Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

or

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 333-153362

GIGOPTIX, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 26-2439072 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

2300 Geng Road, Suite 250

Palo Alto, CA 94303

Registrant’s telephone number: (650-424-1937)

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act:

Common Stock, $0.001 par value per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicated by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting Company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate value of the registrant’s common stock, held by non-affiliates as of July 2, 2010, the last business day of the registrant’s most recently completed second fiscal quarter was approximately $11.8 million.

The number of shares of Common Stock outstanding as of February 25, 2011, the most recent practicable date prior to the filing of this Annual Report on Form 10-K, was 12,288,216 shares.

Table of Contents

GIGOPTIX, INC.

ANNUAL REPORT ON FORM 10-K

FOR FISCAL YEAR ENDED DECEMBER 31, 2010

| PAGE NO | ||||||

| ii | ||||||

| 1 | ||||||

| ITEM 1 |

1 | |||||

| ITEM 1A |

17 | |||||

| ITEM 2 |

33 | |||||

| ITEM 3 |

34 | |||||

| ITEM 4 |

34 | |||||

| 35 | ||||||

| ITEM 5 |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 35 | ||||

| ITEM 7 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 37 | ||||

| ITEM 8 |

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 51 | ||||

| ITEM 9 |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 91 | ||||

| ITEM 9A |

CONTROLS AND PROCEDURES | 91 | ||||

| ITEM 9B |

OTHER INFORMATION | 93 | ||||

| 94 | ||||||

| ITEM 10 |

DIRECTORS, EXECUTIVE OFFICERS, AND CORPORATE GOVERNANCE | 94 | ||||

| ITEM 11 |

EXECUTIVE COMPENSATION | 97 | ||||

| ITEM 12 |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 104 | ||||

| ITEM 13 |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 105 | ||||

| ITEM 14 |

PRINCIPAL ACCOUNTING FEES AND SERVICES | 105 | ||||

| 107 | ||||||

| ITEM 15 |

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 107 | ||||

| 108 | ||||||

References in this Annual Report on Form 10-K to “we,” “us,” “our,” “the Company,” “GigOptix,” and “GGOX” mean GigOptix, Inc. and all entities owned or controlled by GigOptix, Inc.

All brand names, trademarks and trade names referred to in this report are the property of their respective holders.

i

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the documents incorporated herein by reference include “forward-looking statements” within the meaning and protections of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, assumptions, estimates, intentions, and future performance, and involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements.

All statements other than statements of historical fact are statements that could be forward-looking statements. You can identify these forward-looking statements through our use of words such as “may,” “will,” “anticipate,” “assume,” “should,” “indicate,” “would,” “believe,” “contemplate,” “expect,” “estimate,” “continue,” “plan,” “project,” “could,” “intend,” “target” and other similar words and expressions of the future. These forward-looking statements may not be realized due to a variety of factors, including, without limitation:

| • | we are an early stage company and have a history of incurring losses; |

| • | our ability to remain competitive in the markets we serve; |

| • | the effects of future economic, business and market conditions; |

| • | consolidation in the industry we serve; |

| • | our ability to obtain additional funding; |

| • | our ability to continue to develop, manufacture and market innovative products and services that meet customer requirements for performance and reliability; |

| • | our ability to establish effective internal controls over our financial reporting; |

| • | risks relating to the transaction of business internationally; |

| • | our failure to realize anticipated benefits from acquisitions or the possibility that such acquisitions could adversely affect us, and risks relating to the prospects for future acquisitions; |

| • | the loss of key employees and the ability to retain and attract key personnel, including technical and managerial personnel; |

| • | quarterly and annual fluctuations in results of operations; |

| • | investments in research and development; |

| • | protection and enforcement or our intellectual property rights and proprietary technologies; |

| • | costs associated with potential intellectual property infringement claims asserted by a third party; |

| • | our exposure to product liability claims resulting from the use of our products; |

| • | the loss of one or more of our significant customers, or the diminished demand for our products; |

| • | our dependence on contract manufacturing and outsourced supply chain, as well as the costs of materials; |

| • | our reliance on third parties to provide services for the operation of our business; |

| • | the effects of war, terrorism, natural disasters or other catastrophic events; |

| • | our success at managing the risks involved in the foregoing items; and |

| • | other risks and uncertainties, including those listed under the heading “Risk Factors” herein. |

ii

Table of Contents

The forward-looking statements are based upon management’s beliefs and assumptions and are made as of the date of this Annual Report on Form 10-K. We undertake no obligation to publicly update or revise any forward-looking statements included or incorporated by reference in this Annual Report on Form 10-K or to update the reasons why actual results could differ from those contained in such statements, whether as a result of new information, future events or otherwise, except to the extent required by federal securities laws. These forward looking statements are found at various places throughout this Annual Report on Form 10-K. Any investor should consider all risks and uncertainties disclosed in our filings with the Securities and Exchange Commission, or the SEC, described below under the heading “Where You Can Find More Information,” all of which is accessible on the SEC’s website at www.sec.gov.

iii

Table of Contents

| ITEM 1. | BUSINESS |

Overview

We are a leading supplier of electronic and electro-optical semiconductor products that enable high-speed telecommunications and data-communications networks globally. Our products convert signals between electrical and optical formats for transmitting and receiving data over fiber optic networks, a critical function in optical communications equipment. We are an emerging leader and innovator in both telecommunications and data-communications applications for fast growing markets in 10Gbps, 40Gbps and 100Gbps drivers, receiver ICs, electro–optic modulator components and multi-chip-modules (MCM). Our expertise in semiconductor electro-optical and optical technologies has helped us create a broad portfolio of products that addresses customer demand for performance at higher speeds, over wider temperature ranges, in smaller sizes, and at lower power consumption compared to other products currently available in the market. We view ourselves as a strategic vendor to a number of our customers given our early engagement in their product design plans and have well-established relationships with many of the leading telecommunications and data-communications network systems vendors such as Alcatel-Lucent, Cisco, Finisar, Fujitsu, JDSU, Mitsubishi, Multiplex, Opnext, Source Photonics, ZTE, and other “Tier-One” equipment vendors in the United States, Europe and Asia, as well as leading industrial, aerospace and defense customers such as Adtran, Anritsu, Avocent, Boeing, Hamilton Sundstrand, John Deere, LeCroy, National Instruments, Northrop Grumman, Raytheon, Rockwell-Collins, Rohde & Schwartz, and Teradyne.

Telecommunications and data-communications networks are becoming increasingly congested due to the growing demand for high bandwidth applications by consumers and enterprises. This bandwidth constraint has caused network service providers to turn to equipment vendors like us to provide solutions that maximize bandwidth and reliability while minimizing cost. Increasing the communications data rate in networks has been an important element of easing network congestion, and, as a result, network service providers are in process of upgrading their 10Gbps systems to 40Gbps and 100Gbps equipment deployments throughout their networks. We focus on the 10Gbps and above markets which we believe present the fastest growing and primary market opportunity in the communications industry. Based on data from Ovum’s and LightCounting’s market research, we expect sales of electronic and electro-optic components operating at 10Gbps and above in telecommunications and data communications segments to increase from approximately $200 million in 2010 to approximately $800 million in 2015, a compound annual growth rate (CAGR) of approximately 30%.

Since inception, we have expanded our customer base, acquired and integrated four businesses with complementary products and customers, and in so doing expanded our product line from a few 10Gbps ultra-long reach electronic modulator drivers to a line of over 100 products that includes drivers, receivers and modulators for 10 to 100Gbps applications and custom application specific integrated circuits (ASICs). Our direct sales force is based in 5 countries and is supported by more than 50 channel representatives and distributors that are selling our products throughout North America, Europe, Japan and Asia. In 2010, we shipped over 90 products to over 100 customers.

On February 4, 2011, we entered into a merger agreement with Endwave Corporation pursuant to which a wholly-owned subsidiary of ours will, subject to the satisfaction or waiver of the conditions therein, merge with and into Endwave, the result of which the separate corporate existence of the wholly-owned subsidiary shall cease and Endwave will be the successor or surviving corporation of the merger and our wholly-owned subsidiary. Under the terms of the merger agreement, all outstanding shares of Endwave common stock, including those issuable upon settlement of outstanding restricted stock units, and outstanding in-the-money Endwave stock options, will be converted into shares of our common stock such that immediately after the merger, such shares represent approximately 42.5% of all outstanding our common stock. Based on the number of shares of Endwave and GigOptix common stock outstanding as of January 31, 2011, approximately 9.1 million shares of GigOptix common stock will be issued to holders of Endwave common stock, registered

1

Table of Contents

stock units and stock options. On February 3, 2011, our board of directors approved the establishment of a $500,000 retention bonus pool to be payable to our employees who are still so employed 15 days after the closing of the merger. Our board of directors has delegated to the Compensation Committee to approve the amounts that each officer and employee of ours is eligible to receive as part of such retention bonus pool, and such determination, including who will be an eligible participant in such retention bonus pool, has not yet been made, although it is anticipated that the named executive officers will be eligible participants. As of February 25, 2011, we have incurred accounting and banking fees of approximately $290,000 related to the Endwave transaction.

Industry Background

Over the past several years, communications networks have undergone significant challenges as network operators pursue more profitable service offerings while reducing operating costs. The growing demand for bandwidth due to the explosion of data and video across networks by enterprises and consumers has driven service providers to continuously add high speed access such as Wi-Fi, WiMax, 3G, DSL, cable and FTTx, as well as converging their separate voice and data networks into a single IP-based high capacity integrated network to easily manage and provision these services. Other high bandwidth applications such as e-mail, music, video downloads and streaming, on-line social networks, on-line gaming, and VOD or IPTV are also challenging network service providers to supply increasing bandwidth to their customers and results in increased network utilization across the entire core and edge of wireline, wireless and cable networks. Additionally, enterprises and institutions are managing their rapidly escalating demand for data and bandwidth and are upgrading and deploying high speed local, storage and wide area networks (LANs, SANs and WANs, respectively). U.S. Defense and Homeland Security efforts also add to the demand for bandwidth, as vast amounts of data are generated though sophisticated surveillance and defense network applications. The U.S. government and its contractors are incorporating optical technologies into its systems and infrastructure to address these challenges.

Optical networking technologies support higher speeds, added features and offer greater interoperability to accommodate higher bandwidth requirements at a lowest cost. Leading network systems vendors such as Alcatel-Lucent and Cisco are producing optical systems for carriers increasingly based on 10Gbps and 40Gbps speeds including multi-service switches, DWDM transport terminals, access multiplexers, routers, Ethernet switches and other networking systems. Mirroring the convergence of telecommunications and data-communications networks, these systems vendors are increasingly addressing both telecommunications and data-communications applications and are also looking to converge their network equipment offerings to a single product. Faced with technological and cost challenges of building fully integrated systems that can handle voice, data and video, OEMs are re-focusing on core competencies of software and systems integration, and relying on outside module and component suppliers for the design, development and supply of critical electro–optic products that perform the critical transmit and receive functions.

Challenges Faced by Network Equipment Providers

The performance requirements of communications applications and the technical challenges associated with the data-communications and telecommunications markets present difficult obstacles to service providers and equipment designers that serve those markets. The core challenges of processing and transmitting high quality broadband streams include:

| • | Performance: Optical components and systems have to be well integrated and inter–operate with the other components that perform the transmit and receive functions while running at low temperatures in a wide variety of operating environments. |

| • | Power consumption: The increase in optical transmission speeds inherently leads to higher power consumption by the electronic components being used. This in turn leads to thermal management challenges due to the high port densities being demanded by customers. For instance in data centers, there is a significant investment required to cool the facility, for every $1 invested in computer/network infrastructure there is typically another $1 investment required to cool the facility. |

2

Table of Contents

| • | Size: Customers need to maximize the utilization of their central office space and rack size and therefore demand small solution footprints to maximize port density. The industry has responded by migrating from line-cards to 300pin transponders to pluggable transceivers with more than a 60x reduction in size for 10Gbps communication components since 1999. This is turn puts severe size constraints on electronic and optical component suppliers to maintain the pace of size reduction roadmaps. |

| • | Cost: There are significant price pressures within the optical communications markets to reduce component and system costs. End users continually demand more bandwidth and features while the operators generally do not keep pace with the bandwidth usage increases. Moreover, the average sales price (ASP) increase per new generation component does not scale proportionally with the speed increase. For example, a 4x increase in speed can only generate only a 2.5x increase in ASP to the vendor. |

| • | Complexity: The increasing technological complexity of optical systems and components, the need to increase the pace of innovation while also reducing costs have led customers to reduce their number of module and component suppliers and rely on vendors that have more comprehensive product portfolios, deeper product expertise and the ability to support future roadmaps. |

| • | Manufacturing: The optical industry still predominantly utilizes discrete components to implement their systems. Many of these components are manufactured by different vendors and these discrete solutions lead to manufacturing inefficiencies and yield reductions. Integration has been a key enabler in the historical success of the silicon IC technology, enabling the improvement of system performance, reducing system size and cost by increasing the functionality that can be implemented on one device and thereby decreasing the components count required to implement a system. |

Our Solutions

We offer a comprehensive 10Gbps and 40Gbps transceiver product portfolio and are an emerging leader in the developing market for 100Gbps products. We combine high performance analog and mixed signal design skills, with experience in integrated systems, interoperability, power management and size optimization. We believe customers choose to work with us for several reasons including:

Superior Performance: Our performance advantage is derived from industry leading drivers, receivers, modulators and superior integration and module design capabilities. Our core III-V and silicon semiconductor, as well as thin film polymer on silicon (TFPSTM) technology knowledge allows us to design products that exceed the current performance, power, size, temperature and reliability requirements of our customers. We recently introduced a 100 Gbps quad-driver built from indium phosphide that is the market’s first100Gbps driver. Our single, 4 and 12 channel VCSEL drivers and receivers have ultra-low-power consumption and use less than 10mW to stream 1Gbps. We have also developed 10Gbps drivers and receivers for outdoor, non-temperature controlled environments that enable higher capacity in our customers’ next generation data center systems.

Broad Product Line: We have a comprehensive portfolio of products for telecommunications, data-communications, defense and industrial applications designed for speeds of 10Gbps and beyond. Our products support a wide range of data rates, protocols, transmission distances and industry standards. This wide product offering allows us to serve as a “one-stop shop” to our customers in offering them a comprehensive product arsenal, as well as allowing us to be more cost-effective as we re-utilize pre-existing design building-blocks. Our portfolio consists of the following product ranges:

| • | laser and modulator drivers for 10Gbps, 40Gbps and 100Gbps applications |

| • | receiver amplifiers or Trans-impedance Amplifiers (TIAs) for 10Gbps, 40Gbps and 100Gbps applications |

| • | driver & receiver chipsets for 4 and 12 channel parallel optics applications from 3Gbps to 10Gbps |

3

Table of Contents

| • | electro-optic modulators based on proprietary TFPS suitable for various 40Gbps and 100Gbps modulation schemes, such as DPSK, DQPSK and DP-QPSK |

| • | ultra–broadband amplifiers with flat gain response |

| • | Standard Cell, and Structured ASIC and Hybrid ASIC designs and manufacturing service for multiple markets offering ITAR compliance for defense applications |

Power Consumption: Our designs and enabling technologies utilize efficient circuit techniques and material technology to reduce energy usage. For example, we have demonstrated a 10Gbps short-reach optical link that consumes less than 100mW across 100 meter of fiber, representing a 75% reduction over the previous generation of products.

Size Reduction: Our designs have very small footprints. Our recently announced LX8401 40Gbps DPSK TFPS modulator is nearly half the size of competing products enabling an overall smaller transponder design. Similarly, comparable solutions competing with our GX6261 40G DQPSK driver require 40% more board space. Moreover, our GX62455 100Gbps driver integrates four 32Gbps drivers into a single package thereby reducing the total system size while also improving electrical performance.

Cost Reduction: We are skilled in designing and utilizing a number of semiconductor process technologies such as indium phosphide, gallium arsenide, silicon germanium and silicon CMOS. This portfolio of technology solutions provides the flexibility to optimize the cost/performance of our products to the challenge at hand. For instance, our new portfolio of 10Gbps, 40Gbps, and 100Gbps, TIAs were designed using silicon germanium and this enables much cheaper production costs compared with competing TIA solutions using indium phosphide. This coupled with the ability to integrate more complex logic functions into the TIA designs offer compelling value to our customers. We provide a broad portfolio of solutions that customers are now beginning to leverage to extract further volume discounts by consolidating their purchasing power on one vendor.

Integration: Our vision is to leverage our broad portfolio of products to integrate optical modulators monolithically onto our semiconductor chips. The close coupling of optical and electronic components will realize the maximum performance at high speeds while ensuring the smallest size, potentially lower costs, and improved interoperability performance. Our step-wise approach to this goal is aligned to deliver continuously more integrated products along the innovation path starting with bundling in the system level going to package level on to chip level. For instance, we are currently funded by the Air Force Research Labs to develop an integrated modulator-driver capable of 200Gbps optical transmission which is seen as critical to enable lightweight, ultra-high bandwidth optical transceivers to on the road to supporting terra-scale data processing. Integrating optical modulators monolithically onto semiconductor chips coupled with innovative driver design topologies can enable implementation of a monolithic optical modulator/driver component.

Partnership: Through a deep understanding both of the system level challenges faced by our customers developing optical transponders and transceivers and of the capabilities and limitations of our technology, we are able to suggest and implement new system partitioning concepts to ease manufacturing, increase yields and reduce power and cost. For example through the addition of certain design recommendations, we are able to guide our customers to simplify system manufacturing using our novel designs.

Technology Leadership: Our products are built on a strong foundation of semiconductor and electro-optic polymer technologies supported by over 20 years of innovation and research and development experience that has resulted in more than 100 patents awarded and patent applications pending worldwide. Our technology innovation extends from the design of ultra-high speed semiconductor integrated circuits, monolithic microwave integrated circuit design, multi-chip modules, electro-optic thin-film polymer materials, and optical modulator design. These areas of competence include signal integrity, thermal models, power consumption, integration of multiple ICs into sub-system multi-chip module components, and molecular science of electro-optic polymers. Our many years of experience allow us to design solutions that few companies can offer. For this reason we were

4

Table of Contents

selected as a partner to a Tier 1 equipment supplier to develop 100Gbps modulator drivers for the first commercially available 100Gbps systems that was launched in 2010. Additionally, our ASIC portfolio and team has the competency in low cost silicon CMOS design and high volume manufacturing. This will be an important asset in the future transition of optics to consumer applications that call for low cost, high volume designs. We conduct our research both independently, through contractual relationships with U.S. government agencies and in cooperation with customers. We are committed to conduct fundamental research into the integration of electronic and electro-optic (EO) components using semiconductor and EO polymers as a source of differentiation.

Horizontal Business Model: We deploy a horizontal business model as opposed to a vertical integration model since it is our mission to serve the broad customer base in the optical communications and defense markets with best in class components. This will be driven by the system vendor end customers’ desire for continuous price reduction as volumes increase and will be enabled by the growth of capable component suppliers such as GigOptix as well as the availability of high quality electronics contract manufacturers (ECMs). We cultivate the “Virtual Vertical” model, which is based on strong relationships with ECMs and other component vendors in the supply chain with aligned objectives.

Growth Strategy

Our objective is to be the leading provider of high performance electronic and electro-optic components for the optically and wireless connected digital world, growing through both organic and strategic means. Elements of our strategy include the following:

Focus on High Growth Market Opportunities. We will continue to focus our product development resources on high growth market segments both within the markets we currently serve as well as in new markets that utilize our core technologies. We will continue to invest substantially in products for 40Gbps and 100Gbps applications and selectively target new products for the 10Gbps markets where we can sustain a differentiation. We believe high growth opportunities exist even within more established communications segments by virtue of introducing innovative device and system architectures as well as business models to disrupt the established players and value chain relationships. Outside of telecom and data communications, we are able to reuse the same designs re-characterized for radio frequency (RF) systems used in defense applications such as phased array radar, super-computers and in wireless applications, such as point-to-point back-haul systems.

Grow Customer Base. We intend to continue to broaden our strategic relationship with key customers by maximizing design wins across their product lines. We intend to continue to leverage the approved vendor status we have with these key customers to qualify our products into additional optical and wireless systems, a process that is accelerated when we have already been qualified in a customer’s systems. We are adding sales and technical support staff to better serve key customers, markets and regions. We also intend to add to our number of strategic relationships by selectively targeting certain existing customers with whom we are not yet a strategic vendor. We will expand our development efforts with these customers through initiatives including providing specialized sales and support resources, holding technology forums to align our product development effort and implementing custom manufacturing linkages.

Engage Customers Early in their Product Planning Cycle. By engaging our customers early in their system design process, we gain critical information regarding their system requirements and objectives that influences our component design. Our sales force, product marketing teams and developmental engineers engage regularly with our customers to understand their product development plans. Additionally, for certain key customers, which are referred to as GigOptix’ “Lighthouse” customers, we hold periodic technology forums and technology audits so that the product development teams of these customers can interact directly with our research and development teams. Likewise, our early involvement in their system development processes also enables us to influence standards and introduce differentiated products early to market. Moreover, this dynamic interaction between ourselves and our customers provides us a significant competitive advantage, valuable insight and a close customer relationship that grows over each generation of products introduced by our customers.

5

Table of Contents

Partner for Innovation. Over the past few years, we have successfully partnered with lead “Lighthouse” customers, contract manufacturers and U.S. government agencies on research and development in both our electronic components and electro-optics polymer materials. We see this as a core element of our strategy both to support the investment required to maintain our innovation as well as aligning our R&D with the future needs of industry and defense markets. In order to maintain our position at the forefront of next generation optical modules and components, we intend to continue our longstanding relationship with the U.S. government agencies such as the Defense Advanced Research Projects Agency and the Air Force Research Laboratory as well as their network of contractors. We have aligned with our partners on the long term objectives of research and development related to the integration of semiconductor and thin-film polymer modulators to address terra scale computing and communications for defense and commercial markets and we have defined multiyear projects to develop and bring these technologies to reality. Similarly we partner with leading commercial customers on developments of product required in the one to two years horizon, often sharing the investment. This again gives us the assurance of alignment to the market needs when considering the sometimes significant investment in a new development. This model has been used for our 100Gbps modulator drivers for telecom networks, which was launched in 2010. Other cooperative projects include a 100Gbps short reach multi-channel driver and receiver pair with a leading Japanese networking solutions provider, and an innovative ultra-low power 10Gbps single channel chipset for a leading enterprise networking solutions provider in China.

Strategic Acquisitions. To augment our organic growth strategy, we actively pursue acquisitions that provide an efficient alternative to in-house development of technology, products or revenue. The synergies we search for include efficient extension of our product offering to strengthen our market position, enhancing of our technology base, enhancing of our revenue base, and expanding our customer base in selected markets to provide cross selling opportunities or to enhance our geographic or market segment presence. We continuously evaluate potential acquisitions against the above criteria. Our process aims to conduct a swift integration to quickly eliminate duplicate and redundant costs to ensure early accretive performance within one to two quarters. Our acquisition of ChipX in 2009 accomplished physical and systems integration, and reduced headcount, closed a facility in Haifa, Israel and consolidated its Santa Clara, California personnel into our Palo Alto offices.

Technology and Research and Development

We utilize proprietary technology at many levels within our product development, ranging from the basic materials research that created the innovative materials we use in our TFPS modulators to sophisticated integration and optimization techniques we use to design our components. We are committed to conducting fundamental research in thin-film polymer materials and manufacturing technologies. In addition, we have a proven record of successfully productizing this research. Our technology is protected by our patent portfolio and trade secrets developed in deployments with our extensive customer base. Our leading technologies include our fundamental and unique TFPS technology for optical modulation and extend through ultra-broadband monolithic microwave integrated circuit (MMIC) design, multi-chip module (MCM) design, innovative ultra-low power laser driver and receiver IC design in silicon germanium, high speed analog and RF IC design, mixed signal IC design, and Structured and Hybrid ASIC infrastructure. In particular, the following technologies are central to our business:

High Speed Analog Semiconductor Design & Development. One of our key core competences is circuit design for optimal signal integrity performance in high power applications. We use a variety of semiconductor processes to implement our designs including III-V processes such as indium phosphide and gallium arsenide for higher power applications such as long reach telecom transponder. We also have expertise in low power designs in silicon germanium and CMOS silicon for use in short reach data-com and optical interconnects application and circuit design to reduce cross-talking in dense multi-channel designs.

Electro-Optic Thin-Film Polymer on Silicon (TFPS) Material. Our unique, patent-protected technology is used to lithographically form a Mach-Zehnder modulator using standard silicon production technology processes and our proprietary thin-film polymeric materials. Optical modulators are commonly used as high performance shutters to switch optical signals to apply the digital data to light stream. Our technology can support bandwidths of up to 200GHz, while the current generation of material optimized for production is used in 40GHz and

6

Table of Contents

100GHz optical modulators, which are as competitive with leading 40Gbps modulators in the market. The technology has several ground-breaking characteristics as follows: it provides the fastest switching of any available technology and is effectively limited by the bandwidth of the digital control circuit up to 200Gbps bit/second rate; it is suitable for lithographic implementation of an existing semiconductor production line which facilitates both lower cost manufacturing of on-chip modulators and arrays and close proximity to the digital circuits for optimal performance; and the material operates effectively at very low temperatures, which enables increased frequencies due to the absence of thermally induced noise. All of these unique advantages make the material attractive for telecom, defense and super-computing applications.

Our research and development plans are driven by customer and partner input obtained by our sales and marketing teams, through our participation in various standards bodies, and by our long-term technology and product strategies. We review research and development priorities on a regular basis and advise key customers of our progress to achieve better alignment in our product and technology planning. For new components research and development is conducted in close collaboration with our contract manufacturer partners to shorten the time to market and optimize the manufacturability of the products.

Products

We design and market products that amplify electrical signals during both the transmission (drivers) and reception (TIAs) of optical signals as well as modulate optical signals in the transmission of data. We have a comprehensive product portfolio for these markets, particularly at data rates that exceed 10Gbps. The primary target market and application for our products are optical interface modules such as line-cards, transponders and transceivers within telecom and data-communications switches and routers. These are critical blocks used in both telecom or data-communications optical communication networks from the long haul to the short reaches where the conversion of data from the electrical domain to the optical domain occurs. Our drivers amplify the input digital data stream that is used to modulate laser light either by direct modulation of the laser or by use of an external modulator that acts as a precise shutter to switch on and off light to create the optical data stream. At the other end of the optical fiber, our sensitive receiver TIAs detect and amplify the small currents generated by photo-diodes converting the faint received light into an electrical current. The TIAs amplify the small current signals into a larger voltage signal that can be read by the electronics and processors in the network servers. We supply an optimized component for each type of laser, modulator and photo-diode depending upon the speed, reach and required cost. Generally, the shorter the reach is, the higher the volume, the less demanding the product specifications and the greater the pressure to reduce costs. We implement our products on a number of process technologies and have been at the forefront of extracting optimal performance from each technology to be able to address each market segment’s individual requirements in a cost effective manner. Our product portfolio is designed to cover the broad range of solutions needed in these different modules and includes the product lines described below.

Our product portfolio comprises components from 5 product lines:

| 1. | GX Series: Serial drivers and TIA ICs devices for telecom and data-com markets |

| 2. | HX Series: Multi-channel driver and TIA ICs for short reach data-com and optical interconnect applications |

| 3. | LX Series: TFPS modulators for high speed telecom and defense applications |

| 4. | iT Series: High performance amplifiers for microwave applications in defense and instrumentation |

| 5. | CX Series: Family of ASIC solutions for custom integrated circuit design |

7

Table of Contents

GX Series

The GigOptix GX Series services both the telecom and data-com markets with a broad portfolio of drivers and transimpedence amplifiers that address 10Gbps, 40Gbps and 100Gbps speeds over distances that range from 100 meters to more than 4000 kilometers. The GX Series devices are used in FiberChannel, Ethernet, SONET/SDH components and those based upon the OIF standardization.

| • | Within the 10Gbps, market, we have enabled many innovative solutions such as the GX3110 linear TIA for use in systems using Electronic Dispersion Compensation (EDC) and requiring excellent linearity and low total harmonic distortion to address the demanding SONET TIA receiver requirements. Moreover, we also supply the GX6155 Mach-Zehnder driver that is implemented in a ceramic package which enables both high performance electrical signals and robust packaging and improved manufacturability. |

| • | Within the 40Gbps, market, we have enabled significantly lower power transponder designs with our GX6261 40Gbps, DQPSK driver. This compares with competitor solutions that consume 50% more power and require 40% more real estate on the board. Both savings are significant since each 40Gbps, transponder typically requires two drivers. Furthermore, in 2010 we introduced two surface mounted single ended low power driver solutions, the GX6255 single channel driver and GX62255 dual channel driver, each consuming less than 1.6W per channel and available with integrated high frequency chokes to simplify board manufacture. We also supply the GX3220, a low power 40Gbps, DQPSK TIA to amplify the received optical signals. This solution coupled with GigOptix drivers transponder enables customers to implement the lowest overall power transponder solution. Furthermore, we also supply the GX3440 differential amplifier that has broad bandwidth and high gain and enables single chip amplification of 40Gbps DPSK signals as small 50mVpp to 800mVpp and is used extensively in Tier 1 DPSK receivers. |

| • | Within the 100Gbps, market, we supply a high performance monolithic driver solution for both the 4x28Gbps and 4x32Gbps DP-QPSK formats. The GX62450 was developed in close collaboration with a Tier-1 telecom OEM and is designed to plug seamlessly between the transmission multiplexer and the Mach-Zehnder modulator to provide best in industry electrical connectivity quality. Furthermore, in 2010 we introduced two surface mounted single ended low power driver solutions, the GX6255 single channel driver and GX62255 dual channel driver, each consuming less than 1.6W per channel and available with integrated high frequency chokes to simplify board manufacture. We also introduced the highly integrated GX62455 quad driver device that consumes less than 7W and is available in the same form factor as the GX62450. We also supply a 32Gbps TIA that is compliant with the 100Gbps, DP-QPSK standard in a dual channel configuration to enable easier manufacturing within the receiver. |

HX Series

The GigOptix HX Series services the high performance computing (HPC), data-com and consumer markets with a portfolio of parallel VCSEL drivers and TIAs that address 3Gbps, 5Gbps and 10Gbps channel speeds over 100-300 meters distances in 4 and 12 channel configurations. The HX Series devices are used in proprietary HPC formats, Infiniband, Ethernet and optical HDMI components.

| • | Within the 3Gbps market, we supply the HXT3404 VCSEL driver and HXR3404 TIA 4 channel arrays die that enable both proprietary HPC communication and 30 to 100 meter HDMI active optical cables (AOC) in the consumer space. These HDMI AOCs are becoming more prevalent with the move to displays situated further from the signal source such as those found in in-flight entertainment systems, displays in airport and bus terminals as well as advertisement displays in shopping malls. |

| • | Within the higher speed markets, we supply the ultralow power HXT4104/HXR4104 four channel array dies used in 40GBASE-SR4 Ethernet and 40G-IB QDR Infiniband specifications as well as the HXT4112/HXR4112 twelve channel array dies used in both 100GBASE-SR10 Ethernet and 120G-IB QDR Infiniband specification. The HXT4012/HXR4112 solution set has been demonstrated to be able |

8

Table of Contents

| to deliver 120Gbps over 100m with less than 1W of power dissipation signifying an industry leading 8mW/Gbps power link budget. Both arrays also provide superior VCSEL monitoring capabilities to the competition that is becoming more important in large datacenter deployments where there can be 1000’s to 10,000’s of cables that require remote and accurate optical link health monitoring capabilities. |

| • | Within the single channel SFP+ markets, we developed the HXT4101 VCSEL driver and HXR4101 TIA chip set for a new Smart Transmit Optical SubAssembly (TOSA) and Receive Optical SubAssembly (ROSA) solution to address the 10Gbps short reach market. The solution leverages our extensive mixed signal experience in high volume parallel optics devices to combine advanced RF analog circuit techniques that reduce power consumption with integrated on-chip Analog-to-Digital Converters and Digital-to-Analog Converters to enable a fully digitally controlled TOSA and ROSA. This architecture significantly simplifies the design of an optical transceiver such as an SFP+ by eliminating all analog and RF circuits from the PCB. The elimination of RF analog interfaces improves performance and reduces both power consumption and EMI within the transceiver. The new architecture also reduces costs while significantly reducing the engineering effort associated with developing a solution. |

LX Series

The GigOptix LX Series services the 40Gbps and above telecom market for high performance Mach-Zehnder modulators. The LX Series devices are based on our proprietary TFPS EO material technology. The technology provides significant advantages over competing technologies such as indium phosphide (InP) and lithium niobate (LN) in areas such as bandwidth, size and power consumption.

We currently offer two LX products:

| • | The LX8900 is the industry’s only serial 100Gbps Mach-Zehnder modulator with a bandwidth of 65GHz. It is primarily being used in emerging applications such as “Beyond 100G,” optical links trials and ultra-broadband RF photonic military products. |

| • | The LX8401 is the industry’s smallest 40Gbps, DPSK modulator device and is almost half the size of competing technology solutions while providing the same level of performance. The smaller size enables customers to reduce their transponder size considerably which in turn allows more transponders to be placed on a line-card and increases chassis port density for end customers. |

We are now in the process of leveraging our new TFPS technology to enable 40Gbps, DQPSK and 100Gbps, DP-QPSK devices in market leading small form factors and at the same time leveraging our GX Series of drivers to enable a complete integrated solution set for the customer.

iT Series

The GigOptix iT Series of products leverages the high performance die and design techniques developed for the GX Series telecom and data-com drivers for related defense and instrumentation applications. We differentiate ourself in the defense and instrumentation markets by providing high gain, broadband devices that exhibit minimal ripple across the gain spectrum of the device: this ensures optimum performance. Moreover, most of our devices have only a single rail supply which both simplifies the board design and improves reliability of the system. For instance, we provide the single rail supply iT2008 high power 26GHz amplifier with a saturated output power of 1W and 1dB of ripple. This device’s performance and ease of use power up sequence has led to extensive use in military radar and satellite communication systems.

9

Table of Contents

CX Series

The GigOptix CX Series of products offers the broadest portfolio of distinct paths to digital and analog mixed signal ASICs with the capability of supporting designs of up to 10M gates in technologies ranging from 0.6µ through 0.13µ. The CX Series uses our proprietary technology in Structured and Hybrid ASICs to enable a generic ASIC solution that can be customized for a customer using only a few metal mask layers. This ensures fast turnaround times with significant cost advantages for customers over both FPGA and dedicated ASIC implementations. The CX Series also offers value-added ASIC services including integrating proven Analog and Mixed Signal IP into designs and taking customers designs from RTL or gate-level netlist to volume production with major third party foundries. The CX Series has a significant customer base in the consumer, instrumentation, networking, medical, military and aerospace markets.

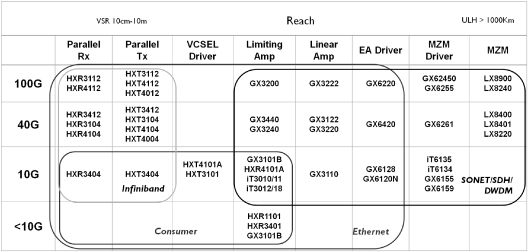

The following is a compilation of our product portfolio for optical communications:

Customers

We have a global customer base in the telecommunications, data-communications, defense and industrial electronics markets. Our customers include many of the leading network systems vendors supplying worldwide. During 2010 we sold to major customers including Alcatel-Lucent, Cisco, Finisar, Fujitsu, JDSU, Mitsubishi, Multiplex, Opnext, Source Photonics, ZTE, and other “Tier-One” equipment vendors in the United States, Europe and Asia, as well as leading industrial, aerospace and defense customers such as Adtran, Anritsu, Avocent, Boeing, Hamilton Sundstrand, John Deere, LeCroy, National Instruments, Northrop Grumman, Raytheon and Rockwell-Collins, Rohde & Schwartz, and Teradyne.

Of our total revenue in 2010, 25%, 51% and 24% were generated by customers located in Asia, North America and Europe, respectively, compared with 24%, 49% and 27%, respectively, for the year ended December 31, 2009. In 2010, 14% of our revenue was contributed by our government contracts and 86% was contributed by product revenue, compared with 24% and 76%, respectively, for the year ended December 31, 2009.

Our customers in the industrial and commercial markets consist of a broad range of companies that design and manufacture electro-optics and high speed information management products. These include medical, industrial, test and measurement, scientific systems, printing engines for high-speed laser printers and defense and aerospace applications. The number of leading network systems vendors which supply the global telecommunications and data communications market is concentrated, and so, in turn, is our customer base. Additionally, Alcatel-Lucent is our largest telecommunications customer representing 11% and 23% of our total

10

Table of Contents

revenues for the years ended December 31, 2010 and December 31, 2009, respectively. Other than Alcatel-Lucent, other telecommunications customer accounted for more than 10% of total revenue for the years ended December 31, 2010 and December 31, 2009, respectively; however, contracts with the U.S. Government accounted for 14% and 24% of our total revenue for the years ended December 31, 2010 and December 31, 2009, respectively.

Manufacturing

Our foundry and contract manufacturing partners are located in China, Japan, the Philippines, Taiwan, and the United States. Certain of our contract manufacturing partners that assemble or produce modules are strategically located close to our customers’ contract manufacturing facilities to shorten lead times and enhance flexibility.

We follow established new product introduction processes that ensure product reliability and manufacturability by controlling when new products move from sampling stage to mass production. We have stringent quality control processes in place for both internal and contract manufacturing. We utilize manufacturing planning systems to coordinate procurement and manufacturing to our customers’ forecasts. These processes and systems help us closely coordinate with our customers, support their purchasing needs and product release plans, and streamline our supply chain.

Electronic components: Integrated circuits and multi-chip modules: For our ICs and MCMs we use an outsourced contract manufacturing model. We have a prototype manufacturing and testing facility in our Palo Alto location which is used to optimize manufacturing and test procedures to achieve internal yield and quality requirements before transferring production to our contract manufacturing partners. We develop long-term relationships with strategic contract manufacturing partners to reduce assembly costs and provide greater manufacturing flexibility. The manufacture of some products such as certain low volume, high complexity or customized multi-chip modules may remain in-house even in mass production to speed time to market and bypass manufacturing transfer costs.

For our less complex packaged chips and bare die products, we typically move new product designs directly to contract manufacturing partners. These products fit easily in a standard fabless semiconductor production flow and ramp up to much greater volumes in mass production.

TFPS EO components: Four chemical synthesis labs within our Bothell facility are equipped with chemical hoods capable of delivering EO polymer and claddings in volumes up to kilogram batch volumes. Polymer manufacturing and development are supported by a characterization and test lab equipped with state-of-the-art equipment for measuring molecular and material properties.

Wafer fabrication is supported within the 1,400 square feet class 100 clean-room equipped with standard semiconductor processing. Wafer dicing, cleaning, and facet polishing is supported in the “back end” processing lab outside of the clean-room. Our Bothell facility is capable of supporting manufacturing and development of up to five 150mm diameter substrates/week. As volumes increase, GigOptix has identified IMT in Santa Barbara, California as an outsourcing partner with a 30,000 square feet class 100 clean-room dedicated to support contract manufacturing, and IMT is able to support high volume wafer manufacturing. Chip level screening and testing is performed in Bothell using a semi-automated fiber alignment station capable of low frequency testing of insertion loss, Vpi and extinction ratio. EO testing at the chip and package level utilizes RF equipment capable of testing modulators up to 40 GHz. Optical pig-tailing, wire bonding, and sealing are also performed in-house. Samina SCI located in Shenzhen, China has been identified as a source to support volume packaging of up to thousands of units per month.

11

Table of Contents

Sales, Marketing and Technical Support

In the communications market, we primarily sell our products through our direct sales force supported by a network of manufacturer representatives and distributors. Our sales force works closely with our field application engineers, product marketing and sales operations teams in an integrated approach to address a customer’s current and future needs. We assign account managers for each strategic customer account to provide a clear interface to our customers, with some account managers responsible for multiple customers. The support provided by our field application engineers is critical in the product qualification stage. Transceiver modules, especially at 10Gbps and above, are complex products that are subject to rigorous qualification procedures of both the product and the supplier and these procedures differ from customer to customer. Also, many customers have custom requirements in addition to those defined by MSAs in order to differentiate their products and meet design constraints. Our product marketing teams interface with our customers’ product development staffs to address customization requests, collect market intelligence to define future product development, and represent us in MSAs.

For our “Lighthouse” customers, we hold periodic technology forums for their product development teams to interact directly with our research and development teams. These forums provide us insight into our customers’ longer term needs while helping our customers adjust their plans to the product advances we can deliver. Also, our customers are increasingly utilizing contract manufacturers while retaining design and key component qualification activities. As this trend matures, we continually upgrade our sales operations and manufacturing support to maximize our efficiency and flexibility and coordination with our customers.

In the industrial and commercial market, we primarily sell through a network of manufacturing representatives and distributors to address the broad range of applications and industries in which our products are used. The sales effort is managed by an internal sales team and supported by dedicated field application engineering and product marketing staff. We also sell direct to certain strategic customers. Through our customer interactions, we continually increase our knowledge of each application’s requirements and utilize this information to improve our sales effectiveness and guide product development.

Since inception, we have actively communicated the GigOptix brand worldwide through participation at trade shows and industry conferences, publication of research papers, bylined articles in trade media, and advertisements in trade publications and interactive media, interactions with industry press and analysts, press releases and our company website, as well as through print and electronic sales material.

Competition

The market for electronic and electro-optic devices is characterized by price competition, rapid technological change, short product life cycles, and global competition. While no one company competes against us in all of our product areas, our competitors range from the large, international companies offering a wide range of products to smaller companies specializing in narrow markets. Due to the increasing demands for high-speed, high-frequency components, we expect competition to increase from existing semiconductor and electro-optical modulator suppliers, in addition to the entry of new competitors to our target markets and from the internal operations of some companies producing products similar to ours for their own internal requirements.

Because some of our competitors are large public companies with longer operating histories and greater financial, technical, marketing and other resources, these companies have the ability to devote greater resources to the development, promotion, sale and support of their products. For example, in the telecommunications and data-communications markets, some of our competitors have deeper relationships with prospective customers, related to wider portfolio of products they are selling to them across the board. Other competitors may also have preferential access to certain network systems vendors, or offer directly competitive products that may have better performance measures than our products. Moreover, competitors that have large market capitalizations or cash reserves may be better positioned than we are to acquire other companies in order to gain new technologies or products that may compete with our product lines. Any of these factors could give our competitors a strategic

12

Table of Contents

advantage. Therefore, although we believe we currently compete favorably with our competitors, we cannot assure you that we will be able to compete successfully against either current or future competitors in the future.

We believe the principal competitive factors impacting all of our products are:

| • | product performance including size, speed, operating temperature range, power consumption and reliability; |

| • | price to performance characteristics; |

| • | delivery performance and lead times; |

| • | time to market; |

| • | breadth of product solutions; |

| • | sales, technical and post-sales service and support; |

| • | technical partnership in early stage of product development; |

| • | sales channels; and |

| • | ability to drive standards and comply with new industry MSAs. |

GX Products

In the telecom and data-communications segments, we compete with Triquint, Rohm, InPhi, Gennum and Vitesse. We compete with Triquint predominantly in the 10Gbps, 40Gbps and 100Gbps Mach Zehnder driver space; Rohm predominantly in the 10Gbps EML driver space; InPhi predominately in the TIA spaces and the 40Gbps driver space; Gennum predominately in the data-communications space and Vitesse in the 10Gbps TIA receiver space.

HX Products

In the market for PMD ICs we compete with Avago, Emcore, Tyco Electronics (formerly Zarlink) and Iptronics. Avago, Emcore and Tyco Electronics are vertically integrated transceiver module manufacturers with in-house PMD ICs designs. These companies have comparable products to our products but have been later to market in offering a 10Gbps solutions. In addition to these companies, Iptronics also competes in this space and is a venture-funded startup specializing in parallel optical interconnect with a family of devices at 10Gbps and is a direct competitor.

LX Products

We compete with JDSU, Oclaro, Sumitomo and Fujitsu that supply lithium niobate modulators for the long haul/Metro market and more recently JDSU, Sumitomo, Emcore and Oclaro that supply indium phosphide modulators for the Metro market. We expect that our TFPS modulators will be competitive with lithium niobate and indium phosphide products in terms of pricing and operating performance and will provide significant performance advantages in areas such as size, bandwidth and optical extinction ratio.

iT Products

Our ultra-broadband amplifiers and limiters offer performance with gain flatness and low noise figures. We compete with Triquint, Hittite, Northrop Grumman (for internal use) and Mimix in this product area.

13

Table of Contents

CX Products

Our ASICs compete in the custom integrated circuit industry, an industry that is intensely competitive. In the low to medium volume market, the primary competitors include Lattice Semiconductor and Actel Corporation. In the medium to high volume market, there are over 30 companies competing in this market. Companies that we compete with most often include On Semiconductor, eSilicon, Open Silicon, Faraday, Toshiba and eASIC.

We believe that important competitive factors specific to the custom integrated circuit industry include: Product pricing, time-to-market, product performance, reliability and quality, power consumption, availability and functionality of predefined IP cores, inventory management, access to leading-edge process technology, track record of successful product execution and achieving first time working silicon, ability to provide excellent applications support and customer service, ability to offer a broad range of ASIC solutions to retain existing customers, and compliance with ITAR.

Patents and Other Intellectual Property Rights

We rely on patent, trademark, copyright and trade secret laws and internal controls and procedures to protect our technology. We believe that a robust technology portfolio that is assessed and refreshed periodically is an essential element of our business strategy. We believe that our success will depend in part on our ability to:

| • | Obtain patent and other proprietary protection for the materials, processes and device designs that we develop; |

| • | Enforce and defend patents and other rights in technology, once obtained; |

| • | Operate without infringing the patents and proprietary rights of third parties; and |

| • | Preserve our company’s trade secrets. |

As of December 31, 2010, we have been issued 67 patents and have 9 patent applications pending. Patents have been issued in various countries with the main concentrations in the United States. Our patent portfolio covers a broad range of intellectual property including semiconductor design and manufacturing, device packaging, module design and manufacturing, electrical circuit design, thin film polymer technology, modulator design and manufacturing. We follow well-established procedures for patenting intellectual property and have internal incentive plans to encourage the protection of new inventions. The portfolio also represents a balanced compilation of intellectual property that has been filed by the various companies we have acquired, and hence protects all of our product lines. We also license patented technology from the University of Washington. Many of the pending and issued U.S. patents have one or more corresponding internal or foreign patents or applications.

We take extensive measures to protect our intellectual property rights and information. For example, every employee enters into a confidential information, non-competition and invention assignment agreement with us when they join and are reminded of their responsibilities when they leave. We also enter into and enforce a confidential information and invention assignment agreement with contractors.

We have patents and patents pending covering technologies relating to:

Polymers

| • | Optical polymers and synthesis; |

| • | Production of polymers in commercial quantities; |

| • | Materials characterization and testing methods; and |

| • | Devices, designs and processes relating to polymers. |

14

Table of Contents

High-Speed Integrated Circuits

| • | Circuit topology to achieve ultra-large frequency bandwidth; |

| • | Efficient voltage control circuit for broadband high voltage drivers; and |

| • | Control circuit to stabilize over temperature gain control functionality. |

ASICs

| • | Customizable integrated circuit devices; |

| • | Single metal programmability in a customizable integrated circuit device; |

| • | Configurable cell for customizable logic array device; |

| • | In-Circuit device, system and method to parallelize design and verification; and |

| • | Method of developing application specific integrated circuit devices. |

Although we believe our patent portfolio is a valuable asset, the discoveries or technologies covered by the patents, patent applications or licenses may not have commercial value. Issued patents may not provide commercially meaningful protection against competitors. Other parties may be able to design around our issued patents or independently develop technology having effects similar or identical to our patented technology. The scope of our patents and patent applications is subject to uncertainty and competitors or other parties may obtain similar patents of uncertain scope. Other parties may discover uses for polymers or technology different from the uses covered in our patents or patent applications and these other uses may be separately patentable. Other parties may have patents covering the composition of polymers for which we have patents or patent applications covering only methods of use of these polymers.

Third parties may infringe the patents that we own or license, or claim that our potential products or related technologies infringe their patents. Any patent infringement claims that might be brought by or against our company may cause us to incur significant expenses, divert the attention of our management and key personnel from other business concerns and, if successfully asserted against us, require us to pay substantial damages. In addition, a patent infringement suit against our company could force us to stop or delay developing, manufacturing or selling potential products that are claimed to infringe a patent covering a third party’s intellectual property.

We periodically evaluate our patent portfolio based on our assessment of the value of the patents and the cost of maintaining such patents, and may choose from time to time to let various patents lapse, terminate or be sold.

Employees

As of December 31, 2010, we had 83 full-time employees, including 37 in research and development, 27 in operations, 9 in sales and marketing, and 10 in general and administrative.

Environmental

Our operations involve the use, generation and disposal of hazardous substances and are regulated under international, federal, state and local laws governing health and safety and the environment. We believe that our products and operations at our facilities comply in all material respects with applicable environmental laws and worker health and safety laws; however, the risk of environmental liabilities cannot be completely eliminated.

15

Table of Contents

Government Regulations

We are subject to federal, state and local laws and regulations relating to the generation, handling, treatment, storage and disposal of certain toxic or hazardous materials and waste products that we use or generate in our operations. We regularly assess our compliance with environmental laws and management of environmental matters.

We are also subject to federal procurement regulations associated with its U.S. government contracts. Violations of these regulations can result in civil, criminal or administrative proceedings involving fines, compensatory and punitive damages, restitution and forfeitures as well as suspensions or prohibitions from entering into government contracts. The reporting and appropriateness of costs and expenses under our government contracts are subject to extensive regulation and audit by the Defense Contract Audit Agency, an agency of the U.S. Department of Defense. The contracts and subcontracts to which we are a party are also subject to potential profit and cost limitations and standard provisions that allow the U.S. government to terminate such contracts at its convenience. We are entitled to reimbursement of our allowable costs and to an allowance for earned profit if the contracts are terminated by the U.S. government for convenience.

Sales of our products and services internationally may be subject to the policies and approval of the U.S. Department of State and Department of Defense. Any international sales may also be subject to United States and foreign government regulations and procurement policies, including regulations relating to import-export control such as ITAR, investments, exchange controls and repatriation of earnings.

Where You Can Find More Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge as soon as possible after we electronically file them with, or furnish them to, the SEC. You can access our filings with the SEC by visiting our website. The information on our website is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K or incorporated into any other filings we make with the SEC. Additionally, the Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended by our predecessor registrant Lumera are available at www.sec.gov.

You can also read and copy any document that we file, including this Annual Report on Form 10-K, at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Call the SEC at 1-800-SEC-0330 for information on the operation of the Public Reference Room. In addition, the SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. You can electronically access our SEC filings there.

16

Table of Contents

| ITEM 1A. | RISK FACTORS |

You should carefully consider the risks described below as well as the other information contained in this Form 10-K before making an investment decision. In addition to the risks described below, there may be additional risks and uncertainties not currently known to us or that we currently deem to be immaterial that may become material risks. Any of these risks could materially affect our businesses, financial condition or results of operations. In such case, you may lose all or part of your original investment.

We and our predecessors have incurred substantial operating losses in the past and we may not be able to achieve profitability in the future.

We have incurred negative cash flows from operations since inception. For the years ended December 31, 2010 and 2009, we incurred net losses of $4.4 million and $10.0 million, respectively, and cash outflows from operations of $3.8 million and $4.1 million, respectively. As of December 31, 2010 and 2009, we had an accumulated deficit of $73.4 million and $69.0 million, respectively. We expect development, sales and other operating expenses to increase in the future as we expand our business. If our revenue does not grow to offset these expected increased expenses, we may not be profitable. In fact, in future quarters we may not have any revenue growth and our revenues could decline. Furthermore, if our operating expenses exceed expectations, financial performance will be adversely affected and we may continue to incur significant losses in the future.

In addition, we acquired ChipX in November 2009. ChipX incurred net losses of $5.7 million for the year ended December 31, 2008 and an additional net loss of $3.3 million for the period from January 1, 2009 through the date of acquisition of November 9, 2009.

We may require additional capital to continue to fund our operations. If we need but do not obtain additional capital, we may be required to substantially limit operations.

We may not generate sufficient cash needed to finance our anticipated operations for the foreseeable future from such operations. Accordingly, we may seek funding through public or private financings, including equity financings, and through other arrangements including collaborations. We could require additional financing sooner than expected if we have poor financial results, including unanticipated expenses, or an unanticipated drop in projected revenues. Such financing may be unavailable when needed or may not be available on acceptable terms. If we raise additional funds by issuing equity or convertible debt securities, the percentage ownership of our current stockholders will be reduced, and these securities may have rights superior to those of our common stock. If adequate funds are not available to satisfy either short-term or long-term capital requirements, or if planned revenues are not generated, we may be required to limit our operations substantially. These limitations of operations may include a possible sale or shutdown of portions of our business, reductions in capital expenditures and reductions in staff and discretionary costs.

We have incurred negative cash flows from operations since inception. For the years ended December 31, 2010 and 2009, we incurred net losses of $4.4 million and $10.0 million, respectively, and cash outflows from operations of $3.8 million and $4.1 million respectively. As of December 31, 2010 and 2009, we had an accumulated deficit of $73.4 million and $69.0 million, respectively. We have incurred significant losses since inception, attributable to our efforts to design and commercialize our products. We have managed our liquidity during this time through a series of cost reduction initiatives and through increasing our line of credit with our bank. Our ability to continue as a going concern is dependent on many events outside of our direct control, including, among other things; obtaining additional financing either privately or through public markets and consumers’ purchasing our products in substantially higher volumes. During 2010, we raised approximately $3.9 million in additional equity capital from institutional investors which stabilized our cash position. We have used that cash to substantially reduce our outstanding accounts payable and accrued expenses balances. In addition, we have access to a line of credit with Silicon Valley Bank which enables us to borrow up to $3 million based on 80% of eligible invoiced amounts to customers. We also were close to breakeven, incurring a loss of $97,000, on

17

Table of Contents

an operating income basis in the fourth quarter of 2010. Additionally, our pending merger with Endwave upon closing will provide us with additional cash and equivalents which should mitigate near-term liquidity issues. Based on these events and factors we believe that our cash, cash from operations, and our line of credit will be sufficient for at least the next 12 months.

We may fail to realize the anticipated benefits of our merger with ChipX.