the surface deposits were of extraordinary richness. As the mines got deeper the veins had a smaller yet more consistent amount of ore in relation to the amount of rock that needed to be removed to expose it. Generally, the value of ore per ton of rock removed remained consistent from a depth of 150 feet to as deep as any of the mines were worked. This would indicate that the extensions of the veins into the deeper levels, not yet reached by the mine shafts, would contain the same percentage of metal ore.

The mines became more expensive to develop and operate as they got deeper. This was not due to a decline in the yield per ton, but due to the increased cost of lifting the mineral ore and of removing water from deeper shafts. The removal of ground water in mines is a persistent expense that must be addressed on a daily basis. When a mine doesn't have a lower working level tunnel – like the Sinker Tunnel Complex – that intersects a vertical shaft, the water must be brought to the surface and disposed of no matter what the expense or technical inconvenience if the mine is to continue operating. This increased cost of mining at depth was one of the most significant problems for the mines on War Eagle Mountain.

Description of Mining Properties

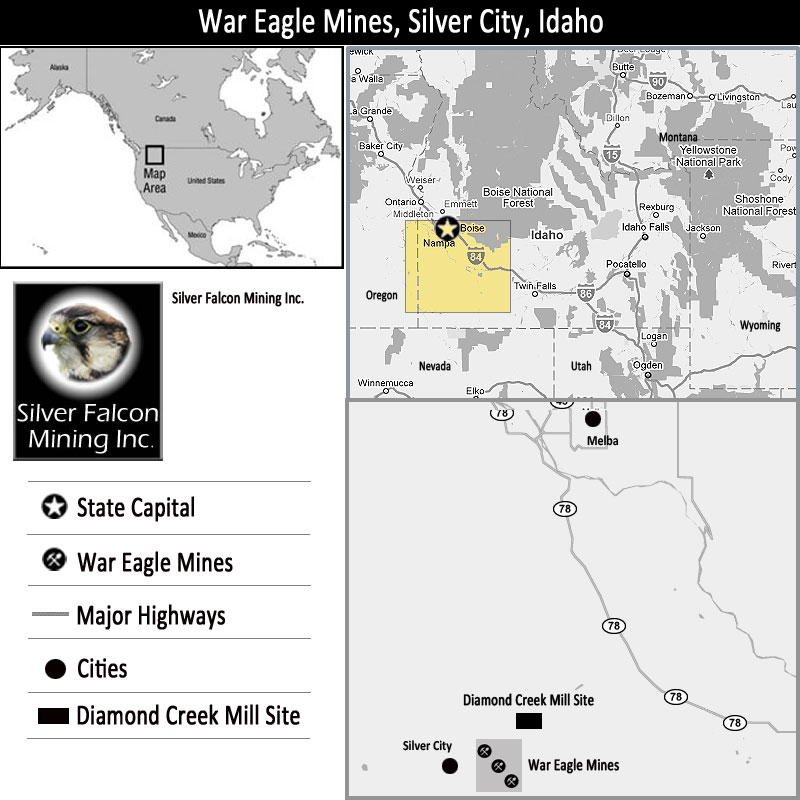

We have one mining property, which is a variety of land and mining claims on and near War Eagle Mountain, Idaho. War Eagle Mountain is located about 50 miles southwest of Boise, Idaho, and about one mile east of Silver City, Idaho. The Sinker Tunnel is about 15 miles off of State Highway 78 and the mine sites on the top of War Eagle Mountain are about 20 miles off of State Highway 78. Access to both the Sinker Tunnel and the mines on the mountain currently is by truck or heavy duty vehicle or ATV, as only the first seven miles of county roadway off of State Highway 78 is paved. Below is a map illustrating the location and access of War Eagle Mountain:

5

Our mine on War Eagle Mountain is a combination of owned and leased land and mining claims.

Leased Properties: GoldLand owns an undivided 29.167% fee title interest in seven properties, and ten unpatented mining claims, which we lease from GoldLand under a lease dated October 11, 2007. The lease expires on April 1, 2025, although we have the right to extend the lease for an additional five years upon payment of a lease extension fee of $1,000,000. Under the lease, we are responsible for all mining activities on the land, and we are obligated to make annual lease payments of $1,000,000 per year payable monthly, a nonaccountable expense allowance of $10,000 per month for any month in which ore is mined from the property, and a royalty of 15% from any proceeds we receive from a smelter of ore produced from land. The properties which we lease from GoldLand are listed below:

6

Name | Ownership Interest | Type of Claim | Acres |

Poorman Lode Claim | 29.167% | Patented claim | 3.44 |

London Lode Claim | 29.167% | Patented claim | 17.52 |

North Empire Lode Claim | 29.167% | Patented claim | 0.98 |

Illinois Central Lode Claim | 29.167% | Patented claim | 2.08 |

South Poorman Lode Claim | 29.167% | Patented claim | 17.06 |

Jackson Lode Claim | 29.167% | Patented claim | 10.33 |

Oso Lode Claim | 29.167% | Patented claim | 20.41 |

Cape Horn No. 1 | 100% | Unpatented Lode Claim | 20.6 |

Great Western No. 1 | 100% | Unpatented Lode Claim | 20.6 |

Great Western No. 2 | 100% | Unpatented Lode Claim | 20.6 |

Great Western No. 3 | 100% | Unpatented Lode Claim | 20.6 |

Great Western No. 4 | 100% | Unpatented Lode Claim | 20.6 |

GoldLand #13 | 100% | Unpatented Placer Claim | 20.6 |

GoldLand #14 | 100% | Unpatented Placer Claim | 20.6 |

GoldLand #15 | 100% | Unpatented Placer Claim | 20.6 |

GoldLand #25 | 100% | Unpatented Placer Claim | 20.6 |

GoldLand #26 | 100% | Unpatented Placer Claim | 20.6 |

A patented mining claim is one which the federal government has passed title to the claimant, making the claimant the owner of the surface and mineral rights. An unpatented mining claim is one which is still owned by the federal government, but which the claimant has a right to possession to extract minerals. Claims to federal land for mining purposes may be obtained by filing a claim with the Bureau of Land Management and paying a nominal fee. A claim may be maintained as long at the holder engages in mining activity on the claim or, in lieu of mining activity, by filing an annual renewal form and paying an annual fee to the Bureau of Land Management by September 1 of each year. The annual fee is $10 per claim for small miners and $140 per claim for large miners. GoldLand is obligated to pay any annual fees to maintain the claims which it leases to us.

GoldLand is not the sole owner of seven of the patented claims that we lease from GoldLand, and instead owns only 29.166% of the claims. The remaining 70.834% of the patented claims are owned by a large number of descendants of the original parties that obtained the patent rights to the mining claims. We are in the process of trying to identify and acquire or lease the remainder of ownership of these mining claims.

Owned Land and Claims: We also own the following claims:

Name | Type of Claim | Acres |

Sinker Tunnel #1 | Unpatented Tunnel location | 20.6 |

Sinker #1 | Unpatented Mill site location | 5 |

Sinker #2 | Unpatented Mill site location | 5 |

Sinker #3 | Unpatented Mill site location | 5 |

Sinker #4 | Unpatented Mill site location | 5 |

7

The Cumberland Lode | Patented Claim | 5.927 |

The Louisiana Lode | Patented Claim | 5.927 |

The Sinker Tunnel is burdened by a royalty obligation to Bisell Investments, Inc. and New Vision Financial, Ltd., under which we are obligated to pay each a quarterly royalty of 7.5% of the net smelter return or net refinery return of any ore which originates, terminates or was gained access through the Sinker Tunnel or the grounds of the Sinker Tunnel complex. The royalty was originally granted by Mineral Extraction, Inc. to Laoshan Group, LLC, and then acquired by the current owners of it, before we acquired the Sinker Tunnel.

We only own the mineral rights to the Cumberland and Louisiana Lode Claims. The surface rights were retained by Mineral Extraction, Inc., although we entered into a license agreement with Mineral Extraction, Inc. under which we have the right to use the surface for all purposes related to mining ore from the claims.

Mill Site: We own 20 acres in Owyhee County at the foot of War Eagle Mountain, where he have offices on site and a milling complex suitable for the present planned production.

Geology of Mining Properties

War Eagle Mountain is the eastern most peak in the War Eagle-Florida-Delamar Mountain trend, which is an east to west chain of mountains in Southwestern Idaho. All three peaks show the same type of gold and silver veins. Kinross Gold Corporation owns Florida and Delamar Mountains. Delamar Mountain, the western most of the three, had been successfully open pit mined from 1977 to the late 1990s.

The host rock on War Eagle Mountain is granite. The veins containing gold and silver are primarily filled fissures in the host rock that occur primarily in a north-south direction. The gold and silver bearing veins of War Eagle Mountain are steeply dipping to subvertical in attitude and are generally oriented in a NS to NW-SE direction. For example, the Oro Fino/Golden Chariot vein, which is the vein that has been mined and explored the most, occurs at an 8 percent tilt to vertical. The textures, mineralogy and geometry of the veins all indicate that they are "epithermal" deposits. This means that, according to the current interpretations, the minerals were deposited by hydrothermal solutions of “supercritical” very hot, high pressure water that made their way upward through the earth’s crust, depositing the minerals in the loose rock in the fissures. The richest ores have been found in ore shoots, which are places where small cross-fractures intersect the main vein.

Historical records indicate that the Oro Fino Vein system extends at least some 12,000 feet in a north-south direction and has been observed to vary greatly in thickness (from 0.5 ft to 25 ft) and mill grades of 0.5 to 1.25 Troy ounces of gold per ton. Our owned and leased land encompasses only about 600 feet of the Oro Fino Vein system, but all of the major mine shafts that exist on the system. Several large pockets of very rich ore concentration have been found scattered throughout the ore shoots. Mill grades at these ore shoots containing up to 25 Troy ounces per ton have been encountered, with some areas showing grades as high as 90 to 300 oz gold/ton.

It is not known exactly how deep the vein systems are on War Eagle Mountain. The Sinker Tunnel cuts through the Oro Fino Vein approximately 2,500 feet below the outcrop on the surface and was still strong and well developed. To date, only about the first 300 to 1100 feet in depth of the Oro Fino Vein has been mined on approximately 15% of its total known length.

8

Because the host rock on War Eagle Mountain is granite, the mine shafts on War Eagle Mountain are very stable, with minimal need to shore the walls with timber. Also, the Sinker Tunnel Complex needs almost no timber to shore or brace its walls or ceilings.

Mining activity to date has focused on three veins that show at the surface of War Eagle Mountain – the Oro Fino Vein system, the Poorman Vein system and the Central Vein system – with the Oro Fino Vein being the most productive. The Poorman Vein is about 1,000 feet to the west of the Oro Fino Vein. Historically, the Poorman vein has produced mostly silver. The Oro Fino Vein system has approximately 6 other vein systems associated with it, while some 40 additional main vein systems are believed to exist on War Eagle Mountain.

At present, work on the mine consists largely of vertical mine shafts at the top of War Eagle Mountain, which were started by miners in the 1800’s, typically on top of a vein that was evident from an outcropping on the surface. The interiors of the mine shafts are believed to be in good shape, but they are all flooded from groundwater and will have to be drained before active mining can commence. We plan to drain the mine shafts by connecting them to the Sinker Tunnel below. We have recollared five mine shafts with stones and steel rails to make them safer and prevent rain water from entering the mines. We have extended the Sinker Tunnel entrance by 70 feet and relandscaped the property around the extension, both on the request of the Bureau of Land Management and of our engineers.

Through December 31, 2010, we spent approximately $868,859 to acquire and refurbish the mine shafts, the Sinker Tunnel and access roads.

Some of the properties have been surveyed by competent professional engineer and surveyors, but we have yet to have the properties evaluated to determine whether any mineral deposits can be mined profitably at current market rates. Therefore, the properties are without known reserves and our proposed mining activities are exploratory in nature at this time. The most comprehensive survey of the mineralogy of War Eagle Mountain is a report issued by the Idaho Bureau of Mines and Geology in 1926. However, the authors of the report did not have access to the flooded mine shafts, and developed their report from visual observation of the surface, reports of past mining activity, and interviews with mining engineers who had previously worked at the site. Other reports include a report prepared in 1928 by Sinker Tunnel Mining Co., which at the time was in the process of refurbishing and extending the Sinker Tunnel, and a report issued by Copper Range Exploration in 1970. However, the mountain has never been surveyed with a comprehensive scheme of core samples to locate and assess the veins that exist on the mountain. All representations of potential quantities of minerals are based on historical records which are believed to be accurate, but which may not have been performed pursuant to modern standards for evaluating mineral claims. We will start core drilling from inside the Sinker tunnel and on the surface of War Eagle Mountain during 2011 and will have a resident geologist analyze the cores and draw a 3D picture of the inside of the mountain and its mineral contents.

Description of Milling Process

We have installed a mill at the foot of War Eagle Mountain which is capable of processing 100 tons of ore per day using a chemical free process. A total of 3 circuits at the mill will produce a gold and silver concentrate as follows:

·

Ore arrives at the mill by truck from the mountain and is weighed and stacked on site in piles clearly identified as to source. A sample is then taken to be assayed for quality

9

control. The ore bearing rock is then loaded into a crushing and sorting circuit consisting of 3 crushers, conveyors and sorters which reduces the ore to 5/16" nuggets or smaller.

·

The crushed ore is brought into the mill via conveyor and mixed with water in a steel ball mill to produce a liquid slurry which is strained through a <270 mm mesh strainer. The ore bearing slurry water is strained, and then pumped into a Falcon Concentrator, which is basically an inverted rubber bell that spins at a high rate of speed. The concentrator forces the heavy particles in the slurry up the sides of the bell, where the heavier metals fall as a paste. The paste is sent to the riffles table where a divider allows the washed ores to go to the concentrate tank for settling. The cloudy water is sent to the belt press which squeezes 97% of the water out of the feed and sends it to the tanks to be reused, while the sediment is sent to a tailings pile. The dry tailings are stored in an outside tailings pile which will then be shaped consistent with the contours of the land and covered and seeded for preservation of land appearance. The water is provided by underground storage tanks and is recycled continuously, thus requiring only a small amount of water to make up for losses due to evaporation and spillage.

·

The paste that collects in the concentrate tank is then remixed with clear water and put through a vibrating process where the heavy metals (gold, silver, titanium, etc.) are separated from other substances and deposited in sealed containers. The final product is then dried, assayed and sent to the contracted smelter for purification. We will pour our own bullion dore bars during the course of this year.

Smelting Operation

We are in the process of building a smelter operation to further process the concentrate that is produced in our milling operation. We estimate it will cost approximately $200,000 to construct and equip the smelter, and should be completed around July 1, 2011. The smelter will enable us to process the gold and silver in our concentrate into dore bars, which will then be assayed and shipped to a refiner for final processing to the level of purity needed to market the ore. Until our smelter is complete, we plan to stockpile our concentrate.

Competition

We have no competition for the extraction of minerals from War Eagle Mountain, since no other mining company has an interest on War Eagle Mountain at this time. However, the mineral extraction business in general is highly competitive. Numerous larger mining companies actively seek out and bid for mining prospects and properties as well as for the services of third-party providers and supplies, such as mining equipment, transportation equipment and smelters, upon which we rely. Many of these companies not only explore for, produce and market minerals, but also carry out smelting and refining operations and market the resultant products on a worldwide basis. Most of our competitors have longer operating histories and substantially greater financial and personnel resources than we do.

Competitive conditions may be substantially affected by various forms of legislation and regulation considered from time to time by the government of the United States and the states in which we have operations, as well as factors that we cannot control, including international political conditions, overall levels of supply and demand for minerals, and currency fluctuations.

Markets and Major Customers

10

Our original plan was to process the ore we mine into concentrate and then contract with a refinery to refine the bullion concentrate and purchase any resulting minerals at market prices, less a commission. While there are a number of refiners which will refine concentrate on a contract basis, our current plan is to construct our own smelting operation to convert our concentrate into dore bars, and then ship the dore bars to a refinery for final processing. Operating our own smelting operation will allow us to control the processing of our minerals better, including the ability to more precisely assay our production before it is shipped to a third party for final processing. Under our lease agreement with GoldLand, we are obligated to pay a royalty of 15% of any amounts we receive from the refinery.

Seasonality of Business

Weather conditions will affect our ability to mine ore from our property. Generally, from November to April of each year the road leading to the top of the mountain property is impassable because of snow. We will be transporting ore from the dumps on the mountain during the coming summer and fall. We are keeping the road to the Sinker Tunnel open year round and plan to mine and deliver more ore to the mill when we start underground mining, to ensure a steady stream of revenues throughout the year.

Operational Risks

Mining involves a high degree of risk, which a combination of experience, knowledge and careful evaluation may not be able to overcome. Mining involves the risk that fires, shaft collapses, flooding, equipment failure, human error and other circumstances may cause significant injury to persons or property, and may affect our ability to extract mined ore from our properties without significant additional capital expenditures. In such event, substantial liabilities to third parties or governmental entities may be incurred, the satisfaction of which could substantially reduce available cash and possibly result in loss of our leased mining properties. Such hazards may also cause damage to or destruction of our mine shafts, producing formations, production facilities, storage and transportation facilities, or other processing facilities.

We will not insure fully against all risks associated with our business either because such insurance is not available or because we believe the premium costs are prohibitive. A loss not fully covered by insurance could have a materially adverse effect on our financial position and results of operations. For further discussion on risks see “Risk Factors” below.

Regulation

Mining operations on War Eagle Mountain will be affected by numerous laws and regulations, including environmental, conservation, tax and other laws and regulations relating to the resource industry. Most of the extraction operations will require permits or authorizations from federal, state or local agencies. We are responsible for compliance with all applicable laws and regulations under the terms of our lease with GoldLand, but the denial or vacating of permits needed by us could have a material adverse effect on our revenues. In view of the many uncertainties with respect to current and future laws and regulations, we cannot predict the overall effect of such laws and regulations on our future revenues.

We expect that our operations will comply in all material respects with applicable laws and regulations. We believe that the existence and enforcement of such laws and regulations will have no more restrictive an effect on our operations than on other similar companies in the resource industry.

Environmental

11

General. Mining operations on War Eagle Mountain are subject to local, state and federal laws and regulations governing environmental quality and pollution control in the United States. The extraction of mineral ore, is subject to stringent environmental regulation by state and federal authorities, including the Environmental Protection Agency ("EPA"). Such regulation can increase the cost of planning, designing, installing and operating mining facilities.

Significant fines and penalties may be imposed for the failure to comply with environmental laws and regulations. Some environmental laws provide for joint and several strict liability for remediation of releases of hazardous substances, rendering a person liable for environmental damage without regard to negligence or fault on the part of such person. In addition, we may be subject to claims alleging personal injury or property damage as a result of alleged exposure to hazardous substances.

Waste Disposal. Mining operations on War Eagle Mountain may generate wastes, including hazardous wastes, that are subject to the federal Resource Conservation and Recovery Act ("RCRA") and comparable state statutes. The EPA has limited the disposal options for certain wastes that are designated as hazardous under RCRA ("Hazardous Wastes"). Furthermore, it is possible that certain wastes generated by mining operations on War Eagle Mountain that are currently exempt from treatment as Hazardous Wastes may in the future be designated as Hazardous Wastes, and therefore be subject to more rigorous and costly operating and disposal requirements.

CERCLA. The federal Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA"), also known as the "Superfund" law, generally imposes joint and several liability for costs of investigation and remediation and for natural resource damages, without regard to fault or the legality of the original conduct, on certain classes of persons with respect to the release into the environment of substances designated under CERCLA as hazardous substances ("Hazardous Substances"). These classes of persons or so-called potentially responsible parties include the current and certain past owners and operators of a facility where there is or has been a release or threat of release of a Hazardous Substance and persons who disposed of or arranged for the disposal of the Hazardous Substances found at such a facility. CERCLA also authorizes the EPA and, in some cases, third parties to take action in response to threats to the public health or the environment and to seek to recover from the potentially responsible parties the costs of such action. Mining operations on War Eagle Mountain may generate wastes that fall within CERCLA's definition of Hazardous Substances, and predecessor mining companies on our properties may have generated wastes that fall within CERCLA's definition of Hazardous Substances.

Air Emissions. Mining operations on War Eagle Mountain may be subject to local, state and federal regulations for the control of emissions of air pollution. Major sources of air pollutants are subject to more stringent, federally imposed permitting requirements, including additional permits. If ozone problems are not resolved by the deadlines imposed by the federal Clean Air Act, or on schedule to meet the standards, even more restrictive requirements may be imposed, including financial penalties based upon the quantity of ozone producing emissions. If the operator of mining operations on War Eagle Mountain fails to comply strictly with applicable air pollution regulations or permits, we may be subject to monetary fines and be required to correct any identified deficiencies. Alternatively, regulatory agencies could require us to forego construction, modification or operation of certain air emission sources.

We believe that we are in substantial compliance with current applicable environmental laws and regulations and that, absent the occurrence of an extraordinary event, compliance with existing local, state, federal and international laws, rules and regulations governing the release of materials in the environment or otherwise relating to the protection of the environment will not have a material effect upon our business, financial condition or results of operations.

12

Research and Development Expenditures

We have not incurred any research or development expenditures in the last two fiscal years.

Patents and Trademarks

We do not own, either legally or beneficially, any patents or trademarks.

Employees and Consultants

At December 31, 2010, we had 21 employees.

We have no collective bargaining agreements with our employees, and believe all consulting and employment agreements relationships are satisfactory. We hire independent contractors on an as- needed basis, and we may retain additional employees and consultants during the next twelve months, including additional executive management personnel with substantial experience in the mining exploration and development business.

ITEM 1A. RISK FACTORS.

We Have Minimal Revenue To Date From Our Mining Properties, Which May Negatively Impact Our Ability To Achieve Our Business Objectives.

Since entering into the lease with GoldLand in October 2007, we have experienced losses from our operations. We began processing tailings left over from prior mining activities in June 2010, and shipped our first load of concentrate to a refiner in late 2010, for which we received a small amount of revenues. We have moved a significant quantity of tailings to our milling site to continue processing tailings through the winter. We are currently stockpiling our concentrate, rather than shipping it to a refiner, while we finish building our own smelting operation. Our ability to become profitable will be dependent on the receipt of revenues from our mining properties being greater than our operational expenses. We need to raise capital to finance the purchase and installation of mining equipment, to complete a survey of War Eagle Mountain, the construction of our smelting operation, and for working capital in order to finance the processing of tailings while we construct our smelter. Until we receive material revenues from our mining operations, we are dependent on our convertible note offering to provide funds for operations, the deferral of salaries by our officers and loans from our officers to pay routine administrative expenses, and the willingness of business parties and consultants to accept our common shares as payment. If we cannot generate sufficient revenues from our mining operations, we may never become profitable.

The Properties In Which We Have An Interest Do Not Have Any Known Reserves.

None of the properties in which we have an interest have any reserves. To date, we have engaged in only limited preliminary exploration activities on the properties. Accordingly, we do not have sufficient information upon which to assess the ultimate success of our exploration efforts. If we do not establish reserves, we may be required to curtail or suspend our operations, in which case the market value of our common stock may decline, and you may lose all or a portion of your investment.

We Have a Limited Operating History as a Mining Company, Which Makes It Hard To Evaluate Our Prospects.

13

We have only a limited operating history as a mining company upon which to base an evaluation of our current business and future prospects. To date, our operations have consisted of transporting tailings left from prior mining activities to our mill site, and processing some of the tailings into concentrate. We recently hired a president who has substantial experience running mining operations for other companies, but the remaining members of our management do not have any prior training or experience in minerals exploration or mining. We do not have an established history of locating and developing properties that have mining reserves. As a result, the revenue and income potential of our business is unproven. In addition, because of our limited operating history, we have limited insight into trends that may emerge and affect our business, and we may not be fully aware of many of the specific requirements related to working in the industry. We may make errors in predicting and reacting to relevant business trends and will be subject to the risks, uncertainties and difficulties frequently encountered by early-stage companies in evolving markets such as ours. We may also make decisions and choices that do not take into account standard engineering or managerial approaches mineral exploration companies commonly use. We may not be able to successfully address any or all of these risks and uncertainties. Our operations, earnings, and ultimate financial success could suffer due to our management's relative lack of experience in this industry.

Our Ability To Become Profitable Is Subject To Our Success in the Mining Business, Which Is Subject To Typical Risks In The Mining Business

Our ability to become profitable is subject to the economic risks typically associated with mineral extraction and processing business, including the necessity of making significant expenditures to mine properties and to test potential reserves. The availability of mining and transportation equipment and the cost of actual mining operations is often uncertain. In conducting mining activities, the presence of unanticipated irregularities in formations, miscalculations or accidents may cause exploration, development and, if warranted, production activities to be unsuccessful. This could result in a total loss of our investment.

Shareholders May Suffer Dilution From the Issuance of Common Stock and Convertible Notes To Finance Our Operations

Since we decided to enter the mining business, we have financed the development of our mining operations through the issuance of common stock for services or the issuance of convertible notes for cash. The amount of common stock and convertible notes that have been issued in the last two years has resulted in substantial dilution to shareholders. For example, at December 31, 2008, we had outstanding 97,843,962 shares of common stock, of which 49,572,217 shares had been issued in 2008 largely for services, rent and the conversion of notes. During the year ended December 31, 2009, we issued an additional 71,986,613 shares, largely for services, rent and acquisitions. During the year ended December 31, 2010, we issued an additional 116,756,429 shares, largely for services, rent and the conversion of notes. In addition, at December 31, 2010, we had $2,236,967 in convertible notes outstanding which were convertible into an additional 31,036,265 shares of common stock.

We have recently entered into an equity line of credit with Centurion Private Equity, LLC, under which we are entitled to raise up to $7.2 million from the sale of our shares to Centurion over a 24 month period. Centurion is obligated to purchase our shares pursuant to put notices that we send from time to time at a purchase price equal to 97% of the market price of our common stock, as defined in the agreement. In order to draw under the equity line of credit, we must first file and obtain approval of a registration statement covering all shares issuable under the equity line of credit. The issuance of shares under the equity line of credit could result in substantial dilution to existing shareholders.

14

We expect that we will need to continue issuing shares of common stock for services and convertible notes in order to finance the development of our mining operations until our mining operations become self-sustaining. The future issuance of shares or convertibles will result in additional dilution to existing shareholders which may be substantial.

We Need Additional Capital To Finance Our Mining Operations And We Expect To Obtain It On Terms That Dilute Existing Shareholders

We still need to raise approximately $7,000,000 in additional capital to finance initial operations at our mining site, which will consist of core drilling in the sinker tunnel to build a 3-D picture of Ware Eagle Mountain and to prepare a Section 43-101 report to validate our proven reserves. The prior issuance of shares and convertible notes to finance our mining operations has resulted in substantial dilution to shareholders and we expect the future issuance of shares and convertible notes will result in additional, substantial dilution to existing shareholders.

We Have A Very Small Management Team And The Loss Of Any Member Of This Team May Prevent Us From Implementing Our Business Plan In A Timely Manner; Some Members of Our Management Have Substantial Outside Business Interests.

We have five executive officers and a limited number of additional consultants. Our success depends largely upon the continuing services of our executive officers. We need additional executive personnel in order to fulfill our business plan and satisfy our reporting obligations as a public company in a timely fashion. We do not maintain key person life insurance policies on the lives of any of our officers. The loss of any of our officers could seriously harm our business, financial condition and results of operations. In such an event, we may not be able to recruit personnel to replace our officers in a timely manner, or at all, on acceptable terms.

Furthermore, our employment agreements with all executives permit them to have outside business interests, such that he is not required to devote 100% of his working time to our business. Mr. Quilliam estimates that he spends about 95% of his working time on activities related to the commencement of mining operations on War Eagle Mountain through GoldLand and us. Roger Schammell, Chrisian Quilliam and Thomas Ridenour all spend about 90% of their working time on activities related to the commencement of mining operations on War Eagle Mountain through GoldLand and us. The fact that our executives have outside business interests could lessen their focus on our business.

Our Officers And Directors Have Voting Control Over Us, And Outside Shareholders Will Have Little Voice In Management.

Pierre and Denise Quilliam currently control us by virtue of their control of the majority of our Class B Common Stock. Each share of our Class A Common Stock is entitled to one vote per share, while each share of our Class B Common Stock is entitled to forty (40) votes per share. Pierre, Denise and Christian Quilliam combined control 3,504,321 shares of Class B Common Stock, which is 90.2% of the outstanding Class B Common Stock, whereas they only control 8,877,650 shares of Class A Common Stock which is 2.9% of the outstanding Class A Common Stock. Because of the voting power of the Class B Common Stock, Mr. and Ms. Quilliam control 32.4% of the possible votes on any matter that must be approved by shareholders, which is likely sufficient to control the outcome of any shareholder vote.

15

Our Directors Have A Material Conflict of Interest With Respect To Our Mining Lease With GoldLand.

Our mining operations are based upon a lease of GoldLand’s mining rights on War Eagle Mountain. Four of our seven directors, Pierre Quilliam, Denise Quilliam, Christian Quilliam and Allan Breitkreuz, are the sole directors of GoldLand. In addition, Denise Quilliam, is the spouse of Pierre Quilliam and Christian Quilliam is the son of Pierre Quilliam, and therefore are not disinterested in matters pertaining to GoldLand either.

Our Directors Have A Material Conflict of Interest With Respect To A Royalty Interest In The Sinker Tunnel.

One of our directors, Pierre Quilliam, controls an entity that owns a 7.5% royalty in the Sinker Tunnel. Under the royalty, we are obligated to pay two entities, one of which is controlled by Mr. Quilliam, an aggregate royalty of 15% of the net smelter return or net refinery return of any ore which originates, terminates or was gained access through the Sinker Tunnel or the grounds of the Sinker Tunnel complex. As a result, Mr. Quilliam’s financial interest in our use of the Sinker Tunnel may cause him to favor use of the Sinker Tunnel to extract ore from War Eagle Mountain over alternative methods that might be more cost effective.

We Have Substantial Commitments That Require That We Raise Capital.

As of December 31, 2010, we had $61,530 of cash, current assets of $414,441, current liabilities of $1,221,784, and a working capital deficit of ($807,343). A substantial part of our current liabilities consist of debts that we only have to pay if funds are available, such as accrued compensation to our officers of $727,633. However, we have $200,930 of accounts payable to third parties, and $237,500 of note payments due in the next year. In addition, we have an additional $2,179,481 of notes payable due in more than one year. We expect that we will be able to pay our liabilities in the normal course of business from cash flow from mining operations if we are able to commence operations on schedule and our mining operations meet our profit expectations. If we are not able to commence operations on schedule, or if our operations are not as profitable as we expect, we will have to raise additional capital in order to pay our liabilities, which we expect would be dilutive to existing shareholders.

The Mining Industry Historically Is A Cyclical Industry And Market Fluctuations In The Prices Of Minerals Could Adversely Affect Our Business.

Prices for minerals tend to fluctuate significantly in response to factors beyond our control. These factors include, but are not limited to:

·

weather conditions in the United States and elsewhere;

·

economic conditions in the United States and elsewhere;

·

political instability in Africa and other major mineral producing regions;

·

governmental regulations, both domestic and foreign;

·

domestic and foreign tax policy;

16

·

the pace adopted by foreign governments for the exploration, development, and production of their national reserves;

·

the price of foreign imports of minerals;

·

the cost of exploring for, producing and processing raw mineral ore;

·

the rate of decline of existing and new mineral reserves;

·

available transportation capacity;

·

the ability of mineral extraction companies to raise capital;

·

the overall supply and demand for minerals; and

Changes in commodity prices may significantly affect our capital resources, liquidity and expected operating results. Price changes will directly affect revenues and can indirectly impact expected production by changing the amount of funds available to reinvest in exploration and development activities. Reductions in mineral prices not only reduce revenues and profits, but could also reduce the quantities of reserves that are commercially recoverable. Significant declines in prices could result in non-cash charges to earnings due to impairment. We do not currently engage in any hedging program to mitigate our exposure to fluctuations in mineral prices.

Changes in commodity prices may also significantly affect our ability to estimate the value of producing properties for acquisition and divestiture and often cause disruption in the market for mineral properties, as buyers and sellers have difficulty agreeing on the value of the properties. Price volatility also makes it difficult to budget for and project the return on acquisitions and the development and exploitation of projects. We expect that commodity prices will continue to fluctuate significantly in the future.

If We Fail To Maintain Adequate Insurance, Our Business Could Be Materially And Adversely Affected.

Our operations are subject to risks typical of the mining industry, such as mine collapses, flooding, explosions, fires, pollution, earthquakes and other environmental risks. These risks could result in substantial losses due to injury and loss of life, severe damage to and destruction of property and equipment, pollution and other environmental damage, and suspension of operations. We could be liable for environmental damages caused by previous property owners. As a result, substantial liabilities to third parties or governmental entities may be incurred, the payment of which could have a material adverse effect on our financial condition and results of operations. We currently carry general liability and worker’s compensation insurance, but we do not carry insurance against environmental claims. We consider our coverage adequate for our current operations. We expect to increase our insurance coverage when we begin mining ore from the interior of War Eagle Mountain.

Complying With Environmental And Other Government Regulations Could Be Costly And Could Negatively Impact Our Production, Which Would Adversely Impact Our Royalty Revenues.

The mining business is governed by numerous laws and regulations at various levels of government. These laws and regulations govern the operation and maintenance of any facilities on War Eagle Mountain, the discharge of materials into the environment and other environmental protection issues.

17

Such laws and regulations may, among other potential consequences, require that any operator of mining operations on War Eagle Mountain acquire permits before commencing operations and restrict the substances that can be released into the environment with mining and production activities.

Under our lease of War Eagle Mountain, we are primarily responsible for compliance with all laws and regulations applicable to the mining operations, and our failure to comply could result in damages or claims for personal injury, clean-up costs and other environmental and property damages, as well as administrative, civil and criminal penalties. We do not currently carry insurance coverage for sudden and accidental environmental damages as well as environmental damage that occurs over time. While we do not believe we need environmental insurance based on our current operations, we will reconsider our decision to not have environmental coverage prior to the time we begin to mine raw ore from the interior of War Eagle Mountain. However, we do not believe that insurance coverage for the full potential liability of environmental damages is available at a reasonable cost, and therefore there is a good possibility that we will not procure insurance for environmental liabilities . Accordingly, we could be liable, or could be required to cease production on properties, if environmental damage occurs.

The costs of complying with environmental laws and regulations in the future may harm our business. Furthermore, future changes in environmental laws and regulations could occur that result in stricter standards and enforcement, larger fines and liability, and increased capital expenditures and operating costs, any of which could have a material adverse effect on our financial condition or results of operations.

Our Common Stock is Subject to the "Penny Stock" Rules of the SEC and the Trading Market in Our Securities is Limited, Which Makes Transactions in Our Stock Cumbersome and May Reduce the Value of an Investment in Our Stock.

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a "penny stock," for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

·

that a broker or dealer approve a person's account for transactions in penny stocks; and

·

the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased.

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

·

obtain financial information and investment experience objectives of the person; and

·

make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks.

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Commission relating to the penny stock market, which, in highlight form:

·

sets forth the basis on which the broker or dealer made the suitability determination; and

18

·

that the broker or dealer received a signed, written agreement from the investor prior to the transaction.

Generally, brokers may be less willing to execute transactions in securities subject to the "penny stock" rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

We Will Incur Significant Costs As A Result Of Operating As A Public Company. We May Not Have Sufficient Personnel For Our Financial Reporting Responsibilities, Which May Result In The Untimely Close Of Our Books And Record And Delays In The Preparation Of Financial Statements And Related Disclosures.

As a registered public company, we experienced an increase in legal, accounting and other expenses. In addition, the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), as well as new rules subsequently implemented by the SEC, has imposed various requirements on public companies, including requiring changes in corporate governance practices. Our management and other personnel need to devote a substantial amount of time to these compliance initiatives. Moreover, these rules and regulations will increase our legal and financial compliance costs and make some activities more time-consuming and costly.

If we are not able to comply with the requirements of Sarbanes-Oxley Act, or if we or our independent registered public accounting firm identifies additional deficiencies in our internal control over financial reporting that are deemed to be material weaknesses, the market price of our stock could decline and we could be subject to sanctions or investigations by the SEC and other regulatory authorities.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

ITEM 2. PROPERTIES.

A description of our mining properties is included in Item 1. Description of Business and is incorporated herein by reference.

We have purchased a 20 acres site in Owyhee County at the foot of War Eagle Mountain for an amount of $250,000 payable as follows; $25,000 at purchase and $22,500 per year for the next ten years interest free. We have offices on site and a milling complex suitable for the present planned production.

We also lease office space at 1385 Broadway, New York, under a lease that runs from October 1, 2008 to September 30, 2011 at a rate of $3,060 per month. Under the lease, we issued the lessor 1,250,000 shares of our common stock valued at $110,160 at the inception of the lease as payment of rent for the entire lease term.

19

We also lease office space at 2520 Manatee Ave. W. Suite #200, Bradenton, FL 34205, which we share with GoldLand Holdings, Co., under a lease that runs from August 8, 2010 to August 1, 2013 at a rate of $1,065 per month for the first 12 months and $1,095 per month for the second 12 months and $1,187.40 for the third 12 months. We share the cost of the lease with GoldLand Holdings, Co. equally.

We also lease office space at 641-2 Chrislea Road, Woodbridge, Ontario Canada, under a lease that runs from January 1, 2009 to December 31, 2011 at a rate of $400 per month. We assumed this lease in March 2010. Under the lease, we issued the lessor 480,000 shares of our common stock valued at $9,600 at the time we assumed the lease as payment of rent for the entire lease term.

We believe that we have satisfactory title to the properties owned and used in our business, subject to liens for taxes not yet payable, liens incident to minor encumbrances, liens for credit arrangements and easements and restrictions that do not materially detract from the value of these properties, our interests in these properties, or the use of these properties in our business. We believe that our properties are adequate and suitable for us to conduct business in the future.

ITEM 3. LEGAL PROCEEDINGS.

We are not a party to any material legal proceedings at this time.

ITEM 4. (REMOVED AND RESERVED)

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES.

From January 1, 2009 to March 3, 2010, our Class A Common Stock was traded on the Pink Sheets, LLC under the symbol “SFMI.” On March 4, 2010, trading in our Class A Common Stock moved to the OTC Bulletin Board, also under the symbol “SFMI”. The following table summarizes the low and high prices for our common stock for each of the calendar quarters of 2010 and 2009.

2010 | 2009 | |||

High | Low | High | Low | |

First Quarter | 0.07 | 0.07 | 0.07 | 0.02 |

Second Quarter | 0.23 | 0.21 | 0.05 | 0.02 |

Third Quarter | 0.19 | 0.16 | 0.03 | 0.01 |

Fourth Quarter | 0.19 | 0.17 | 0.09 | 0.02 |

There were 131 shareholders of record of the common stock as of December 31, 2010. This number does not include an indeterminate number of shareholders whose shares are held by brokers in “street name.”

Our common stock is subject to rules adopted by the Securities and Exchange Commission ("Commission") regulating broker dealer practices in connection with transactions in "penny stocks." Those disclosure rules applicable to "penny stocks"

20

require a broker dealer, prior to a transaction in a "penny stock" not otherwise exempt from the rules, to deliver a standardized disclosure document prepared by the Commission. That disclosure document advises an investor that investment in "penny stocks" can be very risky and that the investor's salesperson or broker is not an impartial advisor, but rather paid to sell the shares. The disclosure contains further warnings for the investor to exercise caution in connection with an investment in "penny stocks," to independently investigate the security, as well as the salesperson the investor is working with and to understand the risky nature of an investment in this security. The broker dealer must also provide the customer with certain other information and must make a special written determination that the "penny stock" is a suitable investment for the purchaser, and receive the purchaser's written agreement to the transaction. Further, the rules require that, following the proposed transaction, the broker provide the customer with monthly account statements containing market information about the prices of the securities. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for our common stock. Many brokers may be unwilling to engage in transactions in our common stock because of the added disclosure requirements, thereby making it more difficult for stockholders to dispose of their shares.

Dividend Policy

We have not declared any cash dividends on our Common Stock during our fiscal years ended on December 31, 2010 or 2009. Our Board of Directors has made no determination to date to declare cash dividends during the foreseeable future, but is not likely to do so. There are no restrictions on our ability to pay dividends.

Securities Issued in Unregistered Transactions

During the quarter ended December 31, 2010, we issued securities in the following unregistered transactions:

·

We issued a total of $768,700 in two year notes payable. Interest accrues on the notes at the rate of 7% per year, and is payable monthly, except for notes issued to New Vision Financial, Ltd., which provide that interest is payable annually. Principal and interest due on the notes is convertible into shares of Class A Common Stock at the election of the holder at conversion prices ranging from $0.12 to $0.25 per share.

·

We issued 43,641,549 shares of Class A Common Stock upon conversion of $2,449,065 of convertible notes payable.

·

We issued 4,491,414 shares of Class A Common Stock to eight different parties for services valued at $250,727.

All securities were issued in reliance on the exemption from registration provided by Section 4(2) of the Securities Act of 1933, during the quarter ended December 31, 2010.

21

Issuer Purchases of Equity Securities

Period |

(a) Total Number of Shares Purchased | (b) Average Price Paid per Share | (c) Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Plans or Programs |

October 2010 | -- | -- | -- | -- |

November 2010 | 101,316 | $0.1283 | -- | -- |

December 2010 | -- | -- | -- | -- |

Total | 101,316 | $0.1283 | -- | -- |

ITEM 6. SELECTED FINANCIAL DATA.

Because we are a smaller reporting company, we are not required to provide the information called for by this Item.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

Disclosure Regarding Forward Looking Statements

This Annual Report on Form 10-K includes forward looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (“Forward Looking Statements”). All statements other than statements of historical fact included in this report are Forward Looking Statements. In the normal course of our business, we, in an effort to help keep our shareholders and the public informed about our operations, may from time-to-time issue certain statements, either in writing or orally, that contain or may contain Forward-Looking Statements. Although we believe that the expectations reflected in such Forward Looking Statements are reasonable, we can give no assurance that such expectations will prove to have been correct. Generally, these statements relate to business plans or strategies, projected or anticipated benefits or other consequences of such plans or strategies, past and possible future, of acquisitions and projected or anticipated benefits from acquisitions made by or to be made by us, or projections involving anticipated revenues, earnings, levels of capital expenditures or other aspects of operating results. All phases of our operations are subject to a number of uncertainties, risks and other influences, many of which are outside of our control and any one of which, or a combination of which, could materially affect the results of our proposed operations and whether Forward Looking Statements made by us ultimately prove to be accurate. Such important factors (“Important Factors”) and other factors could cause actual results to differ materially from our expectations are disclosed in this report, including those factors discussed in “Item 1A. Risk Factors.” All prior and subsequent written and oral Forward Looking Statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the Important Factors described below that could cause actual results to differ materially from our expectations as set forth in any Forward Looking Statement made by or on behalf of us.

Overview

22

On September 14, 2007, GoldLand acquired an interest in 174.82 acres of land on War Eagle Mountain, consisting of a 100% interest in 103 acres, and a 29.166% interest in 71.82 acres. GoldLand also has five placer claims on War Eagle Mountain from the U.S. Bureau of Land Management, each of which covers approximately 20 acres, or approximately 100 acres in total.

On October 11, 2007, GoldLand leased its mineral rights on War Eagle Mountain to us. Under the lease, we are responsible for all mining activities on War Eagle Mountain, and we are obligated to pay GoldLand annual lease payments of $1,000,000, payable on a monthly basis, a monthly non-accountable expense reimbursement of $10,000 during any month in which ore is mined from the leased premises, and a royalty of 15% of all amounts we receive from the processing of ore mined from the properties. The lease, as amended, provides that lease payments must commence July 1, 2010. Effective November 1, 2010, GoldLand agreed to allow us to defer lease payments until December 31, 2011, and to extend the lease term by fourteen months.

We began actual operations in May 2010. Initially, as described below, actual operations consists of processing dump material left on the mine site from prior mining operations. Later, after we complete a confirmation program to prove up and locate reserves on our property, and make further capital improvements to the mine site, we plan to begin mining and processing raw ore.

On September 21, 2008, we acquired from Mineral Extraction, Inc. all mineral, mining and access rights to two mining claims on War Eagle Mountain, covering 18.877 total acres, as well as claims for four mill site locations and the Sinker Tunnel location.

Our plan to develop our mining properties into an active mine will take place in three phases.

Start-up Phase

Our initial phase involved completing construction of a mill, and using the mill to process tailings left over from prior mining operations. We were successful in our negotiations to purchase a parcel of land about half way between Highway 78 and the Sinker Tunnel entrance where we have constructed our mill. We closed on the purchase of this site in December 2009. We have purchased all of the milling equipment we need, which is currently installed and operating in Murphy, Idaho. As the mill is up and running, we plan to haul sufficient dump material, leftover from 6 prior mill sites on the mountain, during the summer months, to our mill site for processing during the summer and winter. Our testing indicates that, as a result of milling techniques used in the 1800’s which failed to extract all of the gold and silver from the ore, there are sufficient quantities of gold and silver remaining in the dump material to justify further processing. We elected to build the mill on private property that we own, rather than BLM property, because of lower reclamation costs, even though the offsite property will entail higher transportation costs.

We report that the installation and startup of the mill and the working capital to begin transport of ore to the mill for processing has necessitated an investment of approximately $3.46 million, as follows:

·

The purchase and the preparation of property for mill use cost about $549,375;

·

The installation and certification of the mill cost about $517,283;

·

Completing the purchase mill equipment cost about $1,617,368;

23

·

Moving ore to stockpile at the mill in 2010 cost about $352,911;

·

Start-up mill salaries to the end of 2010 cost $425,238, and are estimated to be an additional $300,000 until June 2011 when our smelter is due to be completed and we begin receiving revenues from our production.

We believe that we have sufficient capital to finance this phase of development.

We closed on the purchase of our mill site in early December 2009, and have begun processing tailings in May of 2010. Since the closing, we have made improvements to the road to the mill site, located an office on the property, removed the topsoil from an area of the mill site where our tailings are stacked and drilled a water well, erected a mill building with ancillary structures and fenced off the area. We were able to move a sufficient amount of tailings, for the winter's production, to the mill site before the roads became impassable on the mountain. We have sufficient tailings to process through the winter, and will be hauling from the mountain as soon as the spring thaw is over when the roads become passable again.

In 2010, the roads to the Sinker Tunnel Complex were upgraded to allow 25-ton trucks access to the site, and an area 300x400 feet was prepared to act as a staging area at the 5,200 foot level. The Sinker Tunnel was aerated in its entire length and the entrance to the Sinker Tunnel was permanently extended to avoid land or snow slides to block access to the Sinker Tunnel. Permanent drainage pipes are being laid in the tunnel as it was determined that the Sinker Tunnel is the main drain for the War Eagle complex. Mining and shoring or rock bolting of some weak points in the top wall is underway. Permitting for exploration of the Sinker Tunnel is underway with training for underground personnel and safety measures being installed as per the latest mining rules and regulations.

Confirmation Phase

During 2010, we substantially revised the scope and cost of our confirmation phase. Our confirmation phrase refers to a program to prove up and locate reserves on our property. We need to obtain a satisfactory estimate of the remaining reserves on the property and their location in order to develop a comprehensive plan for the full development of the mine site. The program will involve building a three dimensional map of War Eagle Mountain showing the precise location of veins, shafts and tunnels. Through exploratory drilling and core sampling, we hope to obtain as much information as possible about the location, thickness and quality of the vein systems near the main shafts, and later throughout the entire mountain. The map will be a valuable tool in analyzing the extent of the remaining reserves, mineralization trends, and other pertinent geological and mining information. The most significant change to the confirmation phase contemplates a more comprehensive set of core samples, both from the surface of the mountain and from the inside of the mountain using the Sinker Tunnel, and associated costs, including locating drilling equipment at the site, and logistical costs for the crew, such as vehicles, meals, shelter on the mountain, and accommodations for a geologist, field technician and drill crew. We decided to expand the scope of the confirmation phase in order to obtain a National Instrument 43-101, which is a report developed by the Canadian Securities Administrators for mining companies. A National Instrument 43-101 is necessary for listing our common stock on any exchange overseen by the Canadian Securities Authority, including the Toronto Stock Exchange.

We have recently hired Mr. Roger Scammell, a geologist with many years of experience in the mining industry, as our President. Mr. Scammell and Engineering Northwest, Inc., a surveying firm, will perform the confirmation phase. Under the direction of our new president, the drillers and surveyors will perform their services with the help of Mr. William Earll, our general manager for our Idaho operations.

24

Another aspect of the confirmation phase will involve the development of a plan to use the Sinker Tunnel to mine the interior of the mountain on a year round basis. The plan will involve accessing and draining the mine shafts on the top of the mountain from the Sinker Tunnel, as well as relocating and collaring old shafts on the mountain. We estimate that the confirmation phase will take about 18 months, and will cost approximately $7,000,000. We began preliminary work on the confirmation phase in mid-2010.

Development Phase

The development phase involves transitioning the mine from processing tailings leftover from prior mining activities to extracting and processing raw ore from the mountain. We believe that full scale mining of raw ore will be profitable. In particular, historical records of mining on the site, and subsequent reports of the geology of the mountain, indicate that veins containing gold and silver extend much further vertically than could be mined when the site was last mined in the 1880’s. In addition, historical records indicate that gold and silver exists in the veins in sufficient densities to warrant mining using modern extraction and milling techniques. The scope of the development phase will depend on the outcome of the Confirmation Phase, which is designed to test the accuracy of our analysis. Our goal is to develop a drilling program that reaches as many reserves as possible at the lowest cost. Among the improvements to the mine site that we anticipate making in the development phase are:

·

We plan to connect the mine shafts on the top of the mountain to the Sinker Tunnel in order to provide drainage to those shafts;

·

We plan to install a transportation system in the Sinker Tunnel (either tire mounted trams, narrow gauge railway, or conveyor system) to move ore out of the Sinker Tunnel for transport to our mill site; and

·

Additional improvements include housing, storage, food preparation facilities, generators for power, etc.