Attached files

| file | filename |

|---|---|

| EX-32.1 - GLOBAL PARI-MUTUEL SERVICES, INC. | ex321to10k08141_12312010.htm |

| EX-31.2 - GLOBAL PARI-MUTUEL SERVICES, INC. | ex312to10k08141_12312010.htm |

| EX-32.2 - GLOBAL PARI-MUTUEL SERVICES, INC. | ex322to10k08141_12312010.htm |

| EX-31.1 - GLOBAL PARI-MUTUEL SERVICES, INC. | ex311to10k08141_12312010.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _______ to _______.

Commission File No. 000-32509

|

Nevada

|

88-0396452

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

500 Fifth Avenue, Suite 810

New York, New York

|

10110

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code (917) 338-7301

|

Securities registered under Section 12(b) of the Exchange Act:

|

||

|

Title of each class registered:

|

Name of each exchange on which registered:

|

|

|

None

|

Not applicable

|

|

|

Securities registered under Section 12(g) of the Exchange Act:

|

||

|

Common Stock, par value $0.001

|

||

|

(Title of Class)

|

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes o No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

o

|

Accelerated filer

|

o

|

|

|

Non-accelerated filer

(Do not check if a smaller reporting company)

|

o

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2010 was approximately $2,372,580, based on the closing price of the stock on that date.

As of March 17, 2011, there were 222,769,316 shares of the registrant’s common stock, par value $0.001 per share, outstanding.

Documents Incorporated by Reference: None

TABLE OF CONTENTS

|

Page

|

||

|

1

|

||

|

18

|

||

|

25

|

||

|

26

|

||

|

26

|

||

|

26

|

||

|

|

||

|

27

|

||

|

30

|

||

|

31

|

||

| Item 7A. | 37 | |

|

37

|

||

|

37

|

||

|

37

|

||

|

38

|

||

|

39

|

||

|

42

|

||

|

46

|

||

|

49

|

||

|

52

|

||

|

53

|

||

PART I

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. You should assume that the information contained in this document is accurate as of the date of this Annual Report on Form 10-K only.

As used in this Annual Report on Form 10-K, unless the context otherwise requires the terms “we,” “us,” “our,” and “Global” refer to Global Pari-Mutuel Services, Inc., a Nevada corporation.

FORWARD LOOKING STATEMENTS

The statements contained in this document that are not purely historical are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Although we believe that the expectations reflected in such forward-looking statements, including those regarding future operations, are reasonable, we can give no assurance that such expectations will prove to be correct. Forward-looking statements are not guarantees of future performance and they involve various risks and uncertainties. Forward-looking statements contained in this document include statements regarding our proposed services, market opportunities and acceptance, expectations for revenues, cash flows and financial performance, and intentions for the future. Such forward-looking statements are included under Item 1. “Business” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” All forward-looking statements included in this document are made as of the date hereof, based on information available to us as of such date, and we assume no obligation to update any forward-looking statement. It is important to note that such statements may not prove to be accurate and that our actual results and future events could differ materially from those anticipated in such statements. Among the factors that could cause actual results to differ materially from our expectations are those described under Item 1. “Business,” Item 1A. “Risk Factors” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this section and other factors included elsewhere in document.

Item 1. Business

Going Concern

Our independent registered public accounting firm has issued a “going concern” opinion raising substantial doubt about our financial viability. The accompanying consolidated financial statements for the years ended December 31, 2010 and 2009 have been prepared on a basis that contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. We have continuing net losses and negative cash flows from operating activities. In addition, as of March 17, 2011, we have a commitment to pay Bendigo Partners, LLC (“Bendigo Partners”) an additional $2,000,000 for consulting services through November 30, 2011. These conditions raise substantial doubt about our ability to continue as a going concern. Our consolidated financial statements do not include any adjustments to the amounts and classification of assets and liabilities that may be necessary should we be unable to continue as a going concern. These circumstances caused our independent registered public accounting firm to include an explanatory paragraph in its report dated February 18, 2011, except for Note 12 as to which the date is March 16, 2011, regarding their concerns about our ability to continue as a going concern. Substantial doubt about our ability to continue as a going concern may create negative reactions to the price of the common shares of our stock, and we may have a more difficult time obtaining financing.

Overview

We were organized as a Nevada corporation on January 27, 1997. We changed our corporate name to “Global Pari-Mutuel Services, Inc.” on August 30, 2005. Our offices are located at 500 Fifth Avenue, Suite 810, New York, New York 10110, and our telephone number is (917) 338-7301.

Beginning in 2000, we began developing online pari-mutuel wagering technology that facilitates pari-mutuel wagering over the internet for live horse and dog racing. During 2005, our management initiated plans to focus our principal business activities on pari-mutuel activities. It is our intent to become a leading, global provider for online pari-mutuel wagering on thoroughbred, harness and greyhound racing.

Pari-mutuel wagering is a system of cooperative betting in which the holders of winning tickets divide the total amount of money bet on a race, after subtracting taxes, racetrack fees and other expenses. The uniqueness of pari-mutuel wagering is that the public itself determines the payoff odds (e.g., if many people have bet on the actual winner of a contest, then the payoff will be relatively low because many winners will divide the pool).

We are currently pursuing the following business model:

|

|

1.

|

Simulcast Facilities and Off-Track Betting (“OTB”) Parlors:

|

|

|

·

|

To accept and process pari-mutuel wagers placed at simulcast facilities and OTB parlors;

|

|

|

·

|

To provide race content to simulcast facilities and OTB parlors;

|

|

|

2.

|

International Call Center: To accept and process customers’ pari-mutuel wagers on races that are placed over the telephone through our international call-center facility;

|

|

|

3.

|

Settlement and Reconciliation: To provide settlement and reconciliation services to pari-mutuel wagerers, including:

|

|

|

·

|

Keeping track of, billing, collecting and forwarding money due from the tracks to the wagerers; and

|

|

|

·

|

Keeping track of, billing, collecting and forwarding money due from the wagerers to the tracks;

|

|

|

4.

|

Equipment and Software: To resell and rent equipment and software for wagering terminals to physical and virtual OTBs necessary for communication with the tracks;

|

|

|

5.

|

Global Pari-Mutuel Instant Racing Project (“IRP”): To operate, through our hub in Antigua, an online pari-mutuel based instant racing and wagering system;

|

|

|

6.

|

Global Pari-Mutuel Network: To launch an online internet model that allows international players to place wages on U.S. and international tracks through our www.rtcsportofkings.com website and the www.trackplayer.com website (the “Global Pari-Mutuel Network”); and

|

|

|

7.

|

Business Development: To develop a new product that will allow users to compete, using a system of pari-mutuel wagering, on the relative price movements of various financial instruments.

|

We presently rely on the revenues that we earn under two principal contracts pursuant to which we provide pari-mutuel wagering services through our hub operations in Antigua. Revenues earned under these two contracts accounted for approximately 83% and 44% of our total revenues during the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, respectively. Revenues earned under our contract with Promotora Latinamericana de Entretenimiento, S.A. de C.V. (“PLE”) accounted for approximately 76% and 39% of our total revenues during the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, respectively, and revenues earned under our contract with ISI Maritime/Islands, Ltd. accounted for approximately 7% and 5% of our total revenues during the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, respectively.

We are currently pursuing opportunities in the U.S., Mexico, Central and South America and the Caribbean, where we intend to introduce the Global Pari-Mutuel Network. We have signed contracts with approximately 40 horse and dog race tracks, which will provide us with content and race simulcasts. If we are successful in negotiating pari-mutuel license agreements with our customers and if these relationships become commercially viable, we believe the primary advantage of the Global Pari-Mutuel Network will be that it will allow customers of online international off-track betting parlors to have real-time odds and racing forms, access to the direct pari-mutuel pools at host tracks, scratches, daily results lines, daily race programs, past performance programs data, and other handicapping data and information concerning available pools through online operations, call-centers or physical OTBs. During the fiscal year ended December 31, 2010, we did not have any contracts to provide settlement and reconciliation services and we did not enter into any new contracts with OTBs for the resale or rental of equipment and software. The Global Pari-Mutuel Network was launched during the last quarter of 2010 and to date has generated limited revenues.

Our principal cost of sales are (i) net commissions paid to OTBs through which wagers are placed, which were approximately 63% and 59% of total revenues during the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, respectively and (ii) simulcast fees paid to tracks, which were approximately 16% and 18% of our total revenues during the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, respectively.

In order to facilitate the implementation of our pari-mutuel wagering business model, we have taken the following measures over the past five years:

|

|

·

|

In April 2006, we acquired all of the outstanding shares of Royal Turf Club, Inc., a Nevada corporation (“RTCN”), and its subsidiary, Royal Turf Club Limited, an Antigua corporation (“RTCA”), in exchange for 6,000,000 shares of our common stock. RTCN provides software and software services for online pari-mutuel wagering on horses and greyhounds. In addition, RTCN provides content, video-streaming and direct access to the wagering pools at the race tracks through its website, www.rtcsportofkings.com as of the fourth quarter of 2010. We acquired RTCN to concentrate our business efforts on pari-mutuel wagering. Prior to 2006, our principal source of income was from credit card processing and only a small portion of our income was derived from pari-mutuel wagering.

|

|

|

·

|

In December 2006, we entered into a cost and profit share agreement with Global Financial Solutions Holdings, Ltd, a newly-formed corporation organized under the laws and regulation of the Turks and Caicos Islands (“GFS”), due to our need to obtain additional financing in order to pursue our online pari-mutuel wagering model and the principal of GFS’s familiarity with operating a company in Antigua. GFS is not affiliated with us and was organized to enter into the cost and profit share agreement with us and had no prior business operations.

|

|

|

·

|

In October 2007, we acquired Royal Turf Club Limited, a St. Kitts and Nevis corporation (“RTCK”), in exchange for 1,000,000 shares of our common stock; and

|

|

|

·

|

In September 2009, we entered into an agreement with Racetech International under which we obtained a license for an online pari-mutuel based instant racing and wagering system as more fully described below.

|

On December 7, 2010, we entered into an equity contribution agreement (the “Contribution Agreement”) with BERMASE LLC (“BERMASE”), and its members, AVON ROAD BERMASE I LLC (“AVON I”), AVON ROAD BERMASE II LLC (“AVON II”), and JAF-NH, LLC (“JAF-NH”). BERMASE is a Delaware limited liability company whose purpose is to further develop online pari-mutuel wagering technology.

Under the Contribution Agreement, in exchange for all of the membership interests of BERMASE, we agreed to issue AVON I, AVON II and JAF-NH 195,437,962 shares of common stock. In connection with the Contribution Agreement, BERMASE also converted its Senior Secured Convertible Promissory Note due September 2011 in the principal amount of $400,000 issued by us to BERMASE and the related accrued interest of $9,567 into 2,047,836 shares of common stock and distributed those shares, as well as 1,200,000 shares of common stock then held by it, to AVON I, AVON II and JAF-NH.

In connection with the execution of the Contribution Agreement, we issued BERMASE an Unsecured Promissory Note, due January 2011, in the principal amount of $500,000, in respect of a $500,000 unsecured loan from BERMASE to us made simultaneously with the execution of the Contribution Agreement. The Contribution Agreement was subject to customary conditions to closing, including that BERMASE’s bank accounts have balances of at least $2,000,000 in cash at the time of closing.

As a result of the Contribution Agreement, a change of control may be deemed to have occurred since Mr. Berman now beneficially owns 65.89% of our outstanding common stock.

On December 7, 2010, we also entered into a one-year consulting agreement (the “Consulting Agreement”) with Bendigo Partners, pursuant to which Bendigo Partners agreed to provide us with the services of R. Jarrett Lilien to serve as our chief executive officer, J. Leslie Whiteford to serve as our chief financial officer, Richard D. Taylor to serve as our chief operating officer, Stephen Ferrando to serve as our chief information officer, and individuals to serve as our chief marketing officer and internal general counsel, for a $250,000 monthly fee. In addition, pursuant to the Consulting Agreement, we granted Bendigo Partners an option to purchase 56,799,828 shares of our common stock, which option first vests and becomes exercisable over a period of two years. The Consulting Agreement contemplates that upon expiration of its one-year term, Messrs. Lilien, Whiteford, Taylor and Ferrando will enter into employment agreements with us. As a result of the Consulting Agreement, James A. Egide resigned from his position as our chief executive officer, but retained his position as a member of our board of directors, Michael D. Bard resigned from his position as our chief financial officer and a member of our board of directors, and each of Joseph Neglia, Keith Cannon and Michael Michigami resigned as members of our board of directors. Messrs. Lilien and Taylor and Jeffrey P. Camp have been appointed to fill three of the four vacancies on our board of directors created by such resignations and Mr. Lilien will recommend candidates to fill the remaining vacancy.

With our new management team in place and the acquisition of BERMASE as our wholly-owned subsidiary, we intend to continue to pursue the development of new proprietary technology to expand our pari-mutuel trading hub to the financial services industry through the development and commercialization of our new product. See “Business Development” below for more information. To that end, we are currently in the process of developing a new business model and products that will allow users to place bets, using a system of pari-mutuel wagering, on the relative price movements of various financial instruments.

In connection with the development of our new product, on February 9, 2011, our newly-formed, wholly-owned subsidiary, Global Pari-Mutuel Services (Guernsey) Limited (“Global Guernsey”), entered into a three-year agreement with AmTote International Inc. (“AmTote”), pursuant to which AmTote agreed to provide Global Guernsey with a license to use its AmTote pari-mutuel totalisator Spectrum® software and certain maintenance services related thereto. AmTote agreed, subject to certain requirements and exceptions, not to provide or license the software (or permit third parties to do so) to any third parties that are direct competitors to Global Guernsey’s business. Global Guernsey agreed to pay AmTote a license fee to be calculated on an annual basis for each twelve-month period commencing on the earlier to occur of the date on which Global Guernsey’s business platform goes “live” and August 9, 2011, which fee will be based upon the total amount of wagers processed using the software, with a minimum monthly fee of $12,000.

In addition, on March 1, 2011, we entered into a non-binding letter of intent with respect to the proposed sale (the “Proposed Sale”) by us of RTCN and RTCK to a group led by James A. Egide, our founder, former chief executive officer and a current director (the “Acquiror”). Under the terms of the Proposed Sale, the equity holders of the Acquiror would exchange an aggregate of 9,007,613 shares of our common stock held by them for (i) 100% of the outstanding capital stock of RTCN and RTCK and (ii) $1,000,000 in cash, $200,000 of which would be payable upon the closing of the Proposed Sale and $800,000 of which would be payable in four equal installments on the first business day of each of the first four calendar months following the month in which the closing of the Proposed Sale occurs. We will require additional financing in order to consummate the Proposed Sale. There can be no assurance that the Proposed Sale will be consummated on the foregoing terms or at all.

We are also planning to change our state of incorporation from Nevada to Delaware and to move from a calendar year-end based fiscal year, to a fiscal year ending September 30, beginning in 2011.

On March 8, 2011, Global Guernsey entered into a master services agreement with Mechanica, LLC (“Mechanica”), pursuant to which Global Guernsey engaged and appointed Mechanica to develop, produce and execute certain advertising and marketing materials and programs (the “Services Agreement”).

The specific services to be provided to Global Guernsey by Mechanica under the Services Agreement are to be set forth in one or more statements of work, which will describe (i) the specific services and deliverables to be provided, (ii) the country or countries for which the services will be performed, (iii) the required staffing by Mechanica, (iv) the schedule for performance, (v) the compensation to be paid by Global Guernsey to Mechanica, (vi) the expenses to be incurred, (vii) matters relating to the use of third party subcontractors, and (viii) other relevant terms. The initial statement of work provides that Global Guernsey will pay Mechanica fees in the amount of $1,191,674, payable as follows (i) $1,072,507 in cash payable in monthly installments until January 1, 2012, and (ii) $119,167 in the form of a nonqualified stock option to purchase 238,333 shares of our common stock, par value $0.001 per share.

The Services Agreement will continue in effect until January 31, 2012, unless earlier terminated in accordance with its terms, and contains customary non-competition, “work for hire” and confidentiality provisions to which Mechanica is subject. Under the Services Agreement, Global Guernsey has the right to terminate the Services Agreement without cause upon 60 days’ prior written notice, or, immediately, if a certain key person to Mechanica, is no longer employed by Mechanica or is not participating in an ongoing relationship us under the Services Agreement.

On March 8, 2011, as contemplated by the Services Agreement, we entered into a stock option agreement with Mechanica, under which we issued the option to purchase 238,333 shares of our common stock to Mechanica. The option has an exercise price of $2.00 per share, expires on January 31, 2016 and vests as to one-fourth of the shares underlying the option on each of April 30, 2011, July 31, 2011, October 30, 2011 and January 31, 2012.

Research and Development

During the fiscal year ended December 31, 2010 and the fiscal year ended December 31, 2009, we spent approximately $157,000 and $241,000, respectively, on research and development activities. The research and development costs were incurred primarily for the development of software for the Global Pari-Mutuel Network to be used in RTCA’s hub operations in Antigua, including the costs of engaging a full-time consultant to develop the software. Research and development of the Global Pari-Mutuel Network began during the fourth quarter of 2008 and was completed and launched during the fourth quarter of 2010.

Organizational Structure

Our current organizational structure is as follows:

Global Financial Solutions Holdings

Effective as of December 31, 2006, RTCN and RTCA entered into an agreement with GFS, pursuant to which: (a) RTCA issued to GFS 50% of RTCA’s outstanding common stock (the “RTCA Shares”); (b) GFS agreed to make certain payments for the purpose of developing, constructing, implementing and operating a central system horse and dog racing hub (the “Hub Operation”); (c) RTCN agreed to manage the business of RTCA; and (d) RTCN and GFS, as the sole shareholders of RTCA, agreed to enter into certain agreements regarding the Hub Operation and their ownership of RTCA. GFS was organized to enter into the cost and profit share agreement with us and has no prior business operations.

In consideration of the RTCA Shares, GFS provided the funds necessary for all expenses related to the initial development, which included license fees, construction and implementation of the Hub Operation (the “Hub Implementation Expenses”), aggregating approximately $400,000.

The Hub Implementation Expenses included:

|

|

·

|

costs of the software, hardware, and all equipment necessary for the implementation and proper operation of the Hub Operation;

|

|

|

·

|

costs of training employees, management, owners, and contractors on the proper operation of the Hub Operation;

|

|

|

·

|

costs of the licensing rights to the software program for the Hub Operation; and

|

|

|

·

|

operational costs directly related to the running of the Hub Operation.

|

Since the Hub Operation has been launched and is considered operational, all expenses necessary and related to the ongoing operation and management of the Hub Operation (“Hub Operational Expenses”) are paid out of the funds generated by the operation of the Hub Operation prior to any distribution of profits. The Hub Operational Expenses include all costs of operating and managing the Hub Operation. GFS was responsible for all the expenses through June 30, 2008. Subsequent to June 30, 2008, any contributions needed for Hub Operational Expenses are paid by RTCN and GFS equally. Under the terms of the agreement, if either RTCN or GFS fails to make all or a part of any required contribution, at the option of the other shareholder, either (i) such other shareholder must make such payment or (ii) the shareholder failing to make the contribution must forfeit such portion of its stockholding in RTCA as is proportionate to the amount of the failure and a figure equal to an overall capitalization of RTCA of twice the aggregate amount paid by GFS for the RTCA Shares (excluding amounts paid by it under this sentence).

From the gross income of the Hub Operation, the manager must (i) first pay the expenses of the ongoing Hub Operation, (ii) then reimburse a shareholder for any advances or payments made after April 30, 2007, and (iii) then distribute equally to the shareholders the profits of the Hub Operation as they accrue. The term “profits” means any amounts generated by the Hub Operation after payment of all Hub Operational Expenses, and as generally defined and commonly used in practice and custom.

Acquisition of RTCK

On October 23, 2007, we acquired all of the outstanding shares of RTCK in exchange for 1,000,000 shares of our common stock. RTCK is currently licensed by the government of St. Kitts and Nevis to operate pari-mutuel facilities. RTCK is also licensed by the Horsemen’s Association of Nevis. The acquisition of RTCK enabled us to open a call-center in St. Kitts and effectively terminated a contract between us and RTCK under which we paid royalties to RTCK aggregating $640,000. This royalty payment for $640,000 was expensed during 2007 through the issuance of the 1,000,000 shares to acquire RTCK. In May 2008, we moved our St. Kitts operations to Antigua.

Non-binding Letter of Intent to Sell Royal Turf Club Subsidiaries

On March 1, 2011, we entered into a non-binding letter of intent with respect to the Proposed Sale by us of RTCN and RTCK to the Acquiror. Under the terms of the Proposed Sale, the equity holders of the Acquiror would exchange an aggregate of 9,007,613 shares of our common stock held by them for (i) 100% of the outstanding capital stock of RTCN and RTCK and (ii) $1,000,000 in cash, $200,000 of which would be payable upon the closing of the Proposed Sale and $800,000 of which would be payable in four equal installments on the first business day of each of the first four calendar months following the month in which the closing of the Proposed Sale occurs. We will require additional financing in order to consummate the Proposed Sale. There can be no assurance that the Proposed Sale will be consummated on the foregoing terms or at all.

Global Pari-Mutuel Instant Racing Project

On September 1, 2009, we entered into an Instant Racing Web Agreement with Racetech International with a term of seven years (the “Racetech Agreement”) under which (i) we obtained a license to operate, through our hub in Antigua, an online pari-mutuel based instant racing games and wagering system (the “IR Web System”) and (ii) Racetech International agreed to provide us with certain maintenance and support services in connection therewith. In consideration of the license and services, we agreed to pay Racetech International (a) a $10,000 annual fee and (b) 23% of net win from the IR Web System for all IR Web System games.

Instant racing utilizes recorded pari-mutuel events, currently greyhound and thoroughbred races, upon which wagerers place wagers through a terminal that is virtually identical to a self-service wagering terminal. The machine uses a random number generator to select races from a grouping of stored pari-mutuel races located in a main server. The wagerer inserts money and makes a selection of potential finishers, just like making a bet on a live race, based upon certain handicapping data that is provided via performance charts. The wagerer is not provided information concerning the race venue, date of race, name of horse or dog, or the jockey or trainer if applicable. Once the wagerer submits the wager via the terminal, the race is shown and the result is displayed. Payouts are determined by the wagers contributed to the pari-mutuel wagering pools.

During December 2009, we established a joint venture to finance the IRP, which was based on an agreement between us and Racetech, LLC (“RT”). Pursuant to the agreement between us and RT, we have express authority to enter into this joint venture for purposes of promoting RT’s Instant Racing Project. Investors of the joint venture as a group agreed to purchase up to twenty project units from us at a cost of $25,000 per unit, consisting of $5,000 in unsecured liability and $20,000 in a loan which accrues interest at 8% per annum.

Under this arrangement, these investors were to receive 25% of the net proceeds and we were to receive the remaining 75%. Investors were also to receive 80% of the net revenue received by the joint venture until the notes and accrued interest have been paid in full. The joint venture was solely liable for the repayment of any amounts under this arrangement.

On August 10, 2010, the board of directors was authorized to offer the holders of the joint venture notes payable, the opportunity to convert their notes to shares of our common stock at $0.20 per share. This offer was valid until September 30, 2010. In September 2010, holders of notes payable totaling $350,000 less an unpaid investment balance of $10,000 converted their notes payable to 1,700,000 shares of our common stock. We also paid $87,500 in cash to the investors to repay their advances. On September 30, 2010, the joint venture was terminated and we retained all rights to future profits from the IRP.

Global Pari-Mutuel Network

We have a marketing agreement with Vector Enterprises, Inc., under which the internet pari-mutuel wagering website, www.trackplayer.com, a fully integrated advance deposit wagering (“ADW”) pari-mutuel internet horse, dog, and harness racing site, which is co-branded and owned by us, was established to accept pari-mutuel wagering. ADW is a system of wagering that allows wagerers to establish and fund an account from which they may place wagers via telephone, mobile device or through the internet. Under the agreement, Vector Enterprises, Inc. directs traffic to www.trackplayer.com through online advertising. Certain U.S. states prohibit ADW systems. See the section entitled, “Government Regulation,” below.

Business Development

General

With new management in place, we are driving the business in a new direction. We are creating an online experience that will enable users to follow and share information regarding the fast-paced global financial marketplace and to compete against each other in a traditional racing format. In short, we are developing a new way for individuals to interact with the public financial markets. Our goal is to be the leading “social” financial markets destination, and our vision is to be at the intersection of the global financial markets, fantasy sports, horse racing and online gaming community.

We plan to provide a new mix of content related to public companies, financial indices, commodities and currencies. This content mix of fundamental and technical financial data will be combined with a social media platform to encourage users to personalize and connect impersonal financial services data to individuals’ daily lives. Using existing pari-mutuel technology, previously used exclusively for the horse and dog racing industries, we plan to host online games and races to enable users to compete against each other in a new and exciting way.

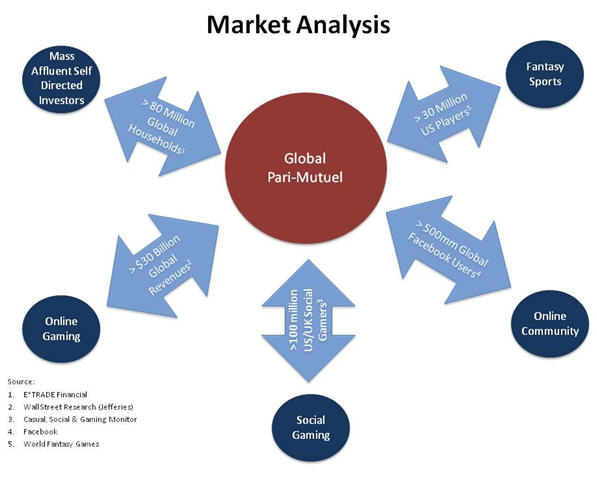

The Market

Our addressable market is at the intersection of five large and fast growing markets: mass affluent self-directed investors, fantasy sports, online gaming, social gaming and online community.

Based on data regarding the markets highlighted above, we believe that we have the opportunity to acquire 5.0 million to 7.0 million users within five years of our product launch.

According to World Fantasy Games, an operator of fantasy games since 1993, the average fantasy sports player in 2006 and 2007 spent an average of $467.60 playing fantasy sports per year. We project that participants in our contests will generate annual average revenue of $440 per player. As is typical for contests that employ a pari-mutuel wagering system, our revenues will be generated by retaining a percentage of the betting pool.

Product Development

We began developing our new product in December 2010 and anticipate a September 2011 launch of our gaming platform. We believe we have made significant progress since December:

|

|

·

|

December 7, 2010 – We engaged Bendigo Partners to develop our new strategic direction. We appointed Jarrett Lilien, former president and chief operating officer of E*TRADE Financial Corporation (“E*TRADE”), and Richard Taylor, former head of global operations at E*TRADE, as our chief executive officer and chief operating officer, respectively, and both serve on our board of directors.

|

|

|

·

|

February 9, 2011 – We formed a wholly-owned subsidiary, Global Guernsey, which will serve as our operations and technology center for our new gaming platform. We have also begun the application process to obtain a gaming license from The Alderney Gambling Control Commission that will ultimately be held by an Alderney subsidiary.

|

|

|

·

|

February 9, 2011 – Global Guernsey entered into an agreement with AmTote, a leading supplier of pari-mutuel totalisator systems and services, whereby AmTote will provide its services on an exclusive basis for our new proprietary financial markets-based technology. The AmTote system will be the core of our back- and middle-office infrastructure.

|

|

|

·

|

February 15, 2011 – We filed a patent application with the United States Patent and Trademark Office related to our new product that will allow people to compete against one another in online games involving financial instruments, such as stocks, indices, commodities and currencies. Both utility and design aspects were included in the patent filing, including methods for defining the games, use of a pari-mutuel system for calculating odds and payouts, visualization of “races” within games, and other processes.

|

|

|

·

|

March 1, 2011 – We signed a non-binding letter of intent to sell our Royal Turf Club subsidiaries to a group of investors led by our former chief executive officer, James Egide. If the sale closes, this restructuring would enable the company to focus exclusively on our new business.

|

|

|

·

|

March 8, 2011 – Global Guernsey entered into an agreement with brand development firm Mechanica to help build, brand and launch our global gaming platform. Mechanica is overseeing the development of the end-user interface of our games, which is already in progress.

|

The Social Community

We are designing the social media aspects of our product offering. These will include the development of online forums with chat capabilities as well as additional content and features.

The Games

Overview

In addition to providing a social media platform where the user community will be able to discuss the financial markets and financial instruments, users will be able to compete against each other in contests that involve picking the best or worst performing racers. We plan to host contests where stocks, indices, commodities or currencies race against each other.

In the United Kingdom, we plan to offer users the opportunity to play single-race and multi-race contests.

In the United States, we plan to offer users the opportunity to play contests that comprise multiple races. We also plan to offer a portfolio contest structured like fantasy football, but instead of drafting players, users will draft securities, and instead of competing against other users with a fantasy team of players, users will compete with their fantasy portfolios of securities.

Structure

In the United Kingdom, single races will constitute a game, but users will be able to compete in multiple races using pari-mutuel wagering.

In the United States, a single contest will either consist of a series of races that the contest’s players will have the opportunity to participate in or in a league format where players’ fantasy portfolio compete against each other as in fantasy football. In the multi-race contests in the United States, players will select the races within a contest in which they want to participate and how many credits they want to wager on a particular race’s entrant and the type of wager (i.e., win, place, show or exotics wagers).

We will determine the specific financial instruments that will be run in, as well as the duration of, individual races. We anticipate that each race will have between six and eight “horses”. We may also offer users the ability to select specific financial instruments from among an authorized pool to race in custom or user-generated races.

We currently plan to organize races designed around a variety of economic, seasonal and event-driven themes. Specific participants in a race will be selected based on their relevance to a particular theme as well as statistical measures such as market capitalization, average trading volume and volatility. We expect that race participants will be selected from a number of global markets to create a 24-hour gaming experience.

In addition to selecting the race’s participants, we will also determine whether races will be one-way (i.e., best performer is the winner) or two-way (i.e., best performer is a winner and worst performer is also a winner). We will also determine the wager types for each race. All races will allow the following straight wagers:

|

|

·

|

Win – the selected security finishes first

|

|

|

·

|

Place – the selected security finishes first or second

|

|

|

·

|

Show – the selected security finishes first, second or third

|

We anticipate that contests may also allow users to make exotic wagers, such as:

|

|

·

|

Exacta – users must pick the two securities that finish first and second, in the exact order

|

|

|

·

|

Quinella – users must pick the two securities that finish first and second, but need not specify which will finish first (similar to an exacta box)

|

|

|

·

|

Trifecta – users must pick the three securities that finish first, second and third, in the exact order

|

|

|

·

|

Sweep or Pick Four/Pick Six – users must pick the winners of four or more successive races with Pick Six paying out a consolation return to users who correctly select five winners out of six races, and with rollover jackpots accumulating each day until one or more users correctly picks all six winners

|

Using a proprietary process, we will set the initial odds for each race. Once wagering begins, odds will be re-calculated based on the pari-mutuel system.

Scoring

The results of the individual races will be determined by a simple ranking of the relative percentage price movements of the securities entered into the race. Specifically, a security will be deemed to come in first, if its percentage price performance is greater than, or, in two-way races, worse than, all the other securities’ performance. The other securities in the race will be ranked in a similar manner. The following hypothetical results table illustrates this concept:

|

Rank

|

Symbol

|

End Price

|

Start Price

|

Price Difference (%)

|

|

1

|

AXP

|

44.76

|

44.64

|

0.268097

|

|

2

|

IN

|

12.7

|

12.7

|

0

|

|

3

|

BMY

|

25.89

|

25.9

|

-0.038625

|

|

4

|

CBS

|

20.84

|

20.865

|

-0.119962

|

|

5

|

YRCW

|

4.1

|

4.11

|

-0.243902

|

Contest Payout

When a race is over, payouts or points, depending on the contest type, will be determined based on the odds that were in effect when wagering was closed. For example, players who place a 10 credit “win” wager on a security with 3-to-1 odds, will have their credit balances increased by 30, representing the 10-credit wager and a 20-credit gain. Payouts for Place, Show and the more exotic wager types will be based on the pari-mutuel system.

Competition

Competition in our market place is primarily based on price and accessibility to the various horse and dog racing wagering pools.

Our principal competition for customers in Mexico and Central America is Hipodromo de Agua Caliente, S.A. de C.V. (“Caliente”). Caliente provides online wagering on horse and dog racing and is our principal competition for the provision of (i) pari-mutuel wagering services and content to physical OTB operators through our hub operations in Antigua and (ii) pari-mutuel wagering services through our international call center. Caliente is a legal bookmaking operator that offers customers track prices with payout limits. The pari-mutuel wagering services that we offer, however, provide for no payout limits due to the common pooling service that we offer.

The following companies compete with us for our customers where we provide pari-mutuel wagering services and content to international simulcast facilities and the Global Pari-Mutuel Network. TVG and the Television Games Network are direct competitors in the interactive, pari-mutuel wagering market. TVG operates an ADW website and currently operates in 15 states. In January 2009, Betfair completed its purchase of TVG. Betfair’s main product is a betting exchange, which is not legal in the United States. Changes by Betfair in the operation of TVG, including investment of significant resources into the operation of TVG or expansion into states where TVG currently does not operate, would increase competition for us. The Television Games Network is a 24-hour national racing channel for distribution over cable, Dish Network and DIRECTV®, along with an in-home pari-mutuel wagering system that requires a dedicated television set-top box. Magna Entertainment Corporation (“Magna”) and its affiliated ADW website, XpressBet, and Churchill Downs and its affiliated ADW website, Twinspires.com, are also direct competitors in the U.S. interactive, pari-mutuel wagering market. In March 2007, Magna and Churchill Downs announced that they had formed a joint venture called TrackNet through which the companies’ horse racing content would be available to each other’s various distribution platforms, including XpressBet and Twinspires, and to third parties, including racetracks, casinos and other ADW providers. Magna and Churchill Downs also jointly own Horse Racing Television (HRTV). Magna filed for Chapter 11 bankruptcy protection on March 5, 2009. On February 18, 2010, Magna filed a Plan and related Disclosure Statement (the “Magna Plan”) in connection with its Chapter 11 proceedings, which was confirmed by order of the Bankruptcy Court on April 26, 2010. On April 30, 2010, the closing conditions of the Magna Plan were satisfied or waived, and the Magna Plan became effective following the close of business on April 30, 2010. Magna’s operations were transferred to MI Developments Inc. on April 30, 2010 pursuant to the Magna Plan.

Youbet.com, Inc. operates as a licensed multi-jurisdictional facilitator of online pari-mutuel horse race wagering, and supplier of tote equipment and services to the racing industry. Its principle product, Youbet Express, offers interactive and real-time audio/video broadcasts, access to database of handicapping information, and the ability to wager on various horse races in the United States, Canada, the United Kingdom, Australia and South Africa. Churchill Downs acquired Youbet.com on June 2, 2010.

Other competitors include Premier Turf Club, The Racing Channel, doing business as Oneclickbetting.com, and AmWest Entertainment. We expect to compete with these entities, as well as new companies, which may enter the interactive, pari-mutuel gaming market. It is possible that our current and potential competitors may have greater resources than us.

Governmental Regulation

We believe that the launch of our new product that is currently in development may, in large part, depend upon our ability to comply with multiple regulatory regimes in the major markets around the world. As such, we are currently in the process of researching regulations related to gaming, gambling and financial products in the jurisdictions in which we intend to offer our new product, once developed. Many of the regulations by which we may be governed are intended to protect the public, our potential customers and the integrity of the markets. If we are required to and are successful in registering in any jurisdiction, these regulators and self-regulatory organizations would regulate the conduct of our business in many ways and conduct regular examinations to monitor our compliance with these regulations.

Electronic transaction processing is regulated in the United States through the banking industry and card issuers, however, we are not aware of any governmental entity that regulates the payment processing services that we propose to market on behalf of banks or of any current attempts to impose governmental regulation on payment processing services.

Gaming activities are subject to extensive statutory and regulatory control in the United States by state and internationally by various government authorities. All 50 U.S. states currently have statutes or regulations restricting gaming activities, and three states do not permit gaming at all. Federal and state statutes and regulations are likely to be significantly affected by any changes in the political climate and economic and regulatory policies. These changes could affect our proposed operations in a materially adverse way.

We believe that our proposed pari-mutuel activities conform to current gaming laws and regulations as we understand them to be currently applied. There is very little clear statutory and case law authority and, therefore, this conclusion can be challenged by either governmental authorities or private citizens. Pari-mutuel wagering is governed by state legislation. States adopt and enforce rules and regulations requiring all entities involved in pari-mutuel horseracing to be licensed. States prohibiting advanced deposit pari-mutuel wagering include Alaska, Arizona, Colorado, District of Columbia, Georgia, Hawaii, Mississippi, Missouri, Nebraska, Nevada, New Mexico, North Carolina, Oklahoma, South Carolina, and Utah.

The Interstate Horseracing Act of 1978 (“IHRA”) regulates pari-mutuel wagering on horseracing across state lines. This statute was created to remove pari-mutuel horseracing from illegal wagering activities covered by the Federal Wire Act (Chapter 18 USC) (the “Wire Act”). The IHRA was amended in December 2000 to clarify that pari-mutuel wagering may be placed via telephone or other electronic media (including the internet), and accepted by an off-track betting system where such wagers are lawful in each state involved. Thus, management believes existing federal statutes appear to allow pari-mutuel wagering on horse races and the Wire Act would not indirectly prohibit such activities. In the fourth quarter of 2006, Congress passed the Unlawful Internet Gambling Enforcement Act of 2006 (the “UIGEA”) which includes certain racing protective provisions by maintaining the status quo with respect to wagering activities covered under the IHRA. The UIGEA prohibits the acceptance of credit cards, electronic funds transfers, checks of the proceeds of other financial transactions by persons engaged in unlawful betting or wagering businesses. However, the UIGEA specifically excludes from the definition of unlawful internet gambling “any activity that is allowed under the Interstate Horseracing Act of 1978”. On November 12, 2009, the Department of the Treasury and the Federal Reserve Board jointly published the final rule implementing the UIGEA.

Other federal laws impacting gaming activities include IHRA, the Interstate Wagering Paraphernalia Act, the Travel Act and the Organized Crime Control Act. Certain legislation is currently being considered in Congress and individual states in this regard. Currently, certain online international off-track betting parlors permit their customers to bet on horse races taking place within the United States. However, their customers are not included in the general pari-mutuel pool created for the races, and they do not normally have access to pari-mutuel pools that result from the betting decisions of other participants.

Employees

As of March 17, 2011, we have one full-time employee and we utilize the services of four consultants that devote substantially all of their time to the company. In addition, as of December 7, 2010, we entered into the Consulting Agreement, pursuant to which R. Jarrett Lilien serves as our chief executive officer, J. Leslie Whiteford serves as our chief financial officer, Richard D. Taylor serves as our chief operating officer, Stephen Ferrando serves as our chief information officer, and one additional individual serves as our chief marketing officer and a law firm serves as our internal general counsel. We consider our relationships with our employees and consultants to be good. In the event that additional full or part-time employees or consultants are required to conduct or expand our business operations, we believe we will be able to identify, hire and/or engage qualified personnel.

Deregistration

On March 31, 2010, we filed a Form 12b-25 notifying the Securities and Exchange Commission (“SEC”) of our inability to timely file an annual report on Form 10-K for the fiscal year ended December 31, 2009 and representing that the Form 10-K would be filed no later than April 15, 2010, the date that was the fifteenth calendar day following the prescribed due date for our Form 10-K. Subsequent to filing the Form 12b-25, we determined that due to the significant costs of operating as a public reporting company, the substantial time that being a public reporting company required of our management team and the availability of deregistration as an option in accordance with SEC rules, we determined that it would be in the best interest of our stockholders and our company at the time to deregister our common stock under Section 12(g) of the Exchange Act. On June 7, 2010, we filed a Form 15 deregistering our common stock under Section 12(g) of the Exchange Act in reliance upon Rule 12g-4(a)(1) and Rule 12g-4(a)(2) without first filing our Form 10-K and our Form 10-Q for the fiscal quarter ended March 31, 2010. As a result, when we filed the Form 15 deregistering our common stock under Section 12(g) of the Exchange Act, we were not in compliance with Section 13(a) of the Exchange Act, which requires every issuer of a security registered pursuant to Section 12 of the Exchange Act to file periodical and other reports with the SEC in accordance with the SEC’s rules and regulations. As a result of such noncompliance, the SEC may determine to revoke or suspend the registration of our common stock under Section 12(g) of the Exchange Act. In addition, there can be no assurance that we will not fall out of compliance with Section 13(a) of the Exchange Act again in the future.

With our new management team in place as of December 7, 2010 and the acquisition of BERMASE as our wholly-owned subsidiary, which was consummated on December 21, 2010, as a result of which we acquired $2,000,000 in cash, we intend to continue to pursue the development of new proprietary technology to expand our pari-mutuel trading hub to the financial services industry, including the development of a new product as more fully described above. We anticipate that we may need to raise additional capital through future financings. As a result, we determined to reregister our securities under Section 12(g) of the Exchange Act in order to better position ourselves to obtain access to capital markets and ultimately be successful in the implementation of our business plan.

Where You Can Find More Information

We file annual, quarterly and current reports and other information with the SEC. Our filings are available to the public at the SEC’s website at http://www.sec.gov. You may also read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, N. E., Washington, DC 20549 You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

|

Item 1A.

|

Risk Factors

|

The launch of our new product that will allow users to compete with each other using a system of pari-mutuel wagering on the relative price movements of various financial instruments may depend, in large part, upon our compliance with government regulations in the major customer markets around the world.

We believe that the launch of our new product that is currently in development may, in large part, depend upon our ability to comply with multiple regulatory regimes in the major markets around the world. We may need to obtain required registrations from the jurisdictions in which we plan to launch our product. As a result, if we do not obtain the required registrations, we would not be able to generate revenues from our new product, and we would not be able to implement our operations, as currently contemplated, in any meaningful way.

Many of the regulations by which we may be governed are intended to protect the public, our potential customers and the integrity of the markets. If we are required to and are successful in registering in any jurisdiction, these regulators and self-regulatory organizations would regulate the conduct of our business in many ways and conduct regular examinations to monitor our compliance with these regulations. If the regulators determine that we breached or violated any rule, law or regulation, we may be subject to sanctions, fines or revocation of our registration in such jurisdiction, which will have a negative impact on our operations and may require that we cease operations assuming that we have developed operations.

With respect to the market in the United States, for example, on July 21, 2010, the Dodd–Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) was enacted into law. The Dodd-Frank Act calls for the Commodity Futures Trading Commission, the SEC and the Federal Reserve to regulate the market for over-the-counter (“OTC”) derivative products. Currently, rulemakings are pending at these agencies, the product of which will be rules that implement the mandates in the Dodd-Frank Act to eliminate the risk of systemic failure of financial markets. The significance of the effect on us will depend in part on whether we are able to successfully develop our new product and whether, as a result of such product, we are determined to be subject to these rules, which have not yet been publicly disseminated, through the classification of our new product as a swap or security-based swap as broadly defined in the Dodd-Frank Act. We continue to monitor the rulemaking procedures and cannot predict the ultimate outcome that the financial reform legislation will have on the development of our new product.

We rely on third parties to develop and supply us with the technology required to operate our current and proposed business. If these third parties do not perform as contractually required or otherwise expected, we may not be able to successfully develop and market our products and services.

We currently outsource our data and technology needs to third parties, including AmTote. Our technology partners may not be able to respond effectively to market changes and we may not be able to maintain strong alliances with those to whom we outsource our data and technology needs. If these third parties do not perform as contractually required or otherwise expected, we may not be able to successfully develop and market our products and services.

We have limited capital resources and cannot ensure access to additional capital if needed.

Our historical operating losses have required us to seek additional capital through the issuance of promissory notes and our common stock on a number of occasions. If we continue to sustain operating losses in future periods, we will be forced to seek additional capital to fund our operations. We do not know whether we will be able to obtain additional capital, or on what terms the capital would be available, if at all. Depending on market conditions and our prospects, additional financing may not be available or may result in significant dilution to our current stockholders.

Our independent registered public accounting firm has issued a “going concern” opinion raising substantial doubt about our financial viability. The accompanying consolidated financial statements for the years ended December 31, 2010 and 2009 have been prepared on a basis that contemplates the realization of assets and the satisfaction of liabilities and commitments in the normal course of business. We have continuing net losses and negative cash flows from operating activities. In addition, as of March 17, 2011, we have a commitment to pay Bendigo Partners an additional $2,000,000 for consulting services through November 30, 2011. These conditions raise substantial doubt about our ability to continue as a going concern. Our consolidated financial statements do not include any adjustments to the amounts and classification of assets and liabilities that may be necessary should we be unable to continue as a going concern. These circumstances caused our independent registered public accounting firm to include an explanatory paragraph in its report dated February 18, 2011, except for Note 12 as to which the date is March 16, 2011, regarding their concerns about our ability to continue as a going concern. Substantial doubt about our ability to continue as a going concern may create negative reactions to the price of the common shares of our stock and we may have a more difficult time obtaining financing.

Since our common stock is classified as “penny stock,” the restrictions of the SEC’s penny stock regulations may result in less liquidity for our common stock.

The SEC has adopted regulations which define a “penny stock” to be any equity security that has a market price (as therein defined) of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. For any transactions involving a penny stock, unless exempt, the rules require the delivery, prior to any transaction involving a penny stock by a retail customer, of a disclosure schedule prepared by the SEC relating to the penny stock market. Disclosure is also required to be made about commissions payable to both the broker/dealer and the registered representative and current quotations for the securities. Finally, monthly statements are required to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. Because the market price for shares of our common stock is less than $5.00, and we do not satisfy any of the exceptions to the SEC’s definition of penny stock, our common stock is classified as penny stock. As a result of the penny stock restrictions, brokers or potential investors may be reluctant to trade in our securities, which may result in less liquidity for our common stock.

When we filed the Form 15 deregistering our common stock under Section 12(g) of the Exchange Act on June 7, 2010, we were not in compliance with Section 13(a) of the Exchange Act and there can be no assurance that we will comply with Section 13(a) of the Exchange Act in the future. Failure to comply with Section 13(a) of the Exchange Act may have a material adverse affect on our stock price and the value of our business because, as a result of such non-compliance, the SEC may determine to revoke or suspend the registration of our common stock under Section 12(g) of the Exchange Act.

On March 31, 2010, we filed a Form 12b-25 notifying the SEC of our inability to timely file an annual report on Form 10-K for the fiscal year ended December 31, 2009 and representing that the Form 10-K would be filed no later than April 15, 2010, the date that was the fifteenth calendar day following the prescribed due date for our Form 10-K. Subsequent to filing the Form 12b-25, we determined that due to the significant costs of operating as a public reporting company, the substantial time that being a public reporting time required of our management team and the availability of deregistration as an option in accordance with SEC rules, we determined that it would be in the best interest of our stockholders and our company at the time to deregister our common stock under Section 12(g) of the Exchange Act. As a result, on June 7, 2010, we filed a Form 15 deregistering our common stock under Section 12(g) of the Exchange Act in reliance upon Rule 12g-4(a)(1) and Rule 12g-4(a)(2) without first filing our Form 10-K and our Form 10-Q for the fiscal quarter ended March 31, 2010. As a result, when we filed the Form 15 deregistering our common stock under Section 12(g) of the Exchange Act, we were not in compliance with Section 13(a) of the Exchange Act, which requires every issuer of a security registered pursuant to Section 12 of the Exchange Act to file periodical and other reports with the SEC in accordance with the SEC’s rules and regulations. There can be no assurance that we will not fall out of compliance with Section 13(a) of the Exchange Act again in the future. Failure to be in compliance with Section 13(a) of the Exchange Act may have a material adverse affect on our stock price and the value of our business because, as a result of such non-compliance, the SEC may determine to revoke or suspend the registration of our common stock under Section 12(g) of the Exchange Act.

Your ability to influence corporate decisions may be limited because ownership of our common stock is concentrated.

Our directors and executive officers as a group beneficially owned 202,982,107 (approximately 90.83% of our outstanding common stock as of March 17, 2011). As a result of their ownership of our common stock, our directors and executive officers, collectively, may be able to control matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. Such concentration of ownership may also have the effect of delaying or preventing a change in control of the company, and this may have a material adverse effect on the trading price of our common stock.

Our limited operating history makes it difficult for investors to evaluate our performance and/or assess our future prospects.

We were initially incorporated in January 1997. From January 1997 to October 1998, our business operations primarily consisted of efforts to develop and market online casino services. We discontinued efforts to develop online casino services in June 1998. We subsequently pursued development of an electronic currency services business, development of a credit card processing services business, a related operation of providing ATM debit card services to online gaming customers and marketing credit card services of international credit card processors to merchants. From 2005 to the present, we have focused on our pari-mutuel business opportunities. As a result, there is a very limited operating history upon which an evaluation of our company can be based. Our future prospects are subject to risks and uncertainties that are generally encountered by newly operational companies in new and rapidly evolving markets. These risks include, but are not limited to:

|

|

·

|

Whether we can successfully market and execute our business model for pari-mutuel wagering;

|

|

|

·

|

Whether the demand for our proposed services will grow to a level sufficient to support our operations;

|

|

|

·

|

Whether governing laws, regulations or regulatory initiatives will force us to discontinue or alter certain business operations or practices;

|

|

|

·

|

Whether we and our strategic partners can develop and maintain products and services that are equal or superior to the services and products of competitors; and

|

|

|

·

|

Whether we can generate the funds as needed to sell the services we intend to offer, and attract, retain, and motivate qualified personnel.

|

There can be no assurance that we can be successful in addressing these risks. Our limited operating history and the uncertain nature of the markets for our proposed services make the prediction of future results of operations extremely difficult. As a result of the foregoing factors and the other factors identified herein, there can be no assurance that we will ever operate profitably on a quarterly or annual basis.

We may become subject to government regulation and legal uncertainties, which may adversely affect our business.

We believe that we are not currently subject to regulation by any U.S. or foreign governmental agency, other than regulations applicable to businesses generally. However, due to the increasing usage of the internet and concerns about online gaming in general, it is possible that a number of laws and regulations may be adopted in the future that would affect our conducting business over the internet. In addition, we may become subject to new laws and regulations directly applicable to the internet and our activities. Any new legislation applicable to us could expose us to substantial liability, including significant expenses necessary to comply with these laws and regulations. Furthermore, the growth and development of the market for electronic commerce may promote more stringent consumer protection and privacy laws that may impose additional burdens on companies conducting business online, including us. The adoption of additional laws or regulations may decrease the growth of the internet or other online services, which could, in turn, decrease the demand for our services and increase our cost of doing business. For example, we may become subject to some or all of the following sources of regulation: state or federal banking regulations; federal money laundering regulations; international banking, financial services or gaming regulations or laws governing other regulated industries; or U.S. and international regulation of internet transactions. The application to us and our new product of existing laws and regulations relating to issues such as banking, currency exchange, online gaming, pricing, taxation, quality of services, electronic contracting, and intellectual property ownership and infringement is unclear. If we are found to be in violation of any current or future regulations, we could be exposed to financial liability, including substantial fines which could be imposed on a per transaction basis; forced to change our business practices; or forced to cease doing business altogether or with the residents of one or more states or countries.

We must adapt to new regulations governing the transmission, use and processing of personal information in electronic commerce.

Our services involve handling, transmitting, verifying and processing personal information of customers that we service. As electronic commerce continues to evolve, federal, state and foreign governments may adopt laws and regulations covering user privacy. New laws regulating the solicitation, collection or processing of personal or consumer information could increase the costs and complexity of our operations and adversely affect our business.

Even if there is a demand for our online pari-mutuel wagering support services, the revenues generated from such services may not exceed the costs associated with providing the services.

We plan to provide settlement and reconciliation services to facilitate online pari-mutuel wagering. We have not entered into any contracts with respect to, or otherwise obtained any commitments from anyone to purchase or use the pari-mutuel support services we propose to offer. We can provide no assurance that there will be any demand for our online pari-mutuel wagering support services. If there is a demand, we can provide no assurance that the revenues generated from such services will exceed the costs associated with providing the services.

We may not attract or retain qualified management and employees.

Our future success and our ability to expand our operations will depend on our ability to retain highly qualified management and employees. As a thinly-capitalized company, we may have difficulty or be unable to retain or attract highly qualified management and employees. Failure to attract and retain personnel will make it difficult for us to manage our business and meet our objectives, and will likely have a material adverse effect on our business operations. We do not carry key person life insurance on any of our senior management personnel. The loss of the services of any of our executive officers or other key employees may have a material adverse effect on our business.

We intend to conduct a significant portion of our business offshore, which is subject to additional risks that may adversely affect our business.

We, or our affiliates, intend to conduct a significant portion of our business offshore. Conducting business outside of the United States is subject to additional risks that may affect our ability to sell our products and services and result in reduced revenues, including, without limitation:

|

|

·

|

Currency exchange fluctuations;

|

|

|

·

|

Changes in regulatory requirements;

|

|

|

·

|

Reduced protection of intellectual property rights;

|

|

|

·

|

Evolving privacy laws in foreign countries;

|

|

|

·

|

The burden of complying with a variety of foreign laws; and

|

|

|

·

|

Political or economic instability or constraints on international trade.

|

We cannot be certain that one or more of these factors will not materially adversely affect our future international operations and, consequently, our business, financial condition, and operating results.

Other than a patent application that we filed on February 15, 2011, we have not sought to protect our intellectual property through registration. We may not be able to protect our intellectual property, which would reduce the value of our products and services.

On February 15, 2011, we filed a patent application with the United States Patent and Trademark Office relating to online games as well as the systems and corresponding methods that allow users to compete against each other in one or more games involving various financial instruments. Although we do own intellectual property, other than the aforementioned patent application, we currently do not have any registered intellectual property, including patents, trademarks and copyrights. Although we may seek to obtain patent protection for our other innovations, it is possible we may not be able to protect some of these innovations. Changes in patent law, such as changes in the law regarding patentable subject matter, can also impact our ability to obtain patent protection for our innovations. In addition, given the costs of obtaining patent protection, we may choose not to protect certain innovations that later turn out to be important. Furthermore, there is always the possibility, despite our efforts, that the scope of the protection gained will be insufficient or that an issued patent may be deemed invalid or unenforceable.

We may also seek to maintain certain intellectual property as trade secrets. The secrecy could be compromised by outside parties, or by our employees, which would cause us to lose the competitive advantage resulting from these trade secrets.

Our inability to protect our intellectual property could reduce the value of our products and services. Various events outside of our control pose a threat to our intellectual property rights as well as to our products and services. For example, effective intellectual property protection may not be available in every country in which our products and services are distributed or made available through the internet. Also, the efforts we have taken to protect our proprietary rights may not be sufficient or effective. Any significant impairment of our intellectual property rights could harm our business or our ability to compete. Also, protecting our intellectual property rights is costly and time consuming. Any increase in the unauthorized use of our intellectual property could make it more expensive to do business and harm our operating results.

We may be unable to obtain the licenses or other proprietary rights necessary to implement our business plan.

We expect to be dependent upon the intellectual property and other resources of our technology providers. We may be required to obtain licenses to certain intellectual property or other proprietary rights from such parties. Such licenses or proprietary rights may not be made available under acceptable terms, if at all. If we do not obtain required licenses or proprietary rights, we could encounter delays in product development or find that the deployment of technology and/or sale of services requiring such licenses are foreclosed.

Our stock price is volatile.

Transactions in our common stock are presently reported on the Pink Sheets. The trading price of our common stock has been and may continue to be subject to wide fluctuations. In the last twelve months transactions in our common stock have been reported as low as $0.11 and as high as $1.45. The wide swings in the price of our common stock have not always been in response to factors that we can identify. Factors that are likely to contribute to the volatility of the trading price of our common stock include, among others:

|

|

·

|

The relatively low volume of trading in our common stock;

|

|

|

·

|

The number of short positions in our common stock;

|

|

|

·

|

The control of the market for our common stock by very few participants;

|

|

|

·

|