Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DARLING INGREDIENTS INC. | d8k.htm |

America’s leading provider of rendering, recycling

and recovery solutions to the nation’s food industry

…converting waste streams into sustainable feed and

fuel ingredients.”

Exhibit 99.1 |

Forward-Looking Statements

This presentation contains forward-looking statements regarding the business

operations of Darling and the industry in which it operates.

These

statements

are

identified

by

words

such

as

“may,”

“will,”

“expect,”

“believe,”

“intend,”

“anticipate,”

“should,”

“estimate,”

“continue,”

and other words referring to events to occur in the future. These statements

reflect Darling's current view of future events and are based on its

assessment of, and are subject to, a variety of risks and uncertainties beyond its control,

including business and economic conditions in its existing markets that could cause

actual results to differ materially from those projected in the

forward-looking statements. Other risks and uncertainties regarding Darling, its business and the industry in

which it operates are referenced from time to time in the Company's filings with

the Securities and Exchange Commission. Darling is under no obligation to

(and expressly disclaims any such obligation to) update or alter its forward-looking statements

whether as a result of new information, future events or otherwise.

This presentation also contains information about Darling’s adjusted EBITDA,

adjusted net income and adjusted earnings per share, which are not measures

derived in accordance with GAAP and which exclude components that are important to

understanding Darling’s financial performance. Investors should recognize that

these non-GAAP measures might not be comparable to similarly titled

measures of other companies. These measures should be considered in addition to, and not as a

substitute for or superior to, any measure of performance, cash flows or liquidity

prepared in accordance with accounting principles generally accepted in the

United States. 2 |

Founded in 1882 and

headquartered in Dallas, TX Approximately 3,300 employees

Listed on the NYSE (DAR)

LARGEST

renderer with over 130 locations nationwide in 42 states

LARGEST

bakery

waste

recycler

in

the

United

States

LARGEST

waste cooking oil recovery business in the country

LARGEST

grease

trap

maintenance

business

in

the

U.S.

One

of

LARGEST

private

fleets

of

tractors,

trucks

and

trailers

in

U.S.

–

over

5,000

units

Seeking

DOE

approval

to

begin

construction

of

LARGEST

animal fat to hydrocarbon facility in the

world with Valero Energy Corporation as our partner.

Converting

Waste

Inputs

into

“Value-Added”

Ingredients

to

Feed

and

Fuel

3

WE are America’s

Leading Provider of Rendering, Recycling

and Recovery Solutions to the Nation’s Food Industry |

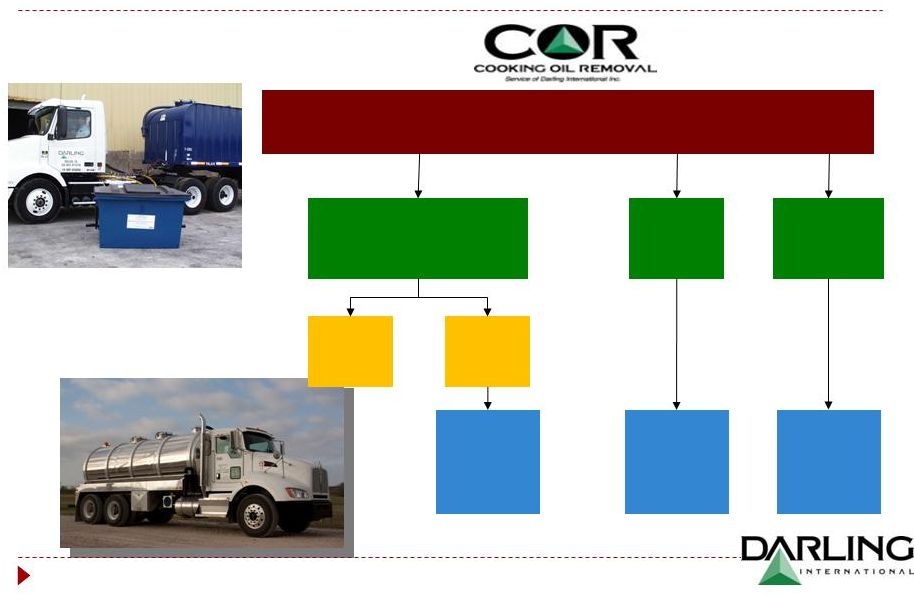

Our

Platform Rendering

Cooking of non-edible meat products (beef, pork,

poultry) into usable ingredients

Collection and processing of spent cooking oil to

produce ingredients for animal feed or bio-fuel

Cooking Oil Removal

Grease trap cleaning and wastewater disposal

Industrial line-jetting

Sell indoor & outdoor grease collection equipment

Environmental Services/Equipment Sales

Collection of dough, ingredients and

sub-standard finished products to produce

high-calorie

ingredients

for

animal feed

Bakery Feed

Key Suppliers

End Products

o

Slaughter houses

o

Grocery stores

o

Food service preparation

o

Animal mortalities

o

Animal fats

o

Meat and bone meal

o

Poultry meals

Key Suppliers

End Products

o

Restaurant chains

o

Grocery stores

o

Food processing facilities

o

Yellow grease

Key Suppliers

End Products

o

Commercial bakeries

o

Snack food companies

o

High-calorie animal

feed

ingredients

Key Customers

o

Restaurants

o

Grocery stores

o

Commercial and industrial

(malls, hospitals)

4 |

Rendering…. Our Core Business

Source: NRA/Harvard Risk Assessment, Supplier Relations U.S.

Raw material volumes expected to

increase

o

Meat production to feed the world

o

Strong exports to China and India

o

Integrated meat processers selectively moving to

outsource rendering activities

o

Consumer expectations of leaner meat products

Finished product prices increasing

o

Global bio-fuel mandates

o

A growing global population

o

Chinese consumption of soybeans and corn

Animal and food by-product recycling industry is

“mission critical”

in the food supply chain

Most efficient and environmentally sound disposal

alternative...reduces greenhouse gas (GHG)

~70 billion pounds of inedible by-products generated

annually

Rendering Industry

Rendering Industry Growth Drivers

5

Rendering –

turing this...

….into this |

What

Does Rendering Do? Average Jacobsen Index Prices (at the

specified delivery point) Kills pathogenic organisms

o

Pathogens that may threaten human and animal health thrive on perishable organic

materials Protects the environment

Recycles nutrients:

o

For use in animal feed and in fertilizer

o

Prevents loading of soil with nitrogen and phosphorus

Recycles carbon:

o

Rendering captures carbon and nitrogen to avoid greenhouse gas emissions

o

Rendering

captures

many

times

more

carbon

than

it

emits

from

its

processes

Recycles energy:

o

Captures the energy in the raw materials and packages it into stable products that

can be stored, transported and used easily

o

All rendered products contain significant amounts of energy

o

Fats, greases and oils are nature’s way of concentrating and storing

energy o

Whether energy is measured in calories or as BTU, it is still energy

Provides control, verification and traceability to regulatory agencies and the

public that condemned or expired meat products are not re-used as human

food The industry does all of this within hours of receiving raw materials,

versus the weeks or months it takes some popular alternative methods

6 |

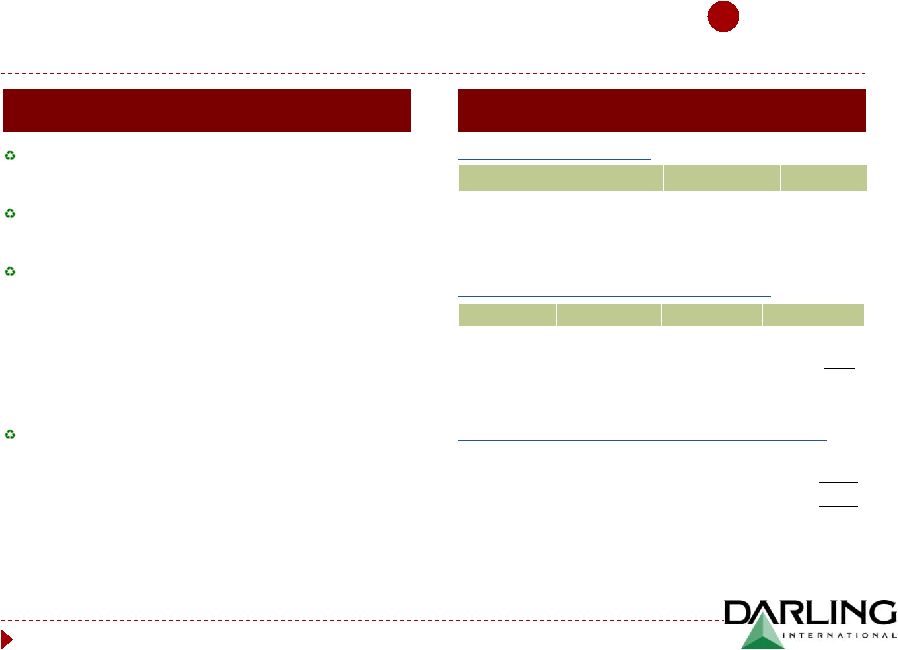

Average Jacobsen Index Prices (at the specified delivery

point) What’s Available to the Rendering Industry to Recycle?

Wastes generated by the meat and food processing industries

Source

Amount

(million pounds)

On-farm and pre-slaughter

3,702.4

Inedible byproducts removed at slaughter

39,047.6

Downstream

Fat, bone and trim from processing

23,850.7

Expired meat from retail stores

3,960.4

Total

70,561.1

7

Source: USDA 2009 data |

Source and Potential Volumes of Animal

Byproducts Available for Rendering

Specie

Weights in million pounds

Farm & pre-slaughter

losses

1

Slaughter

losses

2

Meat processing

losses

3,4

Grocery store

losses

4

Total

Beef

1,932.2

17,115.0

7,083.8

1,350.8

27,481.8

Pork

981.6

7,878.8

4,891.5

1,013.1

14,765.0

Lamb

64.1

214.2

119.2

30.7

428.2

Chickens

598.5

12,398.0

10,649.5

1,289.4

24,935.4

Turkey

126.0

1,441.6

1,106.8

276.3

2,950.7

Totals

3,702.4

39,047.6

23,850.7

3,960.4

70,561.1

Source: USDA 2009, data

1

USDA on-farm mortality and pre-slaughter data.

2

Calculated from USDA data for total live weight at slaughter minus carcass

weights. 3

Calculated from USDA data for meat available at retail subtracted from carcass

weights, adjusted for import and export data. 4

USDA Supermarket losses studies.

8

We estimate 40-50% of tonnage is available to non-integrated rendering

companies |

Rendering: Producing Sustainable Green

Ingredients for Feed and Fuel

Rendering

Animal Fats

Pet

Food

Poultry

Feed

Hog

Feed

Animal

Feed

Pet

Food

Renewable

Fuels

Soap

Fertilizer

Lubricants

Textiles

Plastics

Shampoo

Emulsifiers

Cleaners

Creams

Esters

Paints

Plastics

Lubricants

Inks

Glues

Solvents

Antifreeze

Explosives

Rubber

Plastics

Tires

Lubricants

Finished

Products

Component

By-Products

Component

By-Products

Applications

Linoleic

Acid

Oleic

Acid

Glycerine

Stearic

Acid

Leather

9

Shoes

Garment

Auto Industry

Animal Proteins

Hides |

Restaurant Services: Producing Sustainable

Green Ingredients for Feed and Fuel

Animal

Feed

Rubber

Plastics

Tires

Lubricants

Lubricants

Textiles

Plastics

Cleaners

Chemical

uses

Industrial

uses

Boiler fuel

Biodiesel

Green diesel

Energy

Finished

Products

Renewable

Fuels

Recovery of Used Cooking Oil

10 |

Bakery Waste Recycling

Global Bakery Industry Revenue ($ millions)

Bakery Industry

5-10% of “scrape”

rate and growing

Additional food safety regulations and traceability

should help “scrape”

rates grow

Top tier food processors committed to stringent

sustainability initiatives require reliable company to

pick up and ensure product does not go to landfill or

get into food chain

DAR real estate allows for new growth opportunities

Finished product prices increasing

o

100% tied to corn

o

Priced as ingredient to poultry feed

o

Ethanol and Chinese demand will drive continued corn

price firmness

$351 billion U.S. bakery industry provides billions of

pounds of inedible bakery waste each year

Service wholesale baking, snacks, cookies and

crackers

Distribution centers are growing in importance

Commercial Baking Growth Drivers

Source: IBIS World

11 |

Bakery: Producing Sustainable

Green Ingredients for Feed

Packaging is

burned for fuel

Raw Dough, Baked Goods, Snack Items

Dried and Standardized

Cookie Meal

12 |

Environmental Services

#1 Grease Trap Maintenance and

Cleaning Service

Operates in 35 major markets

Significant synergies with our rendering and grease plants

Approximately 33,000 customers with ample customer bundling opportunities

Municipalities are driving increased regulation and enforcement

Positioned as a “Branded”

player

Used Cooking Oil Storage Tank Systems

Premium service offered in conjunction with COR

Leading equipment provider for used cooking oil collection

Installed inside or outside, this self-contained storage system

offers a clean, efficient and safe storage and collection option

13

(low cost wastewater disposal) |

Grease Trap Maintenance

Wastewater is collected from Food Service Establishments

Solids are filtered

Solid waste is

Land filled

Fuel

Animal

Feed

14

Brown grease is

recovered |

A

Platform of Value and Opportunity Green Diesel

Joint Venture

Positive Industry

Fundamentals

Growth and Margin

Expansion Opportunities

Strong Financial

Performance & Cash

Flow Generation

Attractive Business

Model with Solid

Risk Management

#1 Platform Across

the Food Recycling Spectrum

15

1

6

5

2

3

4 |

Inputs Key Driver –

Animal Production

33 million cattle

(49% of live weight not used for human food)

110 million hogs

(44% not used for human food)

8-9 billion chickens

(37% not used for human food)

245 million turkeys

(36% not used for human food)

o

World population growth

o

U.S. is most efficient animal producer

o

Highest quality product in the world

U.S. Protein Production (million pounds)

U.S. Animal Agriculture Annual

Processing Volume

Producing approximately 68 Billion pounds of raw material

0

10,000

20,000

30,000

40,000

50,000

1970

1977

1984

1991

1998

2005

2012

2019

Poultry

Beef

Pork

1970

–

2009

CAGR:

3.8%

1970–2009 CAGR: 0.5%

1970–2009 CAGR: 1.2%

Source: Equity Research, USDA

16

1

Positive Industry

Fundamentals |

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

OTHER ADVANCED BIOFUEL

0.2

0.3

0.5

0.75

1.0

1.5

2.0

2.5

3.0

3.5

3.5

3.5

4.0

BIOMASS BASED DIESEL

1.15

0.8

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

CELLULOSIC BIOFUEL

0.1

0.25

0.5

1.0

1.75

3.0

4.25

5.5

7.0

8.5

10.5

13.5

16.0

CORN BASED ETHANOL

12.0

12.6

13.2

13.8

14.4

15.0

15.0

15.0

15.0

15.0

15.0

15.0

15.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Inputs Key Driver –

Commodity Momentum

o

Biomass-based Diesel (BMD) cannot be less than 1

billion gallon/year beginning 2012

o

Only Renewable Diesel and Biodiesel can fulfill BMD

requirement

o

BMD can fulfill Other Advanced Biofuel requirement

While the agriculture complex is near historical

highs, it is not supply-constrained but is demand-

driven by global BIOFUEL mandates and strong

Chinese demand

Fuel mandates for ethanol and bio-mass fuels

continue to be implemented here and abroad

Renewable Fuel Standard 2 is our driver in the

United States

Tightening

“Fossil”

crude oil supplies are

constructive

No room in S&D for supply interruption globally for

any crop

Advanced

Biofuels

Source: EPA RFS2

17

1

Positive Industry

Fundamentals |

Corn

Prices: “Firm for the Future” 1

Positive Industry

Fundamentals

World

Bio Fuel

Demand

South America

becomes Primary

World Supplier

U.S. Drought 1995/1996

Prod: 7.374 Billion bushels

Carryout: 426 Million bushels

2008 Commodity

Speculation Run

---------Billions of annual

bushels---------

CORN NON-ETHANOL SURPLUS

SUPPLY

DEMAND NO ETHANOL

99/00

9.4 9.0 0.4

00/01

9.9 9.2 0.7

01/02

9.5 9.1 0.4

02/03

9.0 8.5 0.5

03/04

10.1 9.0 1.1

04/05

11.8 9.3 2.5

05/06

11.1 9.6 1.5

06/07

10.5 9.1 1.4

07/08

12.5 9.0 3.5

08/09

12.0 8.5 3.5

09/10

13.1 8.5 4.6

10/11

12.5 7.7 4.8

Source: DTN Commodity Service

CBOT

Corn

Chart

-

1980 thru Present

18 |

Darling’s National Platform –

A superior Platform to Assist Customers Nationwide

Network of over 130 facilities from coast to coast

Breadth to service national accounts

Footprint that allows Darling to grow organically and acquisitively

Darling International

Griffin Industries

Griffin locations only

Darling and Griffin locations

Darling locations only

2

#1 Platform Across

the Food Recycling

Spectrum

19 |

Diverse Raw Material Suppliers

Diverse mix of beef, pork and poultry raw materials and the largest recycler of

bakery waste and cooking oil

Darling collects raw materials from:

o

Protein processors

o

Grocery stores

o

Butcher shops

o

Food service establishments

o

Bakeries

Processing plants generally within 150 miles of supplier facilities

Spoke and hub transfer station concept supports plant network

Darling’s relationship with its top suppliers averages over 20 years

The collection, processing and pricing of raw materials is key to Darling’s

success 20

2

#1 Platform Across

the Food Recycling

Spectrum |

Strong Rationale for

Griffin Acquisition

Balances Raw Material Sources

Strategic Rationale

Completed missing link in national footprint

Diversification of raw materials supply

Acquired leading bakery recycling business

Collectively formed leading used cooking oil

recovery system

Provides us with additional feedstock for Valero

“Green Diesel”

joint venture

Synergy opportunities and growth platform

Well run, highly profitable and strong

management team

Evaluating 338(H)10 election

Darling 2009

Griffin 2009

Pro Forma 2009

Cooking Oil

12%

Beef/Pork

77%

Poultry

47%

Bakery

31%

Poultry

11%

Beef/Pork

10%

Cooking Oil

12%

Poultry

29%

Beef/Pork

40%

Bakery

21%

Cooking Oil

11%

Source: Company Management

Highly Diversified Business Platform

21

2

#1 Platform Across

the Food Recycling

Spectrum |

Attractive Business Model

“Formula”

basis: fixed margin processing relationship with suppliers

“Non-formula”

basis: suppliers either paid a fixed price, not paid, or charged for the expense

of collection Finished product—

Value Addition

Raw material

procurement

Raw material

volume

Product yield

Natural gas and

diesel

prices

Processing & collecting

expenditures

We create value added ingredients from our inputs

Products are substitutes for corn, soybean oil and soybean meal

Quantity of raw material collected from Rendering, Bakery and Restaurant Services

suppliers Feed stock available to convert into finished goods

Yield on production (production volume / raw material volume) impacted by:

o

Quality of raw material

o

Type of raw material

Exposure to natural gas used for cooking and drying of material

o

Mitigated by ability to burn fats

Exposure to fuel prices through use of diesel fuel for trucks and

tractor-trailers Pricing formulas generally protect against natural gas

and fuel price fluctuations Labor cost

Replacement capex and equipment maintenance

Fuel and utilities

Other operating expenses

Key Metrics

3

Attractive Business

Model with Solid

Risk Management

22 |

Built-In Margin and

Risk Management Tools

Darling Procurement

Darling Formula Pricing Example

Industry has evolved to a shared risk

procurement model

Pricing protocols reduce exposure to commodity

price fluctuation and provide minimum margins

Raw materials procured under two main pricing

arrangements:

o

Formula based Rendering (~70% of total

raw material volume)

o

Used cooking oil (~45% of total raw material volume)

o

Bakery waste is 100% formula tied to corn

Non-formula business generally has a service fee

o

Require supplier to pay Darling for waste removal

service

o

Adjusted to ensure collection costs are covered

Product

Finished price

Total yield

Animal Fats

$30.00cwt

26%

Protein Meals

$15.00cwt

22%

Note: Yield is based on individual supplier’s historical yields and is

adjusted as needed Product

Finished price

Total yield

Value

Animal Fats

$30.00cwt

26%

$7.80

Protein Meals

$15.00cwt

22%

$3.30

Finished product sales value

$11.10

Darling conversion cost with Energy adjuster

($6.00)

Darling fixed margin

($1.50)

Total processing cost

($7.50)

(Charge) / Rebate to supplier per cwt

$3.60

Source: Company Management

Note: When finished product sales value covers Darling’s cost and fixed

spread, a rebate to the supplier is generated. Conversely, when the

finished product sales value is less than Darling’s cost and fixed

spread, the supplier is charged for the difference. Indicative Formula

Terms Theoretical Finished Product Sales Value

Theoretical Darling (Charges)/Rebate to Supplier

23

3

Attractive Business

Model with Solid

Risk Management |

Growth and EBITDA Expansion

Growth and Margin

Expansion

Opportunities

4

Growth and EBITDA Expansion Opportunities

National footprint will provide customer growth opportunities and potential

margin expansion

Value-adding of product streams and new waste inputs

Meaningful synergy opportunity

Bakery business will continue to expand and provide new geographic

opportunities for growth

Continue historical trend of bolt-on acquisitions

Solid history of successful integrations

24 |

Focus on Premium and Value

Added Products

Strategic Focus on Premium and Value-Added Products

Premium Products Pricing Relative to Commodity Meals

Griffin’s Focus on Value-Add and Branding of Ingredients

Opportunity to move more of Darling’s

products into Griffin’s premium/value-added

products

Differentiated and value-added products drive

premium pricing

Value-added products sell for a significant

premium to commodity products

Provides margin expansion for Darling

Commodity Feed

Grade Poultry Meal

Griffin Pet –

Grade

Poultry Meal

Griffin Poultry Meal

(Flash Dried)

Griffin Low Ash

Poultry Meal

Source: Company Management

25

Growth and Margin

Expansion

Opportunities

4

25%

57%

+65%

+75%

+70%

2005

2009 |

Synergy….delivery of value

Routing

improvements

(Florida,

Georgia,

Indiana,

Ohio

and

Texas

in

2011)

o

Closure of transfer stations & some small processing plants

o

Completed Florida integration in February, Georgia and Texas

underway

Scale

and

arbitrage

of

finished

products

to

proper

markets

Realignment

of

our

“Procurement

and

Services”

organizations

National

footprint

will

assist

in

servicing

national

chain

restaurants

Back

office

efficiencies

While limited overlap exists geographically, there is still significant

opportunity to capture synergies over time

26

Growth and Margin

Expansion

Opportunities

4 |

A

proven track record of growth… Dec 2004

Burrows Industries,

Inc. dba Minuteman

Pumping

So CA

July 2007

Ace Grease Service

KC metro

Oct 2005

Southeastern

Maintenance &

Construction Inc.

FL, GA

Dec 2009

Sanimax USA

Great Lakes

May 2006

National By-

Products, LLC

Midwest US

2004

2005

2006

2007

2008

2009

2010

Dec 2008

J&R Rendering, Inc.

NYC metro

Aug 2008

API Recycling, div

of American

Proteins Inc.

GA

Feb 2009

Boca Transport,

Inc.

GA

June 2010

Nebraska By-

Products

NE, KS

27

On December 17, 2010 we acquired Griffin Industries for $840 million.

Growth and Margin

Expansion

Opportunities

4

Since 2003, Darling has acquired and integrated 10 companies investing over $1.1

Billion |

Focus on Growing the Business…

Leader in the bakery waste business

o

Geographic opportunity to build or buy

o

Traceability and no landfill requirement

will drive growth

o

We sell 100% of output to our current

rendering raw material suppliers creating

long-term sustainable linkages

o

Current relationships with large commercial

bakeries, food companies and snack food

processors should create geographic

opportunity for expansion

Take advantage of the existing

Darling footprint

Growing the Bakery Business

Growing Rendering & Grease Collection

Darling is the leader in both rendering

and grease collection

o

Geographic opportunity to build or buy

o

Probably 10-20 meaningful geographic

candidates

Various large-scale acquisition

candidates

o

Succession driven

o

Timing unknown

28

Growth and Margin

Expansion

Opportunities

4 |

A

Potential Game Changer…… Low quality animal fats to

hydrocarbon Green Diesel

Joint Venture

5

Proposed 50/50 JV with Valero subject to DOE Loan

Located adjacent to Valero’s St. Charles Refinery

Creates a new market for Darling’s feed stocks

Represents significant margin opportunity

Creates a natural hedge for Darling’s animal fat

products and improves pricing dynamics

Darling to commit $93 million of equity over the next

three years and the JV received conditional

commitment for a $241 million DOE loan on January

20, 2011

JV 10-year look back of ~$108 million of estimated

average annual EBITDA

Implementing next-generation renewable diesel technology

to open a new market for fats and oils

29 |

What is Diamond Green Diesel?

9,300 Barrel Per Day

US$ million

Total Project Cost

~ $427

Partners Capital

$186

DOE Investment

$241

Animal Fat

1.1 billion lbs

Renewable

Diesel

LPG’s &

Naphtha

136.7 million

gallons

21.7 million

gallons

Annual

Annual

Source: Company Management

Note: Total Project Cost include cost to construct of approximately $360 million,

working capital, and other deal related costs (a portion of which may be

returned at a later date). Joint Venture between Darling International &

Valero Energy Corporation Ownership: 50/50

Management: Valero employees reporting to/directed by Joint Venture

Board Renewable Diesel Plant

Located next to Valero St. Charles

Refinery; Norco, Louisiana

30

Green Diesel

Joint Venture

5 |

Diamond Green Diesel –

What are the Drivers of Profitability?

31

Renewable Fuel

Standard

Fuel Quality

Ability To Process

Low Cost Feedstock

RFS2 requires a MINIMUM of 1 billion gallons of Biomass-based Diesel

be blended annually in U.S. diesel pool

Only

two

products

can

fulfill

Biomass-based

Diesel

mandate

–

they

are

Renewable Diesel (or its co-products) and Biodiesel

Requirement could be more than 1.0 billion gallons annually as

Renewable Diesel also can fulfill the Other Advanced Biofuel Mandate

Renewable Diesel is a true Hydrocarbon (just like diesel fuel) while

Biodiesel is a methyl ester and is not a true hydrocarbon (containing an

oxygen molecule)

As a result Renewable Diesel can be distributed using the current

petroleum

distribution

system,

while

Biodiesel

requires

truck

or

rail

transport (as opposed to pipeline) and additional infrastructure

investment

Renewable

Diesel

has

no

cold

flow

issues

like

Biodiesel

Diamond Green Diesel process allows for use of low quality fats and oils

which traditionally price at substantial discount to feedstock which most

Biodiesel processors must use

Result is feedstock cost advantage of approximately $1.00/gallon

Green Diesel

Joint Venture

5 |

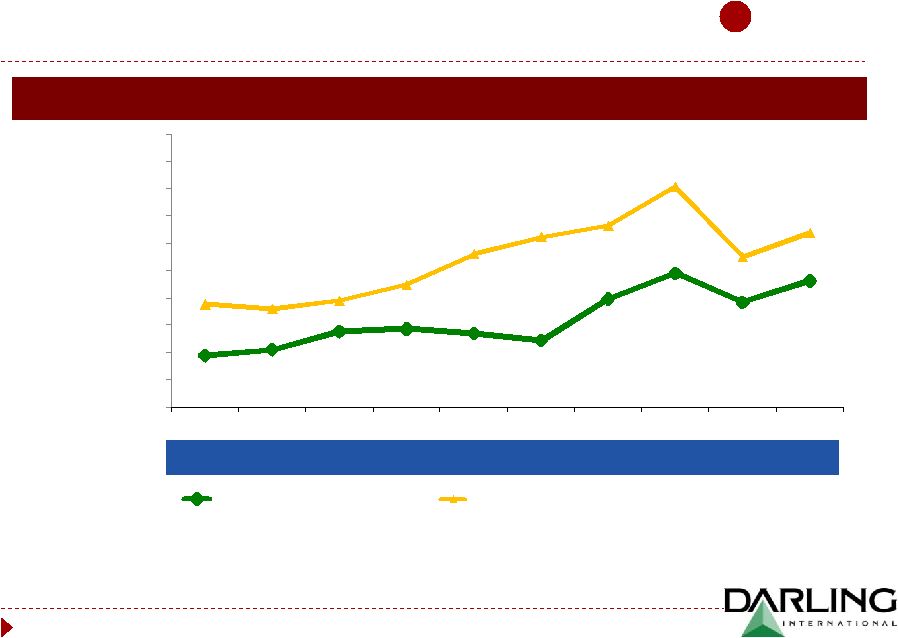

Annual Average Price / Gallon

Why Darling is Investing

$0.95

$1.06

$1.39

$1.44

$1.36

$1.23

$1.99

$2.46

$1.93

$2.32

$1.89

$1.81

$1.96

$2.25

$2.81

$3.12

$3.33

$4.04

$2.76

$3.20

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Diamond Feedstock Cost

Average Diesel Price Plus $1.10 Green Premium

Source: Company Management

Green Premium is a combination of Renewable Identification Numbers, Federal Tax

Credit & wholesale price differential between #2 diesel fuel and Renewable

Diesel 32

Implied

Historical

EBITDA

(US$ million)

$105

$83

$47

$74

$148

$213

$130

$150

$80

$67

Green Diesel

Joint Venture

5 |

The ultimate

built-in hedge!

As corn gets cheaper,

traditionally fat is cheaper and

our earnings are impacted.

Assuming petroleum pricing

remains stable to higher…

Cheaper Corn = Greater Earnings in

the “green diesel”

plant.

33 |

Overview of St. Charles Refinery

Green Diesel Location

34

Green Diesel

Joint Venture

5 |

Historical Financials

Strong Financial

Performance &

Cash Flow

Generation

6

Revenue (US$

millions)

Capex

(US$

millions)

1

EBITDA -

Capex (US$ millions)

EBITDA (US$ millions)

Source: Company Management

1

Griffin capex includes capex and investments, including acquisitions.

35

$1143

$1489 $1123 $1340

$213

$308 $190 $237

$178

$237 $121 $176

$35

$71 $69 $61 |

36

Pro Forma: Balance Sheet

Strong Financial

Performance &

Cash Flow

Generation

6

Balance

Sheet

as

of

January

2011

(US

$

in

millions)

1/01/2011

Equity Adjustments

Pro Forma

Cash and cash equivalents

$19.2

$19.2

Restricted cash

0.4

0.4

Accounts receivables, net

103.7

103.7

Inventories

45.6

45.6

Other current assets

16.7

16.7

Total current assets

$185.6

$185.6

Property, plant and equipment, net

393.4

393.4

Collection route and contracts, net

391.0

391.0

Goodwill

376.3

376.3

Other assets

36.0

36.0

Total assets

$1,382.3

$1,382.3

Current portion of long-term debt

$3.0

$3.0

Accounts payable

70.1

70.1

Accrued expenses

81.7

81.7

Total current liabilities

$154.8

$154.8

Long-term debt

707.0

(292.7)

414.3

Deferred income taxes

5.4

5.4

Other non-current liabilities

50.8

50.8

Total liabilities

$918.0

$625.3

Stockholder's equity

464.3

292.7

757.0

Total liabilities and equity

$1,382.3

$0.0

$1,382.3

Darling

Combined Pro Forma |

The

Original RECYCLING COMPANY….

Sustaining

Innovating

Renewing

Q&A

Q&A |