Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2010

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Transition Period From ____________ to ____________

Commission File No. 000-22400

STRATEGIC DIAGNOSTICS INC.

(Exact name of Registrant as specified in its charter)

|

Delaware

|

56-1581761

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

incorporation or organization)

|

identification no.)

|

|

111 Pencader Drive

|

|

|

Newark, Delaware

|

19702

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (302) 456-6789

Securities registered pursuant to Section 12(b) of the Act: None

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

||||||

|

Common Stock, $0.01 par value

|

The NASDAQ Stock Market LLC

|

||||||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large Accelerated Filer o

|

Accelerated Filer o

|

Non-Accelerated Filer o

|

Smaller Reporting Company x

|

|

(Do not check if a smaller

reporting company)

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the common stock held by non-affiliates of the Registrant was $26,760,698, calculated by using the number of shares outstanding and the closing price of the common stock on June 30, 2010 (the last business day of the Registrant’s most recently completed second fiscal quarter).

As of March 25, 2011 there were 20,536,730 shares outstanding of the Registrant’s common stock, par value $0.01 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement (the “Definitive Proxy Statement”) to be filed no later than April 30, 2011 with the Securities and Exchange Commission relative to the Company’s 2011 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report.

|

PART I

|

|

|||

|

ITEM 1.

|

BUSINESS

|

1

|

||

|

Overview

|

1

|

|||

|

Life Sciences

|

1

|

|||

|

Life Sciences Products and Services

|

2

|

|||

|

Kit Products

|

3

|

|||

|

Food Safety Products

|

3

|

|||

|

Agricultural Testing

|

4

|

|||

|

Water Quality

|

5

|

|||

|

Environmental Contamination Detection Products

|

6

|

|||

|

Sales and Marketing Strategy

|

6

|

|||

|

Competition

|

6

|

|||

|

Markets and Products

|

7

|

|||

|

Geographic and Customer Information

|

7

|

|||

|

Regulatory Approvals

|

7

|

|||

|

Manufacturing

|

8

|

|||

|

Research and Development

|

9

|

|||

|

Proprietary Technology and Patents

|

9

|

|||

|

Employees

|

10

|

|||

|

Organizational History

|

10

|

|||

|

ITEM 1A.

|

RISK FACTORS

|

10

|

||

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

14

|

||

|

ITEM 2.

|

PROPERTIES

|

14

|

||

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

15

|

||

|

ITEM 4.

|

[REMOVED AND RESERVED]

|

15

|

||

|

PART II

|

16

|

|||

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

16

|

||

|

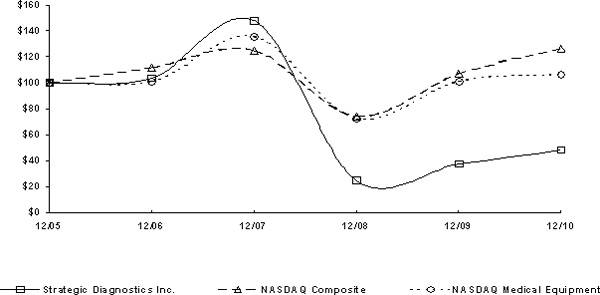

Stock Performance Graph

|

17

|

|||

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

18

|

||

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

19

|

||

|

Forward Looking Statements

|

19

|

|||

|

Overview

|

19

|

|||

|

Results of Operations

|

20

|

|||

|

Year ended December 31, 2010 versus year ended December 31, 2009

|

20

|

|||

|

Year ended December 31, 2009 versus year ended December 31, 2008

|

21

|

|||

|

Liquidity and Capital Resources

|

22

|

|||

|

Off-Balance Sheet Arrangements

|

24

|

|||

|

Contractual Obligations

|

24

|

|||

|

Critical Accounting Policies

|

24

|

|||

|

New Accounting Standards and Disclosures

|

26

|

|||

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

26

|

||

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

27

|

||

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

27

|

||

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

27

|

||

|

ITEM 9B.

|

OTHER INFORMATION

|

27

|

||

|

PART III

|

28

|

|||

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

28

|

||

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

28

|

||

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

28

|

||

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

29

|

||

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

29

|

||

|

PART IV

|

30

|

|||

|

ITEM 15.

|

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES

|

30

|

||

Item 1. Business

Overview

SDIX (“SDIX,” the “Company,” “we,” “our” or “us”), is a biotechnology company with a core mission of developing, commercializing and marketing innovative, effective products and solutions, many of which are proprietary, that preserve and enhance the quality of human health and wellness. The Company serves the pharmaceutical, biotechnology, diagnostics, food safety and environmental markets.

SDIX is a customer-centric organization. Our goals are to consistently deliver increased value to our customers through products and services that facilitate business results, reduce costs and help manage risk. SDIX sales professionals focus among other things on delivering a quantifiable “return on investment” to their customers, demonstrating to them how to reduce time and total costs associated with applications for which the Company’s products are used. In addition, the Company believes its tests and immuno-solutions provide high levels of accuracy and reliability, delivering more actionable results to the customer compared to alternative products.

The Company is focused on achieving profitable growth by leveraging its expertise in antibodies and immuno-technologies to successfully develop proprietary products and services that enhance the competitive advantage of our customers.

The Company believes that our competitive position has been enhanced through the combination of talent, technology, and resources resulting from the business development activities we have pursued since our inception. The Company has achieved meaningful economies of scale for the products it offers through the utilization of its facilities in Newark, Delaware for the manufacture of test kits and antibodies and its facilities located in Windham, Maine for the manufacture of antibodies.

The Company’s Life Sciences product portfolio includes a full suite of integrated immuno-solution capabilities including assay design, development and production. These capabilities, combined with our proprietary Genomic Antibody Technology™ (“GAT™”), are being used today to help discover the mechanisms of disease, facilitate the development of new drugs, and provide the means for rapid diagnosis.

The Company’s Food Safety portfolio includes immunoassays that represent advanced technology for rapid, cost-effective, easy-to-use and accurate detection of food pathogens. SDIX’s RapidChek® and SELECT ™ test kits are experiencing growing adoption for the detection of pathogens such as E. coli, Salmonella and Listeria in the production, processing, and manufacturing of food and beverages.

SDIX has been developing antibodies which have advanced our customers’ immuno-based work for 20 years. By applying its core competencies of creating proprietary, high-quality antibodies and assay development solutions, the Company has produced sophisticated testing and reagent systems that are responsive to our customers’ analytical information needs.

The Company segregates its business into two areas, Life Sciences and Kit Products, which are described below.

Life Sciences

SDIX is a leading provider of a wide range of life sciences products and services, including custom antibodies, in-vitro diagnostic-grade antibodies, proprietary critical reagent products, associated bio-processing services, and custom assay design and development services. The Company’s products and services are sold to, and often embedded in other commercial products used by, a wide range of customers including pharmaceutical, biotechnology and diagnostic companies, and major biomedical research centers both domestically and internationally. The Company is fully integrated to deliver a wide range of services encompassing its customers’ immuno-solution needs from antigen design and antibody development through large scale production and post production bio-processing and immunoassay design and development. Customer service, innovation, and expertise are the foundation of the Company’s competitive advantage. The Company’s ISO9001:2008 accredited facilities employ sophisticated production processes that are reliable and deliver high quality to its customers, and its Newark, Delaware and Windham, Maine facilities are certified and accredited by the Association for the Assessment and Accreditation of Laboratory Animal Care (“AAALAC”), the highest standard in laboratory animal care. The Company is licensed by the U.S. Department of Agriculture for research and its work with laboratory animals.

GAT™ innovation is a key element of the Company’s Life Sciences strategy for establishing and maintaining sustainable differentiation in key markets. The study of gene and protein functionality has created a growing demand for antibody reagents, yet commercially available antibodies exist for only a fraction of the diversity of all proteins and protein modifications. GAT™ was developed to address this growing need for high quality reagents in the Life Science industry. GAT™ products and services utilize sophisticated bioinformatics and immunization strategies to produce high value antibody reagents and biomolecules. SDIX’s application of powerful proprietary algorithms provides GAT™ the ability to “dial in” the precise gene or protein sequence to produce a recombinant protein inside the host animal that in turn elicits an immune response to the encoded protein. This “specificity by design” approach generates antibodies that recognize the conformational epitopes on the native protein. The ability of any antibody to recognize a protein’s naturally folded state has the potential to expand a biomolecule’s utility to advance platforms like flow cytometry. A recognized advantage is the technology’s ability to produce reagents against traditionally difficult cellular targets, such as highly conserved proteins, ion channels and transmembrane proteins.

1

Immunoassay Technology. An immunoassay is an analytical test that uses antibodies to detect the presence of a target in a complex biological sample with high degrees of sensitivity, precision and accuracy. Immunoassays play a central role in the detection and quantitation of proteins associated with disease diagnosis, prognosis and progression, and therapeutic toxicity, efficacy and outcome. Antibody quality and fit for assay application are key to success. The Company’s scientists are experts in antigen design, antibody development and immunoassays. The Company’s scientific expertise with multiple immunoassay formats, coupled with a thorough understanding of the needs of markets and specific customer applications, has allowed the Company to develop a diverse array of immunoassay products.

Life Sciences Products and Services

The overall Life Sciences market is experiencing growth due to the expansion of research in the genomic era into understanding the role of proteins in biology and medicine. According to Frost & Sullivan and other market researchers, the global market for antibody-based reagents and tools in 2008 was approximately $1.8 billion with estimated annual growth in the range of 5-7%. Custom reagent development and production account for approximately $450 million with an estimated 10-12% annual growth rate and premade reagent products comprised approximately $1.4 billion with an estimated annual growth rate in the 5-7% range. We believe that customers in these markets regard the Company as a leader in the design, development and production of critical tools used to target, differentiate, quantify and profile the vast number of proteins related to human health. The Company links its historical expertise in immunotools and immunoassays with the speed and agility of its proprietary GAT™ platform. Post-genomics drug development is a rapidly emerging sector for proteomic immunotools. Within this market, investment has largely shifted from discovery activities into more information-rich integrated development activities. Within the past two years, the Company has supplied 14 of the top 20 pharmaceutical and biopharmaceutical companies with proteomic immunotools to further their drug development programs as well as initial clinical candidates for monoclonal antibody therapeutics. The Company produces antibodies to targets and biomarkers of interest allowing customers to quickly assess the feasibility, efficacy and safety of compounds in their developmental pipelines.

Protein biomarkers as predictive, prognostic, diagnostic, and reporters of activity throughout the drug discovery and development workflow have created increased needs for protein identification and quantitation tools. The Company sees advances in the use of antibodies as tools to measure biomarkers. BCC Research “Biomarkers: The Expanding Global Market”, issued in 2008, projects annual market size for the entire biomarker services industry to be at $13 billion by 2012. The biomarker assay testing market has a proven record of revenue generation. The market was $612 million in 2007 and is estimated to have an annual growth rate of 23.5%. This estimate is based solely on assays and products that are currently available. Currently, high-quality biomarker assays exist for less than 500 proteins (across all species), a fraction (1-2%) of the total number of proteins encoded by the genomes of key species (e.g., human and rodent). We believe that customers in these markets view the Company as a key provider of critical antibody reagents and immunoassay design and development.

We believe that the Company’s experience in antigen design, antibody generation and immunoassay development, together with its proprietary GAT™ platform, put it in a strong position to address these needs. In 2009, SDIX was selected for a third consecutive time through an open Request for Proposal by Science Applications International Corporation (“SAIC”) in cooperation with the National Cancer Institute to generate a library of monoclonal reagents against cancer biomarkers. These antibodies are expected to become part of a reference set of validated tools for researchers. The Company also has a portfolio of catalog antibodies made using its GAT™ platform available for sale online. Within the past year, many new customers have benefitted from these oncology-focused research reagents. In many cases, a singular product has been selected by a client to become a critical testing reagent in long term projects, precipitating the transition of a per-unit sale into a critical reagent supply agreement. These antibodies are now a resource for the Company to assess application in novel platforms, assays and multiplex applications.

The Company offers its services to the IVD market as a CMO (Contract Manufacturing Organization). SDIX’s expertise in immunoassay area and large-scale production capabilities enable it to address IVD clients’ clinical assay needs. Products and services include: analyte specific reagents, custom manufacturing of antibodies (monoclonal and polyclonal) and calibrators, and consultation for immunoassay design.

The Company’s products are suitable for use in a variety of immunoassay formats, including lateral flow devices (LFD) and agglutination assays. The Company’s experience in polyclonal production management and reagent processing ensures lot-to-lot consistency in reagent supply. SDIX facilities (monoclonal as well as polyclonal) are also equipped to meet large volume needs.

The Company maintains regulatory compliance, industrial scale and efficiencies, and necessary quality systems to assure a reliable supply of critical reagents to its partners. The Company offers long-term contracts, in-house quality control and vendor management options in order to address global IVD companies’ immunoassay reagent needs. The Company is supplying diagnostic quality reagents to major global IVD companies, and focuses on high value service areas such as antibody development for new assay targets.

2

Kit Products

The Company’s detection technologies allow industrial customers to rapidly and cost-effectively identify the presence of adulterants, such as chemical toxins, biological pathogens and other contaminants, which can compromise human or environmental safety, and/or financially impact efficiencies of production processes. Many of the Company’s products are in the form of single use test devices, sample prep materials and reagents, thus creating recurring revenue opportunities. Specific industry applications include:

|

|

●

|

Food and Beverage Manufacturing: Systems for high efficiency testing for the identification of pathogens and toxins in food, water and the manufacturing environment.

|

|

|

●

|

Water Utilities: Drinking water facilities test for chemical toxins and pathogens. Wastewater treatment facilities manage pollution control by monitoring efficiency maintenance in biological processing systems, specifically testing for influent and effluent toxic chemicals and pesticides.

|

|

|

●

|

Environmental Management: On-site testing systems to increase the speed and accuracy of environmental monitoring and remediation of soil and ground water pollutants.

|

|

|

●

|

Agriculture and Agro-science: Systems for the detection, identity preservation and quantification testing of genetically modified organisms, and test systems for feed and grain safety testing, including for the presence of mycotoxins.

|

By leveraging its expertise in immunology, proteomics, bio-luminescence and other bio-reactive technologies with innovative application and production capabilities, the Company is able to provide sophisticated diagnostic testing and reagent systems to a diverse customer base serving multiple vertical markets.

Food Safety Products

The Company’s food safety product line includes enrichment media and rapid tests to detect food pathogens, including E. coli O157 (including H7), Listeria and Salmonella.

Food Pathogen Testing

Pathogen specific testing is an increasingly important part of microbiology testing performed in the global food industry. The worldwide market for pathogen tests and media is estimated to be between $850 million and $1 billion according to independent studies and the Company’s own market research. According to several independent studies, the market for pathogen tests grew at a rate of 5 to 7% in 2009 and this growth rate is expected to continue for the next several years. Growth in pathogen testing is driven primarily by regulatory changes, customer testing trends, industry consolidation, and globalization of the world’s food supply.

Since 2001, the Company has invested in the development and market introduction of products for the detection of pathogenic microorganisms in food. In 2002, the Company introduced its first test method for the pathogen E. coli O157 (including H7). The RapidChek® E. coli O157:H7 test strips and proprietary media system have received ongoing market acceptance in the United States. In addition, the RapidChek® test for detection of E. coli O157:H7 was selected by the Food Safety Inspection Service (“FSIS”), the public health agency in the United States Department of Agriculture (“USDA”), as an approved methodology for screening of the organism in raw beef samples. The FSIS section of the USDA conducted a rigorous evaluation of rapid methods that are currently on the market for screening pathogens, including polymerase chain reaction, and automated/manual immunoassays and benchmarked kit performance against the current USDA traditional cultural method. The RapidChek® E. coli O157:H7 method was evaluated and determined to be the “best in class” against the other immunological methods tested. RapidChek® has been included in the USDA Microbiological Laboratory Guidelines as one of only two immunoassays that are recognized for use in screening raw beef for E. coli O157 (including H7). The Company believes that the acceptance of its method by the agencies regulating food safety has increased sales as producers seek to use methods that have been evaluated by the regulatory agencies. The RapidChek® E. coli O157:H7 test system has also received international recognition with regulatory approvals in Canada (Canadian Food Inspection Agency) and Australia (Australian Quarantine and Inspection Service). In 2009, the Company received AOAC Research Institute Performance Tested Method certification for improvements made to the RapidChek E. coli O157 test method including validation of the testing of composite 375g ground beef and beef trim sample.

In June 2004, the Company launched its test for detection of Listeria. This test system received AOAC Research Institute (“AOAC,” “AOAC-RI”) approval for both food and environmental samples, in contrast to several competitive methods on the market that have AOAC approval for food samples only. As a result of new regulations enacted by the USDA in 2003, environmental samples account for approximately 80% of all Listeria testing. The Listeria test incorporates the use of a proprietary enrichment procedure that provides results in 40 hours. In addition, the proprietary enrichment system does not require a transfer step, providing significant labor savings compared to other methods on the market. As with all pathogen systems, food companies require internal evaluations prior to adoption. In these evaluations, the Company’s Listeria test system demonstrated superior performance and improvements in efficiency and productivity compared to most competitive methods on the market. As a result of improvements in performance and cost-in-use, the Company has had the Listeria product adopted by a number of very large food processors.

3

In August 2006, the Company launched its new RapidChek® SELECT™ Salmonella test with AOAC-RI approval at the International Association of Food Protection Meeting in Calgary, Canada. This novel test is based on a patented phage technology combined with the Company’s next generation lateral flow technology and has revolutionized the Salmonella testing arena. The RapidChek® SELECT ™ test was developed to meet some of the challenges faced in Salmonella testing, including high false positive and negative rates, which can be particularly prevalent in high burden samples. The patent claims technology that increases both the specificity and sensitivity of rapid pathogen tests. In September 2006, the RapidChek® SELECT ™ Salmonella test was the first lateral flow test approved for the National Poultry Improvement Plan, and will provide an attractive alternative to current methods used such as labor intensive cultural methodologies. The RapidChek® SELECT ™ Salmonella test was evaluated and adopted by several of the top poultry and beef processors in 2007. The launch and acceptability of RapidChek® SELECT ™ in the market has also facilitated the increase in sales of the RapidChek® Listeria system, as most processors prefer to utilize one platform for multiple testing needs. Customers have cited the use of SELECT ™ contributing to improved laboratory efficiencies and significant savings as compared to what they were previously using to test. In 2010, the Company received AOAC-RI certification for the RapidChek SELECT salmonella system for environmental surface testing using a 24-hour protocol. Also, in 2010, the Company received AFNOR Validation of the RapidChek SELECT Salmonella test system which is critical for marketing of rapid test system in Europe, particularly in France.

In July 2010, the Company launched its new RapidChek SELECT Salmonella Enteritidis (SE) test system. It is applicable to both egg and poultry industries, and will specifically help U.S. commercial egg producers comply with the recent FDA regulation that requires them to test poultry houses and eggs for Salmonella Enteritidis (SE). The new FDA rule became effective July 9, 2010 for commercial egg producers with over 50,000 laying hens and becomes effective July 9, 2012 for egg producers with between 3,000 and 49,999 laying hens. The new rule will affect approximately 3,300 commercial egg producers in the USA. It is estimated that 47 billion eggs are consumed annually in the U.S. and according to reports from the USDA and FDA, there are 2.3 million eggs annually contaminated with Salmonella Enteritidis. In November, 2010 the RapidChek SELECT SE method received AOAC-RI Performance Tested Method certification validating the system for poultry house environmental samples, pooled egg samples and poultry carcass rinses. In January 2011, the US FDA determined that the method was equivalent in accuracy, precision and sensitivity to the traditional testing methods for detecting SE in environmental and pooled egg samples. In February 2011, the RapidChek® SELECT™ Salmonella Enteritidis (SE) test system was granted interim National Poultry Improvement Plan (NPIP) approval by the Secretary’s Advisory Committee on Poultry Health for use in detecting the presence of Salmonella Enteritidis in poultry environments. With these regulatory approvals, the Company believes that its test can help the approximately 3,300 egg producers comply with the new FDA regulations and significantly reduce SE poultry house contamination levels from those being experienced today by providing a more sensitive and accurate detection of SE.

Bacteriophage Technology

Bacteriophage, or phage, are viruses that infect bacteria. They are highly specific for the type of bacteria that they infect and do not infect any other living cell from any other organism including animal, plant, fungus or yeast. Because lytic bacteriophage specifically kill their bacterial hosts and not other living cells, purified preparations of phage have been used medicinally to treat bacterial infections of plants, animals and humans. The use of bacteriophage as a human therapeutic attests to the biological specificity and safety of these viruses. In the last two years, the U.S. Food and Drug Administration (“FDA”) has approved the use of bacteriophage products for direct application to ready-to-eat foods for reduction of Listeria bacteria based on the determination that phage are “generally recognized as safe” (“GRAS”).

The Company is applying its bacteriophage technology in its test kit products for the detection of bacterial food pathogens, including its Salmonella SELECT ™ product. The Company has been awarded a U.S. patent claiming the use of bacteriophage to control competing and cross-reacting bacteria, thereby reducing false positive and negative results and improving analytical test performance.

The Company has also filed patent applications claiming the use of specific lytic bacteriophage to control contaminating bacteria in large scale industrial fermentation processes such as ethanol and lysine production. The Company believes that the use of bacteriophage is a significant improvement over the use of antibiotics and may have a positive impact on yield and cost associated with the production of ethanol from feedstock.

Agricultural Testing

Genetically Modified Crops

Tests for GM traits are generally used to determine whether the sample tested contains the protein associated with the genetic modification. Seeds, grain or leaf tissue are typically tested. The tests may be employed by users desiring to ensure that seed or grain lots are either GM-free or, in other cases, that they contain a specified amount of the GM material in order to meet certain GM requirements. Among the commodities typically tested with the Company’s products are corn, soybeans, rice and cotton. The Company estimates that the worldwide demand for protein based testing of genetically modified crops is $15 million per year. To address this market, the Company entered into an exclusive, worldwide (except Brazil) distribution agreement with Romer Labs (Union, MO) in 2010 for all its TraitChek, SeedChek and GMOChek branded test systems for detecting genetically modified crops.

4

The Company has developed a simple “one-step” test that is used at the point of testing to determine if an individual plant contains the targeted genetic trait. Commercial seed producers use these products to ensure the quality of their products. This type of test also can be used in crops for enforcement purposes to expose unlicensed application of the genetic technology.

Acceptance of GM crops has increased and as the development of new traits has risen, some countries have adopted regulations on biotech crops. In 2004, the European Union (“EU”) adopted regulations regarding labeling and traceability of GM food and feed with enforcement beginning in April 2004. The regulatory tolerance for EU-authorized GM traits is 0.9%, and 0.5% for unauthorized GM traits that have already received a favorable risk assessment from various U.S. regulatory agencies. Traceability systems must be in place and must demonstrate that any traces of GM traits are adventitious and are technically avoidable. The Company no longer believes that the impact of regulations will result in stricter testing of grain and grain exports from countries growing GM crops, or increases in testing to meet these new regulations. Conversely, widespread acceptance of GM crops is generally reducing the practice of grain testing as GM traits are increasingly ubiquitous in the environment.

Water Quality

The Company’s water quality product line includes industrial bio-detection kits for water and soil contaminants such as pesticides, explosives, petroleum related products and polychlorinated biphenyls (PCBs); Microtox® toxicity tests used in a wide array of market segments; and products for detecting polymers and corrosion in water. In addition to use by water utilities and related government agencies, the product line is used in many industrial manufacturing segments, environmental remediation, research and ecological studies. The global market for analytical testing associated with the water and environmental industries is estimated at $1.4 billion based on a compilation of market research studies. The overall annual growth rate in developed markets is estimated at 0-2%, while the annual growth rate in developing markets, primarily Asia, is estimated at 7-9%. The biggest driver for growth is government regulations associated with water quality and environmental protection.

Bioluminescence Technology

The Company’s Microtox® and DeltaTox® tests use a specific strain of luminescent bacteria as biosensors of toxicity, especially in water samples. These bacteria, when exposed to certain chemicals, undergo a chemical reaction resulting in the emission of visible light. Light output is inversely proportional to the toxicity of the sample being tested.

SDIX’s solutions include the instrumentation, reagents and technology necessary to employ testing. The Company has developed proprietary technology to analyze the results and calculate toxicity according to industry standard and regulatory methods. These solutions are highly reliable and offer significantly greater precision than other commonly applied measures of toxicity employing small numbers of living organisms (e.g., fish). The Company’s products, reagent kits, instruments and software provide for rapid and inexpensive assessment of toxicity in multiple applications including approved regulatory methods in many countries worldwide.

Toxicity Testing

In 2001, the Company acquired AZUR Environmental Limited to add the Microtox® product line to its portfolio. Microtox® is a unique rapid acute toxicity test that detects a broad range of toxins and chemical agents. The Microtox® brand is the global reference standard for rapid acute toxicity testing. Microtox® makes toxicity analysis simple and easy to perform and results can be generated in as little as 30 minutes. The Company also markets a portable version of the Microtox® technology known as DeltaTox®. Many water utilities and emergency response teams are using DeltaTox® technology as part of their Water Fit for Use and emergency response programs. Microtox® has been widely accepted by the wastewater treatment industry where managing and controlling costs by accurately assessing the mechanical, operational and chemical performance of these facilities is critical. Microtox® delivers value by helping to improve operating efficiency and by helping facilities stay in compliance with their discharge permits.

In February 2006, the Company announced that its Microtox® bioassay technology was awarded the Designation and Certification as an “Approved Product for Homeland Security” by the Department of Homeland Security. In December 2007, the Company was awarded a Federal Supply Schedule GSA contract. The contract further expands the Company’s reach into federal, state and local agencies, in addition to making it easier for these agencies to do business with the Company.

In March 2010, the Company launched its next generation DeltaTox® instrument. This new instrument, DeltaTox® II, includes features to further enhance business results by enabling global customers implementing strong Water Fit for Use programs.

5

Environmental Contamination Detection Products

The entrance of pesticides into the water supply is a result of agricultural and residential runoff. In areas of substantial agricultural activity, drinking water is tested for pesticides to protect supplies and to comply with federal and state regulations. The Company’s pesticide test kits are used in situations where field testing, or the testing of one specific pesticide gives the test kit much greater utility than a lab-based analyzer. Users include federal agencies such as the U.S. Geological Survey and USDA, state environmental and health departments, water utilities and environmental engineering companies. The Company also sells immunoassay products in the environmental market. The Company offers three different test formats, each with performance characteristics that make them well suited for a particular customer application. All of the Company’s environmental test kits are capable of analyzing multiple samples in parallel. The Company is currently marketing kits for a variety of contaminant classes and has been able to expand its product offerings through distribution agreements to accommodate new technologies.

Sales and Marketing Strategy

The Company markets and sells products in the life sciences, food safety and water quality product categories through a U.S. direct sales force, Internet presence and a network of over 50 distributors in Canada, Mexico, Latin America, Europe and Asia and through the Company’s corporate partners. The Company markets and sells products in agricultural testing exclusively through distributors. The Company also has international sales representatives based in England. The Company evaluates various sales and service models that can contribute to the profitable growth of business. Identifying the most effective channels to market will allow the Company to better allocate resources to both new and existing growth opportunities.

In the United States, the primary sales channel is through a direct sales force comprised of geographically based field sales professionals, key segment managers, and inside sales associates. The sales force is augmented by customer service and project management organizations, and applied technical marketing specialists which assure that all elements of the customer’s buying experience meet and exceed their performance expectations.

On the basis of its strengthening market position, the Company continues to develop channels to market and accelerate predictability and sustainability of revenues. The Company is investing in its direct sales force through the addition of new sales representatives and focused sales and technical training. The Company continually measures sales performance and maintains discipline in the balance between the addition of new sales resources and ongoing efforts to continually improve sales efficiency and effectiveness of existing resources.

The Company is also focusing on its network of quality channel partners. In 2006, the Company added its first distributor for its custom antibody offering. The Company is working to add additional channel partners for both its custom and catalog offerings nationally and internationally.

Since 2007, The Company has expanded its international distribution network for food safety pathogen products, adding and training a total of 15 independent distributors to sell the RapidChek® product line in high growth markets globally, including Southeast Asia, Europe and Latin America. The Company also took a much more aggressive role in marketing these methods. It is anticipated that the additional distributors and international expansions of promotion/sales of the products will increase revenues as they gain acceptability.

Competition

Many of the Company’s potential competitors are large companies with substantially greater financial and other resources than the Company. To the extent that any such companies enter into one or more of the Company’s markets, the Company’s operations could be materially adversely affected. The Company anticipates increased competition as potential competitors perceive that the Company’s products have become commercially proven, or if the Company cannot maintain competitive differentiation.

In the Ag/GMO market, the Company competes with several small, privately held companies (Agdia, Envirologix) that market very similar, if not identical products.

In food pathogen testing, the Company is among the more recent entrants to the market and faces a broad base of competition. The worldwide market for pathogen tests is estimated to be between $850 million and $1 billion annually and as such has drawn many competitive products. The Company’s RapidChek® E. coli O157:H7, Salmonella and Listeria tests compete globally with numerous competitive rapid testing systems. Instrument-based tests are offered by bioMerieux SA and DuPont Qualicon among others. Competitive strip based tests are offered by Neogen Corp., BioControl Systems, Inc. and others. In addition, traditional lab culture methods offer indirect competition. The Company hopes to gain market share from competitive methods and with new users due to key product advantages such as speed of result, ease-of-use, accuracy and by providing overall cost savings.

In rapid toxicity testing, the Company primarily competes against Checklight, Ltd., and one other instrument-based test method produced by Hach Lange, an affiliate of The Danaher Corporation. There are other rapid toxicity competitors based in Europe and China. The Company believes its products have a number of competitive advantages including the comprehensive screening for general toxicity and competes effectively on superior features and functions.

6

With respect to the environmental contaminant test products, the Company currently receives the greatest competition from fixed site environmental laboratories and several small privately held companies. Traditional analytical methods for environmental contamination are often utilized for confirmation and closure of environmental sites. The Company believes it has detection products which are user friendly and provide greater value in use than competitive offerings.

In the antibody product category, the competitive landscape is rapidly changing as the Company continues to shift its emphasis to earlier activities in drug and biomarker discovery. The Company will increasingly compete with technology companies that offer products and services for the discovery and advancement of novel antibodies. The Company believes that its proprietary GAT™ platform coupled with its expertise in assay development provides differentiated access to the high value application markets it is targeting.

The Company also competes in its traditional antibody markets with the internal capabilities of some of the Company’s large pharmaceutical, research and diagnostics customers. These customers often have significantly greater revenues than the Company. Generally these customers produce some products internally and purchase similar products from the Company.

Competitors in the market as third party providers of custom, large scale antibody reagent production include Covance (public), Harlan (private), Lampire (private) and Scantibodies (private). Additionally, there are a number of smaller companies that offer competing products. In the custom research reagent market, the Company has identified approximately 50 companies offering some form of traditional antibody production from customer-provided antigens. The Company believes that its innovation, expertise, and fully integrated suite of immune-solutions plus the scale of its operations are significant competitive advantages against both large and small competitors. In the catalog antibody space, there are over 130 companies competing for this $1.35 billion market.

Markets and Products

The Company sells products in the life sciences, food safety and water quality market categories through its U.S. direct sales force, a network of over 50 distributors in Canada, Mexico, Latin America, Europe and Asia and the Company’s corporate partners. The Company markets and sells products in agricultural testing exclusively through distributors.

Geographic and Customer Information

The following table sets forth sales by geographic region:

|

Year

|

||||||||||||

|

Ended December 31,

|

||||||||||||

|

2010

|

2009

|

2008

|

||||||||||

|

United States

|

$ | 21,269 | $ | 19,739 | $ | 20,744 | ||||||

|

Rest of the world

|

7,080 | 7,415 | 6,915 | |||||||||

|

Total

|

$ | 28,349 | $ | 27,154 | $ | 27,659 | ||||||

The Company’s basis for identifying sales by country is the ship-to location. There were no individual countries outside of the United States that represented more than 10% of the total revenues of the Company.

No single customer accounted for 10% or more of the Company’s revenues in 2010, 2009 or 2008.

Regulatory Approvals

The Company is engaged in the development of antibody and immunoassay products for use in the medical and human healthcare fields. Its current products in this market are intended for “research use only.” The Company also manufactures tests for bacterial food pathogens, mycotoxins, genetically engineered traits in plants and water treatment polymers, which are currently unregulated. However, agencies such as the Environmental Protection Agency (“EPA”), the FDA, and the USDA are engaged in testing and, together with organizations like the AOAC, maintain compilations of official methods for use in testing in certain market segments. Some of these organizations also issue procedures and guidelines for validating new methods. Although not required, official methods adopted by these agencies sometimes have the commercial impact of regulations because the industry and the Company’s customers tend to follow the practices of regulatory agencies.

The Company maintains quality system components compliant with 21 CFR 820, Quality System Regulations, and International Organization for Standardization (“ISO”) 9001:2008 certification for all three of its facilities from an ANSI-ASQ National Accreditation Board (“ANAB”) Accredited International Registrar for ISO 9001 standards. Recognized and respected worldwide, the ISO 9001:2008 standards are put forth by the ISO organization. This certification demonstrates the Company’s commitment to excellence in product and service quality, and a continued focus on improving the customer experience.

7

The Company has maintained AAALAC (Association for the Assessment and Accreditation of Laboratory Animal Care) accreditation at its Delaware facility since 1992 and at its Maine facility since 2000. The Company volunteers to participate in the AAALAC program in addition to complying with the local, state and federal laws that regulate animal research. In order to maintain these accreditations, the Company undergoes regular inspections and reviews. The Company also holds approvals from the USDA, OLAW (Office of Laboratory Animal Welfare), and the NIH, further validating the stewardship of the Company in proper laboratory animal care.

The Company believes that the validation and acceptance of its environmental products by regulatory agencies plays a significant role in market acceptance. EPA SW-846 is the compendium of test methods published by the EPA’s Office of Solid Waste listing those analytical methods that have been validated by the EPA for a stated purpose. The vast majority of the Company’s analytical methods for environmental soil sample analysis are listed in EPA SW-846. Many federal, state and local environmental programs often refer to and rely on EPA SW-846 methods for purposes of remediation and monitoring.

The legislation and regulations that the Company believes are most applicable to its environmental business are the Research Conservation and Recovery Act (“RCRA”), Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), Toxic Substances Control Act (“TSCA”), Federal Insecticide, Fungicide and Rodenticide Act (“FIFRA”) and the Pure Food and Drug Act. For analysis of water and wastewater, the Safe Drinking Water Act, the Clean Water Act and the National Pollution Discharge Elimination System (“NPDES”) permitting program acceptance under the Clean Water Act also will be significant to the Company’s business. As the utility of the Company’s Microtox® products continues to be widely recognized in drinking water security applications, regulations and mandates associated with Homeland Security programs may also have an impact on the Company’s business. Collectively, these programs regulate the management, disposal and clean-up of hazardous substances and protect the nation’s ground and surface water and drinking water supplies.

Manufacturing

The Company manufactures test kits for the detection of a wide array of analytes in five immunoassay formats and one bioluminescence format. The five formats are: one step lateral flow tests; coated tubes; latex particles; magnetic particles; and micro-titer plates. The Company manufactures a biological supplement that enhances the detection of certain analytes and improves overall performance of certain assay formats. In addition to test kits, the Company supplies ancillary equipment and supplies including test evaluation instruments, reagents, sample media, spectrophotometers, pipettes, balances and timers.

The key critical reagent manufacturing technologies are conjugation chemistries, antibody formulations, calibrator preparation, lateral flow strip production, microbiological and immunoassay processes. Reagent production processes include filling and dispensing liquids, subcomponent and finished goods assembly, in-process testing, quality control, packaging and shipping. The critical reagents and production assembly groups produce test kits in the Newark, Delaware laboratories. Biological materials are primarily developed and produced in-house; however, some reagents are licensed from third parties or purchased from commercial sources. A crucial step in the Company’s manufacturing process is the stabilization of the immunoreagents utilizing proprietary lyophilization techniques. In general, raw materials used by the Company in its products are obtainable from multiple sources. The Company purchases instruments and ancillary equipment from outside vendors. A number of the instruments sold by the Company were developed to be used exclusively with the Company’s products and are subject to specific supply agreements. The Company believes that the raw materials, instruments and equipment used in the manufacture of its products are sufficiently available for the Company’s current and foreseeable manufacturing needs.

The Company has implemented data-driven problem solving, measurement and statistical process controls to troubleshoot and continuously improve quality and output performance. Capital investment and equipment automation have reduced key parameter variation, improved production efficiencies and lowered manufacturing costs. The Company utilizes planning tools to control all elements of the supply chain and manufacturing processes, including raw material procurement, inventory management, capacity planning and production scheduling, work-in-process tracking, order processing and fulfillment, shipping and customer invoicing. The Company believes the existing facilities and equipment are sufficient to support a significantly larger production demand.

The Company also supplies a wide array of custom antibody products and services to the in-vitro diagnostic, academic, pharmaceutical and medical research industries. Antibodies are developed and produced using animals or cell culture methods. Laboratories are maintained to prepare immunogens, perform chemical conjugations, purify antibodies, and perform a range of quality control procedures. The cell culture laboratories support the development of hybridomas and manufacture of monoclonal antibodies. The cell culture laboratories also provide services to enhance the productivity of cell lines, establish Master Cell Banks, and store cell lines in secure fail-safe cryogenic systems. In 2010, the Company added antigen strategy and design capabilities along with assay screening capabilities to support antibody and assay development programs for biopharma. Animal facilities house specific-pathogen-free animals that are tested routinely to assure they are maintained under the highest health standards. Capacity utilization in antibody production was approximately 70% during 2010, and there is additional land and zoning clearance on the 64-acre site in Windham, Maine that could be used to potentially double polyclonal operations.

8

Research and Development

The Company engages in substantial research and development activities (R&D) involving development of products, services and technology platforms for its two primary markets, Life Sciences and Food Safety. In the years ended December 31, 2010, 2009 and 2008, the Company incurred approximately $3.1 million, $2.9 million and $3.6 million, respectively, in research and development expenditures.

The Company’s primary laboratory facilities located in Newark, Delaware were designed and built specifically for conducting research and development relating to antibody and immunoassay technology. These facilities include state-of-the art, antibody development and large-scale production facilities. The Company has assembled a scientific staff with extensive experience in the development, production and purification of monoclonal and polyclonal antibodies. The Company also has extensive expertise in the development and production of reagents from the antibodies it produces, as well as commercial immunoassays employing those reagents.

In 2010, the Company continued development of its proprietary GAT™ platform, focusing on advanced methods for development of antibodies to high value proteins that are the targets of pharmaceutical and biotechnology companies. Specificially, the Company carried out a research program to characterize the value of GAT™-produced antibodies as compared to conventionally produced antibodies using peptides for immunization. The resulting data demonstrate that using GAT™ provides higher chances of successfully raising high-quality antibodies for a variety of assay formats compared to conventional, peptide-based immunization strategies. Moreover, this advantage becomes progressively more pronounced with increasingly challenging applications that require particularly high affinity antibodies for high-sensitivity assays.

In the food safety market, the Company completed the development of and commercially launched its new “SE Select™” product to test for Salmonella Enteritidis in the egg and poultry/broiler processing industry, responding to new FDA-mandated testing requirements for the egg-industry implemented in 2010. The test received AOAC RI certification as well as NPIP (National Poultry Improvement Plan) interim certification, and was endorsed by the FDA as a method equivalent to the cultural Bacteriological Analytical Manual (“BAM”) process used by the agency. SE Select is the only thus certified immuno-assay-based low-complexity test currently on the market which significantly outperforms the BAM standard with regard to sensitivity and time-to-result for testing of eggs. Also in the food safety market, the Company received a Certificate of Validation for its RapidChek® SELECT™ Salmonella system from the Association française de Normalisation (AFNOR) thus qualifying the test for the European market.

In 2010, the Company filed one US patent application in the food safety area. The Company’s research and development personnel are experts in many advanced research disciplines in life sciences including immunology, immunochemistry, molecular biology, protein chemistry, biochemistry, microbiology and synthetic organic chemistry. In addition to the technical expertise resident within the research and development organization, the Company’s technical manufacturing organization is expert in large-scale -production, bioprocessing, purification and quality control of antibodies and reagents. The Company’s core expertise is in antibody and immunoassay development and it is a major developer and producer of monoclonal antibodies.

Research and development activities are focused on developing proprietary technology and products to expand the Company’s differentiated market position in Life Science and food safety markets. The Company is a recognized leader in the field of contract antibody and assay development services primarily for large pharmaceutical, biotech, diagnostic and chemical companies, and the development of rapid test kits in the food, water quality and agricultural sectors based on immunoassay technology. In addition, the Company has extensive expertise, facilities and equipment relating to the development and manufacture of one-step lateral flow tests.

The Company’s research and development organization consists of 13 individuals, nine of whom hold advanced academic degrees. In addition, approximately one-third of the Company’s employees are involved in technical job functions.

Proprietary Technology and Patents

The Company’s products are based on the use of proprietary reagents, technology and test systems developed by Company scientists or acquired externally. Accordingly, the Company has implemented a number of procedures to safeguard the proprietary nature of its technology. The Company requires its employees and consultants to execute confidentiality agreements upon the commencement of an employment or consulting relationship with the Company and all employees are required to assign to the Company all rights to any inventions made during their employment or relating to the Company’s activities. Additionally, the Company seeks to protect its technology and processes through the patent process. As of December 31, 2010, the Company holds 24 issued U.S. patents, as well as one U.S. patent licensed for exclusive use by the Company. These patents expire on various dates between June 2012 and September 2026. There can be no assurance that the Company’s patent applications will result in the issuance of any patent or that any patents issued to the Company would provide protection that is sufficiently broad to protect the Company’s technology and products. In addition, the Company cannot be certain that it was the first creator of inventions covered by pending patent applications or that it was the first to file patent applications for such inventions. In addition to seeking patent protection for the Company’s proprietary information, the Company also relies upon trade secrets, know-how and continuing technical innovation to maintain competitiveness for its products and services. The Company has developed a number of proprietary technologies which it has chosen not to patent, including immunization protocols, DNA and plasmid constructs, stabilization systems for reagents, chemical syntheses, and strategies relating to antibody development. While propietary technologies are important to the Company's strategic objectives, the Company derives no revenue from the licensing of any of its intellectual property.

9

|

Expiration Date

|

U.S. Patent

|

Title

|

||

|

6/20/2012

|

5,426,035

|

Method for compensating toxicity test data for the measured toxicity of a reference sample

|

||

|

7/27/2013

|

5,449,611

|

Polyaromatic hydrocarbon (PAH) immunoassay method, its components and a kit for use in performing the same

|

||

|

7/30/2013

|

5,541,079

|

Monoclonal and polyclonal antibodies and test method for determination of organophosphates (license)

|

||

|

10/25/2014

|

5,547,877

|

Methods for the rapid detection of toxic halogenated hydrocarbons and kits useful in performing the same

|

||

|

1/14/2014

|

5,593,850

|

Monitoring of industrial water quality using monoclonal antibodies to polymers

|

||

|

7/27/2013

|

5,618,681

|

Polyaromatic hydrocarbon (PAH) immunoassay method, its components and a kit for use in performing the same

|

||

|

2/23/2016

|

5,780,250

|

Immunoassay standards for polyaromatic hydrocarbon detection

|

||

|

11/10/2015

|

5,834,222

|

Polychlorinated Biphenyls (PCB) immunoassay method

|

||

|

11/10/2015

|

5,858,692

|

PCB immunoassay

|

||

|

2/23/2016

|

5,874,216

|

Indirect label assay device for detecting small molecules and method of use thereof

|

||

|

4/6/2016

|

5,891,657

|

Immunoassay standards for volatile analytes with benzene rings

|

||

|

7/6/2016

|

5,919,645

|

Method for the direct determination of the toxicity of particulate solids

|

||

|

3/29/2016

|

6,096,563

|

Dual particle immunoassay method & kit

|

||

|

11/14/2017

|

6,146,903

|

Method for determination of water treatment polymers

|

||

|

2/23/2016

|

6,376,195

|

Indirect label assay device for detecting small molecules and method of use thereof

|

||

|

9/28/2012

|

6,420,530

|

Determination method

|

||

|

6/1/2019

|

6,524,810

|

Method of making bioluminescent assay reagent based on non-viable E. coli

|

||

|

3/5/2019

|

6,663,833

|

Integrated Assay Device and Methods of Production and Use

|

||

|

8/30/11

|

6,750,328

|

Antibodies for detection of water treatment polymers

|

||

|

9/28/2012

|

6,911,534

|

Method for determination of water treatment polymers

|

||

|

12/12/2023

|

7,189,520

|

Compositions and methods for detecting animal byproduct in feed

|

||

|

5/5/2020

|

7,214,505

|

Cell-based assay for the detection of toxic analytes

|

||

|

11/12/2023

|

7,241,626

|

Isolation and confirmation of analytes from test devices

|

||

|

9/18/2026

|

7,521,201

|

Bacteriophages as Selective Agents

|

||

|

11/27/2027

|

7,532,321

|

Compositions and methods for the detection of water treatment polymers

|

Employees

As of December 31, 2010, the Company employed 150 full time and five part time employees. The workforce was supplemented by five agency-provided contractors. All of the Company’s employees have executed agreements with the Company agreeing not to disclose the Company’s proprietary information and assigning to the Company all rights to inventions made during their employment. Key personnel have signed agreements prohibiting them from competing with the Company. None of the Company’s employees are covered by collective bargaining agreements. The Company believes that its relations with its employees are good.

Organizational History

Strategic Diagnostics Inc. is a Delaware corporation formed in 1990.

Item 1A. Risk Factors

Our results of operations may fluctuate, which could cause volatility in our stock price.

Our results of operations may fluctuate significantly in the future as a result of a number of factors, many of which are outside of our control. These factors include, but are not limited to:

● unanticipated events associated with regulatory changes;

● general economic conditions;

● acceptance of our products;

● the success of products competitive with ours;

● expenses associated with development and protection of intellectual property matters;

● establishing or maintaining commercial scale manufacturing capabilities;

10

● the timing of expenses related to commercialization of new products;

● seasonality; and

● the timing and success in building our distribution channels.

The results of our operations may fluctuate significantly from quarter to quarter and may not meet expectations of securities analysts and investors. This may cause our stock price to be volatile.

If we use hazardous materials in a manner that causes injury or violates laws, we may be liable for damages.

Our research and development activities involve the controlled use of potentially harmful biological materials as well as hazardous materials, chemicals and various radioactive compounds. We use radioactivity in conducting biological assays and we use solvents that could be flammable in conducting our research and development activities. We cannot completely eliminate the risk of accidental contamination or injury from the use, storage, handling or disposal of these materials. We do not maintain a separate insurance policy for these types of risks. In the event of contamination or injury, we could be held liable for damages that result, and any liability could exceed our resources. We are subject to federal, state and local laws and regulations governing the use, storage, handling and disposal of these materials and specified waste products. The cost of compliance with these laws and regulations could be significant.

Our antibody production process utilizes various species of animals that could contract disease or die, interrupting business operations.

Our antibody production process utilizes animals to produce antibodies. We cannot completely eliminate the risks of animals contracting disease or a disaster that could cause death to valuable production animals. Disease or death on a broad scale could interrupt business operations as animals are a key part of the antibody production operation.

If we do not obtain and maintain adequate protection for our intellectual property, the value of our technology and products may be adversely affected.

Our business and competitive positions are dependent in part upon our ability to protect our proprietary technology. To protect our proprietary rights, we rely on a combination of trademark, copyright, patent, trade secret and other intellectual property strategies and laws, employment, confidentiality and invention assignment agreements with our employees and contractors, and confidentiality agreements and protective contractual provisions with other third parties. We attempt to protect our intellectual property position by filing trademark applications and U.S., foreign and international patent applications related to our proprietary technology, inventions and improvements that are important to the development of our business.

As of December 31, 2010, we had 24 issued U.S. patents, two foreign patents and three pending U.S. and international patent applications relating to various aspects of our business. We also had 21 trademark registrations in the United States for a variety of word marks and slogans. We do not believe that any single patent, trademark or other intellectual property right of ours, or combination of our intellectual property rights, is likely to prevent others from competing with us using a similar business model. There are many issued patents and patent applications held by others in our industry. Our competitors may independently develop technologies that are substantially similar or superior to our technologies, or design around our patents or other intellectual property to avoid infringement. In addition, we may not apply for a patent relating to products or processes that are patentable, we may fail to receive any patent for which we apply or have applied, and any patent owned by us or issued to us could be circumvented, challenged, invalidated, or held to be unenforceable, or rights granted thereunder may not adequately protect our technology or provide a competitive advantage to us. If a third-party challenges the validity of any patents or proprietary rights of ours, we may become involved in intellectual property disputes and litigation that would be costly and time-consuming.

Although third parties may infringe on our patents and other intellectual property rights, we may not be aware of any such infringement, or we may be aware of potential infringement but elect not to seek to prevent such infringement or pursue any claim of infringement, and the third party may continue its potentially infringing activities. Any decision whether or not to take further action in response to potential infringement of our patent or other intellectual property rights may be based on any one or more of a variety of factors, such as the potential costs and benefits of taking such action, and business and legal issues and circumstances. Litigation of claims of infringement of a patent or other intellectual property rights may be costly and time-consuming and divert the attention of key company personnel, and may not be successful or result in any significant recovery of compensation for any infringement or enjoining of any infringing activity. Litigation or licensing discussions may also involve or lead to counterclaims that could be brought by a potential infringer to challenge the validity or enforceability of our patents and other intellectual property.

To protect our trade secrets and other proprietary information, we generally require our employees, consultants, contractors and outside collaborators to enter into written nondisclosure agreements. These agreements, however, may not provide adequate protection to prevent any unauthorized use, misappropriation or disclosure of our trade secrets, know-how or other proprietary information. These agreements may be breached, and we may not become aware of, or have adequate remedies in the event of, any such breach. Also, others may independently develop the same or substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets.

11

Our ability to market our services may be impaired by the intellectual property rights of third parties.

Our success is dependent in part upon our ability to avoid infringing the patents or proprietary rights of others. Our industry is characterized by a large number of patents, patent filings and litigation based on allegations of patent infringement. Competitors may have filed applications for or have been issued patents and may obtain additional patents and proprietary rights related to products, services or processes that we compete with or are similar to ours. We may not be aware of all of the patents or patent applications potentially adverse to our interests that may have been or may later be issued to or filed by others.

U.S. patent applications may be kept confidential while pending in the Patent and Trademark Office. If other companies have or obtain patents relating to our products or services, we may be required to obtain licenses to those patents or to develop or obtain alternative technology. We may not be able to obtain any such licenses on acceptable terms, or at all. Any failure to obtain such licenses could impair or foreclose our ability to make, use, market or sell our products and services.

Based on the litigious nature of our industry and the fact that we may pose a competitive threat to some companies who own or control various patents, it is always possible that one or more third parties may assert a patent infringement claim seeking damages and to enjoin the manufacture, use, sale and marketing of our products and services. If a third- party asserts that we have infringed on its patent or proprietary rights, we may become involved in intellectual property disputes and litigation that would be costly and time-consuming and could impair or foreclose our ability to make, use, market or sell our products and services.

Lawsuits may have already been filed against us without our knowledge. Additionally, we may receive notices from other third parties suggesting or asserting that we are infringing their patents and inviting us to license such patents. We do not believe that we are infringing on any other party’s patents or that a license to any such patents is necessary. Should litigation over such patents arise, we intend to vigorously defend against any allegation of infringement.

If we are found to infringe on the patent or intellectual property rights of others, we may be required to pay damages, stop the infringing activity or obtain licenses or rights to the patents or other intellectual property in order to use, manufacture, market or sell our products and services. Any required license may not be available to us on acceptable terms or at all. If we succeed in obtaining such licenses, payments under such licenses would reduce any earnings from our products. In addition, licenses may be non-exclusive and, accordingly, our competitors may have access to the same technology as that which may be licensed to us. If we fail to obtain a required license or are unable to alter the design of our product candidates to make a license unnecessary, we may be unable to manufacture, use, market or sell our products and services, which could significantly affect our ability to achieve, sustain or grow our commercial business.

Moreover, regardless of the outcome, patent litigation against or by us could significantly disrupt our business, divert our management’s attention and consume our financial resources. We cannot predict if or when any third party will file suit for patent or other intellectual property infringement.

The difficulties of operating in international markets may harm sales of our products.

Customers outside of the United States accounted for 25% and 27% of our revenues for the years ended December 31, 2010 and 2009, respectively. The majority of our sales transactions are in U.S. dollars; however, we received payments in British pounds sterling for approximately $0.7 million in sales from our foreign subsidiary.

The international nature of our business subjects us and our representatives, agents and distributors to the laws and regulations of the jurisdictions in which they operate, and in which our products are sold. The types of risks that we face in international operations include, but are not limited to:

● the imposition of governmental controls;

● logistical difficulties in managing international operations; and

● fluctuations in foreign currency exchange rates.

Our international sales and operations may be limited or disrupted if we cannot successfully meet the challenges of operating internationally.

12

Future acquisitions and business combinations that we consummate may be difficult to integrate, disrupt our business, dilute stockholder value or divert management attention.

From time to time, we have considered and may in the future consider expanding our operations and market presence by making acquisitions and entering into business combinations, investments, joint ventures or other strategic alliances with other companies. We may have to issue debt or equity securities to pay for future acquisitions, which could be dilutive to our then current stockholders. We cannot assure you that we will consummate any transactions in the future. However, these transactions create risks, such as:

|

|

●

|

difficulty assimilating the operations, technology and personnel of the combined companies;

|

|

|

●

|

disrupting our ongoing business;

|

|

|

●

|

problems retaining key technical and managerial personnel;

|

|

|

●

|

additional operating losses and expenses of acquired businesses; and

|

|

|

●

|

impairment of relationships with existing employees, customers and business partners.

|

Any of the events described in the foregoing paragraph could have an adverse effect on our business, financial condition and results of operations and could cause our stock price to decline.

If we do not produce future taxable income, our ability to realize the benefits of our net operating loss carryforwards could be significantly reduced.