Attached files

| file | filename |

|---|---|

| EX-3.1.1 - CERT AMENDMENT - Neonode Inc. | f10k2010ex3i_neonode.htm |

| EX-10.19 - NOTE - Neonode Inc. | f10k2010ex10xix_neonode.htm |

| EX-10.17 - EMPLOYMENT AGREEMENT - Neonode Inc. | f10k2010ex10xvii_neonode.htm |

| EX-10.18 - LOAN AGREEMENT - Neonode Inc. | f10k2010ex10xviii_neonode.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO USC 18 SECTION 1350 - Neonode Inc. | f10k2010ex32i_neonode.htm |

| EX-31.1 - CERTIFICATION OF PEO - Neonode Inc. | f10k2010ex31i_neonode.htm |

| EX-23.1 - ACCOUNTANTS CONSENT - Neonode Inc. | f10k2010ex23i_neonode.htm |

| EX-10.20 - WARRANT - Neonode Inc. | f10k2010ex10xx_neonode.htm |

| EX-31.2 - CERTIFICATION OF PFO - Neonode Inc. | f10k2010ex31ii_neonode.htm |

| EX-21.1 - SUBSIDARIES OF THE REGISTRANT - Neonode Inc. | f10k2010ex21_neonode.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2010

|

|

|

or

|

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from ________ to _________

|

|

Commission File No. 0-8419

NEONODE INC.

(Exact name of Registrant as specified in its charter)

|

Delaware

|

94-1517641

|

|

(State or Other Jurisdiction of

|

(I.R.S. Employer

|

|

Incorporation or Organization)

|

Identification Number)

|

Sweden Linnegatan 89, SE-115 23 Stockholm, Sweden

USA 651 Byrdee Way, Lafayette, CA 94549

(Address of principal executive offices and Zip Code)

Sweden + 46 8 667 17 17

USA + 1 925 768 0620

(Registrant's Telephone Numbers, including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

Common Stock, par value $0.001 per share

|

NONE

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

|

Non-accelerated filer ¨

|

Smaller reporting company ý

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act. Yes ¨ No ý

The approximate aggregate market value of the common stock held by non-affiliates of the registrant, based on the closing price for the registrant’s common stock on June 30, 2010 (the last business day of the second quarter of the registrant’s current fiscal year) as reported on the OTC BB, was $8,199,674.

The number of shares of the registrant’s common stock outstanding as of March 31, 2011 was 27,279,672.

The number of shares of the registrant’s Series A Preferred stock outstanding as of March 31, 2011 was 83.

The number of shares of the registrant’s Series B Preferred stock outstanding as of March 31, 2011 was 101.

Neonode Inc. affected a 25-to-1 reverse stock split on the opening of business on March 28, 2011. All per share amounts and calculations in this Annual Report and the accompanying consolidated financial statements have been calculated to reflect the effects of the reverse stock split.

DOCUMENTS INCORPORATED BY REFERENCE

Exhibits incorporated by reference are referred to in Part IV.

2

NEONODE INC.

2010 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

PART I

|

|||

| 4 | |||

| 13 | |||

| 18 | |||

| 18 | |||

| 18 | |||

| 19 | |||

|

PART II

|

|||

| 19 | |||

| 19 | |||

| 19 | |||

| 32 | |||

| 33 | |||

| 73 | |||

| 73 | |||

| 74 | |||

|

PART III

|

|||

| 75 | |||

| 80 | |||

| 85 | |||

| 87 | |||

| 89 | |||

|

PART IV

|

|||

| 90 | |||

| 92 | |||

3

SPECIAL NOTE ON FORWARD LOOKING STATEMENTS

Certain statements set forth in or incorporated by reference in this Annual Report on Form 10-K constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements include, without limitation, our expectations regarding the adequacy of anticipated sources of cash, planned capital expenditures, the effect of interest rate increases, and trends or expectations regarding our operations. Words such as “may,” “will,” “should,” “believes,” “anticipates,” “expects,” “intends,” ”plans,” “estimates” and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements. Such statements are based on currently available operating, financial and competitive information and are subject to various risks and uncertainties. Readers are cautioned that the forward-looking statements reflect management’s estimates only as of the date hereof, and we assume no obligation to update these statements, even if new information becomes available or other events occur in the future. Actual future results, events and trends may differ materially from those expressed in or implied by such statements depending on a variety of factors, including, but not limited to those set forth under “Item 1A Risk Factors” and elsewhere in this Annual Report on Form 10-K.

PART I

|

BUSINESS

|

We provide optical infrared touchscreen solutions for handheld and small to midsized consumer and industrial electronic devices. We license our touchscreen technology to Original Equipment Manufacturers (“OEMs”) and Original Design Manufacturers (“ODMs”) who imbed our touchscreen technology into electronic devices that they develop and sell. The cornerstone of our solution is our innovative optical infrared touchscreen technology, zForce®. Our patented zForce® technology offers a number of benefits compared to other touch screen technologies currently on the market. Our optical infrared technology offers clients lower cost and more functional alternatives to other touch screen technologies. zForce® also consumes less power than our competitor's solutions, is able to function in a wide temperature range, requires no screen overlay and thus offers a much clearer picture while at the same time accommodating multi-touch functionality. zForce® combines full finger touch and high resolution pen support in the same solution.

Our technology licensing model allows us to focus on the development of solutions for multi-touch enabled screens and thus we do not have to contend with the financial and logistical burden of manufacturing products, which is handled by our ODM/OEM clients. We license the right to use zForce® and software which, together with standard components from partners, creates a complete optical touch screen solution. The zForce® multi-touch product is our latest release and is currently being integrated into products such as mobile phones, mobile internet devices, eReaders, digital picture frames, printers, GPS devices and tablet PC’s. It should be noted that our licensing model provides the added benefit of allowing us to grow sales exponentially without the need of increasing costs at anywhere near the same rate to support the sales growth.

Markets

We provide touch screen solutions for navigation for many of the world’s premier eReader OEMs. Our patented touch screen technology, zForce®, supports high resolution pen writing in combination with finger navigation including gestures, multi-touch, sweeps and much more. Unlike resistive and capacitive touch screens, zForce® touch screens have no overlay on top of the display window and provide a 100% clear viewing experience, free from reflection and parallax effects that is required for eReader touch screens. Neonode’s touch solution for portable devices is many times more cost effective than any other high performance touch solution in the market today, and we believe it is the only viable touch screen solution that will operate on the new revolutionary reflective display panels that will offer paper-like reading experience in almost any ambient lighting condition while greatly reducing power consumption. We believe that reflective display panels will be the future display panels of choice for all eReader, tablet PC, GPS devices and many mobile phone and other hand held devices.

4

Industry projections, by the Yankee Group published on February 8, 2011, project that the number of eReaders sold will increase from the estimated 11 million eReaders sold in 2010 to a projected 72 million eReaders in 2014, reflecting the continued migration of paper book sales to electronic books. Based on the strength of our technology and engineering know-how, we believe we are well positioned to take advantage of the growth opportunity in the eReader market and to provide innovative, value-added human interface solutions for each of the key end-user preferences. We believe that the end-user reading experience will be enhanced by the adoption of reflective display panels, including additional functionality, such as multi-touch gesture recognition. We believe we are well positioned within the eReader market as our zForce® product line allows us to address the entire eReader market.

In addition, we believe our intellectual property portfolio, engineering know-how, technological expertise and experience in providing touch screen solutions to major OEMs of portable electronic devices position us to be a key technological enabler for multiple consumer electronic devices including tablet PCs, mobile phones, digital picture frames, remote controls, and global positioning devices, as well as a variety of other mobile, handheld, wireless, and entertainment devices. We believe our existing technologies with our emphasis on low cost, ease of use, small size, low power consumption, advanced functionality, durability, and reliability enable us to serve multiple aspects of the markets for these products, as well as for other electronic devices.

We anticipate that our touch screen solutions for low-cost high-volume mobile phones will constitute an important percentage of our future net revenue. Our ongoing success in serving the low-cost high-volume mobile phone market will depend upon a number of factors, including: (i) the continued growth of the overall mobile phone market, (ii) the utilization of high-functionality interactive infrared touchscreens rather than mechanical buttons or capacitive/resistive touchscreens, as the interface for application access and control in those products, and (iii) our ability to demonstrate to mobile phone OEMs the advantages of our touch screen solutions in terms of price, performance, usability, size, durability, power consumption, and industrial design possibilities.

Industry projections for the low-cost mobile phone market for the period from 2011 through 2013 predict a compound annual growth rate of 21%, which reflects the trend towards greater functionality in low-cost mobile phone products to meet and address the expanded needs and expectations of the consumer-oriented market. These products require a low-cost, simple, durable, and intuitive touch screen solution to enable the user to navigate efficiently through menus and scroll through information contained in the host device. We believe we are well positioned to take advantage of this growing market based on our technology, engineering know-how, and the acceptance of our touchscreen solutions by OEMs in this market.

Our History

Neonode Inc. (the “Company”), formerly known as SBE, Inc., was incorporated in the State of Delaware on September 4, 1997.

On August 10, 2007, SBE, Inc. consummated a reverse merger transaction with Neonode Inc. (the “Merger”), and SBE, Inc.’s name was subsequently changed to “Neonode Inc.” on the completion of the Merger. Prior to the Merger, Neonode Inc. had been incorporated in the State of Delaware in 2006 and was the parent of Neonode AB, a company founded in February 2004 and incorporated in Sweden. Following the closing of the Merger, the business and operations of Neonode Inc. prior to the Merger became the primary business and operations of the newly-combined company. The newly-combined company’s headquarters is located in Stockholm, Sweden.

Through our previously wholly-owned subsidiary, Neonode AB, we developed our touchscreen technology and an optical touchscreen mobile phone product, the N2. We began shipping the N2 to our first customers in July 2007 but faced difficult circumstances in finding a viable market for our N2 mobile phone and subsequently discontinued the manufacturing of mobile phones and the operations of Neonode AB.

5

2008 Corporate Restructuring

In 2008, as a result of our inability to sell a sufficient number of mobile phones to support our operations, we took the following actions to restructure and refinance the Company:

|

●

|

On December 9, 2008, Neonode AB filed a petition for bankruptcy in compliance with the Swedish Bankruptcy Act (1987:672). As of that date, Neonode AB ceased to be owned and operated by Neonode Inc., and Neonode Inc. ceased to have any financial obligations related to the accounts payable or other debts of Neonode AB.

|

|

●

|

On December 29, 2008, we entered into a Share Exchange Agreement with Neonode Technologies AB (f/k/a AB Cypressen AB nr 9683), a Swedish engineering company, and the stockholders of Neonode Technologies AB: Iwo Jima SARL, Wirelesstoys Sweden AB, and Athemis Ltd., pursuant to which we agreed to acquire all of the issued and outstanding shares of Neonode Technologies AB in exchange for the issuance of shares of Company’s Series A Preferred Stock to the Neonode Technologies AB stockholders. Upon the closing of the transaction, Neonode Technologies AB became a wholly-owned subsidiary of the Company. The Neonode Technologies AB stockholders were employees of the Company and/or Neonode AB and, as such were related parties. The acquisition of Neonode Technologies AB by Neonode Inc. did not qualify as a business combination, and accordingly the fair value of the shares of Series A Preferred Stock issued to the sellers of Neonode Technologies AB shares were accounted for as compensation. As there was an 18 month service requirement related to the Neonode Inc. shares issued to the Neonode Technologies AB shareholders, the value of the Series A Preferred Stock was amortized to compensation expense over the 18 month service period beginning January 1, 2009.

|

|

●

|

On December 30, 2008, we entered into a restructuring transaction in which we converted the majority of the outstanding warrants and convertible debt that had been issued in previous financing transactions to shares of Series A and B Preferred Stock, respectively, that were convertible into shares of our common stock in accordance with the Company’s Certificate of Designation filed with the Delaware Secretary of State.

|

2009 Corporate Financing

|

●

|

During the period from August 25, 2009 through December 31, 2009, we completed a private placement of convertible notes totaling $987,000 that can be converted, at the holder’s option, into 1,973,966 shares of our Common Stock at a conversion price of $0.50 per share. The convertible note holders have the right to have the conversion price adjusted to equal the lower stock price if we issue stock or convertible notes at a lower conversion price than $0.50 during the period that the notes are outstanding. These convertible notes were originally due on December 31, 2010, but the due date has been extended until June 30, 2011. They bear an annual interest rate of 7%, payable on June 30 and December 31 of each year that the convertible notes are outstanding. In addition, we issued 986,983 three-year warrants to the convertible note holders with an exercise price of $1.00 per share. The warrants may be exercised and converted to Common Stock, at the warrant holder’s option, beginning on the six-month anniversary date of issuance until the warrant expiration date. We are not obligated to register the Common Stock related to the convertible debt or the warrants.

|

2010 Corporate Financing

|

●

|

During the period from January 1, 2010 through May 20, 2010, we received $1.8 million in proceeds related to a private placement of convertible notes and stock purchase warrants that can be converted, at the holder’s option, into 3,518,287 shares of our Common Stock at a conversion price of $0.50 per share and 1,760,711 stock purchase warrants that have an exercise price of $1.00 per share. The convertible note holders have the right to have the conversion price adjusted to equal the lower stock price if we issue stock or convertible notes at a lower conversion price than $0.50 during the period that the notes are outstanding. These convertible notes were originally due on December 31, 2010, but the due date has been extended until June 30, 2011. They bear an annual interest rate of 7%, payable on June 30 and December 31 of each year that the convertible notes are outstanding. The warrants may be exercised and converted to Common Stock, at the warrant holder’s option, beginning on the six month anniversary date of the issuance until the warrant expiration date. We are not obligated to register the Common Stock related to the convertible debt or the warrants.

|

6

|

●

|

During September and October 2010, we entered into two different types of amendments with the holders of the convertible notes and the holders of the stock purchase warrants issued in the Fall 2009 and Spring 2010 financing transactions. All of the holders of the convertible notes entered into an amendment pursuant to which the due date of the convertible notes was extended until June 30, 2011. A majority of the holders of the stock purchase warrants entered into an amendment pursuant to which they exercised their previously granted warrants at a discounted exercise price of $0.88 per share and was granted a replacement three-year warrant for each original warrant exercised. When exercised, the replacement warrants can be converted into 2,766,856 shares of our common stock at an exercise price of $1.38 per share. A total of 2,766,856 warrants were exercised at the discounted exercise price of $0.88 per share, and a total of $2.4 million was raised by the Company through these warrant exercises. We issued a total of 2,766,856 shares of common stock and replacement warrants to the exercising warrant holders.

|

Technologies

Our touchscreen solutions are based on our patented zForce® and Neno™ hardware and software technology. zForce® is our optical infrared touchscreen technology that supports one-handed navigation, allowing the user to operate the functionality with finger gestures passing over the screen. Neno™ is our software-based user interface.

zForce® has been patented in several countries including the US and has several patents-pending in the US. It uses infrared light that is projected as a grid over the screen. The infrared light pulses a full screen up to 120 times a second so that the grid is constantly being refreshed. Coordinates are produced on the screen and are then converted into mathematical algorithms when a user's fingers move across the screen. This input method is unique to Neonode and is enabled by the zForce® technology.

Currently, there are two dominant types of touchscreen technologies available in the market - capacitive and resistive. Capacitive technology is the technology that the Apple iPhone uses and resistive technology is what is found on most stylus-based PDAs. Resistive technology is pressure sensitive technology. Best used for detailed work and for selection of a particular spot on a screen, resistive technology is not useful for sweeping gestures or motion, such as zooming in and out. Capacitive technology, which is used on a laptop computer mouse pad, is very good for sweeping gestures and motion. The screen actually reacts to the finger’s tiny electric impulses. Capacitive touchscreens work best if the user has unimpeded contact between his finger and the screen.

Our zForce® optical touchscreen technology has a number of key advantages over each of these technologies, including:

|

●

|

No additional layers are added to the screen that may dilute the screen contrast and clarity. Layering technology is required to activate the capacitive and resistive technologies and can be very costly;

|

|

|

●

|

The zForce® grid technology is more responsive than the capacitive screen technology and, as a result, is quicker and less prone to misreads. It allows movement and sweeping motions as compared to point-sensitive, stylus-based resistive screens;

|

|

|

●

|

zForce®, an abbreviation for zero force necessary, obviates the need to use any force to select or move items on the screen as would be the case with a stylus;

|

|

|

●

|

zForce® is cost-efficient due to the lower cost of materials and extremely simple manufacturing process when compared to the expensive layered capacitive and resistive screens;

|

7

|

●

|

zForce® allows multiple methods of input, such as simple finger taps to hit keys, sweeps to zoom in or out, and gestures to write text or symbols directly on the screen;

|

|

|

●

|

zForce® is one of the few viable touch screen solution that will operate on well on the new revolutionary reflective display panels that will offer paper-like reading experience in almost any ambient lighting condition while greatly reducing power consumption. Manufacturers of reflective display panels are targeting eReader, mobile phone and tablet PC markets because these devices require the clear viewing screen and low power consumption of the reflective display panels; and

|

|

|

●

|

zForce® incorporates some of the best functionalities of both the capacitive and resistive touch screen technologies. It works in all climates and, unlike the competing technologies, can be used with thick gloves. In addition, zForce® allows for waterproofing of the device.

|

Because of its uniqueness and flexibility, we believe that our zForce® technology presents a tremendous licensing opportunity for Neonode. The market is vast, given the current rapid increase in touchscreen-based devices such as eReaders, mobile phones, Tablet PCs, media players, printers and GPS navigation devices.

Intellectual Property

We believe that innovation in product engineering, sales, marketing, support, and customer relations, and protection of this proprietary technology and knowledge, will impact our future success. In addition to certain patents that are pending, we rely on a combination of copyright, trademark, trade secret laws and contractual provisions to establish and protect the proprietary rights in our products.

We have been issued patent protection of our invention named “On a substrate formed or resting display arrangement” in five countries, including the US and through a Patent Cooperation Treaty (“PCT”) application and in 24 designated countries through an application to the European Patent Office (“EPO”). We applied for a patent in Sweden relating to a mobile phone and have also applied for a patent in the United States regarding software named “User Interface.” We have 17 other patent applications pending in the US.

We have been granted trademark protection for the word NEONODE in the European Union (“EU”), Sweden, Norway, and Australia. In addition, we have been granted protection for the figurative mark NEONODE in Sweden. Additional applications for the figurative trademark are still pending in Switzerland, China, Russia, and the United States. In addition, our touch screen technology name zForce® is now an official trademark registered by the US Patent and Trademark Office.

Our “User Interface” may also be protected by copyright laws in most countries, including Sweden and the EU (which do not grant patent protection for the software itself), if the software is new and original. Protection can be claimed from the date of creation.

Consistent with our efforts to maintain the confidentiality and ownership of our trade secrets and other confidential information, and to protect and build our intellectual property rights, we require our employees and consultants, and certain customers, manufacturers, suppliers and other persons with whom we do business or may potentially do business, to execute confidentiality and invention assignment agreements upon commencement of a relationship with us, typically extending for a period of time beyond termination of the relationship.

Distribution, Sales and Marketing

We consider both OEMs and ODMs and their contract manufacturers to be our primary customers. Both the OEMs, ODMs and their contract manufacturers may determine the design and pricing requirements and make the overall decision regarding the use of our user interface solutions in their products. The use and pricing of our interface solutions will be governed by a technology licensing agreement.

8

Our sales staff solicits prospective customers and our sales personnel receive substantial technical assistance and support from our internal engineering resources because of the highly technical nature of our product solutions. We expect that sales will frequently result from multi-level sales efforts that involve senior management, design engineers, and our sales personnel interacting with our potential customers’ decision-makers throughout the product development and order process.

Our sales are normally negotiated and executed in U.S. Dollars or Euros.

Our sales force and marketing operations are managed out of our corporate headquarters in Stockholm, Sweden, and our current sales force is comprised of sales offices located in Stockholm, Korea and the US.

Research and Development

We continue to invest in research and development of current and emerging technologies that we deem critical to maintaining our competitive position in the touchscreen user interface markets. Many factors are involved in determining the strategic direction of our product development focus, including trends and developments in the marketplace, competitive analyses, market demands, business conditions, and feedback from our customers and strategic partners. In fiscal years 2010 and 2009, we spent $1.9 million and $1.0 million, respectively, on research and development activities.

We carefully monitor innovations in other technologies and are constantly seeking new areas for application of zForce®. We have developed a technology roadmap that we believe will result in a steady stream of new innovations and areas of use.

Our research and development is predominantly in-house, but is also done in close collaboration with external partners and specialists. Our development areas can be divided into the following areas:

|

●

|

Software

|

|

●

|

Optical

|

|

●

|

Mechanical

|

|

●

|

Electrical

|

Recent Developments

|

●

|

On March 25, 2011, we filed a Certificate of Amendment of our Amended and Restated Certificate of Incorporation affecting a reverse stock split of the Company’s issued and outstanding shares of Common stock and Preferred Stock at a ratio of twenty-five-to-one (the “Reverse Split”). The Certificate of Amendment provides that each twenty-five (25) outstanding shares of the Corporation’s Common Stock, par value $0.001 per share, will be exchanged and combined, automatically, without further action, into one (1) share of common stock, and each twenty-five (25) outstanding shares of the Corporation’s Preferred Stock, par value $0.001 per share, will be exchanged and combined, automatically, without further action, into one (1) share of Preferred stock. The Reverse Split was declared effective on March 28, 2011 and has been reflected in this Annual Report on Form 10-K.

|

|

●

|

In March 2011, we entered into new convertible loan agreements (each a “Convertible Loan Agreement”) with investors who participated in our 2009 and 2010 financing transactions (the “Investors”) and who had been issued common stock purchase warrants with exercise prices of $0.50 per share, $1.00 per share, and $1.38 per share (the “Current Warrants”). Pursuant to the Convertible Loan Agreements, each Investor exercised some or all of its outstanding Current Warrants at the applicable exercise price ($0.50 per share, $1.00 per share, and/or $1.38 per share), and provided us with a convertible loan, bearing interest at a rate of seven percent (7%) per annum, that matures on March 1, 2014.

|

9

Each Investor has the option at any time prior to the repayment of its loan to convert the loan into fully-paid and non-assessable restricted shares of our common stock, at a price of $2.50 per share. The loan will automatically be converted into restricted shares of our common stock in the event that on or before the loan due date either (a) our common stock is traded at a price per share of $6.25 or higher for five (5) consecutive trading days, or (b) we consummate a financing in the amount of at least $5 million. In the event that the loan principal and accrued interest is not repaid by us by the due date, and the Investor has not previously converted the loan, the Investor’s sole remedy for such non-payment shall be the payment of additional annual interest at a rate of 10% per year. The accrued interest will be payable on June 30th and December 31st of each year.

In addition, we issued to each Investor new five-year common stock purchase warrants, with an exercise price of $3.13 per share (the “New Warrants”), with each investor receiving (i) a number of New Warrants equal to fifty percent (50%) of the number of Current Warrants exercised by such Investor under its Convertible Loan Agreement, and (ii) a number of New Warrants that is equal in value to twenty-five percent (25%) of the Investor’s loan to us. The New Warrants may be exercised by cash payment or through cashless exercise by the surrender of warrant shares having a value equal to the exercise price of the portion of the warrants being exercised.

The Investors exercised an aggregate of 493,426 outstanding Current Warrants, for an aggregate investment of $515,000 in the Company, and loaned the Company an aggregate of $4.2 million. In addition, we issued to the Investors New Warrants for the purchase of an aggregate of 669,753 of our restricted shares of common stock.

|

●

|

We have recently developed prototype products and are engaged in product design discussions with several large global OEMs and ODMs that are in the process of qualifying our touchscreen technology for incorporation in various products, such as digital picture frames, GPS devices, eReaders, Touch PC, mobile phones, printer and mobile internet devices. The development and product release cycle for these products may take 6 to 18 months.

|

|

●

|

On March 4, 2011, we signed a technology licensing agreement with a top ten global OEM to integrate our zForce® touch screen technology into a series of products. In conjunction with the signing of this technology license agreement, the OEM agreed to pay us $50,000 in non-recurring engineering development fees. We are deferring the engineering development fee revenue until such time as the engineering work has been completed. We expect to complete all services under this contract by June 30, 2011.

|

|

●

|

On January 28, 2011, our Board of Directors approved certain changes to Neonode’s management team. Thomas Eriksson, one of our founders and current Chief Executive Officer of Neonode Technologies AB, Neonode’s wholly-owned subsidiary, was appointed Neonode’s Chief Executive Officer, effective as of January 28, 2011, replacing Mr. Per Bystedt who resigned from his position as Neonode’s Chief Executive Officer, effective as of January 28, 2011. Mr. Bystedt assumed the role of Executive Chairman and continues to serve as the Chairman of the Board of Directors.

|

|

●

|

On January 4, 2011, we signed a technology licensing agreement with a global retail and internet based OEM to integrate our zForce® touch screen technology into a series of products. In conjunction with the signing of this technology license agreement, the OEM agreed to pay us $65,000 in non-recurring engineering development fees. We are deferring the engineering development fee revenue until such time as the engineering work has been completed. We expect to complete all services under this contract by March 31, 2011.

|

|

●

|

On December 30, 2010, we signed a technology license agreement with an OEM related to our touchscreen technology for a series of eReaders. In conjunction with the signing of this technology license agreement, the OEM agreed to pay us $65,000 in non-recurring engineering development fees. We are deferring the engineering development fee revenue until such time as the engineering work has been completed. We expect to complete all services under this contract by March 31, 2011.

|

10

|

●

|

On June 18, 2010, we signed a technology license agreement with Sony Corporation related to our touchscreen technology for a series of eReaders. In conjunction with the signing of this technology license agreement, Sony Corporation issued an initial purchase order for $475,000 of touchscreen licenses. We are deferring the technology license fee revenue until such time as the warranty period expires on March 18, 2011.

|

Overview of the Touchscreen Market and Competition

Competing Touchscreen Technologies:

Today there are different touchscreen technologies available in the market. All of them with different or slightly different profiles, power consumption, level of maturity, and cost price:

|

●

|

Resistive -- uses conductive and resistive layers separated by thin space;

|

|

●

|

Surface acoustic wave -- uses ultrasonic waves that pass over the touchscreen panel;

|

|

●

|

Capacitive and projected capacitive -- a capacitive touchscreen panel is coated with a material, typically indium tin oxide, that conducts a continuous electrical current across the sensor. When the sensor's 'normal' capacitance field (its reference state) is altered by another capacitance field, e.g., someone's finger, electronic circuits located at each corner of the panel measure the resultant 'distortion' in the sine wave characteristics to detect a touch;

|

|

●

|

Infrared -- uses infrared beams that are broken by finger or heat from the finger sensed from a camera to detect a touch;

|

|

●

|

Strain gauge -- uses a spring mounted on the four corners and strain gauges are used to determine deflection when the screen is touched;

|

|

●

|

Optical imaging -- uses two or more image sensors placed around the edges (mostly the corners) of the screen and a light source to create a shadow of the finger;

|

|

●

|

In-cell optical touch technology -- embeds photo sensors or conductive sensors directly into an LCD glass. By integrating the touch function directly into an LCD glass, the LCD acts like a low resolution camera to “see” the shadow of the finger;

|

|

●

|

Dispersive signal technology -- uses sensors to detect the mechanical energy in the glass that occur due to a touch; and

|

|

●

|

Acoustic pulse recognition -- uses more than two piezoelectric transducers located at some positions of the screen to turn the mechanical energy of a touch (vibration) into an electronic signal.

|

Touchscreen Technologies Competitors:

|

Company

|

Technology

|

|

3M

|

Capacitive, Dispersive Signal Touch

|

|

Synaptics

|

Capacitive sensors and IC controllers

|

|

ATMEL

|

Capacitive touch IC controllers

|

|

Cypress

|

Capacitive touch IC controllers

|

|

Maxim

|

Capacitive touch IC controllers

|

|

RPO

|

Optical wave guide

|

|

Nextwindow

|

Optical with camera sensor

|

|

Zytronic

|

Capacitive

|

|

Tyco Electronics

|

Capacitive, Resistive, Surface Wave,

|

|

Touch International

|

Resistive and Capacitive

|

|

Mass Multimedia Inc.

|

All touchscreen technologies

|

|

Young Fast

|

Capacitive sensor and module maker

|

|

TPK

|

Capacitive (provides the capacitive touch sensor for the Apple iPhone) |

11

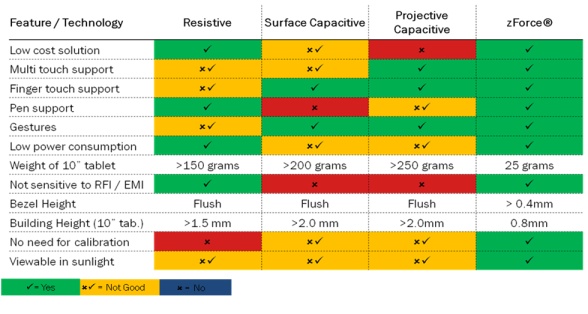

Today’s market leading touch technologies, resistive and capacitive technologies make use of a “touch sensor/window” or an overlay in combination with a controller IC to function. In comparison zForce use a “lightguide” (to reflect and focus light) together with some standard IC components to operate.

Neonode licenses the complete solution to the customers, and thus there is no need for a 3rd party to assemble the touch sensor with the controller (called a module maker) that adds cost to the complete solution.

Below is a comparison table for resistive, capacitive (2 types) and zForce touch technologies. Some of zForce unique selling points include low power, cost and weight, in combination with a 100 % transparent touch window.

Technology License Agreements

As of December 31, 2010, we have entered into four technology license agreements with customers. We signed two additional technology license agreements with customers subsequent to December 31, 2010.

We our dependent on a few customers, and the loss of any one of these customers could have a materially adverse effect on our future revenue stream. In the short term, we anticipate that we will remain dependant on a limited number of customers for substantially all of our future revenue. Failure to anticipate or respond adequately to technological developments in our industry, changes in customer or supplier requirements or changes in regulatory requirements or industry standards, or any significant delays in the development or introduction of products or services, could have a material adverse effect on our business, operating results and cash flows.

Our accounts receivable as of December 31, 2010 was earned from six customers. Our revenue for the year ended December 31, 2010 was earned from seven customers of whom two customers accounted for approximately 84% of our net revenue for the year. Our customers are located in the US, Europe and Asia.

12

Employees

On December 31, 2010, we had fourteen full-time employees and one part-time employee. We augment our staff with consultants on an “as needed” basis. Our full-time and our part-time employees are located in our corporate headquarters in Stockholm, Sweden, and one employee is located in a branch office in the United States. None of our employees are represented by a labor union. We have experienced no work stoppages. We believe our employee relations are positive.

| ITEM 1A. RISK FACTORS |

In addition to the other information in this Annual Report on Form 10-K, stockholders or prospective investors should carefully consider the following risk factors:

Risks Related To Our Business

We may require additional capital to fund our operations, which capital may not be available on commercially attractive terms or at all.

We may require sources of capital in addition to cash on hand to continue operations and to implement our business plan. We project that we have sufficient liquid assets to continue operating at least the next twelve months. We are currently evaluating different financing alternatives, including but not limited to selling shares of our common or preferred stock, or issuing notes that may be converted in shares of our common stock which could result in the issuance of additional shares. If our operations do not become cash flow positive, we will be forced to seek credit line facilities from financial institutions, additional private equity investment, or debt arrangements. No assurances can be given that we will be successful in obtaining such additional financing on reasonable terms, or at all. If adequate funds are not available on acceptable terms, or at all, we may be unable to adequately fund our business plan, which could have a negative effect on our business, results of operations, and financial condition. In addition, if funds are available, the issuance of equity securities or securities convertible into equity could dilute the value of shares of our common stock and cause the market price to fall, and the issuance of debt securities could impose restrictive covenants that could impair our ability to engage in certain business transactions.

We have never been profitable and we anticipate significant additional losses in the future.

Neonode Inc. was formed in 1997 and reconstituted in 2006 as a holding company, owning and operating Neonode AB, which had been formed in 2004. We had been primarily engaged in the business of developing and selling mobile phones. Following the liquidation of Neonode AB, we implemented a new strategy for our business. We have a limited operating history on which to base an evaluation of our business and prospects. Our prospects must be considered in light of the risks and uncertainties encountered by companies in the early stages of development, particularly companies in new and rapidly evolving markets. We were not successful in selling mobile phones and have refocused our business on licensing our touchscreen technology. We may not be successful in entering the technology licensing business. Our success will depend on many factors, including, but not limited to:

|

|

● the growth of touchscreen interface usage;

|

|

|

● the efforts and success of our OEM and other customers;

|

|

|

● the level of competition faced by us; and

|

|

|

● our ability to meet customer demand for engineering support, new technology and ongoing service.

|

In addition, we have experienced substantial net losses in each fiscal period since our inception. These net losses resulted from a lack of substantial revenues and the significant costs incurred in the development of our products and infrastructure. Our ability to continue as a going concern is dependent on our ability to raise additional funds and implement our business plan.

13

Our limited operating history and the emerging nature of our market, together with the other risk factors set forth in this report, make prediction of our future operating results difficult. There can also be no assurance that we will ever achieve significant revenues or profitability or, if significant revenues and profitability are achieved, that they could be sustained.

If we fail to develop and introduce new products and services successfully and in a cost effective and timely manner, we will not be able to compete effectively and our ability to generate revenues will suffer.

We operate in a highly competitive, rapidly evolving environment, and our success depends on our ability to develop and introduce new products, technology, and services that our customers and end users choose to buy. If we are unsuccessful at developing and introducing new products, technology, and services that are appealing to our customers and end users with acceptable quality, prices and terms, we will not be able to compete effectively and our ability to generate revenues will suffer.

The development of new products, technology, and services is very difficult and requires high levels of innovation. The development process is also lengthy and costly. If we fail to anticipate our end users’ needs or technological trends accurately or if we are unable to complete the development of products and services in a cost effective and timely fashion, we will be unable to introduce new products and services into the market or successfully compete with other providers.

As we introduce new or enhanced products or integrate new technology into new or existing products, we face risks including, among other things, disruption in customers’ ordering patterns, excessive levels of older product inventories, inability to deliver sufficient supplies of new products to meet customers’ demand, possible product and technology defects, and potentially unfamiliar sales and support environments. Premature announcements or leaks of new products, features, or technologies may exacerbate some of these risks. Our failure to manage the transition to newer products or the integration of newer technology into new or existing products could adversely affect our business, results of operations, and financial condition.

We are dependent on the ability of our customers to design, manufacture and sell their products that incorporate our touchscreen technologies.

Our products and technologies are licensed to other companies which must be successful in designing, manufacturing and selling the products that incorporate our technologies. If our customers are not able to design, manufacture or sell their products, or are delayed in producing their products, our revenues, profitability, and liquidity, as well as our brand image, may be adversely affected.

We must significantly enhance our sales and product development organizations.

We will need to improve the effectiveness and breadth of our sales operations in order to increase market awareness and sales of our technologies, especially as we expand into new market segments. Competition for qualified sales personnel is intense, and we may not be able to hire the kind and number of sales personnel we are targeting. Likewise, our efforts to improve and refine our products require skilled engineers and programmers. Competition for professionals capable of expanding our research and development organization is intense due to the limited number of people available with the necessary technical skills. If we are unable to identify, hire, or retain qualified sales, marketing, and technical personnel, our ability to achieve future revenue may be adversely affected.

We are dependent on the services of our key personnel.

We are dependent on our current management for the foreseeable future. The loss of the services of any member of management could have a materially adverse effect on our operations and prospects.

14

We are dependent on a few customers.

Currently, we have entered into license agreements with six customers. Since we are dependent on a few customers, the loss of any customer could have a materially adverse effect on our future revenue stream.

If third parties infringe our intellectual property or if we are unable to secure and protect our intellectual property, we may expend significant resources enforcing our rights or suffer competitive injury.

Our success depends in large part on our proprietary technology and other intellectual property rights. We rely on a combination of patents, copyrights, trademarks and trade secrets, confidentiality provisions, and licensing arrangements to establish and protect our proprietary rights. Our intellectual property, particularly our patents, may not provide us with a significant competitive advantage. If we fail to protect or to enforce our intellectual property rights successfully, our competitive position could suffer, which could harm our results of operations.

Our pending patent and trademark applications for registration may not be allowed, or others may challenge the validity or scope of our patents or trademarks, including patent or trademark applications or registrations. Even if our patents or trademark registrations are issued and maintained, these patents or trademarks may not be of adequate scope or benefit to us or may be held invalid and unenforceable against third parties.

We may be required to spend significant resources to monitor and police our intellectual property rights. Effective policing of the unauthorized use of our products or intellectual property is difficult and litigation may be necessary in the future to enforce our intellectual property rights. Intellectual property litigation is not only expensive, but time-consuming, regardless of the merits of any claim, and could divert attention of our management from operating the business. Despite our efforts, we may not be able to detect infringement and may lose competitive position in the market before they do so. In addition, competitors may design around our technology or develop competing technologies. Intellectual property rights may also be unavailable or limited in some foreign countries, which could make it easier for competitors to capture market share.

Despite our efforts to protect our proprietary rights, existing laws, contractual provisions and remedies afford only limited protection. Intellectual property lawsuits are subject to inherent uncertainties due to, among other things, the complexity of the technical issues involved, and we cannot assure you that we will be successful in asserting our intellectual property rights. Attempts may be made to copy or reverse engineer aspects of our products or to obtain and use information that we regard as proprietary. Accordingly, we cannot assure you that we will be able to protect our proprietary rights against unauthorized third party copying or use. The unauthorized use of our technology or of our proprietary information by competitors could have an adverse effect on our ability to sell our products.

We have an international presence in countries whose laws may not provide protection of our intellectual property rights to the same extent as the laws of the United States, which may make it more difficult for us to protect our intellectual property.

As part of our business strategy, we target customers and relationships with suppliers and original equipment manufacturers in countries with large populations and propensities for adopting new technologies. However, many of these countries do not address misappropriation of intellectual property nor deter others from developing similar, competing technologies or intellectual property. Effective protection of patents, copyrights, trademarks, trade secrets and other intellectual property may be unavailable or limited in some foreign countries. In particular, the laws of some foreign countries in which we do business may not protect our intellectual property rights to the same extent as the laws of the United States. As a result, we may not be able to effectively prevent competitors in these regions from infringing our intellectual property rights, which could reduce our competitive advantage and ability to compete in those regions and negatively impact our business.

15

If we are unable to obtain key technologies from third parties on a timely basis, free from errors or defects, we may have to delay or cancel the release of certain products or features in our products or incur increased costs.

We license third-party software for use in our products, including the operating systems. Our ability to release and sell our products, as well as our reputation, could be harmed if the third-party technologies are not delivered to customers in a timely manner, on acceptable business terms, or if they contain errors or defects that are not discovered and fixed prior to release of our products and we are unable to obtain alternative technologies on a timely and cost effective basis to use in our products. As a result, our product releases could be delayed, our offering of features could be reduced, or we may need to divert our development resources from other business objectives, any of which could adversely affect our reputation, business and results of operations.

Changes in financial accounting standards or practices may cause unexpected fluctuations in and adversely affect our reported results of operations.

Any change in financial accounting standards or practices that cause a change in the methodology or procedures by which we track, calculate, record and report our results of operations or financial condition or both could cause fluctuations in, and adversely affect, our reported results of operations and cause our historical financial information not to be reliable as an indicator of future results.

Wars, terrorist attacks or other threats beyond our control could negatively impact consumer confidence, which could harm our operating results.

Wars, terrorist attacks or other threats beyond our control could have an adverse impact on the United States, Europe and the world economy in general, and consumer confidence and spending in particular, which could harm our business, results of operations and financial condition.

Risks Related to Owning Our Stock

During the 2009 fiscal year, due to our lack of cash resources, we were unable to obtain a timely review of our interim financial statements or a timely audit of our 2009 financial statements by our registered independent accountants.

During the 2009 fiscal year, due to our lack of cash resources, we were unable to obtain a timely review of our interim financial statements or a timely audit of our 2009 financial statements by our registered independent accountants in accordance with the Exchange Act’s reporting requirements and Rule 10-01(d) of the Securities and Exchange Commission Regulation S-X. Although our 2009 financial statements have since been audited, our failure to have complied with these SEC requirements could adversely affect the value of our common stock. In addition, our failure in 2009 to satisfy the current public information requirement of Rule 144 means that the reduced Rule 144 holding period prior to the resale of our unregistered stock is unavailable to holders of our unregistered stock until we are current for twelve months. This may adversely affect a stockholder’s ability to resell our stock and cause our share price to decline.

If we continue to experience losses, we could experience difficulty meeting our business plan and our stock price could be negatively affected.

If we are unable to gain market acceptance of our touchscreen technologies, we will experience continuing operating losses and negative cash flow from our operations. Any failure to achieve or maintain profitability could negatively impact the market price of our common stock. We anticipate that we will continue to incur product development, sales and marketing and administrative expenses. As a result, we will need to generate significant quarterly revenues if we are to achieve and maintain profitability. A substantial failure to achieve profitability could make it difficult or impossible for us to grow our business. Our business strategy may not be successful, and we may not generate significant revenues or achieve profitability. Any failure to significantly increase revenues would also harm our ability to achieve and maintain profitability. If we do achieve profitability in the future, we may not be able to sustain or increase profitability on a quarterly or annual basis.

16

Our certificate of incorporation and bylaws and the Delaware General Corporation Law contain provisions that could delay or prevent a change in control.

Our board of directors has the authority to issue up to 2,000,000 shares of Preferred stock and to determine the price, rights, preferences and privileges of those shares without any further vote or action by the stockholders. The rights of the holders of common stock will be subject to, and may be materially adversely affected by, the rights of the holders of any Preferred stock that may be issued in the future. The issuance of Preferred stock could have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock. Furthermore, certain other provisions of our certificate of incorporation and bylaws may have the effect of delaying or preventing changes in control or management, which could adversely affect the market price of our common stock. In addition, we are subject to the provisions of Section 203 of the Delaware General Corporation Law, an anti-takeover law.

Our stock price has been volatile, and your investment in our common stock could suffer a decline in value.

There has been significant volatility in the market price and trading volume of equity securities, which is unrelated to the financial performance of the companies issuing the securities. These broad market fluctuations may negatively affect the market price of our common stock. You may not be able to resell your shares at or above the price you pay for those shares due to fluctuations in the market price of our common stock caused by changes in our operating performance or prospects, and other factors.

Some specific factors that may have a significant effect on our common stock market price include:

|

●

|

actual or anticipated fluctuations in our operating results or future prospects;

|

|

|

●

|

our announcements or our competitors’ announcements of new products;

|

|

|

●

|

the public’s reaction to our press releases, our other public announcements, and our filings with the SEC;

|

|

|

●

|

strategic actions by us or our competitors, such as acquisitions or restructurings;

|

|

|

●

|

new laws or regulations or new interpretations of existing laws or regulations applicable to our business;

|

|

|

●

|

changes in accounting standards, policies, guidance, interpretations or principles;

|

|

|

●

|

changes in our growth rates or our competitors’ growth rates;

|

|

|

●

|

developments regarding our patents or proprietary rights or those of our competitors;

|

|

|

●

|

our inability to raise additional capital as needed;

|

|

|

●

|

concern as to the efficacy of our products;

|

|

|

●

|

changes in financial markets or general economic conditions;

|

|

|

●

|

sales of common stock by us or members of our management team; and

|

|

|

●

|

changes in stock market analyst recommendations or earnings estimates regarding our common stock, other comparable companies, or our industry generally.

|

Future sales of our common stock could adversely affect its price and our future capital-raising activities could involve the issuance of equity securities, which would dilute your investment and could result in a decline in the trading price of our common stock.

We may sell securities in the public or private equity markets if and when conditions are favorable, even if we do not have an immediate need for additional capital at that time. Sales of substantial amounts of common stock, or the perception that such sales could occur, could adversely affect the prevailing market price of our common stock and our ability to raise capital. We may issue additional common stock in future financing transactions or as incentive compensation for our executive management and other key personnel, consultants and advisors. Issuing any equity securities would be dilutive to the equity interests represented by our then-outstanding shares of common stock. The market price for our common stock could decrease as the market takes into account the dilutive effect of any of these issuances. Furthermore, we may enter into financing transactions at prices that represent a substantial discount to the market price of our common stock. A negative reaction by investors and securities analysts to any discounted sale of our equity securities could result in a decline in the trading price of our common stock.

17

Our common stock is currently traded on the OTC Bulletin Board Market. Our stock price and liquidity may continue to be impacted.

Our common stock is traded on the OTC Bulletin Board market, which is generally considered a less efficient and less prestigious market than other markets, such as the Nasdaq Capital Market. The price and liquidity of our stock may continue to be adversely affected as a result of our common stock trading on the OTC Bulletin Board Market.

| ITEM 1B. UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. PROPERTIES |

Our subsidiary, Neonode Technologies AB, entered into a month-to-month lease with Vasakronan Fastigheter AB for approximately 2,000 square feet of office space located at Linnegatan 89, Stockholm, Sweden for approximately $6,000 per month. The annual payment for this space equates to approximately $72,000.

In addition, we lease office space located in Lafayette, California that is provided by our Chief Financial Officer on a rent-free basis.

On March 18, 2011, we entered into a twelve month lease with CA-Santa Clara Office Center Limited Partnership for approximately 1,781 square feet of office space located at 2700 Augustine Drive, Santa Clara, California, USA for approximately $2,600 per month.

| ITEM 3. LEGAL PROCEEDINGS |

On December 9, 2008, Empire Asset Management (“Empire”), a broker dealer that acted as our financial advisor and exclusive placement agent in previous private placement transactions, initiated a law suit against us in the Supreme Court of the State of New York alleging that the Corporation misrepresented the success of its business to induce Empire’s customers to invest in us. We entered into a settlement agreement dated July 9, 2010. The lawsuit was dismissed on September 13, 2010.

On May 11, 2009, Mr. David Berman initiated a lawsuit against us in the Supreme Court of the State of New York alleging that the Corporation misrepresented the success of its business to induce Mr. Berman to invest in us. Mr. Berman, who was a client of Empire, invested $549,860 in our private placement offerings on March 4, 2008 and May 16, 2008, and purchased an additional 6,516 shares totaling $251,082 in the aftermarket. We entered into a settlement agreement dated October 11, 2010. The lawsuit was dismissed on October 13, 2010.

On October 2, 2009, Xerox Corporation (“Xerox”) initiated a law suit against the Company in the Superior Court of California alleging that the Company breached an equipment lease agreement with Xerox and demanding payment of $108,592.81 plus interest, late payment charges, and legal costs. On August 16, 2010, we entered into a settlement agreement that required us to pay a total of $15,000. The lawsuit was dismissed on October 8, 2010.

18

| ITEM 4. (Removed and Reserved) |

PART II

| ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Effective January 2, 2009, our common stock was quoted on the Pink Sheets under the symbol NEON.PK and effective January 26, 2009, our common stock has been quoted on the Over the Counter Bulletin Board Market (OTCBB) under the symbol NEON.OB. From March 28, 2011 through April 15, 2011, the symbol is converted to “NEOND” as a result of our reverse stock split. The table below sets forth the high and low sales prices of our common stock as reported on OTCBB. This information has been adjusted to reflect the 1-for-25 reverse stock split that was effective March 28, 2011. As of December 31, 2010, there were approximately 2,634 holders of record of our common stock.

|

Fiscal Quarter Ended

|

||||||||||||||||

|

March 31

|

June 30

|

September 30

|

December 31

|

|||||||||||||

|

Fiscal 2010

|

||||||||||||||||

|

High

|

$ | 1.00 | $ | 1.25 | $ | 2.00 | $ | 2.00 | ||||||||

|

Low

|

$ | 0.50 | $ | 0.50 | 0.75 | $ | 1.50 | |||||||||

|

Fiscal 2009

|

||||||||||||||||

|

High

|

$ | 1.50 | $ | 1.25 | $ | 1.25 | $ | 1.00 | ||||||||

|

Low

|

$ | 0.50 | $ | 0.50 | $ | 0.50 | $ | 0.50 | ||||||||

There are no restrictions on our ability to pay dividends; however, it is currently the intention of our Board of Directors to retain all earnings, if any, for use in our business and we do not anticipate paying cash dividends in the foreseeable future. Any future determination as to the payment of dividends will depend, among other factors, upon our earnings, capital requirements, operating results and financial condition.

| ITEM 6. SELECTED FINANCIAL DATA |

Not applicable.

| ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations contains forward-looking statements that involve risks and uncertainties. Words such as “believes,” “anticipates,” “expects,” “intends” and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements. Readers are cautioned that the forward-looking statements reflect our analysis only as of the date hereof, and we do not assume any obligation to update these statements. Actual events or results may differ materially from the results discussed in or implied by the forward-looking statements. The following discussion should be read in conjunction with the company’s consolidated financial statements for the years ended December 31, 2010 and 2009 and the related notes included therein.

19

Overview

We provide optical touchscreen solutions for handheld and small to midsized consumer and industrial electronic devices. We license our touchscreen technology to Original Equipment Manufacturers (“OEMs”) and Original Design Manufacturers (“ODMs”) who embed our touchscreen technology into electronic devices that they develop and sell. The cornerstone of our solution is our innovative optical touchscreen technology, zForce®. Our patented zForce® technology offers a number of benefits compared to other touch screen technologies. Our optical technology offers clients low cost and more functional alternatives to other touch screen technologies. zForce® also consumes less power than competitor's screens, is able to function in a wide temperature range, requires no screen overlay and thus offers a much clearer picture while at the same time accommodating multi-touch functionality.

Our technology licensing model allows us to focus on the development of solutions for multi-touch enabled screens and thus we do not have to contend with the financial and logistical burden of manufacturing products, which is handled by our ODM/OEM clients. We license the right to use zForce® and software which, together with standard components from partners, creates a complete optical touch screen solution. The zForce® multi-touch product is our latest release and is currently being integrated into products such as mobile phones, mobile internet devices, eReaders, digital picture frames, printers, GPS devices and tablet PC’s. It should be noted that our licensing model provides the added benefit of allowing us to grow sales exponentially without the need of increasing costs at anywhere near the same rate to support the sales growth.

Through our formerly wholly-owned subsidiary, Neonode AB, we developed our touchscreen technology and an optical touchscreen mobile phone product, the Neonode N2. On December 9, 2008, Neonode AB filed for liquidation under the Swedish bankruptcy laws. Effective with Neonode AB’s bankruptcy filing on December 9, 2008, Neonode Inc. was no longer in the mobile phone business and was relieved of any financial obligations related to the accounts payable or other debts of Neonode AB.

We have not generated sufficient cash from the sale of our products or licensing of our technology to support our operations and have incurred significant losses. During the years ended December 31, 2010 and 2009, we raised approximately $4.0 million and $1.9 million, respectively, net cash proceeds though the sale of our securities and convertible debt. In the first quarter of 2011 we raised approximately $4.7 million through the sale of our securities and convertible debt. We expect this cash plus cash generated from the license of our technology to support our operations for at least the next 12 months.

We have incurred net operating losses and negative operating cash flows since inception. As of December 31, 2010, we had an accumulated deficit of $112.1 million. We expect to incur additional losses and may have negative operating cash flows through the end of 2011. Although we have been able to fund our operations to date, there is no assurance that our capital raising efforts will be able to attract the additional capital or other funds needed to sustain our operations.

Our success is dependent on our obtaining sufficient capital or operating cash flows to fund our operations and to development of our technology and on our bringing such technology to the worldwide market. To achieve our objectives, we may be required to raise additional capital through public or private financings or other arrangements. It cannot be assured that such financings will be available on terms attractive to us, if at all. Such financings may be dilutive to stockholders and may contain restrictive covenants.

In addition to the immediate risks relating to our ability to continue as a going concern and to obtain funding under the current market conditions, we are subject to certain risks common to technology-based companies in similar stages of development. See “Risk Factors” above. Principal risks include risks relating to the uncertainty of growth in market acceptance for our technology, a history of losses since inception, our ability to remain competitive in response to new technologies, the costs to defend, as well as risks of losing, patents and intellectual property rights, a reliance on our future customers’ ability to develop and sell products that incorporate our technology, the concentration of our operations in a limited number of facilities, the uncertainty of demand for our technology in certain markets, our ability to manage growth effectively, our dependence on key members of our management and development team, our limited experience in conducting operations internationally, and our ability to obtain adequate capital to fund future operations.

20

Critical Accounting Policies and Estimates

The preparation of our consolidated financial statements are in conformity with generally accepted accounting principles in the United States of America (“GAAP”) and include the accounts of Neonode Inc. and its wholly-owned subsidiary based in Sweden, Neonode Technologies AB.

All inter-company accounts and transactions have been eliminated in consolidation. Our accounting policies affecting our financial condition and results of operations are more fully described in Note 2 to our consolidated financial statements. Certain of our accounting policies require the application of judgment by management in selecting appropriate assumptions for calculating financial estimates, which inherently contain some degree of uncertainty. Management bases its estimates on historical experience and various other assumptions that are believed to be reasonable under the circumstances. The historical experience and assumptions form the basis for making judgments about the reported carrying values of assets and liabilities and the reported amounts of revenue and expenses that may not be readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. We believe the following are some of the more critical accounting policies and related judgments and estimates used in the preparation of our consolidated financial statements.

Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires making estimates and assumptions that affect, at the date of the consolidated financial statements, the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities and the reported amounts of revenue and expenses. Actual results could differ from these estimates. Significant estimates include, but are not limited to, collectibility of accounts receivable, recoverability of long-lived assets, the valuation allowance recorded related to our deferred tax assets, the fair value of derivative instruments, and the fair value of securities such as options and warrants issued for stock-based compensation and in certain financing transactions.

Concentration of Credit and Business Risks

In the short term, we anticipate that we will depend on a limited number of customers for substantially all of our future revenue. Failure to anticipate or respond adequately to technological developments in our industry, changes in customer or supplier requirements or changes in regulatory requirements or industry standards, or any significant delays in the development or introduction of products or services, could have a material adverse effect on our business, operating results and cash flows.

Our accounts receivable as of December 31, 2010 was earned from six customer. Our revenue for the year ended December 31, 2010 was earned from seven customers of whom two customers accounted for approximately 84% of our net revenue for the year. Our customers are located in the US, Europe and Asia.

Revenue Recognition

Engineering Services:

We may sell engineering consulting services to our customers on a flat rate or hourly rate basis. We recognize revenue from these services when all of the following conditions are met: (1) evidence existed of an arrangement with the customer, typically consisting of a purchase order or contract; (2) our services were preformed and risk of loss passed to the customer; (3) we completed all of the necessary terms of the contract; (4) the amount of revenue to which we were entitled was fixed or determinable; and (5) we believed it was probable that we would be able to collect the amount due from the customer. To the extent that one or more of these conditions has not been satisfied, we defer recognition of revenue. Generally, we recognize revenue as the engineering services stipulated under the contact are completed and accepted by our customers.

21

Licensing Revenues:

We also derive revenue from the licensing of internally developed intellectual property (“IP”). We enter into IP licensing agreements that generally provide licensees the right to incorporate our IP components in their products with terms and conditions that varied by licensee. The IP licensing agreements generally include a nonexclusive license for the underlying IP. Fees under these agreements may include license fees relating to our IP and royalties payable following the sale by our licensees of products incorporating the licensed technology. The license for our IP has standalone value and can be used by the licensee without maintenance and support. We defer the technology license fee revenue until such time as the warranty period stipulated in the license agreement expires. During the warranty period, we agree to correct software issues, as detailed in the underlying technology license agreements.

Hardware Products:

We may from time-to-time develop custom hardware products for our customers that incorporate our touchscreen technology. Our policy is to recognize revenue from hardware product sales when title transfers and risk of loss has passed to the customer, which is generally upon shipment of our hardware products to our customers. We will estimate expected sales returns and record the amount as a reduction of revenue and cost of hardware and other revenue at the time of shipment. To date, we have not sold any hardware products.

Software Products: