Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2010 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission file number 001-34641

FURIEX PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 27-1197863 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

3900 Paramount Parkway, Suite 150

Morrisville, North Carolina 27560

(Address of principal executive offices, including zip code)

(919) 456-7800

(Registrant’s telephone number, including area code):

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, par value $0.001 per share | Nasdaq Global Market | |

| (Title of each class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its Corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer | ¨ | ||||

| Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the common stock held by non-affiliates of the registrant was approximately $93.9 million as of June 30, 2010, based on the closing price of the Common Stock on that date on the Nasdaq Global Market. Shares of common stock held by each executive officer and director and by each person who owns 10% or more of the outstanding common stock have been excluded in that such person might be deemed to be an affiliate. This determination of affiliate status might not be conclusive for other purposes.

As of March 11, 2011, there were 9,881,340 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The Company’s definitive Proxy Statement for its 2011 Annual Meeting of Stockholders (certain parts, as indicated in Part III).

Table of Contents

| Part I. |

||||||||

| Item 1. | 3 | |||||||

| Item 1A. | 18 | |||||||

| Item 1B. | 34 | |||||||

| Item 2. | 34 | |||||||

| Item 3. | 34 | |||||||

| Item 4. | 34 | |||||||

| 34 | ||||||||

| Part II. |

||||||||

| Item 5. | 36 | |||||||

| Item 6. | 38 | |||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

39 | ||||||

| Item 7A. | 50 | |||||||

| Item 8. | 50 | |||||||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

50 | ||||||

| Item 9A. | 50 | |||||||

| Item 9B. | 51 | |||||||

| Part III. |

||||||||

| Item 10. | 52 | |||||||

| Item 11. | 52 | |||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

52 | ||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

53 | ||||||

| Item 14. | 53 | |||||||

| Part IV. |

||||||||

| Item 15. | 54 | |||||||

| 56 | ||||||||

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are subject to risks and uncertainties, including those set forth under “Item 1A. Risk Factors” and “Cautionary Statement” included in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this report, that could cause actual results to differ materially from historical results or anticipated results. Unless otherwise indicated or required by the context, the terms “we,” “our,” “us” and the “Company” refer to Furiex Pharmaceuticals, Inc. and all of its subsidiaries.

2

Table of Contents

PART I

| Item 1. | Business |

Our Business

About Furiex Pharmaceuticals

We are a drug development collaboration company that uses innovative, clinical development strategies to increase the value of pharmaceutical assets and accelerate their development timelines. We collaborate with pharmaceutical and biotechnology companies to increase the value of early stage drug candidates by applying our novel approach to drug development. We believe this approach expedites research and development decision-making and can shorten drug development timelines. We share the risk with our collaborators by running and financing drug development up to agreed clinical milestones, and in exchange, we share the potential rewards, receiving milestone and royalty payments for any successful drug candidates. This business model is designed to help feed product pipelines and deliver therapies to improve lives. The Company’s operations are headquartered in Morrisville, North Carolina.

Our company continues the compound partnering business started by Pharmaceutical Product Development, Inc., or PPD, in 1998. In June 2010, PPD spun-off its compound partnering business through a tax-free, pro-rata dividend distribution of all of the shares of the Company to PPD shareholders. PPD does not have any ownership or other form of equity interest in the Company following the spin-off.

Business Description

Our goal is to in-license from or form strategic alliances with pharmaceutical and biotechnology businesses to develop and commercialize therapeutics in which the risks and rewards are shared. We seek to collaborate with pharmaceutical and biotechnology companies to increase the value of early stage drug candidates by applying our novel approach to drug development that we believe expedites research and development decision-making and can shorten drug development timelines. Furiex’s team is staffed with the same key PPD team members who demonstrated proven success in the drug development collaboration business while at PPD, as well as highly-qualified new members. Our strategy is to invest in drug candidates that have a relatively straightforward path to regulatory approval and a large addressable market. Every drug candidate we review is subjected to our rigorous due diligence process by our team of experts who possess experience in all aspects of the drug development process.

Once we in-license or form an alliance, we use our drug development experience and financial resources to advance the drug candidate through clinical development. We apply a novel approach that shortens drug development timelines that we believe transforms research and development into revenues more rapidly than the typical development cycle for such collaborations. Specifically, we set the development strategy based on a product candidate’s best market position, design and manage nonclinical and clinical studies, manage the drug manufacturing programs, and evaluate the efficacy and safety data necessary to obtain regulatory approvals for the drug candidate. Furiex uses service providers to execute the tasks needed to develop and commercialize its product candidates.

Most of the large pharmaceutical companies with which we collaborate have the option to continue late stage clinical development and commercialization of the drug candidate after it has reached the specified pre-determined milestones. If our collaborator is unable or unwilling to perform late stage development and commercialization, then we have the option to seek a new development and commercialization partner.

In exchange for our drug development efforts and sharing the risk with our collaborator, we are entitled to receive milestone payments and royalties based on the continued development and commercialization success of the drug candidate.

3

Table of Contents

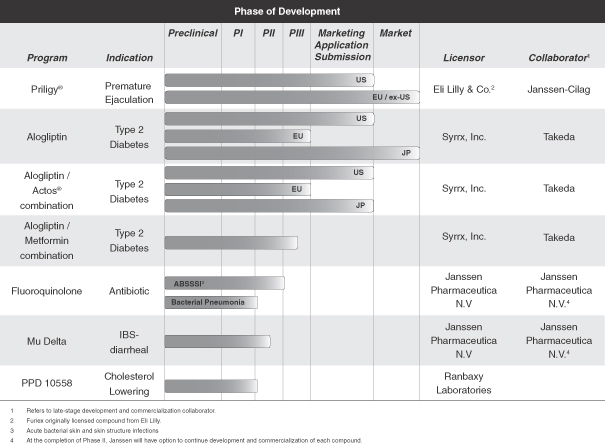

Currently, we have rights to several compounds in various stages of development and commercialization, including:

| • | Rights to royalties and sales-based milestones from the collaboration with ALZA Corporation, an affiliate of Janssen-Cilag Pharmaceutica, N.V., on Priligy™, the first approved treatment in the world for premature ejaculation. Priligy is currently marketed in 14 countries. |

| • | Rights to royalties and regulatory and sales-based milestone payments from Takeda Pharmaceutical Limited for alogliptin. Takeda received regulatory and pricing approval in Japan during the second quarter of 2010 for alogliptin for the treatment of type 2 diabetes. Takeda markets alogliptin in Japan under the name NESINA®. A cardiovascular trial requested by the United States Food and Drug Administration, or FDA, is ongoing. |

| • | A fluoroquinolone antibiotic licensed from Janssen-Cilag, an affiliate of Johnson & Johnson, in November 2009 for the treatment of acute bacterial skin and skin structure infections, such as abscesses that occur deep in the skin layers, and respiratory infections. We recently completed a Phase II clinical trial using the oral formulation for acute bacterial skin infections and are enrolling patients in a Phase II proof-of-concept trial for respiratory infections. |

| • | A compound that is a mu-opioid receptor agonist and delta-opioid receptor antagonist, which we call MuDelta, licensed from Janssen-Cilag in November 2009 for the treatment of diarrhea-predominant irritable bowel syndrome. We initiated a Phase II clinical trial during the second quarter of 2010. |

| • | A novel statin compound we refer to as PPD-10558 licensed from Ranbaxy Laboratories, Ltd. for the treatment of dyslipidemia, which is an excessive level of blood lipids such as cholesterol. Preclinical and Phase I human studies suggest that PPD-10558 has similar cholesterol-lowering properties as a leading marketed statin, and also has pharmacologic properties which suggest that it may have a lower risk of myopathy, a statin side effect involving pain and/or muscle weakness, than currently marketed statins. PPD-10558 may therefore be a useful treatment option for statin-intolerant patients. In early 2011, we initiated start up activities for a Phase II proof-of-concept trial of PPD-10558. |

4

Table of Contents

The following chart summarizes the status of our pipeline of compounds:

Our Solution

The drug development industry is under increasing economic pressure to develop new products more quickly and efficiently. To address this industry issue, we have developed what we believe is a novel approach to drug development. Our approach to drug development involves applying proven solutions from our extensive global drug development experience to reduce development timelines and expedite the decision-making cycle, planning for success and bridging steps in development by conducting earlier elements of a program while simultaneously planning for later phases of development.

In order to obtain regulatory approval from the FDA to market a drug, certain data about the safety and efficacy of the drug is required by the FDA. To obtain such data, drug developers frequently choose to run studies sequentially. For example, they may run one study, wait to see the results, and then they run the next study. Developers prefer this approach primarily to limit upfront expenditures since the success of any given study is not known and the decision may be made not to move forward due to negative data. This sequential approach slows down the development process.

We approach drug development by minimizing the time it takes to bring products to the market. Our novel approach manages drug development with parallel processing and efficient decision-making. We use our drug development experience to predict possible outcomes of a study and take risks based on those predictions. By assuming success at each critical decision point in advance, as opposed to waiting for results, time is reduced. In addition, we seek to mitigate risks by contingency planning for potential problems. As a result, we can accelerate the development process by bridging steps across the developmental program as well as between studies, as was

5

Table of Contents

evidenced with alogliptin where it took just 39 months from the filing of the Investigational New Drug application, or IND, to the filing of the New Drug Application, or NDA. Additionally, we focus our efforts on only those essential studies necessary for regulatory approval. This helps to shorten developmental timelines.

Two key elements to our approach are our due diligence process and our planning for the success of each compound. Before we enter into a collaboration for a compound, we subject it to an intense due diligence review covering every step in the development process, from preclinical and clinical studies through marketing approval. We generally look for and enter into collaborations with respect to compounds that have the following characteristics:

| • | large market potential; |

| • | a straightforward regulatory path; |

| • | a reasonable development time; |

| • | reasonable predictability of non-clinical models; |

| • | clinical evidence no later than Phase Ib; |

| • | a solid patent estate; |

| • | acceptable estimated cost of goods; and |

| • | attractive economic terms with the compound’s innovator and ultimate commercial collaborator. |

If a compound passes our rigorous diligence review hurdles, we then plan the entire development timeline upfront, using a set of assumptions. Part of the upfront planning involves initiating long-term studies, such as carcinogenicity studies, earlier than usual. We also use real-time data analysis tools to monitor the clinical study data of a drug candidate. By initiating long-term studies earlier and reviewing data in real time, we can significantly reduce the time needed after the conclusion of clinical studies to complete the necessary documentation for regulatory filing.

We believe this approach works well because the core development team is empowered to make decisions, real-time technology tools facilitate rapid data review, development programs are designed to optimize market position, and timelines are driven by science and “must have” studies. The resulting ability to reduce development timelines in turn allows us to capitalize more quickly on our investment. We believe our success evolves from our development efficiency.

According to the Tufts University Center for the Study of Drug Development Outlook 2009, since 2002 the average time from the filing of an IND application to the filing of an NDA is over eight years. By contrast, we advanced alogliptin as a treatment for type 2 diabetes (for the monotherapy program) from IND to NDA in only 39 months.

We believe our over 12 years of development experience has earned us a reputation in the pharmaceutical industry such that pharmaceutical companies approach us as a potential compound collaborator. We believe our most recent partnering project, which we entered into in November 2009 with Janssen-Cilag, evolved from our reputation for success.

Our Business Strategy

Our strategy is to leverage our drug development experience to in-license, develop and out-license novel early stage drug candidates that address medical conditions with large unmet markets. We look to invest in drugs whose targets have scientific or clinical validation, and to study disease indications that have a relatively straightforward path to regulatory approval and a large addressable market. We subject every potential drug candidate we consider to a rigorous due diligence review process by our team, who possess experience in all aspects of the drug development process and commercial and intellectual property assessment. This approach has enabled us to build what we believe is a strong, diversified portfolio of products and product candidates. We plan to continue to build our pipeline by seeking to identify and in-license or acquire promising compounds and by developing strong partnerships in the pharmaceutical and biotechnology sectors.

6

Table of Contents

Our Portfolio

We have three products in clinical development. In addition we have two compounds that are commercialized by collaborators for which we are eligible to receive regulatory milestone payments plus worldwide sales royalty and milestone payments. These compounds, Priligy and Nesina, are currently marketed outside of the United States, and require no further cost or development obligations from us.

Compounds in Clinical Development

MuDelta

Diarrhea-predominant irritable bowel syndrome, or IBS-d, affects approximately 28 million patients in the United States and the five major E.U. countries and is characterized by chronic abdominal pain and frequent diarrhea. Studies have demonstrated that IBS-d is associated with work absenteeism, high medical costs and low quality of life. We believe the market for prescription treatments for IBS-d is underserved due to the limited number of available treatments and the adverse side effects associated with those treatments. MuDelta is a novel agent that we are studying for the treatment of IBS-d. It is a mu-opioid receptor agonist and a delta-opioid receptor antagonist. Pharmacology data suggest that this drug acts locally in the digestive tract, thus we believe it should have a low risk of systemic side effects.

We commenced a Phase II trial for patients with IBS-d in the second quarter of 2010. If enrollment continues as expected, we anticipate having data available during the fourth quarter of 2011.

We have recently achieved two important milestones for this program:

| • | After a planned interim analysis to assess the dose-response and safety of the product, we have elected to continue the study to completion. This analysis was performed by a closed committee and in order to preserve the integrity of the study, we do not plan to disclose the interim results. Although Furiex has elected to continue the study, you should not assume the study will reach its endpoints. |

| • | In January 2011, the FDA granted Fast Track designation to the MuDelta IBS program. Fast Track is a process for facilitating the development and expediting the review of drugs to treat serious diseases and fill an unmet medical need. The purpose is to facilitate bringing important new drugs to the patient earlier. |

In November 2009 we entered into a development and license agreement with Janssen-Cilag under which they have the right to continue development and commercialization of the product after we complete Phase II development. In that case, Janssen-Cilag would bear the expenses for development, manufacture and marketing of the compound after Phase II, and Furiex would be eligible to receive up to $90.0 million in regulatory milestone payments and up to $75.0 million in sales-based milestone payments, as well as sales-based royalty payments increasing from mid-single digit to low initial double digit percentages based on worldwide sales. In the event Janssen-Cilag elects not to continue the program, we have the option to continue developing and commercializing the compound and Janssen-Cilag may receive up to $50.0 million in regulatory milestone payments and up to $75.0 million in sales-based milestone payments, and, if approved for marketing, sales-based royalties increasing from the mid to upper single digit percentages as sales volume increases. Royalties are to be paid for a period of ten years after the first commercial sale or, if later, the expiration of the last valid patent claim or the expiration of patent exclusivity. As of December 31, 2010, we had paid Janssen-Cilag $3.5 million as an up-front in-licensing payment.

According to a market report by GlobalData, the global IBS market was estimated to be worth $1.7 billion in 2009 and forecast to grow at 6.0% annually for the next seven years to reach $2.7 billion by 2017. This estimated growth is primarily attributable to high levels of unmet need in the market, which is expected to be served by pipeline candidates. The growth is further expected to be supported by the high prevalence rates of the disease.

7

Table of Contents

Fluoroquinolone (JNJ-Q2)

Community-acquired bacterial pneumonia, or CABP, and acute bacterial skin and skin structure infections, or ABSSSI, are a growing public-health threat due to increasing drug resistance of established antibiotics to causative pathogens.

JNJ-Q2 is a novel broad-spectrum fluoroquinolone antibiotic that also has broad coverage against two important drug resistant pathogens: methicillin-resistant Staphlococcus (“Staph”) aureus, or MRSA; and drug-resistant Streptococcus pneumoniae. In addition, it is highly active against other common and difficult to treat bacteria, including those that are gram-negative, gram-positive, atypical or anaerobic infections, and has a low propensity for development of drug resistance. We are developing JNJ-Q2 in both intravenous and oral formulations, to enable use in a variety of clinical settings. Taken together, the above characteristics of JNJ-Q2 suggest that it has the potential to be an important agent for the treatment of serious skin and respiratory infections.

In November 2010, we reported positive results for our randomized, double-blind, multicenter Phase II clinical trial comparing the efficacy, safety and tolerability of JNJ-Q2 with linezolid (Zyvox®). The study used a non-inferiority design to test the efficacy of JNJ-Q2 relative to linezolid. One hundred sixty-one patients with ABSSSI received oral treatment twice a day with either JNJ-Q2 (250 mg twice daily) or linezolid (600 mg twice daily) for 7 to14 days.

JNJ-Q2 had positive results for both clinical cure and early response endpoints. Results for the intent-to-treat population are provided herein. JNJ-Q2 was statistically non-inferior to linezolid for all clinical test-of-cure endpoints at various times in the intent-to-treat population. The following clinical cure endpoints are based on clinical assessment by the treating physicians, who were blinded to the study treatment:

| • | At seven days of therapy, 44.6% of patients receiving JNJ-Q2 were assessed as cured, compared with 37.2% of patients receiving linezolid; |

| • | At 10 to 14 days of therapy, 66.3% of patients receiving JNJ-Q2 were assessed as cured, compared with 61.5% of patients receiving linezolid; and |

| • | At the traditional test-of-cure endpoint, namely short-term follow-up done 2 to 14 days after treatment was completed, 83.1% of patients receiving JNJ-Q2 were assessed as cured, compared with 82.1% of patients receiving linezolid. |

In this trial we assessed both (l) cessation of skin lesion spread or reduction in lesion size, and (2) absence of fever. JNJ-Q2 showed a slightly inferior response rate of 74.7% versus linezolid’s 79.5% at 36 to 84 hours after starting treatment. However, we reached statistical non-inferiority in an analysis of the clinical response within 48 to 72 hours after starting treatment, consistent with the latest FDA draft guidance, with a slightly higher response rate for JNJ-Q2 at 62.7% than for linezolid at 57.7%. In this protocol, all patients required at least one systemic sign of infection (e.g, abnormal temperature, increased white blood cell count, etc.) for inclusion in the study. Five percent of patients in the study had baseline temperatures of 100°F or greater.

JNJ-Q2 had a favorable safety profile and was well tolerated. Serious adverse events were infrequent in both treatment groups. Nausea and vomiting were more frequent with JNJ-Q2 than linezolid, however, symptoms were mild for both treatment groups. Nausea rates were 22.9% for JNJ-Q2 and 11.4% for linezolid; vomiting rates were 12.0% JNJ-Q2 and 6.3% for linezolid. The vast majority of these events occurred on day 1 to 2 of treatment. Long-term clinical follow-up data collected 12 weeks after the last dose of medication showed similar low rates of recurrent infections for both treatment groups, 1.2% for JNJ-Q2 and 2.6% for linezolid.

This study represents an important milestone for JNJ-Q2, demonstrating its potential value in the treatment of acute bacterial skin infections, particularly those caused by methicillin-resistant and fluoroquinolone-resistant

8

Table of Contents

Staphlococcus aureus. JNJ-Q2’s demonstrated ability to successfully treat severe skin infections as an oral agent differentiates it from a number of other approved and developmental products for treating MRSA, which are only available for intravenous treatment.

In 2010, there were a number of impactful publications by both Furiex and by Johnson and Johnson Pharmaceutical Research and Development, describing the broad spectrum and potent bactericidal activity of JNJ-Q2 toward a diverse variety of drug-resistant pathogens. Additional studies have demonstrated the low propensity of bacteria to develop resistance to JNJ-Q2 compared with ciprofloxacin, a commonly prescribed quinolone.

We believe that the broad spectrum and potent activity of JNJ-Q2 makes it well suited to a wide variety of indications with large markets. To leverage this significant potential, we initiated a Phase II study in severe community-acquired pneumonia in late 2010. Enrollment of this study has been slower than expected and we have taken steps to increase the rate of enrollment. These steps include adding a number of global sites and potentially modifying the study protocol. Given that these changes will be implemented over the next six months, it will be easier to project the enrollment later in 2011.

In November 2009 we entered into a development and license agreement with Janssen-Cilag, under which Janssen-Cilag has the right to continue development and commercialization of the product after we complete Phase II development. In that case, Janssen-Cilag would bear the expenses for development, manufacture and marketing of the compound after Phase II, and Furiex would be eligible to receive up to $90.0 million in regulatory milestone payments and up to $75.0 million in sales-based milestone payments, as well as sales-based royalty payments increasing from mid-single digit to low initial double digit percentages based on worldwide sales. In the event Janssen-Cilag elects not to continue the program, we have the option to continue developing and commercializing the compound and Janssen-Cilag may receive up to $50.0 million in regulatory milestone payments and up to $75.0 million in sales-based milestone payments, and, if approved for marketing, sales-based royalties increasing from the mid to upper single digit percentages as sales volume increases. Royalties are to be paid for a period of ten years after the first commercial sale or, if later, the expiration of the last valid patent claim or the expiration of patent exclusivity. As of December 31, 2010, we had paid Janssen-Cilag $3.5 million as an up-front in-licensing payment.

Because of the emerging resistance to established antibiotics, there is a large unmet need for antibiotics such as JNJ-Q2, that cover a broad range of pathogens, including resistant Staph and Strep, and that have the potential for both intravenous and oral use. Bacterial infections are a major cause of morbidity and mortality, and antibiotic resistant infections have become a growing public health concern. More than 14 million ambulatory physician visits each year are related to skin and soft-tissue infections, and approximately 94,000 Americans developed serious MRSA infections in 2005, according to a recent study published in the Journal of the American Medical Association. We estimate that the worldwide market for antibiotics to treat MRSA is approximately $2.0 billion annually, based on 2009 sales of $1.14 billion for Zyvox, $538 million for Cubicin®, $303 million for Tygacil® and $185 million for generic vancomycin, which are the products primarily used to treat MRSA. Fluoroquinolone antibiotics generated $7 billion in sales in 2009.

Novel statin compound (PPD-10558)

Our novel statin, which we call PPD-10558, is a potential treatment for dyslipidemia, a condition characterized by high cholesterol. We licensed exclusive rights to PPD-10558 for this indication from Ranbaxy. Ranbaxy retained co-marketing rights for the compound in India, and for generic forms of the compound in countries where such generic forms are already being sold.

Statins are highly-effective therapies for lowering cholesterol leading to prevention of heart attacks and strokes, leading to lower death rates from these potentially devastating events. One of the most common side effects of statins is chronic muscle pain, sometimes associated with weakness, known as statin-associated myalgia, or SAM. Chronic muscle problems are reported to occur in up to 10% of statin users, limiting both their

9

Table of Contents

exercise tolerance as well as their ability to reach their target cholesterol levels. Given that the overall high cholesterol market is estimated to be more than $35 billion, the statin-intolerant population represents a large potential market.

PPD-10558 is a muscle-sparing statin that could be a valuable new therapy for the large population of statin-users who cannot reach their target cholesterol levels due to SAM. Pre-clinical and Phase I human studies demonstrate that PPD-10558 has similar cholesterol-lowering efficacy as atorvastatin (Lipitor®), a best-in-class statin. The pharmacologic and toxicological profile of PPD-10558 suggests that it should have lower risk of muscle-related toxicity than currently marketed statins.

In addition to its muscle-sparing properties, PPD-10558 does not interact with cytochrome P450 metabolizing enzymes, which mitigates the risk of toxic drug interactions that can occur with most other statins. Also, PPD-10558 can be safely used with gemfibrozil, a trigycleride-lowering agent. This is in contrast to several popular statins, which can cause significant toxicity if used concomitantly with gemfibrozil due to significant drug-drug interactions.

A number of pre-clinical studies have previously been conducted to investigate the muscle toxicity of PPD-10558 in comparison to atorvastatin. These studies showed that high doses of atorvastatin cause severe muscle necrosis and death in rats. In contrast, the same dosing regimen of PPD-10558 did not cause any toxicity. We have pre-clinical results that further support our hypothesis that PPD-10558 could be a muscle-sparing statin. In a drug distribution study, rats were treated with high doses of atorvastatin or PPD-10558; drug concentrations in muscle of atorvastatin-treated rats were approximately 40-fold higher relative to drug concentrations in muscle of rats treated with PPD-10558. The findings from these studies suggest that accumulation of atorvastatin in rat muscle tissue is related to muscle toxicity, and the lack of muscle toxicity seen in the rat following dosing of PPD-10558 is consistent with the low levels of PPD-10558 seen in the rat muscle. Taken together, these data support the clinical hypothesis that PPD-10558 could be as effective as atorvastatin, yet with lower risk of muscle side effects.

In December 2010, Furiex had a teleconference with the FDA as well as additional follow-up correspondence. The following points were communicated by the agency: (1) the FDA accepts our Phase II study design, (2) the FDA concurs with Furiex’s development strategy to seek an indication for cholesterol-lowering in patients with SAM, and (3) there is not an expectation that a cardiac outcomes study will be needed. We have finalized the protocol for Phase II proof-of-concept study, which will test whether PPD-10558 is better tolerated by SAM patients than atorvastatin. We are currently recruiting study sites and have received indications of interest from investigators; we anticipate that we will be able to start enrolling patients around mid-2011.

If we further develop PPD-10558 and it were to be approved and commercialized, and it meets specific commercialization and sales milestones, the potential clinical and sales-based milestones that we are obligated to pay Ranbaxy would total $43.0 million. We also would be obligated to pay Ranbaxy sales-based royalties of a mid-single digit percentage. We will be solely responsible and will bear all costs and expenses for the development, manufacture, and marketing of the compound and licensed products. If advanced, we estimate the costs of development could be $15.0 to $20.0 million over the next two years. If we exercise our right to terminate early, other than for safety or efficacy reasons, a material product failure or Ranbaxy breach, we must pay Ranbaxy $1 million. As of December 31, 2010, we had paid Ranbaxy $1.5 million in up-front and development milestone payments.

The American Heart Association estimates that there are more than 35 million adults in the U.S. with total cholesterol greater than or equal to 240 milligrams per deciliter of blood, or mg/dL, and that there are more than 71 million adults in the U.S. with low-density lipoprotein, or LDL, equal to or greater than 130 mg/dL. The American Heart Association has determined that a total cholesterol level of 240 mg/dL and above presents high risk for heart disease and that an LDL level of between 130 and 159 mg/dL presents borderline high risk of heart disease. In 2009, worldwide sales of lipid regulators amounted to $35.3 billion.

10

Table of Contents

Marketed Products

Nesina (alogliptin)

Nesina, which is marketed by Takeda, is the trade name for alogliptin, a member of a relatively new class of drugs for the oral treatment of Type-2 diabetes, or T2D. Nesina is a highly selective dipeptidyl peptidase-4, or DPP-4, inhibitor that slows the inactivation of hormones known as incretins, which play a major role in regulating blood sugar levels and might improve pancreatic function. Pivotal trials demonstrated that Nesina was well-tolerated when given as a single daily dose and it significantly improved glycemic control in T2D patients without raising the incidence of hypoglycemia. Additionally, Nesina has been shown to enhance glycemic control when used in combination with other commonly prescribed diabetes drugs.

In 2003, PPD entered into a collaboration agreement to develop Syrrx’s orally active DPP4 inhibitors to treat type 2 diabetes and other major human diseases. In March 2005, Takeda acquired Syrrx. In July 2005, Takeda acquired development and commercialization rights to these DPP4 inhibitors from PPD for an upfront payment, potential milestone payments and royalties associated with the future development and commercialization of specified DPP4 inhibitors and the right to serve as the sole provider of clinical and bioanalytical services to Takeda for Phase II and Phase III trials of DPP4 inhibitors conducted in the United States and Europe.

In December 2007, Takeda submitted an NDA for alogliptin to the FDA. In September 2008, Takeda submitted an NDA for alogliptin in Japan. In September 2008, Takeda also submitted an NDA for a fixed dose product containing alogliptin and Actos® to the FDA. In June 2009, the FDA issued a complete response to Takeda on its alogliptin NDA. A complete response letter indicates that the review cycle for an application is complete and that the application cannot be approved in its present form, and informs sponsors of changes that must be made before an application can be approved, with no implication as to the ultimate approvability of the application. In the complete response letter, the FDA requested Takeda to conduct an additional cardiovascular safety trial that satisfies the FDA’s December 2008 guidance on anti-diabetes therapies. In September 2009, the FDA issued a complete response to Takeda on its NDA for the fixed dose combination of alogliptin and Actos, stating that further review would be dependent on the cardiovascular safety data that would be submitted in support of the alogliptin monotherapy NDA. This trial is ongoing. The European Medicines Agency, or EMA, issued draft guidance with respect to cardiovascular safety requirements for its Type 2 diabetes drugs on February 10, 2010. Takeda has indicated that it intends to pursue marketing approval of Nesina, Nesina/Actos and Nesina/Metformin both in the United States and Europe, and they anticipate launches in the 2012 and 2013-2014 time frames, respectively.

Nesina received regulatory and pricing approval in Japan during the second quarter of 2010 and for co-administration of Nesina with thiazolidinediones, including Takeda’s Actos (pioglitazone), which is a multi-billion dollar a year product, in August 2010. In February 2011, Takeda reported that the Japanese Ministry of Health, Labour and Welfare approved combination therapy for Nesina with sulfonylureas and combination therapy for Nesina with biguanides.

Under our agreement with Takeda, we will be entitled to receive up to $45.0 million in future regulatory milestone payments, and up to $33.0 million in sales-based milestone payments, if targets are achieved. In addition, we are entitled to receive payments on worldwide sales of Nesina based on royalty rates of 7% to 12% in the U.S., 4% to 8% in Europe and Japan and 3% to 7% in regions other than the U.S., Europe or Japan. These royalty payments are subject to a reduction of up to 0.5% for a portion of payments by Takeda to a licensor for intellectual property related to Nesina. As of December 31, 2010, we had received $55.5 million in development and regulatory milestone payments. Royalties are to be paid for the later of ten years following the first commercial sale or two years following the expiration of the last to expire patent.

11

Table of Contents

The Centers for Disease Control and Prevention estimates that there are approximately 25.8 million people in the U.S. with type 1 and type 2 diabetes. The World Health Organization estimates that more than 170 million people worldwide have type 1 and type 2 diabetes and that the number will double by 2030. Worldwide sales of antidiabetic treatments in 2009 were $30.4 billion.

In addition to all the rights to receive milestone payments and royalties, Furiex received from PPD the following material rights and/or obligations:

| • | to indemnify Takeda for various claims and losses arising out of or under the agreement; and |

| • | to not discover, develop, or commercialize any product directed to the DPP4 inhibitors. |

Priligy (dapoxetine)

Priligy is the trade name for dapoxetine, a drug in tablet form specifically indicated for the “on-demand” treatment of premature ejaculation, or PE. Priligy is a unique, short-acting, selective serotonin reuptake inhibitor, or SSRI, designed to be taken only when needed, one to three hours before sexual intercourse, rather than every day. It is the first oral medication to be approved for PE anywhere in the world, and no products are currently approved for the treatment of premature ejaculation in the United States. The reported percentage of men affected with PE at some point during their lives ranges from 4% to 30%, depending on the methodology and criteria used. Priligy has been studied in five randomized, placebo-controlled Phase III clinical trials involving more than 6,000 men with PE and is marketed in 14 countries in Europe, Asia-Pacific and Latin America. In December 2004, Janssen-Cilag, an affiliate of ALZA, submitted an NDA to the FDA for dapoxetine. Janssen-Cilag received a “not approvable” letter from the FDA in October 2005, but continued its global development program. Janssen-Cilag is conducting additional studies with Priligy in the United States and abroad.

PPD acquired an exclusive license from Eli Lilly and Company in 1998 to develop and commercialize dapoxetine for genitourinary indications, including premature ejaculation. In December 2003, PPD acquired Lilly’s patents and remaining rights to develop and commercialize dapoxetine in the field of genitourinary disorders. PPD developed the compound through Phase II proof-of-concept and, in January 2001, out-licensed it to ALZA, which is now part of Johnson & Johnson. ALZA is responsible for all clinical, regulatory, manufacturing, sales and marketing costs associated with the compound. As of December 31, 2010, we had received $35.9 million in combined development and regulatory milestone payments. Under our license agreement with ALZA, we have the right to receive up to $15.0 million in additional regulatory milestone payments, up to $50.0 million in sales-based milestone payments, and sales-based royalties ranging from 10% to 20% for sales of patented products without generic competition and ranging from 10% to 17.5% for non-patented products without generic competition, in both cases the percentages rise as sales volume increases, and a royalty of 7.5% for patented and non-patented products with generic competition regardless of sales volume based on the level of Priligy sales worldwide. We must pay Lilly a royalty of 5% on annual sales in excess of $800.0 million.

ALZA has worldwide rights to develop and commercialize dapoxetine. In addition to all the rights to receive milestone payments and royalties, Furiex has the following material rights and/or obligations:

| • | to prosecute patent applications and maintain granted patents, and allow ALZA to comment on such prosecution; |

| • | to notify ALZA of any actual, potential or suspected infringement of licensed patents by a third party of which Furiex becomes aware and of any claim of infringement of a third party’s proprietary rights of which Furiex receives notice with regard to the license grant; |

| • | to not publish any data regarding dapoxetine; |

| • | to not assert any patent or other intellectual property right owned by the Company against ALZA; |

| • | to indemnify ALZA for various claims and losses arising out of or under the agreement; |

12

Table of Contents

| • | to defend licensed patents against infringers (in the event ALZA does not desire to defend) and be entitled to all recoveries, damages or awards if it defends. |

Our Drug Development Capabilities

Our drug development capabilities embody over 12 years of research and development experience. This experience includes a deep understanding of the biological causes of human diseases and the factors that impact all aspects of successful drug development such as manufacturing, formulation, the cause of drug side effects, drug interactions and drug pharmacokinetics. We believe that our drug development capability and proven success rate will continue to provide a pipeline of unique compounds. Depending upon the availability of our development resources, our preclinical candidates might be added to our own internal clinical pipeline, or out-licensed to other companies for clinical development and commercialization.

Our Patents and Other Proprietary Rights

Patents and other proprietary rights are important to our business. It is our policy to seek patent protection for our assets, and also to rely upon trade secrets, know-how and licensing opportunities to develop and maintain our competitive position.

We own or have exclusively licensed six issued U.S. patents and have approximately 290 pending patent applications. We have a policy to seek worldwide patent protection for our products and have foreign patent rights corresponding to most of our U.S. patents.

On May 18, 2010, the United States Patent and Trademark Office, or USPTO, issued a patent for the method for treatment of premature ejaculation using dapoxetine (trademark Priligy). U.S. Patent No. 7,718,705 includes claims directed to dosing dapoxetine on an as-needed basis, capturing the advantage dapoxetine has over other compounds in the same class, which require a pre-loading period for efficacy. The patent term will expire in 2022. Furiex has received grants of similar patent claims in over 45 countries around the world including major and emerging markets.

We license the rights to the following patents related to our product candidates:

| • | PPD-10558. Licensed from Ranbaxy. The license expires 10 years after the first commercial sale or expiration of the last to expire enforceable patent claim. As of December 31, 2010, nine U.S. and foreign patents have been issued to Ranbaxy in this patent family. The USPTO issued a Notice of Allowance of claims covering the PPD-10558 compound. This patent has also received a patent term adjustment from the USPTO that extends the patent term to 2026. Corresponding foreign patent applications and additional U.S. and foreign patent applications are still pending; |

| • | MuDelta. Licensed from Janssen-Cilag. The license expires upon the exercise of an option by Janssen to continue the development and commercialization of MuDelta after completion of Phase II studies. If Janssen rejects the option, then the license continues until no further payments are owed to Janssen. As of December 31, 2010, over 10 U.S. and foreign patents have been issued to Janssen in this patent family. Additional U.S. and foreign patent applications are still pending; and |

| • | Fluoroquinolone. Licensed from Janssen-Cilag. The license expires upon the exercise of an option by Janssen to continue the development and commercialization of fluoroquinolone after completion of Phase II studies. If Janssen rejects the option, then the license continues until no further payments are owed to Janssen. As of December 31, 2010, over 30 U.S. and foreign patents have been issued to Janssen in this patent family. Additional U.S. and foreign patent applications are still pending. |

Pursuant to the terms of the Uruguay Round Agreements Act, patents issued from applications filed on or after June 8, 1995, have a term of 20 years from the date of filing, no matter how long it takes for the patent to

13

Table of Contents

issue. Because patent applications in the pharmaceutical industry often take a long time to issue, this method of patent term calculation can result in a shorter period of patent protection afforded to us compared to the prior method of term calculation, which was 17 years from the date of issue. Our issued U.S. patents expire between 2023 and 2029, excluding any potential patent term extension available under U.S. federal law. We actively seek full patent term adjustment following allowance of a patent. We also actively seek patent term extensions covering products following marketing approval. Under the Drug Price Competition and Patent Term Restoration Act of 1984 and the Generic Animal Drug and Patent Term Restoration Act of 1988, a patent that claims a product, use or method of manufacture covering drugs may be extended for up to five years to compensate the patent holder for a portion of the time required for FDA review. However, we might not be able to take advantage of the patent term extension provisions of this law.

While we file and prosecute patent applications to protect our inventions, our pending patent applications might not result in the issuance of patents or our issued patents might not provide competitive advantages. Also, our patent protection might not prevent others from developing competitive products using related or other technology.

In addition to seeking the protection of patents and licenses, we also rely upon trade secrets, know-how and continuing technological innovation, which we seek to protect, in part, by confidentiality agreements with employees, consultants, suppliers and licensees. If these agreements are not honored, we might not have adequate remedies for any breach. Additionally, our trade secrets might otherwise become known or patented by our competitors.

The scope, enforceability and effective term of issued patents can be highly uncertain and often involve complex legal and factual questions. No consistent policy has emerged regarding the breadth of claims in pharmaceutical patents, so that even issued patents might later be modified or revoked by the relevant patent authorities or courts. Moreover, the issuance of a patent in one country does not assure the issuance of a patent with similar claim scope in another country, and claim interpretation and infringement laws vary among countries, so we are unable to predict the extent of patent protection in any country. The patents we obtain and the unpatented proprietary technology we hold might not afford us significant commercial protection. Additional information regarding risks associated with our patents and other proprietary rights that affect our business is contained under the headings “We must protect our patents and other intellectual property rights to succeed” and “We might need to obtain patent licenses from others in order to manufacture or sell our potential products and we might not be able to obtain these licenses on terms acceptable to us or at all” under the heading “Risk Factors”.

Manufacturing and Supply

We currently rely on our collaborators and contract manufacturers to produce drug substances and drug products required for our clinical trials under current good manufacturing practices, with oversight by our internal managers. We plan to continue to rely upon contract manufacturers and collaboration partners to manufacture commercial quantities of our drug candidates if and when approved for marketing by the applicable regulatory agency. We generally rely on one manufacturer for the active pharmaceutical ingredient and another manufacturer for the formulated drug product for each of our drug candidate programs. At the early stage of clinical studies, we do not believe that we are substantially dependent on any supplier, or that additional manufacturers would be beneficial due the possibility of changes in the method of manufacturing of the drug candidate. As a drug candidate moves to later stages of development and the drug formulation method is established, we then seek additional manufacturers for the drug.

Sales and Marketing

We currently have no marketing, sales or distribution capabilities. We plan to rely on third party collaborators to market our products, like ALZA for Priligy and Takeda for Nesina, and therefore we are subject to the strategic marketing decisions of such third parties. We generally plan to out-license our commercial rights

14

Table of Contents

in a territory to a third party with marketing, sales and distribution capabilities in exchange for one or more of the following: up-front payments; research funding; development funding; milestone payments; and royalties on drug sales. In some instances, however, we might choose to develop our own staff for marketing, sales or distribution.

Government Regulation

The manufacturing, testing, labeling, approval and storage of our products are subject to rigorous regulation by numerous governmental authorities in the United States and other countries at the federal, state and local level, including the FDA. The process of obtaining approval for a new pharmaceutical product or for additional therapeutic indications within this regulatory framework requires expenditure of substantial resources and usually takes several years. Companies in the pharmaceutical and biotechnology industries, including us, have suffered significant setbacks in various stages of clinical trials, even in advanced clinical trials after promising results had been obtained in earlier trials.

The process for obtaining FDA approval of drug candidates customarily begins with the filing of an IND with the FDA for the use of a drug candidate to treat a particular indication. If the IND is accepted by the FDA, we would then start human clinical trials to determine, among other things, the proper dose, safety and efficacy of the drug candidate in the stated indication. The clinical trial process is customarily divided into three phases—Phase I, Phase II and Phase III. Each successive phase is generally larger and more time-consuming and expensive than the preceding phase. Throughout each phase we are subject to extensive regulation and oversight by the FDA. Even after a drug is approved and being marketed for commercial use, the FDA may require that we conduct additional trials, including Phase IV trials, to further study safety or efficacy.

As part of the regulatory approval process, we must demonstrate to the FDA the ability to manufacture a pharmaceutical product before we receive marketing approval. We and our manufacturing collaborators must conform to rigorous standards regarding manufacturing and quality control procedures in order to receive FDA approval. The validation of these procedures is a costly endeavor. Pharmaceutical manufacturers are subject to inspections by the FDA and local authorities as well as inspections by authorities of other countries. To supply pharmaceutical products for use in the United States, foreign manufacturers must comply with these FDA-approved guidelines. These foreign manufacturers are also subject to periodic inspection by the FDA or by corresponding regulatory agencies in these countries under reciprocal agreements with the FDA. Moreover, state, local and other authorities may also regulate pharmaceutical product manufacturing facilities. Before we are able to manufacture commercial products, we or our contract manufacturer, as the case may be, must meet FDA guidelines.

Both before and after marketing approval is obtained, a pharmaceutical product, its manufacturer and the holder of the Biologics License Application, or BLA, or NDA for the pharmaceutical product are subject to comprehensive regulatory oversight. The FDA may deny approval to a BLA or NDA if applicable regulatory criteria are not satisfied. Moreover, even if regulatory approval is granted, such approval may be subject to limitations on the indicated uses for which we may market the pharmaceutical product. Further, marketing approvals may be withdrawn if compliance with regulatory standards is not maintained or if problems with the pharmaceutical product occur following approval. In addition, under a BLA or NDA, the manufacturer of the product continues to be subject to facility inspections and the applicant must assume responsibility for compliance with applicable pharmaceutical product and establishment standards. Violations of regulatory requirements at any stage may result in various adverse consequences, which may include, among other adverse actions, withdrawal of the previously approved pharmaceutical product or marketing approvals or the imposition of criminal penalties against the manufacturer or BLA or NDA holder.

For the development of pharmaceutical products outside the United States, we and our collaborators are subject to foreign regulatory requirements and the ability to market a drug is contingent upon receiving marketing authorizations from the appropriate regulatory authorities. The requirements governing the conduct of

15

Table of Contents

clinical trials and marketing authorization vary widely from country to country. In countries other than European Union countries, foreign marketing authorizations are applied for at a national level. Within the European Union, procedures are available to companies wishing to market a product in more than one European Union member state. Clinical trial applications must be filed with the relevant regulatory authority in each country in which we would want to conduct a clinical trial. Assuming approval and the success of any clinical trial, we would then need to seek marketing approval for the drug. The process for obtaining marketing approval of drug candidates in the European Union begins with the filing with the European Medicines Agency, or EMA, of a Marketing Authorization Application, or MAA, for the use of a drug candidate to treat a particular indication. Similar processes and outcomes of such human clinical trials that are required by the FDA are also required by the EMA including testing for dose, safety and efficacy in three phases. Similar to the FDA, we are subject to extensive regulation and oversight by the European regulators throughout each phase. Even after a drug is approved and being marketed for commercial use, the EMA may require that we conduct additional trials, including Phase IV trials, to further study safety or efficacy. As a result, the EMA regulatory approval process includes all of the risks associated with FDA approval set forth above.

If and when necessary, we will choose the appropriate route of European or other international regulatory filing to accomplish the most rapid regulatory approvals. Requirements relating to manufacturing, conduct of clinical trials and product licensing vary widely in different countries, and the chosen regulatory strategy might not secure regulatory approvals or approvals of our chosen product indications. In addition, if a particular product to be used outside of the United States is manufactured in the United States, FDA requirements and U.S. export provisions will apply.

Outside of the United States, many countries require us to obtain pricing approval in addition to regulatory approval prior to launching the product in the approving country. We or our licensees may encounter difficulties or unanticipated costs or price controls in our respective efforts to secure necessary governmental approvals. Failure to obtain pricing approval in a timely manner or approval of pricing which would support an adequate return on investment or generate a sufficient margin to justify the economic risk might delay or prohibit the commercial launch of the product in those countries.

The marketing and sale of approved pharmaceutical product is subject to strict regulation. Promotional materials and activities must comply with the approving agency’s regulations and other guidelines. Physicians may prescribe pharmaceutical or biologic products for uses that are not described in a product’s labeling or differ from those approved by the approving agency. While such “off-label” uses are common and regulatory agencies do not regulate physicians’ choice of treatments, many approving agencies restrict a company’s communications on the subject of “off-label” use. Companies cannot promote approved pharmaceutical or biologic products for off-label uses. If any advertising or promotional activities we undertake fail to comply with applicable regulations or guidelines regarding “off-label” use, we may be subject to warnings or enforcement action.

Competition

The pharmaceutical industry is highly competitive. Many of our competitors are worldwide conglomerates with substantially greater resources than we have to develop and commercialize their drugs and drug candidates. Potential competitors have developed and are developing compounds for treating the same indications as our product candidates. In addition, a number of academic and commercial organizations are actively pursuing similar technologies, and several companies have developed or may develop technologies that might compete with our compounds.

Priligy, indicated for premature ejaculation, competes with Cromadyn, a generic paroxetine sold by More Pharmaceuticals in Mexico. We are aware of three other compounds in development for premature ejaculation: PD502, a novel metered-dose aerosol formulation of lidocaine and prilocaine being developed by Shionogi; DMI-7958, a opioid mu receptor agonist, 5-HT receptor agonist, being developed by Ampio Pharma, and GSK-557296, a oxytocin receptor antagonist, being developed by GSK. All of these products are in late stage (Phase II/III) development.

16

Table of Contents

Nesina competes in the type 2 diabetes space with two DPP4 inhibitors currently on the market, Bristol-Myers Squibb/AstraZeneca’s Onglyza® (saxagliptin) and Merck’s Januvia® (sitagliptin). Merck also markets Janumet®, a fixed-dose combination of sitagliptin and metformin and Bristol-Myers Squibb/AstraZeneca, Kombiglyze®, a combination of saxagliptin and extended release metformin. Novartis markets the DPP4 inhibitor Galvus® (vildagliptin) and Eucreas® (vildagliptin/metformin) in Europe. Other marketed oral anti-diabetic competitors include generic metformin, generic sulfonylureas, and thiazolidinediones, including GlaxoSmithKline’s Avandia® (rosiglitazone) and Takeda’s Actos (pioglitazone). Generic competitors to Avandia and Actos are expected to enter the market in 2012.

The diabetes pipeline is crowded, with, to our knowledge, approximately 50 compounds in Phase I development, approximately 70 in Phase II development, and approximately 30 in Phase III development or preregistration. In addition to DPP4 inhibitors, competitors are also developing GLP-1 agonists, SGLT-2 antagonists, PPAR agonists, and compounds with other mechanisms for treatment of diabetes. Other companies with DPP4 inhibitors in clinical development of which we are aware include Amgen/Servier, Arisaph Pharmaceuticals, Boehringer Ingelheim, Dong-A Pharmaceuticals (South Korea), Dainippon Sumitomo Pharma, Phenomix, Glenmark Pharmaceuticals, Kyorin Pharmaceuticals, LG Life Sciences (South Korea), Mitsubishi Tanabe Pharma, and Sanwa Kagaku Kenkyusho (Japan). In addition, Merck is developing a fixed-dose combination of sitagliptin and pioglitazone (Actos), currently in Phase III development.

If approved, PPD-10558, indicated for the treatment of dyslipidemia, would compete with a wide variety of lipid lowering drugs. Generic statins are expected to dominate the market by 2012 when Pfizer’s Lipitor® (atorvastatin) patent expires. PPD-10558 may be differentiated from these products if it is proved to be safe in patients who cannot tolerate currently marketed statins due to muscle pain symptoms. There are several competing statins and statin combination products in development, including AstraZeneca/Abbott’s Certriad® (rosuvastatin/fibrate), Merck’s MK-0524A (laropiprant/niacin/simvastatin), Sciele Pharma’s fenofibrate/pravastatin combination, Abbott/Solvay’s Zolip® (fenofibrate/simvastatin), and NicOx’s NCX-6560, a novel statin. Companies developing compounds with other mechanisms of action for use in hyperlipidemia of which we are aware include Aegerion Pharmaceuticals, Amarin Corporation, Bristol-Myers Squibb, Cortria Corporation, Dr. Reddys Laboratories, Esperion Therapeutics, Essentialis, Genfit, GlaxoSmithKline, Isis Pharmaceuticals/Genzyme, Japan Tobacco, Karo Bio, Kythera Biopharmaceuticals, The Medicines Company, Merck, Metabasis Therapeutics, Metabolex, Mitsubishi Tanabe Pharma, Sanofi-Aventis, and Surface Logix.

If approved, the fluoroquinolone antibiotic compound licensed from Janssen-Cilag will compete with other fluoroquinolones currently on the market, including Johnson and Johnson’s Levaquin® (levofloxacin), Bayer/Merck’s Avelox® (moxifloxacin), Bayer/Merck’s Cipro® (ciprofloxacin), and Oscient’s Factive® (gemifloxacin). Generic versions of ciprofloxacin are currently available, and generic versions of moxifloxacin and levofloxacin will likely become available when the patents covering these products expire in 2014 and 2011, respectively. If the fluoroquinolone from Janssen-Cilag is found to be effective against MRSA infections, it would compete with Pfizer’s Zyrox® (linezolid), Cubist’s Cubicin (daptomycin), Wyeth’s Tygacil (tigecycline), Theravance’s Vibativ® (telavancin), Forest’s Teflro™ (ceftaroline), and the generic drug vancomycin.

Companies developing compounds to treat MRSA infections in clinical trials include Baselia, Trius, Paratek/Novartis, Cempra, Durata, e-Therapeutics, FAB Pharma, Medicines Company, Novexel (now AstraZeneca), Phico Therapeutics, PolyMedix, Rib-X Pharmaceuticals, TaiGen, Theravance, and Wockhardt (India). The Rib-X and Wockhardt compounds are both fluoroquinolones. In addition, MerLion Pharmaceuticals is developing a fluoroquinolone in Phase II. Merck and Nabi Biopharmaceuticals are both developing vaccines against staphylococcus aureus.

If approved, the MuDelta compound, also licensed from Janssen-Cilag, will compete with Lotronex® (alosetron), marketed by Prometheus Laboratories, and over-the-counter treatments for diarrhea-predominant irritable bowel syndrome (IBS) such as loperamide (Imodium®). The pipeline for diarrhea-predominant IBS includes: asimadoline, which is being developed by Tioga Pharmaceuticals and is entering Phase III;

17

Table of Contents

mesalamine, currently in Phase II, crofelemer, currently in Phase III and rifaximin, an approved product subject of an sNDA, by Salix Pharmaceuticals; AST-120, currently in Phase II development by Ocera; ibodutant, currently in Phase II development by Menarini Group; YM060, currently in Phase II development by Astellas Pharma; dextofisopam, currently in Phase II development by Pharmos Corporation; and LX1031, currently in Phase II development by Lexicon Pharmaceuticals.

Competitors might succeed in more rapidly developing and marketing technologies and products that are more effective than our products or that would render our products or technology obsolete or noncompetitive. Our collaborators might also independently develop products that are competitive with products that we have licensed to them. Any product that we or our collaborators succeed in developing and for which regulatory approval is obtained must then compete for market acceptance and market share. The relative speed with which we and our collaborators can develop products, complete clinical testing and approval processes, and supply commercial quantities of the products to the market compared to competitive companies will affect market success. In addition, the amount of marketing and sales resources, and the effectiveness of the marketing used with respect to a product will affect its success. In addition, some CRO services providers and private equity funds are developing risk sharing models to finance the pharmaceutical industry’s pipeline. NovaQuest, a subsidiary of Quintiles Transnational, is active in this business. As these types of business models evolve, there will be increasing competition for compounds and funds that will affect our ability to add to our portfolio.

Other competitive factors affecting our business generally include:

| • | product efficacy and safety; |

| • | timing and scope of regulatory approval; |

| • | product availability, marketing and sales capabilities; |

| • | reimbursement coverage; |

| • | the amount of clinical benefit of our product candidates relative to their cost; |

| • | method of and frequency of administration of any of our product candidates which may be commercialized; |

| • | patent protection of our product candidates; |

| • | the capabilities of our collaborators; and |

| • | the ability to hire qualified personnel. |

Employees

We have approximately 25 full-time employees, a majority of whom are engaged in research and development activities. Our success depends in large part on our ability to attract and retain skilled and experienced employees. None of our employees is covered by a collective bargaining agreement. We consider our relations with our employees to be good.

| Item 1A. | Risk Factors |

Our business operations face a number of risks. These risks should be read and considered with other information provided in this report.

Risks Relating to Furiex’s Business

We anticipate that we will incur additional losses. We might never achieve or sustain profitability. If additional capital is not available, we might have to curtail or cease operations.

Our business has experienced significant net losses. We had net income of $5.8 million in 2008, and a net loss of $8.9 million and $54.7 million in 2009 and 2010, respectively. The results for 2008, 2009 and 2010

18

Table of Contents

included aggregate milestone payments of $18.0 million, $5.0 million, and $7.5 million, respectively. We expect to continue to incur additional net losses as we continue our research and development activities and incur significant preclinical and clinical development costs. Since we or our collaborators or licensees might not successfully develop additional products, obtain required regulatory approvals, manufacture products at an acceptable cost or with appropriate quality, or successfully market products with desired margins, our expenses might continue to exceed any revenues we receive. Our commitment of resources to the continued development of our products might require significant additional funds for development. Our operating expenses also might increase if we:

| • | move our earlier stage potential products into later stage clinical development, which is generally a more expensive stage of development; |

| • | encounter problems during clinical development that require a change in scope and/or timelines resulting in higher costs; |

| • | select additional preclinical product candidates for preclinical development and then clinical development; |

| • | pursue clinical development of our potential products in new indications; |

| • | increase the number of patents we are prosecuting or otherwise expend additional resources on patent prosecution or defense; |

| • | invest in or acquire additional technologies, product candidates or businesses although we have no current agreements to do so; or |

| • | impair any of our investments in our product candidates. |

In the absence of substantial licensing, milestone and other revenues from third-party collaborators, royalties on sales of products licensed under our intellectual property rights, future revenues from our products in development or other sources of revenues, we will continue to incur operating losses and might require additional capital to fully execute our business strategy. The likelihood of reaching, and time required to reach, sustained profitability are highly uncertain.

Although we expect that we will have sufficient cash to fund our operations and working capital requirements for at least the next 12 months based on current operating plans, we might need to raise additional capital in the future to:

| • | acquire complementary businesses or technologies; |

| • | respond to competitive pressures; |

| • | fund our research and development programs; or |

| • | commercialize our product candidates. |

Our future capital needs depend on many factors, including:

| • | the scope, duration and expenditures associated with our research and development programs; |

| • | continued scientific progress in these programs; |

| • | the outcome of potential licensing transactions, if any; |

| • | competing technological developments; |

| • | our proprietary patent position, if any, in our product candidates; |

| • | the regulatory approval process for our product candidates; and |

| • | the cost of attracting and retaining employees. |

19

Table of Contents

We might seek to raise necessary funds through public or private equity offerings, debt financings or additional collaborations and licensing arrangements. We might not be able to obtain additional financing on terms favorable to us, if at all. General market conditions might make it difficult for us to seek financing from the capital markets. We might have to relinquish rights to our technologies or product candidates, or grant licenses on terms that are not favorable to us, in order to raise additional funds through collaborations or licensing arrangements. If adequate funds are not available, we might have to delay, reduce or eliminate one or more of our research or development programs and reduce overhead expenses, or restructure or cease operations. These actions might reduce the market price of our common stock.

Our near-term revenue is largely dependent on the success of Priligy and Nesina as well as our other drug candidates, and we cannot be certain that we will be able to obtain regulatory approval for or commercialize any of these drug candidates.

We currently are relying on Priligy and Nesina to generate revenue for us to supplement our cash. While Priligy is approved for marketing outside of the U.S., it has not been approved in the U.S. and the FDA issued a not approvable letter to our collaborative partner Janssen-Cilag in October 2005. Janssen-Cilag is investigating regulatory strategies for a potential refiling with the FDA. Takeda, our collaborative partner on Nesina must perform a cardiovascular safety trial for alogliptin and does not expect results from that trial to be available for submission to the FDA for approximately two years after that trial began. We have also invested a significant amount of time and financial resources in the development of fluoroquinolone. FDA guidance for developing drugs to treat community acquired bacterial pneumonia includes challenging requirements for the drug developer. Our future success will depend on our ability to successfully complete the clinical trial for this pneumonia indication using our fluoroquinolone in view of the FDA guidelines. We have also invested a significant amount of time and financial resources in the development of our other drug candidates. We anticipate that our success will depend largely on the receipt of regulatory approval and successful commercialization of these drug candidates. The future success of these drug candidates will depend on several factors, including the following:

| • | our ability to provide acceptable evidence of their safety and efficacy; |

| • | receipt of marketing approval from the FDA and any similar foreign regulatory authorities; |

| • | obtaining and maintaining commercial manufacturing arrangements with third-party manufacturers or establishing commercial-scale manufacturing capabilities; |

| • | collaborating with pharmaceutical companies or contract sales organizations to market and sell any approved drug; |

| • | acceptance of any approved drug in the medical community and by patients and third-party payors; and |

| • | successful completion of the alogliptin cardiovascular safety trial that generates safety data acceptable to the FDA. |

Many of these factors are beyond our control. Accordingly, we cannot assure you that we will be able to continue generating revenues through the sale of Priligy or Nesina or generate any revenue from the sale of other drug candidates.

Our milestone and royalty payments from collaborators depend on our collaborators continuing to develop and commercialize drug candidates.

Our ability to succeed in our drug development business will depend on our collaborators successfully executing late-stage development and commercialization of drug candidates. We generally conduct our drug development business in two stages. During the first stage, we in-license a drug candidate from a collaborator and develop that candidate through Phase II clinical trials. If the drug candidate successfully completes Phase II testing, we enter a second stage during which we seek a collaborator, which might be the same collaborator as in the first stage, for the continued late stage development and ultimate commercialization of the drug candidate.

20

Table of Contents

The drug development industry is under increasing economic pressure. The third parties that we collaborate with might not perform their obligations as expected or they might breach or terminate their agreements with us or otherwise fail to conduct their collaborative activities successfully or in a timely manner. Further, parties collaborating with us might elect not to develop the product candidates or devote sufficient resources to the development, manufacture, regulatory strategy and approvals, marketing or sale of these product candidates. If the parties to our collaborative agreements do not fulfill their obligations, elect not to develop a candidate or fail to devote sufficient resources to it, our business could be materially and adversely affected. If we cannot find a collaborator for final development and commercialization, we might not be able to complete the development and commercialization on our own due to the significant costs associated with these activities. As a result, we may not be able to recoup all or any part of our investment in the drug candidate.

If our collaborations are not successful or are terminated by our collaborators, we might not effectively develop and market some of our product candidates.