Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - PREFORMED LINE PRODUCTS CO | c13813exv21.htm |

| EX-32.1 - EXHIBIT 32.1 - PREFORMED LINE PRODUCTS CO | c13813exv32w1.htm |

| EX-31.2 - EXHIBIT 31.2 - PREFORMED LINE PRODUCTS CO | c13813exv31w2.htm |

| EX-31.1 - EXHIBIT 31.1 - PREFORMED LINE PRODUCTS CO | c13813exv31w1.htm |

| EX-23.1 - EXHIBIT 23.1 - PREFORMED LINE PRODUCTS CO | c13813exv23w1.htm |

| EX-32.2 - EXHIBIT 32.2 - PREFORMED LINE PRODUCTS CO | c13813exv32w2.htm |

| EX-10.15 - EXHIBIT 10.15 - PREFORMED LINE PRODUCTS CO | c13813exv10w15.htm |

| EX-10.16 - EXHIBIT 10.16 - PREFORMED LINE PRODUCTS CO | c13813exv10w16.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2010

Commission file number 0-31164

Preformed Line Products Company

(Exact name of registrant as specified in its charter)

| Ohio | 34-0676895 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 660 Beta Drive Mayfield Village, Ohio |

44143 | |

| (Address of Principal Executive Office) | (Zip Code) |

(440) 461-5200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Shares, $2 par value per share | NASDAQ |

Securities registered pursuant to Section 12(g) of the Act: (None)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of

the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or

Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by

Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports) and (2) has been subject

to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its

corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (S232.405 of this chapter) during the preceding 12

months (or for such shorter period that the registrant was required to submit and post such

files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is

not contained herein, and will not be contained, to the best of the registrant’s knowledge, in

definitive proxy or information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, or a smaller reporting company. See definitions of “accelerated filer,”

“large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange act.

| Large accelerated filer o | Accelerated filer þ | Non-accelerated filer o | Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the

Exchange Act). Yes o No þ

The aggregate market value of voting and non-voting common shares held by non-affiliates of the

registrant as of June 30, 2010 was $61,224,698 based on the closing price of such common shares, as

reported on the NASDAQ National Market System. As of March 9, 2011, there were 5,272,804 common

shares of the Company ($2 par value) outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement for the Annual Meeting of Shareholders to be held April

25, 2011 are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14.

Table of Contents

| Page | ||||||||

| 4 | ||||||||

| 13 | ||||||||

| 14 | ||||||||

| 15 | ||||||||

| 16 | ||||||||

| 16 | ||||||||

| 17 | ||||||||

| 19 | ||||||||

| 19 | ||||||||

| 35 | ||||||||

| 36 | ||||||||

| 68 | ||||||||

| 68 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 70 | ||||||||

| 73 | ||||||||

| 74 | ||||||||

| Exhibit 10.15 | ||||||||

| Exhibit 10.16 | ||||||||

| Exhibit 21 | ||||||||

| Exhibit 23.1 | ||||||||

| Exhibit 31.1 | ||||||||

| Exhibit 31.2 | ||||||||

| Exhibit 32.1 | ||||||||

| Exhibit 32.2 | ||||||||

2

Table of Contents

Forward-Looking Statements

This Form 10-K and other documents we file with the Securities and Exchange Commission (“SEC”)

contain forward-looking statements regarding Preformed Line Products Company’s (the “Company”) and

management’s beliefs and expectations. As a general matter, forward-looking statements are those

focused upon future plans, objectives or performance (as opposed to historical items) and include

statements of anticipated events or trends and expectations and beliefs relating to matters not

historical in nature. Such forward-looking statements are subject to uncertainties and factors

relating to the Company’s operations and business environment, all of which are difficult to

predict and many of which are beyond the Company’s control. Such uncertainties and factors could

cause the Company’s actual results to differ materially from those matters expressed in or implied

by such forward-looking statements.

The following factors, among others, could affect the Company’s future performance and cause

the Company’s actual results to differ materially from those expressed or implied by

forward-looking statements made in this report:

| • | The overall demand for cable anchoring and control hardware for electrical transmission and distribution lines on a worldwide basis, which has a slow growth rate in mature markets such as the United States (U.S.), Canada, and Western Europe and may not grow as expected in developing regions; | ||

| • | The ability of our customers to raise funds needed to build the facilities their customers require; | ||

| • | Technological developments that affect longer-term trends for communication lines such as wireless communication; | ||

| • | The decreasing demands for product supporting copper-based infrastructure due to the introduction of products using new technologies or adoption of new industry standards; | ||

| • | The Company’s success at continuing to develop proprietary technology and maintaining high quality products and customer service to meet or exceed new industry performance standards and individual customer expectations; | ||

| • | The Company’s success in strengthening and retaining relationships with the Company’s customers, growing sales at targeted accounts and expanding geographically; | ||

| • | The extent to which the Company is successful in expanding the Company’s product line or production facilities into new areas; | ||

| • | The Company’s ability to identify, complete and integrate acquisitions for profitable growth; | ||

| • | The potential impact of consolidation, deregulation and bankruptcy among the Company’s suppliers, competitors and customers; | ||

| • | The relative degree of competitive and customer price pressure on the Company’s products; | ||

| • | The cost, availability and quality of raw materials required for the manufacture of products; | ||

| • | The effects of fluctuation in currency exchange rates upon the Company’s reported results from international operations, together with non-currency risks of investing in and conducting significant operations in foreign countries, including those relating to political, social, economic and regulatory factors; | ||

| • | Changes in significant government regulations affecting environmental compliances; | ||

| • | The telecommunication market’s continued deployment of Fiber-to-the-Premises; |

3

Table of Contents

| • | The Company’s ability to obtain funding for future acquisitions; | ||

| • | The potential impact of the global economic condition and the depressed U.S. housing market on the Company’s ongoing profitability and future growth opportunities in our core markets in the U.S. and other foreign countries where the financial situation is expected to be similar going forward; | ||

| • | The continued support by Federal, State, Local and Foreign Governments in incentive programs for upgrading electric transmission lines and promoting renewable energy deployment; | ||

| • | Those factors described under the heading “Risk Factors” on page 13. |

Part I

| Item 1. | Business |

Background

Preformed Line Products Company and its subsidiaries (the “Company”) is an international

designer and manufacturer of products and systems employed in the construction and maintenance of

overhead and underground networks for the energy, telecommunication, cable operators, information

(data communication) and other similar industries. The Company’s primary products support,

protect, connect, terminate and secure cables and wires. The Company also provides solar hardware

systems and mounting hardware for a variety of solar power applications. The Company’s goal is to

continue to achieve profitable growth as a leader in the innovation, development, manufacture and

marketing of technically advanced products and services related to energy, communications and cable

systems and to take advantage of this leadership position to sell additional quality products in

familiar markets.

The Company serves a worldwide market through strategically located domestic and international

manufacturing facilities. Each of the Company’s domestic and international manufacturing

facilities have obtained an International Organization of Standardization (“ISO”) 9001:2000

Certified Management System, with the exception of Direct Power and Water Corporation (DPW), which

was acquired during 2007. The ISO 9001:2000 certified management system is a globally recognized

quality standard for manufacturing and assists the Company in marketing its products throughout the

world. The Company’s customers include public and private energy utilities and communication

companies, cable operators, financial institutions, governmental agencies, contractors and

subcontractors, distributors and value-added resellers. The Company is not dependent on a single

customer or a few customers. No single customer accounts for more than ten percent of the

Company’s consolidated revenues.

The Company’s products include:

| • | Formed Wire and Related Hardware Products |

| • | Protective Closures |

| • | Data Communication Cabinets |

| • | Plastic Products |

| • | Other Products |

Formed Wire Products and Related Hardware Products are used in the energy, communications,

cable and special industries to support, protect, terminate and secure both power conductor and

communication cables and to control cable dynamics (e.g., vibration). Formed wire products are

based on the principle of forming a variety of stiff wire materials into a helical (spiral) shape.

Advantages of using the Company’s helical formed wire products are that they are economical,

dependable and easy to use. The Company introduced formed wire products to the power industry over

60 years ago and such products enjoy an almost universal acceptance in the Company’s markets.

Related hardware products include hardware for supporting and protecting transmission conductors,

spacers, spacer-dampers, stockbridge dampers, corona suppression devices and various compression

fittings for

dead-end applications. Formed wire and related hardware products are approximately 65% of the

Company’s revenues in 2010, 62% in 2009 and 59% in 2008.

4

Table of Contents

Protective Closures, including splice cases, are used to protect fixed line communication

networks, such as copper cable or fiber optic cable, from moisture, environmental hazards and other

potential contaminants. Protective closures are approximately 17% of the Company’s revenues in

2010, 22% in 2009 and 24% in 2008.

Data Communication Cabinets are products used in high-speed data systems to hold and protect

electronic equipment. Data communication cabinets are approximately 4% of the Company’s revenues

in 2010 and 2009 and 5% in 2008.

Plastic Products, including guy markers, tree guards, fiber optic cable markers and pedestal

markers, are used in energy, communications, cable television and special industries to identify

power conductors, communication cables and guy wires. Plastic products are approximately 3% of the

Company’s revenues in 2010, 2009 and 2008.

Other Products include hardware assemblies, pole line hardware, resale products, underground

connectors, solar hardware systems and urethane products. They are used by energy, renewable

energy, communications, cable and special industries for various applications and are defined as

products that compliment the Company’s core line offerings. Other products are approximately 11%

of the Company’s revenues in 2010, 9% in 2009 and 5% in 2008.

Corporate History

The Company was incorporated in Ohio in 1947 to manufacture and sell helically shaped “armor

rods” which are sets of stiff helically shaped wires applied on an electrical conductor at the

point where it is suspended or held. Thomas F. Peterson, the Company’s founder, developed and

patented a unique method to manufacture and apply these armor rods to protect electrical conductors

on overhead power lines. Over a period of years, Mr. Peterson and the Company developed, tested,

patented, manufactured and marketed a variety of helically shaped products for use by the

electrical and telephone industries. Although all of Mr. Peterson’s patents have now expired,

those patents served as the nucleus for licensing the Company’s formed wire products abroad.

The success of the Company’s formed wire products in the U.S. led to expansion abroad. The

first international license agreement was established in the mid-1950s in Canada. In the late

1950s the Company’s products were being sold through joint ventures and licensees in Canada,

England, Germany, Spain and Australia. Additionally, the Company began export operations and

promoted products into other selected offshore markets. The Company continued its expansion

program, bought out most of the original licensees, and, by the mid-1990s, had complete ownership

of operations in Australia, Brazil, Canada, Great Britain, South Africa and Spain and held a

minority interest in two joint ventures in Japan. The Company’s international subsidiaries have

the necessary infrastructure (i.e. manufacturing, engineering, marketing and general management) to

support local business activities. Each is staffed with local personnel to ensure that the Company

is well versed in local business practices, cultural constraints, technical requirements and the

intricacies of local client relationships.

In 1968, the Company expanded into the underground telecommunications field by its acquisition

of the Smith Company located in California. The Smith Company had a patented line of buried

closures and pressurized splice cases. These closures and splice cases protect copper cable

openings from environmental damage and degradation. The Company continued to build on expertise

acquired through the acquisition of the Smith Company and in 1995 introduced the highly successful

COYOTEâ Closure line of products. Since 1995 fourteen domestic and three international

patents have been granted to the Company on the COYOTE Closure. None of the COYOTE Closure patents

have expired. The earliest COYOTE Closure patent was filed April 1995 and will not expire until

April 2015.

In 1993, the Company purchased the assets of Superior Modular Products Company,located in

Asheville, North Carolina.

Recognizing the need for a stronger presence in the fast growing Asian market, in 1996 the

Company formed a joint venture in China and, in 2000, became sole owner of this venture.

5

Table of Contents

In 2000, the Company acquired Rack Technologies Pty. Ltd, headquartered in Sydney, Australia.

Rack Technologies was a specialist manufacturer of rack system enclosures for the communications,

electronics and securities industries. This acquisition complemented and broadens the Company’s

existing line of data communication products used inside a customer’s premises.

In 2002, the Company acquired the remaining 2.6% minority interest in its operations in

Mexico. The 97.4% interest was acquired in 1969.

In 2003, the Company sold its 24% interest in Toshin Denko Kabushiki Kaisha in Osaka, Japan.

The Company’s investment in Toshin Denko dated back to 1961 when the joint venture company was

founded.

In 2004, the Company acquired the assets of Union Electric Manufacturing Co. Ltd, located in

Bangkok, Thailand.

In 2004, the Company sold its 49% interest in Japan PLP Co. Ltd., a joint venture in Japan.

In 2007, the Company acquired the shares of DPW, located in New Mexico, U.S. This acquisition

broadened the Company’s product lines and manufactures mounting hardware for a variety of solar

power applications and provides designs and installations of solar power systems.

In 2007, the Company acquired 83.74% of Belos SA (Belos), located in Bielsko-Biala, Poland.

Belos is a manufacturer and supplier of fittings for various voltage power networks. This

acquisition complements the Company’s existing line of energy products. In 2008, the Company

acquired an additional 8.3% of the outstanding shares of Belos. In 2009, the Company acquired an

additional 4.1% of the outstanding shares of Belos. In 2010, the Company acquired the remaining

3.86% of the outstanding shares of Belos.

In 2008, the Company divested its data communication business, Superior Modular Products.

In 2008, the Company formed a joint venture between the Company’s Australian subsidiary,

Preformed Line Products Australia Pty Ltd (PLP-AU) and BlueSky Energy Pty Ltd, a solar systems

integration and installation business based in Sydney, Australia. PLP-AU holds a 50% ownership

interest in the joint venture company, which operates under the name BlueSky Energy Australia

(BlueSky), with the option to acquire the remaining 50% ownership interest from BlueSky Energy Pty

Ltd over the next five years.

In 2009, the Company acquired a 33.3% investment in Proxisafe Ltd. Proxisafe is a Canadian

developmental company formed to design and commercialize new industrial safety equipment located in

Calgary, Alberta.

In 2009, the Company acquired the Dulmison business from Tyco Electronics Group S.A. (Tyco

Electronics), which includes both the acquisition of equity of certain Tyco Electronics entities

and the acquisition of assets from other Tyco Electronics entities. Dulmison was a leader in the

supply and manufacturer of electrical transmission and distribution products. Dulmison designed,

manufactured and marketed pole line hardware and vibration control products for the global

electrical utility industry. Dulmison had operations in Australia, Thailand, Indonesia, Malaysia,

Mexico and the United States. The Dulmison business has been fully integrated into the Company’s

core businesses.

In 2010, the Company acquired Electropar Limited (Electropar), a New Zealand corporation.

Electropar designs, manufactures and markets pole line and substation hardware for the global

electrical utility industry. Electropar is based in New Zealand with a subsidiary operation in

Australia. The acquisition has and is expected to continue to strengthen the Company’s position in

the power distribution, transmission and substation hardware markets and will expand the Company’s

presence in the Asia-Pacific region.

The Company’s World headquarters is located at 660 Beta Drive, Mayfield Village, Ohio 44143.

6

Table of Contents

Business

The demand for the Company’s products comes primarily from new, maintenance and repair

construction for the energy, telecommunication and data communication industries. The Company’s

customers use many of the Company’s products, including formed wire products, to revitalize the

aging outside plant infrastructure. Many of the Company’s products are used on a proactive basis

by the Company’s customers to reduce and prevent lost revenue. A single malfunctioning line could

cause the loss of thousands of dollars per hour for a power or communication customer. A

malfunctioning fiber cable could also result in substantial revenue loss. Repair construction by

the Company’s customers generally occurs in the case of emergencies or natural disasters, such as

hurricanes, tornadoes, earthquakes, floods or ice storms. Under these circumstances, the Company

provides 24-hour service to provide the repair products to customers as quickly as possible.

The Company has adapted the formed wire products’ helical technology for use in a wide variety

of fiber optic cable applications that have special requirements. The Company’s formed wire

products are uniquely qualified for these applications due to the gentle gripping over a greater

length of the fiber cable. This is an advantage over traditional pole line hardware clamps that

compress the cable to the point of possible fatigue and optical signal deterioration.

The Company’s protective closures and splice cases are used to protect cable from moisture,

environmental hazards and other potential contaminants. The Company’s splice cases are easily

re-enterable closures that allow utility maintenance workers access to the cables located inside

the closure to repair or add communications services. Over the years, the Company has made many

significant improvements in the splice case that have greatly increased their versatility and

application in the market place. The Company also designs and markets custom splice cases to

satisfy specific customer requirements. This has allowed the Company to remain a strong partner

with several primary customers and has earned the Company the reputation as a responsive and

reliable supplier.

Fiber optic cable was first deployed in the outside plant environment in the early 1980s.

Through fiber optic technologies, a much greater amount of both voice and data communication can be

transmitted reliably. In addition, this technology solved the cable congestion problem that the

large count copper cable was causing in underground, buried and aerial applications. The Company

developed and adapted copper closures for use in the emerging fiber optic world. In the late

1980s, the Company developed a series of splice cases designed specifically for fiber application.

In the mid-1990s, the Company developed its plastic COYOTE Closure, and has since expanded the

product line to address Fiber-to-the-Premise (FTTP) applications. The COYOTE Closure is an example

of the Company developing a new line of proprietary products to meet the changing needs of its

customers.

The Company also designs and manufactures data communication cabinets and enclosures for data

communication networks, offering a comprehensive line of copper and fiber optic cross-connect

systems. The product line enables reliable, high-speed transmission of data over customers’ local

area networks.

With the acquisition of DPW in 2007, the Company expanded into the fast growing renewable

energy sector. DPW provides a comprehensive line of mounting hardware for a variety of solar power

applications including residential roof mounting, commercial roofing systems, top of pole mounting

and customized solutions. DPW also provides design and installation services for residential and

commercial solar power systems primarily in the western U.S.

Markets

The Company markets its products to the energy, telecommunication, cable, data communication

and special industries. While rapid changes in technology have blurred the distinctions between

telephone, cable, and data communication, the energy industry is clearly distinct. The Company’s

role in the energy industry is to supply formed wire products and related hardware used with the

electrical conductors, cables and wires that transfer power from the generating facility to the

ultimate user of that power. Formed wire products are used to support, protect, terminate and

secure both power conductor and communication cables and to control cable dynamics.

7

Table of Contents

Electric Utilities — Transmission. The electric transmission grid is the interconnected

network of high voltage aluminum conductors used to transport large blocks of electric power from

generating facilities to

distribution networks. Currently, there are three major power grids in the U.S.: the Eastern

Interconnect, the Western Interconnect and the Texas Interconnect. Virtually all electrical energy

utilities are connected with at least one other utility by one of these major grids. The Company

believes that the transmission grid has been neglected throughout much of the U.S. for more than a

decade. Additionally, because of deregulation, some electric utilities have turned this

responsibility over to Independent System Operators (ISOs), who have also been slow to add

transmission lines. With demand for power now exceeding supply in some areas, the need for the

movement of bulk power from the energy-rich areas to the energy-deficient areas means that new

transmission lines will likely be built and many existing lines will likely be refurbished. In

addition, passage of the economic stimulus bill in early 2009 that contains provisions for

upgrading the aging transmission infrastructure and connecting renewable energy sources to the grid

should attract new investment to fund new infrastructure projects in the industry. The Company

believes that this will generate growth for the Company’s products in this market over at least the

next several years. In addition, increased construction of international transmission grids is

occurring in many regions of the world. However, consolidations in the markets that the Company

services’ may also have an adverse impact on the Company’s revenues.

Electric Utilities — Distribution. The distribution market includes those utilities that

distribute power from a substation where voltage is reduced to levels appropriate for the consumer.

Unlike the transmission market, distribution is still handled primarily by local electric

utilities. These utilities are motivated to reduce cost in order to maintain and enhance their

profitability. The Company believes that its growth in the distribution market will be achieved

primarily as a result of incremental gains in market share driven by emphasizing the Company’s

quality products and service over price. Internationally, particularly in the developing regions,

there is increasing political pressure to extend the availability of electricity to additional

populations. Through its global network of factories and sales offices, the Company is prepared to

take advantage of this new growth in construction.

Renewable Energy. The renewable energy market includes residential consumers, commercial

businesses, off-grid operators, and utility companies that have an interest in alternative energy

sources. Environmental concerns along with federal, state, and local utility incentives have

fueled demand for renewable energy systems including solar, wind, and biofuel. The industry

continues to grow rapidly as advancements in technology lead to greater efficiencies which drive

down overall system costs. The Company currently provides hardware solutions, system design and

installation services for solar power applications. The Company markets and sells these products

and services to end-users, distributors, installers and integrators.

Communication and Cable. Major developments, including growing competition between the cable

and communications industries and increasing overall demand for high-speed communication services,

have led to a changing regulatory and competitive environment in many markets throughout the world.

The deployment of new access networks and improvements to existing networks for advanced

applications continues to gain momentum.

Cable operators, local communication operators and power utilities are building, rebuilding or

upgrading signal delivery networks in developed countries. These networks are designed to deliver

video and voice transmissions and provide Internet connectivity to individual residences and

businesses. Operators deploy a variety of network technologies and architectures to carry

broadband and narrowband signals. These architectures are constructed of electronic hardware

connected via coaxial cables, copper wires or optical fibers. The Company manufactures closures

that these industries use to securely connect and protect these vital networks.

As critical components of the outdoor infrastructure, closures provide protection against

weather and vandalism, and permit technicians who maintain and manage the system ready access to

the devices. Cable operators and local telephone network operators place great reliance on

manufacturers of protective closures because any material damage to the signal delivery networks is

likely to disrupt communication services. In addition to closures, the Company supplies the

communication and cable industry with its formed wire products to hold, support, protect and

terminate the copper wires and cables and the fiber optic cables used by that industry to transfer

voice, video or data signals.

The industry has developed technological methods to increase the usage of copper-based plant

through high-speed digital subscriber lines (DSLs). The popularity of these services, the

regulatory environment and the increasingly fierce competition between communications and cable

operators has driven the move toward building out the “last mile” in fiber networks. FTTP

technology supports the next wave in broadband innovation by carrying

fiber optic technology into homes and businesses. The Company has been actively developing

products that address this market.

8

Table of Contents

Data Communication. The data communication market is being driven by the continual demand for

increased bandwidth. Growing Internet Service Providers (ISPs), construction in Wide Area Networks

(WANs) and demand for products in the workplace are all key elements to the increased demand for

the connecting devices made by the Company. The Company’s products are sold to a number of

categories of customers including, (i) ISPs, (ii) large companies and organizations which have

their own local area network for data communication, and (iii) distributors of structured cabling

systems and components for use in the above markets.

Special Industries. The Company’s formed wire products are also used in other industries

which require a method of securing or terminating cables, including the metal building, tower and

antenna industries, the arborist industry, and various applications within the marine systems

industry. Products other than formed wire products are also marketed to other industries. For

example, the Company’s urethane capabilities allow it to market products to the light rail

industry. The Company continues to explore new and innovative uses of its manufacturing

capabilities; however, these markets remain a small portion of overall consolidated sales.

International Operations

The international operations of the Company are essentially the same as its domestic (PLP-USA)

business. The Company manufactures similar types of products in its international plants as are

sold domestically, sells to similar types of customers and faces similar types of competition (and

in some cases the same competitors). Sources of supply of raw materials are not significantly

different internationally. See Note K in the Notes To Consolidated Financial Statements for

information and financial data relating to the Company’s international operations that represent

reportable segments.

While a number of the Company’s international plants are in developed countries, the Company

believes it has strong market opportunities in developing countries where the need for the

transmission and distribution of electrical power is significant. The Company is now serving the

Far East market, other than China and Japan, primarily from Thailand and Indonesia. In addition,

as the need arises, the Company is prepared to establish new manufacturing facilities abroad.

Sales and Marketing

Domestically and internationally, the Company markets its products through a direct sales

force and manufacturing representatives. The direct sales force is employed by the Company and

works with the manufacturer’s representatives, as well as key direct accounts and distributors who

also buy and resell the Company’s products. The manufacturer’s representatives are independent

organizations that represent the Company as well as other complimentary product lines. These

organizations are paid a commission based on the sales amount.

Research and Development

The Company is committed to providing technical leadership through scientific research and

product development in order to continue to expand the Company’s position as a supplier to the

communications and power industries. Research is conducted on a continuous basis using internal

experience in conjunction with outside professional expertise to develop state-of-the-art materials

for several of the Company’s products. These products capitalize on cost-efficiency while offering

exacting mechanical performance that meets or exceeds industry standards. The Company’s research

and development activities have resulted in numerous patents being issued to the Company (see

“Patents and Trademarks” below).

Early in its history, the Company recognized the need to understand the performance of its

products and the needs of its customers. To that end, the Company developed a 29,000 square feet

Research and Engineering Center located at its corporate headquarters in Mayfield Village, Ohio.

Using the Research and Engineering Center, engineers and technicians simulate a wide range of

external conditions encountered by the Company’s products to ensure quality, durability and

performance. The work performed in the Research and Engineering Center includes

advanced studies and experimentation with various forms of vibration. This work has contributed

significantly to the collective knowledge base of the industries the Company serves and is the

subject matter of many papers and seminars presented to these industries.

9

Table of Contents

The Company believes that its Research and Engineering Center is one of the most sophisticated

in the world in its specialized field. The expanded Research and Engineering Center also has an

advanced prototyping technology machine on-site to develop models of new designs where intricate

part details are studied prior to the construction of expensive production tooling. Today, the

Company’s reputation for vibration testing, tensile testing, fiber optic cable testing,

environmental testing, field vibration monitoring and third-party contract testing is a competitive

advantage. In addition to testing, the work done at the Company’s Research and Development Center

continues to fuel product development efforts. For example, the Company estimates that

approximately 18% of 2010 revenues were attributed to products developed by the Company in the past

five years. In addition, the Company’s position in the industry is further reinforced by its

long-standing leadership role in many key international technical organizations which are charged

with the responsibility of establishing industry wide specifications and performance criteria,

including IEEE (Institute of Electrical and Electronics Engineers), CIGRE (Counsiel Internationale

des Grands Reseaux Electriques a Haute Tension), and IEC (International Electromechanical

Commission). Research and development costs are expensed as incurred. Research and development

costs for new products were $1.7 million in 2010, $2.3 million in 2009 and $2 million in 2008.

Patents and Trademarks

The Company applies for patents in the U.S. and other countries, as appropriate, to protect

its significant patentable developments. As of December 31, 2010, the Company had in force 32 U.S.

patents and 67 international patents in 11 countries and had pending six U.S. patent applications

and 24 international applications. While such domestic and international patents expire from time

to time, the Company continues to apply for and obtain patent protection on a regular basis.

Patents held by the Company in the aggregate are of material importance in the operation of the

Company’s business. The Company, however, does not believe that any single patent, or group of

related patents, is essential to the Company’s business as a whole or to any of its businesses.

Additionally, the Company owns and uses a substantial body of proprietary information and numerous

trademarks. The Company relies on nondisclosure agreements to protect trade secrets and other

proprietary data and technology. As of December 31, 2010, the Company had obtained U.S.

registration on 31 trademarks and no trademark applications remained pending. International

registrations amounted to 229 registrations in 38 countries, with no pending international

registrations.

Since June 8, 1995, U.S. patents have been issued for terms of 20 years beginning with the

date of filing of the patent application. Prior to that time, a U.S. patent had a term of 17 years

from the date of its issuance. Patents issued by international countries generally expire 20 years

after filing. U.S. and international patents are not renewable after expiration of their initial

term. U.S. and international trademarks are generally perpetual, renewable in 10-year increments

upon a showing of continued use. To the knowledge of management, the Company has not been subject

to any significant allegation or charges of infringement of intellectual property rights by any

organization.

In the normal course of business, the Company occasionally makes and receives inquiries with

regard to possible patent and trademark infringement. The extent of such inquiries from third

parties has been limited generally to verbal remarks to Company representatives. The Company

believes that it is unlikely that the outcome of these inquiries will have a material adverse

effect on the Company’s financial position.

10

Table of Contents

Competition

All of the markets that the Company serves are highly competitive. In each market, the

principal methods of competition are price, performance, and service. The Company believes,

however, that several factors (described below) provide the Company with a competitive advantage.

| • | The Company has a strong and stable workforce. This consistent and continuous knowledge base has afforded the Company the ability to provide superior service to the Company’s customers and representatives. |

| • | The Company’s Research and Engineering Center in Mayfield Village, Ohio and Research and Engineering department’s subsidiary locations maintain a strong technical support function to develop unique solutions to customer problems. |

| • | The Company is vertically integrated both in manufacturing and distribution and is continually upgrading equipment and processes. |

| • | The Company is sensitive to the marketplace and provides an extra measure of service in cases of emergency, storm damage and other rush situations. This high level of customer service and customer responsiveness is a hallmark of the Company. |

| • | The Company’s 17 manufacturing locations ensure close support and proximity to customers worldwide. |

Domestically, there are several competitors for formed wire products. Although it has other

competitors in many of the countries where it has plants, the Company has leveraged its expertise

and is very strong in the global market. The Company believes that it is the world’s largest

manufacturer of formed wire products for energy and communications markets. However, the Company’s

formed wire products compete against other pole line hardware products manufactured by other

companies.

Minnesota Manufacturing and Mining Company (“3M”) is the primary domestic competitor of the

Company for pressurized copper closures. Based on its experience in the industry, the Company

believes it maintains a strong market share position.

The fiber optic closure market is one of the most competitive product areas for the Company,

with the Company competing against, among others, Tyco International Ltd., 3M and Corning Cable

Systems. There are a number of primary competitors and several smaller niche competitors that

compete at all levels in the marketplace. The Company believes that it is one of four leading

suppliers of fiber optic closures.

The Company’s data communication competitors range from assemblers of low cost, low quality

components, to well-established multinational corporations. The Company’s competitive strength is

its technological leadership and manufacturing expertise.

Sources and Availability of Raw Materials

The principal raw materials used by the Company are galvanized wire, stainless steel, aluminum

covered steel wire, aluminum re-draw rod, plastic resins, glass-filled plastic compounds, neoprene

rubbers and aluminum castings. The Company also uses certain other materials such as fasteners,

packaging materials and communications cable. The Company believes that it has adequate sources of

supply for the raw materials used in its manufacturing processes and it regularly attempts to

develop and maintain sources of supply in order to extend availability and encourage competitive

pricing of these products.

Most plastic resins are purchased under contracts to stabilize costs and improve delivery

performance and are available from a number of reliable suppliers. Wire and re-draw rod are

purchased in standard stock diameters and coils under contracts from a number of reliable

suppliers. Contracts have firm prices except for fluctuations of base metals and petroleum prices,

which result in surcharges when global demand is greater than the available supply.

The Company also relies on certain other manufacturers to supply products that complement the

Company’s product lines, such as aluminum and ferrous castings, fiber optic cable and connectors

and various metal racks and cabinets. The Company believes there are multiple sources of supply

for these products.

11

Table of Contents

The Company relies on sole source manufacturers for certain raw materials used in production.

The current state of economic uncertainty presents a risk that existing suppliers could go out of

business. However, there are

other potential sources for these materials available, and the Company could relocate the

tooling and processes to other manufacturers if necessary.

Due to capacity constraints and increased worldwide demand, raw material costs increased

throughout 2010. This increasing trend is expected to continue throughout 2011.

Backlog Orders

The Company’s backlog was approximately $59.1 million at the end of 2010 and $38 million at

the end of 2009. The Company’s order backlog generally represents six to nine weeks of sales. All

customer orders entered are firm at the time of entry. Substantially all orders are shipped within

a two to four week period unless the customer requests an alternative date.

Seasonality

The Company markets products that are used by utility maintenance and construction crews

worldwide. The products are marketed through distributors and directly to end users, who maintain

stock to ensure adequate supply for their customers or construction crews. As a result, the

Company does not have a wide variation in sales from quarter to quarter.

Environmental

The Company is subject to extensive and changing federal, state, and local environmental laws,

including laws and regulations that (i) relate to air and water quality, (ii) impose limitations on

the discharge of pollutants into the environment, (iii) establish standards for the treatment,

storage and disposal of toxic and hazardous waste, and (iv) require proper storage, handling,

packaging, labeling, and transporting of products and components classified as hazardous materials.

Stringent fines and penalties may be imposed for noncompliance with these environmental laws. In

addition, environmental laws could impose liability for costs associated with investigating and

remediating contamination at the Company’s facilities or at third-party facilities at which the

Company has arranged for the disposal treatment of hazardous materials.

The Company believes it is in compliance in all material respects, with all applicable

environmental laws and the Company is not aware of any noncompliance or obligation to investigate

or remediate contamination that could reasonably be expected to result in a material liability.

The Company does not expect to make any material capital expenditure during 2011 for environmental

control facilities. The environmental laws continue to be amended and revised to impose stricter

obligations, and compliance with future additional environmental requirements could necessitate

capital outlays. However, the Company does not believe that these expenditures should ultimately

result in a material adverse effect on its financial position or results of operations. The

Company cannot predict the precise effect such future requirements, if enacted, would have on the

Company. The Company believes that such regulations would be enacted over time and would affect

the industry as a whole.

Employees

At December 31, 2010, the Company had 2,617 employees. Approximately 31% of the Company’s

employees are located in the U.S.

Available Information

The Company maintains an Internet site at http://www.preformed.com, on which the Company makes

available, free of charge, the annual report on Form 10-K, quarterly reports on Form 10-Q, current

reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after

the Company electronically files such material with, or furnishes it to, the SEC. The Company’s

SEC reports can be accessed through the investor relations section of its Internet site. The

information found on the Company’s Internet site is not part of this or any other report that is

filed or furnished to the SEC.

12

Table of Contents

The public may read and copy any materials the Company files with or furnishes to the SEC at

the SEC’s Public Reference Room at 100 F. Street, NE., Washington, DC 20549. Information on the

operation of the Public Reference Room is available by calling the SEC at 1-800-SEC-0330. In

addition, the SEC maintains an Internet site that contains reports, proxy and information

statements, and other information filed with the SEC by electronic filers. The SEC’s Internet site

is http://www.sec.gov. The Company also has a link from its Internet site to the SEC’s Internet

site, this link can be found on the investor relations page of the Company’s Internet site.

| Item 1A. | Risk Factors |

Due to the Company’s dependency on the energy and telecommunication industries, the Company is

susceptible to negative trends relating to those industries that could adversely affect the

Company’s operating results.

The Company’s sales to the energy and telecommunication industries represent a substantial

portion of the Company’s historical sales. The concentration of revenue in such industries is

expected to continue into the foreseeable future. Demand for products to these industries depends

primarily on capital spending by customers for constructing, rebuilding, maintaining or upgrading

their systems. The amount of capital spending and, therefore, the Company’s sales and

profitability are affected by a variety of factors, including general economic conditions, access

by customers to financing, government regulation, demand for energy and cable services, and

technological factors. As a result, some customers may not continue as going concerns, which could

have a material adverse effect on the Company’s business, operating results and financial

condition. Consolidation and deregulation present the additional risk to the Company in that

combined or deregulated customers will rely on relationships with a source other than the Company.

Consolidation and deregulation may also increase the pressure on suppliers, such as the Company, to

sell product at lower prices.

The Company’s business will suffer if the Company fails to develop and successfully introduce new

and enhanced products that meet the changing needs of the Company’s customers.

The Company’s ability to anticipate changes in technology and industry standards and to

successfully develop and introduce new products on a timely basis will be a significant factor in

the Company’s ability to grow and remain competitive. New product development often requires

long-term forecasting of market trends, development and implementation of new designs and processes

and a substantial capital commitment. The trend toward consolidation of the energy,

telecommunication and data communication industries may require the Company to quickly adapt to

rapidly changing market conditions and customer requirements. Any failure by the Company to

anticipate or respond in a cost-effective and timely manner to technological developments or

changes in industry standards or customer requirements, or any significant delays in product

development or introduction or any failure of new products to be widely accepted by the Company’s

customers, could have a material adverse effect on the Company’s business, operating results and

financial condition as a result of reduced net sales.

The intense competition in the Company’s markets, particularly telecommunication, may lead to a

reduction in sales and profits.

The markets in which the Company operates are highly competitive. The level of intensity of

competition may increase in the foreseeable future due to anticipated growth in the

telecommunication and data communication industries. The Company’s competitors in the

telecommunication and data communication markets are larger companies with significant influence

over the distribution network. The Company may not be able to compete successfully against its

competitors, many of which may have access to greater financial resources than the Company. In

addition, the pace of technological development in the telecommunication and data communication

markets is rapid and these advances (i.e., wireless, fiber optic network infrastructure, etc.) may

adversely affect the Company’s ability to compete in this market.

13

Table of Contents

The introduction of products embodying new technologies or the emergence of new industry standards

can render existing products or products under development obsolete or unmarketable and result in

lost sales.

The energy, telecommunication and data communication industries are characterized by rapid

technological change. Satellite, wireless and other communication technologies currently being

deployed may represent a threat to copper, coaxial and fiber optic-based systems by reducing the

need for wire-line networks. Future advances or

further development of these or other new technologies may have a material adverse effect on the

Company’s business, operating results and financial condition as a result of lost sales.

Price increases of raw materials could result in lower earnings.

The Company’s cost of sales may be materially adversely affected by increases in the market

prices of the raw materials used in the Company’s manufacturing processes. The Company may not be

able to pass on price increases in raw materials to the Company’s customers through increases in

product prices. As a result, the Company’s operating results could be adversely affected.

The Company’s international operations subject the Company to additional business risks that may

have a material adverse effect on the Company’s business, operating results and financial

condition.

International sales account for a substantial portion of the Company’s net sales (58%, 54% and

54% in 2010, 2009 and 2008, respectively) and the Company expects these sales will increase as a

percentage of net sales in the future. Due to its international sales, the Company is subject to

the risks of conducting business internationally, including unexpected changes in, or impositions

of, legislative or regulatory requirements, fluctuations in the U.S. dollar which could materially

adversely affect U.S. dollar revenues or operating expenses, tariffs and other barriers and

restrictions, potentially longer payment cycles, greater difficulty in accounts receivable

collection, reduced or limited protection of intellectual property rights, potentially adverse

taxes and the burdens of complying with a variety of international laws and communications

standards. The Company is also subject to general geopolitical risks, such as political and

economic instability and changes in diplomatic and trade relationships, in connection with its

international operations. These risks of conducting business internationally may have a material

adverse effect on the Company’s business, operating results and financial condition.

The Company may not be able to successfully integrate businesses that it may acquire in the future

or complete acquisitions on satisfactory terms, which could have a material adverse effect on the

Company’s business, operating results and financial condition.

A portion of the Company’s growth in sales and earnings has been generated from acquisitions.

The Company expects to continue a strategy of identifying and acquiring businesses with

complementary products. In connection with this strategy, the Company faces certain risks and

uncertainties relating to acquisitions. The factors affecting this exposure are in addition to the

risks faced in the Company’s day-to-day operations. Acquisitions involve a number of special

risks, including the risks pertaining to integrating acquired businesses. In addition, the Company

may incur debt to finance future acquisitions, and the Company may issue securities in connection

with future acquisitions that may dilute the holdings of current and future shareholders. Covenant

restrictions relating to additional indebtedness could restrict the Company’s ability to pay

dividends, fund capital expenditures, consummate additional acquisitions and significantly increase

the Company’s interest expense. Any failure to successfully complete acquisitions or to

successfully integrate such strategic acquisitions could have a material adverse effect on the

Company’s business, operating results and financial condition.

The Company may have interruptions in or lost businesses due to the uncertainty of the global

economy, specifically the potential impact of bankruptcy among the Company’s suppliers and lack of

available funding for the Company’s customers.

The Company relies on sole source manufacturers for certain materials that complement the

Company’s product lines. The current state of economic uncertainty presents a risk that existing

suppliers could go out of business. If, due to any of these risk factors, the Company had to

relocate the tooling and processes to other manufacturers, there could be an adverse effect on the

supply and the Company’s ability to make products on a timely basis. Additionally, as the

financial markets are experiencing unprecedented volatility, lower levels of liquidity may be

available. The inability to obtain funding may postpone customer spending and adversely affect the

Company’s business, operating results and financial condition.

| Item 1B. | Unresolved Staff Comments |

The Company does not have any unresolved staff comments.

14

Table of Contents

| Item 2. | Properties |

The Company currently owns or leases 20 facilities, which together contain approximately 2

million square feet of manufacturing, warehouse, research and development, sales and office space

worldwide. Most of the Company’s international facilities contain space for offices, research and

engineering (R&E), warehousing and manufacturing with manufacturing using a majority of the space.

The following table provides information regarding the Company’s principal facilities:

| Reportable | ||||||||||

| Location | Use | Owned/Leased | Square Feet | Segment | ||||||

1. Mayfield Village, Ohio |

Corporate Headquarters R&E |

Owned | 62,000 | PLP-USA | ||||||

2. Rogers, Arkansas |

Manufacturing Warehouse Office |

Owned | 310,000 | PLP-USA | ||||||

3. Albemarle, North Carolina |

Manufacturing Warehouse Office |

Owned | 261,000 | PLP-USA | ||||||

4. Sydney, Australia |

Manufacturing R&E Warehouse Office |

Owned | 123,000 | Asia-Pacific | ||||||

5. São Paulo, Brazil |

Manufacturing R&E Warehouse Office |

Owned | 148,500 | The Americas | ||||||

6. Cambridge, Ontario, Canada |

Manufacturing Warehouse Office |

Owned | 73,300 | The Americas | ||||||

7. Andover, Hampshire, England |

Manufacturing R&E Warehouse Office |

Land Leased; Building Owned |

89,400 | EMEA | ||||||

8. Queretaro, Mexico |

Manufacturing Warehouse Office |

Owned | 82,900 | The Americas | ||||||

9. Beijing, China |

Manufacturing Warehouse Office |

Land Leased; Building Owned |

180,900 | Asia-Pacific | ||||||

10. Pietermarizburg, South Africa |

Manufacturing R&E Warehouse Office |

Owned | 73,100 | EMEA | ||||||

15

Table of Contents

| Reportable | ||||||||||

| Location | Use | Owned/Leased | Square Feet | Segment | ||||||

11. Sevilla, Spain |

Manufacturing R&E Warehouse Office |

Owned | 63,300 | EMEA | ||||||

12. Bangkok, Thailand |

Manufacturing Warehouse Office |

Owned | 60,000 | Asia-Pacific | ||||||

13. Albuquerque, New Mexico |

Manufacturing Warehouse Office |

Leased | 27,200 | The Americas | ||||||

14. Bielsko-Biala, Poland |

Manufacturing Warehouse Office |

Land Leased; Buildings Owned |

174,400 | EMEA | ||||||

15. Bekasi, Indonesia |

Manufacturing Office |

Owned | 31,700 | Asia-Pacific | ||||||

16. Selangor, Malaysia |

Manufacturing Warehouse Office |

Leased | 18,600 | Asia-Pacific | ||||||

17. Bangkok, Thailand |

Manufacturing Warehouse Office |

Leased | 135,700 | Asia-Pacific | ||||||

18. Auckland, New Zealand |

Manufacturing Warehouse Office |

Leased | 46,200 | Asia-Pacific | ||||||

| Item 3. | Legal Proceedings |

From time to time, the Company may be subject to litigation incidental to its business. The

Company is not a party to any pending legal proceedings that the Company believes would,

individually or in the aggregate, have a material adverse effect on its financial condition,

results of operations or cash flows.

| Item 4. | (Removed and Reserved) |

Executive Officers of the Registrant

Each executive officer is elected by the Board of Directors, serves at its pleasure and holds

office until a successor is appointed, or until the earliest of death, resignation or removal.

| Name | Age | Position | ||||

Robert G. Ruhlman

|

54 | Chairman, President and Chief Executive Officer | ||||

Eric R. Graef

|

58 | Chief Financial Officer and Vice President — Finance | ||||

William H. Haag

|

47 | Vice President — International Operations | ||||

J. Cecil Curlee Jr.

|

54 | Vice President — Human Resources | ||||

Dennis F. McKenna

|

44 | Vice President — Marketing and Business Development | ||||

David C. Sunkle

|

52 | Vice President — Research and Engineering and Manufacturing | ||||

Caroline S. Vaccariello

|

44 | General Counsel and Corporate Secretary | ||||

16

Table of Contents

The following sets forth the name and recent business experience for each person who is an

executive officer of the Company at March 1, 2011.

Robert G. Ruhlman was elected Chairman in July 2004. Mr. Ruhlman has served as Chief

Executive Officer since July 2000 and as President since 1995 (positions he continues to hold).

Mr. Ruhlman is the brother of Randall M. Ruhlman and son of Barbara P. Ruhlman, both Directors of

the Company.

Eric R. Graef was elected Vice President—Finance in December 1999 and Chief Financial Officer

in December 2007.

William H. Haag was elected Vice President—International Operations in April 1999.

J. Cecil Curlee Jr. was elected Vice President—Human Resources in January 2003.

Dennis F. McKenna was elected Vice President—Marketing and Business Development in April 2004.

David C. Sunkle was elected Vice President-Research and Engineering in January 2007. In

addition, Mr. Sunkle has taken on the role of the Vice President — Manufacturing since July 2008.

Mr. Sunkle joined the Company in 1978. He has served a variety of positions in Research and

Engineering until 2002 when he became Director of International Operations. In 2006, Mr. Sunkle

rejoined Research and Engineering as the Director of Engineering.

Caroline S. Vaccariello was elected General Counsel and Corporate Secretary in January 2007.

Ms. Vaccariello joined the Company in 2005 as General Counsel and has led the Company’s legal

affairs since that time. Prior to that time, Ms. Vaccariello worked as an attorney for The Timken

Company from 2003 to 2005.

Part II

| Item 5. | Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

The Company’s Common Shares are traded on NASDAQ under the trading symbol “PLPC”. As of March

9, 2011, the Company had approximately 900 shareholders of record. The following table sets forth

for the periods indicated (i) the high and low closing sale prices per share of the

Company’s Common Shares as reported by the NASDAQ and (ii) the amount per share of cash dividends

paid by the Company.

While the Company expects to continue to pay dividends of a comparable amount in the near

term, the declaration and payment of future dividends will be made at the discretion of the

Company’s Board of Directors in light of then current needs of the Company. Therefore, there can

be no assurance that the Company will continue to make such dividend payments in the future.

| Year ended December 31 | ||||||||||||||||||||||||

| 2010 | 2009 | |||||||||||||||||||||||

| Quarter | High | Low | Dividend | High | Low | Dividend | ||||||||||||||||||

First |

$ | 44.14 | $ | 34.60 | $ | 0.20 | $ | 47.65 | $ | 28.26 | $ | 0.20 | ||||||||||||

Second |

39.06 | 27.95 | 0.20 | 48.96 | 32.70 | 0.20 | ||||||||||||||||||

Third |

35.64 | 27.50 | 0.20 | 44.16 | 33.06 | 0.20 | ||||||||||||||||||

Fourth |

62.14 | 33.60 | 0.20 | 44.40 | 37.85 | 0.20 | ||||||||||||||||||

17

Table of Contents

Equity Compensation Plan Information

| Number of securities | ||||||||||||

| Number of securities | remaining available for | |||||||||||

| to be issued upon | future issuance under | |||||||||||

| exercise of | Weighted-average | equity compensation | ||||||||||

| outstanding options, | exercise price of | plans (excluding | ||||||||||

| warrants and rights | outstanding options, | securities reflected in | ||||||||||

| Plan Category | (a) | warrants and rights | column (a) | |||||||||

Equity compensation plans approved by security holders |

183,233 | $ | 34.46 | 177,403 | ||||||||

Equity compensation plans not approved by security

holders |

72,057 | $ | 35.89 | — | ||||||||

Total |

255,290 | 177,403 | ||||||||||

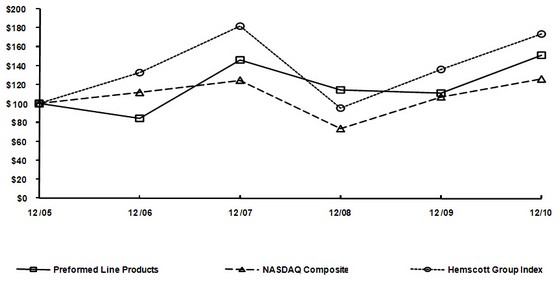

Performance Graph

Set forth below is a line graph comparing the cumulative total return of a hypothetical

investment in the Company’s Common Shares with the cumulative total return of hypothetical

investments in the NASDAQ Market Index and the Hemscott Industry Group 627 (Industrial Electrical

Equipment) Index based on the respective market price of each investment at December 31, 2005,

December 31, 2006, December 31, 2007, December 31, 2008, December 31, 2009, and December 31, 2010,

assuming in each case an initial investment of $100 on December 31, 2005, and reinvestment of

dividends.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Preformed Line Products, the NASDAQ Composite Index

and a Hemscott Group Index

Among Preformed Line Products, the NASDAQ Composite Index

and a Hemscott Group Index

| * | $100 invested on 12/31/05 in stock or index, including reinvestment of dividends. Fiscal year ending December 31. |

| COMPANY / INDEX / MARKET | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||

PREFORMED LINE PRODUCTS

CO |

100.00 | 84.34 | 145.96 | 114.00 | 110.57 | 150.95 | ||||||||||||||||||

NASDAQ MARKET INDEX |

100.00 | 111.74 | 124.67 | 73.77 | 107.12 | 125.93 | ||||||||||||||||||

HEMSCOTT GROUP INDEX |

100.00 | 132.35 | 181.83 | 95.26 | 135.74 | 173.54 | ||||||||||||||||||

18

Table of Contents

Purchases of Equity Securities

On August 4, 2010, the Company announced the Board of Directors authorized a plan to

repurchase up to 250,000 of Preformed Line Products common shares. The repurchase plan does not

have an expiration date. There were no repurchases for the three-month period ended December 31,

2010.

| Item 6. | Selected Financial Data |

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (Thousands of dollars, except per share data) | ||||||||||||||||||||

Net Sales and Income |

||||||||||||||||||||

Net sales |

$ | 338,305 | $ | 257,206 | $ | 269,742 | $ | 233,289 | $ | 196,910 | ||||||||||

Operating income |

28,480 | 19,460 | 23,988 | 21,133 | 16,359 | |||||||||||||||

Income before income taxes and discontinued operations |

30,183 | 29,593 | 24,760 | 21,321 | 17,180 | |||||||||||||||

Income from continuing operations, net of tax |

23,008 | 22,833 | 17,042 | 13,820 | 11,827 | |||||||||||||||

Net income |

23,008 | 22,833 | 17,911 | 14,213 | 12,103 | |||||||||||||||

Net income (loss) attributable to noncontrolling interest, net of tax |

(105 | ) | (524 | ) | 288 | 54 | — | |||||||||||||

Net income attributable to PLPC |

23,113 | 23,357 | 17,623 | 14,159 | 12,103 | |||||||||||||||

Per Share Amounts |

||||||||||||||||||||

Income from continuing operations attributable to PLP shareholders —

basic |

$ | 4.41 | $ | 4.46 | $ | 3.17 | $ | 2.57 | $ | 2.11 | ||||||||||

Net income attributable to PLPC common shareholders — basic |

4.41 | 4.46 | 3.34 | 2.64 | 2.16 | |||||||||||||||

Income from continuing operations attributable to PLPC shareholders

— diluted |

4.33 | 4.35 | 3.14 | 2.54 | 2.09 | |||||||||||||||

Net income attributable to PLPC common shareholders — diluted |

4.33 | 4.35 | 3.30 | 2.61 | 2.14 | |||||||||||||||

Dividends declared |

0.80 | 0.80 | 0.80 | 0.80 | 0.80 | |||||||||||||||

PLPC Shareholders’ equity |

37.21 | 32.58 | 26.09 | 27.82 | 24.47 | |||||||||||||||

Other Financial Information |

||||||||||||||||||||

Current assets |

$ | 167,342 | $ | 138,440 | $ | 112,670 | $ | 123,450 | $ | 100,374 | ||||||||||

Total assets |

280,979 | 235,372 | 190,875 | 203,866 | 170,852 | |||||||||||||||

Current liabilities |

56,558 | 46,340 | 35,248 | 42,349 | 32,372 | |||||||||||||||

Long-term debt (including current portion) |

10,650 | 4,429 | 3,147 | 4,959 | 4,361 | |||||||||||||||

Capital leases |

590 | 239 | 112 | 373 | 478 | |||||||||||||||

PLPC Shareholders’ equity |

196,140 | 170,966 | 136,265 | 149,721 | 131,148 | |||||||||||||||

On December 18, 2009, the Company completed a business combination acquiring certain

subsidiaries and other assets from Tyco Electronics. The 2009 results were impacted by a $9.1

million gain, after taxes, on the acquisition, or $1.74 per basic share and $1.69 per diluted

share. On May 30, 2008, the Company divested its Superior Modular Products subsidiary (SMP). The

net sales and income and per share amounts sections for the years noted above have been restated to

provide comparable information excluding the divestiture of the SMP operations.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

OVERVIEW

The following discussion and analysis should be read in conjunction with the Consolidated

Financial Statements and related Notes To Consolidated Financial Statements included in Item 8 in

this report.

Preformed Line Products Company (the “Company”, “PLPC”, “we”, “us”, or “our”) was incorporated

in Ohio in 1947. We are an international designer and manufacturer of products and systems

employed in the construction and maintenance of overhead and underground networks for the energy,

telecommunication, cable operators, information (data communication), and other similar industries.

Our primary products support, protect, connect, terminate, and secure cables and wires. We also

provide solar hardware systems and mounting hardware

for a variety of solar power applications. Our goal is to continue to achieve profitable

growth as a leader in the innovation, development, manufacture, and marketing of technically

advanced products and services related to energy, communications, and cable systems and to take

advantage of this leadership position to sell additional quality products in familiar markets. We

have 17 sales and manufacturing operations in 14 different countries.

19

Table of Contents

RECENT DEVELOPMENTS/ ACQUISITIONS

As a result of several global acquisitions since 2007 and corresponding significant changes in

the Company’s internal structure, we realigned our business units as of the fourth quarter of 2010,

into four operating segments to better capitalize on business development opportunities, improve

ongoing services, enhance the utilization of our worldwide resources and global sourcing

initiatives and to manage the Company better.

We report our segments in four geographic regions: PLP-USA, The Americas, EMEA (Europe, Middle

East & Africa) and Asia-Pacific in accordance with accounting standards codified in Financial

Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 280, Segment Reporting.

Each segment distributes a full range of our primary products. Our PLP-USA segment is comprised of

our U.S. operations manufacturing our traditional products primarily supporting our domestic energy

and telecommunications products. Our other three segments, The Americas, EMEA and Asia-Pacific

support the Company’s energy, telecommunications, data communication and solar products in each

respective geographical region.

The segment managers responsible for each region report directly to the Company’s Chief

Executive Officer, who is the chief operating decision maker and are accountable for the financial

results and performance of their entire segment for which they are responsible. The business

components within each segment are managed to maximize the results of the entire company rather

than the results of any individual business component of the segment.

The amount of each segment’s performance reported is the measure reported to the chief

operating decision maker for purposes of making decisions about allocating resources to the segment

and assessing its performance. We evaluate segment performance and allocate resources based on

several factors primarily based on sales and net income. The segment information of all prior

periods has been recast to conform to the current segment presentation.

On May 15, 2010, we agreed to purchase Electropar Limited (Electropar), a New Zealand

corporation.

Electropar Limited designs, manufactures and markets pole line and substation hardware for the

global electrical utility industry. Electropar is based in New Zealand with a subsidiary operation

in Australia. We believe that the acquisition of Electropar has and will continue to strengthen our

position in the power distribution, transmission and substation hardware markets and expand our

presence in the Asia-Pacific region.

The acquisition of Electropar closed on July 31, 2010. Pursuant to the Purchase Agreement, we

acquired all of the equity outstanding of Electropar for NZ$20.3 million or $14.8 million U.S.

dollars, net of a customary post-closing working capital adjustment of $.2 million. The Purchase

Agreement includes customary representations, warranties, covenants and indemnification provisions.

In addition, we may be required to make an additional earn-out consideration payment up to NZ$2

million or $1.5 million U.S. dollars based on Electropar achieving a financial performance target

(Earnings Before Interest, Taxes, Depreciation and Amortization) over the twelve months ending July

31, 2011. The fair value of the contingent consideration arrangement is determined by estimating

the expected (probability-weighted) earn-out payment discounted to present value. Based upon our

initial evaluation of the range of outcomes for this contingent consideration, we have accrued $.4

million for the additional earn-out consideration payment as of the acquisition date. Electropar

has been included in our Asia-Pacific reporting segment.

On December 18, 2009, the Company and Tyco Electronics Group S.A. (Tyco Electronics) completed

a Stock and Asset Purchase Agreement, pursuant to which we acquired from Tyco Electronics its

Dulmison business for $16 million and the assumption of certain liabilities. The acquisition of

Dulmison strengthened our position in the power distribution and transmission hardware market and

expanded our presence in the Asia-Pacific region. As

a result of the acquisition, we added operations in Indonesia and Malaysia and strengthened

our existing positions in Australia, Thailand, Mexico and the United States.

20

Table of Contents

We apply the purchase method of accounting to our acquisitions pursuant to FASB ASC 805,

Business Combinations. Under this method, we allocate the cost of business acquisitions to the

assets acquired and liabilities assumed based on their estimated fair values at the date of

acquisition, commonly referred to as the purchase price allocation. As part of the purchase price

allocations for our business acquisitions, identifiable intangible assets are recognized as assets

apart from goodwill if they arise from contractual or other legal rights, or if they are capable of