Attached files

| file | filename |

|---|---|

| EX-31.1 - China Internet Cafe Holdings Group, Inc. | v216179_ex31-1.htm |

| EX-32.1 - China Internet Cafe Holdings Group, Inc. | v216179_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

FORM 10-K

|

¨

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended _____________________________________________

or

|

x

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from July 1, 2010 to December 31, 2010

Commission file number: 000-52832

CHINA INTERNET CAFÉ HOLDINGS GROUP, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

98-0500738

|

|

|

State of other jurisdiction of

incorporation or organization

|

(I.R.S. Employer Identification No.)

|

|

#2009-2010, 4th Building, ZhuoYue Century Centre, FuHua third Road,

FuTian District, Shenzhen, Guangdong Province, People’s Republic of China

|

518048

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: 86-755-2894-3820

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Not Applicable

|

Not Applicable

|

Securities registered pursuant to section 12(g) of the Act:

|

Common Stock, $0.00001 par value

|

|

Title of Class

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. x Yes ¨ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company)

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

¨ Yes x No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Note.—If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided that the assumptions are set forth in this Form.

The aggregate market value of the voting and non-voting common stock of the issuer held by non-affiliates as of December 31, 2010was approximately $18,232,434 (9,116,217 shares of common stock held by non-affiliates) based upon the closing price of $2.00 per share of common stock as quoted by OTC Bulletin Board on March 18, 2011

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ¨ Yes ¨ No

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

As of March 4, 2011 there are 21,124,967shares of common stock, par value $0.00001 issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980).

TABLE OF CONTENTS

|

|

Page

|

||

|

|

|||

|

PART I

|

|||

|

Item 1.

|

Business.

|

3 | |

|

Item 1A.

|

Risk Factors.

|

15 | |

|

Item 1B.

|

Unresolved Staff Comments.

|

30 | |

|

Item 2.

|

Properties.

|

30 | |

|

Item 3.

|

Legal Proceedings.

|

30 | |

|

Item 4.

|

(Removed and Reserved).

|

30 | |

|

|

|

||

|

PART II

|

|||

|

Item 5.

|

Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

31 | |

|

Item 6.

|

Selected Financial Data.

|

33 | |

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

33 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. | 43 | |

| Item 8. | Financial Statements and Supplementary Data. | 43 | |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. | 43 | |

| Item 9A. | Controls and Procedures. | 43 | |

| Item 9B. | Other Information. | 43 | |

|

|

|||

|

PART III

|

|||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance.

|

44 | |

|

Item 11.

|

Executive Compensation.

|

47 | |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

|

49 | |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence.

|

50 | |

|

Item 14.

|

Principal Accountant Fees and Services.

|

51 | |

|

|

|||

|

PART IV

|

|||

|

Item 15.

|

Exhibits and Financial Statement Schedules.

|

52 | |

2

PART I

|

Item 1.

|

Business.

|

Our Corporate Structure

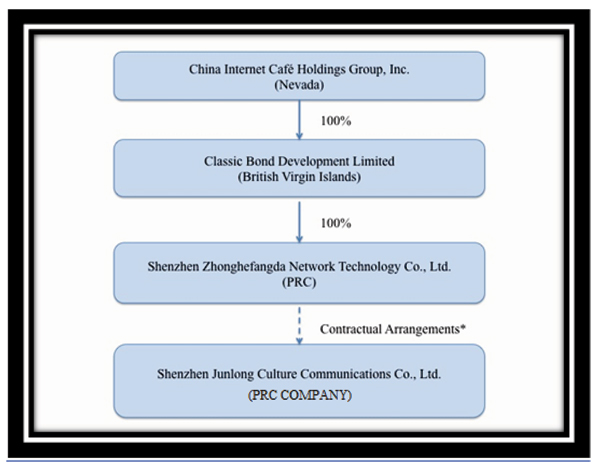

China Internet Café Holdings Group, Inc. (“we”, “us”, or the “Company”) is a Nevada holding company for our direct and indirect subsidiaries in the British Virgin Islands (“BVI”) and the People’s Republic of China (“PRC”). We own all of the issued and outstanding capital stock of Classic Bond, a BVI corporation. Classic Bond is a holding company that owns 100% of the outstanding capital stock of Shenzhen Zhonghefangda Internet Technology Co., Limited (“Zhonghefangda”), a PRC company.

Current PRC laws and regulations impose substantial restrictions on foreign ownership of the internet café business in the PRC. Therefore, our principal operations and sales and marketing activities in the PRC are conducted through Shenzhen Junlong Culture Communications Co., Ltd (“Junlong”), our variable interest entity (“VIE”), which holds the licenses and approvals for conducting the internet café business in the PRC.

Junlong was incorporated in the PRC in December 2003. It obtained its license to operate internet cafés in 2005. We control the VIE through a series of contractual arrangements. These contracts include a Management and Consulting Services Agreement, an Option Agreement, an Equity Pledge Agreement, and a Voting Rights Proxy Agreement. The Management and Consulting Services Agreement, dated June 11, 2010, is between our indirect, wholly owned subsidiary, Zhonghefangda, and our VIE. The rest of the agreements, also dated June 11, 2010, are among Zhonghefangda, our VIE and its shareholders. These contracts are summarized below. Please also refer to the full text of the contracts, which are filed as exhibits to this report.

|

|

·

|

Management and Consulting Services Agreement. Under the Management and Consulting Services Agreement between Junlong and Zhonghefangda, Zhonghefangda provides management and consulting services to the VIE in exchange for service fees up to 100% of the VIE’s Aggregate Net Profits (as defined in the agreement). In consideration for its right to receive the VIE’s aggregate net profits, Zhonghefangda will reimburse to the VIE the full amount of Net Losses (as defined in the Agreement) incurred by the VIE. During the term of the agreement, the VIE may not contract with any other party to provide services that are the same or similar to the services to be provided by Zhonghefangda pursuant to the agreement. The term of this agreement is 20 years, renewable for succeeding periods of the same duration until terminated pursuant to terms of the agreement.

|

|

|

·

|

Option Agreement. Under the Option Agreement, the shareholders of the VIE, Mr. Dishan Guo, Mr. Jinzhou Zeng and Ms. Xiaofen Wang, or the VIE Shareholders, who collectively own 100% of the equity interest in the VIE, granted Zhonghefangda an exclusive, irrevocable option to purchase all or part of their equity interests in the VIE, exercisable at any time and from time to time, to the extent permitted under PRC law. The purchase price of the equity interest will be equal to the original paid-in registered capital of the transferor, adjusted proportionally if less than all of the equity interest owned by the transferor is purchased.

|

|

|

·

|

Equity Pledge Agreement. The VIE Shareholders have pledged their entire equity interest in the VIE to Zhonghefangda pursuant to the Equity Pledge Agreement. The equity interests are pledged as collateral to secure the obligations of the VIE under the Management and Consulting Services Agreement and the VIE Shareholders’ obligations under the Option Agreement and the Proxy Agreement.

|

|

|

·

|

Voting Rights Proxy Agreement. Pursuant to the Voting Rights Proxy Agreement, each of the VIE Shareholders has irrevocably granted and entrusted Zhonghefangda with all of the voting rights as a shareholder of the VIE for the maximum period of time permitted by law. Each VIE Shareholder has also covenanted not to transfer his or her equity interest in the VIE to any party other than Zhonghefangda or a designee of Zhonghefangda.

|

We believe that the terms of these agreements are no less favorable than the terms that we could obtain from disinterested third parties. According to our PRC counsel, China Commercial Law Firm, our conduct of business through these agreements complies with existing PRC laws, rules and regulations.

3

As a result of these contractual arrangements, Junlong became our controlled VIE. A variable interest represents a contractual or ownership interest in another entity that causes the holder to absorb the changes in fair value of the other entity’s net assets. Potential variable interests include: holding economic interests, voting rights, or obligations to an entity; issuing guarantees on behalf of an entity; transferring assets to an entity; managing the assets of an entity; leasing assets from an entity; and providing financing to an entity. In such cases consolidation of the VIE is required by the enterprise that controls the economic risks and rewards of the entity, regardless of ownership. We have consolidated Junlong’s historical financial results in our financial statements as a variable interest entity pursuant to U.S. generally accepted accounting principles (“GAAP”).

The following chart reflects our organizational structure as of the date of this report.

*Contractual agreements consisting of a management and consulting service agreement, equity pledge agreement, option agreement and proxy agreement, which allow the Company to control Junlong.

Our Corporate History

We were incorporated under the name China Unitech Group, Inc. in the State of Nevada on March 14, 2006. From our office in China, we planned to operate in the online travel business using the website www.chinabizhotel.com. The website was planned to offer viewers the ability to book hotel rooms in China and earn us booking fees from the respective hotels. However, we did not engage in any operations and were dormant from our inception until our reverse acquisition of Classic Bond on July 2, 2010. As a result of the reverse acquisition, we ceased to be a shell company on July 2, 2010.

4

Acquisition of Classic Bond

On July 2, 2010, we completed a reverse acquisition transaction through a share exchange with Classic Bond and its shareholders, whereby we acquired 100% of the issued and outstanding capital stock of Classic Bond, in exchange for 19,000,000 shares of our common stock, which shares constituted 94% of our issued and outstanding shares on a fully-diluted basis, as of and immediately after the consummation of the reverse acquisition. As a result of the reverse acquisition, Classic Bond became our wholly owned subsidiary and the former shareholders of Classic Bond, became our controlling shareholders. The share exchange transaction with Classic Bond was treated as a reverse acquisition, with Classic Bond as the acquirer and China Internet Café Holdings Group, Inc. as the acquired party. Unless the context suggests otherwise, when we refer in this report to business and financial information for periods prior to the consummation of the reverse acquisition, we are referring to the business and financial information of Classic Bond and its consolidated subsidiaries.

Upon the closing of the reverse acquisition, Xuezheng Yuan, our sole director and officer, submitted a resignation letter pursuant to which he resigned, with immediate effect, from all offices that he held and from his position as our sole director that became effective on the August 13 2010, ten days following the mailing by us of an information statement to our stockholders complying with the requirements of Section 14f-1 of the Exchange Act (the “Information Statement”). Also upon the closing of the reverse acquisition, our board of directors increased its size from one to five members and appointed Dishan Guo, Zhenquan Guo, Lei Li, Wenbin An and Lizong Wang to fill the vacancies created by the resignation of Xuezheng Yuan and such increase. Mr. Dishan Guo's appointment became effective upon closing of the reverse acquisition, while the remaining appointments became effective on August 13, 2010, the tenth day following our mailing of the Information Statement to our stockholders. In addition, our executive officers were replaced by the Classic Bond executive officers upon the closing of the reverse acquisition as indicated in more detail below.

As a result of our acquisition of Classic Bond, we now own all of the issued and outstanding capital stock of Classic Bond. Classic Bond was incorporated in the British Virgin Islands on November 2, 2009 to serve as an investment holding company. Junlong was incorporated in the PRC in December 2003. It obtained its first licenses from the Ministry of Culture to operate an internet café chain in 2005 and opened its first internet café in April 2006.

On July 2, 2010, our board of directors approved a change in our fiscal year end from June 30 to December 31, which was effectuated in connection with the reverse acquisition transaction described above.

On January 20, 2011, China Internet Café Holdings Group, Inc. (the “Company”) filed with the Nevada Secretary of State an amendment to its Amended and Restated Articles of Incorporation to give effect to a name change from “China Unitech Group, Inc.” to “China Internet Café Holdings Group, Inc.” The Amended and Restated Articles of Incorporation were approved by our board of directors on July 30, 2010 and were approved by a stockholder holding 59.45% of our outstanding common stock by written consent on July 30, 2010. In connection with the name change, on January 25, 2011, the Company filed an Issuer Company-Related Action Notification Form with the Financial Industry Regulatory Authority (“FINRA”) requesting a name change from “China Unitech Group, Inc.” to “China Internet Café Holdings Group, Inc.” as well as an OTC voluntary symbol change from “CUIG” to “CICC.” These changes became effective on February 1, 2011. Our common stock began trading under the Company’s new name on the Over-the Counter Bulletin Boards on Tuesday, February 1, 2011 under our new trading symbol “CICC”.

On February 16, 2011, the Company filed with the Secretary of State of Nevada a Certificate of Designation, Preferences and Rights for the 5% Series A Convertible Preferred Stock (the “Certificate of Designation”) as an amendment to its Articles of Incorporation. Capitalized terms not defined herein shall have the meaning ascribed to them in the Certificate of Designation.

For each outstanding share of Series A Preferred Stock, dividends shall be payable quarterly, at the rate of 5% per annum, on or before each date that is thirty days following the last day of each June, September, December and March of each year. Dividends on the Series A Preferred Stock shall accrue and be cumulative from and after the date of the initial issuance of the Series A Preferred Stock.

Upon liquidation of the Company, holders of Series A Preferred Stock are entitled to be paid, prior to any distribution to any holders of common stock, or any other class or series of stock issued hereafter or junior to the Series A Preferred Stock, an amount equal to $1.35 per share plus the amount of any accrued but unpaid dividends thereon, as of the date of liquidation (the “Series A Liquidation Preference Amount”).

5

Each share of Series A Preferred Stock at the option of the holder may be convertible into a number of fully paid and nonassessable shares of Common Stock equal to the quotient of (i) the Series A Liquidation Preference Amount divided by (ii) the Conversion Price in effect as of the date of the Conversion Notice.

Until conversion, the Preferred Stock shall have no voting rights other than with respect to matters that may adversely affect the rights of the holders of the Series A Preferred Stock.

The description of the Series A Preferred Stock above is qualified in its entirety by reference to a copy of the Certificate of Designation attached to this Annual Report on Form 10-K.

On February 22, 2011, in connection with a security purchase agreement between the Company and the investors identified on Exhibit A thereto (collectively, the “Investors”), we closed a private placement of approximately $6.4 million from offering a total of 474,967 units (the “Units”) at a purchase price of $13.50 per Unit, each consisting of:(i) nine shares of the Company’s 5% Series A Convertible Preferred Stock, par value $0.00001 per share (the “Preferred Shares”), convertible on a one to one basis into nine shares of the Company’s common stock, par value $0.00001 per share (the “Common Stock”); (ii) one share of Common Stock; (iii) two three-year Series A Warrants (the “Series A Warrants”),each exercisable for the purchase of one share of Common Stock, at an exercise price of $2.00 per share; and (iv) two three-year Series B Warrants (the “Series B Warrants”), each exercisable for the purchase of one share of Common Stock, to purchase one share of Common Stock, at an exercise price of $3.00 per share.

Business Overview

We operate a chain of 46 internet cafés in Shenzhen, Guangdong, PRC that are generally open 24 hours a day, seven days a week. We provide top quality internet café facilities and we believe we are the largest internet café chain in Shenzhen. We provide internet access at reasonable prices to students and migrant workers. Although we sell snacks, drinks, and game access cards, over 95% of our revenue comes from selling access time to our computers. We sell internet café memberships to our customers. Members purchase prepaid IC cards (a pocket-sized card with embedded integrated circuits that can be used for identification, authentication, data storage and application processing), which include stored value that will be deducted based on time usage of a computer at the internet café. The cards are only sold at our cafés. We deduct the amount that reflects the access time used by a customer when the customer’s IC card is inserted into the IC card slot on the computer.

Background on Internet Cafés in the PRC

Internet cafés have been booming in the PRC in the recent years. According to the "Survey of China Internet Café Industry" by the Ministry of Culture in 2005, the PRC had 110,000 internet cafés, with more than 1,000,000 employees and contributing RMB 18,500,000,000 to China's GDP. According to an article entitled “China Surpasses U.S. in Number of Internet Users” written by David Barboza on the New York Times July 26, 2008 issue, the number of internet users in the PRC reached about 253 million in June 2008, thereby, putting China ahead of the United States as the world’s biggest internet market. According to the research conducted by China Internet Network Information Center(CNNIC) in March 2011, the amount of internet users in China in 2009 was 385 million, 135 million of which (35.1%) surf the internet via internet cafes. By the end of 2010, the amount of internet users in China reached 457 million, 35.7% of which surf the internet via internet cafes. It is clear that internet cafés have been a fast growing segment of the Chinese internet market.

The internet café market in the PRC, like most places worldwide, originally started out simply as a location to access the internet. However, PRC internet cafés have changed into full service entertainment centers where people can relax outside work and home. These cafés provide services that are vastly different from the internet cafés initially established in the PRC. They provide decent facilities at a reasonable fee, with specific configuration for online games and audio visual entertainment. They are a source of cost effective entertainment for low-income earners who cannot afford computers, game consoles or an internet connection, such as migrant workers and students. In internet cafés, customers have access to popular online games and can either socialize or entertain themselves. Players gather together in internet cafés for games such as World of Warcraft (WOW) and Call to Arms, played either with their friends in the café or with users across the globe.

6

Due to tightened regulations on the operations of internet cafés, there are currently around 81,000 internet cafés in the PRC (Source: “Internet café ban call draws Chinese hacker wrath”. AFP 3 Mar 2010. http://www.google.com/hostednews/afp/article/ALeqM5gJus4tWVAaeWI8IoS-n238PYpFjw).The largest chain has over 1,000 locations. There are currently 10 chains which have licenses to operate nationally.

Computer Gaming Industry in China

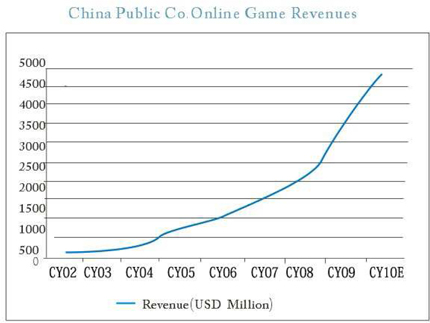

According to Pearl Research, a business intelligence and consulting firm, the PRC online game market rose 63% in 2008 to $2.8 billion, rose 36% in 2009 to $3.8 billion, and rose 26% in 2010 to $4.8 billion. Given the relatively low rate of computer ownership in the PRC as compared to Western countries, internet cafés have become the primary distribution point for games in the PRC. A substantial number of game players access online games through internet cafés and these players are crucial for survival of internet cafés. The chart below shows the robust revenue growth of online game companies from 2003 to 2010.

The following diagram prepared by Morgan Stanley depicts the interdependent relations between online game developers and internet cafés. (Source: Ji Richard and Meeker, Mary. "Creating Consumer Value in Digital China" Morgan Stanley Equity Research Global. September 12, 2005.)

7

Given the pivotal position of internet cafés, many online game companies have been making great efforts to support internet cafés to expand their customer base.

Partnerships between Internet Cafés and Other Online Information Providers

Besides games, internet cafés are able to develop partnerships with other online information providers. These companies provide games as well as other information services. As can be seen by the chart below, these providers have significant revenues and profits.

|

2010 Q4 Revenue

|

||||||||||||||||||||

|

Company

|

Million US$

|

YOY

|

Net Profit

|

%Net

|

Market Cap

|

|||||||||||||||

|

Tencent Q3

|

$ | 5,277 | 55.10 | % | $ | 2,168.0 | 41.18 | % | $ | 49,230 | ||||||||||

|

Shanda

|

$ | 174 | -13.70 | % | $ | 55.4 | 31.84 | % | $ | 1,653 | ||||||||||

|

Netease

|

$ | 254 | 30.77 | % | $ | 108.0 | 42.43 | % | $ | 5,926 | ||||||||||

|

ChangYou

|

$ | 92 | 30 | % | $ | 47.8 | 52.13 | % | $ | 1,966 | ||||||||||

|

Giant

|

$ | 56 | 33.40 | % | $ | 35.0 | 62.72 | % | $ | 1,802 | ||||||||||

|

Perfect World Q3

|

$ | 98 | 12 | % | $ | 31.9 | 32.42 | % | $ | 1,019 | ||||||||||

|

Kingsoft Q3

|

$ | 35 | -6.95 | % | $ | 12.9 | 37.12 | % | $ | 597 | ||||||||||

|

NetDragon Q3

|

$ | 19 | -15 | % | $ | 0.4 | 2.21 | % | $ | 283 | ||||||||||

|

DragonCity Q2

|

$ | 3.7 | -0.91 | % | $ | 0.5 | 0.1351 | % | $ | 188 | ||||||||||

|

Total

|

$ | 5,959 | $ | 2,459.96 | $ | 62,664 | ||||||||||||||

(Source: I Research. “China Online Game Quarterly Research Report” Jan 2011. )

8

Competitive Strengths

We believe that the following competitive strengths enable us to compete effectively in and to capitalize on growth in the internet café market in the PRC:

|

|

·

|

Company-owned Cafés. Unlike most of our competitors who franchise their internet cafés, all of our cafés are direct outlets. This model makes it easier to carry out management decisions at each of our cafés. It also allows us to maximize operating profit and create a consistent name brand.

|

|

|

·

|

Good Scale of Operation. We have a registered capital of RMB 10 million (approximately $1.47 million) with 36 cafés. The scale of operations allows us to control cost and standardize store management.

|

|

|

·

|

Proprietary Software. We developed the software “SAFLASH” that provides fast and stable internet connections. Its automatic flow control prevents users from being disconnected when there is a disruption of internet traffic. Stability is a key requirement for online gamers. Our research and development team is working constantly to improve the software.

|

|

|

·

|

Government and Industry Relations. We have developed an excellent working relationship with the government that has assisted us to better comply with internet café related laws and regulations and to understand regulatory trends in our industry. Our CEO and CFO, Mr. Dishan Guo, is the executive president of Shenzhen Longgang District Internet Industry Association. This association is an associated department of the Ministry of Culture and sets the internet café industry standards. As a result of his involvement, Mr. Guo gains valuable insight into new standards and may also have the opportunity to influence industry standards.

|

|

|

Centralized Oversight. All of our café managers are trained by, and under the supervision of, our centralized operations manager, who is based at our headquarters. As a result, our local managers are able to effectively handle operational issues at the cafés. The local managers are trained to provide a service level that meets Junlong’s service standards, and our operations manager is able to effectively enforce policies and procedures implemented by us.

|

Our Growth Strategy

We are committed to enhancing our sales, profitability and cash flows through the following strategies:

|

|

·

|

We will seek to grow by business expansion. We plan to expand in the southwest and mid-east regions of the PRC through acquisitions of local small chains, in order to meet the requirements of applying for a national chain license. The national chain license requires 30 internet cafés in three provinces. We plan to accomplish acquisitions of internet cafés in Guizhou in the third quarter, and Sichuan in the fourth quarter in order to help us satisfy the requirements of obtaining a national chain license. We also want to fully develop our wholly-owned branches through effective integration of resources. Most of our current competitors that offer franchising simply provide a franchise license to entrepreneurs to get started in exchange for a yearly fee. Junlong, on the other hand, is deeply involved in the operational management of its company-owned cafés. After we obtain a national chain license, we will focus on developing high-end internet cafés in the more developed cities to create new concepts of internet café operation. We expect to spread to the less developed cities in three years in order to gain competitive market shares. We plan to put 20% of our resources to the less developed cities for market integration after we are granted a national license, which will effectively lay the foundation for us in those cities.

|

|

|

·

|

We will seek to grow by improving our company structure. To optimize our resources and operations, we plan to improve our company structure so that 20% of our internet cafés will be large stores, each with 300 or more computers mainly focusing on movies, high-end games and entertainment; 50% of cafés will be medium stores with 150 to 300 computers and a few movie suites focusing on high-end games; 10% of cafés will be small stores in the developed cities to spread our reputation with 100 to 150 computers. In order to penetrate the less developed cities, we want to open 20% of our stores in those cities. Our mission is to set up internet cafés all over the PRC to become a real national chain and the industry leader, and we have begun to implement these plans in the first quarter of 2011.

|

9

|

|

·

|

We will seek to grow by location selection. Running internet cafés is a retail business. Internet cafés are located in highly populated areas so as to attract customers. Junlong’s internet cafés are located at busy and well attended areas such as industrial zones and business quarters. We conducted market research in Sichuan, Guizhou, and Yunan provinces and Chonqing municipalities in March2011. As a result of this market research, we have identified the university areas in Sichuan and Chongqing, the residential areas and business quarters in Yunan and Guizhou as prime areas for the establishment of internet cafés. Our future expansion in the south-western region will be built on the basis of these locations beginning with Guizhou in the second quarter of 2011, Yunnan in the fourth quarter of 2011, and Sichuan in the year 2012.

|

Internet café members purchase prepaid IC cards which include stored value that is deducted based on time usage of a computer at the internet café. The cards are only sold at our cafés. We deduct from the stored value amount to reflect customer usage when the customers’ IC cards are inserted into the IC card slot on the computer. Revenues derived from the prepaid IC cards at the internet café are recognized when services are provided. Below is our IC card sample.

Outstanding customer balances on the IC cards are included in deferred revenue on the balance sheets. We do not charge any service fees that cause a decrease in customer balances.

The basic membership comes with the IC card and costs RMB 10 (approximately $1.52) on top of the initial credits deposited. Members receive a discount (e.g. RMB 50 (approximately $7.60) deposit gets RMB 60 (approximately $9.12) credit in the IC card). There is no expiration date for IC cards, but money deposited into the IC cards is not refundable.

Software on the Computers

We have on average 239 computers in each location and a total of 10,989 computers for the 46 cafés as of March 23, 2011. We install more than 100 online games on each of our computers. We also provide movies, music and online chatting software. We use Microsoft Word compatible software called “WPS,” which is a freeware provided by Kingsoft, a Chinese software company, so that we do not pay for the higher priced Microsoft Office license.

10

Third Party Gaming Cards, Snacks and Drinks

We also sell third party on-line gaming cards, snacks and drinks. The commission for the sale of gaming cards is generally 20% of the value of the cards. Concessions (snacks and drinks) are also sold to customers.

We are considering opening more “luxury” cafés in the future to meet the needs of high income groups. This strategy is only in the planning stage. Further, although this is potentially a very interesting marketing and branding tool, we do not expect these locations to significantly increase our overall revenues.

Franchising

We own all of our cafés. However, beginning in 2012 we anticipate utilizing a modified franchise model as well. We expect that our franchisees will pay the startup costs for a new internet café. After the initial investment, we will select the location and staff and provide the staff with intensive training to run the café. Once the café becomes operational, our employees will run the café and provide management support. We expect the franchisee to be more akin to an investor than an owner/operator. We will pay the franchisee a percentage of the café’s profit for providing the funds necessary to open the café and operate it.

Our Customers

Our customers are individuals who come into the location to surf the internet and/or play online games with their friends locally and remotely with individuals around the world.

Internet café users are mainly young males with low incomes, mainly migrant workers. At our cafés, migrant workers are provided a convenient channel at low cost to communicate with their families and friends. For example, VOIP (Voice over IP) service at the café is much cheaper than any other telecommunications method. Low income earners can arrange a time to chat online with their friends and families in their home cities.

We estimate that at our internet café approximately 50% of computer time is spent on gaming, 30% for other entertainment (e.g. online chatting, online movies, or online music); and 20% for other purposes (e.g. work).

In the last few years there has been a decrease in the number of internet café users as a result of increased availability of internet connections at home. However, we believe that we will be able to maintain organic growth by providing quality services to our core customers. Even if someone has internet access in their home or dormitory, these locations do not provide the atmosphere and services provided by internet cafés at a reasonable cost. For example, if a computer is set up in the limited space of a dormitory, an additional internet connection would need to be purchased. A computer suitable for online gaming costs RMB 5,000 (approximately $760.47) or more. The monthly rent for an ADSL connection costs an additional RMB 100 (approximately $15.21) and even this may not be good enough for some online games such as WOW. In these types of games, there is a very important play mode called RAID, where, for example, 40 people are needed on a team to kill some monster in the dungeon. This requires all players to have very stable internet connections. A typical low-end computer and ADSL connection would suffer significant lags and cause performance issues. Internet cafés, on the other hand, can provide high speed computers and internet connections at much lower cost to the players.

In the year 2012 we plan to open internet cafés around university areas in the south-western provinces including Sichuan and Chongqing. Students spend more time in internet cafés because their time is very flexible. We believe that major users of internet cafés in the future will be young game players.

11

There are approximately 130,000 Internet cafés in the PRC in 2010. (Source: http://www.cnnic.com “The 27th CNNIC Report” (accessed January 2010)) The market is extremely fragmented. One of the largest national chains which has around 1,000 locations has less than 2% of the national market. The following describes some of the local, regional and national competitors.

Local Competitors in Shenzhen

|

|

·

|

Shenzhen Weiwo Internet Café Chain Company. Weiwo was founded in 1997. Currently, Weiwo has 14 cafés. The company mainly operates a franchise model, with only 3 company owned cafés. The cafés are mainly located in Futian district, Shenzhen City. The company concentrates on mid-range market. Each café is relatively small with 100 to150 computers (for a total of around 1,600 computers). Its franchised stores are charged a franchising fee per month of approximately RMB 5,000 (approximately $735.29). Weiwo is the smallest internet café chain company in Shenzhen.

|

|

|

·

|

Shenzhen Bian Internet Co. Ltd. Although the company entered into the internet café industry in 2003, its current structure was founded on February 22, 2007 and obtained its regional internet café chain license in 2007. The company operates mostly as a franchise model with 30 registered café, only 3 of which are directly owned by the company. Each café has 80-150 computers. It also has a few large cafés with more than 200 computers. The estimated total number of computers owned by the company is 4,500. There is a significant turnover in franchise ownership with around one third of the franchise cafés transferring their licenses to other internet café owners.

|

|

|

·

|

Quansu Internet Café Chain Company. Quansu was founded in 1998 as a subsidiary investment project of the Shenzhen Commercial Bank Investment Co. Ltd. The company owns 36 cafés, 8 of which are directly owned and 28 of which are franchises. Each café has 80-150 computers. The total number of computers is approximately 6,200. The cafés are located in Baoan District, Futian District and Luohu District. In May 2009, Quansu switched its major business towards its internet cable connection business and public telephone business.

|

National Competitors

Currently there are ten national internet café chains:

|

|

·

|

Zhongqing Network Home Co., Ltd.

|

|

|

·

|

Beijing Cultural Development Co., Ltd.

|

|

|

·

|

China Digital Library Co., Ltd.

|

|

|

·

|

Yalian Telecommunication Network Co., Ltd.

|

|

|

·

|

China Heritage Information Center

|

|

|

·

|

Capital Networks Limited

|

|

|

·

|

Great Wall Broadband Network Service Co., Ltd.

|

|

|

·

|

China United Telecommunications Co., Ltd. (China Unicom)

|

|

|

·

|

CLP Chinese Tong Communication Co., Ltd.

|

|

|

·

|

Reid Investment Holding Company

|

The ten national chains generally have strong financial support. However, to our knowledge these chains have not been successful in expanding their operations.

Competitors in Potential Markets

As we plan to expand our operations in other major cities, we identify the following competitors in the potential new markets where we expect to operate in the future:

12

|

|

·

|

Kunming – Yunnan Jin-Zhao Yuan Culture Communication Network Co., Ltd. The company was founded on May 1, 2003 by the Yunnan Provincial Department of Culture. It obtained its business license and registration to operate a chain of Internet cafés from the Industrial and Commercial Bureau of Yunnan Province on April 31, 2004. It has a registered capital of RMB 10 million. The company has opened approximately 19cafés with an average of 200 computers in each café and a total of nearly 4,000 computers.

|

|

|

·

|

Chengdu – Chengdu Shang Dynasty Networks Co., Ltd. The company was founded in 2002 with a registered capital of RMB 12 million. It would be most accurately described as a multifunctional entertainment facility with coffee bars and multi-function rooms. Its facilities have full range of digital entertainment including hardware and software products, and professional e-sport training. The company has four wholly owned cafés, and has more than 20,000 registered members.

|

Intellectual Property

Trademark

Junlong owns the trademark Junlong, as specified in the Registration Certificate No. 4723040 issued by the Trademark Office under the State Administration of Industry and Commerce of the PRC. The registration is valid from January 28, 2009 to January 27, 2019.

Domain Name

We own and currently utilize the domain name, www.cnculture.com.cn. We have recently also acquired the domain name www.chinainternetcafé.com, which we believe better reflects our business. We will transition from our old domain name to our new one during the third quarter of 2010.

Software

The main piece of intellectual property for Junlong is the SAFLASH software. This software, developed on a Microsoft Windows platform, increases internet connection stability. Its automatic flow control prevents users from being disconnected when there is a disruption in internet traffic. The stability is a key requirement for online gamers.

Although there are no patents or copyrights for this software, it is only used internally on our computer systems and is not available for download. We also entered into a confidentiality agreement with the IT manager Zhenfan Li whose team developed this software. Our competitive advantage lies in continually updating SAFLASH to assure internet connection stability.

Because our controlled VIE is located in the PRC, we are regulated by the national and local laws of the PRC.

In 2001, the PRC government imposed a minimum capital requirement of RMB 10 million (approximately $1.47 million) for regional café chains and RMB 50 million (approximately $7.35 million) for national café chains. On September 29, 2002, Ministry of Information Industry, Ministry of Public Security, Ministry of Culture and State Administration for Commerce and Industry issued “Regulations on the Administration of Business Sites of Internet Access Services.” The regulations require a license to operate internet cafés which may not be assigned or leased to any third parties. The regulations also have detailed provisions regarding internet cafes’ business operations and security control.

13

We have been in compliance of these regulations. In August 2004, we increased our registered capital to RMB 10 million (approximately $1.46 million). In 2005, Junlong obtained internet café licenses of operating internet café chain in Shenzhen from the local counterpart of Ministry of Culture.

The Ministry of Culture of China is in charge of regulating national internet café chains. To obtain a license to operate a national internet café chain, an applicant must, among other things, (i) a minimum registered capital of RMB 50 million, (ii) own or control at least 30 internet cafés, which shall cover at least three provinces or municipalities under direct administration of the State Council, and (iii) have been in full compliance with administrative regulations with respect to internet cafés for at least one year before submitting the application. Other requirements include having appropriate computer and ancillary facilities, necessary and qualified personnel and sound internal policy. Application for a national internet café chain shall be first made to the provincial counterpart of the Ministry of Culture. After preliminary approval, the provincial authority will submit the application to the Ministry of Culture for final approval. In rendering its approval, the authorities consider such factors as the then existing number of the internet café chains.

We are subject to PRC foreign currency regulations. The PRC government has controlled Renminbi reserves primarily through direct regulation of the conversion of Renminbi into other foreign currencies. Although foreign currencies, which are required for “current account” transactions, can be bought at authorized PRC banks, the proper procedural requirements prescribed by PRC law must be met. At the same time, PRC companies are also required to sell their foreign exchange earnings to authorized PRC banks, and the purchase of foreign currencies for capital account transactions still requires prior approval of the PRC government.

Under current PRC laws and regulations, Foreign Invested Entities, or FIEs, may pay dividends only out of their accumulated after-tax profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, FIEs in China are required to set aside at least 10% of their after-tax profit based on PRC accounting standards each year to their general reserves until the cumulative amount of such reserves reaches 50% of their registered capital. These reserves are not distributable as cash dividends. The board of directors of an FIE has the discretion to allocate a portion of the FIEs’ after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

Our Employees

As of December 31, 2010, we had 523 employees. The following table sets forth the number of employees by function:

|

Number of

|

|||

|

Function

|

Employees

|

||

|

Senior Management

|

55

|

||

|

Accounting

|

16

|

||

|

Staff employees

|

452

|

||

|

Total

|

|

523

|

As required by applicable PRC law, we have entered into employment contracts with most of our officers, managers and employees. We are working towards entering employment contracts with those employees who do not currently have employment contracts with us. We believe that we maintain a satisfactory working relationship with our employees, and we have not experienced any significant disputes or any difficulty in recruiting staff for our operations.

Litigation

From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. We are currently not a party to any legal proceeding and are not aware of any legal claims that we believe will have a material adverse effect on our business, financial condition or operating results.

14

|

Item 1A.

|

Risk Factors.

|

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

RISKS RELATED TO OUR BUSINESS

Our limited operating history makes evaluating our business and prospects difficult.

Our VIE, Junlong, was established in December 2003 and obtained the license to operate internet cafés in Shenzhen in 2005. Our limited operating history may not provide a meaningful basis for you to evaluate our business and prospects. Our business strategy has not been proven over time and we cannot be certain that we will be able to successfully expand our business.

Fluctuations in operating results or the failure of operating results to meet the expectations of public market analysts and investors may negatively impact the market price of our securities. Operating results may fluctuate in the future due to a variety of factors that could affect revenues or expenses in any particular quarter. Fluctuations in operating results could cause the value of our securities to decline. Investors should not rely on comparisons of results of operations as an indication of future performance. As a result of the factors listed below, it is possible that in future periods results of operations may be below the expectations of public market analysts and investors. This could cause the market price of our securities to decline. Factors that may affect our quarterly results include:

|

|

|

vulnerability of our business to a general economic downturn in the PRC;

|

|

|

|

changes in the laws of the PRC that affect our operations;

|

|

|

|

competition from other similar service providers; and

|

|

|

|

our ability to obtain necessary government certifications and/or licenses to conduct our business.

|

We are dependent on our management team and the loss of any key member of that team could have a material adverse effect on our operations and financial condition.

We attribute our success to the leadership and contributions of our managing team comprising executive directors and key executives, in particular, to our Chief Executive Officer and Chief Financial Officer, Dishan Guo and our Chief Technology Officer Zhenfan Li.

Our continued success is therefore dependent to a large extent on our ability to retain the services of these key management personnel. The loss of their services without timely and qualified replacement, will adversely affect our operations and hence, our revenue and profits.

We have not obtained social insurance benefits for all of our employees and could incur administrative fines and penalties that could materially affect our financial condition and reputation.

We have obtained social benefits coverage for employees who work at the headquarters of Junlong. For other employees, because of the high mobility of their work, they usually work on a probationary basis and will not enter into a long employment relationship with us. We are subject to administrative fines and penalties as a result of our failure to obtain social insurance for these employees. The amount of these fines and penalties, in the aggregate, may adversely affect our financial condition and our public image.

15

Tightened regulations on internet cafés may adversely affect our operations and revenues.

The PRC government has been tough on internet café regulations. In 2003, the PRC government imposed a minimum capital requirement of RMB 10 million (approximately $1.47 million) for regional café chains and RMB 50 million (approximately $7.32 million) for national café chains. On September 29, 2002, the State Council issued “Regulations on the Administration of Business Sites of Internet Access Services.” The regulations require a license to operate internet cafés which may not be assigned or leased to any third parties. The regulations also have detailed provisions regarding internet cafes’ business operations and security control. The number of internet cafés in China was reduced after these regulations went effective.

If the PRC government decided to impose more stringent regulations on internet cafés and their operations, our business may be adversely affected and our revenues may decrease as a result.

There may be reduced use of internet cafés with the increase in computer ownership and internet connections at home and any such reduction would negatively affect our financial performance.

With the rapid economic development and growing disposable income, computer ownership and internet connections at home will gradually increase as the price for computer hardware, software and internet access decreases. Although internet cafés provide easy access to the latest games, movies and music, fast and stable internet connections and a sense of community, there is no guarantee that individuals will continue to use internet cafés when they can have internet access at home.

Negative media coverage of internet cafés may reduce the number of customers that visit our internet cafés and result in lower revenues.

In the last few years there have been several negative stories in the media about internet cafés. A fatal fire in Beijing's Lanjisu Internet café in June 2002 raised nationwide concern about the country’s burgeoning internet café business. In 2006, a report from the China National Children's Center, a government think-tank, said that 13 percent of the PRC's 18 million internet users under 18 were internet addicts. Responding to the problems associated with internet cafés, the PRC imposed more stringent laws and regulations on internet cafés. In 2007, fearful of soaring internet addiction and juvenile crime, the PRC banned the opening of new internet cafés for a year. Such negative media coverage may result in stricter government regulations and reduced number of customers.

Interruption or failure of our own information technology and communications systems or those of third-party service providers we rely upon could impair our ability to effectively provide our services, which could damage our reputation and harm our operating results.

Our ability to provide our services depends on the continuing operation of our information technology and communications systems. Any damage to or failure of our systems could interrupt our service. Service interruptions could reduce our revenues and profits, and damage our brand if our system is perceived to be unreliable. Our systems are vulnerable to damage or interruption as a result of terrorist attacks, wars, earthquakes, floods, fires, power loss, telecommunications failures, undetected errors or “bugs” in our software, and computer viruses.

Our servers are vulnerable to break-ins, sabotage and vandalism. The occurrence of a natural disaster or a closure of an Internet data center by a third-party provider without adequate notice could result in lengthy service interruptions.

The steps we take to increase the reliability and redundancy of our systems are expensive, reduce our operating margin and may not be successful in reducing the frequency or duration of service interruptions.

Our business may be adversely affected by third-party software applications or practices that interfere with our receipt of information from, or provision of information to, our customers, which may impair our customers’ experience.

Our business may be adversely affected by third-party malicious or unintentional software applications that make changes to our computers and interfere with our services. These software applications may be difficult or impossible to remove or disable, may reinstall themselves and may circumvent other applications’ efforts to block or remove them. The ability to provide a superior user experience is critical to our success. If we are unable to successfully combat third-party software applications that interfere with our products and services, our reputation may be harmed.

16

The successful operation of our business depends upon the performance and reliability of the Internet infrastructure and fixed telecommunications networks in China.

Our business depends on the performance and reliability of the Internet infrastructure in China. Almost all access to the Internet is maintained through state-owned telecommunication operators under the administrative control and regulatory supervision of the Ministry of Industry and Information Technology (or its predecessor, the Ministry of Information Industry, before its formal establishment in 2008), or the MIIT. In addition, the national networks in China are connected to the Internet through international gateways controlled by the PRC government. These international gateways are the only channels through which a domestic user can connect to the Internet. We cannot assure you that a more sophisticated Internet infrastructure will be developed in China. We may not have access to alternative networks in the event of disruptions, failures or other problems with China’s Internet infrastructure. In addition, the Internet infrastructure in China may not support the demands associated with continued growth in Internet usage.

Any unscheduled service interruption could damage our reputation and result in a decrease in our revenues. Furthermore, if the prices that we pay for telecommunications and Internet services rise significantly, our gross margins could be adversely affected.

Concerns about the security of electronic commerce transactions and confidentiality of information on the Internet may reduce use of our internet cafes and impede our growth.

A significant barrier to electronic commerce and communications over the Internet in general has been a public concern over security and privacy, including the transmission of confidential information. If these concerns are not adequately addressed, they may inhibit the growth of the Internet and other online services generally, especially as a means of conducting commercial transactions. If a well-publicized Internet breach of security were to occur, general Internet usage could decline, which could cause our operations to be adversely affected.

Regulation and censorship of information disseminated over the Internet in China may adversely affect our business.

The PRC government has adopted regulations governing Internet access and the distribution of news and other information over the Internet. Under these regulations, Internet content providers and Internet publishers are prohibited from posting or displaying over the Internet content that, among other things, violates PRC laws and regulations, impairs the national dignity of China, or is reactionary, obscene, superstitious, fraudulent or defamatory. Failure to comply with these requirements may result in the revocation of licenses to provide Internet content and other licenses and the closure of the concerned websites.

The Ministry of Public Security has the authority to order any local Internet service provider to block any Internet website at its sole discretion. From time to time, the Ministry of Public Security has stopped the dissemination over the Internet of information which it believes to be socially destabilizing. The State Secrecy Bureau is also authorized to block any website it deems to be leaking state secrets or failing to meet the relevant regulations relating to the protection of State secrets in the dissemination of online information.

Such regulation and censorship could lead to a decrease in our customers’ interest in utilizing our internet cafes which would cause our operations to be adversely affected.

17

Intensified government regulation of Internet cafes could cause our operations to be adversely affected.

The PRC government has tightened its regulation of Internet cafes in recent years. In particular, a large number of unlicensed Internet cafes have been closed. In addition, the PRC government has imposed higher capital and facility requirements for the establishment of Internet cafes. Furthermore, the PRC government’s policy, which encourages the development of a limited number of national and regional Internet cafe chains and discourages the establishment of independent Internet cafes, may slow down the growth of Internet cafes. In June 2002, the Ministry of Culture, together with other government authorities, issued a joint notice, and in February 2004, the State Administration for Industry and Commerce issued another notice, suspending the issuance of new Internet cafe licenses. In May 2007, the State Administration for Industry and Commerce reiterated its position not to register any new Internet cafes in 2007. In 2008 and 2009, the Ministry of Culture, the State Administration for Industry and Commerce and other relevant government authorities, individually or jointly, issued several notices that provide various ways to strengthen the regulation of Internet cafes, including investigating and punishing Internet cafes that accept minors, cracking down on Internet cafes without sufficient and valid licenses, limiting the total number of Internet cafes and approving Internet cafes within the planning made by relevant authorities, screening unlawful and adverse games and websites, and improving the coordination of regulation over Internet cafes and online games.

If we fail to successfully update our computer hardware, software, and systems to customer requirements or emerging industry standards, our business, prospects and financial results may be materially and adversely affected.

To remain competitive, we must continue to update the computer hardware, software and systems in our internet cafes. The computer industry is characterized by rapid technological evolution, changes in user requirements and preferences, frequent introductions of new products and services embodying new technologies and the emergence of new industry standards and practices that could render our existing proprietary technologies and systems obsolete. If we are unable to adapt in a cost-effective and timely manner in response to changing market conditions or customer requirements, whether for technical, legal, financial or other reasons, our business, prospects, financial condition and results of operations would be materially adversely affected.

We may be unable to adequately safeguard our intellectual property or we may face claims that may be costly to resolve or that limit our ability to use such intellectual property in the future.

Our business is reliant on our intellectual property. Our software SAFLASH is the result of our research and development efforts, which we believe to be proprietary and unique. However, we are unable to assure you that third parties will not assert infringement claims against us in respect of our intellectual property or that such claims will not be successful. It may be difficult for us to establish or protect our intellectual property against such third parties and we could incur substantial costs and diversion of management resources in defending any claims relating to proprietary rights. If any party succeeds in asserting a claim against us relating to the disputed intellectual property, we may need to obtain licenses to continue to use the same. We cannot assure you that we will be able to obtain these licenses on commercially reasonable terms, if at all. The failure to obtain the necessary licenses or other rights could cause our business results to suffer.

Further, we rely upon a combination of trade secrets, non-disclosure and other contractual agreements with our employees as well as limitation of access to and distribution of our intellectual property in our efforts to protect intellectual property. However, our efforts in this regard may be inadequate to deter misappropriation of our proprietary information or we may be unable to detect unauthorized use and take appropriate steps to enforce our rights. Policing unauthorized use of our intellectual property is difficult and there can be no assurance that the steps taken by us will prevent misappropriation of our intellectual property.

Where litigation is necessary to safeguard our intellectual property, or to determine the validity and scope of the proprietary rights of others, this could result in substantial costs and diversion of our resources and could have a material adverse effect on our business, financial condition, operating results or future prospects.

We may not have sufficient insurance coverage and an interruption of our business or loss of a significant amount of property could have a material adverse effect on our financial condition and operations.

We currently do not maintain any insurance policies against loss of key personnel and business interruption as well as product liability claims. If such events were to occur, our business, financial performance and financial position may be materially and adversely affected.

18

Inability to maintain our competitiveness would adversely affect our financial performance.

We operate in a competitive environment and face competition from existing competitors and new market entrants. Some of these existing competitors, especially the national chains of internet cafés have more resources than us and may provide better services to customers.

There is no assurance that we will be able to compete successfully in the future. Any failure by us to remain competitive would adversely affect our financial performance.

We may be adversely affected by a significant or prolonged economic downturn in the level of consumer spending in the industries and markets served by our customers.

We rely on the spending of our customers in our cafés for our revenues, which may in turn depend on the customers’ level of disposable income, perceived future earning capabilities and willingness to spend. Any significant or prolonged decline of the PRC economy or economy of such markets served by our customers will affect consumers’ disposable income and consumer spending in these markets, and lead to a decrease in demand for consumer products.

To the extent that such decrease in demand for consumer products translates into a decline in the demand for internet café services, our performance will be adversely affected.

Revocation of the license for operating internet café chain will adversely affect our business.

We hold a license for operating a regional internet café chain in Shenzhen and each of our internet cafés obtains a license for the internet access services. These licenses are currently valid, and will continue to be valid within the term of the corresponding business licenses. These licenses do not need to be renewed unless there is change of information thereon. But the competent authorities are entitled to examine and reevaluate our internet cafés any time upon their initiatives or following orders of the higher-level authorities, and we must comply with the then prevailing standards and regulations which may change from time to time. Failure to comply with these changing standards and regulations could result in our licenses being revoked or suspended, which could have a material adverse effect on our operations. Furthermore, if escalating compliance costs associated with governmental standards and regulations restrict or prohibit any part of our operations, it may adversely affect our operations and profitability.

We may be unable to effectively manage our expansion.

We have identified several growth plans. These expansion plans may strain our financial resources. In addition, any significant growth into new markets may require an expansion of our employee base for managerial, operational, financial, and other purposes. During any growth, we may face problems related to our operational and financial systems and controls. We would also need to continue to expand, train and manage our employee base. Continued future growth will impose significant added responsibilities upon the members of management to identify, recruit, maintain, integrate, and motivate new employees.

If we are unable to successfully manage our expansion, we may encounter operational and financial difficulties which would in turn adversely affect our business and financial results.

We may require additional funding for our growth plans, and such funding may result in a dilution of your investment.

We attempted to estimate our funding requirements in order to implement our growth plans.

If the costs of implementing such plans should exceed these estimates significantly or if we come across opportunities to grow through expansion plans which cannot be predicted at this time, and our funds generated from our operations prove insufficient for such purposes, we may need to raise additional funds to meet these funding requirements.

19

These additional funds may be raised by issuing equity or debt securities or by borrowing from banks or other resources. We cannot assure you that we will be able to obtain any additional financing on terms that are acceptable to us, or at all. If we fail to obtain additional financing on terms that are acceptable to us, we will not be able to implement such plans fully. Such financing even if obtained, may be accompanied by conditions that limit our ability to pay dividends or require us to seek lenders’ consent for payment of dividends, or restrict our freedom to operate our business by requiring lender’s consent for certain corporate actions.

Further, if we raise additional funds by way of a rights offering or through the issuance of new shares, any shareholders who are unable or unwilling to participate in such an additional round of fund raising may suffer dilution in their investment.

Our strategy to acquire companies may result in unsuitable acquisitions or failure to successfully integrate acquired companies, which could lead to reduced profitability.

We intend to expand our business through acquisitions of companies or operations similar to our own. We may be unsuccessful in identifying suitable acquisition candidates, or may be unable to consummate a desired acquisition. To the extent any future acquisitions are completed, we may be unsuccessful in integrating acquired companies or their operations, or if integration is more difficult than anticipated, we may experience disruptions that could have a material adverse impact on future profitability. Some of the risks that may affect our ability to integrate, or realize any anticipated benefits from, acquisitions include:

|

|

|

unexpected losses of key employees or customer of the acquired company;

|

|

|

|

difficulties integrating the acquired company's standards, processes, procedures and controls;

|

|

|

|

difficulties hiring additional management and other critical personnel;

|

|

|

|

difficulties increasing the scope, geographic diversity and complexity of our operations;

|

|

|

|

difficulties consolidating facilities, transferring processes and know-how;

|

|

|

|

difficulties reducing costs of the acquired company's business; and

|

|

|

|

diversion of management's attention from our management.

|

We may be exposed to potential risks relating to our internal controls over financial reporting and our ability to have those controls attested to by our independent auditors.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002, or SOX 404, the SEC adopted rules requiring public companies to include a report of management on the company’s internal controls over financial reporting in their annual reports, including Form 10-K. In addition, the independent registered public accounting firm auditing a company's financial statements must also attest to and report on the operating effectiveness of the company’s internal controls. We were not subject to these requirements for the fiscal year ended December 31, 2010, but we have evaluated our internal control systems in order to allow our management to report on our internal controls as required by these requirements of SOX 404. We can provide no assurance that we will comply with all of the requirements imposed thereby. In the event we identify significant deficiencies or material weaknesses in our internal controls that we cannot remediate in a timely manner or we are unable to receive a positive attestation from our independent auditors with respect to our internal controls, investors and others may lose confidence in the reliability of our financial statements.

Our holding company structure may limit the payment of dividends.

We have no direct business operations, other than our ownership of our subsidiaries and contractual relationship with Junlong. While we have no current intention of paying dividends, should we decide in the future to do so, as a holding company, our ability to pay dividends and meet other obligations depends upon the receipt of dividends or other payments from our operating subsidiaries and other holdings and investments. In addition, our operating subsidiaries, from time to time, may be subject to restrictions on their ability to make distributions to us, including as a result of restrictive covenants in loan agreements, restrictions on the conversion of local currency into U.S. dollars or other hard currency and other regulatory restrictions as discussed below. If future dividends are paid in RMB, fluctuations in the exchange rate for the conversion of RMB into U.S. dollars may reduce the amount received by U.S. stockholders upon conversion of the dividend payment into U.S. dollars. Further, dividends paid to non-PRC stockholders may be subject to a 10% withholding, as further discussed in a later section. Under the EIT Law, we may be classified as a ‘resident enterprise’ of the PRC. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders.”

20

PRC regulations currently permit the payment of dividends only out of accumulated profits as determined in accordance with PRC accounting standards and regulations. Our subsidiary in the PRC is also required to set aside a portion of its after tax profits according to PRC accounting standards and regulations to fund certain reserve funds. Currently, our subsidiary in the PRC is the only sources of revenues or investment holdings for the payment of dividends. If it does not accumulate sufficient profits under PRC accounting standards and regulations to first fund certain reserve funds as required by PRC accounting standards, we will be unable to pay any dividends.

Our contractual arrangements with Junlong and its shareholders may not be as effective in providing control over them as direct ownership.

We rely on contractual arrangements with our VIE and its shareholders to operate our business. In the opinion of our PRC legal counsel, China Commercial Law Firm, these contractual arrangements are valid, binding and enforceable, and will not result in any violation of PRC laws or regulations currently in effect. These contractual arrangements may not be as effective in providing us with control over these entities as direct ownership. If we had direct ownership of these entities, we would be able to exercise our rights as a shareholder to effect changes in the boards of directors of these entities, which in turn could effect changes, subject to any applicable fiduciary obligations, at the management level. However, if Junlong or any of its shareholders fails to perform its or his respective obligations under these contractual arrangements, we may not be able to enforce the relevant agreements. If the agreements are ruled in violation of the PRC laws, even if the contracts are otherwise legal and valid, we may not be able to enforce our rights under these contracts. We may have to incur substantial costs and resources to enforce them, and seek legal remedies under PRC law, including specific performance or injunctive relief, and claiming damages, which may not be effective. Accordingly, it may be difficult for us to change our corporate structure or to bring claims against any of these entities if they do not perform their obligations under their contracts with us.

All of our revenues are generated through our VIE, and we rely on payments made by our VIE to Zhonghefangda, our subsidiary, pursuant to contractual arrangements to transfer any such revenues to Zhonghefangda. Any restriction on such payments and any increase in the amount of PRC taxes applicable to such payments may materially and adversely affect our business and our ability to pay dividends to our shareholders.