Attached files

| file | filename |

|---|---|

| 10-K - FORM 10-K - HOPFED BANCORP INC | d10k.htm |

| EX-99.1 - EXHIBIT 99.1 - HOPFED BANCORP INC | dex991.htm |

| EX-31.1 - EXHIBIT 31.1 - HOPFED BANCORP INC | dex311.htm |

| EX-31.2 - EXHIBIT 31.2 - HOPFED BANCORP INC | dex312.htm |

| EX-32.1 - EXHIBIT 32.1 - HOPFED BANCORP INC | dex321.htm |

| EX-99.2 - EXHIBIT 99.2 - HOPFED BANCORP INC | dex992.htm |

| EX-32.2 - EXHIBIT 32.2 - HOPFED BANCORP INC | dex322.htm |

| EX-23.1 - EXHIBIT 23.1 - HOPFED BANCORP INC | dex231.htm |

| EX-21.1 - EXHIBIT 21.1 - HOPFED BANCORP INC | dex211.htm |

Table of Contents

Exhibit 13.1

SELECTED FINANCIAL INFORMATION AND OTHER DATA

The following summary of selected financial information and other data does not purport to be complete and is qualified in its entirety by reference to the detailed information and Consolidated Financial Statements and accompanying Notes appearing elsewhere in this Report.

Financial Condition and Other Data

| At December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||

| Total amount of: |

||||||||||||||||||||

| Assets |

$ | 1,082,591 | $ | 1,029,876 | $ | 967,560 | $ | 808,352 | $ | 770,888 | ||||||||||

| Loans receivable, net |

600,215 | 642,355 | 628,356 | 576,252 | 494,968 | |||||||||||||||

| Federal funds sold |

— | — | 16,080 | 3,755 | 3,270 | |||||||||||||||

| Cash and due from banks |

54,042 | 37,938 | 15,268 | 17,343 | 14,423 | |||||||||||||||

| Interest-bearing deposits in Federal Home Loan Bank (FHLB) |

6,942 | 3,173 | 5,727 | 931 | 4,190 | |||||||||||||||

| Federal Home Loan Bank stock |

4,378 | 4,281 | 4,050 | 3,836 | 3,639 | |||||||||||||||

| Securities available for sale |

357,738 | 289,691 | 246,952 | 142,310 | 183,339 | |||||||||||||||

| Securities held to maturity: |

||||||||||||||||||||

| U.S. Government agency securities |

— | — | — | 13,541 | 17,318 | |||||||||||||||

| Mortgage-backed Securities |

— | — | 454 | 554 | 700 | |||||||||||||||

| Deposits |

826,929 | 794,144 | 713,005 | 598,753 | 569,433 | |||||||||||||||

| FHLB advances |

81,905 | 102,465 | 130,012 | 101,882 | 113,621 | |||||||||||||||

| Subordinated debentures |

10,310 | 10,310 | 10,310 | 10,310 | 10,310 | |||||||||||||||

| Total stockholders’ equity |

111,444 | 79,949 | 78,284 | 55,803 | 52,270 | |||||||||||||||

| Number of active: |

||||||||||||||||||||

| Real estate loans Outstanding (1) |

4,715 | 5,886 | 6,313 | 6,211 | 5,316 | |||||||||||||||

| Deposit accounts (1) |

40,359 | 40,783 | 94,171 | 76,823 | 67,252 | |||||||||||||||

| Offices open |

18 | 18 | 18 | 18 | 15 | |||||||||||||||

| Operating Data |

||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||

| Interest and dividend income |

$ | 52,417 | $ | 53,141 | $ | 49,477 | $ | 49,033 | $ | 40,668 | ||||||||||

| Interest expense |

22,246 | 26,312 | 26,420 | 28,891 | 23,288 | |||||||||||||||

| Net interest income before provision for loan losses |

30,171 | 26,829 | 23,057 | 20,142 | 17,380 | |||||||||||||||

| Provision for loan losses |

5,970 | 4,199 | 2,417 | 976 | 1,023 | |||||||||||||||

| Net interest income |

24,201 | 22,630 | 20,640 | 19,166 | 16,357 | |||||||||||||||

| Non-interest income |

11,106 | 10,225 | 8,344 | 7,231 | 5,765 | |||||||||||||||

| Non-interest expense |

26,178 | 30,483 | 22,417 | 20,553 | 16,514 | |||||||||||||||

| Income before income taxes |

9,129 | 2,372 | 6,567 | 5,844 | 5,608 | |||||||||||||||

| Provision for income taxes |

2,613 | 397 | 1,952 | 1,728 | 1,700 | |||||||||||||||

| Net income |

$ | 6,516 | $ | 1,975 | $ | 4,615 | $ | 4,116 | $ | 3,908 | ||||||||||

| Preferred stock dividend and accretion of stock warrants |

1,031 | 1,031 | 56 | — | — | |||||||||||||||

| Net income available to common shareholders |

$ | 5,485 | $ | 944 | $ | 4,559 | $ | 4,116 | $ | 3,908 | ||||||||||

| (1) | In 2009, the Bank purged all closed deposit accounts from its system, significantly reducing the amount of deposit accounts. Prior to 2009, the total amount of deposit accounts included closed accounts. |

1

Table of Contents

Selected Quarterly Information (Unaudited)

| First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

|||||||||||||

| ( Dollars in thousands) | ||||||||||||||||

| Year Ended December 31, 2010: |

||||||||||||||||

| Interest and dividend income |

$ | 13,106 | $ | 13,656 | $ | 13,196 | $ | 12,459 | ||||||||

| Net interest income after provision for losses on loans |

6,663 | 7,086 | 6,327 | 4,125 | ||||||||||||

| Non-interest income |

2,309 | 2,456 | 3,085 | 3,256 | ||||||||||||

| Non-interest expense |

6,386 | 6,587 | 6,856 | 6,349 | ||||||||||||

| Net income available to common shareholders |

1,606 | 1,814 | 1,508 | 557 | ||||||||||||

| Year Ended December 31, 2009: |

||||||||||||||||

| Interest and dividend income |

$ | 13,194 | $ | 13,307 | $ | 13,505 | $ | 13,135 | ||||||||

| Net interest income after provision for losses on loans |

5,421 | 5,600 | 5,491 | 6,118 | ||||||||||||

| Non-interest income |

2,359 | 2,741 | 2,085 | 3,040 | ||||||||||||

| Non-interest expense |

5,962 | 6,781 | 11,675 | 6,065 | ||||||||||||

| Net income (loss) available to common shareholders |

1,012 | 854 | (2,875 | ) | 1,953 | |||||||||||

2

Table of Contents

Key Operating Ratios

| At or for the Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| Performance Ratios |

||||||||||||

| Return on average assets (net income available to common shareholders divided by average total assets) |

0.51 | % | 0.09 | % | 0.55 | % | ||||||

| Return on average equity (net income available to common shareholders divided by average total equity) |

5.38 | % | 1.18 | % | 8.08 | % | ||||||

| Interest rate spread (combined weighted average interest rate earned less combined weighted average interest rate cost) |

3.01 | % | 2.74 | % | 2.81 | % | ||||||

| Ratio of average interest-earning assets to average interest-bearing liabilities |

108.19 | % | 107.86 | % | 107.19 | % | ||||||

| Ratio of non-interest expense to average total assets |

2.42 | % | 3.03 | % | 2.67 | % | ||||||

| Ratio of net interest income after provision for loan losses to non-interest expense |

96.96 | % | 76.54 | % | 93.63 | % | ||||||

| Efficiency ratio (non-interest expense divided by sum of interest income plus non-interest income) |

61.65 | % | 80.73 | % | 70.41 | % | ||||||

| Asset Quality Ratios |

||||||||||||

| Non-performing assets to total assets at end of period |

1.37 | % | 1.28 | % | 0.84 | % | ||||||

| Non-accrual loans to total loans at end of period |

0.82 | % | 1.72 | % | 1.16 | % | ||||||

| Allowance for loan losses to total loans at end of period |

1.61 | % | 1.36 | % | 0.97 | % | ||||||

| Allowance for loan losses to non-performing loans at end of period |

195.35 | % | 78.96 | % | 83.01 | % | ||||||

| Provision for loan losses to total loans receivable, net |

0.98 | % | 0.64 | % | 0.39 | % | ||||||

| Net charge-offs to average loans outstanding |

0.79 | % | 0.23 | % | 0.20 | % | ||||||

| Capital Ratios |

||||||||||||

| Total equity to total assets at end of period |

10.29 | % | 7.76 | % | 8.10 | % | ||||||

| Average total equity to average assets |

9.41 | % | 7.95 | % | 6.85 | % | ||||||

Regulatory Capital

| December 31, 2010 | ||||||||

| (Dollars in thousands) | ||||||||

| Company | Bank | |||||||

| Tangible capital |

$ | 119,971 | $ | 99,111 | ||||

| Less: Tangible capital requirement |

16,204 | 15,872 | ||||||

| Excess |

103,767 | 83,239 | ||||||

| Core capital |

$ | 119,971 | $ | 99,111 | ||||

| Less: Core capital requirement |

43,212 | 42,326 | ||||||

| Excess |

76,759 | 56,785 | ||||||

| Total risk-based capital |

$ | 125,515 | $ | 104,655 | ||||

| Less: Risk-based capital requirement |

52,186 | 51,602 | ||||||

| Excess |

$ | 73,329 | $ | 53,053 | ||||

3

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

General

This discussion relates to the financial condition and results of operations of the Company, which became the holding company for the Bank in February 1998. The principal business of the Bank consists of accepting deposits from the general public and investing these funds primarily in loans and in investment securities and mortgage-backed securities. The Bank’s loan portfolio consists primarily of loans secured by residential real estate located in its market area.

For the year ended December 31, 2010, the Company recorded net income available for common shareholders of $5,485,000, a return on average assets of 0.51% and a return on average equity of 5.38%. In June and July of 2010, the Company issued 3,583,334 shares of common stock, receiving net proceeds of $30.4 million. The additional capital improved the Company’s capital position but resulted in a lower return on average equity. The Company’s results of operations for the year ended December 31, 2010, was also negatively affected by the issuance of $18.4 million of preferred stock and the issuance of common stock warrants to the United States Treasury on December 12, 2008 as part of the Treasury Capital Purchase Program. For the years ended December 31, 2010, and December 31, 2009, the Company’s net income available to common shareholders was reduced by $1,031,000 as a result of its issuance of preferred stock to the United States Treasury.

For the year ended December 31, 2009, the Company recorded net income available for common shareholders of $944,000, a return on average assets of 0.09% and a return on average equity of 1.18%. In 2009, the Company’s net income was adversely affected by a $5.0 million ($3.3 million after tax) goodwill impairment charge.

For the year ended December 31, 2008, the Company recorded net income available for common shareholders of $4.6 million, a return on average assets of 0.55% and a return on average equity of 8.08%. For the year ended December 31, 2008, the Company’s total cost related to the issuance of preferred stock was approximately $56,000.

The Company’s net income is dependent primarily on its net interest income, which is the difference between interest income earned on its loans, investment securities and mortgage-backed securities portfolios and interest paid on interest-bearing liabilities. Net interest income is determined by (i) the difference between yields earned on interest-earning assets and rates paid on interest-bearing liabilities (“interest rate spread”) and (ii) the relative amounts of interest-earning assets and interest-bearing liabilities. The Company’s interest rate spread is affected by regulatory, economic and competitive factors that influence interest rates, loan demand and deposit flows. To a lesser extent, the level of non-interest expenses such as compensation, employee benefits, data processing expenses, local deposit and federal income taxes also affect the Company’s net income.

The operations of the Company and the entire thrift industry are significantly affected by prevailing economic conditions, competition and the monetary, fiscal and regulatory policies of governmental agencies. Lending activities are influenced by the demand for and supply of housing, competition among lenders, the level of interest rates and the availability of funds. Deposit flows and costs of funds are influenced by prevailing market rates of interest, primarily on competing investments, account maturities and the levels of personal income and savings in the Company’s market area.

4

Table of Contents

Aggregate Contractual Obligations

| Maturity by Period | ||||||||||||||||||||

| December 31, 2010 (In thousands) | Less than 1 year |

Greater than 1 year to 3 years |

Greater than 3 year to 5 years |

Greater than 5 years |

Total | |||||||||||||||

| Deposits |

$ | 574,088 | 203,858 | 46,071 | 2,912 | 826,929 | ||||||||||||||

| FHLB borrowings |

15,000 | 13,272 | 6,149 | 47,484 | 81,905 | |||||||||||||||

| Repurchase agreements |

29,110 | — | 10,000 | 6,000 | 45,110 | |||||||||||||||

| Subordinated debentures |

— | — | — | 10,310 | 10,310 | |||||||||||||||

| Lease commitments |

65 | 14 | 8 | — | 87 | |||||||||||||||

| Purchase obligations |

1,508 | 3,091 | 1,235 | — | 5,834 | |||||||||||||||

| Total |

$ | 619,771 | 220,235 | 63,463 | 66,706 | 970,175 | ||||||||||||||

Deposits represent non-interest bearing, money market, savings, NOW, certificates of deposit and all other deposits held by the Company. Amounts that have an indeterminate maturity period are included in the less than one-year category.

FHLB borrowings represent the amounts that are due to FHLB of Cincinnati. All amounts have fixed maturity dates. The Company has three callable FHLB advances, totaling $27 million. Callable advances may be called quarterly. With a weighted average cost of 4.37%, management does not anticipate that these advances will be called in 2011. The Company’s callable advances have a final maturity in 2017.

Subordinated debentures represent the amount borrowed in a private pool trust preferred issuance group on September 25, 2003. The debentures are priced at the three-month LIBOR plus 3.10%. At December 31, 2010, the three-month Libor rate was 0.30%. The debentures re-price and pay interest quarterly and have a thirty-year final maturity. The debentures may be called at the issuer’s discretion on a quarterly basis after five years. The interest rate of the debentures reset on the 8th day of January, April, August and November of each year.

Lease commitments represent the total minimum lease payments under non-cancelable operating leases.

The most significant operating contract is for the Company’s data processing services, which re-prices monthly based on the number of accounts and other operational factors. Estimates have been made to include reasonable growth projections. In December 2010, the Company renewed the operating contract with the current data processing provider for a period not to exceed five years. The Company anticipates only a minor increase in fixed and variable cost rates with this contract.

Off Balance Sheet Arrangements

| Maturity by Period | ||||||||||||||||||||

| December 31, 2010 (In thousands) | Less than 1 year |

Greater than 1 year to 3 years |

Greater than 3 years to 5 years |

Greater than 5 years |

Total | |||||||||||||||

| Commercial lines of credit |

$ | 113 | 10,769 | 352 | 22 | 11,256 | ||||||||||||||

| Commitments to extend credit |

1,372 | 23,048 | 8,806 | 1,582 | 34,808 | |||||||||||||||

| Standby letters of credit |

992 | 347 | 154 | 7 | 1,500 | |||||||||||||||

| Home equity lines of credit |

340 | 1,869 | 711 | 26,642 | 29,562 | |||||||||||||||

| Total |

$ | 2,817 | 36,033 | 10,023 | 28,253 | 77,126 | ||||||||||||||

Standby letters of credit represent commitments by the Company to repay a third party beneficiary when a customer fails to repay a loan or debt instrument. The terms and risk of loss involved in issuing standby letters of credit are similar to those involved in issuing loan commitments and extending credit. In addition to credit risk, the Company also has liquidity risk associated with stand-by letters of credit because funding for these obligations could be required immediately. Unused lines of credit represent commercial and residential equity lines of credit with maturities ranging from one to fifteen years.

5

Table of Contents

Accounting for Derivative Instruments and Hedging Activities

In October 2008, Heritage Bank entered into a receive fixed pay variable swap transaction in the amount of $10 million with Compass Bank of Birmingham in which Heritage Bank will pay Compass a fixed rate of 7.27% quarterly for seven years while Compass will pay Heritage Bank a rate equal to the three month London Interbank Offering Rate (“LIBOR”) plus 3.10%, the rate banks in London charge one another for overnight borrowings. Heritage Bank has signed an inter-company transfer with the Company that allows the Company to convert its variable rate subordinated debenture issuance to a fixed rate. The critical terms of the interest rate swap match the term of the corresponding variable rate subordinated debt issuance. The Company considers the interest rate swap a cash flow hedge and conducts a quarterly analysis to ensure that the hedge is effective. At December 31, 2010, the Company’s review indicates that the cash flow hedge is effective. At December 31, 2010, the approximate market loss on the cash flow hedge is $1,088,000.

Quantitative and Qualitative Disclosure about Market Risk

Quantitative Aspects of Market Risk. The principal market risk affecting the Company is risk associated with interest rate volatility (interest rate risk). The Company maintains a trading account for investment securities that may be used to periodically hedge short-term interest rate risk. The Company did not have any activity in its trading account for the years ended December 31, 2010, December 31, 2009 and December 31, 2008, respectively. The Company is not subject to foreign currency exchange rate risk or commodity price risk. Substantially all of the Company’s interest rate risk is derived from the Bank’s lending, deposit taking, and investment activities. This risk could result in reduced net income, loss in fair values of assets and/or increases in fair values of liabilities due to upward changes in interest rates.

Qualitative Aspects of Market Risk. The Company’s principal financial objective is to achieve long-term profitability while reducing its exposure to fluctuating market interest rates. The Company has sought to reduce the exposure of its earnings to changes in market interest rates by attempting to manage the mismatch between assets and liabilities maturities and interest rates. The principal element in achieving this objective is to increase the interest-rate sensitivity of the Company’s interest-earning assets by retaining for its portfolio loans with interest rates subject to periodic adjustment to market conditions. The Company relies on retail deposits as its primary source of funds. However, management is utilizing brokered deposits, wholesale repurchase agreements and FHLB borrowings as sources of liquidity. As part of its interest rate risk management strategy, the Bank promotes demand accounts, overnight repurchase agreements and certificates of deposit with primarily terms of up to five years.

Asset / Liability Management

Key components of a successful asset/liability strategy are the monitoring and managing of interest rate sensitivity of both the interest-earning asset and interest-bearing liability portfolios. The Company has employed various strategies intended to minimize the adverse affect of interest rate risk on future operations by providing a better match between the interest rate sensitivity between its assets and liabilities. In particular, the Company’s strategies are intended to stabilize net interest income for the long-term by protecting its interest rate spread against increases in interest rates. Such strategies include the origination of adjustable-rate mortgage loans secured by one-to-four family residential real estate, and, to a lesser extent, multi-family real estate loans and the origination of other loans with interest rates that are more sensitive to adjustment based upon market conditions than long-term, fixed-rate residential mortgage loans. At December 31, 2010, approximately $199.5 million of the $229.1 million of one-to-four family residential loans originated by the Company (comprising 87.1% of such loans) had adjustable rates or will mature within one year.

The U.S. government agency securities generally are purchased for a term of fifteen years or less. Securities may or may not have call options. A security with call options improves the yield on the security but also has little or no positive price convexity. Non-callable securities or securities with one time calls offer a lower yield but more positive price convexity and an improved predictability of cash flow. Generally, securities with the greater call options (continuous and quarterly) are purchased only during times of extremely low interest rates. The reasons for purchasing these securities generally focus on the fact that a non callable or one time call is of little value if rates are exceptionally low.

6

Table of Contents

At December 31, 2010, the Company’s agency security portfolio consisted of $12.4 million in unsecured debt issued by Federal National Mortgage Corporation (FNMA), $3.2 million issued by Federal Home Loan Mortgage Corporation (FHLMC), $2.9 million issued by the Federal Farm Credit Bank (FFCB) and $15.5 million issued by the Federal Home Loan Bank (FHLB). During 2008, both FNMA and FHLMC required substantial government assistance and were taken into conservatorship by their regulator. All debt securities of both FNMA and FHLMC remain AAA rated and both agencies maintain the implicit backing of the United States of America.

At December 31, 2010, $2.1 million in agency securities were due within five years, approximately $12.1 million were due in five to ten years and approximately $19.8 million were due after ten years. At December 31, 2010, $26.1 million of these securities had a call provision, which authorizes the issuing agency to prepay the securities at face value at certain pre-established dates. If, prior to their maturity dates, market interest rates decline below the rates paid on the securities, the issuing agency may elect to exercise its right to prepay the securities. At December 31, 2010, $12.7 million of these securities may be called one time only prior to December 31, 2012, but not before January 1, 2012 and $4.1 million is callable only in February of 2013. An additional $9.3 million of these securities may be called prior to December 31, 2011, but provide the issuer with multiple call dates and therefore are not as likely to be called. Given the current economic climate as well as the relatively high coupon rates accompanying the one time calls owned by the Company, we anticipate that the majority of eligible one time call provisions for 2012 will be exercised. At December 31, 2010, the estimated average life of this portfolio is 4.7 years and its modified duration is 4.3 years.

Since 2008, the Company has purchased a significant number of agency securities issued by the Small Business Administration. These securities are classified as either SBAPs or SBICs. The SBAP notes have a twenty year maturity, pay interest monthly and principal semi-annually. The SBIC notes have a ten year final maturity and pay principal and interest quarterly. Both securities are classified as a zero risk based agency bond, have a history of slow prepayment speeds and provide yields that are considerable higher than fifteen year GNMA mortgage backed securities. At December 31, 2010, the Company’s agency bond portfolio includes approximately $79.4 million in SBAP securities and $51.0 million in SBIC securities. At December 31, 2010, the estimated average life of this portfolio is 6.3 years and its modified duration is 5.3 years.

In both 2009 and 2010, the Company’s municipal portfolio grew significantly. This growth occurred as municipal bond yields increased to levels not seen in the last ten years despite record low Treasury rates. The value of the municipal bond purchases should be enhanced over time as the Company’s earnings increase and with the possibilities of higher income tax rates in the future. The municipal bond portfolio largely consists of local school district bonds with the guarantee of the State of Kentucky or out of state bonds insured by private companies. At December 31, 2010, the Company has $64.4 million in tax free municipal bonds and $16.8 million in taxable Build America Bonds. Municipal bonds were purchased to provide long-term income stability and higher tax equivalent yields as compared to other portions of the Company’s investment portfolio. At December 31, 2010, approximately $70.1 million in municipal bonds were issued by Kentucky municipalities, $9.3 million were issued by Texas municipalities, $1.3 million were issued by Tennessee municipalities and $500,000 were issued by Indiana municipalities.

At December 31, 2010, $800,000 in municipal bonds were due in less than one year, $4.7 million were due within one to five years, $10.0 million were due in five to ten years, $29.6 million were due in ten to fifteen years and approximately $36.1 million were due after fifteen years. At December 31, 2010, approximately $69.8 million of the Company’s municipal bond portfolio is callable with call dates ranging from February 2011 to December 2020. The call dates are staggered to eliminate the excessive cash flows within any one-year period. At December 31, 2010, approximately $2.7 million of municipal bonds had a call date of less than one year; approximately $6.0 million had a call date from one to five years and approximately $61.1 million in more than five years but less than ten years. At December 31, 2010, the average life of the tax free municipal bond portfolio is approximately 12.6 years and the modified duration of the tax free municipal bond portfolio is approximately 9.8 years. At December 31, 2010, the average life of the taxable municipal bond portfolio is approximately 11.4 years and the modified duration of the taxable municipal bond portfolio is approximately 8.3 years. In recent weeks, several media outlets have raised concerns that the many municipalities may be unable to meet their credit obligations due to a shrinking tax base. As a result of these concerns, municipal fund prices and yields have been adversely affected.

7

Table of Contents

Mortgage-backed securities entitle the Company to receive a pro-rata portion of the cash flow from an identified pool of mortgages. Although mortgage-backed securities generally offer lesser yields than the loans for which they are exchanged, mortgage-backed securities present lower credit risk by virtue of the guarantees that back them, are more liquid than individual mortgage loans, and may be used to collateralize borrowings or other obligations of the Company. Further, mortgage-backed securities provide a monthly stream of both interest and principal, thereby providing the Company with a cash flow to reinvest at current market rates and limit the Company’s interest rate risk. At December 31, 2010, the Company held approximately $72.0 million in fixed rate mortgage backed securities and approximately $6.9 million in adjustable rate mortgage backed securities. The average life of the mortgage backed securities portfolio is approximately 4.9 years and a modified duration of approximately 3.8 years.

At December 31, 2010, the Company held approximately $28.3 million in Collateral Mortgage Obligations (CMO) issued by various agencies of the United States government and $3.5 million in Private Label CMOs issued by private companies. A CMO is a mortgage-backed security that has a structured payment stream based on various factors and does not necessarily remit monthly principal and interest on a pro-rata basis. At December 31, 2010, the Company’s CMO portfolio had an average life of approximately 3.4 years and a modified duration of approximately 3.0 years.

The Company’s Whole Loan CMO portfolio includes two securities that have been downgraded below investment grade. As a result of these downgrades, the Company contracted with an independent third party to conduct an impairment analysis of all Private Label securities owned during 2009. This analysis indicated that the following securities were other than temporarily impaired:

| CUSIP |

Description | Moody’s Credit Rating |

Original Par Value |

Par Value 12/31/2010 |

OTTI Charge 12/31/2009 |

|||||||||||

| 362290AC2 | GSR 2007 TR AR1 | CCC | $ | 2,000,000 | $ | 1,121,352 | $ | 180,000 | ||||||||

| 12638PCQ0 | CSMC 200-3 4A15 | Caa3 | $ | 2,000,000 | $ | 963,047 | $ | 20,000 | ||||||||

As a result of this analysis, the Company incurred a total impairment charge related to its Private Label CMO portfolio of $200,000 during the fourth quarter of 2009. The most recent testing was conducted as of December 31, 2010 and does not indicate additional charges are necessary at this time. The Company will continue to monitor the performance of the Private Label CMO portfolio for additional charges as may be necessary.

Interest Rate Sensitivity Analysis

The Company’s profitability is affected by fluctuations in interest rates. A sudden and substantial increase or decrease in interest rates may adversely impact the Company’s earnings to the extent that the interest rates on interest earning assets and interest bearing liabilities do not change at the same speed, to the same extent or on the same basis. As part of its effort to manage interest rate risk, the Bank monitors its net portfolio value (NPV), a methodology adopted by the OTS to assist the Bank in assessing interest rate risk.

Generally, NPV is the discounted present value of the difference between incoming cash flows on interest-earning assets and other assets and outgoing cash flows on interest-bearing liabilities and other liabilities. The application of the methodology attempts to quantify interest rate risk as the change in the NPV, which would result from a theoretical 200 basis point (1 basis point equals .01%) change in market rates. Both a 300 basis point increase in market interest rates and a 100 basis point decrease in market interest rates are considered.

8

Table of Contents

The following table presents the Bank’s NPV at December 31, 2010, as calculated by the OTS, based on information provided to the OTS by the Bank.

| Change | Net Portfolio Value | NPV as % of PV of Assets | ||||||||||||||||||

| In Rates |

$ Amount | $ Change | % Change | NPV Ratio | Change | |||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||

| +300 bp | $ | 61,044 | $ | (47,811 | ) | (44 | )% | 6.03 | % | (395 | ) bp | |||||||||

| +200 bp | 78,379 | (30,476 | ) | (28 | )% | 7.54 | % | (243 | ) bp | |||||||||||

| +100 bp | 94,383 | (14,472 | ) | (13 | )% | 8.86 | % | (112 | ) bp | |||||||||||

| 0 bp | 108,855 | — | — | 9.97 | % | — | ||||||||||||||

| –100 bp | 125,034 | 16,179 | 15 | % | 11.20 | % | 122 | bp | ||||||||||||

Interest Rate Risk Measures: 200 Basis Point (bp) Rate Shock

| Pre-Shock NPV Ratio: NPV as % of Present Value of Assets |

9.97 | % | ||

| Exposure Measure: Post-Shock NPV Ratio |

7.54 | % | ||

| Sensitivity Measure: Change in NPV Ratio |

243 bp |

The computation of prospective effects of hypothetical interest rate changes are based on numerous assumptions, including relative levels of market interest rates, loan prepayments and deposit decay rates, and should not be relied upon as indicative of actual results. The computations do not contemplate any actions the Bank could undertake in response to changes in interest rates. The matching of assets and liabilities may be analyzed by examining the extent to which such assets and liabilities are “interest rate sensitive” and by monitoring an institution’s interest rate sensitivity “gap.” An asset or liability is said to be interest rate sensitive within a specific period if it will mature or re-price within that period.

Interest Income Analysis

As a part of the Company’s asset liability management process, an emphasis is placed on the effect that changes in interest rates have on the net interest income of the Bank and the resulting change in the net present value of capital. As a part of its analysis, the Company uses third party software and analytical tools derived from the Company’s regulatory reporting models to analyze the re-pricing characteristics of both assets and liabilities and the resulting net present value of the Company’s capital given various changes in interest rates. The model also uses mortgage prepayment assumptions obtained from third party vendors to anticipate prepayment speeds on both loans and investments. The Company’s model uses incremental changes in interest rates. For example, a 3.0% change in annual rates includes a 75 basis point change in each of the next four quarters.

For the year ended December 31, 2010, the Company’s previous efforts to increase duration had a positive effect on its results of operations. At December 31, 2010, the extended duration remains in effect. In an effort to prepare for higher interest rates, the Company has begun the process of extending the duration of its long term liabilities. The Company is using both local and brokered deposits and FHLB advances to accomplish this goal. When attempting to extend duration, both brokered deposits and FHLB advances offer several advantages as compared to locally obtained deposits. Specifically, management has determined that it is easier to more accurately target specific maturities using FHLB advances and brokered deposits as compared to local deposits. In addition, the Company has approximately $65 million in short term deposit balances that are currently priced with floors. In most cases, short term federal funds rates can increase 75 basis points without resulting in an increase to the Company’s interest expense.

9

Table of Contents

During 2011, it is the intent of management to continue to extend duration of its liabilities and take opportunities to reduce the duration of its investment portfolio. The amount of change in interest rate sensitivity eventually achieved by management will be largely dependent on its ability to make changes at a reasonable cost. The reduction of interest rate in the one to two year time frame can dramatically reduce the Company’s net income due to the severe upward slope of the interest rate yield curve. To the extent possible, management will reduce its balances in FHLB deposits to ensure greater flexibility in the event of a sudden change of interest rates.

The Company’s analysis at December 31, 2010, indicates that changes in interest rates are less likely to result in significant changes in the Company’s annual net interest income. A summary of the Company’s analysis at December 31, 2010, for the twelve month period ending December 31, 2011, is as follows:

| Down 1.00% | No change | Up 1.00% | Up 2.00% | Up 3.00% | ||||||||||||||||

| (Dollars In Thousands) | ||||||||||||||||||||

| Net interest income |

$ | 29,368 | $ | 29,653 | $ | 30,268 | $ | 31,062 | $ | 31,752 | ||||||||||

Gap Analysis

The interest rate sensitivity gap is defined as the difference between the amount of interest-earning assets maturing or re-pricing within a specific time period and the amount of interest-bearing liabilities maturing or re-pricing within that time period. A gap is considered positive when the amount of interest rate sensitive assets exceeds the amount of interest rate sensitive liabilities, and is considered negative when the amount of interest rate sensitive liabilities exceeds the amount of interest rate sensitive assets.

At December 31, 2010, the Company had a negative one year or less interest rate sensitivity gap of 20.06% of total interest-earning assets. Generally, during a period of rising interest rates, a negative gap position would be expected to adversely affect net interest income while a positive gap position would be expected to result in an increase in net interest income. Conversely during a period of falling interest rates, a negative gap would be expected to result in an increase in net interest income and a positive gap would be expected to adversely affect net interest income. This analysis is considered less reliable as compared to the Company’s ALM models as changes in various interest rate spreads are not incorporated in Gap Analysis.

10

Table of Contents

The following table sets forth the amounts of interest-earning assets and interest-bearing liabilities outstanding at December 31, 2010, which are expected to mature, are likely to be called or re-priced in each of the time periods shown.

| One Year or Less |

Over one Through Five Years |

Over Five Through Ten Years |

Over Ten Through Fifteen Years |

Over Fifteen Years |

Total | |||||||||||||||||||

| Interest-earning assets |

||||||||||||||||||||||||

| Loans: |

||||||||||||||||||||||||

| 1 - 4 family residential |

$ | 127,207 | $ | 80,346 | $ | 17,252 | $ | 3,670 | $ | 583 | $ | 229,058 | ||||||||||||

| Multi-family residential |

3,883 | 25,452 | 81 | — | — | 29,416 | ||||||||||||||||||

| Construction |

22,233 | 1,128 | — | — | — | 23,361 | ||||||||||||||||||

| Non-residential |

129,357 | 89,871 | 21,695 | 2,034 | 12,391 | 255,348 | ||||||||||||||||||

| Secured by deposits |

2,241 | 1,840 | — | — | — | 4,081 | ||||||||||||||||||

| Other loans |

36,438 | 28,627 | 2,678 | 675 | — | 68,418 | ||||||||||||||||||

| Time deposits and interest bearing deposits in FHLB |

6,942 | — | — | — | — | 6,942 | ||||||||||||||||||

| Non-amortizing securities |

7,897 | 37,685 | 68,285 | 201 | 2,382 | 116,450 | ||||||||||||||||||

| Mortgage-backed securities |

33,877 | 84,121 | 67,254 | 37,529 | 18,507 | 241,288 | ||||||||||||||||||

| Total |

370,075 | 349,070 | 177,245 | 44,109 | 33,863 | 974,362 | ||||||||||||||||||

| Interest bearing liabilities: |

||||||||||||||||||||||||

| Deposits |

511,080 | 243,798 | 2,912 | — | — | 757,790 | ||||||||||||||||||

| Borrowed funds |

54,420 | 35,421 | 47,484 | — | — | 137,325 | ||||||||||||||||||

| Total |

565,500 | 279,219 | 50,396 | — | — | 895,115 | ||||||||||||||||||

| Interest sensitivity gap |

($ | 195,425 | ) | $ | 69,851 | $ | 126,849 | $ | 44,109 | $ | 33,863 | $ | 79,247 | |||||||||||

| Cumulative interest sensitivity gap |

($ | 195,425 | ) | ($ | 125,574 | ) | $ | 1,275 | $ | 45,384 | $ | 79,247 | $ | 79,247 | ||||||||||

| Ratio of interest-earning assets to interest bearing liabilities |

65.44 | % | 125.02 | % | 351.70 | % | — | — | 108.85 | % | ||||||||||||||

| Ratio of cumulative gap to total interest-earning assets |

(20.06 | %) | (12.89 | %) | 0.13 | % | 4.66 | % | 8.13 | % | 8.13 | % | ||||||||||||

The preceding table was prepared based upon the assumption that loans will not be repaid before their respective contractual maturities, except for adjustable rate loans, which are classified, based upon their next re-pricing date. Further, it is assumed that fixed maturity deposits are not withdrawn prior to maturity and other deposits are withdrawn or re-priced within one year. Mortgage-backed securities are classified based on their lifetime prepayment speeds. In 2010, the Company is aware that the decision by Freddie Mac and Fannie Mae to redeem all mortgages past due more than 120 days will result in faster prepayment speeds for its mortgage backed security portfolio. However, management does not have enough information specific to its portfolio to model the changes on prepayment speeds that may result. As a result, the preceding table does not reflect possible changes in cash flows that may result from this change in Fannie Mae and Freddie Mac portfolio servicing practices. The actual interest rate sensitivity of the Company’s assets and liabilities could vary significantly from the information set forth in the table due to market and other factors. The retention of adjustable-rate mortgage loans in the Company’s portfolio helps reduce the Company’s exposure to changes in interest rates. However, there are unquantifiable credit risks resulting from potential increased costs to borrowers as a result of re-pricing adjustable-rate mortgage loans. It is possible that during periods of rising interest rates, the risk of default on adjustable-rate mortgage loans may increase due to the upward adjustment of interest costs to the borrowers.

11

Table of Contents

Average Balance, Interest and Average Yields and Rates

The following table sets forth certain information relating to the Company’s average interest-earning assets and average interest-bearing liabilities and reflects the average yield on assets and average cost of liabilities for the periods and at the date indicated. Such yields and costs are derived by dividing income or expense by the average monthly balance of assets or liabilities, respectively, for the periods presented. Average balances are derived from month-end balances. Management does not believe that the use of month-end balances instead of daily balances has caused any material difference in the information presented.

The table also presents information for the periods and at the date indicated with respect to the difference between the average yield earned on interest-earning assets and average rate paid on interest-bearing liabilities, or “interest rate spread,” which savings institutions have traditionally used as an indicator of profitability. Another indicator of an institution’s net interest income is its “net yield on interest-earning assets,” which is its net interest income divided by the average balance of interest-earning assets. Net interest income is affected by the interest rate spread and by the relative amounts of interest-earning assets and interest-bearing liabilities. When interest-earning assets approximate or exceed interest-bearing liabilities, any positive interest rate spread will generate net interest income.

| December 2010 Averages | ||||||||

| Balance | Weighted Average Yield/Cost |

|||||||

| (Dollars in thousands) | ||||||||

| Interest-earning assets: |

||||||||

| Loans receivable, net |

$ | 605,597 | 5.96 | % | ||||

| Non taxable securities available for sale |

66,060 | 5.75 | % * | |||||

| Taxable securities available for sale Federal Home Loan Bank stock |

|

300,452 4,378 |

|

|

3.67 3.12 |

% % | ||

| Time deposits and other interest-bearing cash deposits |

— | — | ||||||

| Total interest-earning assets |

976,487 | 5.23 | % | |||||

| Non-interest-earning assets |

110,281 | |||||||

| Total assets |

$ | 1,086,768 | ||||||

| Interest-bearing liabilities: |

||||||||

| Deposits |

$ | 760,022 | 2.08 | % | ||||

| FHLB borrowings |

84,091 | 3.77 | % | |||||

| Repurchase agreements |

39,191 | 2.13 | % | |||||

| Subordinated debentures |

10,310 | 3.54 | % | |||||

| Total interest-bearing liabilities |

893,614 | 2.26 | % | |||||

| Non-interest-bearing liabilities |

76,687 | |||||||

| Total liabilities |

970,301 | |||||||

| Common stock |

77 | |||||||

| Common stock warrants |

556 | |||||||

| Additional paid-in capital |

74,914 | |||||||

| Retained earnings |

39,920 | |||||||

| Treasury stock |

(5,076 | ) | ||||||

| Accumulated other comprehensive income |

6,076 | |||||||

| Total liabilities and equity |

$ | 1,086,768 | ||||||

| Interest rate spread |

2.97 | % | ||||||

| Ratio of interest-earning assets to interest-bearing liabilities |

109.3 | % | ||||||

| * | Tax equivalent yield at the Company’s 34% tax bracket and a 2.25% cost of funds rate. |

12

Table of Contents

| Years Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2010 | 2009 | 2008 | ||||||||||||||||||||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||||||||||||||||||

| Average Balance |

Interest | Average Yield/Cost |

Average Balance |

Interest | Average Yield/Cost |

Average Balance |

Interest | Average Yield/Cost |

||||||||||||||||||||||||||||

| Interest-earning assets: |

||||||||||||||||||||||||||||||||||||

| Loans receivable, net |

$ | 629,633 | 38,089 | 6.05 | % | $ | 633,143 | 38,921 | 6.15 | % | $ | 601,847 | 41,692 | 6.93 | % | |||||||||||||||||||||

| Taxable securities AFS |

289,556 | 11,923 | 4.12 | % | 252,707 | 12,635 | 5.00 | % | 141,668 | 7,115 | 5.02 | % | ||||||||||||||||||||||||

| Non-taxable securities AFS |

63,179 | 3,587 | 5.68 | % | 36,559 | 2,268 | 6.20 | % | 17,038 | 916 | 5.38 | % | ||||||||||||||||||||||||

| Securities held to maturity |

— | — | — | 280 | 12 | 4.29 | % | 3,534 | 155 | 4.39 | % | |||||||||||||||||||||||||

| Time deposits and other interest-bearing cash deposits |

— | — | — | 3,270 | 8 | 0.24 | % | 8,171 | 147 | 1.80 | % | |||||||||||||||||||||||||

| Total interest-earning assets |

$ | 982,368 | 53,599 | 5.46 | % | $ | 925,959 | 53,844 | 5.81 | % | $ | 772,258 | 50,025 | 6.48 | % | |||||||||||||||||||||

| Non-interest-earning assets |

101,119 | 80,423 | 66,573 | |||||||||||||||||||||||||||||||||

| Total assets |

1,083,487 | 1,006,382 | 838,831 | |||||||||||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||||||||||||||

| Deposits |

$ | 762,418 | 17,384 | 2.28 | % | $ | 698,367 | 20,833 | 2.98 | % | $ | 581,817 | 20,789 | 3.57 | % | |||||||||||||||||||||

| Borrowings |

145,582 | 4,862 | 3.34 | % | 160,081 | 5,479 | 3.42 | % | 138,671 | 5,631 | 4.06 | % | ||||||||||||||||||||||||

| Total interest-bearing liabilities |

908,000 | 22,246 | 2.45 | % | 858,448 | 26,312 | 3.07 | % | 720,488 | 26,420 | 3.67 | % | ||||||||||||||||||||||||

| Non-interest-bearing liabilities |

73,552 | 67,944 | 60,897 | |||||||||||||||||||||||||||||||||

| Total liabilities |

981,552 | 926,392 | 781,385 | |||||||||||||||||||||||||||||||||

| Common stock |

59 | 41 | 41 | |||||||||||||||||||||||||||||||||

| Common stock warrants |

556 | 556 | 29 | |||||||||||||||||||||||||||||||||

| Additional paid-in capital |

61,949 | 44,324 | 26,998 | |||||||||||||||||||||||||||||||||

| Retained earnings |

39,119 | 38,599 | 37,605 | |||||||||||||||||||||||||||||||||

| Treasury stock |

(5,786 | ) | (6,495 | ) | (6,350 | ) | ||||||||||||||||||||||||||||||

| Accumulated other comprehensive (loss) |

6,038 | 2,965 | (877 | ) | ||||||||||||||||||||||||||||||||

| Total liabilities and equity |

1,083,487 | 1,006,382 | 838,831 | |||||||||||||||||||||||||||||||||

| Net interest income |

31,353 | 27,532 | 23,605 | |||||||||||||||||||||||||||||||||

| Interest rate spread |

3.01 | %* | 2.74 | %* | 2.81 | %* | ||||||||||||||||||||||||||||||

| Net interest margin |

3.19 | %* | 2.97 | %* | 3.06 | %* | ||||||||||||||||||||||||||||||

| Ratio of average interest-earning assets to average interest-bearing liabilities |

108.19 | % | 107.86 | % | 107.19 | % | ||||||||||||||||||||||||||||||

| Using a 34% tax rate. |

||||||||||||||||||||||||||||||||||||

| * | The tax equivalent adjustments were $1,182, $703 and $392 for 2010, 2009 and 2008, respectively |

Rate Volume Analysis

The following table sets forth certain information regarding changes in interest income and interest expense of the Company for the periods indicated. For each category of interest-earning asset and interest-bearing liability, information is provided on changes attributable to: (i) changes in volume (changes in volume from year to year multiplied by the average rate for the prior year) and (ii) changes in rate (changes in the average rate from year to year multiplied by the prior year’s volume).

13

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 vs. 2009 | 2009 vs. 2008 | |||||||||||||||||||||||

| Increase (Decrease) due to |

Increase (Decrease) due to |

|||||||||||||||||||||||

| Rate | Volume | Total Increase (Decrease) |

Rate | Volume | Total Increase (Decrease) |

|||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Interest-earning assets: |

||||||||||||||||||||||||

| Loans receivable |

$ | (620 | ) | (212 | ) | (832 | ) | $ | (4,695 | ) | 1,924 | (2,771 | ) | |||||||||||

| Securities available for sale, taxable |

(2,229 | ) | 1,517 | (712 | ) | (32 | ) | 5,552 | 5,520 | |||||||||||||||

| Securities available for sale, non-taxable |

(192 | ) | 1,511 | 1,319 | 141 | 1,211 | 1,352 | |||||||||||||||||

| Securities held to maturity |

— | (12 | ) | (12 | ) | (3 | ) | (140 | ) | (143 | ) | |||||||||||||

| Other interest-earning assets |

— | (8 | ) | (8 | ) | (51 | ) | (88 | ) | (139 | ) | |||||||||||||

| Total interest-earning assets |

(3,041 | ) | 2,796 | (245 | ) | (4,640 | ) | 8,459 | 3,819 | |||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||

| Deposits |

(4,584 | ) | 1,135 | (3,449 | ) | (4,379 | ) | 4,423 | 44 | |||||||||||||||

| Borrowings |

84 | (701 | ) | (617 | ) | (905 | ) | 753 | (152 | ) | ||||||||||||||

| Total interest-bearing liabilities |

(4,500 | ) | 434 | (4,066 | ) | (5,284 | ) | 5,176 | (108 | ) | ||||||||||||||

| Increase (decrease) in net interest income |

$ | 1,459 | 2,362 | 3,821 | $ | 644 | 3,283 | 3,927 | ||||||||||||||||

Critical Accounting Policies and Estimates

The Company’s financial statements are prepared in accordance with accounting principles generally accepted in the United States of America. The financial information contained within these statements is, to a significant extent, financial information that is based on appropriate measures of the financial effects of transactions and events that have already occurred. Based on its consideration of accounting policies that involved the most complex and subjective decisions and assessments, management has identified its most critical accounting policy to be that related to the allowance for loan losses. The Company’s allowance for loan loss methodology incorporates a variety of risk considerations, both quantitative and qualitative; in establishing an allowance for loan loss that management believes is appropriate at each reporting date. Quantitative factors included the Company’s historical loss experience, delinquency and charge-off trends, collateral values, changes in non-performing loans, and other factors. Quantitative factors also incorporate known information about individual loans, including borrower’s sensitivity to economic conditions throughout the southeast and particular, the state of certain industries. Size and complexity of individual credits in relation to loan structure, existing loan policies and pace of portfolio growth are other qualitative factors that are considered in the methodology. As the Company adds new products and increases the complexity of the loan portfolio, its methodology accordingly may change. In addition, it may report materially different amounts for the provision for loan losses in the statement of operations if management’s assessment of the above factors changes in future periods. This discussion and analysis should be read in conjunction with the Company’s consolidated financial statements and the accompanying notes presented elsewhere herein. Although management believes the levels of the allowance for loan losses as of both December 31, 2010 and 2009 were adequate to absorb inherent losses in the loan portfolio, a decline in local economic conditions, or other factors, could result in increasing losses that cannot be reasonably predicted at this time. The Company also considers its policy on non-accrual loans as a critical accounting policy. Loans are placed on non-accrual when a loan is specifically determined to be impaired or when principal or interest is delinquent for 91 days or more.

14

Table of Contents

Comparison of Financial Condition at December 31, 2010 and December 31, 2009

The Company’s total assets increased by $52.7 million, from $1.03 billion at December 31, 2009, to $1.08 billion at December 31, 2010. The Company did not sell any federal funds at December 31, 2009 and 2010. The Company no longer has any agency securities classified as held to maturity. The available for sale portfolio increased $68.0 million, from $289.7 million at December 31, 2009, to $357.7 million at December 31, 2010. At December 31, 2010, the Company’s investment in Federal Home Loan Bank stock was carried at an amortized cost of $4.4 million. See Note 2 of Notes to Consolidated Financial Statements.

The Company’s net loan portfolio declined by $42.2 million during the year ended December 31, 2010. Net loans totaled $642.4 and $600.2 at December 31, 2009, and December 31, 2010, respectively. The decline in the loan activity during the year ended December 31, 2010, was primarily the result of weak loan demand and limitations placed on the Company by the Office of Thrift Supervision (OTS) on certain types of lending deemed most profitable to the Company as well as the implementation of more conservative loan underwriting standards. In 2010, economic activity remained subdued in the majority of the Company’s markets. For the year ended December 31, 2010, the Company’s tax equivalent average yield on loans was 6.05%, compared with 6.15% for the year ended December 31, 2010.

The allowance for loan losses totaled $9.8 million at December 31, 2010, an increase of approximately $900,000 from the allowance for loan losses of $8.9 million at December 31, 2009. The ratio of the allowance for loan losses to total loans was 1.61% and 1.36% at December 31, 2010, and December 31, 2009, respectively. Also, at December 31, 2010, the Company’s non-accrual loans were approximately $5.0 million or 0.82% of total loans, compared to $11.2 million, or 1.72% of total loans, at December 31, 2009. The Company’s ratio of allowance for loan losses to non-accrual loans at December 31, 2010 and 2009 was 195.35% and 78.96%, respectively.

Comparison of Operating Results for the Years Ended December 31, 2010 and 2009

Net Income. The Company’s net income available for common shareholders for the year ended December 31, 2010, was $5.5 million compared to $944,000 for the year ended December 31, 2009. In 2009, net income available for common shareholders was adversely affected by a $5.0 million goodwill impairment charge and a $1.5 million increase in assessments from the FDIC. The Company’s provision expenses in both 2010 and 2009 are well in excess of our normally operating expectations and reflect the continued challenges in our local and national economies. Improved profitability in 2010 resulted from improved net interest margins and the lack of a goodwill impairment charge.

Net Interest Income. Net interest income for the year ended December 31, 2010, was $30.2 million, compared to $26.8 million for the year ended December 31, 2009. The increase in net interest income for the year ended December 31, 2010, was the result of Company’s ability to re-price time deposits at lower rates due to the continued struggles in the economy. The Company’s level of average interest bearing assets increased $56.4 million during 2010. However, the increase in average interest bearing assets was insufficient to offset the decline in yields, resulting in a slightly reduced level of interest income. For the year ended December 31, 2010, the Company’s tax equivalent average yield on total interest-earning assets was 5.46% compared to 5.81% for the year ended December 31, 2009, and its average cost of interest-bearing liabilities was 2.45%, compared to 3.07% for the year ended December 31, 2009. As a result, the Company’s tax equivalent interest rate spread for the year ended December 31, 2010 was 3.01%, compared to 2.74% for the year ended December 31, 2009 and its tax equivalent net interest margin was 3.19% for the year ended December 31, 2010, compared to 2.97% for the year ended December 31, 2009.

Interest Income. Interest income declined $700,000 from $53.1 million to $52.4 million, or 1.3% during the year ended December 31, 2010 compared to 2009. The modest decline was attributable to a decline in yields on assets that was not fully offset by an increase in the volume of investments outstanding. The average balance on taxable securities available for sale increased $36.9 million, from $252.7 million for the year ended December 31, 2010, to $289.6 million for the year ended December 31, 2009. The average balance of non-taxable securities available for sale increased approximately $26.6 million, from $36.6 million for the year ended December 31, 2009, to $63.2 million for the year ended December 31, 2010. The Company did not carry time deposits or held to maturity securities in its portfolio at December 31, 2010.

15

Table of Contents

Interest Expense. Interest expense declined to $22.2 million for the year ended December 31, 2010, compared to $26.3 million for 2009. The decline in interest expense was attributable to a decline in the average cost interest bearing deposits. The average cost of average interest-bearing deposits declined to 2.28% for the year ended December 31, 2010, from 2.98% for the year ended December 31, 2009. Over the same period, the average balance of interest bearing deposits increased from $698.4 million for the year ended December 31, 2009, to $762.4 million for the year ended December 31, 2010. The average balance of FHLB borrowings declined from $119.1 million for the year ended December 31, 2009 to $92.8 million for the year ended December 31, 2010. The average cost of FHLB borrowings increased from 3.42% for the year ended December 31, 2009, to 3.55% for the year ended December 31, 2010 due to the maturity of lower costing advances. The Company’s recent practice is to allow FHLB advances to mature and not renew. The Company anticipates this practice to continue into 2011 with $15 million in advances set to renew, including $10 million in February 2011 at an interest rate of 5.24%.

Provision for Loan Losses. The Company determined that an additional $6.0 million and $4.2 million in provision for loan losses was required for the years ended December 31, 2010, and December 31, 2009, respectively. The increase in the Company’s provision for loan loss expense is the result of both local and national economic conditions, including an increase in the unemployment rate in the communities served by the Company, higher levels of non-performing assets and lower appraised values for problem loans secured by real estate.

Non-Interest Income. Non-interest income increased by $900,000 for the year ended December 31, 2010, to $11.1 million, compared to $10.2 million for the year ended December 31, 2009. The increase in non-interest income is largely the result of an $800,000 increase on gains taken on the sale of investments. For the year ended December 31, 2010, income from deposit accounts and financial services income were relatively unchanged as lower brokerage income was offset by higher mortgage origination income. Non-interest income for the year ended December 31, 2009, included a $200,000 other than temporary impairment charge on two Private Label CMOs.

Non-Interest Expense. Total non-interest expense for the year ended December 31, 2010, was $26.2 million, compared to $30.5 million in 2009. The decline was the result of the Company’s $5.0 million goodwill impairment charge in 2009 and a net gain on the sale of real estate owned of approximately $300,000. For the year ended December 31, 2010, the Company’s salaries and benefits expense increased by approximately $500,000 as compared to the year ended December 31, 2009, due to higher staffing levels and an increase in the cost of health insurance. Professional services expenses, data processing expenses and other expenses are the only additional non-interest expense items that increased by more than $200,000 in 2010 as compared to 2009.

Income Taxes. The effective tax rates for the years ended December 31, 2010, and December 31, 2009, was 28.6% and 16.7%, respectively. The Company’s effective tax rate increased sharply due to higher levels of pre-tax income as the majority of the overall increase in the Company’s net income for 2009 was the result of lower expenses and higher levels of net interest income.

Comparison of Operating Results for the Years Ended December 31, 2009 and 2008

Net Income. The Company’s net income available for common shareholders for the year ended December 31, 2009 was $944,000 compared to $4.6 million at December 31, 2008. In 2009, net income available for common shareholders was adversely affected by a $5.0 million goodwill impairment charge, $4.2 million in provision for loan loss expense, $1.5 million increase in assessments from the FDIC and $1.0 million in dividends and accretion of preferred stock discount related to the Company’s issuance of preferred stock in December 2008.

Net Interest Income. Net interest income for the year ended December 31, 2009, was $26.8 million, compared to $23.1 million for the year ended December 31, 2008. The increase in net interest income for the year ended December 31, 2009, was the result of a sharp decline in market interest rates, allowing the Company to reduce its cost of funds. At the same time, higher average balances of both taxable and tax free investments provided higher levels of interest income. For the year ended December 31, 2009, the Company’s tax equivalent average yield on total interest-earning assets was 5.81% compared to 6.48% for the year ended December 31, 2008, and its average cost of interest-bearing liabilities was 3.07%, compared to 3.67% for the year ended December 31, 2008. As a result, the Company’s tax equivalent interest rate spread for the year ended December 31, 2009 was 2.74%, compared to 2.81% for the year ended December 31, 2008 and its tax equivalent net interest margin was 2.97% for the year ended December 31, 2009, compared to 3.06% for the year ended December 31, 2008. At December 31, 2009, the Company reduced interest income on loans by $229,000 to eliminate all interest income on non-accrual loans. For the year ended December 31, 2009, the change in income recognition reduced the Company’s net interest margin by 0.03%.

16

Table of Contents

Interest Income. Interest income increased $3.6 million from $49.5 million to $53.1 million, or 7.3% during the year ended December 31, 2009 compared to 2008. The modest increase was attributable to an increase in the volume of loans and investments outstanding, offsetting a decline in market interest rates. The Company does not classify any securities as held to maturity at December 31, 2009, as compared to an average balance of $3.5 million for the year ended December 31, 2008. The average balance on taxable securities available for sale increased $111.0 million, from $141.7 million for the year ended December 31, 2008, to $252.7 million for the year ended December 31, 2009. The average balance of non-taxable securities available for sale increased approximately $19.6 million, from $17.0 million for the year ended December 31, 2008, to $36.6 million for the year ended December 31, 2009. Average time deposits and other interest-bearing cash deposits declined from $8.2 million for the year ended December 31, 2008, to $3.3 million for the year ended December 31, 2009. Overall, average total interest-earning assets increased $153.7 million from December 31, 2008, to December 31, 2009.

Interest Expense. Interest expense declined to $26.3 million for the year ended December 31, 2009, compared to $26.4 million for 2008. The decline in interest expense was attributable to a decline in the average cost of both interest bearing deposits and Federal Home Loan Bank (“FHLB”) borrowings. The average cost of interest-bearing deposits declined from 3.57% for the year ended December 31, 2008, to 2.98% for the year ended December 31, 2009. Over the same period, the average balance of interest bearing deposits increased from $581.8 million for the year ended December 31, 2008, to $698.4 million for the year ended December 31, 2009. The average balance of FHLB borrowings increased from $95.0 million for the year ended December 31, 2008 to $119.1 million for the year ended December 31, 2009. The average cost of FHLB borrowings declined from 4.15% for the year ended December 31, 2008, to 3.42% for the year ended December 31, 2009.

Provision for Loan Losses. The Company determined that an additional $4.2 million and $2.4 million in provision for loan losses was required for the years ended December 31, 2009, and December 31, 2008, respectively. The increase in the Company’s provision for loan loss expense is the result of both local and national economic conditions, including an increase in the unemployment rate in the communities served by the Company as well as higher levels of non-performing loans.

Non-Interest Income. Non-interest income increased by $1.9 million for the year ended December 31, 2009, to $10.2 million, compared to $8.3 million for the year ended December 31, 2008. The increase in non-interest income is the result of a $2.0 million increase on gains taken on the sale of investments. For the year ended December 31, 2009, income from deposit accounts and financial services income were marginally lower while the Company experienced a 15% decline in the level of brokerage income. Non-interest income for the year ended December 31, 2009, included a $200,000 other than temporary impairment charge on two Private Label CMOs previously discussed.

Non-Interest Expense. Total non-interest expense for the year ended December 31, 2009, was $30.5 million, compared to $22.4 million in 2008. The increase was the result of the Company’s $5.0 million goodwill impairment charge and the sharp increase in cost associated with the Company’s FDIC expenses. The Company’s cost related to FDIC coverage increased from $463,000 in 2008 to $2.0 million in 2009. The increase in FDIC expenses relates to the cost incurred by the FDIC to pay for more than 130 bank failures in 2009, The Company anticipates that FDIC expense will remain elevated for the next five years. For the year ended December 31, 2009, the Company’s compensation expense increased by approximately $800,000 as compared to the year ended December 31, 2008, due to higher payroll and insurance expenses.

Income Taxes. The effective tax rates for the years ended December 31, 2009, and December 31, 2008, was 16.7% and 29.7%, respectively. The Company’s effective tax rate declined sharply due to higher levels of tax free investments, a higher level of income related to bank owned life insurance and lower levels of taxable income in 2009.

Liquidity and Capital Resources

The Company’s primary business is that of the Bank. Management believes dividends that may be paid from the Bank to the Company will provide sufficient funds for the Company’s current and anticipated needs; however, no assurance can be given that the Company will not have a need for additional funds in the future. The Bank is subject to certain regulatory limitations with respect to the payment of dividends to the Company.

Capital Resources. At December 31, 2010, the Bank exceeded all regulatory minimum capital requirements. For a detailed discussion of the Office of Thrift Supervision regulatory capital requirements, and for a tabular presentation of the Bank’s compliance with such requirements, see Note 16 of Notes to Consolidated Financial Statements.

17

Table of Contents

Liquidity. Liquidity management is both a daily and long-term function of business management. If the Bank requires funds beyond its ability to generate them internally, the Bank believes that it could borrow funds from the FHLB. At December 31, 2010, the Bank had outstanding advances of $81.9 million from the FHLB and $29.3 million of letters of credit issued by the FHLB to secure municipal deposits. The Bank can immediately borrow an additional $56.3 million from the FHLB. See Note 7 of Notes to Consolidated Financial Statements.

Subordinated Debentures Issuance. On September 25, 2003, the Company issued $10,310,000 of subordinated debentures in a private placement offering. The securities have a thirty-year maturity and are callable at the issuer’s discretion on a quarterly basis beginning five years after issuance. The securities are priced at a variable rate equal to the three-month LIBOR (London Interbank Offering Rate) plus 3.10%. Interest is paid and the rate of interest may change on a quarterly basis. The Company’s subsidiary, a federal chartered thrift supervised by the Office of Thrift Supervision (OTS) may recognize the proceeds of trust preferred securities as capital. OTS regulations provide that 25% of Tier I capital may consist of trust preferred proceeds. See Note 10 of Notes to Consolidated Financial Statements.

The Bank’s primary sources of funds consist of deposits, repayment of loans and mortgage-backed securities, maturities of investments and interest-bearing deposits, and funds provided from operations. While scheduled repayments of loans and mortgage-backed securities and maturities of investment securities are predictable sources of funds, deposit flows and loan prepayments are greatly influenced by the general level of interest rates, economic conditions and competition. The Bank uses its liquidity resources principally to fund existing and future loan commitments, to fund maturing certificates of deposit and demand deposit withdrawals, to invest in other interest-earning assets, to maintain liquidity, and to meet operating expenses.

Management believes that loan repayments and other sources of funds will be adequate to meet the Bank’s liquidity needs for the immediate future. A portion of the Bank’s liquidity consists of cash and cash equivalents. At December 31, 2010, cash and cash equivalents totaled $61.0 million. The level of these assets depends upon the Bank’s operating, investing and financing activities during any given period.

Cash flows from operating activities for the years ended December 31, 2010, 2009 and 2008 were $12.4 million, $2.7 million, and $7.7 million, respectively.

Cash flows from investing activities were a net use of funds of $41.0 million, $57.0 million and $142.8 million in 2010, 2009 and 2008, respectively. A principal use of cash in this area has been purchases of securities available for sale of $290.8 million partially offset by proceeds from sales, calls and maturities of securities of $221.9 million during 2010. At the same time, the investment of cash in loans was $19.9 million in 2009 and $55.6 million in 2008 while the loan portfolio provided cash of $24.7 million in 2010. Purchases of securities available for sale exceeded maturities and sales by $68.9 million in 2010, $37.8 million in 2009 and $100.9 million in 2008. There were no purchases of securities classified as held to maturity in 2010, 2009 and 2008.

At December 31, 2010, the Bank had $34.8 million in outstanding commitments to originate loans and unused lines of credit of $40.8 million. The Bank anticipates that it will have sufficient funds available to meet its current loan origination and lines of credit commitments. The Bank has certificates of deposit maturing in one year or less of $302.2 million at December 31, 2010. Based on historical experience, management believes that a significant portion of such deposits will remain with the Bank.

Impact of Inflation and Changing Prices

The consolidated financial statements and notes thereto presented herein have been prepared in accordance with accounting principles generally accepted in the United States of America, which require the measurement of financial position and operating results in terms of historical dollars without considering the change in the relative purchasing power of money over time and due to inflation. The impact of inflation is reflected in the increased cost of the Bank’s operations.

Unlike most industrial companies, nearly all the assets and liabilities of the Company are monetary in nature. As a result, changes in interest rates have a greater impact on the Company’s performance than do the effects of general levels of inflation. Interest rates do not necessarily move in the same direction or to the same extent as the price of goods and services.

18

Table of Contents

Forward-Looking Statements

Management’s discussion and analysis includes certain forward-looking statements addressing, among other things, the Bank’s prospects for earnings, asset growth and net interest margin. Forward-looking statements are accompanied by, and identified with, such terms as “anticipates,” “believes,” “expects,” “intends,” and similar phrases. Management’s expectations for the Bank’s future involve a number of assumptions and estimates. Factors that could cause actual results to differ from the expectations expressed herein include: substantial changes in interest rates, and changes in the general economy; changes in the Bank’s strategies for credit-risk management, interest-rate risk management and investment activities. Accordingly, any forward-looking statements included herein do not purport to be predictions of future events or circumstances and may not be realized.

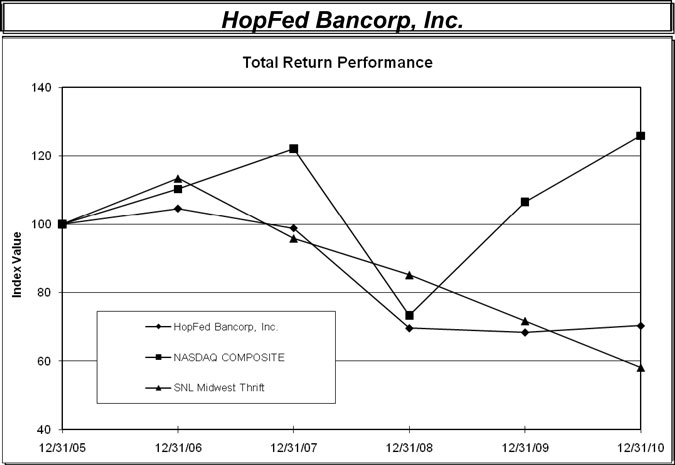

Stock Performance Comparison

The following graph, which was prepared by SNL Financial LC (“SNL”), shows the cumulative total return of the Common Stock of the Company since December 31, 2005, compared with the (1) NASDAQ Composite Index, comprised of all U.S. Companies quoted on NASDAQ, (2) the SNL Midwest Thrift Index, comprised of publically traded thrifts and thrift holding companies operating in the Midwestern United States. Cumulative total return on the Common Stock or the index equals the total increase in the value since December 31, 2005, assuming reinvestment of all dividends paid into the Common Stock or the index, respectively. The graph was prepared assuming that $100 was invested on December 31, 2005, in the Common Stock, the securities included in the indices. The stock price performance included in this graph is not necessarily indicative of future stock price performance.

19

Table of Contents

| Period Ending | ||||||||||||||||||||||||

| Index |

12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 | ||||||||||||||||||

| HopFed Bancorp, Inc. |

100.00 | 104.62 | 98.83 | 69.67 | 68.43 | 70.36 | ||||||||||||||||||

| NASDAQ COMPOSITE |

100.00 | 110.39 | 122.15 | 73.32 | 106.57 | 125.91 | ||||||||||||||||||

| SNL Midwest Thrift |

100.00 | 113.49 | 95.86 | 85.19 | 71.76 | 58.17 | ||||||||||||||||||

Source : SNL Financial LC, Charlottesville, VA

© 2011

20

Table of Contents

Consolidated Financial Statements

HopFed Bancorp, Inc.

and Subsidiaries

December 31, 2010, 2009 and 2008

Table of Contents

| Page Number | ||

| Report of Independent Registered Public Accounting Firm |

1 | |

| Consolidated Balance Sheets as of December 31, 2010 and 2009 |

2-3 | |

| Consolidated Statements of Income for the Years ended December 31, 2010, 2009 and 2008 |

4-5 | |

| Consolidated Statements of Comprehensive Income for the Years ended December 31, 2010, 2009 and 2008 |

6 | |

| Consolidated Statements of Changes in Stockholders’ Equity for the Years ended December 31, 2010, 2009 and 2008 |

7-8 | |

| Consolidated Statements of Cash Flows for the Years ended December 31, 2010, 2009 and 2008 |

9-10 | |

| Notes to Consolidated Financial Statements |

11-68 | |

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders

of HopFed Bancorp, Inc.

Hopkinsville, Kentucky

We have audited the accompanying consolidated balance sheets of HopFed Bancorp, Inc. and subsidiaries (the “Company”) as of December 31, 2010 and 2009, and the related consolidated statements of income, comprehensive income, changes in stockholders’ equity, and cash flows for each of the years in the three-year period ended December 31, 2010. These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of HopFed Bancorp, Inc. and subsidiaries as of December 31, 2010 and December 31, 2009, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2010, in conformity with accounting principles generally accepted in the United States of America.

/s/ Rayburn, Bates & Fitzgerald, P.C.

Brentwood, Tennessee

March 31, 2011