Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 25, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-18914

DORMAN PRODUCTS, INC.

(Exact name of registrant as specified in its charter)

| Pennsylvania | 23-2078856 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. - Employer Identification No.) |

3400 East Walnut Street, Colmar, Pennsylvania 18915

(Address of principal executive offices) (Zip Code)

(215) 997-1800

(Registrants telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: NONE

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.01 Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ¨ No x

As of March 1, 2011 the registrant had 17,878,709 shares of common stock, $.01 par value, outstanding. The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 26, 2010 was $214,804,518.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s definitive proxy statement, in connection with its Annual Meeting of Shareholders, to be filed with the Securities and Exchange Commission within 120 days after December 25, 2010, are incorporated by reference into Part III of this Annual Report on Form 10-K

Table of Contents

DORMAN PRODUCTS, INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

DECEMBER 25, 2010

| Page | ||||||

| Part I | ||||||

| Item 1. |

3 | |||||

| 3 | ||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 5 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 7 | ||||||

| 7 | ||||||

| Item 1A. |

7 | |||||

| Item 1B. |

12 | |||||

| Item 2. |

12 | |||||

| Item 3. |

12 | |||||

| Item 4. |

12 | |||||

| Part II | ||||||

| Item 5. |

13 | |||||

| Item 6. |

14 | |||||

| Item 7. |

Management’s Discussion and Analysis of Results of Operations and Financial Condition |

15 | ||||

| Item 7A. |

20 | |||||

| Item 8. |

20 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

35 | ||||

| Item 9A. |

35 | |||||

| Part III | ||||||

| Item 10. |

37 | |||||

| Item 11. |

37 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

37 | ||||

| Item 13. |

37 | |||||

| Item 14. |

37 | |||||

| Part IV | ||||||

| Item 15. |

38 | |||||

| 41 | ||||||

| 42 | ||||||

2

Table of Contents

PART I

Dorman Products, Inc. (formerly R&B, Inc.) was incorporated in Pennsylvania in October 1978. As used herein, unless the context otherwise requires, “Dorman”, the “Company”, “we”, “us”, or “our” refers to Dorman Products, Inc. and its subsidiaries.

We are a supplier of automotive replacement parts and fasteners and service line products primarily for the automotive aftermarket. We market approximately 122,000 different automotive replacement parts (including brake parts), fasteners and service line products. Approximately 21% of our parts are comprised of parts and fasteners that were original equipment dealer “exclusive” items at the time of their introduction. Original equipment dealer “exclusive” parts are those which were traditionally available to consumers only from original equipment manufacturers or salvage yards and include, among other parts, intake manifolds, exhaust manifolds, oil cooler lines, window regulators, radiator fan assemblies, power steering pulleys and harmonic balancers. Fasteners include such items as oil drain plugs and wheel lug nuts. These dealer “exclusive” parts represent 66% of our net sales for the year ended December 25, 2010. Approximately 85% of our products are sold under our brand names and the remainder is sold for resale under customers’ private labels, other brands or in bulk. Our products are sold primarily in the United States through automotive aftermarket retailers (such as AutoZone, Advance Auto, and O’Reilly), national, regional and local warehouse distributors (such as Carquest and NAPA) and specialty markets and salvage yards. Through our Scan-Tech subsidiary, we are increasing our international distribution of automotive replacement parts, with sales into Europe, the Middle East and Asia. We are increasing distribution of automotive replacement parts in Canada through our Dorman Canada business unit.

The automotive replacement parts market is made up of two components: parts for passenger cars and light trucks, which accounted for sales of approximately $214.5 billion in 2010, and parts for medium and heavy duty trucks, which accounted for sales of approximately $69.9 billion in 20101. We currently market products primarily for passenger cars and light trucks.

Two distinct groups of end-users buy replacement automotive parts: (i) individual consumers, who purchase parts to perform “do-it-yourself” repairs on their own vehicles; and (ii) professional installers, which include automotive repair shops and the service departments of automobile dealers. The individual consumer market is typically supplied through retailers and through the retail arms of warehouse distributors. Automotive repair shops generally purchase parts through local independent parts wholesalers and through national automotive parts distributors. Automobile dealer service departments generally obtain parts through the distribution systems of automobile manufacturers and specialized national and regional automotive parts distributors.

The increasing complexity of automobiles and the number of different makes and models of automobiles have resulted in a significant increase in the number of products required to service the domestic and foreign automotive fleet. Accordingly, the number of parts required to be carried by retailers and wholesale distributors has increased substantially. The requirement to include more products in inventory and the significant consolidation among distributors of automotive replacement parts have in turn resulted in larger distributors.

Retailers and others who purchase aftermarket automotive repair and replacement parts for resale are constrained to a finite amount of space in which to display and stock products. Thus, the reputation for quality, customer service, and line profitability which a supplier enjoys is a significant factor in a purchaser’s decision as to which product lines to carry in the limited space available. Further, because of the efficiencies achieved through the ability to order all or part of a complete line of products from one supplier (with possible volume discounts), as opposed to satisfying the same requirements through a variety of different sources, retailers and other purchasers of automotive parts seek to purchase products from fewer but stronger suppliers.

| 1 | Source: AAIA Fact Book 2011 |

3

Table of Contents

We sell approximately 122,000 different automotive replacement parts, fasteners and service line products to meet a variety of needs. Our DORMAN® NEW SINCE 1918™ marketing campaign launched in 2005 repositioned our brands under a single corporate umbrella - DORMAN®. Our products are now sold under one of the seven DORMAN® sub-brands as follows:

|

DORMAN® OE Solutions ™ |

- Automotive replacement parts, such as intake manifolds, exhaust manifolds, oil cooler lines, window regulators, harmonic balancers and radiator fan assemblies. | |

|

DORMAN® HELP! ® |

- Automotive replacement parts, including window handles, and switches, door hardware, interior trim parts, headlamp aiming screws and retainer rings, radiator parts, battery hold-down bolts and repair kits, valve train parts and power steering filler caps. | |

|

DORMAN® AutoGrade™ |

- A line of application specific and general automotive hardware that is a necessary element to a complete repair. Product categories include body hardware, general automotive fasteners, oil drain plugs, and wheel hardware. | |

|

DORMAN® Conduct-Tite!® |

- A selection of electrical connectors, wire, tools, testers, and accessories. | |

|

DORMAN® FirstStop™ |

- Value priced technician quality brake and clutch program containing more than 8,500 SKU’s. | |

|

DORMAN® Pik-A-Nut® |

- A line of home hardware and home organization products specifically designed for retail merchandisers. | |

|

DORMAN® Scan-Tech® |

- Based in Stockholm, Sweden, DORMAN Scan-Tech sells a complete line of Volvo and Saab replacement parts throughout the world. | |

We also generate revenues by the sale of parts that we package for ourselves, or others, for sale in bulk or under the private labels of parts manufacturers and national warehouse distributors (such as Carquest and NAPA).

We group our products into four major classes: automotive body, powertrain, chassis, and hardware. The following table represents each of the four classes as a percentage of net sales for each of the last three fiscal years.

| Percentage of Net Sales | ||||||||||||

| Year Ended | ||||||||||||

| December 25, 2010 | December 26, 2009 | December 27, 2008 | ||||||||||

| Automotive Body |

28 | % | 27 | % | 25 | % | ||||||

| Power-train |

32 | % | 33 | % | 33 | % | ||||||

| Chassis |

25 | % | 23 | % | 23 | % | ||||||

| Hardware |

15 | % | 17 | % | 19 | % | ||||||

| Total |

100 | % | 100 | % | 100 | % | ||||||

Our line of automotive body products include door handles and hinges, window lift motors, regulators, switches and handles, wiper components, lighting, electrical, and other interior and exterior automotive body components. Our power-train product line includes intake and exhaust manifolds, cooling products, balancers, fluid lines, reservoirs, and connectors, 4 wheel drive components and axles, drain plugs, and other engine, transmission and axle components. Chassis products include brake hardware and hydraulics, wheel and axle hardware, suspension arms, knuckles, links and bushings; and other suspension, steering and brake components. Hardware products include threaded bolts, auto body and home fasteners, automotive and home electrical wiring components, and other hardware assortments and merchandise.

We warrant our products against certain defects in material and workmanship when used as designed on the vehicle on which it was originally installed. We offer a limited lifetime warranty on all of our products. Our warranty limits the customer’s remedy to the repair or replacement of the part that is defective.

4

Table of Contents

Product development is central to our business. The development of a broad range of products, many of which are not conveniently or economically available elsewhere, has in part, enabled us to grow to our present size and is important to our future growth. In developing our products, our strategy has been to design and package parts so as to make them better and easier to install and/or use than the original parts they replace and to sell automotive parts for the broadest possible range of uses. Each new product idea is reviewed by our product management staff, as well as by members of the production, sales, finance, marketing, and administrative staffs.

Through careful evaluation, exacting design and precise tooling, we are frequently able to offer products which fit a broader range of makes and models than the original equipment parts they replace. One such innovation is our neoprene replacement oil drain plug which fits not only a variety of Chevrolet, Ford and Chrysler models, but also a range of foreign makes and models. We also developed a window lift motor which fits not only a variety of General Motors models, but also Toyota, Mitsubishi and Suzuki vehicles. This flexibility assists retailers and other purchasers in maximizing the productivity of the limited space available for each class of part sold. Further, where possible, we improve our parts so they are better than the parts they replace. Thus, many of the our products are simpler to install or use, such as a replacement “split boot” for a constant velocity joint that can be installed without disassembling the joint itself and a replacement spare tire hold-down bolt that is longer and easier to thread than the original equipment bolt it replaced. In addition, we often package different items in complete kits to ease installation.

Ideas for expansion of our product lines arise through a variety of sources. We maintain an in-house product management staff that routinely generates ideas for new parts and the expansion of existing lines. Further, we maintain an “800” telephone number and an Internet site for “New Product Suggestions” and receive, either directly or through our sales force, many ideas from our customers as to which types of presently unavailable parts the ultimate consumers are seeking.

We market our products to three groups of purchasers who in turn supply individual consumers and professional installers:

(i) Approximately 44% of our revenues are generated from sales to automotive aftermarket retailers (such as AutoZone, Advance Auto, and O’Reilly), local independent parts wholesalers and national general merchandise chain retailers. We sell some of our products to virtually all major chains of automotive aftermarket retailers;

(ii) Approximately 42% of our revenues are generated from sales to automotive parts distributors (such as Carquest and NAPA), which may be local, regional or national in scope, and which may also engage in retail sales; and

(iii) The balance of our revenues (approximately 14%) are generated from international sales and sales to special markets, which include, among others, mass merchants (such as Wal-Mart), salvage yards and the parts distribution systems of parts manufacturers.

We use a number of different methods to sell our products. Our more than 50 person direct sales force and sales support staff solicits purchases of our products directly from customers, as well as manages the activities of 10 independent manufacturers’ representative agencies. We use independent manufacturers’ representative agencies to help service existing automotive retail and automotive parts distribution customers, providing frequent on-site contact. We increase sales by securing new customers and by adding new product lines and expanding product selection within existing customers. For certain of our major customers, and our private label purchasers, we rely primarily upon the direct efforts of our sales force who, together with our marketing department and our executive officers, coordinate the more complex pricing and ordering requirements of these accounts.

Our sales efforts are not directed merely at selling individual products, but rather more broadly towards selling groups of related products that can be displayed on attractive Dorman-designed display systems, thereby maximizing each customer’s ability to present our product line within the confines of the available area.

We prepare a number of catalogs, application guides and training materials designed to describe our products and other applications as well as to train our customers’ salesmen in the promotion and sale of our products. Every two to three years we prepare a new master catalog which lists all of our products. The catalog is updated periodically through supplements and is available on our website.

We currently service more than 2,800 active accounts. During 2010, four customers (AutoZone, Advance Auto, O’Reilly and Genuine Parts Co.) each accounted for more than 10% and in the aggregate accounted for 55% of net sales. During 2009 and 2008, three customers (AutoZone, Advance Auto, and O’Reilly) each accounted for more than 10% of net sales and in the aggregate accounted for 39% and 40% of net sales, respectively.

5

Table of Contents

Substantially all of our products are manufactured to our specifications by third parties. Because numerous contract manufacturers are available to manufacture our products, we are not dependent upon the services of any one contract manufacturer or any small group of them. No one manufacturer supplies more than 10% of our products. In 2010, as a percentage of our total dollar volume of purchases, approximately 24% of our products were purchased from various suppliers throughout the United States and the balance of our products were purchased directly from vendors in a variety of foreign countries.

Once a new product has been identified, our engineering department produces detailed proprietary engineering drawings and prototypes which are used to solicit bids for manufacture from a variety of vendors in the United States and abroad. After a vendor is selected, tooling for a production run is produced by the vendor at our expense. A pilot run of the product is produced and subjected to rigorous testing by our engineering department and, on occasion, by outside testing laboratories and facilities in order to evaluate the precision of manufacture and the resiliency and structural integrity of the materials used. If acceptable, the product then moves into full production.

Packaging, Inventory and Shipping

Finished products are received at one or more of our facilities, depending on the type of part. It is our practice to inspect samples of shipments based upon vendor performance. If cleared, these shipments of finished parts are logged into our computerized production tracking systems and staged for packaging, if necessary.

We employ a variety of custom-designed packaging machines which include blister sealing, skin film sealing, clamshell sealing, bagging and boxing lines. Packaged product contains our label (or a private label), a part number, a universal packaging bar code suitable for electronic scanning, a description of the part and, if appropriate, installation instructions. Products are also sold in bulk to automotive parts manufacturers and packagers. Computerized tracking systems, mechanical counting devices and experienced workers combine to assure that the proper variety and numbers of parts meet the correct packaging materials at the appropriate places and times to produce the required quantities of finished products.

Completed inventory is stocked in the warehouse portions of our facilities and is stored and organized to facilitate the most efficient methods of retrieving product to fill customer orders. We strive to maintain a level of inventory to adequately meet current customer order demand with additional inventory to satisfy new customer orders and special programs. We maintain a “safety stock” of inventory to compensate for fluctuations in demand and delivery.

We ship our products from all of our locations by contract carrier, common carrier or parcel service. Products are generally shipped to the customer’s main warehouse for redistribution within their network. In certain circumstances, at the request of the customer, we ship directly to the customer’s stores either via smaller direct ship orders or consolidated store orders that are cross docked.

The replacement automotive parts industry is highly competitive. Various competitive factors affecting the automotive aftermarket are price, product quality, breadth of product line, range of applications and customer service. Substantially all of our products are subject to competition with similar products manufactured by other manufacturers of aftermarket automotive repair and replacement parts. Some of these competitors are divisions and subsidiaries of companies much larger than us, and possess a longer history of operations and greater financial and other resources than we do. Further, some of our private label customers also compete with us.

While we take steps to register our trademarks when possible, we believe that our business is not heavily dependent on such trademark registration. Similarly, while we actively seek patent protection for the products and improvements which we develop, we do not believe that patent protection is critical to the success of our business. Rather, the quality, price and availability of our products is critical to our success.

6

Table of Contents

At December 25, 2010, we had 1,185 employees worldwide, of whom 1,170 were employed full-time and 15 were employed part-time. Of these employees, 675 were engaged in production, inventory, or quality control, 158 were involved in engineering, product development and brand management, 107 were employed in sales and order entry, and the remaining 245 were devoted to administration, finance, legal, and strategic planning.

No domestic employees are covered by any collective bargaining agreement. Approximately 30 employees at our Swedish subsidiary are governed by a national union. We consider our relations with our employees to be generally good.

Our Internet address is www.dormanproducts.com. The information on this website is not and should not be considered part of this Form 10-K and is not incorporated by reference in this Form 10-K. This website is, and is only intended to be, for reference purposes only. We make available free of charge on our web site our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. In addition, we will provide, at no cost, paper or electronic copies of our reports and other filings made with the SEC. Requests should be directed to: Dorman Products, Inc. - Office of General Counsel, 3400 East Walnut Street, Colmar, Pennsylvania 18915.

In addition to the other information set forth in this report, you should carefully consider the following factors, which could materially affect our business, financial condition or future results. The risks described below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially affect our business, financial conditions or results of operations.

We May Lose Business to Competitors.

Competition within the automotive aftermarket parts business is intense. We compete in North America with both original equipment parts manufacturers and with companies that, like us, supply parts only to the automotive aftermarket. We expect such competition to continue. Our inability to compete successfully in our industry could cause us to lose customers.

Unfavorable Economic Conditions May Adversely Affect Our Business.

Adverse changes in economic conditions, including inflation, recession, or instability in the financial markets or credit markets may either lower demand for our products or increase our operational costs, or both. Such conditions may also materially impact our customers, suppliers and other parties with whom we do business. Our revenue will be adversely affected if demand for our products declines. The impact of unfavorable economic conditions may also impair the ability of our customers to pay for products they have purchased. As a result, reserves for doubtful accounts and write-offs of accounts receivables may increase and failure to collect a significant portion of amounts due on those receivables could have a material adverse effect on our results of operations and financial condition.

The Loss or Decrease in Sales Among One of Our Top Customers Could Have a Substantial Negative Impact on Our Sales and Operating Results.

A significant percentage of our sales has been, and will continue to be, concentrated among a relatively small number of customers. During 2010, four customers (AutoZone, Advance Auto, O’Reilly and Genuine Parts Co.) each accounted for more than 10% of net sales and in the aggregate accounted for 55% of net sales. During 2009 and 2008, three customers (AutoZone, Advance Auto, and O’Reilly) each accounted for more than 10% of net sales and in the aggregate accounted for 39% and 40% of net sales, respectively. We anticipate that this concentration of sales among customers will continue in the future. The loss of a significant customer or a substantial decrease in sales to such a customer could have a material adverse effect on our sales and operating results.

Customer Consolidation in the Automotive Aftermarket May Lead to Customer Contract Terms Less Favorable to Us Which May Negatively Impact Our Financial Results.

The automotive aftermarket has been consolidating over the past several years. As a result, many of our customers have grown larger and therefore have more leverage in the arms-length negotiations of agreements with us for the sale of our products.

7

Table of Contents

Customers may require us to provide extended payment terms and returns of slow moving product in order to obtain new or retain existing business. While we attempt to avoid or minimize such concessions, in some cases payment terms to customers have been extended and returns of product have exceeded historical levels. The product returns primarily affect our profit levels while payment terms extensions generally reduce operating cash flow and require additional capital to finance the business. We expect both of these trends to continue for the foreseeable future.

The Cancellation or Rescheduling of Orders May Cause Our Operating Results to Fluctuate.

The cancellation or rescheduling of orders may cause our operating results to fluctuate. Although we make every reasonable effort to maintain ongoing relationships with our customers, there is an ongoing risk that orders may be cancelled or rescheduled due to fluctuations in our customers’ business needs or overall market demand for our products. Additionally, although we serve more than 2,800 individual accounts, the cancellation or rescheduling of orders by larger customers may still have a material adverse effect on our operating results from time to time.

Our Business May be Negatively Impacted By Foreign Currency Fluctuations and Our Dependence on Foreign Suppliers.

In 2010, approximately 76% of our products were purchased from vendors in a variety of foreign countries. The products generally are purchased through purchase orders with the purchase price specified in U.S. dollars. Accordingly, we do not have exposure to fluctuations in the relationship between the dollar and various foreign currencies between the time of execution of the purchase order and payment for the product. To the extent that the dollar decreases in value relative to foreign currencies in the future, the price of the product in dollars for new purchase orders may increase.

The largest portion of our overseas purchases is from China. The value of the Chinese Yuan had been relatively constant relative to the U.S. dollar for approximately two years. However, since June 2010, it has increased approximately 3% relative to the U.S. Dollar. A continued increase in the value of the Yuan relative to the U.S. Dollar will likely result in an increase in the cost of products that we purchase from China.

As a result of the magnitude of our foreign sourcing, our business may be subject to risks, including the following:

| • | uncertainty caused by the elimination of import quotas and the possible imposition of additional quotas or antidumping or countervailing duties or other retaliatory or punitive trade measures; |

| • | imposition of duties, taxes and other charges on imports; |

| • | significant devaluation of the dollar against foreign currencies; |

| • | restrictions on the transfer of funds to or from foreign countries; |

| • | political instability, military conflict or terrorism involving the United States or any of the countries where our products are manufactured, which could cause a delay in transportation or an increase in costs of transportation, raw materials or finished product or otherwise disrupt our business operations; and |

| • | disease, epidemics and health-related concerns, such as swine flu, SARS or the mad cow or hoof and mouth disease outbreaks in recent years, which could result in closed factories, reduced workforces, scarcity of raw materials and scrutiny and embargoing of goods produced in infected areas. |

If these risks limit or prevent us from acquiring products from foreign suppliers or significantly increase the cost of our products, our operations could be seriously disrupted until alternative suppliers are found, which could negatively impact our business.

We Extend Credit to Our Customers Who May Be Unable to Pay In the Future.

We regularly extend credit to our customers. A significant percentage of our accounts receivable have been, and will continue to be concentrated among a relatively small number of automotive retailers and automotive parts distributors in the United States. Our five largest customers accounted for 78% and 76% of total accounts receivable as of December 25, 2010 and December 26, 2009, respectively. Management continually monitors the credit terms and credit limits of these and other customers. If any of these customers were unable to pay, our business and financial condition would be adversely affected.

8

Table of Contents

The Loss of a Key Vendor Could Lead to Increased Costs and Lower Profit Margins.

The majority of the products we sell are purchased from a number of foreign vendors. If any of our existing vendors fail to meet our needs, we believe that sufficient capacity exists in the open market to supply any shortfall that may result. Nevertheless, it is not always possible to replace a key vendor without a disruption in our operations and replacement of a significant vendor is often at higher prices.

Limited Shelf Space May Adversely Affect Our Ability to Expand Our Product Offerings.

Since the amount of space available to a retailer and other purchasers of our products is limited, our products compete with other automotive aftermarket products, some of which are entirely dissimilar and otherwise non-competitive (such as car waxes and engine oil), for shelf and floor space. No assurance can be given that additional space will be available in our customers’ stores to support the expansion of the number of products that we offer.

If We Do Not Continue to Develop New Products and Bring Them to Market, Our Business, Financial Condition and Results of Operations Could Be Materially Impacted.

The development and production of new products is often accompanied by design and production delays and related costs typically associated with the development and production of new products. While we expect and plan for such delays and related costs, we cannot predict with precision the time and expense required to overcome these initial problems so that the products comply with specifications. There is a risk that we may not be able to introduce or bring to full-scale production new products as quickly as we expected in our product introduction plans, which could have a material adverse effect on our business, financial condition, and results of operations.

An Increase in Patent Filings by Original Equipment Manufacturers Could Negatively Impact Our Ability to Develop New Products.

We have seen an increase in patent requests for new designs made by original equipment manufacturers. If original equipment manufacturers are able to obtain patents on new designs at a rate higher than historical levels, we could be restricted or prohibited from selling aftermarket products covered by such items until such patents expire, which could have an adverse impact on our business.

Quality Problems with Our Products Could Damage Our Reputation and Adversely Affect Our Business.

We have experienced, and in the future may experience, reliability, quality, or compatibility problems in products after their production and sale to customers. Product quality problems could result in damage to our reputation, loss of customers, a decrease in revenue, litigation, unexpected expenses, and a loss of market share. We have invested and will continue to invest in our engineering, design, and quality infrastructure in an effort to reduce and eventually eliminate these problems; however, there can be no assurance that we can successfully remedy all of these issues. To the extent we experience significant quality problems in the future our business and results of operations may be negatively impacted.

Loss of Third-Party Transportation Providers Upon Whom We Depend or Increases in Fuel Prices Could Increase Our Costs or Cause a Disruption in Our Operations.

We depend upon third-party transportation providers for delivery of our products to us and to our customers. Strikes, slowdowns, transportation disruptions or other conditions in the transportation industry, including, but not limited to, shortages of truck drivers, disruptions in rail service, decreases in ship building or increases in fuel prices, could increase our costs and disrupt our operations and our ability to service our customers on a timely basis.

We May Not Properly Execute, or Realize Anticipated Cost Savings or Benefits from, Our Ongoing Information Technology Initiatives.

Our success is partly dependent on properly executing, and realizing cost savings or other benefits from, our ongoing information technology initiatives. These initiatives are primarily designed to make us more efficient in the development, acquisition and distributions of our products, which is necessary in our highly competitive industry. These initiatives are often complex, and a failure to implement them properly may, in addition to not meeting projected cost savings or benefits, result in an interruption to our business functions.

9

Table of Contents

Unfavorable Results of Legal Proceedings Could Materially Adversely Affect Us.

We are subject to various legal proceedings and claims that have arisen out of the ordinary course of our business which are not yet resolved and additional claims may arise in the future. Although we currently believe that resolving all of these matters, individually or in the aggregate, will not have a material adverse impact on our financial position, legal claims and proceedings are subject to inherent uncertainty and our view on these matters may change in the future. Regardless of merit, litigation may be both time-consuming and disruptive to our operations and cause significant expense and diversion of management attention. Should we fail to prevail in certain matters, we may be faced with significant monetary damages or injunctive relief that would materially adversely affect our business and financial condition and operating results.

We Have No History of Paying Dividends.

We do not intend to pay cash dividends for the foreseeable future. Rather, we intend to retain our earnings, if any, for the operation and expansion of our business.

Dorman’s Officers, Directors and Their Family Members Control the Company.

As of March 1, 2011, Steven L. Berman, our Chairman and Chief Executive Officer and director of Dorman Products, Inc., and his family members beneficially own approximately 43% of the outstanding Common Stock and are able to elect the Board of Directors, have a controlling influence over the outcome of most corporate actions requiring shareholder approval (including certain fundamental transactions) and the affairs of the Company.

Our Success Depends on the Efforts of Our Management Team.

The success of our business will continue to be dependent upon Steven L. Berman, Chairman of the Board and Chief Executive Officer, Secretary and Treasurer, other executive officers and key employees and our ability to attract and retain other skilled managers. The loss of the services of any of these individuals for an extended period of time could have a material adverse effect on our business.

We May be Exposed to Certain Regulatory and Financial Risks Related to Climate Change.

Climate change is receiving increasing attention worldwide. Some scientists, legislators and others attribute global warming to increased levels of greenhouse gases, including carbon dioxide, which has led to significant legislative and regulatory efforts to limit greenhouse gas emissions.

There are a number of pending legislative and regulatory proposals to address greenhouse gas emissions. For example, in June 2009 the U.S. House of Representatives passed the American Clean Energy and Security Act that would phase-in significant reductions in greenhouse gas emissions if enacted into law. The U.S. Senate is considering a different bill, and it is uncertain whether, when and in what form a federal mandatory carbon dioxide emissions reduction program may be adopted. Similarly, certain countries have adopted the Kyoto Protocol. These actions could increase costs associated with our operations, including costs for components used in the manufacture of our products and freight costs.

Because it is uncertain what laws and regulations will be enacted, we cannot predict the potential impact of such laws and regulations on our future consolidated financial condition, results of operations or cash flows.

Healthcare Reform Legislation could have an Adverse Impact on our Business.

The recently enacted Patient Protection and Affordable Care Act (the “Patient Act”) as well as other healthcare reform legislation being considered by Congress and state legislatures may have an impact on our business. While we are currently evaluating the potential effects of the Patient Act on our business, the impact could be extensive and may increase our employee healthcare-related costs. While the significant costs of the recent healthcare legislation enacted will occur after 2013 due to provisions of the legislation being phased in over time, changes to our healthcare costs structure could have a significant, material adverse impact on our business.

10

Table of Contents

Executive Officers of the Registrant.

The following table sets forth certain information with respect to our executive officers:

| Name | Age | Position with the Company | ||

| Mathias J. Barton | 51 | Co-President | ||

| Joseph M. Beretta | 56 | Co-President | ||

| Steven L. Berman | 51 | Chairman of the Board, Chief Executive Officer, Secretary-Treasurer, and Director | ||

| Fred V. Frigo | 54 | Senior Vice President, Operations | ||

| Thomas J. Knoblauch | 54 | Vice President, General Counsel and Assistant Secretary | ||

| Matthew S. Kohnke | 39 | Vice President, Chief Financial Officer |

Mathias J. Barton joined the Company in November 1999 as Senior Vice President, Chief Financial Officer. He became co-President of the Company in February, 2011. Prior to joining the Company, Mr. Barton was Senior Vice President and Chief Financial Officer of Central Sprinkler Corporation, a manufacturer and distributor of automatic fire sprinklers, valves and component parts. From May 1989 to September 1998, Mr. Barton was employed by Rapidforms, Inc., most recently as Executive Vice President and Chief Financial Officer. He is a graduate of Temple University.

Joseph M. Beretta joined the Company in January 2004 as Senior Vice President, Product. He became co-President of the Company in February, 2011. Prior to joining the Company, Mr. Beretta was employed by Cardone Industries, Inc., most recently as its Chief Operating Officer. Cardone is a re-manufacturer and supplier of automotive replacement parts. He is a graduate of Oral Roberts University.

Steven L. Berman is Chairman of the Board, Chief Executive Officer, President, Chief Operating Officer, Secretary-Treasurer and a Director of the Company. Mr. Berman became Chairman and Chief Executive Officer in January, 2011. He previously held the positions of President, Secretary-Treasurer and a director of the Company since October 24, 2007. He became Chairman of the Board and Chief Executive Officer on January 30, 2011. Prior to October 24, 2007, he served as Executive Vice President, Secretary-Treasurer and a director of the Company since its inception in 1978. Since the inception of the Company in October 1978 until October 25, 2007, Mr. Berman served as Executive Vice President. He attended Temple University.

Fred V. Frigo joined the Company in March 1997 as Director, Operations and was named Senior Vice President, Operations in September 2003. Prior to joining the Company, Mr. Frigo was the Plant Manager for Cooper Industries (Federal Mogul), where he was responsible for their Wagner Brake Plant in Boston and following that the Wagner Lighting Operations in Boyertown, Pennsylvania. He is a graduate of Elmhurst College.

Thomas J. Knoblauch joined the Company in April 2005 as Vice President and General Counsel. In May 2005, Mr. Knoblauch was appointed Assistant Secretary. Prior to joining the Company he was Corporate Counsel at SunGard Data Systems, Inc. from 1996 to 2000 and General Counsel at Rosenbluth International, Inc. from 2000 to May, 2005. He is a graduate of Widener University, St. Joseph’s University, the Widener University School of Law, and the Temple University Beasley School of Law Graduate Tax Program. Mr. Knoblauch is a member of both the Pennsylvania and New York Bar.

Matthew S. Kohnke joined Dorman Products in May 2002 as Vice President - Corporate Controller. He became Vice President and Chief Financial Officer of the Company in February, 2011. Prior to joining the Company, Mr. Kohnke worked for Arthur Andersen LLP, beginning as an intern in January 1992 and advancing to manager in the Audit and Business Advisory practice. He is a graduate of Villanova University.

We have adopted a written code of ethics, “Our Values and Standards of Business Conduct,” which is applicable to all of our directors, officers and employees, including our chief executive officer, chief financial officer, and principal accounting officer and controller and other executive officers identified pursuant to this Item 10 (collectively, the “Selected Officers”). In accordance with the SEC’s rules and regulations a copy of the code is posted on our website www.dormanproducts.com. We intend to disclose any changes in or waivers from our code of ethics applicable to any Selected Officer or director on our website at www.dormanproducts.com.

11

Table of Contents

Item 1B.

Item 1B. Unresolved Staff Comments. None

Facilities

We currently have 13 warehouse and office facilities located throughout the United States, Canada, Sweden, China and Korea. Two of these facilities are owned and the remainders are leased. Our headquarters and principal warehouse facilities are as follows:

| Location | Description | |

| Colmar, PA | Corporate Headquarters and Warehouse and office - 339,500 sq. ft. (leased) (1) | |

| Warsaw, KY | Warehouse and office - 362,000 sq. ft. (owned) (2) | |

| Portland, TN | Warehouse and office - 414,043 sq. ft. (leased) | |

| Louisiana, MO | Warehouse and office - 90,000 sq. ft. (owned) |

| (1) | We lease the Colmar facility from a partnership of which Steven L. Berman, Chairman of the Board and Chief Executive Officer of the Company, and his family members are partners. Under the lease agreement we paid rent of $4.19 per square foot ($1.4 million per year) in 2010. The rents payable will be adjusted on January 1 of each year to reflect annual changes in the Consumer Price Index for All Urban Consumers - U.S. City Average, All Items. The current lease agreement expires in December, 2012. In the opinion of management, the terms of this lease are no less favorable than those which could have been obtained from an unaffiliated party. |

| (2) | In October, 2010, we began construction of a 150,000 square foot expansion of our Warsaw, KY, warehouse facility. The project is expected to be completed in April, 2011. |

We are a party to or otherwise involved in legal proceedings that arise in the ordinary course of business, such as various claims and legal actions involving contracts, competitive practices, trademark and patent rights, product liability claims and other matters arising out of the conduct of our business. In the opinion of management, none of the actions, individually or in the aggregate, would likely have a material financial impact on the Company.

Item 4. (Removed and Reserved)

12

Table of Contents

PART II

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

Our shares of common stock are traded publicly on the NASDAQ Global Select Stock Market under the trading symbol DORM. At March 1, 2011 there were 169 holders of record of common stock, representing more than 1,400 beneficial owners. The last price for our common stock on March 1, 2011, as reported by NASDAQ, was $33.08 per share. Since our initial public offering, we have paid no cash dividends. We do not presently contemplate paying any such dividends in the foreseeable future. The range of high and low sales prices for our common stock for each quarterly period of 2010 and 2009 are as follows:

| 2010 | 2009 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| First Quarter |

$ | 20.35 | $ | 14.88 | $ | 13.60 | $ | 6.12 | ||||||||

| Second Quarter |

26.00 | 18.87 | 14.44 | 7.90 | ||||||||||||

| Third Quarter |

28.63 | 17.84 | 17.25 | 12.76 | ||||||||||||

| Fourth Quarter |

49.32 | 27.29 | 16.65 | 12.70 | ||||||||||||

For the information regarding our compensation plans, see Item 12, Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

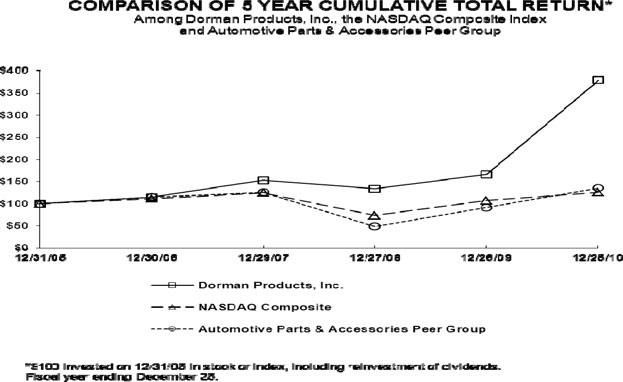

Stock Performance Graph. Below is a line graph comparing the cumulative total shareholder return on our common stock with the cumulative total shareholder return on the Automotive Parts & Accessories Peer Group of the Hemscott Group Index and the NASDAQ Market Index for the period from December 31, 2005 to December 25, 2010. The Automotive Parts & Accessories Peer Group is comprised of 40 public companies and the information was furnished by Research Data Group, Inc. The graph assumes $100 invested on December 31, 2005 in our common stock and each of the indices, and that the dividends were reinvested when and as paid. In calculating the cumulative total shareholder returns, the companies included are weighted according to the stock market capitalization of such companies.

13

Table of Contents

Stock Repurchases

Share Repurchase Program. On February 22, 2008, we announced that our Board of Directors authorized the repurchase of up to 500,000 shares of our outstanding common stock. Under this program, share repurchases may be made from time to time depending upon market conditions, share price and availability, and other factors at our discretion. Repurchases will take place in open market transactions or in privately negotiated transactions in accordance with applicable laws. We purchased 3,600 shares under the plan since its inception, all of which were purchased during fiscal year ended December 26, 2009. No shares were purchased under the plan during fiscal year ended December 25, 2010.

In addition, we periodically repurchase shares from our 401(k) Plan. Shares are generally purchased from our 401(k) Plan when participants elect to sell units as permitted by the Plan or to leave the Plan upon retirement, termination or other reasons. We purchased 50,266 shares from the 401(k) Plan during the fiscal year ended December 25, 2010.

During the last three months of fiscal year ended December 25, 2010, we purchased shares of our Common Stock as follows:

| Period |

Total Number of Shares Purchased (1) |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Plans or Programs |

||||||||||||

| September 26, 2010 through October 23, 2010 |

1,961 | $ | 31.86 | — | — | |||||||||||

| October 24, 2010 through November 20, 2010 |

— | — | — | — | ||||||||||||

| November 21, 2010 through December 25, 2010 |

12,190 | $ | 41.96 | — | — | |||||||||||

| Total |

14,151 | $ | 40.56 | — | — | |||||||||||

| (1) | All of the shares indicated in the above table were purchased from our 401(k) Plan. This table does not include shares tendered to satisfy the exercise price in connection with cashless exercises of employee stock options or shares tendered to satisfy tax withholding obligations in connection with equity awards. |

In February 2009, the Company filed a registration statement to register 1,000,000 shares of its common stock issuable upon the exercise of outstanding stock options and options to be issued, if any, under the Company’s Amended and Restated Incentive Stock Plan. Prior to this time, the Company’s reserve of registered shares became depleted and the Company issued unregistered shares upon exercise of options. Upon discovery of this matter, the Company offered former option holders the ability to rescind these option exercise transactions where registered shares were not actually available upon exercise for all transactions which occurred within the relevant statute of limitations period. The Company opted for rescission in lieu of investigating the availability of exemptions from registration, given the time and expense associated therewith. This rescission offer was effected as a private placement which was exempt from registration pursuant to Section 4(2) of the Securities Act of 1933, as amended.

Item 6. Selected Financial Data.

| (in thousands, except per share data) | 2010(a) | 2009 | 2008 (b) | 2007(c) | 2006(d) | |||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Net sales |

$ | 455,716 | $ | 377,378 | $ | 342,325 | $ | 327,725 | $ | 295,825 | ||||||||||

| Income from operations |

74,882 | 43,669 | 28,404 | 33,972 | 26,770 | |||||||||||||||

| Net income |

46,138 | 26,495 | 17,813 | 19,193 | 13,799 | |||||||||||||||

| Earnings per share |

||||||||||||||||||||

| Basic |

$ | 2.60 | $ | 1.50 | $ | 1.01 | $ | 1.08 | $ | 0.78 | ||||||||||

| Diluted |

$ | 2.55 | $ | 1.47 | $ | 0.99 | $ | 1.06 | $ | 0.76 | ||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Total assets |

323,159 | 257,402 | 243,422 | 230,655 | 217,758 | |||||||||||||||

| Working capital |

218,935 | 173,153 | 160,237 | 138,288 | 126,804 | |||||||||||||||

| Long-term debt |

— | 266 | 15,356 | 8,942 | 20,596 | |||||||||||||||

| Shareholders’ equity |

263,153 | 215,335 | 187,844 | 173,858 | 153,843 | |||||||||||||||

| (a) | Results for 2010 include a $1.0 million write down for intangible asset impairment ($0.03 per share). |

| (b) | Results for 2008 include a $0.7 million reduction ($0.04 per share) in income tax expense as a result of the disposition of our Canadian subsidiary. |

14

Table of Contents

| (c) | Results for 2007 include a $1.8 million reduction ($1.1 million after tax or $0.06 per share) in our vacation liability as a result of a change in our policy, a $0.4 million write down for goodwill impairment ($0.02 per share), and establishment of a valuation reserve of deferred tax assets totaling $0.6 million ($0.03 per share). |

| (d) | Results for 2006 include a $3.2 million non-cash write-down for goodwill impairment ($2.9 million or $0.16 per share) and the write-off of deferred tax benefits ($0.3 million or $0.02 per share). |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Cautionary Statement Regarding Forward Looking Statements

Certain statements in this document constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. While forward-looking statements sometimes are presented with numerical specificity, they are based on various assumptions made by management regarding future circumstances over many of which the Company has little or no control. Forward-looking statements may be identified by words including “anticipate,” “believe,” “estimate,” “expect,” and similar expressions. The Company cautions readers that forward-looking statements, including, without limitation, those relating to future business prospects, revenues, working capital, liquidity, and income, are subject to certain risks and uncertainties that would cause actual results to differ materially from those indicated in the forward-looking statements. Factors that could cause actual results to differ from forward-looking statements include but are not limited to competition in the automotive aftermarket industry, unfavorable economic conditions, loss of key suppliers, loss of third-party transportation providers, an increase in patent filings by original equipment manufacturers, quality problems, delay in the development and design of new products, space limitations on our customers’ shelves, concentration of the Company’s sales and accounts receivable among a small number of customers, the impact of consolidation in the automotive aftermarket industry, foreign currency fluctuations, dependence on senior management and other risks and factors identified from time to time in the reports the Company files with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. For additional information concerning factors that could cause actual results to differ materially from the information contained in this report, reference is made to the information in “Part I, Item 1A, Risk Factors.”

Overview

We are a supplier of automotive replacement parts and fasteners and service line products primarily for the automotive aftermarket. We market approximately 122,000 different automotive replacement parts (including brake parts), fasteners and service line products manufactured to our specifications. Approximately 21% of our parts and 66% of our net sales consists of parts and fasteners that were original equipment dealer “exclusive” items at the time of their introduction. Original equipment dealer “exclusive” parts are those which were traditionally available to consumers only from original equipment manufacturers or salvage yards and include, among other parts, intake manifolds, exhaust manifolds, oil cooler lines, window regulators, radiator fan assemblies, power steering pulleys and harmonic balancers. Fasteners include such items as oil drain plugs and wheel lug nuts. Approximately 85% of our products are sold under our brand names and the remainder is sold for resale under customers’ private labels, other brands or in bulk. Our products are sold primarily in the United States through automotive aftermarket retailers (such as AutoZone, Advance Auto and O’Reilly), national, regional and local warehouse distributors (such as Carquest and NAPA) and specialty markets and salvage yards. Through our Scan-Tech subsidiary, we are increasing our international distribution of automotive replacement parts, with sales into Europe, the Middle East and Asia. We are increasing distribution of automotive replacement parts in Canada through our Dorman Canada business unit.

We generate over 90% of our revenues from customers in the North American automotive aftermarket. The aftermarket has benefited from some of the factors affecting the general economy including the recent recession, tighter credit and higher unemployment. These conditions as well as others have resulted in a recent decline in new vehicle sales and the increase in the average age of vehicles on the road. These trends will increase the number of automotive aftermarket parts that need replacing. Another important statistic impacting our market is total miles driven. Total U.S. miles driven were up slightly in 2009 and 2010 after being down in each of the two prior years. We believe that the combination of these factors accounted for a portion of our 2009 and 2010 sales growth.

While the overall automotive aftermarket in which we compete has benefited from the conditions mentioned above; our customer base has been consolidating over the past several years. As a result, our customers regularly seek more favorable pricing, product returns and extended payment terms when negotiating with us. While we attempt to avoid or minimize such concessions, in some cases pricing concessions have been made, customer payment terms have been extended and returns of product have exceeded historical levels. The product returns and more favorable pricing primarily affect our profit levels while terms extensions generally reduce operating cash flow and require additional capital to finance the business. We expect these trends to continue for the foreseeable future. Gross profit margins declined in each of the three years prior to 2009 as a result of this pricing pressure. During 2009 and 2010 we were able to offset the negative impact of the pricing pressures and mix shift by reducing product warranty and return costs and by lowering freight and material costs. As a result, our 2009 and 2010 gross profit margins improved despite the negative factors impacting the automotive aftermarket mentioned above. We expect our customers to continue to exert pressure on our margins. We have increased our focus on efficiency improvements and product cost reduction initiatives to offset the impact of further price pressures.

15

Table of Contents

In addition, we are relying on new product development as a way to offset some of these customer demands and as our primary vehicle for growth. As such, new product development is a critical success factor for us. We have invested heavily in resources necessary for us to increase our new product development efforts and to strengthen our relationships with our customers. These investments are primarily in the form of increased product development resources and awareness programs and customer service improvements. This has enabled us to provide an expanding array of new product offerings and grow our revenues.

We may experience significant fluctuations from quarter to quarter in our results of operations due to the timing of orders placed by our customers. Generally, the second and third quarters have the highest level of customer orders, but the introduction of new products and product lines to customers may cause significant fluctuations from quarter to quarter.

We operate on a fifty-two, fifty-three week period ending on the last Saturday of the calendar year. The fiscal years ended December 25, 2010, December 26, 2009, and December 27, 2008 are all fifty-two week periods.

Asset Write Down

During the fourth quarter of 2010, we determined that certain acquired intangible assets were impaired. As such, we recorded an impairment charge of $1.0 million in 2010 to fully write-off these assets.

Results of Operations

The following table sets forth, for the periods indicated, the percentage of net sales represented by certain items in our Consolidated Statements of Operations:

| Percentage of Net Sales | ||||||||||||

| Year Ended | ||||||||||||

| December 25, 2010 | December 26, 2009 | December 27, 2008 | ||||||||||

| Net Sales |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cost of goods sold |

62.1 | 65.1 | 67.8 | |||||||||

| Gross profit |

37.9 | 34.9 | 32.2 | |||||||||

| Selling, general and administrative expenses |

21.5 | 23.3 | 23.9 | |||||||||

| Income from operations |

16.4 | 11.6 | 8.3 | |||||||||

| Interest expense, net |

— | 0.1 | 0.3 | |||||||||

| Income before taxes |

16.4 | 11.5 | 8.0 | |||||||||

| Provision for taxes |

6.3 | 4.5 | 2.8 | |||||||||

| Net Income |

10.1 | % | 7.0 | % | 5.2 | % | ||||||

Fiscal Year Ended December 25, 2010 Compared to Fiscal Year Ended December 26, 2009

Net sales increased 20.8% to $455.7 million in 2010 from $377.4 million in 2009. Our revenue growth was driven by overall strong demand for our products and higher new product sales.

Cost of goods sold, as a percentage of net sales, decreased to 62.1% in 2010 from 65.1% in the same period last year. The decrease is primarily due to a reduction in certain material costs along with lower defective return costs.

Selling, general and administrative expenses in 2010 increased 11.2% to $98.0 million from $88.1 million in 2009. The spending increase is the result of higher variable costs related to our sales increase, increased new product development spending and a $1.0 million charge to write off certain intangible assets.

Interest expense, net, decreased to $0.2 million in 2010 from $0.3 million in 2009 due to lower borrowing levels.

Our effective tax rate decreased to 38.2% in 2010 from 38.8% in the prior year. The decrease was the result of lower provisions for state income taxes in 2010.

16

Table of Contents

Fiscal Year Ended December 26, 2009 Compared to Fiscal Year Ended December 27, 2008

Net sales increased 10.2% to $377.4 million in 2009 from $342.3 million in 2008. Revenues before the impact of currency exchange and the sale of our Canadian subsidiary were up 11.4% over the prior year. Our revenue growth was driven by overall strong demand for our products and higher new product sales.

Cost of goods sold, as a percentage of net sales, decreased to 65.1% in 2009 from 67.8% in the same period last year. The increase was the result of lower warranty and product return costs along with a reduction in freight expenses and certain material costs.

Selling, general and administrative expenses in 2009 increased 7.7% to $88.1 million from $81.8 million in 2008. The spending increase was the result of higher variable costs related to our sales increase as well as increased new product development spending and higher incentive compensation expense due to higher earnings levels.

Interest expense, net, decreased to $0.3 million in 2009 from $0.9 million in 2008 due to lower borrowing levels and lower interest rates.

Our effective tax rate increased to 38.8% in 2009 from 35.2% in the prior year. The increase was the result of a non-recurring $0.7 million tax benefit realized upon the disposition of our Canadian subsidiary in 2008 and higher provisions for state income taxes in 2009.

Liquidity and Capital Resources

Historically, we have financed our growth through a combination of cash flow from operations, accounts receivable sales programs provided by certain customers and through the issuance of senior indebtedness through our bank credit facility and senior note agreements. At December 25, 2010, working capital was $218.9 million, and shareholders’ equity was $263.2 million. At December 25, 2010, we had no long-term debt or borrowings under our revolving credit facility. Cash and cash equivalents as of December 25, 2010 was $30.5 million.

Over the past several years we have continued to extend payment terms to certain customers as a result of customer requests and market demands. These extended terms have resulted in increased accounts receivable levels and significant uses of cash flow. We participate in accounts receivable sales programs with several customers which allow us to sell our accounts receivable on a non-recourse basis to financial institutions to offset the negative cash flow impact of these payment terms extensions. As of December 25, 2010 and December 26, 2009, we sold $77.1 million and $55.9 million in accounts receivable, respectively, under these programs and removed them from our balance sheets based upon standard payment terms. We expect continued pressure to extend our payment terms for the foreseeable future. Further extensions of customer payment terms will result in additional uses of cash flow or increased costs associated with the sale of accounts receivable.

We have a $30.0 million revolving credit facility which expires in June 2013. Borrowings under the facility are on an unsecured basis with interest at rates ranging from LIBOR plus 100 basis points to LIBOR plus 250 basis points based upon the achievement of certain benchmarks related to the ratio of funded debt to EBITDA. The interest rate at December 25, 2010 was LIBOR plus 100 basis points (1.26%). There were no borrowings under the facility as of December 25, 2010. Letters of credit outstanding under the facility as of December 25, 2010 amounted to $2.0 million. We had approximately $28.0 million available under the facility at December 25, 2010. The loan agreement also contains covenants, the most restrictive of which pertain to net worth and the ratio of debt to EBITDA. As of December 25, 2010, the Company was in compliance with the financial covenants contained in the loan agreement.

Off-Balance Sheet Arrangements

Our business activities do not include the use of unconsolidated special purpose entities, and there are no significant business transactions that have not been reflected in the accompanying financial statements.

17

Table of Contents

Contractual Obligations and Commercial Commitments

We have future obligations for future minimum rental and similar commitments under noncancellable operating leases as well as contingent obligations related to outstanding letters of credit. These obligations as of December 25, 2010 are summarized in the tables below (in thousands):

| Payments Due by Period | ||||||||||||||||||||

| Contractual Obligations |

Total | Less than 1 year | 1-3 years | 4-5 years | After 5 years | |||||||||||||||

| Operating leases |

$ | 11,948 | $ | 3,236 | $ | 4,836 | $ | 2,374 | $ | 1,502 | ||||||||||

| Construction contracts |

4,354 | 4,354 | — | — | — | |||||||||||||||

| $ | 16,302 | $ | 7,590 | $ | 4,836 | $ | 2,374 | $ | 1,502 | |||||||||||

| Amount of Commitment Expiration Per Period | ||||||||||||||||||||

| Other Commercial Commitments |

Total

Amount Committed |

Less than 1 year | 1-3 years | 4-5 years | After 5 years | |||||||||||||||

| Letters of Credit |

$ | 1,995 | $ | — | $ | 1,995 | $ | — | $ | — | ||||||||||

| $ | 1,995 | $ | — | $ | 1,995 | $ | — | $ | — | |||||||||||

The Company has excluded from the table above unrecognized tax benefits due to the uncertainty of the amount and period of payment. As of December 25, 2010, the Company has gross unrecognized tax benefits of $2.5 million (see Note 8 to the consolidated financial statements).

We reported a net source of cash from our operating activities of $30.7 million in the year ended December 25, 2010. Net income, depreciation and a $17.8 million increase in accounts payable were the primary sources of operating cash flow. Accounts payable increased primarily as a result of higher inventory levels and the timing of payments to our suppliers. Accounts receivable and inventory were the primary uses of cash. Accounts receivable increased $13.7 million due primarily to higher sales levels. Inventory increased $30.1 million due to the sales growth and increases in safety stock levels.

Investing activities used $11.5 million of cash in 2010 primarily as a result of additions to property, plant and equipment. Capital spending in 2010 consisted of tooling associated with new products, upgrades to information systems and scheduled equipment replacements. In the third quarter of 2010, we began a project to replace our enterprise resource planning system. This project is expected to cost approximately $9.5 million in software and installation services over the next 3 years of which $1.9 million was spent in 2010. No disruption to our operations is anticipated. In addition, we are expanding our distribution facility located in Warsaw, Kentucky. The total cost of this expansion will be approximately $9.0 million, of which $1.5 million was spent in 2010.

Financing activities provided $0.5 million of cash in the year ended December 25, 2010, primarily related to the net effect of stock option activity and the repurchase of common stock from our 401(k) plan during 2010.

Based on our current operating plan, we believe that our sources of available capital are adequate to meet our ongoing cash needs for at least the next twelve months.

Foreign Currency Fluctuations

In 2010, approximately 76% of our products were purchased from vendors in a variety of foreign countries. The products generally are purchased through purchase orders with the purchase price specified in U.S. dollars. Accordingly, we do not have exposure to fluctuations in the relationship between the dollar and various foreign currencies between the time of execution of the purchase order and payment for the product. To the extent that the dollar decreases in value relative to foreign currencies in the future, the price of the product in dollars for new purchase orders may increase.

The largest portion of our overseas purchases is from China. The value of the Chinese Yuan had been relatively constant relative to the U.S. dollar for two years. However, since June 2010, it has increased approximately 3% relative to the U.S. Dollar. A continued increase in the value of the Yuan relative to the U.S. Dollar will likely result in an increase in the cost of products that we purchase from China.

18

Table of Contents

Impact of Inflation

The overall impact of inflation has not resulted in a significant change in labor costs or the cost of general services utilized. During 2008 we experienced significant increases in the cost of materials and transportation costs as a result of commodity price increases and weakness in the U.S. Dollar. The upward pressure on materials and transportation costs eased in 2009 as the U.S. economy weakened. We were able to offset the 2008 cost increases with selling price increases and certain cost saving measures; however, we may not be able to do so in the future. We will attempt to offset further cost increases by passing along selling price increases to customers, through the use of alternative suppliers and by resourcing purchases to other countries. However there can be no assurance that we will be successful in these efforts.

Related-Party Transactions

We have a noncancelable operating lease for our primary operating facility from a partnership in which Steven L. Berman, our Chairman and Chief Executive Officer, and his family members are partners. Total rental payments each year to the partnership under the lease arrangement were $1.4 million in 2010, 2009 and 2008. Our Audit Committee is responsible for reviewing and approving all related party transactions. In the opinion of our Audit Committee, the terms and rates of this lease are no less favorable than those which could have been obtained from an unaffiliated party.

Critical Accounting Policies

Our discussion and analysis of our financial condition and results of operations are based upon the consolidated financial statements, which have been prepared in accordance with U.S. generally accepted accounting principles. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities and the reported amounts of revenues and expenses. We regularly evaluate our estimates and judgments, including those related to revenue recognition, bad debts, customer credits, inventories, goodwill and income taxes. Estimates and judgments are based upon historical experience and on various other assumptions believed to be accurate and reasonable under the circumstances. Actual results may differ materially from these estimates under different assumptions or conditions. We believe the following critical accounting policies affect our more significant estimates and judgments used in the preparation of our consolidated financial statements.

Allowance for Doubtful Accounts. The preparation of our financial statements requires us to make estimates of the collectability of our accounts receivable. We specifically analyze accounts receivable and historical bad debts, customer creditworthiness, current economic trends and changes in customer payment patterns when evaluating the adequacy of the allowance for doubtful accounts. A significant percentage of our accounts receivable have been, and will continue to be, concentrated among a relatively small number of automotive retailers and warehouse distributors in the United States. Our five largest customers accounted for 78% and 76% of net accounts receivable as of December 25, 2010 and December 26, 2009, respectively. A bankruptcy or financial loss associated with a major customer could have a material adverse effect on our sales and operating results.

Revenue Recognition and Allowance for Customer Credits. Revenue is recognized from product sales when goods are shipped, title and risk of loss have been transferred to the customer and collection is reasonably assured. We record estimates for cash discounts, product returns and warranties, discounts and promotional rebates in the period of the sale (“Customer Credits”). The provision for Customer Credits is recorded as a reduction from gross sales and reserves for Customer Credits are shown as a reduction of accounts receivable. Amounts billed to customers for shipping and handling are included in net sales. Costs associated with shipping and handling are included in cost of goods sold. Actual Customer Credits have not differed materially from estimated amounts for each period presented.

Excess and Obsolete Inventory Reserves. We must make estimates of potential future excess and obsolete inventory costs. We provide reserves for discontinued and excess inventory based upon historical demand, forecasted usage, estimated customer requirements and product line updates. We maintain contact with our customer base in order to understand buying patterns, customer preferences and the life cycle of our products. Changes in customer requirements are factored into the reserves as needed.

Goodwill. We employ a market comparable approach in conducting our annual impairment tests. Earnings multiples of 5.75 to 6.0 times EBITDA were used when conducting these tests in 2010. See Note 1 of the Notes to Consolidated Financial Statements in this report.

19

Table of Contents