Attached files

| file | filename |

|---|---|

| EX-23 - EXHIBIT 23 - MARINE PRODUCTS CORP | ex23.htm |

| EX-24 - EXHIBIT 24 - MARINE PRODUCTS CORP | ex24.htm |

| EX-32.1 - EXHIBIT 32.1 - MARINE PRODUCTS CORP | ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - MARINE PRODUCTS CORP | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - MARINE PRODUCTS CORP | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

(Mark One)

|

|

|

x

|

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

|

o

|

Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

Commission File No. 1-16263

MARINE PRODUCTS CORPORATION

|

Delaware

(State of Incorporation)

|

58-2572419

(I.R.S. Employer Identification No.)

|

2801 BUFORD HIGHWAY, SUITE 520

ATLANTA, GEORGIA 30329

(404) 321-7910

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

COMMON STOCK, $0.10 PAR VALUE

|

Name of each exchange on which registered

NEW YORK STOCK EXCHANGE

|

Securities registered pursuant to section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). o Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer o Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of Marine Products Corporation common stock held by non-affiliates on June 30, 2010, the last business day of the registrant’s most recent second fiscal quarter, was $53,642,986 based on the closing price on the New York Stock Exchange on June 30, 2010 of $5.66 per share.

Marine Products Corporation had 37,324,801 shares of common stock outstanding as of February 18, 2011.

Documents Incorporated by Reference

Portions of the Proxy Statement for the 2011 Annual Meeting of Stockholders of Marine Products Corporation are incorporated by reference into Part III, Items 10 through 14 of this report.

1

PART I

References in this document to “we,” “our,” “us,” “Marine Products,” or “the Company” mean Marine Products Corporation (“MPC”) and its subsidiaries, Chaparral Boats, Inc. (“Chaparral”) and Robalo Acquisition Company LLC (“Robalo”), collectively or individually, except where the context indicates otherwise.

Forward-Looking Statements

Certain statements made in this report that are not historical facts are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. Such forward-looking statements may include, without limitation, statements that relate to our business strategy, plans and objectives, and our beliefs and expectations regarding future demand for our products and services and other events and conditions that may influence our performance in the future.

The words “may,” “should,” “will,” “expect,” “believe,” “anticipate,” “intend,” “plan,” “seek,” “project,” “estimate,” and similar expressions used in this document that do not relate to historical facts are intended to identify forward-looking statements. Such statements are based on certain assumptions and analyses made by our management in light of its experience and its perception of historical trends, current conditions, expected future developments and other factors it believes to be appropriate. The forward-looking statements include, without limitation, statements regarding our belief that international sales could produce additional sales growth; our belief that the Wide TechTM bow design may be incorporated on other Chaparral boat models in subsequent model years; management’s belief that Marine Products is well positioned to take advantage of current market conditions which characterize the industry; our intention to continue seeking the most advantageous purchasing arrangements from our suppliers; our ability to execute our marketing strategy to increase market share by expanding our presence by building dedicated sales, marketing and distribution systems; our intention to continue to strengthen our dealer network and build brand loyalty with dealers and customers; our ability to locate and complete strategic acquisitions that will complement our existing product lines, expand our geographic presence and strengthen our capabilities; our belief that our corporate infrastructure and marketing and sales capabilities, in addition to our cost structure and nationwide presence, enable us to compete effectively; our belief that we do not currently anticipate that any material expenditures will be required to continue to comply with existing environmental or safety regulations; our belief that the increase in prices of certain commodities is likely to lead to higher costs in 2011 and that we may not be able to increase prices to compensate for increased costs; our belief that our product liability insurance will be adequate; our belief that we have not suffered an increased risk of default among our municipal securities investments; our intention to pursue acquisitions and form strategic alliances that will enable us to acquire complementary skills and capabilities, offer new products, expand our customer base and obtain other competitive advantages; our belief that the ultimate outcome of litigation arising in the ordinary course of business will not have a material adverse effect on our liquidity, financial condition or results of operations; our ability to execute stated business and financial strategies in the future to better manage our Company; our belief that net sales will increase moderately in 2011 compared to 2010 and that our operating results will improve; our belief that the downturn in recreational boating has ended; our belief that our dealers’ inventory levels are appropriate which will allow us to increase production in the event of an increase in demand; our belief that retail sales will not increase significantly in 2011; our belief that advertising and consumer targeting efforts will benefit the industry and Marine Products; our anticipation that the Company will continue to be challenged by the effect of an uncertain level of consumer demand; expectations about the amount of contributions to our defined benefit plan and capital expenditures during 2011 and the purpose of those capital expenditures; the adequacy of the Company’s capital resources; the amount and timing of future contractual obligations; judgments about the Company’s critical accounting policies; and the effect of various recent accounting pronouncements on the Company, its operating results and financial condition. These statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Marine Products Corporation to be materially different from any future results, performance or achievements expressed or implied in such forward-looking statements. These risks involve the outcome of current and future litigation, the impact of interest rates, economic conditions, fuel costs and weather on our business, our dependence on a network of independent boat dealers, the possibility of defaults by our dealers in their obligations to third-party dealer floor plan lenders, and our reliance on third-party suppliers. We caution you that such statements are only predictions and not guarantees of future performance and that actual results, developments and business decisions may differ from those envisioned by the forward-looking statements. See “Risk Factors” on page 11 for a discussion of factors that may cause actual results to differ from our projections.

2

Item 1. Business

Marine Products manufactures fiberglass motorized boats distributed and marketed through its independent dealer network. Marine Products’ product offerings include Chaparral sterndrive and inboard pleasure boats and Robalo outboard sport fishing boats.

Organization and Overview

Marine Products is a Delaware corporation incorporated on August 31, 2000, in connection with a spin-off from RPC, Inc. (NYSE: RES) (“RPC”). Effective February 28, 2001, RPC accomplished the spin-off by contributing 100 percent of the issued and outstanding stock of Chaparral to Marine Products, a newly formed wholly owned subsidiary of RPC, and then distributing the common stock of Marine Products to RPC stockholders.

Marine Products designs, manufactures and sells recreational fiberglass powerboats in the sportboat, deckboat, cruiser, sport yacht and sport fishing markets. The Company sells its products to a network of 137 domestic and 55 international independent authorized dealers. Marine Products’ mission is to enhance its customers’ boating experience by providing them with high quality, innovative powerboats. The Company intends to remain a leading manufacturer of recreational powerboats for sale to a broad range of consumers worldwide.

The Company manufactures Chaparral sterndrive and inboard-powered pleasure boats including SSi Sportboats, SSX Sportdecks, Sunesta Wide TechTM and Xtreme boats, Signature Cruisers, Premiere Sport Yachts and Robalo outboard sport fishing boats. The most recent available industry statistics [source: Statistical Surveys, Inc. report dated September 30, 2010] indicate that Chaparral is the fourth largest manufacturer of sterndrive boats in lengths from 18 to 35 feet in the United States.

Chaparral was founded in 1965 in Ft. Lauderdale, Florida. Chaparral’s first boat was a 15-foot tri-hull design with a retail price of less than $1,000. Over time Chaparral grew by offering exceptional quality and consumer value. In 1976, Chaparral moved to Nashville, Georgia, where a manufacturing facility of a former boat manufacturing company was available for purchase. This provided Chaparral an opportunity to obtain additional manufacturing space and access to a trained work force. With almost 45 years of boatbuilding experience, Chaparral continues to improve the design and manufacturing of its product offerings to meet the growing needs of discriminating recreational boaters.

Robalo was founded in 1969 and its first boat was a 19-foot center console salt-water fishing boat, among the first of this type of boat to have an “unsinkable” hull. The Company believes that Robalo’s share of the outboard sport fishing boat market is approximately three percent.

3

Products

Marine Products distinguishes itself by offering a wide range of products to the family recreational, cruiser and sport yacht markets through its Chaparral brand, and to the sport fishing market through its Robalo brand.

The following table provides a brief description of our product lines and their particular market focus:

|

Product Line

|

Number

of

Models

|

Overall

Length

|

Approximate

Retail

Price Range

|

Description

|

||||

|

Chaparral - SSi Sportboats

|

7

|

18′-25′

|

$35,000 - $83,000

|

Fiberglass closed deck runabouts. Encompasses affordable, entry-level to mid-range and larger sportboats. Marketed as high value runabouts for family groups.

|

||||

|

Chaparral - SSX Sportdecks

|

4

|

26′-32′

|

$79,000 - $297,000

|

Fiberglass bowrider crossover sportboats that combine the ride of a sportboat and the usefulness of a deckboat. Marketed as high value runabouts for family groups.

|

||||

|

Chaparral - Sunesta Xtreme Tow Boats

|

8

|

20′-28′

|

$61,000 - $160,000

|

Fiberglass pleasure boats with a high-performance hull design and updated styling. Wide TechTM is marketed as an affordable, entry-level to mid-range pleasure boat with the handling of a runabout, the style of a sportboat and the roominess of a cruiser. Xtreme is marketed as a high-performance wakeboard/ski boat with technical features and styling that appeal to wakeboard and ski enthusiasts.

|

||||

|

Chaparral - Signature Cruisers

|

6

|

27′-37′

|

$92,000 - $419,000

|

Fiberglass, accommodation-focused cruisers. Marketed to experienced boat owners through trade magazines and boat show exhibitions.

|

||||

|

Chaparral - Premiere Sport Yacht

|

1

|

42′

|

$680,000 - $877,000

|

High value, fiberglass sport yacht with a Wide TechTM bow design marketed to experienced boat owners through trade magazines and boat show exhibitions.

|

||||

|

Robalo - Sport Fishing Boats

|

10

|

22′-30′

|

$54,000 - $277,000

|

Sport fishing boats for large freshwater lakes or saltwater use. Marketed to experienced fishermen.

|

4

Manufacturing

Marine Products’ manufacturing facilities are located in Nashville, Georgia and Valdosta, Georgia. Since 2008, the Company idled its plant located in Valdosta, Georgia in response to the decline in production volumes but this is expected to be temporary. Marine Products utilizes five different plants to, among other things, manufacture interiors, design new models, create fiberglass hulls and decks, and assemble various end products. Quality control is conducted throughout the manufacturing process. The Company’s manufacturing operations are ISO 9001: 2008 certified, which is an international designation of design, manufacturing, and customer service processes. ISO 9001: 2008 surpasses previous ISO designations. Management believes Chaparral is the third largest sterndrive boat manufacturing brand to hold the ISO 9001: 2008 certification. When fully assembled and inspected, the boats are loaded onto either company-owned trailers or third-party marine transport trailers for delivery to dealers. The manufacturing process begins with the design of a product to meet dealer and customer needs. Plugs are constructed in the research and development phase from designs. Plugs are used to create a mold from which prototype boats can be built. Adjustments are made to the plug design until acceptable parameters are met. The final plug is used to create the necessary number of production molds. Molds are used to produce the fiberglass hulls and decks. Fiberglass components are made by applying the outside finish or gel coat to the mold, then numerous layers of fiberglass and resin are applied during the lamination process over the gel coat. After curing, the hull and deck are removed from the molds and are trimmed and prepared for final assembly, which includes the installation of electrical and plumbing systems, engines, upholstery, accessories and graphics.

Product Warranty

For most of our Chaparral products, Marine Products provides a lifetime limited structural hull warranty against defects in material and workmanship for the original purchaser, and a five-year limited structural hull warranty for one subsequent owner. Additionally, a non-transferable five-year limited structural deck warranty against defects in materials and workmanship is available to the original owner. Warranties on additional items are provided for periods of one to five years.

For our Chaparral Premiere model, Marine Products provides a transferable structural hull and deck warranty against defects in material and workmanship for the original and one subsequent owner. A one-year limited warranty is available on most other components to the original owner and one subsequent owner along with warranties on some addition items ranging from one to five years.

For our Robalo products, Marine Products provides a transferable 10-year limited structural hull warranty against defects in material and workmanship to the original owner, and a five-year limited hull warranty to one subsequent owner. Additionally, Marine Products provides a transferable one-year limited warranty on other components.

The engine manufacturers for our Robalo and Chaparral products warrant engines included in the boats as well.

Suppliers

Marine Products’ two most significant components used in manufacturing its boats, based on cost, are engines and fiberglass. For each of these, there is currently an adequate supply available in the market. Marine Products has not experienced any material shortages in any of these products. Temporary shortages, when they do occur, usually involve manufacturers of these products adjusting model mixes, introducing new product lines or limiting production in response to an industry-wide reduction in boat demand. Marine Products obtains most of its fiberglass from a leading domestic supplier. Marine Products believes that there are several alternative suppliers if this supplier fails to provide adequate quality or quantities at acceptable prices.

Marine Products does not manufacture the engines installed in its boats. Engines are generally specified by the dealers at the time of ordering, usually on the basis of anticipated customer preferences or actual customer orders. Sterndrive engines are purchased through the American Boatbuilders Association (“ABA”), which has entered into engine supply arrangements with Mercury Marine and Volvo Penta, the two currently existing suppliers of sterndrive engines. These arrangements contain incentives and discount provisions, which may reduce the cost of the engines purchased, if specified purchase volumes are met during specified periods of time. Although no minimum purchases are required, Marine Products expects to continue purchasing sterndrive engines through the ABA on a voluntary basis in order to receive volume-based purchase discounts. Marine Products does not have a long-term supply contract with the ABA. Marine Products has an outboard engine supply contract with Yamaha. This engine supply arrangement was not negotiated through the ABA. In the event of a sudden and extended interruption in the supply of engines from these suppliers, our sales and profitability could be negatively impacted. See “Risk Factors” below.

Marine Products uses other raw materials in its manufacturing processes. Among these are stainless steel, copper and resins made from hydrocarbon feedstocks. In response to global economic weakness impacting demand, the average prices of these commodities fell during 2008 and the first two quarters of 2009, but began to rise during the last two quarters of 2009 and during 2010 as the global economy improved. See “Inflation” below.

5

Sales and Distribution

Domestic sales are made through approximately 94 Chaparral dealers, 18 Robalo dealers and 25 dealers that sell both brands located in markets throughout the United States. Marine Products also has 55 international dealers. During 2009 a number of our dealers ceased operations for various reasons, although we were able to replace many of them with new dealers in the same markets. During 2010 the financial strength of our dealer network improved due to lower field inventories and greater availability of floorplan financing. Most of our dealers inventory and sell boat brands manufactured by other companies, including some that compete directly with our brands. The territories served by any dealer are not exclusive to the dealer; however, Marine Products uses discretion in establishing relationships with new dealers in an effort to protect the mutual interests of the existing dealers and the Company. Marine Products’ eight independent field sales representatives call upon existing dealers and develop new dealer relationships. The field sales representatives are directed by a National Sales Coordinator, who is responsible for developing a full dealer distribution network for the Company’s products. The marketing of boats to retail customers is primarily the responsibility of the dealer. Marine Products supports dealer marketing efforts by supplementing local advertising, sales and marketing follow up in boating magazines, and participation in selected regional, national, and international boat show exhibitions. No single dealer accounted for more than 10 percent of net sales during 2010 or 2008; however, due to significantly lower sales in 2009, one dealer accounted for approximately 13 percent of net sales in 2009.

Marine Products continues to seek new dealers in many areas throughout the U.S., Europe, South America, Asia, Russia and the Middle East. In general, Marine Products requires payment in full before it will ship a boat overseas. Consequently, there is no credit risk associated with its international sales or risk related to foreign currency fluctuation. Marine Products believes international sales could produce additional sales growth. The volume of sales to international dealers increased in 2010 compared to 2009 while there was a decline in 2009 compared to 2008. International sales are also affected by the value of the U.S. dollar relative to other currencies. International net sales as a percentage of total net sales were 30.5 percent in 2010, 29.4 percent in 2009, and 33.4 percent in 2008.

Marine Products’ sales orders are indicators of strong interest from its dealers. Historically, dealers have in most cases taken delivery of all their orders. The Company attempts to ensure that its dealers do not accept an excessive amount of inventory by monitoring their inventory levels. During 2009, the Company produced and sold its products to dealers at a much lower level than the level of retail sales in order to facilitate a reduction in field inventory. Knowledge of inventory levels at the individual dealers facilitates production scheduling with very short lead times in order to maintain flexibility, in the event that adjustments need to be made to dealer shipments. In the past, Marine Products has been able to resell any boat for which the order has been cancelled.

Approximately half of Marine Products’ domestic shipments are made pursuant to “floor plan financing” programs in which Marine Products’ subsidiaries participate on behalf of their dealers with major third-party financing institutions. The remaining dealers finance their boat inventory with smaller regional financial institutions in local markets or pay cash. Under these established arrangements with qualified lending institutions, a dealer establishes a line of credit with one or more of these lenders for the purchase of boat inventory for sales to retail customers in their showroom or during boat show exhibitions. In general, when a dealer purchases and takes delivery of a boat pursuant to a floor plan financing arrangement, it draws against its line of credit and the lender pays the invoice cost of the boat directly to Marine Products generally within 10 business days. When the dealer in turn sells the boat to a retail customer, the dealer repays the lender, thereby restoring its available credit line. Each dealer’s floor plan credit facilities are secured by the dealer’s inventory, letters of credit, and perhaps other personal and real property. Until recently, most dealers maintained financing arrangements with more than one lender, although that is less common at the present time, given that there are fewer lenders. In connection with a dealer’s floor plan financing arrangements with a qualified lending institution, Marine Products or its subsidiaries have agreed to repurchase inventory which the lender repossesses from a dealer and returns to Marine Products in a “new and unused” condition subject to normal wear and tear, as defined. The contractual agreements that Marine Products or its subsidiaries have with these qualified lenders contain the Company’s assumption of specified percentages of the debt obligation on repossessed boats, up to certain contractually determined dollar limits set by the lender.

During 2009, an amendment to the current agreement with one of the Company’s floor plan lenders was executed with a contractual repurchase limit of $9.0 million effective January 1, 2009 which expired June 30, 2010. Effective July 1, 2010, this agreement was further amended to change the contractual repurchase limit to not exceed 15 percent of the amount of the average net receivables financed by the floor plan lender for dealers during the prior 12 month period. The Company has contractual repurchase agreements with additional lenders with an aggregate maximum repurchase obligation of approximately $5.0 million, with various expiration and cancellation terms of less than one year, for an aggregate repurchase obligation with all financing institutions of approximately $9.4 million as of December 31, 2010. In the event that a dealer defaults under a credit line, the qualified lender may then invoke the manufacturers’ repurchase obligation with respect to that dealer. In that event, all repurchase agreements of all manufacturers supplying a defaulting dealer are generally invoked regardless of the boat or boats with respect to which the dealer has defaulted. Unlike Marine Products’ obligation to repurchase boats repossessed by lenders, Marine Products is under no obligation to repurchase boats directly from dealers. Marine Products does not sponsor financing programs to the consumer; any consumer financing promotions for a prospective boat purchaser would be the responsibility of the dealer.

6

Marine Products’ dealer sales incentive programs are generally designed to promote early replenishment of the stock in dealer inventories depleted throughout the prime spring and summer selling seasons, and to promote the sales of older models in dealer inventory and particular models during specified periods. These programs help to stabilize Marine Products’ manufacturing between the peak and off-peak periods, and promote sales of certain models. For the 2011 model year (which commenced July 1, 2010), Marine Products offered its dealers several sales incentive programs based on dollar volumes and timing of dealer purchases. Program incentives offered include sales discounts, retail sales incentives and payment of floor plan financing interest charged by qualified floor plan providers to dealers generally through May 1, 2011. After the interest payment programs end, interest costs revert to the dealer at rates set by the lender. A dealer makes periodic curtailment payments (principal payments) on outstanding obligations against its dealer inventory as set forth in the floor plan financing agreements between the dealer and their particular lender.

As part of Marine Products’ strategy to assist dealers in reducing their inventories, the Company assisted dealers during 2009 in liquidating non-current models in dealer inventories in addition to the sales incentive programs described above. During the 2009 retail selling season, Marine Products supported its dealers by sharing in the additional cost of retail incentives for non-current models totaling approximately $8.6 million. We believe this effort to liquidate inventory was successful in reducing our dealer field inventories during 2009 and 2010. As a result, in 2010 our production increased significantly in comparison to 2009 in order to meet dealer demand for our products. Additionally, we recorded much lower retail incentive costs in 2010 compared to 2009 due to the renewed financial strength of our dealer network and their ability to maintain appropriate inventory levels relative to customer retail demand.

The sales order backlog as of December 31, 2010 was approximately 490 boats with estimated net sales of approximately $19.5 million. This represents an approximate 12 week backlog based on recent production levels. The Company will continue to monitor the number of boats in dealer inventory and is prepared to adjust its production levels as it deems necessary to manage dealer inventory levels. The Company typically does not manufacture a significant number of boats for its own inventory. The Company occasionally manufactures boats for its own inventory because the number of boats required for immediate shipment is not always the most efficient number of boats to produce in a given production schedule.

Research and Development

Essentially the same technologies and processes are used to produce fiberglass boats by all boat manufacturers. The most common method is open-face molding. This is usually a labor-intensive, manual process whereby employees hand spray and apply fiberglass and resin in layers on open molds to create boat hulls, decks and other smaller fiberglass components. This process can result in inconsistencies in the size and weight of parts, which may lead to higher warranty costs. A single open-face mold is typically capable of producing approximately three hulls per week.

Marine Products has been a leading innovator in the recreational boating industry. One of the Company’s most innovative designs is the full-length “Extended V-Plane” running surface on its Chaparral boat models. Typically, sterndrive boats have a several foot gap on the bottom rear of the hull where the engine enters the water. With the Extended V-Plane, the running surface extends the full length to the rear of the boat. The benefit of this innovation is more deck space, better planing performance and a more comfortable ride. Although the basic hull designs are similar, the Company has historically introduced a variety of new models each year and periodically replaces, updates or discontinues existing models.

Another hull design is the Hydro LiftTM used on the Robalo boat models. This variable dead rise hull design provides a smooth ride in rough conditions. It increases the maximum speed obtainable by a given engine horsepower and weight of the boat. Robalo’s current models utilize the Hydro LiftTM design and we plan to continue to provide this design on Robalo models.

A bow design known as the Wide TechTM was first used on the Chaparral Sunesta Wide TechTM and Xtreme models for the 2008 model year, and for the 2011 model year is being used on Chaparral’s Premiere Sport Yacht, SSi Wide TechTM Sport Boats, Sunesta Sportdecks, Xtreme Tow Boats and two Signature Cruisers. The Wide TechTM bow design allows the models to have the Extended V-Plane hull, with the features and benefits that this hull design offers. In addition, the Wide TechTM bow design provides a larger seating area, as well as additional storage space, in the front of the boat. Furthermore, it allows the models to have a non-skid walkway on the bow, which makes entering and leaving the boat easier than in other boat models. This bow design may be incorporated on other Chaparral boat models in subsequent model years.

In support of its new product development efforts, Marine Products incurred research and development costs of $489 thousand in 2010, $712 thousand in 2009, and $1.8 million in 2008.

Industry Overview

For 2010, the recreational boating industry accounted for less than one percent of the United States gross domestic product. The recreational marine market is a mature market, with 2009 (latest data available to us) retail expenditures of approximately $31 billion spent on new and used boats, motors and engines, trailers, accessories and other associated costs as estimated by the National Marine Manufacturers Association (“NMMA”). Pleasure boats compete for consumers’ free time with all other leisure activities, from computers and video games to other outdoor sports. Non-active boat owners cite the lack of leisure time as the primary reason for not using their boats.

7

The NMMA conducts various surveys of pleasure boat industry trends, and the most recent surveys indicate that 66 million adults in the United States participated in recreational boating in 2009, a decrease of six percent compared to the prior year. There are currently approximately 17 million boats owned in the United States, including outboard, inboard, sterndrive, sailboats, personal watercraft, and miscellaneous (canoes, kayaks, rowboats, etc.). Marine Products competes in the sterndrive and inboard boating category with its five lines of Chaparral boats, and in the outboard boating category with its Robalo sport fishing boats. More than 90 percent of the Company’s unit sales are sterndrive boats.

Industry sales of new sterndrive boats in the United States during 2010 totaling 14,922 (source: Info-Link Technologies, Inc.) accounted for approximately 33 percent of the total new fiberglass powerboats sold that were between 18 and 35 feet in hull length. Sales of sterndrive boats had an estimated total retail value of $0.7 billion, or an average retail price per boat of approximately $47,000. Management believes that the five largest states for boat sales at the present time are Florida, Texas, California, North Carolina and New York. Marine Products has dealers in each of these states.

The U.S. domestic recreational boating industry includes sales in the segments of new and used boats, motors and engines, trailers, and other boat accessories. The new fiberglass boat market segment with hull lengths of 18 to 35 feet, the primary market segment in which Marine Products competes, represented $1.9 billion in retail sales during 2010. The table below reflects the estimated sales within this segment by category for 2010 and 2009, ranked by 2010 retail sales (source: Info-Link Technologies, Inc.):

|

2010

|

2009

|

|||||||||||||||

|

Boats

|

Sales ($ B)

|

Boats

|

Sales ($ B)

|

|||||||||||||

|

Sterndrive Boats

|

14,922 | $ | 0.7 | 21,655 | $ | 1.0 | ||||||||||

|

Outboard Boats

|

23,031 | 0.8 | 28,545 | 1.0 | ||||||||||||

|

Inboard Boats

|

5,290 | 0.3 | 6,880 | 0.4 | ||||||||||||

|

Jet Boats

|

2,518 | 0.1 | 2,522 | 0.1 | ||||||||||||

|

TOTAL

|

45,761 | $ | 1.9 | 59,602 | $ | 2.5 | ||||||||||

Chaparral’s products are categorized as sterndrive and inboard boats and Robalo’s products are categorized as outboard boats. As shown in the table above, the sterndrive boat segment experienced the largest percentage decline in unit sales between 2009 and 2010. The Company believes that the larger decline in unit sales of sterndrive boats in 2010 was due to these units’ higher average retail selling prices, which made consumers more reluctant to purchase them during the recent recession.

The recreational boat manufacturing market remains highly fragmented with the exception of Brunswick Corporation, which has acquired and currently operates a number of recreational boat brands. We estimate that the boat manufacturing industry includes over 130 sterndrive manufacturers and over 300 outboard boat manufacturers, largely small, privately held companies with varying degrees of professional management and manufacturing skill. According to estimates provided by Statistical Surveys, Inc., during the nine months ended September 30, 2010 (latest information available), the top five sterndrive manufacturers, which includes Chaparral, have a market share of approximately 52 percent. Chaparral’s market share in units during the period was 7.5 percent, which represents a decrease of 0.4 percent compared to the 12 months ended December 31, 2009. The Company believes that Chaparral’s market share declined during this period because of competition from other manufacturers and dealers who were forced to liquidate inventory during 2009 and 2010 because of pressure from floorplan lenders or other financial constraints.

Several factors influence sales trends in the recreational boating industry, including general economic growth, consumer confidence, household incomes, the availability and cost of financing for our dealers and customers, weather, fuel prices, tax laws, demographics and consumers’ leisure time. Also, the value of residential and vacation real estate in strong boating states such as California and Florida influences recreational boat sales. In addition, inflation, the cost of certain components and the impact of environmental regulation have increased the cost of boats in recent years. As the cost of certain raw materials used in the manufacturing process has increased, the cost of boat ownership has increased as well, prompting consumers either to buy a smaller or less expensive boat or defer or forego their purchase. Competition from other leisure and recreational activities, such as vacation properties and travel, can also affect sales of recreational boats.

Management believes Marine Products is well positioned to take advantage of the following conditions, which continue to characterize the industry:

● labor-intensive manufacturing processes that remain largely unautomated;

● increasingly strict environmental standards derived from governmental regulations and customer sensitivities;

● a lack of focus on coordinated customer service and support by dealers and manufacturers;

● a lack of financial strength among retail boat dealers and many manufacturers, and tight credit availability by floor plan lenders; and

8

● a high degree of fragmentation and competition among the large number of sterndrive and outboard recreational boat manufacturers.

Business Strategies

Recreational boating is a mature industry. According to Info-Link Technologies, Inc., sales of sterndrive boats declined at a compounded annual rate of approximately 34 percent between 2007 and 2010. During this period, Marine Products experienced a compounded annual decline rate of approximately 27 percent in the number of boats sold. The Company has historically grown its boat sales and net sales primarily through increasing market share and by expanding its number of models and product lines. While the Company’s strategy in 2009 was to reduce dealer inventories dramatically, in 2010 the Company has been replenishing dealer inventories. As a result, the Company’s unit sales to dealers increased in 2010 by more than 111.1 percent in comparison to 2009. Chaparral has grown its sterndrive market share in the 18 to 35 feet length category from 5.9 percent in fiscal 1996 to 7.5 percent during the nine months ended September 30, 2010 (the most recent information provided to us by Statistical Surveys, Inc.). Market share is greater than this in several of our larger boat models, although this increased market share declined during 2010, as consumers purchased smaller boats with lower average selling prices. The Company continues to expand its product offerings in the outboard boat market and by improvement of existing models and expansion into larger boats within its sterndrive and inboard offerings.

During 2010 we significantly increased our production levels as compared to 2009 in order for dealers to replenish their inventories of updated models in response to consumer demand. In 2010 incentive programs offered to dealers were more normalized in comparison to 2009 when we supported our dealers with retail incentive programs which included financial support in the form of additional incentives during the traditional peak retail selling season.

Marine Products’ operating strategy emphasizes innovative designs and manufacturing processes, by producing a high quality product while seeking to lower manufacturing costs through increased efficiencies in our facilities. In the current and projected near-term depressed selling environment for our products, our operating strategy also includes producing fewer models, with fewer options and more standard features, in order to maximize profitability at lower production levels and reduce the amount and value of inventory our dealers are forced to carry. In addition, we seek opportunities to leverage our buying power through economies of scale. Management believes its membership in the ABA positions Marine Products as a significant third-party customer of major suppliers of sterndrive engines. Marine Products’ Chaparral subsidiary is a founding member of the ABA, which collectively represents 13 independent boat manufacturers that have formed a buying group to pool their purchasing power in order to gain improved pricing on engines, fiberglass, resin and many other components. Marine Products intends to continue seeking the most advantageous purchasing arrangements from its suppliers.

Our marketing strategy seeks to increase market share by enabling Marine Products to expand its presence by building dedicated sales, marketing and distribution systems. Marine Products has a distribution network of 192 dealers located throughout the United States and internationally. Our strategy is to increase selectively the quantity of our dealers, and work to improve the quality and effectiveness of our entire dealer network. We have implemented a marketing program for potential new dealers which emphasizes our financial strength and product quality as an alternative to many competitors who are less financially stable and less able to support their dealers with quality products and good service. During 2009 we lost a number of dealers who exited the business; however, we gained almost as many new dealers because dealers who sell other brands approached us because their manufacturer became insolvent or ceased production. Marine Products seeks to capitalize on its strong dealer network by educating its dealers on the sales and servicing of our products and helping them provide more comprehensive customer service, with the goal of increasing customer satisfaction, customer retention and future sales. Marine Products provides promotional and incentive programs to help its dealers increase product sales and customer satisfaction. Marine Products believes that the challenging selling environment for our industry provides an opportunity for us to strengthen our dealer network and build brand loyalty with both dealers and customers because Marine Products is better capitalized than most of its competitors.

A component of Marine Products’ overall strategy is to consider making strategic acquisitions in order to complement existing product lines, expand its geographic presence in the marketplace and strengthen its capabilities depending upon availability, price and complementary product lines. We constantly review potential acquisition targets and intend to continue doing so in the future.

Competition

The recreational boat industry is highly fragmented, resulting in intense competition for customers, dealers and boat show exhibition space. There is significant competition both within markets we currently serve and in new markets that we may enter. Marine Products’ brands compete with several large national or regional manufacturers that have substantial financial, marketing and other resources. However, we believe that our corporate infrastructure and marketing and sales capabilities, in addition to our cost structure and our nationwide presence, enable us to compete effectively against these companies. In each of our markets, Marine Products competes on the basis of responsiveness to customer needs, the quality and range of models offered, and the competitive pricing of those models. Additionally, Marine Products faces general competition from all other recreational businesses seeking to attract consumers’ leisure time and discretionary spending dollars.

9

According to Statistical Surveys, Inc., the following is a list of the top ten (largest to smallest) sterndrive boat manufacturers in the United States based on unit sales in 2010. According to Statistical Surveys, Inc., the companies set forth below represent approximately 75 percent of all United States retail sterndrive boat registrations for the nine months ended September 30, 2010.

| 1. | Bayliner * | ||

| 2. | Sea Ray * | ||

| 3. | Tahoe | ||

| 4. | Chaparral | ||

| 5. | Cobalt | ||

| 6. | Stingray | ||

| 7. | Glastron | ||

| 8. | Crownline | ||

| 9. | Four Winns | ||

| 10. | Regal |

The outboard engine powered market has a large breadth and depth, accounting for approximately 70 percent of traditional powerboat unit sales during 2009 (the latest year available). Robalo’s share of the outboard sport fishing boat market during the nine months ended September 30, 2010 was approximately three percent. Primary competitors for Robalo during 2010 included Sea Hunt, Grady-White, Sea Fox, Boston Whaler*, Hydro Sports, Everglades and Parker.

* Division or subsidiary of Brunswick Corporation.

Environmental and Regulatory Matters

Certain materials used in boat manufacturing, including the resins used to make the decks and hulls, are toxic, flammable, corrosive, or reactive and are classified by the federal and state governments as “hazardous materials.” Control of these substances is regulated by the Environmental Protection Agency (“EPA”) and state pollution control agencies, which require reports and inspect facilities to monitor compliance with their regulations. The Occupational Safety and Health Administration (“OSHA”) standards limit the amount of emissions to which an employee may be exposed without the need for respiratory protection or upgraded plant ventilation. Marine Products’ manufacturing facilities are regularly inspected by OSHA and by state and local inspection agencies and departments. Marine Products believes that its facilities comply in all material aspects with these regulations. Although capital expenditures related to compliance with environmental laws are expected to increase during the coming years, we do not currently anticipate that any material expenditure will be required to continue to comply with existing environmental or safety regulations in connection with our existing manufacturing facilities.

Recreational powerboats sold in the United States must be manufactured to meet the standards of certification required by the United States Coast Guard. In addition, boats manufactured for sale in the European Community must be certified to meet the European Community’s imported manufactured products standards. These certifications specify standards for the design and construction of powerboats. All boats sold by Marine Products meet these standards. In addition, safety of recreational boats is subject to federal regulation under the Boat Safety Act of 1971. The Boat Safety Act requires boat manufacturers to recall products for replacement of parts or components that have demonstrated defects affecting safety. Marine Products has instituted recalls for defective component parts produced by other manufacturers and for one issue related to Marine Products’ design or manufacturing process. None of the recalls has had a material adverse effect on Marine Products.

During 2009 the EPA adopted regulations stipulating that many marine propulsion engines manufactured for the 2010 model year and later meet an air emission standard that requires fitting a catalytic converter to the engine. These regulations also require, among other things, that the engine manufacturer provide a warranty that the engine meets EPA emission standards. The majority of the engines used in Marine Products’ Chaparral product line and all of the engines used in the Company’s Robalo product line are subject to these regulations. These regulations are similar to regulations adopted by the California Air Resources Board in 2007, but apply to all U.S. states and territories. This regulation will increase the cost of the majority of the Company’s sterndrive products. The additional cost of complying with these EPA regulations may reduce Marine Products’ profitability, because the Company may have to absorb the increased cost. It may also reduce Marine Products’ net sales, because the increased cost of owning a boat may force consumers to buy a smaller or less expensive boat or forego a boat purchase, and because increased product cost will reduce the amount of inventory that Marine Products’ dealers can carry, thus reducing retail consumers’ choices.

Employees

As of December 31, 2010, Marine Products had approximately 360 employees (an increase from approximately 300 at December 31, 2009), of whom six were management and 29 administrative. Although the number of employees has increased in 2010 compared to 2009 in order to increase production levels, the Company continues to maintain a significantly smaller work force during 2010 and throughout 2011 compared to years prior to 2009 in an effort to align costs with sales and consumer demand for our products.

10

None of Marine Products’ employees are party to a collective bargaining agreement. Marine Products’ entire workforce is currently employed in the United States and Marine Products believes that its relations with its employees are good.

Proprietary Matters

Marine Products owns a number of trademarks, trade names and patents that it believes are important to its business. Except for the Chaparral, Robalo and Wahoo! trademarks, however, Marine Products is not dependent upon any single trademark or trade name or group of trademarks or trade names. The Chaparral, Robalo and Wahoo! trademarks are currently registered in the United States. The current duration for such registration ranges from seven to 15 years but each registration may be renewed an unlimited number of times.

Several of Chaparral’s and Robalo’s designs are protected under the U.S. Copyright Office’s Vessel Hull Design Protection Act. This law grants an owner of an original vessel hull design certain exclusive rights. Protection is offered for hull designs that are made available to the public for purchase provided that the application is made within two years of the hull design being made public. As of December 31, 2010, there were 22 Chaparral hull designs and four Robalo hull designs registered under the Vessel Hull Design Protection Act.

During 2008 Chaparral was granted a design patent on its Wide TechTM hull design by the U.S. Patent and Trademark Office. The patent has a term of 14 years and protects the Wide TechTM hull currently used on the Sunesta Wide TechTM and Xtreme, 400 Premiere, SSi Wide TechTM and two of its Signature Cruisers from being used by other pleasure boat manufacturers. Marine Products believes that this patent is important to its business.

Seasonality

Marine Products’ quarterly operating results are affected by weather and general economic conditions. Quarterly operating results for the second quarter have historically recorded the highest sales volume for the year because this corresponds with the highest retail sales volume period. The results for any quarter are not necessarily indicative of results to be expected in any future period.

Inflation

The market prices of certain material and component costs used in manufacturing the Company’s products, especially resins that are made with hydrocarbon feedstocks, copper and stainless steel, have been extremely volatile since the third and fourth quarters of 2008. The prices of these commodities fell dramatically due to the global recession and financial crisis in late 2008. During 2009, these commodity prices began to rise, and continued to rise throughout 2010. By the end of 2010, the prices of some of these commodities, such as copper, were higher than the peak market prices reached during 2008. These increased commodity prices are likely to lead to higher materials costs in 2011. Since retail demand for pleasure boats remains weak in 2011, we cannot be confident that the Company will be able to institute sufficient price increases to its dealers to compensate for these increased materials costs. It is likely that these increased commodity prices will negatively impact the Company’s operating results in 2011 compared to 2010.

New boat buyers typically finance their purchases. Higher inflation typically results in higher interest rates that could translate into an increased cost of boat ownership. Prospective buyers may choose to forego or delay their purchases or buy a less expensive boat in the event that interest rates rise or credit is not available to finance boat purchase.

Availability of Filings

Marine Products makes available free of charge on its website, www.marineproductscorp.com, the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports on the same day as they are filed with the Securities and Exchange Commission.

Item 1A. Risk Factors

Economic Conditions, Availability of Credit and Consumer Confidence Levels Affect Marine Products’ Sales Because Marine Products’ Products are Purchased with Discretionary Income

11

During an economic recession or when an economic recession is perceived as a threat, Marine Products will be adversely affected as consumers have less discretionary income or are more apt to save their discretionary income rather than spend it. During times of global political or economic uncertainty, Marine Products will be negatively affected to the extent consumers forego or delay large discretionary purchases pending the resolution of those uncertainties. The recent financial crisis and deep, enduring recession may have long-term effects on consumer behavior with regard to pleasure boating as well. Volatility in financial markets may force consumers to delay retirement, or to choose more modest lifestyles when they do retire. In such a case, consumers may not purchase boats, may purchase boats later in their lives, or may purchase smaller or less expensive boats. Tight lending and credit standards, such as those currently in use by lenders in the United States, can make loans for boats harder to secure, and such loans may carry unfavorable terms, which may force consumers to forego boat purchases. These factors have also resulted in the past, and may continue to result in the future, in a reduction in the quality and number of dealers upon which Marine Products relies to sell its products.

Marine Products Relies upon Third-Party Dealer Floor Plan Lenders Which Provide Financing to its Network of Independent Dealers

Marine Products sells its products to a network of independent dealers, most of whom rely on one or more third-party dealer floor plan lenders to provide financing for their inventory prior to its sale to retail customers. In general, this source of financing is vital to Marine Products’ ability to sell products to its dealer network. The credit crisis and financial market volatility that occurred in late 2008 and extended into 2009 caused disruptions among dealer floor plan lenders. While dealer floor plan credit is currently available for many of our dealers during the 2011 model year, it is less available and more costly than in prior years. Such factors may have reduced the availability of floor plan loans to our dealers, increased the cost of financing, and may change the limits under which Marine Products or its subsidiaries are required to repurchase inventory in the event of a dealer default. Any of these factors negatively impact Marine Products’ sales and profitability.

Interest Rates and Fuel Prices Affect Marine Products’ Sales

The Company’s products are often financed by our dealers and the retail boat consumers. Higher interest rates increase the borrowing costs and, accordingly, the cost of doing business for dealers and the cost of boat purchases for consumers. Fuel costs can represent a large portion of the costs to operate our products. Therefore, higher interest rates and fuel costs can adversely affect consumers’ decisions relating to recreational boating purchases.

Marine Products’ Dependence on its Network of Independent Boat Dealers may Affect its Operating Results and Sales

Virtually all of Marine Products’ sales are derived from its network of independent boat dealers. Marine Products has no long-term agreements with these dealers. Competition for dealers among recreational powerboat manufacturers continues to increase based on the quality of available products, the price and value of the products, and attention to customer service. The Company faces intense competition from other recreational powerboat manufacturers in attracting and retaining independent boat dealers. The number of independent boat dealers supporting the Chaparral and Robalo trade names and the quality of their marketing and servicing efforts are essential to Marine Products’ ability to generate sales. A deterioration in the number or quality of Marine Products’ network of independent boat dealers which occurred during the current challenging selling environment, has had and could continue to have a material adverse effect on its boat sales. Marine Products’ inability to attract new dealers and retain those dealers, or its inability to increase sales with existing dealers, could substantially impair its ability to execute its business plans.

Although Marine Products’ management believes that the quality of its products and services in the recreational boating market should permit it to maintain its relationship with its dealers and its market position, there can be no assurance that Marine Products will be able to sustain its current sales levels. In addition, independent dealers in the recreational boating industry have experienced significant consolidation in recent years, which could result in the loss of one or more of Marine Products’ dealers in the future if the surviving entity in any such consolidation purchases similar products from a Marine Products competitor. During the 2009 depressed selling environment, some boat dealers included within the Marine Products’ dealer network ceased operations and this trend may continue given the continued challenging business environment in which boat dealers operate. See “Business Strategies” above.

Marine Products’ Financial Condition and Operating Results may be Adversely Affected by Boat Dealer Defaults

The Company’s products are sold through dealers and the financial health of these dealers is critical to the Company’s continued success. The Company’s results can be negatively affected if a dealer defaults because Marine Products or its subsidiaries may be contractually required to repurchase inventory up to certain limits, although for business reasons, the Company may decide to purchase additional boats in excess of this contractual obligation.

Marine Products’ Ability to Adjust its Business Operations to Compensate for Reduced Sales of Boats may be Restricted in the Future

In 2008 Marine Products idled certain production facilities and reduced its number of employees to offset the impact that reduced net sales had on the Company’s operating results and cash flows. As a result the Company experienced lower rates of absorption of its fixed costs. The Company results have significantly improved with operating and net income in 2010 compared to operating and net losses reported in 2009. Although the Company’s sales have significantly improved, this prolonged downturn in the Company’s sale of boats may continue to have an adverse affect in 2011 and in future periods beyond 2011. In addition, the Company’s ability to reduce its fixed costs in the future to respond to potential future reduced net sales is limited.

12

Marine Products’ Sales are Affected by Weather Conditions

Marine Products’ business is subject to weather patterns that may adversely affect its sales. For example, drought conditions, or merely reduced rainfall levels, or excessive rain, may close area boating locations or render boating dangerous or inconvenient, thereby curtailing customer demand for our products. In addition, unseasonably cool weather and prolonged winter conditions may lead to a shorter selling season in some locations. Hurricanes and other storms could cause disruptions of our operations or damage to our boat inventories and manufacturing facilities.

Marine Products Encounters Intense Competition Which Affects our Sales and Profits

The recreational boat industry is highly fragmented, resulting in intense competition for customers, dealers and boat show exhibition space. This competition affects both the markets which we currently serve and new markets that we may enter in the future. We compete with several large national or regional manufacturers that have substantial financial, marketing and other resources. Competitive manufacturers have executed a strategy of constructing entry-level smaller boats which are constructed in off-shore manufacturing plants with lower labor costs. These competitive conditions have contributed to our inability to pass along our increased manufacturing costs to customers, reduced our market share in various selling categories including particularly smaller boats, and negatively impacted our profit margins.

Marine Products has Potential Liability for Personal Injury and Property Damage Claims

The products we sell or service may expose Marine Products to potential liabilities for personal injury or property damage claims relating to the use of those products. Historically, the resolution of product liability claims has not materially affected Marine Products’ business. Marine Products maintains product liability insurance that it believes to be adequate. However, there can be no assurance that Marine Products will not experience legal claims in excess of its insurance coverage or that claims will be covered by insurance. Furthermore, any significant claims against Marine Products could result in negative publicity, which could cause Marine Products’ sales to decline.

Because Marine Products Relies on Third-party Suppliers, Marine Products may be Unable to Obtain Adequate Raw Materials and Components

Marine Products is dependent on third-party suppliers to provide raw materials and components essential to the construction of its various powerboats. Especially critical are the availability and cost of marine engines and commodity raw materials used in the manufacture of Marine Products’ boats. While Marine Products’ management believes that supplier relationships currently in place are sufficient to provide the materials necessary to meet present production demands, there can be no assurance that these relationships will continue, that these suppliers will remain in operation given the extended business downturn in the recreational boating industry or that the quantity or quality of materials available from these suppliers will be sufficient to meet Marine Products’ future needs. Disruptions in current supplier relationships or the inability of Marine Products to continue to purchase construction materials in sufficient quantities and of sufficient quality at acceptable prices to meet ongoing production schedules could cause a decrease in sales or a sharp increase in the cost of goods sold. Additionally, because of this dependence, the volatility in commodity raw materials or current or future price increases in construction materials or the inability of Marine Products’ management to purchase materials required to complete its growth and acquisition strategies could cause a reduction in Marine Products’ profit margins or reduce the number of boats Marine Products may be able to produce for sale.

Marine Products may be Unable to Identify, Complete or Successfully Integrate Acquisitions

Marine Products intends to pursue acquisitions and form strategic alliances that will enable Marine Products to acquire complementary skills and capabilities, offer new products, expand its customer base, and obtain other competitive advantages. There can be no assurance, however, that Marine Products will be able to successfully identify suitable acquisition candidates or strategic partners, obtain financing on satisfactory terms, complete acquisitions or strategic alliances, integrate acquired operations into its existing operations, or expand into new markets. Once integrated, acquired operations may not achieve anticipated levels of sales or profitability, or otherwise perform as expected. Acquisitions also involve special risks, including risks associated with unanticipated problems, liabilities and contingencies, diversion of management resources, and possible adverse effects on earnings and earnings per share resulting from increased interest costs, the issuance of additional securities, and difficulties related to the integration of the acquired business. The failure to integrate acquisitions successfully may divert management’s attention from Marine Products’ existing operations and may damage Marine Products’ relationships with its key customers and suppliers.

Marine Products’ Success will Depend on its key Personnel, and the Loss of any key Personnel may Affect its Powerboat Sales

Marine Products’ success will depend to a significant extent on the continued service of key management personnel. The loss or interruption of the services of any senior management personnel or the inability to attract and retain other qualified management, sales, marketing and technical employees could disrupt Marine Products’ operations and cause a decrease in its sales and profit margins.

Marine Products’ Ability to Attract and Retain Qualified Employees is Crucial to its Results of Operations and Future Growth

13

Marine Products relies on the existence of an available hourly workforce to manufacture its products. As with many businesses, we are challenged at times to find qualified employees. There are no assurances that Marine Products will be able to attract and retain qualified employees to meet current and/or future growth needs.

If Marine Products is Unable to Comply with Environmental and Other Regulatory Requirements, its Business may be Exposed to Liability and Fines

Marine Products’ operations are subject to extensive regulation, supervision and licensing under various federal, state and local statutes, ordinances and regulations. While Marine Products believes that it maintains all requisite licenses and permits and is in compliance with all applicable federal, state and local regulations, there can be no assurance that Marine Products will be able to continue to maintain all requisite licenses and permits and comply with applicable laws and regulations. The failure to satisfy these and other regulatory requirements could cause Marine Products to incur fines or penalties or could increase the cost of operations. The adoption of additional laws, rules and regulations could also increase Marine Products’ costs.

The U.S. Environmental Protection Agency (EPA) adopted regulations affecting many marine propulsion engines manufactured for the 2010 model year and later. This regulation will increase the cost of boats subject to the regulation, which may either reduce the Company’s profitability or reduce sales.

As with boat construction in general, our manufacturing processes involve the use, handling, storage and contracting for recycling or disposal of hazardous or toxic substances or wastes. Accordingly, we are subject to regulations regarding these substances, and the misuse or mishandling of such substances could expose Marine Products to liability or fines.

Additionally, certain states have required or are considering requiring a license in order to operate a recreational boat. While such licensing requirements are not expected to be unduly restrictive, regulations may discourage potential first-time buyers, thereby reducing future sales.

Marine Products’ Stock Price has been Volatile

Historically, the market price of common stock of companies engaged in the discretionary consumer products industry has been highly volatile. Likewise, the market price of our common stock has varied significantly in the past. In addition, the availability of Marine Products common stock to the investing public is limited to the extent that shares are not sold by the executive officers, directors and their affiliates, which could negatively impact the trading price of Marine Products’ common stock, increase volatility and affect the ability of minority stockholders to sell their shares. Future sales by executive officers, directors and their affiliates of all or a substantial portion of their shares could also negatively affect the trading price of Marine Products’ common stock.

Marine Products’ Management has a Substantial Ownership Interest; Public Stockholders may have no Effective Voice in Marine Products’ Management

The Company has elected the “Controlled Corporation” exemption under Rule 303A of the New York Stock Exchange (“NYSE”) Company Guide. The Company is a “Controlled Corporation” because a group that includes the Company’s Chairman of the Board, R. Randall Rollins and his brother, Gary W. Rollins, who is also a director of the Company, and certain companies under their control, controls in excess of fifty percent of the Company’s voting power. As a “Controlled Corporation,” the Company need not comply with certain NYSE rules including those requiring a majority of independent directors.

Marine Products’ executive officers, directors and their affiliates hold directly or through indirect beneficial ownership, in the aggregate, approximately 73 percent of Marine Products’ outstanding shares of common stock. As a result, these stockholders effectively control the operations of Marine Products, including the election of directors and approval of significant corporate transactions such as acquisitions. This concentration of ownership could also have the effect of delaying or preventing a third-party from acquiring control of Marine Products at a premium.

Provisions in Marine Products’ Certificate of Incorporation and Bylaws may Inhibit a Takeover of Marine Products

Marine Products’ certificate of incorporation, bylaws and other documents contain provisions including advance notice requirements for stockholder proposals and staggered terms of office for the Board of Directors. These provisions may make a tender offer, change in control or takeover attempt that is opposed by Marine Products’ Board of Directors more difficult or expensive.

The Market Prices of Marine Products’ Marketable Securities may Become Volatile due to the Downgrading of Insurance Companies Which Insure Some of These Marketable Securities as well as the Overall Financial Difficulties of Some of the Issuers of These Marketable Securities

14

Marine Products maintains a diversified portfolio of short-duration, investment-grade municipal debt securities managed by a large, well-capitalized financial institution. Approximately 24 percent of this portfolio is insured by three large insurance companies. Due to the problems confronting the financial system over the past few years, these insurance companies have become much less active in issuing credit insurance for municipal debt securities, either because they have exited the business or merged with other insurance companies. Our investment manager selects securities based on underlying credit quality rather than relying on credit insurance, and our securities are short in duration, so we do not believe that this disruption among insurers of municipal securities increases the risk of default among these securities. In addition, many municipal governments are currently struggling with lower tax revenues and budgets. While our investment manager does not believe that there is any risk of default in our portfolio of marketable securities, these two factors may increase the volatility of the market prices of these marketable securities. The market prices of these securities may continue to be volatile during periods of uncertainty in the bond insurance industry and difficult economic conditions among municipalities.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Marine Products’ corporate offices are located in Atlanta, Georgia. These offices are currently shared with RPC and are leased. The monthly rent paid is allocated between Marine Products and RPC. Under this arrangement, Marine Products pays approximately $2,000 per month in rent. Marine Products may cancel this arrangement at any time after giving a 30 day notice.

Chaparral owns and maintains approximately 1,011,000 square feet of space utilized for manufacturing, research and development, warehouse, and sales office and operations in Nashville, Georgia. In addition, the Company leases 83,000 square feet of manufacturing space at the Robalo facility in Valdosta, Georgia, under a long-term arrangement expiring in 2014. During the fourth quarter of 2008, the Robalo facility was temporarily idled and production of these boats was moved to the Nashville facility. There are no plans or current intentions to dispose of the facilities in Valdosta, Georgia. The Company also leases 111,000 square feet of warehouse space in Nashville, Georgia under a long-term arrangement expiring in 2018. Marine Products’ total square footage under roof is allocated as follows: manufacturing — 712,000, research and development — 67,100, warehousing — 294,500, office and other — 131,400.

Item 3. Legal Proceedings

Marine Products is involved in litigation from time to time in the ordinary course of its business. Marine Products does not believe that the ultimate outcome of such litigation will have a material adverse effect on its liquidity, financial condition or results of operations.

Item 4. Reserved

15

Item 4A. Executive Officers of the Registrant

Each of the executive officers of Marine Products was elected by the Board of Directors to serve until the Board of Directors’ meeting immediately following the next annual meeting of stockholders or until his or her earlier removal by the Board of Directors or his or her resignation. The following table lists the executive officers of Marine Products and their ages, offices, and date first elected to office.

|

Name and Office with Registrant

|

Age

|

Date First Elected

to Present Office

|

||

|

R. Randall Rollins (1)

|

79

|

2/28/01

|

||

|

Chairman of the Board

|

||||

|

Richard A. Hubbell (2)

|

66

|

2/28/01

|

||

|

President and Chief Executive Officer

|

||||

|

James A. Lane, Jr. (3)

|

68

|

2/28/01

|

||

|

Executive Vice President and President of Chaparral Boats, Inc.

|

||||

|

Linda H. Graham (4)

|

74

|

2/28/01

|

||

|

Vice President and Secretary

|

||||

|

Ben M. Palmer (5)

|

50

|

2/28/01

|

||

|

Vice President, Chief Financial Officer and Treasurer

|

|

(1)

|

R. Randall Rollins began working for Rollins, Inc. (consumer services) in 1949. At the time of the spin-off of RPC from Rollins, Inc. in 1984, Mr. Rollins was elected Chairman of the Board and Chief Executive Officer of RPC. He remains Chairman of RPC and stepped down from the position of Chief Executive Officer effective in 2003. He has served as Chairman of the Board of Marine Products since 2001 and Chairman of the Board of Rollins, Inc. since 1991. He is also a director of Dover Downs Gaming and Entertainment, Inc. and Dover Motorsports, Inc.

|

|

(2)

|

Richard A. Hubbell has been the President and Chief Executive Officer of Marine Products since it was spun off in 2001. He has also been President of RPC since 1987 and its Chief Executive Officer since 2003. Mr. Hubbell serves on the Board of Directors for both of these companies.

|

|

(3)

|

James A. Lane, Jr. has held the position of President of Chaparral Boats (formerly a subsidiary of RPC) since 1976. Mr. Lane has been Executive Vice President and Director of Marine Products since it was spun off in 2001. He is also a director of RPC and has served in that capacity since 1987.

|

|

(4)

|

Linda H. Graham has been Vice President and Secretary of Marine Products since it was spun off in 2001, and Vice President and Secretary of RPC since 1987. Ms. Graham serves on the Board of Directors for both of these companies.

|

|

(5)

|

Ben M. Palmer has been Vice President, Chief Financial Officer and Treasurer of Marine Products since it was spun off in 2001 and has served the same roles at RPC since 1996.

|

16

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

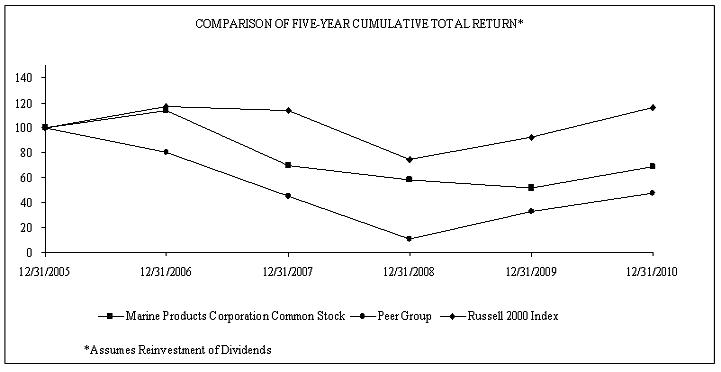

Marine Products’ common stock is listed for trading on the New York Stock Exchange under the symbol “MPX.” As of February 18, 2011, there were 37,324,801 shares of common stock outstanding.

At the close of business on February 18, 2011, there were approximately 2,425 beneficial holders of record of the Company’s common stock. The high and low prices of Marine Products’ common stock and dividends paid for each quarter in the years ended December 31, 2010 and 2009 were as follows:

|

2010

|

2009