Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - EXELON GENERATION CO LLC | d8k.htm |

Morgan Stanley Utilities Conference

March 10, 2011

Exhibit 99.1 |

2

Forward-Looking Statements

This presentation includes forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995, that are subject to risks

and uncertainties. The factors that could cause actual results to differ

materially from these forward-looking statements include those discussed

herein as well as those discussed in (1) Exelon’s 2010 Annual Report on

Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s

Discussion and Analysis of Financial Condition and Results of Operations and

(c) ITEM 8. Financial Statements and Supplementary Data: Note 18; and (2)

other factors discussed in filings with the Securities and Exchange Commission

(SEC) by Exelon Corporation, Commonwealth Edison Company, PECO Energy

Company and Exelon Generation Company, LLC (Companies). Readers are cautioned

not to place undue reliance on these forward-looking statements, which

apply only as of the date of this presentation. None of the Companies

undertakes any obligation to publicly release any revision to its

forward-looking statements to reflect events or circumstances after the

date of this presentation. This presentation includes references to adjusted

(non-GAAP) operating earnings and non-GAAP cash flows that exclude

the impact of certain factors. We believe that these adjusted

operating

earnings

and

cash

flows

are

representative

of

the

underlying

operational results of the Companies. Please refer to the appendix to this

presentation for a reconciliation of adjusted (non-GAAP) operating

earnings to GAAP earnings. Please refer to the footnotes of the

following slides for a reconciliation of non-GAAP cash flows to GAAP

cash flows. |

3

Largest merchant nuclear fleet in the U.S.

Consistent world-class performance in nuclear

operations

Utilities serving two of the largest metropolitan areas

in the U.S.

Stable dividend that has yielded ~5% on average

over the past year

Why Is Exelon a Good Investment?

Commitment to investment grade credit ratings and

financial discipline

Exelon is able to execute from a position of strength based on solid

fundamentals |

4

2011 Events of Interest

Q1

Q2

Q3

Q4

RPM Auction results

(5/13)

Illinois Power Agency

RFP (April)

ALJ Proposed Order

–

DST Rate Case

(3/31)

Procurement RFP

(bids due 5/23;

results by 6/23)

DST Rate Case Final

Order (by 5/31)

EPA Final HAP

Rule (November)

Retirement of Cromby

1 & Eddystone

1 units

(5/31)

Proposed HAP EPA

Regulation (by 3/16)

Procurement RFP

(bids due 9/19;

results by 10/19)

Retirement of

Cromby

2 unit

(12/31)

Proposed 316(b) EPA

Regulation (by 3/14)

EPA Final Transport

Rule (June)

For definition of the EPA regulations referred to on this slide, please see the EPA’s Terms of

Environment (http://www.epa.gov/OCEPAterms/). Note: ALJ = administrative law judge; DST =

delivery service tariff |

5

5

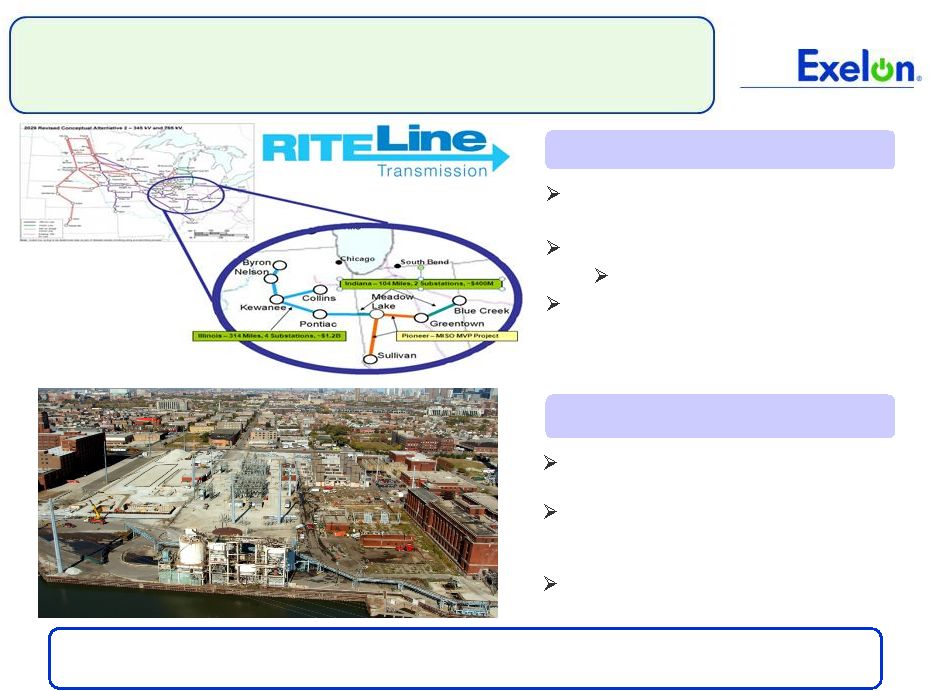

Pursuing Transmission Investment

Moving forward on project planning

with partner ETA

Total Investment ~$1.6 billion

ComEd/Exelon ~$1.1 billion

FERC incentive rate joint filing

expected late 1Q or early 2Q 2011

Exelon companies are investing in projects that enhance reliability and

support further clean energy development

Note: Electric Transmission America (ETA) is an American Electric Power &

MidAmerican Energy Holdings joint venture company. RITE Line

Enhance reliable service to the

Chicago central business district

Estimated cost of ~$170 million

recoverable under ComEd’s FERC

formula rate

Expected in-service December 2011

West Loop Phase II |

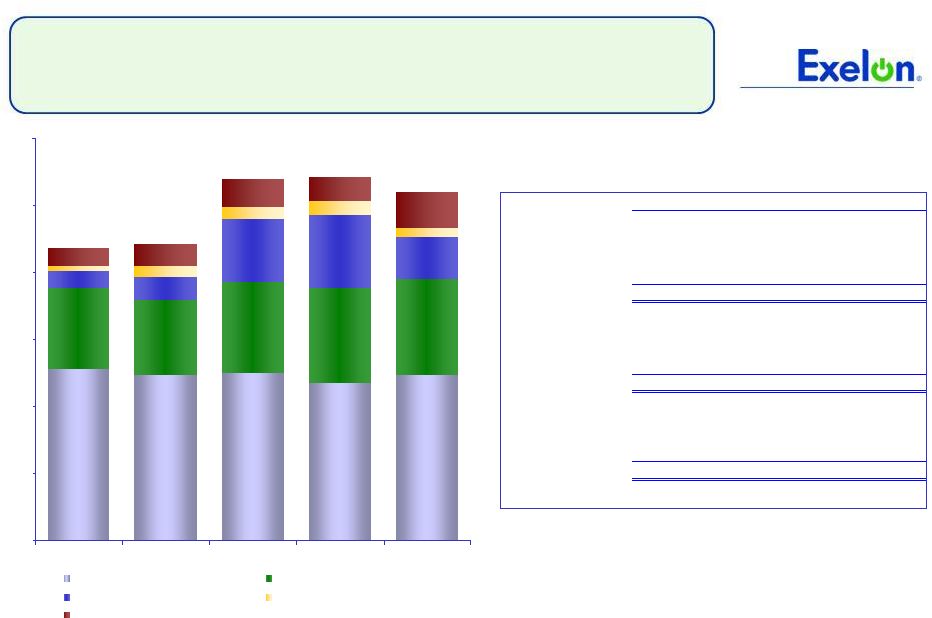

6

2011 Operating Earnings Guidance

2011E

(2)

2010A

$0.54

$2.91

$4.06

(1)

ComEd

PECO

Exelon

Generation

ComEd

PECO

Exelon

Generation

Holdco

Holdco

Exelon

$0.68

Exelon

$3.90 -

$4.20

(1)

$0.55 -

$0.65

$0.50 -

$0.55

$2.85 -

$3.05

(1)

We provided 2011 earnings guidance on January 26, 2011, and we are not updating

earnings guidance at this time. Earnings guidance is only reviewed in connection

with our quarterly earnings announcements or if we expressly indicate that we are

updating the guidance. Refer to slides 45-47 for a reconciliation of adjusted (non-

GAAP) operating earnings

to GAAP earnings.

(2)

Earnings

guidance

for

OpCos

may

not

add

up

to

consolidated

EPS

guidance.

Key Drivers of FY Guidance

+

Generation margins driven by PECO

PPA roll-off, partially offset by lower

capacity revenues

+

Higher PECO gross margin driven by

new distribution rates effective 1/1/11

-

Higher O&M expense

-

Higher depreciation & amortization

expense

2011

operating

earnings

guidance

of

$3.90

–

$4.20/share

and

1Q

2011

guidance

of

$1.00

–

$1.10/share

(1) |

7

$0.98

$0.68

$2.74

$2.91

$1.07

$0.71

2010A

2011E

PECO

ComEd

ExGen

Operating O&M Outlook

2010 to 2011 Drivers (per share)

Inflation $(0.08)

Full year of Exelon Wind $(0.05)

Two additional nuclear refueling

outages $(0.05)

ComEd

uncollectibles

$(0.04)

Estimated

2011

O&M

represents

a

new

“base”

level

for

operating

O&M

$4.39B

$4.68B

2010 Operating O&M below 2008 levels for second consecutive year

One-time savings in 2010 included executive salary freezes and reduced

compensation benefits

Anticipate annual O&M growth rate of ~2% for 2011-2013

(1)

Amounts

may

not

add

due

to

rounding.

Refer

to

slide

47

for

a

reconciliation

of

GAAP

O&M

to

Operating

O&M.

(1)

(1) |

8

Exelon Generation 2011 EPS Contribution

(1)

Estimated contribution to Exelon’s operating earnings guidance.

RNF = revenue net fuel

$ / Share

$0.35

$(0.03)

RNF

O&M

Other

Depreciation &

Amortization

$(0.08)

Key Items:

Inflation

$(0.05)

Exelon

Wind $(0.05)

Nuclear

Outages $(0.05)

2010A

2011E

(1)

$2.85 -

$3.05

$2.91

Key Items:

PECO

PPA

Exelon Wind

Capacity Market Prices

Nuclear Fuel

Market/portfolio conditions

and Exelon Energy

$(0.17)

$(0.03)

Interest

Expense

Note: Drivers add up to mid-point of 2011 EPS range. We

provided 2011 earnings guidance on January 26, 2011, and we are not updating earnings guidance at this time.

Earnings guidance is only reviewed in connection with our quarterly earnings

announcements or if we expressly indicate that we are updating the guidance. Refer to

slides

45-47

for

a

reconciliation

of

adjusted

(non-GAAP)

operating

earnings

to

GAAP

earnings.

$0.62

$0.08

$(0.29)

$(0.09)

$0.07 |

9

ComEd 2011 EPS Contribution

2010A

Depreciation &

Amortization

Interest

Expense

$0.55 -

$0.65

$0.03

$(0.08)

$(0.03)

2011E

(3)

$ / Share

$(0.02)

$0.02

Other

RNF

(1)

O&M

(1)

Key Items:

Weather

$(0.04)

Uncollectibles

$(0.02)

Appellate Court ruling

$(0.01) Distribution revenue

(2)

$0.08

Key Items:

Uncollectibles $(0.04)

Inflation

$(0.02) $0.68

Note: Drivers add up to mid-point of 2011 EPS range. We provided 2011

earnings guidance on January 26, 2011, and we are not updating earnings guidance at this time. Earnings

guidance is only reviewed in connection with our quarterly earnings announcements or if we expressly

indicate that we are updating the guidance. Refer to slides 45-47 for a

reconciliation of adjusted (non-GAAP) operating earnings to GAAP earnings.

(1)

Excludes estimated impact of Rider EDA (Energy Efficiency and Demand Response Adjustment) of

+/-$0.05/share. 2010 net income includes a one-time benefit for collections of

under-recovered 2008 and 2009 bad debt costs, as provided by the uncollectible expense rider

approved by the ICC in February 2010. Going forward, the rider provides for full recovery

of all bad debt costs. (2)

Distribution rate case currently pending, new rates will be effective in June 2011. Earnings

guidance assumes mid-point of ComEd’s requested revenue increase. (3)

Estimated contribution to Exelon’s operating earnings guidance.

|

10

PECO 2011 EPS Contribution

$ / Share

RNF

(2)

$(0.03)

$0.54

(1)

CTC, net

2011E

(3)

Key Items:

Electric & Gas

Distribution Rate

$0.19

Weather

$(0.05) Key Items:

Inflation

$(0.01) Bad

Debt $(0.01)

$0.14

O&M

(2)

$0.50 -

$0.55

(1)

$(0.04)

2010A

(1)

Excludes preferred dividends.

(2)

Excludes items that are income statement neutral and estimated impact of energy

efficiency and smart meter costs recoverable under a rider of $0.10/share.

(3)

Estimated contribution to Exelon’s operating earnings guidance.

CTC = competitive transition charge

Note: Drivers add up to mid-point of 2011 EPS range. We

provided 2011 earnings guidance on January 26, 2011, and we are not updating earnings guidance at this time.

Earnings guidance is only reviewed in connection with our quarterly earnings

announcements or if we expressly indicate that we are updating the guidance. Refer

to

slides

45-47

for

a

reconciliation

of

adjusted

(non-GAAP)

operating

earnings

to

GAAP

earnings.

$(0.03)

Depreciation

$(0.05)

Income Taxes

Key Items:

Revenue net $(0.06)

of amortization

Interest on PECO

transition bonds $0.02 |

11

1,925

1,850

1,875

1,775

1,850

900

850

1,025

1,050

1,075

250

200

700

825

475

125

50

125

150

100

200

400

275

325

250

$0

$750

$1,500

$2,250

$3,000

$3,750

$4,500

2009

2010

2011E

2012E

2013E

Base CapEx

Nuclear Fuel

Nuclear Uprates and Solar/Wind

Smart Grid

New Business at Utilities

Capital Expenditures Expectations

$ millions

Exelon

$3,275

$3,325

$4,050

$4,075

$3,900

Note: Data contained on this slide is rounded.

2009

2010

2011E

2012E

2013E

Exelon Generation

Base CapEx

875

775

850

800

775

Nuclear Fuel

(1)

900

850

1,025

1,050

1,075

Nuclear Uprates

(2)

150

250

475

550

475

Solar / Wind

(3)

50

-

225

275

-

Total ExGen

1,975

1,875

2,575

2,675

2,325

ComEd

Base CapEx

650

650

700

625

675

Smart Grid/Meter

(4)

50

100

50

100

50

New Business

(5)

150

200

275

225

325

Total ComEd

850

950

1,025

950

1,050

PECO

Base CapEx

350

475

325

325

375

Smart Grid/Meter

-

25

75

50

50

New Business

50

50

50

50

75

Total PECO

400

550

450

425

500

Corporate

(6)

50

(50)

25

25

(1)

Nuclear fuel shown at ownership, including Salem.

(2)

Excludes TMI and Clinton EPUs, which are under review.

(3)

Does not include $900 million related to acquisition of John Deere Renewables.

(4)

ComEd does not plan to move forward with these Smart Grid/Meter investments unless appropriate cost

recovery mechanisms are in place. (5)

Includes transmission growth projects.

(6)

Represents capital projects transferred from Business Services Company (BSC) to Exelon Generation,

ComEd and PECO. These projects are shown as capital expenditures at Generation, ComEd and PECO

and the capital expenditure is eliminated upon consolidation - |

12

2011 Projected Sources and Uses of Cash

(1)

Excludes counterparty collateral activity.

(2)

Cash Flow from Operations primarily includes net cash flows provided by operating

activities and net cash flows used in investing activities other than capital expenditures.

(3)

Assumes 2011 dividend of $2.10/share. Dividends are subject to declaration by

the Board of Directors. (4)

Includes $475

million

in

Nuclear

Uprates

and

$225

million

for

Exelon Wind.

(5)

Represents new business, smart grid/smart meter investment and transmission growth

projects. (6)

Excludes ComEd’s $191 million of tax-exempt bonds that are backed by

letters of credit (LOCs). Excludes PECO’s $225 million Accounts Receivable (A/R) Agreement with Bank of Tokyo.

PECO’s A/R Agreement was extended in accordance with its terms through

September 6, 2011. (7)

“Other”

includes proceeds from options and expected changes in short-term debt.

(8) Includes cash flow activity from Holding Company, eliminations, and

other corporate entities. ($ millions)

Exelon

(8)

Beginning Cash Balance

(1)

$800

Cash Flow from Operations

(2)

425

775

3,150

4,325

CapEx (excluding Nuclear Fuel, Nuclear

Uprates, Exelon Wind, Utility Growth CapEx)

(700)

(325)

(850)

(1,875)

Nuclear Fuel

n/a

n/a

(1,025)

(1,025)

Dividend

(3)

(1,400)

Nuclear Uprates and Exelon Wind

(4)

n/a

n/a

(700)

(700)

Utility Growth CapEx

(5)

(325)

(125)

n/a

(450)

Net Financing (excluding Dividend):

Planned Debt Issuances

(6)

1,000

--

--

1,000

Planned Debt Retirements

(350)

(250)

--

(600)

Other

(7)

250

--

--

300

Ending Cash Balance

(1)

$375 |

13

Pension and OPEB Expense and

Contributions –

As of 12/31/10

($ in millions)

Asset Returns

(actual for 2010 and

expected for

2011 and 2012)

Discount Rate

(used for

expense)

Pre-tax

expense

Actual

contribution

Pre-tax

expense

Expected

contribution

Pre-tax

expense

Expected

contribution

Pension

Assets

Obligations

Unfunded balance –

end of year

11.9% in 2010

8.0% in 2011

7.5% in 2012

5.83% in 2010

5.26% in 2011

5.48% in 2012

$240

$765

$8,860

$12,525

$3,665

$200

$2,100

(1)

$1,305

$240

$110

$1,015

OPEB

Assets

Obligations

Unfunded balance –

end of year

11.6% in 2010

7.08% in 2011

7.08% in 2012

5.83% in 2010

5.30% in 2011

5.52% in 2012

$190

$205

$1,655

$3,875

$2,220

$210

$185

$2,180

$225

$210

$2,140

Assumptions

2011

2012

2010

The decrease in pension expense in 2011 is primarily due to the $2.1 billion pension

contribution,

partially

offset

by

the

effects

of

lower

discount

rates

and

a

decrease

in

EROA

(1)

Exelon made a $2.1B pension contribution on January 31, 2011

(2) Pension expense amounts exclude settlement charges.

(3)

Management considers various factors when making pension funding decisions, including actuarially

determined minimum contribution requirements under ERISA, contributions required to avoid

benefit restrictions and at-risk status as defined by the Pension Protection Act of 2006 (the Act), management of the pension obligation and regulatory

implications. The Act requires the attainment of certain funding levels to avoid benefit restrictions

(such as an inability to pay lump sums or to accrue benefits prospectively), and at-risk

status (which triggers higher minimum contribution requirements and participant notification).

Note: Slide provided for illustrative purposes and not intended to represent a forecast of future

outcomes. Assumes an ~25% capitalization of pension and OPEB costs.

EROA = earned return on assets

|

14

Driving Financial Discipline

Currently refinancing ExGen, PECO and Corp facilities; expect to close by Q1

2011 •

Three facilities totaling $6.4B will have 5-year tenor (maturing in March

2016) ($ millions)

Generation

PECO

Corporate

ComEd

Total

New Unsecured Revolving

Credit Facilities

(4)

$5,300

$600

$500

$1,000

$7,400

Expiration date

March 2016

March 2016

March 2016

March 2013

Maintaining a strong balance sheet and liquidity position

$2.1B Pension Contribution in 2011

Credit Facilities

Continued Strong Balance Sheet

FFO / Debt

(1)(2)

Pension Contributions

615

2,100

765

110

175

160

195

780

790

170

485

2010

2011

2012

2013

2014

2015

With $2.1B

Original Plan*

($ millions)

* Original

Plan

reflects

preliminary

2010

underlying

assumptions

(including

discount rate and asset returns).

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009A

2010A

2011E

2012E

2013E

ExGen/Corp

ComEd

PECO

(3)

S&P Target Range

S&P Target Range

(1)

Reflects FFO / Debt as calculated by S&P.

(2)

Dashed lines represent S&P Target Ranges (30-35% for ExGen/Corp and 15-18% for ComEd and

PECO). See slide 15 for reconciliations to GAAP.

(3)

FFO/Debt Target Range reflects ExGen FFO/Debt in addition to the debt obligations of Exelon

Corp.

(4)

Excludes $94 million of credit facility agreements arranged with minority and community banks on

10/22/10 that are utilized solely to issue letters of credit. |

15

Metric Calculations and Ratios

FFO Calculation:

Net Cash Flows provided by Operating Activities

+/-

Change in Working Capital

+

Other

Non-Cash

items

(1)

-

AFUDC/Cap. Interest

-

Decommissioning activity

-

PECO Transition Bond Principal Paydown

= FFO

Interest Coverage:

FFO + Adjusted Interest

Adjusted Interest

Adjusted Interest:

Net Interest Expense

-

PECO Transition Bond Interest Expense

+ AFUDC & Capitalized interest

+ Interest on Present Value (PV) of Operating Leases

+ Interest on Imputed Debt Related to PV of Power Purchase Agreements (PPA)

= Adjusted Interest

FFO / Debt:

FFO

Adjusted Debt

(2)

Adjusted Debt:

LTD

+ STD

-

PECO Transition Bond Principal Balance

+

Off-balance

sheet

debt

equivalents

(3)

= Adjusted Debt

Debt / Cap:

Adjusted Debt

(2)

Adjusted Capitalization

Adjusted Capitalization:

Total shareholder’s equity

+ Preferred Securities of Subsidiaries

+ Adjusted Debt

(3)

= Adjusted Capitalization

(1)

Reflects depreciation adjustment for PPAs and operating leases and pension/OPEB contribution

normalization. (2)

Uses current year-end adjusted debt balance.

(3)

Metrics are calculated in presentation adjusted for debt equivalents for Present Value of Operating

Leases, PPAs, unfunded Pension and OPEB obligations (after-tax) and other

minor debt equivalents. |

16

Key Assumptions

2009 Actual

2010 Actual

2011 Est.

(3)

Nuclear Capacity Factor (%)

(1)

93.6

93.9

93.0

Total Generation Sales Excluding Trading (GWh)

173,065

171,789

168,700

Henry Hub Gas Price ($/mmBtu)

3.92

4.37

4.56

PJM West Hub ATC Price ($/MWh)

38.30

45.93

45.45

Tetco M3 Gas Price ($/mmBtu)

4.64

5.10

5.32

PJM West Hub Implied ATC Heat Rate (mmbtu/MWh)

8.25

9.01

8.54

NI Hub ATC Price ($/MWh)

28.85

33.09

30.69

Chicago City Gate Gas Price ($/mmBtu)

3.92

4.46

4.61

NI Hub Implied ATC Heat Rate (mmbtu/MWh)

7.36

7.42

6.66

MAAC Capacity Price ($/MW-day)

158.48

181.34

136.59

EMAAC Capacity Price ($/MW-day)

173.73

181.34

136.59

RTO Capacity Price ($/MW-day)

106.13

144.40

136.59

Electric Delivery Growth (%)

(2)

PECO

0.6

0.1

0.0

ComEd

(0.1)

0.2

0.0

Effective Tax Rate -

Operating (%)

37.2

36.7

38.1

Exelon Generation

38.3

37.5

37.1

ComEd

37.9

39.7

40.8

PECO

29.5

31.1

38.0

(1)

Excludes Salem.

(2)

Weather-normalized retail load growth.

(3)

Reflects forward market prices as of December 31, 2010; Reflects assumptions used in original 2010

earnings guidance provided on

January 26, 2011.

Note: The estimates of planned generation do not represent guidance or a forecast of future

results as Exelon has not completed its planning or optimization processes.

|

17 |

18

Factors Influencing PJM RPM Capacity Auction

(Comparison of PY 14/15 and PY 13/14 Price Drivers)

Exelon

Price Impact

Cost of Environmental Upgrades

(1)

Higher Net CONE

(2)

Higher Net ACRs for Coal Units

(3)

Import Transmission Limits and Objectives

(muted impact on portfolio revenues due to regional diversification)

NJ CCGT Proposal / PJM Minimum Offer Price Rules

Peak Load

(4)

Demand Response Growth

2014/15 PJM Capacity Auction: Expected

Changes Since Planning Year 2013/14

(1) We expect generators to reflect cost of capital expenditures into their

cost based offers at the upcoming auction. (2) Cost of new entry

(CONE) increased by 7.6% (for RTO) and 5.3% to 6.5% (within Locational Deliverability Areas (LDAs)).

(3) Replacing 2007 net revenues with significantly lower 2010 revenues in the

Net ACR (avoidable cost rate) calculations for coal generators may increase offer caps for certain

coal

generators

in

the

next

auction.

However,

some

coal

units

may

not

be

affected

due

to

high

net

revenues

compared

to

avoidable

costs.

(4) Peak load reduced by approx. 1% in RTO (excluding the impact from Duke

Ohio integration). Note:

RPM

=

Reliability

Pricing

Model;

CCGT

=

combined

cycle

gas

turbine

Exelon’s capacity position, split almost evenly between the west and the east,

dampens the volatility to portfolio revenues from changes to transmission

limits while retaining upside across the fleet from upcoming EPA

regulations |

19

19

Moving Generation to Market

110,594

142,400

42,003

5,295

13,897

26,300

0

50,000

100,000

150,000

200,000

2010

2011E

ComEd Swap

IL Auction

PECO Load

Actual Forward Hedges & Open Position

171,789

168,700

(1) Represents values as of December 31, 2010.

Transition to market at PECO provides additional channels to market for

Exelon Generation, including opportunities at Exelon Energy

Exelon Energy Electric Volumes

-

5

10

15

20

25

30

2008

2009

2010

2011E

2012E

2013E

MWh - Millions

COMED / Ameren

PECO/PPL

Other

Expected

Total

Sales

(GWh)

(1)

2011-2013 Sales as % of

Expected Generation

(1)

Exelon

Energy

6%

Standard

Product Sales

29%

Open

Generation

36%

Options

5%

Utility

Procurements

24% |

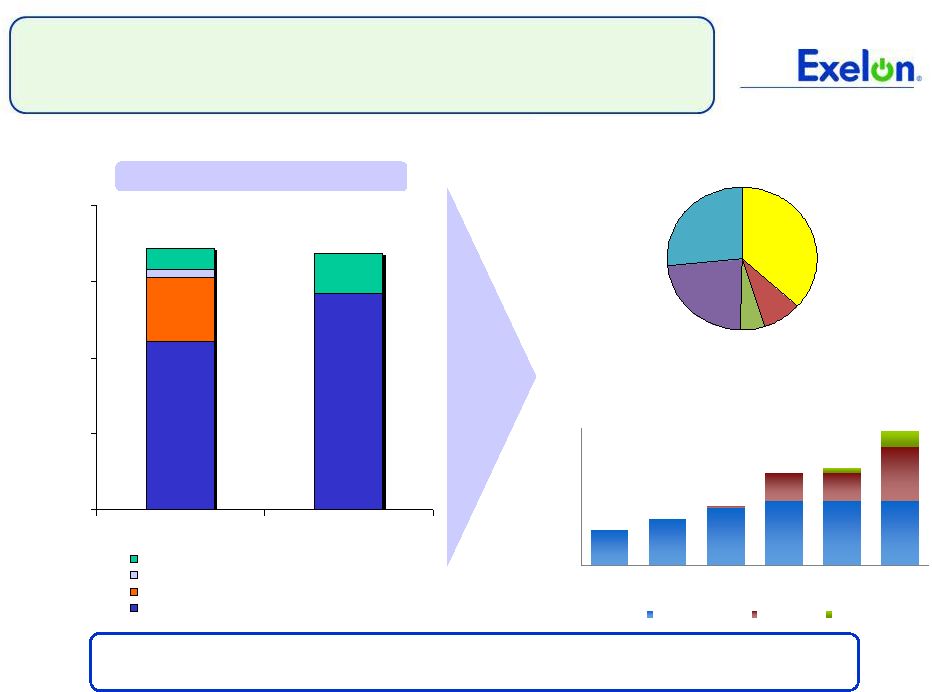

Exelon's Uprate Plan

Expenditures (1)

$0

$100

$200

$300

$400

$500

$600

$700

2008A

2009A

2010A

2011E

2012E

2013E

0

100

200

300

400

500

Megawatt Recovery

MUR

EPU

MW Online (Cumulative)

20

Exelon Wind Expenditures

(Advanced Development Projects)

$0

$50

$100

$150

$200

$250

$300

2010A

2011E

2012E

0

50

100

150

200

250

300

Annual Project CapEx

MW Online (Cumulative)

(1) Dollars shown are nominal, reflecting 6% escalation, in millions and

exclude TMI and Clinton extended power uprates, which are currently under review. MW shown at ownership.

Note: PPA = power purchase agreement; MUR = measurement uncertainty recapture; EPU

= extended power uprate. Data contained in this slide is rounded.

$150

$250

$550

$475

$475

$ millions

$50

Exelon is positioned as a key player in the US wind market and has the

largest size and scale for nuclear uprates

$ millions

Wind Development Projects

Nuclear Uprates Program

Highest return projects are being completed in

early years

Leverages Exelon’s substantial experience

managing

successful

uprate

projects

–

1,100

MW completed from 1999 to 2008, 101

MWs added in 2009-2010

Attractive economics for both operating and

advanced

development

projects

–

PPAs

already executed

Provides diversity in geographic presence

and generation type

$225

$275

Growing Our Clean Generation |

21

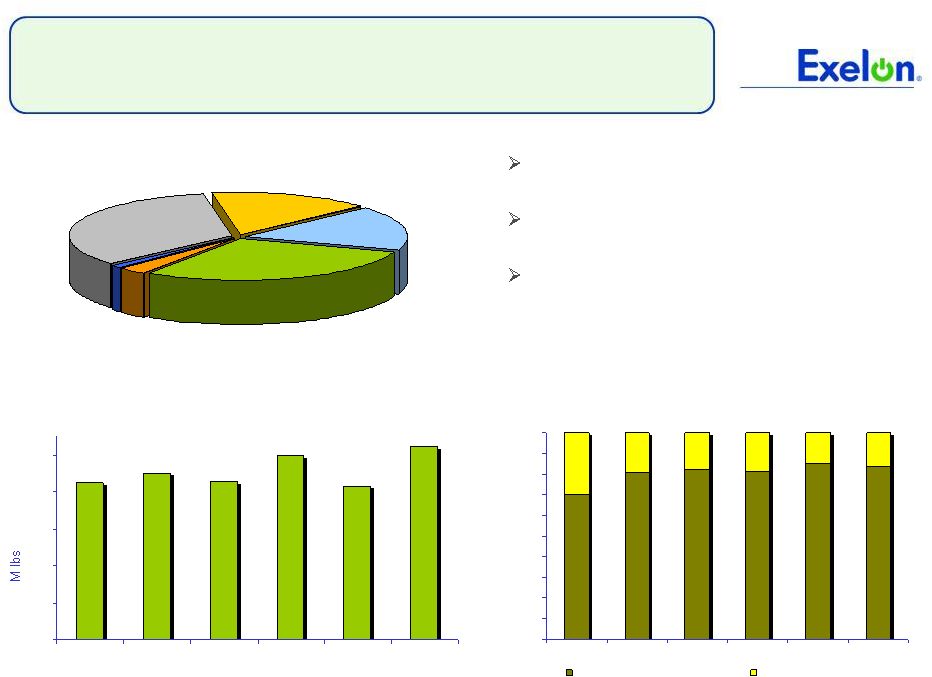

Effectively Managing Nuclear Fuel Costs

Uranium

29%

Conversion

3%

Tax/Interest

1%

Nuclear Waste

Fund

17%

Fabrication

16%

Enrichment

34%

Components of Fuel Expense in 2010

Projected Exelon Average Uranium Cost vs. Market

Projected Exelon Uranium Demand

2010 –

2015:

100% hedged in volume

0.0

2.0

4.0

6.0

8.0

10.0

2010

2011

2012

2013

2014

2015

Exelon Nuclear’s uranium demand is 100%

physically hedged for 2010-2015

Contracted prices continue to be below market

prices

Uranium prices were volatile over last 5 years,

but have stabilized in the $40-$60/lb range

All charts exclude Salem.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010

2011

2012

2013

2014

2015

Exelon Average Reload Price

Projected Market Price |

22

Environmental |

23

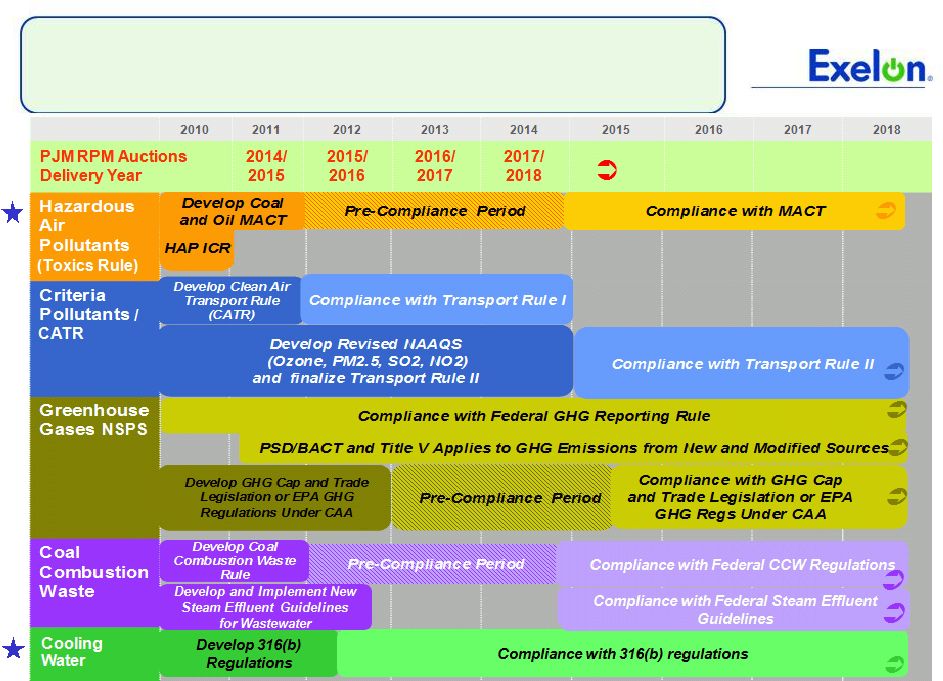

EPA Regulations Will Move Forward in 2011

Note: RPM auctions take place annually in May.

For

definition

of

the

EPA

regulations

referred

to

on

this

slide,

please

see

the

EPA’s

Terms

of

Environment

(http://www.epa.gov/OCEPAterms/). |

24

24

Exelon’s Exposure to EPA Regulations

EPA Regulation

Units Affected

Exelon Investment

Needed

(1)

Industry Impact

(2)

Hazardous Air

Pollutants

(Toxics Rule)

Keystone & Conemaugh

(3)

Oil-Fired Units >25 MW: ~935 MW

~$10 million

Impact to be determined

Significant, primarily fossil

fuel-fired generation

Criteria

Pollutants /

CATR

Keystone & Conemaugh

(3)

Fossil-fuel fired units >25 MW: ~4,000 MW

(4)

~$125 million

None anticipated

Compliance costs of up to

$2.8 billion / year

GHG NSPS

Fossil-fuel fired generation

(5)

Minimal due to low carbon

position of fossil fleet

Significant, primarily fossil

fuel-fired generation

Coal combustion

waste

Keystone & Conemaugh

(3)

Subtitle C: < $100 million

(6)

Subtitle D: no impact

Compliance costs up to $20

billion

Cooling Water

Facilities without closed-cycle recirculating

systems (e.g. cooling towers)

POWER: Schuylkill, Eddystone

3 & 4,

Fairless Hills, Mountain Creek, Handley

NUCLEAR: Clinton, Dresden, Quad Cities,

Peach

Bottom,

and

Salem

(7)

Impact to be determined

once rule is promulgated;

Cost to retrofit Salem

estimated at $500 million

(3)

Significant, impacts all fuel

types including large base

load and intermediate units

(1)

These rules are in the proposed or pre-proposed stage and estimates are based on published cost

studies used as inputs to IPM modeling. (2)

EPA’s estimated costs, where applicable.

(3)

Investment needed shown is Exelon’s share of the cost. Exelon owns 21% share in Keystone

and Conemaugh and 42.59% share in Salem. Keystone & Conemaugh units all have

scrubbers and Keystone units have SCRs. Salem investment estimates based on 2006 studies.

(4)

Exelon’s existing coal-fired units will be retired before this rule will take effect.

(5)

This rule applies to new sources or major modifications of existing sources and will establish

guidelines for States to incorporate into SIPS for existing sources.

(6)

Excludes Eddystone 1 and 2 and Cromby, which are scheduled to retire in 2011 and 2012.

(7)

Excludes Oyster Creek due to settlement with NJ DEP that does not require closed cycle cooling.

For definition of the EPA regulations referred to on this slide,

please see the EPA’s Terms of Environment (http://www.epa.gov/OCEPAterms/). |

25

Why EPA Regulations Will Not Be Delayed

Opposition will have a voice, but the framework and timetable have been set

Opposing Argument

Reality

Supporting Facts

Courts will suspend the

rules or the President will

intervene

Federal court would have to determine

that the rules are inconsistent with

applicable law, which is unlikely to

occur because the amended rules are

aligned with the court’s expectations

Up to 1 year extension by EPA only if necessary

for installation of controls

President has only used exemption two times in

history (only for national security interests)

Costs are prohibitive for

industry and consumer

Proven technologies are commercially

available and have already been

installed demonstrating that the costs

can be managed

Total savings to consumer, including

healthcare impacts

Well over half of existing units have already

installed pollution controls

EPA estimates in 2014 that the proposed

Transport Rule will have annual net benefits (in

2006$) of $120-290 billion using a 3% discount

rate

Timeline is too tight for

compliance

Recent industry trends suggest that it

is reasonable to install this quantity of

scrubbers according to the proposed

timeframe.

EPA's modeling indicates that only 14 GW of

additional capacity would need to be retrofitted

with flue gas desulfurization (FGD) for Phase 2

of the Transport rule (2014)

Industry has already demonstrated ability to

schedule and sequence outages to comply

Retirements will cause

reliability issues on the

grid

Electric system reliability will not be

compromised if the industry and its

regulators manage the transition

Each NERC region has excess capacity,

totaling over 100 GW nationwide

Between 2001-2003, industry built over 160 GW

of

new

generation

–

four

times

what

is

projected

will retire over next 5 years |

26 |

27

27

ComEd Load Trends

Note: C&I = Commercial & Industrial

Weather-Normalized Load Year-over-Year

4Q10

2010 2011E

Average Customer Growth

0.4%

0.2%

0.5%

Average Use-Per-Customer

(4.5)%

(1.4)%

0.0%

Total Residential

(4.1)%

(1.2)% 0.5%

Small C&I

(1.5)%

(0.6)% (0.3)%

Large C&I

1.9%

2.6% (0.2)%

All Customer Classes

(1.2)%

0.2% 0.0%

(1)

Source: U.S. Dept. of Labor (December 2010) and Illinois

Department of Security (December 2010)

(2) Source: Global Insight December 2010

-6.0%

-3.0%

0.0%

3.0%

6.0%

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

-6.0%

-3.0%

0.0%

3.0%

6.0%

All Customer Classes

Large C&I

Residential

Gross Metro Product

Key Economic Indicators

Weather-Normalized Load

Chicago

U.S.

Unemployment rate

(1)

9.3%

9.4%

2010 annualized growth in

gross domestic/metro product

(2)

1.6%

2.8% |

28

28

28

ComEd 2010 Rate Case Update

ComEd Reply Brief (2/23/11)

$343M increase requested

11.50% ROE / 47.28% equity ratio

Rate base $7,349M

2009 test year with pro forma plant

additions through 6/30/11

ICC Staff Reply Brief Position

$113M increase proposed

10.00% ROE / 47.11% equity ratio

Rate base $6,480M

Pro forma plant additions and

depreciation reserve through 12/31/10

(ICC Docket No. 10-0467)

$ millions

ComEd Original Request (6/30/10)

396

$

Adjustments:

Bonus Depreciation

(14)

Pro forma plant adds/O&M update

(4)

Errata in Initial Filing

(12)

Reduction to Reg Asset Amortization

(8)

Other Items

(4)

ComEd Rebuttal (11/22/10)

354

$

Adjustments:

New Bonus Depreciation

(22)

Pro forma plant adds/O&M update

(4)

Reduction to AMI/Other

(2)

ComEd Surrebuttal (1/3/2011)

326

$

Adjustments:

IL Business Tax Increase

17

ComEd Reply Brief (2/23/11)

343

$

Reconciliation of ComEd Initial Request to Reply Brief

* ComEd request does not reflect Appellate Court decision relating to

depreciation reserve, which we estimate would have a $85M reduction

to revenue requirement

* |

29

29

ComEd –

Proposed Infrastructure

Investment and Modernization Legislation

Proposed Grid Modernization

Legislation Key Concepts

Incremental investment of $2.6B of capital

over 10 years

•

$1.5B smart grid/smart meter

•

$1.1B infrastructure improvements

Incorporates an annual formula rate

proceeding, similar to FERC Transmission

rate

•

Protocols clarify treatment of several

significant items, including pension costs

and pension asset

•

ROE formula based on average 30-year

Treasury yield

Reduces proceeding timeframe from 11

months to less than 9 months

ComEd is driving innovative regulatory and legislative strategy to benefit customers,

improve the transparency of the ratemaking process and enable economic

development Proposed Grid Modernization

Legislation Customer Benefits

Quantifiable benefits to customers of 12

million avoided outages and hundreds of

millions in avoided costs

Put a smart meter in every home and

provide extensive consumer education

Significantly improve meter reading

Create 2,000 jobs at the peak of the

investment cycle

Create $100M in Illinois tax revenues over

the life of the program

Enhance the economic competitiveness of

Illinois; make our state better positioned to

attract businesses and jobs |

30

2009

2010

Target

Equity

~46%

~45%

~45%

Earned ROE

8.5%

10.6%

30

6.7

7.3

1.9

2.0

6.7

1.9

Transmission

Distribution

ComEd

Rate Base Growth

ELECTRIC

DISTRIBUTION

Prior Rate Case

ComEd

Surrebuttal

1/3/2011

Rates Effective

October 1, 2008

June 1, 2011

Test Year

2006 pro forma

2009 pro forma

Rate Base

$6,694 million

$7,349 million

ROE

10.3%

11.5%

Equity %

45.04%

47.28%

TRANSMISSION

FERC Formula rate

Rates Effective

June 1, 2010

Test Year

2009 pro forma

Rate Base

$1,949 million

ROE

11.5%

Equity %

56%

Transmission: FERC

formula rate adjusted

every year on June 1

Distribution rate

cases expected every

~1-2 years

$8.6

$8.6

2009

2010

2011E

$9.3

ComEd

executing on regulatory recovery plan

Rate Base in Rates

End of Year ($ in billions)

(1)

Recent Rate Cases

10%

(1)

Amounts include pro forma adjustments. On September 30, 2010, the Illinois Appellate Court ruled

with regard to ComEd’s 2007 distribution rate case and held that the ICC abused its

discretion in not reducing ComEd’s rate base to account for an additional 18 months of accumulated depreciation while including pro forma plant additions post-test

year through that period. The Court remanded the case to the ICC. For the 2007 rate case,

the Court’s ruling would reduce the $6,694 million rate base by ~$500 - $670 million

resulting in a revenue reduction between $57 and $77 million. For the current rate case,

updating the depreciation and deferred tax reserves to June 2011 would reduce the $7,349

million rate base by an estimated $667 million and would reduce the revenue requirement by approximately $85 million.

Note: Amounts may not add due to rounding.

|

31 |

32

PECO Load Trends

Philadelphia

U.S.

Unemployment rate

(1)

8.4%

9.4% 2010 annualized growth in

gross

domestic/metro

product

(2)

2.8%

2.8% Note: C&I = Commercial & Industrial

Weather-Normalized Load Year-over-Year

Key Economic Indicators

Weather-Normalized Load

4Q10

2010 2011E

Average Customer Growth

0.5%

0.3%

0.4%

Average Use-Per-Customer

(1.2)%

0.3%

(0.3)%

Total Residential

(0.7)%

0.5% 0.1%

Small C&I

(2.0)%

(1.9)% (0.5)%

Large C&I

1.5%

0.8% 0.1%

All Customer Classes

0.0%

0.1% 0.0%

(1)

Source:

U.S

Dept.

of

Labor

(PHL

–

November

2010

preliminary data, US -

December 2010)

(2)

Source: Global Insight December 2010

-5.0%

-2.5%

0.0%

2.5%

5.0%

1Q10

2Q10

3Q10

4Q10

1Q11E

2Q11E

3Q11E

4Q11E

-5.0%

-2.5%

0.0%

2.5%

5.0%

All Customer Classes

Large C&I

Residential

Gross Metro Product |

33

3.0

3.2

3.3

0.6

0.6

0.6

1.1

1.1

1.1

0.9

Electric Distribution

Electric Transmission

CTC

Gas

PECO Executing on Transition Plan

ELECTRIC

DISTRIBUTION

Filing

3/31/2010

Rates Effective

January 1, 2011

Test Year

2010

Revenue Increase

$225 million

GAS DELIVERY

Filing

3/31/2010

Rates Effective

January 1, 2011

Test Year

2010

Revenue Increase

$20 million

TRANSMISSION

Stated rate; no

recent rate cases

$5.6

$4.9

2009

2010

(1)

As determined for rate-making purposes. Amounts reflect pro forma adjustments

that may be made to determine rate base for rate case filing purposes.

(2)

Operating Net income basis

$5.0

2011E

PECO

is

managing

through

its

transition

period

and

is

positioned

for

continued strong financial performance post-2010

Rate Base in Rates

End of Year Balance ($ in billions)

(1)

Recent Rate Cases

(1)

Periodic rate

cases

going forward

2009

2010

Target

Equity

(1)

53%

53%

51-53%

Earned ROE

(2)

14.8%

12.9%

10% |

34

Exelon Generation Hedging Disclosures

(as of December 31, 2010) |

35

35

Important Information

The following slides are intended to provide additional information regarding the hedging

program at Exelon Generation and to serve as an aid for the purposes of modeling Exelon

Generation’s gross margin (operating revenues less purchased power and fuel expense). The

information on the following slides is not intended to represent earnings guidance or a forecast

of future events. In fact, many of the factors that ultimately will determine Exelon

Generation’s actual gross margin are based upon highly variable market factors outside of

our control. The information on the following slides is as of December 31, 2010. We

update this information on a quarterly basis. Certain information on the following slides is based upon an internal simulation model that

incorporates assumptions regarding future market conditions, including power and commodity

prices, heat rates, and demand conditions, in addition to operating performance and dispatch

characteristics of our generating fleet. Our simulation model and the assumptions therein are

subject to change. For example, actual market conditions and the dispatch profile of our

generation fleet in future periods will likely differ – and may differ significantly –

from the assumptions underlying the simulation results included in the slides. In addition,

the forward- looking information included in the following slides will likely change over time

due to continued refinement of our simulation model and changes in our views on future market

conditions. |

36

36

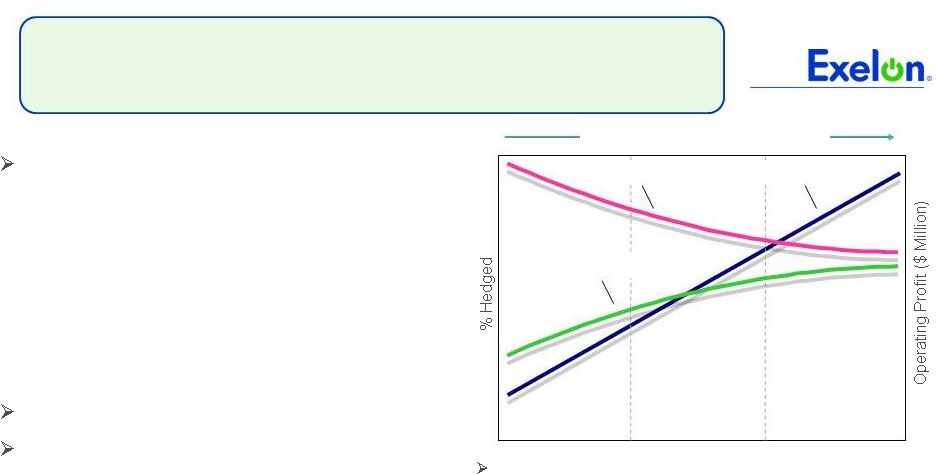

Portfolio Management Objective

Align Hedging Activities with Financial Commitments

Power Team utilizes several product types

and channels to market

•

Wholesale and retail sales

•

Block products

•

Load-following products

and load auctions

•

Put/call options

Exelon’s hedging program is designed to

protect the long-term value of our

generating fleet and maintain an

investment-grade balance sheet

•

Hedge enough commodity risk to meet future cash

requirements if prices drop

•

Consider: financing policy (credit rating objectives,

capital structure, liquidity); spending (capital and

O&M); shareholder value return policy

Consider market, credit, operational risk

Approach to managing volatility

•

Increase hedging as delivery approaches

•

Have enough supply to meet peak load

•

Purchase fossil fuels as power is sold

•

Choose hedging products based on generation

portfolio

–

sell

what

we

own

•

Heat rate options

•

Fuel products

•

Capacity

•

Renewable credits

% Hedged

High End of Profit

Low End of Profit

Open Generation

with LT Contracts

Portfolio

Optimization

Portfolio

Management

Portfolio Management Over Time |

37

37

Percentage of Expected

Generation Hedged

•

How many equivalent MW have been

hedged at forward market prices; all hedge

products used are converted to an

equivalent average MW volume

•

Takes ALL

hedges into account whether

they are power sales or financial products

Equivalent MWs

Sold

Expected Generation

=

Our normal practice is to hedge commodity risk on a ratable basis

over the three years leading to the spot market

•

Carry operational length into spot market to manage forced outage and

load-following risks

•

By

using

the

appropriate

product

mix,

expected

generation

hedged

approaches

the

mid-90s percentile as the delivery period approaches

•

Participation in larger procurement events, such as utility auctions, and some

flexibility in the timing of hedging may mean the hedge program is not

strictly ratable from quarter to quarter

Exelon Generation Hedging Program |

38

38

2011

2012

2013

Estimated Open Gross Margin ($ millions)

(1)(2)(3)

$5,200

$5,050

$5,700

Open gross margin assumes all expected generation is sold

at the Reference Prices listed below

Reference Prices

(1)

Henry Hub Natural Gas ($/MMBtu)

NI-Hub ATC Energy Price ($/MWh)

PJM-W ATC Energy Price ($/MWh)

ERCOT

North

ATC

Spark

Spread

($/MWh)

(4)

$4.56

$30.69

$45.45

$1.12

$5.08

$32.38

$46.41

$0.82

$5.33

$35.09

$48.25

$1.84

Exelon Generation Open Gross Margin and

Reference Prices

(1)

Based on December 31, 2010 market conditions.

(2)

Gross margin is defined as operating revenues less fuel expense and purchased power

expense, excluding the impact of decommissioning and other incidental revenues. Open

gross margin is estimated based upon an internal model that is developed by

dispatching our expected generation to current market power and fossil fuel prices. Open gross margin

assumes

there

is

no

hedging

in

place

other

than

fixed

assumptions

for

capacity

cleared

in

the

RPM

auctions

and

uranium

costs

for

nuclear

power

plants.

Open

gross

margin

contains assumptions for other gross margin line items such as various ISO bill and

ancillary revenues and costs and PPA capacity revenues and payments. The estimation of open

gross margin incorporates management discretion and modeling assumptions that are

subject to change. (3)

As of December 31, 2010 disclosure, Exelon Wind included. Assets in IL,

MI and MN are in Midwest region and assets in ID, KS, MO, OR and TX are in South and West region.

(4)

ERCOT North ATC spark spread using Houston Ship Channel Gas, 7,200 heat rate, $2.50

variable O&M. |

39

39

2011

2012

2013

Expected Generation

(GWh)

(1)

165,900

165,800

163,300

Midwest

99,600

98,500

96,200

Mid-Atlantic

56,800

57,200

56,500

South & West

9,500

10,100

10,600

Percentage

of

Expected

Generation

Hedged

(2)

90-93%

67-70%

32-35%

Midwest

91-94

69-72

31-34

Mid-Atlantic

93-96

67-70

36-39

South & West

70-73

51-54

39-42

Effective

Realized

Energy

Price

($/MWh)

(3)

Midwest

$43.00

$41.50

$43.50

Mid-Atlantic

$57.00

$50.50

$51.50

South & West

$2.50

$(1.00)

$(3.50)

Generation Profile

(1)

Expected generation represents the amount of energy estimated to be generated or purchased through

owned or contracted for capacity. Expected generation is based upon a simulated dispatch

model that makes assumptions regarding future market conditions, which are calibrated to market quotes for power, fuel, load following products, and options.

Expected generation assumes 12 refueling outages in 2011 and 10 refueling outages in 2012 and 2013 at

Exelon-operated nuclear plants and Salem. Expected generation assumes capacity

factors of 93.0%, 93.6% and 93.1% in 2011, 2012 and 2013 at Exelon-operated nuclear plants. These estimates of expected generation in 2012 and 2013 do

not represent guidance or a forecast of future results as Exelon has not completed its planning or

optimization processes for those years. (2)

Percent of expected generation hedged is the amount of equivalent sales divided by the expected

generation. Includes all hedging products, such as wholesale and retail sales of power,

options, and swaps. Uses expected value on options. Reflects decision to permanently retire Cromby Station and Eddystone Units 1&2 as of May 31, 2011.

(3)

Effective realized energy price is representative of an all-in hedged price, on a per MWh basis,

at which expected generation has been hedged. It is developed by considering the energy

revenues and costs associated with our hedges and by considering the fossil fuel that has been purchased to lock in margin. It excludes uranium costs and RPM capacity

revenue, but includes the mark-to-market value of capacity contracted at prices other than RPM

clearing prices including our load obligations. It can be compared with the reference

prices used to calculate open gross margin in order to determine the mark-to-market value of Exelon Generation's energy hedges. |

40

40

Gross Margin Sensitivities with Existing Hedges ($ millions)

(1)

Henry Hub Natural Gas

+ $1/MMBtu

-

$1/MMBtu

NI-Hub ATC Energy Price

+$5/MWH

-$5/MWH

PJM-W ATC Energy Price

+$5/MWH

-$5/MWH

Nuclear Capacity Factor

+1% / -1%

2011

$5

$(5)

$30

$(20)

$15

$(10)

+/-

$40

2012

$175

$(95)

$185

$(165)

$115

$(110)

+/-

$45

2013

$495

$(445)

$340

$(335)

$200

$(195)

+/-

$50

Exelon Generation Gross Margin Sensitivities

(with Existing Hedges)

(1)

Based on December 31, 2010 market conditions and hedged position. Gas price

sensitivities are based on an assumed gas-power relationship derived from an

internal

model

that

is

updated

periodically.

Power

prices

sensitivities

are

derived

by

adjusting

the

power

price

assumption

while

keeping

all

other

prices

inputs

constant. Due to correlation of the various assumptions, the hedged gross margin

impact calculated by aggregating individual sensitivities may not be equal to the

hedged gross margin impact calculated when correlations between the various

assumptions are also considered. |

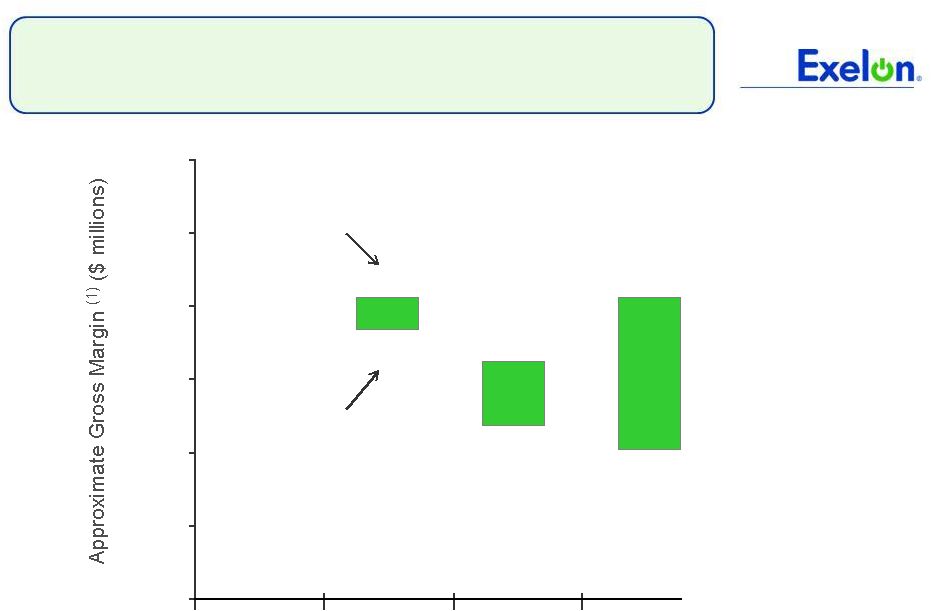

41

41

95% case

5% case

$5,400

$7,100

$6,800

$6,300

Exelon Generation Gross Margin Upside / Risk

(with Existing Hedges)

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2011

2012

$7,200

$5,000

2013

(1)

Represents an approximate range of expected gross margin, taking into account hedges in place, between

the 5th and 95th percent confidence levels assuming all unhedged supply is sold into the spot

market. Approximate gross margin ranges are based upon an internal simulation model and are subject to change based upon market inputs, future

transactions and potential modeling changes. These ranges of approximate gross margin in 2012 and 2013

do not represent earnings guidance or a forecast of future results as Exelon has not completed

its planning or optimization processes for those years. The price distributions that generate this range are calibrated to market quotes for power, fuel,

load following products, and options as of December 31, 2010. |

42

42

Midwest

Mid-Atlantic

South & West

Step 1

Start

with

fleetwide

open

gross

margin

$5.20 billion

Step 2

Determine

the

mark-to-market

value

of

energy hedges

99,600GWh * 92% *

($43.00/MWh-$30.69MWh)

= $1.13 billion

56,800GWh * 94% *

($57.00/MWh-$45.45MWh)

= $0.62 billion

9,500GWh * 71% *

($2.50/MWh-$1.12/MWh)

= $0.01 billion

Step 3

Estimate

hedged

gross

margin

by

adding open gross margin to mark-to-

market value of energy hedges

Open gross margin:

MTM

value

of

energy

hedges:

Estimated hedged gross margin:

Illustrative Example

of Modeling Exelon Generation 2011 Gross Margin

(with Existing Hedges)

$1.13

billion

+

$0.62

billion

+

$0.01

billion

$5.20 billion

$6.96 billion |

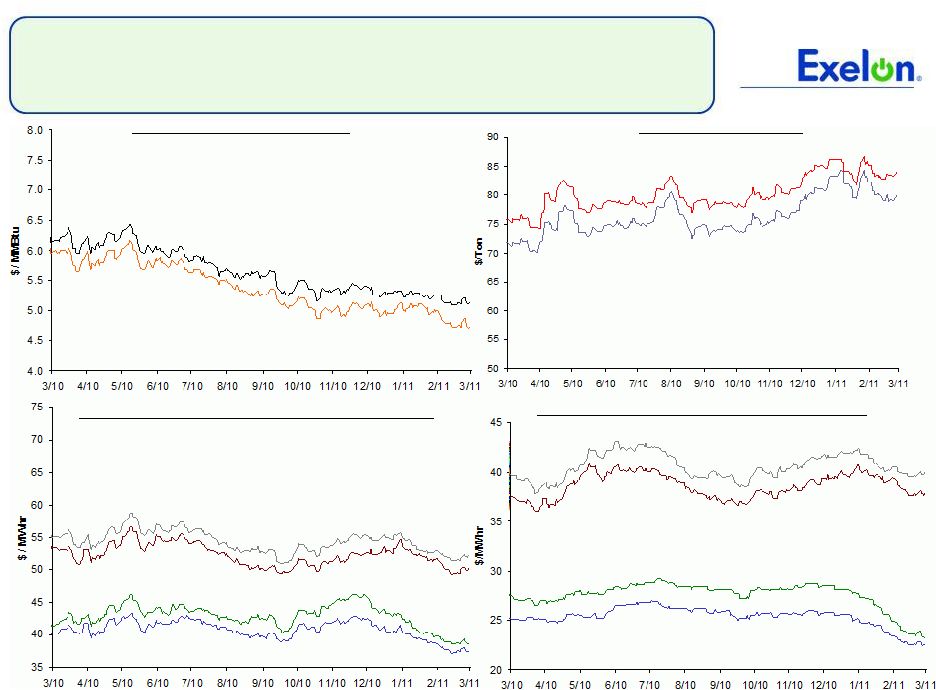

Market Price Snapshot

Forward NYMEX Natural Gas

PJM-West and Ni-Hub On-Peak Forward Prices

PJM-West and Ni-Hub Wrap Forward Prices

2012

$5.37

2013

$5.64

Rolling

12

months,

as

of

March

4

2011.

Source:

OTC

quotes

and

electronic

trading

system.

Quotes

are

daily.

Forward NYMEX Coal

2012

$76.44

2013

$80.28

2012

Ni-Hub

$40.80

2013

Ni-Hub

$42.87

2013

PJM-West

$54.34

2012

PJM-West

$52.32

2012

Ni-Hub

$25.40

2013

Ni-Hub

$27.58

2013

PJM-West

$40.56

2012

PJM-West

$38.63

43

th |

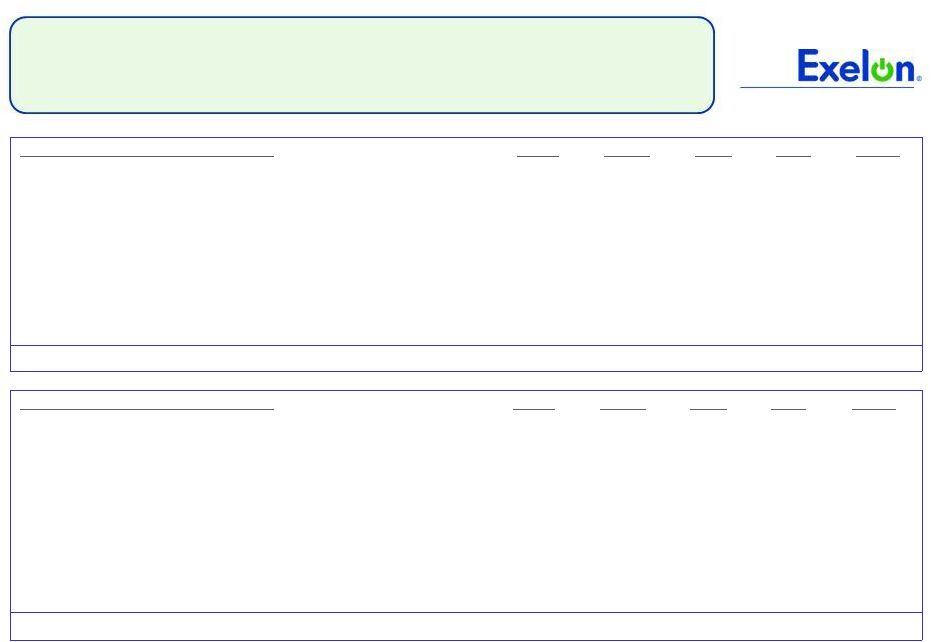

44

4.5

5.5

6.5

7.5

8.5

9.5

10.5

11.5

12.5

13.5

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

35

40

45

50

55

60

65

70

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/10

11/10

12/10

1/11

2/11

3/11

Market Price Snapshot

2013

9.31

2012

9.15

2012

$48.07

2013

$51.38

2012

$5.26

2013

$5.52

Houston Ship Channel Natural Gas

Forward Prices

ERCOT North On-Peak Forward Prices

ERCOT North On-Peak v. Houston Ship Channel

Implied Heat Rate

2012

$7.64

2013

$9.05

ERCOT North On Peak Spark Spread

Assumes a 7.2 Heat Rate, $1.50 O&M, and $.15 adder

Rolling

12

months,

as

of

March

4

2011.

Source:

OTC

quotes

and

electronic

trading

system.

Quotes

are

daily.

th |

45

4Q GAAP EPS Reconciliation

Three Months Ended December 31, 2010

ExGen

ComEd

PECO

Other

Exelon

2010 Adjusted (non-GAAP) Operating Earnings (Loss) Per Share

$0.81

$0.13

$0.03

$(0.01)

$0.96

Mark-to-market adjustments from economic hedging activities

(0.17)

-

-

-

(0.17)

2007 Illinois electric rate settlement

(0.01)

-

-

-

(0.01)

Unrealized gains related to nuclear decommissioning trust funds

0.04

-

-

-

0.04

Retirements of fossil generation units / plant retirements

(0.03)

-

-

-

(0.03)

John Deere Renewables acquisition costs

(0.01)

-

-

-

(0.01)

Asset Retirement Obligation reduction

-

0.01

-

-

0.01

4Q 2010 GAAP Earnings (Loss) Per Share

$0.63

$0.14

$0.03

$(0.01)

$0.79

NOTE: All amounts shown are per Exelon share and represent contributions to

Exelon's EPS. Amounts may not add due to rounding. Three Months Ended

December 31, 2009 ExGen

ComEd

PECO

Other

Exelon

2009 Adjusted (non-GAAP) Operating Earnings (Loss) Per Share

$0.66

$0.16

$0.12

$(0.02)

$0.92

Mark-to-market adjustments from economic hedging activities

0.04

-

-

-

0.04

2007 Illinois electric rate settlement

(0.02)

-

-

-

(0.02)

Unrealized gains related to nuclear decommissioning trust funds

0.02

-

-

-

0.02

City of Chicago settlement with ComEd

-

(0.01)

-

-

(0.01)

Costs associated with early debt retirements

(0.01)

-

-

(0.01)

(0.02)

Retirement of fossil generating units

(0.05)

-

-

-

(0.05)

4Q 2009 GAAP Earnings (Loss) Per Share

$0.64

$0.15

$0.12

$(0.03)

$0.88 |

46

Full Year GAAP EPS Reconciliation

NOTE: All amounts shown are per Exelon share and represent contributions to

Exelon's EPS. Amounts may not add due to rounding. Twelve Months Ended

December 31, 2010 ExGen

ComEd

PECO

Other

Exelon

2010 Adjusted (non-GAAP) Operating Earnings (Loss) Per Share

$2.91

$0.68

$0.54

$(0.07)

$4.06

Mark-to-market adjustments from economic hedging activities

0.08

-

-

-

0.08

2007 Illinois electric rate settlement

(0.02)

-

-

-

(0.02)

Unrealized gains related to nuclear decommissioning trust funds

0.08

-

-

-

0.08

Asset Retirement Obligation reduction

-

0.01

-

-

0.01

Retirement of fossil generating units

(0.08)

-

-

-

(0.08)

Non-cash remeasurement of income tax uncertainties

0.10

(0.16)

(0.03)

(0.01)

(0.10)

Non-cash charge resulting from health care legislation

(0.04)

(0.02)

(0.02)

(0.02)

(0.10)

Impact of certain emission allowances

(0.05)

-

-

-

(0.05)

John Deere Renewables acquisition costs

(0.01)

-

-

-

(0.01)

FY 2010 GAAP Earnings (Loss) Per Share

$2.97

$0.51

$0.49

$(0.10)

$3.87

Twelve Months Ended December 31, 2009

ExGen

ComEd

PECO

Other

Exelon

2009 Adjusted (non-GAAP) Operating Earnings (Loss) Per Share

$3.16

$0.54

$0.54

$(0.12)

$4.12

Mark-to-market adjustments from economic hedging activities

0.16

-

-

-

0.16

2007 Illinois electric rate settlement

(0.09)

(0.01)

-

-

(0.10)

Unrealized gains related to nuclear decommissioning trust funds

0.19

-

-

-

0.19

Nuclear decommissioning obligation reduction

0.05

-

-

-

0.05

City of Chicago settlement with ComEd

-

(0.01)

-

-

(0.01)

NRG acquisition costs

-

-

-

(0.03)

(0.03)

Impairment of certain generating assets

(0.20)

-

-

-

(0.20)

2009 severance charges

(0.01)

(0.02)

(0.00)

-

(0.03)

Non-cash remeasurement of income tax uncertainties and reassessment of state

deferred income taxes

0.06

0.06

-

(0.02)

0.10

Costs associated with early debt retirements

(0.07)

-

-

(0.04)

(0.11)

Retirement of fossil generating units

(0.05)

-

-

-

(0.05)

FY 2009 GAAP Earnings (Loss) Per Share

$3.21

$0.56

$0.53

$(0.21)

$4.09 |

47

GAAP to Operating Adjustments

Exelon’s 2011 adjusted (non-GAAP) operating earnings outlook excludes the

earnings effects of the following:

•

Mark-to-market adjustments from economic hedging activities

•

Unrealized gains and losses from nuclear decommissioning trust fund investments to

the extent not offset by contractual accounting as described in the notes

to the consolidated financial statements •

Significant impairments of assets, including goodwill

•

Changes in decommissioning obligation estimates

•

Costs associated with ComEd’s 2007 settlement with the City of Chicago

•

Financial impacts associated with the planned retirement of fossil generating

units •

Other unusual items

•

Significant changes to GAAP

Operating earnings guidance assumes normal weather for full year

O&M reconciliation:

2010

2011

ExGen

ComEd

PECO

Other

Exelon

ExGen

ComEd

PECO

Other

Exelon

Operating and maintenance (GAAP)

2,812

1,069

733

(14)

4,600

3,010

1,220

820

(10)

5,040

JDR acquisition costs

(11)

-

-

-

(11)

-

-

-

-

-

Retirement of fossil generating units

(3)

-

-

-

(3)

(30)

-

-

-

(30)

Non-cash charge resulting from health care legislation

(4)

(3)

(2)

8

(1)

-

-

-

-

-

Asset retirement obligation reduction

-

10

1

-

11

-

-

-

-

-

Adjusted Non-GAAP O&M

2,794

1,076

732

(6)

4,596

2,980

1,220

820

(10)

5,010

Decommissioning accretion

(57)

-

-

-

(57)

(70)

-

-

-

(70)

Regulatory required programs

-

(94)

(53)

-

(147)

-

(150)

(110)

-

(260)

Operating O&M (as shown on slide 7)

2,737

982

679

(6)

4,392

2,910

1,070

710

(10)

4,680

($ millions) |