Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF SHERB & CO., LLP - Celsius Holdings, Inc. | f10k2010ex23i_celsius.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO SECTION 906 OF SARBANES OXLEY ACT OF 2002 - Celsius Holdings, Inc. | f10k2010ex32i_celsius.htm |

| EX-31.1 - CERTIFICATION PURSUANT TO SECTION 302 OF SARBANES OXLEY ACT OF 2002 - Celsius Holdings, Inc. | f10k2010ex31i_celsius.htm |

| EX-32.2 - CERTIFICATION PURSUANT TO SECTION 906 OF SARBANES OXLEY ACT OF 2002 - Celsius Holdings, Inc. | f10k2010ex32ii_celsius.htm |

| EX-31.2 - CERTIFICATION PURSUANT TO SECTION 302 OF SARBANES OXLEY ACT OF 2002 - Celsius Holdings, Inc. | f10k2010ex31ii_celsius.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.20549

FORM 10-K

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2010

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

CELSIUS HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

|

NEVADA

|

001-34611

|

20-2745790

|

||

|

(State or other jurisdiction of incorporation)

|

(Commission File Number)

|

(IRS Employer Identification No.)

|

2424 N Federal Hwy, Suite 208

Boca Raton, FL 33431

(Address of principal executive offices) (Zip Code)

(561) 276-2239

(Registrant’s telephone number, including area code)

| Securities registered under Section 12(b) of the Exchange Act: | None |

| Securities registered under Section 12(g) of the Exchange Act: | Common Stock, par value $0.001 |

| Common Stock Purchase Warrants |

(Former name, former address and former fiscal year, if changed since last report)

Check whether the issuer has (1) filed all reports required to be files by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Check if there is no disclosure of delinquent filers in response to Item 405 of Regulation S-B contained in this form, and no disclosure will be contained, to the best of Company's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

o Large accelerated filer o Accelerated filer o Non-accelerated filer x Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter: $15.5 million.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date 18,515,575 as of March 25, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

None

As used throughout this report, the terms “we,” “us,” ”our” and “our company” refer to Celsius Holdings, Inc., and all of its subsidiaries. Unless otherwise noted, all share and per share data in this report gives effect to 1-for-20 reverse stock split of our common stock implemented on December 23, 2009.

General information about our company can be found at www.celsius.com. We make our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendment to these reports filed or furnished pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 available free of charge on our website, as soon as reasonably practicable after they are electronically filed with the Security and Exchange Commission.

FORWARD-LOOKING STATEMENTS

Information included in this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. This information involves known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by any forward-looking statements. Forward-looking statements, which involve assumptions and describe our future plans, strategies and expectations, are generally identifiable by use of the words “may”, “should”, “expect”, “anticipate”, “estimate”, “believe”, “intend” or “project” or the negative of these words or other variations on these words or comparable terminology.

The forward-looking statements in this report include statements regarding, among other things, (a) our projected sales and profitability, (b) our growth strategies, (c) anticipated trends in our industry, (d) our future financing plans and (e) our anticipated needs for working capital. These statements may be found under “Item 1 Business”, “Item 1A Risk Factors”, and “Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations”, as well as elsewhere in this report. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under “Item 1A Risk Factors” and matters described in this report generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this report will in fact occur.

PART I

ITEM 1 DESCRIPTION OF BUSINESS

Business Overview — General

We are engaged in the development, marketing, sale and distribution of “functional” calorie-burning fitness beverages under the Celsius® brand name. According to multiple clinical studies we funded, a single serving (12 ounce can) of Celsius® burns up to 100 calories by increasing a consumer’s resting metabolism an average of 12% and providing sustained energy for up to a three-hour period. Our exercise focused studies show Celsius delivers additional benefits when consumed prior to exercise. The studies shows benefits such as increase in fat burn, increase in lean muscle mass and increased endurance.

We seek to combine nutritional science with mainstream beverages by using our proprietary thermogenic (calorie-burning) MetaPlus® formulation, while fostering the goal of healthier everyday refreshment by being as natural as possible without the artificial preservatives often found in many energy drinks and sodas. Celsius® has no artificial preservatives, aspartame or high fructose corn syrup and is very low in sodium. Celsius® uses good-for-you ingredients and supplements such as green tea (EGCG), ginger, calcium, chromium, B vitamins and vitamin C. The main Celsius line of products are sweetened with sucralose, a sugar-derived sweetener that is found in Splenda®, which makes our beverages low-calorie and suitable for consumers whose sugar intake is restricted. In 2010, we also introduced a Celsius version sweetened with Stevia.

We have undertaken significant marketing efforts aimed at building brand awareness, including a wide variety of marketing vehicles such as television, radio, on-line and magazine advertising. We also undertake various promotions at the retail level such as coupons and other discounts in addition to in-store sampling. We engaged Mario Lopez, a well-known television personality, to be our national celebrity spokesperson.

2

We do not directly manufacture our beverages, but instead outsource the manufacturing process to established third-party co-packers. We do, however, provide our co-packers with flavors, ingredient blends, cans and other raw materials for our beverages purchased by us from various suppliers.

On February 16, 2010, the Company sold 900,000 units in a secondary public offering, generating gross proceeds of $14.5 million and net proceeds of approximately $13.1 million, after deduction of underwriting discounts and payment of offering expenses. Each unit consisted of four shares of common stock and one warrant to purchase one share of common stock exercisable at a price of $5.32 per share at any time through February 8, 2013.

A substantial portion of the net proceeds of the secondary public offering, together with approximately $2.0 million in debt financing provided to us by an affiliate of our principal shareholder in July 2010, was used for marketing and sales efforts aimed at penetrating the direct to retail (DTR) market and building brand awareness through a wide variety of marketing media and retail level promotions such as coupons and other discounts. While our efforts met with a degree of success in penetrating major retailers, we found that we were unable to achieve product sell through at the retail level at a rate adequate to generate the revenues that would be needed to fund the ongoing costs of building brand awareness and achieving profitability in the DTR channel, as well as sustaining our operations.

Accordingly, in August 2010, we engaged a consulting and advisory firm with experience in the beverage industry, to explore strategic options, including additional financing and/or a potential sale of the Company. To date, the Company has not received any offers for either additional financing or a potential sale transaction.

As a result of the losses we incurred, the Company decided in December 2010 to significantly reduce overhead, downsize operations, decrease consumer marketing expenses and review unprofitable accounts and undertake corrective action in order to reduce cash outlays and allow the Company to operate on a break-even or close to break-even basis. While the Company believes it has sufficient capital resources to fund its operation for the balance of 2011, the Company believes that without a capital infusion or other strategic transaction, its ability to achieve revenue growth will be limited. Accordingly, management continues to explore strategic options with respect to the financing, sale or restructuring of the Company.

Corporate History and Information

We were incorporated in Nevada on April 26, 2005 under the name “Vector Ventures, Inc” and originally we engaged in mineral exploration. Such business was unsuccessful. On January 26, 2007, we acquired the Celsius® beverage business of Elite FX, Inc., a Florida corporation engaged in the development of functional beverages since 2004 in a reverse merger, and subsequently changed our name to Celsius Holdings, Inc.

Our principal executive offices are located at 2424 N Federal Hwy, Boca Raton, Florida 33431.Our telephone number is (561) 276-2239 and our website is www.celsius.com. The information accessible through our website does not constitute part of this report.

Industry Overview

The “functional” beverage category includes a wide variety of beverages with one or more added ingredients to satisfy a physical or functional need, such as sports drinks, energy drinks, and non-carbonated ready to drink teas.

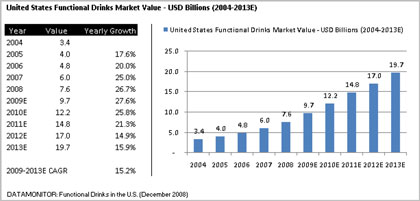

Size of Market — According to a report by Accenture Consulting, the size of the annual non-alcoholic beverage market was estimated to have grown to more than $17.4 billion in the United States in 2010. A growing portion of this market is the functional beverage market, which was estimated at $9.7 billon, in 2010, according to Datamonitor. This market is estimated to grow to $19.7 billion by 2013, a compound annual growth rate of 15.2% over that time period.

3

Current Market Segmentation — The growing functional beverage market can be further segmented into several different sub-categories, such as energy drinks, sports drinks, and nutraceutical drinks. According to Datamonitor, as of 2009, the largest category of functional drinks was energy drinks with approximately 62% market share and sports drinks with an approximately 26% market share.

We believe that Celsius® is both a member of the energy drink sub-category, as well as creating a new category of beverages, calorie-burning. It has some of the same functional elements of an energy drink, but unlike the majority of the sugary (high calorie) competitors in this space, Celsius® does not contain high fructose corn syrup and burns up to 100 calories by increasing a drinker’s metabolism an average of 12% for up to a three-hour period. We believe that Celsius® is a superior product to currently available energy drinks due to its low caloric content, its calorie burning capabilities and its lack of artificial preservatives, colors and flavors.

Changing Industry Trends — There is an increased concern among consumers, the public health community and various government agencies of the potential health problems associated with inactive lifestyles and obesity. There are currently several proposals in the U.S. Congress seeking to address the issue of consumption of sugary drinks by children and other consumers. Participants in the non-alcoholic beverage market are responding to these concerns by bringing to market new healthier products such as diet and light beverages, juices and juice drinks, sports drinks and water products.

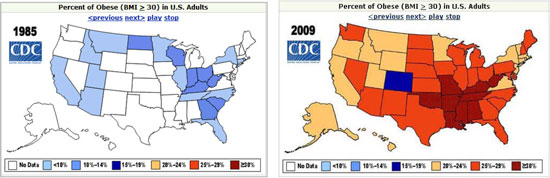

Growing Number of Adults with Obesity— According to statistics from the U.S. Center for Disease Control and Prevention (CDC) during the past 20 years there has been a dramatic increase in obesity in the United States. In 2009, only one state (Colorado) had a prevalence of obesity less than 20%. Thirty-two states had prevalence equal to or greater than 25%; six of these states (Alabama, Mississippi, Oklahoma, South Carolina, Tennessee, and West Virginia) had a prevalence of obesity equal to or greater than 30%.

The maps below show the change in obesity prevalence from 1985 through 2009 in the United States.

Industry Trends Benefit Celsius® — We believe that Celsius® is strategically placed to capitalize on several macro-trends in the beverage space by filling a need that is not currently being met by its competitors in both the functional and general non-alcoholic beverage markets.

4

With a growing number of consumers seeking functional beverages, we believe that they are also increasingly seeking out products that are the healthiest alternative within those product categories. Many of the leading functional beverage products contain high doses of sugar or high fructose corn syrup, sodium, artificial flavors, and preservatives which may counter-balance some of the other benefits the consumer is looking for.

Celsius® has created its portfolio of beverages to specifically address these issues. While maintaining great taste to the consumer, a 12 ounce can of Celsius® has a number of competitive advantages over some of the currently leading beverages including:

|

§

|

less artificial preservatives than almost all other energy drinks or sodas;

|

|

§

|

no artificial colors or flavors;

|

|

§

|

no aspartame;

|

|

§

|

no high fructose corn syrup;

|

|

§

|

low sodium content;

|

|

§

|

use of good-for-you ingredients and supplements such as green tea (EGCG), ginger, calcium, chromium, B vitamins and vitamin C; and

|

|

§

|

use of our proprietary thermogenic (calorie-burning) MetaPlus® formulation that allows Celsius® to burn up to 100 calories by increasing a consumer’s metabolism an average of 12% and providing sustained energy for up to a 3-hour period.

|

Our Products

Celsius® calorie-burning beverages were first introduced to the marketplace in 2005.

According to multiple clinical studies we funded, a single serving (12 ounce can) of Celsius® burns up to 100 calories by increasing a consumer’s metabolism an average of 12% for up to a three-hour period. In addition, these studies have indicated that drinking a single serving of Celsius® prior to exercising may improve cardiovascular health and fitness and enhance the loss of fat and gain of muscle from exercise.

We seek to combine nutritional science with mainstream beverages by using our proprietary thermogenic (calorie-burning) MetaPlus® formulation, while fostering the goal of healthier everyday refreshment by being as natural as possible without the artificial preservatives often found in many energy drinks or sodas. Celsius® has no chemical preservatives, aspartame or high fructose corn syrup and is very low in sodium. Celsius® uses good-for-you ingredients and supplements such as green tea (EGCG), ginger, calcium, chromium, B vitamins and vitamin C. Celsius is sweetened with sucralose, a sugar-derived sweetener that is found in Splenda®, which makes our beverages low-calorie and suitable for consumers whose sugar intake is restricted. Each 12 ounce can of Celsius® contains 200 milligrams of caffeine which is comparable to two cups of coffee.

We currently offer Celsius® in nine flavors, ginger ale, cola, orange and wild berry (which are carbonated) and non-carbonated green tea raspberry/acai, green tea/peach mango, Lemon Iced Tea, Strawberry/Kiwi and the new Stevia based, Apple Orchard. Our beverages are sold in 12 and 10.5 ounce cans, and we have recently begun to market the active ingredients in powdered form in individual On-The-Go packets as well as 2.5 ounce shots.

Celsius® is packaged in a distinctive twelve ounce sleek can that uses vivid colors in abstract patterns to create a strong on-shelf impact. The cans are sold as singles or in four-packs.

We target a niche in the functional beverage segment of the beverage industry consisting of consumers seeking calorie-burning beverages to help them manage their weight and enhance their exercise regimen. Our target consumers are generally individuals that exercise two to five times a week and are concerned about their health.

Clinical Studies

It is our belief that clinical studies substantiating product claims will become more important as more and more beverages are marketed with health claims. Celsius® was one of the first functional beverages to be launched along with a clinical study. Celsius® is also one of very few functional beverages that has clinical research on the actual product itself. Some beverage companies that do mention studies backing their claims are actually referencing independent studies conducted on one or more of the ingredients in the product. We believe that it is important and will become more important to have studies on the actual product.

We have funded seven U.S. based clinical studies for Celsius®. Each was conducted by a research organizations and each studied the total Celsius® formula. The first study was conducted by the Ohio Research Group of Exercise Science and Sports Nutrition. The remaining studies were conducted by the Applied Biochemistry & Molecular Physiology Laboratory of the University of Oklahoma. We funded all of the studies and provided Celsius® beverage for the studies. However, none of our directors, executive officers or principal shareholders is in any way affiliated with either of the two research organizations which conducted the studies.

5

The first study was conducted in 2005 by the Ohio Research Group of Exercise Science and Sports Nutrition. The Ohio Research Group of Exercise Science & Sports Nutrition is a multidisciplinary clinical research team dedicated to exploring the relationship between exercise, nutrition, dietary supplements and health, www.ohioresearchgroup.com. This placebo-controlled, double-blind cross-over study compared the effects of Celsius® and the placebo on metabolic rate. Twenty-two participants were randomly assigned to ingest a twelve ounce serving of Celsius® and on a separate day a serving of twelve ounces of Diet Coke®. All subjects completed both trials using a randomized, counterbalanced design. Randomized means that subjects were selected for each group randomly to ensure that the different treatments were statistically equivalent. Counterbalancing means that individuals in one group drank the placebo on the first day and drank Celsius® on the second day. The other group did the opposite. Counterbalancing is a design method that is used to control “order effects.” In other words, to make sure the order that subjects were served, does not impact the results and analysis.

Metabolic rate (via indirect calorimetry, measurements taken from breaths into and out of calorimeter) and substrate oxidation (via respiratory exchange ratios) were measured at baseline (pre-ingestion) and for ten minutes at the end of each hour for three hours post-ingestion. The results showed an average increase of metabolism of twelve percent over the three hour period, compared to statistically insignificant change for the control group. Metabolic rate, or metabolism, is the rate at which the body expends energy. This is also referred to as the “caloric burn rate.” Indirect calorimetry calculates heat that living organisms produce from their production of carbon dioxide. It is called “indirect” because the caloric burn rate is calculated from a measurement of oxygen uptake. Direct calorimetry would involve the subject being placed inside the calorimeter for the measurement to determine the heat being produced. Respiratory Exchange Ratio is the ratio oxygen taken in a breath compared to the carbon dioxide breathed out in one breath or exchange. Measuring this ratio can be used for estimating which substrate (fuel such as carbohydrate or fat) is being metabolized or ‘oxidized’ to supply the body with energy.

The second study was conducted by the Applied Biochemistry & Molecular Physiology Laboratory of University of Oklahoma in 2007. This blinded, placebo-controlled study was conducted on a total of 60 men and women of normal weight. An equal number of participants were separated into two groups to compare one serving (a single 12 ounce can) of Celsius to a placebo of the same amount. According to the study, those subjects consuming Celsius burned significantly more calories versus those consuming the placebo, over a three-hour period. The study confirmed that over the three-hour period, subjects consuming a single serving of Celsius® burned 65% more calories than those consuming the placebo beverage and burned an average of more than 100 calories compared to the placebo. These results were statistically significant.

The third study, conducted by the Applied Biochemistry & Molecular Physiology Laboratory of University of Oklahoma in 2007, extended our second study with the same group of 60 individuals and protocol for 28 days and showed the same statistical significance of increased calorie burn (minimal attenuation). While the University of Oklahoma study did extend for 28 days, more testing would be needed for long term analysis of the Celsius® calorie-burning effects. Also, these studies were on relatively small numbers of subjects, they have statistically significant results. Additional studies on a larger number and wider range of body compositions can be considered to further the analysis.

Our fourth study, conducted by the Applied Biochemistry & Molecular Physiology Laboratory of University of Oklahoma in 2009, combined Celsius® use with exercise. This ten-week placebo-controlled, randomized and blinded study was conducted on a total of 37 subjects. Participants were randomly assigned into one of two groups: Group 1 consumed one serving of Celsius® per day, and Group 2 consumed one serving of an identically flavored and labeled placebo beverage. Both groups participated in ten weeks of combined aerobic and weight training, following the American College of Sports Medicine guidelines of training for previously sedentary adults. The results showed that consuming a single serving of Celsius® prior to exercising may enhance the positive adaptations of exercise on body composition, cardio-respiratory fitness and endurance performance. According to the preliminary findings, subjects consuming a single serving of Celsius® lost significantly more fat mass and gained significantly more muscle mass than those subjects consuming the placebo — a 93.75% greater loss in fat and 50% greater gain in muscle mass, respectively. The study also confirmed that subjects consuming Celsius® significantly improved measures of cardio-respiratory fitness and the ability to delay the onset of fatigue when exercising to exhaustion.

6

Our fifth study was conducted by the Applied Biochemistry & Molecular Physiology Laboratory of University of Oklahoma in 2009. This ten-week placebo-controlled, randomized and blinded study was conducted on a total of 27 previously sedentary overweight and obese female subjects. Participants were randomly assigned into groups that consumed identically tasting treatment beverages with exercise or without exercise. All participants consumed one drink, either placebo or Celsius, per day for 10 weeks. The exercise groups participated in ten weeks of combined aerobic and weight training, following the American College of Sports Medicine guidelines of training for previously sedentary adults. No changes were made to their diet. The results showed that consuming a single serving of Celsius® prior to exercising may improve cardiovascular health and fitness and enhance the positive adaptations of exercise on body composition. According to the preliminary findings, subjects consuming a single serving of Celsius® lost significantly more fat mass and gained significantly more muscle mass when compared to exercise alone — a 46% greater loss in fat, 27% greater gain in muscle mass, respectively. The study also confirmed that subjects consuming Celsius® significantly improved measures of cardio-respiratory fitness — 35% greater endurance performance with significant improvements to lipid profiles — total cholesterol decreases of 5 to 13% and bad LDL cholesterol 12 to 18%. Exercise alone had no effect on blood lipid levels.

Our sixth study was conducted by the Applied Biochemistry & Molecular Physiology Laboratory of University of Oklahoma in 2009. This ten-week placebo-controlled, randomized and blinded study was conducted on a total of 37 previously sedentary male subjects. Participants were randomly assigned into groups that consumed identically tasting treatment beverages with exercise or without exercise. All participants consumed one drink, either placebo or Celsius, per day for 10 weeks. The exercise groups participated in ten weeks of combined aerobic and weight training, following the American College of Sports Medicine guidelines of training for previously sedentary adults. No changes were made to their diet. The results showed that consuming a single serving of Celsius® prior to exercising may improve cardiovascular health and fitness and enhance the positive adaptations of exercise on body composition. Significantly greater decreases in fat mass and percentage body fat and increases in VO2were observed in the subjects that consumed Celsius before exercise versus those that consumed the placebo before exercise. Mood was not affected. Clinical markers for hepatic, renal, cardiovascular and immune function, as determined by pre and post blood work revealed no adverse effects.

Our seventh study was conducted by Miami Research Institute in 2010 and showed the efficacy and safety of the powders and the shots. This study allows the Company to make the same structure/function claims as the ready to drink beverages.

Manufacture and Supply of Our Products

Our beverages are produced by established third party beverage co-packers. A co-packer is a manufacturing plant that provides the service of filling bottles or cans for the brand owner. We believe one benefit of using co-packers is that we do not have to invest in the production facility and can focus our resources on brand development, sales and marketing. It also allows us produce in multiple locations strategically placed throughout the country. Currently our products are produced in Cold Spring, Minnesota and Charlotte, North Carolina. We usually produce about 34,000 cases (24 units per case) of Celsius® in a production run. We purchase most of the ingredients and all packaging materials. The co-pack facility assembles our products and charges us a fee by the case. The shelf life of Celsius® is specified as 15 to 18 months.

Substantially all of the raw materials used in the preparation, bottling and packaging of our products are purchased by us or by our co-packers in accordance with our specifications. Generally, we obtain the ingredients used in our products from domestic suppliers and some ingredients have several reliable suppliers. The ingredients in Celsius® include green tea (EGCG), ginger (from the root), caffeine, B vitamins, vitamin C, taurine, guarana, chromium, calcium, glucuronolactone, sucralose, natural flavors and natural colorings. Celsius® is labeled with a supplements facts panel. We have no major supply contracts with any of our suppliers. We single-source all our ingredients for purchasing efficiency; however, we have identified a second source for our critical ingredients and there are many suppliers of flavors, colorings and sucralose. In case of a supply restriction or interruption from any of the flavor and coloring suppliers, we would have to test and qualify other suppliers that may disrupt our production schedules.

Packaging materials, except for our distinctive sleek aluminum cans, are easily available from multiple sources in the United States; however, due to efficiencies we utilize single source vendor relationships. There is currently only one factory in the United States that produces the 12 ounce can. In case of an interruption at that supplier, we would be forced to change our design and structure of the can.

We believe that our co-packing arrangement and supply sources are adequate for our present needs.

7

Marketing

During 2010, we focused on growing our product distribution through DTR sales from small regional areas to more of a national footprint with Celsius® being increasingly available at large, well-known retailers. In order to support this growth, throughout 2010 we conducted a nationwide marketing campaign focused on television, radio, on-line and magazine and newspaper advertising. We also supported our retail sales by retail level promotions such as coupons, in-store discounts and in-store sampling.

While our efforts met with a degree of success in penetrating major retailers, we found that we were unable to achieve product sell-through at the retail level at a rate adequate to generate the revenues that would be needed to fund the ongoing costs of building and achieving profitability in the DTR channel, as well as sustaining our operations. Accordingly, in the fourth quarter of 2010, we significantly reduced consumer marketing expenses, as part of a reduction in overhead designed to allow us to operate at a break-even or near break-even level. The Company’s current marketing plan for 2011 (absent a capital infusion) is based mainly on trade promotions and grass roots sampling events and does not include significant amounts for television, radio, and other mass marketing vehicles.

Distribution

Celsius® is sold across many retail segments. They include supermarkets, convenience stores, drug stores, nutritional stores, mass merchants and club warehouses. We also sell to health clubs, spas, gyms, the military, e-commerce websites and to a limited number of international markets. Given our current capital constraints, we are currently focusing on the retail and health and fitness segments.

We distribute our products through a hybrid of direct-store delivery (DSD) distributors and as well as sales direct to retailers (DTR).

Seasonality of Sales

As is typical in the beverage industry, sales of our beverages are seasonal, with the highest sales volumes generally occurring in the second and third fiscal quarters, which correspond to the warmer months of the year in our major markets.

Competition

We believe that we are one of the few calorie-burning fitness beverages whose effectiveness is supported by clinical studies, which gives us a unique position in the beverage market. However, our products do compete broadly with all categories of consumer beverages. The beverage market is highly competitive, and includes international, national, regional and local producers and distributors, most of whom have greater financial, management and other resources than us. Our direct competitors in the functional beverage market include, but are not limited to The Coca-Cola Company, Dr. Pepper Snapple Group, PepsiCo, Inc., Nestlé, Waters North America, Inc., Hansen Natural Corp., and Red Bull.

Proprietary Rights

We have registered the Celsius® and MetaPlus® trademarks with the United States Patent and Trademark Office, as well as a number of additional trademarks.

We have and will continue to take appropriate measures, such as entering into confidentiality agreements with our contract packers and ingredient suppliers, to maintain the secrecy and proprietary nature of our MetaPlus® formulation and product formulas.

We maintain our MetaPlus® formulation and product formulas as trade secrets. We believe that trade secrecy is a preferable method of protection for our formulas as patenting them might require their disclosure. Other than a company that is our outsourced production manager, no single member of the raw material supply chain or our co-packers has access to the complete formula.

We consider our trademarks and trade secrets to be of considerable value and importance to our business. No successful challenges to our registered trademarks have arisen and we have no reason to believe that any such challenges will arise in the future.

8

Government Regulation

The production, distribution and sale of our products in the United States is subject to the Federal Food, Drug and Cosmetic Act, the Dietary Supplement Health and Education Act of 1994, the Occupational Safety and Health Act, various environmental statutes and various other federal, state and local statutes and regulations applicable to the production, transportation, sale, safety, advertising, labeling and ingredients of such products. California law requires that a specific warning appear on any product that contains a component listed by California as having been found to cause cancer or birth defects. The law exposes all food and beverage producers to the possibility of having to provide warnings on their products because the law recognizes no generally applicable quantitative thresholds below which a warning is not required. Consequently, even trace amounts of listed components can expose affected products to the prospect of warning labels. Products containing listed substances that occur naturally in the product or that are contributed to the product solely by a municipal water supply are generally exempt from the warning requirement. While none of our products are required to display warnings under this law, we cannot predict whether an important component of any of our products might be added to the California list in the future. We also are unable to predict whether or to what extent a warning under this law would have an impact on costs or sales of our products.

Measures have been enacted in various localities and states that require that a deposit be charged for certain non-refillable beverage containers. The precise requirements imposed by these measures vary. Other deposit, recycling or product stewardship proposals have been introduced in certain states and localities and in Congress, and we anticipate that similar legislation or regulations may be proposed in the future at the local, state and federal levels, both in the United States and elsewhere.

Our facilities in the United States are subject to federal, state and local environmental laws and regulations. Compliance with these provisions has not had, and we do not expect such compliance to have, any material adverse effect upon our business, financial condition and results of operations.

ITEM 1A RISK FACTORS

Our business faces certain risks. The risks described below may not be the only risks we face. Additional risks that we do not yet know of, or that we currently think as immaterial, may also impair our business. If any of the events anticipated by the risks described below or elsewhere in this report occur, our results of operations and financial conditions could be adversely affected.

Risk Factors Relating to Our Business

We have an operating history with significant losses and expect losses to continue for the foreseeable future.

The Company has experienced operating losses in all years since its inception. Our future operating results will depend on many factors, both in and out of our control, including the ability to increase and sustain demand for and acceptance of our products, the level of our competition, and our ability to attract and maintain key management and employees.

We have incurred a significant operating loss during the year ended December 31, 2010 of $19.5 million. As a result, at December 31, 2010, we had an accumulated deficit of $38.6 million. Our revenues have not been sufficient to sustain our operations. Our profitability will require the successful commercialization of our current Celsius® product line. No assurances can be given when this will occur or that we will ever be profitable.

We require additional capital, which at present has not been available to us.

In the fourth quarter of 2010, we reduced overhead with a view to allow the Company to sustain its operations at a break-even or profitable level. We believe that our existing cash on hand and the $1.0 million available line of credit will enable us to fund our operations at our retooled level through 2011. Our current cash position allows us to undertake only limited marketing efforts without additional financing. However, we have not been able to secure additional financing on commercially reasonable terms or otherwise. Even if we are ultimately able to raise capital through equity or debt financings, the interest of existing shareholders in our company will likely be diluted, and the securities we issue may have rights, preferences and privileges that are senior to those of our common stock or may otherwise materially and adversely affect the holdings or rights of our existing shareholders. Without additional financing we may not be able to successfully market our products, and our business, results of operations and financial condition will likely be adversely affected.

9

We are currently only undertaking limited marketing efforts.

Because of our current capital constraints, we have significantly reduced and limited our marketing efforts. We cannot estimate the effects of reducing and limiting our marketing efforts on our total sales volume, which may be materially adverse.

We rely on third party co-packers to manufacture our products. If we are unable to maintain good relationships with our co-packers and/or their ability to manufacture our products becomes constrained or unavailable to us, our business could suffer.

We do not directly manufacture our products, but instead outsource such manufacturing to established third party co-packers. These third party co-packers may not be able to fulfill our demand as it arises, could begin to charge rates that make using their services cost inefficient or may simply not be able to or willing to provide their services to us on a timely basis or at all. In the event of any disruption or delay, whether caused by a rift in our relationship or the inability of our co-packers to manufacture our products as required, we would need to secure the services of alternative co-packers. We may be unable to procure alternative packing facilities at commercially reasonable rates and/or within a reasonably short time period and any such transition could be costly. In such case, our business, financial condition and results of operations would be adversely affected.

We rely on distributors to distribute our products in the DSD sales channel. If we are unable to secure such distributors and/or we are unable to maintain good relationships with our existing distributors, our business could suffer.

We distribute Celsius® in the DSD sales channel by entering into agreements with direct-to-store delivery distributors having established sales, marketing and distribution organizations. Many of our distributors are affiliated with and manufacture and/or distribute other beverage products. In many cases, such products compete directly with our products. The marketing efforts of our distributors are important for our success. If Celsius® proves to be less attractive to our distributors and/or if we fail to attract distributors, and/or our distributors do not market and promote our products with greater focus in preference to the products of our competitors, our business, financial condition and results of operations could be adversely affected.

Our customers are material to our success. If we are unable to maintain good relationships with our existing customers, our business could suffer.

Unilateral decisions could be taken by our distributors, grocery chains, convenience chains, drug stores, nutrition stores, mass merchants, club warehouses and other customers to discontinue carrying all or any of our products that they are carrying at any time, which could cause our business to suffer.

Increases In cost or shortages of raw materials or increases in costs of co-packing could harm our business.

The principal raw materials used by us are flavors and ingredient blends as well as aluminum cans, the prices of which are subject to fluctuations. We are uncertain whether the prices of any of the above or any other raw materials or ingredients we utilize will rise in the future and whether we will be able to pass any of such increases on to our customers. We do not use hedging agreements or alternative instruments to manage the risks associated with securing sufficient ingredients or raw materials. In addition, some of these raw materials, such as our distinctive sleek 12 ounce can, are available from a single or a limited number of suppliers. As alternative sources of supply may not be available, any interruption in the supply of such raw materials might materially harm us.

Our failure to accurately estimate demand for our products could adversely affect our business and financial results.

We may not correctly estimate demand for our products. If we materially underestimate demand for our products and are unable to secure sufficient ingredients or raw materials, we might not be able to satisfy demand on a short-term basis, in which case our business, financial condition and results of operations could be adversely affected.

We depend upon our trademarks and proprietary rights, and any failure to protect our intellectual property rights or any claims that we are infringing upon the rights of others may adversely affect our competitive position.

Our success depends, in large part, on our ability to protect our current and future brands and products and to defend our intellectual property rights. We cannot be sure that trademarks will be issued with respect to any future trademark applications or that our competitors will not challenge, invalidate or circumvent any existing or future trademarks issued to, or licensed by, us.

Our products are manufactured using our proprietary blends of ingredients. These blends are created by third-party suppliers to our specifications and then supplied to our co-packers. Although all of the third parties in our supply and manufacture chain execute confidentiality agreements, there can be no assurance that our trade secrets, including our proprietary ingredient blends will not become known to competitors.

10

We believe that our competitors, many of whom are more established, and have greater financial and personnel resources than we do, may be able to replicate or reverse engineer our processes, brands, flavors, or our products in a manner that could circumvent our protective safeguards. Therefore, we cannot give you any assurance that our confidential business information will remain proprietary. Any such loss of confidentiality could diminish or eliminate any competitive advantage provided by our proprietary information.

We may incur material losses as a result of product recall and product liability.

We may be liable if the consumption of any of our products causes injury, illness or death. We also may be required to recall some of our products if they become contaminated or are damaged or mislabeled. A significant product liability judgment against us, or a widespread product recall, could have a material adverse effect on our business, financial condition and results of operations. The amount of the insurance we carry is limited, and that insurance is subject to certain exclusions and may or may not be adequate.

Our lack of product diversification and inability to timely introduce new or alternative products could cause us to cease operations.

Our business is centered on Celsius®. The risks associated with focusing on a limited product line are substantial. If consumers do not accept our products or if there is a general decline in market demand for, or any significant decrease in, the consumption of functional beverages, we are not financially or operationally capable of introducing alternative products within a short time frame. As a result, such lack of acceptance or market demand decline could cause us to cease operations.

We are dependent on our key executives and employees and the loss of any of their services could materially adversely affect us which may have a material adverse effect on our Company.

Our future success will depend substantially upon the abilities of, and personal relationships developed by a limited number of key executives and employees, including Stephen C. Haley, our Chief Executive Officer, President and Chairman of the Board, Geary W. Cotton, our Chief Financial Officer and Irina Lorenzi, our Innovations Vice President. The loss of the services of Mr. Haley, Mr. Cotton, Ms. Lorenzi or any other key employee could materially adversely affect our business and our prospects for the future. We do not have key person insurance on the lives of such individuals and the loss of any of their services could materially adversely affect us.

We are dependent on our ability to attract and retain qualified technical, sales and managerial personnel.

Our future success depends in part on our continuing ability to attract and retain highly qualified technical, sales and managerial personnel. Competition for such personnel in the beverage industry is intense and we may not be able to retain our key managerial, sales and technical employees or attract and retain additional highly qualified technical, sales and managerial personnel in the future. Any inability to attract and retain the necessary technical, sales and managerial personnel could materially adversely affect us.

The FDA has not passed on the efficacy of our products or the accuracy of any claim we make related to our products.

Although six independent clinical studies have been conducted relating to the calorie-burning and related effects of our products, the results of these studies have not been submitted to or reviewed by the FDA. Further, the FDA has not passed on the efficacy of any of our products nor has it reviewed or passed on any claims we make related to our products, including the claim that our products aid consumers in burning calories or enhancing their metabolism.

Risk Factors Relating to Our Industry

We are subject to significant competition in the beverage industry.

The beverage industry is highly competitive. The principal areas of competition are pricing, packaging, distribution channel penetration, development of new products and flavors and marketing campaigns. Our products compete with a wide range of drinks produced by a relatively large number of manufacturers, most of which have substantially greater financial, marketing and distribution resources and name recognition than we do.

11

Important factors affecting our ability to compete successfully include the taste and flavor of our products, trade and consumer promotions, rapid and effective development of new, unique cutting edge products, attractive and different packaging, branded product advertising and pricing. Our products compete with all liquid refreshments and with products of much larger and substantially better financed competitors, including the products of numerous nationally and internationally known producers, such as The Coca Cola Company, Dr. Pepper Snapple Group, PepsiCo, Inc., Nestle, Waters North America, Inc., Hansen Natural Corp. and Red Bull. We also compete with companies that are smaller or primarily local in operation. Our products also compete with private label brands such as those carried by supermarket chains, convenience store chains, drug store chains, mass merchants and club warehouses.

There can be no assurance that we will compete successfully in the functional beverage industry. The failure to do so would materially adversely affect our business, financial condition and results of operations.

We compete in an industry that is brand-conscious, so brand name recognition and acceptance of our products are critical to our success and significant marketing and advertising could be needed to achieve and sustain brand recognition.

Our business is substantially dependent upon awareness and market acceptance of our products and brands by our targeted consumers. Our business depends on acceptance by our independent distributors of our brand as one that has the potential to provide incremental sales growth rather than reduce distributors’ existing beverage sales. The development of brand awareness and market acceptance is likely to require significant marketing and advertising expenditures. There can be no assurance that Celsius® will achieve and maintain satisfactory levels of acceptance by independent distributors and retail consumers. Any failure of Celsius® brand to maintain or increase acceptance or market penetration would likely have a material adverse effect on business, financial condition and results of operations.

Our sales are affected by seasonality.

As is typical in the beverage industry, our sales are seasonal. Our highest sales volumes generally occur in the second and third quarters, which correspond to the warmer months of the year in our major markets. Consumer demand for our products is also affected by weather conditions. Cool, wet spring or summer weather could result in decreased sales of our beverages and could have an adverse effect on our results of operations.

Our business is subject to many regulations and noncompliance is costly.

The production, marketing and sale of our beverage products are subject to the rules and regulations of various federal, state and local health agencies. If a regulatory authority finds that a current or future product or production run is not in compliance with any of these regulations, we may be fined, or production may be stopped, thus adversely affecting our financial conditions and operations. Similarly, any adverse publicity associated with any noncompliance may damage our reputation and our ability to successfully market our products. Furthermore, the rules and regulations are subject to change from time to time and while we closely monitor developments in this area, we have no way of anticipating whether changes in these rules and regulations will impact our business adversely. Additional or revised regulatory requirements, whether labeling, environmental, tax or otherwise, could have an adverse effect on our business, financial condition and results of operations.

ITEM 2 DESCRIPTION OF PROPERTY

Our executive offices are located at 2424 N. Federal Hwy, Suite 208, Boca Raton, FL 33431. We are currently being provided with space at this location by a related party, pursuant to a 12 month lease expiring in August, 2011 for $10,662 per month.

The Company has no warehouses or other facilities as we store our product at third party contract warehouse facilities.

ITEM 3 LEGAL PROCEEDINGS

On June 4, 2010, a lawsuit was commenced against us, entitled Ryan Fletcher v. Celsius Holdings, Inc., Case No. BC439055, pending in Los Angeles Superior Court, State of California (the "Litigation"). In the Litigation, plaintiff asserts that the Company is liable to him for violations of the California Consumer Legal Remedies Act, California Business and Professions Code Section 17200, et seq., and California Business and Professions Code Section 17500, et seq., arising out of the Company's advertising, marketing and packaging of its Celsius products. Plaintiff seeks to recover damages from the Company in an amount to be determined.

We have answered the complaint, exchanged written discovery and have deposed the plaintiff. Based on the foregoing, we believe that not only is the complaint without merit, but that the Litigation is frivolous. Accordingly, we have filed motions which, if granted will result in dismissal of the complaint, as well as possibly imposing sanctions upon the Plaintiff’s counsel. However, as the Litigation is still in its initial stages, it is impossible to predict the ultimate outcome at this time.

12

We are involved in other routine litigation arising in the ordinary course of our business, none of is expected to have a material adverse effect on our business, results of operations or financial condition.

There are no proceedings in which any of our directors, officers or affiliates, or any record or beneficial shareholder, is an adverse party or has a material interest adverse to our interest.

ITEM 4 RESERVED

PART II

ITEM 5 MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Market Information

Our common stock was traded on the OTC Bulletin Board until the February 9, 2010 consummation of our 2010 public offering at which time our common stock and warrants were listed on the NASDAQ Capital Market. On December 31, 2010, our common stock and warrants were delisted from the NASDAQ Capital Market for failure to comply with the requirements for continued listing and are traded in the OTC Market (formerly the pink sheets) The trading symbols for our common stock and warrants are CELH.PK and CELHW.PK, respectively. The prices represent inter-dealer quotations based without retail mark-up, mark-down or commission and may not represent actual transactions. The prices have been adjusted for the 1-for-20 reverse split implemented on December 23, 2009.

|

Quarter Ended(1)

|

High

|

Low

|

||||||

|

31-Dec-10

|

$ | 1.65 | $ | 0.32 | ||||

|

30-Sep-10

|

$ | 2.74 | $ | 1.16 | ||||

|

30-Jun-10

|

$ | 4.49 | $ | 1.46 | ||||

|

31-Mar-10

|

$ | 5.45 | $ | 2.92 | ||||

|

31-Dec-09

|

$ | 12.00 | $ | 2.25 | ||||

|

30-Sep-09

|

$ | 14.00 | $ | 4.00 | ||||

|

30-Jun-09

|

$ | 4.00 | $ | 2.00 | ||||

|

31-Mar-09

|

$ | 3.00 | $ | 0.80 | ||||

|

31-Dec-08

|

$ | 1.60 | $ | 0.60 | ||||

|

30-Sep-08

|

$ | 3.00 | $ | 1.00 | ||||

|

30-Jun-08

|

$ | 3.80 | $ | 1.60 | ||||

|

31-Mar-08

|

$ | 5.60 | $ | 2.00 | ||||

Holders of Record

As of December 31, 2010, we had 31 holders of record of our common stock. The number of record holders was determined from the records of our transfer agent and does not include beneficial owners of common stock whose shares are held in the names of various security brokers, dealers, and registered clearing agencies. We believe that there are in excess of 7,000 beneficial shareholders of our common stock.

Dividends

The Company has never declared nor paid any cash dividends on its capital stock and does not anticipate paying cash dividends in the foreseeable future. By agreement, we are obligated to issue dividends in preferred stock to preferred stock holders; however, we do not anticipate paying cash dividends to preferred stock holders in the foreseeable future. The Company’s current policy is to retain any earnings in order to finance the expansion of its operations. The Company’s Board of Directors will determine future declaration and payment of dividends, if any, in light of the then-current conditions they deem relevant and in accordance with applicable law.

Recent Sales of Unregistered Securities

Not applicable.

13

ITEM 7 MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF OPERATION

General

The following is a discussion of our financial condition and results of operations, comparing the year ended December 31, 2010 to the year ended December 31, 2009. You should read this section together with the Company’s financial statements included in Item 8 of this report, including the notes to those financial statements. Dollar amounts of $1.0 million or more are rounded to the nearest one tenth of a million; all other dollar amounts are rounded to the nearest one thousand and all percentages are stated to the nearest one tenth of one percent.

Reverse Stock Split

We implemented a 1-for-20 reverse stock split on December 23, 2009. Accordingly, unless otherwise noted, all share and per share data has been adjusted to give effect to the reverse stock split.

Accounting Policies and Pronouncements

Critical Accounting Policies

The discussion and analysis of our financial condition and results of operations is based upon our consolidated financial statements, which have been prepared in accordance with Generally Accepted Accounting Principles (GAAP). The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. On an on-going basis, we evaluate our estimates including, among others, those affecting revenues, the allowance for doubtful accounts, the salability of inventory and the useful lives of tangible and intangible assets. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances, the results of which form our basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions, or if management made different judgments or utilized different estimates. Many of our estimates or judgments are based on anticipated future events or performance, and as such are forward-looking in nature, and are subject to many risks and uncertainties, including those discussed below and elsewhere in this report. We do not undertake any obligation to update or revise this discussion to reflect any future events or circumstances.

Although our significant accounting policies are described in Note 2 of the notes to consolidated financial statement, the following discussion is intended to describe those accounting policies and estimates most critical to the preparation of our consolidated financial statements. For a detailed discussion on the application of these and our other accounting policies, see Note 2 contained in Part II, Item 7 to the Consolidated Financial Statements for the year ended December 31, 2010.

Accounts Receivable – We evaluate the collectability of its trade accounts receivable based on a number of factors. In circumstances where we become aware of a specific customer’s inability to meet its financial obligations, a specific reserve for bad debts is estimated and recorded, which reduces the recognized receivable to the estimated amount we believe will ultimately be collected. In addition to specific customer identification of potential bad debts, bad debt charges are recorded based on our recent past loss history and an overall assessment of past due trade accounts receivable outstanding.

Revenue Recognition – Our products are sold to distributors, wholesalers and retailers for cash or on credit terms. Our credit terms, which are established in accordance with local and industry practices, typically require payment within 30 days of delivery. We recognize revenue when persuasive evidence of an arrangement exists, delivery has occurred, the sales price is fixed or determinable and collectability is reasonably assured. All sales to distributors and retailers are final sales and we have a “no return” policy; however, in limited instances, due to credit issues or distributor changes, we may take back product. We believe that adequate provision has been made for cash discounts, returns, customer incentives and spoilage based on the Company’s historical experience. Revenue recognized is reduced by any cash discounts, returns and customer incentives related to the revenue originally recognized for the sale of the product.

Inventory – We hold raw materials and finished goods inventories, which are manufactured and procured based on our sales forecasts. We value inventory at the lower of cost and estimated net realizable value and include adjustments for estimated obsolescence, principally on a first in-first out basis. These valuations are subject to customer acceptance and demand for the particular products, and our estimates of future realizable values are based on these forecasted demands. We regularly review inventory detail to determine whether a write-down is necessary. We consider various factors in making this determination, including recent sales history and predicted trends, industry market conditions and general economic conditions. Differences could result in the amount and timing of write-downs for any period if we make different judgments or use different estimates.

14

Intangibles – Intangibles are comprised primarily of trademarks that represent our exclusive ownership of the Celsius® trademark in connection with the manufacture, sale and distribution of supplements and beverages. The Company also owns, or is in process of registering, some other trademarks in the United States, as well as in a number of countries around the world.

We evaluate our trademarks annually for impairment or earlier if there is an indication of impairment. If there is an indication of impairment of identified intangible assets not subject to amortization, management compares the estimated fair value with the carrying amount of the asset. An impairment loss is recognized to write down the intangible asset to its fair value if it is less than the carrying amount. The fair value is calculated using the income approach. However, preparation of estimated expected future cash flows is inherently subjective and is based on management’s best estimate of assumptions concerning expected future conditions. Based on management’s impairment analysis performed for the year ended December 31, 2010, the estimated fair values of trademarks exceeded the carrying value of $0.

In estimating future revenues, we use internal budgets. Internal budgets are developed based on recent revenue data and future marketing plans for existing product lines and planned timing of future introductions of new products and their impact on our future cash flows.

Stock-Based Compensation –We use the Black-Scholes-Merton option pricing formula to estimate the fair value of its stock options at the date of grant. The Black-Scholes-Merton option pricing formula was developed for use in estimating the fair value of traded options that have no vesting restrictions and are fully transferable. The Company’s employee stock options, however, have characteristics significantly different from those of traded options. For example, employee stock options are generally subject to vesting restrictions and are generally not transferable. In addition, option valuation models require the input of highly subjective assumptions, including the expected stock price volatility, the expected life of an option and the number of awards ultimately expected to vest. Changes in subjective input assumptions can materially affect the fair value estimates of an option. Furthermore, the estimated fair value of an option does not necessarily represent the value that will ultimately be realized by an employee. The Company uses historical data to estimate the expected price volatility, the expected option life and the expected forfeiture rate. The risk-free rate is based on the U.S. Treasury yield curve in effect at the time of grant for the estimated life of the option. If actual results are not consistent with the Company’s assumptions and judgments used in estimating the key assumptions, the Company may be required to increase or decrease compensation expense or income tax expense, which could be material to its results of operations.

Newly Issued Accounting Pronouncements

Information regarding newly issued accounting pronouncements is contained in Part II, Item 7, Note 2 to the Consolidated Financial Statements for the year ended December 31, 2010.

Results of Operations

On February 16, 2010, the Company sold 900,000 units in a secondary public offering, generating gross proceeds of $14.5 million and net proceeds of approximately $13.1 million, after deduction of underwriting discounts and payment of offering expenses. Each unit consisted of four shares of common stock and one warrant to purchase one share of common stock exercisable at a price of $5.32 per share at any time through February 8, 2013.

A substantial portion of the net proceeds of the secondary public offering, together with approximately $2.0 million in debt financing provided to us by an affiliate of our principal shareholder in July 2010, was used for marketing and sales efforts aimed at penetrating the direct to retail (DTR) market and building brand awareness through a wide variety of marketing media and retail level promotions such as coupons and other discounts. While our efforts met with a degree of success in penetrating major retailers, we found that we were unable to achieve product sell through at the retail level at a rate adequate to generate the revenues that would be needed to fund the ongoing costs of building brand awareness and achieving profitability in the DTR channel, as well as sustaining our operations.

Accordingly, in August 2010, we engaged a consulting and advisory firm with experience in the beverage industry, to explore strategic options, including additional financing and/or a potential sale of the Company. To date, the Company has not received any offers for either additional financing or a potential sale transaction.

15

As a result of the losses we incurred, the Company decided in December 2010 to significantly reduce overhead, downsize operations, decrease consumer marketing expenses and review unprofitable accounts and undertake corrective action in order to reduce cash outlays and allow the Company to operate on a break-even or close to break-even basis. While the Company believes it has sufficient capital resources to fund its operations for the balance of 2011, the Company believes that without a capital infusion or other strategic transaction, its ability to achieve revenue growth will be limited. Accordingly, management continues to explore strategic options with respect to the financing, sale or restructuring of the Company.

Year Ended December 31, 2010 Compared to Year Ended December 31, 2009

Revenue

Revenue increased 41.7% for the year 2010 to $8.3 million, as compared to $5.9 million in 2009. The increase was mainly due to increased sales directly to new retailers.

Revenue for the 4th quarter of 2010 was $103,000 as compared to $2.4 million for the same period in 2009. The decrease largely resulted from returns of overstock inventory by three major customers. Revenue for the 4th quarter would have been approximately $1.3 million, without these returns and credits. During the 4th quarter 2009 we recorded a pipe-line fill of $1.4 million to a major customer, and without this initial order, revenue for the 4th quarter of 2009 would have been approximately $1.0 million.

Net Revenue in 2010 was significantly adversely affected by trade promotions. Gross revenue before promotional discounts, coupons, slotting fees and rebates was $13.1 million in 2010 as compared to $6.7 million for 2009.

Gross Profit

Gross profit was 13.2% of net revenue for 2010, as compared to 47.8% in 2009. Gross profit for the fourth quarter of 2010 was significantly impacted by the above discussed returns and credits in addition to an increase in the reserve for inventory obsolescence related to the expected lower salvage value of the returned products. Gross profit for the 4th quarter was a negative $1.6 million. Without the returns, credits and allowance for obsolescence the gross profit would have been approximately $464,000 or 34.2% which is comparable to the first nine months of 2010. Gross profits were also affected by the increase in trade promotions and discounts in 2010 compared to 2009.

Operating Expenses

Sales and marketing expenses increased to $15.2 million in 2010 as compared to $8.0 million in 2009, an increase of $7.2 million or 89.8%. This increase was mainly due to increased cost of samplings at retailers, print, TV and radio advertising. General and administrative expenses increased to $4.7 million in 2010 as compared to $2.3 million in 2009, an increase of $2.4 million. The increase was mainly due to increased cost for issuance and cancellation of stock options, $1.3 million, increased administrative employee cost, including severance, of $722,000, and increased professional fees, $335,000.

Other Expense

Other expense consists of interest on outstanding loans of $396,000 in 2010 as compared to $322,000 in 2009. The increase of $74,000 was mainly due to an increase in total debt as well as increased interest rates. Our interest income increased from $16,000 in 2009 to $18,000 in 2010, an increase of $2,000. We also incurred a loss on extinguishment of debt for $322,000 in 2010, in connection with a renegotiation of the $6.5 million loan in February 2010.

Liquidity and Capital Resources

We have yet to establish any history of profitable operations. As a result, at December 31, 2010, we had an accumulated deficit of $38.6 million. At December 31, 2010, we had working capital of $1.4 million. We have had operating cash flow deficits in all quarters of our operations. Our revenue has not been sufficient to sustain our operations.

On February 16, 2010, the Company sold 900,000 units in a secondary public offering, generating gross proceeds of $14.5 million and net proceeds of approximately $13.1 million, after deduction of underwriting discounts and payment of offering expenses. Each unit consisted of four shares of common stock and one warrant to purchase one share of common stock exercisable at a price of $5.32 per share at any time through February 8, 2013.

A substantial portion of the net proceeds of the secondary public offering, together with approximately $2.0 million in debt financing provided to us by an affiliate of our principal shareholder in July 2010, was used for marketing and sales efforts aimed at penetrating the direct to retail (DTR) market and building brand awareness through a wide variety of marketing media and retail level promotions such as coupons and other discounts. While our efforts met with a degree of success in penetrating major retailers, we found that we were unable to achieve product sell through at the retail level at a rate adequate to generate the revenues that would be needed to fund the ongoing costs of building brand awareness and achieving profitability in the DTR channel, as well as sustaining our operations.

16

Accordingly, in August 2010, we engaged a consulting and advisory firm with experience in the beverage industry, to explore strategic options, including additional financing and/or a potential sale of the Company. To date, the Company has not received any offers for either additional financing or a potential sale transaction.

As a result of the losses we incurred, the Company decided in December 2010 to significantly reduce overhead, downsize operations, decrease consumer marketing expenses and review unprofitable accounts and undertake corrective action in order to reduce cash outlays and allow the Company to operate on a break-even or close to break-even basis. While the company believes it has sufficient capital resources to fund its operations for the balance of 2011, the Company believes that without a capital infusion or other strategic transaction, its ability to achieve revenue growth will be limited. Accordingly, management continues to explore strategic options with respect to the financing, sale or restructuring of the Company.

Our financial statements for the period ended December 31, 2010 were prepared assuming we would continue as a going concern, which contemplates the realization of assets and the settlement of liabilities and commitments in the normal course of business. The accompanying consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that could result should we be unable to continue as a going concern.

We borrowed $50,000 from the CEO of the Company in February 2006. We also owed the CEO $171,000 for accrued salaries from 2006 and 2007. The two debts were restructured in to one note accruing 3% interest, monthly payments of $5,000 and with a balloon payment of $64,000 in January 2011. The outstanding balance under the note as of December 31, 2010 was $64,000. The note was restructured in January 2011 to continue monthly payments of $5,000 until paid in full.

In September 2009, we entered into a $6.5 million loan agreement with CDS Ventures of South Florida, LLC. The loan is due in September 2012. Interest was set at 300 basis points over the one-month LIBOR rate. The interest rate was re-negotiated on February 1, 2010 to 700 basis points over one (1) month LIBOR. Interest is payable quarterly. On March 10, 2010, CDS converted $4.5 million of the convertible note into common stock at the exercise price of $10.20 per share.

In July 2010, we entered into a $3.0 million line of credit agreement with CD Financial, LLC. The amounts borrowed thereunder are due in July 2012. Interest was set at five percent per annum and paid quarterly. As of December 31, 2010, the outstanding debt was $2.0 million and we can draw the remaining $1.0 million upon request.

The following table summarizes contractual obligations and borrowings as of December 31, 2010, and the timing and effect that such commitments are expected to have on our liquidity and capital requirements in future periods (in thousands). We expect to fund these commitments primarily with raise of debt or equity capital.

|

Payments Due by Period

|

||||||||||||||||||||

|

Contractual

|

Total

|

Less Than

|

1 to

|

3 to

|

More Than

|

|||||||||||||||

|

Obligations

|

1 Year

|

3 Years

|

5 Years

|

5 Years

|

||||||||||||||||

|

Debt to related party

|

$ | 2,064 | 64 | 2,000 | — | — | ||||||||||||||

|

Convertible note, related parties

|

2,000 | — | 2,000 | — | — | |||||||||||||||

|

Purchase obligations

|

— | — | — | — | — | |||||||||||||||

|

Total

|

$ | 4,064 | $ | 64 | $ | 4,000 | $ | — | $ | — | ||||||||||

Our Securities Purchase Agreement with Golden Gate Investors, Inc.

On December 19, 2007, we entered into a securities purchase agreement with Golden Gate Investors, Inc (GGI). The purchase agreement included four tranches of $1,500,000 each. The first tranche consisted of our 7.75% convertible debenture issued in exchange for $250,000 in cash and a promissory note for $1,250,000 issued by GGI which was to mature on February 1, 2012. The promissory note contained a prepayment provision which required GGI to make prepayments of interest and principal of $250,000 monthly upon satisfaction of certain conditions. One of the conditions to prepayment was that GGI may immediately sell all of the common stock issued upon Conversion (as defined in the debenture) pursuant to Rule 144 of the Securities Act of 1933. We were under no contractual obligation to ensure that GGI may immediately sell all of the Common Stock Issued at Conversion (as defined in the debenture) pursuant to Rule 144 under the Securities Act of 1934. In the event that GGI may not immediately sell all of the Common Stock Issued at Conversion pursuant to Rule 144, GGI would be under no obligation to prepay the promissory note and likewise under no obligation to exercise its conversion rights under the debenture. If GGI did not fully convert the debenture by its maturity on December 19, 2011, the balance of the debenture was to be offset by any balance due to us under the promissory note. On September 8, 2009, the Company entered into an addendum to the agreement with GGI. The balance of the note receivable, $250,000 was netted against the balance of the debenture. All future tranches were cancelled and terminated without penalty to either party. The remaining balance of the debenture was converted in June 2010. In total, GGI converted $1.2 million of its convertible debenture through June 2010 receiving 972,078 shares of common stock.

17

Our Securities Purchase Agreements with CDS Ventures of South Florida, LLC