Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[ X ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: January 29, 2011

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from: __________________________ to __________________________

Commission file number: 000-20969

HIBBETT SPORTS, INC.

(Exact name of registrant as specified in its charter)

|

DELAWARE

(State or other jurisdiction of

incorporation or organization)

|

20-8159608

(I.R.S. Employer

Identification No.)

|

451 Industrial Lane, Birmingham, Alabama 35211

(Address of principal executive offices, including zip code)

205-942-4292

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Common Stock, $0.01 Par Value Per Share

|

NASDAQ Global Select Market

|

|

|

Title of Class

|

Name of each exchange on which registered

|

|

Securities registered pursuant to section 12(g) of the Act:

|

NONE

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

Yes

|

No

|

X

|

||||

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

||||||

|

Yes

|

No

|

X

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

Yes

|

X

|

No

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232-405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

Yes

|

X

|

No

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ____

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

X

|

Accelerated filer

|

||

|

Non-accelerated filer

|

Smaller reporting company

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

|

Yes

|

No

|

X

|

The aggregate market value of the voting stock held by non-affiliates of the Registrant (assuming for purposes of this calculation that all executive officers and directors are “affiliates”) was $754,585,663 on July 31, 2010, based on the closing sale price of $26.47 at July 30, 2010 for the common stock on such date on the NASDAQ Global Select Market.

The number of shares outstanding of the Registrant’s common stock, as of March 18, 2011 was 27,344,943.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Annual Report to Stockholders for the year ended January 29, 2011 are incorporated by reference into Part II and portions of the Registrant’s Proxy Statement for the 2011 Annual Meeting of Stockholders to be held on May 26, 2011 are incorporated by reference into Part III of this Annual Report on Form 10-K. Registrant’s definitive Proxy Statement will be filed with the Securities and Exchange Commission on or before April 25, 2011.

2

HIBBETT SPORTS, INC.

|

Page

|

|||

|

Item

|

1.

|

5

|

|

|

Item

|

1A.

|

9

|

|

|

Item

|

1B.

|

15

|

|

|

Item

|

2.

|

15

|

|

|

Item

|

3.

|

16

|

|

|

Item

|

4.

|

Removed and Reserved.

|

16

|

|

Item

|

5.

|

17

|

|

|

Item

|

6.

|

19

|

|

|

Item

|

7.

|

20

|

|

|

Item

|

7A.

|

29

|

|

|

Item

|

8.

|

30

|

|

|

Item

|

9.

|

50

|

|

|

Item

|

9A.

|

50

|

|

|

Item

|

9B.

|

50

|

|

|

Item

|

10.

|

51

|

|

|

Item

|

11.

|

51

|

|

|

Item

|

12.

|

51

|

|

|

Item

|

13.

|

51

|

|

|

Item

|

14.

|

52

|

|

|

Item

|

15.

|

52

|

|

|

55

|

|||

3

A warning about Forward-Looking Statements

This document contains “forward-looking statements” as that term is used in the Private Securities Litigation Reform Act of 1995. Forward-looking statements address future events, developments and results. They include statements preceded by, followed by or including words such as “believe,” “anticipate,” “expect,” “intend,” “plan,” “target” or “estimate.” For example, our forward-looking statements include statements regarding:

|

|

·

|

our anticipated sales, including comparable store net sales changes, net sales growth and earnings;

|

|

|

·

|

our growth, including our plans to add, expand or relocate stores and square footage growth, our markets’ ability to support such growth and the suitability of our distribution facility;

|

|

|

·

|

the cost of regulatory compliance, including those directed at climate change and its effects and the costs and possible outcomes of pending legal actions and other contingencies;

|

|

|

·

|

our cash needs, including our ability to fund our future capital expenditures and working capital requirements;

|

|

|

·

|

our ability and plans to renew or increase our revolving credit facilities;

|

|

|

·

|

our seasonal sales patterns and assumptions concerning customer buying behavior;

|

|

|

·

|

our expectations regarding competition;

|

|

|

·

|

our ability to renew or replace store leases satisfactorily;

|

|

|

·

|

our estimates and assumptions as they relate to preferable tax and financial accounting methods, accruals, inventory valuations, dividends, carrying amount and liquidity of financial instruments and fair value of options and other stock-based compensation as well as our estimates of economic and useful lives of depreciable assets and leases;

|

|

|

·

|

our expectations concerning future stock-based award types;

|

|

|

·

|

our expectations concerning employee stock option exercise behavior;

|

|

|

·

|

the possible effect of inflation, market decline and other economic changes on our costs and profitability, including the impact of changes in fuel costs and a downturn in the retail industry or changes in levels of store traffic;

|

|

|

·

|

the possible effects of continued volatility and further deterioration of the capital markets, the commercial and consumer credit environment and the continuation of lowered levels of consumer spending resulting from the global economic downturn, lowered levels of consumer confidence and higher levels of unemployment;

|

|

|

·

|

our analyses of trends as related to earnings performance;

|

|

|

·

|

our target market presence and its expected impact on our sales growth;

|

|

|

·

|

our expectations concerning vendor level purchases and related discounts;

|

|

|

·

|

our estimates and assumptions related to income tax liabilities and uncertain tax positions;

|

|

|

·

|

the future reliability of, and cost associated with, our sources of supply, particularly imported goods;

|

|

|

·

|

the possible effect of recent accounting pronouncements;

|

|

|

·

|

the loss of key vendor support; and

|

|

|

·

|

our ability to mitigate the risk of possible business interruptions.

|

You should assume that the information appearing in this report is accurate only as of the date it was issued. Our business, financial condition, results of operations and prospects may have changed since that date.

For a discussion of the risks, uncertainties and assumptions that could affect our future events, developments or results, you should carefully review the “Risk Factors” described beginning on page 9, as well as “Management’s Discussion and Analysis of Financial Condition and Results of Operations” beginning on page 20.

Our forward-looking statements could be wrong in light of these risks, uncertainties and assumptions. The future events, developments or results described in this report could turn out to be materially different. We have no obligation to publicly update or revise our forward-looking statements after the date of this annual report and you should not expect us to do so.

Investors should also be aware that while we do, from time to time, communicate with securities analysts and others, we do not, by policy, selectively disclose to them any material non-public information with any statement or report issued by any analyst regardless of the content of the statement or report. We do not, by policy, confirm forecasts or projections issued by others. Thus, to the extent that reports issued by securities analysts contain any projections, forecasts or opinions, such reports are not our responsibility.

Introductory Note

Unless specifically indicated otherwise, any reference to “2012” or “Fiscal 2012” relates to our year ending January 28, 2012. Any reference to “2011” or “Fiscal 2011” relates to our year ended January 29, 2011. Any reference to “2010” or “Fiscal 2010” relates to our year ended January 30, 2010. Any reference to “2009” or “Fiscal 2009” relates to our year ended January 31, 2009. References to “we”, “our”, “us” and the “Company” used throughout this document refer to Hibbett Sports, Inc. and its subsidiaries as well as its predecessors.

4

Our Company

Our Company was originally organized in 1945 under the name Dixie Supply Company in Florence, Alabama, specializing primarily in the marine and small aircraft business. In 1951, the Company started targeting school athletic programs in North Alabama and by the end of the 1950’s had developed a profitable team sales business. In 1960, we sold the marine portion of our business and have been solely in the sporting goods business since that time. In 1965, we opened Dyess & Hibbett Sporting Goods in Huntsville, Alabama, and hired Mickey Newsome, our current Executive Chairman of the Board. The next year, we opened another sporting goods store in Birmingham and by the end of 1980, we had 12 stores in central and northwest Alabama with a distribution center located in Birmingham and our central accounting office in Florence. We went public in October 1996 when we had 79 stores and were incorporated under the laws of the State of Delaware as Hibbett Sporting Goods, Inc. We incorporated under the laws of the State of Delaware as Hibbett Sports, Inc. in January 2007 and on February 10, 2007, Hibbett Sports, Inc. became the successor holding company for Hibbett Sporting Goods, Inc., which is now our operating subsidiary.

Today, we operate sporting goods stores in small to mid-sized markets predominantly in the Southeast, Southwest, Mid-Atlantic and the Midwest. As of January 29, 2011, we operated 779 Hibbett Sports stores as well as 16 smaller-format Sports Additions athletic shoe stores and 3 larger-format Sports & Co. superstores in 26 states. Our primary retail format and growth vehicle is Hibbett Sports, a 5,000 square foot store located primarily in strip centers which are usually influenced by a Wal-Mart store. Approximately 76% of our Hibbett Sports store base is located in strip centers, which includes free-standing stores, while approximately 24% of our Hibbett Sports store base is located in enclosed malls. We expect to continue our store base growth in strip centers versus enclosed malls.

Our stores offer a broad assortment of quality athletic equipment, footwear and apparel with a high level of customer service. Our merchandise assortment emphasizes team sports complemented by localized apparel and accessories designed to appeal to a wide range of customers within each individual market.

Available Information

The Company maintains an Internet website at the following address: www.hibbett.com.

We make available free of charge on or through our website under the heading “Investor Information,” certain reports that we file with or furnish to the Securities and Exchange Commission (SEC) in accordance with the Securities Exchange Act of 1934 (Exchange Act). These include our annual reports on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K. We make this information available on our website as soon as reasonably practicable after we electronically file the information with or furnish it to the SEC. In addition to accessing copies of our reports online, you may request a copy of our Annual Report on Form 10-K for the fiscal year ended January 29, 2011, at no charge, by writing to: Investor Relations, Hibbett Sports, Inc., 451 Industrial Lane, Birmingham, Alabama 35211.

Reports filed with or furnished to the SEC are also available free of charge upon request by contacting our corporate office at (205) 942-4292.

The public may also read or copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100F Street, N.E., Washington, DC 20549. Information may be obtained on the operation of the Public Reference Room by calling the SEC at 1-800-732-0330. The SEC also maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically at www.sec.gov.

Our Business Strategy

We target markets with county populations that range from 25,000 to 75,000. By targeting these smaller markets, we believe that we achieve important strategic advantages, including store growth opportunities, comparatively low operating costs and a more limited competitive environment than generally faced in larger markets. In addition, we establish greater customer, vendor and landlord recognition as a leading sporting goods retailer in these local communities.

We believe our ability to merchandise to local sporting and community interests differentiates us from our national competitors. This strong regional focus also enables us to achieve significant cost benefits including lower corporate expenses, reduced distribution costs and increased economies of scale from marketing activities. Additionally, we also use sophisticated information systems to maintain tight controls over inventory and operating costs and continually search for ways to improve efficiencies through information system upgrades.

5

We strive to hire enthusiastic sales people with an interest in sports. Our extensive training program focuses on product knowledge and selling skills and is conducted through the use of in-store clinics, DVDs, self-study courses, interactive group discussions and Hibbett University designed specifically for store management.

Our Store Concepts

Hibbett Sports

Our primary retail format is Hibbett Sports, a 5,000 square foot store located primarily in strip centers which are usually influenced by a Wal-Mart store. In considering locations for our Hibbett Sports stores, we take into account the size, demographics, quality of real estate and competitive conditions of each market. Of these stores, 589 Hibbett Sports stores are located in strip centers, which include free-standing stores, with the remaining 190 stores located in enclosed malls, the majority of which are the only enclosed malls in the county.

Hibbett Sports stores offer a core selection of quality, brand name merchandise with an emphasis on team sports. This merchandise mix is complemented by a selection of localized apparel and accessories designed to appeal to a wide range of customers within each market. We strive to respond quickly to major sporting events of local interest. Such events in the last few years included Auburn University’s and The University of Alabama’s historic football seasons and ultimate victories in the Bowl Championship Series (BCS) National Championship games as well as the successful seasons of the Texas Rangers professional baseball team, the New Orleans Saints professional football team and the University of Kentucky college basketball program.

Sports Additions

Our 16 Sports Additions stores are small, enclosed mall-based stores, averaging 2,500 square feet with approximately 90% of merchandise consisting of athletic footwear and the remainder consisting of caps and a limited assortment of apparel. Sports Additions stores offer a broader assortment of athletic footwear, with a greater emphasis on fashion than the athletic footwear assortment offered by our Hibbett Sports stores. All but two Sports Additions stores are currently located in enclosed malls in which Hibbett Sports stores are also present.

Sports & Co.

We operate three Sports & Co. superstores that were opened between March and November 1995. Sports & Co. superstores average 25,000 square feet and offer a broader assortment of athletic footwear, apparel and equipment than our Hibbett Sports stores. Athletic equipment and apparel represent a higher percentage of the overall merchandise mix at Sports & Co. superstores than they do at Hibbett Sports stores. Sports & Co. superstores are designed to project the same in-store atmosphere as our Hibbett Sports stores but on a larger scale. We have no plans to open any superstores in the future.

Team Sales

Hibbett Team Sales, Inc. (Team Sales), a wholly-owned subsidiary of the Company, is a leading supplier of customized athletic apparel, equipment and footwear primarily to school athletic programs in Alabama and parts of Georgia, Florida and Mississippi. Team Sales sells its merchandise directly to educational institutions and youth associations. The operations of Team Sales are independent of the operations of our retail stores. Team Sales does not meet the quantitative or qualitative reporting requirements of the Accounting Standards Codification (ASC) Topic 280, Segment Reporting.

Our Expansion Strategy

In Fiscal 1994, we began to accelerate our rate of new store openings to take advantage of the growth opportunities in our target markets. We have currently identified 350 to 375 potential markets for future Hibbett Sports stores within the states in which we operate. Our clustered expansion program, which calls for opening new stores within a two-hour driving distance of an existing Hibbett location, allows us to take advantage of efficiencies in distribution, marketing and regional management. It also allows us to build on our understanding of merchandise selection for that area. We believe our current distribution center can support over 1,200 stores.

In Fiscal 2012, we expect our net store openings to accelerate somewhat over Fiscal 2011. We have identified potential markets but have experienced difficulty in securing suitable real estate or leases within the targeted market over the last few years. Although new construction store sites continue to be a challenge to find, we have been able to capitalize on prime locations left vacant by franchised and entertainment-related business closings. While we expect new store growth at a faster pace than the last few years, we still anticipate that the current economic environment, particularly in the commercial real estate market, will continue to make it harder to open our stores at our historical rate of growth. Because of the slowdown of new store openings, we have turned our focus somewhat on expanding high performing stores and have seen successful results from this strategy.

6

In evaluating potential markets, we consider population, economic conditions, local competitive dynamics, availability of suitable real estate and proximity to existing Hibbett stores. Our continued growth largely depends on our ability to open new stores in a timely manner, to operate them profitably and to manage them effectively. Additionally, successful expansion is subject to various contingencies, many of which are beyond our control. See “Risk Factors.”

Our Distribution

We maintain a single distribution center in Birmingham, Alabama. The distribution process is centrally managed from our corporate headquarters, which is located in the same building as the distribution center. We believe strong distribution support for our stores is a critical element of our expansion strategy and is central to our ability to maintain a low cost operating structure. In addition, we also use third party logistics providers to gain efficiencies in the cost of distribution to approximately 17% of our outlying stores, which also saves space in our distribution center. We believe our current distribution infrastructure, which includes the use of third party logistics providers, improved technology and vendor assistance with cross-docking, can service over 1,200 stores.

We receive substantially all of our merchandise at our distribution center. For key products, we maintain backstock at the distribution center that is allocated and distributed to stores through an automatic replenishment program based on items that are sold. Merchandise is typically delivered to stores weekly via Company-operated vehicles or third party logistics providers.

Our Merchandising Strategy

Our merchandising strategy is to provide a broad assortment of quality brand name footwear, apparel and athletic equipment at competitive prices in a full service environment. Historically, as well as for Fiscal 2011, our most popular consumer item was athletic footwear, followed by performance and fashion apparel and team sports equipment, ranked according to sales.

We believe that the breadth and depth of our brand name merchandise selection generally exceeds the merchandise selection carried by local independent competitors. Many of these brand name products are highly technical and require considerable sales assistance. We coordinate with our vendors to educate the sales staff at the store level on new products and trends.

Although the core merchandise assortment tends to be similar for each Hibbett Sports store, important local or regional differences frequently exist. Accordingly, our stores regularly offer products that reflect preferences for particular sporting activities in each community and local interests in college and professional sports teams. Our knowledge of these interests, combined with access to leading vendors, enables our stores to react quickly to emerging trends or special events, such as college or professional championships.

Our merchandising staff, operations staff and management analyze current sporting goods trends primarily through the gathering and analyzing of daily sales activity available through point-of-sale terminals located in the stores. Other strategic measures we utilize to recognize trends or changes in our industry include:

|

|

·

|

studying other retailers for best practices in merchandising;

|

|

|

·

|

attending various trade shows, both in our industry and outside as well as reviewing industry trade publications;

|

|

|

·

|

staying active in industry associations such as the National Sporting Goods Association (NSGA);

|

|

|

·

|

visiting competitor store locations;

|

|

|

·

|

monitoring product selection at competing stores;

|

|

|

·

|

maintaining close relationships with vendors and other retailers; and

|

|

|

·

|

communicating with our regional vice presidents, district managers and store managers.

|

The merchandising staff works closely with store personnel to meet the requirements of individual stores for appropriate merchandise in sufficient quantities. Our success depends in part on our ability to anticipate and respond to changing merchandise trends and consumer demand on a store level in a timely manner. See “Risk Factors.”

Our Vendor Relationships

The sporting goods retail business is brand name driven. Accordingly, we maintain positive relationships with a number of well-known sporting goods vendors to satisfy customer demand. We believe that our stores are among the primary retail distribution avenues for brand name vendors that seek to penetrate our target markets. As a result, we are able to attract considerable vendor interest and establish long-term partnerships with vendors. As our vendors expand their product lines and grow in popularity, we expand sales and promotions of these products within our stores. In addition, as we continue to increase our store base and enter new markets, our vendors increase their brand presence within these regions. We also emphasize and work with our vendors to establish favorable pricing and to receive cooperative marketing funds. We believe that we maintain good working relationships with our vendors. For the fiscal year ended January 29, 2011, Nike, our largest vendor, represented 47.8% of our total purchases while our next largest vendor represented 8.3% of our total purchases. For the fiscal year ended January 30, 2010, Nike, our largest vendor, represented 49.9% of our total purchases while our next largest vendor represented 9.0% of our total purchases.

7

The loss of key vendor support could be detrimental to our business, financial condition and results of operations. We believe that we have long-standing and strong relationships with our vendors and that we have adequate sources of brand name merchandise on competitive terms; however, we cannot guarantee that we will be able to acquire such merchandise at competitive prices or on competitive terms in the future. In this regard, certain merchandise that is high profile and in high demand may be allocated by vendors based upon the vendors’ internal criterion, which is beyond our control. See “Risk Factors.”

Our Information Systems

We maintain sophisticated information systems and use technology as an enabler of our business strategies. For example, we have implemented systems targeted at improving financial control, cost management, inventory control, merchandise planning, replenishment and product allocation. In recent years, we have focused on information systems that are designed to be used in all stores, yet are flexible enough to meet the unique needs of each specific store location.

A communications network sends and receives critical business data to and from our stores, providing timely and extensive information on business activity in every location. Our information is processed in a secure environment to protect both the actual data and the physical assets. We attempt to mitigate the risk of possible business interruptions by maintaining a disaster recovery plan, which includes storing critical business information off-site.

We strive to maintain highly qualified and motivated individuals to support our information systems, which includes help desk staff, programmers, system analysts, business analysts, project managers and a security officer. Our systems are monitored 24 hours a day. Our management believes that our current systems and practice of implementing regular updates position us well to support current needs and future growth. We use a strategic information systems planning process that involves senior management and is integrated into our overall business planning and enterprise risk management. Information systems projects are prioritized based upon strategic, financial, regulatory and other business criteria.

Our Advertising and Promotion

We target special advertising opportunities in our markets to increase the effectiveness of our advertising budget. Our advertising and promotional spending is centrally directed. Print advertising, including direct mail catalogs and postcards to customers, serves as the foundation of our promotional program and accounted for the majority of our total advertising costs in Fiscal 2011.

Other advertising means, such as television commercials, outdoor billboards, Hibbett trucks, our MVP customer loyalty program and the Hibbett website, are used to reinforce Hibbett’s name recognition and brand awareness in the community. By allowing us to reach and interact with our customers on a regular basis through e-mail, the MVP program marketing effort is quickly becoming the most efficient, timely and targeted segment of our marketing program.

Our Competition

The business in which we are engaged is highly competitive. Many of the items we offer in our stores are also sold by local sporting goods stores, athletic footwear and other specialty athletic stores, traditional shoe stores and national and regional sporting goods stores. The marketplace for sporting goods is highly fragmented as many different retailers compete for market share by utilizing a variety of store formats and merchandising strategies. However, we believe the competitive environment for sporting goods is different in smaller markets where retail demand may not support larger format stores.

Our stores compete with national chains that focus on athletic footwear, local sporting goods stores, department and discount stores, traditional shoe stores and mass merchandisers. On a limited basis, we have competition from national sporting goods chains in some of our larger markets. Although we face competition from a variety of competitors, including on-line competitors, we believe that our stores are able to compete effectively by being distinguished as sporting goods stores emphasizing team sports and fitness merchandise complemented by a selection of localized apparel and accessories. Our competitors may carry similar product lines and national brands, but we believe the principal competitive factors for all of our stores are service, breadth of merchandise offered, availability of brand names and availability of local merchandise. We believe we compete favorably with respect to these factors in the smaller markets predominantly in the Southeast, Southwest, Mid-Atlantic and Midwest regions of the United States. However, we cannot guarantee that we will be able to continue to compete successfully against existing or future competitors. Expansion into markets served by our competitors, entry of new competitors or expansion of existing competitors into our markets, could be detrimental to our business, financial condition and results of operations. See “Risk Factors.”

Our Trademarks

Our Company, by and through subsidiaries, is the owner or licensee of trademarks that are very important to our business. For the most part, trademarks are valid as long as they are in use and/or their registrations are properly maintained. Registrations of trademarks can generally be renewed indefinitely as long as the trademarks are in use.

8

Following is a list of active trademarks registered and owned by the Company:

|

|

·

|

Hibbett Sports, Registration No. 2717584

|

|

|

·

|

Sports Additions, Registration No. 1767761

|

|

|

·

|

Hibbett, Registration No. 3275037

|

Our Employees

As of January 29, 2011, we employed approximately 2,150 full-time and approximately 3,900 part-time employees, none of whom are represented by a labor union. The number of part-time employees fluctuates depending on seasonal needs. We cannot guarantee that our employees will not, in the future, elect to be represented by a union. We consider our relationship with our employees to be good and have not experienced significant interruptions of operations due to labor disagreements.

Employee Development. We develop our training programs in a continuing effort to service the needs of our customers and employees. These programs are designed to increase employee knowledge and include DVD training in all stores for the latest in technical detail of new products and new operational and service techniques. Because we primarily promote or relocate current employees to serve as managers for new stores, training and assessment of our employees is essential to our sustained growth.

We have implemented programs in our stores and corporate offices to ensure that we hire and promote the most qualified employees in a non-discriminatory way. One of the most significant programs we have is Hibbett University or “Hibbett U” which is an intensive, four-day training session held at our corporate offices and designed specifically for store management.

Seasonality

We experience seasonal fluctuations in our net sales and results of operations. Customer buying patterns around the spring sales period and the holiday season historically result in higher first and fourth quarter net sales. In addition, our quarterly results of operations may fluctuate significantly as a result of a variety of factors, including the timing of new store openings, the amount and timing of net sales contributed by new stores, merchandise mix and demand for apparel and accessories driven by local interest in sporting events.

Item 1A. Risk Factors.

You should carefully consider the following risks, as well as the other information contained in this report, before investing in shares of our common stock. If any of the following risks actually occur, our business could be harmed. In that case, the trading price of our common stock could decline, and you might lose all or part of your investment.

Risks Related to Our Business and Industry.

A further downturn in the economy could adversely affect consumer purchases of discretionary items, which could reduce our net sales.

In general, our sales represent discretionary spending by our customers. The failure of U.S. government programs to bolster the economy, a further slowdown in the U.S. economy or other economic conditions affecting disposable consumer income, such as volatile fuel and energy costs, depressed real estate values, employment levels, inflation, business conditions, consumer debt levels, lack of available credit, interest rates and tax rates may adversely affect our business. A reduction in overall consumer spending which causes customers to shift their spending to products other than those sold by us or to products sold by us that are less profitable could result in lower net sales, decreases in inventory turnover or a reduction in profitability due to lower margins.

A slower pace of new store openings may negatively impact our net sales growth and operating income and we may be unable to achieve our expansion plans for future growth.

The opening of new retail stores has contributed significantly to our growth in net sales. In light of the challenging economic environment that has faced real estate developers over the past three years, we have slowed down the pace of our new store openings compared to our historical rate. We expect that this pressure on the commercial market and developers will continue throughout Fiscal 2012 and that we will be able to increase our overall store base by approximately 5% in Fiscal 2012 compared to 4% in Fiscal 2011 and 3% in Fiscal 2010. A slower pace of new store openings may negatively impact our net sales growth and operating income.

We have grown rapidly, primarily through opening new stores, growing from 67 stores at the beginning of Fiscal 1997 to 798 stores at January 29, 2011. Our continued growth depends, in large part, upon our ability to open new stores in a timely manner and to operate them profitably. Successful expansion is subject to various contingencies, many of which are beyond our control. In order to open and operate new stores successfully, we must secure leases on suitable sites with acceptable terms, build-out and equip the stores with furnishings and appropriate merchandise, hire and train personnel and integrate the stores into our operations.

9

In addition, our expansion strategy may be subject to rising real estate and construction costs, available credit to landlords and developers and landlord bankruptcies that could inhibit our ability to sustain our rate of growth. We may also face new competitive, distribution and merchandising challenges different from those we currently face. We cannot give any assurances that we will be able to continue our expansion plans successfully; that we will be able to achieve results similar to those achieved with prior locations; or that we will be able to continue to manage our growth effectively. Our failure to achieve our expansion plans could materially and adversely affect our business, financial condition and results of operations. Furthermore, our operating margins may be impacted in periods in which incremental expenses are incurred as a result of new store openings.

Our estimates concerning long-lived assets and store closures may accelerate.

Our long-term success depends, in part, on our ability to operate stores in a manner that achieves appropriate returns on capital invested. This is particularly challenging with the volatility of the current economic environment and customer behavior. We will only continue to operate existing stores if they meet required sales or profit levels. In the current macroeconomic environment, the results of our existing stores are impacted not only by a volatile sales environment, but by a number of things that are outside our control, such as the loss of traffic resulting from store closures by significant other retailers in our stores’ immediate vicinity.

The uncertainty of the economy, coupled with the volatility in the capital markets, affects our business and, ultimately, our revenue and profitability. To the extent our estimates for net sales, gross profit and store expenses are not realized, future assessments of recoverability could result in impairment charges. In addition, if we were to close stores, we could be subject to costs and charges that may adversely affect our financial results.

Our stores are concentrated within the Southeast, Southwest, Mid-Atlantic and Midwest regions of the United States, which could subject us to regional risks.

Because our stores are located primarily in a concentrated area of the United States, we are subject to regional risks, such as the regional economy, weather conditions and natural disasters such as floods, droughts, tornadoes and hurricanes, increasing costs of electricity, oil and natural gas, as well as, government regulations specific in the states and localities within which we operate. We sell a significant amount of team sports merchandise which can be adversely affected by significant weather events that postpone the start of or shorten sports seasons or that limit participation of fans and sports enthusiasts.

Professional team lockouts, as well as the poor performance of college and professional sports teams within our core regions of operation, could adversely affect our financial results.

We sell a significant amount of team sports merchandise, the sale of which may be subject to fluctuations based on the success or failure of such teams. Professional team lockouts, as well as poor performance by the college and professional sports teams within our core regions of operation, could cause our financial results to fluctuate accordingly year over year.

The occurrence of severe weather events, catastrophic health events or natural disasters could significantly damage or destroy our retail locations, could prohibit consumers from traveling to our retail locations or could prevent us from resupplying our stores or distribution center, especially during peak shopping seasons.

Unforeseen events, including public health issues and natural disasters such as earthquakes, hurricanes, snow or ice storms, floods and heavy rains, could disrupt our operations or the operations of our suppliers, as well as the behavior of our consumer. We believe that we take reasonable precautions to prepare particularly for weather-related events, however, our precautions may not be adequate to deal with such events in the future. As these events occur in the future, if they should impact areas in which we have our distribution center or a concentration of retail stores, such events could have a material adverse effect on our business, financial condition and results of operations, particularly if they occur during peak shopping seasons.

Unauthorized disclosure of sensitive or confidential information could harm our business and reputation with our consumers.

The protection of Company, customer and employee data is critical to us. We rely on third-party systems, software and monitoring tools to provide security for processing, transmission and storage of confidential customer and employee information such as payment card and personal information. Despite the security measures we and our third-party providers have in place, our data may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming and/or human errors, theft or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or our providers, could damage our reputation, expose us to risk of litigation and liability and harm our business.

10

Our inability to identify, and anticipate changes in consumer demands and preferences and our inability to respond to such consumer demands in a timely manner could reduce our net sales.

Our products appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to rapid change. Our success depends on our ability to identify product trends as well as to anticipate and respond to changing merchandise trends and consumer demand in a timely manner. We cannot assure you that we will be able to continue to offer assortments of products that appeal to our customers or that we will satisfy changing consumer demands in the future. Accordingly, our business, financial condition and results of operations could be materially and adversely affected if:

|

|

·

|

we are unable to identify and respond to emerging trends, including shifts in the popularity of certain products;

|

|

|

·

|

we miscalculate either the market for the merchandise in our stores or our customers’ purchasing habits; or

|

|

|

·

|

consumer demand unexpectedly shifts away from athletic footwear or our more profitable apparel lines.

|

In addition, we may be faced with significant excess inventory of some products and missed opportunities for other products, which could decrease our profitability.

If we lose any of our key vendors or any of our key vendors fail to supply us with merchandise, we may not be able to meet the demand of our customers and our net sales could decline.

We are a reseller of manufacturers’ branded items and are thereby dependent on the availability of key products and brands. Our business is dependent to a significant degree upon close relationships with vendors and our ability to purchase brand name merchandise at competitive prices. As a reseller, we cannot control the supply, design, function or cost of many of the products we offer for sale. In addition, many of our vendors provide us with incentives, such as return privileges, volume purchasing allowances and cooperative advertising. The loss of key vendor support or decline or discontinuation of vendor incentives could have a material adverse effect on our business, financial condition and results of operations. We cannot guarantee that we will be able to acquire such merchandise at competitive prices or on competitive terms in the future. In this regard, certain merchandise that is in high demand may be allocated by vendors based upon the vendors’ internal criterion which is beyond our control.

A disruption in the flow of imported merchandise or an increase in the cost of those goods may significantly decrease our net sales and operating income.

We believe many of our largest vendors source a substantial majority of their products from foreign countries. Imported goods are generally less expensive than domestic goods and indirectly contribute significantly to our favorable profit margins. We may experience a disruption or increase in the cost of imported vendor products at any time for reasons beyond our control. If imported merchandise becomes more expensive or unavailable, the transition to alternative sources by our vendors may not occur in time to meet our demands or the demands of our customers. Products from alternative sources may also be more expensive than those our vendors currently import. Risks associated with reliance on imported goods include:

|

|

·

|

disruptions in the flow of imported goods because of factors such as:

|

|

|

·

|

raw material shortages, work stoppages, strikes and political unrest;

|

|

|

·

|

problems with oceanic shipping, including blockages at U.S. or foreign ports;

|

|

|

·

|

economic crises and international disputes; and

|

|

|

·

|

increases in the cost of purchasing or shipping foreign merchandise resulting from:

|

|

|

·

|

foreign government regulations;

|

|

|

·

|

rising commodity prices;

|

|

|

·

|

changes in currency exchange rates or policies and local economic conditions; and

|

|

|

·

|

trade restrictions, including import duties, import quotas or loss of “most favored nation” status with the United States.

|

In addition, to the extent that any foreign manufacturer from whom our vendors are associated may directly or indirectly utilize labor practices that are not commonly accepted in the United States, we could be affected by any resulting negative publicity. Our net sales and operating income could decline if vendors are unable to promptly replace sources providing equally appealing products at a similar cost.

11

Problems with our information system software could disrupt our operations and negatively impact our financial results and materially adversely affect our business operations.

The efficient operation of our business is dependent on the successful integration and operation of our information systems. In particular, we rely on our information systems to effectively manage our sales, distribution, merchandise planning and replenishment, to process financial information and sales transactions and to optimize our overall inventory levels. We attempt to mitigate the risk of possible business interruptions by maintaining a disaster recovery plan, which includes storing critical business information off-site. Most of our information systems are centrally located at our headquarters, with offsite backup at other locations. Our systems, if not functioning properly, could disrupt our ability to track, record and analyze sales and inventory movement and could cause disruptions of operations, including, among other things, our ability to process and ship inventory, process financial information including credit card transactions, process payrolls or vendor payments or engage in other similar normal business activities. Although we attempt to mitigate the risk of possible business interruptions, any material disruption, malfunction or any other similar problem in or with our information systems could negatively impact our financial results and materially adversely affect our business operations.

Pressure from our competitors may force us to reduce our prices or increase our spending, which would lower our net sales and operating income.

The business in which we are engaged is highly competitive. The marketplace for sporting goods is highly fragmented as many different retailers compete for market share by utilizing a variety of store formats and merchandising strategies. We compete with national chains that focus on athletic footwear, local sporting goods stores, department and discount stores, traditional shoe stores and mass merchandisers and, on a limited basis, national sporting goods stores. Many of our competitors have greater financial resources than we do. In addition, many of our competitors employ price discounting policies that, if intensified, may make it difficult for us to reach our sales goals without reducing our prices. As a result of this competition, we may also need to spend more on advertising and promotion than we anticipate. We cannot guarantee that we will continue to be able to compete successfully against existing or future competitors. Expansion into markets served by our competitors, entry of new competitors or expansion of existing competitors into our markets could be detrimental to our business, financial condition and results of operations.

Our operating results are subject to seasonal and quarterly fluctuations. Furthermore, our quarterly operating results, including comparable store net sales, will fluctuate and may not be a meaningful indicator of future performance.

We have historically experienced and expect to continue to experience seasonal fluctuations in our net sales, operating income and net income. Our net sales, operating income and net income are typically higher in the spring, back-to-school and holiday shopping seasons. An economic downturn during these periods could adversely affect us to a greater extent than if a downturn occurred at other times of the year.

Customer buying patterns around the spring sales period and the holiday season historically result in higher first and fourth quarter net sales. In addition, our quarterly results of operations may fluctuate significantly as a result of a variety of factors, many outside our control, including the timing of new store openings, the amount and timing of net sales contributed by new stores, merchandise mix, demand for apparel and accessories driven by local interest in sporting events, the demise of sports superstars key to certain product promotions or strikes or lockouts involving professional sports teams. Any of these events, particularly in the fourth quarter, could have a material adverse effect on our business, financial condition and operating results for the entire fiscal year.

Comparable store net sales vary from quarter to quarter, and an unanticipated decline in comparable store net sales may cause the price of our common stock to fluctuate significantly.Factors which have historically affected, and will continue to affect our comparable store net sales results, include:

|

|

·

|

shifts in consumer tastes and fashion trends;

|

|

|

·

|

calendar shifts of holiday or seasonal periods;

|

|

|

·

|

the timing of income tax refunds to customers;

|

|

|

·

|

calendar shifts or cancellations of tax-free holidays in certain states;

|

|

|

·

|

the success or failure of college and professional sports teams within our core regions;

|

|

|

·

|

changes in the other tenants in the shopping centers in which we are located;

|

|

|

·

|

pricing, promotions or other actions taken by us or our existing or possible new competitors; and

|

|

|

·

|

unseasonable weather conditions or natural disasters.

|

We cannot assure you that comparable store net sales will trend at the rates achieved in prior periods or that rates will not decline.

New stores may also affect our net sales through the timing of new store openings and the relative proportion of new stores to mature stores, the level of pre-opening expenses associated with new stores and the amount and timing of net sales contributed by new stores.

12

We would be materially and adversely affected if our single distribution center were shut down.

We currently operate a single centralized distribution center in Birmingham, Alabama. We receive and ship substantially all of our merchandise at our distribution center. Any natural disaster or other serious disruption to this facility due to fire, tornado or any other cause would damage a portion of our inventory and could impair our ability to adequately stock our stores and process returns of products to vendors and could adversely affect our sales and profitability. In addition, we could incur significantly higher costs and longer lead times associated with distributing our products to our stores during the time it takes for us to reopen or replace the center.

We depend on key personnel, the loss of which may adversely affect our ability to run our business effectively and our results of operations.

We have benefited from the leadership and performance of our senior management, especially Michael J. Newsome, our Executive Chairman and former Chief Executive Officer. If we lose the services of any of our principal executive officers or Mr. Newsome, we may not be able to run our business effectively and operating results could suffer. In particular, Mr. Newsome has been instrumental in directing our business strategy and maintaining long-term relationships with our key vendors.

In March 2005, we entered into a Retention Agreement (the Agreement) with Mr. Newsome. The purpose of the Agreement is to secure the continued employment of Mr. Newsome as an advisor to us following his future retirement from the duties of Chief Executive Officer of our Company. Although, Mr. Newsome stepped down as Chief Executive Officer in March 2010, he is actively involved in the daily operations of our Company and his retirement is not currently planned.

Provisions in our charter documents and Delaware law might deter acquisition bids for us.

Certain provisions of our certificate of incorporation and bylaws may be deemed to have anti-takeover effects and may discourage, delay or prevent a takeover attempt that a stockholder might consider in its best interest. These provisions, among other things:

|

|

·

|

classify our Board of Directors into three classes, each of which serves for different three-year periods;

|

|

|

·

|

provide that a director may be removed by stockholders only for cause by a vote of the holders of not less than two-thirds of our shares entitled to vote;

|

|

|

·

|

provide that all vacancies on our Board of Directors, including any vacancies resulting from an increase in the number of directors, may be filled by a majority of the remaining directors, even if the number is less than a quorum;

|

|

|

·

|

provide that special meetings of the common stockholders may only be called by the Board of Directors, the Chairman of the Board of Directors or upon the demand of the holders of a majority of the total voting power of all outstanding securities of the Company entitled to vote at any such special meeting; and

|

|

|

·

|

call for a vote of the holders of not less than two-thirds of the shares entitled to vote in order to amend the foregoing provisions and certain other provisions of our certificate of incorporation and bylaws.

|

In addition, our Board of Directors, without further action of the stockholders, is permitted to issue and fix the terms of preferred stock which may have rights senior to those of common stock. We are also subject to the Delaware business combination statute, which may render a change in control of us more difficult. Section 203 of the Delaware General Corporation Laws would be expected to have an anti-takeover effect with respect to transactions not approved in advance by the Board of Directors, including discouraging takeover attempts that might result in a premium over the market price for the shares of common stock held by stockholders.

Increases in transportation costs due to rising fuel costs, climate change regulation and other factors may negatively impact our results of operations.

We rely upon various means of transportation, including ship and truck, to deliver products from vendors to our distribution center and from our distribution center to our stores. Consequently, our results can vary depending upon the price of fuel. The price of oil has fluctuated drastically over the last few years, and has recently increased again, which has increased our fuel costs. In addition, efforts to combat climate change through reduction of greenhouse gases may result in higher fuel costs through taxation or other means. Any such future increases in fuel costs would increase our transportation costs for delivery of product to our distribution center and distribution to our stores, as well as our vendors’ transportation costs, which could adversely affect our results of operations.

In addition, labor shortages in the transportation industry could negatively affect transportation costs and our ability to supply our stores in a timely manner. In particular, our business is highly dependent on the trucking industry to deliver products to our distribution center and our stores. Our operating results may be adversely affected if we or our vendors are unable to secure adequate trucking resources at competitive prices to fulfill our delivery schedules to our distribution center or our stores.

13

Our costs may change as a result of currency exchange rate fluctuations.

We source goods from various countries, including China, and thus changes in the value of the U.S. dollar compared to other currencies may affect the costs of goods that we purchase.

We manage cash and cash equivalents beyond federally insured limits per financial institution and purchase investments not fully guaranteed by the Federal Deposit Insurance Corporation (FDIC), subjecting us to investment and credit availability risks.

We manage cash and cash equivalents in various institutions at levels beyond federally insured limits per institution, and we purchase investments not guaranteed by the FDIC. Accordingly, there is a risk that we will not recover the full principal of our investments or that their liquidity may be diminished. In an attempt to mitigate this risk, our investment policy emphasizes preservation of principal and liquidity. With the current financial environment and the instability of financial institutions, we cannot be assured that we will not experience losses on our deposits.

We face risk that financial institutions may fail to fulfill commitments under our committed credit facilities.

We have financial institutions that are committed to providing loans under our revolving credit facilities. With the current financial environment and the instability of financial institutions, there is a risk that these institutions cannot deliver against these obligations in a timely matter, or at all. If the financial institutions that provide these credit facilities were to default on their obligation to fund the commitments, these facilities would not be available to us, which could adversely affect our liquidity and financial condition. For discussion of our credit facilities, see “Liquidity and Capital Resources” in Item 7 and Note 5 to our consolidated financial statements.

Risks Related to Ownership of Our Common Stock.

The market price of our common stock, like the stock market in general, is likely to be highly volatile. Factors that could cause fluctuation in our common stock price may include, among other things:

|

|

·

|

actual or anticipated variations in quarterly operating results;

|

|

|

·

|

changes in financial estimates by investment analysts and our inability to meet or exceed those estimates;

|

|

|

·

|

additions or departures of key personnel;

|

|

|

·

|

market rumors or announcements by us or by our competitors of significant acquisitions, divestitures or joint ventures, strategic partnerships, large capital commitments or other strategic initiatives; and

|

|

|

·

|

sales of our common stock by key personnel or large institutional holders.

|

Many of these factors are beyond our control and may cause the market price of our common stock to decline, regardless of our operating performance.

Risks Related to Regulatory, Legislative and Legal Matters.

We operate in a number of jurisdictions. It can be cumbersome to fill needed positions and comply with labor laws and regulations, many of which vary from jurisdiction to jurisdiction.

We are heavily dependent upon our labor force. We attempt to attract and retain an appropriate level of personnel in both field operations and corporate functions. Our compensation packages are designed to provide benefits commensurate with our level of expected service. However, within our retail operations, we face the challenge of filling many positions at wage scales that are appropriate to the industry and competitive factors. We operate in a number of jurisdictions which can make it cumbersome to comply with labor laws and regulations, many of which vary from jurisdiction to jurisdiction. As a result of these and other factors, we face many external risks and internal factors in meeting our labor needs, including competition for qualified personnel, overall unemployment levels, prevailing wage rates, as well as rising employee benefit costs, including insurance costs and compensation programs. We also engage third parties in some of our process such as delivery and transaction processing and these providers may face similar issues. Changes in any of these factors, including a shortage of available workforce in areas in which we operate, could interfere with our ability to adequately service our customers or to open suitable locations and could result in increasing labor costs.

We cannot be assured that we will not experience pressure from labor unions or become the target of labor union campaigns.

While we believe we maintain good relations with our employees, we cannot be assured that we will not experience pressure from labor unions or become the target of labor union campaigns. The potential for unionization could increase in the United States if Congress passes federal legislation that would facilitate labor organization. The unionization of a significant portion of our workforce could increase our overall costs at the affected locations and adversely affect our flexibility to run our business in the most efficient manner to remain competitive or acquire new business. In addition, significant union representation would require us to negotiate wages, salaries, benefits and other terms with many of our employees collectively and could adversely affect our results of operations by increasing our labor costs or otherwise restricting our ability to maximize the efficiency of our operations.

14

Changes in federal, state or local law, or our failure to comply with such laws, could increase our expenses and expose us to legal risks.

While businesses are subject to regulatory matters relating to the conduct of their business, including consumer protection laws, consumer credit privacy acts, product safety regulations, advertising regulations, zoning and land use regulations, sales and use tax laws, wage and hour regulations, workplace safety regulations, environmental laws (including measures related to climate change, greenhouse gas emissions, soil and groundwater contamination and disposal of waste and hazardous materials) and the like, certain jurisdictions have taken a particularly aggressive stance with respect to such matters and have stepped up enforcement, including fines and other sanctions. An increasing regulatory environment could expose us to a challenging enforcement environment or to third party liability (such as monetary recoveries and recoveries of attorneys fees) and could have a material adverse affect on our business and results of operations, including the added cost of increased preventative measures that we may determine to be necessary to conduct our business in certain locales.

We believe that we are in substantial compliance with applicable environment and other laws and regulations and, although no assurance can be given, we do not foresee the need for any significant expenditures in this area in the near future.

Changes in rules related to accounting for income taxes, changes in tax laws in any of the jurisdictions in which we operate or adverse outcomes from audits by taxing authorities could result in an unfavorable change in our effective tax rate.

We operate our business in several jurisdictions. As a result, our effective tax rate is derived from a combination of the federal rate and applicable tax rates in the various states in which we operate. Our effective tax rate may be lower or higher than our tax rates have been in the past due to numerous factors, including the sources of our income and the tax filing positions we take. We base our estimate of an effective tax rate at any given point in time upon a calculated mix of the tax rates applicable to our Company and to estimates of the amount of business likely to be done in any given jurisdiction. Changes in rules related to accounting for income taxes, changes in tax laws in any of the jurisdictions in which we operate or adverse outcomes from tax audits that we may be subject to in any of the jurisdictions in which we operate could result in an unfavorable change in our effective tax rate.

Litigation may adversely affect our business, financial condition and results of operations.

Our business is subject to the risk of litigation by employees, consumers, suppliers, competitors, stockholders, government agencies or others through private actions, class actions, administrative proceedings, regulatory actions or other litigation. The outcome of litigation, particularly class action lawsuits and regulatory actions, is difficult to assess or quantify. We may incur losses relating to these claims and, in addition, these proceedings could cause us to incur costs and may require us to devote resources to defend against these claims which could adversely affect our results of operations. For a description of current legal proceedings, see “Part I, Item 3, Legal Proceedings.”

None.

Item 2. Properties.

We currently lease all of our existing 798 store locations and expect that our policy of leasing rather than owning will continue as we continue to expand. Our leases typically provide for terms of five to ten years with options on our part to extend. Most leases also contain a kick-out clause if projected sales levels are not met and an early termination/remedy option if co-tenancy and exclusivity provisions are violated. We believe this leasing strategy enhances our flexibility to pursue various expansion opportunities resulting from changing market conditions and to periodically re-evaluate store locations. Our ability to open new stores is contingent upon locating satisfactory sites, negotiating acceptable leases, recruiting and training qualified management personnel and the availability of market relevant inventory.

As current leases expire, we believe we will either be able to obtain lease renewals for present store locations or to obtain leases for equivalent or better locations in the same general area. Historically, we have not experienced any significant difficulty in either renewing leases for existing locations or securing leases for suitable locations for new stores. However, we experienced difficulty in securing leases for new stores related to new construction in Fiscal 2011 and Fiscal 2010 due to the economic issues facing the commercial real estate market and landlords, thus reducing our ability to open stores at our historical rates. Based primarily on our belief that we maintain good relations with our landlords, that most of our leases are at approximate market rents and that generally we have been able to secure leases for suitable locations, we believe our lease strategy will not be detrimental to our business, financial condition or results of operations. Although we do expect continued difficulty in securing leases for new stores throughout Fiscal 2012, we believe we will be able to somewhat accelerate our new store growth compared to the last few years by negotiating acceptable leases for suitable locations left vacant by recent closings of franchised and entertainment-related businesses.

15

Our corporate offices and our retail distribution center are leased under an operating lease. We own the Team Sales’ facility located in Birmingham, Alabama that warehouses inventory for educational institutions and youth associations. We believe our current distribution center is suitable and adequate to support our needs in the next few years.

Store Locations

As of January 29, 2011, we currently operate 798 stores in 26 contiguous states. Of these stores, 208 are located in enclosed malls and 590 are located in strip-shopping centers which are typically influenced by a Wal-Mart store. Strip-shopping centers include free-standing stores. The following shows the number of locations by state as of January 29, 2011:

|

Alabama

|

82

|

Kansas

|

19

|

Oklahoma

|

37

|

||

|

Arizona

|

6

|

Kentucky

|

40

|

South Carolina

|

31

|

||

|

Arkansas

|

41

|

Louisiana

|

44

|

South Dakota

|

1

|

||

|

Colorado

|

3

|

Missouri

|

25

|

Tennessee

|

56

|

||

|

Florida

|

37

|

Mississippi

|

56

|

Texas

|

80

|

||

|

Georgia

|

87

|

Nebraska

|

5

|

Virginia

|

19

|

||

|

Iowa

|

6

|

New Mexico

|

10

|

West Virginia

|

9

|

||

|

Illinois

|

18

|

North Carolina

|

46

|

Wisconsin

|

2

|

||

|

Indiana

|

19

|

Ohio

|

19

|

TOTAL

|

798

|

As of March 18, 2011, we operated 798 stores in 26 states.

We are a party to various legal proceedings incidental to our business. We do not believe that any of these matters will, individually or in the aggregate, have a material adverse effect on our business or financial condition. We cannot give assurance, however, that one or more of these lawsuits will not have a material adverse effect on our results of operations for the period in which they are resolved. At January 29, 2011, we estimate that the liability related to these matters is approximately $0.4 million and accordingly, have accrued $0.4 million as a current liability in our consolidated balance sheet. As of January 30, 2010, we had accrued $0.3 million as it related to our estimated liability for legal proceedings.

The estimates of our liability for pending and unasserted potential claims do not include litigation costs. It is our policy to accrue legal fees when it is probable that we will have to defend against known claims or allegations and we can reasonably estimate the amount of the anticipated expense.

From time to time, we enter into certain types of agreements that require us to indemnify parties against third party claims under certain circumstances. Generally, these agreements relate to: (a) agreements with vendors and suppliers under which we may provide customary indemnification to our vendors and suppliers in respect to actions they take at our request or otherwise on our behalf; (b) agreements to indemnify vendors against trademark and copyright infringement claims concerning merchandise manufactured specifically for or on behalf of the Company; (c) real estate leases, under which we may agree to indemnify the lessors from claims arising from our use of the property; and (d) agreements with our directors, officers and employees, under which we may agree to indemnify such persons for liabilities arising out of their relationship with us. We have director and officer liability insurance, which, subject to the policy’s conditions, provides coverage for indemnification amounts payable by us with respect to our directors and officers up to specified limits and subject to certain deductibles.

If we believe that a loss is both probable and estimable for a particular matter, the loss is accrued in accordance with the requirements of ASC Topic 450, Contingencies. With respect to any matter, we could change our belief as to whether a loss is probable or estimable, or its estimate of loss, at any time.

Item 4. Removed and Reserved.

16

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the NASDAQ Global Select Market (NASDAQ/GS) under the symbol HIBB. The following table sets forth, for the periods indicated, the high and low sales prices of shares of our Common Stock as reported by NASDAQ.

|

High

|

Low

|

|||||||

|

Fiscal 2011:

|

||||||||

|

First Quarter ended May 1, 2010

|

$ | 28.54 | $ | 20.77 | ||||

|

Second Quarter ended July 31, 2010

|

$ | 28.58 | $ | 23.12 | ||||

|

Third Quarter ended October 30, 2010

|

$ | 28.13 | $ | 22.09 | ||||

|

Fourth Quarter ended January 29, 2011

|

$ | 39.84 | $ | 25.96 | ||||

|

Fiscal 2010:

|

||||||||

|

First Quarter ended May 2, 2009

|

$ | 22.39 | $ | 12.82 | ||||

|

Second Quarter ended August 1, 2009

|

$ | 21.62 | $ | 16.08 | ||||

|

Third Quarter ended October 31, 2009

|

$ | 21.17 | $ | 16.00 | ||||

|

Fourth Quarter ended January 30, 2010

|

$ | 23.61 | $ | 18.24 | ||||

On March 18, 2011, the last reported sale price for our common stock as quoted by NASDAQ was $30.78 per share. As of March 18, 2011, we had 20 stockholders of record.

17

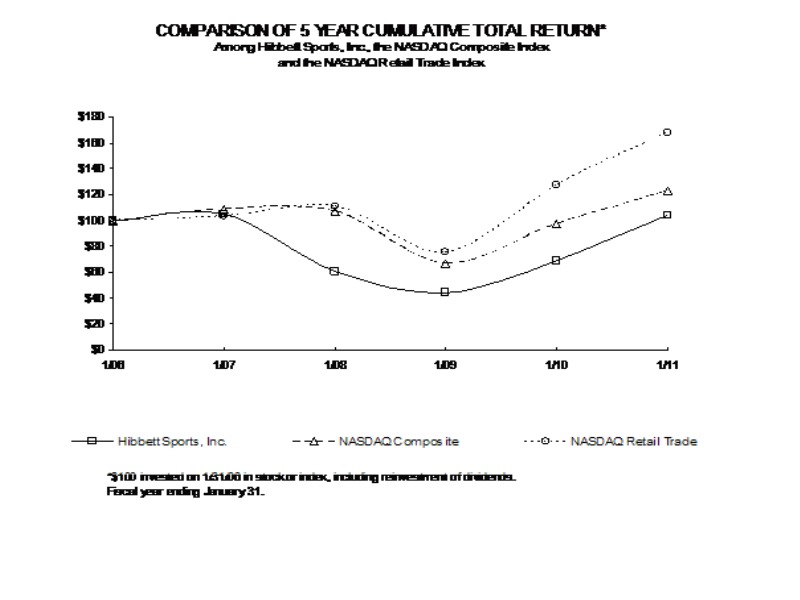

The Stock Price Performance Graph below compares the percentage change in our cumulative total stockholder return on our common stock against a cumulative total return of the NASDAQ Composite Index and the NASDAQ Retail Trade Index. The graph below outlines returns for the period beginning on January 31, 2006 to January 31, 2011. We have not paid any dividends. Total stockholder return for prior periods is not necessarily an indication of future performance.

Dividend Policy. We have never declared or paid any dividends on our common stock. We currently intend to retain our future earnings to finance the growth and development of our business and for our stock repurchase program, and therefore do not anticipate declaring or paying cash dividends on our common stock for the foreseeable future. Any future decision to declare or pay dividends will be at the discretion of our Board of Directors and will be dependent upon our financial condition, results of operations, capital requirements and such other factors as our Board of Directors deems relevant.

Equity Compensation Plans. For information on securities authorized for issuance under our equity compensation plans, see “Part III, Item 12, Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Issuer Repurchases of Equity Securities

The following table presents our shares repurchase activity for the thirteen weeks and quarter ending January 29, 2011 (1):

|

Period

|

Total Number of Shares Purchased

|

Average Price per Share

|

Total Number of Shares Purchased as Part of Publicly Announced Programs

|

Approximate Dollar Value of Shares that may yet be Purchased Under the Programs (in thousands)

|

||||||||||||

|

October 31, 2010 to November 27, 2010

|