Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Axos Financial, Inc. | d8k.htm |

Sandler O’Neill & Partners, L.P.

West Coast

Financial Services Conference

Marina del Rey

March 8, 2011

Andy Micheletti

Executive Vice President and

Chief Financial Officer

Exhibit 99.1 |

1

Safe Harbor

This presentation contains forward-looking

statements within the meaning of the Private

Securities Litigation Reform Act of 1995 (the

“Reform

Act”).

The

words

“believe,”

“expect,”

“anticipate,”

“estimate,”

“project,”

or the

negation thereof or similar expressions

constitute forward-looking statements within

the meaning of the Reform Act. These

statements may include, but are not limited to,

projections of revenues, income or loss,

estimates of capital expenditures, plans for

future operations, products or services, and

financing needs or plans, as well as

assumptions relating to these matters. Such

statements involve risks, uncertainties and

other factors that may cause actual results, performance or achievements of the

Company and its subsidiaries

to

be

materially

different

from

any

future

results,

performance

or

achievements

expressed

or

implied

by

such

forward-looking

statements.

For

a

discussion

of

these

factors,

we

refer

you

to

the

Company's reports filed with the Securities and Exchange Commission, including its

Annual Report on Form 10-K for the year ended June 30, 2010 and its

Earnings Report on Form 10-Q for the quarter ended December 31,

2010. In light of the significant uncertainties inherent in the forward-looking statements

included

herein,

the

inclusion

of

such

information

should

not

be

regarded

as

a

representation

by

the

Company

or

by

any

other

person

or

entity

that

the

objectives

and

plans

of

the

Company

will

be

achieved.

For all forward-looking statements, the Company claims the protection of the

safe-harbor for forward- looking statements contained in the Reform

Act. |

Key

Accomplishments Common stock currently trading at: 116.2%

2

of book; 7.17x TTM P/E

2

Return on equity of 15.1% (YTD 12/10)

Efficiency ratio of 37.1% (YTD 12/10)

5-year asset growth of 18.4% (CAGR)

5-year deposit growth of 21.8% (CAGR)

Third highest ranking on SNL list of top performing thrifts (March 2010)

Bank Tier 1 Capital Ratio 8.10% / Tier 1 Risk-based Capital Ratio 13.18% at

12/30/10; Pro-forma

Tier

1

Capital

Ratio

of

8.52%

1

/

Tier

1

Risk-based

Capital

Ratio

of

13.87%

1

BofI joins the Russell 3000 index on June 25, 2010

Recent accretive $15 million capital raise

1

2

3

4

5

6

7

8

2

1. Assumes pushdown of existing cash of $7M from Holding company to Bank.

2. As of 2/25/11 closing price of $15.05 per share.

|

3

Corporate Profile

1. Quarter ended December 31, 2010 2. As of 2/25/11 closing

price of $15.05 per share $1.7 billion asset savings and loan

holding company

1

10 years operating history, publicly

traded on NASDAQ(BOFI) since

2005

Headquartered in single branch

location in San Diego, CA

33,000 deposit and loan customers

1

140 employees ($12 million in assets

per employee)

1

Market Capitalization of $154 million

2

Price/Tangible Book Value =

116.2%

2 |

4

Primary Business –

Deposits

Deposit products

•

Deposit

base:

~$1,061M

•

Full-featured products

•

Self-service operations

•

Highly efficient operations

(12 CSRs; 29,000

accounts)

•

Deposit

base:

~$55M

•

Strong start in first full

year of operations

•

One dedicated employee

•

Significant expansion

opportunities

1. Bank as of 12/31/2010

1

1 |

5

Primary Businesses –

Lending

Lending

Single family

Multifamily

Wholesale

banking

Gain-on-sale

Mortgage

Banking

Wholesale

Jumbo

Retail

Wholesale

Bank loan

purchase

Special

situations

•

Internet-focused lend sources

•

Self-service operation

•

Low-fixed costs

•

High-end portfolio lender

–

“Common Sense”

underwriting

–

Average LTV = 56.9%

•

13 high quality originators with

average experience of 15+ years

•

Highly ranked website-

apartmentbank.com

•

10-year history as portfolio bank

•

High credit quality

•

Year-to-date origination average

LTV of 59.3% and DSCR of

1.48%

•

Wide network of relationships

•

Significant due diligence experience

•

Over $1bn of closed transactions

•

Complex transaction structure

assistance

•

Highly creative and opportunistic |

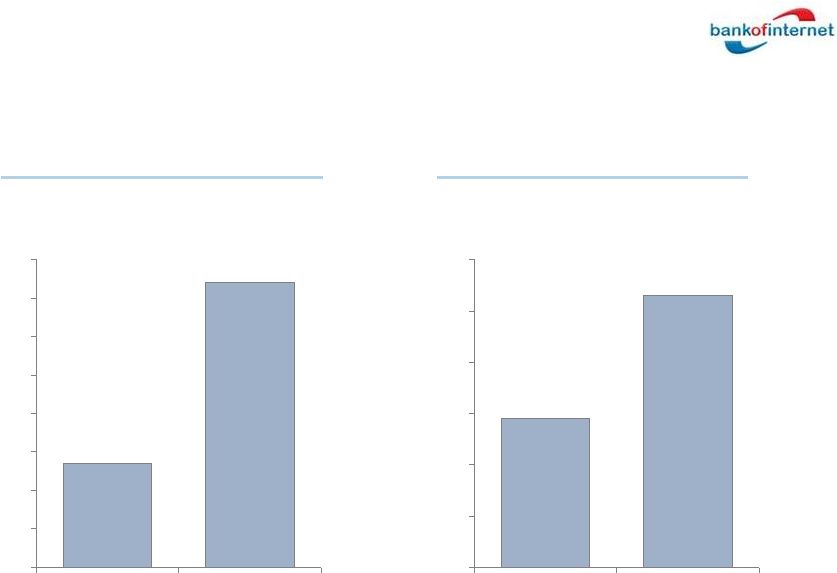

6

Multi Family and Single Family Production are a

Reliable Asset Generation Platform for the Bank

$74

$27

0

10

20

30

40

50

60

70

80

($ Million)

Q1

Q2

$53

$29

0

10

20

30

40

50

60

($ Million)

Q1

Q2

Pipeline [$mil] $66.0

$94.0

[10-31-10]

[1-31-11]

Pipeline [$mil] $45.3

$89.4

[10-31-10]

[1-31-11]

Multifamily Loan Production

Single Family Jumbo |

7

Our Business Model is More Profitable

Because Our Costs are Lower

Salaries and benefits

Premises and equipment

BofI

(%)

0.77

0.13

Other non-interest

expense

0.41

Total non-interest

expense

1.31

Core business margin

2.09

1.35

0.37

1.55

3.27

0.22

Banks

$1-$10bn

(%)

Net interest income

3.40

3.49

As % of average assets

1

2

1. Bank of Internet USA only for three months ended 12/31/10 - the most recent data on FDIC

website “Statistics on Depository Institutions Report. ” Excludes BofI Holding company

to compare to FDIC data.

2. Commercial banks by asset size. FDIC reported for three months ended 12/31/10. Total of 424

institutions $1-$10 billion. |

8

Our Efficiency Ratio Consistently is One

of the Industry's Lowest

Efficiency Ratio

(Bank of Internet USA, for the fiscal quarter ended)

63.24

34.49

30.67

31.39

29.21

0

20

40

60

80

(%)

Banks

Q2 ‘11

Q1 ‘11

Q4 ‘10

Q3 ’10

One of the lowest

rates in the

industry

1. Reported by FDIC – 424 commercial banks with $1-$10 billion in assets for the

quarter ended 12/31/10. Source: FDIC Statistics on Depository Institutions. All data excludes

holding companies for banks. 1 |

9

Best in Class Asset Quality

0.83

0.27

0

1

2

3

(%)

BofI

1

Bank $1-10bn

2

Assets 30-89 days delinquent

Assets in non-accrual

2.66

1.01

0

1

2

3

(%)

BofI

1

Bank $1-10bn

2

1. Bank of Internet USA only at 12/31/10 (excludes BofI Holding, Inc. to

compare to FDIC data). 2. Commercial banks by asset size. FDIC reported at 12/31/10. Total of 424

institutions $1-$10 billion. |

10

Mortgage Loan Portfolio –

Years Seasoned

and Loan-to-Value

12/31/10

3.7

4.4

3.5

3.7

0

1

2

3

4

5

6

Single Family

Multifamily

Commercial

Home Equity

Weighted-average number of years since origination

Weighted-average loan-to-value

53

47

52

55

0

20

40

60

Percent

1. Based on current loan balance and collateral value at origination or

purchase. 1 |

11

Loan Diversity –

December 31, 2010

Loan Portfolio

1

100% = $1,108 mm

Multifamily

SF residential

Home equity

Commercial

Consumer and other

48

4

9

4

35

1. Gross loans before premiums, discounts and allowances

|