Attached files

| file | filename |

|---|---|

| 8-K - Frontier Communications Parent, Inc. | c64565_8-k.htm |

Exhibit 99.1

Investor Presentation

March 2011

2

Safe Harbor Statement

Forward-Looking Language

This document contains forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the statements.

Statements

that are not historical facts are forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Words such as “believe,”

“anticipate,” “expect” and

similar expressions are intended to identify forward-looking statements. Forward-looking statements (including oral representations) are only predictions or statements of

current plans, which we review continuously. Forward-looking

statements may differ from actual future results due to, but not limited to, and our future results may be materially affected by,

potential risks or uncertainties. You should understand that it is not possible to predict or identify all potential

risks or uncertainties. You should understand that it is not possible to predict all

potential risks or uncertainties. We note the following as a partial list: our ability to successfully

integrate the operations of the acquired business into Frontier’s existing operations; the

risk that the growth opportunities and cost synergies from the transaction may not be fully realized or may take longer to realize than expected; our indemnity

obligation to Verizon

for taxes which may be imposed upon them as a result of changes in ownership of our stock may discourage, delay or prevent a third party from acquiring control of us during the

two-year period ending July 2012 in a transaction

that stockholders might consider favorable; the effects of increased expenses incurred due to activities related to the transaction

and the integration of the acquired business; our ability to maintain relationships with customers, employees or suppliers;

the effects of greater than anticipated competition

requiring new pricing, marketing strategies or new product or service offerings and the risk that we will not respond on a timely or profitable basis; reductions in the number of our

access lines that

cannot be offset by increases in HSI subscribers and sales of other products and services; the effects of ongoing changes in the regulation of the

communications industry as a result of federal and state legislation and regulation, or changes in the enforcement

or interpretation of such legislation and regulation; the effects of

changes in the availability of federal and state universal funding to us and our competitors; the effects of competition from cable, wireless and other wireline carriers; our ability to

adjust successfully to changes in the communications industry and to implement strategies for growth; adverse changes in the credit markets or in the ratings given to our debt

securities by nationally accredited ratings organizations, which could limit

or restrict the availability, or increase the cost, of financing; continued reductions in switched access

revenues as a result of regulation, competition or technology substitutions; our ability to effectively manage service quality in our territories and

meet mandated service quality

metrics; our ability to successfully introduce new product offerings, including our ability to offer bundled service packages on terms that are both profitable to us and attractive to

customers; changes in accounting policies

or practices adopted voluntarily or as required by generally accepted accounting principles or regulations; our ability to effectively

manage our operations, operating expenses and capital expenditures, and to repay, reduce or refinance our debt; the effects

of changes in both general and local economic

conditions on the markets that we serve, which can affect demand for our products and services, customer purchasing decisions, collectability of revenues and required levels of

capital expenditures related

to new construction of residences and businesses; the effects of customer bankruptcies and home foreclosures, which could result in difficulty in

collection of revenues and loss of customers; the effects of technological changes and competition on our capital

expenditures and product and service offerings, including the

lack of assurance that our network improvements will be sufficient to meet or exceed the capabilities and quality of competing networks; the effects of increased medical, retiree

and pension

expenses and related funding requirements; changes in income tax rates, tax laws, regulations or rulings, or federal or state tax assessments; the effects of state

regulatory cash management practices that could limit our ability to transfer cash among

our subsidiaries or dividend funds up to the parent company; our ability to successfully

renegotiate union contracts expiring in 2011 and thereafter; declines in the value of our pension plan assets, which would require us to make increased contributions

to the

pension plan in 2011 and beyond; limitations on the amount of capital stock that we can issue to make acquisitions or to raise additional capital until July 2012; our ability to pay

dividends on our common shares, which may be affected by our

cash flow from operations, amount of capital expenditures, debt service requirements, cash paid for income taxes

and liquidity; the effects of any unfavorable outcome with respect to any current or future legal, governmental or regulatory proceedings, audits

or disputes; and the effects of

severe weather events such as hurricanes, tornados, ice storms or other natural or man-made disasters. These and other uncertainties related to our business

are described in greater

detail in our filings with the Securities and Exchange Commission, including our reports on Forms 10-K and 10-Q, and the foregoing information should be read in conjunction with these filings. We undertake no obligation

to publicly update or revise any forward-looking statements or to make any other forward-looking statement, whether as a result of new information, future events or otherwise unless required to do so by securities laws.

3

Non-GAAP Financial Measures

Non-GAAP Financial Measures

The Company uses certain non-GAAP financial measures in evaluating its performance. These include free cash flow, EBITDA or “operating cash flow”, which we define as operating income

plus

depreciation and amortization (“EBITDA”), and Adjusted EBITDA; a reconciliation of the differences between EBITDA and free cash flow and the most comparable financial measures calculated

and presented in accordance with GAAP is included

in the appendix. The non-GAAP financial measures are by definition not measures of financial performance under generally accepted

accounting principles and are not alternatives to operating income or net income reflected in the statement of operations

or to cash flow as reflected in the statement of cash flows and are not

necessarily indicative of cash available to fund all cash flow needs. The non-GAAP financial measures used by the Company may not be comparable to similarly titled measures

of other companies.

The Company believes that the presentation of non-GAAP financial measures provides useful information to investors regarding the Company’s financial condition and results of operations because

these measures, when used in conjunction with related GAAP financial measures, (i) together provide a more comprehensive view of the Company’s core operations and ability to generate cash

flow, (ii) provide investors with the financial analytical

framework upon which management bases financial, operational, compensation and planning decisions and (iii) presents measurements that

investors and rating agencies have indicated to management are useful to them in assessing the Company and its results

of operations. Management uses these non-GAAP financial measures to plan

and measure the performance of its core operations, and its divisions measure performance and report to management based upon these measures. In addition, the Company believes

that free cash

flow and EBITDA, as the Company defines them, can assist in comparing performance from period to period, without taking into account factors affecting cash flow reflected in the statement of

cash flows, including changes in working capital

and the timing of purchases and payments.

The Company has shown adjustments to its financial presentations to exclude $11.3 million and $13.9 million of acquisition and integration costs in the fourth quarter of 2010 and 2009,

respectively,

and $137.1 million and $28.3 million of acquisition and integration costs in the full year of 2010 and 2009, respectively, because the Company believes that such costs in the fourth

quarter and full year of 2010 and 2009 are unusual, and that the magnitude

of such costs in the full year of 2010 materially exceed the comparable costs in the full year of 2009. In addition, the

Company has shown adjustments to its financial presentations to exclude $15.8 million and $9.4 million of non-cash pension

and other postretirement benefit costs in the fourth quarters of 2010 and

2009, respectively, and $40.1 million and $34.2 million of non-cash pension and other postretirement benefit costs in the full year of 2010 and 2009, respectively, and $2.7 million

and $1.2 million

of severance and early retirement costs in the fourth quarters of 2010 and 2009, respectively, and $10.4 million and $3.8 million of severance and early retirement costs in the full years of 2010 and

2009, respectively, because investors

have indicated to management that such adjustments are useful to them in assessing the Company and its results of operations.

Management uses these non-GAAP financial measures to (i) assist in analyzing the Company’s underlying financial performance from period to period, (ii) evaluate the financial performance of its

business units, (iii) analyze and evaluate strategic and operational decisions, (iv) establish criteria for compensation decisions, and (v) assist management in understanding the Company’s ability to

generate cash flow and, as a result, to plan

for future capital and operational decisions. Management uses these non-GAAP financial measures in conjunction with related GAAP financial measures.

These non-GAAP financial measures have certain shortcomings. In particular, free cash flow does not represent the residual cash flow available for discretionary expenditures, since items

such as

debt repayments and dividends are not deducted in determining such measure. EBITDA has similar shortcomings as interest, income taxes, capital expenditures, debt repayments and dividends are

not deducted in determining this measure. Management

compensates for the shortcomings of these measures by utilizing them in conjunction with their comparable GAAP financial measures. The

information in this document should be read in conjunction with the financial statements and footnotes contained

in our documents filed with the U.S. Securities and Exchange Commission.

4

Frontier Introduction

A transformational

acquisition of

properties from

Verizon tripled

Frontier’s business

size on July 1, 2010

Key Stats (December 31, 2010)

1

States

27

Total Access Lines

5,746

High Speed Internet Subscribers

1,697

Satellite & FiOS Video Subscribers

531

Employees

14,798

Revenues

$5,652

% Business Customer

43

%

% Residential Customer

45

%

% Regulatory

12

%

Adjusted EBITDA

$2,645

% Revenues

47

%

Free Cash Flow

$1,194

% Paid as Dividends

62

%

Total Debt

$8,264

Cash

$251

Leverage Ratio

3.0

(1) $ Millions; Units 000s. Pro forma for acquisition. Revenues, Adjusted

EBITDA ("operating cash flow"), and FCF are for the Last Twelve Months.

Frontier Communications (NYSE: FTR)

was founded in 1935 as Citizens Utilities

and became a pure-play telecom network

operator in 2004

Frontier’s network provides fast, reliable

data, voice, and video service to 3.4 million

residential customers and 344,000 business

customers across 27 states

Frontier is the largest communications

company focused on rural America

5

Investment Summary

Opportunity

Manage the acquired properties with Frontier’s proven Local

Engagement Model and innovative marketing

Bring margins up to Legacy levels

Harness economics of scale from business that is 3x its former size

Markets

Expand broadband availability in new markets from 70% towards

Legacy Frontier’s 91%

Rural profile, less competition, less regulatory reform exposure

Business & Broadband are 62% of customer revenues

Returns

Revenue upside from increased product penetration

$550 million operating expense synergy target by 2013

Consistent execution, solid free cash flow, stable dividend

Credit Quality

Significantly deleveraged on July 1, 2010

Target leverage of 2.5x or below

Well structured maturity schedule

6

Frontier Local Engagement

Local Area Manager

Residential

High Speed Internet (DSL

& FTTP)

Voice

Video (Satellite & FiOS)

Wireless Data (WiFi mesh)

Online backup

24/7 U.S. Tech Support

Business

Managed IP VPN

VoIP systems

High-Capacity fiber data

Metro Ethernet

Wireless backhaul

Managed router

Over 120 Local Area Managers at the community level respond to unique

customer needs in each market across Frontier’s 27 states

Employees live in the markets they serve, and put the customer first

Innovative marketing, 2-hour appointment windows, exceptional service levels

7

Robust Local Network

Expansion to Drive Penetration

Acquired network has 70% broadband

availability vs. Legacy 91%

FCC Commitments:

1.

12/31/13 – 3Mbps for 85% of households

2.

12/31/15 – 4Mbps for 85% of households

Note: 1) Based on product availability to customers; loop length availability is higher.

75%

62%

50%

13%

76%

64%

52%

13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1+ Mbps

3+ Mbps

6+ Mbps

20 Mbps

Frontier Broadband Network Availability 1

Sep '10 New Frontier

Dec '10 New Frontier

Extensive Local Networks

2,609 ILEC exchanges, 2,700 central

offices

Fiber-to-the-Home in all greenfield

builds

Linked by national fiber backbone

8

High-Capacity National Backbone

Frontier’s fiber network interconnects its 27-state footprint

9

Consistent Execution

Stability of Revenues

Driving recurring customer revenues

Delivering reliable, quality products and

services at a good price

Reducing churn with bundles

Maintaining strong Business/Enterprise

exposure

Note: Broadband expansion capital expenditures will increase significantly from 4Q10 through 2012.

$1,277

$1,264

$1,252

$1,281

$1,194

25 %

30 %

35 %

40 %

45 %

50 %

55 %

60 %

$0

$250

$500

$750

$1,000

$1,250

$1,500

4Q09

1Q10

2Q10

3Q10

4Q10

Pro Forma Frontier

Notes: Customer revenue is defined as total revenue less access services revenue. Access services include

switched network access and

subsidies.

Stability of Cash Flows

Focus on expense reduction;

competitively fit and flexible

Disciplined capital spending

Legacy EBITDA margins of 54% for 10

quarters through Q2 2010

High conversion rate of EBITDA into free

cash flow (FCF)

ARPU

Residential Revenue

Business Revenue

Pro Forma Frontier Customer Revenue

4Q10

3Q10

2Q10

1Q10

4Q09

3Q09

2Q09

$75

$70

$65

$60

$55

$50

$45

$40

$35

$30

$25

$1,500

$1,250

$1,000

$750

$500

$250

$0

$69

$69

$69

$68

$66

$67

$67

10

Attractive Revenue Base

Frontier generates 62% of its

customer revenue from

Business and Broadband

sources

Our business capabilities

are very broad and include:

- Advanced IP switching

- VoIP systems

- High-capacity fiber data systems

- Wireless cell site backhaul

- Ethernet

We are re-focusing the

residential relationship on

broadband

For the quarter ended 12/31/10

62%

38%

Business & Broadband Revenue

Other Customer Revenue

11

88.2 %

Switched 6.0 %

Federal 3.2 %

State 0.8 %

Surcharge 1.8 %

Regulatory Revenue

Customer Revenue

For the quarter ended 12/31/10

The acquired

properties reduced

Frontier’s Regulatory

Revenue exposure

from 17.5% at 4Q09 to

11.8% at 4Q10

We continue to replace

this uncertain, high-

margin revenue stream

with Customer Revenue

Minimizing Regulatory Risk

12

Key Pro Forma Financial Data

LTM 4Q10

LTM 4Q10

LTM 4Q10

Actual

Pro Forma

Pro Forma

Legacy

Acquired

New

Statistics

Frontier

Properties

Frontier

Synergies

Total

Revenue

$2,050

$3,602

$5,652

$0

$5,652

Adjusted EBITDA

(1)

1,066

1,579

2,645

246

(3)

2,891

% EBITDA Margin

52.0%

43.8%

46.8%

51.2%

Bridge to Free Cash Flow:

Interest Expense

(670)

(2)

(670)

Cash Taxes

(63)

(2)

(94)

(157)

Capital Expenditures

(227)

(459)

(686)

(686)

Other

(32)

(32)

Free Cash Flow

$1,194

$152

$1,346

Net Debt / Adj. EBITDA

3.0x

2.7x

Adj. EBITDA / Interest Exp.

3.9x

4.3x

Dividend ($0.75 / share)

$745

(2)

$745

FCF Dividend Payout Ratio

62%

55%

Notes: ($ millions)

(1) See adjustments in Appendix, Reconciliation of Non-GAAP Financial Measures.

(2) Annualized actual 3 Months Ended 12/31/10.

(3) Represents $550 million estimate less annualized synergies realized through 12/31/10

13

9.3 %

11.2 %

14.9 %

0 %

5 %

10 %

15 %

20 %

Acq Prop

Pro Forma

Legacy

48.6 %

72.5 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

Acq Prop

Legacy

70 %

76 %

91 %

0 %

20 %

40 %

60 %

80 %

100 %

Acq Prop

Pro Forma

Legacy

Note: As of the quarter ended 12/31/2010; percentage changes are year-over-year.

HSI Penetration

Satellite TV Penetration

Broadband Availability

Our ability to migrate the

acquired properties to

Frontier’s performance

metrics offers the potential

for significant operational

enhancement

Driven by broadband and

Local Engagement

Revenue Opportunity

Legacy

Pro Forma

Acq Prop

34 %

32 %

30 %

28 %

26 %

24 %

22 %

32.8 %

29.5 %

27.8 %

Long Distance Penetration

Legacy

Pro Forma

Acq Prop

0 %

(2)%

(4)%

(6)%

(8)%

(10)%

(12)%

(14)%

(6.0)%

(9.0)%

(10.4)%

Access Line Decline

14

Broadband Buildout Drives Growth

12/31/10

12/31/11

12/31/12

12/31/13

Acquired

Properties

Legacy

Note:

(i) Based on

Frontier

commitments

to the FCC on

5/21/10 for

3Mbps

broadband

availability.

This chart

assumes no

change in

Legacy

footprint.

70%

72%

80%

85%

91%

91%

91%

91%

i

i

i

Revenue opportunity

driven by 850,000 new

broadband homes open

for sale

Emphasis on double and

triple-play packages,

which lower churn

significantly

15

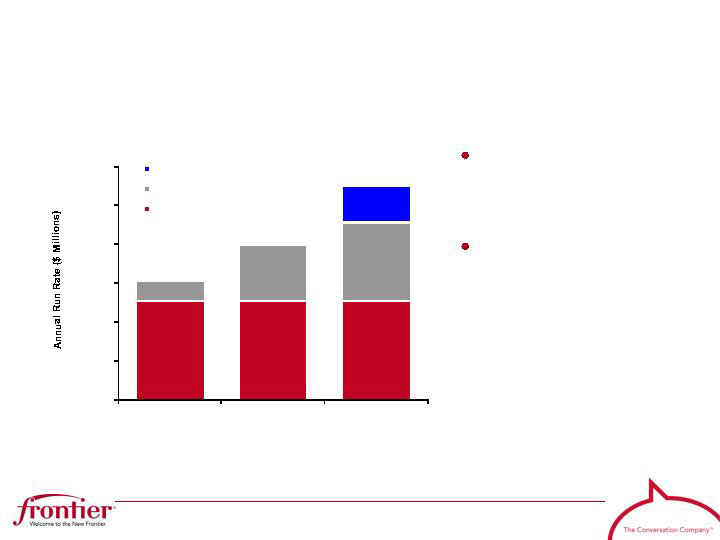

Cost Synergy Overview

$252

$252

$252

$52

$148

$204

$94

$0

$100

$200

$300

$400

$500

$600

2010

2011

2012

Estimated Cost Synergies

Software License

Other Projects

Allocated Overhead

$304

$400

$550

Significant savings from

reducing cash operating

expenses

Numerous projects

underway; synergy

estimates include:

- Network savings

- Outside contractors

- IT savings from conversion

- Real estate savings

- Operations

16

Systems Integration Plan

West Virginia

Frontier 13

Successful conversion despite a

firm July 1 deadline

Billing cycles kept within days of

prior scheduled dates, and all

systems functional out of the gate

Backlog managed downward with

“

bubble workforce” and current

levels within normal range

System mapping and analysis in

process

Systems are identical across all 13

states; processes on the first

conversions will be replicated

Initial expectation is a few states in

the second half of 2011, and the

remaining states in two groups by

end of 2012

Frontier converted West Virginia, which utilized BellAtlantic systems, on July 1, 2010

The remaining 13 states of the acquired properties (detailed in the

appendix) will be converted off Verizon (GTE) systems onto existing

Frontier systems by the end of 2012

17

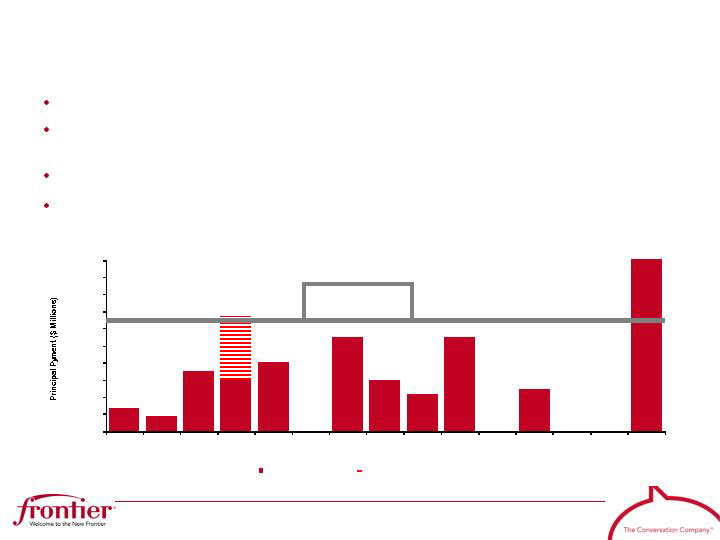

Financing Overview

Deleveraged from 4.0x (6/30/10) to 2.98x (12/31/10)

Strong $1.0 billion liquidity with an undrawn $750M R/C and $250M minimum cash-on-

hand objective

Maturity schedule is well balanced and below run rate FCF levels

Free cash flow levels match well with scheduled debt amortization.

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025+

Existing FTR Debt

Undrawn Revolver

LTM 4Q10 Pro Forma

Frontier FCF with

Synergies

18

Industry Comparisons

Change in Lines + HSI (2)

0%

10%

20%

30%

40%

50%

60%

FTR

Line Loss Yr/Yr (3)

Notes:

1.

Data for the 3-months ended 12/31/10. Adjusted EBITDA; excludes wireless; Cable is network operations only.

2.

Data for the 3-months ended 12/31/10. Represents the yr/yr change in the combined ending base of total access lines and HSI subscribers.

3.

Data for the 3-months ended 12/31/10.

Source: SEC filings; Wall Street research; Frontier.

Results, as expected, weakened from

the Acquired Properties

Operational metrics have begun to

turn around

Focusing on: i) implement local

engagement; ii) sell & retain

customers; iii) get the expenses out;

and iv) build and improve the

network

EBITDA Margin (1)

VZ

T

Q

CTL

WIN

New FTR

(3)%

(4)%

(5)%

(6)%

(7)%

(8)%

(9)%

(10)%

(11)%

19

Doing What We Say…

Goal

Status

Regulatory approval with appropriate conditions

Completion of financing within expected cost

Distribution of shares with minimal market disruption

Completion of West Virginia systems conversion

Continued delivery of solid Legacy Frontier results

Customer metric improvement and synergy realization

of acquired properties

In Process

20

Appendix

21

Access Lines by State

As of 12/31/10

FRONTIER

ACQUIRED

COMBINED

% Total

West Virginia

134,373

482,433

616,806

10.7

%

Indiana

3,879

570,109

573,988

10.0

%

Illinois

89,650

463,233

552,883

9.6

%

Ohio

506

503,760

504,266

8.8

%

Michigan

16,740

379,268

396,008

6.9

%

Wisconsin

53,456

225,150

278,606

4.8

%

Oregon

11,769

240,183

251,952

4.4

%

California

127,461

19,875

147,336

2.6

%

Arizona

130,958

2,900

133,858

2.3

%

Idaho

17,595

90,903

108,498

1.9

%

Nevada

21,950

27,103

49,053

0.9

%

COMBINED

608,337

3,004,917

3,613,254

62.9

%

Washington

0

440,111

440,111

7.7

%

North Carolina

0

213,684

213,684

3.7

%

South Carolina

0

97,532

97,532

1.7

%

NEW STATES

0

751,327

751,327

13.1

%

New York

586,469

0

586,469

10.2

%

Pennsylvania

373,517

0

373,517

6.5

%

Minnesota

188,231

0

188,231

3.3

%

Tennessee

70,198

0

70,198

1.2

%

Iowa

40,165

0

40,165

0.7

%

Nebraska

38,471

0

38,471

0.7

%

Alabama

23,929

0

23,929

0.4

%

Utah

20,330

0

20,330

0.4

%

Georgia

16,995

0

16,995

0.3

%

New Mexico

7,305

0

7,305

0.1

%

Montana

7,242

0

7,242

0.1

%

Mississippi

5,014

0

5,014

0.1

%

Florida

3,271

0

3,271

0.1

%

FRONTIER

1,381,137

0

1,381,137

24.0

%

TOTAL

1,989,474

3,756,244

5,745,718

100.0

%

Note: Numbers may not sum due to rounding

22

Reconciliation of Non-GAAP Financial Measures

Notes:

1.

Includes pension and other

postretirement benefit

(OPEB) expense of $21.1

million and

$11.4 million, less

amounts capitalized into the

cost of capital expenditures

of $2.9 million and $2.0

million, for the quarters

ended December 31, 2010

and 2009, respectively, and

pension/OPEB expense of

$61.5 million and $41.7

million, less amounts

capitalized into the cost of

capital expenditures of $8.3

million and $7.5 million, for

the years ended December

31, 2010 and 2009,

respectively. Amounts for

the quarter and year ended

December

31, 2010 have

also been reduced by $2.4

million and $13.1 million,

respectively, for cash

pension contributions.

2.

Includes premium on debt

repurchases of $53.7 million

($33.8 million or $0.11 per

share after tax) for the

quarter ended December

31,

2009 and premium, net of

gains, on debt repurchases

of $45.9 million ($28.9 million

or $0.09 per share after tax)

for the year ended December

31, 2009.

3.

Excludes capital expenditures

for integration activities.

(Amounts in thousands)

2010

2009

2010

2009

Net Income to Free Cash Flow;

Net Cash Provided by Operating Activities

Net income

46,622

$

5,170

$

155,717

$

123,181

$

Add back:

Depreciation and amortization

352,802

102,892

893,719

476,391

Income tax expense

26,247

4,600

114,999

69,928

Acquisition and integration costs

11,275

13,877

137,142

28,334

Pension/OPEB costs (non-cash)

(1)

15,826

9,394

40,050

34,196

Stock based compensation

4,543

2,394

14,473

9,368

Subtract:

Cash paid (refunded) for income taxes

15,843

(218)

19,885

59,735

Other income (loss), net

(2)

(2)

(54,171)

17,067

(40,133)

Capital expenditures - Business operations

(3)

228,528

69,073

480,888

230,966

Free cash flow

212,946

123,643

838,260

490,830

Add back:

Deferred income taxes

75,340

50,120

85,432

61,217

Non-cash (gains)/losses, net

24,575

66,269

64,595

91,583

Other income (loss), net

(2)

(2)

(54,171)

17,067

(40,133)

Cash paid (refunded) for income taxes

15,843

(218)

19,885

59,735

Capital expenditures - Business operations

(3)

228,528

69,073

480,888

230,966

Subtract:

Changes in current assets and liabilities

163,329

(27,648)

(22,717)

9,652

Income tax expense

26,247

4,600

114,999

69,928

Acquisition and integration costs

11,275

13,877

137,142

28,334

Pension/OPEB costs (non-cash)

(1)

15,826

9,394

40,050

34,196

Stock based compensation

4,543

2,394

14,473

9,368

Net cash provided by operating activities

336,010

$

252,099

$

1,222,180

$

742,720

$

For the quarter ended December 31,

For the year ended December 31,

23

Reconciliation of Non-GAAP Financial Measures

Notes:

1. Includes pension and other

postretirement benefit

(OPEB) expense of $21.1

million and $11.4 million,

less amounts capitalized

into

the cost of capital

expenditures of $2.9 million

and $2.0 million, for the

quarters ended December

31, 2010 and 2009,

respectively, and

pension/OPEB expense of

$61.5 million and $41.7

million, less amounts

capitalized

into the cost of

capital expenditures of $8.3

million and $7.5 million, for

the years ended December

31, 2010 and 2009,

respectively. Amounts for

the quarter and year ended

December 31, 2010 have

also been reduced

by $2.4

million and $13.1 million,

respectively, for cas

h pension contributions.

(Amounts in thousands)

Acquisition

Severance

Acquisition

Severance

and

Non-cash

and Early

and

Non-cash

and Early

Operating Cash Flow and

As

Integration

Pension/OPEB

Retirement

As

As

Integration

Pension/OPEB

Retirement

As

Operating Cash Flow Margin

Reported

Costs

Costs

(1)

Costs

Adjusted

Reported

Costs

Costs

(1)

Costs

Adjusted

Operating Income

239,680

$

(11,275)

$

(15,826)

$

(2,704)

$

269,485

$

157,549

$

(13,877)

$

(9,394)

$

(1,221)

$

182,041

$

Add back:

Depreciation and

amortization

352,802

-

-

-

352,802

102,892

-

-

-

102,892

Operating cash flow

592,482

$

(11,275)

$

(15,826)

$

(2,704)

$

622,287

$

260,441

$

(13,877)

$

(9,394)

$

(1,221)

$

284,933

$

Revenue

1,358,721

$

1,358,721

$

520,980

$

520,980

$

Operating income margin

(Operating income divided

by revenue)

17.6%

19.8%

30.2%

34.9%

Operating cash flow margin

(Operating cash flow divided

by revenue)

43.6%

45.8%

50.0%

54.7%

Acquisition

Severance

Acquisition

Severance

and

Non-cash

and Early

and

Non-cash

and Early

Operating Cash Flow and

As

Integration

Pension/OPEB

Retirement

As

As

Integration

Pension/OPEB

Retirement

As

Operating Cash Flow Margin

Reported

Costs

Costs

(1)

Costs

Adjusted

Reported

Costs

Costs

(1)

Costs

Adjusted

Operating Income

771,998

$

(137,142)

$

(40,050)

$

(10,362)

$

959,552

$

606,165

$

(28,334)

$

(34,196)

$

(3,788)

$

672,483

$

Add back:

Depreciation and

amortization

893,719

-

-

-

893,719

476,391

-

-

-

476,391

Operating cash flow

1,665,717

$

(137,142)

$

(40,050)

$

(10,362)

$

1,853,271

$

1,082,556

$

(28,334)

$

(34,196)

$

(3,788)

$

1,148,874

$

Revenue

3,797,675

$

3,797,675

$

2,117,894

$

2,117,894

$

Operating income margin

(Operating income divided

by revenue)

20.3%

25.3%

28.6%

31.8%

Operating cash flow margin

(Operating cash flow divided

by revenue)

43.9%

48.8%

51.1%

54.2%

For the year ended December 31, 2010

For the year ended December 31, 2009

For the quarter ended December 31, 2009

For the quarter ended December 31, 2010

24

Frontier Values

Put the customer first

Treat one another with respect

Keep our commitments; be accountable

Be ethical in all of our dealings

Take the initiative

Be team players

Be innovative; practice continuous improvement

Be active in our communities

Do it right the first time

Use resources wisely

Have a positive attitude

Use Frontier products and

services

25

Frontier Communications Corp.

(NYSE: FTR)

Investor Relations

3 High Ridge Park

Stamford, CT 06905

203.614.4606

IR@FTR.com