Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - FlexShopper, Inc. | ex311.htm |

| EX-32.2 - EXHIBIT 32.2 - FlexShopper, Inc. | ex322.htm |

| EX-99.4 - EXHIBIT 99.4 - FlexShopper, Inc. | ex994.htm |

| EX-31.2 - EXHIBIT 31.2 - FlexShopper, Inc. | ex312.htm |

| EX-32.1 - EXHIBIT 32.1 - FlexShopper, Inc. | ex321.htm |

| EX-10.24 - EXHIBIT 10.24 - FlexShopper, Inc. | ex1024.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

or

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 12 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____ to ____

Commission File Number: 0-52589

ANCHOR FUNDING SERVICES, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 20-545-6087 |

|

(State of jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification Number) |

10801 Johnston Road, Suite 210

Charlotte, North Carolina 28226

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (866) 950-6669

Securities registered pursuant to Section 12 (b) of the Act: None

Securities registered pursuant to Section 12 (g) of the Act: Common Stock, $.0001 Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes No [X]

Check whether the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. [ ]

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ].

Indicate by check mark whether the Registrant has submitted electronically and posted on it corporate Web site, if any, every Interactive data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained in this form, and no disclosure will be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in part III of this Form 10-K or any amendment to this Form 10-K [X].

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company as defined by Rule 12b-2 of the Exchange Act: smaller reporting company [X].

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

1

As of June 30, 2010, the number of shares of Common Stock held by non-affiliates was approximately 8,626,000 shares (excluding 381,886 shares of Series A Preferred Stock convertible into 1,949,510 common shares). The approximate market value based on the last sale (i.e. $0.50 per share as of June 30, 2010) of the Company’s Common Stock was approximately $4,313,000.

The number of shares outstanding of the Registrant’s Common Stock, as of February 14, 2011, was 18,634,369. The Registrant also has outstanding 376,387 shares of Series 1 Preferred Stock convertible into 1,881,935 shares of Common Stock.

FORWARD-LOOKING STATEMENTS

We believe this annual report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are subject to risks and uncertainties and are based on the beliefs and assumptions of our management, based on information currently available to our management. When we use words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “should,” “likely” or similar expressions, we are making forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations set forth under “Business” and/or “Management's Discussion and Analysis of Financial Condition and Results of Operations.”

Forward-looking statements reflect only our current expectations. We may not update these forward-looking statements, even though our situation may change in the future. In any forward-looking statement, where we express an expectation or belief as to future results or events, such expectation or belief is expressed in good faith and believed to have a reasonable basis, but there can be no assurance that the statement of expectation or belief will be achieved or accomplished. Our actual results, performance or achievements could differ materially from those expressed in, or implied by, the forward-looking statements due to a number of uncertainties, many of which are unforeseen, including:

|

•

|

the timing and success of our acquisition strategy;

|

|

|

•

|

the timing and success of expanding our market presence in our current locations, successfully entering into new markets, adding new services and integrating acquired businesses;

|

|

|

•

|

the timing, magnitude and terms of a revised credit facility to accommodate our growth;

|

|

|

•

|

competition within our industry; and

|

|

|

•

|

the availability of additional capital on terms acceptable to us.

|

In addition, you should refer to the “Risk Factors” section of this Form 10-K under Item 1 for a discussion of other factors that may cause our actual results to differ materially from those implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Registration Statement will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, if at all. Accordingly, you should not place undue reliance on these forward-looking statements.

We qualify all the forward-looking statements contained in this Form 10-K by the foregoing cautionary statements.

2

PART I

Item 1. Business

Corporate Structure - History

Anchor Funding Services, Inc. (formerly BTHC XI, Inc.) was originally organized in the State of Texas as BTHC XI LLC. On September 29, 2004, BTHC XI LLC and its sister companies filed an amended petition under Chapter 11 of the United States Bankruptcy Code. On November 29, 2004, the court approved BTHC XI LLC’s Amended Plan of Reorganization. On August 16, 2006, and in accordance with its Amended Plan of Reorganization, BTHC XI LLC changed its state of organization from Texas to Delaware by merging with and into BTHC XI, Inc., a Delaware corporation formed solely for the purpose of effecting the reincorporation.

Anchor Funding Services LLC, a limited liability company, was originally formed under the laws of the State of South Carolina in January 2003 and later reorganized under the laws of the State of North Carolina on August 29, 2005. Anchor Funding Services, LLC was formed for the purposes of providing factoring and back office services to businesses located in the United States and Canada. On January 31, 2007, the former BTHC XI, Inc. and certain principal stockholders entered into a Securities Exchange Agreement (the “Securities Agreement”) with Anchor Funding Services, LLC and its members for Anchor Funding Services, LLC to become a wholly-owned subsidiary of the former BTHC XI, Inc. in exchange for 8,000,000 shares of Common Stock of BTHC XI, Inc. (the “Exchange”).

At the time of the Exchange, the former BTHC XI, Inc. had limited operations and limited assets or liabilities. Because the members of Anchor Funding Services, LLC exchanged their equity ownership interests for an aggregate 67.7% equity ownership interest in the former BTHC XI, Inc. (computed immediately after the completion of the Exchange and before the consummation of a financing), this transaction was for accounting purposes, treated as if Anchor Funding Services, LLC was the surviving entity, as if a merger occurred between the parties. Accordingly, for the periods prior to the Exchange, our consolidated financial statements are based upon the consolidated financial position, results of operations and cash flows of Anchor Funding Services LLC. The assets, liabilities, operations and cash flows of the former BTHC XI, Inc. are included in our consolidated financial statements from January 31, 2007, the effective date of the Exchange, onward.

On April 4, 2007, the former BTHC XI, Inc. changed its corporate name to Anchor Funding Services, Inc., which is currently a holding corporation for its wholly owned subsidiary, Anchor Funding Services, LLC. Except as otherwise provided in this Form 10-K, unless the context otherwise requires, references in this Form 10-K to the “Company,” “Anchor,” “we,” “us” and “our” refers collectively to the consolidated business and operations of Anchor Funding Services, Inc. and its wholly-owned operating subsidiary, Anchor Funding Services LLC.

On December 4, 2009, the Company entered into an Asset Purchase Agreement (the “Asset Purchase Agreement”) with Brookridge Funding, LLC (“Seller”) providing for the acquisition of certain assets and accounts of Seller’s purchase order finance business (the “Acquired Business”). The closing of the acquisition took place on December 7, 2009. In connection with the transaction, the Company and Seller’s principals, namely, John A. McNiff III and Michael P. Hilton (collectively "M & H") invested $1.5 million in Brookridge Funding Services, LLC, the Company’s newly formed 80% owned subsidiary which operated the Acquired Business (“Brookridge”). The purchase price for the Acquired Business was $2.4 million (i.e. the Acquired Business’s outstanding client account balances at closing), plus an earn-out payment based on the Acquired Business’s operating income of up to $800,000.

In connection with closing, Brookridge entered into a credit agreement (the “Credit Agreement”) with MGM Funding, LLC, a limited liability owned and controlled by the Company’s Co-Chairmen, Morry F. Rubin and George Rubin, and an investor (“Lender”), pursuant to which Lender provided a senior credit facility to Brookridge of up to $3.7 million. Morry F. Rubin is the managing member of MGM and Chief Executive Officer of the Company. Loans under the Credit Agreement were secured by all of Brookridge’s assets and bore interest at a 20% annual rate. See "Item 13."

Recent Developments

On October 6, 2010, we entered into a Rescission Agreement (the "Agreement”) with the Minority Members, namely, John A. McNiff, III and Michael P. Hilton of its 80% owned subsidiary, Brookridge Funding Services, LLC ("Brookridge"). The purpose of this Agreement is to rescind the Company's acquisition of certain assets of Brookridge Funding, LLC pursuant to an Asset Purchase Agreement dated December 4, 2009. Under the terms of the Agreement, M & H purchased Anchor's interest in Brookridge at book value of approximately $783,000.

3

At closing, the Company delivered an Assignment of its Membership Interests of Brookridge to M & H. The Company executed a Confidentiality Agreement agreeing to keep confidential and not to use certain information concerning Brookridge. M & H executed the Confidentiality Agreement agreeing to keep confidential certain information concerning the Company and the parties executed a Mutual Release Agreement. The Termination Agreement provides that the Company during a Restricted Period of two years may not directly or indirectly call upon, contact, solicit, divulge, encourage or appropriate or attempt to call upon, contact, solicit, diverge, encourage or approach any customer or interfere with the business relationship between customer and Brookridge. The Company is not prohibited from competing with Brookridge or engaging in the business conducted by Brookridge.

Separately from the Rescission Agreement, Brookridge and MGM Funding LLC, a company controlled by our Chief Executive Officer and a director, Morry F. Rubin, by our director, George Rubin, and by a principal stockholder of the Company, agreed to terminate their Credit Agreement. At closing, no monies were owed by Brookridge to MGM.

Effective as of immediately prior to the Closing and in consideration for the sale of the Purchased Interest, M & H and Brookridge agreed to assign their rights and interest in the following assets to the Company:

(a) Brookridge’s current website (not including any rights or interest with respect to the Brookridge name, web address or domain name); and

(b) the Sherburne Account (described below).

The Agreement provides that the Company shall control collection and recovery efforts under the Sherburne Account and shall keep M & H reasonably informed concerning substantive developments pertaining thereto. M & H and the Company in connection with such collection and recovery efforts shall share all out-of-pocket costs and expenses, as well as all collections, in the proportion of eighty percent (80%) by the Company and twenty percent (20%) by M & H. The Company shall pay to M & H their share of any collections promptly after receipt of same and shall, from time to time, provide M & H with copies of any and all invoices related to the shared costs and expenses, proof of payment therefor and invoice for such expenses as they are incurred, which such invoices shall be payable by M & H within twenty (20) days after delivery. In the event M & H shall fail to make any payment due in accordance with the foregoing within ten (10) days after receiving notice concerning a failure to pay any such invoice, they shall forfeit any and all rights to share in collections.

In April 2010, Brookridge incurred a credit loss of approximately $650,000 due to what appears to be a fraud committed by a Brookridge client (hereinafter referred to as a "Sherburne Account" client). Anchor’s interest in this loss is 80% or approximately $520,000. Brookridge financed inventory purchased by this client who sold the inventory for the benefit of another company not funded by Brookridge resulting in the loss of Brookridge’s collateral rights in the inventory. As a result, Brookridge recorded a charge of $650,000 for credit losses in April, 2010. Brookridge is currently pursuing all collection remedies available to it under its purchase order and factoring agreements. The Agreement provides for 80% of any recovery of the credit loss to benefit the Company and the remaining 20% to benefit M & H. As of March 22, 2011, the Company has recouped a total of $177,000 of the $650,000 of credit losses.

Business Overview - Factoring

Our business objective is to create a well-recognized, national financial services firm for small businesses providing accounts receivable funding (factoring), purchase order finance, outsourcing of accounts receivable management including collections and the risk of customer default and other specialty finance products including, but not limited to trade finance and government contract funding. For certain service businesses, Anchor also provides back office support including payroll, payroll tax compliance and invoice processing services. We provide our services to clients nationwide and may expand our services internationally in the future. We plan to achieve our growth objectives as described below through a combination of strategic and add-on acquisitions of other factoring and related specialty finance firms that serve small businesses in the United States and Canada and internal growth through mass media marketing initiatives. Our principal operations are located in Charlotte, North Carolina and we maintain an executive office in Boca Raton, Florida, which includes its sales and marketing functions.

Factoring is the purchase of a company’s accounts receivable, which provide businesses with critical working capital so they can meet their operational costs and obligations while waiting to receive payment from their customers. Factoring services also provide businesses with credit and accounts receivable management services. Typically, these businesses do not have adequate resources to manage internally their credit and accounts receivable functions. Factoring services are typically a non-recourse arrangement whereby the factor takes the entire credit risk if the customer does not pay due to insolvency for any period of time or on a partial non-recourse basis where the factor takes the credit risk for a period of time, which could be 30 to 90 days after the factor purchases an account receivable such that if a client’s customer becomes insolvent during this specific period of time, the factor bears the loss. Under partial non-recourse factoring, after a specific period of time, if the accounts receivable invoice is not collected, the client is required to purchase the accounts receivable invoice back from Anchor. Factoring may also be on a full recourse basis whereby the factor bears no risk of loss if the client’s customer becomes insolvent. We typically advance our clients 75% to 95% of the face value of invoices that we approve in advance on a partial non-recourse or full recourse basis and pay them the difference less our fees when the invoice is collected. For our years ended December 31, 2010 and 2009, our fees for services averaged approximately 2.6% and 3.3%, respectively of the invoice value and are tiered such that the longer it takes us to collect on the accounts receivable invoice, the greater our fee. Since our inception, Anchor has incurred credit losses related to the volume of its invoice purchases totaling approximately $26,000, $252,000 and $41,000 in 2010, 2009 and 2008, respectively. We also offer a factoring product to independent truckers and trucking companies through our transportation funding division, TruckerFunds.com. TruckerFunds.com focuses on buying freight bills from independent, owner operators of trucks and small fleets with less than six trucks. We typically advance our trucking clients 90% to 95% of the invoices that we approve in advance on a non-recourse basis and pay them the difference less our fees when the invoice is collected.

4

A summary of some of the advantages of factoring for a small business is as follows:

|

·

|

Faster application process since factoring is focused on credit worthiness of the accounts receivable as security and not the financial performance of the company;

|

|

·

|

Unlimited funding based on “eligible” and “credit worthy” accounts receivable; and

|

|

·

|

No financial covenants.

|

We offer our services nationwide to any type of business where we can verify and substantiate an accounts receivable invoice for delivery of a product or performance of a service. We believe that this market is under served by banks and other funding institutions that find many of these companies not “bankable” because of their size, limited operating history, thin capitalization, seasonality patterns or poor, inconsistent financial performance. Anchor’s focus is providing funding based on the quality of our clients’ customers’ ability to pay and the validity of the account receivable invoice. Anchor utilizes credit and verification processes to assist in assuring that customers are creditworthy and invoices are valid. We predominantly secure our funding by having a senior first lien on all clients’ accounts receivable and other tangible and intangible assets. At times we enter into Intercreditor agreements with banks or other financial institutions that subordinate the accounts receivable to us so we may purchase them. We also often obtain personal and validity guarantees from our clients’ owners.

Business Overview – Purchase Order Financing

Many businesses have orders from creditworthy companies, but do not have the financial resources to fill the orders by contracting for the manufacturing of the products ordered. Based on these orders which are generally non-cancelable, we pay our clients’ suppliers and manufacturers directly so they may procure their products. This occurs after the products meet certain inspection requirements or specifications. Subsequently the products are shipped to the customer and billed by our client. Once billed, Anchor is typically paid by another lender or factors the invoice and collects payment from the customer. For purchase order financing, Anchor will pay for 100% of the product’s cost. Purchase order finance is often used by importers. For importers, Anchor will provide a letter of credit to an overseas supplier. This letter of credit will be paid after the products meet inspection criteria. Once shipped, Anchor is secured by the value of the products since it has a first lien on all clients’ inventory, accounts receivable and other tangible and intangible assets. Anchor charges a fee which is a percentage of the total amount paid to the supplier or the manufacturer. This fee increases the longer it takes for Anchor to be paid.

5

GROWTH OPPORTUNITIES AND STRATEGIES

Our strategy is to become a nationally recognized brand for accounts receivable and purchase order funding and other related financial services for small businesses. This expansion is expected to be accomplished with media marketing campaigns targeting small businesses and through accretive acquisitions of competitive firms and add-on purchases which broaden our mix of services, brands, customers and geographic and economic diversity. Our focus is to increase revenues and profits, through a combination of internal growth and acquisitions, primarily within our core disciplines and expansion into new service offerings. The key elements to our acquisition growth strategy include the following:

|

·

|

Acquire companies that provide factoring services to small businesses. Our primary strategy is to increase revenues and profitability by acquiring the accounts receivable portfolios and possibly the business development and management teams of other local and regional factoring firms, primarily firms in the United States with revenues of generally less than $10 million. Significant operating leverage and reduced costs are achieved by consolidating back office support functions. Increased revenues across a larger accounts receivable portfolio is anticipated to lead to lower costs of capital, which may enhance profitability. We intend to evaluate acquisitions using numerous criteria including historical financial performance, management strength, service quality, diversification of customer base and operating characteristics. Our senior management team has prior experience in other service industries in identifying and evaluating attractive acquisition targets and integrating acquired businesses.

|

|

·

|

Expand our service offerings by acquiring related specialty finance firms that serve small businesses. These specialty firms will broaden the services that we provide so that we can fulfill additional financial service needs of existing clients and target additional small businesses in different industries.. The following are types of specialty finance firms that we will target and is not all-inclusive:

|

|

o

|

Purchase order and import/export financing;

|

|

o

|

Government contract financing; and

|

|

o

|

Transportation / freight invoice financing

|

|

·

|

Expand our discount factoring business by creating a national factoring brand. Inform and educate small businesses owners that factoring can increase cash flow and outsource credit risk and accounts receivable management. Our experience has been that many small businesses have limited awareness that factoring exists and is a viable financing alternative option for them. We have a marketing strategy that focuses on creating a national factoring brand identity. This is expected to be accomplished through various marketing initiatives and business alliances that will create in-bound sales leads. These marketing strategies include:

|

|

o

|

Media advertising in key metropolitan markets;

|

|

|

Increase our pay-per-click internet advertising which in the past has been a successful strategy for Anchor; and

|

||

|

Radio spot advertising on talk radio and sports oriented programming whose primary demographic are small business owners.

|

||

|

o

|

Establish cross-selling alliances with other small business providers including:

|

|

|

Small business accounting and tax preparation service firms;

|

|

|

Small business service centers, providing packing and shipping; and

|

|

|

Commercial insurance brokers.

|

|

|

o

|

Develop a referral network of business brokers, consultants, accountants and attorneys;

|

|

INDUSTRY OVERVIEW

Factoring as it functions today has been in existence for nearly 200 years. Its historical focus has been in the textile and apparel industries, which provides products to major retailers. The factoring industry has expanded beyond the textile and apparel industries into other mainstream businesses. Anchor may provide funding to businesses where the performance of a service or the delivery of a product can be verified. We have the ability to check a company’s credit and evaluate its ability to pay across most industries. Hence, Anchor’s target prospects are most small businesses.

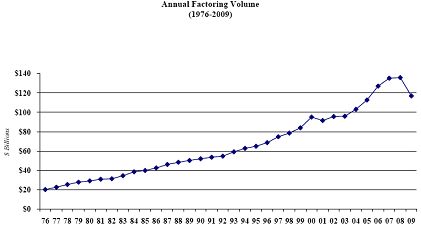

According to the Commercial Finance Association (CFA), an industry trade association for asset based lending and factoring companies, factoring volume (the dollar value of invoices purchased) in 2009 in the United States decreased to $116.6 billion from $136 billion in 2008, representing a 14.2% decrease. The decline is attributable to the economic recession in the United States. Generally, as highlighted in the chart below, except for recession-driven decreases, factoring has sustained a 30 year pattern of growth and there is a greater acceptance of the factoring product. A primary strategy of the Company is to increase revenues and profitability by acquiring the accounts receivable portfolios and possibly the business development and management teams of other local and regional factoring firms by primarily targeting acquisition firms in the United States with revenues of generally less than $10 million. Management of our company is unable to estimate the portion of the $116.6 billion market which consists of companies in our targeted market for acquisition. Nevertheless, Management believes that our targeted market for acquisitions represents a small portion of the overall United States factoring volume.

6

Management estimates, based on examination of Dun & Bradstreet data and a market overview provided by a merger and acquisition advisory firm, that there are approximately 2,900 accounts receivable factoring and financing firms in the United States with over 2,000 firms with revenues of less than $1 million. Management believes that the fragmentation of the market among other factors, make this industry attractive for consolidation. Driving factors for consolidation include:

|

o

|

Limited growth capital for small factors. Small factoring firms may have credit availability constraints limiting the business volume which they can factor. The financial leverage that banks typically provide a finance company is a function of the capital in the business. The opportunity to combine their businesses with Anchor’s capital and possible lower cost of funds, back office support and potentially a larger credit facility are incentives to sell their business, particularly where they would receive our capital stock in return as part or all of the transaction price.

|

|

o

|

Anchor would provide an exit strategy for owners of small factoring firms who may have much of their personal wealth tied to the business and want to retire. A cash sale of a factoring firm would provide liquidity to the owner of a factoring firm and the opportunity to receive a price over the factoring firm’s book value.

|

OPERATIONS

Our executive officers, namely Morry F. Rubin, CEO and Brad Bernstein, President/CFO, manage our day to day operations and internal growth and oversee our growth strategy. Anchor has three account executives, an underwriter, a Controller/Vice President of factoring operations, and one sales person. Our sales person handles in-bound sales calls. Our Controller/Vice President of factoring operations monitors the portfolio (along with the President), oversees credit, maintains our books and records, wires funds daily to clients and provides back office oversight. The underwriter analyzes prospective funding transactions

Underwriting Process

We have developed and utilize standard underwriting procedures, which are controlled in a checklist format that is reviewed and approved by members of the credit committee. The credit committee is presently comprised of our executive officers, although these functions may be delegated to other responsible personnel in the future as our company expands our operations. A member or members of the credit committee approve all new accounts and conduct periodic credit reviews of the client portfolio. Underwriting criteria include the following:

|

o

|

Background and credit checks are performed on the owners.

|

|

o

|

Personal or validity guarantees are sometimes obtained from the owners.

|

7

|

o

|

We “Notify” all accounts that are purchased. Anchor is a notification factor, which means that we notify in writing all accounts purchased that we have purchased the account and payments are to be made to Anchor’s central lockbox. Our client’s invoices also provide Anchor’s lockbox as address for payments. We typically also have a notification statement on our clients’ invoices that indicate we have purchased the account and payment is to be made to Anchor.

|

|

o

|

Initially we attempt to verify most of a new customer’s accounts. Verification includes review of third-party documentation and telephone discussions with the client’s customer so that we may substantiate that invoices are valid and without dispute.

|

|

o

|

We typically evaluate the creditworthiness on accounts with more than a $2,500 balance.

|

|

o

|

Other standard diligence testing includes payroll tax payment verification, company status with state of incorporation, pre and post filing lien searches and review of prior years’ corporate tax returns. For TruckerFunds.com accounts we do not verify payroll tax payments or review prior years’ tax returns.

|

|

o

|

We require that our clients enter into a factoring and security agreement or purchase order finance agreement and file a first senior lien on purchased accounts, and on a case-by-case basis, sometimes on all of our clients’ tangible and intangible assets. For purchase order financings we also have a senior lien on inventory.

|

Credit Management

To efficiently and quickly determine the credit worthiness of an account, we utilize an instant credit checking system that we call Creditguard. Creditguard is an in-house evaluation tool that we have developed, but we do not claim any proprietary rights at this time. Creditguard utilizes a proven credit formula that combines various Dun & Bradstreet credit data elements. This formula and system provide an initial credit limit so that accounts can be approved or rejected quickly. If additional credit is necessary beyond the initial credit limit, we then independently check three vendor references and a bank reference to determine if additional credit can be extended. Collection calls are usually made in advance of their due date to secure a commitment or estimated time to receive payment.

CLIENTS

Our clients are all small businesses that typically range in size from start-up to $30 million in annual sales. We provide our factoring services to any type of business where we can verify and substantiate an accounts receivable invoice for delivery of a product or performance of a service. Examples of current factoring clients include a commercial janitorial company, transportation company, medical staffing firm, and an IT consulting company. We typically provide our purchase order finance services to companies that have non-cancelable orders from credit worthy companies. Examples of current purchase order finance clients include an importer/distributor of after-market auto parts and a distributor of plastics. We target all small businesses to educate and convert them to factoring and purchase order finance. We believe that this small business market is under served by banks and other funding institutions that view many of these companies not “bankable” because of their size, limited operating history, thin capitalization or poor / inconsistent financial performance. Our focus is funding based on the quality of our clients’ customer’s ability to pay and the validity of the accounts receivable invoice or purchase order. Anchor has credit and verification processes to assist in assuring that customers are creditworthy and invoices and purchase orders are valid. We secure our funding by placing a senior first lien on all clients’ accounts receivable, inventory for purchase order finance transactions and other tangible and intangible assets. We also often obtain personal guarantees from our clients’ owners.

SALES AND MARKETING

Our marketing strategies include, without limitation, the following:

|

●

|

Media advertising in key metropolitan markets;

|

|

|

|

Increase our internet advertising which in the past has been a successful strategy for Anchor; and

|

|

|

|

Radio spot advertising on talk radio and sports oriented programming whose primary demographic are small business owners.

|

|

|

●

|

Establish cross-selling alliances with other small business providers including:

|

|

|

|

Small business accounting and tax preparation service firms; and

|

|

●

|

Commercial insurance brokers; and

|

|

●

|

Develop a referral network of business brokers, consultants and accountants and attorneys;

|

In key metropolitan areas, we plan on hiring business development officers to follow up on in-bound sales leads in person and develop additional business by networking with other small business providers including traditional bankers, accountants, lawyers and insurance brokers.

8

MANAGEMENT INFORMATION SYSTEMS

We utilize a factoring industry software program designed to effectively manage and operate a factoring company. This system currently manages multiple functions from purchasing invoices, advancing funds, recording collections and rebating clients. The system generates, on demand, numerous management reports including purchase activity, collections activity, return on capital, advances outstanding, accounts receivable trends, and credit reports which provide us with the ability to track, monitor and control the collateral (purchased accounts receivable). In addition, the software integrates with our general ledger accounting package, which enables us to meet our financial reporting requirements. Our clients can retrieve key on-line management reports and statements.

Purchase order financing transactions are also currently managed through the factoring software.

Our current software platform can support our growth. Hardware redundancy, backup strategies and disaster recovery have been planned to reduce the risk of downtime.

GOVERNMENT REGULATIONS

To Management’s knowledge, factoring receivables and purchase order finance are not regulated industries, as we do not make loans. Nevertheless, if any of the transactions entered into by us are deemed to be loans or financing transactions by a court of law instead of a true purchase of accounts receivable, then various state laws and regulations would become applicable to us and could limit the fees and other charges we are able to charge our customers and may further subject us to any penalties under such state laws and regulations. These laws would also:

|

•

|

regulate credit granting activities, including establishing licensing requirements, if any, in various jurisdictions,

|

|

•

|

require disclosures to customers,

|

|

•

|

govern secured transactions,

|

|

•

|

set collection, foreclosure, repossession and claims handling procedures and other trade practices,

|

|

•

|

prohibit discrimination in the extension of credit, and

|

|

•

|

regulate the use and reporting of information related to a seller’s credit experience and other data collection.

|

This could have a material adverse effect on our business, financial condition, liquidity and results of operations. See “Risk Factors.”

COMPETITION

The factoring and financial service industry is highly fragmented and competitive. Competitive factors vary depending upon financial services products offered, customer, and geographic region. Competitive forces may limit our ability to charge our customary fees and raise fees to our customers in the future. Pressure on our margins is intensive and we cannot assure you that we will be able to successfully compete with our competitors. We are currently an insignificant competitor in our industry, which includes national, regional and local independent and bank owned factoring and finance companies and other full service factoring and financing organizations. Many of these competitors are larger than we are and may have access to capital at a lower cost than we do. Management estimates, based on examination of Dun & Bradstreet data and a market overview provided by a merger and acquisition advisory firm, that there are approximately 2,900 accounts receivable factoring and/or business financing firms in the United States, including us, with over 2,000 with revenues of less than $1 million. To our knowledge, no single firm dominates the small business segment of the industry.

EMPLOYEES

As of March 22, 2011, we have 8 full-time employees.

9

Item 1.A. Risk Factors

You should carefully consider the following risk factors, in addition to the other information presented in this Form 10-K, in evaluating us and our business. Any of the following risks, as well as other risks and uncertainties, could harm our business and financial results and cause the value of our securities to decline, which in turn could cause you to lose all or part of your investment.

Limited operating history. Anchor Funding Services, LLC was formed in 2003. Anchor has only a limited operating history upon which investors may judge our performance. Future operating results will depend upon many factors, including, without limitation our ability to keep credit losses to a minimum, fluctuations in the economy, the degree and nature of competition, demand for our services, and our ability to integrate the operations of acquired businesses, to expand into new markets and to maintain margins in the face of pricing pressures. We can provide no assurances that our operations will result in us meeting our anticipated level of projected profitable operations, if at all.

Competition for customers in our industry is intense, and if we are not able to effectively compete, our financial results could be harmed and the price of our Shares could decline. The factoring and financial service industry is highly competitive. There are many large full-service and specialized financing companies, as well as local and regional companies, which compete with us in the factoring and purchase order financing industry. Competition in our markets is intense. These competitive forces limit our ability to raise fees to our customers. Pressure on our margins is intense, and we cannot assure you that we will be able to successfully compete with our competitors, many of whom have substantially greater resources than we do. If we are not able to effectively compete in our targeted markets, our operating margins and other financial results will be harmed and the market price of our securities could decline.

If we are not able to maintain adequate lines of credit on commercially reasonable terms, our financial condition or results of operations could suffer. We have the availability of a $7 million (expandable to $9 million) senior accounts receivable facility with an institutional asset based lender which advances funds against up to 90% of “eligible net factored accounts receivable” (minus client reserves as lender may establish in good faith) as defined in Anchor’s agreement with its institutional lender. The agreement’s anniversary date is November 30, 2010 and automatically renews each year for an additional year provided that the Company has not provided 60 days notice to the financial institution in advance of the anniversary date. The Company did not provide notice and the agreement will expire November 30, 2011. This facility is secured by our assets, and contains certain standard covenants, representations and warranties for loans of this type. In the event that we fail to comply with the covenant(s) and the lender does not waive such non-compliance, we could be in default of our credit facility, which could subject us to penalty rates of interest and accelerate the maturity of the outstanding balances. The Credit Agreement contains standard representations, warranties and events of default for facilities of this type. Occurrences of an event of default under our credit facility allow the lender to accelerate the payment of the loans and/or terminate the commitments to lend, in addition to other legal remedies, including foreclosure on collateral. In the event we are not able to maintain adequate credit facilities for our factoring, purchase order financing and acquisition needs on commercially reasonable terms, our ability to operate our business and complete one or more acquisitions would be significantly impacted and our financial condition and results of operations could suffer. We can provide no assurances that replacement facilities will be obtained by us on terms satisfactory to us, if at all.

We may acquire companies in the future and these acquisitions could disrupt our business or adversely affect our earnings. Further, we may complete acquisitions without first obtaining stockholder approval under applicable Delaware Law. We intend to acquire small and/or medium local and/or regional factoring and financial service businesses. Our ability to complete acquisitions in the future may be impacted by many factors, including, without limitation, companies available for acquisition and the ability to achieve favorable terms. Entering into an acquisition entails many risks, any of which could harm our business, including, without limitation, failure to successfully integrate the acquired company with our existing business, retention of key employees, alienation or impairment of relationships with substantial customers or key employees of the acquired business or our existing business, and assumption of liabilities of the acquired business. Any acquisition that we consummate also may have an adverse affect on our liquidity or earnings and may be dilutive to our earnings. Adverse business conditions or developments suffered by or associated with any business we acquire additionally could result in impairment to the goodwill or intangible assets associated with the acquired businesses, and a related write down of the value of these assets, and adversely affect our earnings. Further, we may complete acquisitions without first obtaining stockholder approval under applicable Delaware Law.

Risks Associated with our Growth Strategy. Our plans for growth, both internal and through acquisition of other factoring and financial service companies, are subject to numerous and substantial risks. We can provide no assurances that we will be able to expand our market presence in our current locations, successfully enter new markets, add new services and/or integrate acquired businesses into our operations. Our continued growth is dependent upon a number of factors, including the availability of working capital to support such growth, our response to existing and emerging competition, our ability to maintain sufficient profit margins while experiencing pricing pressures, our efforts to develop and maintain customer and employee relationships, and the hiring, training and retention of qualified personnel. We can provide no assurances that we will be able to identify acceptable acquisition candidates on terms favorable to us in a timely manner, if at all. We expect to require additional debt or equity financing for future acquisitions, which additional financing may not be available on terms favorable to the Company, if at all. We can provide no assurances that any acquired business will be profitable.

10

We will seek to make acquisitions that may prove unsuccessful or strain or divert our resources. We intend to seek to expand our business through the acquisition of competitors’ factoring and service businesses and assets. We may not be able to complete any acquisitions on favorable terms, if at all. Acquisitions present risks that could materially and adversely affect our business and financial performance, including:

|

· the diversion of our management's attention from our everyday business activities;

|

|

|

· the contingent and latent risks associated with the past operations of, and other unanticipated problems arising in, the acquired business; and

|

|

· the need to expand management, administration, and operational systems.

|

If we make, or plan to make, such acquisitions we cannot predict whether:

|

· we will be able to successfully integrate the operations and personnel of any new businesses into our business;

|

|

|

· we will realize any anticipated benefits of completed acquisitions;

|

|

· there will be substantial unanticipated costs associated with acquisitions, including potential costs associated with liabilities undiscovered at the time of acquisition; or

|

|

|

· stockholder approval of an acquisition will be sought.

|

In addition, future acquisitions by us may result in:

|

· potentially dilutive issuances of our equity shares;

|

|

|

· the incurrence of additional debt;

|

|

· restructuring charges; and

|

|

|

· the recognition of significant charges for depreciation and amortization related to intangible assets.

|

We purchase accounts receivable primarily from and make purchase order advances to privately owned small companies, which present a greater risk of loss than purchasing accounts receivable from and purchase order advances to larger companies. Our portfolio consists primarily of accounts receivable and purchase order advances from small, privately owned businesses with annual revenues ranging from start-up to $30 million. Compared to larger, publicly owned firms, these companies generally have more limited access to capital and higher funding costs, may be in a weaker financial position and may need more capital to expand or compete. These financial challenges may make it difficult for our clients to continue as a going concern. Accordingly, advances made to these types of clients entail higher risks than advances made to companies who are able to access traditional credit sources. In part because of their smaller size, our clients may:

• experience significant variations in operating results;

• have narrower product lines and market shares than their larger competitors;

• be particularly vulnerable to changes in customer preferences and market conditions;

• be more dependent than larger companies on one or more major customers, the loss of which could materially impair their business, financial condition and prospects;

• face intense competition, including from companies with greater financial, technical, managerial and marketing resources;

• depend on the management talents and efforts of a single individual or a small group of persons for their success, the death, disability or resignation of whom could materially harm the client’s financial condition or prospects;

• have less skilled or experienced management personnel than larger companies; and/or

• do business in regulated industries, such as the healthcare industry, and could be adversely affected by policy or regulatory changes.

11

Accordingly, any of these factors could impair a client’s cash flow or result in other events, such as bankruptcy, which could limit our ability to collect on this client’s purchased accounts receivable or purchase order advances, and may lead to losses in our portfolio and a decrease in our revenues, net income and assets.

We may be adversely affected by deteriorating economic or business conditions. Our business, financial condition and results of operations may be adversely affected by various economic factors, including the level of economic activity in the markets in which we operate. Delinquencies and credit losses generally increase during economic slowdowns or recessions. Because we fund primarily small businesses, many of our clients may be particularly susceptible to economic slowdowns or recessions and could impair a client’s cash flow or result in other events, such as bankruptcy, which could limit our ability to collect on this client’s purchased accounts receivable and purchase order advances, and may lead to losses in our portfolio and a decrease in our revenues, net income and assets. Unfavorable economic conditions may also make it more difficult for us to maintain both our new business origination volume and the credit quality of new business at levels previously attained. Unfavorable economic conditions also could increase our funding costs, limit our access to the capital markets or result in a decision by lenders not to extend credit to us. These events could significantly harm our operating results.

Our limited operating history makes it difficult for us to accurately judge the credit performance of our portfolio and, as a result, increases the risk that our allowance for credit losses may prove inadequate. Our business depends on the creditworthiness of our clients’ customers and our clients. While we conduct due diligence and a review of the creditworthiness of most of our clients’ customers and all of our clients, this review requires the application of significant judgment by our management. Our judgment may not be correct. We maintain an allowance for credit losses on our consolidated financial statements in an amount that reflects our judgment concerning the potential for losses inherent in our portfolio. Management periodically reviews the appropriateness of our allowance considering economic conditions and trends, collateral values and credit quality indicators. We cannot assure you that our estimates and judgment with respect to the appropriateness of our allowance for credit losses are accurate. Our allowance may not be adequate to cover credit losses in our portfolio as a result of unanticipated adverse changes in the economy or events adversely affecting specific clients, industries or markets. If our allowance for credit losses is not adequate, our net income will suffer, and our financial performance and condition could be significantly impaired.

We may not have all of the material information relating to a potential client at the time that we make a credit decision with respect to that potential client or at the time we advance funds to the client. As a result, we may suffer credit losses or make advances that we would not have made if we had all of the material information. There is generally no publicly available information about the privately owned companies to which we generally purchase accounts receivable from. Therefore, we must rely on our clients and the due diligence efforts of our employees to obtain the information that we consider when making our credit decisions. To some extent, our employees depend and rely upon the management of these companies to provide full and accurate disclosure of material information concerning their business, financial condition and prospects. If we do not have access to all of the material information about a particular client’s business, financial condition and prospects, or if a client’s accounting records are poorly maintained or organized, we may not make a fully informed credit decision which may lead, ultimately, to a failure or inability to collect our purchased accounts receivable and purchase order advances in their entirety.

We may make errors in evaluating accurate information reported by our clients and, as a result, we may suffer credit losses. We underwrite our clients and clients’ customers based on certain financial information. Even if clients provide us with full and accurate disclosure of all material information concerning their businesses, we may misinterpret or incorrectly analyze this information. Mistakes by our staff and credit committee may cause us to make purchase order advances and purchase accounts receivable that we otherwise would not have purchased, to fund advances that we otherwise would not have funded or result in credit losses.

Risks Related to Our Financing Activities. In April 2010, our then 80% owned subsidiary suffered a credit loss of approximately $650,000 due to an alleged fraud by one of its clients. We are currently pursuing all legal remedies to recover our losses incurred in connection with such fraud as described under "Item 3." If we were to experience other material losses on our accounts receivable and purchase order portfolio, they could have a material adverse effect on (i) our ability to fund our business and, (ii) to the extent the losses exceed our provision for credit losses, our revenues, net income and assets.

12

A client’s fraud could cause us to suffer material losses. A client could defraud us by, among other things:

|

·

|

directing the proceeds of collections of its accounts receivable to bank accounts other than our established lockboxes;

|

|

·

|

failing to accurately record accounts receivable aging;

|

|

·

|

overstating or falsifying records showing accounts receivable or inventory;

|

|

·

|

providing inaccurate reporting of other financial information;

|

|

·

|

falsifying purchase orders to suppliers and from customers or;

|

|

·

|

stealing inventory that we have purchased.

|

|

|

|

As of December 31, 2010, clients that represent 5% or more of our accounts receivable and purchase order portfolio include a publishing company in Florida that accounts for 18.81%, a food service client in Missouri that accounts for 5.97%, an auto parts supplier in Michigan which accounts for 7.83% and a computer supplier for public school systems that accounts for 5.49%. A client’s fraud could cause us to suffer material losses.

We may be unable to recognize or act upon an operational or financial problem with a client in a timely fashion so as to prevent a credit loss of purchased accounts receivable from that client or purchase order advances to that client. Our clients may experience operational or financial problems that, if not timely addressed by us, could result in a substantial impairment or loss of the value of our purchased accounts receivable or collateral underlying our purchase order advances. We may fail to identify problems because our client did not report them in a timely manner or, even if the client did report the problem, we may fail to address it quickly enough or at all. As a result, we could suffer credit losses, which could have a material adverse effect on our revenues, net income and results of operations.

The security interest that we have in our clients’ assets may not be sufficient to protect us from a partial or complete loss if we are required to foreclose. While we are secured by a lien on specified collateral of the client, there is no assurance that the collateral will protect us from suffering a partial or complete loss if we move to foreclose on the collateral. The collateral is primarily the purchased accounts receivable for factoring transactions and inventory for purchase order transactions. Factors that could reduce the value of the collateral that we have a security interest in include among other things:

|

•

|

problems with the client’s underlying product or services which result in greater than anticipated returns or disputed accounts;

|

|

|

•

|

unrecorded liabilities such as rebates, warranties or offsets;

|

|

•

|

the disruption or bankruptcy of key customers who are responsible for material amounts of the accounts receivable; and

|

|

|

• the client misrepresents, or does not keep adequate records of, important information concerning the accounts receivable.

|

||

Any one or more of the preceding factors could materially impair our ability to collect purchase order advances and all of the accounts receivable we may purchase from a client.

Errors by or dishonesty of our employees could result in credit losses. We rely heavily on the performance and integrity of our employees in making our initial credit decision with respect to our clients and on-going credit decisions on our clients’ customers. Because there is generally little or no publicly available information about our clients or clients’ customers, we cannot independently confirm or verify the information our employees provide us for use in making our credit and funding decisions. Errors by our employees in assembling, analyzing or recording information concerning our clients and clients’ customers could cause us to fund clients and purchase accounts receivable that we would not otherwise fund or purchase. This could result in losses. Losses could also arise if any of our employees were dishonest. A dishonest employee could collude with our clients to misrepresent the creditworthiness of a prospective client or client customers or to provide inaccurate reports or invoices. If, based on an employee’s dishonesty, we may have funded a client and purchased accounts that were not creditworthy, this could result in our suffering credit losses.

We may incur lender liability as a result of our funding activities. A number of judicial decisions have upheld the right of borrowers to sue lending institutions on the basis of various evolving legal theories, collectively termed “lender liability.” Generally, lender liability is founded on the premise that a lender has either violated a duty, whether implied or contractual, of good faith and fair dealing owed to the borrower or has assumed a degree of control over the borrower resulting in the creation of a fiduciary duty owed to the borrower or its other creditors or shareholders. We may be subject to allegations of lender liability if it were determined that our advances were in fact loans and the relationship between Anchor and a client was that of lender and borrower rather than purchaser and seller. We cannot assure you that these claims will not arise or that we will not be subject to significant liability if a claim of this type did arise.

We may incur liability under state usury laws or other state laws and regulations if any of our funding arrangements are deemed to be loans or financing transactions instead of a true purchase of accounts receivable. Various state laws and regulations limit the interest rates, fees and other charges lenders are allowed to charge their borrowers. If any of the factoring transactions entered into by us are deemed to be loans or financing transactions instead of a true purchase of accounts receivable, such laws and regulations may become applicable to us and could limit the interest rates, fees and other charges we are able to charge our customers and may further subject us to any penalties under such state laws and regulations. This could have a material adverse effect on our business, financial condition, liquidity and results of operations.

13

We are in a highly competitive business and may not be able to take advantage of attractive funding opportunities. The factoring and purchase order finance industries are highly competitive. We have competitors who offer the same types of services to small privately owned businesses that are our target clients. Our competitors include a variety of:

|

•

|

specialty and commercial finance companies; and

|

|

|

•

|

national and regional banks that have factoring and purchase order divisions or subsidiaries.

|

Some of our competitors have greater financial, technical, marketing and other resources than we do. They also have greater access to capital than we do and at a lower cost than is available to us. Furthermore, we would expect to face increased price competition if other factors seek to expand within or enter our target markets. Increased competition could cause us to reduce our pricing and advance greater amounts as a percentage of a client’s eligible accounts receivable. Even with these changes, in an increasingly competitive market, we may not be able to attract and retain new clients. If we cannot engage new clients, our net income could suffer, and our financial performance and condition could be significantly impaired.

Our information and computer processing systems are critical to the operations of our business and any failure could cause significant problems. Our information technology systems, located at our Charlotte, North Carolina headquarters, are essential for data exchange and operational communications to service our clients. Any interruption, impairment or loss of data integrity or malfunction of these systems could severely hamper our business and could require that we commit significant additional capital and management resources to rectify the problem.

The loss of any of our key personnel could harm our business. Our future financial performance will depend to a significant extent on our ability to motivate and retain key management personnel. Competition for qualified management personnel is intense and in the event we experience turnover in our senior management positions, we cannot assure you that we will be able to recruit suitable replacements. We must also successfully integrate all new management and other key positions within our organization to achieve our operating objectives. Even if we are successful, turnover in key management positions may temporarily harm our financial performance and results of operations until new management becomes familiar with our business. At present, we do not maintain key-man life insurance on any of our executive officers, although we entered into employment contracts with each of Morry F. Rubin, Chief Executive Officer, and Brad Bernstein, President. Our Board of Directors is responsible for approval of all future employment contracts with our executive officers. We can provide no assurances that said future employment contracts and/or their current compensation is or will be on commercially reasonable terms to us in order to retain our key personnel. The loss of any of our key personnel could harm our business.

Lack of Committees. Currently we have no audit, compensation, nominating or other committees of the board. In the future, we may establish committees at such time as the board deems it to be in the best interest of our stockholders. We can provide no assurances that our lack of committees will not continue in future operating periods. Since we have no audit committee composed solely of independent directors, as required by the Sarbanes-Oxley Act of 2002, as amended, our board of directors has all the responsibilities of the audit committee.

Risks associated with intangible assets. A substantial portion of our future assets may consist of intangible assets including goodwill (excess of cost over fair value of net assets acquired and other intangible assets) relating to the potential acquisition of businesses. In the event of any sale or liquidation of us, there can be no assurance that the value of such intangible assets will be realized. In addition, any significant decrease in the value of such intangible assets could have a material adverse effect on us.

We are continually subject to the risk of new regulation, which could harm our business and/or operating results. Congress and/or various state legislatures may pass new regulations governing the financial services industry. The enactment of any such new laws or regulations may negatively impact our business, financial condition and/or our financial results.

Control of the Company. Our executive officers, directors and principal stockholders beneficially own more than 50% of the voting control of our capital stock. As a result, such persons, in the event that they act in concert, will have the ability to affect the election of all of our directors and the outcome of all issues submitted to our stockholders. Such concentration of ownership could limit the price that certain investors might be willing to pay in the future for shares of Common Stock, and could have the effect of making it more difficult for a third party to acquire, or of discouraging a third party from attempting to acquire, control of us. See “Item 12.”

Risks associated with the development of the Company’s management information and internal control systems. Our data processing, accounting and analysis capabilities are important components of our business. As we make acquisitions, we will convert certain systems of the acquired companies to our systems. These conversions and the continued development and installation of such systems involve the risk of unanticipated complications and expenses. We can provide no assurances that we will be successful in this regard.

We have no established public market for our Securities. Our outstanding Common Stock and Series 1 Convertible Preferred Stock (collectively the “Securities”) do not have an established trading market in the Over-the-Counter Market or on the OTC Bulletin Board, although our Common Stock has been quoted on the OTC Bulletin Board under the symbol “AFNG.” Trading in our Common Stock has been sporadic since it began in December 2007. The availability for sale of restricted securities pursuant to Rule 144 or otherwise could adversely affect the market for our Common Stock, if any. We can provide no assurances that an established public market will ever develop or be sustained for our common stock in the future. Further, we do not anticipate a public market will ever develop for our Series 1 Convertible Preferred Stock.

The price of our Common Stock may fluctuate significantly. The market price for our Common Stock, if any, can fluctuate as a result of a variety of factors, including the factors listed above, many of which are beyond our control. These factors include: actual or anticipated variations in quarterly operating results; announcements of new services by our competitors or us; announcements relating to strategic relationships or acquisitions; changes in financial estimates or other statements by securities analysts; and other changes in general economic conditions. Because of this, we may fail to meet or exceed the expectations of our shareholders or others, and the market price for our Common Stock could fluctuate as a result.

Our Common Stock is considered to be a “penny stock” and, as such, the market for our Common Stock, should one develop, may be further limited by certain Commission rules applicable to penny stocks. To the extent the price of our Common Stock remains below $5.00 per share or we have a net tangible assets of $2,000,000 or less, our common shares will be subject to certain “penny stock” rules promulgated by the Securities and Exchange Commission. Those rules impose certain sales practice requirements on brokers who sell penny stock to persons other than established customers and accredited investors (generally institutions with assets in excess of $5,000,000 or individuals with net worth in excess of $1,000,000). For transactions covered by the penny stock rules, the broker must make a special suitability determination for the purchaser and receive the purchaser’s written consent to the transaction prior to the sale. Furthermore, the penny stock rules generally require, among other things, that brokers engaged in secondary trading of penny stocks provide customers with written disclosure documents, monthly statements of the market value of penny stocks, disclosure of the bid and asked prices and disclosure of the compensation to the brokerage firm and disclosure of the sales person working for the brokerage firm. These rules and regulations adversely affect the ability of brokers to sell our common shares in the public market should one develop and they limit the liquidity of our Shares.

An investment in the Company is subject to dilution. We may require substantial additional financing in order to achieve our business objectives. The Company may generate such financing through the sale of securities (including potentially to the owners of businesses we acquire) that would dilute the ownership of its existing security holders. In subsequent rounds of financing, the Company will likely issue securities that will have rights, preferences or privileges senior to our outstanding securities and that will include financial and other covenants that will restrict the Company’s flexibility.

We have never declared or paid cash dividends on our common stock and we do not anticipate paying any cash dividends on our common stock in the foreseeable future. We have never declared or paid cash dividends on our common stock and we do not anticipate paying any cash dividends on our common stock in the foreseeable future. We currently intend to retain future earnings, if any, to fund the development and growth of our business. Any future determination to pay cash dividends will be dependent upon our financial condition, operating results, capital requirements, applicable contractual restrictions and other such factors as our Board of Directors may deem relevant.

14

THE FOREGOING RISK FACTORS DO NOT PURPORT TO BE A COMPLETE EXPLANATION OF THE RISKS INHERENT IN AN INVESTMENT IN THE COMPANY.

Item 2. Description of Property

The Company has lease agreements for office space in Charlotte, NC and Boca Raton, FL. All lease agreements are with unrelated parties.

The Charlotte lease is effective on August 15, 2007, is for a twenty-four month term and includes an option to renew for an additional three year term at substantially the same terms. On November 1, 2007, the Company entered into a lease for additional space adjoining its Charlotte office. Both leases expire May 31, 2011 and the company plans to renew for another year. The monthly rent for the combined space is approximately $2,340.

The Boca Raton lease was effective on August 20, 2007 and is for a sixty-one month term. The monthly rental was approximately $8,300. Pursuant to an agreement dated as of October 16, 2009, Anchor entered into an agreement to terminate its lease covering premises currently known as 800 Yamato Road, Suite 102, Boca Raton, FL 33431. The lease agreement which was entered into on April 16, 2007 and would have expired on May 31, 2012 terminated on October 31, 2009 and Anchor vacated the premises. Anchor bought out the lease at a total cost of $100,000 in order to reduce net leasing costs of an estimated $8,300 per month or approximately $100,000 per annum.

Beginning November 1, 2009, the company entered into a 24 month lease for office space in Boca Raton, FL. The monthly rental is approximately $1,313.

|

|

Item 3. Legal Proceedings

|

We are not a party to any pending material legal proceedings except as described below. To our knowledge, no governmental authority is contemplating commencing a legal proceeding in which we would be named as a party.

In April 2010, Brookridge incurred a credit loss of approximately $650,000 due to what appears to be a fraud committed by a Brookridge client (hereinafter referred to as a "Sherburne Account" client). Anchor’s interest in this loss is 80% or approximately $520,000 and is included in discontinued operations. Brookridge financed inventory purchased by this client who sold the inventory for the benefit of another company not funded by Brookridge resulting in the loss of Brookridge’s collateral rights in the inventory. As a result, Brookridge recorded a charge of $650,000 for credit losses in April, 2010. As of March 22, 2011, the Company has recouped a total of $177,000 of the $650,000 of credit losses. Anchor is currently pursuing all collection remedies and on October 22, 2010 filed a complaint in the Superior Court of Stamford/Norwalk, Connecticut against the Administrators of the Estate of David Harvey (“Harvey”). Harvey was the owner of Sherburne and the Company is pursuing its rights under the personal guarantee that Harvey provided. The Complaint is demanding principal of approximately $485,000 plus interest and damages.

Item 4. Reserved.

15

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is quoted on the OTC Electronic Bulletin Board under the symbol “AFNG.” The following table sets forth the range of high and low closing sale prices of our Common Stock for our last three fiscal periods.

|

Quarters Ended

|

High

|

Low

|

||||||

|

March 31, 2008

|

$ | 1.15 | $ | 1.15 | ||||

|

June 30, 2008

|

$ | 1.15 | $ | 1.05 | ||||

|

September 30, 2008

|

$ | 1.05 | $ | 1.05 | ||||

|

December 31, 2008

|

$ | 1.05 | $ | 0.60 | ||||

|

March 31, 2009

|

$ | 0.90 | $ | 0.10 | ||||

|

June 30, 2009

|

$ | 1.25 | $ | 0.60 | ||||

|

September 30, 2009

|

$ | 1.25 | $ | 0.15 | ||||

|

December 31, 2009

|

$ | 1.05 | $ | 0.30 | ||||

|

March 31, 2010

|

$ | 0.83 | $ | 0.28 | ||||

|

June 30, 2010

|

$ | 0.50 | $ | 0.35 | ||||

|

September 30, 2010

|

$ | 0.75 | $ | 0.50 | ||||

|

December 31, 2010

|

NT(1)

|

NT(1)

|

||||||

(1)NT - No Trades

All quotations reflect inter-dealer prices, without retail mark-up, markdown or commissions, and may not necessarily represent actual transactions.

As of December 31, 2010, there were 18,634,369 shares of Common Stock issued and outstanding. As of December 31, 2010, there were (i) outstanding options to purchase 2,440,000 shares of our Common Stock, (ii) outstanding Placement Agent Warrants to purchase 1,342,500 shares of our Common Stock, and (iii) outstanding 376,387 shares of our Series 1 Preferred Stock which are convertible into 1,881,935 shares of our Common Stock.

In January 2007, we had an initial float of 525,555 shares which were issued as free trading shares by the Bankruptcy Court under Section 1145(a)(1) of the Bankruptcy Code. Since then, our remaining outstanding equity securities have become eligible for sale pursuant to the requirements of Rule 144 of the Securities Act of 1933, as amended. In this respect, shares of our common stock beneficially owned by a person for at least six months (as defined in Rule 144) are eligible for resale under Rule 144 subject to the availability of current public information about us and, in the case of affiliated persons, subject to certain additional volume limitations, manner of sale provisions and notice provisions. Pursuant to Rule 144(b)(1) of the Securities Act, our non-affiliates (who have been non-affiliates for at least three months) may sell their common stock that they have held for one year (as defined in Rule 144) without compliance with the availability of current information.

Holders of Record

As of February 14, 2011, there were 581 holders of record of shares of Common Stock and 68 holders of record of our Series 1 Preferred Stock. The Company's Transfer Agent is Continental Stock Transfer & Trust Company, 17 Battery Place, New York, NY 10004.

Dividend Policy

The holders of our Series 1 Preferred Stock were entitled to receive dividends from issuance in 2007 through December 31, 2009 as more fully described below. We have not paid or declared any cash dividends on our Common Stock. We currently intend to retain any earnings for future growth and, therefore, do not expect to pay cash dividends on our Common Stock in the foreseeable future.