Attached files

EXHIBIT 13 – REGISTRANT’S ANNUAL REPORT TO SHAREHOLDERS

The First National Bank of Long Island

Where Everyone Knows Your Name ®

Balance + Momentum

2010 Annual Report

[PHOTO OMITTED]

[LOGO]

The First of Long Island Corporation

[PHOTO OMITTED]

Table of Contents

|

2-3

|

President & CEO Message

|

|

4

|

Board of Directors & Executive Officers

|

|

5

|

Financial Strength

|

|

6

|

Loan Growth & Asset Quality

|

|

7

|

Branch Expansion

|

|

8-9

|

New Branches

|

|

10-11

|

Branch Location Map

|

|

12

|

Disaster Recovery Center

|

|

13

|

Community Outreach

|

|

14

|

Selected Financial Data

|

|

15-65

|

Financials

|

|

66

|

Officers & Official Staff

|

|

67

|

Business Advisory Board

|

2010 Financial Highlights

|

|

·

|

Net income was $18.4 million, up 37%, or $4.9 million versus 2009

|

|

|

·

|

Earnings per share were $2.30, up 25%, or $.46 per share versus 2009

|

On an average balance basis:

|

|

·

|

Total assets were $1.66 billion, up 17%, or $244 million versus 2009

|

|

|

·

|

Loans were $864 million, up 21%, or $148 million versus 2009

|

|

|

·

|

Deposits were $1.3 billion, up 19%, or $209 million versus 2009

|

|

|

·

|

Residential Mortgages were $291 million, up 30%, or $66 million versus 2009

|

|

|

·

|

Commercial Mortgages were $409 million, up 29%, or $92 million versus 2009

|

1

A Message from the President & CEO

[PHOTO OMITTED]

Dear Shareholder:

It gives me great pride to report to you that as of year end 2010, The First National Bank of Long Island was the largest independent commercial bank headquartered on Long Island. On an average balance basis, the Bank’s total assets grew $244 million, or 17.2%, during 2010. Profits were at a historic high of $18.4 million, an increase of almost 37% over 2009. On a per share basis, we were up 46 cents, or 25%. We improved our returns on average assets and average equity, which were 1.11% and 12.94%, respectively, in 2010 compared to .95% and 12.15%, respectively, for last year. More importantly, this was the third year in a row our stock price appreciated. Using year end measurement dates, the compounded annual growth rate of our stock price over the last three years was 15.74%. In 2010, our dividend increased by 8 cents per share, or 10.5%. We continued to increase our dividend at a double digit rate because of the confidence we have in our earnings power. Our positioning within the market is gaining momentum and our future remains bright. We are proud of the many accomplishments of our organization.

There are many reasons for the Bank’s positive performance, the most significant being our corporate culture of balance and discipline. The growth of the institution over the last five years has been built upon the foundation of meticulous attention to the risks associated with the business, namely liquidity, interest rate and, most of all, credit risk. Regardless of the temptation for instant gratification, we have remained measured and disciplined with our underwriting standards, our loan review process, and the selection of investment securities; and after we have checked it twice, we do not hesitate to check it again. Our securities portfolio of over $700 million remains our first line of defense as a liquidity cushion. This cushion is backed by the placement of loans and securities at the Federal Reserve Bank and the Federal Home Loan Bank of New York that gives us a borrowing capacity of approximately $700 million. We have, by all accounts, tremendous funding capacity if needed. We have used this capacity sparingly as the Management Team has been able to organically grow deposits at a comfortable double digit rate. In 2010, on an average balance basis, our deposits grew $209 million, or 19%, which funded the growth of our balance sheet. More importantly, our average Checking Deposits grew by $39.3 million, or 11.7%. Growth in Checking Deposits was primarily driven by our market share penetration associated with small business and middle market customers, a valuable and lucrative market segment. We remain dedicated to growing the institution organically, and building the franchise stone by stone.

The First National Bank of Long Island is becoming a unique banking organization that is developing its brand and reputation based on unparalleled customer service. What differentiates us is a culture dedicated to personalizing our service quality approach. We believe the only long-term sustainable competitive advantage we have in the marketplace is the level of service we deliver. This is the overriding fulcrum of our success.

Our history dates back to 1927 and 2011 will be our 84th year of serving the Long Island marketplace. Over the last seven years we have built 14 new branches and converted two commercial banking units into full service branches. This growth represents an increase of 70% to the branch distribution system. With each and every new branch location, we have been able to hire individuals dedicated to the principle of service quality and personalization. With each and every hire of a new commercial banker or new commercial lender, we have attracted a high degree of professional talent as well as an individual who can fit into the culture we are building. As we expand into new markets on Long Island, each newly hired individual and each new branch location work to enhance our reputation and recognition of our brand of banking within the geography. We pride ourselves in knowing every one of our customers, both from a business and personal perspective. That is why we call ourselves the Bank “Where Everyone Knows Your Name.” The Bank is gaining momentum as a recognizable Long Island institution, attracting many new customers, and significantly increasing our market share within one of the most affluent geographies in the country. We will open our 35th branch by this summer.

As we continue to build talent and add branches, our franchise value grows, benefitting our shareholders. The case in point is that over the last two years our Bank has been able to establish relationships with over 100 upper-end small businesses and middle market customers. This increase of market share is a significant part of our deposit growth and exactly the kind of business we want to attract to enhance the future prospects of our stock price. Our momentum is building and has not been interrupted by credit quality concerns.

Our credit quality remains excellent, not only with our loans, but also with our securities. At December 31, 2010, we had only four nonaccruing loans which represent .44% of our total loans. Net chargeoffs in 2010 were four basis points of average loans. We have no more than a handful of delinquencies, almost all of which are 30-day items. Although no one can predict what the future holds, the balance sheet of The First National Bank of Long Island remains among the strongest in the country. We are determined to continue our measured and disciplined approach in booking new earning assets.

In the short term, we do not have plans to redirect tactics. Our strategic initiatives remain the same. We continue to change the composition of our earning assets from securities to loans to enhance our earnings prospects. We are confident loan growth will drive our deposit balances and corresponding franchise value. Our target markets remain consistent: lower middle market companies, small businesses, professionals, and service conscious affluent consumers. We will keep building branch locations in micro-markets we presently do not service, which inevitably will add to the enhancement and recognition of our reputation and brand of banking. Commensurate with our good fortune and success, we have been receiving more calls and interest from the marketplace, both in terms of new business prospects who desire real relationship banking and individual bankers who want to associate themselves with a growing and well disciplined organization. It is our intent to choose the best from both of these categories, and in the process, create additional value.

2

Regardless of our performance to date, I want to assure you the Management Team feels we can not in any way let down our guard. It is hard not to notice record foreclosures, bankruptcies, and an unemployment rate that remains stubbornly high. We remain cautiously optimistic that with our focus on booking loan products we consider to be of a lower risk, we will maintain the quality of our loan portfolio. You may have noticed on our balance sheet that as of December 31, 2010 our Bank had no construction loans in its portfolio. Evergreen and unsecured loans to individuals also remain loan products of which we are wary. We remain strictly “cash flow” lenders who structure our credits carefully with guarantees and collateral as secondary and tertiary sources of repayment.

In closing, I would be remiss if I did not mention the efforts of our employees who certainly are among the most important factors associated with our success. I am extremely proud of our Senior Management Team and our employees at The First National Bank of Long Island. They are, in aggregate, a great group of people and are the secret behind the franchise value we are creating. I would also like to express my appreciation to all of my fellow stockholders for your investment in our company. I can assure you the Executive Team of The First National Bank of Long Island will continue to work diligently with a long-term view towards increasing shareholder value. That objective is what our job is all about; and each and every day, we do not take our eye off that ball. It is our hope our track record and potential for future success will continue to attract an ever-growing number of additional stockholders, and we are confident over the long-term our company will continue to meet your expectations as investors. Although we have been around for almost 85 years, it was only a few years ago that most of Long Island did not seem to recognize The First National Bank of Long Island name. Today, in ever-growing numbers, the marketplace is recognizing our expanding franchise and our reputation for a high quality service culture.

Our people are committed. Our energy level is high. Our work ethic is strong. We are not distracted from building our momentum with capital constraints, credit quality problems or the lack of products to service our desired targeted market segments. Our technology investments have been significant and integrate well into our growth strategy. We have capacity, timely information and processing efficiency. Despite challenges, my expectations are that we will continue to grow and prosper in terms of household share, size, profitability and reputation. More and more customers, more and more people will continue to hear about The First National Bank of Long Island, the Bank “Where Everyone Knows Your Name.”

“We have taken a measured and disciplined approach in growing the Bank’s franchise value.”

Michael N. Vittorio

President and Chief Executive Officer

3

Board of Directors and Executive Officers

|

Board of Directors

|

The First of Long Island Corporation

|

Allen E. Busching

Principal

B&B Capital

(consulting and private investment)

Paul T. Canarick

President & Principal

Paul Todd, Inc.

(construction company)

Alexander L. Cover

Management Consultant

Self Employed

(financial consulting)

Howard Thomas Hogan Jr., Esq.

Director

Hogan & Hogan

(attorney at law)

John T. Lane

Retired Managing Director

J.P. Morgan & Co.

J. Douglas Maxwell Jr.

Chief Financial Officer

NIRx Medical Technologies LLC

(medical instrumentation)

Stephen V. Murphy

President

S.V. Murphy & Co., Inc.

(investment banking)

Milbrey Rennie Taylor

Strategic and Media Consultant

Walter C. Teagle III

Non-executive Chairman

President

Teagle Management, Inc.

(private investment company)

Chairman

Teagle Foundation, Inc.

Michael N. Vittorio

President & Chief Executive Officer

[PHOTO OMITTED]

From left to right (Standing): Allen E. Busching, Stephen V. Murphy, Milbrey Rennie Taylor, Howard Thomas Hogan Jr., Esq. and Paul T. Canarick. From left to right (Sitting): J. Douglas Maxwell, Jr., Michael N. Vittorio, Walter C. Teagle III, Alexander L. Cover and John T. Lane.

|

Executive Officers

|

The First National Bank of Long Island

|

Michael N. Vittorio

President & Chief Executive Officer

4

Sallyanne K. Ballweg

Senior Executive Vice President

Mark D. Curtis

Executive Vice President

Chief Financial Officer & Cashier

Brian J. Keeney

Executive Vice President

Executive Trust Officer

Richard Kick

Executive Vice President

Senior Operations Officer

Donald L. Manfredonia

Executive Vice President

Senior Lending Officer

[PHOTO OMITTED]

From left to right: Sallyanne K. Ballweg, Brian J. Keeney, Michael N. Vittorio, Mark D. Curtis, Richard Kick and Donald L. Manfredonia

Financial Strength

2010 was a year of steady growth for the Bank. We maintained our financial strength by closely managing our credit quality and balance sheet. Plus, we were consistent with our values of personalizing our banking approach with customers.

In June of 2010, Bank Intelligence Solutions, a banking research company, identified 61 banks in the nation as “top performing banks.” Within the State of New York, only two banks were identified. One bank out of Ithaca, New York and ourselves, The First National Bank of Long Island. We are very proud of this achievement and look forward to building momentum as one of the strongest Regional Banks in the country.

Capital Raise

In July 2010, we bolstered our capital position through the sale of 1.4 million shares of common stock at a price of $24 per share. The net proceeds of the offering, after underwriting discount and expenses, were $32.4 million. The purpose of the capital raise was to enable the Corporation to continue to grow in a measured and disciplined manner and meet current regulatory expectations as to what constitutes an appropriate level of capital. The offering was very well received and resulted in the Bank adding a number of high quality institutional investors such as Wellington Management, Putnam Investments, Goldman Sachs Asset Management and JP Morgan Asset Management. Institutional ownership now represents 35% of total shares outstanding.

[PHOTOS OMITTED]

“We look forward to building momentum as one of the strongest Regional Banks in the country.”

Mark D. Curtis

Executive Vice President

Chief Financial Officer & Cashier

Loan Growth & Asset Quality

During 2010, the Bank continued its success of growing its loan portfolio while maintaining exceptional asset quality. On an average balance basis, loans grew in 2010 by 21%, or $148 million.

Our loan originators were able to find attractive loan opportunities that met our underwriting standards despite the challenging economic conditions on Long Island. Growth was generated in two primary loan categories – residential mortgages and commercial mortgages. A significant portion of our growth is attributed to refinance activity.

Toward the latter half of 2009 and the beginning of last year, we embarked upon a comprehensive review of our credit policies in order to insure that our underwriting standards reflected the current economic climate. With certain loan products we became more conservative. For example, we totally eliminated our exposure to construction loans. In addition, in the multifamily product category we elected not to underwrite transactions where there were limited residential units, and in the residential mortgage category we increased our required FICO score minimums.

5

The credit quality of the Bank’s loan portfolio remains excellent, as evidenced by a very low level of delinquent and nonperforming loans. During the year, we built our reserve for loan losses in light of current economic conditions. Our approach toward risk management has served us well. We were able to grow our loans and maintain asset quality. We believe credit risk is the most critical risk we manage for the benefit of our shareholders.

[PHOTO OMITTED]

“We believe credit risk is the most critical risk we manage for the benefit of our shareholders.”

Sallyanne K. Ballweg

Senior Executive Vice President

Branch Expansion

At The First National Bank of Long Island, we continue to build momentum by opening new branch locations and delivering more service to our customers including small businesses, professionals, middle market companies and service conscious consumers.

Our branch expansion strategy has proven to be successful as demonstrated by our deposit growth. On an average balance basis our deposits grew by 19%, or $209 million, in 2010. Ours is a relationship management strategy, not a pricing strategy. We want to know our customers and we want them to know us. Over the long-term, we are confident that building the Bank’s franchise through the growth of deposits will enhance shareholder value.

Our momentum will continue in 2011. The outlook for the Bank is promising. We opened our 34th branch in February in Point Lookout and we are currently scheduled to open a new full service branch in Massapequa, New York later this year. As of today, we have tentative plans to open two more branches in 2012. Our Bank continues to grow because of the dedication and hard work of our employees who contribute to our everyday success. Our employees are the strength behind our balance sheet.

[PHOTOS OMITTED]

“Our employees are the strength behind our balance sheet.”

Richard P. Perro

Senior Vice President

New Branches

[PHOTOS OMITTED]

2010 was a very busy year for the Bank as we opened four new branches on Long Island in Sea Cliff, Cold Spring Harbor, Bellmore and East Meadow. Each branch is richly decorated and designed to create a welcoming, friendly atmosphere with a living room style. The beauty of our branches speaks for itself and our banking professionals are dedicated towards delivering unparalleled service to their customers. These new locations were instrumental in developing household share with the commercial segment and individual consumers. They are all in key markets that will add to our organization’s franchise value in the years that lie ahead.

[PHOTO OMITTED]

Branch Locations

Full Service Offices

[PHOTO OMITTED]

BABYLON

42 Deer Park Avenue

Babylon, NY 11702

(631) 422-1700

Colleen A. Vogelsberg

Vice President & Branch Manager

[PHOTO OMITTED]

BAYVILLE

282 Bayville Avenue

Bayville, NY 11709

(516) 628-1288

Keith DeCuir

Vice President & Branch Manager

Elizabeth A. Materia

Vice President & Branch Market Manager

6

[PHOTO OMITTED]

BELLMORE

408 Bedford Avenue

Bellmore, NY 11710

(516) 679-6200

Julie Freund

Assistant Vice President & Branch Manager

Cathy C. O’Malley

Vice President & Branch Market Manager

[PHOTO OMITTED]

COLD SPRING HARBOR

147 Main Street

Cold Spring Harbor, NY 11724

(631) 367-3600

Colleen De Stefano

Vice President & Branch Manager

Allison Stansfield

Vice President & Branch Market Manager

EAST MEADOW

1975 Hempstead Turnpike

East Meadow, NY 11554

(516) 357-7200

Larry McGovern

Assistant Vice President & Branch Manager

Cathy C. O’Malley

Vice President & Branch Market Manager

[PHOTO OMITTED]

GARDEN CITY

1050 Franklin Avenue

Garden City, NY 11530

(516) 742-6262

Carol A. Kolesar

Vice President & Branch Manager

[PHOTO OMITTED]

GLEN HEAD

10 Glen Head Road

Glen Head, NY 11545

(516) 671-4900

John J. Mulder Jr.

Vice President & Branch Manager

[PHOTO OMITTED]

GREENVALE

7 Glen Cove Road

Greenvale, NY 11548

(516) 621-8811

Christina Marotta

Vice President & Branch Manager

[PHOTO OMITTED]

HUNTINGTON

253 New York Avenue

Huntington, NY 11743

(631) 427-4143

Frank M. Plesche

Vice President & Branch Manager

7

[PHOTO OMITTED]

LOCUST VALLEY

108 Forest Avenue

Locust Valley, NY 11560

(516) 671-2299

Elizabeth A. Materia

Vice President & Branch Market Manager

COMING SOON!

MASSAPEQUA

[PHOTO OMITTED]

MERRICK

1810 Merrick Avenue

Merrick, NY 11566

(516) 771-6000

Cathy C. O’Malley

Vice President & Branch Market Manager

[PHOTO OMITTED]

NORTHPORT

711 Fort Salonga Road

Northport, NY 11768

(631) 261-4000

Mary T. Sullivan

Vice President & Branch Market Manager

[PHOTO OMITTED]

NORTHPORT VILLAGE

105 Main Street

Northport, NY 11768

(631) 261-0331

Vincent P. Bartilucci

Vice President & Branch Manager

Mary T. Sullivan

Vice President & Branch Market Manager

[PHOTO OMITTED]

OLD BROOKVILLE

209 Glen Head Road

Old Brookville, NY 11545

(516) 759-9002

Henry C. Suhr

Vice President & Branch Manager

[PHOTO OMITTED]

POINT LOOKOUT

26A Lido Boulevard

P.O. Box 173

Point Lookout, NY 11569

(516) 431-3144

Linda A. Rowse

Assistant Vice President & Branch Manager

Cathy C. O’Malley

Vice President & Branch Market Manager

8

[PHOTO OMITTED]

ROCKVILLE CENTRE

310 Merrick Road

Rockville Centre, NY 11570

(516) 763-5533

Linda Roldan

Vice President & Branch Manager

[PHOTO OMITTED]

ROSLYN HEIGHTS

130 Mineola Avenue

Roslyn Heights, NY 11577

(516) 621-1900

Lorraine Russo

Vice President & Branch Manager

[PHOTO OMITTED]

SEA CLIFF

299 Sea Cliff Avenue

Sea Cliff, NY 11579

(516) 671-7868

Kirk B. Thomas

Vice President & Branch Manager

[PHOTO OMITTED]

VALLEY STREAM

127 East Merrick Road

Valley Stream, NY 11580

(516) 825-0202

Toni Valente

Vice President & Branch Manager

[PHOTO OMITTED]

WOODBURY

800 Woodbury Road, Suite M

Woodbury, NY 11797

(516) 364-3434

Allison Stansfield

Vice President & Branch Market Manager

Commercial Banking Offices

[PHOTO OMITTED]

BOHEMIA

30 Orville Drive

Bohemia, NY 11716

(631) 218-2500

Kathleen M. Crowe

Vice President & Branch Manager

[PHOTO OMITTED]

DEER PARK

60 East Industry Court

Deer Park, NY 11729

(631) 243-2600

Joanne Maiorana-Davis

Vice President & Branch Manager

[PHOTO OMITTED]

FARMINGDALE

22 Allen Boulevard

Farmingdale, NY 11735

(631) 753-8888

9

Sandy F. Buttacy

Vice President & Branch Manager

[PHOTO OMITTED]

FARMINGDALE

2091 New Highway

Farmingdale, NY 11735

(631) 454-2022

Robert A. Pizza

Vice President & Branch Manager

[PHOTO OMITTED]

GREAT NECK

536 Northern Boulevard

Great Neck, NY 11021

(516) 482-6666

Joanne Bosco

Vice President & Branch Manager

[PHOTO OMITTED]

HAUPPAUGE

330 Motor Parkway

Hauppauge, NY 11788

(631) 952-2900

JoAnn Diamond

Vice President & Branch Manager

[PHOTO OMITTED]

HICKSVILLE

106 Old Country Road

Hicksville, NY 11801

(516) 932-7150

Joyce C. Graber

Vice President & Branch Manager

[PHOTO OMITTED]

NEW HYDE PARK

243 Jericho Turnpike

New Hyde Park, NY 11040

(516) 328-3100

Susan Costabile

Vice President & Branch Manager

[PHOTO OMITTED]

PORT JEFFERSON STATION

Davis Professional Park

5225 Nesconset Highway

Building 4, Suite 21

Port Jefferson Station, NY 11776

(631) 928-4411

Susan Donovan

Vice President & Branch Manager

MANHATTAN

[PHOTO OMITTED]

232 Madison Avenue

New York, NY 10016

(212) 213-8111

10

Judith A. Ferdinand

Vice President & Branch Manager

[PHOTO OMITTED]

225 Broadway, Suite 703

New York, NY 10007

(212) 693-1515

Gladys Ruggiero

Vice President & Branch Manager

[PHOTO OMITTED]

1501 Broadway, Suite 301

New York, NY 10036

(212) 278-0707

Doris M. Burkett

Vice President & Branch Manager

Select Service Banking Centers

[PHOTO OMITTED]

LAKE SUCCESS

3000 Marcus Avenue

Lake Success, NY 11042

(516) 775-3133

Jerry Scansarole

Vice President & Branch Manager

[PHOTO OMITTED]

SMITHTOWN

285 Middle Country Road, Suite 104

Smithtown, NY 11787

(631) 265-0200

Frances A. Koslow

Vice President & Branch Manager

[PHOTO OMITTED]

Disaster Recovery Center

Our detailed Technology Plan supports our business goals, optimizes business investment, and manages the technology related risks and opportunities for the Bank. In order to help drive shareholder value and deliver more effective and convenient services to our customers, we use technology as a tool to increase our business capacity and create expense efficiencies. Plus, it allows us to be the provider of choice within the markets that we service.

In 2010, the Bank built a new Data Center, which serves as the IT Department’s base of operations, as well as our Disaster Recovery Facility. This state-of-the-art facility was built to the highest technological and engineering standards and employs best practices. This includes a Server Room with the appropriate technology, equipment and security to enable substantial future growth of the Bank and ensure we have the appropriate backup capability to manage in the event of a disaster.

We are very proud of the technological investment we made in 2010. The security and protection of our customers’ financial assets are a priority to us.

[PHOTO OMITTED]

“The security and protection of our customers’ financial assets are a priority to us.”

Richard Kick

Executive Vice President

Senior Operations Officer

11

Community Outreach

The First National Bank of Long Island made significant charitable donations in 2010 to support local organizations and activities in the communities we serve. Many of our employees have volunteered their time to support those in need and we thank each and every individual for contributing to the success we have achieved with our community service initiatives.

In order to continue our momentum, the Bank organized a community service committee to help identify future community involvement programs. We look forward to establishing more community initiatives and events in the years to come.

Some of our initiatives are listed below:

|

|

·

|

Toys for Tots – The Bank was proud to participate in the Young CPAs Committee of the NYSSCPA Suffolk Chapter’s 16th Annual Holiday Toy Drive. Hundreds of toys were collected in the Bank’s branches to benefit the U.S. Marine Corps’ Toys for Tots Program. The event was the single largest pickup in all of Suffolk County.

|

|

|

·

|

Toys of Hope Coat Drive – We sponsored a drive for the not-for-profit organization named Toys of Hope located in Huntington Station, New York. Numerous coats, toys and clothing were collected for Long Island homeless children and families.

|

|

|

·

|

The INN (Interfaith Nutrition Network) – The Bank held an Employee Food Drive and collected 700 lbs of food and monetary donations for the INN in Hempstead, Long Island. The organization helps homeless people and families overcome the challenge of hunger.

|

|

|

·

|

Teach Kids to Save Program – The Bank continues to work with local schools on Long Island to promote financial literacy to elementary school students. “Banking Days” are held at the schools and a local Branch Manager makes a presentation to students. In 2010, more than ten schools participated in our program and hundreds of students learned about the importance of saving money and developing good banking habits.

|

|

|

·

|

Long Island Cares Inc., The Harry Chapin Food Bank – We collected 618 pounds of food in our branches to help feed Long Island children and families.

|

|

|

·

|

Operation Warmth – The Bank participated in Northport’s Chamber of Commerce “Operation Warmth” donation drive. We collected over 100 coats, jackets, hats, scarves and gloves that were delivered to those in need on Long Island.

|

[PHOTOS OMITTED]

12

S E L E C T E D F I N A N C I A L D A T A

The following is selected consolidated financial data for the past five years. This data should be read in conjunction with the information contained under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the accompanying consolidated financial statements and related notes.

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

INCOME STATEMENT DATA:

|

||||||||||||||||||||

|

Interest Income

|

$ | 72,369,000 | $ | 66,274,000 | $ | 59,686,000 | $ | 53,023,000 | $ | 49,000,000 | ||||||||||

|

Interest Expense

|

16,774,000 | 18,334,000 | 16,743,000 | 16,269,000 | 12,949,000 | |||||||||||||||

|

Net Interest Income

|

55,595,000 | 47,940,000 | 42,943,000 | 36,754,000 | 36,051,000 | |||||||||||||||

|

Provision for Loan Losses

|

3,973,000 | 4,285,000 | 1,945,000 | 575,000 | 670,000 | |||||||||||||||

|

Net Income

|

18,392,000 | 13,463,000 | 12,962,000 | 11,482,000 | 11,227,000 | |||||||||||||||

|

PER SHARE DATA:

|

||||||||||||||||||||

|

Basic Earnings

|

$ 2.33 | $ 1.87 | $ 1.79 | $ 1.52 | $ 1.47 | |||||||||||||||

|

Diluted Earnings

|

2.30 | 1.84 | 1.78 | 1.51 | 1.45 | |||||||||||||||

|

Cash Dividends Declared

|

.84 | .76 | .66 | .58 | .50 | |||||||||||||||

|

Dividend Payout Ratio

|

36.52 | % | 41.30 | % | 37.08 | % | 38.41 | % | 34.48 | % | ||||||||||

|

Stock Splits/Dividends Declared

|

- | - | - |

2-for-1

|

- | |||||||||||||||

|

Book Value

|

$ 17.99 | $ 16.15 | $ 14.25 | $ 13.73 | $ 12.60 | |||||||||||||||

|

Tangible Book Value

|

17.97 | 16.12 | 14.22 | 13.71 | 12.57 | |||||||||||||||

|

BALANCE SHEET DATA AT YEAR END:

|

||||||||||||||||||||

|

Total Assets

|

$ | 1,711,023,000 | $ | 1,675,169,000 | $ | 1,261,609,000 | $ | 1,069,019,000 | $ | 954,166,000 | ||||||||||

|

Loans

|

902,959,000 | 827,666,000 | 658,134,000 | 525,539,000 | 449,465,000 | |||||||||||||||

|

Allowance for Loan Losses

|

14,014,000 | 10,346,000 | 6,076,000 | 4,453,000 | 3,891,000 | |||||||||||||||

|

Deposits

|

1,292,938,000 | 1,277,550,000 | 900,337,000 | 869,038,000 | 824,797,000 | |||||||||||||||

|

Borrowed Funds

|

253,590,000 | 273,407,000 | 251,122,000 | 92,110,000 | 28,143,000 | |||||||||||||||

|

Stockholders' Equity

|

156,694,000 | 116,462,000 | 102,532,000 | 102,384,000 | 95,561,000 | |||||||||||||||

|

AVERAGE BALANCE SHEET DATA:

|

||||||||||||||||||||

|

Total Assets

|

$ | 1,657,396,000 | $ | 1,413,632,000 | $ | 1,181,655,000 | $ | 1,003,240,000 | $ | 977,232,000 | ||||||||||

|

Loans

|

864,163,000 | 716,569,000 | 572,356,000 | 480,166,000 | 418,746,000 | |||||||||||||||

|

Allowance for Loan Losses

|

11,954,000 | 6,357,000 | 4,947,000 | 4,167,000 | 3,609,000 | |||||||||||||||

|

Deposits

|

1,310,507,000 | 1,101,828,000 | 919,490,000 | 868,421,000 | 842,399,000 | |||||||||||||||

|

Borrowed Funds

|

193,823,000 | 194,129,000 | 157,275,000 | 32,705,000 | 37,989,000 | |||||||||||||||

|

Stockholders' Equity

|

142,140,000 | 110,767,000 | 100,710,000 | 98,402,000 | 93,064,000 | |||||||||||||||

|

FINANCIAL RATIOS:

|

||||||||||||||||||||

|

Return on Average Assets (ROA)

|

1.11 | % | 0.95 | % | 1.10 | % | 1.14 | % | 1.15 | % | ||||||||||

|

Return on Average Stockholders' Equity (ROE)

|

12.94 | % | 12.15 | % | 12.87 | % | 11.67 | % | 12.06 | % | ||||||||||

|

Average Equity to Average Assets

|

8.58 | % | 7.84 | % | 8.52 | % | 9.81 | % | 9.52 | % | ||||||||||

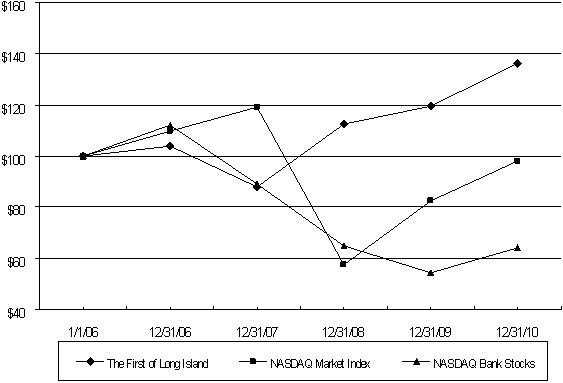

S T O C K P R I C E S

The Corporation's Common Stock trades on The Nasdaq Capital Market tier of The Nasdaq Stock Market under the symbol FLIC. The following table sets forth high and low sales prices for the years ended December31, 2010 and 2009.

|

2010

|

2009

|

|||||||||||||||

|

Quarter

|

High

|

Low

|

High

|

Low

|

||||||||||||

|

First

|

$25.97 | $22.46 | $23.75 | $19.34 | ||||||||||||

|

Second

|

28.08 | 23.62 | 26.25 | 19.75 | ||||||||||||

|

Third

|

27.00 | 24.01 | 30.00 | 22.25 | ||||||||||||

|

Fourth

|

29.24 | 24.55 | 28.50 | 22.75 | ||||||||||||

At December 31, 2010, there were 559 stockholders of record of the Corporation's Common Stock. The number of stockholders of record includes banks and brokers who act as nominees, each of whom may represent more than one stockholder.

13

M A N A G E M E N T ' S D I S C U S S I O N A N D A N A L Y S I S O F

F I N A N C I A L C O N D I T I O N A N D R E S U L T S O F O P E R A T I O N S

The following is management's discussion and analysis of certain significant factors that have affected the Corporation’s financial condition and operating results during the periods included in the accompanying consolidated financial statements, and should be read in conjunction with such financial statements. The Corporation’s financial condition and operating results principally reflect those of its wholly-owned subsidiary, The First National Bank of Long Island (the “Bank”), and subsidiaries wholly-owned by the Bank, either directly or indirectly, The First of Long Island Agency, Inc., FNY Service Corp. (“FNY”), and The First of Long Island REIT, Inc. (“REIT”). The consolidated entity is referred to as the “Corporation” and the Bank and its subsidiaries are collectively referred to as the “Bank.” The Bank’s primary service area is Nassau and Suffolk Counties, Long Island. However, the Bank has three commercial banking branches in Manhattan and may open additional New York City branches in the future.

Overview

Overview – 2010 Versus 2009. The Corporation earned $18.4 million in 2010. This is an increase of 36.6% over 2009 earnings of $13.5 million. On a per share basis, earnings for 2010 were $2.30. This is $.46 better than $1.84 per share earned in 2009. Returns on average assets and equity were 1.11% and 12.94%, respectively, for 2010 compared to .95% and 12.15%, respectively, for 2009. Cash dividends per share grew by 8 cents, or 10.5%, from 76 cents per share in 2009 to 84 cents this year. In July 2010 the Corporation bolstered its capital position through the sale of 1.4 million shares of common stock at a price of $24 per share. The resulting net proceeds of the offering after underwriting discount and expenses was $32.4 million.

Earnings for the fourth quarter of 2010 were $.46 per share, representing an increase of $.16 per share, or 53.3% over $.30 per share earned in the same quarter last year. The improvement was primarily due to the fact that the provision for loan losses was $2.1 million higher in the fourth quarter of 2009, which impacted earnings by approximately $.17 per share. When comparing fourth quarter to third quarter 2010 results, earnings are down $.09 per share, or 16.4%, primarily as a result of an increase in the provision for loan losses of $725,000, the establishment of a $300,000 valuation allowance on one loan held for sale and the full quarter dilutive impact of the common stock offering. The increase in the provision for loan losses was driven by the establishment of an impairment reserve of $870,000 on one nonaccrual loan.

The large drivers of earnings per share growth in 2010 were growth in the average balances of loans and tax-exempt municipal securities and decreases in the rates paid on various categories of deposits. The positive impact of these items was partially offset by decreases in overall yield on the Bank’s loan and taxable securities portfolios, expense increases attributable to the Bank’s branch growth initiative and general inflation in the cost of goods and services, and the dilutive impact of the 2010 common stock offering which is estimated to be approximately $.16 per share.

On an average balance basis, loans grew by $147.6 million, or 20.6% when comparing 2010 to 2009. Almost all of the growth occurred in commercial and residential mortgages, the average balances of which were up $92.4 million, or 29.2%, and $66.3 million, or 29.5%, respectively. A significant portion of the growth in the average balance of residential mortgages was attributable to loans originated during 2010, with the remainder attributable to loans originated in 2009. By contrast, almost all of the growth in the average balance of commercial mortgages was attributable to loans originated in 2009, with the remainder attributable to loans originated this year. The large reduction in commercial mortgage originations in 2010 was the result of a variety of factors including, but not limited to, a deliberate reduction in originations during the first half of 2010 in order to build the Bank’s Tier 1 leverage capital ratio, a softening in loan demand during the latter half of 2010 and a reduction in multifamily loan originations throughout 2010 in an effort to diversify the Bank’s commercial mortgage portfolio.

The overall yield earned on the Bank’s loan portfolio declined by 26 basis points in 2010 and the overall yield on the Bank’s taxable securities portfolio declined by 70 basis points. The decline in yield on the loan portfolio was primarily attributable to a decline in general interest rates and competitive conditions in the local marketplace. The decline in yield on the taxable securities portfolio was also attributable to a decline in general interest rates and, additionally, a significant increase in the size of the short-term mortgage securities portfolio relative to the total taxable securities portfolio. Short-term mortgage securities, which the Bank generally defines as those having an estimated average life of 2.5 years or less at the date of purchase, represented 38.8% of the average balance of the total taxable securities portfolio in 2010 as compared to 18.2% last year. Management grew this segment of the taxable securities portfolio as a hedge against potential future increases in interest rates, to balance the duration of the overall securities portfolio in light of the increased size of the longer-term municipal securities portfolio, and because the incremental yield that could be earned on longer average life mortgage securities was relatively small. In addition, management temporarily invested a significant portion of the proceeds of the 2010 common stock offering in short-term mortgage securities with the intention of reinvesting the monthly paydowns on such securities in better yielding loans.

14

The credit quality of the Bank’s loan portfolio remains excellent as evidenced by, among other things, low levels of past due, nonaccrual and impaired loans. In an attempt to maintain credit quality, management continues to focus its loan portfolio growth efforts on what it considers lower risk loan categories (i.e., owner occupied commercial mortgages, multifamily loans, and first lien residential mortgages having terms generally between ten and fifteen years) and continues to avoid growing what it considers higher risk loan categories (i.e., construction loans and unsecured loans to individuals). The credit quality of the Bank’s securities portfolio also remains excellent. All of the Bank’s mortgage securities are backed by mortgages underwritten on conventional terms, and almost all of these securities are full faith and credit obligations of the U.S. government. The remainder of the Bank’s securities portfolio consists principally of municipal securities rated AA or better by major rating agencies.

Looking forward to 2011, challenges for the Bank and our industry as a whole will likely include, among others, the maintenance of net interest margin and the cost of complying with the abundance of recently enacted laws and regulations impacting the financial services industry. With respect to net interest margin, the general level of interest rates and competition could cause the yields available on securities and loans to remain relatively low, while at the same time the Bank may have limited opportunity to further reduce its deposit rates. Furthermore, earnings per share in 2011 will include the dilutive impact of the July 2010 common stock offering for a full year. Notwithstanding these challenges, the Bank enters 2011 with a record of steady earnings growth, excellent credit quality, sufficient capital to provide for growth and a corporate philosophy that remains focused on maintaining the strength and quality of the Bank’s balance sheet and creating long-term shareholder value.

Key strategic initiatives for 2011 and beyond include continued loan growth, maintenance of asset quality, maintenance of capital strength and expansion of the Bank’s branch distribution system both on Long Island and in New York City. During 2010 the Bank opened four full service branches on Long Island in Sea Cliff, Cold Spring Harbor, East Meadow and Bellmore. Thus far in 2011, the Bank opened a full service branch in Point Lookout, Long Island and plans to open a full service branch in Massapequa, Long Island later in the year.

Overview – 2009 Versus 2008. The Corporation earned $1.84 per share in 2009, an increase of 6 cents, or 3.4%, over $1.78 earned in 2008. Cash dividends per share grew by 10 cents, or 15.2%, from 66 cents per share in 2008 to 76 cents in 2009.

The Bank’s core business of gathering deposits and making loans was strong in 2009. Total deposits grew by $377.2 million, or 41.9%, and gross loans grew by $169.5 million, or 25.8%. Two thirds of the overall deposit growth came from savings and money market products, with most of the remaining growth occurring in time deposits. Contributing to deposit growth were new branch openings and expansion of existing branches, competitively priced deposit products, a high level of customer service and deposit rate promotions. In addition, management believed that uncertainty in the equity markets and the negative publicity surrounding money center banks also played a role.

Loan growth, the primary driver of earnings growth in 2009, principally occurred in what management considers to be lower risk loan categories including multifamily loans, owner occupied commercial mortgages, and first lien residential mortgages with ten to fifteen year terms. By contrast, management considers construction and land development loans to be high risk and had purposely not grown this category. Construction and land development loans amounted to only $3.1 million, or .4% of gross loans, at year-end 2009. Loan growth occurred in 2009 as part of management’s continued efforts to improve the Bank’s earnings prospects by making loans a larger portion of the overall balance sheet.

National and local economic conditions remained unfavorable throughout 2009. Furthermore, management believed that economic conditions would not improve considerably in 2010, and any improvement beyond 2010 would occur slowly over an extended period of time. In addition the Bank grew its loan portfolio at a compound annual growth rate of 19% over the five year period ended December 31, 2009 and its loan portfolio was primarily comprised of commercial and residential real estate loans concentrated on Long Island and in New York City. Based on these and other factors, and despite the fact that the Bank had a very low level of identified problem loans, in closing the fourth quarter of 2009 management decided to increase the Bank’s allowance for loan losses relative to gross loans. The Bank’s allowance for loan losses at year-end 2009 was $10.3 million, or 1.25% of gross loans, compared to $6.1 million, or .92% of gross loans, at year-end 2008.

The Bank’s capital ratios trended down in 2009 due to overall balance sheet growth and growth in the Bank’s loan portfolio, but at year-end 2009 still exceeded the regulatory criteria for a well-capitalized bank. Total stockholders’ equity before accumulated other comprehensive income or loss grew by $8.7 million in 2009 versus $3.4 million in 2008. The larger growth in 2009 was primarily attributable to the fact that the Corporation significantly reduced its share repurchases in order to preserve and build capital in light of the unfavorable economic climate.

15

Net interest margin declined in 2009 because the rates available for investments in loans and securities declined, and rapid deposit growth resulted in the need to temporarily invest excess cash in low yielding balances with correspondent banks until better yielding loans and securities could be originated or purchased. Margin also declined because management shortened the average duration of the Bank’s taxable securities portfolio as a prudent measure to, among other things, protect the Bank’s net interest income in the event of an increase in interest rates. Noninterest income increased by $1.5 million, or 23.6%, in 2009 because of increases in service charge income and gains on sales of securities of $518,000 and $1.2 million, respectively. FDIC insurance expense increased by $1,630,000, or from $558,000 in 2008 to $2,188,000 in 2009. The increase was caused by failures in the industry and their adverse impact on the deposit insurance fund (“DIF”). Pension plan expense increased by $1,041,000, or from $576,000 in 2008 to $1,617,000 in 2009. The increase resulted from a decline in long-term interest rates and the poor performance of the equity markets in 2008.

The Corporation’s effective tax rate, or income tax expense as a percentage of book income, declined from 26.3% in 2008 to 18.8% in 2009. The decline was attributable to a restructuring of the ownership of the Corporation’s REIT entity in December 2008 and a significant increase during 2009 in the size of the Bank’s tax-exempt municipal securities portfolio. The REIT restructuring, which reduced the Corporation’s 2009 income tax burden by approximately $700,000, was done in response to a change in New York State tax law in 2008. The law change deprived the Corporation in 2008 of the tax benefit that had traditionally been derived from its REIT entity and the restructuring restored that benefit. The Bank significantly increased the size of its tax-exempt municipal securities portfolio in 2009 in response to provisions of the American Recovery and Reinvestment Act of 2009 which enabled the Bank to buy certain tax-exempt securities at what it believed to be attractive yields without the usual limitations imposed by the federal alternative minimum tax.

In the first quarter of 2009, the Bank opened a commercial banking office in Port Jefferson Station, Long Island. Subsequently in 2009, a full service branch was opened in Bayville, Long Island and the Valley Stream commercial banking office was converted to a full service branch.

16

Net Interest Income

Average Balance Sheet; Interest Rates and Interest Differential. The following table sets forth the average daily balances for each major category of assets, liabilities and stockholders’ equity as well as the amounts and average rates earned or paid on each major category of interest-earning assets and interest-bearing liabilities.

|

2010

|

2009

|

2008

|

||||||||||||||||||||||||||||||||||

|

Average Balance

|

Interest/ Dividends

|

Average Rate

|

Average Balance

|

Interest/ Dividends

|

Average Rate

|

Average Balance

|

Interest/ Dividends

|

Average Rate

|

||||||||||||||||||||||||||||

|

Assets:

|

(dollars in thousands)

|

|||||||||||||||||||||||||||||||||||

|

Federal funds sold and overnight investments

|

$ | 283 | $ | - | - | % | $ | 374 | $ | - | - | % | $ | 19,362 | $ | 480 | 2.48 | % | ||||||||||||||||||

|

Investment securities:

|

||||||||||||||||||||||||||||||||||||

|

Taxable

|

472,039 | 16,845 | 3.57 | 443,559 | 18,926 | 4.27 | 386,404 | 18,857 | 4.88 | |||||||||||||||||||||||||||

|

Nontaxable (1)

|

242,830 | 14,945 | 6.15 | 181,084 | 11,508 | 6.36 | 143,121 | 9,373 | 6.55 | |||||||||||||||||||||||||||

|

Loans (1) (2)

|

864,163 | 45,683 | 5.29 | 716,569 | 39,780 | 5.55 | 572,356 | 34,193 | 5.97 | |||||||||||||||||||||||||||

|

Total interest-earning assets (1)

|

1,579,315 | 77,473 | 4.91 | 1,341,586 | 70,214 | 5.23 | 1,121,243 | 62,903 | 5.61 | |||||||||||||||||||||||||||

|

Allowance for loan losses

|

(11,954 | ) | (6,357 | ) | (4,947 | ) | ||||||||||||||||||||||||||||||

|

Net interest-earning assets

|

1,567,361 | 1,335,229 | 1,116,296 | |||||||||||||||||||||||||||||||||

|

Cash and due from banks

|

40,261 | 42,962 | 32,524 | |||||||||||||||||||||||||||||||||

|

Premises and equipment, net

|

20,442 | 16,937 | 11,587 | |||||||||||||||||||||||||||||||||

|

Other assets

|

29,332 | 18,504 | 21,248 | |||||||||||||||||||||||||||||||||

| $ | 1,657,396 | $ | 1,413,632 | $ | 1,181,655 | |||||||||||||||||||||||||||||||

|

Liabilities and

|

||||||||||||||||||||||||||||||||||||

|

Stockholders' Equity:

|

||||||||||||||||||||||||||||||||||||

|

Savings and money market deposits

|

$ | 651,506 | 4,049 | .62 | $ | 501,125 | 5,287 | 1.06 | $ | 364,974 | 4,576 | 1.25 | ||||||||||||||||||||||||

|

Time deposits

|

285,213 | 5,977 | 2.10 | 266,216 | 6,485 | 2.44 | 236,820 | 6,782 | 2.86 | |||||||||||||||||||||||||||

|

Total interest-bearing deposits

|

936,719 | 10,026 | 1.07 | 767,341 | 11,772 | 1.53 | 601,794 | 11,358 | 1.89 | |||||||||||||||||||||||||||

|

Short-term borrowings

|

28,864 | 108 | .37 | 40,663 | 221 | .54 | 48,379 | 746 | 1.54 | |||||||||||||||||||||||||||

|

Long-term debt

|

164,959 | 6,640 | 4.03 | 153,466 | 6,341 | 4.13 | 108,896 | 4,639 | 4.26 | |||||||||||||||||||||||||||

|

Total interest-bearing liabilities

|

1,130,542 | 16,774 | 1.48 | 961,470 | 18,334 | 1.91 | 759,069 | 16,743 | 2.21 | |||||||||||||||||||||||||||

|

Checking deposits

|

373,788 | 334,487 | 317,696 | |||||||||||||||||||||||||||||||||

|

Other liabilities

|

10,926 | 6,908 | 4,180 | |||||||||||||||||||||||||||||||||

| 1,515,256 | 1,302,865 | 1,080,945 | ||||||||||||||||||||||||||||||||||

|

Stockholders' equity

|

142,140 | 110,767 | 100,710 | |||||||||||||||||||||||||||||||||

| $ | 1,657,396 | $ | 1,413,632 | $ | 1,181,655 | |||||||||||||||||||||||||||||||

|

Net interest income (1)

|

$ | 60,699 | $ | 51,880 | $ | 46,160 | ||||||||||||||||||||||||||||||

|

Net interest spread (1)

|

3.43 | % | 3.32 | % | 3.40 | % | ||||||||||||||||||||||||||||||

|

Net interest margin (1)

|

3.84 | % | 3.87 | % | 4.12 | % | ||||||||||||||||||||||||||||||

|

(1)

|

Tax-equivalent basis. Interest income on a tax-equivalent basis includes the additional amount of interest income that would have been earned if the Corporation's investment in tax-exempt loans and investment securities had been made in loans and investment securities subject to Federal income taxes yielding the same after-tax income. The tax-equivalent amount of $1.00 of nontaxable income was $1.52 in each period presented, based on a Federal income tax rate of 34%.

|

|

(2)

|

For the purpose of these computations, nonaccruing loans are included in the daily average loan amounts outstanding.

|

17

Rate/Volume Analysis. The following table sets forth the effect of changes in volumes, rates, and rate/volume on tax-equivalent interest income, interest expense and net interest income.

|

Year Ended December 31,

|

||||||||||||||||||||||||||||||||

|

2010 versus 2009

|

2009 versus 2008

|

|||||||||||||||||||||||||||||||

|

Increase (decrease) due to changes in:

|

Increase (decrease) due to changes in:

|

|||||||||||||||||||||||||||||||

|

Volume

|

Rate

|

Rate/ Volume (1)

|

Net Change

|

Volume

|

Rate

|

Rate/ Volume (1)

|

Net Change

|

|||||||||||||||||||||||||

|

(in thousands)

|

||||||||||||||||||||||||||||||||

|

Interest Income:

|

||||||||||||||||||||||||||||||||

|

Federal funds sold and overnight investments

|

$ | - | $ | - | $ | - | $ | - | $ | (471 | ) | $ | (480 | ) | $ | 471 | $ | (480 | ) | |||||||||||||

|

Investment securities:

|

||||||||||||||||||||||||||||||||

|

Taxable

|

1,215 | (3,097 | ) | (199 | ) | (2,081 | ) | 2,789 | (2,370 | ) | (350 | ) | 69 | |||||||||||||||||||

|

Nontaxable

|

3,924 | (363 | ) | (124 | ) | 3,437 | 2,486 | (278 | ) | (73 | ) | 2,135 | ||||||||||||||||||||

|

Loans

|

8,194 | (1,899 | ) | (392 | ) | 5,903 | 8,615 | (2,419 | ) | (609 | ) | 5,587 | ||||||||||||||||||||

|

Total interest income

|

13,333 | (5,359 | ) | (715 | ) | 7,259 | 13,419 | (5,547 | ) | (561 | ) | 7,311 | ||||||||||||||||||||

|

Interest Expense:

|

||||||||||||||||||||||||||||||||

|

Savings and money market deposits

|

1,587 | (2,173 | ) | (652 | ) | (1,238 | ) | 1,707 | (725 | ) | (271 | ) | 711 | |||||||||||||||||||

|

Time deposits

|

463 | (906 | ) | (65 | ) | (508 | ) | 842 | (1,013 | ) | (126 | ) | (297 | ) | ||||||||||||||||||

|

Short-term borrowings

|

(64 | ) | (69 | ) | 20 | (113 | ) | (119 | ) | (483 | ) | 77 | (525 | ) | ||||||||||||||||||

|

Long-term debt

|

475 | (164 | ) | (12 | ) | 299 | 1,899 | (140 | ) | (57 | ) | 1,702 | ||||||||||||||||||||

|

Total interest expense

|

2,461 | (3,312 | ) | (709 | ) | (1,560 | ) | 4,329 | (2,361 | ) | (377 | ) | 1,591 | |||||||||||||||||||

|

Increase (decrease) in net interest income

|

$ | 10,872 | $ | (2,047 | ) | $ | (6 | ) | $ | 8,819 | $ | 9,090 | $ | (3,186 | ) | $ | (184 | ) | $ | 5,720 | ||||||||||||

|

(1)

|

Represents the change not solely attributable to change in rate or change in volume but a combination of these two factors. The rate/volume variance could be allocated between the volume and rate variances shown in the table based on the absolute value of each to the total for both.

|

Net Interest Income – 2010 Versus 2009

Net interest income on a tax-equivalent basis increased by $8.8 million, or from $51.9 million in 2009 to $60.7 million this year. The most significant reasons for the increase in net interest income were growth in the Bank’s loan and tax-exempt securities portfolios and decreases in the rates paid on various categories of deposits. On an average balance basis, loans grew by $147.6 million, or 20.6%, and tax-exempt securities grew by $61.7 million, or 34.1%. Growth in these asset categories was funded by an increase in interest-bearing deposits, which on an average balance basis grew by $169.4 million, or 22.1%, and an increase in checking deposits, which on an average balance basis grew by $39.3 million, or 11.7%. The positive impact of loan and securities growth and decreases in deposit rates was partially offset by decreases in the overall yield on the Bank’s loan and taxable securities portfolios.

Net interest spread, or the difference between the overall yield on interest-earning assets and the overall cost of interest-bearing liabilities, increased by 11 basis points in 2010. This occurred primarily because management, through a steady reduction in the Bank’s deposit rates throughout 2010, was able to lower the Bank’s cost of deposits by 46 basis points while at the same time the overall yield on the Bank’s interest-earning assets declined by only 32 basis points. The spread increase, when applied to those interest-earning assets funded by interest-bearing liabilities, positively impacted both net interest income and net interest margin. On the other hand, for those interest-earning assets funded by noninterest-bearing checking deposits and capital, the 32 basis point decline in asset yield had a more than offsetting negative impact on net interest income and net interest margin and thereby caused net interest margin to decline. The 32 basis point decline in overall asset yield was primarily attributable to a decline in general interest rates, competitive loan pricing in the Bank’s marketplace, and a significant increase, for reasons previously discussed, in the Bank’s short-term mortgage securities portfolio.

18

Net Interest Income – 2009 Versus 2008

Net interest income on a tax-equivalent basis increased by $5,720,000 or from $46,160,000 in 2008 to $51,880,000 in 2009. The most significant reason for the increase was growth in the Bank’s loan portfolio, which, on an average balance basis, grew by $144.2 million, or 25.2%. Loan growth was funded by an increase in interest-bearing deposits, which, on an average balance basis, grew by $165.5 million, or 27.5%. Deposit growth in excess of that needed to grow loans was mostly invested in a combination of taxable and nontaxable securities. Also contributing to the growth in net interest income was a 30 basis point reduction in the overall cost of deposits and borrowings in 2009 resulting from the steady decline in market interest rates in 2008 and the Bank’s ability to lower its deposit rates throughout 2009 in response to more rational pricing in its marketplace.

The positive impact of loan growth and lower deposit and borrowing costs was partially offset by a decline in rates available for investments in loans and securities. Other offsetting factors were management shortened the average duration of the Bank’s taxable securities portfolio as a prudent measure to, among other things, protect the Bank’s net interest income in the event of an increase in interest rates, and the Bank’s need to temporarily invest excess cash resulting from rapid deposit growth in low yielding balances with correspondent banks until better yielding loans and securities could be originated or purchased. These offsetting factors are the principal causes of the 38 basis point reduction in the overall yield on interest-earning assets in 2009.

While net interest income increased in 2009, net interest spread declined by 8 basis points as the yield on interest-earning assets declined more than the cost of deposits and borrowings. Net interest margin declined even more than net interest spread, or by 38 basis points, because a significant portion of the Corporation’s interest-earning assets are funded by noninterest-bearing liabilities and capital. For these assets, a reduction in yield has no offsetting reduction in interest cost and therefore results in a corresponding reduction in net interest margin. Also negatively impacting net interest margin were deposit rate promotions associated with new branch openings, expansion of existing branches and management’s desire to grow certain categories of deposits.

Noninterest Income, Noninterest Expense, and Income Taxes

Noninterest income includes service charges on deposit accounts, Investment Management Division income, gains or losses on sales of securities, and all other items of income, other than interest, resulting from the business activities of the Corporation. Noninterest income was $8.0 million and $7.8 million in 2010 and 2009, respectively, representing increases over prior year amounts of $201,000, or 2.6%, and $1.5 million, or 23.6%.

The increase in noninterest income in 2010 is almost entirely due to a $291,000 increase in net gains on sales of available-for-sale securities, as partially offset by small decreases in the other categories of noninterest income. The gains on sales of securities resulted from the sale of approximately $77 million of available-for-sale securities. The proceeds of the sales were used to limit the growth of the balance sheet by paying down short-term borrowings and thereby preserving the Bank’s Tier I leverage capital ratio.

The increase in noninterest income in 2009 was almost entirely due to a $1.2 million increase in net gains on sales of available-for-sale securities and a $518,000 increase in service charge income, as partially offset by a $219,000 decrease in Investment Management Division income. The gains on sales of securities resulted from the sale of approximately $49 million of available-for-sale securities. The proceeds of the sale were generally reinvested in securities having a longer duration and average yield slightly higher than the securities sold. Service charge income increased primarily as a result of an increase in return check charges. Investment Management Division income was down primarily as a result of a market related decrease in the value of assets under management.

Noninterest expense is comprised of salaries, employee benefits, occupancy and equipment expense and other operating expenses incurred in supporting the various business activities of the Corporation. Noninterest expense was $35.8 million and $34.8 million in 2010 and 2009, respectively, representing increases over prior year amounts of $986,000, or 2.8%, and $5.2 million, or 17.3%.

The increase in noninterest expense in 2010 is comprised of increases in salaries of $589,000, or 4.0%, occupancy and equipment expense of $461,000, or 7.7%, and other operating expenses of $460,000, or 5.7%, as partially offset by a decrease in employee benefits of $524,000, or 9.0%. The increase in salaries expense is primarily due to normal annual salary adjustments and additions to staff related to the opening of four full service branches during 2010. Occupancy and equipment expense increased primarily due to branch expansion, technology upgrades and the creation of a state-of-the-art disaster recovery center for both information technology and back office functions. The increase in other operating expenses is the result of a $221,000 increase in data processing expense and a number of other small increases, as partially offset by a $279,000 decrease in FDIC deposit insurance expense from $2.2 million in 2009 to $1.9 million this year. The decline in deposit insurance expense occurred because 2009 was burdened with a $647,000 FDIC special assessment. In February 2011, the FDIC approved a final rule which implements changes to the deposit insurance assessment system effective April 1, 2011. These changes include, among other things, basing deposit insurance assessments on average total assets less average tangible capital (rather than total deposits) and changing the assessment rate applicable to each risk category defined by the FDIC. Based on the Bank’s total asset and tangible capital levels at year end 2010 and, assuming that the Bank’s current FDIC risk category remains the same, the changes to the deposit insurance assessment system would reduce the Bank’s FDIC premiums by approximately $900,000 on an annual basis. However, management is concerned about the high level of bank failures that have occurred in the last two years and the resulting depletion of the FDIC deposit insurance fund. Management believes that continued bank failures could make it necessary for the FDIC to raise its assessment rates, impose additional special assessments or both.

19

The 2010 decrease in employee benefits expense is primarily the result of a decrease in retirement plan expense, as partially offset by increases in group health insurance. Retirement plan expense decreased due to additional funding of the Bank’s defined benefit pension plan and improved market performance of plan assets in 2009.

The increase in noninterest expense for 2009 was comprised of increases in other operating expenses of $2.1 million, or 33.8%, employee benefits expense of $1.2 million, or 26.7%, occupancy and equipment expense of $1.0 million, or 20.8%, and salaries of $832,000, or 5.9%. The increase in other operating expenses is largely attributable to a $1.6 million increase in FDIC deposit insurance expense caused by failures in the banking industry. Such failures resulted in an increase in the FDIC’s base assessment rates for 2009 and an industry wide special assessment of 5 basis points on total assets minus Tier 1 capital as of June 30, 2009. The special assessment cost the Bank approximately $647,000.

The increase in employee benefits expense for 2009 was largely the result of a $1.0 million increase in pension plan expense. The increase resulted from the poor performance of the equity markets in 2008. Occupancy and equipment expense increased primarily due to branch expansion, technology upgrades and maintenance of facilities. The increase in salaries expense is primarily due to normal annual salary adjustments and additions to staff related to branch expansion.

Income tax expense as a percentage of book income (“effective tax rate”) was 22.6% in 2010, 18.8% in 2009 and 26.3% in 2008. The effective tax rate was elevated in 2008 because the Corporation lost the tax benefit derived from its REIT entity. The loss of the REIT tax benefit resulted from a change in New York State tax law effective January 1, 2008. In December 2008, the ownership of the REIT entity within the consolidated group was changed to once again obtain favorable tax treatment. This change, combined with an increase in tax-exempt income, caused the effective tax rate to decrease in 2009. The effective tax rate increased in 2010 because tax-exempt income as a percentage of income before income taxes declined. Also contributing to the increase in the effective tax rate was the fact that the tax benefit derived from the Corporation’s FNY and REIT entities decreased somewhat in 2010 while income before income taxes increased significantly.

Application of Critical Accounting Policies

In preparing the consolidated financial statements, management is required to make estimates and assumptions that affect the reported asset and liability balances and revenue and expense amounts. Our determination of the allowance for loan losses is a critical accounting estimate because it is based on our subjective evaluation of a variety of factors at a specific point in time and involves difficult and complex judgments about matters that are inherently uncertain. In the event that management’s estimate needs to be adjusted based on, among other things, additional information that comes to light after the estimate is made or changes in circumstances, such adjustment could result in the need for a significantly different allowance for loan losses and thereby materially impact, either positively or negatively, the Bank’s results of operations.

The Bank’s Management Loan Committee, which is chaired by the Senior Lending Officer, meets on a quarterly basis and is responsible for determining the allowance for loan losses after considering, among other things, the results of credit reviews performed by the Bank’s loan review officer. In addition, and in consultation with the Bank’s Chief Financial Officer, the Management Loan Committee is responsible for implementing and maintaining policies and procedures surrounding the calculation of the required allowance. The Bank’s allowance for loan losses is reviewed by the Loan Committee of the Board of Directors and is subject to periodic examination by the Office of the Comptroller of the Currency, the Bank’s primary federal banking regulator, whose safety and soundness examination includes a determination as to its adequacy to absorb probable incurred losses.

The first step in determining the allowance for loan losses is to identify loans in the Bank’s portfolio that are individually deemed to be impaired. In doing so, subjective judgments need to be made regarding whether or not it is probable that a borrower will be unable to pay all principal and interest due according to contractual terms. Once a loan is identified as being impaired, management uses the fair value of the underlying collateral and/or the discounted value of expected future cash flows to determine the amount of the impairment loss, if any, that needs to be included in the overall allowance for loan losses. In estimating the fair value of real estate collateral, management utilizes appraisals and also makes qualitative judgments based on, among other things, its knowledge of the local real estate market and analyses of current economic conditions and trends. Estimating the fair value of collateral other than real estate is also subjective in nature and sometimes requires difficult and complex judgments. Determining expected future cash flows can be more subjective than determining fair values. Expected future cash flows could differ significantly, both in timing and amount, from the cash flows actually received over the loan’s remaining life.

20

In addition to estimating losses for loans individually deemed to be impaired, management also estimates collective impairment losses for pools of loans that are not specifically reviewed. Statistical information regarding the Bank’s historical loss experience over a period of time is the starting point in making such estimates. However, future losses could vary significantly from those experienced in the past and on a quarterly basis management adjusts its historical loss experience to reflect current conditions. In doing so, management considers a variety of general qualitative factors and then subjectively determines the weight to assign to each in estimating losses. The factors include, among others, loan risk ratings, national and local economic conditions and trends, environmental risks, trends in volume and terms of loans, concentrations of credit, changes in lending policies and procedures, changes in the quality of the Bank’s loan review function, and experience, ability, and depth of the Bank’s lending staff. Because of the nature of the factors and the difficulty in assessing their impact, management’s resulting estimate of losses may not accurately reflect actual losses in the portfolio.

Although the allowance for loan losses has two separate components, one for impairment losses on individual loans and one for collective impairment losses on pools of loans, the entire allowance for loan losses is available to absorb realized losses as they occur whether they relate to individual loans or pools of loans.

Asset Quality

The Corporation has identified certain assets as risk elements. These assets include nonaccruing loans, foreclosed real estate, loans that are contractually past due 90 days or more as to principal or interest payments and still accruing and troubled debt restructurings. These assets present more than the normal risk that the Corporation will be unable to eventually collect or realize their full carrying value. Information about the Corporation’s risk elements is as follows:

|

December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

(dollars in thousands)

|

||||||||||||||||||||

|

Nonaccrual loans (including loan held for sale)

|

$ | 3,936 | $ | 432 | $ | 112 | $ | 257 | $ | 135 | ||||||||||

|

Loans past due 90 days or more and still accruing

|

- | - | 42 | 95 | 50 | |||||||||||||||

|

Foreclosed real estate

|

- | - | - | - | - | |||||||||||||||

|

Total nonperforming assets

|

3,936 | 432 | 154 | 352 | 185 | |||||||||||||||

|

Troubled debt restructurings

|

2,433 | 200 | - | - | - | |||||||||||||||

|

Total risk elements

|

$ | 6,369 | $ | 632 | $ | 154 | $ | 352 | $ | 185 | ||||||||||

|

Nonaccrual loans as a percentage of total loans

|

.44 | % | .05 | % | .02 | % | .05 | % | .03 | % | ||||||||||

|

Nonperforming assets as a percentage of total loans and foreclosed real estate

|

.44 | % | .05 | % | .02 | % | .07 | % | .04 | % | ||||||||||

|

Risk elements as a percentage of total loans and foreclosed real estate

|

.70 | % | .08 | % | .02 | % | .07 | % | .04 | % | ||||||||||

|

Year Ended December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

(in thousands)

|

||||||||||||||||||||

|

Gross interest income on nonaccrual loans:

|

||||||||||||||||||||

|

Amount that would have been recorded during the year under original terms

|

$ 185 | $ 24 | $ 10 | $ 13 | $ 12 | |||||||||||||||

|

Actual amount recorded during the year

|

156 | 16 | - | 10 | - | |||||||||||||||

|

Commitments for additional funds - troubled debt restructurings

|

None

|

None

|

None

|

None

|

None

|

|||||||||||||||

21

Allowance and Provision for Loan Losses

The allowance for loan losses increased by $3.7 million during 2010, amounting to $14.0 million, or 1.55% of total loans, at December 31, 2010 as compared to $10.3 million, or 1.25% of total loans, at December 31, 2009. During 2010, the Bank had loan chargeoffs and recoveries of $377,000 and $72,000, respectively, and recorded a $4.0 million provision for loan losses. Although the provision for loan losses decreased by $312,000 when comparing 2010 to 2009, the provision in both years was elevated versus prior years. The elevated provisioning in 2010 was primarily attributable to: (1) management’s decision to increase the Bank’s allowance for loan losses relative to gross loans in recognition of, among other things, unfavorable economic conditions and the large concentration of real estate loans in the Bank’s portfolio; (2) the establishment of an $870,000 impairment reserve on one nonaccruing loan; and (3) a $300,000 chargeoff upon the transfer of one nonaccruing loan to the held-for-sale category. The elevated provisioning in 2009 was also primarily attributable to unfavorable economic conditions and the Bank’s large real estate loan concentration and, additionally, robust loan growth.

The allowance for loan losses is an amount that management currently believes will be adequate to absorb probable incurred losses in the Bank’s loan portfolio. As more fully discussed in the “Application of Critical Accounting Policies” section of this discussion and analysis of financial condition and results of operations, the process for estimating credit losses and determining the allowance for loan losses as of any balance sheet date is subjective in nature and requires material estimates. Actual results could differ significantly from those estimates.

The following table sets forth changes in the Bank’s allowance for loan losses.

|

Year ended December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

(dollars in thousands)

|

||||||||||||||||||||

|

Balance, beginning of year

|

$ | 10,346 | $ | 6,076 | $ | 4,453 | $ | 3,891 | $ | 3,282 | ||||||||||

|

Loans charged off:

|

||||||||||||||||||||

|

Commercial and industrial

|

- | 162 | 275 | - | 65 | |||||||||||||||

|

Commercial mortgages

|

325 | - | - | - | - | |||||||||||||||

|

Residential mortgages

|

22 | - | - | - | - | |||||||||||||||

|

Other

|

30 | 13 | 50 | 14 | 11 | |||||||||||||||

| 377 | 175 | 325 | 14 | 76 | ||||||||||||||||

|

Recoveries of loans charged off:

|

||||||||||||||||||||

|

Commercial and industrial

|

46 | 148 | - | - | - | |||||||||||||||

|

Other

|