Attached files

| file | filename |

|---|---|

| EX-10 - ALFRED KAHN SEPARATION AGREEMENT - 4Licensing Corp | akahnsepagt.htm |

| EX-23 - AUDITORS CONSENT DATED DECEMBER 31, 2010 - 4Licensing Corp | eisnerconsent123110.htm |

| EX-31.1 - PEO CERTIFICATION DATED DECEMBER 31, 2010 - 4Licensing Corp | peocertification123110.htm |

| EX-31.2 - CFO CERTIFICATION DATED DECEMBER 31, 2010 - 4Licensing Corp | cfocertification123110.htm |

| EX-32 - JOINT CERTIFICATION DATED DECEMBER 31, 2010 - 4Licensing Corp | jointcertification123110.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the fiscal year ended December 31, 2010

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from _______________ to _______________

Commission File No. 0-7843

4Kids Entertainment, Inc.

(Exact name of registrant as specified in its charter)

New York 13-2691380

(State or other jurisdiction of (I.R.S. Employer

incorporation or organization) Identification No.)

53 West 23rd Street, New York, New York 10010

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (212) 758-7666

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.01 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes __ No X

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes___ No X

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. Yes X No ___

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes X No __

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer,” “accelerated filer" and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ___ Accelerated filer___ Non-accelerated filer ___ Smaller reporting company X

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes___ No X

The aggregate market value of the voting stock held by non-affiliates of the registrant, based on the closing price of the Common Stock on June 30, 2010 as reported on the OTC Bulletin Board, was approximately $4,976,372. The calculation of the aggregate market value of voting stock excludes shares of Common Stock held by current executive officers, directors, and stockholders that the registrant has concluded are affiliates of the registrant. Exclusion of such shares should not be construed to indicate that any such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the registrant or that such person is controlled by or under common control with the registrant.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Common Stock, $.01 Par Value 13,528,958

(Title of Class) (No. of Shares Outstanding at March 30, 2011)

Portions of the registrant’s Proxy Statement for the Annual Meeting of Stockholders to be held on May 25, 2011 are incorporated by reference into Part III of this Annual Report on Form 10-K.

|

10-K Part

and Item No.

|

Page No.

|

|

|

PART I

|

||

|

Item 1

|

Business

|

1

|

|

Item 1A

|

Risk Factors

|

4

|

|

Item 1B

|

Unresolved Staff Comments

|

8

|

|

Item 2

|

Properties

|

9

|

|

Item 3

|

Legal Proceedings

|

9

|

|

Item 4

|

Removed and Reserved

|

11

|

|

PART II

|

||

|

Item 5

|

Market for the Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities

|

11

|

|

Item 6

|

Selected Consolidated Financial Data

|

12

|

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

14

|

|

Item 7A

|

Quantitative and Qualitative Disclosures About Market Risk

|

28

|

|

Item 8

|

Financial Statements and Supplementary Data

|

29

|

|

Item 9

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

29

|

|

Item 9A

|

Controls and Procedures

|

29

|

|

Item 9B

|

Other Information

|

30

|

|

PART III

|

||

|

Item 10

|

Directors and Executive Officers of the Registrant

|

30

|

|

Item 11

|

Executive Compensation

|

30

|

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

30

|

|

Item 13

|

Certain Relationships and Related Transactions

|

30

|

|

Item 14

|

Principal Accountant Fees and Services

|

30

|

|

PART IV

|

||

|

Item 15

|

Exhibits and Financial Statement Schedules

|

31

|

PART I

Throughout this Annual Report on Form 10-K, we “incorporate by reference” certain information in parts of other documents filed with the Securities and Exchange Commission (the “SEC”). The SEC allows us to disclose important information by referring to it in that manner. Please refer to such information.

This Annual Report on Form 10-K, including the sections titled "Item 1A. Risk Factors" and "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" contains forward-looking statements that relate to future events or our future financial performance. We may also make written and oral forward-looking statements in our Securities and Exchange Commission ("SEC") filings and otherwise. We have tried, where possible, to identify such statements by using words such as "believe," "expect," "intend," "estimate," "anticipate," "will," "project," "plan" and similar expressions in connection with any discussion of future operating or financial performance. Any forward-looking statements are and will be based upon our then-current expectations, estimates and assumptions regarding future events and are applicable only as of the dates of such statements. By their nature, forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those anticipated in any forward-looking statements. Such risks and uncertainties include those described in "Item 1A. Risk Factors" below as well as other factors. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Throughout this Annual Report on Form 10-K, all dollar amounts are reported in thousands unless otherwise specified.

General Development and Narrative Description of Business - 4Kids Entertainment, Inc., together with the subsidiaries through which its businesses are conducted (the “Company”), is a diversified entertainment and media company specializing in the youth oriented market with operations in the following business segments: (i) Licensing; (ii) Advertising Media and Broadcast; and (iii) Television and Film Production/Distribution. The Company was organized as a New York corporation in 1970.

Licensing - The Licensing business segment consists of the results of operations of the following wholly-owned subsidiaries of the Company: 4Kids Entertainment Licensing, Inc. (“4Kids Licensing”); 4Sight Licensing Solutions, Inc. (“4Sight Licensing”); 4Kids Entertainment International, Ltd. (“4Kids International”); and 4Kids Technology, Inc. (“4Kids Technology”). 4Kids Licensing is engaged in the business of licensing the merchandising rights to popular children’s television series, properties and product concepts (individually, the “Property” or collectively the “Properties”). 4Kids Licensing typically acts as exclusive merchandising agent in connection with the grant to third parties of licenses to manufacture and sell all types of merchandise, including toys, videogames, trading cards, apparel, housewares, footwear, books and other published materials, based on such Properties. 4Sight Licensing is engaged in the business of licensing properties and product concepts to adults, teens and “tweens”. 4Sight Licensing focuses on brand building through licensing. 4Kids International, based in London, manages Properties represented by the Company in the United Kingdom and European marketplaces. 4Kids Technology develops ideas and concepts for licensing which integrate new and existing technologies with traditional game and toy play patterns.

The Licensing segment accounted for approximately 83%, 70% and 41% of consolidated net revenues for the years ended December 31, 2010, 2009 and 2008, respectively.

Advertising Media and Broadcast - The Company, through a multi-year agreement with The CW Network, LLC (“The CW”), leases The CW’s Saturday morning programming block (“The CW4Kids”), which broadcasts in most markets from 7am to 12pm, for an initial term of five years beginning with The CW's 2008-2009 broadcast season. The Company provides substantially all programming content to be broadcast on The CW4Kids. 4Kids Ad Sales, Inc. (“4Kids Ad Sales”), a wholly-owned subsidiary of the Company, retains a portion of the revenue from its sale of network advertising time for the five-hour time period.

The Company, through a multi-year agreement (the “Fox Agreement”) with Fox Broadcasting Corporation (“Fox”), leased Fox’s Saturday morning programming block (“4Kids TV”) from 8am to 12pm eastern/pacific time (7am to 11am central time) until December 31, 2008. The Company provided substantially all programming content to be broadcast on 4Kids TV and 4Kids Ad Sales retained all of the revenue from its sale of network advertising time for the four-hour programming block.

The Advertising Media and Broadcast segment also generates revenues from the sale of advertising on the Company’s multiple websites. These websites showcase and promote The CW4Kids, as well as 4Kids’ many Properties.

The Advertising Media and Broadcast segment accounted for 6%, 8% and 39% of consolidated net revenues for the years ended December 31, 2010, 2009 and 2008, respectively.

1

Television and Film Production/Distribution - The Television and Film Production/Distribution business segment consists of the results of operations of the following wholly-owned subsidiaries of the Company: 4Kids Productions, Inc. (“4Kids Productions”); 4Kids Entertainment Music, Inc. (“4Kids Music”); and 4Kids Entertainment Home Video, Inc. (“4Kids Home Video”). 4Kids Productions produces and adapts animated and live-action television programs and theatrical motion pictures for distribution to the domestic and international television, home video and theatrical markets. 4Kids Music composes original music for incorporation into television programming produced by 4Kids Productions and markets and manages such music. 4Kids Home Video distributes home videos associated with television programming produced by 4Kids Productions

The Television and Film Production/Distribution segment accounted for 11%, 22% and 20% of consolidated net revenues for the years ended December 31, 2010, 2009 and 2008, respectively.

Discontinued Operation - Trading Card and Game Distribution - Through its wholly-owned subsidiary, 4Kids Digital Games, Inc. (“4Kids Digital”), the Company owns 55% of TC Digital Games LLC, a Delaware limited liability company (“TC Digital”) which produces, markets and distributes the “Chaotic” trading card game. Through its wholly-owned subsidiary, 4Kids Websites, Inc. (“4Kids Websites”), the Company owns 55% of TC Websites LLC, a Delaware limited liability company (“TC Websites”) which owns and operates www.chaoticgame.com, the companion website for the “Chaotic” trading card game. TC Digital and TC Websites were the exclusive licensees of certain patents covering the uploading of coded trading cards to a website where online game play and community activities occur. Effective September 30, 2010, the Company terminated the operations of TC Digital and TC Websites due to their continued lack of profitability. The termination of the business of TC Digital and TC Websites will enable the Company to further reduce costs and focus on its core businesses. As a consequence of the termination of their operations, TC Digital and TC Websites ceased supporting the Chaotic trading card game and website, effective October 1, 2010. The results of operations of TC Digital and TC Websites are reported in the Company’s consolidated financial statements as discontinued operations subject to a noncontrolling interest (see Note 12 of the notes to the Company’s consolidated financial statements). All prior financial statements have been reclassified to conform to the presentation of this discontinued operation.

Certain of the Company’s former executive officers have interests in Chaotic USA Digital Games LLC (“CUSA LLC”), Chaotic USA Entertainment Group, Inc. (“CUSA”) and certain other entities with which TC Digital and TC Websites have engaged in transactions since their formation. Information regarding these relationships can be found in Note 18 of the notes to the Company’s consolidated financial statements.

Recent Developments; A Going Concern- We have experienced substantial net losses, as well as negative cash flows from operations, in recent years, and have used substantial amounts of cash to fund our operating activities. Sales by us of certain securities held in our investment portfolio as well as certain other assets have significantly contributed to the funding of these operating losses. In addition to the financial challenges we are facing, on March 24, 2011, the Company received a letter from Asatsu-DK Inc (“ADK”) on behalf of itself and TV Tokyo Corporation (collectively, the “Licensors”) purporting to terminate the agreement dated July 1, 2008 between the Licensors and the Company with respect to the Yu-Gi-Oh! Property (the “Yu-Gi-Oh! Agreement”), which accounted for approximately 36% of the Company’s net revenue for the year ended December 31, 2010, for alleged breaches of the Yu-Gi-Oh! Agreement by the Company. On March 24, 2011, the Licensors filed a lawsuit against the Company in the United States District Court for the Southern District of New York also claiming that the Company has breached the Yu-Gi-Oh! Agreement and seeking more than $4,700 in damages. While the Company believes that the Licensors’ purported termination of the Yu-Gi-Oh! Agreement is invalid and ineffective, a finding that such purported termination is valid would have a material adverse effect on the Company’s financial condition and results of operations and would likely significantly impede the Company’s ability to continue its operations. Our overall cash and investment position as of December 31, 2010 together with the realized and anticipated effects of the significant cost cutting initiatives we implemented during 2009 and 2010 provides limited liquidity to fund our day-to-day operations. The financial challenges facing us as a result of our recent history of losses and the limited liquidity available to us to fund day-to-day operations, together with the potential loss of the benefits of the Yu-Gi-Oh! Agreement as a result of the actions of the Licensors raise substantial doubt regarding our ability to continue as a going concern. Our ability to achieve and maintain profitability and positive cash flow is dependent upon our ability to retain the benefits of the Yu-Gi-Oh Agreement and successfully dispute the Licensors damages claims as well as our ability to generate other revenues. If the Company’s continued attempts to resolve the dispute with the Licensors are unsuccessful, the Company intends to take all actions it deems necessary to preserve its business and assets, including the potential filing of a petition under Chapter 11 of the United States Bankruptcy Code. A bankruptcy filing by us would subject our business and operations to various risks.

Our consolidated financial statements have been prepared assuming that we will be able to continue to operate as a going concern. Our historical recurring losses and negative cash flows from operations together with the dispute with the Licensors under the Yu-Gi-Oh! Agreement has caused our independent registered public accounting firm to include an explanatory paragraph in their report dated March 30, 2011 expressing substantial doubt about our ability to continue as a going concern.

2

Financial Information About Industry Segments - Financial information regarding the Company’s industry segments and non-U.S. sales and assets can be found in Note 20 of the notes to the Company’s consolidated financial statements.

Dependence on a Few Sources of Revenues - The Company typically derives a substantial portion of its revenues from a small number of Properties, which usually generate revenues for only a limited period of time. The Company’s revenues are highly subject to changing trends in the toy, game and entertainment businesses, causing dramatic increases and decreases from year to year due to the popularity of particular Properties. It is not possible to accurately predict the length of time that a Property will be commercially successful and/or if a Property will be commercially successful at all. Due to these factors, the Company must continually seek new properties from which it can derive revenues. In addition, the Company also does not control the timing of the release of products by licensees which can affect both the amount of licensing revenues earned and the periods during which such revenues are recognized.

Two Properties, “Yu-Gi-Oh!” and “Pokémon” represented 36% and 20%, respectively, of consolidated net revenues for fiscal 2010. One licensee, Konami Corporation, represented 39% of consolidated net revenues for fiscal 2010. For more information on the Company’s Revenues/Major Customers, please see Note 8 of the notes to the Company’s consolidated financial statements.

Trademarks and Copyrights - Except as provided below, the Company generally does not own any trademarks or copyrights in Properties which the Company represents as a merchandising agent. The trademarks and copyrights are typically owned by the creators of the Properties or by other entities, which may have expended substantial amounts of resources in developing or promoting the Properties.

The Company owns the copyrights and trademarks to “Charlie Chan” and the “WMAC Masters” live action television series. The Company is also a joint copyright holder of the “Cubix” CGI television series and the “Chaotic” animated television series produced by 4Kids Productions. Additionally, the Company is a joint copyright holder of the “Chaotic” trading card artwork for the “Chaotic” trading card game. The Company also jointly owns the copyright to the “Chaotic” trading card game as it relates to revisions to the original “Chaotic” trading card game previously sold in Denmark. The Company, through its 55% ownership interest in TC Websites, jointly owns the intellectual property rights to the website, including certain proprietary software contained in the website which enables “Chaotic” website visitors to play the “Chaotic” trading card game online at www.chaoticgame.com.

Seasonal Aspects - A substantial portion of the Company’s revenues and net income are subject to the seasonal and trend variations of the toy and game industry. Typically, a majority of toy orders are shipped in the third and fourth calendar quarters. Historically, the Company’s net revenues from toy and game royalties during the second half of the year have generally been greater than during the first half of the year. Additionally, advertising revenues derived from the sale of commercial time on The CW4Kids is generally higher in the fourth quarter due to higher advertising rates typically charged to children’s advertisers for advertising during the holiday season.

Competition - The Company’s principal competitors in the Licensing segment are the large media companies (e.g., Disney, Time Warner and Nickelodeon, which is owned by Viacom) with consumer products/merchandise licensing divisions, toy companies, other licensing companies, and numerous individuals who act as merchandising agents. There are also many independent product development firms with which the Company competes. Many of these companies have substantially greater resources than the Company and represent properties which have been commercially successful for longer periods than the Properties represented by the Company. The Company believes it would be relatively easy for a potential competitor to enter the market in light of the relatively small investment required to commence operations as a merchandising agent.

The Company’s Advertising Media and Broadcast segment also operates in a highly competitive marketplace against large media companies (e.g., Disney, Time Warner, CBS, NBC and Nickelodeon, which is owned by Viacom) with substantially greater resources and distribution networks than the Company. The Company’s ability to derive advertising revenue from the sale of commercial time on The CW4Kids, as well as internet advertising on its websites, substantially depends on the popularity of the television shows that the Company broadcasts. The Company also faces significant competition from other television broadcasters and cable networks, which also broadcast children’s television shows on Saturday mornings and sell advertising on their related websites.

The Company’s Television and Film Production/Distribution segment competes with all forms of entertainment directed at children. There are a significant number of companies that produce and/or broadcast television programming, distribute theatrical motion pictures and home videos for the children’s audience and program websites directed to children. The Company also competes with these companies to obtain creative talent to write, adapt, score, provide voice-overs and produce the television programs and theatrical motion pictures marketed by the Company.

3

Employees - As of March 30, 2011, the Company had a total of 89 full-time employees in its domestic and international operations. Of the total, 46 employees were primarily rendering services for the Licensing segment, 17 were primarily rendering services for the Advertising Media and Broadcasting segment and 26 were primarily rendering services for the Television and Film Production/Distribution segment. The Company also hires additional employees on a program-by-program basis whose compensation is typically allocated to the capitalized cost of the related programming.

Available Information - The Company’s Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports, and the Proxy Statement for its Annual Meeting of Stockholders are made available, free of charge, through its website, www.4kidsentertainment.com, as soon as reasonably practicable after such reports have been filed with or furnished to the Securities and Exchange Commission (the “SEC”). In addition, you may read and copy any materials the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site, www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Executive Officers of the Company

|

Name

|

Age

|

Employed By Registrant Since

|

Recent Position(s) Held As Of March 30, 2011

|

|||

|

Bruce R. Foster

|

51

|

2002

|

Executive Vice President and Chief Financial Officer (since 2005); Senior Vice President of Finance (2002 to 2005)

|

|||

|

Samuel R. Newborn

|

56

|

2000

|

Executive Vice President and General Counsel

|

|||

|

Brian Lacey

|

60

|

2003

|

Executive Vice President, International

|

|||

|

Daniel Barnathan

|

56

|

2002

|

President of 4Kids Ad Sales, Inc.

|

Item 1A. Risk Factors.

The following significant factors, as well as others of which we are unaware or deem to be immaterial at this time, could materially adversely affect our business, financial condition or operating results in the future. Therefore, the following information should be considered carefully together with other information contained in this report. Past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods.

We have experienced operating losses and negative cash flows from operations during recent years and these financial challenges together with the possible loss of our license to the Yu-Gi-Oh! Property has caused substantial doubt about our ability to continue as a going concern and could lead to a Chapter 11 bankruptcy filing.

We have experienced substantial net losses, as well as negative cash flows from operations, in recent years, and have used substantial amounts of cash to fund our operating activities. Sales by us of certain securities held in our investment portfolio as well as certain other assets have significantly contributed to the funding of these operating losses. If we do not become profitable and generate positive cash flows from operations, we will require additional sources of cash to fund continued operations. If such additional funding is needed, we will consider all alternatives available to us, including, but not limited to sales of assets, issuance of equity or debt securities and third party arrangements. There can be no assurance, however, that we would be able to generate such additional cash in a timely manner or that such additional cash could be obtained on terms acceptable to us.

In addition to the financial challenges we are facing, on March 24, 2011, the Company received a letter from the Licensors purporting to terminate the agreement dated July 1, 2008 between the Licensors and the Company with respect to the Yu-Gi-Oh! Agreement, which accounted for approximately 36% of the Company’s net revenue for the year ended December 31, 2010, for alleged breaches of the Yu-Gi-Oh! Agreement by the Company. On March 24, 2011, the Licensors filed a lawsuit against the Company in the United States District Court for the Southern District of New York also claiming that the Company has breached the Yu-Gi-Oh! Agreement and seeking more than $4,700 in damages. While the Company believes that the Licensors’ purported termination of the Yu-Gi-Oh! Agreement is invalid and ineffective, a finding that such purported termination is valid would have a material adverse effect on the Company’s financial condition and results of operations and would likely significantly impede the Company’s ability to continue its operations. If the Company’s continued attempts to resolve the dispute with the Licensors are unsuccessful, the Company intends to take all actions it deems necessary to preserve its business and assets, including the potential filing of a petition under Chapter 11 of the United States Bankruptcy Code.

4

A bankruptcy filing by us would subject our business and operations to various risks, including but not limited to, the following:

|

·

|

A bankruptcy filing may adversely affect our business prospects, including our ability to continue to obtain and maintain the contracts necessary to operate our business on competitive terms;

|

|

·

|

We may be unable to retain and motivate key executives and employees through the bankruptcy process, and we may have difficulty attracting new employees;

|

|

·

|

There can be no assurance as to our ability to maintain or obtain sufficient financing sources for operations or to fund any reorganization plan and meet future obligations;

|

|

·

|

There can be no assurance that we will be able to successfully develop, prosecute, confirm and consummate one or more plans of reorganization that are acceptable to the bankruptcy court and our creditors, equity holders and other parties in interest;

|

|

·

|

The value of our common stock could be reduced to zero as result of a bankruptcy filing.

|

Our overall cash and investment position as of December 31, 2010 together with the realized and anticipated effects of the significant cost cutting initiatives we implemented during 2009 and 2010 provides only limited liquidity to fund our day-to-day operations. The financial challenges facing us as a result of its recent history of losses and the limited liquidity available to us to fund day-to-day operations, together with the potential loss of the benefits of the Yu-Gi-Oh! Agreement as a result of the actions of the Licensors raise substantial doubt regarding our ability to continue as a going concern. Our ability to achieve and maintain profitability and positive cash flow is dependent upon a number of factors, including our ability to retain the benefits of the Yu-Gi-Oh Agreement and successfully dispute the Licensors damages claims as well as our ability to generate additional revenues.

Our common stock was delisted from the New York Stock Exchange

On June 1, 2010, our common stock was delisted from the New York Stock Exchange. Our common stock currently trades on the over-the-counter bulletin board market, although there are no assurances that it will continue to trade on this market. Over-the-counter (“OTC”) transactions involve risks in addition to those associated with transactions on a stock exchange. The delisting and OTC status could harm the trading volume and liquidity of our common stock and, as a result, the market price for our common stock might become more volatile. The delisting and OTC status could also cause a reduction in the number of investors willing or able to hold or acquire our common stock, transactions in our common stock could be delayed and securities analysts’ and news media coverage of us may be reduced. These factors could result in lower prices and larger spreads in the bid and ask prices for shares of our common stock. Delisting and OTC status could also make our common stock substantially less attractive as collateral for loans, for investment by potential financing sources under their internal policies or state legal investment laws or as consideration in future capital raising transactions. Furthermore, the delisting and OTC status may have other negative implications, including the potential loss of confidence by suppliers, partners and employees. Our OTC status may also make it more difficult and expensive for us to comply with state and federal securities laws in connection with future financings, acquisitions or equity issuances to employees and other service providers, thereby making it more difficult and expensive for us to raise capital, acquire other businesses using our stock and compensate our employees using equity.

We have been and may continue to be negatively affected by adverse general economic and other conditions.

Conditions in the domestic and global economies are extremely unpredictable and our business has been impacted by changes in such conditions. Softening global economies, stock market uncertainty and wavering consumer confidence caused by economic weakness, the decline in the housing market, the threat or occurrence of terrorist attacks, war or other factors generally affecting economic conditions have adversely affected our business, financial condition and results of operations and may continue to do so in the future.

Recent turmoil in U.S. and foreign credit markets, equity markets, and in the global financial services industry, including the bankruptcy, failure, collapse or sale of various financial institutions and an unprecedented level of intervention from the U.S. and foreign governments, have continued to place pressure on the global economy and affect overall consumer spending, spending by advertisers and the availability of credit to us, our clients, and our customers. If conditions in the global economy, U.S. economy or other key vertical or geographic markets remain uncertain or weaken further, they may have a further material adverse effect on our business, financial condition and results of operations.

5

The changing entertainment preferences of consumers could adversely affect our business.

Our business and operating results depend upon the appeal of our Properties, product concepts and programming to consumers. Consumer entertainment preferences, as well as industry trends and demands are continuously changing and are difficult to predict as they vary over time. In addition, as entertainment properties often have short life cycles, there can be no assurances that:

|

(i)

|

our current Properties, product concepts or programming will continue to be popular for any significant period of time;

|

|

(ii)

|

new Properties, product concepts or programming we represent or produce will achieve and or sustain popularity in the marketplace;

|

|

(iii)

|

a Property’s life cycle will be sufficient to permit us to recover revenues in excess of the costs of advance payments, guarantees, development, marketing, royalties and other costs relating to such Property; or

|

|

(iv)

|

we will successfully anticipate, identify and react to consumer preferences.

|

Our failure to accomplish any of these events could result in reduced overall revenues, which could have a material adverse effect on our business, financial condition and results of operations. In addition, the volatility of consumer preferences could cause our revenues and net income to vary significantly between comparable periods.

Revenues from our Licensing segment are largely derived from a small number of Properties and are subject to changing industry trends.

We have historically derived a substantial portion of our licensing revenues from a small number of Properties which usually generate revenues only for a limited period of time. For the year ended December 31, 2010, we derived approximately 65%, or $7,745 of our licensing revenues from two Properties. Our licensing revenues are also subject to the changing trends in the toy, game and entertainment industries. Consequently, our licensing revenues may be subject to dramatic increases and decreases from particular sources over time. In addition, we do not control the timing of the release of products by licensees which can affect both the amount of licensing revenues earned and the periods during which such revenues are recognized. A significant decrease in our licensing revenues could have a material adverse impact on our financial condition and results of operations. Additionally, due to the expiration or termination in 2010 of representation agreements between the Company and various licensors and the expiration of the “Teenage Mutant Ninja Turtles”, “Monster Jam” and “Cabbage Patch Kids” license agreements, the Company is likely to receive only a small share of merchandise licensing revenues in 2011 from those long-standing Properties. There can be no assurance that the Company will be able to license new properties to replace the substantial revenue streams contributed by the “Teenage Mutant Ninja Turtles”, “Monster Jam” and “Cabbage Patch Kids” Properties to the Company in previous years.

Revenues from our Licensing segment are directly impacted by the amount of retail shelf space dedicated to our Properties.

As an exclusive merchandising agent, we grant licenses to third parties to manufacture and sell all types of merchandise based on the Properties that we represent. The ability of these third parties to design, manufacture, and ultimately market and sell this merchandise through various distribution channels has a direct impact on our revenues. If these third parties are not successful in obtaining distribution or placement for this merchandise at retail, the performance of certain Properties could suffer which could have a material adverse impact on our financial condition and results of operations.

Our operating margins could be adversely impacted by the mix of Properties we represent.

Historically, the majority of the television episodes produced by our production studio were English language dubbed versions of previously produced foreign language programming. We were able to license television broadcast rights, home video rights and merchandising rights to such foreign language programming for rights fees that were substantially below the cost of producing original programming. Beginning in 2005, we began shifting our strategic focus toward the production of more original animated programming in an effort to obtain a higher percentage of revenues and build the value of our programming library. The investment required to produce original animated programming is substantially greater than our historical cost of dubbing and adapting existing foreign language animated programming. Our production of original programming funded in whole or in part by us has resulted in a substantial increase in capitalized film costs that will be amortized based on overall market acceptance and projected revenues. To the extent that a Property performs at a level lower than our expectations, the ratio of amortization expense will increase and may adversely impact our operating margins and results of operations. Our investment in original programming has not been successful and we have been required to write-down capitalized film costs associated with the unsuccessful series, which has had a material adverse impact on our financial condition and results of operations.

6

We must continually seek new Properties from which we can derive revenues.

It is difficult to predict whether a Property will be successful, and if so, for how long. Because of this, we are constantly seeking new Properties that are already successful or that we believe are likely to become successful in the future. If we are unable to identify and acquire the rights to successful new Properties, our revenues, financial condition and results of operations could be adversely affected.

Our business is seasonal and highly dependent on our performance during the holiday season.

A high percentage of our annual operating results have historically depended on our performance during the holiday season. Sales of our licensed toy and game concepts are seasonal and most retail sales of these products occur during the third and fourth fiscal quarters. Also, as a result of the increased demand for commercial time by children’s advertisers during the holiday season, a significant portion of the revenues of 4Kids Ad Sales is generated during the fourth fiscal quarter. The financial results of The CW4Kids will be affected by how successful it is in attracting viewers during the holiday season. As a result of the seasonal nature of our business, we would be significantly and adversely affected by unfavorable economic conditions and other unforeseen events during the holiday season, such as a terrorist attack or a military engagement, that negatively affect the retail environment or consumer buying patterns. In addition, a failure by us to supply programming to The CW4Kids during the holiday season could have a material adverse impact on our financial condition and results of operations.

We operate in a highly competitive marketplace.

Licensing. Our principal competitors in the Licensing segment are the large media companies (e.g., Disney, Time Warner and Nickelodeon, which is owned by Viacom) with consumer products/merchandise licensing divisions, toy companies, other licensing companies, and numerous individuals who act as merchandising agents. There are also many independent product development firms with which we compete. Many of these companies have substantially greater resources than we do and represent properties which have been commercially successful for longer periods than our Properties. We believe that it would be relatively easy for a potential competitor to enter this market in light of the relatively small investment required to commence operations as a merchandising agent.

Advertising Media and Broadcast. Our Advertising Media and Broadcast segment also operates in a highly competitive marketplace against large media companies (e.g., Disney, Time Warner, CBS, NBC and Nickelodeon, which is owned by Viacom) with substantially greater resources and distribution networks than we have. Our ability to derive advertising revenues from the sale of commercial time on The CW4Kids, substantially depends on the popularity of the television shows that we broadcast. We also face significant competition from other television broadcasters and cable networks, which also broadcast children’s television shows on Saturday mornings. Saturday morning broadcast television for children has been losing popularity over the last few years to the children’s cable television channels such as Nickelodeon, Cartoon Network and the Disney Channel. In addition, the popularity of the internet, video on demand, digital video recording of programming and other trends have caused a fragmentation of the audience. Both of these trends have resulted in lower advertising revenues from the sale of advertising time on The CW4Kids. The continued reduction of advertising revenues, as a result of these and other trends, has adversely affected our business and the results of operations.

Television and Film Production/Distribution. Our Television and Film Production/Distribution segment competes with all forms of entertainment directed at children. There are a significant number of companies that produce and/or broadcast television programming and distribute theatrical motion pictures and home videos for the children’s audience. We also compete with these companies to obtain creative talent to write, adapt, score, provide voice-overs and produce the television programs and theatrical motion pictures marketed by us.

Our broadcasting costs may increase or our advertising revenues may decrease due to events beyond our control.

The success of our Advertising Media and Broadcast segment is largely dependent on the amount of advertising revenues generated from sales of network advertising on The CW4Kids. Recently, there has been increased scrutiny of food advertising directed at children as a result of childhood obesity concerns. In response to these concerns, many significant food advertisers have reduced or eliminated advertising of food products directed toward children resulting in a reduction in the advertising dollars spent in the children’s television and internet advertising marketplace. In addition, international, political and military developments may result in increases in broadcasting costs or loss of advertising revenue due to, among other things, the preemption of our programming.

7

Our future success is dependent on certain key employees.

The success of our business depends to a significant extent upon the skills, experience and efforts of a number of senior management personnel and other key employees. In certain instances, we have employment agreements in place as a method of retaining the services of these key employees. The loss of the services of any of our senior management personnel or other key employees could have a material adverse effect on our business, results of operations or financial condition. On January 11, 2011, we announced that Alfred R. Kahn had retired and resigned from his position as Chief Executive Officer of the Company, as Chairman of the Company’s Board of Directors, and as a member of our Board of Directors, effective January 10, 2011. Our Company’s Board of Directors has appointed Director Michael Goldstein as interim Chairman and our existing executive senior management personnel are currently responsible for running our operations. We are not currently seeking a replacement chief executive officer pending the outcome of the process currently being undertaken by a special committee of our Board of Directors formed for the purpose of exploring potential strategic alternatives. Due to financial uncertainty affecting the Company and our limited resources, we may have difficulty in attracting new executive talent.

We may not be able to successfully protect our intellectual property rights.

We rely on a combination of copyright, trademark, patent and other proprietary rights laws to protect the intellectual property rights that we own or license. It is possible that third parties may challenge our rights to such intellectual property. In addition, there is a risk of third parties infringing upon our licensors’ or our intellectual property rights and producing counterfeit products. These events may result in lost revenue as well as litigation, which may be expensive and time-consuming even if a favorable outcome is obtained. There can be no assurance that adequate remedies would be available for any infringement of the intellectual property rights owned or licensed by the Company. Any such failure to successfully protect our intellectual property rights may have a material adverse effect on our competitive position.

We may be subject to audit claims from our partners.

We are currently participating in audits by certain of our Property partners. The parties have met several times to discuss a resolution of the audit issues. There can be no assurance that the parties will conclude their discussions regarding the audit issues satisfactorily. Any such failure to successfully resolve the audit issues may result in litigation which may have a material adverse effect on our financial position or the results of our operations.

We must be able to respond to rapidly changing technology occurring within our industry.

Our success will depend, in part, on our ability to anticipate and adapt to numerous changes in our industry resulting from technological developments such as the internet, broadband distribution of entertainment content and the adoption of digital television standards. These new distribution technologies may diminish the size of the audience watching broadcast television and require us to fundamentally change the way we market and distribute our Properties. For example, digital technology is likely to accelerate the convergence of broadcast, telecommunications, internet and other media and could result in material changes in the regulations, intellectual property usage and technical platforms on which our business relies. These changes could significantly decrease our revenues or require us to incur significant capital expenditures.

Potential labor disputes may lead to increased costs or disrupt the operation of our business.

The success of our business is dependent on our employees who are involved with our domestic and international operations. Any labor dispute may adversely affect one or more of our business segments through increased costs of operating such segment or disruption of the operations of such segment which could adversely affect our results of operations.

Item 1B. Unresolved Staff Comments.

None.

8

Item 2. Properties.

The following table sets forth, with respect to properties leased (none are owned) by the Company on December 31, 2010, the location of the property, the date on which the lease expires and the use which the Company makes of such facilities:

|

Address

|

Expiration of Lease

|

Use

|

Approximate Square Feet

|

|

53 West 23rd Street, 11th Floor

New York, New York

|

June 30, 2017

|

Executive, Administrative and Production Facilities

|

25,000

|

|

53 West 23rd Street, 6th Floor

New York, New York

|

February 29, 2012

|

Sales, Marketing and Website Development

|

5,600

|

|

1st Floor Mutual House

70 Conduit Street

London, England

|

July 30, 2011

|

International Sales

Office

|

2,400

|

|

12481 High Bluff Drive,

Suite 110

San Diego, California

|

February 24, 2011

|

Trading Card and Game Distribution – Discontinued Operation

|

4,200

|

The executive, marketing, sales and administrative offices are utilized by the Licensing and Advertising Media and Broadcast segments. The international sales office is utilized primarily by the Licensing Segment. The production and the website development facilities are primarily utilized by the Television and Film Production/Distribution segment.

Item 3. Legal Proceedings.

TCD International, Ltd. - On February 12, 2010, Home Focus Development, Ltd., a British Virgin Islands Corporation, (“Home Focus”) filed suit against 4Kids in the United States District Court for the Southern District of New York. Home Focus alleged that 4Kids owed Home Focus $1,075 under an Interest Purchase Agreement among 4Kids, Home Focus and TC Digital entered into on March 2, 2009, pursuant to which the Company acquired a 25% ownership interest in TCD International, Ltd. (“TDI”).

On April 26, 2010, 4Kids filed an answer and asserted various counterclaims against Home Focus and its owners, in their individual capacities. In its counterclaims, 4Kids has alleged that Home Focus failed to make its contractually required initial capital contribution of $250 to TDI necessary to acquire the 25% ownership interest in TDI it purported to sell to the Company and also failed to contribute its 50% share of the expenses. 4Kids has further asserted counterclaims of fraud and misrepresentation.

During the last few months, the parties have had substantive discussions and have exchanged draft agreements regarding the possible resolution of the claims and counterclaims. There can be no assurance that the parties will conclude their settlement discussions satisfactorily.

Pokémon Royalty Audit - During the first quarter of 2010, The Pokémon Company International (“TPC”) commenced an audit of 4Kids covering the period from mid-2001 through 2008. On May 28, 2010, 4Kids received a letter from counsel for TPC ("TPC Letter") claiming that the audit “identified deficiencies totaling almost $4,700” and demanding payment of the deficiency together with interest thereon. The TPC Letter failed to provide any schedules or other specific information regarding the alleged deficiencies. By letter dated June 11, 2010 (“4Kids Letter”), 4Kids disputed the allegations made in the TPC Letter and advised TPC that 4Kids would not be paying the alleged deficiency or any interest thereon. The 4Kids Letter also proposed that, as had been discussed by the parties, 4Kids would audit TPC which was the recipient and payee of Pokémon merchandise licensing, television broadcast and home video proceeds during the 2001 - 2008 period, and that after the completion of the parties’ respective audits, the parties would review the audit reports and discuss any outstanding issues.

On July 14, 2010, 4Kids and TPC executed a tolling agreement tolling the statute of limitations until October 21, 2010 with respect to TPC’s claims. 4Kids and TPC also agreed in the tolling agreement that neither party would commence any litigation against the other party until after the expiration of the tolling period in order to allow for the parties to complete their respective audits and to discuss the results thereof. During mid-June 2010, 4Kids commenced its audit of TPC which 4Kids expects to complete over the next few months. On October 12, 2010, 4Kids and TPC executed an amendment to the tolling agreement extending the tolling of the statute of limitations until January 15, 2011. On January 26, 2011, 4Kids and TPC executed a second amendment to the tolling agreement extending the tolling of the statute of limitations until March 15, 2011. On March 25, 2011, 4Kids and TPC executed a third amendment to the tolling agreement extending the tolling of the statute of limitations until April 15, 2011.

9

Over the last several weeks, the parties have had productive discussions with regard to the resolution of the Pokémon royalty audit.

Yu-Gi-Oh! Royalty Audit - During the first quarter of 2010, ADK, a member of the consortium of Japanese companies that controls the rights to Yu-Gi-Oh! ("Yu-Gi-Oh! Consortium"), commenced an audit of 4Kids with respect to the amounts paid by 4Kids to ADK during the course of the 4Kids representation of Yu-Gi-Oh!, which started in 2001.

On June 25, 2010, 4Kids received a letter from counsel for ADK (“ADK Letter”) alleging that 4Kids had improperly deducted certain expenses from amounts paid to ADK and had failed to pay ADK a share of certain Yu-Gi-Oh! home video revenues. In addition, the ADK Letter requested that 4Kids provide additional documentation with respect to withholding taxes deducted from ADK’s share of Yu-Gi-Oh! revenues. The ADK Letter claimed that the total of the improper deductions and underpayments was approximately $3,000. By letter dated June 29, 2010 (“4Kids Yu-Gi-Oh! Letter”), 4Kids disputed substantially all of the allegations contained in the ADK Letter.

The ADK Letter also demanded that 4Kids and ADK sign a tolling agreement with an effective date of June 1, 2010 which would stop the running of the statute of limitations during the four month tolling period starting on June 1, 2010 and concluding on September 30, 2010. On June 29, 2010, 4Kids and ADK entered into the tolling agreement described above. On October 19, 2010, 4Kids and ADK signed an amendment to the tolling agreement extending the tolling period through December 31, 2010.

On December 20, 2010, 4Kids received a letter from ADK which alleged audit findings of $4,819. By letters dated December 29, 2010, 4Kids disputed substantially all of the alleged audit findings. On January 11, 2011, the parties entered into another amendment to the tolling agreement extending the tolling period through March 31, 2011.

On March 4, 2011, ADK requested a payment from the Company in order for representatives of the Licensors to agree to meet with representatives of the Company. On March 17, 2011, 4Kids made a $1 million payment to ADK as a show of good-faith so that a meeting could take place with ADK to attempt to resolve the audit claims. Notwithstanding the $1 million good-faith payment, the Company also reserved its rights to dispute all of ADK’s audit claims. On March 18, 2011, representatives of 4Kids met with representatives of ADK in a further, but ultimately unsuccessful, attempt to resolve the outstanding issues.

On March 24, 2011, 4Kids received a letter from the Licensors purporting to terminate the agreement dated July 1, 2008 between the Licensors and 4Kids with respect to the Yu-Gi-Oh! Property (the “Yu-Gi-Oh! Agreement”) for alleged breaches of the Yu-Gi-Oh! Agreement by 4Kids. The purported termination letter did not comply with the 10 business day notice and cure provision in the Yu-Gi-Oh! Agreement. On March 24, 2011, the Licensors filed a lawsuit against the Company in the United States District Court for the Southern District of New York also claiming that the Company has breached the Yu-Gi-Oh! Agreement on grounds substantially the same as those asserted in its audit findings and seeking more than $4,700 in damages.

On March 27, 2011, 4Kids, responding to the letter from the Licensors, completely rejected the purported termination of the Yu-Gi-Oh! Agreement by the Licensors as wrongful and devoid of any factual and legal basis. On March 30, 2011, the Company received a letter from counsel to the Licensors reiterating the Licensors’ position with respect to the termination of the Yu-Gi-Oh! Agreement. 4Kids intends to vigorously oppose the purported termination of the Yu-Gi-Oh! Agreement and to defend itself against the claims brought in the lawsuit. Also, notwithstanding the lawsuit and the other actions taken by the Licensors, 4Kids continues its efforts to resolve the dispute with the Licensors.

While 4Kids believes that the Licensors’ purported termination of the Yu-Gi-Oh! Agreement is invalid and ineffective, a finding that such purported termination is valid would have a material adverse effect on the Company’s financial condition and results of operations and would likely significantly impede 4Kids’ ability to continue its operations. If 4Kids’ continued attempts to resolve the dispute with the Licensors are unsuccessful, 4Kids intends to take all actions it deems necessary to preserve its business and assets, including the potential filing of a petition under Chapter 11 of the United States Bankruptcy Code.

4Kids’ consolidated financial statements have been prepared assuming that we will be able to continue to operate as a going concern. 4Kids historical recurring losses and negative cash flows from operations together with the dispute with the Licensors under the Yu-Gi-Oh! Agreement has caused 4Kids’ independent registered public accounting firm to include an explanatory paragraph in their report dated March 30, 2011 regarding their concerns about 4Kids’ ability to continue as a going concern.

10

The Company, from time to time, is involved in litigation, contract disputes and claims arising in the ordinary course of its business. Except as described above, the Company does not believe that such litigation to which the Company or any subsidiary of the Company is a party or of which any of their Properties is the subject or any claims made against it will, individually or in the aggregate, have a material adverse effect on the Company’s financial position or the results of its operations or cash flows.

Item 4. [Removed and Reserved]

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities

(a) Market Information - Our Common Stock has been quoted on the OTC Bulletin Board Market since June 1, 2010 under the trading symbol “KIDE.PK”. Prior to June 1, 2010, our common stock was listed for trading on the New York Stock Exchange under the symbol “KDE”. The following table indicates high and low sales quotations for the periods indicated based upon information reported by the New York Stock Exchange and the OTC Bulletin Board. The prices quoted on the OTC Bulletin Board reflect inter-dealer prices, without retail mark-up, markdown or commissions. The OTC Bulletin Board prices listed below may not represent actual transaction prices.

|

2010

|

Low

|

High

|

||||||

|

First Quarter

|

$ | 1.01 | $ | 1.70 | ||||

|

Second Quarter

|

0.55 | 1.25 | ||||||

|

Third Quarter

|

0.53 | 0.80 | ||||||

|

Fourth Quarter

|

0.32 | 0.64 | ||||||

|

|

||||||||

|

2009

|

Low

|

High

|

||||||

|

First Quarter

|

$ | 1.01 | $ | 2.48 | ||||

|

Second Quarter

|

1.09 | 2.24 | ||||||

|

Third Quarter

|

1.35 | 2.43 | ||||||

|

Fourth Quarter

|

1.30 | 2.15 | ||||||

(b) Holders - The approximate number of holders of record of the Company’s Common Stock on March 30, 2011 was 4,830.

(c) Dividends - There were no dividends or other distributions made by the Company during 2010 or 2009. Future dividend policies will be determined by the Board of Directors based on the Company’s earnings, financial condition, capital requirements and other existing conditions. It is anticipated that cash dividends will not be paid to the holders of the Company’s Common Stock in the foreseeable future.

(d) Equity Compensation Plan Information - Information regarding the Company’s equity compensation plans is incorporated by reference to Item 12 in Part III of this Form 10-K.

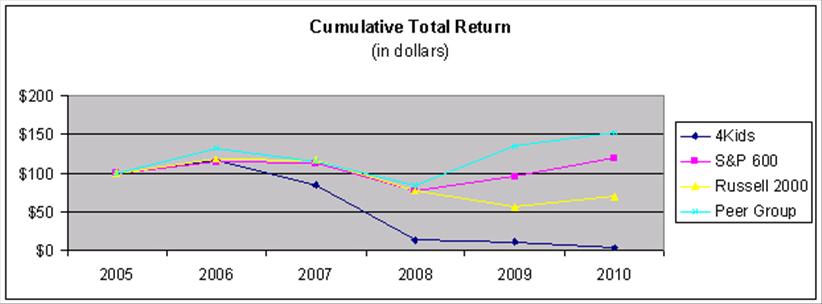

(e) Performance Graph - The following graph compares the cumulative total shareholders return of our common stock with the cumulative return of the Standard & Poor’s Small Cap 600 Index (“S&P 600”), the Russell 2000 Index (“Russell 2000”) and a group of companies, consisting of The Walt Disney Company, Time Warner, Inc., World Wrestling Entertainment, Inc., and Mattel, Inc. (“Peer Group”) for the period beginning December 31, 2005 and ending December 31, 2010. The graph assumes that $100 was invested on December 31, 2005, and that any dividends were reinvested. Marvel Entertainment, Inc. was removed from the peer group as it was purchased by The Walt Disney Company in the current year. The Company intends to continue to evaluate and identify potential companies which may be appropriate for its Peer Group.

11

|

December 31,

|

||||||||||||||||||||||||

|

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

|||||||||||||||||||

|

4Kids

|

$ | 100.00 | $ | 116.12 | $ | 83.81 | $ | 12.49 | $ | 10.13 | $ | 2.61 | ||||||||||||

|

S&P 600

|

$ | 100.00 | $ | 114.07 | $ | 112.68 | $ | 76.63 | $ | 94.85 | $ | 118.55 | ||||||||||||

|

Russell 2000

|

$ | 100.00 | $ | 118.37 | $ | 116.51 | $ | 77.15 | $ | 55.27 | $ | 69.25 | ||||||||||||

|

Peer Group

|

$ | 100.00 | $ | 132.12 | $ | 114.85 | $ | 83.20 | $ | 134.47 | $ | 152.07 | ||||||||||||

ISSUER PURCHASE OF EQUITY SECURITIES

|

Period During 2010

|

Total Number of Shares Purchased

|

Average Price Paid Per Share

|

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs

|

Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs

|

||||||||||||

|

Jan. 1 – Jan. 31

|

— | — | — | — | ||||||||||||

|

Feb. 1 – Feb. 28

|

— | — | — | — | ||||||||||||

|

Mar. 1 – Mar. 31

|

— | — | — | — | ||||||||||||

|

Apr. 1 – Apr. 30

|

— | — | — | — | ||||||||||||

|

May 1 – May 31

|

64,841 | $ | 0.84 | — | — | |||||||||||

|

Jun. 1 – Jun. 30

|

— | — | — | — | ||||||||||||

|

Jul. 1 – Jul. 31

|

— | — | — | — | ||||||||||||

|

Aug. 1 – Aug. 31

|

— | — | — | — | ||||||||||||

|

Sep. 1 – Sep. 30

|

— | — | — | — | ||||||||||||

|

Oct. 1 – Oct. 31

|

— | — | — | — | ||||||||||||

|

Nov. 1 – Nov. 30

|

— | — | — | — | ||||||||||||

|

Dec. 1 – Dec. 31

|

— | — | — | — | ||||||||||||

|

Total

|

64,841 | $ | 0.84 | — | — | |||||||||||

In May 2010, 64,841shares were repurchased to discharge withholding tax obligations upon the vesting of certain employees’ restricted stock awards.

Item 6. Selected Consolidated Financial Data.

(In thousands of dollars, except share and per share data)

Our selected consolidated financial data presented below has been derived from our audited consolidated financial statements and should be read in conjunction with the notes to the Company’s consolidated financial statements and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

12

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Net revenues:

|

||||||||||||||||||||

|

Service revenue

|

$ | 14,478 | $ | 24,394 | $ | 41,925 | $ | 48,428 | $ | 61,661 | ||||||||||

|

Other revenue

|

— | 9,786 | — | — | — | |||||||||||||||

|

Total net revenues

|

14,478 | 34,180 | 41,925 | 48,428 | 61,661 | |||||||||||||||

|

Costs and expenses:

|

||||||||||||||||||||

|

Selling, general and administrative (*)

|

28,011 | 33,175 | 36,966 | 34,974 | 39,001 | |||||||||||||||

|

Amortization of television and film costs

|

6,827 | 21,511 | 7,707 | 8,179 | 8,041 | |||||||||||||||

|

Amortization of 4Kids TV broadcast fee

|

— | — | 16,022 | 21,472 | 22,462 | |||||||||||||||

|

Impairment of investment in international

|

||||||||||||||||||||

|

trading card subsidiary

|

— | 2,430 | — | — | — | |||||||||||||||

|

Total costs and expenses

|

34,838 | 57,116 | 60,695 | 64,625 | 69,504 | |||||||||||||||

|

Loss from operations

|

(20,360 | ) | (22,936 | ) | (18,770 | ) | (16,197 | ) | (7,843 | ) | ||||||||||

|

Interest income

|

403 | 1,076 | 2,722 | 5,281 | 4,143 | |||||||||||||||

|

Impairment of investment securities

|

(3,578 | ) | (6,175 | ) | (7,834 | ) | — | — | ||||||||||||

|

Loss on sale of investment securities

|

(1,616 | ) | (7,647 | ) | — | — | — | |||||||||||||

|

Total other (expense) income

|

(4,791 | ) | (12,746 | ) | (5,112 | ) | 5,281 | 4,143 | ||||||||||||

|

Loss before income taxes

|

(25,151 | ) | (35,682 | ) | (23,882 | ) | (10,916 | ) | (3,700 | ) | ||||||||||

|

Benefit from (provision for) income taxes

|

— | 3,805 | (300 | ) | (2,436 | ) | 3,506 | |||||||||||||

|

Loss from continuing operations

|

(25,151 | ) | (31,877 | ) | (24,182 | ) | (13,352 | ) | (194 | ) | ||||||||||

|

Loss from discontinued operations

|

(6,489 | ) | (20,579 | ) | (12,637 | ) | (9,974 | ) | (812 | ) | ||||||||||

|

Net loss

|

(31,640 | ) | (52,456 | ) | (36,819 | ) | (23,326 | ) | (1,006 | ) | ||||||||||

|

Loss attributable to noncontrolling interests

|

4,479 | 10,380 | — | — | — | |||||||||||||||

|

Net loss attributable to 4Kids Entertainment, Inc.

|

$ | (27,161 | ) | $ | (42,076 | ) | $ | (36,819 | ) | $ | (23,326 | ) | $ | (1,006 | ) | |||||

|

Per share amounts:

|

||||||||||||||||||||

|

Basic and diluted loss per share attributable to

|

||||||||||||||||||||

|

4Kids Entertainment, Inc. common shareholders

|

||||||||||||||||||||

|

Continuing operations

|

$ | (1.87 | ) | $ | (2.40 | ) | $ | (1.81 | ) | $ | (1.01 | ) | $ | (0.01 | ) | |||||

|

Discontinued operations

|

(0.15 | ) | (0.76 | ) | (0.98 | ) | (0.76 | ) | (0.07 | ) | ||||||||||

|

Basic and diluted loss per share attributable to

|

||||||||||||||||||||

|

4Kids Entertainment, Inc. common shareholders

|

$ | (2.02 | ) | $ | (3.16 | ) | $ | (2.79 | ) | $ | (1.77 | ) | $ | (0.08 | ) | |||||

|

Weighted average common shares

|

||||||||||||||||||||

|

outstanding – basic and diluted

|

13,460,214 | 13,303,192 | 13,181,549 | 13,209,495 | 13,104,051 | |||||||||||||||

|

Net loss attributable to 4Kids Entertainment, Inc.:

|

||||||||||||||||||||

|

Loss from continuing operations

|

$ | (25,151 | ) | $ | (31,877 | ) | $ | (24,182 | ) | $ | (13,352 | ) | $ | (194 | ) | |||||

|

Loss from discontinued operations

|

(6,489 | ) | (20,579 | ) | (12,637 | ) | (9,974 | ) | (812 | ) | ||||||||||

|

Loss attributable to noncontrolling interests

|

4,479 | 10,380 | — | — | — | |||||||||||||||

|

Net loss from discontinued operations

|

(2,010 | ) | (10,199 | ) | (12,637 | ) | (9,974 | ) | (812 | ) | ||||||||||

|

Net loss attributable to 4Kids Entertainment, Inc.

|

$ | (27,161 | ) | $ | (42,076 | ) | $ | (36,819 | ) | $ | (23,326 | ) | $ | (1,006 | ) | |||||

* Included as a reduction of selling, general and administrative expenses for 2006 is income of $722 reclassified from income from discontinued operations of the Summit Media Group to conform to 2010 presentation.

13

|

Year Ended December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Other Operating Data:

|

||||||||||||||||||||

|

Cash flow (used in) provided by:

|

||||||||||||||||||||

|

Operating activities

|

$ | (6,139 | ) | $ | (13,580 | ) | $ | (33,334 | ) | $ | (15,850 | ) | $ | (1,057 | ) | |||||

|

Investing activities

|

6,812 | 3,429 | 24,432 | 22,605 | (18,047 | ) | ||||||||||||||

|

Financing activities

|

(44 | ) | 74 | (2,641 | ) | 2 | 1,445 | |||||||||||||

|

Year Ended December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Total assets

|

$ | 29,070 | $ | 56,653 | $ | 100,574 | $ | 151,079 | $ | 181,395 | ||||||||||

|

Working capital

|

2,052 | 4,859 | 17,579 | 65,135 | 123,906 | |||||||||||||||

|

Stockholders’ equity

|

10,258 | 35,117 | 74,991 | 128,088 | 154,737 | |||||||||||||||

The Company did not declare or pay any cash dividends during the five-year period ended December 31, 2010.

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

The following is a discussion and analysis of our financial position and results of operations for each of the three years in the period ended December 31, 2010. This commentary should be read in conjunction with our consolidated financial statements and the notes to the Company’s consolidated financial statements, which begin on page F-1 under “Item 7. Financial Statements and Supplementary Data”.

Overview

The Company’s operating results for the year ended December 31, 2010 were negatively impacted by the decline in licensing revenue from the “Monster Jam”, “Teenage Mutant Ninja Turtles” and “Yu-Gi-Oh!” Properties. Accordingly, the Company experienced an overall significant decrease in licensing revenues worldwide during 2010 as compared with 2009. The Company also experienced a decrease in television and film revenues during 2010 relating to its broadcast sales both domestically and internationally. These declines are generally the result of the declining popularity of the Company’s existing Properties combined with the failure of new Properties to achieve similar popularity levels. During 2009 and continuing in 2010, the Company implemented significant cost-cutting initiatives, primarily pertaining to personnel related costs and advertising and marketing expenses, in an effort to offset its poor operating results; however, these initiatives failed to offset lower revenues and other charges.

On January 11, 2011, 4Kids announced the retirement of our Chief Executive Officer and Chairman, and the appointment of Director Michael Goldstein as interim Chairman. At the request of our Board of Directors (“Board”), including all members of a special committee formed for purposes of exploring potential strategic alternatives for the Company, Director Wade Massad has agreed to actively investigate and pursue potential strategic alternatives for the Company and oversee certain operational matters on behalf of the Board. In recognition of the additional time and effort that will be expended by Mr. Massad in performing such services, the Board has determined that Mr. Massad will receive an additional $13 for January, $17 for February, $12 for March and $10 for each additional month he is performing such activities.

General

The Company receives revenues from the following three business segments: (i) Licensing; (ii) Advertising, Media and Broadcasting; and (iii) Television and Film Production/Distribution. The Company typically derives a substantial portion of its licensing revenues from a small number of Properties, which usually generate revenues for only a limited period of time. The Company’s revenues are highly subject to changing trends in the toy, game and entertainment businesses, potentially causing dramatic increases and decreases from year to year due to the popularity of particular Properties. It is not possible to accurately predict the length of time a Property will be commercially successful and/or if a Property will be commercially successful at all. Popularity of Properties can vary from months to years. As a result, the Company’s revenues from particular Properties may fluctuate significantly between comparable periods.

14

The Company’s licensing revenues have historically been derived primarily from the licensing of toy and game concepts. As a result, a substantial portion of the Company’s revenues and net income are subject to the seasonal variations of the toy and game industry. Typically, a majority of toy orders are shipped in the third and fourth calendar quarters resulting in increased royalties earned by the Company during such calendar quarters. The Company recognizes revenues from the sale of advertising time on the leased Saturday morning programming block from The CW (“The CW4Kids”), as more fully described in Note 2 of the notes to the Company’s consolidated financial statements. The Company’s advertising sales subsidiary, 4Kids Ad Sales, sells advertising time on The CW4Kids at higher rates in the fourth quarter due to the increased demand for commercial time by children’s advertisers during the holiday season. As a result, much of the revenues of 4Kids Ad Sales are earned in the fourth quarter when the majority of toy and video game advertising occurs. As a result of the foregoing, the Company has historically experienced greater revenues during the second half of the year than during the first half of the year.

Effective September 30, 2010, the Company terminated the operations of TC Digital Games LLC (“TC Digital”), the joint venture which produces, markets and distributes the “Chaotic” trading card game, and TC Websites LLC (“TC Websites”), the joint venture that owns and operates www.chaoticgame.com, the companion website for the “Chaotic” trading card game. The Company owns 55% of each of TC Digital and TC Websites. The closing of these companies will enable the Company to further reduce costs and focus on its core businesses. As a consequence of the termination of their operations, TC Digital and TC Websites ceased supporting the Chaotic trading card game and website, effective October 1, 2010. TC Digital and TC Websites are consolidated in the Company’s consolidated financial statements, subject to a noncontrolling interest.

Critical Accounting Policies

The Company’s accounting policies are fully described in Note 2 of the notes to the Company’s consolidated financial statements. Below is a summary of the critical accounting policies, among others, that management believes involve significant judgments and estimates used in the preparation of its consolidated financial statements.

Accounting for Film and Television Costs - The Company amortizes the costs of production for film and television programming using the individual-film-forecast method under which such costs are amortized for each film or television program in the ratio that revenue earned in the current period for such title bears to management’s estimate of the total revenues to be realized from all media and markets for such title. All exploitation costs, including advertising and marketing costs, are expensed as incurred.

Management regularly reviews, and revises when necessary, its total revenue estimates on a title-by-title basis, which may result in a change in the rate of amortization and/or a write-down of the film or television asset to estimated fair value. The Company determines the estimated fair value for individual film and television Properties based on the estimated future ultimate revenues and costs.