Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Pinnacle Foods Finance LLC | d8k.htm |

Pinnacle

Foods Barclays Capital 2011 High Yield Bond

and Syndicated Loan Conference

March 24, 2011

Exhibit

99.1 |

| 2

Forward-Looking Statements and GAAP Reconciliation

Forward-looking statements should not be read as a guarantee of future performance or

results, and will not necessarily be accurate indications of the times at, or by which,

such performance or results will be achieved or whether such performance or results will

ever be achieved. Forward-looking information is based on information available at

the time and management’s good faith belief with respect to future events, and is

subject to risks and uncertainties that could cause actual performance or results to differ

materially from those expressed in the statements.

Forward-looking statements speak only as of the date the statements are made.

Pinnacle Foods Finance LLC (“Pinnacle Foods,” “Pinnacle”

or the “Company”) assumes no obligation to update forward-looking statements to

reflect actual results, changes in assumptions or changes in other factors affecting

forward-looking information except to the extent required by applicable securities

laws. If the Company does update one or more forward-looking statements, no

inference should be drawn that the Company will make additional updates with respect

thereto or with respect to other forward-looking statements. SEC

rules

regulate

the

use

of

“non-GAAP

financial

measures”

in

public

disclosures,

such

as

free

cash

flow,

“EBITDA”

“Adjusted

EBITDA”

and “Consolidated EBITDA”, that are derived on the basis of methodologies other

than in accordance with generally accepted accounting principles, or

“GAAP.” These rules govern the manner in which non-GAAP financial

measures may be publicly presented and prohibit in all filings with the SEC, among

other things: •

exclusion of charges or liabilities that require, or will require, cash settlement or would

have required cash settlement, absent an ability to settle in another manner, from a

non-GAAP financial measure; and •

adjustment of a non-GAAP financial measure to eliminate or smooth items identified as

non-recurring, infrequent or unusual, when the nature of the charge or gain is such

that it has occurred in the past two years or is reasonably likely to recur within the

next two years.

We have included non-GAAP financial measures in this presentation, including free cash

flow, EBITDA, Adjusted EBITDA and Consolidated EBITDA, that may not comply with the SEC

rules governing the presentation of non-GAAP financial measures. In addition,

the Company’s measurements of Consolidated EBITDA are based on definitions of EBITDA included in certain of the

Company’s debt agreements and, as a result, may not be comparable to those of other

companies. Also, free cash flow may not be comparable to similarly titled amounts

presented by other companies. |

3

The Marketplace was Challenging in 2010…

“In short, revenue growth is being compressed for food

manufacturers because a protracted lack of growth for

their retailer partners is creating a more adversarial,

discount oriented dynamic.”

UBS -

June 3, 2010

“Current industry volume growth is so bleak already that

it’s hard for us to see the possibility of a significant further

deterioration.”

Barclays Capital -

October 21, 2010

“We see risk that food company’s margins retrace recent

gains given the sluggish topline growth and heightened

competitive backdrop.”

Goldman Sachs -

October 17, 2010 |

4

In a Tough Environment, Pinnacle Delivered Solid

Results in 2010

* Product Contribution = Gross Margin less consumer marketing and brokerage

**After adjusting actual results for adjustments per Senior Credit Facility and Bond

Indentures |

5

Key Performance Drivers

•

Brand strength

•

Pinnacle brands hold #1 or #2 market position in 8 of 12 major category segments in which

they compete

•

Limited private label penetration

•

Enhanced innovation capabilities driving improved pipeline

•

New agency partners |

Category

Segments Major Brands

Market Position

IRI Market

Share

Frozen Vegetables

#1

26.7

Shelf-Stable Pickles, Peppers and Relish

#1

18.7

Baking Mixes and Frostings

#2

17.1

Frozen Complete Bagged Meals

#2

17.4

Table Syrups

#2

18.5

Frozen Prepared Seafood

#2

19.2

Frozen Waffles, Pancakes and French Toast

#2

15.1

Frozen Breakfast Entrées / Savory

Handhelds

#2

7.9

Canned Meat

#3

10.5

Bagels

#3

7.4

Single-Serve Frozen Dinners and Entrées

#4

8.8

Frozen Pizza-for-One

#4

10.1

Source: IRI -

52 week end Dec. 26, 2010 -

Total US Food

Iconic, Leading Brand Equities

Pinnacle holds the #1 or #2 market position in 8 of the 12 major

category segments

Categories with above average private label penetration

6 |

Enhanced

Innovation Capabilities Driving Improved Pipeline New Consumers

Health & Wellness

Premium / Experience

New Segment

7 |

8

Improved Marketing/Alignment with New Agency Partners

Agency

Key Clients

BBDO (Creative Advertising)

Starbucks, GE, Fed Ex, Mars, Diageo, Gillette

TBWA (Creative Advertising)

Apple, Absolute, Adidas, Visa, McDonalds, P+G

Zenith Optimedia (Media Buying)

HP, Lexus, Nestle, Verizon, Darden, P+G

8 |

| Key Performance

Drivers •

Brand strength

•

Pinnacle brands hold #1 or #2 market position in 8 of 12 major category segments in which

they compete

•

Limited private label penetration

•

Enhanced innovation capabilities driving improved pipeline

•

New agency partners

•

Portfolio diversification

•

Participation in a broad set of categories

•

Scale where needed –

5

largest frozen food company

th

9 |

10

Snacks

4% 4%

Private Label 7%

4%

5%

5%

20%

Canada

3% Other 5% 5%

6%

9%

10%

Other

5% Foodservice 7% Participation in a Broad Set of Categories

___________________________

LTM as of 12/26/10.

Duncan Hines Grocery Division

Birds Eye Frozen Division

Specialty Foods Division |

11

$5,342

16.8

$1,712

5.4

$1,508

4.7

$1,450

4.6

$1,288

4.0

$1,231

3.9

$913

2.9

$801

2.5

$618

1.9

$553

1.7

$ Share

Source: IRI -

52 week end Dec. 26, 2010 -

Total US Food

Pinnacle Ranks Fifth in Frozen

$ Sales ($MM) |

| 12

Key Performance Drivers

•

Brand strength

•

Pinnacle brands hold #1 or #2 market position in 8 of 12 major category segments in which they

compete •

Limited private label penetration

•

Enhanced innovation capabilities driving improved pipeline

•

New agency partners

•

Portfolio diversification

•

Participation in a broad set of categories

•

Scale

where

needed

–

5

largest

frozen

food

company

•

Nimble, responsive organization

•

Experienced senior team

•

Management alignment to value creation

•

Speed

–

Birds

Eye

integration

th |

|

14

Birds Eye integration has been well executed

Supply Chain integrated by 6/30/10 -

“one order/one invoice”

Supply Chain integrated by 6/30/10 -

“one order/one invoice”

Full business integration by 9/30/2010

Full business integration by 9/30/2010

Hired/on-boarded 130 open positions

Hired/on-boarded 130 open positions

Upgraded management capabilities

Upgraded management capabilities

Achieved $25MM of synergies in 2010

Achieved $25MM of synergies in 2010

Actions in place to deliver an additional $25MM of synergies in 2011

Actions in place to deliver an additional $25MM of synergies in 2011

|

15

Key Performance Drivers

•

Brand strength

•

Pinnacle brands hold #1 or #2 market position in 8 of 12 major category segments in which they

compete •

Limited private label penetration

•

Enhanced innovation capabilities driving improved pipeline

•

New agency partners

•

Portfolio diversification

•

Participation in a broad set of categories

•

Scale

where

needed

–

5

largest

frozen

food

company

•

Nimble, responsive organization

•

Experienced senior team

•

Management alignment to value creation

•

Speed

–

Birds

Eye

integration

•

Dependable financial model

•

Solid 2010 financial results

•

Refinanced debt; extending maturity and lowering debt service cost

•

Accelerating productivity / pricing actions

th |

Financial Performance |

17

2010 Year in Review

•

Strong

results

with

Adjusted

EBITDA

up

+14%

y-o-y

to

$447

million

(1)

•

Generated $202 million of free cash flow in FY 2010

•

Gross Margin +240 bps from favorable product mix, Birds Eye acquisition synergies,

productivity initiatives and favorable commodity prices as a result of good 2009 crop

season

(2)

.

•

Net

Leverage

has

declined

from

6.0x

at

the

time

of

the

Birds

Eye

transaction

to

5.7x

as

of

December 2010

•

Net Sales decline of -4.7% in 2010 was driven by the Company’s continued efforts to

deemphasize Private Label and Foodservice offerings, its announced discontinuation of

Birds Eye's Steamfresh Meals and Swanson Classics in the U.S., and a tough trading

environment •

North American Retail sales (ex. Exited Businesses) declined 1.2% 2010 vs. 2009

•

Refinanced debt…extending maturity and lowering debt service cost

•

Leverage neutral transaction with reduction in overall cost of capital

•

Replaced Term Loan C with $442MM Term Loan D and $400MM 8.25% Senior Notes

•

Term Loan D applicable margin 150bps lower than Term Loan C

•

Enhanced current debt maturity profile (New Senior Notes due September 2017)

___________________________

1.

Before variable product contribution from exited businesses of $2.8mm and estimated synergies

yet to be realized associated with the Birds Eye Acquisition of $25mm.

2.

After adjusting actual results for adjustments per Senior Credit Facility and Bond

Indentures |

18

2010 Financial Summary

___________________________

1.

Pro forma for Birds Eye acquisition.

Actual

Actual

($s in millions)

2009

(1)

2010

$

%

Net Sales

2,548

$

2,437

$

(111)

$

-4.4%

North American Retail (ex. exited businesses)

2,036

2,012

(24)

-1.2%

COPS

1,935

1,835

100

5.2%

% Net Sales

75.9%

75.3%

Gross Profit

613

602

(11)

-1.8%

% Net Sales

24.1%

24.7%

Advertising and Consumer

84

59

25

29.8%

% Net Sales

3.3%

2.4%

SG&A and other

273

278

(5)

-1.8%

% Net Sales

10.7%

11.4%

EBIT

256

265

9

3.5%

% Net Sales

10.0%

10.9%

Depreciation & Amortization

83

78

(5)

-6.0%

Reported EBITDA

339

343

4

1.2%

% Net Sales

13.3%

14.1%

Adjusted EBITDA

391

$

447

$

56

14.3%

% Net Sales

15.3%

18.3%

Variance to Prior Year |

19

2010 Consolidated EBITDA Reconciliation

___________________________

1.

Pro forma for Birds Eye acquisition.

Actual

Actual

($s in millions)

2009

(1)

2010

Reported EBITDA

339

$

343

$

Adjustments per Senior Credit Facility and Bond Indentures

Non-cash items

8

72

Non-recurring items

40

27

Other adjustment items

4

5

Subtotal - Adjusted EBITDA

391

447

Variable product contribution from exited businesses

24

3

Net cost savings to be realized as a result of initiatives taken

12

Estimated synergies associated with the Birds Eye acquisition

45

25

Consolidated EBITDA (per Senior Credit Facility and Bond Indentures)

472

$

475

$ |

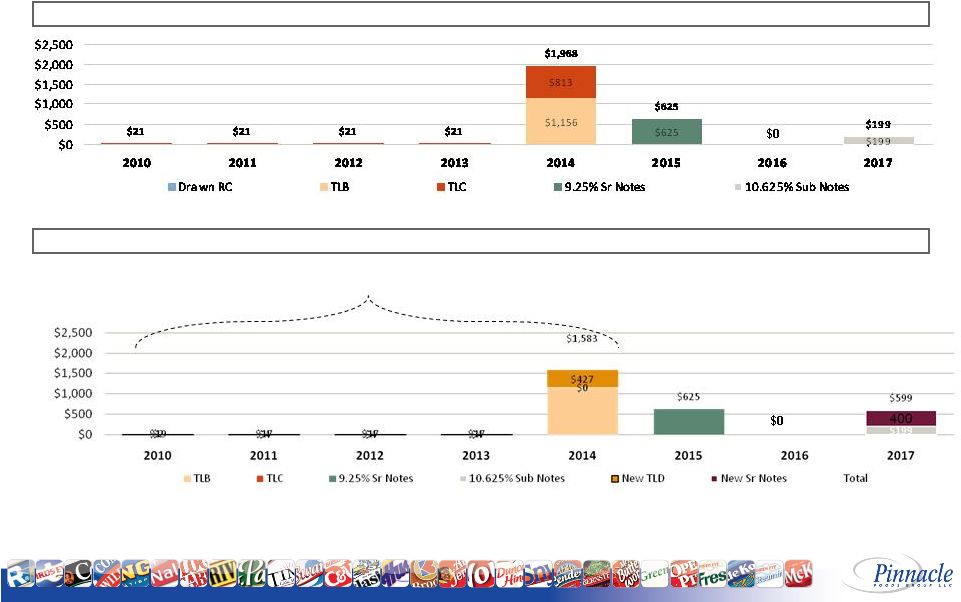

20

Refinanced Debt; Extending Maturity and Lowering

Debt Service Costs

Debt Maturities Post Refinancing

Debt Maturities Pre Refinancing

~$400mm

Reduction

___________________________

Note: Excludes maturity of Revolving Credit Facility which was undrawn as of

December 26, 2010. |

21

December 2010 Debt Structure

($s in millions)

December 2010

Revolving Credit Facility

$ ----

Term Loan B

1,199.4

Term Loan D

368.2

9.25% Senior Notes

625.0

8.25% Senior Notes

400.0

10.625% Senior Subordinated Notes

199.0

Other Debt

15.8

Total Debt

2,807.4

Cash

(115.3)

Total Net Debt

2,692.1

Total Leverage Ratio (per Senior Credit Facility and

Bond Indentures)

5.7 |

22

Accelerating Productivity Initiatives

Targeting

the

high

end

of

our

range

of

3.5%

-

-

4.0%

of

cost

of

products

sold

Productivity

and

pricing

actions

offsetting

inflation

Full

line

of

sight

on

2011

input

costs

Structured,

multi-functional

team

and

process

in

place

Multi-year

capital

investment

to

accelerate

productivity

including

2011

footprint

consolidation

___________________________

1.

Excluding Birds Eye

Procurement

Procurement

Procurement

Manufacturing

Manufacturing

Manufacturing

Logistics

Logistics

Logistics

2009 (1)

2010

2011 Target |

23

Announced Pricing Partially Offsetting Inflation

Category

Effective Date

Baking Mixes / Frosting

1/03/11

Syrups

3/07/11

Canned Fruit

3/07/11

Waffles

3/28/11

Bagels

3/28/11

Vegetables

5/2/11

Seafood

5/2/11

Hungry-Man

(classic fried chicken)

5/2/11 |

Food for

Thought: Solid 2010 Financial Results in

a Challenging Environment

Successful Integration of

Birds Eye Acquisition

Re-energized Innovation

Pipeline

Accelerating Productivity

Refinanced Debt; Extending

Maturity and Lowering Debt

Service Costs |

25

Key Investment Highlights

Successful History

of Brand

Renovation and

Product

Innovation

Proven

Management

Team

Continued

Solid Financial

Performance

Delivering

$50mm in

Synergies

Proven Brand

Equities

Birds Eye

Integration

Successfully

Completed

High Recurring

Cash Flow |